December 2017

DORIAN LPG ®

Forward-Looking Statements

This presentation contains certain forward-looking statements including analyses and other information based on forecasts of future results and estimates of amounts not yet determinable and statements relating to our future prospects, developments and business strategies. Forward-looking statements are identified by their use of terms and phrases such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “predict,” “project,” “will” and similar terms and phrases, including references to assumptions. The forward-looking statements in this presentation are based upon various assumptions, many of which are based, in turn, upon further assumptions, including without limitation, management’s examination of historical operating trends, data contained in our records and other data available from third parties. Although we believe that these assumptions were reasonable when made, because these assumptions are inherently subject to significant uncertainties and contingencies that are difficult or impossible to predict and are beyond our control, we cannot assure you that we will achieve or accomplish these expectations, beliefs or projections.

Actual results could differ materially from expectations expressed in the forward-looking statements if one or more of the underlying assumptions or expectations proves to be inaccurate or is not realized. Our actual future results may be materially different from and worse than what we expect. We qualify all of the forward-looking statements by these cautionary statements. We caution readers of this presentation not to place undue reliance on forward-looking statements. Any forward-looking statements contained herein are made only as of the date of this presentation, and we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Disclaimer

2

Dorian LPG at a glance

3

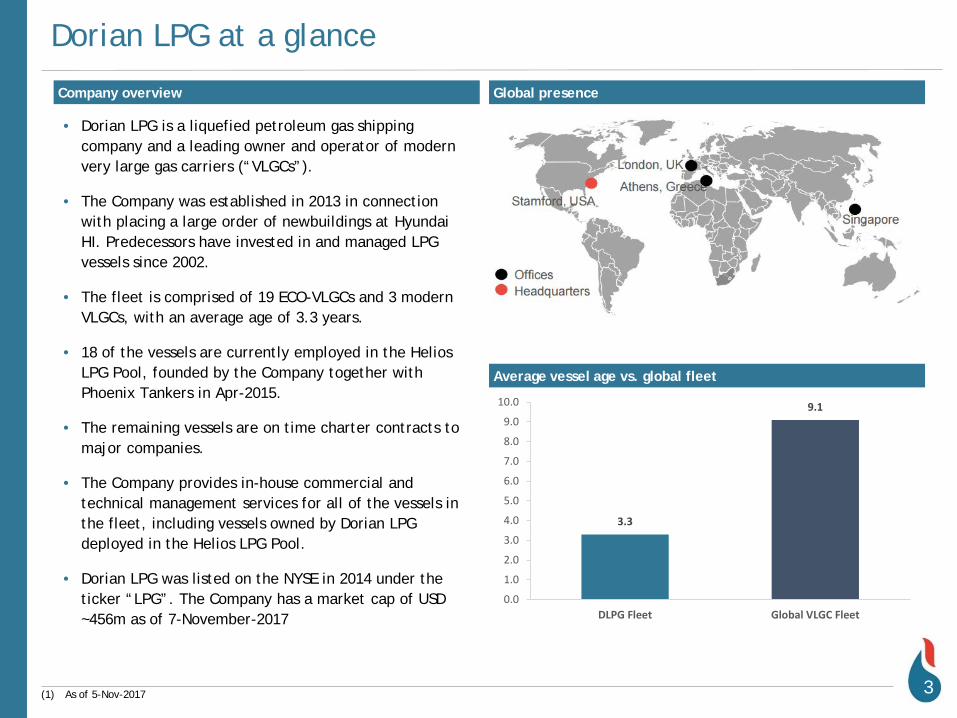

Company overview Global presence

Average vessel age vs. global fleet

• Dorian LPG is a liquefied petroleum gas shipping company and a leading owner and operator of modern very large gas carriers (“VLGCs”).

• The Company was established in 2013 in connection with placing a large order of newbuildings at Hyundai HI. Predecessors have invested in and managed LPG vessels since 2002.

• The fleet is comprised of 19 ECO-VLGCs and 3 modern VLGCs, with an average age of 3.3 years.

• 18 of the vessels are currently employed in the Helios LPG Pool, founded by the Company together with Phoenix Tankers in Apr-2015.

• The remaining vessels are on time charter contracts to major companies.

• The Company provides in-house commercial and technical management services for all of the vessels in the fleet, including vessels owned by Dorian LPG deployed in the Helios LPG Pool.

• Dorian LPG was listed on the NYSE in 2014 under the ticker “LPG”. The Company has a market cap of USD ~456m as of 7-November-2017

