Outlook for the San Diego Metro Office Market with Green and Medical Office Breakdown

By Norm Miller, PhD, with Bryan Masters, Lawrence Kopp and Charles Tu, PhD

Preface: The purpose of this report is not to replace the forecasting work of the excellent consultants and real

estate firms in the region. Rather, it is intended to provide an independent, aggregate and longer‐term

outlook on the health of the office market.

Demand and Supply: San Diego appears to be on a good track with respect to the metro office market.

Normal additions to supply run about 2 percent of the stock each year and that suffices for normal wear and

tear and attrition of the old stock—estimated at 1 percent per year—as well as net new demand from normal

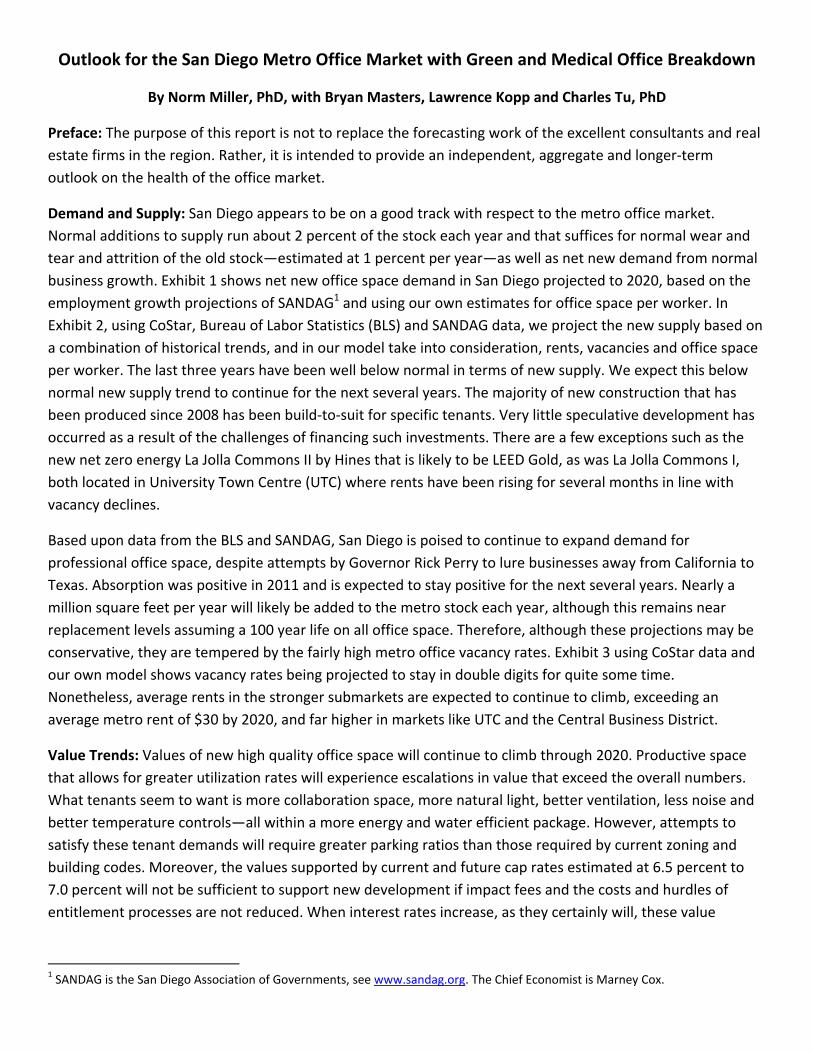

business growth. Exhibit 1 shows net new office space demand in San Diego projected to 2020, based on the

employment growth projections of SANDAG1 and using our own estimates for office space per worker. In

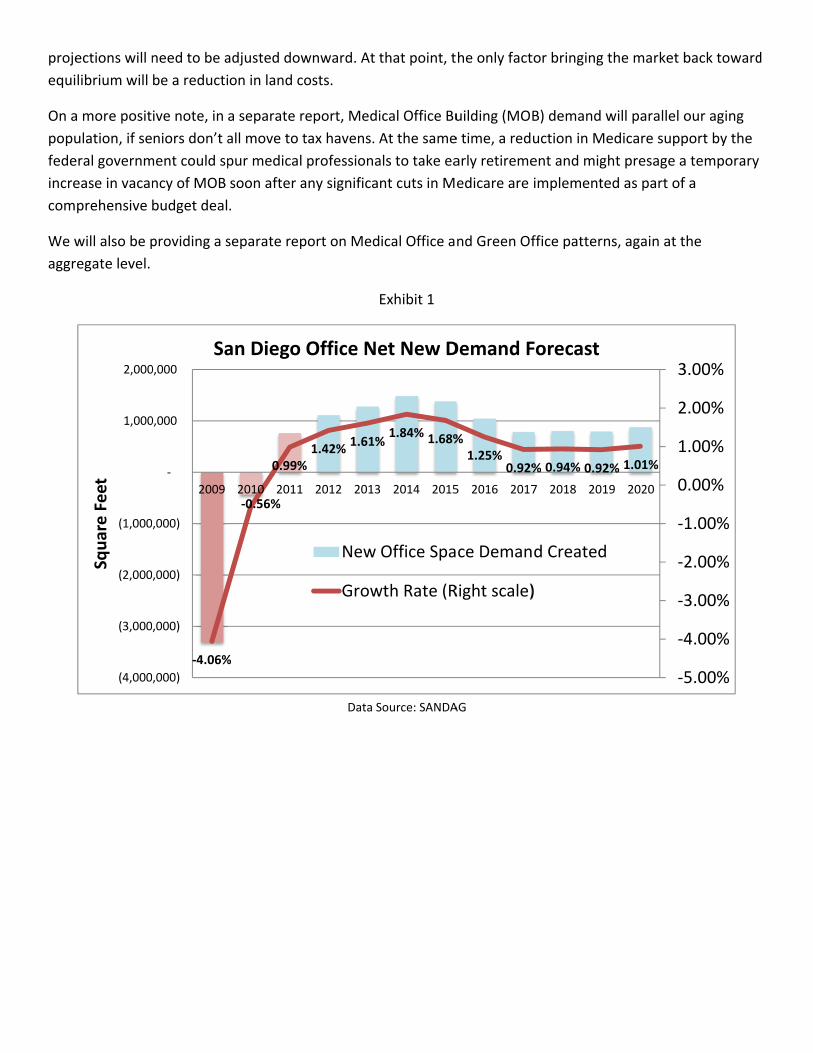

Exhibit 2, using CoStar, Bureau of Labor Statistics (BLS) and SANDAG data, we project the new supply based on

a combination of historical trends, and in our model take into consideration, rents, vacancies and office space

per worker. The last three years have been well below normal in terms of new supply. We expect this below

normal new supply trend to continue for the next several years. The majority of new construction that has

been produced since 2008 has been build‐to‐suit for specific tenants. Very little speculative development has

occurred as a result of the challenges of financing such investments. There are a few exceptions such as the

new net zero energy La Jolla Commons II by Hines that is likely to be LEED Gold, as was La Jolla Commons I,

both located in University Town Centre (UTC) where rents have been rising for several months in line with

vacancy declines.

