Economic Policy Uncertainty and the Yield Curve∗

Markus Leippold† Felix H. A. Matthys‡

October 30, 2015

Abstract

We study the impact of economic policy uncertainty on the term structure of nominal interest

rates. We develop a general equilibrium model, in which the real side of the economy is driven by

government policy uncertainty and the central bank sets money supply endogenously following a

Taylor rule. We analyze the impact of government and monetary policy uncertainty on nominal

yields, short rates, bond risk premia, and the term structure of bond yield volatility. Our affine

yield curve model is able to capture both the shape of the interest rate term structure as well as

the hump-shape of bond yield volatilities. Our empirical analysis shows that higher government

policy uncertainty leads to a decline in yields and an increase in bond yield volatility, whereas

monetary policy uncertainty has no significant contemporaneous effect on yields nor volatilities.

However, it is an important predictor for bond risk premia.

JEL classification: G01, G12, G14, G18

Key Words: Term structure modeling, yield volatility curve, policy uncertainty, bond risk premia

∗This paper benefited greatly from discussions with Yacine Aıt-Sahalia, Caio Almeida, Markus Brunnermeier,Jerome Detemple, Itamar Drechsler, Darell Duffie, Fabio Trojani, Valentin Haddad, Oleg Itskhoki, Jakub Jurek,Philippe Mueller, Jean-Charles Rochet, Christopher Sims, David Srear, Adi Sunderam, Josef Teichmann, and WeiXiong. For helpful comments we would like to thank the seminar participants of the 2015 SAFE Asset PricingWorkshop in Frankfurt, the Finance and Math Seminar ETH and University of Zurich, the 12th Doctorial Workshop inFinance at Gerzensee, the Princeton Student Research Workshop, Financial Mathematics Seminar at ORFE PrincetonUniversity, Bank of England, Central Bank of Mexico, and ITAM. Financial support from the Swiss Finance Institute(SFI), Bank Vontobel, the Swiss National Science Foundation and the National Center of Competence in Research“Financial Valuation and Risk Management” is gratefully acknowledged.†Swiss Finance Institute (SFI) and University of Zurich, Department of Banking and Finance, Plattenstrasse 14,

8032 Zurich, Switzerland; [email protected].‡Princeton University, Bendheim Center For Finance; [email protected].

1 Introduction

Economic policy is driven by government and central banking actions. Governments define fiscal

policy and impose regulations, while central banks manage the money supply and set nominal short

rates. These policies have a fundamental impact on financial markets. However, despite good

intentions their effectiveness remains uncertain at best. In this paper, we explore the impact of such

policy uncertainty on the term structure of interest rates, its corresponding volatility curve, and on

bond risk premia. We develop a general equilibrium model, in which the real side of the economy

is subject to government policy uncertainty and the nominal side of the economy is affected by

monetary policy shocks. Our model setup allows us to derive an approximate analytical solution for

the general equilibrium in the case where the representative agents has CRRA-utility. A key model

device is the assumption of the central bank following a Taylor rule, which links the real with the

nominal side of the economy and turns out to be crucial in reproducing the salient features of the

nominal term structure and its volatility curve.

Our general equilibrium framework builds upon Buraschi & Jiltsov (2005). However, the key

distinction is that for our representative agent we depart from the log-utility assumption and impose

a constant relative risk aversion (CRRA) utility. It is well known that for such a utility specification,

no closed-form solution for the term structure of interest rates can be obtained. Using perturbation

methods, we find that the agents’ optimal controls remain affine in the state variables up to a first

order approximation in the risk aversion coefficient. This result allows us to study the effect of

changing risk aversion on the term structure of interest rates and the yield volatility curve, which

previous papers such as Buraschi & Jiltsov (2005) or Ulrich (2013) were not able to do, and which

turn out to be non-trivial.

In our model, both government and monetary policy uncertainty are affecting nominal yields, the

term structure of volatility, and bond risk premia in a fundamentally different way. An increase in

government policy uncertainty adversely affects the trend component of real output growth. There-

fore, it renders capital investments more risky, which will eventually induce investors to favor safe

assets such as government bonds. Such a flight-to-quality behavior will raise government bond

prices and therefore drives down its yields. This observation is in line with Bloom (2009), who

1

argues that productivity growth falls, because higher uncertainty causes firms to temporarily pause

their investment. Moreover, in our model economy higher government policy uncertainty will not

only negatively affect the long run growth path of production. It also increases its volatility and

therefore leads to a worsening of economic growth prospects, which are fundamental to the agents

consumption-investment allocation problem.1

Not only does government policy uncertainty play an important role in determining the level of

interest rates, but it has also a crucial impact on the level and shape of the term structure of bond

yield volatilities. Although our model belongs to the class of affine models as introduced by Duffie &

Kan (1996), we can replicate the typical hump-shape of the volatility term structure, caused by the

empirical observation that volatility tends to be highest around the two-year maturity bucket. The

key mechanism leading to this result is that government policy uncertainty negatively affects the long

run growth path of productivity, which translates into a hump-shaped curve at a higher volatility

level. With this amplification mechanism we can also explain the ‘excess bond yield volatility puzzle’

that empirical bond yields, especially at the long end of the term structure, cannot be reproduced

by standard affine models of the term structure of interest rates (see Shiller (1979) and Piazzesi &

Schneider (2006)).2

Dealing wit policy uncertainty, a fundamental question that arises in this context is: What is

an appropriate measure for government and monetary policy uncertainty? As starting point, we use

the economic policy uncertainty (EPU) index developed by Baker et al. (2012). According to their

definition, the EPU index contains uncertainty related to both government and monetary policy.

Hence, we aggregate the corresponding EPU constituents into a government (GPU) and a monetary

policy uncertainty (MPU) index.

[Figure 1 about here]

1Our model is similar in style to the long run risk model of Bansal & Yaron (2004). However, the key distinctivedifference is that the long run growth component and the market price of output risk are both driven by the sameunderlying risk factor, namely government policy uncertainty. Furthermore, our setting can also be compared to theliterature on real business cycle analysis. For instance, shocks to trend growth exhibit fundamentally different effectson the (real) economy as opposed to transitory fluctuations. The agents or county’s reaction to temporary shocks is toborrow in the short run to smooth out consumption. However, if the shock is more persistent, the long run consumptionlevel has to be adjusted as borrowing for an infinite time horizon is not longer possible.

2A possible solution to this problem is to introduce heterogeneous agents who have different prior beliefs about somefundamental economic variable, such as for instance inflation as in Xiong & Yan (2010) or to introduce time-varyingrisk preference as in Buraschi & Jiltsov (2007), which are however analytically less tractable.

2

In Figure 1 we plot the relationship between U.S. treasury bond yields and volatilities together

with the EPU, GPU, and MPU index for the period of 1995 to 2014. The first two prominent spikes

of the EPU index are related to the terrorist attacks on the World Trade Center and the 2nd Gulf

War. By the end of 2003 and until the outbreak of the financial crisis in 2008, the US economy

entered a steady economic growth phase. Both, the EPU and GPU show similar patterns. They

declined in the pre-crisis period and started to peak at the onset of the financial crisis. The EPU

and GPU index remain at a high level ever since, exhibiting highly volatile behavior. In contrast, the

MPU index slowly reversed to its pre-crisis level. We attribute this observation to the fact that the

EPU and GPU index captures political uncertainty, which was especially high during the debt-ceiling

crisis of 2011 and lasted until late 2013 where some governmental authorities were even forced to

suspend their services temporarily.

Figure 1 also shows that both the EPU and GPU index exhibit a countercyclical pattern with

nominal yields. When the EPU or GPU index is high, yields tend to go down. This apparent negative

relationship is also confirmed by computing the sample correlation coefficient, which ranges from -

0.544 (EPU, 1 year) to -0.32 (GPU, 10 years) for the period January 1990 until June 2014.3 These

numbers suggest that higher economic or government policy uncertainty leads to lower treasury bond

yields. Thus, as political risk increases, investors seek safer assets and therefore start to shift from

stocks to (government) bonds, which is in line with the predictions in Pastor & Veronesi (2013).4

The discussion above suggests that government and monetary policy uncertainty may have dif-

ferent effects on yields and volatilities. Therefore, we not only split economic uncertainty into these

two different components, but we allow government policy uncertainty to play a role for interest rate

policy. The empirical analysis of the model confirms our theoretical prediction in that government

policy uncertainty is the main driver in contemporaneous movements in the term structure of interest

rates and its volatility curve.

3The time series correlation between the EPU and GPU (MPU) is 0.857 (0.657) and 0.572 between the GPU andMPU index. As can be inferred from Figure 1, the monetary policy uncertainty index appears to have no link withcontemporaneous movements in nominal yields. Indeed, the estimated time series correlation is roughly zero along theentire term structure. We collect the all empirical sample correlation of treasury bond yields and the EPU, GPU andMPU indexes in Table 6 as well as realized volatility and EPU, GPU and MPU indexes in Table 7 in Appendix B.Furthermore, the sample correlation between the EPU and the VIX index is 0.44 for the same period.

4Using also the EPU index of Baker et al. (2012), they show that political uncertainty raises not only the equityrisk premium but also the volatilities and correlations of stock returns.

3

There is increasing evidence that policy uncertainty leads to direct reactions of the central bank

authority (see for instance David & Veronesi (2014)). To motivate a link between government policy

uncertainty and yields for our model design, we estimate pairwise Vector Auto Regressions (VAR)

for the GPU and MPU with the three-month T-bill rate, which we take as proxy for monetary policy.

[Figure 2 about here]

Figure 2 reports the resulting impulse responses for the time period from January 1995 to June

2014. Panel A reveals that a shock to the GPU index leads to a sustained negative impact on the

short-term rate and hence on future monetary policy. This impact remains highly significant up to

a time horizon of more than 20 months. In contrast, from Panel B we observe that a shock to the

short-term rate has no significant impact on the GPU index.5 This suggests that government policy

uncertainty shocks drives monetary policy actions, but not the other way around. Hence, the central

bank conducts its monetary policy taking into account uncertainty shocks from the real side whereas

the central banks interest rate policy does not seem to affect fiscal uncertainty.

We provide a theoretical explanation for the empirical results above. In our model economy,

higher real uncertainty lowers productivity growth, which feeds into the monetary policy through

our assumption that the central bank controls the money supply growth following a Taylor rule.

Hence, the monetary authority’s efforts to stabilize growth (and inflation) causes it to react to real

uncertainty by lowering the cost of capital. Moreover, since we assume money neutrality, nominal

shocks do not have an impact on the real side of the economy. However, the converse is not true.

The equilibrium price level growth is driven by the capital accumulation growth, which implies that

the nominal side is also driven by shocks from the real side, namely government policy shocks.

Through these two transmission channels, inflation and capital accumulation growth targeting, the

money supply growth becomes a function of government policy uncertainty. Therefore, by letting

the central bank react endogenously to deviations from long run capital growth and inflation targets

establishes an important link between the real and the nominal side of the economy that allows

5Further analyzing the impulse responses from our VAR model, we find that the MPU index has a similar behavioras the GPU index in that it does (negatively) influence monetary policy, but the MPU does not respond to a shock inthe short rate. Furthermore, the response of the short rate from a MPU shock is less pronounced than from a GPUshock. Finally, the MPU and GPU responses to GPU and MPU shocks are negligible and become insignificant afterfour to five months. We do not report these graphs here, but they can be obtained on request.

