8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 1/44

A

PROJECT REPORT

ON

“CONSUMER BUYING BEHAVIOR FOR

COLOUR TELEVISIONS’’

MASTER OF BUSINESS ADMINISTRATION

Submitted By: Submitted To:

Nandhakumar.R Dr.R.Varadarajan

Roll No. A929027

Session 2009-2011

Madurai Kamaraj University

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 2/44

INTRODUCTION

Two movies a week at the theatre, getting together with friends and relatives,

playing cards, listening to the radio and may be reading were the only

available outlets for the consumer to pass their time before the introduction of

television.

By the late 70’s consumer demands were becoming strident aspirations

and expectations began out growing available options The culmination of this was

in 1982(when the colour television was introduced and the network was partially

expended) and 1984 (with the one transmitter a day expansion) However these

changes perhaps were more the results of political considerations rather than

meeting the consumer demand for change.

The magazine boom of the mid 70’s had limited impact as it was catering

to more or less the homogeneous group of people dictated by language, style, and

content. But for the first time in country, TV a single medium was reaching out

nationally. Radio while the forerunner did not have the same impact.

The advantage of TV since 1984 was that it could be received through out

the country. It therefore operated as a catalyst in defining social moves of the

times. Being a truly mass medium it drew viewership from all stratas of thesociety. Each individual picked what he or she wanted from the medium.

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 3/44

The advent of satellite and cable TV has now totally changed the situation. With

satellite programmes are beamed to many countries at the same time. Operating in

a protected economy Indian advertisers have a no market outside the borders of

India. But consumers have no such restrictions They are more happy to adopt the

latest entertainment media.

Consumers now demand quality as never before. The best available

internationally is preferred to Indian as economy liberalizes. An even more

suitable change is imminent. Consumers have begun to think international and

over time behave international.

Consumers and technology are marching hand in hand today. IT is thus

incumbent upon the marketers, manufacturers, advertisers, and agencies to

understand this new consumer and keep pace or face the alternative of being left

behind. To establish their standing in the market they have to be constantly on the

search for customers and have to find out what consumer buy , how much can they

pay and what is being made available to them by the competitors not only in India

but internationally too.

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 4/44

COLOR TELEVISION INDUSTRY

Television has recorded a phenomenal growth in India. It has become an accepted

part of our daily life in very short span. Television is affecting customers,

domestic routines, educational techniques and entertainment pattern. In the recent

past television was luxury item meant for rich people only but now a days, it is

considered as necessity by most of the people. However the role of audio visual

media of communication for a country like India with large population, high

illiteracy and vast area assumes critical importance and television can be regarded

as harbinger of social, economic, and cultural development. Television combinesin it all the benefit of the radio, newspaper and cinema and therefore it is the most

popular media for education, information and entertainment. Before understanding

any market adventure, it is important to understand the industry. Therefore, it is

useful to study background of TV industry of India briefly.

The first demonstration of actual television was made in 1925-27 by J.Lbaird

and C.F Jenkins. The Black and White TV broadcast was introduced in UK in

1937. A color sequential system developed by Columbia Broadcasting service was

adopted in U.S.A. in 1950 for coloured T.V. transmission. After a great deal of

internal debate, the government of India decided to introduce television in the year

1959. Commercial production of T.V. sets was started in 1970. Later on

doordarshan stations was set up in Bombay(1972), Amritsar(1973),

Srinagar(1973), Calcutta(1975), Madras(1975) and Lucknow(1975).

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 5/44

HISTORICAL DEVELOPMENT IN INDIA

The 80’s

The 80’s saw the industry growing at a fast rate of 30% per annum. The years

following the 1982 Asian games saw an exponential rise in growth, which

coincided with the setting up of Doordarshan kendras in many parts of the country.

Moreover, the government adopted a policy of encouraging the sector, which saw

the birth of many TV companies namely Weston, Dyanora and Televista. Even

state government owned companies like Uptron, Keltron and Meltron came up. By

1989, there were over 200 TV companies with sales of 5.2mn sets.

The 90’s

The early years of the 90’s decade saw TV sales falling to 4mn units due to a high

tax regime. However, with the onset of the liberalization era, the year 1993 saw a

reversal in fortunes for the industry with both import duties and excise duties

being slashed. Accompanying it was a rise in the general purchasing power of the

populace, a greater variety in TV software (with the coming in of foreign satellitechannels) and a strong rise in replacement demand. Sales touched almost 9mn

units in 1998. This period also saw the entry of MNC’s.

The years 1998 and 1999 have seen events like, the large pay-out to the

government staff through the implementation of the 5th Pay Commission, World

Cup 1999 and the success of the rabi crop. These events have changed the face of

the CTV industry, which realized a growth of 29-30% for the last two years. In

fact, for LG, (official sponsor of the World Cup 1999) this was the most successful

brand building exercise, as the company saw a 95% growth in 1999.

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 6/44

THE PRESENT SCENARIO

CTV market has grown by around 30% to 5mn units . After an accelerated performance in the last two years, The Rs75bn the industry has seen a slow growth

of just 25% in this year (January-April2000).

While some players have seen a steady decline in sales, a few others have

performed exceptionally well. Brands like Philips, Sony, Aiwa have seen their

market shares dipping continuously, while the Korean multinationals, LG and

Samsung, are on a rampage, having shown a commendable performance, contrary

to the overall CTV industry performance. BPL has held its leadership in FY2000

by sacrificing margins with a 20.3% market share, despite the onslaught of

multinationals. BPL volume sales increased by 35% to 1.18mn units for FY2000

whereas net sales increased by 4% only. The company showed a jump in CTV

exports by 148%. However, the company did not perform well in the 1QFY2001

with its sales dipping by 25% to Rs. 3,720.5mn. Most of the players are slashing

prices and taking a re-look at their schemes. Prices are down by more than 20%

and industry majors predict a sharper fall by 8% in the next two years. However,

reduction in prices is not a viable option in the long run, and will definitely affect

the profit margins. Contrary to this, LG has priced its products 10% higher than

the market price and still managed to be the largest brand in consumer electronics

and white goods for April 2000 by achieving sales of Rs1.95bn

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 7/44

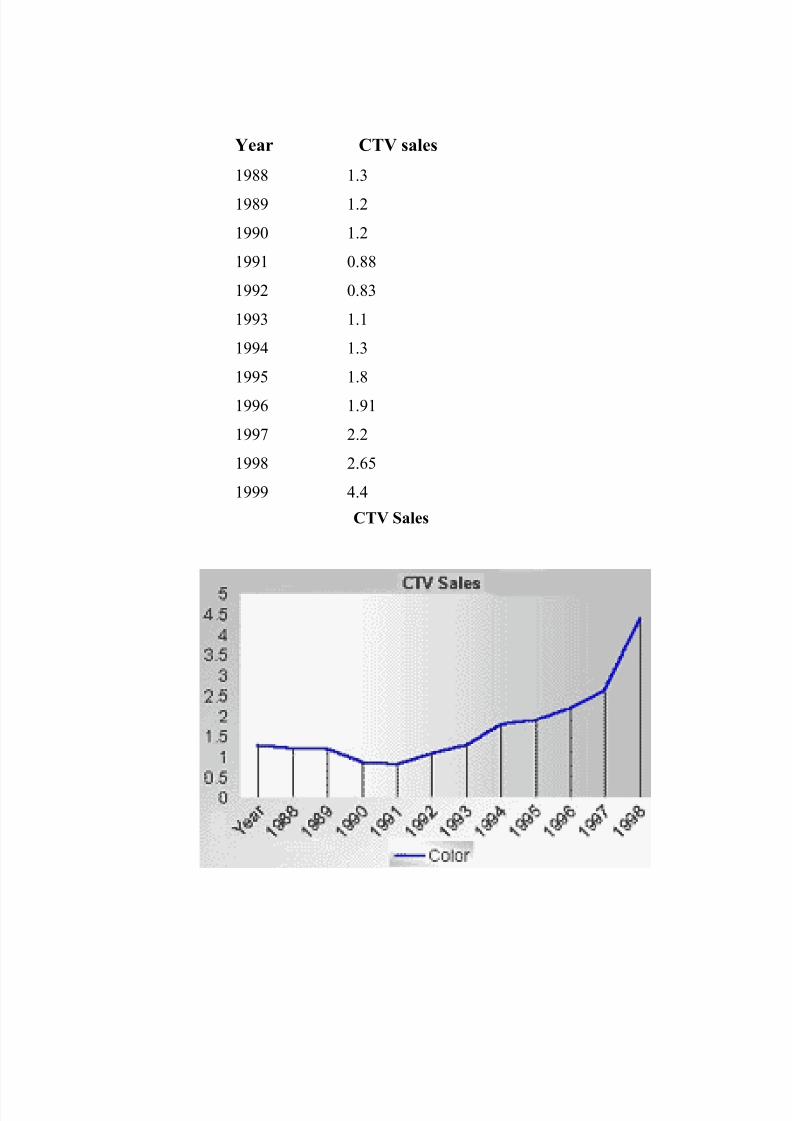

Year CTV sales

1988 1.3

1989 1.2

1990 1.2

1991 0.88

1992 0.83

1993 1.1

1994 1.3

1995 1.8

1996 1.91

1997 2.2

1998 2.65

1999 4.4

CTV Sales

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 8/44

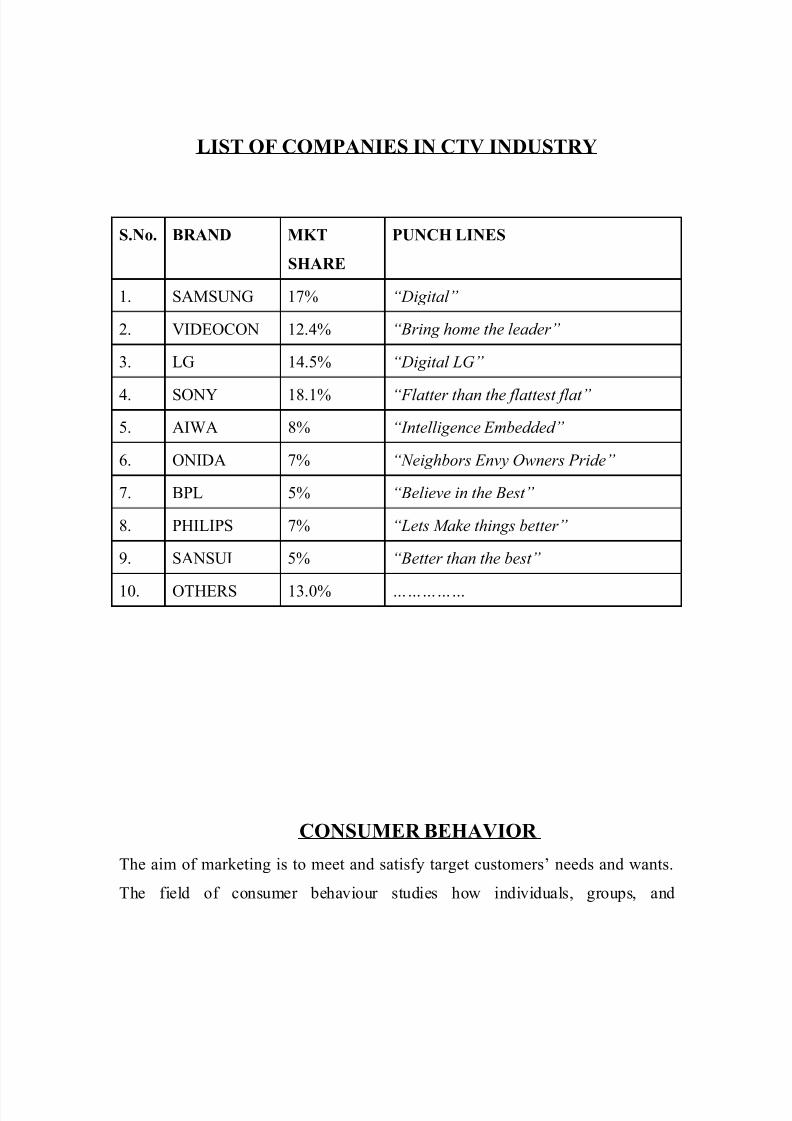

LIST OF COMPANIES IN CTV INDUSTRY

S.No. BRAND MKT

SHARE

PUNCH LINES

1. SAMSUNG 17% “Digital”

2. VIDEOCON 12.4% “Bring home the leader”

3. LG 14.5% “Digital LG”

4. SONY 18.1% “Flatter than the flattest flat”

5. AIWA 8% “Intelligence Embedded”

6. ONIDA 7% “Neighbors Envy Owners Pride”

7. BPL 5% “Believe in the Best”

8. PHILIPS 7% “Lets Make things better”

9. SANSUI 5% “Better than the best”

10. OTHERS 13.0% ……………

CONSUMER BEHAVIOR

The aim of marketing is to meet and satisfy target customers’ needs and wants.