Based upon data from the BLS and SANDAG, San Diego is poised to continue to expand demand for

professional office space, despite attempts by Governor Rick Perry to lure businesses away from California to

Texas. Absorption was positive in 2011 and is expected to stay positive for the next several years. Nearly a

million square feet per year will likely be added to the metro stock each year, although this remains near

replacement levels assuming a 100 year life on all office space. Therefore, although these projections may be

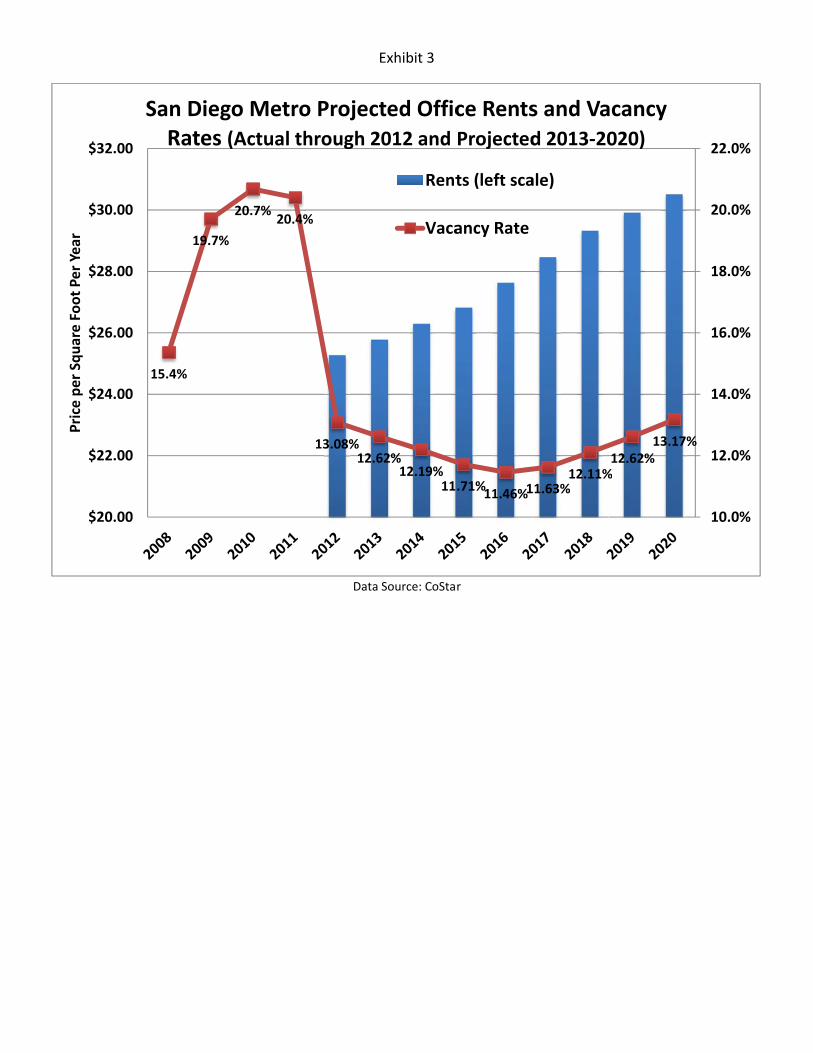

conservative, they are tempered by the fairly high metro office vacancy rates. Exhibit 3 using CoStar data and

our own model shows vacancy rates being projected to stay in double digits for quite some time.

Nonetheless, average rents in the stronger submarkets are expected to continue to climb, exceeding an

average metro rent of $30 by 2020, and far higher in markets like UTC and the Central Business District.

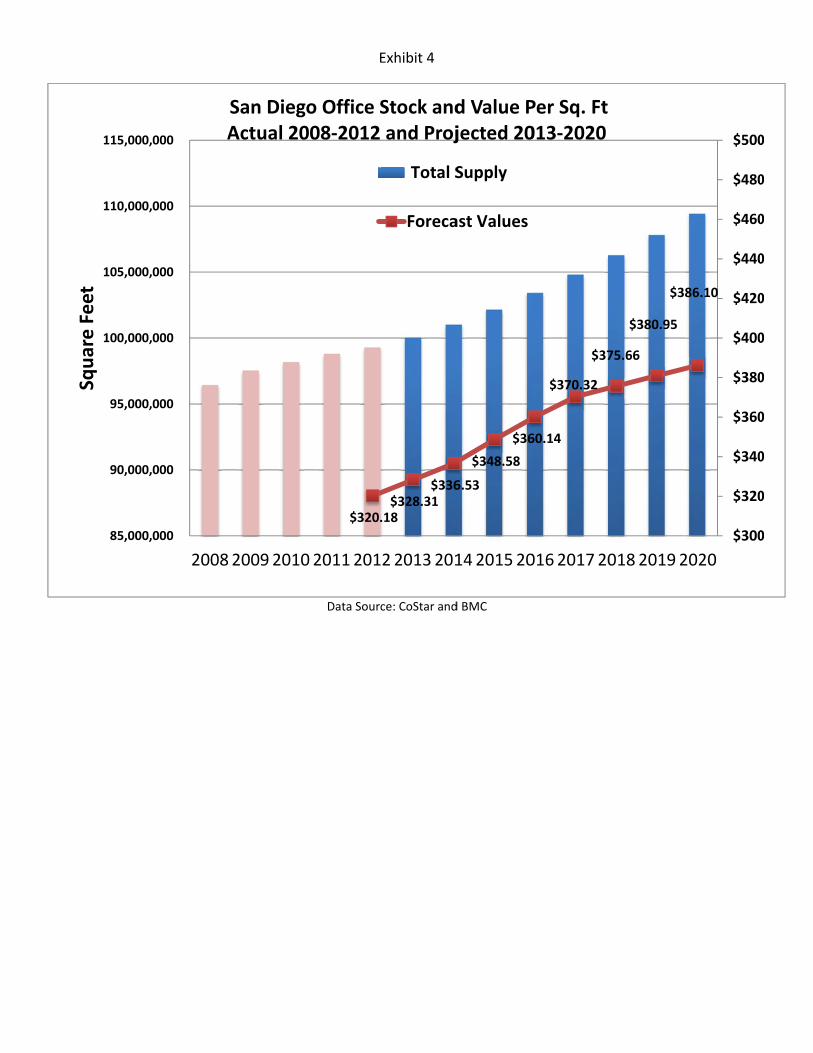

Value Trends: Values of new high quality office space will continue to climb through 2020. Productive space

that allows for greater utilization rates will experience escalations in value that exceed the overall numbers.