(1) As of 5-Nov-2017

1

3.3

9.1

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

DLPG Fleet Global VLGC Fleet

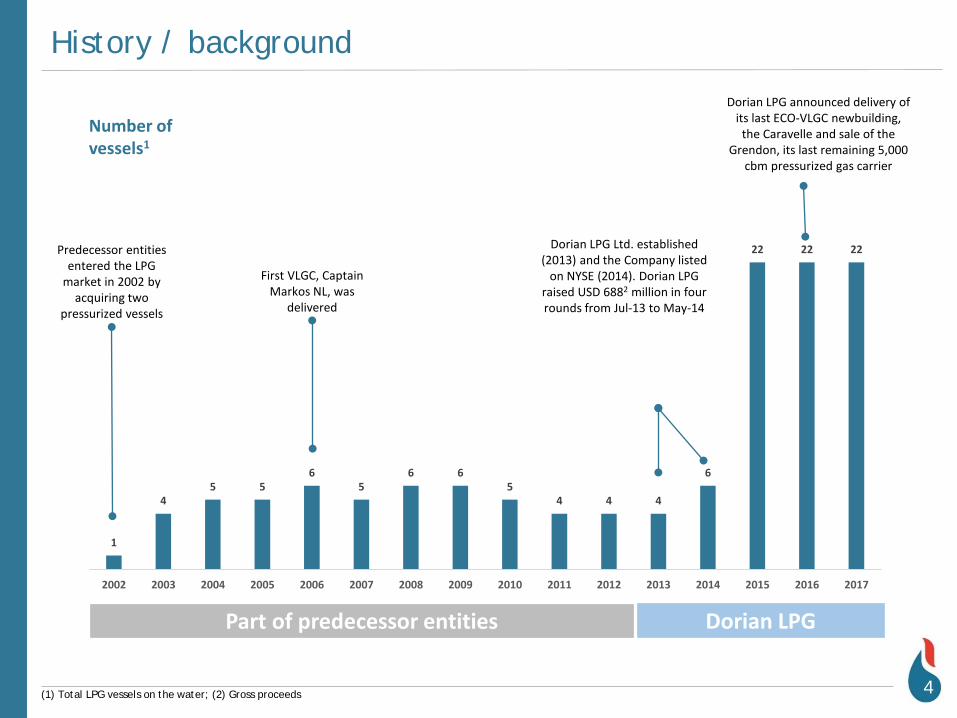

History / background

4

Predecessor entities entered the LPG

market in 2002 by acquiring two

pressurized vessels

Dorian LPG Ltd. established (2013) and the Company listed

on NYSE (2014). Dorian LPG raised USD 6882 million in four rounds from Jul-13 to May-14

Number of vessels1

Dorian LPG announced delivery of its last ECO-VLGC newbuilding,

the Caravelle and sale of the Grendon, its last remaining 5,000

cbm pressurized gas carrier

Part of predecessor entities Dorian LPG

First VLGC, Captain Markos NL, was

delivered

(1) Total LPG vessels on the water; (2) Gross proceeds

1

45 5

65

6 65

4 4 4

6

22 22 22

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

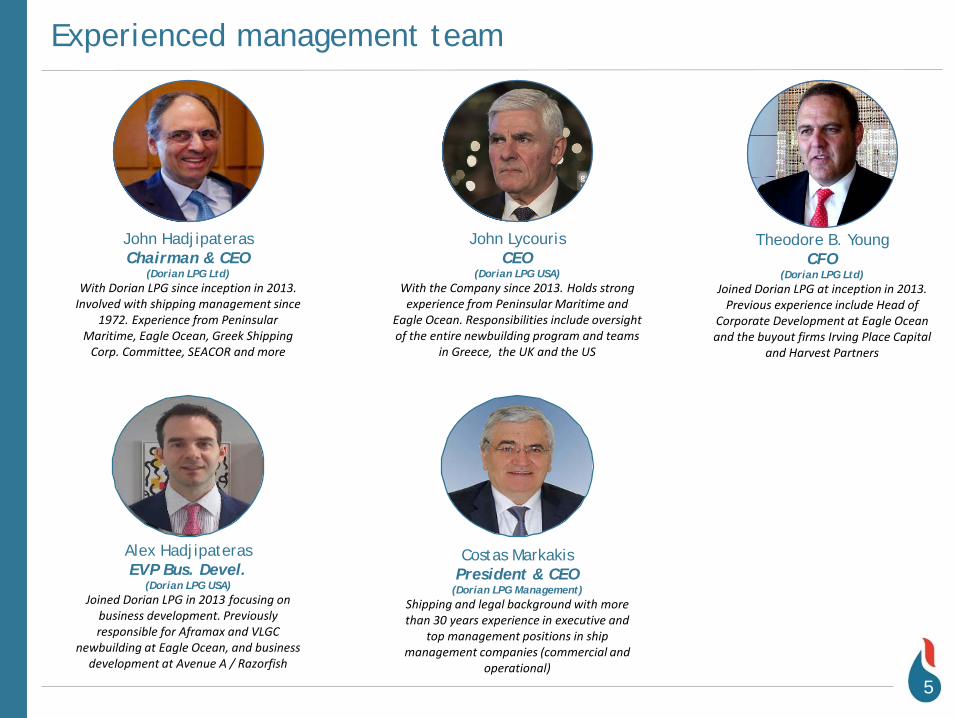

Experienced management team

5

John HadjipaterasChairman & CEO

(Dorian LPG Ltd)With Dorian LPG since inception in 2013.

Involved with shipping management since 1972. Experience from Peninsular

Maritime, Eagle Ocean, Greek Shipping Corp. Committee, SEACOR and more

John LycourisCEO

(Dorian LPG USA)With the Company since 2013. Holds strong

experience from Peninsular Maritime and Eagle Ocean. Responsibilities include oversight of the entire newbuilding program and teams

in Greece, the UK and the US

Costas MarkakisPresident & CEO

(Dorian LPG Management)Shipping and legal background with more than 30 years experience in executive and

top management positions in ship management companies (commercial and

operational)

Theodore B. YoungCFO

(Dorian LPG Ltd)Joined Dorian LPG at inception in 2013.

Previous experience include Head of Corporate Development at Eagle Ocean and the buyout firms Irving Place Capital

and Harvest Partners

Alex HadjipaterasEVP Bus. Devel.

