Chapter 2Financial Statements

and Cash Flows

2.1Financial Statements

Financial Statements Balance sheetIncome statementStatement of cash flows

Balance SheetStatement of financial position.The balance sheet is a financial statement

that shows the firm’s assets, liabilities and equity at a given point in time.

Balance Sheet IdentityAssets = Liabilities + Shareholders’ Equity

(Owner’s Equity)

Assets and LiquidityThe speed and ease with which an asset can

be converted to cash.Ease of conversion to cash.Without significant loss in value.

Trade-off between the advantages of liquidity and foregone potential profits.The more liquid a firm is, the less likely it is to

experience financial distress.The return on liquid assets is low.

Debt versus EquityShareholder’s equity = Assets – LiabilitiesShareholder’s equity is the residual portion

and equity owners are entitled to only the residual value.

The use of debt in a firm’s capital is called financial leverage. The more debt a firm has, the greater of financial leverage.

Net Working CapitalNet Working Capital = Current Assets – Current

LiabilitiesPositive when current assets exceed current

liabilities.Positive when the cash that will become

available over the next 12 months exceeds the cash that will be paid over the next 12 months.

Usually positive in a healthy firm.

Market Value versus Book ValueBook value – the balance sheet

Assets at historical costs.Market value - the price at which an item

could be bought or soldStockholder wealth maximization is to

maximize the market value of the stock, not the book value.

Income StatementProfit and loss statement.Statement of financial performance.The income statement shows the revenue and

expenses of a firm during a period of time.Revenue – Expenses = IncomeAccounting net income is not the same as

cash flow. Depreciation, a noncash expense, is deducted

when net income is calculated.

Sources and Uses of CashSources of cash

Cash inflowsDecrease in assets other than cash Increase in liabilities or equity

Uses of cashCash outflowsIncrease in assets other than cashDecrease in liabilities or equity

Statement of Cash FlowsThe statement which summarizes the

sources and uses of cash.Three categories

Operating activitiesInvestment activities Financing activities

2.2Cash Flows

Cash FlowThe difference between the number of money

that came in and the number that went out.The actual net cash, as opposed to

accounting net income, that flows into or out of a firm during a certain period.

Free cash flow refers to the cash that the firm is free to distribute to creditors or stockholders because it is not needed for working capital or fixed asset investment.

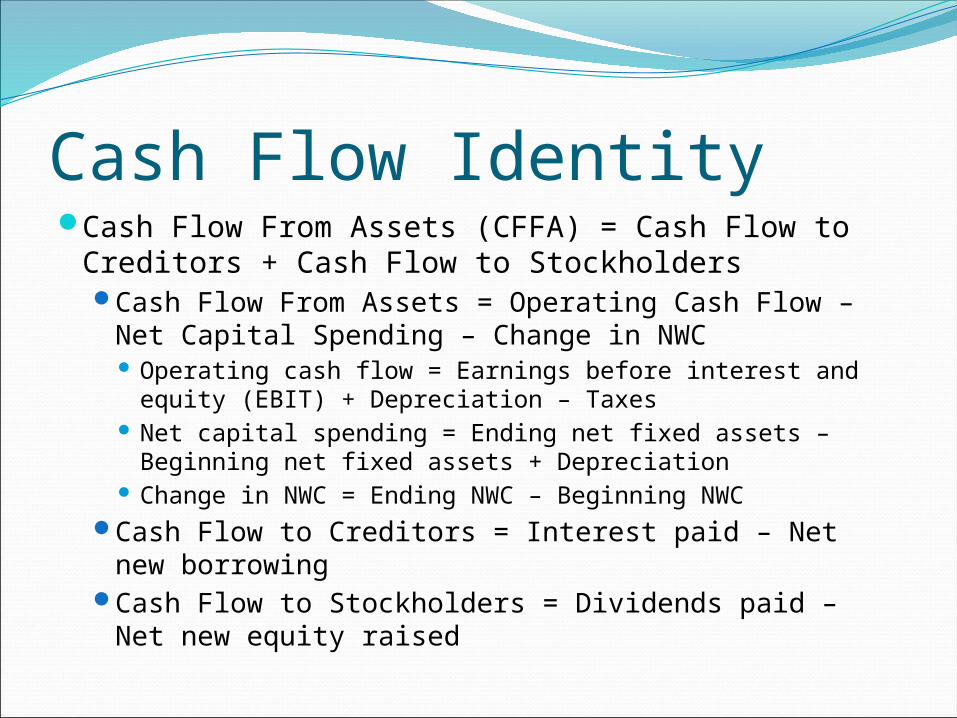

Cash Flow IdentityCash Flow From Assets (CFFA) = Cash Flow to

Creditors + Cash Flow to StockholdersCash Flow From Assets = Operating Cash Flow –