The field of consumer behaviour studies how individuals, groups, and

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 9/44

organizations select, buy, use, and dispose of goods, services, ideas, or

experiences to satisfy their needs and desires. The consumer buyer behaviour is

the buying behaviour of final consumer–individuals and households who buys

goods and services for personal consumption.Understanding consumer behaviour and “knowing customers” are never

simple. Customers may state their needs and wants but act otherwise. They may

not be in touch with their deeper motivations. They may respond to influences that

change their mind at the last minute. Nevertheless, marketers must study their

target customers’ wants, perceptions, preferences, and shopping and buying

behavior:

Studying consumers provides clues for developing new products, product features,

prices, channels, messages, and other marketing-mix elements.

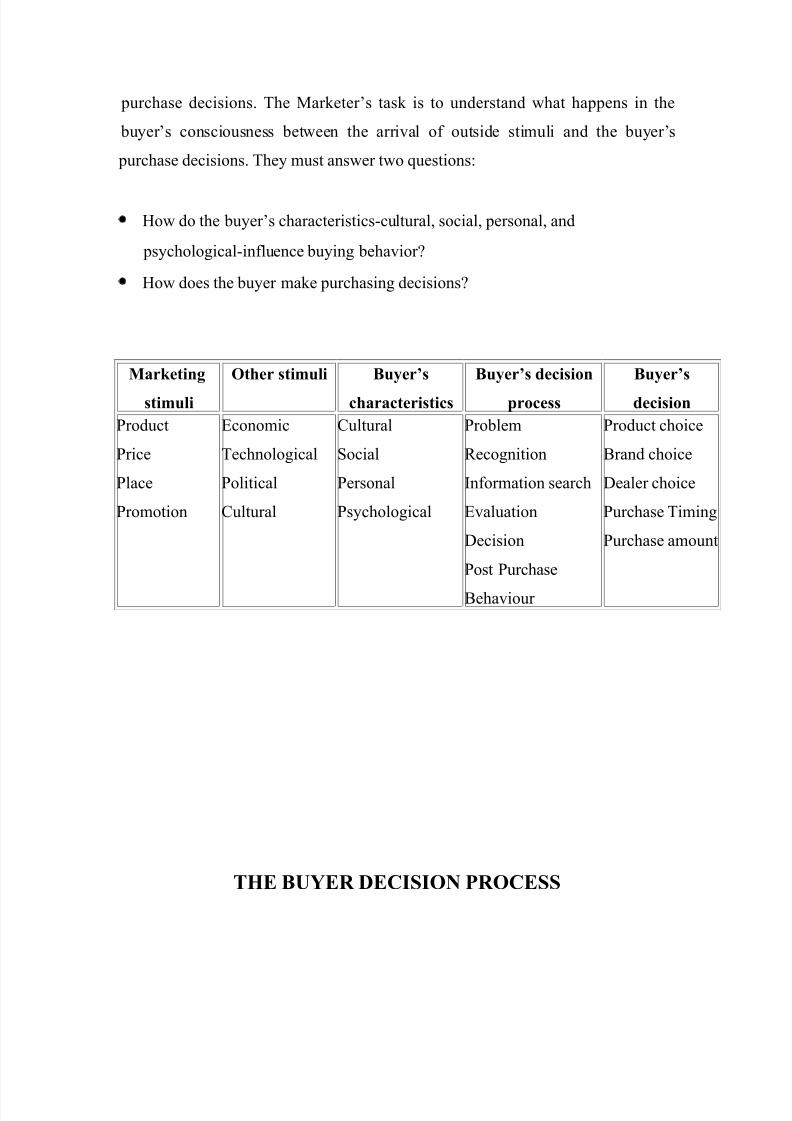

A Model of Consumer Behavior

At one time, marketers could understand consumers through the daily experience

of selling to them. But the growth of companies and markets has removed many

marketing managers from direct contact with customers. Increasingly, managers

have had to rely on the 7 O’s framework for consumer research to answer the

following key questions about any market:

Who constitutes the market? Occupants

What does the market buy? Objects

Why does the market buy? Objectives

Who participates in the buying? Organizations

How does the market buy? Operations

When does the market buy? Occasions

Where does the market buy? Outlets

The starting point for understanding buyer behavior is stimulus-response model

shown below. Marketing and environmental stimuli enter the buyer’s

consciousness. The buyer’s characteristics and decision process lead to certain

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 10/44

purchase decisions. The Marketer’s task is to understand what happens in the

buyer’s consciousness between the arrival of outside stimuli and the buyer’s

purchase decisions. They must answer two questions:

• How do the buyer’s characteristics-cultural, social, personal, and

psychological-influence buying behavior?

• How does the buyer make purchasing decisions?

Marketing

stimuli

Other stimuli Buyer’s

characteristics

Buyer’s decision

process

Buyer’s

decision

Product

Price

Place

Promotion

Economic

Technological

Political

Cultural

Cultural

Social

Personal

Psychological

Problem

Recognition

Information search

Evaluation

Decision

Post Purchase

Behaviour

Product choice

Brand choice

Dealer choice

Purchase Timing

Purchase amount

THE BUYER DECISION PROCESS

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 11/44

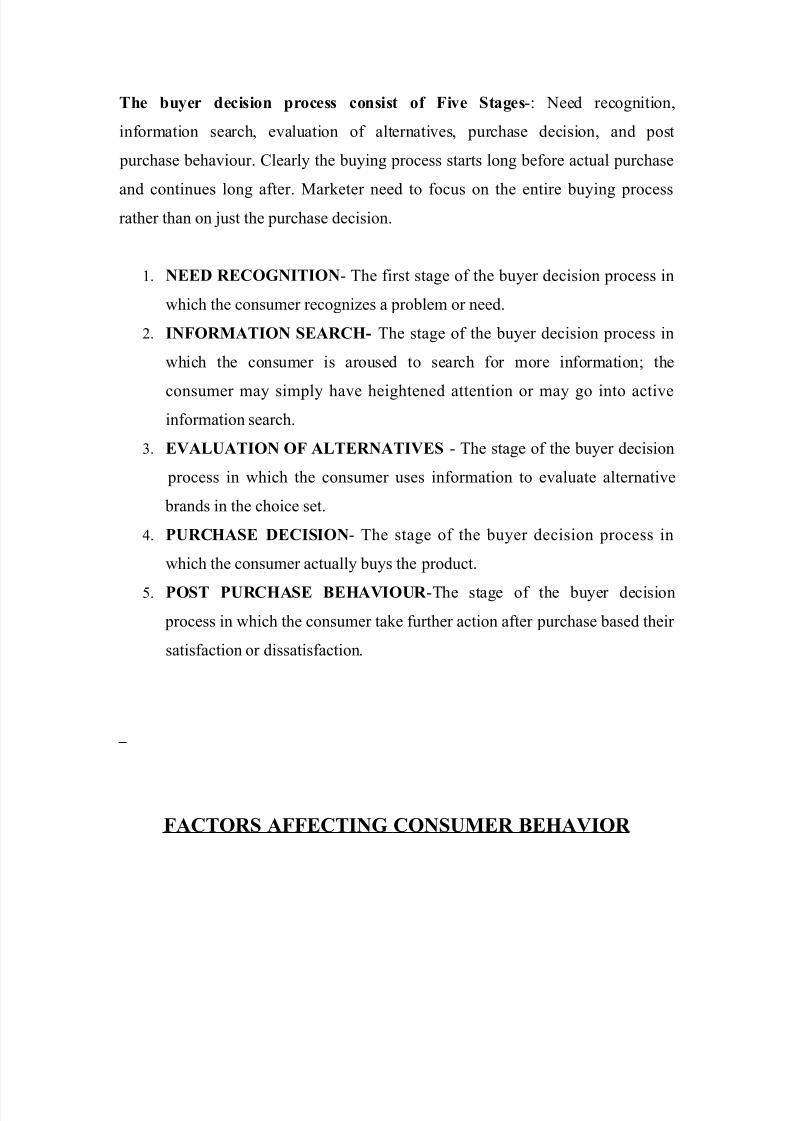

The buyer decision process consist of Five Stages-: Need recognition,

information search, evaluation of alternatives, purchase decision, and post

purchase behaviour. Clearly the buying process starts long before actual purchase

and continues long after. Marketer need to focus on the entire buying processrather than on just the purchase decision.

1. NEED RECOGNITION- The first stage of the buyer decision process in

which the consumer recognizes a problem or need.

2. INFORMATION SEARCH- The stage of the buyer decision process in

which the consumer is aroused to search for more information; the

consumer may simply have heightened attention or may go into active

information search.

3. EVALUATION OF ALTERNATIVES - The stage of the buyer decision

process in which the consumer uses information to evaluate alternative

brands in the choice set.

4. PURCHASE DECISION- The stage of the buyer decision process in

which the consumer actually buys the product.

5. POST PURCHASE BEHAVIOUR -The stage of the buyer decision

process in which the consumer take further action after purchase based their

satisfaction or dissatisfaction.