What tenants seem to want is more collaboration space, more natural light, better ventilation, less noise and

better temperature controls—all within a more energy and water efficient package. However, attempts to

satisfy these tenant demands will require greater parking ratios than those required by current zoning and

building codes. Moreover, the values supported by current and future cap rates estimated at 6.5 percent to

7.0 percent will not be sufficient to support new development if impact fees and the costs and hurdles of

entitlement processes are not reduced. When interest rates increase, as they certainly will, these value

1 SANDAG is the San Diego Association of Governments, see www.sandag.org. The Chief Economist is Marney Cox.

proje

equi

On a

popu

fede

incre

com

We w

aggr

ections will n

librium will

a more posit

ulation, if se

eral governm

ease in vacan

prehensive

will also be p

egate level.

(4,000

(3,000

(2,000

(1,000

1,000

2,000

Square Feet

need to be a

be a reducti

ive note, in

niors don’t a

ment could sp

ncy of MOB

budget deal

providing a s

‐4.06%

,000)

,000)

,000)

,000)

‐

0,000

0,000

2009

Sa

adjusted dow

on in land co

a separate r

all move to t

pur medical

soon after a

.

separate rep

%

‐0.56%

0.99%

2010 2011

an Diego

wnward. At t

osts.

report, Medi

tax havens. A

professiona

any significan

port on Med

E

Data S

%1.42%

1.61%

2012 2013

Office Ne

New

Grow

that point, t

ical Office Bu

At the same

als to take ea

nt cuts in M

ical Office a

Exhibit 1

Source: SANDA

%1.84% 1.68%

2014 2015

et New D

Office Spa

wth Rate (R

he only fact

uilding (MOB

e time, a red

arly retireme

edicare are

nd Green Of

AG

%1.25%

0.92%

5 2016 2017

Demand F

ce Deman

Right scale)

tor bringing t

B) demand w

uction in Me

ent and migh

implemente

ffice pattern

% 0.94% 0.92

7 2018 201

Forecast

d Created

)

the market b

will parallel o

edicare supp

ht presage a

ed as part of

ns, again at t

2% 1.01%

‐5

‐4

‐3

‐2

‐

0

1

2

3

9 2020

back toward

our aging

port by the

a temporary

f a

the

5.00%

4.00%

3.00%

2.00%

1.00%

0.00%

1.00%

2.00%

3.00%

d

80,000,00

85,000,00

90,000,00

95,000,00

100,000,00

105,000,00

110,000,00

115,000,00

Square Feet

1.01%1.18%

00

00

00

00

00

00

00

00

20032004

SupA

R

Data Source

%

2.17%

2.76%

3.36

420052006200

pply of OActual 200

RBA witho

E

e: CoStar, Bure

6%

2.70%

1.13%

0.6

072008200920

Office Sp03‐2012 a

ut MOB

Exhibit 2

eau of Labor St

66%0.63%0.48%

0

010201120122

ace in Sand Proje

Tota

tatistics and SA

%

0.76%0.97%

1.13

201320142015

an Diegoected 201

al Annual G

ANDAG

%1.25%

1.33%1.4

52016201720

o Count13‐2020

Growth Rat

40%

1.45%

1.49%

01820192020

y

te

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

Price

perSquareFootPerYear

1

$20.00

$22.00

$24.00

$26.00

$28.00

$30.00

$32.00

Price per Square Foot Per Year

S

15.4%

19.7%

San DiegRates

%

20.7%20.4%

go Metro(Actual th

E

Data

%

13.08%12.6

o Projecthrough 2

Exhibit 3

Source: CoSta

62%12.19%

11

ted Offic012 and

Rent

Vaca

r

.71%11.46%1

ce RentsProjected

ts (left sca

ancy Rate

11.63%12.11%

s and Vad 2013‐20

ale)

%12.62%

13.17

acancy 020)

7%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

22.0%

85,000,

90,000,

95,000,

100,000,

105,000,

110,000,

115,000,

Square Feet

000

000

000

000

000

000

000

2008

A

20092010

San DiegActual 20

E

Data Sour

$320.

