Seðlabanki Íslands

Financial stability in Iceland d

Capital controls

29 November 2012

Financial Stability Department

Overview

• Run up to the financial crises

• Current economic affairs

• Main risks to financial stability

• Capital controls

• Prudential rules

Seðlabanki Íslands

Run up…..

Iceland

• In the 20th century Iceland went from being one of the poorest economies in Europe to a prosperous one – High but volatile growth, -mostly led by fisheries

– From 2/3 of labour force in agriculture to 2/3 in services

• In past decades: liberalization, deregulation and privatization

• Member of the EEA in 1994 – Free movement of capital

– European “passport” for financial institutions headquartered in any country within the area

• At the turn of the century things started to heat up – … and the banks grew

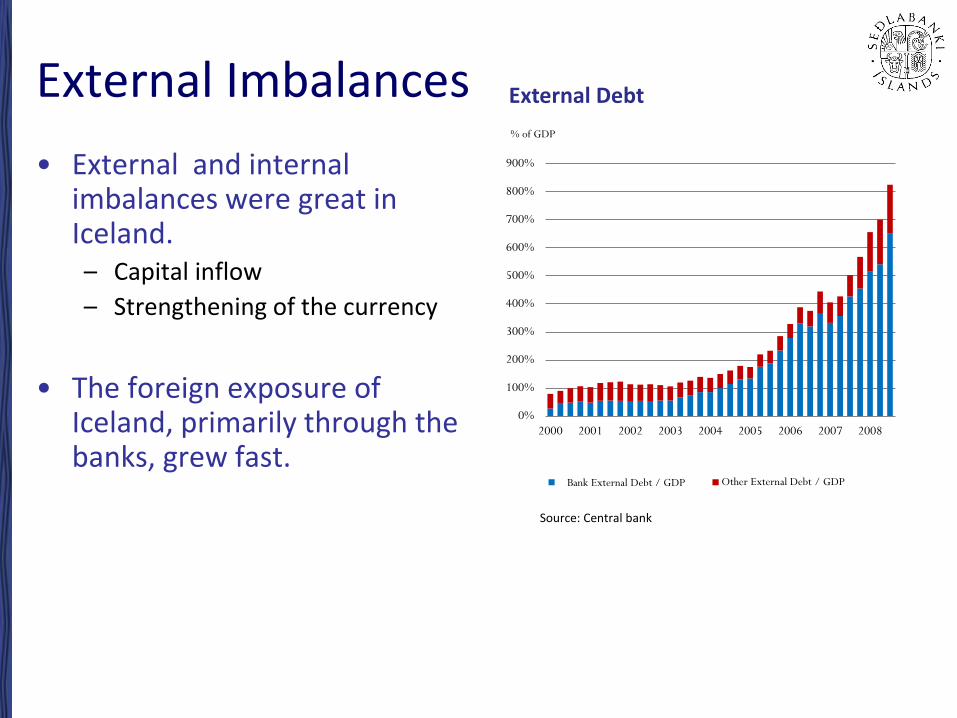

External Imbalances

• External and internal imbalances were great in Iceland. – Capital inflow

– Strengthening of the currency

• The foreign exposure of Iceland, primarily through the banks, grew fast.

0%

100%

200%

300%

400%

500%

600%

700%

800%

900%

2000 2001 2002 2003 2004 2005 2006 2007 2008

% of GDP

External Debt

EBank External Debt/ GDP Other External Debt / GDP

Source: Central bank

Bank External Debt / GDP

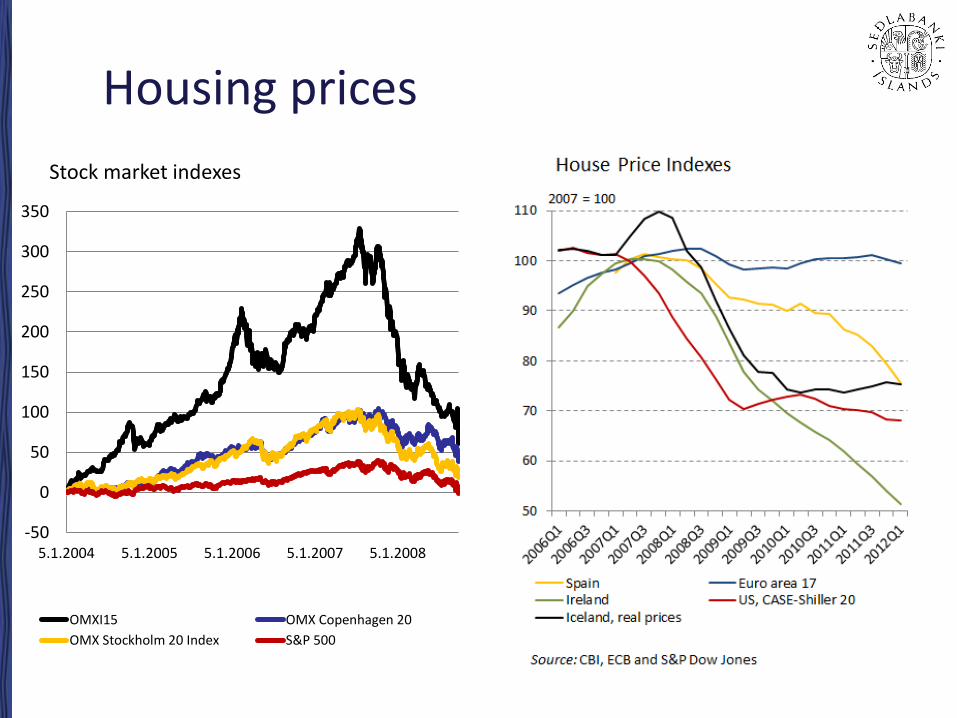

Housing prices

-50

0

50

100

150

200

250

300

350

5.1.2004 5.1.2005 5.1.2006 5.1.2007 5.1.2008

Stock market indexes

OMXI15 OMX Copenhagen 20

OMX Stockholm 20 Index S&P 500

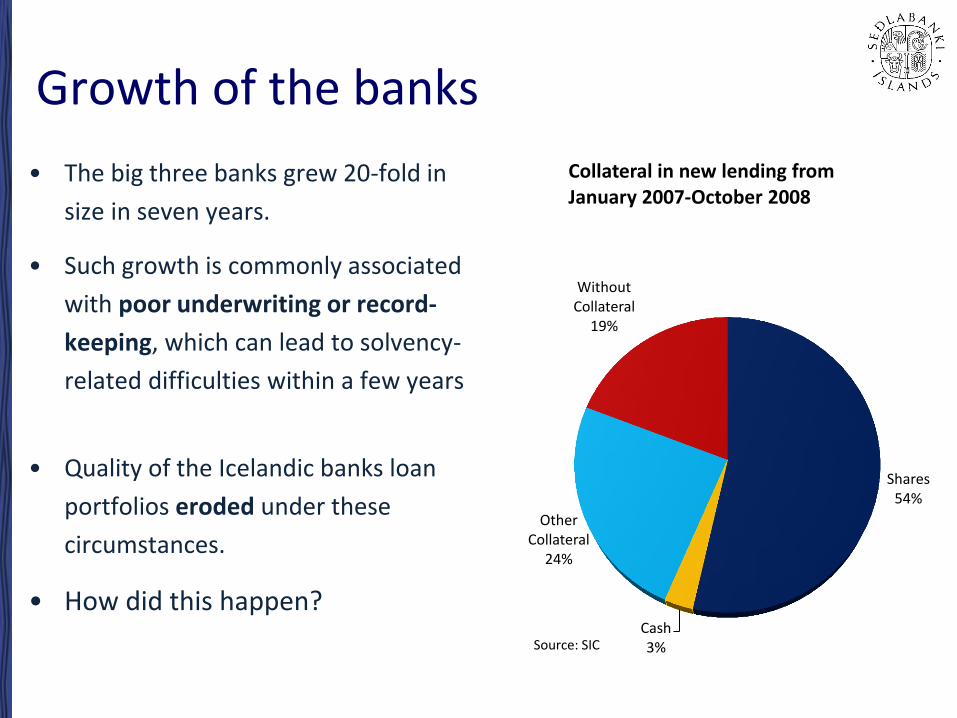

Growth of the banks

• The big three banks grew 20-fold in

size in seven years.

• Such growth is commonly associated

with poor underwriting or record-

keeping, which can lead to solvency-

related difficulties within a few years

• Quality of the Icelandic banks loan

portfolios eroded under these

circumstances.

• How did this happen?

Shares 54%

Cash 3%

Other Collateral

24%

Without Collateral

19%

Collateral in new lending from January 2007-October 2008

Source: SIC

How did they grow?

• A opening of global debt financing markets drove the growth of the banks.

• High credit ratings inherited from Iceland’s sovereign debt rating.

