Foreign Exchange Risks

International Investment

Exchange Risk Exposure

Accounting exposure = (foreign-currency denominated assets) – (foreign-currency denominated liabilities)

Transaction exposure: uncertainty in the domestic currency value of the transaction using foreign currency

Economic exposure = exposure of the value of the firm (the present value of future cash flows) to changes in exchange rates

How to hedge FX risk

Use forward contracts, futures or options. Use the domestic currency Speed up payments (collections) of

currencies expected to appreciate (depreciate)

Slow down payments (collections) of currencies expected to depreciate (appreciate)

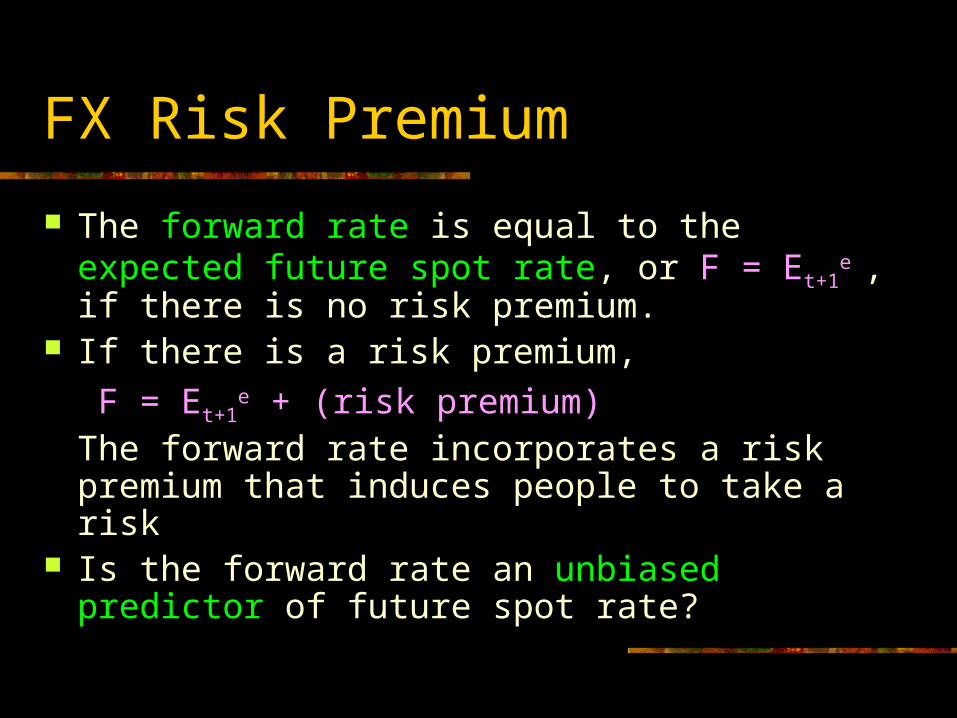

FX Risk Premium

The forward rate is equal to the expected future spot rate, or F = Et+1

e , if there is no risk premium.

If there is a risk premium,

F = Et+1e + (risk premium)

The forward rate incorporates a risk premium that induces people to take a risk

Is the forward rate an unbiased predictor of future spot rate?