0 2011201

go Office S008‐2012

Exhibit 4

ce: CoStar and

.18 $328.31

$336

122013201

Stock and and Proj

Total S

Foreca

d BMC

6.53

$348.58

$36

14201520

d Value Pjected 20

Supply

ast Values

60.14

$370.32

$37

0162017 20

Per Sq. Ft013‐2020

75.66

$380.95

$3

018 2019 2

86.10

$300

$320

$340

$360

$380

$400

$420

$440

$460

$480

$500

2020

0

0

0

0

0

0

0

0

0

0

0

Outlook for the San Diego Green Office Market

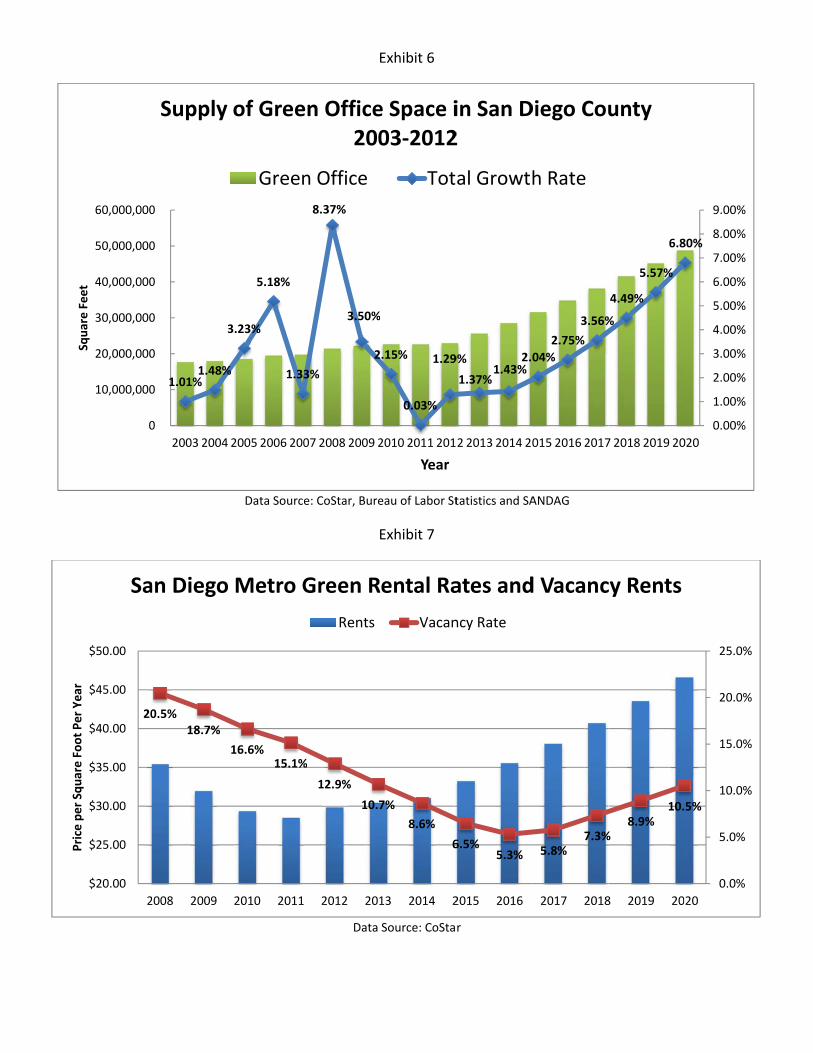

Demand and Supply: The San Diego Green office market appears to be recovering at a more rapid pace than

the general metro office market. Most green buildings are already superior in quality with a large proportion

of Class A quality inventory. Many tenants realizing the historically low rental rates bargains in the past few

years have made the “flight to quality.” The overall vacancy rate for green buildings has come down faster

than the overall market. Normal additions to supply run about 2.8 percent of the stock each year in San Diego

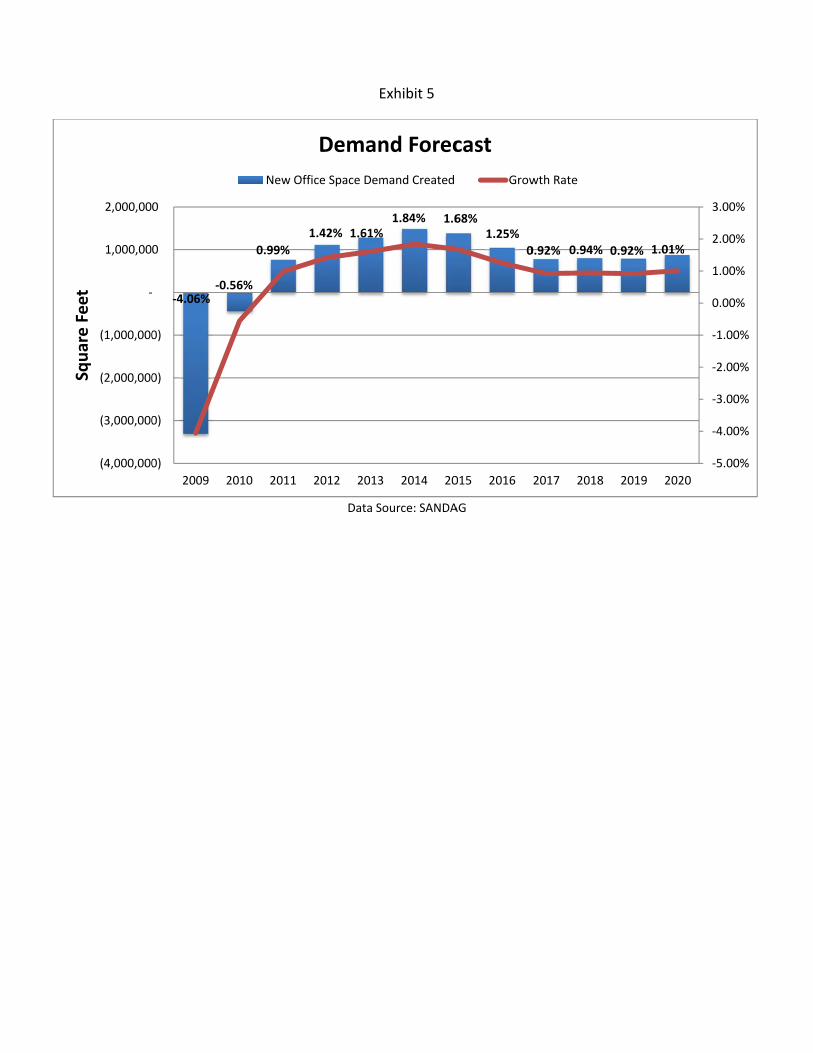

County, included in this figure is the addition of new construction and existing building conversion. Exhibit 5

shows net new office space demand in San Diego projected through 2020, based on the employment growth

projections of SANDAG and using our own estimates for office space per worker. In Exhibit 6, using CoStar, BLS

and SANDAG data, we project the new supply based on a combination of historical trends, as well as rental

rates, vacancies and office space per worker.

The last three years have been well below normal in terms of net new supply. Due to the lengthy permitting

process for new construction, we expect this below normal new supply trend to continue for the next several

years. In regards to office buildings, the majority of new construction since 2008 has been green buildings. We

expect this trend to continue, whether or not the owner decides to certify the building is their decision. Those

few projects currently under construction are green buildings including La Jolla Commons II in the UTC

submarket, which is likely to be LEED Gold and will be one of the largest ‘net‐zero’ buildings in the United

States. The other, the FBI headquarters building in Sorrento Mesa, is projected to be LEED Gold. In addition,

Rio San Diego I, a Class A building in Mission Valley, achieved LEED EB certification last year.