(Dorian LPG USA)Joined Dorian LPG in 2013 focusing on

business development. Previously responsible for Aframax and VLGC

newbuilding at Eagle Ocean, and business development at Avenue A / Razorfish

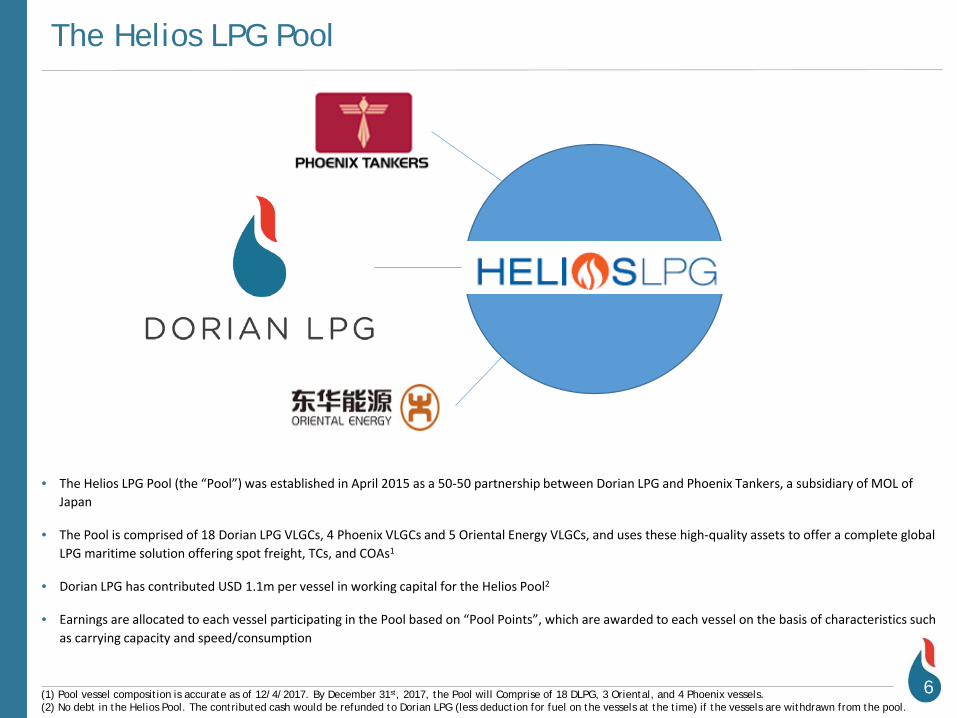

The Helios LPG Pool

6

• The Helios LPG Pool (the “Pool”) was established in April 2015 as a 50-50 partnership between Dorian LPG and Phoenix Tankers, a subsidiary of MOL of Japan

• The Pool is comprised of 18 Dorian LPG VLGCs, 4 Phoenix VLGCs and 5 Oriental Energy VLGCs, and uses these high-quality assets to offer a complete global LPG maritime solution offering spot freight, TCs, and COAs1

• Dorian LPG has contributed USD 1.1m per vessel in working capital for the Helios Pool2

• Earnings are allocated to each vessel participating in the Pool based on “Pool Points”, which are awarded to each vessel on the basis of characteristics such as carrying capacity and speed/consumption

(1) Pool vessel composition is accurate as of 12/4/2017. By December 31st, 2017, the Pool will Comprise of 18 DLPG, 3 Oriental, and 4 Phoenix vessels.(2) No debt in the Helios Pool. The contributed cash would be refunded to Dorian LPG (less deduction for fuel on the vessels at the time) if the vessels are withdrawn from the pool.