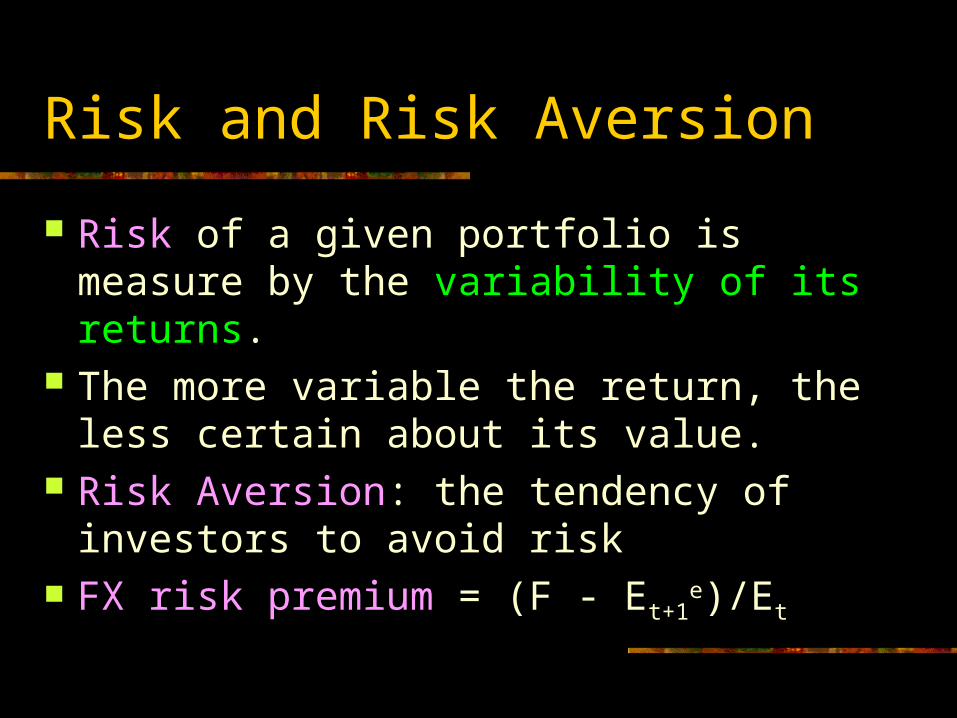

Risk and Risk Aversion

Risk of a given portfolio is measure by the variability of its returns.

The more variable the return, the less certain about its value.

Risk Aversion: the tendency of investors to avoid risk

FX risk premium = (F - Et+1e)/Et

FX Risk Premium

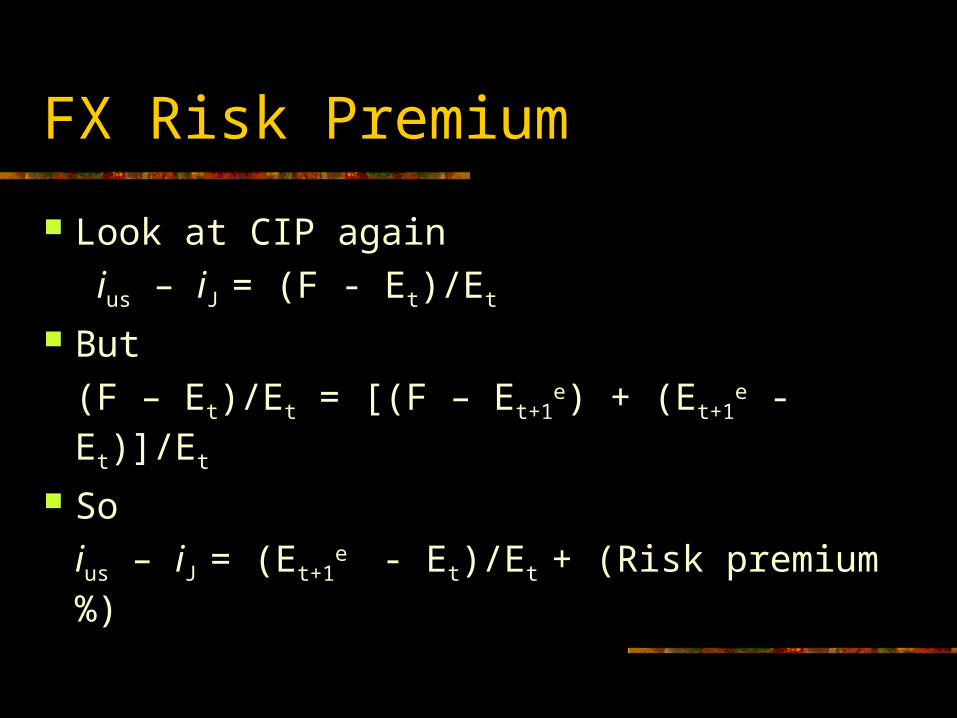

Look at CIP again

ius – iJ = (F - Et)/Et

But

(F – Et)/Et = [(F – Et+1e) + (Et+1

e - Et)]/Et

So

ius – iJ = (Et+1e - Et)/Et + (Risk premium %)