Based upon data from the Bureau of Labor Statistics and SANDAG, San Diego is poised to continue to expand

demand for professional office space. Absorption in green buildings has been positive in 18 of the last 20

quarters and is expected to stay positive for the next several years. Just under three million square feet per

year will likely be added to the green metro stock each year, this includes about two million square of existing

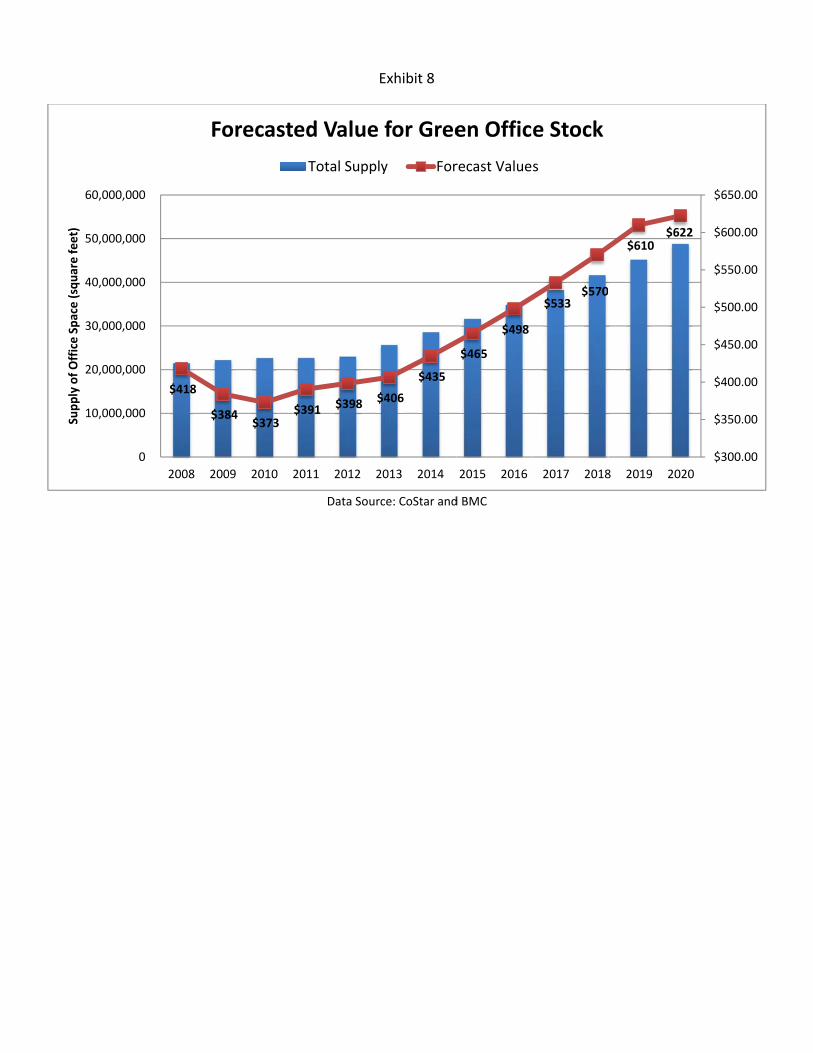

construction being retrofitted to meet green standards. Exhibit 7 using CoStar data and our own model shows

the vacancy rate for green space is projected to reach single digits again in 2014. With this trend, the average

green rental rate is expected to climb, exceeding an average metro rent of $47 by 2020, with some of the

stronger submarkets like Del Mar Heights and UTC being even higher.

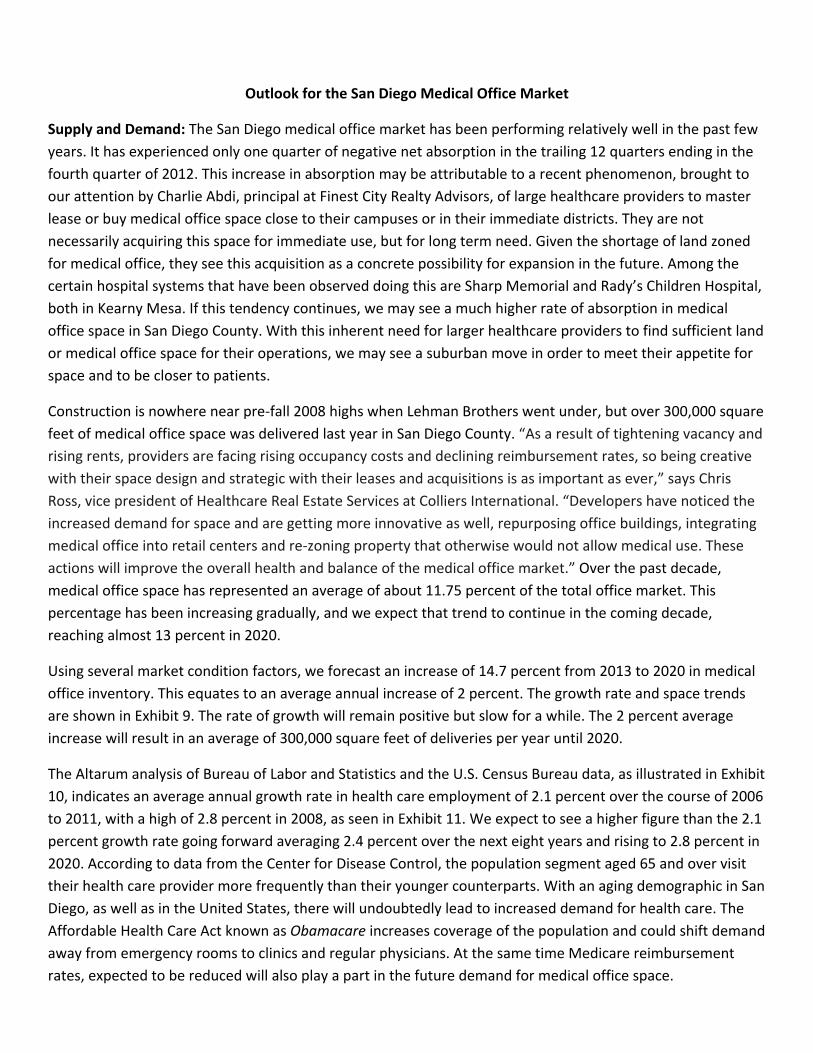

Value Trends: Values of green office buildings will continue to climb through 2020 as seen in Exhibit 8.

Buildings that offer the greatest amenities and are in premium locations will experience escalations in value

that exceed the average price per square foot. More tenants that desire to be in more convenient locations,

require more collaborative space, better natural lighting, better ventilation, less noise and better temperature

controls, along with more energy and water efficient package will be attracted to green buildings. Moreover,

as land availability is limited in the ideal locations for green buildings and land values and entitlement costs

remain high, especially in the desirable submarkets, the feasibility of new construction will be limited. In

addition, when interest rates increase, the interest of new spec office development will be reduced. We

anticipate that with the demand and land shortage, that the spread between green building and non‐green

building values will become greater before green becomes the standard benchmark required for all

competitive buildings.

