DrakeDRAKE UNIVERSITY

UNIVERSITED’AUVERGNE

Recent Changes in The United States Financial Services

Industry

UNIVERSITED’AUVERGNE

DrakeDrake University

Introduction

Thank you for inviting me to visit your universityTom Root

PhD Economics University of [email protected]

Drake UniversityDes Moines, IowaApproximately 4,000 students

UNIVERSITED’AUVERGNE

DrakeDrake University

Outline

Recent changes in U. S. Financial MarketsOverview of the role of the Financial Services Industry in an EconomyRegulatory Changes, Recent Trends, and Current Events

Financial Services Modernization ActSecuritization and Role of Government Sponsored Enterprises.Recent Scandals

Mutual FundsCorporate Governance

UNIVERSITED’AUVERGNE

DrakeDrake University

Trends in the Market

Market Broadening InstrumentsIncrease liquidity of the market attracts new investors and provides opportunities for borrowers. Securitization

Risk Management InstrumentsReallocate financial risks to those willing and able to accept them.

Arbitraging Instruments Allow investors and borrowers to take advantage of differences between markets

UNIVERSITED’AUVERGNE

DrakeDrake University

Regulation

Given the important roles played by the Financial Services Industry in the economy, it is highly regulated.

UNIVERSITED’AUVERGNE

DrakeDrake University

Justification of Regulation of FI’s

Safety and Soundness RegulationMonetary Policy RegulationPromotion of “Fair” CompetitionCredit Allocation RegulationConsumer Protection RegulationInvestor Protection RegulationEntry Regulation

UNIVERSITED’AUVERGNE

DrakeDrake University

Regulatory Overview

1933 Glass-Steagall Act: Separates securities and banking activitiesProhibited commercial banks from most underwriting of securities. Fear of conflict of interestEstablished Federal Deposit Insurance CorporationNational banks allowed to branch state wide if state chartered banks were allowed to do so.

UNIVERSITED’AUVERGNE

DrakeDrake University

1999 Financial ServicesModernization Act

Allowed banks, insurance companies, and securities firms to enter each others’ business areasStreamlined regulation of Bank Holding CompaniesProhibited FDIC assistance to affiliates and subsidiaries of banks and savings institutionsProvided for national treatment of foreign banksFederal Crime to steal account information