FX Risk Premium

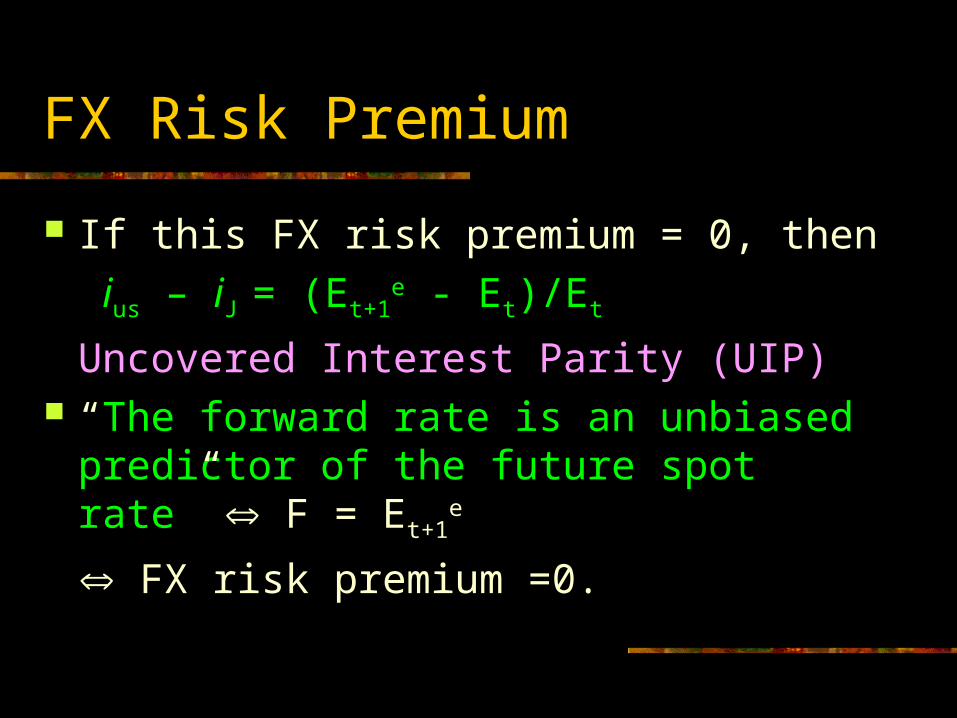

If this FX risk premium = 0, then

ius – iJ = (Et+1e - Et)/Et

Uncovered Interest Parity (UIP) “The forward rate is an unbiased predictor

of the future spot rate” F = Et+1e

FX risk premium =0.

Example

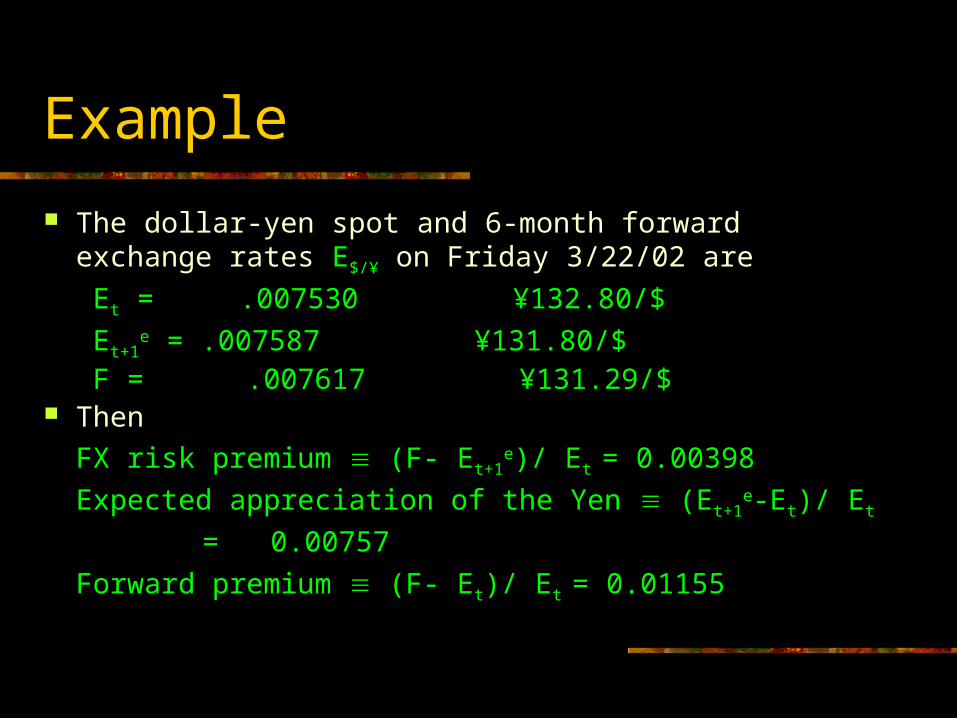

The dollar-yen spot and 6-month forward exchange rates E$/¥ on Friday 3/22/02 are

Et = .007530 ¥132.80/$

Et+1e = .007587 ¥131.80/$

F = .007617 ¥131.29/$ Then

FX risk premium (F- Et+1e)/ Et = 0.00398

Expected appreciation of the Yen (Et+1e-Et)/ Et

= 0.00757

Forward premium (F- Et)/ Et = 0.01155

Example (cont’d)