4

government policy shocks to affect nominal quantities. This link proves to be essential in order to

simultaneously match both the term structure of interest rates and its corresponding volatility curve.

Finally, we allow both monetary and government policy shocks to carry a risk premium. Hence,

our model accommodates a time-varying risk premia in bond returns, which implies that mone-

tary and government policy uncertainty are priced risk factors and the equilibrium inflation process

exhibits heteroskedastic time-variation in both variables.

While our paper belongs to the class of equilibrium finance models of the term structure, it is

specifically related to the following strands of literature.6 Traditional work on asset pricing usually

abstracts from modeling government uncertainty and its impact on asset prices. However, especially

since the European debt crisis starting in 2010 and the 2011 Congress debate about raising the

fiscal debt ceiling in the US, policy uncertainty has recently attracted interest from academia. For

instance, Pastor & Veronesi (2012) and Pastor & Veronesi (2013) develop a general equilibrium

model, in which the profitability of firms is driven by government policy, and discuss the impact of

policy risk on stock prices. Several empirical papers have shown that uncertainty about political

outcomes has a significant effect on asset returns and corporate decisions.7 There is also a large

strand of literature trying to infer political risk from government bond yields such as, e.g., Huang

et al. (2015) who empirically study the relationship between political risk and government bond

yields. For an overview of this literature, we refer to Bekaert et al. (2014).

While the literature on government policy impacts is sparse but growing, the fundamental link

between monetary policy and the term structure of interest rates and volatilities has been studies

6Equilibrium term structure models include, among many others, Wachter (2006), Piazzesi & Schneider (2006),Buraschi & Jiltsov (2007), Gallmeyer et al. (2007), Bekaert et al. (2009), and Bansal & Shaliastovich (2013). Recently,macro-finance term structure models have been critisized for their failure to accomodate for the presence of “unspannedmacroeconomic risk,” see Joslin, Priebsch & Singleton (2014). However, there is support for spanned macro-financeterm structure models. Basically, Bauer & Rudebusch (2015) claim to have resolved the unspanning puzzle. Althoughour model belongs to the spanned model class, we do not delve further into this discussion but refer the interestedreader to the two cited papers above.

7For instance, early studies include Rodrik (1991) or Pindyck & Solimano (1993). They show empirically thatuncertainty about political factors can lead to lower investment expenditures, especially when investment is irreversible.More recently, Durnev (2010) and Julio & Yook (2012) document that firms tend to withhold their investment activityprior to national elections. Gulen & Ion (2012) argue, based on the newly developed policy index by Baker et al.(2012), that policy uncertainty reduces firm and industry level investment and that the magnitude of reduction issubstantial. Boutchkova et al. (2012) take the analysis further and show that some industries are more sensitive topolitical uncertainty than others. Some further related articles analyzing the relationship between political uncertaintyand asset returns include Belo et al. (2013), Bialkowski et al. (2008) or Bond & Goldstein (2012).

5

more extensively. For the yield effects we refer to, e.g., Kuttner (2001), Piazzesi (2005), Fleming

& Piazzesi (2005), Gurkaynak et al. (2005a), and Wright (2012). For the volatility effects see, e.g.,

Balduzzi et al. (2001), Piazzesi (2005) or de Goeij & Marquering (2006), among others. The literature

on the link between monetary policy and bond risk premia is surveyed in Buraschi et al. (2014). In

an empirical study, they find that monetary shocks are indeed an important source of priced risk,

helping to explain the risk premia in bond markets. Using a standard predictability regression of

excess bond returns, they find that monetary policy shocks account for a substantial part of the

variance of bond excess returns, which is in line with our empirical results.

Despite the recent attention brought to modeling the impact of policy uncertainty on asset prices,

the papers mentioned above either address the empirical link between government bond yields and

policy uncertainty or focus on the theoretical impact that a given government policy has on stock

returns. Our paper provides a theoretical framework for studying the impact of both government and

monetary policy uncertainty on the nominal yield curve and its implications for the term structure

of bond yield volatility.

The reminder of the paper is organized as follows. Section 2 presents the model. Section 3

discusses the impact of government as well as monetary policy uncertainty on the term structure of

nominal interest rates, the yield volatility curve and the bond risk premium. Section 4 summarizes

our empirical results and Section 5 concludes.

2 The baseline model economy

Our model economy consists of a real and a monetary sector. For the real sector, we consider a

production economy with a representative agent producing a single good at a constant return-to-

scale production technology. As in Buraschi & Jiltsov (2005), real monetary holdings Mdt provide

a transaction service by reducing the total amount of gross resources required for a given level of

consumption Ct.

Assumption 1 (Preferences of Representative Agent). Let U(Xt) denote expected utility over the

real net consumption holdings X and β > 0 the subjective discount factor. The agent has constant

6

relative risk aversion (CRRA) preferences given by

U(Xt) = Et

[∫ ∞t

e−β(u−t)U(Xu)du

], (1)

with

U(Xt) =

1γ (Xγ

t − 1) , if γ < 1, γ 6= 0,

log(Ct) + ξ log(Mdt

)if γ = 0,

(2)

where γ is equal to one minus the coefficient of risk aversion. In addition, the real net consumption

holdings depend on both consumption Ct and real cash balances Mdt :8

Xt = Ct(Mdt )ξ, 0 ≤ ξ ≤ 1. (3)

The agent’s real output is denoted by Yt. The drift of Yt is influenced by a productivity factor

At that depends on a process gt, which we refer to as government policy or real uncertainty.

Assumption 2 (Real Sector Dynamics). Given a filtered probability space (Ω,F , Ftt≥0,P) satis-

fying the usual conditions, the dynamics of real output Yt, productivity At, and government policy

uncertainty gt have the following dynamics:

dYtYt

= (µY + qAAt)dt+ σY√gtdW

Yt , Y0 ∈ R+, (4)

dAt = (κA(θA −At) + λgt) dt+ σA√gtdW

At , A0 ∈ R, (5)

dgt = κg (θg − gt) dt+ σg√gtdW

gt , g0 ∈ (0,∞), (6)

with constants µY > 0, qA, θA, λ, κi > 0, ∀i ∈ A, g, σ2j > 0, and P-Brownian motions W j

t ,∀j ∈

Y,A, g. The processes in (4) to (6) may have nonzero instantaneous correlation:

dW Yt dW

At = ρAY dt, dW Y

t dWgt = ρY gdt, dWA

t dWgt = ρAgdt. (7)

Productivity At in Equation (5) is a mean reverting process with a trend and diffusion term that

depend on government policy uncertainty gt. Hence, not only is the productivity’s long run mean

stochastic, but also its volatility is time-varying. A crucial role is played by the parameter λ. If

8If ξ = 0, money does not provide any service and ξ = 1 implies that the agent needs to hold exactly one unit ofcurrency for every unit of consumption holdings. Since 0 ≤ ξ ≤ 1, a higher level of monetary holdings provides a higherlevel of transaction services, but at a decreasing return to scale.

7

λ < 0 (λ > 0), an increasing gt will have a negative (positive) effect on long run productivity. If

λ = 0, we obtain a process with constant long run mean θA and time-varying volatility.

The government policy uncertainty process gt in Equation (6) describes an unconditionally mean-

reverting stationary process. It not only affects productivity At, but also the output growth rate

dYt/Yt through two channels. First, gt renders output volatility time-varying which, as we will

prove in a later section, leads to a stochastic real market risk. Second, it affects the trend output

growth rate indirectly as it influences the growth rate of productivity. For example, if λ < 0, higher

government policy uncertainty will reduce the long run level of productivity. Provided that qA > 0,

this reduction leads to a decline in expected output growth. To get some further intuition about our

model design, we derive the unconditional expectation, variance, and covariance of productivity and

government uncertainty below.

Proposition 1 (Stationary moments of productivity and government policy uncertainty process).

The unconditional expectation and variance of productivity At and government policy uncertainty gt,

and their covariance are given by9

E[At] = limT→∞

Et[AT ] = θA +λθgκA

, (8)

V[At] = limT→∞

Vt[AT ] = θg

(σ2A

2κA+

2κgλρAgσAσg + λ2σ2

g

2κAκg(κA + κg)

), (9)

E[gt] = limT→∞

Et[gT ] = θg, V[gt] = limT→∞

Vt[gT ] =θgσ

2g

2κg, (10)

C[At, gt] = limT→∞

Ct[AT , gT ] =θgσg(2κgρ

AgσA + λσg)

2κg(κA + κg). (11)

A first important observation is that the long run level of government policy uncertainty θg affects

all moments. First it raises (lowers) the unconditional expected productivity growth whenever λ > 0

(λ < 0). Second, it not only raises the stationary long run level of gt proportionally, but also the

variance of At and gt. Hence, an increase in θg will lead to higher government policy uncertainty

and simultaneously also to a higher variance of productivity.

Assuming that the impact of government policy uncertainty on the drift of productivity is negative

(λ < 0) and setting ρAg = 0 for simplicity, the effect of λ has three important implications. First,

9By E [·], V [·], and C [·, ·] (Et [·], Vt [·], Ct [·, ·]) we denote the unconditional (conditional on Ft) expectation, variance,and covariance operators.

8

it lowers expected growth of productivity proportionally to θg/κA. Second, it increases volatility of

At linearly. Lastly, it renders C[At, gt] negative, which will be of central importance to capture the

stylized facts of bond yield volatility within our model.

We can now proceed with the formulation of the agent’s capital budget constraint. Without loss

of generality, we use capital depreciation as the only cost component.10

Assumption 3 (Capital budget constraint). The real return on capital that can either be allocated

to consumption Ctdt or cash balances Mdt dt or reinvested dKt is given by

Ctdt+Mdt dt+ dKt = Kt

dYtYt− δKtdt, (12)

where KtdYtYt

is the change in total output and δKtdt is the capital depreciation with deprecation rate

δ ∈ [0, 1].

Substituting output growth from Equation (4), and rearranging we obtain the capital accumula-

tion process as

dKt

Kt= −

(CtKt

+Mdt

Kt

)dt+ (µy + qAAt − δ) dt+ σy

√gtdW

Yt . (13)

The capital accumulation process is decreasing in the optimal control variables consumption Ct and

money demand Mdt , which is intuitive as higher Ct and/or Md

t diminish available resources to be

invested in the production technology Kt. Similar to real output, capital is nonstationary whenever

µy 6= δ and time-varying in productivity At. Furthermore, Equation (13) implies money-neutrality,

i.e., monetary shocks do not have an effect on the real side of the economy.11

10In our model, we do not include a variable cost component as was done, e.g., in Buraschi & Jiltsov (2005).11Whether or not real output and capital are money-shock-neutral is debated in macroeconomics for a long time.