UNIVERSITED’AUVERGNE

DrakeDrake University

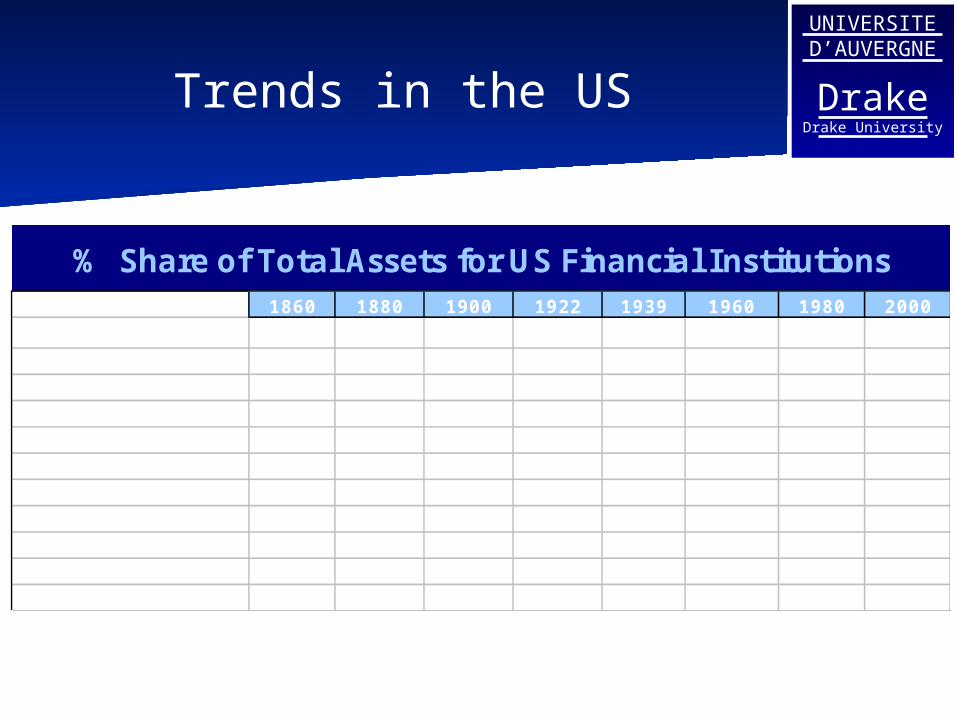

Trends in the US

1860 1880 1900 1922 1939 1960 1980 2000

Commercail Banks 71.4% 60.6% 62.9% 63.3% 51.2% 38.2% 34.8% 35.6%Thrift Institutions 17.8% 22.8% 18.2% 13.9% 13.6% 19.7% 21.4% 10.0%Insurance Companies 10.7% 13.9% 13.8% 16.7% 27.2% 23.8% 16.1% 16.8%investment co's 0.0% 1.9% 2.9% 3.6% 17.0%Pension Funds 0.0% 0.0% 2.1% 9.7% 17.4% 10.7%Finance Co's 0.0% 0.0% 0.0% 2.0% 4.6% 5.1% 7.9%Securities Brokers 0.0% 0.0% 3.8% 5.3% 1.5% 1.1% 1.1% 1.5%Mortgage Co's 0.0% 2.7% 1.3% 0.8% 0.3% 0.0% 0.4% 0.3%Real Estate Ivest. Trusts 0.0% 0.1% 0.2%Total 99.9% 100.0% 100.0% 100.0% 99.8% 100.0% 100.0% 100.0%Total Trillion dollars 0.00 0.01 0.02 0.08 0.13 0.60 4.03 14.75

% Share of Total Assets for US Financial Institutions

UNIVERSITED’AUVERGNE

DrakeDrake University

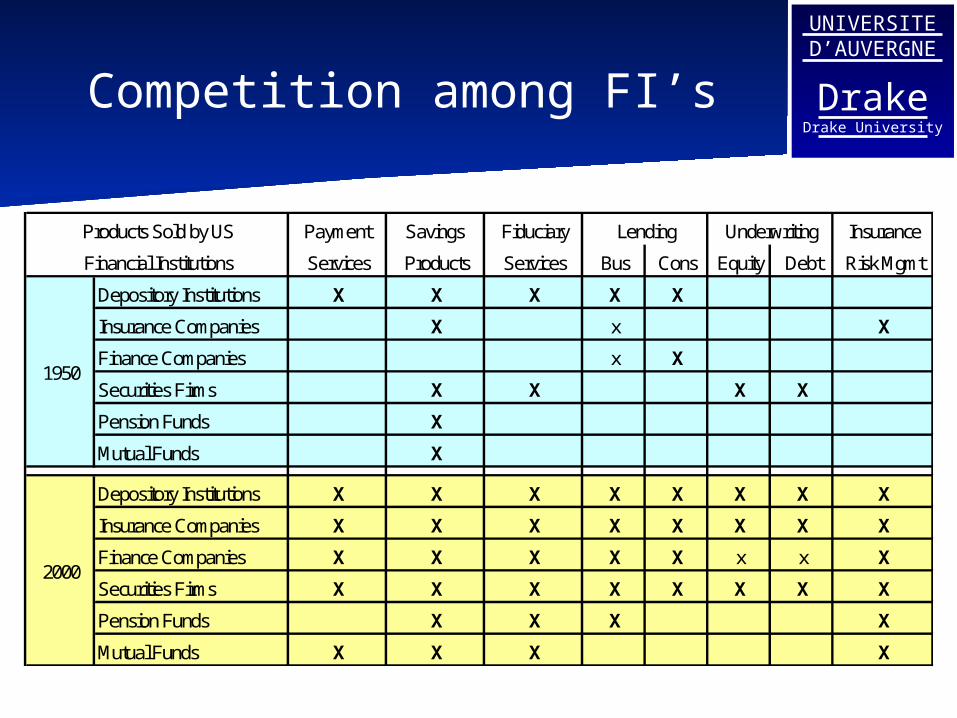

Competition among FI’s

Payment Savings Fiduciary Insurance

Services Products Services Bus Cons Equity Debt Risk Mgmt

Depository Institutions X X X X X

Insurance Companies X x X

Finance Companies x X

Securities Firms X X X X

Pension Funds X

Mutual Funds X

Depository Institutions X X X X X X X X

Insurance Companies X X X X X X X X

Finance Companies X X X X X x x X

Securities Firms X X X X X X X X

Pension Funds X X X X

Mutual Funds X X X X

UnderwritingLending

1950

2000

Products Sold by US

Financial Institutions

UNIVERSITED’AUVERGNE

DrakeDrake University

Impact on US Market

Increased merger and acquisition activity in financial services industry.Demutualization of insurance firms and savings and loans

UNIVERSITED’AUVERGNE

DrakeDrake University

Asset Securitization

Securitization is the pooling and repackaging of loans so they have the characteristics of security instruments which enable them to be more easily resold. Creates both Maturity Intermediation and Denomination Intermediation while spreading credit riskShould broaden the market and decrease risk

UNIVERSITED’AUVERGNE

DrakeDrake University

Use of Securitization in the Mortgage Market

The market that has been impacted the most by increased securitization is the secondary market for mortgages.The largest participants in this market are government sponsored enterprises (GSE).