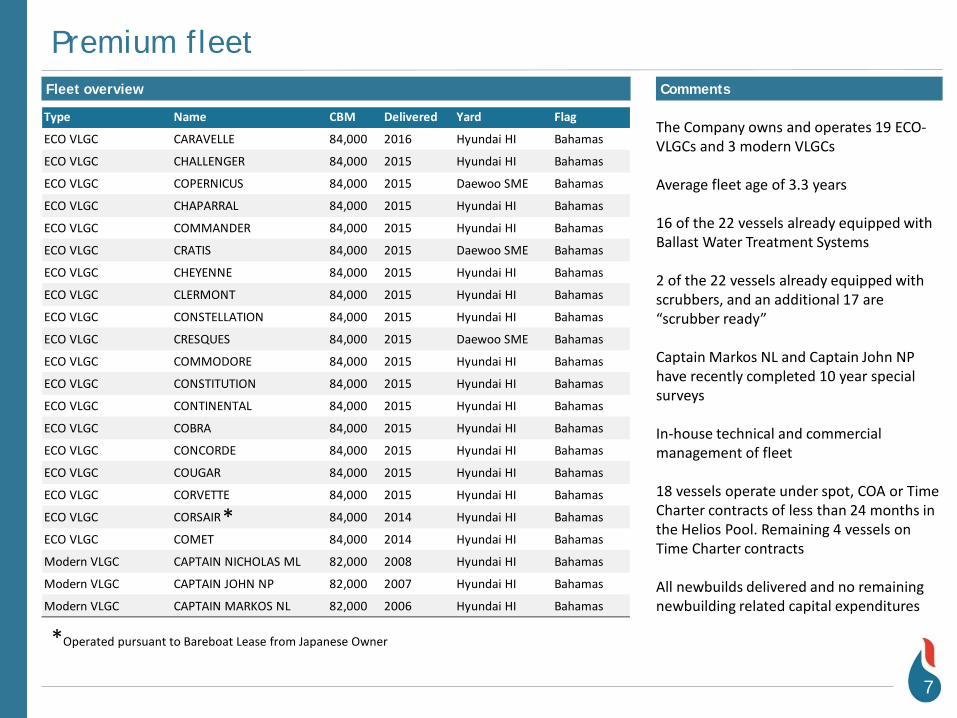

Type Name CBM Delivered Yard Flag

ECO VLGC CARAVELLE 84,000 2016 Hyundai HI Bahamas

ECO VLGC CHALLENGER 84,000 2015 Hyundai HI Bahamas

ECO VLGC COPERNICUS 84,000 2015 Daewoo SME Bahamas

ECO VLGC CHAPARRAL 84,000 2015 Hyundai HI Bahamas

ECO VLGC COMMANDER 84,000 2015 Hyundai HI Bahamas

ECO VLGC CRATIS 84,000 2015 Daewoo SME Bahamas

ECO VLGC CHEYENNE 84,000 2015 Hyundai HI Bahamas

ECO VLGC CLERMONT 84,000 2015 Hyundai HI Bahamas

ECO VLGC CONSTELLATION 84,000 2015 Hyundai HI Bahamas

ECO VLGC CRESQUES 84,000 2015 Daewoo SME Bahamas

ECO VLGC COMMODORE 84,000 2015 Hyundai HI Bahamas

ECO VLGC CONSTITUTION 84,000 2015 Hyundai HI Bahamas

ECO VLGC CONTINENTAL 84,000 2015 Hyundai HI Bahamas

ECO VLGC COBRA 84,000 2015 Hyundai HI Bahamas

ECO VLGC CONCORDE 84,000 2015 Hyundai HI Bahamas

ECO VLGC COUGAR 84,000 2015 Hyundai HI Bahamas

ECO VLGC CORVETTE 84,000 2015 Hyundai HI Bahamas

ECO VLGC CORSAIR 84,000 2014 Hyundai HI Bahamas

ECO VLGC COMET 84,000 2014 Hyundai HI Bahamas

Modern VLGC CAPTAIN NICHOLAS ML 82,000 2008 Hyundai HI Bahamas

Modern VLGC CAPTAIN JOHN NP 82,000 2007 Hyundai HI Bahamas

Modern VLGC CAPTAIN MARKOS NL 82,000 2006 Hyundai HI Bahamas

Premium fleet

7

Fleet overview Comments

The Company owns and operates 19 ECO-VLGCs and 3 modern VLGCs

Average fleet age of 3.3 years

16 of the 22 vessels already equipped with Ballast Water Treatment Systems

2 of the 22 vessels already equipped with scrubbers, and an additional 17 are “scrubber ready”

Captain Markos NL and Captain John NP have recently completed 10 year special surveys

In-house technical and commercial management of fleet

18 vessels operate under spot, COA or Time Charter contracts of less than 24 months in the Helios Pool. Remaining 4 vessels on Time Charter contracts

All newbuilds delivered and no remaining newbuilding related capital expenditures

*

*Operated pursuant to Bareboat Lease from Japanese Owner

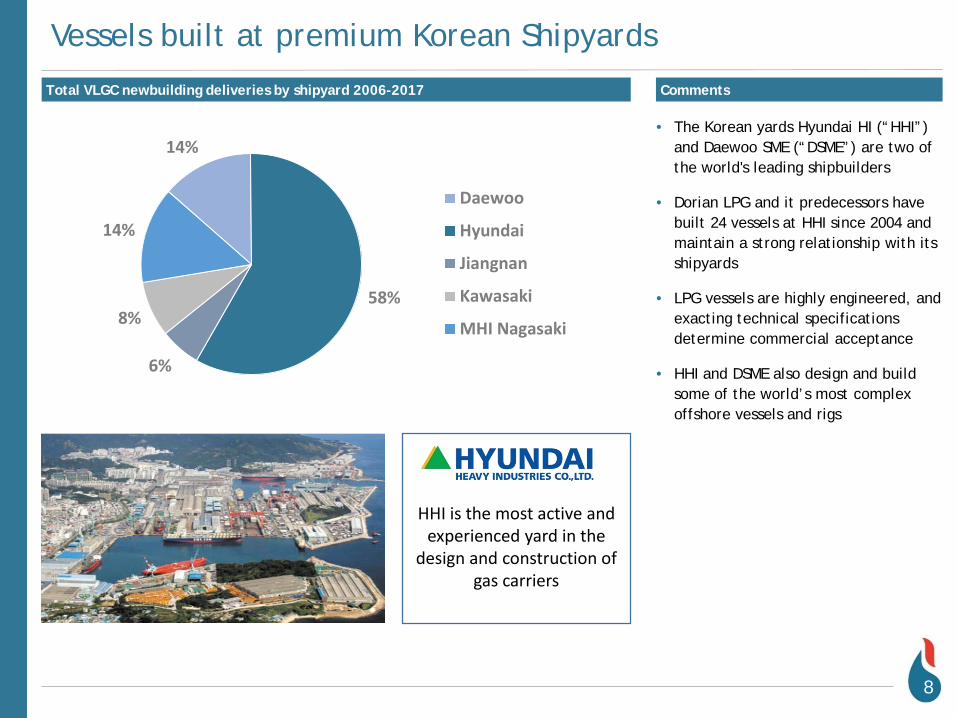

14%

58%

6%

8%

14%

Daewoo

Hyundai

Jiangnan

Kawasaki

MHI Nagasaki

Vessels built at premium Korean Shipyards

8

Total VLGC newbuilding deliveries by shipyard 2006-2017 Comments

• The Korean yards Hyundai HI (“HHI”) and Daewoo SME (“DSME”) are two of the world's leading shipbuilders

• Dorian LPG and it predecessors have built 24 vessels at HHI since 2004 and maintain a strong relationship with its shipyards

• LPG vessels are highly engineered, and exacting technical specifications determine commercial acceptance

• HHI and DSME also design and build some of the world’s most complex offshore vessels and rigs

HHI is the most active and experienced yard in the

design and construction of gas carriers

LPG Fundamentals

9

Hundreds of millions of people around the world use LPG at home for applications such as cooking and heating.

LPG is the preferred alternative automotive transportation fuel and is increasingly being used as a marine fuel.

Millions of businesses rely on LPG. It is the ideal fuel choice for businesses that are not connected to an existing electrical grid.

Farmers across the world rely on LPG to meet the challenge of staying competitive in the modern agricultural environment

Industries such as aerosol, refrigeration, and chemical feedstock all look to LPG to provide sustainable fuel alternatives

What is LPG?Liquefied petroleum gas ("LPG") is a fossil fuel made during natural gas processing and oil refining. LPG is a by product of both oil and natural gas production and more than two-thirds of the LPG people use is extracted directly from the earth. The rest of it is manufactured indirectly from crude oil refining.

Why use LPG?LPG is cleaner than coal and oil and an alternative to gasoline. It generates less air pollution and produces fewer emissions of carbon dioxide. LPG is also highly portable, making it a convenient source of energy usable in remote places where ordinary gas supplies are unavailable or have been interrupted.