Net Capital Spending – Change in NWC Operating cash flow = Earnings before interest and

equity (EBIT) + Depreciation – Taxes Net capital spending = Ending net fixed assets –

Beginning net fixed assets + Depreciation Change in NWC = Ending NWC – Beginning NWC

Cash Flow to Creditors = Interest paid – Net new borrowing

Cash Flow to Stockholders = Dividends paid – Net new equity raised

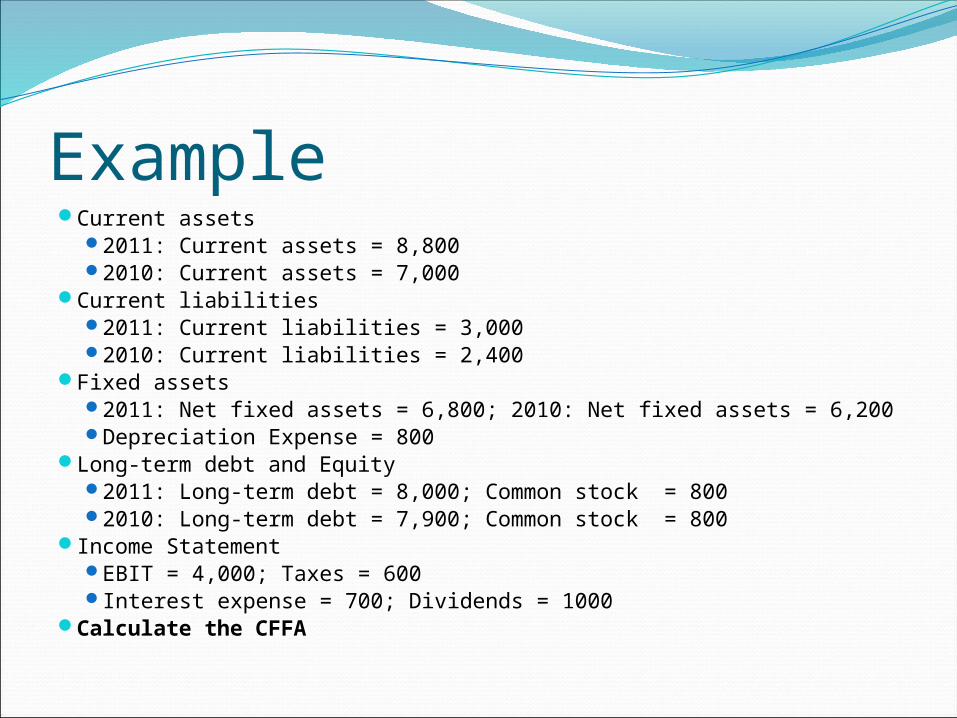

Example Current assets

2011: Current assets = 8,800 2010: Current assets = 7,000

Current liabilities 2011: Current liabilities = 3,000 2010: Current liabilities = 2,400

Fixed assets 2011: Net fixed assets = 6,800; 2010: Net fixed assets = 6,200 Depreciation Expense = 800

Long-term debt and Equity 2011: Long-term debt = 8,000; Common stock = 800 2010: Long-term debt = 7,900; Common stock = 800

Income Statement EBIT = 4,000; Taxes = 600 Interest expense = 700; Dividends = 1000