FACTORS AFFECTING CONSUMER BEHAVIOR

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 12/44

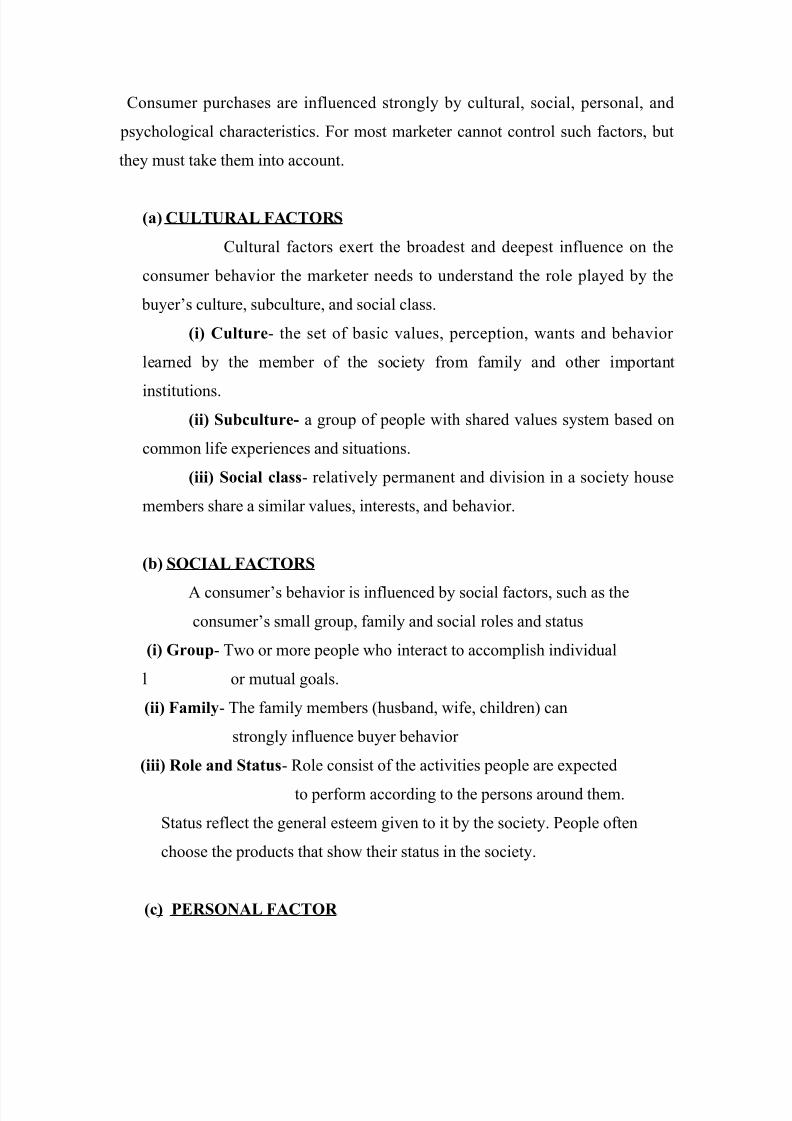

Consumer purchases are influenced strongly by cultural, social, personal, and

psychological characteristics. For most marketer cannot control such factors, but

they must take them into account.

(a) CULTURAL FACTORS

Cultural factors exert the broadest and deepest influence on the

consumer behavior the marketer needs to understand the role played by the

buyer’s culture, subculture, and social class.

(i) Culture- the set of basic values, perception, wants and behavior

learned by the member of the society from family and other important

institutions.

(ii) Subculture- a group of people with shared values system based on

common life experiences and situations.

(iii) Social class- relatively permanent and division in a society house

members share a similar values, interests, and behavior.

(b) SOCIAL FACTORS

A consumer’s behavior is influenced by social factors, such as the

consumer’s small group, family and social roles and status

(i) Group- Two or more people who interact to accomplish individual

l or mutual goals.

(ii) Family- The family members (husband, wife, children) can

strongly influence buyer behavior

(iii) Role and Status- Role consist of the activities people are expected

to perform according to the persons around them.

Status reflect the general esteem given to it by the society. People often

choose the products that show their status in the society.

(c) PERSONAL FACTOR

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 13/44

A buyer decision also are influenced by personal characteristics such as

the buyer’s age life style, and life cycle stage, occupation ,economic situation ,

lifestyle , and personality and self concept.

(i) Age and Life cycle stage- People change the goods and services they buyover their lifetime. Tastes of the people undergo change with their age.

Family life cycle- the stages through which families might pass as they

mature over time.

(ii) Occupation – A person’s occupation also affect the goods and services

they bought

(iii) Life Style- A person’s pattern of living as expressed in his/her activities,

interest, and opinion.

(iv) Personality-A person’s distinguishing psychological characterstics that

lead to relatively consistent and lasting responses to his or her own

environment.

(d) PSYCHOLOGICAL FACTORS

A person’s buying choices are influenced by four major psychological

factors: motivation, perception, learning, and beliefs and attitudes.

(i) Motivation- A need that is sufficiently pressing to direct the person to seek

satisfaction of the need.

(ii) Perception- The process by which people select, organize, and interpret

information to form a meaningful picture of the world.

(iii) Learning- Changes in the individual’s behavior arising from experience.

(iv) Beliefs and Attitude- Belief is a descriptive thought a person hold about

something.

Attitude is a person’s consistently favorable or unfavorable

evaluation, feelings, and tendencies towards an object or idea.

RESEARCH METHODOLOGY

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 14/44

1. Primary data collection- The information was collected by the way

of face to face interviews. This method was adopted to make the

survey interactive and also awareness enhancing.

2. Research-Survey

3. Research instrument- Structured Questionnaire.

4. Area covered/scope of the study-Madurai Kamaraj University.

5. Sample Size-50

6. Sample Unit- Students.

7. Sample Procedure- Convenience Sampling

8. Contact Method-Personal Interview Method

GENDER %OF RESPONDENTS

Male 58

Female 42

OBJECTIVES OF THE STUDY

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 15/44

The buying behavior of the consumer with regard to CTV is influenced by number

of external and internal factors and this study attempts to know about the

consumer buying behavior and at the same time what factors do the consumers

have in their mind before they make up their mind to purchase a CTV so the main

aim of my study was:-

1. To determine factors that influence the buying behavior of consumer.

2. To determine the most preferred brand.

3. To find out reasons and analysis for the most preferred brand.

4. To determine the most preferred features that the consumers look for while

the selection of any brand.

5. To have an idea about the future purchase plan of the consumers.

6. To determine the level of satisfaction with regard to services provided by the

retailers and brand already owned by the consumer.

7. To determine the promotional schemes that attracts the consumer the most.

8. To know whether CTV are bought on a particular occasion or purchases are

need driven.

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 16/44

LIMITATION

Although sincere efforts were made by me to collect the maximum, most authentic

and relevant information even then this study may have the following limitations:-

1. This study cannot be generalized for all the consumers of CTV since the

universe under study in my research was limited to Jalandhar and Nakodar

city.

2. All the results and conclusion have been drawn on the basis of information

provided by the respondent so there is the possibility of “individual bias”on the part of respondent.

3. Time was an another limiting factor

4. The method used for data collection is convenience sampling method

therefore ‘drop in’ or go through error might have crept in .

5. Buying behavior is an attitudinal which need specialized knowledge of the

area so there is a chance of interpretational error. .

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 17/44

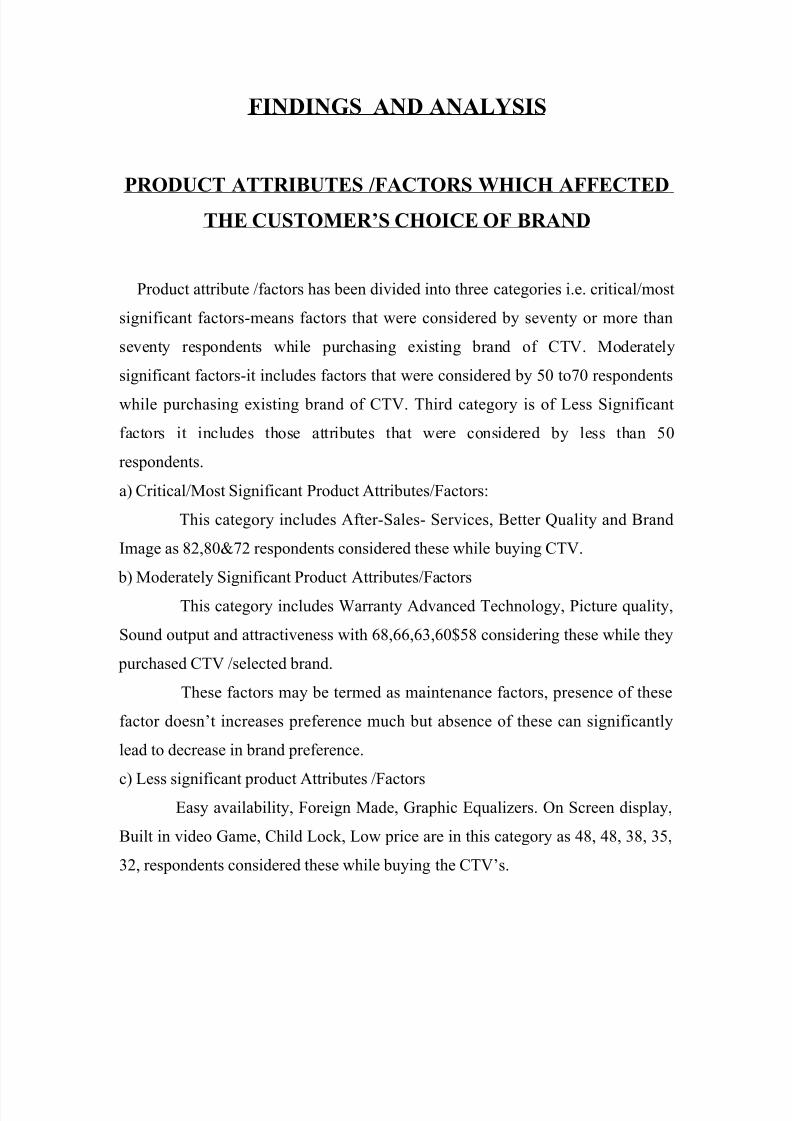

FINDINGS AND ANALYSIS

PRODUCT ATTRIBUTES /FACTORS WHICH AFFECTED

THE CUSTOMER’S CHOICE OF BRAND

Product attribute /factors has been divided into three categories i.e. critical/most

significant factors-means factors that were considered by seventy or more than

seventy respondents while purchasing existing brand of CTV. Moderately

significant factors-it includes factors that were considered by 50 to70 respondents

while purchasing existing brand of CTV. Third category is of Less Significant

factors it includes those attributes that were considered by less than 50

respondents.

a) Critical/Most Significant Product Attributes/Factors:

This category includes After-Sales- Services, Better Quality and Brand

Image as 82,80&72 respondents considered these while buying CTV.

b) Moderately Significant Product Attributes/Factors

This category includes Warranty Advanced Technology, Picture quality,

Sound output and attractiveness with 68,66,63,60$58 considering these while they

purchased CTV /selected brand.

These factors may be termed as maintenance factors, presence of these

factor doesn’t increases preference much but absence of these can significantly

lead to decrease in brand preference.

c) Less significant product Attributes /FactorsEasy availability, Foreign Made, Graphic Equalizers. On Screen display,

Built in video Game, Child Lock, Low price are in this category as 48, 48, 38, 35,

32, respondents considered these while buying the CTV’s.