AT HOME

ON THE GO

AT THEFARM

AT WORK

OTHER

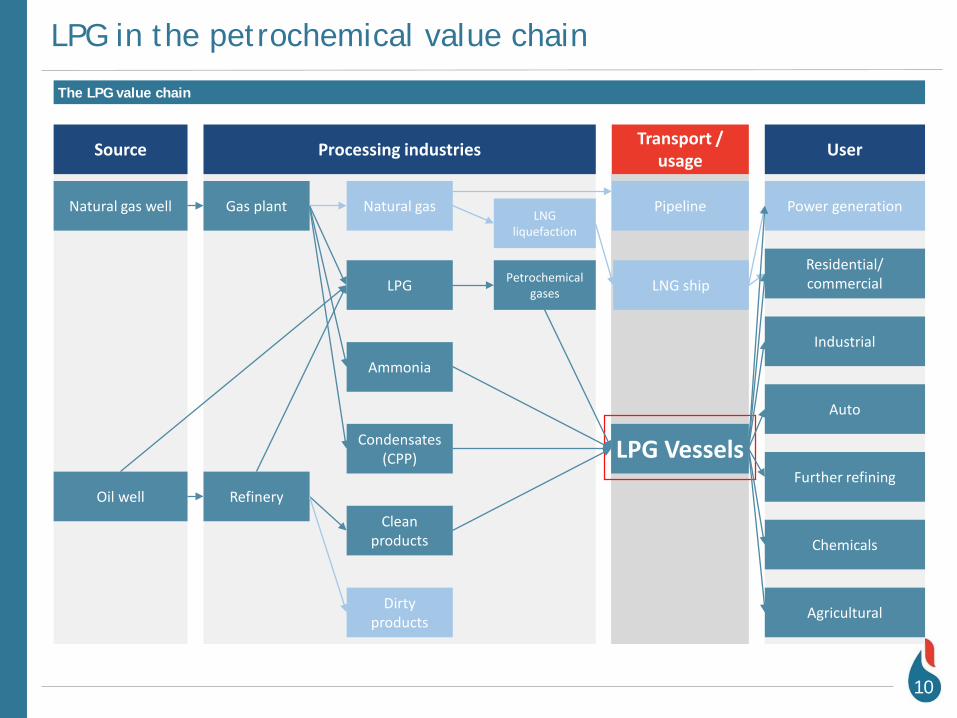

LPG in the petrochemical value chain

10

The LPG value chain

Source Processing industries Transport / usage User

Natural gas well

Oil well

Gas plant Natural gasLNG

liquefaction

Refinery

LPG

Ammonia

Condensates (CPP)

Clean products

Dirty products

Petrochemical gases

Pipeline

LNG ship

LPG Vessels

Power generation

Residential/commercial

Industrial

Auto

Further refining

Chemicals

Agricultural

LPG Supply and Export Dynamics

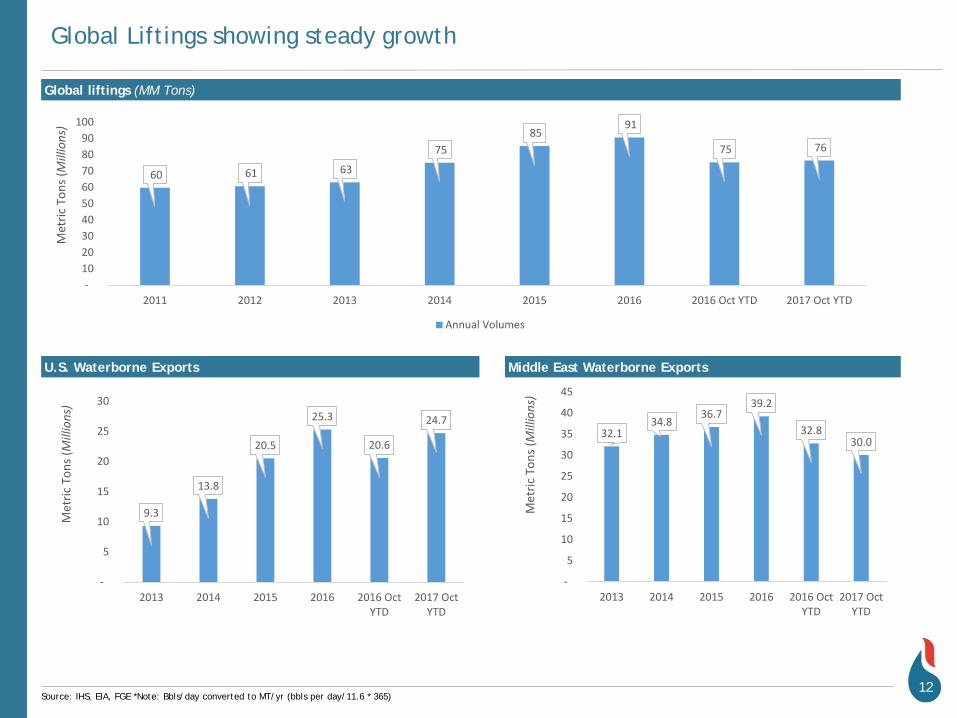

Global Liftings showing steady growth

Global liftings (MM Tons)

12Source: IHS, EIA, FGE *Note: Bbls/day converted to MT/yr (bbls per day/11.6 * 365)

U.S. Waterborne Exports Middle East Waterborne Exports

9.3

13.8

20.5

25.3

20.6

24.7

-

5

10

15

20

25

30

2013 2014 2015 2016 2016 OctYTD

2017 OctYTD

Met

ric T

ons (

Mill

ions

)

32.134.8

36.739.2

32.830.0

-

5

10

15

20

25

30

35

40

45

2013 2014 2015 2016 2016 OctYTD

2017 OctYTD

Met

ric T

ons (

Mill

ions

)