Calculate the CFFA

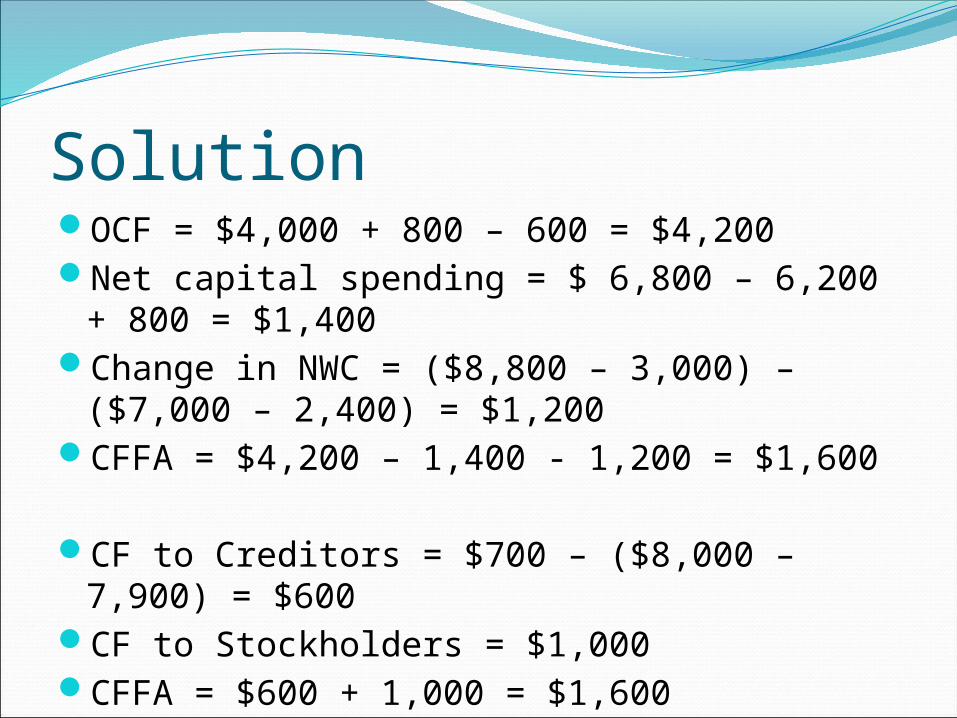

SolutionOCF = $4,000 + 800 – 600 = $4,200Net capital spending = $ 6,800 – 6,200 + 800

= $1,400Change in NWC = ($8,800 – 3,000) – ($7,000

– 2,400) = $1,200CFFA = $4,200 – 1,400 - 1,200 = $1,600

CF to Creditors = $700 – ($8,000 – 7,900) = $600

CF to Stockholders = $1,000CFFA = $600 + 1,000 = $1,600

2.3Working withFinancial Statements

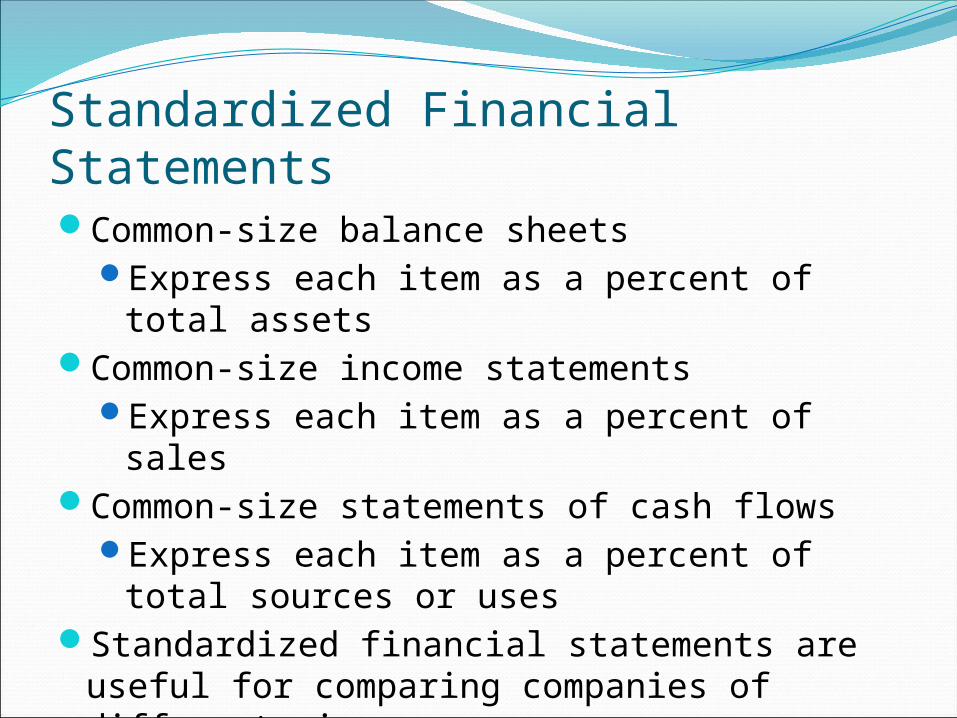

Standardized Financial StatementsCommon-size balance sheets

Express each item as a percent of total assets

Common-size income statementsExpress each item as a percent of sales

Common-size statements of cash flowsExpress each item as a percent of total

sources or usesStandardized financial statements are useful

for comparing companies of different sizes.