The neo-classical Keynesian literature argues that any increase in money supply has to be offset by an equivalentproportional rise in prices and wages. A recent paper using a similar setup as ours is Ulrich (2013), who sticks tothis neo-classical view. However, there are a number of reasons why inflation may affect the real economy. See, e.g.,Fisher & Modigliani (1978), who argue that inflation has a direct influence on purchasing power, because many privatecontracts are not indexed. A first quantitative study that allows for dependence of the expected return on capital oninflation is Pennacchi (1991), who uses survey data to identify inflationary expectations. Another channel throughwhich inflation can affect the real economy is through taxation of nominal asset returns. This channel was exploitedby Buraschi & Jiltsov (2005) to account for the violation of the expectation hypothesis and the determination ofthe inflation risk premium. Since policy uncertainty affects the real and nominal side of the economy (through theendogenous equilibrium price level), we assume money-neutrality throughout the paper. However, we acknowledge thata feasible extension of our model is to let the capital accumulation process be a function of the price level. We leavethis as an interesting theoretical idea which is worthwhile to be considered.

9

For the monetary sector, we assume that there exists a central bank controlling money supply

MSt on the basis of a Taylor rule. The monetary authority targets a long term nominal constant

money growth rate µM , a capital growth rate k, and an inflation rate equal to π. We assume that

transitory deviations from the optimal long run money growth exhibit stochastic volatility. We can

interpret this time-variation in money supply, denoted by mt, as the monetary policy uncertainty

factor.

Assumption 4 (Monetary Sector). The central bank controls money supply growth according to a

Taylor rule as follows:

dMSt

MSt

= µMdt+ η1

(dKt

Kt− kdt

)+ η2

(dptpt− πdt

)+ σM

√mtdW

Mt , (14)

dmt = κm(θm −mt)dt+ σm√mtdW

mt , dWM

t dWmt = ρMmdt, (15)

where pt and Kt are the price level and capital accumulation process. We assume that the monetary

policy innovation correlates with the money supply by ρMm, but is independent of all other sources

of risk in the economy.

The crucial parameters in Assumption 4 are η1 and η2 in Equation (14). Their magnitude

determines the sensitivity of money supply growth with respect to deviations of endogenous capital

and inflation from their long run target levels. For example, if output growth is above target (dK∗tK∗t−

kdt > 0) and provided that η1 < 0, the monetary authority shrinks the money supply, causing interest

rates to rise and investment activity to slow down. When inflation is below target (dp∗tp∗t− πdt < 0)

and provided that η2 < 0, the central bank’s response is to increase the money supply. In the case

when η1 = η2 = 0 money supply is exogenous and therefore does not react to deviations from long

run capital nor inflation growth rate. Furthermore, given the money supply rule in Equation (14),

monetary policy uncertainty renders money supply time-varying in mt. Having introduced both the

real and monetary side of the economy, we next characterize the representative agent’s equilibrium.

Definition 2 (Equilibrium Capital Stock and Money Holdings). Under Assumptions 1 to 4, the

representative agent’s equilibrium is defined as a vector of optimal consumption, money demand,

price and capital processes [C∗t ,Md∗t ,K∗t , p

∗t ] that is a solution to the following dynamic Hamilton-

10

Jacobi-Bellmann programming problem12

0 =∂V (t,Kt, At, gt)

∂t+ maxCt,Md

t

U(Ct,M

dt ) +AV (t,Kt, At, gt)

, (16)

subject to money market-clearing MSt = p∗tM

d∗t , the bugdet constraint in (12), and the transversality

condition limT→∞ Et[e−βTV (t,Kt, At, gt)

]= 0.

For the problem in Equation (16), an explicit solution can only be obtained for the log-utility

case. The resulting optimal consumption and money demand holdings are proportional to capital Kt.

However, for γ 6= 0, the asymptotic optimal controls Ct and Mdt remain linear in the state variables

Kt, At, and gt (up to a first-order approximation in γ). This feature allows us to find an explicit

affine representation of the term structure of real and nominal interest rates beyond the log-utility

case.13

Proposition 3 (Perturbed equilibrium of the representative agent’s investment and consumption

problem). In equilibrium, the representative agent’s value function is

V (t,Kt, At, gt) =e−βt

βγ

((eφ(At,gt)K1+ξ

t

)γ− 1), (17)

for some function φ(At, gt) of the form

φ(At, gt) = φ0(At, gt) + γφ1(At, gt) +O(γ2). (18)

The agent’s first order asymptotic optimal controls are

C∗t =βKt

1 + ξ[1 + γ (L− φ0(At, gt))] , Md∗

t = ξC∗t , (19)

and the equilibrium first order asymptotic capital accumulation K∗t and price process p∗t satisfy

dK∗tK∗t

= µK∗ (At, gt) dt+ σY√gtdW

Yt , (20)

dp∗tp∗t

=

[µM − η1k − η2π

1− η2+η1 − 1

1− η2µK∗ (At, gt)− gt

(η1 − 1)σ2Y

1− η2

]dt

+σM√mt

1− η2dWM

t +(η1 − 1)σY

√gt

1− η2dW Y

t . (21)

12By A we denote the infinitesimal generator. See, e.g., Øksendal (2003) for technical details.13Our solution strategy is based on the perturbation method. In particular, we follow the approach of Kogan &

Uppal (2001) and approximate our model with respect to the risk aversion parameter around the explicit equilibriumcomputed under the log-utility assumption. Perturbation methods have been successfully applied in many other studiessuch as, e.g., Hansen et al. (2008).

11

where

µK∗(At, gt) := µY + qAAt − β − δ + γβ (φ0(At, gt)− L) (22)

denotes the equilibrium drift of the capital accumulation process and L = log(

β1+ξξξ

(1+ξ)1+ξ

)is a constant.

Furthermore,

φ0(At, gt) = φ00 + φ0AAt + φ0ggt (23)

is an affine function in the state variables (At, gt) with constants φ00, φ0A, φ0g provided in Appendix

A.2.

Since nominal shocks have no real effects, the equilibrium capital accumulation process is only

driven by the real sector of the economy, i.e., by productivity At and by the government policy

uncertainty process gt. Note that for γ = 0 the equilibrium capital drift µK∗ becomes independent

of gt. The weighting factor η2 on inflation-target deviation enters non-linearly into the equilibrium

price process.14

Proposition 3 also implies that the equilibrium price process is driven by both real and monetary

shocks. This result is a consequence of the central bank authority controlling money supply growth

based on a Taylor-rule. Hence, by endogenizing money supply growth, we allow for an important link

between the real and the nominal sector and government policy uncertainty enters the nominal side

of the economy through two different channels, namely though its impact on both the equilibrium

capital accumulation process and inflation. This link will prove to be essential to capture key

empirical properties of the yield curve and its corresponding term structure of yield volatility.

3 The term structure of nominal interest rates

Having obtained the dynamics of the equilibrium price level, we can now solve for the term structure

of nominal and real bond prices. Let B(t, τ) be the nominal pure discount bond paying one unit of

14Note that for η2 ≈ 1, small innovations in either At, gt or mt result in dramatic changes in the equilibrium priceprocess. However, from an economic viewpoint, the parameter η2 should be negative which, as we will see later, isconfirmed by the data.

12

currency in t+ τ periods. The price of the nominal bond must satisfy the following Euler equation

B(t, τ) = e−βτEt

[UC(C∗t+τ ,M

d∗t+τ )

UC(C∗t ,Md∗t )

p∗tp∗t+τ

]= e−βτEt

[exp− log

(K∗t+τ

)

exp− log (K∗t )p∗tp∗t+τ

], (24)

which states that in equilibrium the investor should be indifferent between consuming one more unit

of currency now or investing one unit of currency in the t+ τ period nominal discount bond.

Proposition 4 (Equilibrium Nominal Term Structure of Interest Rates). Under time-separable

CRRA utility as in Equation (2), the nominal discount bond B(t, τ) with maturity τ is given by

B(t, τ) = exp −b0(τ)− bA(τ)At − bg(τ)gt − bm(τ)mt (25)

where

bA(τ) = CA1− e−κAτ

κA, (26)

−b′g(τ) = Z0g(τ) + Z1g(τ)bg(τ) + Z2gb2g(τ) , (27)

bm(τ) =−Z1m +Hm Cot

(12

(−Hmτ − Tan

(2√Z0mZ2mHm

)))2Z2m

, Hm = 4Z0mZ2m − Z21m, (28)

b0(τ) =

∫ τ

0C0(u)du (29)

and the constant parameters Z0m, Z2i, i ∈ g,m and Z0g(τ), Z1g(τ), C0(τ) are time-to-maturity

functions that only depend on the structural model parameters of the economy and are defined in

Appendix A.3.

The nominal term structure of interest rates in Proposition 4 belongs to the general affine class of

term structure models of discount bond prices introduced by Duffie & Kan (1996). Using Equation

(25), we obtain the time t yield curve Y (t, τ) with maturity τ as

Y (t, τ) := −1

τlog (B(t, τ)) =

b0(τ)

τ+bA(τ)

τAt +

bg(τ)

τgt +

bm(τ)

τmt (30)

The affine yield model in Equation (30) is driven by three factors. As noted, e.g., by Litterman &

Scheinkman (1991), such a three factor structure model of the term structure is able to reproduce

most if not all empirically relevant shapes of the yield curve, such as upward sloping, inverted or

hump shapes. The affine property in the factor loadings implies linearity of the local variance as in

Vasicek (1977), Cox et al. (1985), and others.

13

Analyzing the expressions for the constant and time-varying parameters Z·,·, Z0g(τ), and C0(τ)

given in Appendix A.3, we make the following three observations. First, the target growth rates for

output k and inflation π, the depreciation rate δ, and output µY and money supply growth rate µM

solely affect the intercept of the yield curve but not its slope. In contrast, their weighting factors η1

and η2 affect both the intercept and the slope of the yield curve. Moreover, they do so in a non-linear

way.

Second, the parameter λ has a key impact not only on the level of the term structure but also

on its slope. The parameter λ affects the level of yields, since both CA = CA(λ) and Cg = Cg(λ)

enter the expression for b0(τ) and are functions of λ. This dependence in turn implies that λ also

affects the slope of the term structure through bA(τ) and bg(τ). Furthermore, λ also determines the

long run level of productivity At. To see this, recall that the trend growth rate of the productivity

process At is not only dependent on the long run level of productivity θA but also on the long run

level government policy θg.15 Suppose that θg > 0 and λ < 0, and θA +

λθgκA

< 0, the term bA(τ)τ At,

provided that bA(τ) > 0, will be positive with high probability and therefore will lead to a declining

yield curve for any maturity.

Third, the subjective discount factor β and the degree of transaction service money provides ξ

also impact the slope of the yield curve through the factor loadings bA(τ) and bg(τ) whenever γ 6= 0.

Hence, if the representative agent would have log-utility, β and ξ would only exhibit a level effect.

In the following section we explore the impact of government and monetary policy uncertainty on

the nominal term structure of interest rates in more detail.