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 18/44

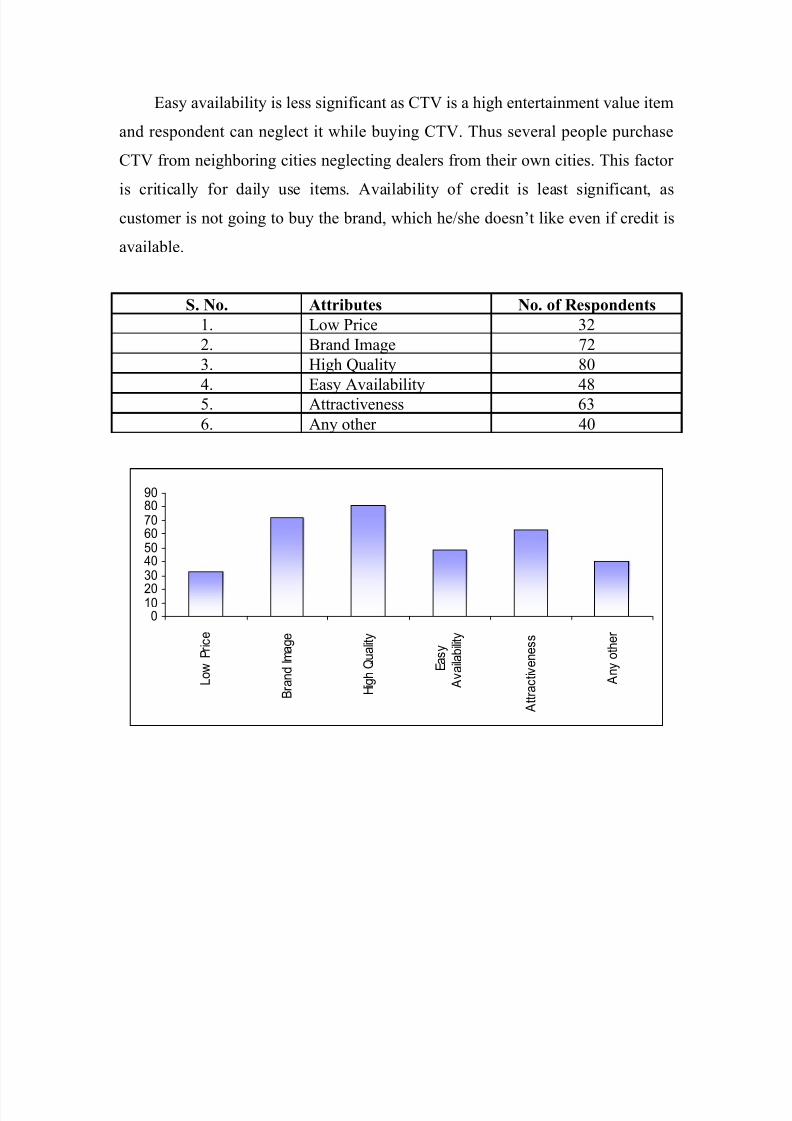

Easy availability is less significant as CTV is a high entertainment value item

and respondent can neglect it while buying CTV. Thus several people purchase

CTV from neighboring cities neglecting dealers from their own cities. This factor

is critically for daily use items. Availability of credit is least significant, ascustomer is not going to buy the brand, which he/she doesn’t like even if credit is

available.

S. No. Attributes No. of Respondents

1. Low Price 32

2. Brand Image 72

3. High Quality 80

4. Easy Availability 485. Attractiveness 63

6. Any other 40

01020

30405060708090

L o w P

r i c e

B r a n d I m a g e

H i g h Q u a l i t y

E a s y

A v a i l a b i l i t y

A t t r a c t i v e n e s s

A n y o t h e r

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 19/44

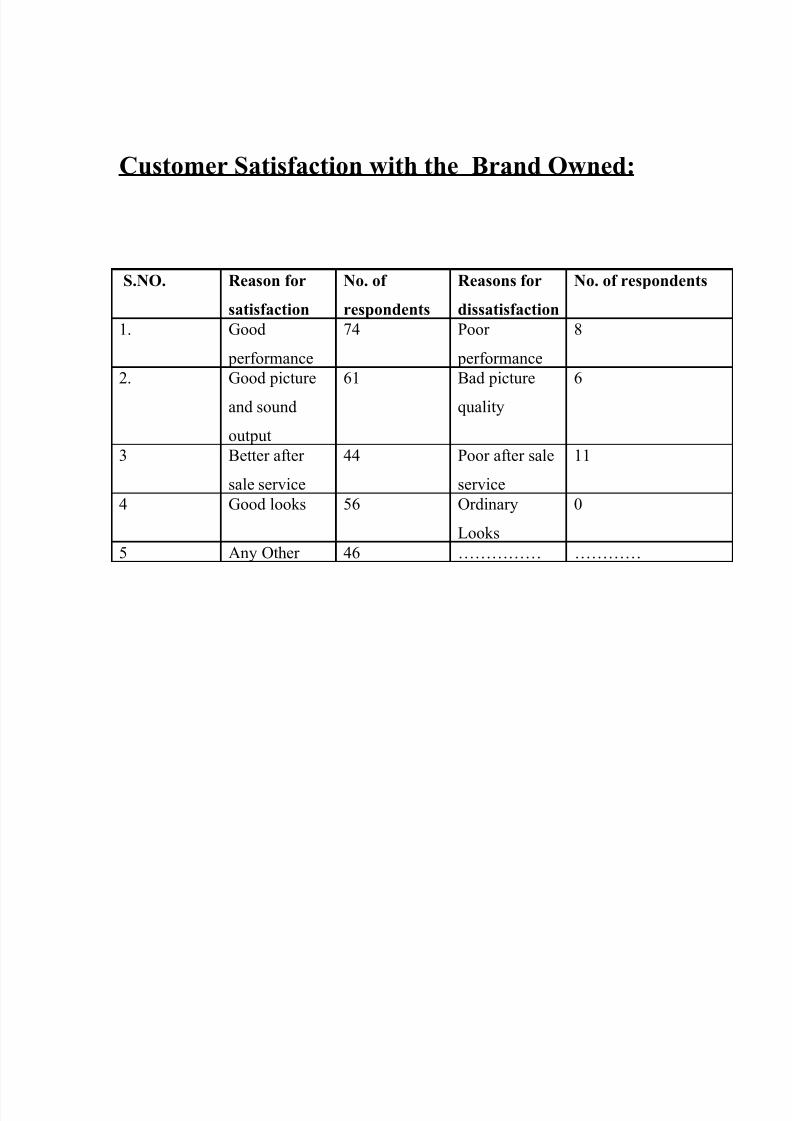

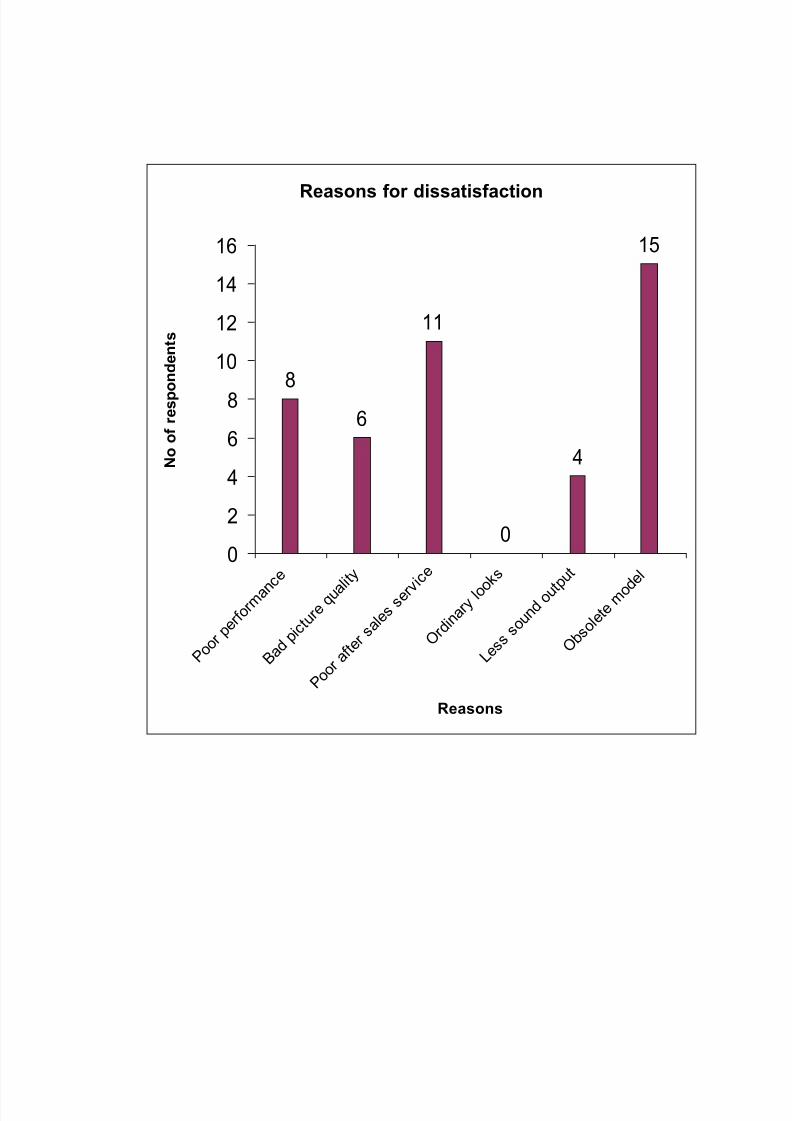

Customer Satisfaction with the Brand Owned:

S.NO. Reason for

satisfaction

No. of

respondents

Reasons for

dissatisfaction

No. of respondents

1. Good

performance

74 Poor

performance

8

2. Good picture

and sound

output

61 Bad picture

quality

6

3 Better after

sale service

44 Poor after sale

service

11

4 Good looks 56 Ordinary

Looks

0

5 Any Other 46 …………… …………

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 20/44

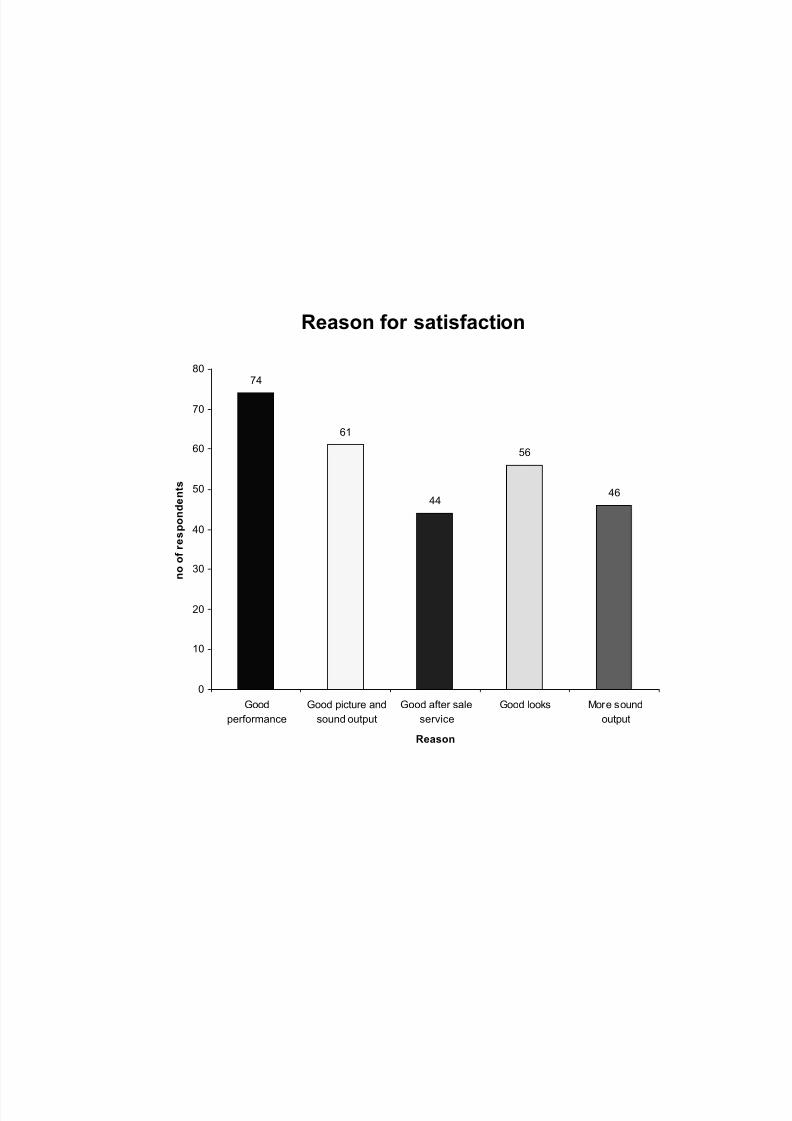

Reason for satisfaction

74

61

44

56

46

0

10

20

30

40

50

60

70

80

Good

performance

Good picture and

sound output

Good after sale

service

Good looks More sound

output

Reason

n o o f r e s p o n d e n t s

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 21/44

Reasons for dissatisfaction

8

6

11

0

4

15

0

2

4

6

8

10

12

14

16

P o o r

p e r f o

r m a n

c e

B a d p i c t u r e q u a l

i t y

P o o r

a f t e

r s a l e s

s e r v

i c e

O r d i n

a r y l o o

k s

L e s s

s o u

n d o u t p

u t

O b s

o l e t e m o d

e l

Reasons

N o o f r e s p o n d e n t s

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 22/44

BRAND PREFERENCE FOR CTV’S:

“A brand is a name, item, sign, symbol or design or a combination of them,

intended to identify the goods or services of one sellers or group of sellers and

to differentiate them from those of competitors.”

Thus a brand identifies the seller or market. Under trademark law , the seller

is granted exclusive rights to the use of the brand name in property.

Brands vary in the amount of power and value they have in the

market place. Brand preference means that the consumer would select that

particular brand over others. A powerful brand is to have a high brand equity.

Survey reveals that Sony, Samsung and LG have the high brand

preference. Philips, Videocon, Onida enjoy moderate preference. Akai, Aiwa,

Sansui has got low brand preference.

Brand preference for Thomson among consumers is minuscule .Sony and

Samsung have high preference because of their excellent performance in terms of

quality and high brand loyalty build over the years. Philips has been able to build

high preference due to aggressive promotional campaign and excellent service

backup.

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 23/44

S. no. Brand name Rating score Rank 1. SONY 850 1

2. SAMSUNG 810 2

3. LG 778 3

4. VIDEOCON 728 4

5. ANY OTHER ….. …….

660

680

700

720

740

760

780

800

820

840

860

SONY SAMSUNG LG VIDEOCON

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 24/44

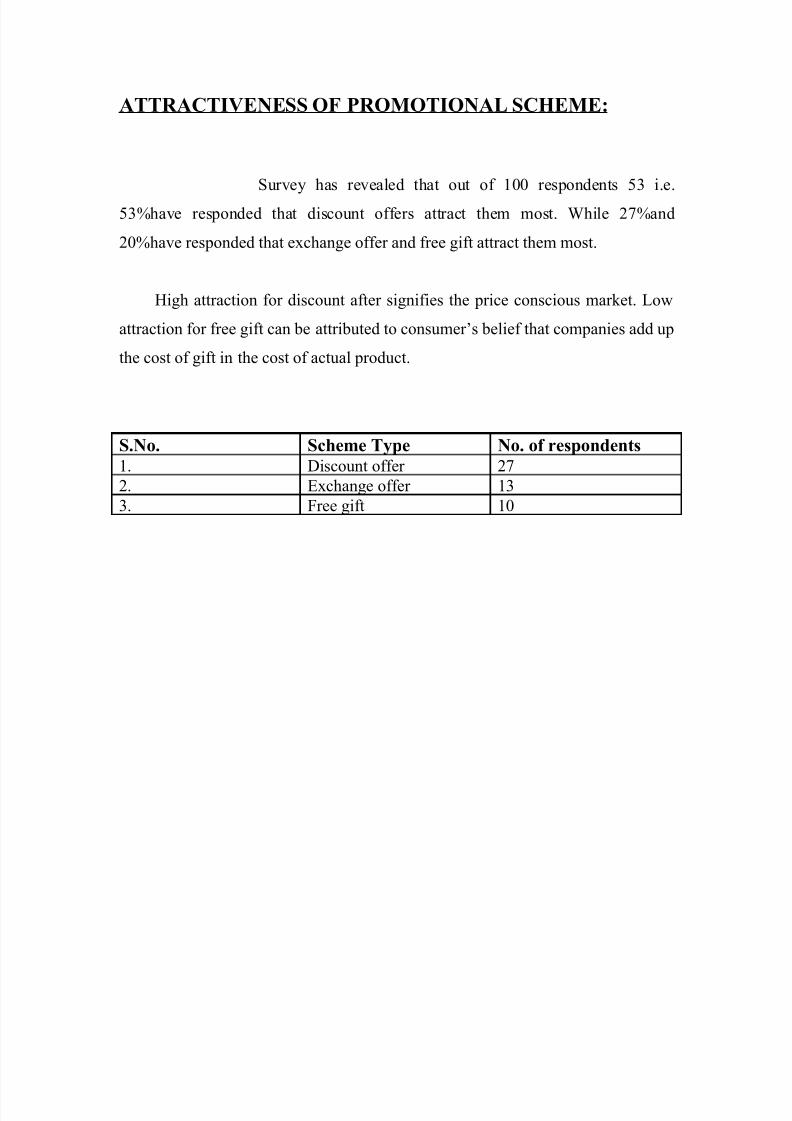

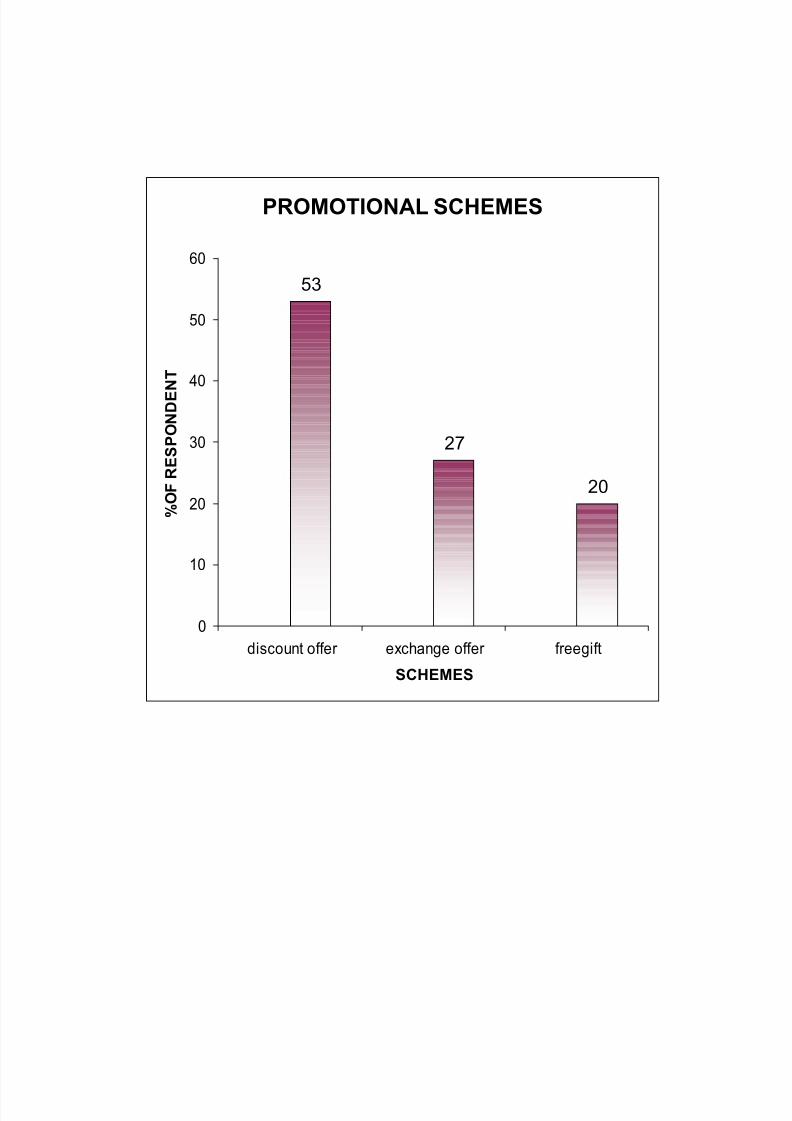

ATTRACTIVENESS OF PROMOTIONAL SCHEME:

Survey has revealed that out of 100 respondents 53 i.e.

53%have responded that discount offers attract them most. While 27%and

20%have responded that exchange offer and free gift attract them most.

High attraction for discount after signifies the price conscious market. Low

attraction for free gift can be attributed to consumer’s belief that companies add up

the cost of gift in the cost of actual product.