SF

(4,000,000

(3,000,000

(2,000,000

(1,000,000

‐

1,000,00

2,000,00

Square Feet ‐4.06%

‐0.

0)

0)

0)

0)

0

0

2009 2

.56%

0.99%

2010 2011

New Of

E

Data S

1.42% 1.61%

2012 2013

Deman

ffice Space Dem

Exhibit 5

Source: SANDA

%1.84% 1.6

3 2014 20

nd Forec

mand Created

AG

68%1.25%

0

015 2016

cast

Grow

0.92% 0.94%

2017 2018

wth Rate

0.92% 1.01%

2019 202

‐5.00%

‐4.00%

‐3.00%

‐2.00%

‐1.00%

0.00%

1.00%

2.00%

3.00%

0

Price

perSquareFootPerYear

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

Square Feet

20

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

$50.00

2

Price per Square Foot Per Year

Sa

1.01%1.48%

3

0

0

0

0

0

0

0

2003 2004

Supply

0.5%18.7%

2008 2009

an Diego

Data Source

%

3.23%

5.18%

1.33

2005 2006 200

of Gree

Green

16.6%15.1%

2010 2011

Metro G

E

e: CoStar, Bure

E

Data

3%

8.37%

3.50%

2

07 2008 2009 2

en Office200

n Office

%

12.9%

10.7

2012 201

Green R

Rents

Exhibit 6

eau of Labor St

Exhibit 7

Source: CoSta

%

.15%

0.03%

1.29

2010 2011 201

Year

e Space i03‐2012

Tot

7%

8.6%

6

13 2014 2

Rental Ra

Vacan

tatistics and SA

r

9%

1.37%1.43%

2.0

2 2013 2014 20

in San D2

al Growth

6.5%5.3%

2015 2016

ates and

ncy Rate

ANDAG

04%

2.75%

3.56%

015 2016 2017

Diego Cou

h Rate

5.8%7.3%

2017 2018

d Vacanc

%

4.49%

5.57%

6.8

7 2018 2019 20

unty

%8.9%

10.

8 2019 20

cy Rents

80%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

020

5%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

20

SupplyofOfficeSpace(squarefeet)

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

Supply of Office Space (square feet)

$418

$38

2008 200

Fo

84 $373

$3

09 2010 20

orecaste

E

Data Sour

391 $398 $

011 2012 2

ed Value

Total Suppl

Exhibit 8

ce: CoStar and

$406

$435

2013 2014

for Gree

y For

d BMC

$465

$498

2015 2016

en Offic

recast Value

$533 $570

2017 2018

e Stock

s

$610 $62

8 2019 202

22

$300.00

$350.00

$400.00

$450.00

$500.00

$550.00

$600.00

$650.00

20

Outlook for the San Diego Medical Office Market

Supply and Demand: The San Diego medical office market has been performing relatively well in the past few

years. It has experienced only one quarter of negative net absorption in the trailing 12 quarters ending in the

fourth quarter of 2012. This increase in absorption may be attributable to a recent phenomenon, brought to

our attention by Charlie Abdi, principal at Finest City Realty Advisors, of large healthcare providers to master

lease or buy medical office space close to their campuses or in their immediate districts. They are not

necessarily acquiring this space for immediate use, but for long term need. Given the shortage of land zoned

for medical office, they see this acquisition as a concrete possibility for expansion in the future. Among the

certain hospital systems that have been observed doing this are Sharp Memorial and Rady’s Children Hospital,

both in Kearny Mesa. If this tendency continues, we may see a much higher rate of absorption in medical

office space in San Diego County. With this inherent need for larger healthcare providers to find sufficient land

or medical office space for their operations, we may see a suburban move in order to meet their appetite for

space and to be closer to patients.

Construction is nowhere near pre‐fall 2008 highs when Lehman Brothers went under, but over 300,000 square

feet of medical office space was delivered last year in San Diego County. “As a result of tightening vacancy and

rising rents, providers are facing rising occupancy costs and declining reimbursement rates, so being creative

with their space design and strategic with their leases and acquisitions is as important as ever,” says Chris

Ross, vice president of Healthcare Real Estate Services at Colliers International. “Developers have noticed the

increased demand for space and are getting more innovative as well, repurposing office buildings, integrating

medical office into retail centers and re‐zoning property that otherwise would not allow medical use. These

actions will improve the overall health and balance of the medical office market.” Over the past decade,

medical office space has represented an average of about 11.75 percent of the total office market. This

percentage has been increasing gradually, and we expect that trend to continue in the coming decade,

reaching almost 13 percent in 2020.

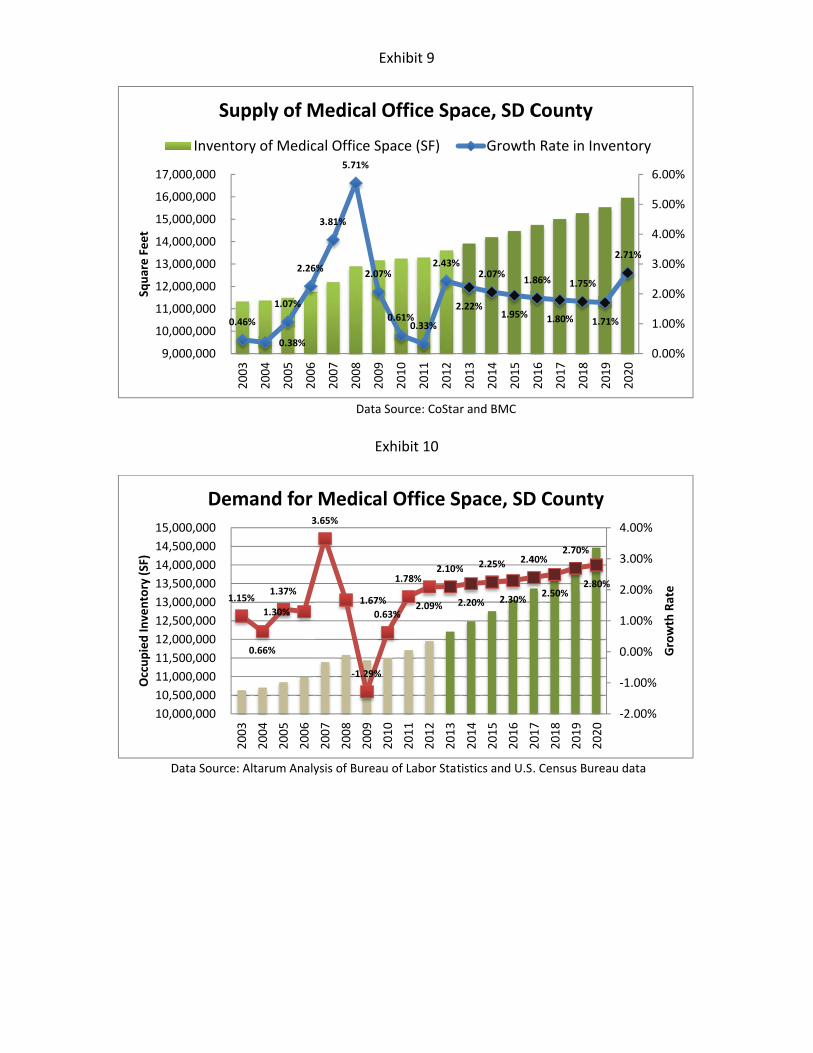

Using several market condition factors, we forecast an increase of 14.7 percent from 2013 to 2020 in medical