60 61 63

75 85

91

75 76

- 10 20 30 40 50 60 70 80 90

100

2011 2012 2013 2014 2015 2016 2016 Oct YTD 2017 Oct YTD

Met

ric T

ons (

Mill

ions

)

Annual Volumes

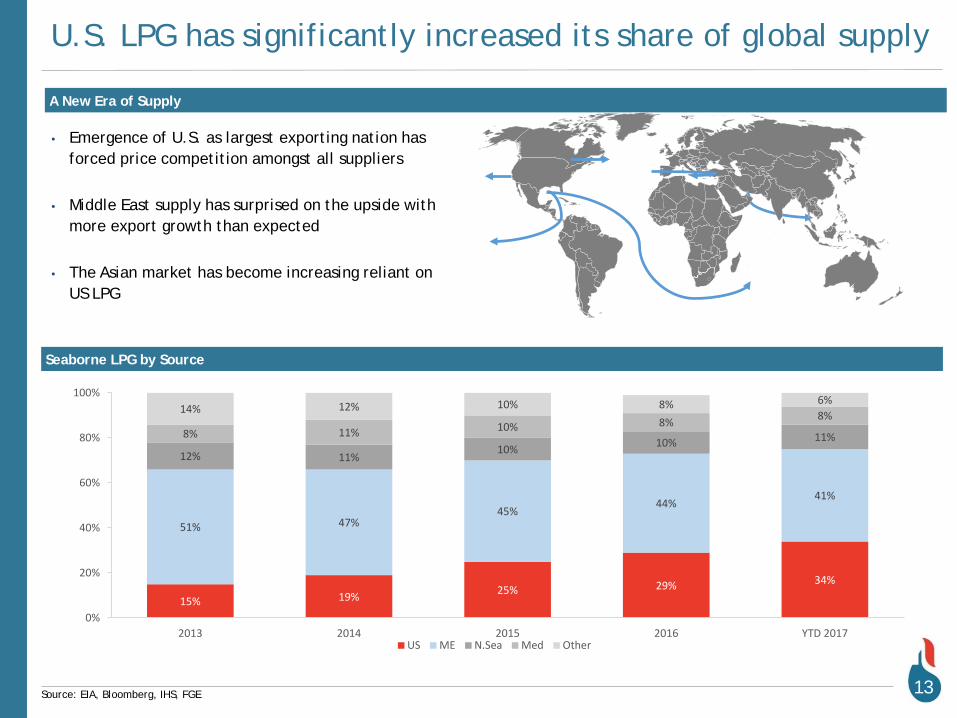

U.S. LPG has significantly increased its share of global supply

Source: EIA, Bloomberg, IHS, FGE

A New Era of Supply

13

• Emergence of U.S. as largest exporting nation has forced price competition amongst all suppliers

• Middle East supply has surprised on the upside with more export growth than expected

• The Asian market has become increasing reliant on US LPG

Seaborne LPG by Source

15% 19% 25% 29% 34%

51% 47%45%

44%41%

12% 11%10% 10% 11%8% 11% 10% 8% 8%14% 12% 10% 8% 6%

0%

20%

40%

60%

80%

100%

2013 2014 2015 2016 YTD 2017US ME N.Sea Med Other

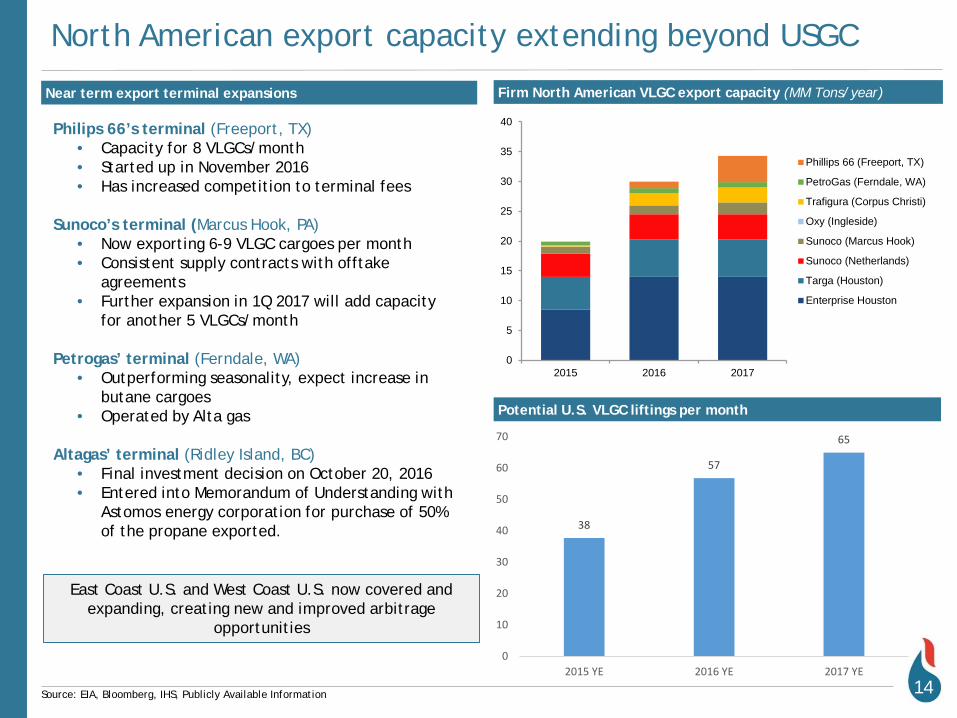

North American export capacity extending beyond USGC

Firm North American VLGC export capacity (MM Tons/year)

East Coast U.S. and West Coast U.S. now covered and expanding, creating new and improved arbitrage

opportunities

Philips 66’s terminal (Freeport, TX) • Capacity for 8 VLGCs/month• Started up in November 2016• Has increased competition to terminal fees

Sunoco’s terminal (Marcus Hook, PA)• Now exporting 6-9 VLGC cargoes per month• Consistent supply contracts with offtake

agreements• Further expansion in 1Q 2017 will add capacity

for another 5 VLGCs/month

Petrogas’ terminal (Ferndale, WA)• Outperforming seasonality, expect increase in

butane cargoes• Operated by Alta gas

Altagas’ terminal (Ridley Island, BC)• Final investment decision on October 20, 2016• Entered into Memorandum of Understanding with

Astomos energy corporation for purchase of 50% of the propane exported.