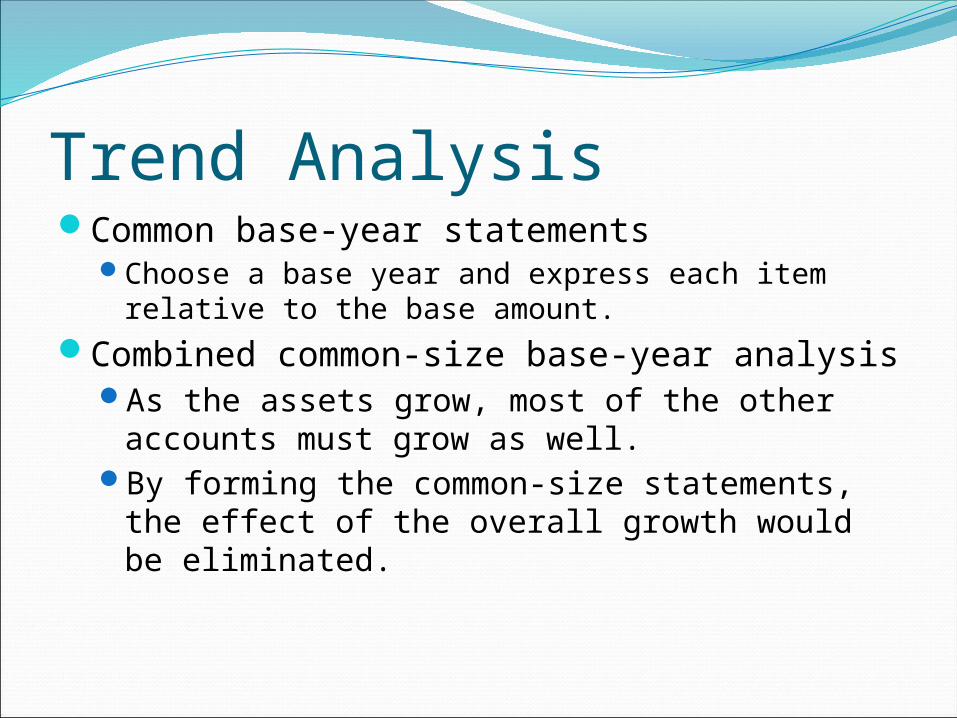

Trend AnalysisCommon base-year statements

Choose a base year and express each item relative to the base amount.

Combined common-size base-year analysisAs the assets grow, most of the other accounts

must grow as well.By forming the common-size statements, the

effect of the overall growth would be eliminated.

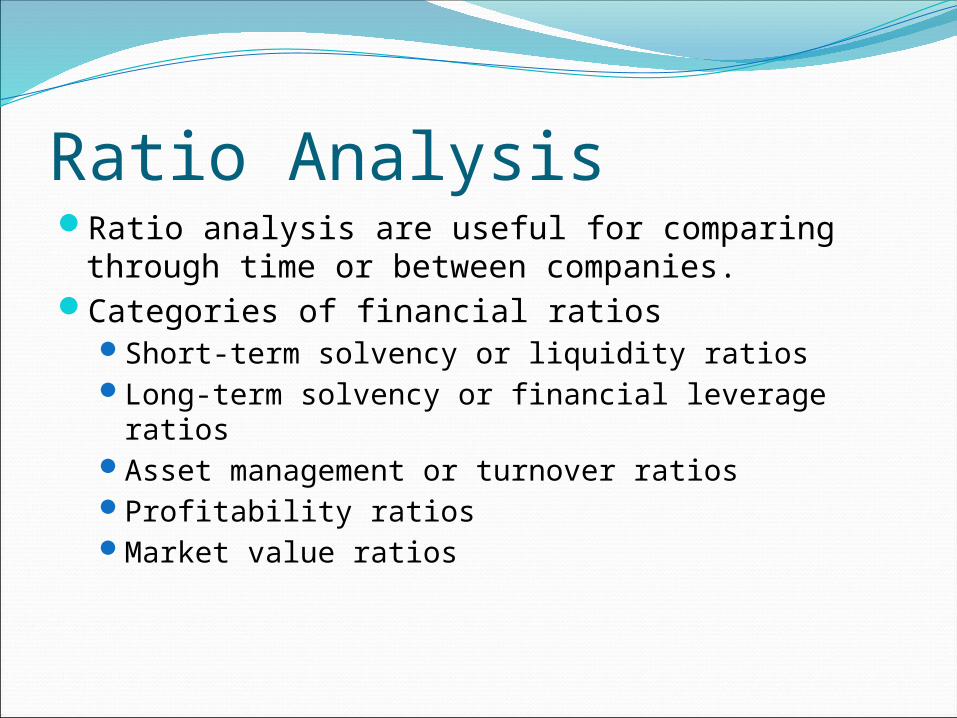

Ratio AnalysisRatio analysis are useful for comparing through

time or between companies.Categories of financial ratios

Short-term solvency or liquidity ratiosLong-term solvency or financial leverage ratiosAsset management or turnover ratiosProfitability ratiosMarket value ratios