3.1 Fitting the model to the data

To fit the model to the term structure data we proceed as follows. We estimate a subset of parameters

using maximum likelihood estimation (MLE) and calibrate the remaining parameters to the nominal

yield and its corresponding volatility curve simultaneously. We estimate the parameters of the policy

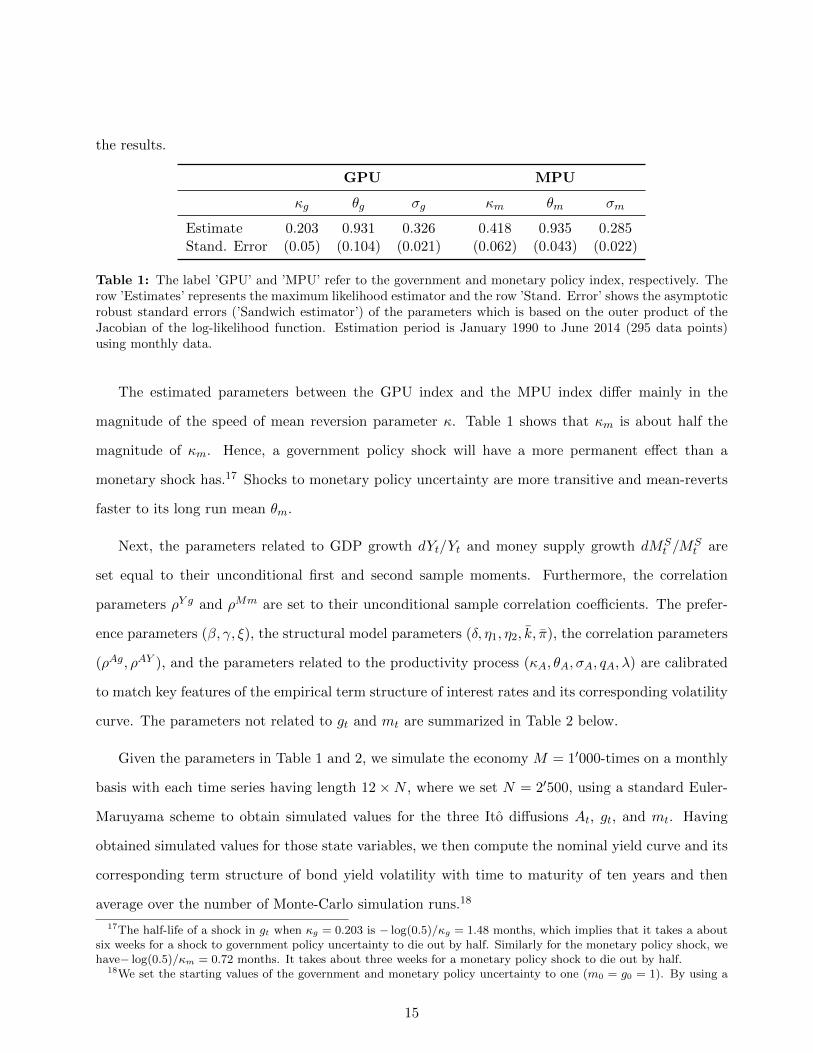

uncertainty variables gt and mt using (exact) maximum likelihood estimation.16 Table 1 summarizes

15In particular, we have E[At] = θA +λθgκA

(see Equation (8) in Proposition 1).16Since for the Feller diffusion the transition density is known in closed-form (non-central chi-squared), the transition

density does not need to be approximated via quasi maximum likelihood techniques.

14

the results.

GPU MPU

κg θg σg κm θm σm

Estimate 0.203 0.931 0.326 0.418 0.935 0.285Stand. Error (0.05) (0.104) (0.021) (0.062) (0.043) (0.022)

Table 1: The label ’GPU’ and ’MPU’ refer to the government and monetary policy index, respectively. Therow ’Estimates’ represents the maximum likelihood estimator and the row ’Stand. Error’ shows the asymptoticrobust standard errors (’Sandwich estimator’) of the parameters which is based on the outer product of theJacobian of the log-likelihood function. Estimation period is January 1990 to June 2014 (295 data points)using monthly data.

The estimated parameters between the GPU index and the MPU index differ mainly in the

magnitude of the speed of mean reversion parameter κ. Table 1 shows that κm is about half the

magnitude of κm. Hence, a government policy shock will have a more permanent effect than a

monetary shock has.17 Shocks to monetary policy uncertainty are more transitive and mean-reverts

faster to its long run mean θm.

Next, the parameters related to GDP growth dYt/Yt and money supply growth dMSt /M

St are

set equal to their unconditional first and second sample moments. Furthermore, the correlation

parameters ρY g and ρMm are set to their unconditional sample correlation coefficients. The prefer-

ence parameters (β, γ, ξ), the structural model parameters (δ, η1, η2, k, π), the correlation parameters

(ρAg, ρAY ), and the parameters related to the productivity process (κA, θA, σA, qA, λ) are calibrated

to match key features of the empirical term structure of interest rates and its corresponding volatility

curve. The parameters not related to gt and mt are summarized in Table 2 below.

Given the parameters in Table 1 and 2, we simulate the economy M = 1′000-times on a monthly

basis with each time series having length 12×N , where we set N = 2′500, using a standard Euler-

Maruyama scheme to obtain simulated values for the three Ito diffusions At, gt, and mt. Having

obtained simulated values for those state variables, we then compute the nominal yield curve and its

corresponding term structure of bond yield volatility with time to maturity of ten years and then

average over the number of Monte-Carlo simulation runs.18

17The half-life of a shock in gt when κg = 0.203 is − log(0.5)/κg = 1.48 months, which implies that it takes a aboutsix weeks for a shock to government policy uncertainty to die out by half. Similarly for the monetary policy shock, wehave− log(0.5)/κm = 0.72 months. It takes about three weeks for a monetary policy shock to die out by half.

18We set the starting values of the government and monetary policy uncertainty to one (m0 = g0 = 1). By using a

15

Model Parameters

β 0.02 qA 0.28 σM 0.45 κA 1.08ξ 0.85 k 0.03 ρAY 0.14 θA 4.19γ -0.82 π 0.03 ρAg -0.98 σA 0.27δ 0.08 µY 0.38 ρgY -0.27 λ -1.93η1 -1.80 σY 0.23 ρMm 0.12 A0 1η2 -2.34 µM 0.26

Table 2: Summary of parameter values selected for Monte-Carlo Analysis: All parameter values for theprocess At as given in Equation (5) and the model parameters β, γ, ξ, qA, δ, η1, η2, k, π, ρAg and ρAY arecalibrated to match simultaneously, the average yield curve and bond volatility curve over the sample periodJanuary 1990 to June 2014. A0 refers to the initial value of At.

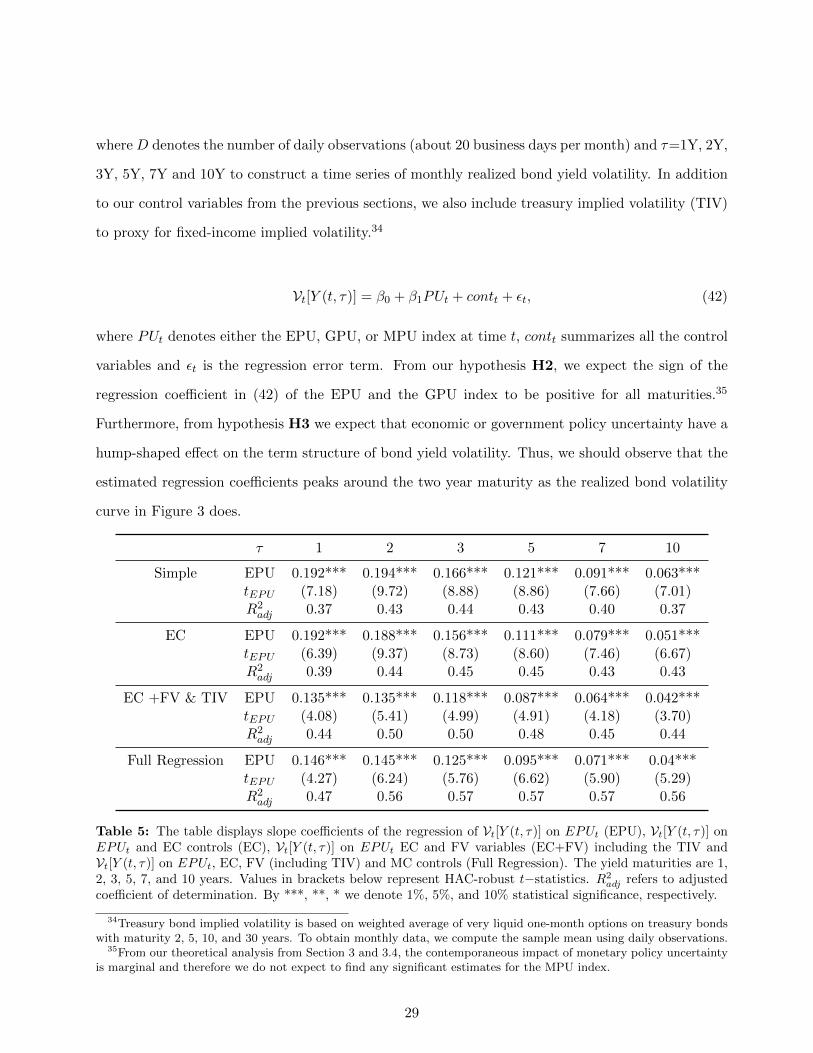

[Figure 3 about here]

From Figure 3, Panel A, we see that the model is overestimating the yield curve at medium

maturities (three to seven years), whereas at the short and at the long end, the model implied yield

curve is underestimating the actual the term structure. However, the overall mean error along the

entire term structure is 3.07%.19 As Panel B of Figure 3 shows, our fitted model is able to reproduce

the hump-shape in the term structure of bond yield volatility. This stylized fact of interest rates

is very challenging to replicate within the framework of affine term structure models. Indeed, even

with their more flexible specification of essentially affine price of risk, Buraschi & Jiltsov (2005)

acknowledge that their model cannot fully match the second moments of yields. In contrast, we

capture the short end of the yield volatility curve very accurately. We slightly overestimate the

actual bond volatility at medium to longer maturities. Nevertheless, the error remains with 4.71%

relatively small.

3.2 Yield curve and policy uncertainty

We now test a series of implications regarding the effect of policy uncertainty on the yield curve

based on our fitted model parameters. Our preliminary empirical analysis between nominal bond

yields and policy uncertainty as measured by the EPU index of Baker et al. (2012) shows that there

long time series, we avoid dependence on starting values.19The error is calculated as 1

T

∑τ∈T |Y (t, τ)− Y (t, τ)|/m where m = 1

T

∑τ∈T Y (t, τ), Y (t, τ) is the fitted yield curve

and T = 6, i.e. the number of maturities.

16

is significant negative correlation between economic policy uncertainty and movements in the yield

curve. Splitting the index into government and monetary policy uncertainty shows that the GPU

index maintains high negative correlation whereas the MPU index seems to have no correlation with

nominal yields at any maturity. Using our affine yield model, we can compute the model-implied

correlation in a straightforward way. More specifically, we can show that a higher level (gt or mt) in

either fiscal or monetary policy uncertainty will lead to a downward shift in yields.

Proposition 5 (Model-implied correlation and impact of policy uncertainty on the yield curve). 1.