• Early 2006 internatinal debt funding dried up temporary – Geysir Crises

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

2004 2005 2006 2007 2008

bln.Euro

Aggregate bond issues the three big banks

EMTN USMTN OtherSource: SIC

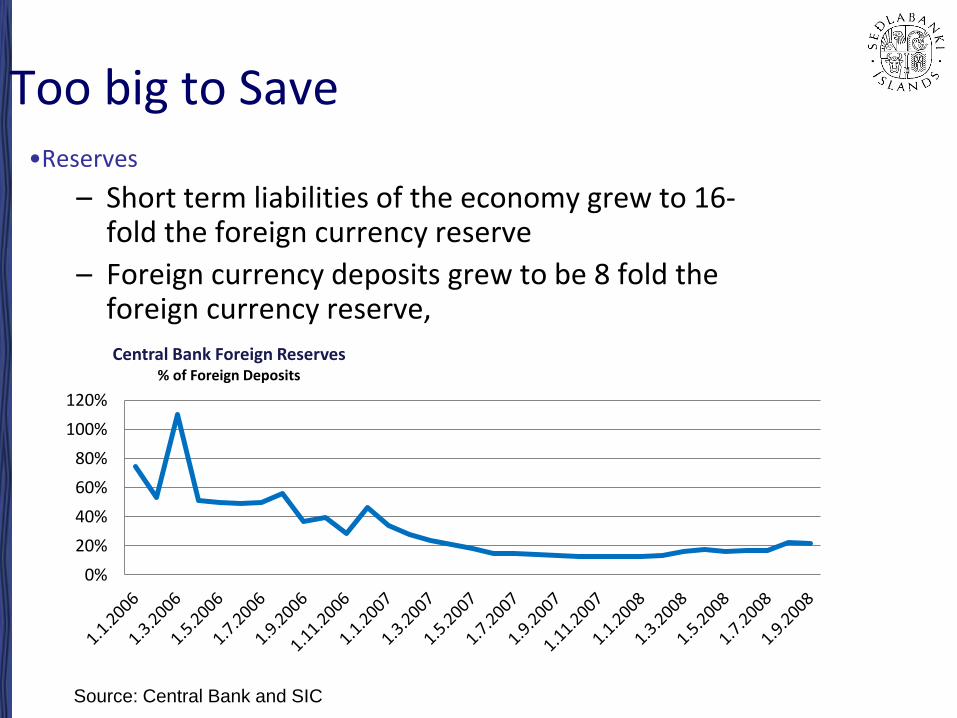

Too big to Save •Reserves

– Short term liabilities of the economy grew to 16-fold the foreign currency reserve

– Foreign currency deposits grew to be 8 fold the foreign currency reserve,

0%

20%

40%

60%

80%

100%

120%

Central Bank Foreign Reserves % of Foreign Deposits

Source: Central Bank and SIC

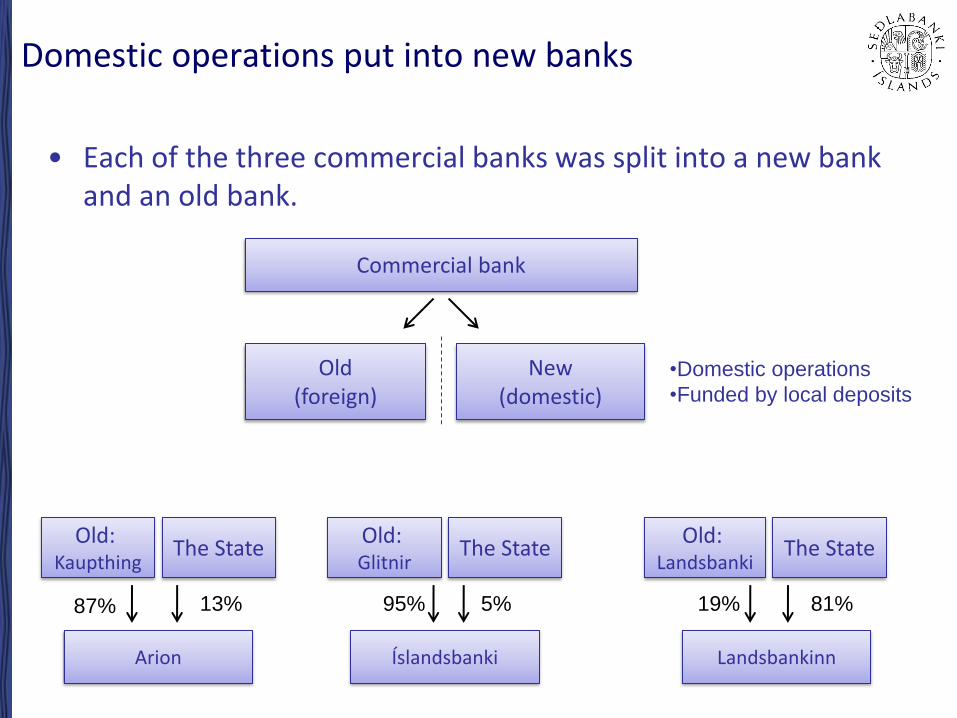

Domestic operations put into new banks

• Each of the three commercial banks was split into a new bank and an old bank.

Old (foreign)

New (domestic)

Commercial bank

•Domestic operations

•Funded by local deposits

Old: Kaupthing

87% 13%

The State Old:

Landsbanki Old: Glitnir

The State The State

Landsbankinn Arion Íslandsbanki

81% 19% 5% 95%

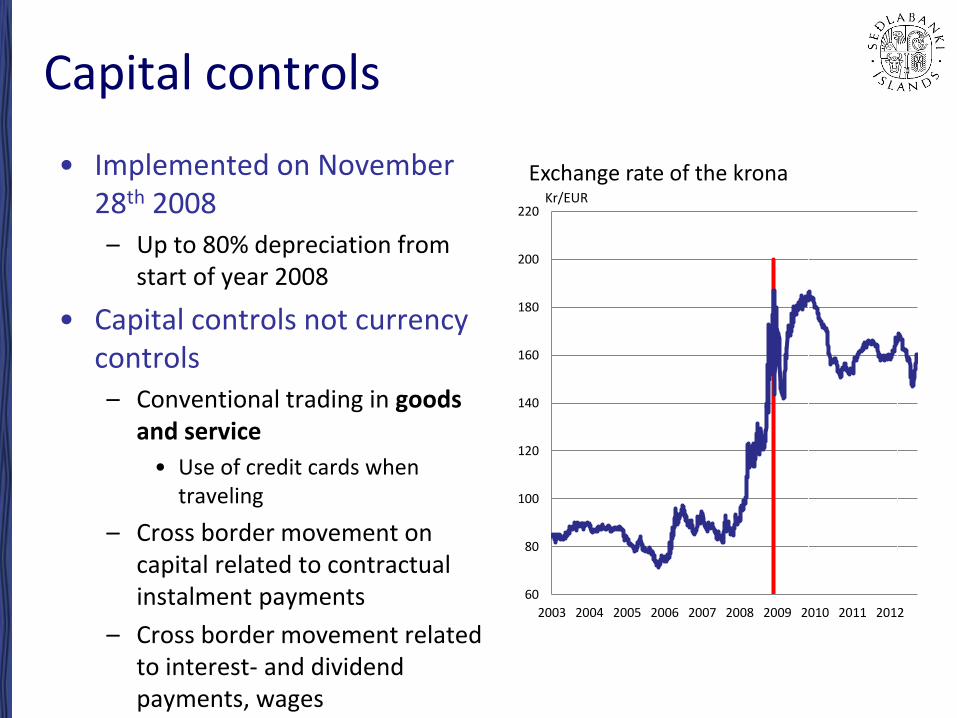

Capital controls

• Implemented on November 28th 2008 – Up to 80% depreciation from

start of year 2008

• Capital controls not currency controls – Conventional trading in goods

and service

• Use of credit cards when traveling

– Cross border movement on capital related to contractual instalment payments

– Cross border movement related to interest- and dividend payments, wages

60

80

100

120

140

160

180

200

220

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Exchange rate of the krona Kr/EUR

