MANAGEMENT REPORT

MA

NA

GEM

ENT

REP

OR

T

CONTENTS

1. ABOUT THE BANK

2. FINANCIAL RESULTS •MacroeconomicEnvironment •OurResults

3. OUR BANK AT THE SERVICE OF CUSTOMERS

•OurSegments •ProductsandServices •PhysicalandElectronicChannels •TreasuryandForeignCurrency •Customer’sstories

4. TOWARDS A MORE DIGITAL BANK

5. WE ARE HELPING TO BUILD A BETTER SOCIETY

•OurTalent •OurCommitmenttoSociety

12

24

44

72

78

Management Report 2018 3

*Employees include full-time employees, personnel employed through temporary agencies and outsourced personnel. It does not include 663 SENA students (contract trainees).**Reflects the number of Banco de Bogotá, Porvenir, Almaviva, Banco de Bogotá Panama, Fiduciaria Bogotá and BAC Credomatic branches. Banco de Bogotá and BAC represent 1,443 branches.

Financial Performance

Banco de Bogotá - Main Indicators UNCONSOLIDATED CONSOLIDATED

2017 2018 2017 2018

Net Income (2)

1,924 2,8252,296 3,131

Net Income Attributable to Shareholders(2) 2,064 2,937Profitability RatiosROAA (3) 2.3% 3.3% 1.6% 2.1%ROAE (4) 12.0% 16.8% 12.5% 17.1%Net Interest Margin (5) 5.4% 5.2% 6.0% 5.7%Fee Income (6) 21.8% 22.3% 35.6% 34.8%Administrative Efficiency (7) 38.7% 35.9% 49.2% 47.5%Total Solvency Ratio 21.2% 20.7% 13.5% 13.5%Basic Solvency Ratio 13.8% 13.2% 8.8% 8.9%Loan Portfolio Quality (8)

Past Due Loans / Gross Loans (9) 3.9% 4.4% 3.5% 4.0%Loan Allowances / Past Due Loans (9) 123.4% 136.0% 90.8% 116.7%

(1) Includes repos and interbank operations.(2) Figures in billions of pesos. (3) Annual Net Income/Average Quarterly Assets for the year (includes the quarters ending in December of the previous year, and those ending in March, June, September and December of the current year).(4) Annual Net Income Attributable to Shareholders/Average Attributable Quarterly Equity for the year (includes the quarters ending in December of the previous year, and those ending in March, June, Septem-ber and December of the current year).(5) Net Interest Income from the Period/Average Quarterly Earning Assets for the year (includes the quarters ending in December of the previous year, and those ending in March, June, September and Decem-ber of the current year).(6) Gross fee-income/net interest income from allowances + gross fee-income + other operating income. Excludes other income from operations. (Does not include Net Income Share from affiliates, nor dividends from the unconsolidated operation.)(7) Personnel expenses + administrative expenses before annual depreciation and amortization/operating income before allowances. For the Unconsolidated Bank the 2017 ratio was recalculated due to the deterioration of other assets being reclassified as “other operating expenses”; they were previously included as “administrative expenses.”(8) Loan portfolio indicators are calculated with gross loans, including portfolio accounts receivable.(9) Past due loans: more than 30 days overdue.

Banco de Bogotá - Balance sheetUNCONSOLIDATED CONSOLIDATED

Figures in IFRS (billions of COP) 2017 2018 2017 2018

Assets 83,276 91,360 149,405 163,303Cash and Equivalents 6,195 8,214 16,925 22,061Loans and Financial Leases, Net (1) 53,183 55,843 104,244 111,018Fixed Income Investments, Net 4,594 4,526 12,337 11,989Equity Investment, Net 16,294 19,113 4,967 6,169Other Assets 3,009 3,665 10,932 12,065Liabilities 66,553 73,098 131,195 143,635Deposits 51,973 54,131 100,947 108,405Other Liabilities 14,580 18,966 30,248 35,230Equity 16,723 18,263 18,210 19,668