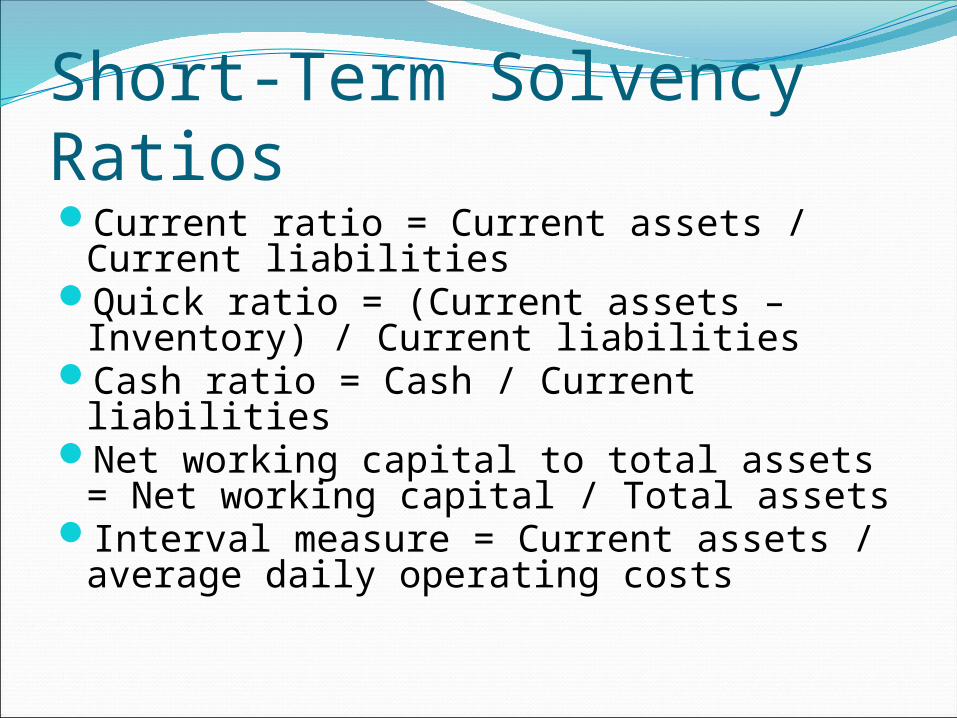

Short-Term Solvency RatiosCurrent ratio = Current assets / Current

liabilitiesQuick ratio = (Current assets – Inventory)

/ Current liabilitiesCash ratio = Cash / Current liabilitiesNet working capital to total assets = Net

working capital / Total assetsInterval measure = Current assets /

average daily operating costs

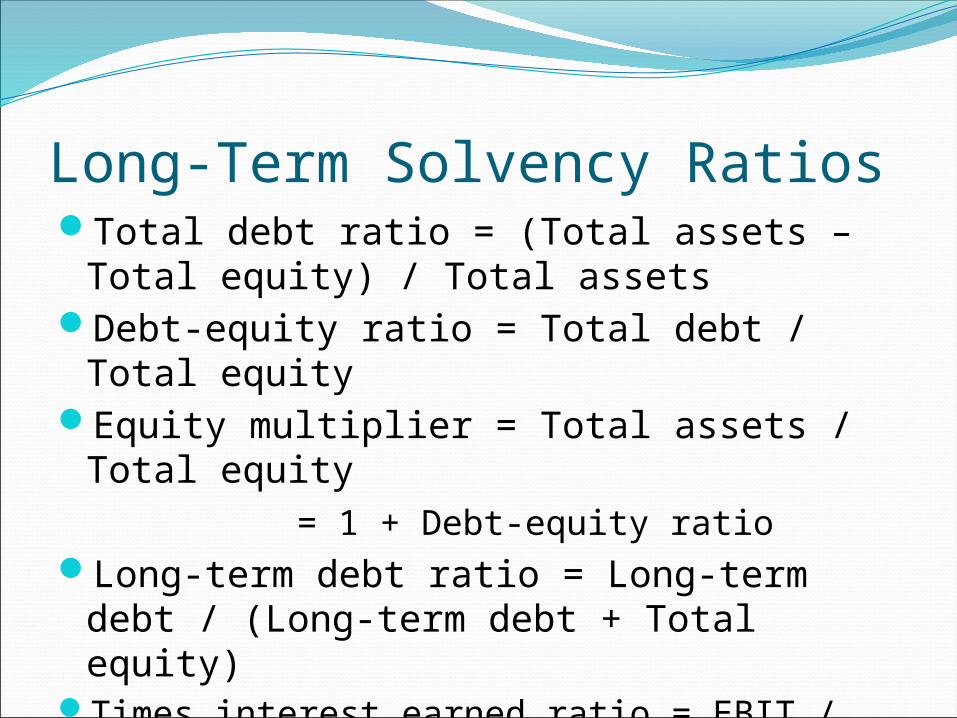

Long-Term Solvency RatiosTotal debt ratio = (Total assets – Total

equity) / Total assetsDebt-equity ratio = Total debt / Total

equityEquity multiplier = Total assets / Total

equity = 1 + Debt-equity ratio

Long-term debt ratio = Long-term debt / (Long-term debt + Total equity)