S.No. Scheme Type No. of respondents1. Discount offer 27

2. Exchange offer 13

3. Free gift 10

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 25/44

PROMOTIONAL SCHEMES

53

27

20

0

10

20

30

40

50

60

discount offer exchange offer freegift

SCHEMES

% O F R E S P O N D E N T

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 26/44

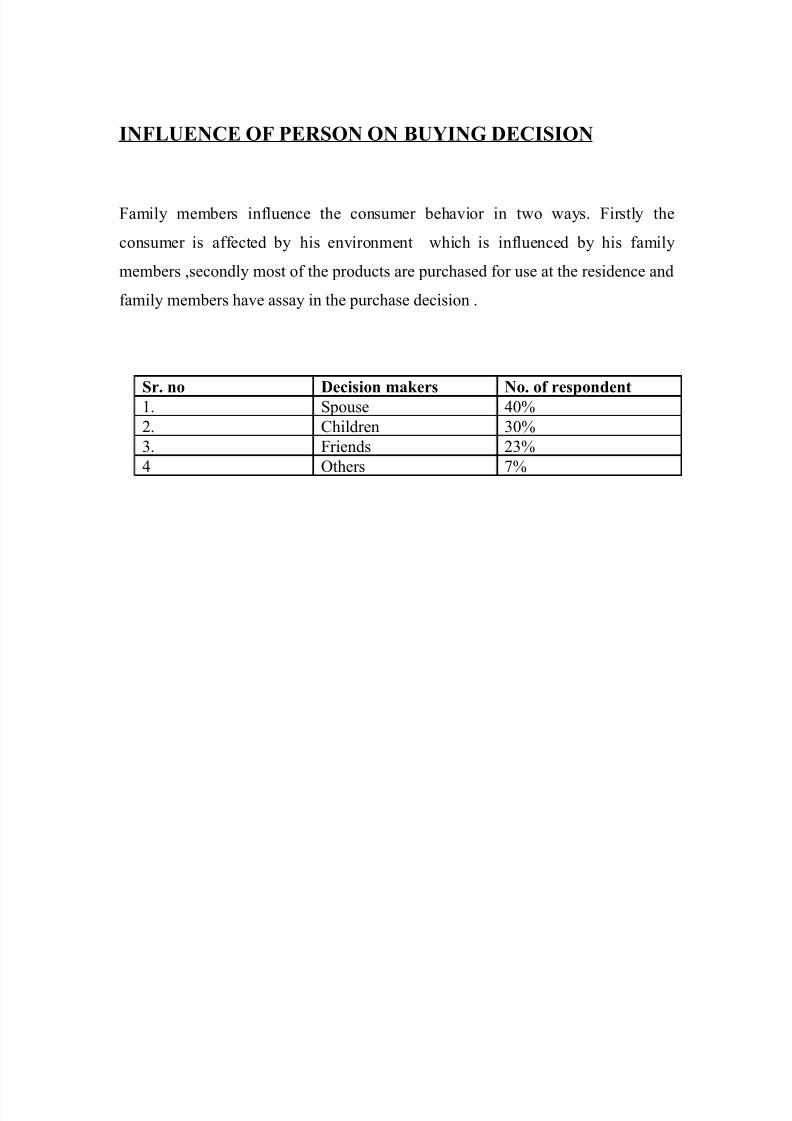

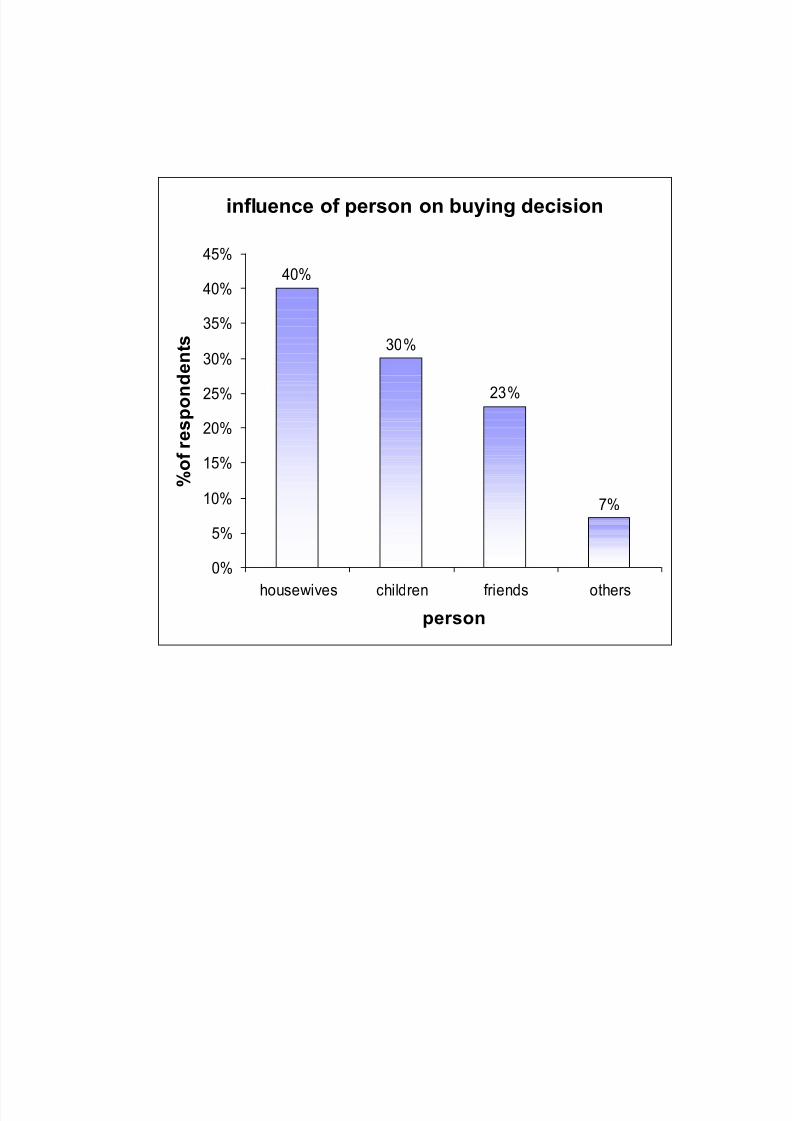

INFLUENCE OF PERSON ON BUYING DECISION

Family members influence the consumer behavior in two ways. Firstly the

consumer is affected by his environment which is influenced by his family

members ,secondly most of the products are purchased for use at the residence and

family members have assay in the purchase decision .

Sr. no Decision makers No. of respondent1. Spouse 40%

2. Children 30%

3. Friends 23%

4 Others 7%

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 27/44

influence of person on buying decision

40%

30%

23%

7%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

housewives children friends others

person

% o f r e s p o n

d e n t s

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 28/44

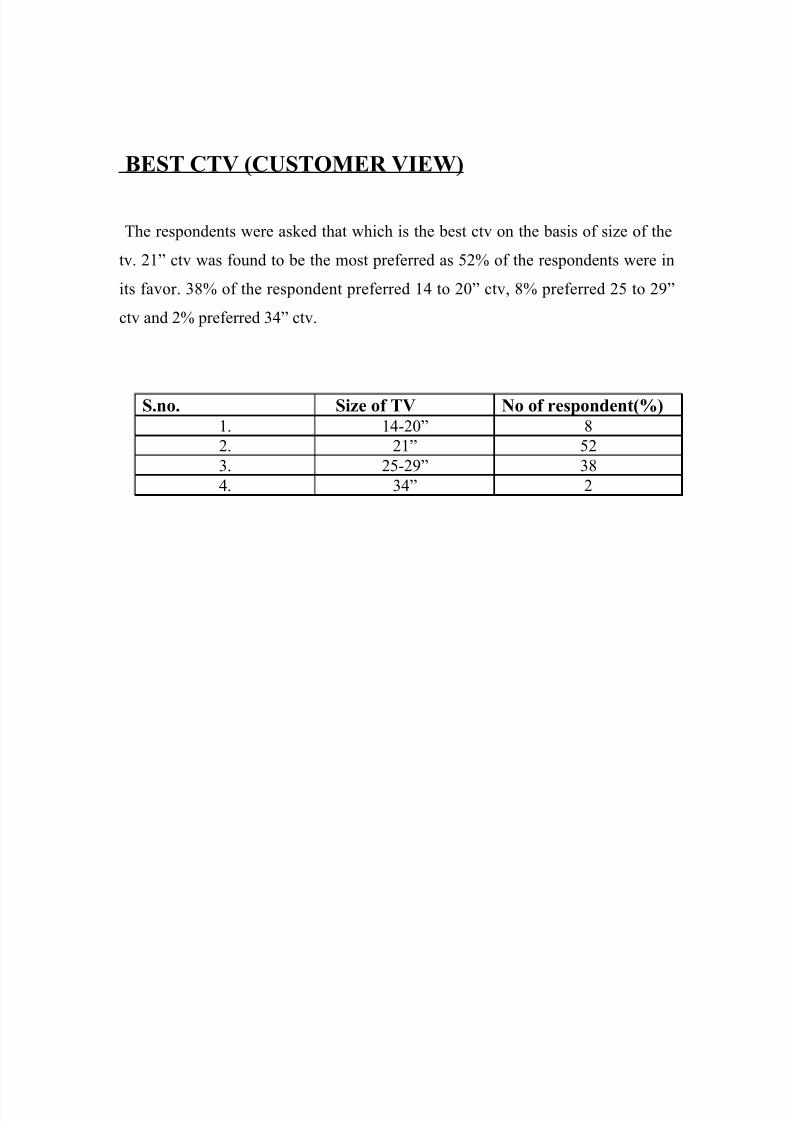

BEST CTV (CUSTOMER VIEW)

The respondents were asked that which is the best ctv on the basis of size of the

tv. 21” ctv was found to be the most preferred as 52% of the respondents were in

its favor. 38% of the respondent preferred 14 to 20” ctv, 8% preferred 25 to 29”

ctv and 2% preferred 34” ctv.

S.no. Size of TV No of respondent(%)1. 14-20” 8

2. 21” 52

3. 25-29” 38

4. 34” 2

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 29/44

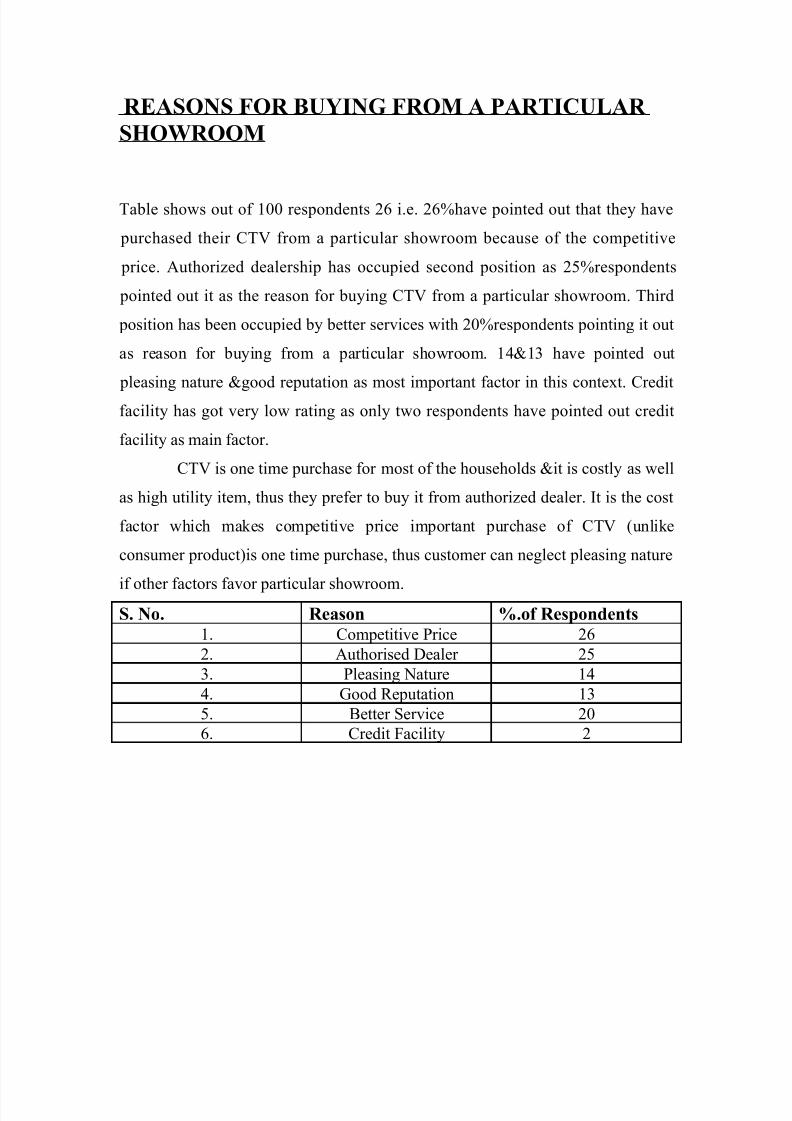

REASONS FOR BUYING FROM A PARTICULAR

SHOWROOM

Table shows out of 100 respondents 26 i.e. 26%have pointed out that they have

purchased their CTV from a particular showroom because of the competitive

price. Authorized dealership has occupied second position as 25%respondents

pointed out it as the reason for buying CTV from a particular showroom. Third

position has been occupied by better services with 20%respondents pointing it out

as reason for buying from a particular showroom. 14&13 have pointed out

pleasing nature &good reputation as most important factor in this context. Credit

facility has got very low rating as only two respondents have pointed out credit

facility as main factor.