UNIVERSITED’AUVERGNE

DrakeDrake University

Government Sponsored Enterprises

Privately owned, government sponsored entities.Created to lower the cost of capital for a specific sectorGenerally issue two types of notes and debt

UNIVERSITED’AUVERGNE

DrakeDrake University

Special Treatment of GSE’s

Debt and mortgage backed securities are exempt from SEC registrationAgencies are exempt from state and local taxesTreasury can purchase up to $2.2 B of FNMA and $4B of FHLB debt via line of creditBanks can make unlimited investment in debt issued by GSE’sGSE securities are eligible as collateral for public deposits and for loans from the Federal Reserve

UNIVERSITED’AUVERGNE

DrakeDrake University

GSE’s and Mission

Federal National Mortgage Association (Fannie Mae) & Federal Home Loan Mortgage Association (Freddie Mac) promote secondary market for mortgagesGovernment National Mortgage Association (Ginnie Mae) – promote secondary market for government sponsored mortgagesFederal Home Loan Bank – Liquidity in banking system

UNIVERSITED’AUVERGNE

DrakeDrake University

GSE’s and Mission

Student Loan Marketing Association (Sallie Mae) – promote a secondary market for student loansFederal Farm Credit Bank – promote a secondary market for lending in agricultural industry

UNIVERSITED’AUVERGNE

DrakeDrake University

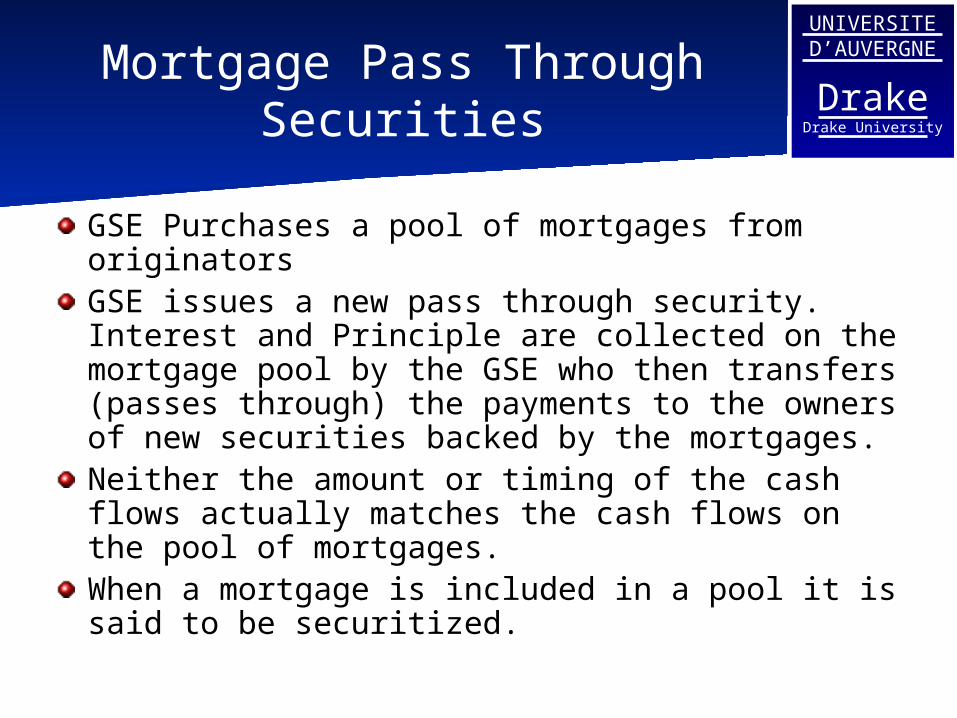

Mortgage Pass Through Securities

GSE Purchases a pool of mortgages from originatorsGSE issues a new pass through security. Interest and Principle are collected on the mortgage pool by the GSE who then transfers (passes through) the payments to the owners of new securities backed by the mortgages. Neither the amount or timing of the cash flows actually matches the cash flows on the pool of mortgages.When a mortgage is included in a pool it is said to be securitized.