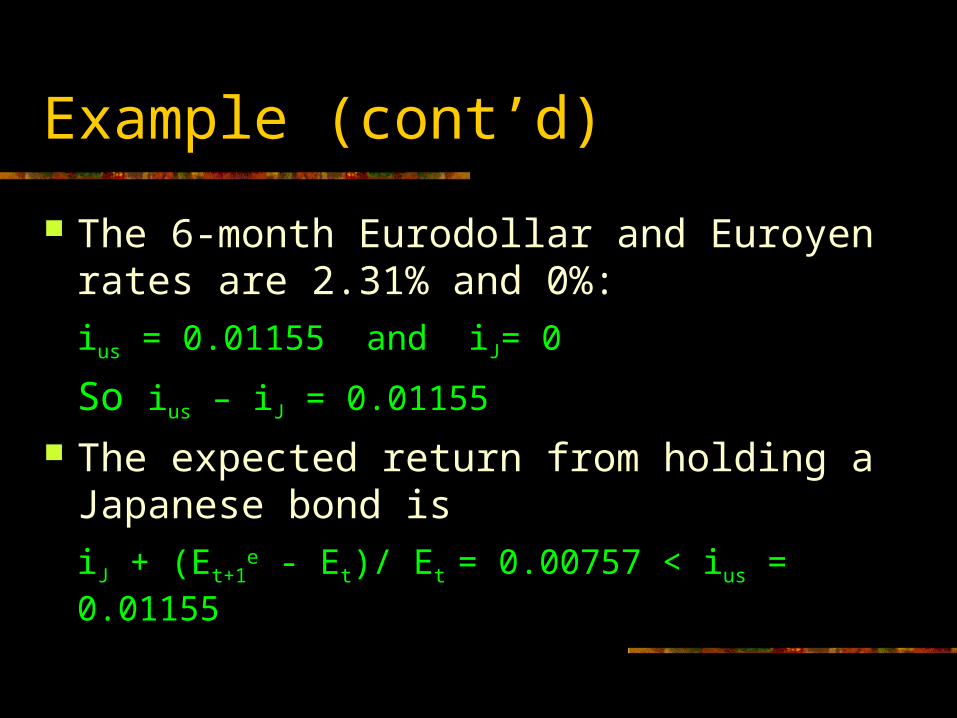

The 6-month Eurodollar and Euroyen rates are 2.31% and 0%:

ius = 0.01155 and iJ= 0

So ius – iJ = 0.01155

The expected return from holding a Japanese bond is

iJ + (Et+1e - Et)/ Et = 0.00757 < ius = 0.01155

Market Efficiency

Prices reflect all available information Efficient Market

The Fed unexpectedly lowers the interest rate. An immediate decline of the dollar or Et

In an efficient market,

F - Et+1e = FX risk premium.

Market Efficiency (cont’d)

Suppose F > Et+1e + FX risk premium.

An investor would get profits by selling forward currency now (short position in the Euro) and buying it back later.

If F < Et+1e + risk premium, an investor should

buy forward currency now (long position in the Euro) and sell it later.

Test for Market Efficiency

Statistical tests for the efficiency of the FX market

Is there any other variables in addition to the forward rate (F) that can help predict the future spot rate (Et+1

e)? If no, then the forward rate contains all

relevant information about the future spot rate.

Foreign Exchange Forecasting

There is some evidence that the forward rate is not an unbiased predictor of the future spot rate.

But conflicting evidence on the ability of exchange rate forecasting to forecast better than the forward rate.

International Investment

Differences in the returns on assets in different countries

Diversified portfolio provides lower risk with the same expected return.

International Investment (cont’d)

Systematic risk: The risk common to all investment opportunities. Related to Business cycles.

Non-systematic risk: The risk that can be eliminated by diversification.

International Investment (cont’d)

Direct Foreign Investment (DFI or FDI): actual establishment of a foreign operating unit

Portfolio Investment: purchase of foreign securities

International Investment (cont’d)

Late 1970s: “Recycling” of the oil money International bank lending

mid 1980s: Debt crises and non-repayment Bank lending

Early 1990s: “Emerging market” boom portfolio investment Mexico currency crisis (1994) “Tequila effect” portfolio investment