Times interest earned ratio = EBIT / InterestCash coverage ratio = (EBIT +

Depreciation) / Interest

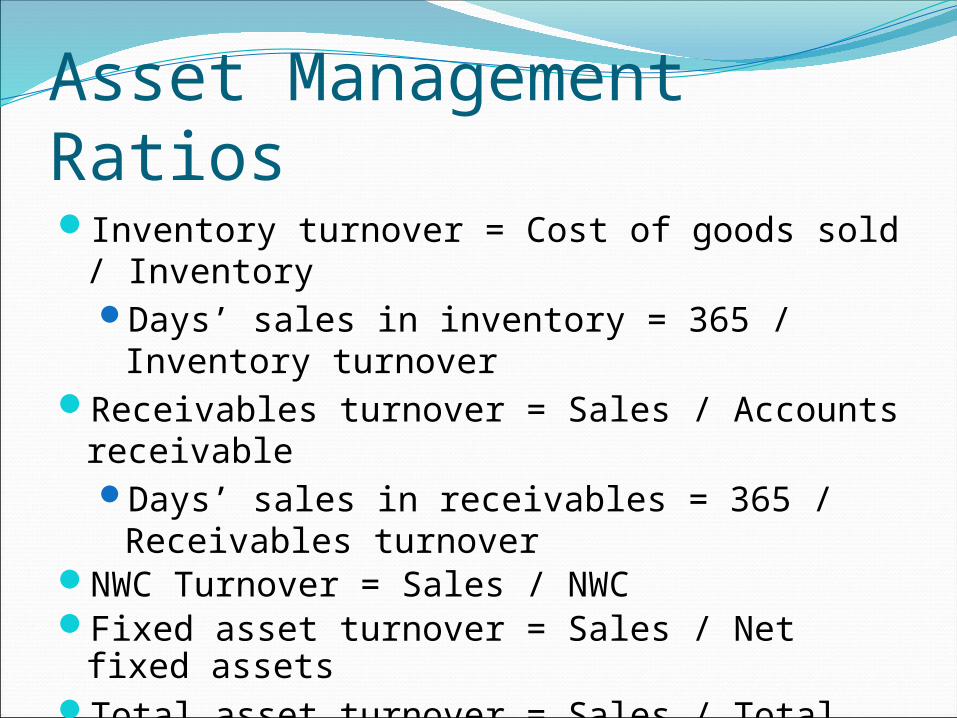

Asset Management RatiosInventory turnover = Cost of goods sold /

InventoryDays’ sales in inventory = 365 / Inventory

turnoverReceivables turnover = Sales / Accounts

receivableDays’ sales in receivables = 365 /

Receivables turnoverNWC Turnover = Sales / NWCFixed asset turnover = Sales / Net fixed