MILLIONSOF CLIENTS

21.3 45,536

EMPLOYEES* BRANCHES**

1,564 3,804

ATMS

MARKET

Net Loans12.2% 13.8%

11

PRESENCE

11,739

SHAREHOLDERS

SHAREMARKET

SHARE

Deposits Net Loans10.1% 9.4%

Deposits

Countries

Razones de Rentabilidad

Balance General - Consolidado

Activos

Pasivos

Patrimonio

Efectivo y Equivalentes de Efectivo

Cartera de Créditos y Leasing Financiero, Netos

Inversiones en Títulos de Deuda, Netas

Inversiones en Títulos Participativos, Netas

Otros Activos

Depósitos

Otros Pasivos

2,296 3,131

Principales Indicadores

2,064 2,937

Utilidad Neta

Utilidad Neta Atribuible a Accionistas

Relación deSolvencia Básica

Cartera Vencida /Cartera Bruta

Provisión Cartera /Cartera Vencida

ROAA ROAE Margen Netode Intereses

Ingresos porComisiones

EficienciaAdministrativa

Relación deSolvencia Total

1.6%2.1%

8.8%8.9%

3.5%4.0%

90.8%116.7%

12.5%17.1%

6.0%5.7%

35.1%33.2%

49.2%47.5%

13.5%13.5%

2017

2018

149,405

16,925

131,195

2017

104,244

12,337

4,967

10,932

100,947

30,248

18,210

163,303

22,061

143,635

2018

111,018

11,989

6,169

12,065

108,405

35,230

19,668

MARKETSHARE

MARKETSHARE

Management Report 2018 Management Report 2018 54

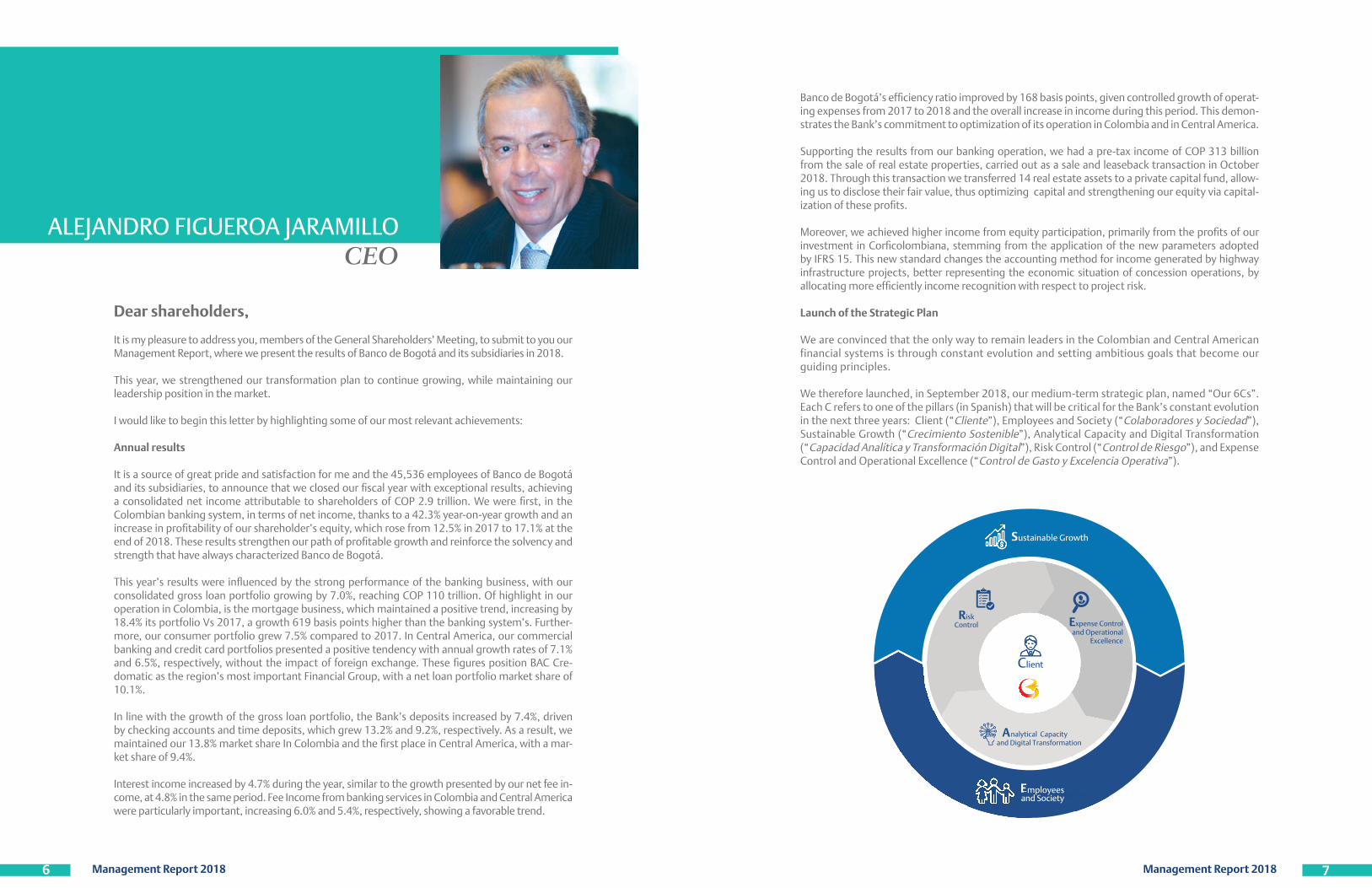

ALEJANDRO FIGUEROA JARAMILLOCEO

Dear shareholders,

Itismypleasuretoaddressyou,membersoftheGeneralShareholders’Meeting,tosubmittoyouourManagementReport,wherewepresenttheresultsofBancodeBogotáanditssubsidiariesin2018.

Thisyear,westrengthenedour transformationplan tocontinuegrowing,whilemaintainingourleadershippositioninthemarket.

Iwouldliketobeginthisletterbyhighlightingsomeofourmostrelevantachievements:

Annual results

Itisasourceofgreatprideandsatisfactionformeandthe45,536employeesofBancodeBogotáanditssubsidiaries,toannouncethatweclosedourfiscalyearwithexceptionalresults,achievinga consolidatednet incomeattributable to shareholdersofCOP2.9 trillion.Wewerefirst, in theColombianbankingsystem,intermsofnetincome,thankstoa42.3%year-on-yeargrowthandanincreaseinprofitabilityofourshareholder’sequity,whichrosefrom12.5%in2017to17.1%attheendof2018.TheseresultsstrengthenourpathofprofitablegrowthandreinforcethesolvencyandstrengththathavealwayscharacterizedBancodeBogotá.

Thisyear’s resultswere influencedbythestrongperformanceof thebankingbusiness,withourconsolidatedgross loanportfoliogrowingby7.0%,reachingCOP110trillion.Ofhighlight inouroperationinColombia,isthemortgagebusiness,whichmaintainedapositivetrend,increasingby18.4%itsportfolioVs2017,agrowth619basispointshigherthanthebankingsystem’s.Further-more,ourconsumerportfoliogrew7.5%comparedto2017.InCentralAmerica,ourcommercialbankingandcreditcardportfoliospresentedapositivetendencywithannualgrowthratesof7.1%and6.5%,respectively,withoutthe impactof foreignexchange.ThesefigurespositionBACCre-domaticastheregion’smostimportantFinancialGroup,withanetloanportfoliomarketshareof10.1%.

Inlinewiththegrowthofthegross loanportfolio,theBank’sdeposits increasedby7.4%,drivenbycheckingaccountsandtimedeposits,whichgrew13.2%and9.2%,respectively.Asaresult,wemaintainedour13.8%marketshareInColombiaandthefirstplaceinCentralAmerica,withamar-ketshareof9.4%.