Nominal yields are negatively correlated with either fiscal (gt) or monetary (mt) policy uncer-

tainty, i.e.

% [Y (t, τ), gt] ≤ 0, % [Y (t, τ),mt] ≤ 0, ∀τ ≥ 0

and the effect is stronger for fiscal as opposed to monetary policy uncertainty, in other words

|% [Y (t, τ), gt] | > |% [Y (t, τ),mt] |

2. Nominal yields yields are decreasing in both fiscal (gt) and monetary (mt) policy uncertainty

∂Y (t, τ)

∂gt=bg(τ)

τ< 0,

∂Y (t, τ)

∂mt=bm(τ)

τ< 0, ∀τ ≥ 0. (31)

and this effect is again stronger for fiscal as opposed to monetary policy uncertainty, i.e.,∣∣∣∣bg(τ)

τ

∣∣∣∣ > ∣∣∣∣bm(τ)

τ

∣∣∣∣ , ∀τ ≥ 0. (32)

The results in Proposition 5 above are in line with the empirical observations. The reason why the

model implied correlation is negative for any maturity can be directly deduced from the covariance

between Y (t, τ) and gt which is,

C[Y (t, τ), gt] =bA(τ)

τ

θgσg(2κgλρ

AgσA + λσg)

2κg(κA + κg)+bg(τ)

τ

θgσ2g

2κg. (33)

Given the fitted parameters in Table 1 and 2, the factor loading bA(τ) is always positive whereas

bg(τ) is negative, which implies that the first and second term in Equation (33) will be negative.

In this setting, we obtain a model-implied average (along maturity τ) correlation of -0.2934 which

is comparable to the empirical sample correlation between nominal yields and the GPU (-0.40).

Likewise, since bm(τ) ≤ 0 we obtain C(Y (t, τ),mt) = θmσ2m

2κm

bm(τ)τ ≤ 0, ∀τ ≥ 0. Comparing this model

17

correlation coefficient of -0.021 to its empirical counterpart (-0.011), we see that the model is able

to match both sample correlation coefficients.

3.3 Equilibrium nominal short rate and bond excess returns

We now discuss how the short end of the term structure of interest rates and the bond risk premium

are affected by government and monetary policy uncertainty.

Proposition 6 (Equilibrium nominal short rate and bond risk premium). With time-separable

CRRA utility, we have the following first order asymptotic results:

1. The nominal short rate Rt is given by

Rt =(µY − β − δ − k)η1 + β + µM − η2(µY + π − δ)

1− η2+ γ

β(η1 − η2)(L− φ00)

1− η2−

σ2M

(η2 − 1)2mt

− (qA + γβφ0A)

(η1 − η2

η2 − 1

)At −

((η1 − η2)2σ2

Y

(η2 − 1)2+ γ

βφ0g(η1 − η2)

η2 − 1

)gt (34)

2. The nominal price of fiscal risk λN,gt as well as the market price of monetary risk λN,mt are

λN,gt =η2 − η1

η2 − 1σY√gt, λN,mt =

σMη2 − 1

√mt. (35)

3. The bond risk premia RP (t, τ) per unit of time is given by

RP (t, τ) :=1

dtEt[dB(t, τ)

B(t, τ)−Rtdt

]= λN,Yt

[bA(τ)ρAY σA + bg(τ)ρgY σg

]√gt + λN,Mt bm(τ)ρMmσm

√mt (36)

= ΛN,gt + ΛN,mt (37)

where ΛN,gt = λN,Yt

[bA(τ)ρAY σA + bg(τ)ρgY σg

]√gt and ΛN,mt = λN,Mt bm(τ)ρMmσm

√mt are

the factor loadings of government and monetary policy uncertainty, respectively.

The nominal short rate and the nominal market price of risk are all influenced by both the real

and nominal sector of the economy, which is a direct consequence of the Taylor rule in Assumption

4. In the special case when money supply is entirely decoupled from the real sector (η1 = η2 = 0),

the nominal short rate reduces to Rt = µM + β − σ2Mmt and λN,Yt = 0 so that the real side does

18

not affect the nominal short rate and output risk is no longer a nominal risk factor. We get the

same result when η1 = η2 = η, i.e., when the central bank reacts to deviations from its nominal

and real targets equally. Then, the nominal short rate is also an affine function of mt and the risk

premium does not depend on gt. In both cases, the nominal short rate becomes independent of the

risk aversion parameter γ.

In the general case, Rt depends on the money supply control variables η1 and η2 in a non-linear

way. This suggests that relatively small fluctuations in either productivity At, monetary or govern-

ment policy uncertainty may lead to drastic movements in the nominal short rate. Furthermore, risk

aversion affects Rt through different channels. First, it affects its level through the second term in

Equation (34). If risk aversion increases, i.e., if γ decreases, the short rate becomes smaller since

β(η1−η2)(L−φ00)η2−1 > 0. Secondly, the risk aversion coefficient γ loads on both real sector variables At

and gt. Therefore, risk aversion also impacts the slope and curvature of the term structure. To

what extent risk aversion changes slope and curvature depends on the magnitude of the estimated

parameter values.

When η1 6= 0 and η2 6= 0, the nominal price of risk decomposes into two state-dependent market

prices of risks λN,Yt and λN,Mt , which are driven by government and monetary policy risk, respec-

tively.20 Furthermore, the sign of those market prices of risk is determined by η1 and η2, the

parameters controlling the intensity of adjustments to the long run real output growth target k and

inflation target π and therefore can become negative depending on the values of η1 and η2.

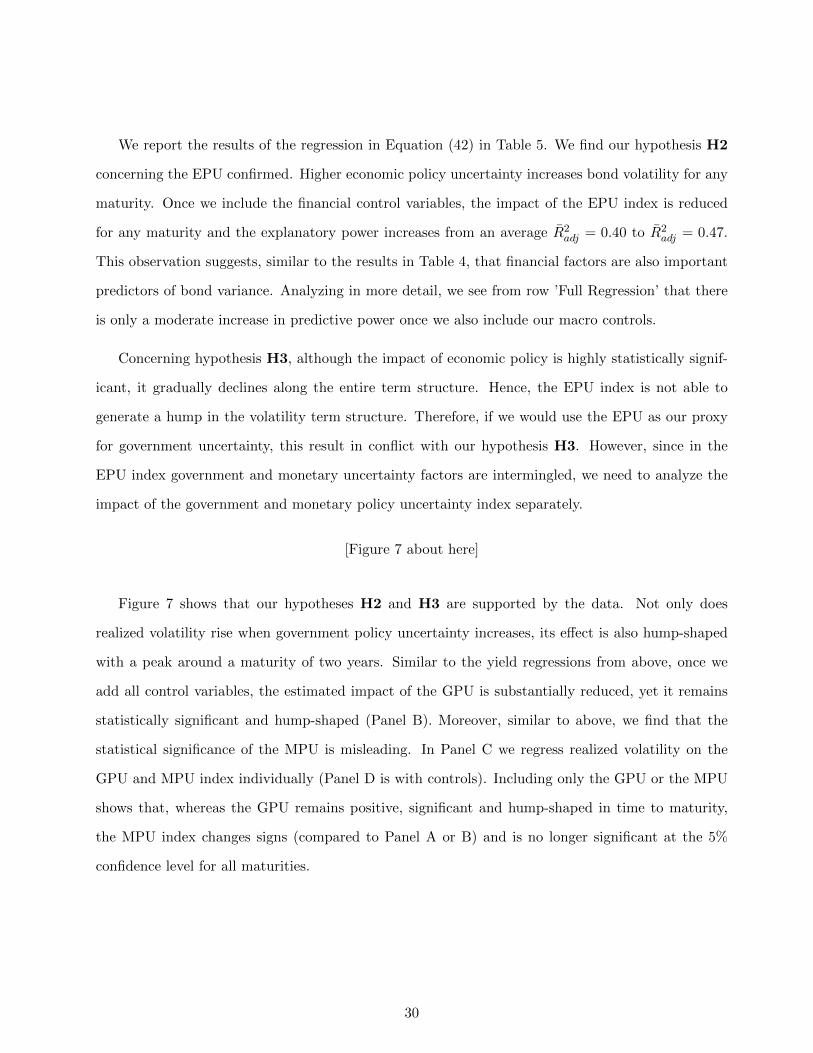

[Figure 4 about here]

For the bond risk premium in Equation (37), we plot in Figure 4, Panel A, the loadings of the

government policy uncertainty factor gt and the monetary policy uncertainty factor mt. Under our

estimated parameters, both government and monetary policy uncertainty load positively on the risk

premium. Monetary policy uncertainty has a larger impact at the short end of the curve, but flattens

out at longer maturities and eventually becomes dominated by government policy uncertainty. Hence,

20The results in Proposition 6 reveal that equilibrium relations such as the expected bond excess premium andinterest rate volatility as well as the forward term premium, i.e., violation of the expectation hypothesis, will be drivenby government and monetary policy uncertainty whenever η1 6= 0 and η2 6= 0.

19

our model predicts that the dominant factor at the short end is monetary policy uncertainty, while

the dominant role at the long end of the bond risk premia curve is played by the government policy

uncertainty factor.

3.4 Bond yield volatility

Many empirical studies find that long run bond yields exhibit higher volatility than implied by

the expectation hypothesis. Already Shiller (1979) shows that long term bond yields exhibit excess

volatility relative to their model-implied values. From Piazzesi & Schneider (2006) we know that their

representative agent-based model explains a smaller fraction of observed volatility of the long-end

yields than of the short-end yields. Xiong & Yan (2010) argue that excess bond volatility might be due

to differences in beliefs about the long run level of inflation. They show that a higher belief dispersion

leads to volatility amplification which allows them to account not only for the empirically observed

high bond yield volatility, but also for the hump-shape of the term structure of bond volatility.21 To

explore the key determinants that allow to reproduce the hump-shape in bond volatility, we need to

derive the model-implied unconditional variance of nominal yields. It turns out that the variance is

a linear combination of the variances of monetary and government policy uncertainty, the variance

of productivity, and the covariance of productivity and government policy uncertainty.

Corollary 1 (Term Structure of Nominal Bond Yield Variance). Let Y (t, τ) denote the current time

t yield with maturity τ . Then the unconditional term structure of bond yield variance is given by

V[Y (t, τ)] =b2A(τ)

τ2V[At] +

b2g(τ)

τ2V[gt] +

b2m(τ)

τ2V[mt] + 2

bA(τ)bg(τ)

τ2C[At, gt] (38)

where V[mt] = θmσ2m

2κmand the expressions for V[At], C[At, gt], and V[gt] are given in Proposition 1.

To explore the key determinants in generating the hump-shape in bond yield variance, Figure 4

plots the different components contributing to the bond yield variance in Equation (38).

[Figure 4 about here]

21Closely related to the ’excess volatility puzzle’ phenomenon are also the findings of Gurkaynak et al. (2005b). Theydocument that bond yields exhibit excess sensitivity to macroeconomic announcements.