assetsTotal asset turnover = Sales / Total assets

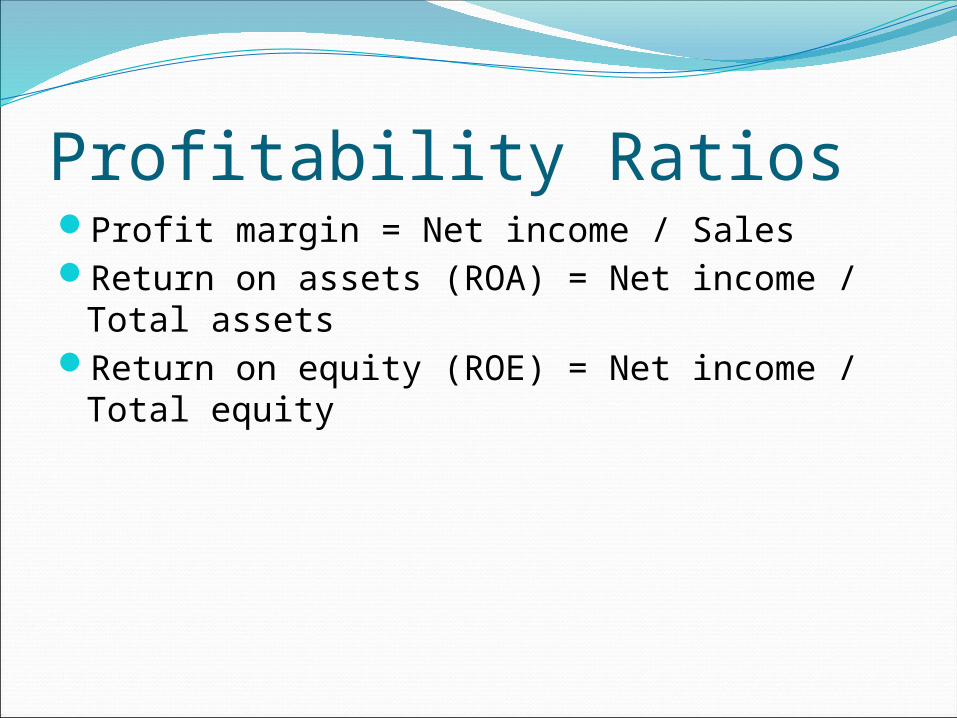

Profitability RatiosProfit margin = Net income / SalesReturn on assets (ROA) = Net income / Total

assetsReturn on equity (ROE) = Net income / Total

equity

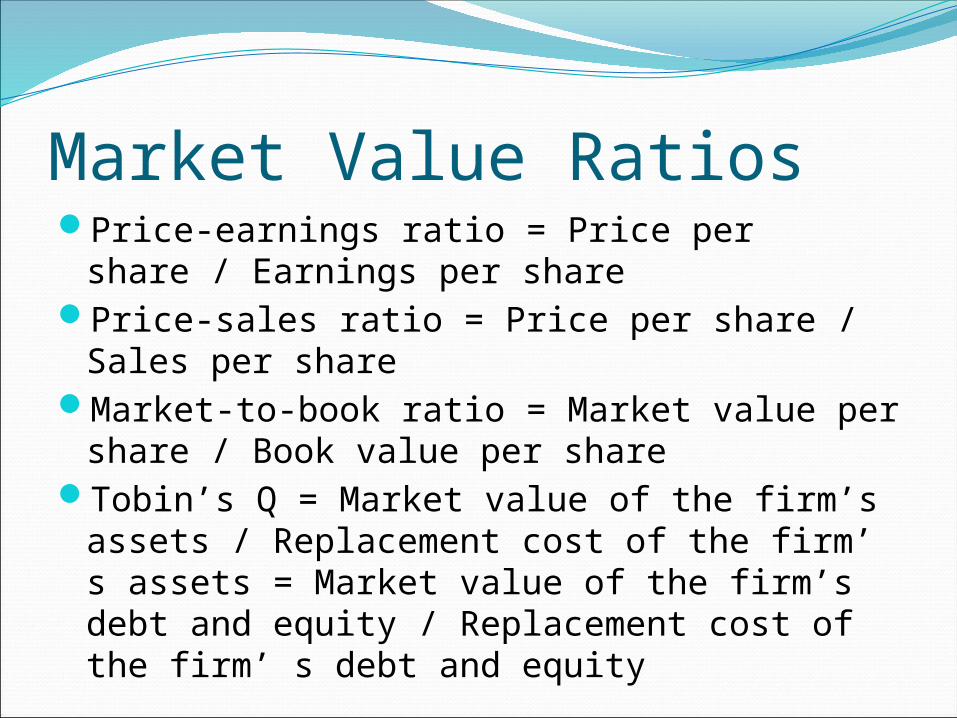

Market Value RatiosPrice-earnings ratio = Price per share /

Earnings per sharePrice-sales ratio = Price per share / Sales per

shareMarket-to-book ratio = Market value per

share / Book value per shareTobin’s Q = Market value of the firm’s

assets / Replacement cost of the firm’ s assets = Market value of the firm’s debt and equity / Replacement cost of the firm’ s debt and equity

