Research PREVIEW for

ICT Spend in South Africa—Financial Services Sector

Financial Institutions Become More

Customer Centric by Investing in

Advanced Technologies

Key Highlights

• Banks and insurance companies, in particular, are becoming more customer-centric in

their drive to boost their revenues and improve customer loyalty.

• As a result, they are investing heavily in digitising their service delivery by augmenting

their branch presence through mobile and online service channels.

• They are increasingly adopting the omni-channel approach to service delivery and

engaging with their customers.

• Leveraging big data solutions, they are positioning themselves to more closely match

the needs of their increasingly tech-savvy and demanding customer base.

• In order to keep their operations lean and contain costs, financial services companies

are turning to cloud computing services.

• However, due to concerns over security, they mostly favour private and hybrid cloud

models over the public models, despite the relative cost advantage of the latter.

South Africa’s Financial Services Sector at a Glance

• South Africa’s GDP per

capita: $6,617.9; ranked

82nd highest in the world

• Financial services sector:

$67.7 billion, or 19.3% of

GDP

• Bank penetration: 27.4

million bank accounts (75%

of people aged 16 and

older)

• Digital penetration:

Mobile penetration – 146%

Internet penetration – 41%

ICT in Financial Services:

Macroeconomic Trends,

South Africa, 2014 Financial Services Sector in South Africa

• Financial service providers are looking to

differentiate themselves by offering increasingly

personalised offerings.

• This requires increased understanding of the

needs of sophisticated and demanding financial

services customers.

• The sector has a focus across a range of

services, including commercial, merchant and

retail banking, insurance, investment, and

mortgage lending.