Late 1990s: DFI

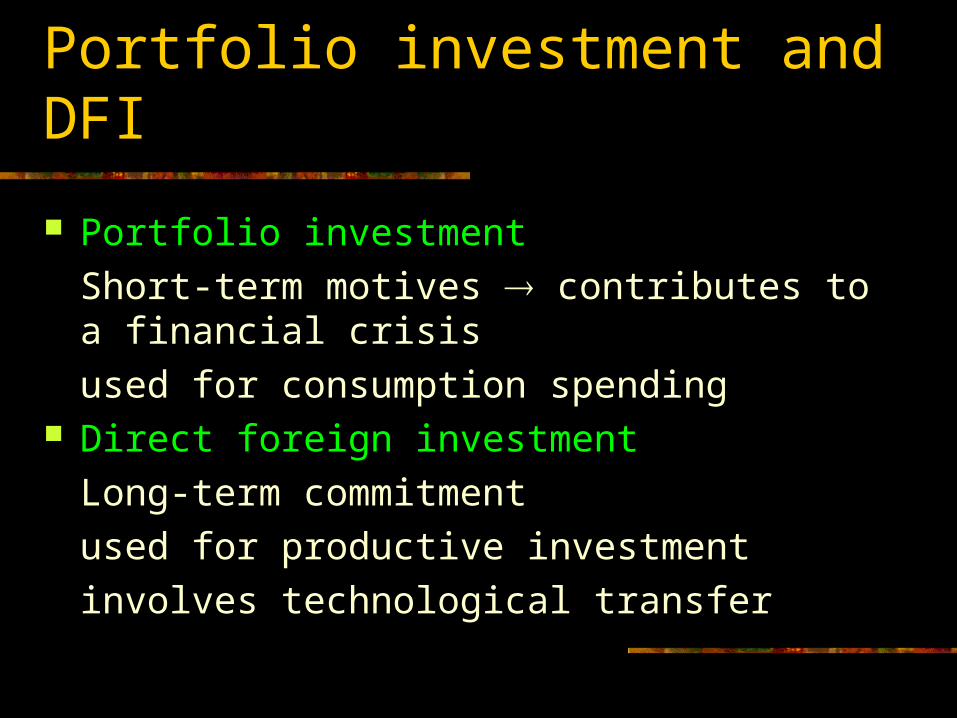

Portfolio investment and DFI

Portfolio investment

Short-term motives contributes to a financial crisis

used for consumption spending Direct foreign investment

Long-term commitment

used for productive investment

involves technological transfer

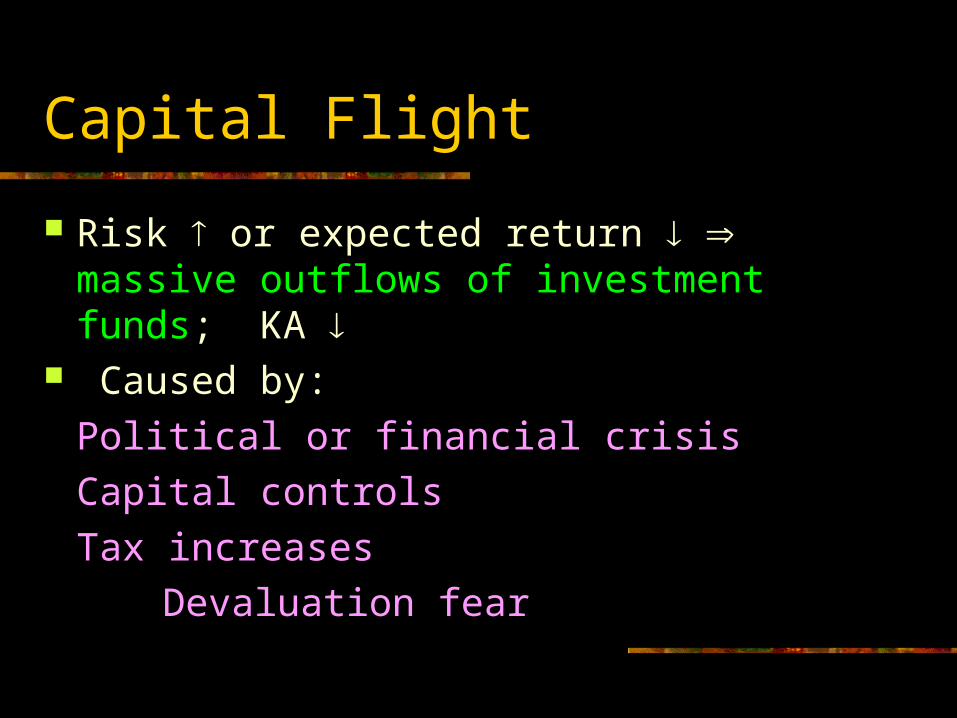

Capital Flight

Risk or expected return massive outflows of investment funds; KA

Caused by:

Political or financial crisis

Capital controls

Tax increases

Devaluation fear

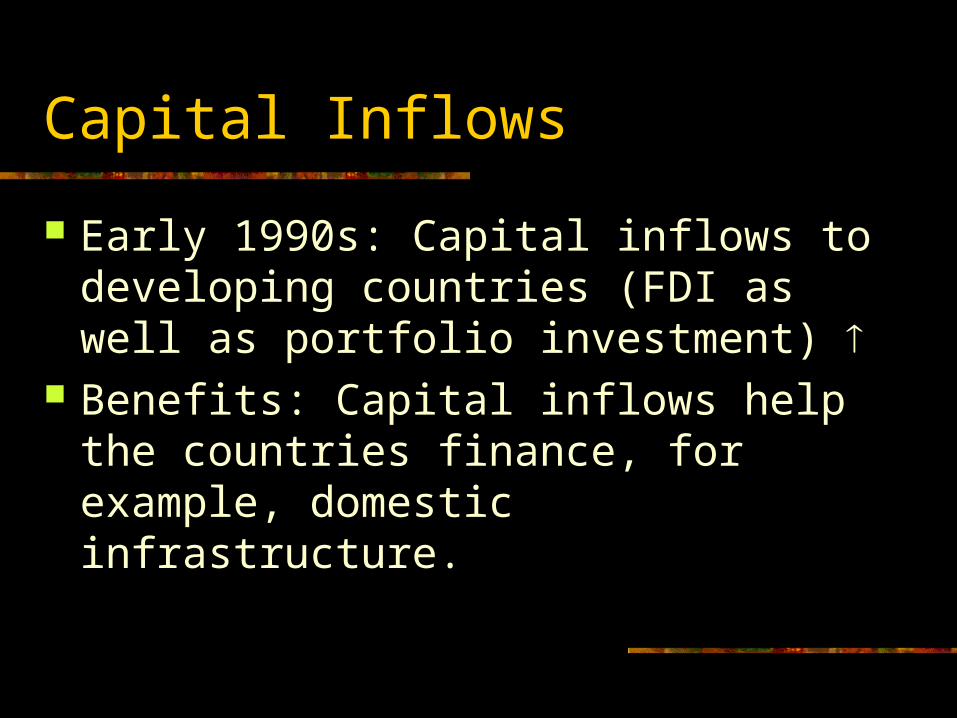

Capital Inflows

Early 1990s: Capital inflows to developing countries (FDI as well as portfolio investment)

Benefits: Capital inflows help the countries finance, for example, domestic infrastructure.

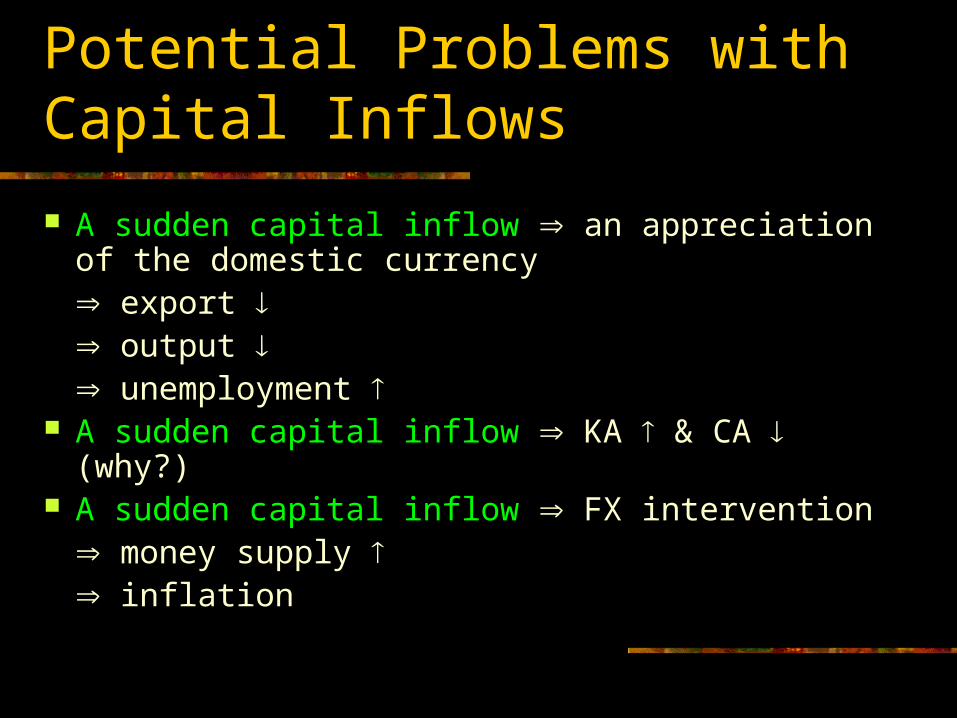

Potential Problems with Capital Inflows

A sudden capital inflow an appreciation of the domestic currency export output unemployment