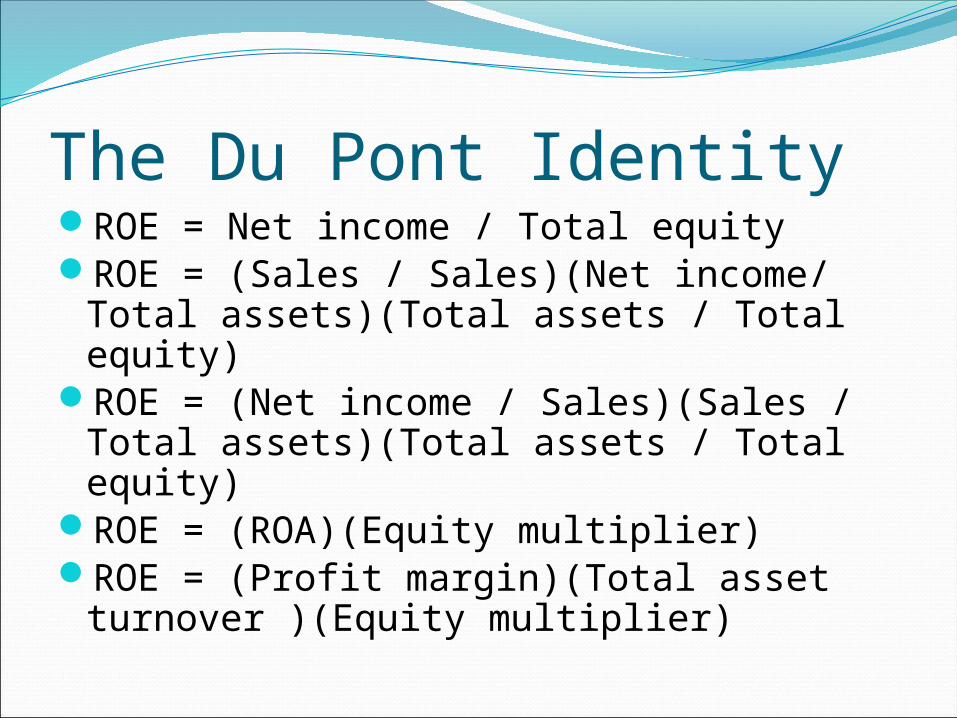

The Du Pont IdentityROE = Net income / Total equityROE = (Sales / Sales)(Net income/ Total

assets)(Total assets / Total equity)ROE = (Net income / Sales)(Sales / Total

assets)(Total assets / Total equity)ROE = (ROA)(Equity multiplier)ROE = (Profit margin)(Total asset

turnover )(Equity multiplier)

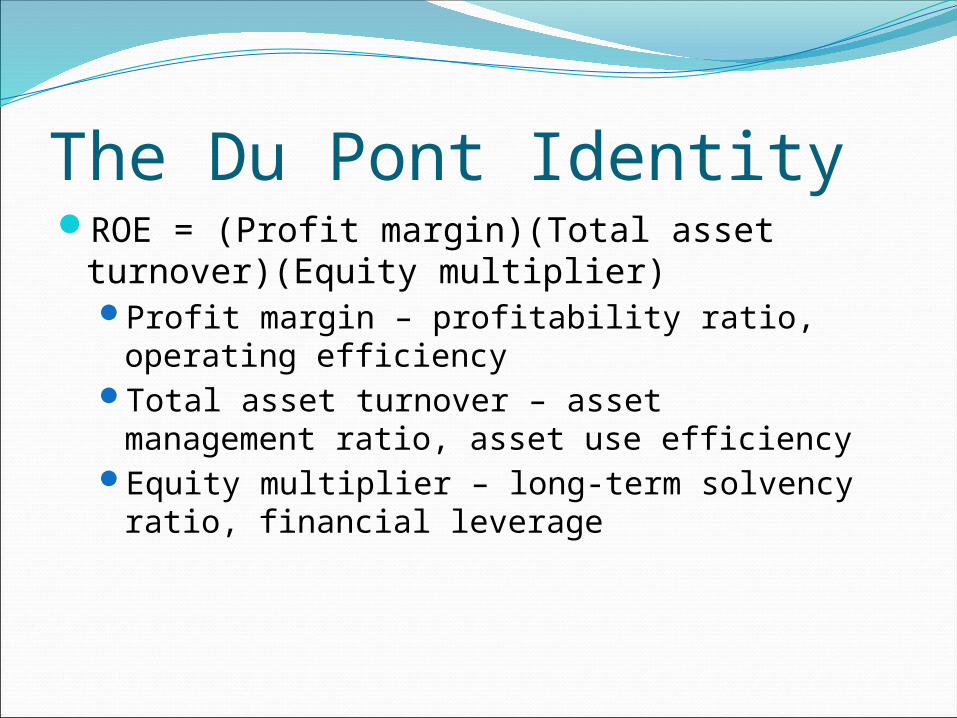

The Du Pont IdentityROE = (Profit margin)(Total asset

turnover)(Equity multiplier)Profit margin – profitability ratio, operating

efficiency Total asset turnover – asset management

ratio, asset use efficiencyEquity multiplier – long-term solvency ratio,

financial leverage

Why Evaluate Financial Statements?Internal uses

Performance evaluationPlanning for the future

External usesCreditorsSuppliersCustomersCredit-rating agencies

Choosing a BenchmarkTime-trend analysis

Compared to historyPeer group analysis

Compare to the peer group

LimitationsThe results of ratio analysis depend on the

quality of financial statements. It is difficult for diversified firms to find a

benchmark.Factors such as inflation, different operating

and accounting practices, seasonal factors can distort comparisons.

It is difficult to judge whether a particular ratio is “good” or “bad”.

It is difficult to judge whether a firm is “good” or “bad” if some ratios look “good” and some ratios look “bad”.

Recommended