UNIVERSITED’AUVERGNE

DrakeDrake University

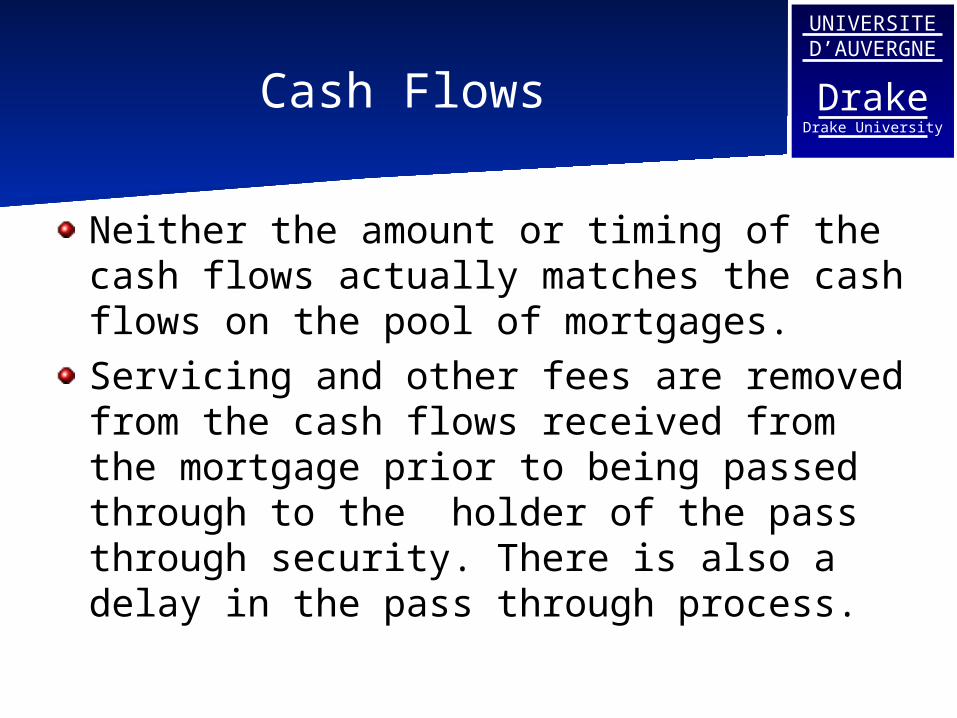

Cash Flows

Neither the amount or timing of the cash flows actually matches the cash flows on the pool of mortgages.Servicing and other fees are removed from the cash flows received from the mortgage prior to being passed through to the holder of the pass through security. There is also a delay in the pass through process.

UNIVERSITED’AUVERGNE

DrakeDrake University

Terminology

The pool of mortgages will have a variety of different rates and maturities. Therefore, the description of the pass through is based upon weighted averages of the coupon and maturity.

UNIVERSITED’AUVERGNE

DrakeDrake University

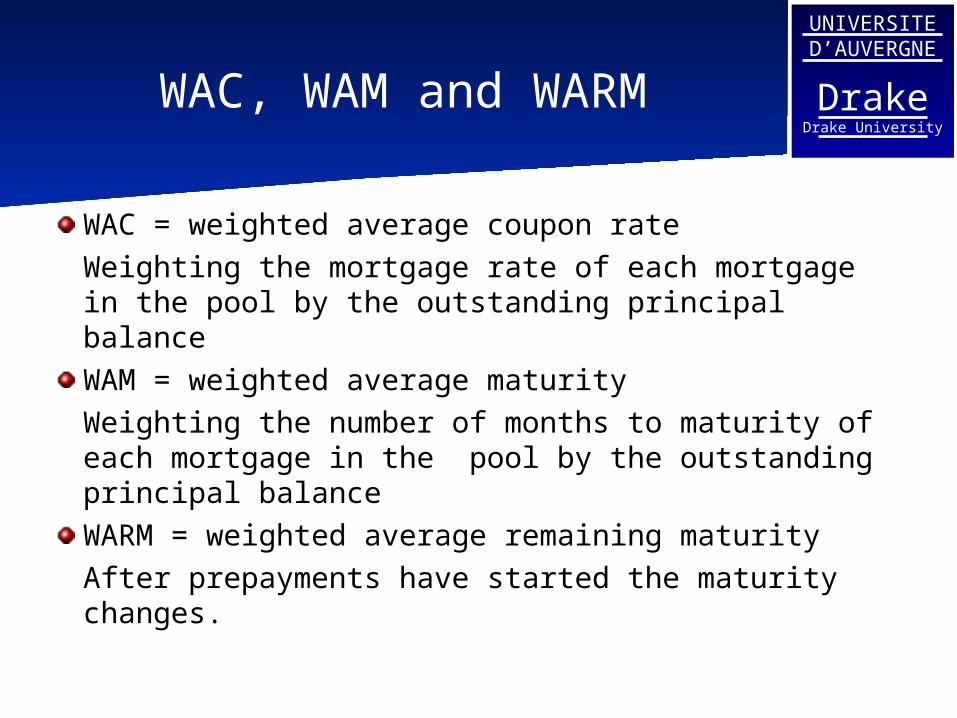

WAC, WAM and WARM

WAC = weighted average coupon rateWeighting the mortgage rate of each mortgage in the pool by the outstanding principal balanceWAM = weighted average maturityWeighting the number of months to maturity of each mortgage in the pool by the outstanding principal balanceWARM = weighted average remaining maturityAfter prepayments have started the maturity changes.

UNIVERSITED’AUVERGNE

DrakeDrake University

Guarantee Types

Fully Modified Pass Throughs: Guarantees that the principal and interest will be paid regardless of whether the borrower is late.

Modified Pass Through: Guarantees the timely payment of interest, the principal is passed through when it is received.