office inventory. This equates to an average annual increase of 2 percent. The growth rate and space trends

are shown in Exhibit 9. The rate of growth will remain positive but slow for a while. The 2 percent average

increase will result in an average of 300,000 square feet of deliveries per year until 2020.

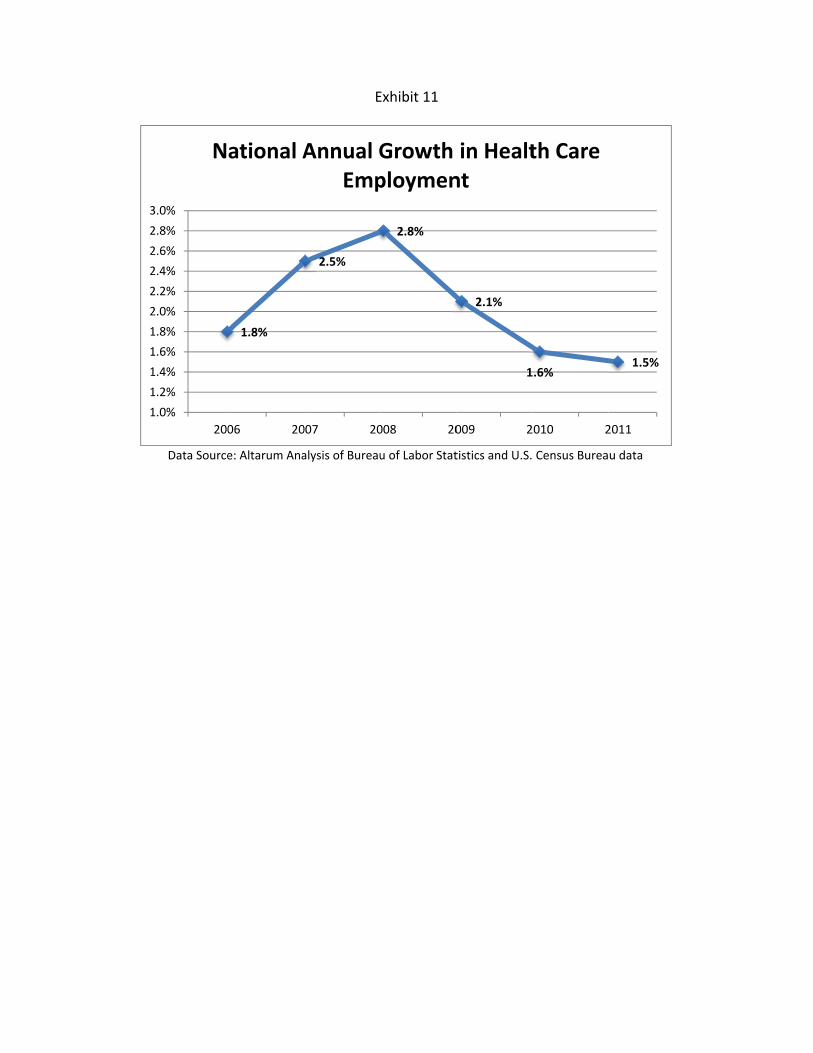

The Altarum analysis of Bureau of Labor and Statistics and the U.S. Census Bureau data, as illustrated in Exhibit

10, indicates an average annual growth rate in health care employment of 2.1 percent over the course of 2006

to 2011, with a high of 2.8 percent in 2008, as seen in Exhibit 11. We expect to see a higher figure than the 2.1

percent growth rate going forward averaging 2.4 percent over the next eight years and rising to 2.8 percent in

2020. According to data from the Center for Disease Control, the population segment aged 65 and over visit

their health care provider more frequently than their younger counterparts. With an aging demographic in San

Diego, as well as in the United States, there will undoubtedly lead to increased demand for health care. The

Affordable Health Care Act known as Obamacare increases coverage of the population and could shift demand

away from emergency rooms to clinics and regular physicians. At the same time Medicare reimbursement

rates, expected to be reduced will also play a part in the future demand for medical office space.

Reimbursement rates are simply the payment a doctor receives for a particular procedure performed on a

patient in the Medicare system. The lower reimbursements suggested by current policy strategies and the

greater the regulatory reporting and billing costs burden imposed, the less incentive doctors have to accept

and treat such patients. With an aging physician population, many of them may decide retirement or selling

their practice to larger hospitals and clinics is a better alternative to staying in private practice. This may shift

some of the demand away from smaller medical office tenancy towards larger facilities affecting the vacancy

rates of the lower quality smaller scaled and generally older medical office stock. In the past few years, there

have also been reports of Medicare dependent doctors and their practices entering into financial difficulties

due to not being able to cover their operating expenses with declining reimbursement rates. Smaller medical

office tenants, especially those with a heavy Medicare practice, may not be as reliable and secure as they once

were. “With the uncertainty of the future of this country’s healthcare system, it is more important than ever

for physicians to control their overhead costs and reduce their risk exposure in order to most effectively

position their practices for the future,” added JP Roach of Hughes Marino.

Value Trends: Characteristics of highly‐sought after medical office space includes higher quality space with

more efficient layouts and close proximity to hospitals. We will see a premium being paid for these buildings.