Interestincomeincreasedby4.7%duringtheyear,similartothegrowthpresentedbyournetfeein-come,at4.8%inthesameperiod.FeeIncomefrombankingservicesinColombiaandCentralAmericawereparticularlyimportant,increasing6.0%and5.4%,respectively,showingafavorabletrend.

BancodeBogotá’sefficiencyratioimprovedby168basispoints,givencontrolledgrowthofoperat-ingexpensesfrom2017to2018andtheoverallincreaseinincomeduringthisperiod.Thisdemon-stratestheBank’scommitmenttooptimizationofitsoperationinColombiaandinCentralAmerica.

Supportingtheresults fromourbankingoperation,wehadapre-tax incomeofCOP313billionfromthesaleofrealestateproperties,carriedoutasasaleandleasebacktransactioninOctober2018.Throughthistransactionwetransferred14realestateassetstoaprivatecapitalfund,allow-ingustodisclosetheirfairvalue,thusoptimizingcapitalandstrengtheningourequityviacapital-izationoftheseprofits.

Moreover,weachievedhigherincomefromequityparticipation,primarilyfromtheprofitsofourinvestment inCorficolombiana, stemming fromtheapplicationof thenewparametersadoptedbyIFRS15.Thisnewstandardchangestheaccountingmethodforincomegeneratedbyhighwayinfrastructureprojects,better representing theeconomicsituationofconcessionoperations,byallocatingmoreefficientlyincomerecognitionwithrespecttoprojectrisk.

Launch of the Strategic Plan

WeareconvincedthattheonlywaytoremainleadersintheColombianandCentralAmericanfinancialsystemsisthroughconstantevolutionandsettingambitiousgoalsthatbecomeourguidingprinciples.

Wethereforelaunched,inSeptember2018,ourmedium-termstrategicplan,named“Our6Cs”.EachCreferstooneofthepillars(inSpanish)thatwillbecriticalfortheBank’sconstantevolutioninthenextthreeyears:Client(“Cliente”),EmployeesandSociety(“ColaboradoresySociedad”),SustainableGrowth(“CrecimientoSostenible”),AnalyticalCapacityandDigitalTransformation(“CapacidadAnalíticayTransformaciónDigital”),RiskControl(“ControldeRiesgo”),andExpenseControlandOperationalExcellence(“ControldeGastoyExcelenciaOperativa”).

Expense Controland Operational

Excellence

RiskControl

Analytical Capacityand Digital Transformation

Client

EEmployees

Sustainable Growth

and Society

Management Report 2018 Management Report 2018 76

1. Client:Thecentralpillarofourstrategy isourClient,also recognizedas thecenterofourbusinessmodel.Weensurememorableexperiencestowinourcustomers’loyaltyandreferrals.

2. Employees and Society:Wesupportouremployees’growthandwatchovertheirwellbeing,positivelyimpactingsociety.

3. Sustainable Growth:Weexpandourbusinessprofitably, focusingoncapturingnewcus-tomersbycomprehensivelymanagingtheirlifecyclesandtheirmulti-channelexperience.

4. Risk Control:Wecomprehensivelymanagetherisksinherenttothebusiness,maintaininghealthygrowthofourportfolioandstrengthofourbalancesheet.

5. Expense Control and Operational Excellence:Weefficientlycontrolspendingandestab-lishagile,simpleandsecureprocessestoachieveexcellenceinouroperations. 6. Analytical Capacity and Digital Transformation:Wetransformourcustomers’livesbyof-feringdigitalexperiences,applying technology tobusinessprocessesandstrengtheningourcapabilitiesindataanalysis.

Withthedefinitionofthisstrategy,westrivetomaintainourleadershipincommercialbankingandexpandourpresenceinretailbankingthroughenhancedcustomerexperiences,leading-edgedigi-taltools,andcontinuousconsolidationofoperationalexcellenceandriskmanagement.

Commitment with the Bank’s Digital Transformation

Consideringtheimportanceofdigitization,Iwouldliketofocusononeofourstrategiccorporatepillarsinparticular:“AnalyticalCapacityandDigitalTransformation.”Throughthispillar,wedi-rectlyaddressthechallengesoftoday’ssocietyand,bydoingso,createtoolsthataddvalueandrepresentuniquesolutionsthatimprovecustomerexperienceandprocessefficiency.

TheWorld Economic Forumhas referred to our era as the “Fourth Industrial Revolution”,whichhasbroughtaboutthefastestandmostdrasticsocialandeconomicchangeinhistory;thebankingindus-tryhasnotbeenstrangertothistransformation.Digitization,efficiency,timetomarket,apps,FinTechs,Google,Facebookandbotsarewordsthathavetakenoverthebankingvocabularyand,BancodeBogotá,alwaysattheforefrontofthefinancialsysteminColombia,hassuccessfullyundertakenthischallenge.

Ourdigitalstrategyisbasedontwocoreprinciples:providebetterservicetoourcustomers,anddoitinamoreefficientway.Notlongago,achievingthesetwoobjectivessimultaneouslywouldhavebeenunthinkable,butbybuildingupourinternaldigitalcapabilities,todaywearereachingmorecustomerswithbetterservicesandproductsatafractionofthecost.

Undertheseparameters,wehaveundertakenourdigital transformation inColombia,throughthefollowing:

1. Digital sales channel:Weareworkingtomakeallofourretailbankingproductsandservicesavail-ablethroughdigitalchannels,improvingcustomerexperienceand,atthesametime,optimizingprof-itabilityofouroperation.In2018,morethan36%ofsavingaccountsand31%ofcreditcardswereopenedviadigitalchannels.Furthermore,wecontinueconsolidatingourdigitalportfoliobylaunch-ingotherproductssuchasPersonal,PayrollandMortgageLoansthroughourwebsiteandapp.