Source: ITU; Stats SA; Ventures Africa; World Bank and Frost & Sullivan

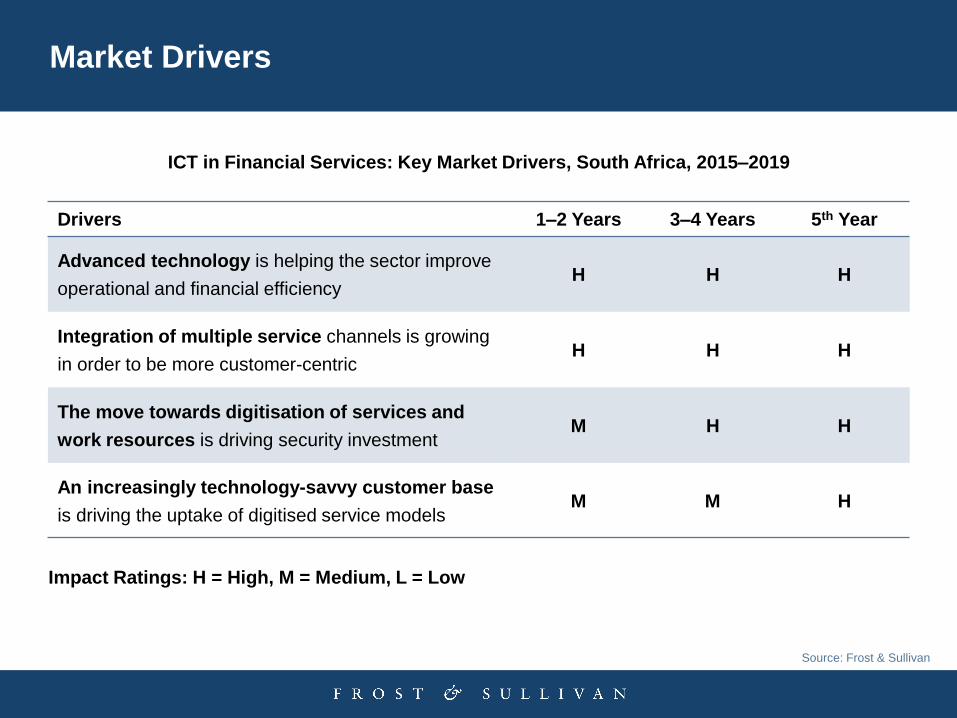

Market Drivers

Drivers 1–2 Years 3–4 Years 5th Year

Advanced technology is helping the sector improve

operational and financial efficiency H H H

Integration of multiple service channels is growing

in order to be more customer-centric H H H

The move towards digitisation of services and

work resources is driving security investment M H H

An increasingly technology-savvy customer base

is driving the uptake of digitised service models M M H

Impact Ratings: H = High, M = Medium, L = Low

ICT in Financial Services: Key Market Drivers, South Africa, 2015–2019

Source: Frost & Sullivan

Market Restraints

Impact Ratings: H = High, M = Medium, L = Low

ICT in Financial Services: Key Market Restraints, South Africa, 2015–2019

Restraints 1–2 Years 3–4 Years 5th Year

Security concerns and a lack of trust in third-party

services are limiting the adoption of cloud and bring

your own device

H H M

Service delivery on mobile devices is still an

unproven business model H M M

Implementation of analytics and cloud services is

limited by a shortage of skilled support staff M M L

Source: Frost & Sullivan

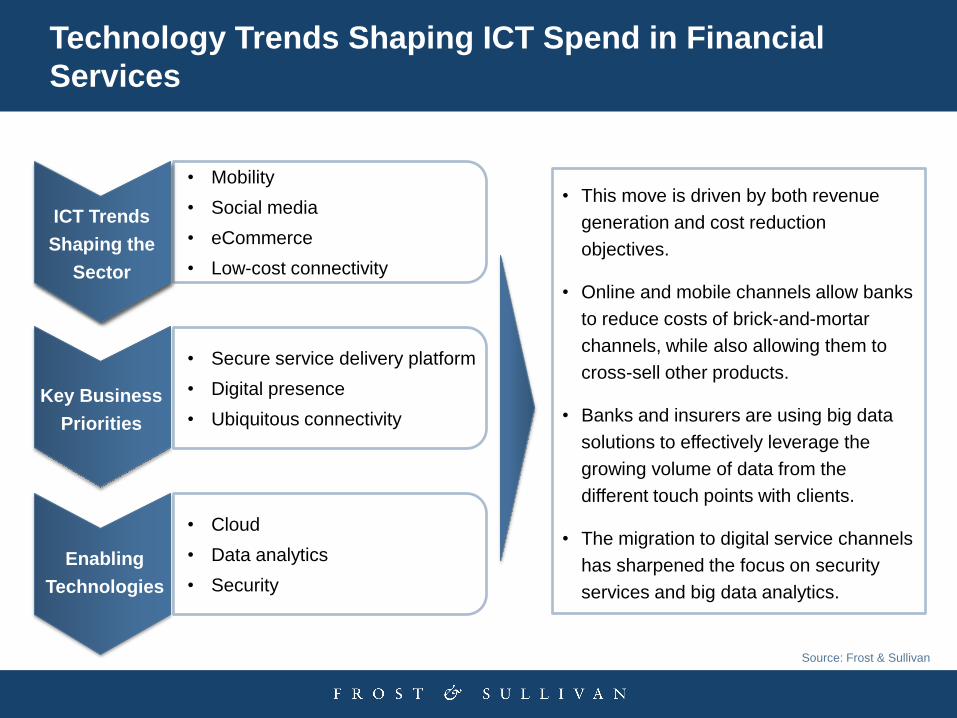

• Secure service delivery platform

• Digital presence

• Ubiquitous connectivity

Technology Trends Shaping ICT Spend in Financial

Services

ICT Trends

Shaping the

Sector

• Mobility

• Social media

• eCommerce

• Low-cost connectivity

• Cloud

• Data analytics

• Security

Key Business

Priorities

Enabling

Technologies

• This move is driven by both revenue

generation and cost reduction

objectives.

• Online and mobile channels allow banks

to reduce costs of brick-and-mortar

channels, while also allowing them to

cross-sell other products.

• Banks and insurers are using big data

solutions to effectively leverage the

growing volume of data from the

different touch points with clients.

• The migration to digital service channels

has sharpened the focus on security

services and big data analytics.

Source: Frost & Sullivan

Cloud Services in South African Banking (Trends)

• Given the technology intensity in financial

services, cloud computing has been touted

as a natural fit for the sector.

• South African banks are consolidating their

data facilities in preparation for increasing

migration to the cloud.

• However, due to concerns over the security

of the public cloud, adoption has been

limited to the private cloud.

• Moreover, they are planning to only place

non-core, non-mission critical applications in

the cloud.

• As a result, cloud vendors will need to put

security and reliability at the centre of their

service offering in order to get financial

institutions to trust the cloud with more of

their applications.

ICT in Financial Services: Technology Steps into

Cloud Computing, South Africa, 2014

Transforming information systems for the cloud

Consolidation of data centres

Virtualisation of the data centre

Source: Frost & Sullivan

Overview of Enterprise ICT Spend by Sector

5-y

ea

r G

row

th F

ore

ca

st

Magnitude of ICT Spending

• Agriculture

• Construction

• Energy and

utilities

• Manufacturing

• Mining

• Transport and logistics

• Financial

services

• Public

sector

• Information and

communication

technology

• Retail

• Healthcare

Key Takeaway: Overall ICT spend by large enterprises across all industries in South Africa was $5.0

billion in 2014, and is expected to grow at a compound annual growth rate of 2.7% reaching $5.7

billion by 2019.

• Oil and gas

ICT in Financial Services: Enterprise ICT Spend by Sector, South Africa, 2014

High

High Low Source: Frost & Sullivan

The Full Analysis Features the Following Content

Section Slide Numbers

Executive Summary 3

Research Overview 5

Market Definitions 11

Overview of the Financial Services Sector 15

ICT in the Financial Services Sector 20

ICT Spend in the Financial Services Sector 25

Drivers and Restraints 30

The Last Word 37

Appendix 39

The Frost & Sullivan Story 43

Key Questions the Analysis Answers

What is the current spend on ICT in the South African financial services sector?

What main ICT categories are financial services companies spending on?

How is this spend expected to evolve over the next five years?

What technologies are shaping the current and future investment in ICT?

Which financial services sector needs are driving ICT investment?

Interested in Full Access? Connect With Us

Facebook https://www.facebook.com/FrostandSullivan

LinkedIn Group https://www.linkedin.com/company/frost-&-sullivan

SlideShare http://www.slideshare.net/FrostandSullivan

Twitter https://twitter.com/FrostSullivanSA

Frost & Sullivan Events http://bit.ly/MvPRbQ

GIL Community http://ww2.frost.com/gil-community/

Research Authors

Lehlohonolo Mokenela

Research Analyst

Information & Communication

Technologies

http://za.linkedin.com/pub/lehloh

onolo-mokenela/41/269/30

Samantha James Corporate Communications – Africa

(+27) 21 680 3574

Global Perspective 40+ Offices Monitoring for Opportunities and Challenges

Industry Convergence Comprehensive Industry Coverage Sparks Innovation Opportunities

Automotive &

Transportation

Aerospace & Defense Measurement &

Instrumentation

Information &

Communication Technologies

Healthcare Environment & Building

Technologies

Energy & Power

Systems

Chemicals, Materials

& Food

Electronics &

Security

Industrial Automation

& Process Control

Automotive

Transportation & Logistics

Consumer

Technologies

Minerals & Mining

Recommended