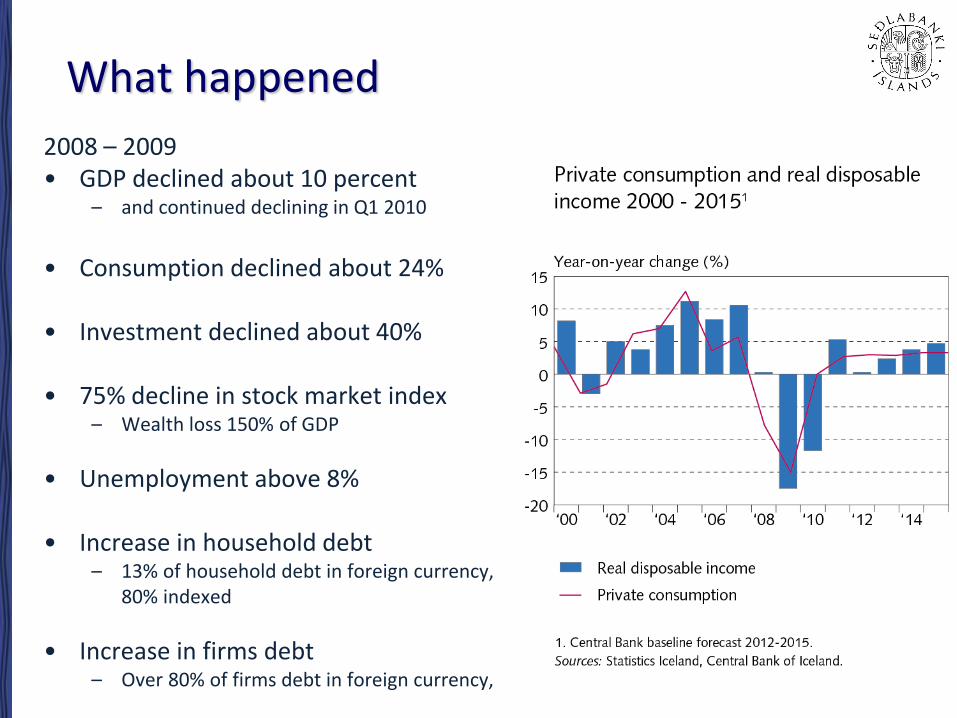

What happened

2008 – 2009 • GDP declined about 10 percent

– and continued declining in Q1 2010

• Consumption declined about 24%

• Investment declined about 40%

• 75% decline in stock market index

– Wealth loss 150% of GDP

• Unemployment above 8%

• Increase in household debt – 13% of household debt in foreign currency,

80% indexed

• Increase in firms debt – Over 80% of firms debt in foreign currency,

Seðlabanki Íslands

Where are we now?

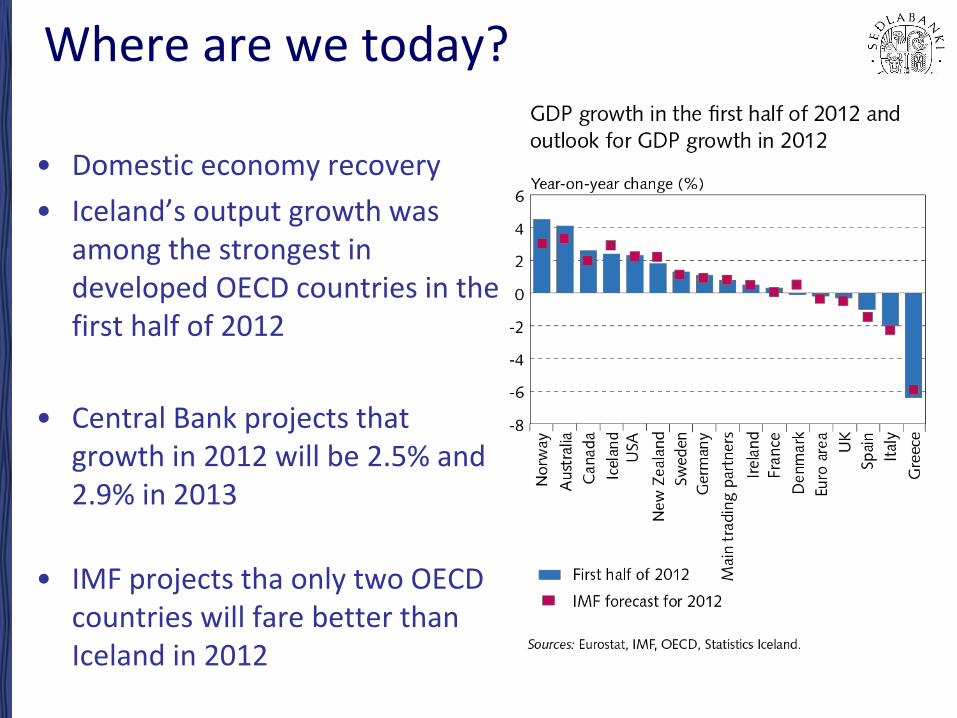

Where are we today?

• Domestic economy recovery

• Iceland’s output growth was among the strongest in developed OECD countries in the first half of 2012

• Central Bank projects that growth in 2012 will be 2.5% and 2.9% in 2013

• IMF projects tha only two OECD countries will fare better than Iceland in 2012

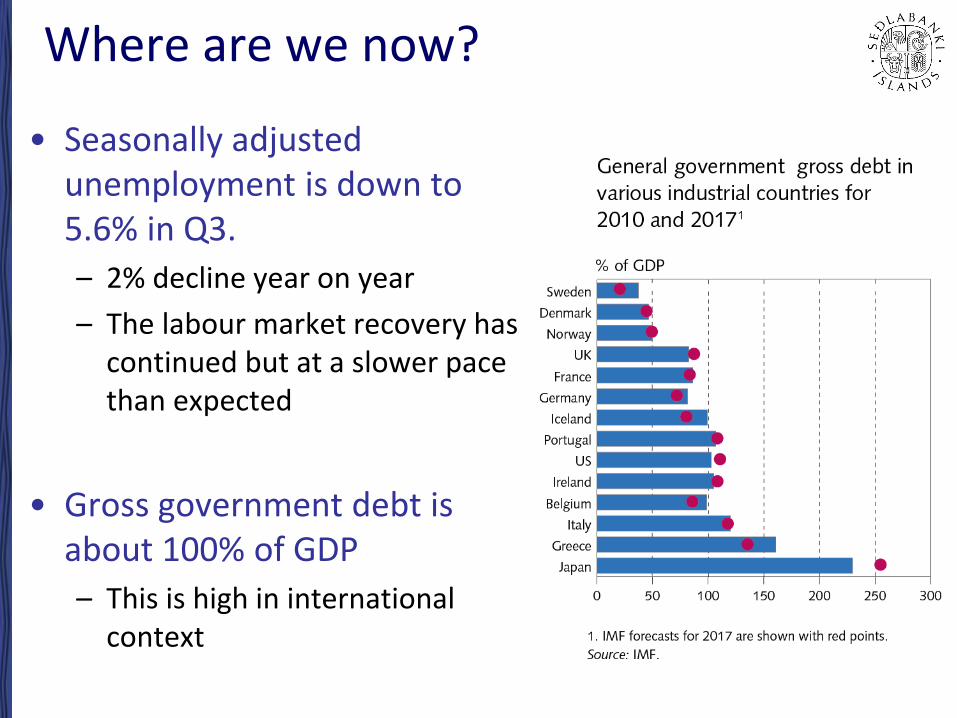

Where are we now?

• Seasonally adjusted unemployment is down to 5.6% in Q3.

– 2% decline year on year

– The labour market recovery has continued but at a slower pace than expected

• Gross government debt is about 100% of GDP

– This is high in international context

Where are we today?