A sudden capital inflow KA & CA (why?) A sudden capital inflow FX intervention

money supply inflation

Policy responses

Fiscal restraint: cut gov’t spending and raise taxes (contractionary fiscal policy)

Exchange rate policy Capital controls: taxes and quotas in

capital flows; raise reserve requirements; restriction on FX transactions.

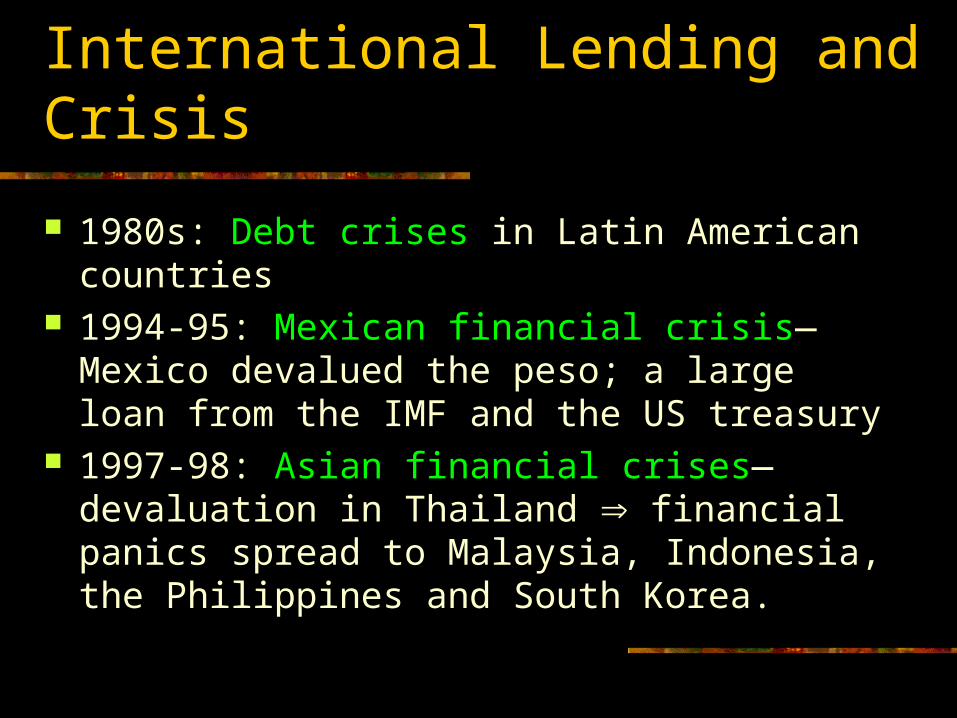

International Lending and Crisis

1980s: Debt crises in Latin American countries 1994-95: Mexican financial crisis—Mexico

devalued the peso; a large loan from the IMF and the US treasury

1997-98: Asian financial crises—devaluation in Thailand financial panics spread to Malaysia, Indonesia, the Philippines and South Korea.