2. Digital service channel:Nowthatourmobileappandwebsitearethepreferredoptiontocompletetransactions,wehavemorethan1.2millioncustomersusingourdigitalsolutions,rep-resentingaparticipationofourcustomersindigitalchannelsof73.5%.

3. Analytical capacity:Toleverageopportunitiesinthisfieldandcreatevalueforourcustomersandshareholders,weareusingITtoolsandexpertdata-analyststomoveforwardinthedevelop-mentofpredictivemodels-whichallowustoofferpersonalizedservices,therebyimprovingour

valuepropositionandtheexperienceweoffertocustomers-suchastheuseofinformationtoimproveouroperationalefficiency.

OursubsidiaryBACCredomatichasalsobeenmovingaheadindigitaltransformation,withposi-tiveresultsforbusinessesandcustomers inCentralAmerica.Asaresult,wehavebeenabletopositionourserviceportfolioindigitalchannelsandstrengthencommercialrelationships.Mean-while,thepaymentmethodstrategyhasbeenstrengthenedthroughinitiativesgearedtowardspromotionandusageofon-lineproducts,processsimplification,andimproveduserexperienceondigitalplatforms.Bytheendof2018,thereweremorethan1.1millionusers.

Financial Inclusion and Access

Webelieveintheprogressofoursocietyandourcountry.Thatiswhywearecommittedtofurtherpenetrationintheuseofbankingservices(“bancarización”)andfinancialinclusion,sothatmoreandmoreColombianshaveaccesstothebenefitsofthefinancialsystem.

In2018webegangrantingloanstocustomersinruralareas,backedbyguarantees-“RespaldoDCA”-promotedbytheUnitedStatesAgencyforInternationalDevelopment,USAID,thatcover50%ofloantransactions,inmorethan245municipalitiesnationwide.Throughthisguarantee,wehavegrantedmorethan7,100loansworthCOP40billion.Also,throughourmicrofinancemodel,weareservingcustomersinmorethan730municipalitiesand,thankstoourpartnershipwiththeCoffeeGrowersNationalFederation(FederaciónNacionaldeCafeteros),morethan370,000coffeegrowershaveac-cesstothebankingsystemviathe“CoffeeGrower’sSmartCard”(“CédulaCafeteraInteligente”).

WehavealsomovedforwardwithourFinancialEducationprogram,targetedforchildren,youngpeople,adultsandsmallbusinessownersacrossthecountry.In2018,wetrained40,395peoplethroughworkshopsandlivelecturesinourmobileclassrooms. Conclusion

Wehope that the local economy continues along the road to recovery,withgrowth above lastyear’s,andthatinflationremainsundercontrol.Weareoptimisticthattheresurgenceofinternalconsumption, infrastructureprojectsandconstruction, aswell as a strongperformanceofnon-traditionalexportswilldrivethenationaleconomy.

ThesuccessofourstrategyisbasedonourhumantalentatalltheBank’slevels.Withtheirknowl-edge,professionalismandappropriateriskmanagement,theymakeitpossibleforustoachieveourgoalsandobjectives.

TheBankismorepreparedeverydaytoconsolidateandincreaseitsnationalandregionalleader-ship,witharobustbalancesheet,efficientandprofitableresults,andaculturefocusedonconstantevolutionandexcellentcustomerservice.

Ithankeachandeveryoneofyou,ourshareholders,becausewithyourconstantsupportandcon-fidenceinourBank,wewillcontinueofferingfinancialservicesthathelpbuildabettersocietyinallofthecountrieswhereweoperate.

Sincerely,

Alejandro Figueroa JaramilloCEO

Management Report 2018 Management Report 2018 98

Best Bank in Central America andThe Caribbean, 2018.

Best Bank in Costa Rica 2018

Best Bank in Central America 2018,Best Bank in Nicaragua 2018

Digital Innovator Bank of the year 2018 inCentral America and The Caribbean.

Best Bank of the year 2018 – Costa Rica

Best Digital Bank in Costa Rica.Best Digital Bank in Panama.

Best Mobile Bank App in Costa Rica.Best Mobile Bank App in Panama.

Award “Learning readiness, innovation,organizational culture and

digital sustainability”.

Bank with the best reputationin the country, Costa Rica

Inclusive company, Costa Rica Socially responsible company award since 2007to date. 2018 Award, XII edition – Honduras.

Together, we did itTheconfidenceofourcustomersandshareholders,aswellasthehardworkofourem-ployees,earnedusthesehonors.TheyinspireustokeepworkingtosupportthegrowthofColombiansandourcountry.

Best Bank of the year in Colombia 2018 Best Bank in Colombia 2018 Best Foreing Exchange ProvidersAwards 2019

Best Trade Finance ProvidersAwards 2019

Project and Infraestructure�nancing 2018:

Paci�co II Project

Best Economic Research Areain Colombia, Macroeconomic

Aggregates, chosen byindustrial sector

The Green Collectionproduct was rewarded in theSustaniable Finance category

The Bizz Awards – World Confederationof Businesses (WORLDCOB)in the category “Be a legend”

Capital Finance International Award 2018,Excellent governance performance

Global Brands Magazine Award –Best CSR pension fund initiative, 2018

Fiduciaria Bogotá among thebest places to work in 2018.

Number 20 – Category:more than 500 employees.

Derivative market forum“Market dynamizing”

Our subsidiary BAC Credomatic has been recognized as the Best Bank in Central America:

Our subsidiary Porvenir has been recognized as:

Our subsidiary Fidubogotá has been recognized as:

Management Report 2018 Management Report 2018 1110

About the Bank

Presence and

GuatemalaBranches: 208

Bankingcorrespondents: 969

ATMs: 269

El Salvador

Branches: 81

Bankingcorrespondents: 309

ATMs 298

PanamaBranches: 53

Bankingcorrespondents: 788

ATMs: 230

Costa RicaBranches: 125

Bankingcorrespondents: 2,081

ATMs: 545

HondurasBranches: 146

Bankingcorrespondents: 1,419

ATMs: 435

NicaraguaBranches: 129

Bankingcorrespondents: 2,748

ATMs: 285

ColombiaBranches: 701

Bankingcorrespondents: 9,444

ATMs: 1,742

Coverage

TotalBranches: 1,443*

Banking correspondents: 17,758

ATMs: 3,804

United States New York

Miami

*Corresponds to Banco de Bogotá and BAC Credomatic Branches

Chapter 1 • About the Bank Management Report 2018 13

For further details, our shareholders’ information is pub-lishedattheBank’swebsiteandisalsoavailableontheSe-curitiesMarket InformationSystem(SIMEV, for theSpanishoriginal) of the Financial Superintendence of Colombia atwww.superfinanciera.gov.co.