UNIVERSITED’AUVERGNE

DrakeDrake University

Possible Benefits of Securitization

Benefits to IssuersDiversification – Broadens funding sourceAbility to manage capital requirementsProvides Fee IncomeManage interest rate volatility

Benefits to investorsIncreased LiquidityReduced Credit Risk

Benefits to BorrowersReduced spreads

UNIVERSITED’AUVERGNE

DrakeDrake University

Composition of US Debt Market Sept 2003 (Total value $22.6

Trillion)

Mortgage Related $5.129TCorporate

$4.347T

Federal Agency $2.636T

Money Market, $2.526T

Asset Backed $1.68T

Muni 1.883T

Treasury $3.446T

Bond Market Association 2003 is as of Sept 30,2003

UNIVERSITED’AUVERGNE

DrakeDrake University

% of Outstanding Debt Market

0%

20%

40%

60%

80%

100%

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Municipal Treasury Corporate* FedAgencies MoneyMarket Mortgage-Related Asset-Backed

8.1%

23.6

%

7.8%

Bond Market Association 2003 as of Sept 30,2003

UNIVERSITED’AUVERGNE

DrakeDrake University

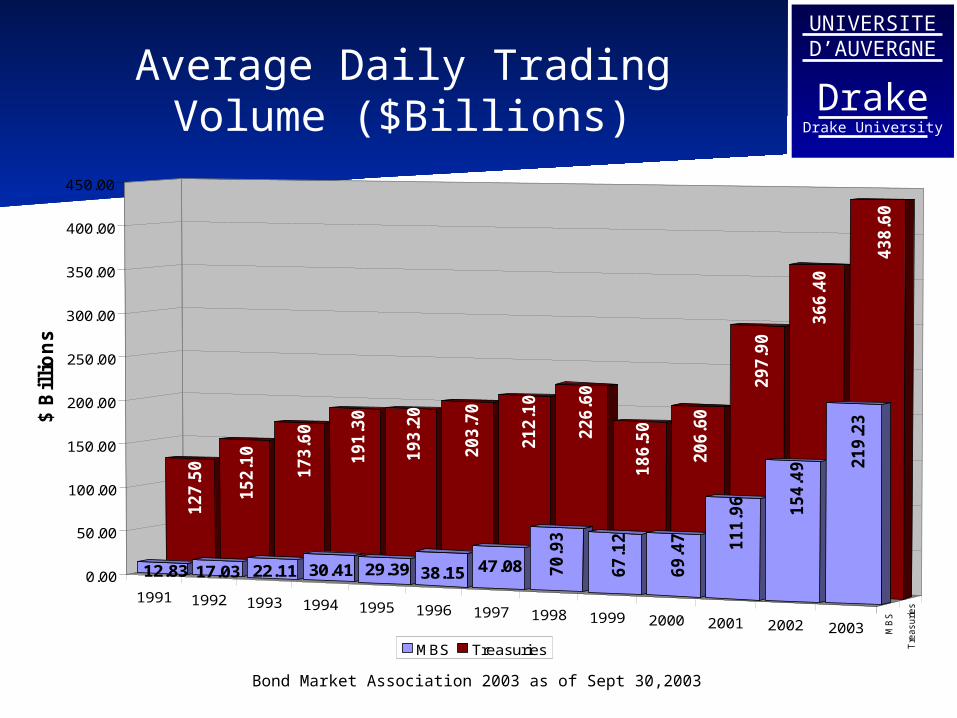

Average Daily Trading Volume ($Billions)