20

The contribution of both the factor loadings bg(τ) and the cross term bA(τ)bg(τ) are hump shaped,

which causes the term structure of yield variance to exhibit a similar pattern. The government policy

factor gt exhibits a hump shape that peaks around the two year maturity. The covariance term

C(At, gt) is also contributing significantly to the hump. Its magnitude is determined by two factors,

by the correlation between government policy uncertainty and productivity (ρAg < 0) and by the

impact of government policy uncertainty on productivity (λ < 0). The impact of the production

variance V[At] as well as of monetary policy uncertainty is monotonically decreasing in τ . The latter

factor has only little impact. From Corollary 1 and Figure 4 we can deduce the following:

Proposition 7 (Policy Uncertainty and the term structure of bond yield volatility).

Government gt and monetary mt policy uncertainty raise the level of bond yield volatility.

However, the effect is much stronger for fiscal as opposed to monetary policy uncertainty, i.e.

b2g(τ)

τ2V[gt] >

b2g(τ)

τ2V[mt] (39)

The function F g(τ) =b2g(τ)

τ2V[gt] is hump-shaped across maturities. This implies that the effect

of government policy uncertainty is highest for about 2 years maturity according to Figure 4.

The first result in Proposition 7 is straight-forward. Since clearlyb2g(τ)

τ2V[gt] > 0,

(b2m(τ)τ2

V[mt] > 0)

and C(At, gt) > 0 adding the government (monetary) policy uncertainty factor raises the level of

volatility. The second statement above is far less obvious to see, as it crucially depends on the

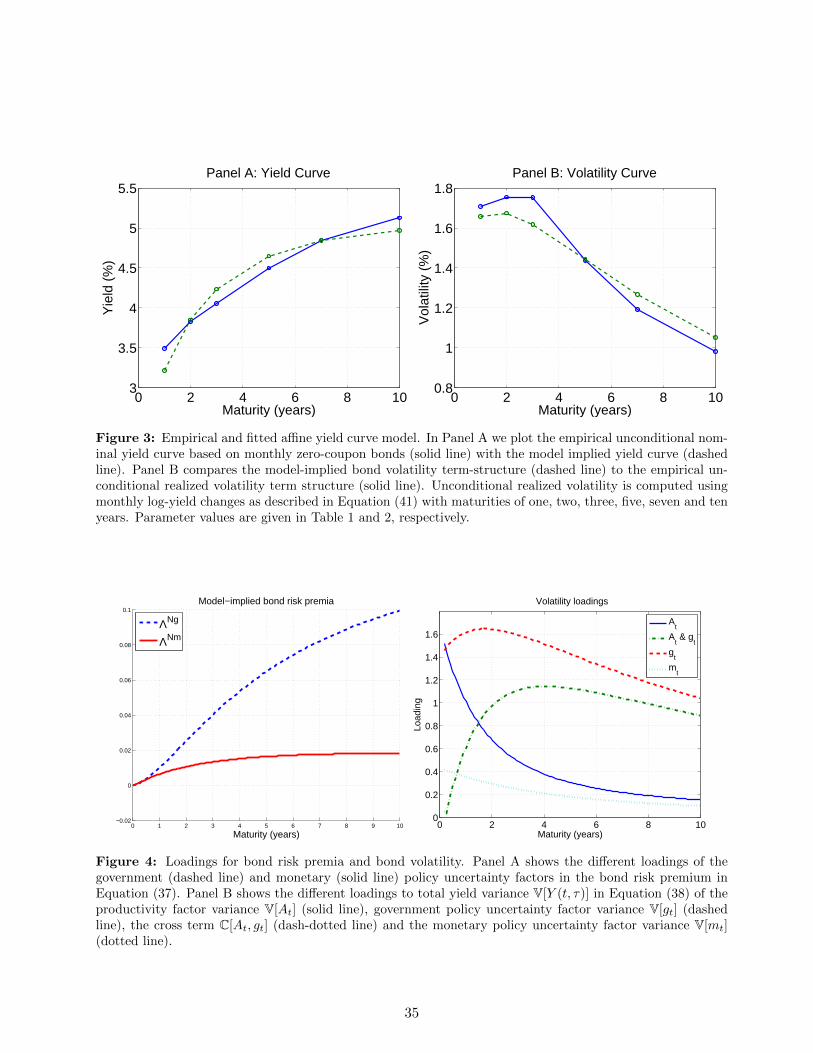

parameter specifications of the model. Therefore, in Panels A through F of Figure 5, we explore in

more detail the parameters responsible for generating the hump shape.

[Figure 5 about here]

As Panel A illustrates, the term structure of bond yield volatility exhibits a fundamentally dif-

ferent shape whenever λ is negative or when λ is set to zero, in which case government policy

uncertainty does not affect the drift of productivity. Not only is the level of the term structure

significantly higher whenever λ < 0 than compared to the case when λ = 0 but also, bond yield

volatility becomes hump-shaped in time to maturity. Panels B and C show that the speed of mean

21

reversion level κg and volatility σg have a similar effect on bond volatility. A more persistent and a

highly volatile uncertainty process generate not only to an upward shift of the bond volatility term

structure, but also a hump shape.22 Similar to Panel B, we observe in Panel D that a more perma-

nent shock in productivity (decrease in κA) also accentuates the hump shape. In contrast, increasing

production volatility σA shifts the volatility term structure upward such that it eventually becomes

monotonically decreasing (Panel E). This follows because the factorb2A(τ)

τ2V(At) increases proportion-

ally in σ2A and since

b2A(τ)

τ2is monotonically decreasing. Finally, Panel F shows that bond volatility

is highly sensitive to changes in either η1 or η2. When the central bank becomes less responsive

to deviations of the long term real target k, the level of bond volatility decreases substantially. In

contrast, if the central bank becomes less responsive to deviations of the long term nominal target

π, bond volatility increases significantly.23

4 Empirical analysis

Our theoretical model gives rise to several theoretical predictions. In the subsequent empirical

analysis, we examine the following four testable hypotheses.

Hypothesis 1 (H1): Our first prediction can be deduced directly from Proposition 5, which

implies that nominal yields fall when either government or monetary policy uncertainty increases

and vice versa. From Proposition 5, this effect is mainly driven by government policy uncertainty

(see Equation (31)).

Hypothesis 2 (H2): Higher (lower) fiscal or monetary policy uncertainty increases (decreases)

nominal yield volatility (see Equation (39) in Proposition 7). This effect is again mainly driven by

government policy uncertainty.

22The long run mean of government policy uncertainty θg increases yield dispersion proportionally, since ∂V(Y (t,τ)∂θg

> 0.

Hence, the long term mean does not contribute to a hump shape.23Without providing the corresponding plots, we remark that whenever both η1 and η2 are both reduced, there will

be a parallel downward shift in the level of bond yield volatility. Furthermore, the impact of risk aversion on the termstructure of bond volatilities is less pronounced and leads to an almost parallel downward shift of the term structure.

22

Hypothesis 3 (H3): From the second result in Proposition 7, the hump shape of the term structure

of bond yield volatility is mainly driven by government policy uncertainty and not by monetary policy

uncertainty.

Hypothesis 4 (H4): From Equation (37), bond risk premia are affected by both monetary and

government policy uncertainty.

To investigate the joint effect of government and monetary policy uncertainty on the yield curve,

its term structure of volatility, and on risk premia, we use as a proxy for both types of policy

uncertainties, the economic policy uncertainty (EPU) index developed by Baker et al. (2012). Thus,

in our model this index would be approximately equivalent to setting EPUt ≈ gt + mt. In what

follows, we will empirically test the above hypotheses by regressing nominal yields and yield volatility

on the EPU index and our time series of government and monetary policy as well as a set of control

variables.

4.1 Data

We obtain monthly Treasury Bill yields with maturity one, two, three, five, seven, and ten years from

the Federal Reserve Board ranging from January 1990 until July 2014, from which we bootstrap the

zero-coupon yield curve treating the treasury yields as par yields. From Datastream, we collect

monthly data on a total of 2 macro variables, which we aggregate into a real business cycle activity

factor and an inflation factor.24 As a measure for real activity we use industrial production (IP). As

an inflation factor, we use the consumer price index (CPI). We then compute monthly log-growth

rates over one year for each of the macro control variables.

As an alternative to the EPU, we proxy for (policy) uncertainty using the VIX index. As a

measure for economic condition we include the Chicago Fed National Activity Index (CFNAI), which

we obtain from the FRED database (St. Louis Fed).25 We also use treasury bond implied volatility

24Similar control variables have also been used by Ang & Piazzesi (2003), Evans & Marshall (2007), Ludvigson &Ng (2009) or Joslin, Priebisch & Singleton (2014) in their study of the economic determinants of the term structure ofnominal interest rates.

25The reason why we include the CFNAI regressor is to test whether either monetary or government policy uncertaintyhas predictive power after controlling for the state the economy is in. This is because it is reasonable to assume thatuncertainty about the government’s future policy choice is in general larger in weaker economic conditions.

23

(TIV) based on weighted average of one-month options on treasury bonds with maturity of two, five,

ten, and 30 years as a proxy for bond market volatility.

In addition we collect two time series, which we refer to as Financial Variables’ (FV). They

include the monthly log growth rate of the S&P composite dividend yield index (DY), which has

been shown to have forecasting power by Fama & French (1989), and the term spread measured as

the ten-year yield less the federal funds rate (TS).

4.2 Construction of government and monetary policy uncertainty index

The economic policy uncertainty (EPU) index developed by Baker et al. (2012) has been recently used

by a number of studies.26 The EPU index is constructed from three main components, namely a news

impact part which is based on news paper discussing economic policy uncertainty, a component that

summarizes reports by the Congressional Budget Office (CBO) that compile lists of temporary federal

tax code provisions, and a third component called ‘economic forecaster disagreement’, which draws

on the Federal Reserve Bank of Philadelphia’s Survey of Professional Forecasters and summarizes

data on consumer price forecast dispersion and predictions for purchases of goods and services by

state, local and federal government.27

For our setting, we need to decompose the EPU index into uncertainty related to government

and monetary policy. To disentangle the two types of uncertainties, we use the ‘categorical EPU

data’, which contains time-series on uncertainty related to government and monetary policy as well

as further categorical variables.28 For our measure of government policy uncertainty, we extract the

time-series ‘fiscal policy’, ‘taxes’, and ‘government spending’. Furthermore, we argue that disagree-

ment about temporary federal tax code provisions and forecast variation in local state and federal

purchases of goods and services are sources of government policy uncertainty, whereas disagreement

26For instance, Pastor & Veronesi (2013) show that government policy uncertainty carries a risk premium, and thatstocks are more volatile and more correlated in times of high uncertainty. Brogaard & Detzel (2012) use the sameindex and find that economic policy uncertainty forecast future market excess returns. Similarly, Gulen & Ion (2012)show that policy-related uncertainty is negatively correlated with firm and industry level investment. When policyuncertainty increases firm’s tend to reduce their investment.

27As Kelly et al. (2013) argue, it is difficult isolate exogenous variation in political uncertainty as it likely depends onvarious factors such as overall macro uncertainty. Therefore, the EPU index may not only capture government relateduncertainty, but can be interpreted as a broader measure of uncertainty about economic fundamentals.

28This data is also available from http://www.policyuncertainty.com/.

24

about future inflation (CPI disagreement) can be related to monetary uncertainty.