11.3%

11.7%

68.7%

Other companiesSarmiento Angulo Organization

Others

668 7

7%

68 7

%

68

%

68

%%%%%%%%%%

8.3%

PazBautistaGroup

Attheendof2018,wecontinuedtobeoneofthelargestbanksintheColombianandCentralAmericanfinancialsectors.Ourcommitmenttosustainablegrowththatcontributestotheeco-nomicdevelopmentofthecountryaswellasthegrowthofourcustomersandemployeeshelpustostandout.

WehighlighttheevolutionofourMortgage,Micro-creditandConsumerportfolios,whichhasallowedustodiversifyourport-foliooffinancialproducts.Furthermore,theoptimizationofourexpenseshasresultedinanimprovedefficiencyratio.

Wearesettingthebarfordigitalbanking,leadinginnovationinfinancialservicesforthebenefitofourcustomers,andbecom-ingmoreefficientandresponsiveintheprocess.Byincorporat-ingnewprocesses,talentandworkstreams,wehavebeenabletoexpandourdigitalportfolio.

Corporate GovernanceThroughoutourhistory,wehavebeencommittedtoatrans-parentCorporateGovernancemodel thathas evolvedoverour148yearsofexperience,byimplementingbestpractices.Thiscommitmentallowsustoproduceresultsthataresus-tainable for our shareholders, customers, employees andotherstakeholders.

The significant events of 2018 that have strengthened ourGovernancemodelarehighlightedbelow:

1. OnMarch 22, the General Meeting of Shareholders ap-provedtheBoardofDirectorsAppointmentandRemunera-tionPolicy,incompliancewiththecorporateguidelines.

2.AtthesameMeeting,shareholderswereinformedoftheCorporateGovernanceCode,whosereformwasapprovedbythe Board ofDirectors onDecember 5, 2017. The reformsimplementedrecommendationsfromtheCodeofBestBusi-nessPracticesoftheFinancialSuperintendenceofColombia(“CódigoPaís”).

3.We submitted the 2018 Best Business Practices Imple-mentation Report to the Financial Superintendence ofColombia,which continues to reflect theevolutionof the“Código País” recommendations. The report is publishedonourwebsitewww.bancodebogota.com, in the InvestorRelationssection.

4.TheBankComptroller’sOfficereviewedtheCorporateGover-nanceprocesses,consideringaspectsrelatedtotheimplemen-tationof“CódigoPaís”,aswellas thepublicationofRelevantInformation.Thefindingsoftheassessmentshowsatisfactoryperformanceoftheseprocesses,indicatingprogressintheim-plementationofCorporateGovernancestandardsandcompli-ancewiththecontrolsestablishedtoensurethatthemarketisprovidedwithtimelyandtransparentinformation.

General Meeting of ShareholdersAsthehighestgovernancebody,theGeneralMeetingofShare-holdersguidesandoverseestheBank’soperations,aswellastheprinciplesunderwhichthoseoperationsareperformed.

The Bank’s capital as ofDecember 2018was represented byatotalof331,280,555commonsharesheldby11,739share-holders.Themainshareholdersare:

BankAbout the

Board of Directors

Board of Directors

Principal members Alternate Members

Luis Carlos Sarmiento Gutiérrez Jorge Iván Villegas Montoya

Sergio Uribe Arboleda* Sergio Arboleda Casas*

Alfonso de la Espriella Ossio Ana María Cuellar de Jaramillo

Carlos Arcesio Paz Bautista Álvaro Velásquez Cock

José Fernando Isaza Delgado* Carlos Ignacio Jaramillo Jaramillo*

Board of Directors’ Advisor

Luis Carlos Sarmiento Angulo

General Secretary

Alberto Pérez Vélez

Statutory Auditing Firm

KPMG S.A.S.

Represented by:Pedro Ángel Preciado Villarraga T.P.30723-T

Financial Consumer Ombudsman

Octavio Gutiérrez Díaz

*Independent members.

Luis Carlos Sarmiento Gutiérrez, President of the Board and Luis Carlos Sarmiento Angulo, Advisor of the Board.

Chapter 1 • About the Bank Management Report 2018 Chapter 1 • About the Bank Management Report 2018 1514

Jorge Iván Villegas Montoya

PhDinLegalandEconomicSciencesfromUniversidadJaverianawithaSpecializationinBusi-nessLawfromColegioMayorNuestraSeñoradelRosario.HehasbeenanalternatememberofBancodeBogotá’sBoardofDirectorssince1988.HeisalsoamemberoftheBoardofDi-rectorsofCorporaciónFinancieraColombianaandFidubogotá.

Sergio Arboleda Casas

Civil Engineer fromUniversidadde losAndes.HehasbeenanalternatememberofBancodeBogotá’sBoardofDirectorssince1990.HeisalsoamemberoftheBoardofDirectorsofBancodeBogotáS.A.PanamaandCasaEditorialElTiempo.

Ana María Cuéllar de Jaramillo

AccountantfromUniversidadJorgeTadeoLozano.ShehasbeenanalternatememberofBancodeBogotá’sBoardofDirectorsandtheBoardofDirectorsofMegalíneasince2007.She isamemberoftheBoardofDirectorsofBACCredomaticandGrupoAval.