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 MB

S

Tre

asuries

127.5

0

152.1

0

173.6

0

191.3

0

193.2

0

203.7

0

212.1

0

226.6

0

186.5

0

206.6

0

297.9

0

366.4

0

438.6

0

12.83 17.03 22.11 30.41 29.39 38.15 47.08 70.9

3

67.1

2

69.4

7 111.9

6

154.4

9 219.2

3

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

400.00

450.00

$ B

illi

on

s

MBS Treasuries

Bond Market Associattion 2003 as of Sept 30, 2003

UNIVERSITED’AUVERGNE

DrakeDrake University

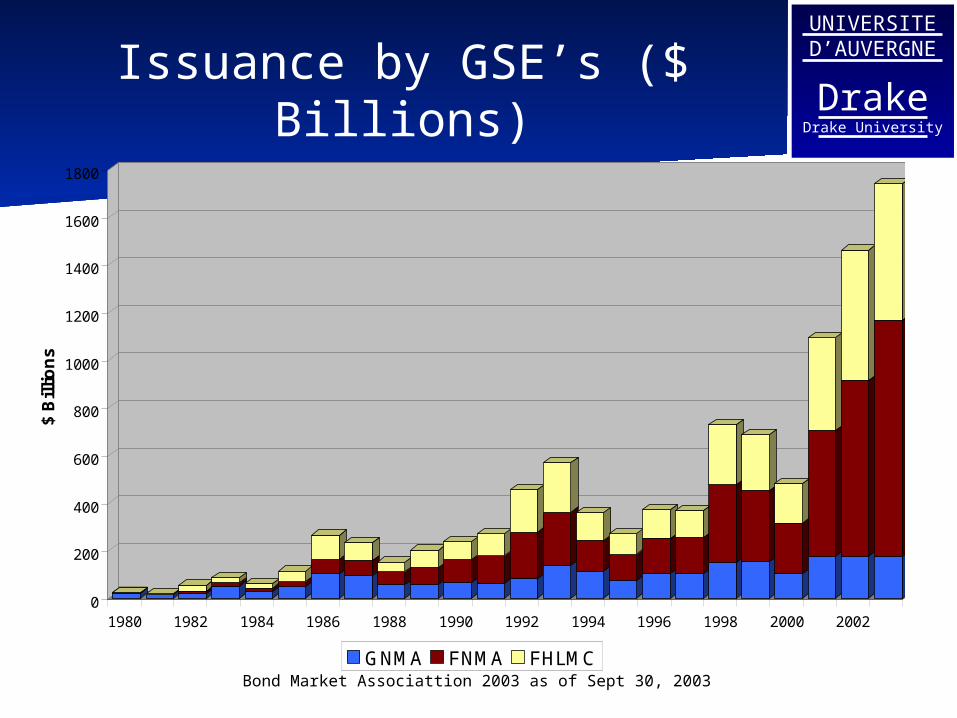

Issuance by GSE’s ($ Billions)

0

200

400

600

800

1000

1200

1400

1600

1800

$ B

illi

on

s

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002

GNMA FNMA FHLMC

Securitization Davidson et al Wiley Pub. 2003

UNIVERSITED’AUVERGNE

DrakeDrake University

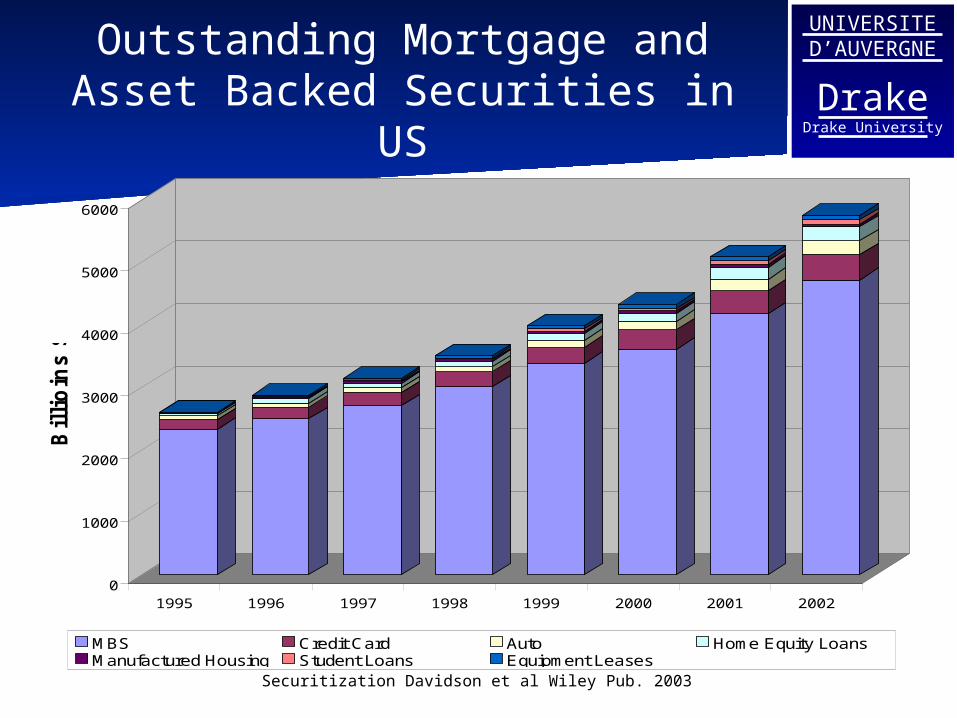

Outstanding Mortgage and Asset Backed Securities in US

0

1000

2000

3000

4000

5000

6000

Bil

lio

ins

$

1995 1996 1997 1998 1999 2000 2001 2002

MBS Credit Card Auto Home Equity LoansManufactured Housing Student Loans Equipment Leases

2595.72840.4

3146.8

3536.2

4006.94330.4

5077.9

5802.3

UNIVERSITED’AUVERGNE

DrakeDrake University

Current Questions in the Market Place relating to GSE’s

Are the GSE’s, especially Fannie Mae and Freddie Mac growing too fast?Do they pose a systematic risk for the US economy?Should the special treatment they receive be changed?

UNIVERSITED’AUVERGNE

DrakeDrake University

Recent Study by Federal Reserve

Wayne Passmore, an economist at the Federal Reserve Bank has recently completed a study on the impact of GSE’s

The GSE’s have a funding advantageSlightly lower mortgage rtes for a few borrowersImplicit subsidy from government relationshipImplicit subsidy responsible for much of GSE Market ValueMBS have not increased homebuilding

UNIVERSITED’AUVERGNE

DrakeDrake University

Mutual Fund Industry

In the fall of 2003 the US mutual fund industry was impacted by a wave of scandals revolving around market timing activity.“Market Timing Activity” – The movement of funds into and out of an asset in an attempt to take advantage of short term fluctuations in the value of the asset.