Therefore, in order to construct our index of ‘government policy uncertainty’ labeled as ‘GPU’ we

include the time series ‘fiscal policy’, ’Taxes’, ’Government’, ‘FedStateLocal Ex disagreement’ and

‘Tax expiration’. We place half of the weight to the time series ‘fiscal policy’ and the other half is

equally distributed among the time series ’Taxes’, ’Government’, ’FedStateLocal Ex disagreement’

and ’Tax expiration’.29 Our measure of ‘monetary policy’ uncertainty, which we abbreviate by

‘MPU’, consists of the time series ‘monetary policy uncertainty’ and ‘CPI disagreement’ of which

each obtain weight 1/2.

4.3 Policy uncertainty and the yield curve

To investigate the relationship between the yield curve and the EPU index, we make the following

regression,

Y (t, τ) = β0 + β1PUt + εt, PUt ∈ EPUt, GPUt,MPUt, (40)

where PUt denotes either the EPU, GPU, or MPU index at time t, and εt is the regression error

term.30

According to hypothesis H1, we expect the coefficient in Equation (40) to be negative for all

the three uncertainty indexes. Additionally, we run the same regression as in Equation (40) above,

just replacing the PUt index with the VIX index. Since the VIX index is a generally accepted

measure of overall economic uncertainty and positively correlated with the EPU index,31 we expect

the regression coefficient to be negative as well. We also regress Y (t, τ) on both the VIX and the

EPU index, and on the VIX together with the GPU and MPU indices. By doing so, we can identify

those variables that exhibit greater predictive power.

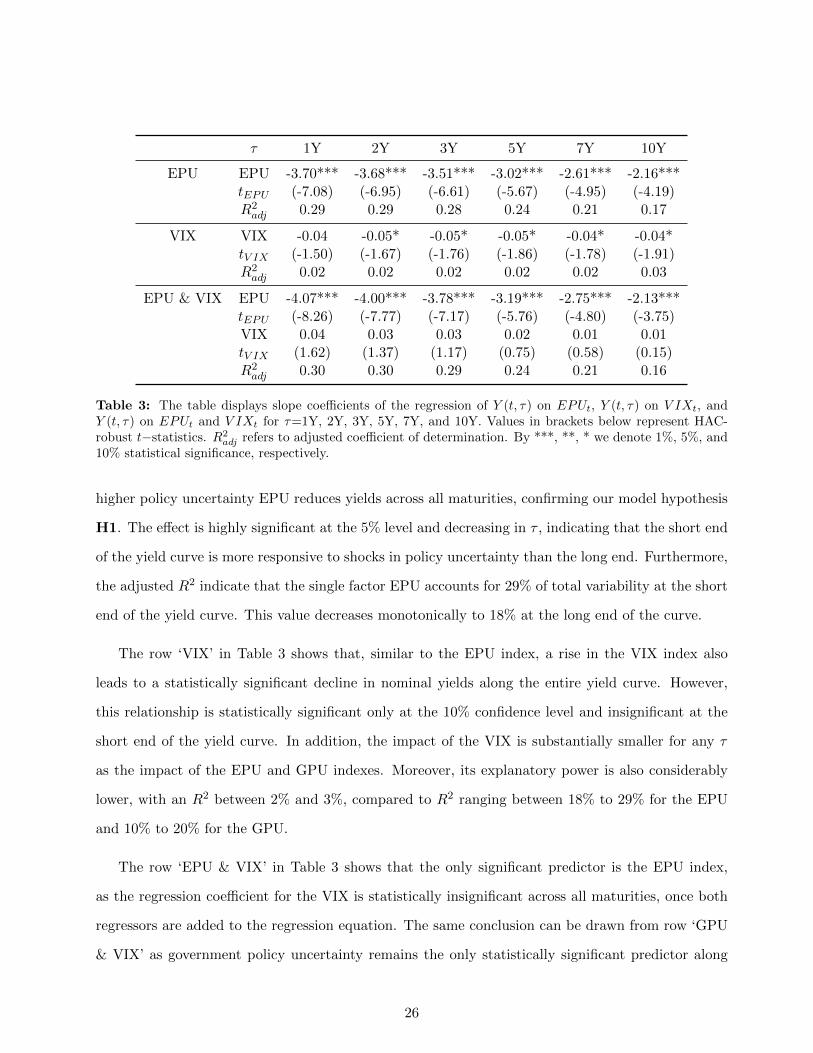

In Table 3 we summarize the results for the EPU index.32 The first row labeled ‘EPU’ shows that

29We divided the time series ‘Tax expiration’ by a factor of ten, because its impact would otherwise pull the index upsubstantially at the end of the time series. Furthermore, as tax laws are only altered infrequently, the ‘Tax expiration’remains constant over several months up to two years. Its unscaled inclusion would lead to an underestimation inpolicy uncertainty variation.

30To address potential concerns about robustness of our results, we compute following Newey & West (1994) standarderrors with five lags to account for heteroskedasticity and autocorrelation (HAC) in residuals.

31For our sample, the correlation coefficient between VIX and EPU is 0.45.32For all the regressions tables that follow the intercept estimate β0 and corresponding HAC errors are not displayed.

25

τ 1Y 2Y 3Y 5Y 7Y 10Y

EPU EPU -3.70*** -3.68*** -3.51*** -3.02*** -2.61*** -2.16***tEPU (-7.08) (-6.95) (-6.61) (-5.67) (-4.95) (-4.19)R2adj 0.29 0.29 0.28 0.24 0.21 0.17

VIX VIX -0.04 -0.05* -0.05* -0.05* -0.04* -0.04*tV IX (-1.50) (-1.67) (-1.76) (-1.86) (-1.78) (-1.91)R2adj 0.02 0.02 0.02 0.02 0.02 0.03

EPU & VIX EPU -4.07*** -4.00*** -3.78*** -3.19*** -2.75*** -2.13***tEPU (-8.26) (-7.77) (-7.17) (-5.76) (-4.80) (-3.75)VIX 0.04 0.03 0.03 0.02 0.01 0.01tV IX (1.62) (1.37) (1.17) (0.75) (0.58) (0.15)R2adj 0.30 0.30 0.29 0.24 0.21 0.16

Table 3: The table displays slope coefficients of the regression of Y (t, τ) on EPUt, Y (t, τ) on V IXt, andY (t, τ) on EPUt and V IXt for τ=1Y, 2Y, 3Y, 5Y, 7Y, and 10Y. Values in brackets below represent HAC-robust t−statistics. R2

adj refers to adjusted coefficient of determination. By ***, **, * we denote 1%, 5%, and10% statistical significance, respectively.

higher policy uncertainty EPU reduces yields across all maturities, confirming our model hypothesis

H1. The effect is highly significant at the 5% level and decreasing in τ , indicating that the short end

of the yield curve is more responsive to shocks in policy uncertainty than the long end. Furthermore,

the adjusted R2 indicate that the single factor EPU accounts for 29% of total variability at the short

end of the yield curve. This value decreases monotonically to 18% at the long end of the curve.

The row ‘VIX’ in Table 3 shows that, similar to the EPU index, a rise in the VIX index also

leads to a statistically significant decline in nominal yields along the entire yield curve. However,

this relationship is statistically significant only at the 10% confidence level and insignificant at the

short end of the yield curve. In addition, the impact of the VIX is substantially smaller for any τ

as the impact of the EPU and GPU indexes. Moreover, its explanatory power is also considerably

lower, with an R2 between 2% and 3%, compared to R2 ranging between 18% to 29% for the EPU

and 10% to 20% for the GPU.

The row ‘EPU & VIX’ in Table 3 shows that the only significant predictor is the EPU index,

as the regression coefficient for the VIX is statistically insignificant across all maturities, once both

regressors are added to the regression equation. The same conclusion can be drawn from row ‘GPU

& VIX’ as government policy uncertainty remains the only statistically significant predictor along

26

the entire term structure. Lastly, row ‘MPU & VIX’ shows that the MPU index has no predictive

power for any τ .

To check for the robustness of our results, we add different controls to the regression equation.

We add the economic condition (EC) controls ‘CFNAI’ and ‘VIX’. Furthermore, we also include the

financial variables (FV) factor and macro controls (MC) as discussed in Section 4.1.

τ 1Y 2Y 3Y 5Y 7Y 10Y

EC EPU -4.14*** -4.05*** -3.83*** -3.24*** -2.78*** -2.17***tEPU (-9.51) (-8.79) (-7.95) (-6.15) (-5.10) (-4.03)R2adj 0.30 0.30 0.28 0.24 0.21 0.16

EC+FV EPU -2.56*** -2.82*** -2.87*** -2.72*** -2.48*** -2.09***tEPU (-4.07) (-4.27) (-4.23) (-3.91) (-3.62) (-3.22)R2adj 0.47 0.40 0.35 0.26 0.22 0.17

EC+FV+MC EPU -2.75** -3.02** -3.07** -2.91** -2.66** -2.28**tEPU (-5.60) (-5.81) (-5.75) (-5.47) (-5.14) (-4.73)R2adj 0.62 0.56 0.52 0.47 0.44 0.42

Table 4: The table reports slope coefficients of the regression, Y (t, τ) on EPUt and EC controls (EC), Y (t, τ)on EPUt and EC, FV variables (EC+FV), Y (t, τ) on EPUt and Y (t, τ) on EPUt, and EC, FV, MC controls(Full Reg.) for τ = 1Y, 2Y, 3Y, 5Y, 7Y and 10Y. Values in brackets below represent HAC-robust t−statistics.R2adj refers to adjusted coefficient of determination. By ***, **, * we denote 1%, 5%, and 10% statistical

significance, respectively.