Álvaro Velásquez Cock

PhD in Economic Sciences fromUniversidad de Antioquia,MSc candidate from the LondonSchoolofEconomics.HewasanalternatememberofBancodeBogotá’sBoardofDirectorsfrom1983to1988,andagainsince2001;DirectoratGrupoAvalandCorporaciónFinancieraColombiana.

Carlos Ignacio Jaramillo Jaramillo

Lawyer from Universidad Javeriana, MSc in Insurance Law and Economics from UniversitéCatholiquedeLouvainandPhDinLawfromUniversidaddeSalamanca.Hehasbeenanalter-natememberofBancodeBogotá’sBoardofDirectorssince2018.

Alternate Members

ThedecisionsofourBoardofDirectorsarecontinuouslyalignedwithourinternalcontrolsystem,whichgovernstheperformanceofouroperations.Aspartofitsstructure,theBoardofDirectorshasestablishedaworkplanthatallowsittomeetasoftenasneces-sarytofulfillitsrolesofdirectionandoversight.Todoso,theBoardhascreatedthreesupportingcommittees:CreditCommittee,AuditCommitteeandComprehensiveRiskManagementCommittee,whichoperateunderitsdirectionandsupervision.

In2018,feestotalingCOP885millionwerepaidtothemembersoftheBoardofDirectorsfortheirattendancetoBoardandCom-mitteemeetings.AttheGeneralMeetingofShareholdersheldonMarch22,2018,Mr.CarlosIgnacioJaramillowaselectedasaBoardmemberoftheBank.

InformationontheprofessionalbackgroundofthemembersofBancodeBogotá’sBoardofDirectorsisavailableatwww.banco-debogota.com.

Luis Carlos Sarmiento Gutiérrez

CivilEngineerfromtheUniversityofMiamiandMBAwithemphasisonFinancefromJohnsonGraduateSchoolofManagementofCornellUniversity.HehasbeentheCEOofGrupoAvalsince2000andChairmanofBancodeBogotá’sBoardofDirectorssince2004.

Sergio Uribe Arboleda

EconomistfromUniversidaddelosAndes.HehasbeenaprincipalmemberofBancodeBo-gotá’sBoardofDirectorssince1989andwaspreviouslyanalternatemembersince1987.HeisalsoontheBoardofDirectorsofBancodeBogotáS.A.Panama.

Alfonso de la Espriella Ossio

HestudiedLawandPoliticalSciencesatUniversidadLaGranColombia,CurrencyandBank-ingatTulaneUniversity,NewOrleans,andBankingSupervisionattheFederalReserveBank,BatonRouge.HehasbeenaprincipalmemberofBancodeBogotá’sBoardofDirectorssince1988,andAlmaviva’sBoardofDirectorssince1989.

Carlos Arcesio Paz Bautista

BusinessAdministrator fromUniversidadEafitwithaSpecialization inMarketing fromUni-versidadIcesi-Eafit.PrincipalmemberofBancodeBogotá’sBoardofDirectorssince1990.

José Fernando Isaza Delgado

Electrical Engineer fromUniversidadNacionaldeColombiaandMSc inTheoreticalPhysicsfrom the sameuniversity; BSc andMSc inPureMathematics, both from the Louis PasteurUniversityinStrasbourg,France.HehasbeenaprincipalmemberofBancodeBogotá’sBoardofDirectorssince1997.

Principal Members

Chapter 1 • About the Bank Management Report 2018 Chapter 1 • About the Bank Management Report 2018 1716

Senior ManagementThethirdlevelinourCorporateGovernancestructureisSeniorManagement,whichisresponsibleforperformingdaytodayoperationsandbusiness.Itisalsoresponsibleforthedesign,implementationandfollow-upofourobjectivesandstrategies,inaccordancewiththeguidelinessetbytheBoardofDirectors.

AnoverviewoftheprofessionalbackgroundofourSeniorManagementisavailableatwww.bancodebogota.com.

OurCorporateGovernancestructureisdesignedtoachieveourstrategicobjectives,actingwithinaframeworkthatfollowstheprinciplesofethics,equalityandtransparencyatalltimes.Thus,weaimtomakeapositivecontributiontotheprogressofthemarketsinwhichBancodeBogotáanditssubsidiariesareoperating.

ThemaindocumentsthatcontainourgeneralCorporateGovernancepoliciesare:TheCompanyBylaws,theCorporateGov-ernanceCode,theCodeofEthics,andtheRulesofProceduresfortheAuditCommittee,allofwhichcanbefoundatwww.bancodebogota.com.

General Shareholders’Meeting

Senior Management

Board of Directors

PresidenceAlejandro Figueroa

Jaramillo

General SecretaryAlberto Pérez Vélez

Financial ConsumerOmbudsman Statutory Auditing Firm

Credit Committee

Comprehensive RiskManagement Committee

ManagementCommittee

Executive Vice-presidencyJuan María Robledo Uribe

Financial Control andRegulation Vice-presidency

María Luisa Rojas Giraldo

Chief Financial Of�cerJulio Rojas Sarmiento

Legal ManagementJosé Joaquín Díaz Perilla

Credit and TreasuryRisk Management

Carlos Nieto Martínez

CommercialVice-presidency

for Retail BankingFernando Pineda

Otálora

Corporate BankingVice-presidency Rafael Arango

Calle

Sales ChannelsVice-presidencyJulián Sinisterra

Reyes

International and TreasuryVice-presidency

Germán Salazar Castro

National Directorate ofOperations and Process

Graciela Rey Barbosa

Administrative Vice-presidencyIsabel Cristina Martínez Coral

Credit Vice-presidencyCésar Castellanos Pabón

National Directorate of SystemsÓscar Bernal Quintero

Audit Committee General ComptrollerHerbert Dulce Ospina

Control andCompliance Unit

Luis Bernardo QuevedoQuintero

Business Areas Support Areas

Executives

Alejandro Figueroa Jaramillo

CivilEngineerfromUniversidadNacionaldeColombia,MScinEconomicsfromHarvardUni-versityandcandidateforaPhDinEconomicsatthesameuniversity.EmployedatBancodeBogotásince1973.HeservedasExecutiveVicePresidentandChiefFinancialOfficer.HehasbeentheBank’sCEOsince1988.