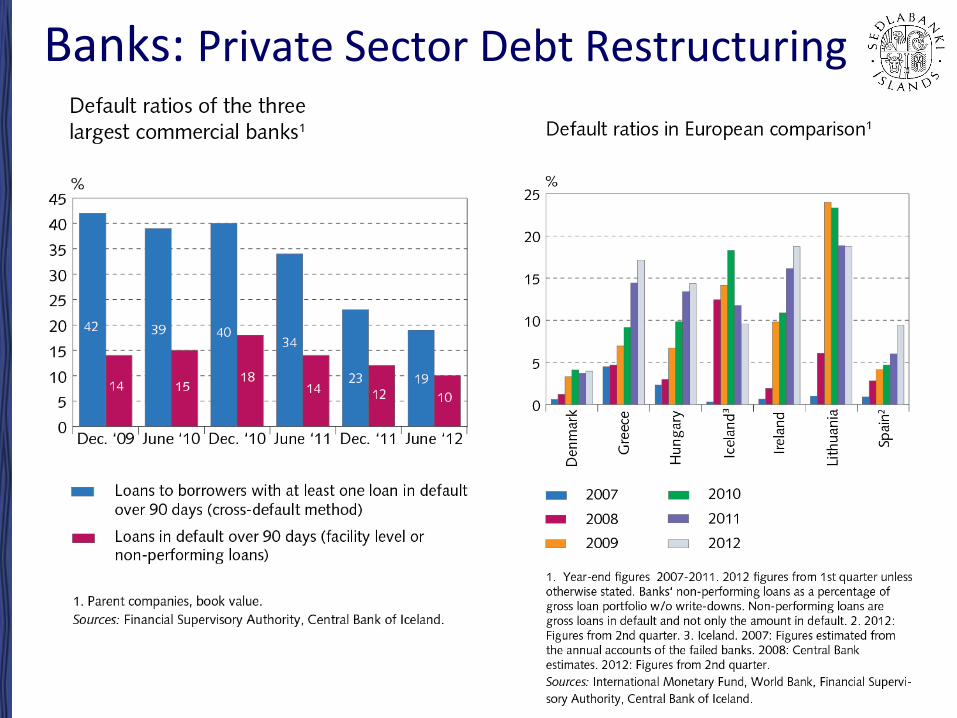

• The Banks seem strong – Average CAD over 23%

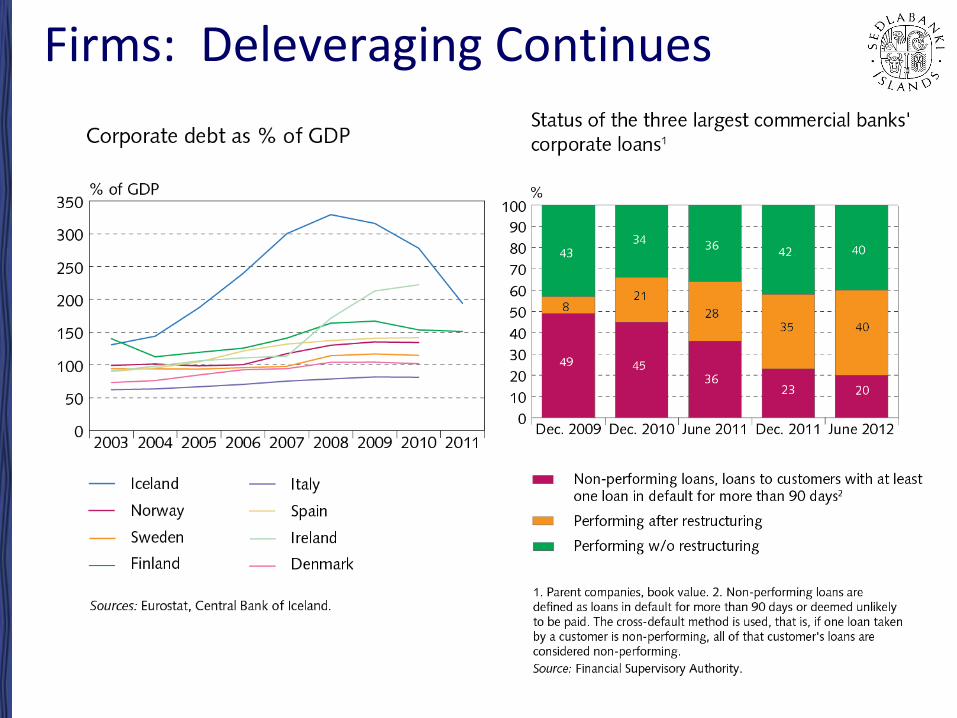

– but we are mindful that they are operating under capital controls

• Deleveraging is ongoing – Financial conditions of households

and firms are improving

Banks: Private Sector Debt Restructuring

Firms: Deleveraging Continues

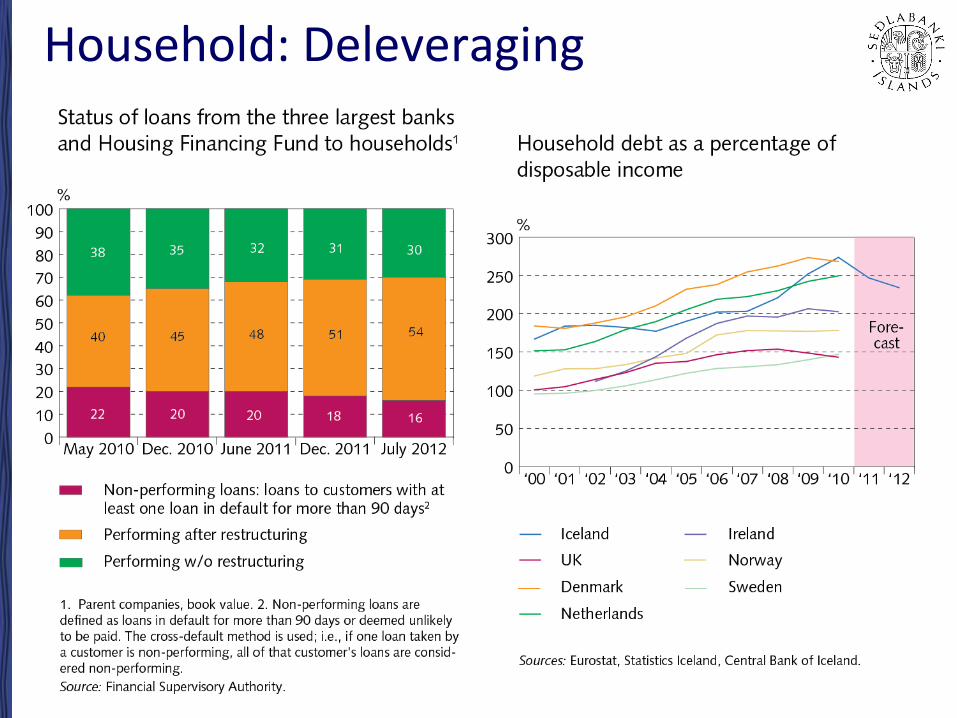

Household: Deleveraging

Main risk factors: Financial Stability Report October 5th

• Ongoing sovereign and financial crises in Europe

• Foreign refinancing risk

• Capital controls

– Risks connected to the liberalization

• Legal uncertainty and uncertainty about government actions

• The Housing Finance Fund

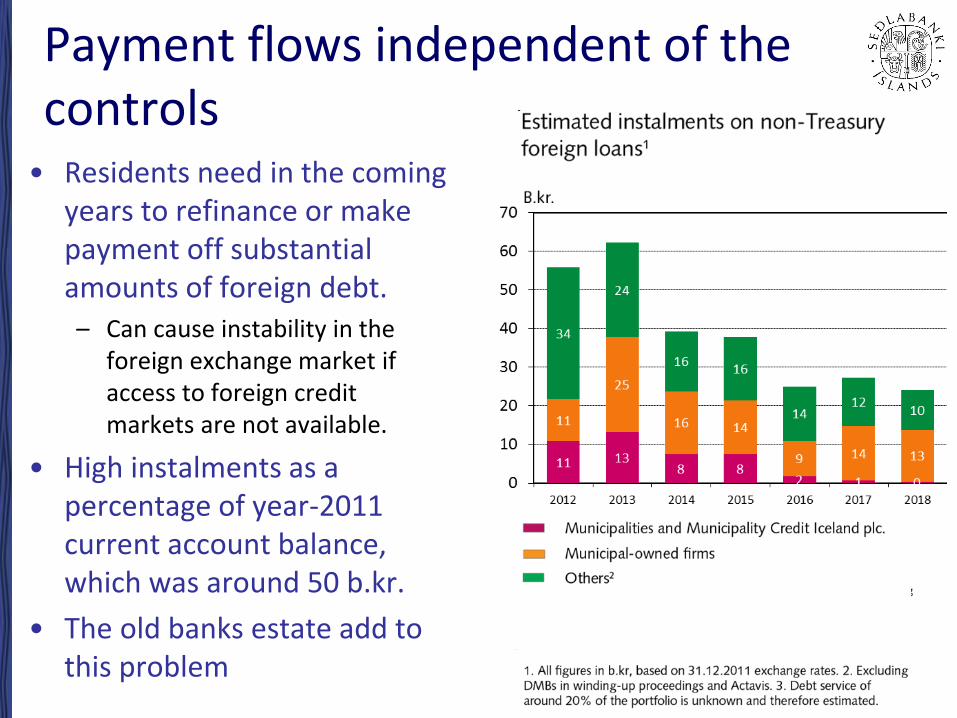

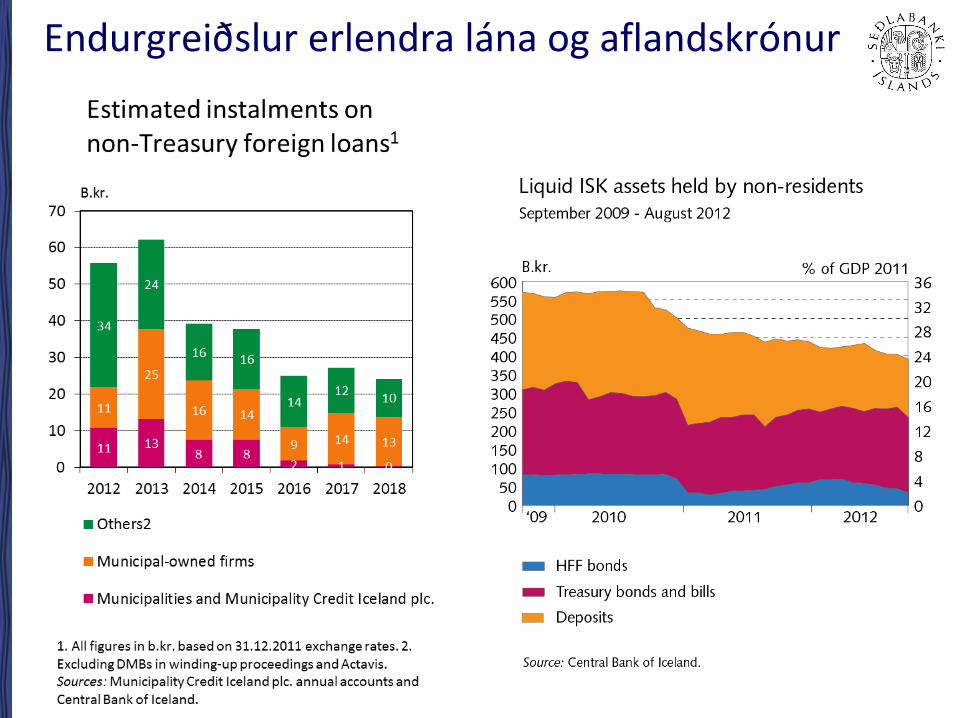

Payment flows independent of the controls

• Residents need in the coming years to refinance or make payment off substantial amounts of foreign debt. – Can cause instability in the

foreign exchange market if access to foreign credit markets are not available.