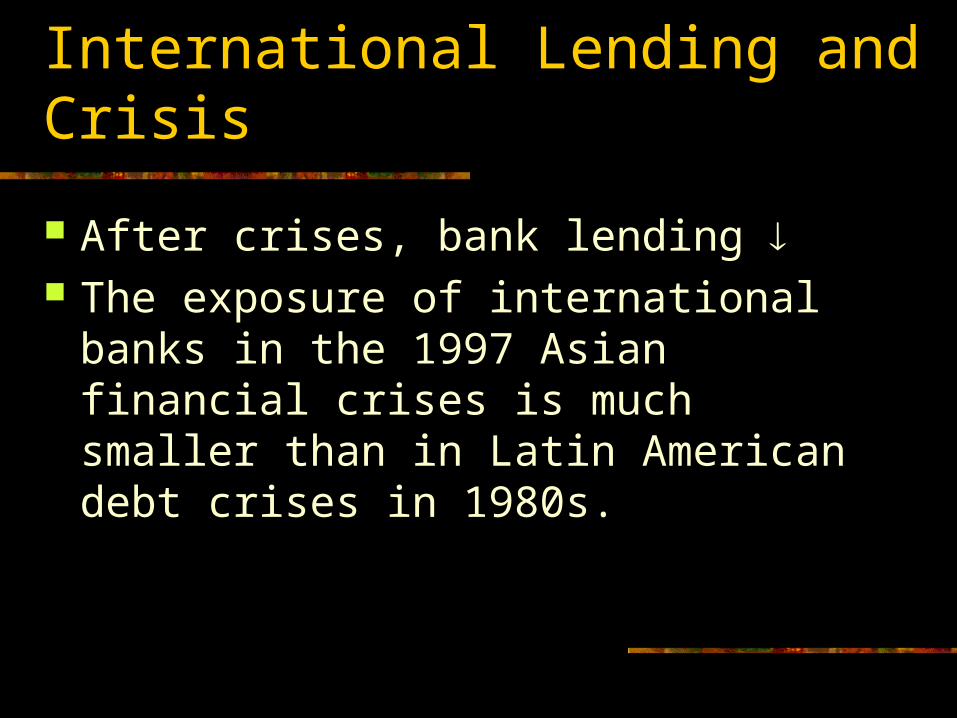

International Lending and Crisis

After crises, bank lending The exposure of international banks in the

1997 Asian financial crises is much smaller than in Latin American debt crises in 1980s.

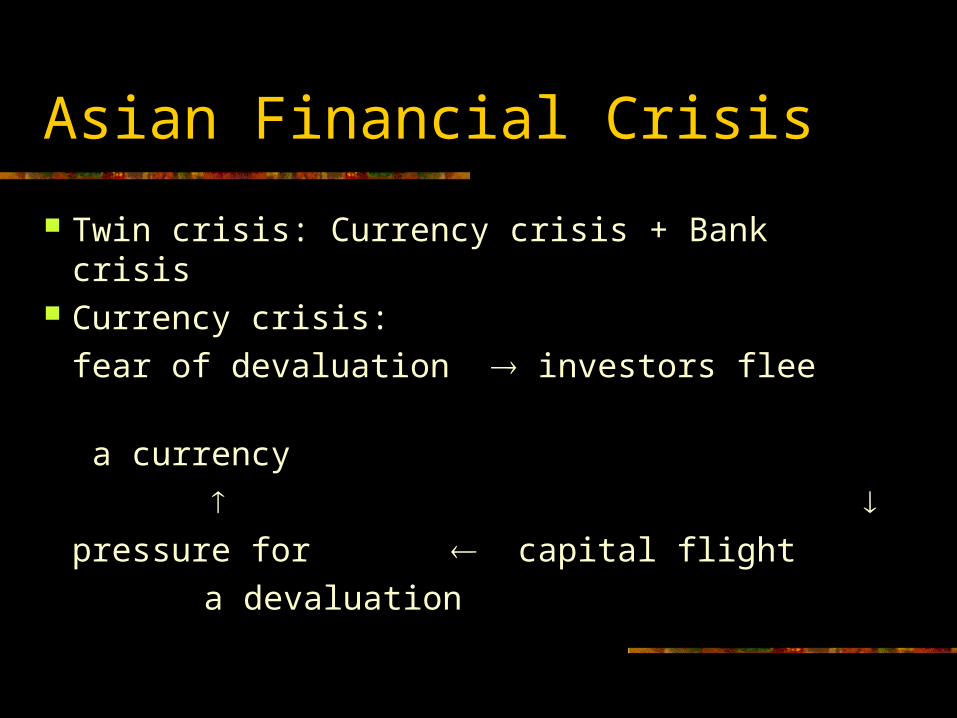

Asian Financial Crisis

Twin crisis: Currency crisis + Bank crisis Currency crisis:

fear of devaluation investors flee

a currency

pressure for capital flight

a devaluation

Causes of Asian financial crises

External shocks: depreciation of Yen and renminbi

Macroeconomic policy: Fixed exchange rates

Financial system flaws: “Crony capitalism”Moral Hazard

Defense of Fixed rate and Crisis

Pressure for a devaluation (e.g. CA) defend the fixed rate (FX intervention,

raise interest rate, capital controls) Speculative attack abandon the fixed rate—devaluation (foreign currency denominated) debt

Financial system flaws

A banking system based excessively on directed lending, connected lending, and other collusive personal relations. “Crony capitalism”

Bank bailout guarantee by the gov’t

banks take excessive risk (Moral hazard)

Recommended