CTV is one time purchase for most of the households &it is costly as well

as high utility item, thus they prefer to buy it from authorized dealer. It is the cost

factor which makes competitive price important purchase of CTV (unlike

consumer product)is one time purchase, thus customer can neglect pleasing nature

if other factors favor particular showroom.S. No. Reason %.of Respondents

1. Competitive Price 26

2. Authorised Dealer 25

3. Pleasing Nature 14

4. Good Reputation 13

5. Better Service 20

6. Credit Facility 2

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 30/44

Reasons for buying from a particular showroom

2625

1413

20

2

0

5

10

15

20

25

30

c o m p e t i t i v e p r i c e

a u t h

o r i s e d

d e a l e

r

p l e a

s i n g n a t u

r e

g o o d

r e p u t a t i o

n

b e t t e

r s e v i c e

c r e d i t f a

c i l i t y

Reasons

n o . o f r e s p o n d e n t %

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 31/44

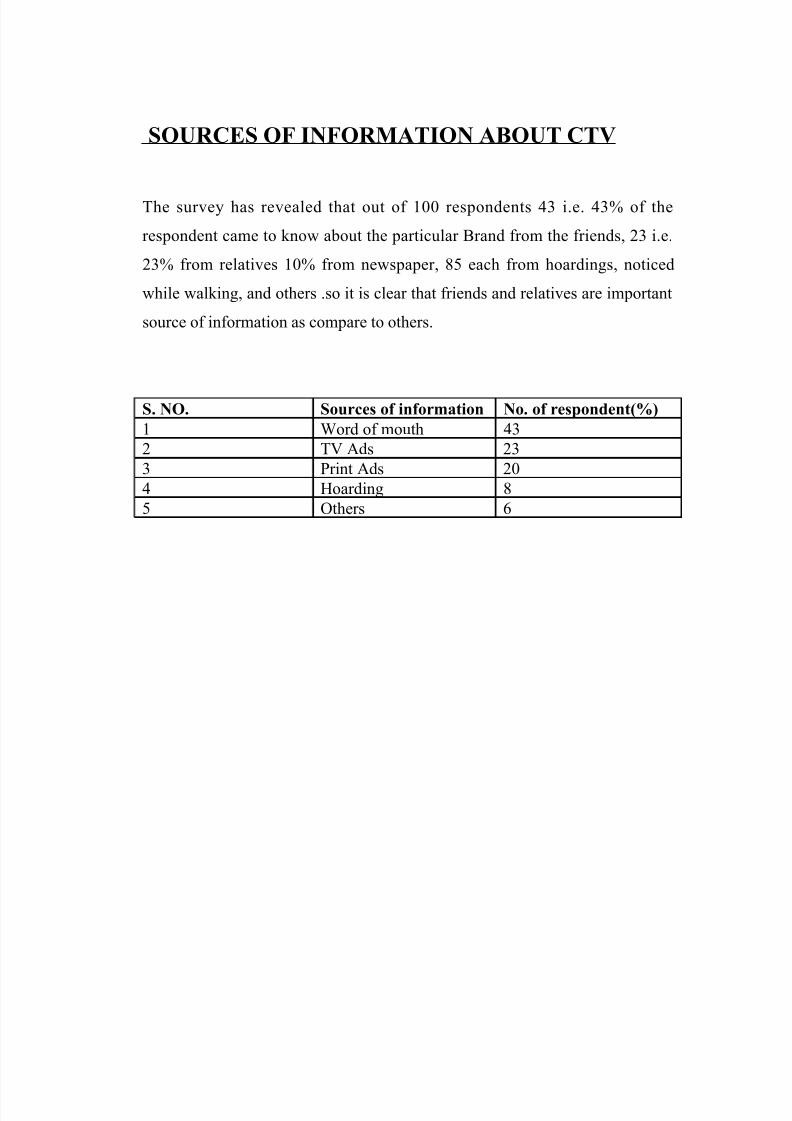

SOURCES OF INFORMATION ABOUT CTV

The survey has revealed that out of 100 respondents 43 i.e. 43% of the

respondent came to know about the particular Brand from the friends, 23 i.e.

23% from relatives 10% from newspaper, 85 each from hoardings, noticed

while walking, and others .so it is clear that friends and relatives are important

source of information as compare to others.

S. NO. Sources of information No. of respondent(%)

1 Word of mouth 43

2 TV Ads 23

3 Print Ads 20

4 Hoarding 8

5 Others 6

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 32/44

sources of information about showroom

43

23

10

8 8 8

0

5

10

15

20

25

30

35

40

45

50

Friends Relatives New spaper Hoarding Noticed w hile

w alking

Others

sources

%

o f r e s p o n d e n t s

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 33/44

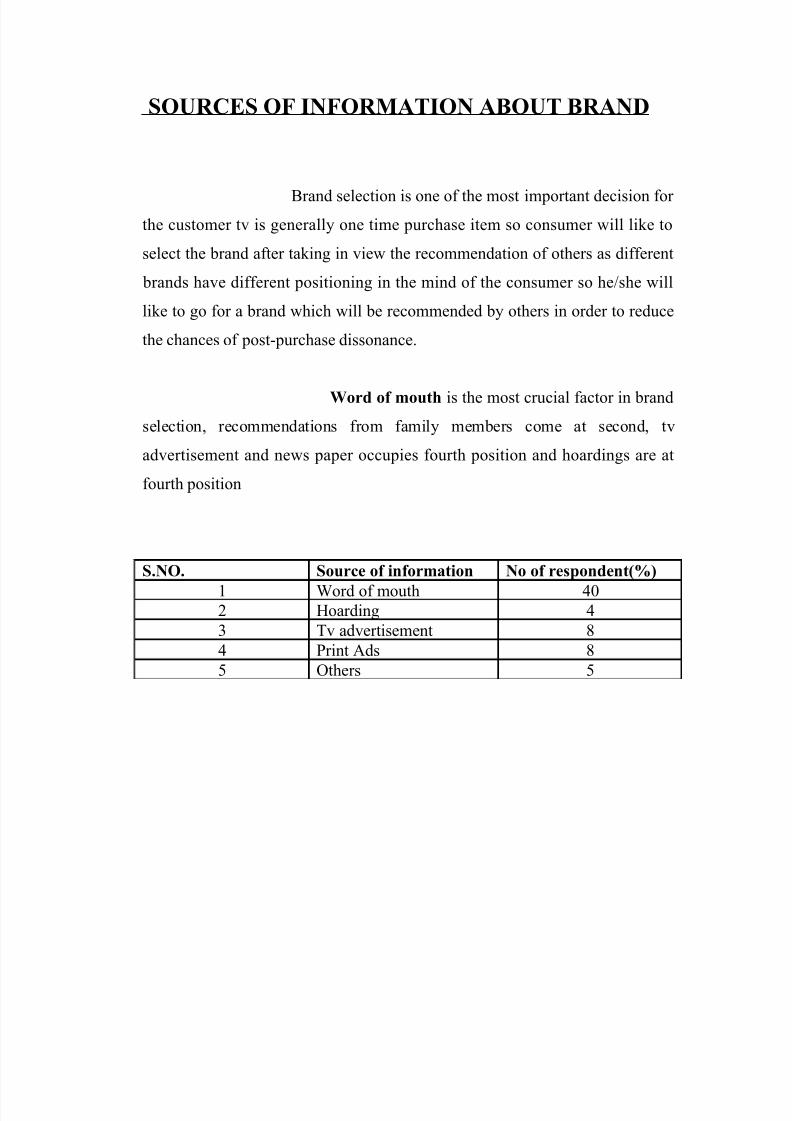

SOURCES OF INFORMATION ABOUT BRAND

Brand selection is one of the most important decision for

the customer tv is generally one time purchase item so consumer will like to

select the brand after taking in view the recommendation of others as different

brands have different positioning in the mind of the consumer so he/she will

like to go for a brand which will be recommended by others in order to reduce

the chances of post-purchase dissonance.

Word of mouth is the most crucial factor in brand

selection, recommendations from family members come at second, tv

advertisement and news paper occupies fourth position and hoardings are at

fourth position

S.NO. Source of information No of respondent(%)

1 Word of mouth 402 Hoarding 4

3 Tv advertisement 8

4 Print Ads 8

5 Others 5

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 34/44

Sources of information

WORD OF MOUYH

40%

HOARDING

4%TV AD

8%

NEWSPAPER/MAGAZIN

E

8%

VIDEOCASETTES

5%

RECOMMENDATIONS

FROM FAMILY

MEMBERS

33%

OTHERS

2%

WORD OF MOUYH

HOARDING

TV AD

NEWSPAPER/MAGAZINE

VIDEOCASETTES

RECOMMENDATIONS FROM FAMILY

MEMBERS

OTHERS

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 35/44

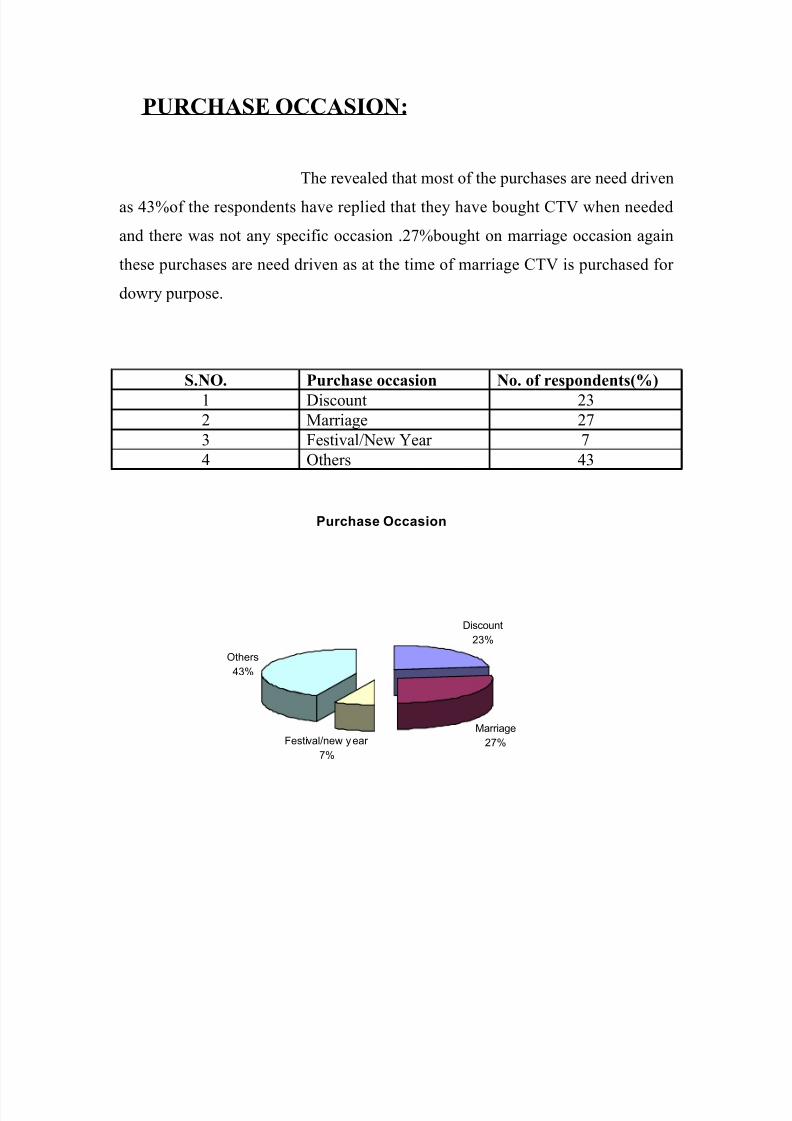

PURCHASE OCCASION:

The revealed that most of the purchases are need driven

as 43%of the respondents have replied that they have bought CTV when needed

and there was not any specific occasion .27%bought on marriage occasion again

these purchases are need driven as at the time of marriage CTV is purchased for

dowry purpose.