• High instalments as a percentage of year-2011 current account balance, which was around 50 b.kr.

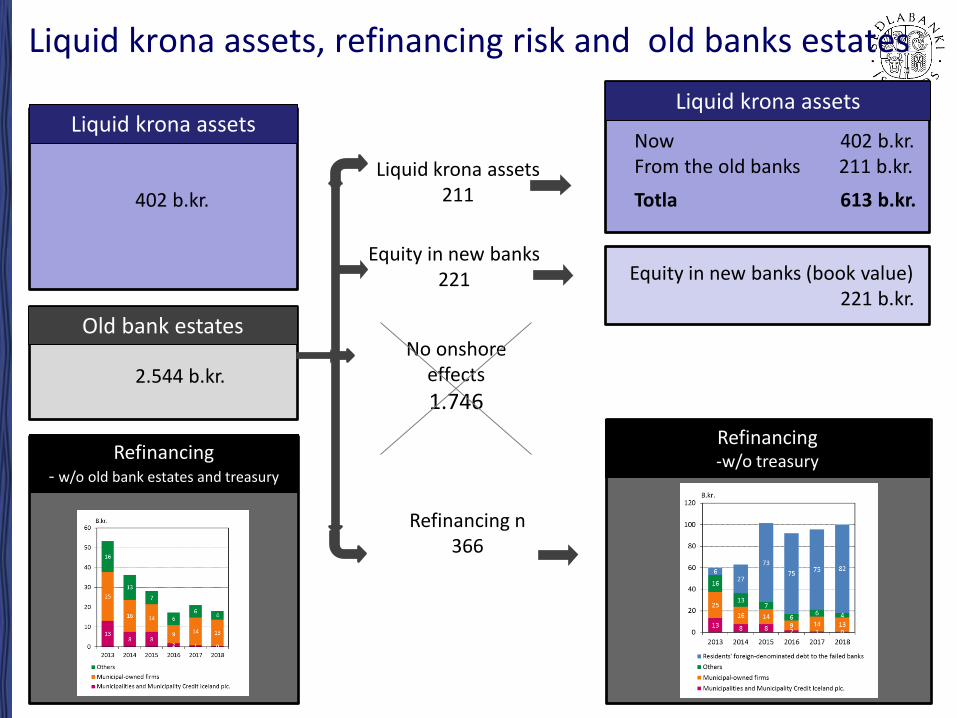

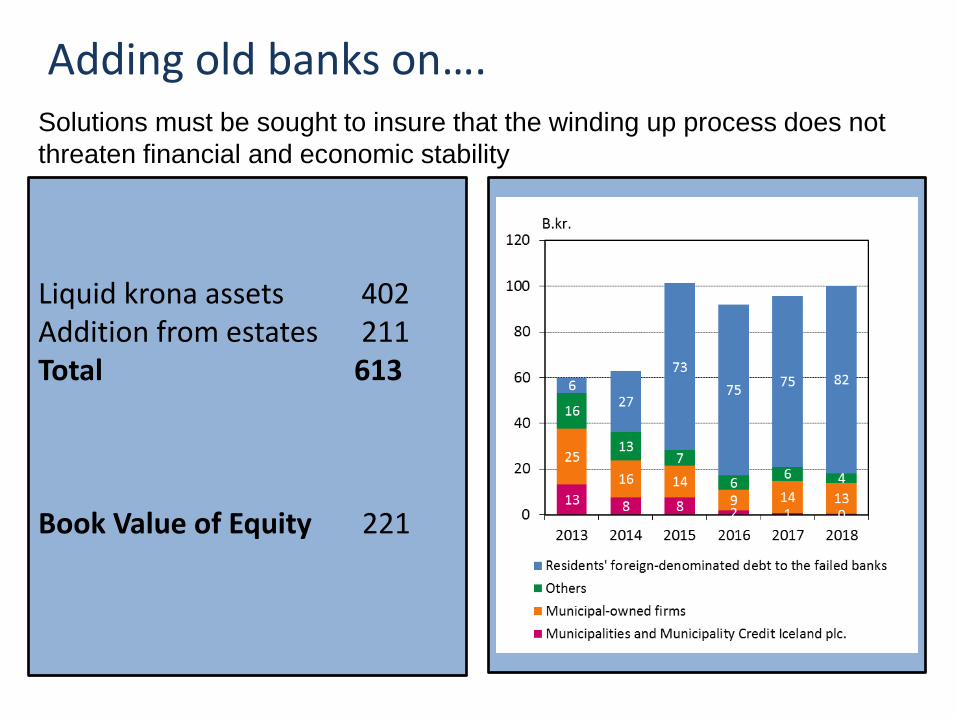

• The old banks estate add to this problem

Seðlabanki Íslands

Capital Controls

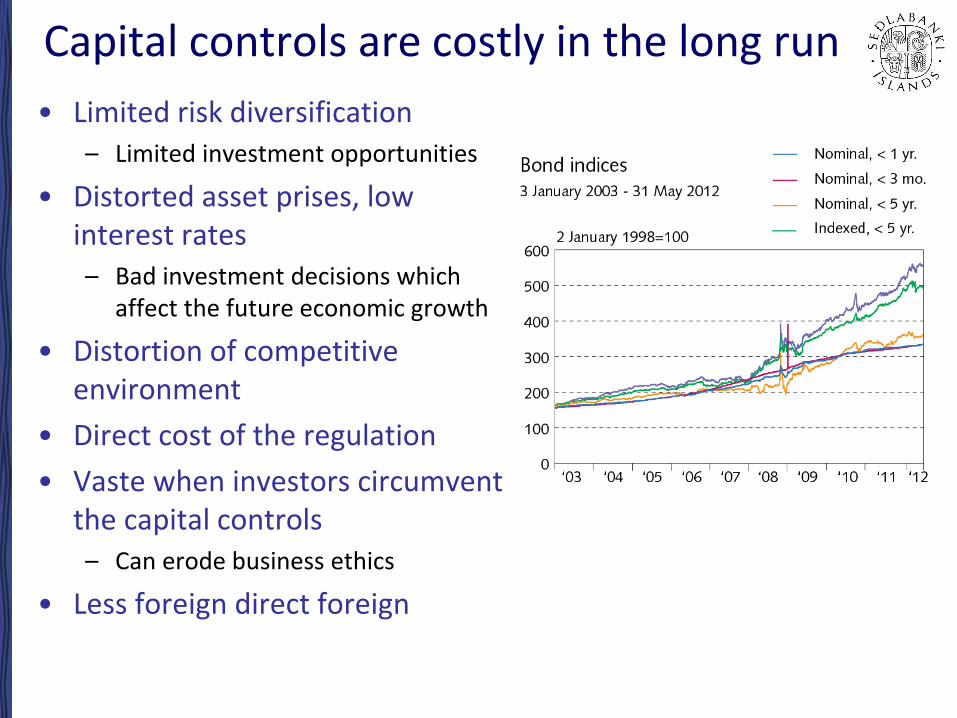

Capital controls are costly in the long run

• Limited risk diversification – Limited investment opportunities

• Distorted asset prises, low interest rates – Bad investment decisions which

affect the future economic growth

• Distortion of competitive environment

• Direct cost of the regulation

• Vaste when investors circumvent the capital controls – Can erode business ethics