UNIVERSITED’AUVERGNE

DrakeDrake University

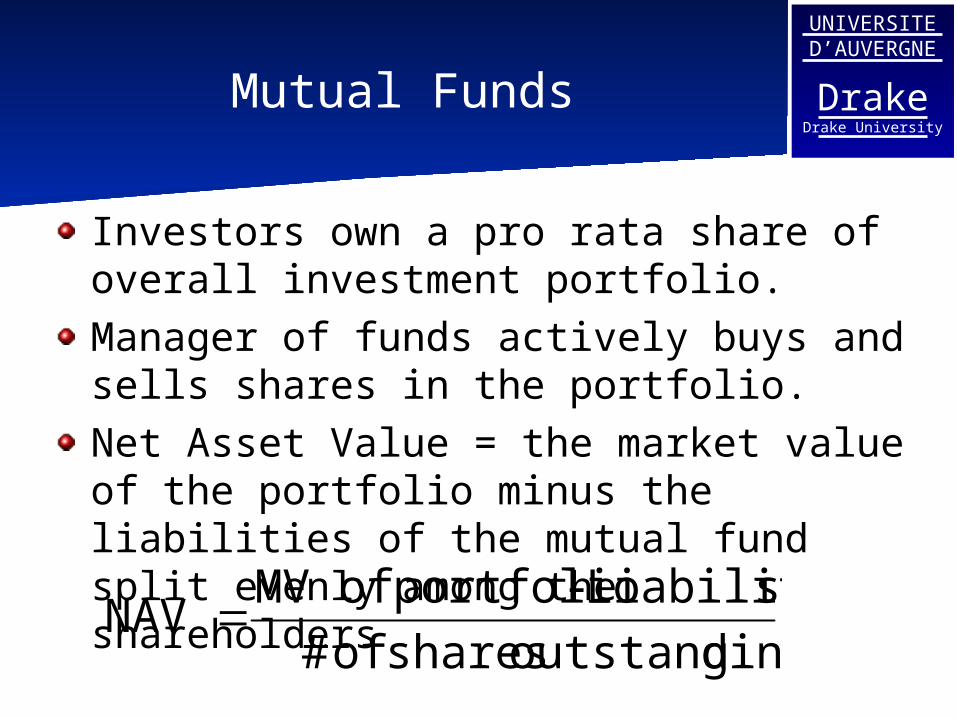

Mutual Funds

Investors own a pro rata share of overall investment portfolio.Manager of funds actively buys and sells shares in the portfolio.Net Asset Value = the market value of the portfolio minus the liabilities of the mutual fund split evenly among the shareholders

goutstandin shares of #

sLiabilitie- portfolio of MVNAV

UNIVERSITED’AUVERGNE

DrakeDrake University

Open End Funds

NAV is determined a the close of each day and all new investment into the fund or withdraws from the fund are priced at NAV. (NAV = price)The total number of shares in the fund increases if there are more investments than withdraws.

UNIVERSITED’AUVERGNE

DrakeDrake University

Open End Funds

Either changes in the price of securities held in the portfolio or in the amount of funds invested can change the price of a share of the fund. New funds provide cash which must be invested. Withdraws require cash, and may force the sale of securities in the portfolio.

UNIVERSITED’AUVERGNE

DrakeDrake University

Open End Funds

Whenever the fund sells securities if there is a capital gain, there is a tax for the holder of the fund.

UNIVERSITED’AUVERGNE

DrakeDrake University

Closed End Fund

The number of shares remain constant, similar to the shares of a corporation. However the fund cannot issue new shares Shares are sold in a secondary market. Demand and Supply for the shares determine the price of the shares along with the NAV.Price may not equal NAV

UNIVERSITED’AUVERGNE

DrakeDrake University

Closed End Funds

Shares may sell at a discount (below NAV) if investors expect future liabilities to decrease its profitability (taxes for example)Shares may sell at a premium (above NAV) if investors value access to a specific market or professional management of the portfolio.

UNIVERSITED’AUVERGNE

DrakeDrake University

Market Timing Activity

Groups of mutual funds were allowing institutions and individuals to move money between different mutual funds, for example an international fund and a fund designed to follow the S&P 500.In theory this can decrease the long run return of a shareholder who is buying into the fund and holding the asset.