Juan María Robledo Uribe

EconomistfromtheUniversidaddelRosario.EmployedatBancodeBogotáformorethan50years.HehasservedasVicePresidentofBankingServicesandVicePresidentofCom-mercialBanking.HehasbeenExecutiveVicePresidentfrom1990to1992,1993to2001andsince2003.

Julio Rojas Sarmiento

Hegraduated fromPrincetonUniversityasaBAwith theSummaCumLaudedistinctionandasanMBAwithhonors:GeorgeF.BakerScholar(Top5%ofhisclass)fromHarvardBusi-nessSchool.PastexperienceatGrupoAvalandGoldmanSachs. JoinedBancodeBogotáin2016asChiefStrategy&DigitalOfficer.HehasbeenChiefFinancialOfficersince2018.

María Luisa Rojas Giraldo

EconomistfromUniversidaddelosAndes,withgraduatestudiesinFinancialAdministra-tionatStanfordUniversityandEconomicDevelopmentatBostonUniversity.EmployedatBancodeBogotásince1981.SheservedasChiefFinancialOfficerfrom1995to2018.SinceMarch2018,sheisFinancialControllerandRegulatoryOfficer.

Germán Salazar Castro

EconomistfromUniversidadJaveriana,withgraduatestudiesinBankCreditandFinanceattheChemicalBankandFinanceatNewYorkUniversity.EmployedatBancodeBogotásince1979.Heheld thepositionofVicePresidentofBancodeBogotáTrustCoNewYorkandPresidentoftheFirstBankoftheAmericas.InternationalandTreasuryVicePresidentfrom1992to1996andsince1998.

Chapter 1 • About the Bank Management Report 2018 Chapter 1 • About the Bank Management Report 2018 1918

César Castellanos Pabón

Economist from Universidad Santo Tomás and Systems Administrator from PolitécnicoGrancolombiano.EmployedbyBancodeBogotásince2002.HehasbeenCreditVicePresi-dentsince2012.

Isabel Cristina Martínez Coral

ElectronicandTelecommunicationsEngineering fromUniversidaddelCauca,MBAwithem-phasisonFinancefromUniversidaddelosAndes,MScinTelecommunicationsEconomicsfromUNEDandSpecialistinMobileCommunicationsfromUniversidadDistrital.ShejoinedBancodeBogotáastheTransformationDirectorin2017.SheisAdministrativeVicePresidentsince2018.

Fernando Pineda Otálora

Industrial Engineer fromUniversidad Javeriana andMBA from the School of BusinessandManagement,UniversidaddelaSabana.EmployedatBancodeBogotásince1983.HeservedasSMEandPersonalBankingVicePresident.HeiscurrentlyCommercialVicePresidentforRetailBanking.

Julián Sinisterra Reyes

BusinessAdministratorfromUniversidadIcesi.EmployedatBancodeBogotásince2012asCreditCardsVicePresident.HehasbeenSalesChannelsVicePresidentsince2018.

Rafael Arango Calle

Economist from Universidad Javeriana, with Higher Studies in Strategic Management andLeadership fromUniversidaddeLosAndesand theExecutiveDevelopmentProgramof In-alde. EmployedatBancodeBogotá since1999 in theCreditDivisionand theCommercialarea.HehasbeenCorporateBankingVicePresidentsince2012.

Herbert Francisco Dulce Ospina

IndustrialEngineerfromUniversidadJaverianawithgraduatestudiesinCorporateFinanceatCESAandAdvancedFinancialRiskattheLondon-basedIFF-InternationalFacultyofFinance.HehasbeenGeneralComptrollerofBancodeBogotásince2018.

Alberto Pérez Vélez

LawyerfromUniversidaddelRosario.EmployedatBancodeBogotásince1973.HehasbeenGeneralSecretarysince2007.

José Joaquín Díaz Perilla

LawyerfromUniversidaddelRosario.EmployedatBancodeBogotásince1967.HehasbeenLegalDirectorofthefinancialentitysince1974.

Óscar Bernal Quintero

Systems Engineer fromUniversidadDistrital. Graduate studies in E-BusinessManagementfromUniversidaddeSantanderandMBAfromUniversidaddeLosAndes.EmployedatBancodeBogotásince2008.HeiscurrentlyNationalSystemsDirector.

Carlos Fernando Nieto Martínez

IndustrialEngineerfromUniversidaddeLosAndesandMBAfromInaldeBusinessSchool.EmployedatBancodeBogotásince1998.HehasbeenCreditandTreasuryRiskDirectorsince2009.

Luis Bernardo Quevedo Quintero

LawyerandPhilosopherfromUniversidaddeLosAndes.AtBancodeBogotá,hehasheldthepositionsofRegionalComptrollerandHeadoftheSecurityDepartment.EmployedatBancodeBogotásince1981.HeiscurrentlyDirectoroftheComplianceControlUnit.

Graciela Rey Barbosa

IndustrialEngineerfromtheUniversidadDistrital.SpecialistinFinancefromUniversidadEx-ternado and Specialist inOnline Business fromUniversidadde La Sabana andUniversidadIcesi.EmployedatBancodeBogotásince1995.ShecurrentlyholdsthepositionofNationalOperationsDirector.

Chapter 1 • About the Bank Management Report 2018 Chapter 1 • About the Bank Management Report 2018 2120

Internal AuditThe Bank’s internal audit function is performed through theGeneralComptroller’sOffice,whichprovides an independentassessmentofriskmanagement,controlandgovernancepro-cesses,inaccordancewiththecorporateguidelinesandinstruc-tionsgivenbyGrupoAval,throughrisk-basedaudits.Todoso,wehaveacorporategovernancestructurethatallowsaccesstoallactivitiesandcompaniesthatcompriseit,withnotypeofex-ception;italsocoverstheprimaryoutsourcedservices.