• Less foreign direct foreign

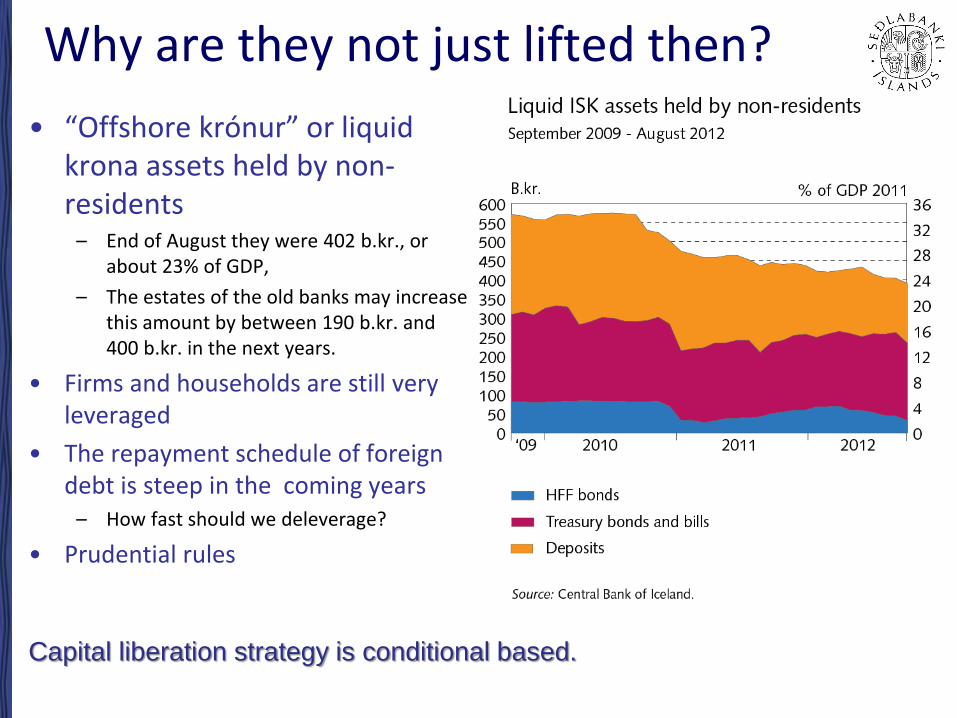

Why are they not just lifted then?

• “Offshore krónur” or liquid krona assets held by non-residents

– End of August they were 402 b.kr., or about 23% of GDP,

– The estates of the old banks may increase this amount by between 190 b.kr. and 400 b.kr. in the next years.

• Firms and households are still very leveraged

• The repayment schedule of foreign debt is steep in the coming years

– How fast should we deleverage?

• Prudential rules

Capital liberation strategy is conditional based.

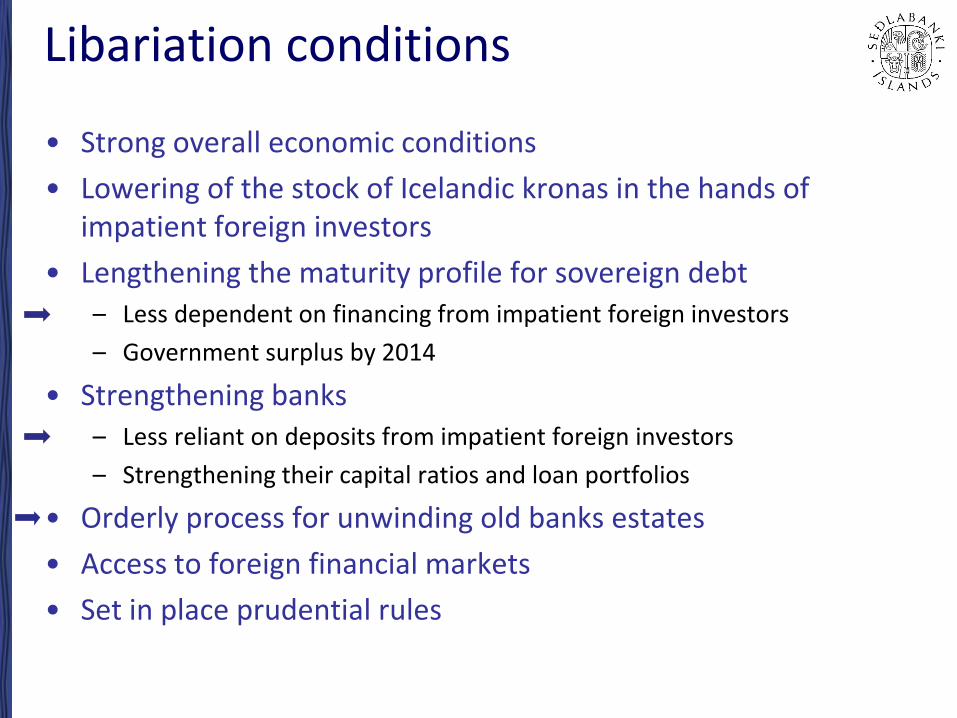

Libariation conditions

• Strong overall economic conditions

• Lowering of the stock of Icelandic kronas in the hands of impatient foreign investors

• Lengthening the maturity profile for sovereign debt – Less dependent on financing from impatient foreign investors

– Government surplus by 2014

• Strengthening banks – Less reliant on deposits from impatient foreign investors