Table 4 shows that the EPU regression coefficient remains significant for any maturity and across

all regressions. However, compared to Table 3, its impact is considerably reduced (primarily at the

short end), especially when we include the financial variables (FV). The reason for this decline is

because those regressors exhibit strong positive correlation with the EPU index. Not surprisingly,

their estimated impact on contemporaneous yield changes is also negative. Their average is -4.62

(DY), and -0.16 (TS). Whereas the R2adj essentially stays the same after adding the CFNAI control

(row ’EC’), it increases considerably, although mainly at the short-end of the yield curve, after

adding the financial factors (see row ‘EC+FV’). Lastly, as the row labeled ‘EC,FV+MC’ shows, that

whereas adding macro controls to the regression equation does not impact the statistical significance

and magnitude of the EPU index, it considerably increases the amount of explained variation as the

R2adj increases substationally across every maturity.33

33This increase in R2adj is predominantly driven by inflation as it has a statistically significant, very large and positive

27

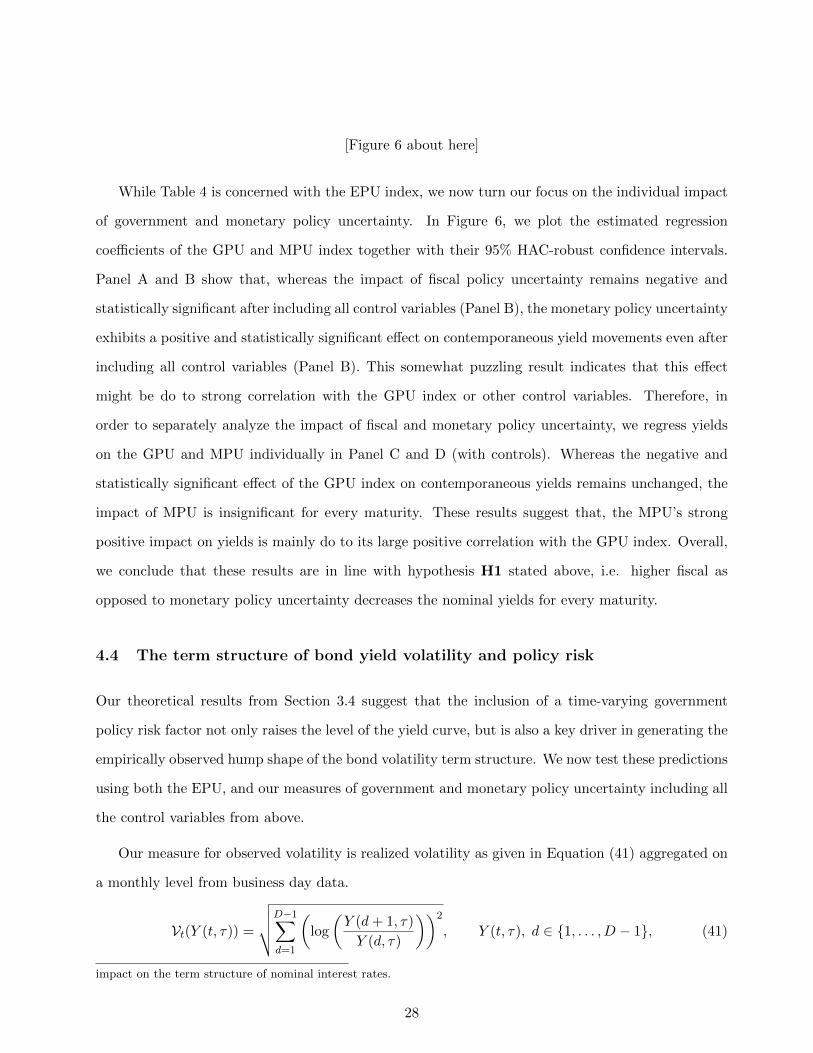

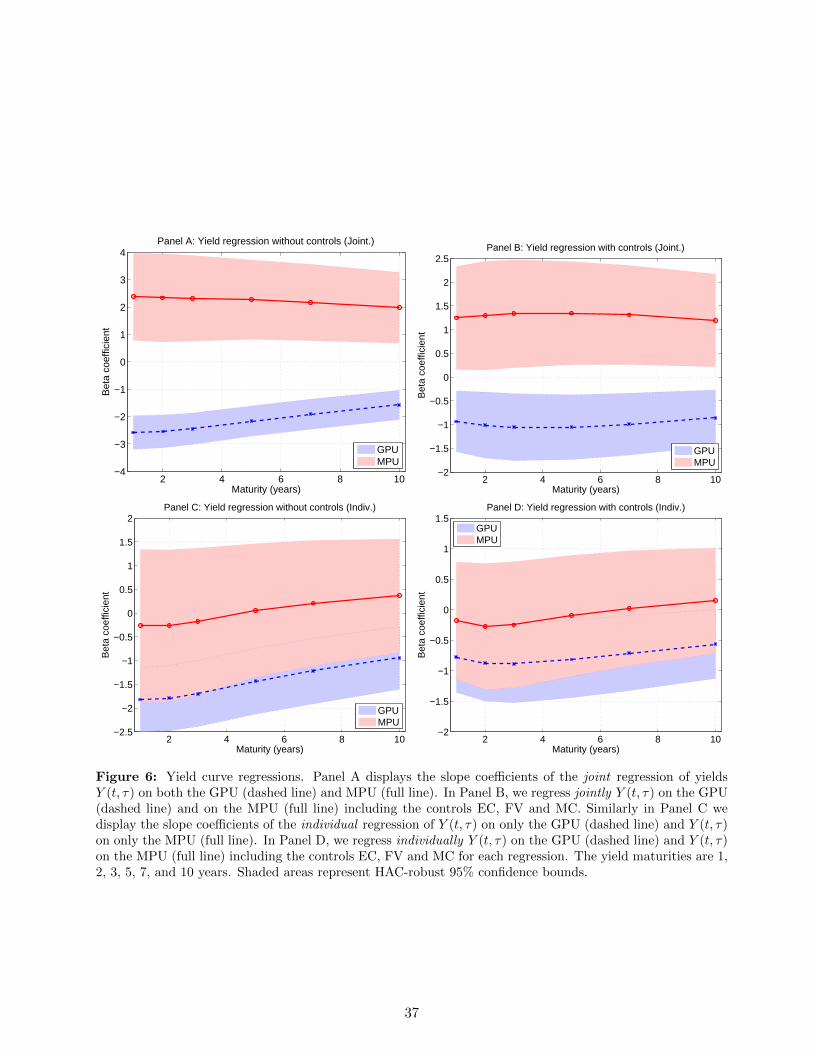

[Figure 6 about here]

While Table 4 is concerned with the EPU index, we now turn our focus on the individual impact

of government and monetary policy uncertainty. In Figure 6, we plot the estimated regression

coefficients of the GPU and MPU index together with their 95% HAC-robust confidence intervals.

Panel A and B show that, whereas the impact of fiscal policy uncertainty remains negative and

statistically significant after including all control variables (Panel B), the monetary policy uncertainty

exhibits a positive and statistically significant effect on contemporaneous yield movements even after

including all control variables (Panel B). This somewhat puzzling result indicates that this effect

might be do to strong correlation with the GPU index or other control variables. Therefore, in

order to separately analyze the impact of fiscal and monetary policy uncertainty, we regress yields

on the GPU and MPU individually in Panel C and D (with controls). Whereas the negative and

statistically significant effect of the GPU index on contemporaneous yields remains unchanged, the

impact of MPU is insignificant for every maturity. These results suggest that, the MPU’s strong

positive impact on yields is mainly do to its large positive correlation with the GPU index. Overall,

we conclude that these results are in line with hypothesis H1 stated above, i.e. higher fiscal as

opposed to monetary policy uncertainty decreases the nominal yields for every maturity.

4.4 The term structure of bond yield volatility and policy risk

Our theoretical results from Section 3.4 suggest that the inclusion of a time-varying government

policy risk factor not only raises the level of the yield curve, but is also a key driver in generating the

empirically observed hump shape of the bond volatility term structure. We now test these predictions

using both the EPU, and our measures of government and monetary policy uncertainty including all

the control variables from above.

Our measure for observed volatility is realized volatility as given in Equation (41) aggregated on

a monthly level from business day data.

Vt(Y (t, τ)) =

√√√√D−1∑d=1

(log

(Y (d+ 1, τ)

Y (d, τ)

))2

, Y (t, τ), d ∈ 1, . . . , D − 1, (41)

impact on the term structure of nominal interest rates.

28

where D denotes the number of daily observations (about 20 business days per month) and τ=1Y, 2Y,

3Y, 5Y, 7Y and 10Y to construct a time series of monthly realized bond yield volatility. In addition

to our control variables from the previous sections, we also include treasury implied volatility (TIV)

to proxy for fixed-income implied volatility.34

Vt[Y (t, τ)] = β0 + β1PUt + contt + εt, (42)

where PUt denotes either the EPU, GPU, or MPU index at time t, contt summarizes all the control

variables and εt is the regression error term. From our hypothesis H2, we expect the sign of the

regression coefficient in (42) of the EPU and the GPU index to be positive for all maturities.35

Furthermore, from hypothesis H3 we expect that economic or government policy uncertainty have a

hump-shaped effect on the term structure of bond yield volatility. Thus, we should observe that the

estimated regression coefficients peaks around the two year maturity as the realized bond volatility

curve in Figure 3 does.

τ 1 2 3 5 7 10

Simple EPU 0.192*** 0.194*** 0.166*** 0.121*** 0.091*** 0.063***tEPU (7.18) (9.72) (8.88) (8.86) (7.66) (7.01)R2adj 0.37 0.43 0.44 0.43 0.40 0.37

EC EPU 0.192*** 0.188*** 0.156*** 0.111*** 0.079*** 0.051***tEPU (6.39) (9.37) (8.73) (8.60) (7.46) (6.67)R2adj 0.39 0.44 0.45 0.45 0.43 0.43

EC +FV & TIV EPU 0.135*** 0.135*** 0.118*** 0.087*** 0.064*** 0.042***tEPU (4.08) (5.41) (4.99) (4.91) (4.18) (3.70)R2adj 0.44 0.50 0.50 0.48 0.45 0.44

Full Regression EPU 0.146*** 0.145*** 0.125*** 0.095*** 0.071*** 0.04***tEPU (4.27) (6.24) (5.76) (6.62) (5.90) (5.29)R2adj 0.47 0.56 0.57 0.57 0.57 0.56

Table 5: The table displays slope coefficients of the regression of Vt[Y (t, τ)] on EPUt (EPU), Vt[Y (t, τ)] onEPUt and EC controls (EC), Vt[Y (t, τ)] on EPUt EC and FV variables (EC+FV) including the TIV andVt[Y (t, τ)] on EPUt, EC, FV (including TIV) and MC controls (Full Regression). The yield maturities are 1,2, 3, 5, 7, and 10 years. Values in brackets below represent HAC-robust t−statistics. R2

adj refers to adjustedcoefficient of determination. By ***, **, * we denote 1%, 5%, and 10% statistical significance, respectively.

34Treasury bond implied volatility is based on weighted average of very liquid one-month options on treasury bondswith maturity 2, 5, 10, and 30 years. To obtain monthly data, we compute the sample mean using daily observations.

35From our theoretical analysis from Section 3 and 3.4, the contemporaneous impact of monetary policy uncertaintyis marginal and therefore we do not expect to find any significant estimates for the MPU index.

29

We report the results of the regression in Equation (42) in Table 5. We find our hypothesis H2

concerning the EPU confirmed. Higher economic policy uncertainty increases bond volatility for any

maturity. Once we include the financial control variables, the impact of the EPU index is reduced

for any maturity and the explanatory power increases from an average R2adj = 0.40 to R2

adj = 0.47.

This observation suggests, similar to the results in Table 4, that financial factors are also important

predictors of bond variance. Analyzing in more detail, we see from row ’Full Regression’ that there

is only a moderate increase in predictive power once we also include our macro controls.

Concerning hypothesis H3, although the impact of economic policy is highly statistically signif-

icant, it gradually declines along the entire term structure. Hence, the EPU index is not able to

generate a hump in the volatility term structure. Therefore, if we would use the EPU as our proxy

for government uncertainty, this result in conflict with our hypothesis H3. However, since in the

EPU index government and monetary uncertainty factors are intermingled, we need to analyze the

impact of the government and monetary policy uncertainty index separately.

[Figure 7 about here]

Figure 7 shows that our hypotheses H2 and H3 are supported by the data. Not only does

realized volatility rise when government policy uncertainty increases, its effect is also hump-shaped