14Source: EIA, Bloomberg, IHS, Publicly Available Information

Near term export terminal expansions

38

57

65

0

10

20

30

40

50

60

70

2015 YE 2016 YE 2017 YE

Potential U.S. VLGC liftings per month

0

5

10

15

20

25

30

35

40

2015 2016 2017

Phillips 66 (Freeport, TX)

PetroGas (Ferndale, WA)

Trafigura (Corpus Christi)

Oxy (Ingleside)

Sunoco (Marcus Hook)

Sunoco (Netherlands)

Targa (Houston)

Enterprise Houston

15

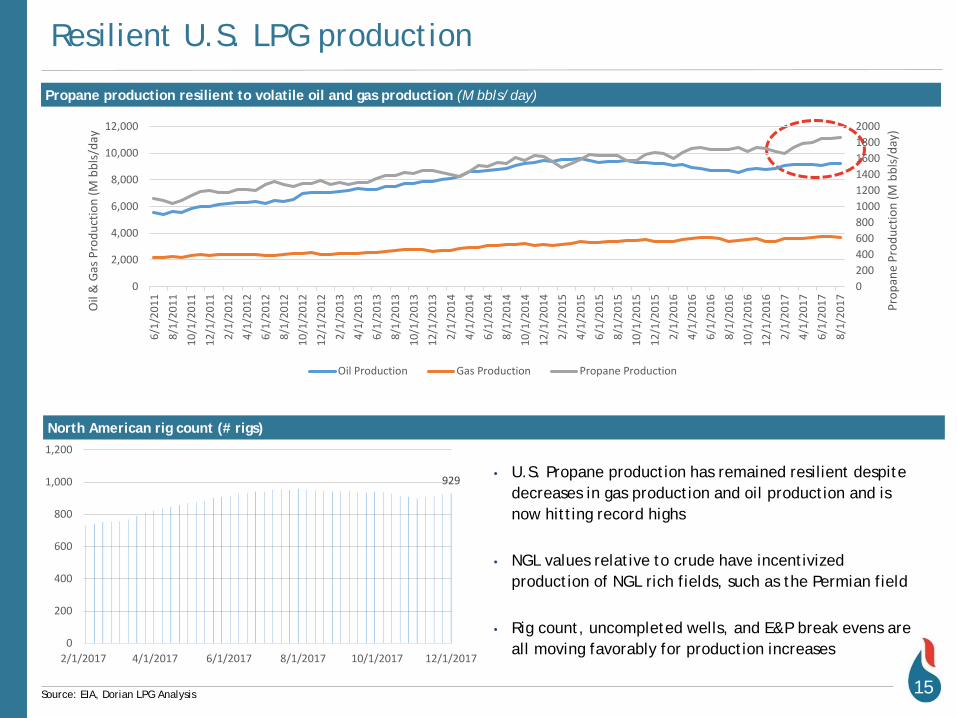

Propane production resilient to volatile oil and gas production (M bbls/day)

Source: EIA, Dorian LPG Analysis

• U.S. Propane production has remained resilient despite decreases in gas production and oil production and is now hitting record highs

• NGL values relative to crude have incentivized production of NGL rich fields, such as the Permian field

• Rig count, uncompleted wells, and E&P break evens are all moving favorably for production increases

Resilient U.S. LPG production

North American rig count (# rigs)

0200400600800100012001400160018002000

0

2,000

4,000

6,000

8,000

10,000

12,000

6/1/

2011

8/1/

2011

10/1

/201

112

/1/2

011

2/1/

2012

4/1/

2012

6/1/

2012

8/1/

2012

10/1

/201

212

/1/2

012

2/1/

2013

4/1/

2013

6/1/

2013

8/1/

2013

10/1

/201

312

/1/2

013

2/1/

2014

4/1/

2014

6/1/

2014

8/1/

2014

10/1

/201

412

/1/2

014

2/1/

2015

4/1/

2015

6/1/

2015

8/1/

2015

10/1

/201

512

/1/2

015

2/1/

2016

4/1/

2016

6/1/

2016

8/1/

2016

10/1

/201

612

/1/2

016

2/1/

2017

4/1/

2017

6/1/

2017

8/1/

2017 Pr

opan

e Pr

oduc

tion

(M b

bls/

day)

Oil

& G

as P

rodu

ctio

n (M

bbl

s/da

y

Oil Production Gas Production Propane Production

929

0

200

400

600

800

1,000

1,200

2/1/2017 4/1/2017 6/1/2017 8/1/2017 10/1/2017 12/1/2017

LPG Demand & Consumption

Growing markets for LPG: CHINA

• will be used as

primary fuel source

Annual China LPG imports (Tons)