– Strengthening their capital ratios and loan portfolios

• Orderly process for unwinding old banks estates

• Access to foreign financial markets

• Set in place prudential rules

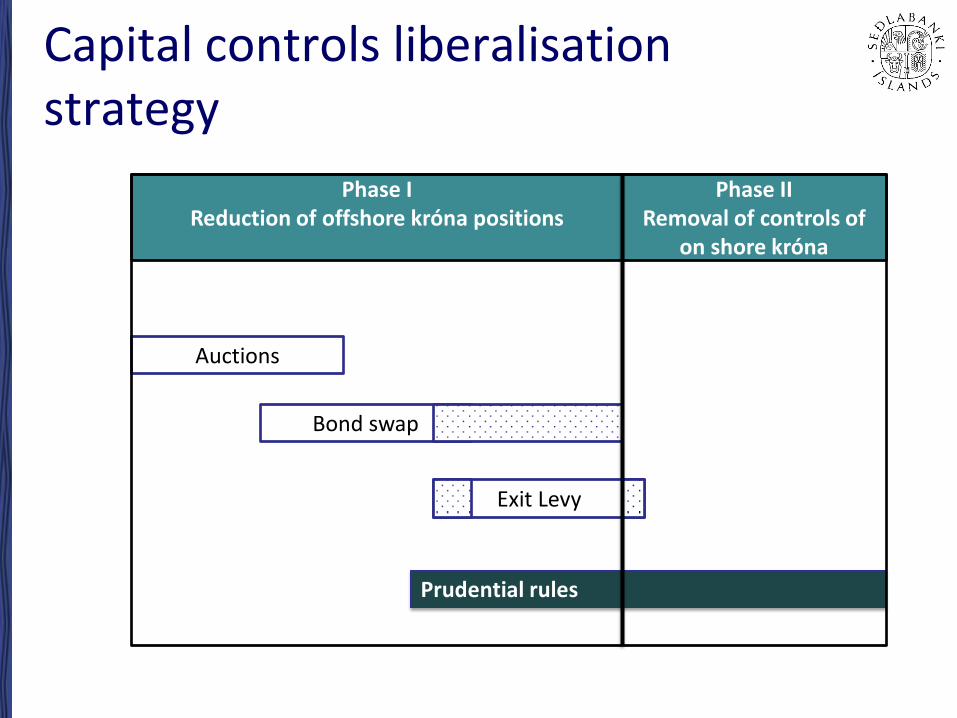

Capital controls liberalisation strategy

Auctions

Prudential rules

Bond swap

Exit Levy

Phase I Reduction of offshore króna positions

Phase II Removal of controls of

on shore króna

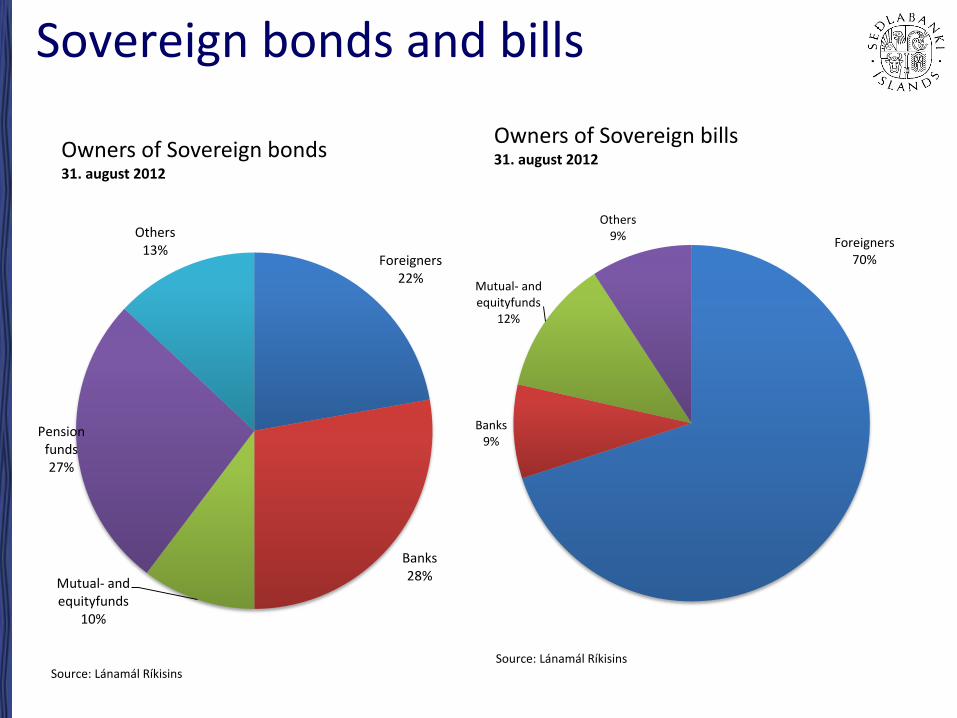

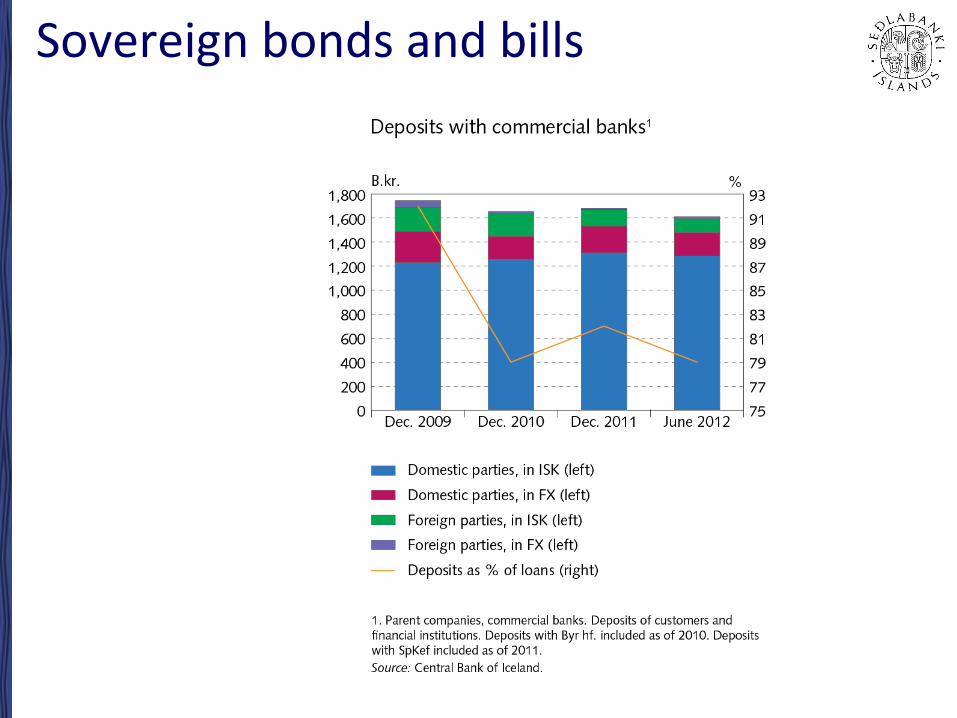

Sovereign bonds and bills

Foreigners 22%

Banks 28%

Mutual- and equityfunds

10%

Pension funds 27%

Others 13%

Owners of Sovereign bonds 31. august 2012

Source: Lánamál Ríkisins

Foreigners 70%

Banks 9%

Mutual- and equityfunds

12%

Others 9%

Owners of Sovereign bills 31. august 2012

Source: Lánamál Ríkisins

Sovereign bonds and bills

Seðlabanki Íslands

Old Bank Estates

Will make liberation harder….why?

Endurgreiðslur erlendra lána og aflandskrónur

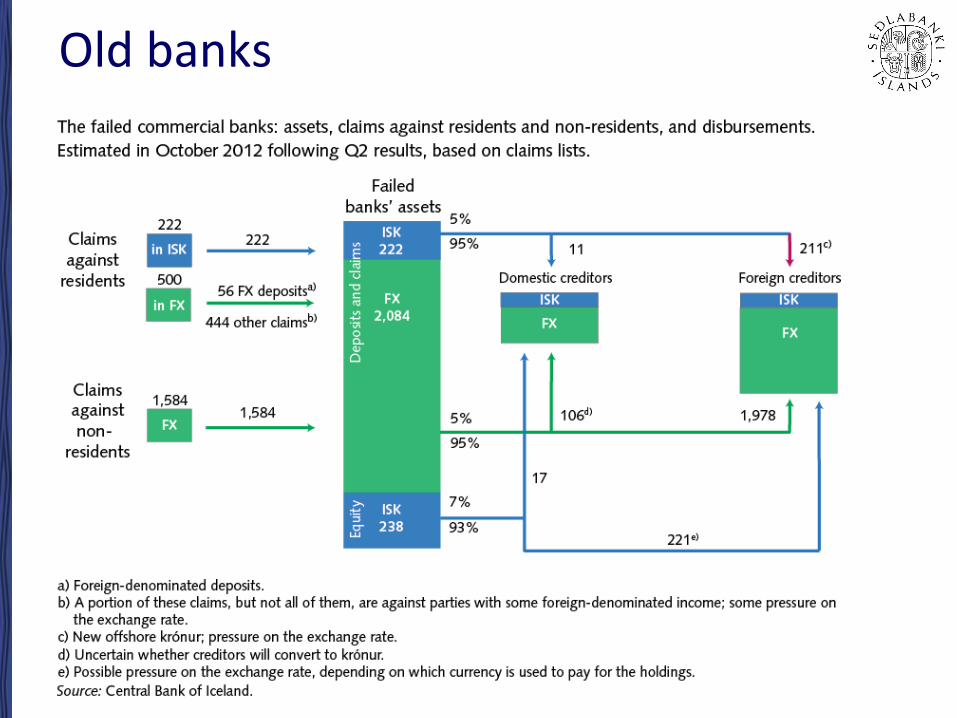

Old banks

Liquid krona assets, refinancing risk and old banks estates

Refinancing -w/o treasury

Now 402 b.kr. From the old banks 211 b.kr.

Totla 613 b.kr.

Liquid krona assets

No onshore effects

1.746

402 b.kr.

2.544 b.kr.

Refinancing n 366

Liquid krona assets 211

Liquid krona assets

Refinancing - w/o old bank estates and treasury

Old bank estates

Equity in new banks (book value) 221 b.kr.

Equity in new banks 221

Adding old banks on….

Liquid krona assets 402 Addition from estates 211 Total 613 Book Value of Equity 221

Solutions must be sought to insure that the winding up process does not

threaten financial and economic stability

Seðlabanki Íslands

Prudential rules

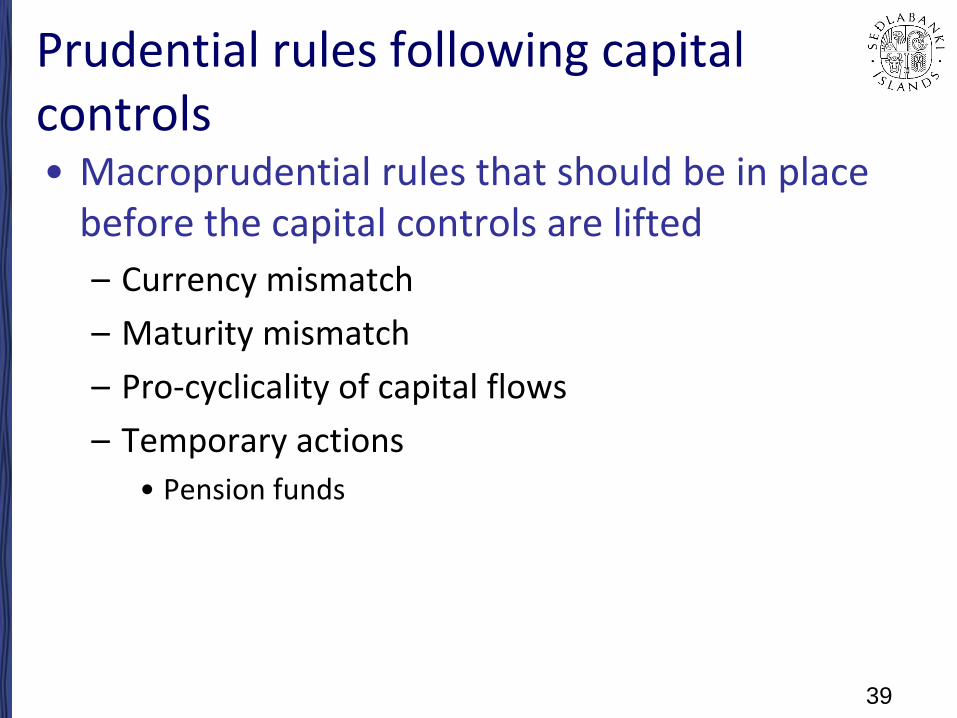

Prudential rules following capital controls • Macroprudential rules that should be in place