UNIVERSITED’AUVERGNE

DrakeDrake University

Impact of timing on Long run Shareholder

Increased transaction costs in the fund decrease returnIncreased holding of cash decrease returnIncreased tax burden from the fund being forced to sell securities

UNIVERSITED’AUVERGNE

DrakeDrake University

Legality of Timing Activity

Timing on its own is legal. Each group of funds has the right to restrict or not restrict the activity. Violations

Allowing preferred investors to time, while not allowing the average shareholder to do the sameAllowing preferred investors into the fund late, after the close of trading (at the previous NAV)

UNIVERSITED’AUVERGNE

DrakeDrake University

Basis for legal claims and possible new regulation

Investor Protection and Consumer protection

Possible violation of fiduciary responsibility to shareholders Violation of rules specified in the funds prospectus

UNIVERSITED’AUVERGNE

DrakeDrake University

Other Current Topics

Social SecurityDerivative Reporting on Financial StatementsCorporate Governance and Increased Accountability of ManagementConsolidated Risk Management

UNIVERSITED’AUVERGNE

DrakeDrake University

Saving for Retirement

Two main ways US residents plan for retirementPrivate Pension PlansSocial Security (required by the government)

UNIVERSITED’AUVERGNE

DrakeDrake University

Social Security Introduction

Approximately 6% of your income is withheld by your employer and sent to the Social Security Administration. Your employer matches the amount withheld and sends it to the Social Security administration as well. Upon retirement you receive benefits based upon total contributions, and your last 5 years contributions.

UNIVERSITED’AUVERGNE

DrakeDrake University

Social Security and other Public Pension plans

Social Security is essentially a public defined benefit plan that all employees participate in via payroll taxes.Private pension plans are required to be “Fully Funded”Social Security is partially a “pay as you go” system. Any amount collected above that needed to make payments is sent to a trust fund.Investment is entirely in US treasury securities.

UNIVERSITED’AUVERGNE

DrakeDrake University

Fully Funded Pension Plans

Fully funded plans are required to maintain a balance that is capable of covering future expected payouts.The interest rates allowed in the calculation are set based upon long term US treasuries. Declining interest rates have forced US firms to contribute more to their Retirement Funds, impacting earnings.

UNIVERSITED’AUVERGNE

DrakeDrake University

Pay as You Go

Pay as you go pension plans take current contributions and use the contributions to pay for the current benefits of the retirees in the plan. Any amount above the amount needed for current payouts can be saved for future payouts. Currently the US Social Security system is receiving payments greater than needed to pay benefits and the excess funds are placed in a “trust account”

UNIVERSITED’AUVERGNE

DrakeDrake University

Social Security

In 2000 there are 3.4 workers paying into social security for each person receiving benefits. By 2030 it is estimated that there will be 2 workers paying into the system for each receiving benefits. It is estimated that by 2015 outlays will be greater than payments into the system and the trust fund will decline, reaching a zero balance in 2037.In 2037 it is estimated that contributions will equal 70% of needed outlays.

UNIVERSITED’AUVERGNE

DrakeDrake University

Privatizing Social Security

Should the Social Security Trust Fund be allowed to invest a portion of its assets in other markets such as corporate equity?

Increase return potential, increase risk

UNIVERSITED’AUVERGNE

DrakeDrake University

Corporate Governance

Recently there has been increased interest in the accountability of upper level management. Enron, Tyco, MCI World Com and other firms have recently disclosed mistakes in their financial reports, including intentionally misrepresenting the financial statements.

UNIVERSITED’AUVERGNE

DrakeDrake University

Sarbanes Oxly Act of 2002

Established Auditing Board under the SECIncreased accountability on the Board of Directors of firms for accuracy in audits.Separated auditing functions from investment banking functions

UNIVERSITED’AUVERGNE

DrakeDrake University

Consolidated Risk Management

The increased interaction of different institutions has required a new approach to risk management.The key is looking at risk management on a firm wide basis and coordinating between differenet business lines.

*Cumming and Hirtle, The Challenges of Risk Management in DIversified Financial Compaies.

UNIVERSITED’AUVERGNE

DrakeDrake University

Consolidated Risk Management

“A coordinated process of measuring and managing risk on firmwide basis.”*Requires a system that includes identification of risks, measurement of risk, methods for controlling the level of risk accepted, checks and balances, review and oversight at all levels of management (including the board of directors)

UNIVERSITED’AUVERGNE

DrakeDrake University

Benefits of Consolidating Risk Management

Diversification benefits are ignored without consolidation, leading to increased risk management costsLack of coordination can increase firm wide risk in times of market problems (unwinding similar position in different business lines for example).Without consolidation contagion risks are ignored Improves the “internal capital market” of the firm.Promote more transparency and better risk analysis by creditors.

UNIVERSITED’AUVERGNE

DrakeDrake University

Barriers to Consolidated Risk Management

Consolidation of financial firms has produced increased product and geographic diversification which has made business wide risk management more difficult.Information Costs

The cost of integrating, recording and analyzing risk across separate business lines.

UNIVERSITED’AUVERGNE

DrakeDrake University

Barriers to Consolidated Risk Management

Regulatory CostsConsolidation has created a framework where firms are required to respond to multiple regulators. Capital and Liquidity requirements may prohibit the movement of funds from one business line to another.Cost associated with managing the separate regulatory requirements including opportunity costs

Recommended