Duringthecourseoftheyear,weconductedon-siteauditvisitstobranchesandcentralareasofhigherrisk,aswellascontinu-ousdistanceassessmentsthereof,basedonpredefinedindica-torsandwarnings,byusingdataanalyticstools.

With regard to the information technologyaudit reviews,wehaveaspecializedteamthatcoversinfrastructure,aswellasap-plications,theirrisksandrelevantbusinessprocesses,includingthosederivedfromnewdigitaltechnologies.

Themain findings of 2018were reported to theAudit Com-mittee,whichmadetherespectiverecommendationsandfol-lowedupontheissuesreported,inordertostrengthenthein-ternalcontrolandriskmanagementsystemsoftheBankanditssubsidiaries,inColombiaandabroad.

Wehavealsobeendevelopingandimplementingstrategiestostandardizestructuresandmethodologies inthesubsidiaries,aswellastoalignourselveswithinternationalauditstandardsandthebestpracticesoftheInstituteofInternalAuditors.

Investor RelationsWearecontinuallyworking to strengthenour relationswithstakeholders.Therefore,wereporttheevolutionandperfor-manceofourbusinessinaclearandtimelymanner,usingthedifferent tools that facilitate interaction with stakeholders,basedontheprincipleoftransparencythatgovernsourCor-porateGovernancestructure.

Wehaveprovidedrelevantinformationinapersonalizedman-nerbythefollowingmeans:

•Conferencecallsonresults:Wereportourresultsonaquar-terlybasis, inordertodisclosetheBank’sfinancialevolutionandprovideanadditionalopportunityforcommunicationbe-tweenexecutives,investors,analystsandstakeholders.

•Website:Ourwebpageprovides linksto informationonInvestor Relations, which serve as a fundamental tool forachievingourobjectives related to transparency in thedis-closureofinformation.

In2018,weheldtwoMeetingsofShareholders,oneordinaryandoneextraordinary,withanaverageattendanceof92%.

AttheOrdinaryGeneralShareholders’MeetingheldonMarch22, 2018,we addressed the items included on the agenda,published in the announcement within the correspondingterms,asfollows:

Review and approval of the 2017Management Report pre-sentedby theBank’sBoardofDirectorsandCEO;presenta-tionoftheInternalControlSystemManagementReport;pre-sentation of the Financial Consumer Ombudsman’s Report;approval of the Unconsolidated and Consolidated Year-endFinancial Statements corresponding to theyear2017,alongwiththeirnotesandotherannexes;presentationoftheStatu-toryAuditor’sopiniononthefinancialstatements;reviewandapprovaloftheEarningsDistributionProject;electionoftheBoardofDirectors;electionoftheStatutoryAuditor;decisiononcompensationfortheBoardofDirectors;decisiononcom-pensation for the Statutory Auditor; additionally, proposalswereapprovedregardingtheappropriationofreserves,dona-tions,BylawsreformandtheBoardofDirectorsAppointmentand Remuneration Policy; in accordance with the agenda,shareholderswerepresentedwiththereformoftheCorporateGovernanceCode,approvedinDecember2017bytheBank’sBoardofDirectors.

At the Extraordinary General Meeting of Shareholders heldonAugust 6, 2018, the followingproposalswere approved,inaccordancewiththeagendapublishedinthemeetingan-nouncement:

1.WaiverofBancodeBogotá’spreemptivesubscriptionrighton Corficolombiana S.A.’s shares, derived from the publicshareofferingaspertheofferingnoticedatedJuly30/2018,publishedbyCorficolombianaS.A.inElTiemponewspaper.

2.MethodologyfortheproportionaltransferofBancodeBo-gotá’spreemptivesubscriptionrightstotheBank’ssharehold-ers,onCorficolombianaS.A.’ssharesderivedfromthepublicshareofferingaspertheofferingnoticedatedJuly30/2018,publishedbyCorficolombianaS.A.inElTiemponewspaper.

3.ReformofArticle21oftheBank’sBylaws.

4.AppointmentoftheFinancialConsumerOmbudsman,theAlternateFinancialConsumerOmbudsmanandallocationofthebudgetfortheFinancialConsumerOmbudsman.

FortheaforementionedMeetings,allthenecessaryinforma-tionfordecision-makingpurposeswasmadeavailabletoourshareholders, as required by regulations on the right to in-spection and the Bank’s CorporateGovernance documents.Becauseofourcommitmenttotransparentandtimelyinfor-mation disclosure, we have maintained the IR Recognitiongrantedby theColombianSecuritiesExchange (BVC),whichstressestheimplementationofbestpracticesrelatedtoinfor-mationdisclosureandinvestorrelations.

Banco de Bogotá and its Subsidiary Group, direct and indirect share

Note: All shares are ordinary

Affiliates in Colombia

Porvenir36.51%

Fiduciaria Bogotá94.99%

Almaviva94.93%

Megalínea94.90%

Associates and JointVentures

Agencies andSubsidiaries AbroadForeign Affiliates

Corficolombiana32.93%

Casa de Bolsa22.80%

ATH19.99%

Sucursal Panamá

46.91%

95.81%

10.40%0.88%

100% 100%

Direct

Indirect

Direct +Indirect

Aval SolucionesDigitales S.A.

38.90%

LeasingBogotáPanamá

(Panama)100%

Banco deBogotáPanamá100%

Ficentro(Panama)49.77%

BogotáFinance

Corp.(Cayman Islands)

100%

BACCredomatic

Inc.

Banco deBogotá

Nassau Ltd.(Bahamas)

Chapter 1 • About the Bank Management Report 2018 Chapter 1 • About the Bank Management Report 2018 2322

Recommended