S.NO. Purchase occasion No. of respondents(%)

1 Discount 23

2 Marriage 27

3 Festival/New Year 7

4 Others 43

Purchase Occasion

Discount

23%

Marriage

27%Festival/new year

7%

Others

43%

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 36/44

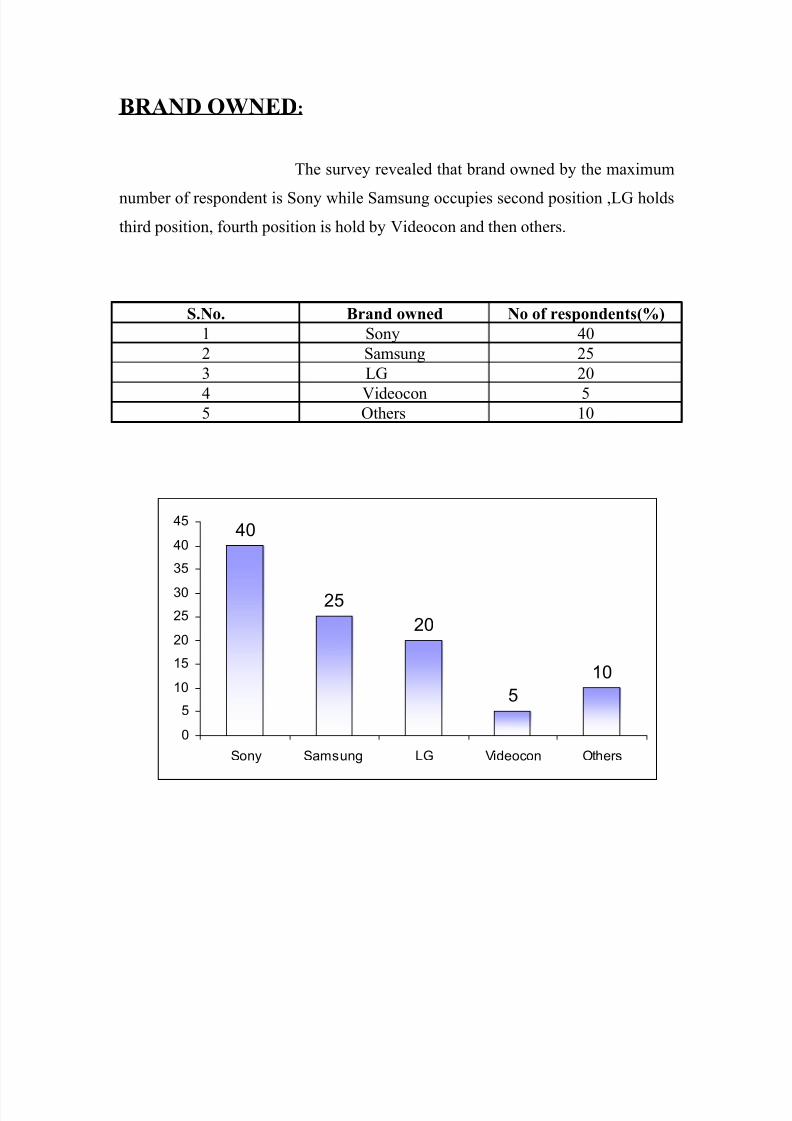

BRAND OWNED :

The survey revealed that brand owned by the maximum

number of respondent is Sony while Samsung occupies second position ,LG holds

third position, fourth position is hold by Videocon and then others.

S.No. Brand owned No of respondents(%)

1 Sony 40

2 Samsung 25

3 LG 20

4 Videocon 55 Others 10

40

25

20

5

10

0

5

10

15

20

25

30

35

40

45

Sony Samsung LG Videocon Others

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 37/44

SUMMARY AND CONCLUSIONS

This study attempts to know about the consumer buying behavior with regardto CTVs. What factors do the consumers have in their mind before they make up

their mind to purchase a CTV, this study finds to gain insight into these factors.

It has been observed from survey that Sony enjoys highest

penetration level, as 40% respondents own Sony, Samsung comes second as 25%

respondent owns it.

Majority of CTV owned by the respondent (about 77%) are of

capacity 21”, 20% are of size 25”.

Most of the Indian consumer purchases are need driven.

43% of the respondents have replied that they bought CTV when need and there

was not any specific occasion. 27% bought on marriage occasion, again these

purchase s are need driven as at the time of marriage CTV is purchased for dowry

purpose.

When it comes to source of information for the selection of

showroom it has been observed that friends and relatives are the major source of

information about the showroom.. Out of 100 respondents 43 and 33 relied on

friends and relatives (respectively) as source of information. Thus for selecting

showroom consumer relies on the personal sources than the impersonal sources

like advertisement, hoarding, newspaper etc.

Again as a source of information for brand choice consumer

relies heavily on word of mouth and recommendation of family members. Survey

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 38/44

has revealed that 40% of respondents relied on word of mouth and 33%on

recommendations of family members. Spouse has been found to be most

influential during purchase decision of CTVs.

Majority of respondents have pointed out that they bought

CTV from particular showroom because of competitive prices and authorized

dealership. This has been confirmed from the rating of factors affecting choice of

showroom/retailer as authorized dealer and competitive price are two top factors.

When it comes to the selection of showroom after sales service is less important

than above two factors as it (after sale service) is considered to be the

responsibility of company. After sale service is usually provided by the company.

After sale service, high quality, brand image, child lock are the

most significant factors influencing choice of brands with rating score more than

700.

Attractiveness of model, picture quality, advanced technology, warranty and

looks have been found to be the moderately significant with rating score between

500-700.

Availability of credit, easy availability, low price, foreign make and

graphic equalizers are less important factors with rating score less than 500. This

pattern has been confirmed from the analysis of factor that influenced the

respondents while buying their existing brand of CTV. Child lock, video games

which lies in less significant category according to the analysis of factors which

influenced customers while selecting their existing brands comes to most

significant category from of attributes. This can be attributed to the fact that most

of the existing CTVs (about 88%) have been purchased after (1991), before that

only 12%had purchased CTVs.

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 39/44

It has been clearly depicted from the study that level of

satisfaction among consumer is very high. Out of 100 respondents 83 i.e. 83%are

satisfied from the service of the showroom. So far as the satisfaction from the

brand /model owned 81 i.e.81%are satisfied. Good performance, picture qualityand good after sale service are the most important reasons for the high level of

satisfaction among the consumer. 15 out of 19 are dissatisfied consumers pointed

out that obsolete model as a reason for their dissatisfaction. From this we can

interpret that taste for more features is growing among consumers.

Sony and Samsung are found to be the most preferred brands,

Whereas preference for Videocon is minuscule. LG and Philips enjoy moderate

preference. Aiwa and Akai are less preferred brands.

In terms of popularity (brand recall test) Sony has been found to be most

popular brand with weighted mean of (first, second, third)20.66 Samsung and LG

comes second and third respectively in popularity with weighted average 15.66

and 13.66 respectively. Thus Sony and Samsung can be attributed to these fact that

these two are very old and reliable in CTV market. Popularity of Samsung is high

because of the aggressive advertisement campaign by the company.

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 40/44

RECOMMENDATIONS

1) Sony, LG, Samsung, Philips have been able to dominate the market with

simple, brief and heart winning messages. So by giving more importance

to the composition of the messages the companies can increase their impact

on the consumers.

2) To attract consumers the company should improve the quality of their CTV.

The advertisement copies should stress on the quality of the brands, their

superiority, highlighting technological, features, and the wide network of

after- sale- services.

3) The present study reveals that the ‘Brand Name’ has most important

bearing on the minds of the consumer at the time of deciding their choice of

brand of color TV there fore every effort should be made through

advertisement to build up and strengthen the brand image.

4) Proper feedback should be undertaken by the marketer in order to find out

the loopholes in their performance and undertake all possible actions to

overcome the same.

5) The role of advertisement as the study has highlighted needs to be

appreciated. Since attractive well-planned advertisement campaign can play a

very vital role in the increasing the share of brand in the CTV market. Every

manufacturing organization should have a separate ‘advertisement cell’ with

intelligent and experienced marketing professional who should be made

responsible of making advertisements more attractive .eye catching and

purposeful.

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 41/44

QUESTIONNAIRE

Q1. Name the brands of CTVs which you can recall first?

(a) (b) (c)

Q2. Which brand of CTV do you own?

(a) Name ………(b) Size………(c)Year of purchase…………

Q3 On which occasion you bought CTV?

(a) New Year (b) Festival (c) Marriage

(d) Discount Offer (e) Any Other

Q5 What were the information sources used by you while selecting the

brand of CTV?

(a) Word of mouth (b) Hoarding

(c) TV advertisement (d) Print ads

(e) Any others(Specify)

Q5 Who influenced your decision the most to buy a particular brand of

CTV?

(a) parents (b) Children

(c) Friends (d) Any other

Q6 Which of the following factors influence you while buying particular

brand of CTV(please tick as many as possible)

(a) Low price (b) Brand image

(c) Better quality (d) Easy availability

(e) Attractiveness of the model (f) Any Other(Please Specify)

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 42/44

Q7. Are you satisfied with the service / after –sale- service ?

(a) Yes (b) No

Q8.

(I) Are you satisfied with the brand or model you

bought?

Yes No

(II) If no then tick as many as possible:-

(a) Poor performance

(b) Poor after sale service

(c) Model looks obsolete

(d) Picture quality

(e) Any other (specify)

(III) If yes tick as many as possible:-

(a) Good performance

(b) Good after sale service

(c) Picture quality

(d) Better looks

(e) Any other `

Q9. Rank the following according to your preference.

(a) Samsung (b) LG (c) Sony

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 43/44

(d) Videocon (e) Any other

Q10. What attracts you more?

(a) Free gifts (b) Discount factor (c) Exchange offer

8/3/2019 FINAL Television Industry

http://slidepdf.com/reader/full/final-television-industry 44/44

Recommended