before the capital controls are lifted

– Currency mismatch

– Maturity mismatch

– Pro-cyclicality of capital flows

– Temporary actions

• Pension funds

39

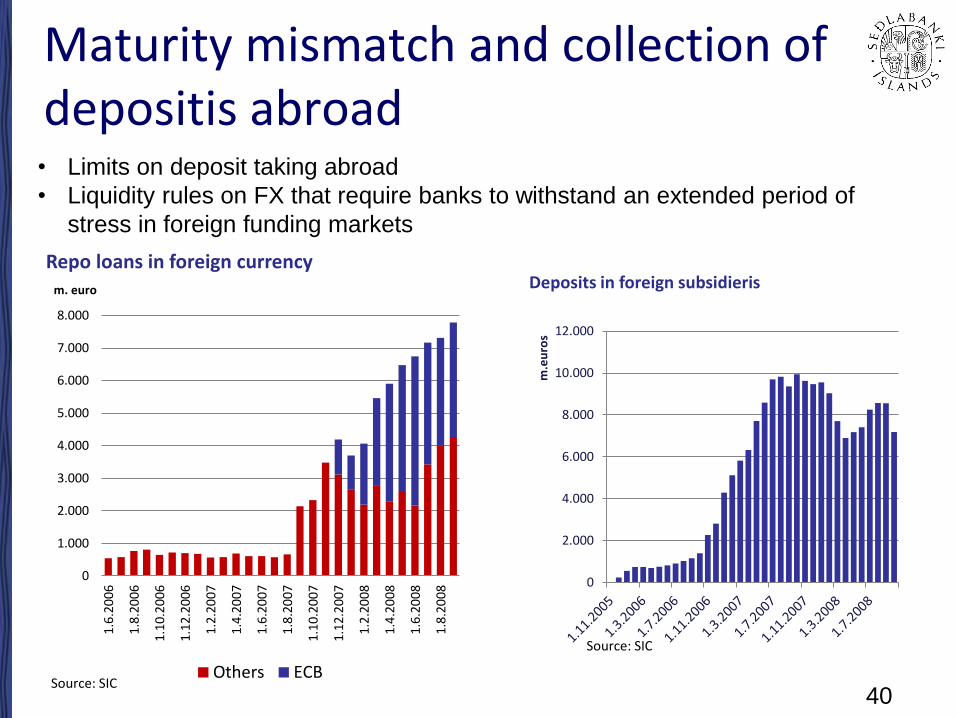

Maturity mismatch and collection of depositis abroad

40

0

2.000

4.000

6.000

8.000

10.000

12.000

m.e

uro

s

Deposits in foreign subsidieris

Source: SIC

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

1.6

.20

06

1.8

.20

06

1.1

0.2

006

1.1

2.2

006

1.2

.20

07

1.4

.20

07

1.6

.20

07

1.8

.20

07

1.1

0.2

007

1.1

2.2

007

1.2

.20

08

1.4

.20

08

1.6

.20

08

1.8

.20

08

m. euro

Repo loans in foreign currency

Others ECBSource: SIC

• Limits on deposit taking abroad

• Liquidity rules on FX that require banks to withstand an extended period of

stress in foreign funding markets

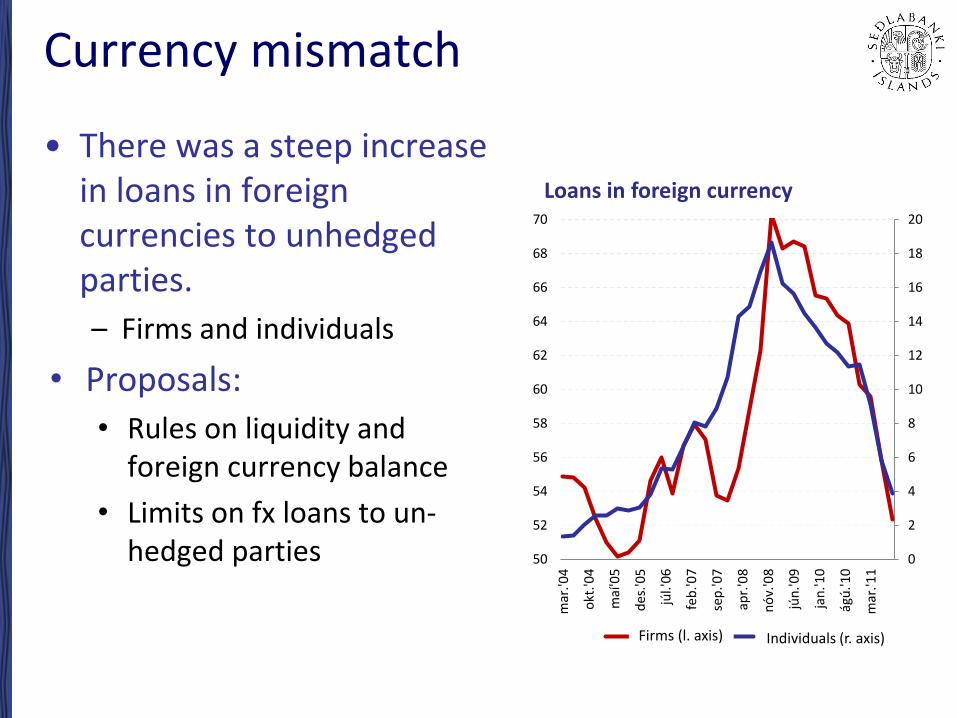

0

2

4

6

8

10

12

14

16

18

20

50

52

54

56

58

60

62

64

66

68

70

mar

.'04

okt

.'04

maí

'05

des

.'05

júl.'

06

feb

.'07

sep

.'07

apr.

'08

nó

v.'0

8

jún

.'09

jan

.'10

ágú

.'10

mar

.'11

Loans in foreign currency

Firma (v.as) Personer (h.as)

Currency mismatch

• There was a steep increase in loans in foreign currencies to unhedged parties.

– Firms and individuals

• Proposals:

• Rules on liquidity and foreign currency balance

• Limits on fx loans to un-hedged parties

Firms (l. axis) Individuals (r. axis)

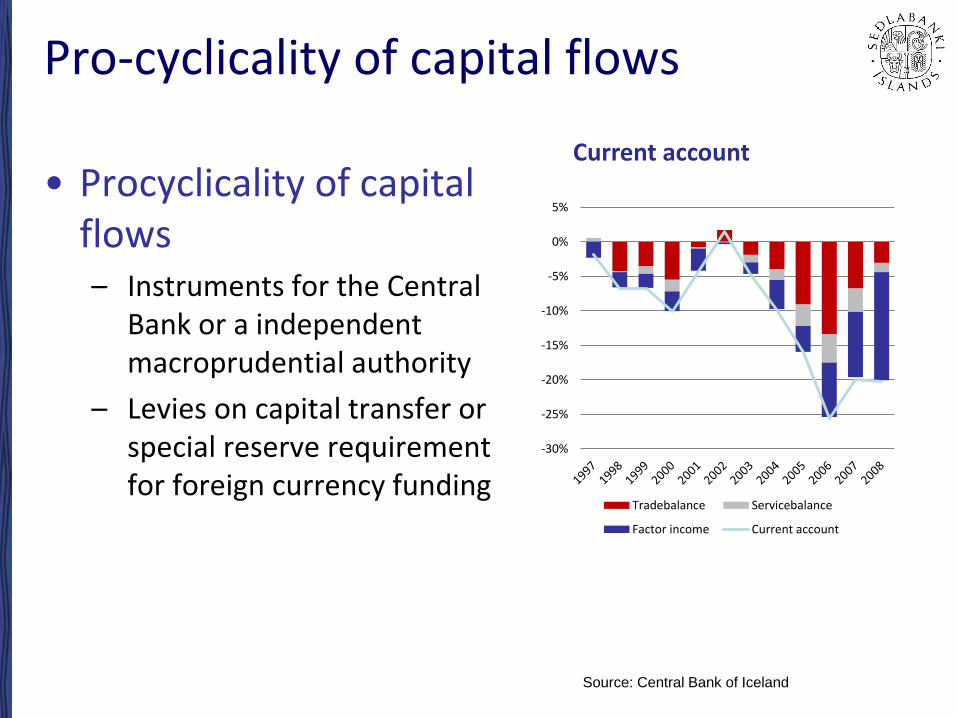

Pro-cyclicality of capital flows

• Procyclicality of capital flows – Instruments for the Central

Bank or a independent macroprudential authority

– Levies on capital transfer or special reserve requirement for foreign currency funding

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

Current account

Tradebalance Servicebalance

Factor income Current account

Source: Central Bank of Iceland

43 Thank you

Recommended