In regards to multi‐tenant medical office spaces, we see a continued trend of preferences for ancillary services

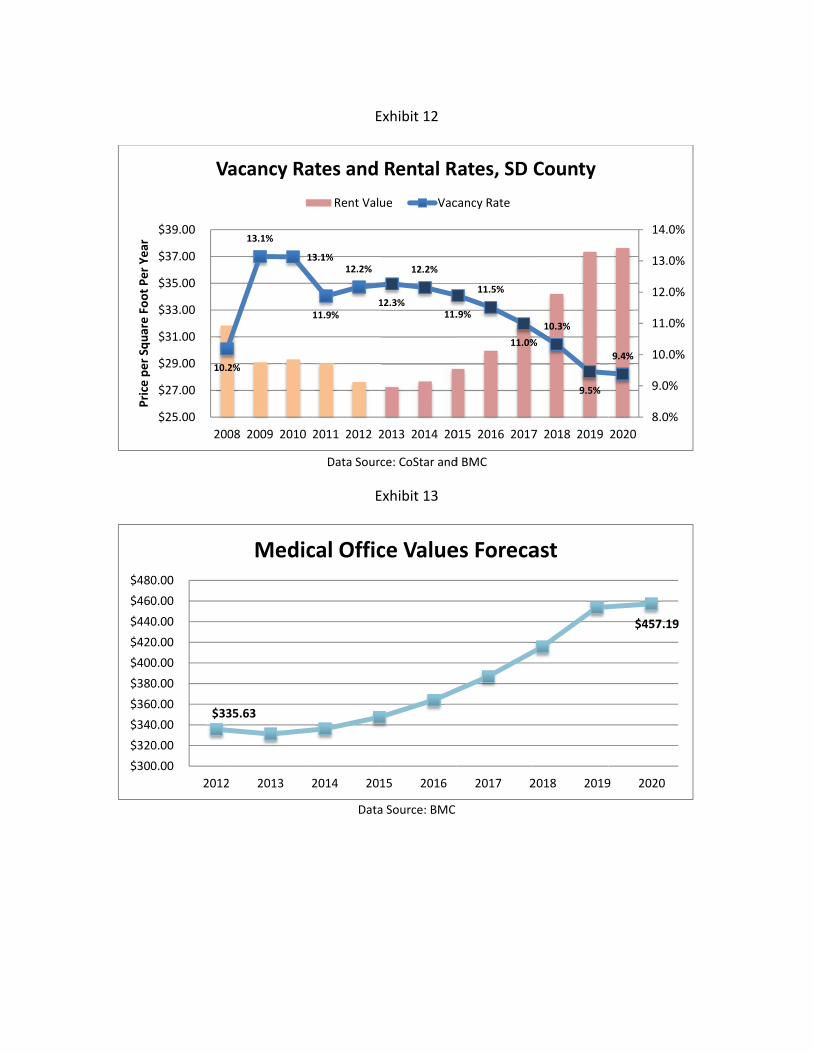

to be located in the same building. In 2012, vacancy for medical office buildings in San Diego was 12.2 percent.

We expect this vacancy rate to increase in 2013. In the long term, vacancy rates will decline, reaching a low of

9.4 percent by the end of the decade. According to our model, average rental rates will rise as vacancy falls,

reaching $37.65 in 2020. This analysis is shown in Exhibit 12. This rental rate, of $37.65, is 36 percent higher

than the average rental rate of $27.64 observed in 2012. In the value analysis, seen in Exhibit 13, average price

per square foot for medical office space in San Diego County is forecast to rise to $457 by 2020. This is a 38

percent increase from our 2013 values. Although this is an optimistic scenario, we believe that the

fundamental trends show us that values will reach that vicinity later this decade. At the same time, there will

be a high dispersion of medical office property values with the new on‐campus facilities at high premiums

compared to that of older medical office buildings. Technological advancements and flight to quality will add

to the price dispersion observed.

Square Feet

Occupied In

ventory (SF)

Data Sourc

9,000,000

10,000,000

11,000,000

12,000,000

13,000,000

14,000,000

15,000,000

16,000,000

17,000,000

S

Inven

10,000,000

10,500,000

11,000,000

11,500,000

12,000,000

12,500,000

13,000,000

13,500,000

14,000,000

14,500,000

15,000,000

De

ce: Altarum An

0.46%

0.38%

1.07%

2.

2003

2004

2005

Supply of

ntory of Med

1.15%

0.66%

1.37%

1.30%

2003

2004

2005

2006

emand fo

E

Data

E

alysis of Burea

%

.26%

3.81%

5.71%

2.07

2006

2007

2008

2009

Medical

dical Office S

3.65%

1.67%

‐1.29%

0.

2006

2007

2008

2009

or Medica

Exhibit 9

a Source: CoSta

Exhibit 10

au of Labor Sta

7%

0.61%0.33%

2.43%

2

2009

2010

2011

2012

Office Sp

Space (SF)

%

%

.63%

1.78%

2.09%

2.10%

2010

2011

2012

2013

al Office S

ar and BMC

tistics and U.S

%

2.22%

2.07%

1.95%

1.8

2013

2014

2015

pace, SD C

Growth

%

2.20%

2.25%

2.30%

2.4

2014

2015

2016

2017

Space, SD

. Census Burea

86%

1.80%

1.75%

1.71

2016

2017

2018

2019

County

h Rate in Inv

40%

2.50%

2.70%

2.80%

2017

2018

2019

2020

D County

au data

1%

2.71%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

2019

2020

entory

%

‐2.00%

‐1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

Growth Rate

%

%

%

%

%

%

%

1

1

1

1

1

2

2

2

2

2

3

Data Source

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

2.2%

2.4%

2.6%

2.8%

3.0%

200

N

e: Altarum Ana

1.8%

06 20

ational A

E

alysis of Bureau

2.5%

007 20

Annual GEmp

Exhibit 11

u of Labor Stat

2.8%

008 20

Growth ploymen

tistics and U.S.

2.1%

1

009 2

in Healtnt

Census Burea

1.6%

2010 2

th Care

u data

1.5%

2011

Price per Square Foot Per Year

$300

$320

$340

$360

$380

$400

$420

$440

$460

$480

10.2

$25.00

$27.00

$29.00

$31.00

$33.00

$35.00

$37.00

$39.00

200

Va

$33

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

2012

2%

13.1%

08 2009 2010

Vacancy R

35.63

2 2013

Medi

E

Data Sour

E

Data

13.1%

11.9%

12.2%

1

0 2011 2012 2

ates and

Rent Valu

2014 20

ical Offic

Exhibit 12

ce: CoStar and

Exhibit 13

a Source: BMC

12.3%

12.2%

11.

2013 2014 20

Rental R

ue Vac

15 2016

ce Value

d BMC

.9%

11.5%

11.0%

015 2016 2017

Rates, SD

cancy Rate

2017 2

es Foreca

%

10.3%

9.5%

7 2018 2019

County

2018 2019

ast

9.4%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

2020

$457.19

9 2020

%

%

%

%

%

Recommended