17Source: FGE

4M

7M

12M

16M

12M

14M

M

2M

4M

6M

8M

10M

12M

14M

16M

18M

2013 2014 2015 2016 2016 Sep YTD 2017 Sep YTD

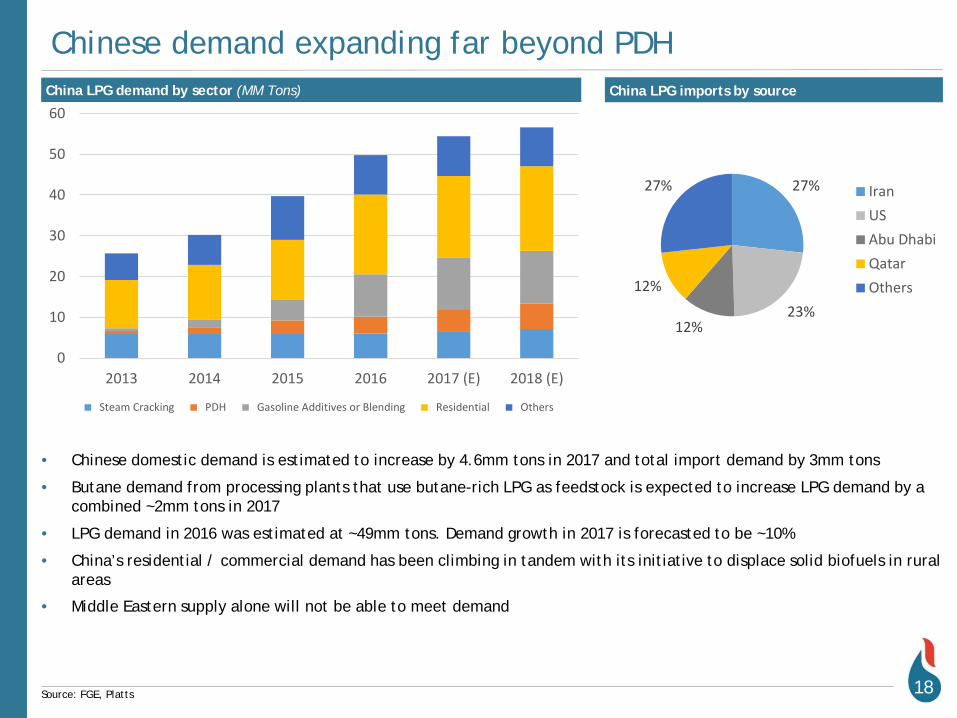

China LPG demand by sector (MM Tons)

Chinese demand expanding far beyond PDH

18Source: FGE, Platts

• Chinese domestic demand is estimated to increase by 4.6mm tons in 2017 and total import demand by 3mm tons

• Butane demand from processing plants that use butane-rich LPG as feedstock is expected to increase LPG demand by a combined ~2mm tons in 2017

• LPG demand in 2016 was estimated at ~49mm tons. Demand growth in 2017 is forecasted to be ~10%

• China’s residential / commercial demand has been climbing in tandem with its initiative to displace solid biofuels in rural areas

• Middle Eastern supply alone will not be able to meet demand

27%

23%12%

12%

27% IranUSAbu DhabiQatarOthers

China LPG imports by source

0

10

20

30

40

50

60

2013 2014 2015 2016 2017 (E) 2018 (E)

Steam Cracking PDH Gasoline Additives or Blending Residential Others

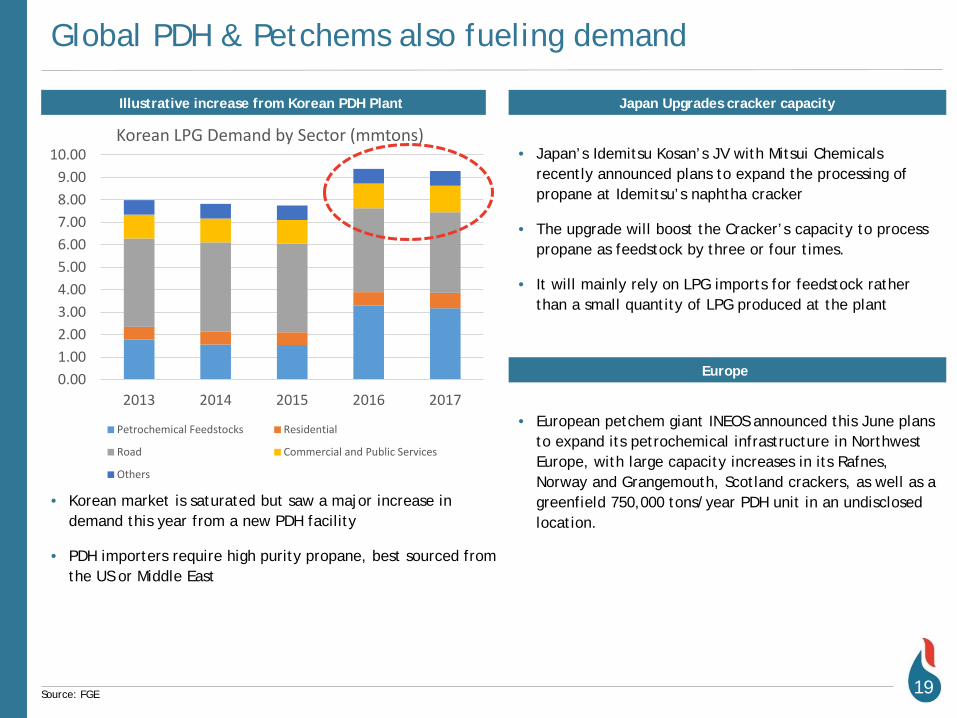

Global PDH & Petchems also fueling demand

19

Illustrative increase from Korean PDH Plant

• Korean market is saturated but saw a major increase in demand this year from a new PDH facility

• PDH importers require high purity propane, best sourced from the US or Middle East

Japan Upgrades cracker capacity

• Japan’s Idemitsu Kosan’s JV with Mitsui Chemicals recently announced plans to expand the processing of propane at Idemitsu’s naphtha cracker

• The upgrade will boost the Cracker’s capacity to process propane as feedstock by three or four times.

• It will mainly rely on LPG imports for feedstock rather than a small quantity of LPG produced at the plant

0.001.002.003.004.005.006.007.008.009.00

10.00

2013 2014 2015 2016 2017

Korean LPG Demand by Sector (mmtons)

Petrochemical Feedstocks Residential

Road Commercial and Public Services

Others

Source: FGE

Europe

• European petchem giant INEOS announced this June plans to expand its petrochemical infrastructure in Northwest Europe, with large capacity increases in its Rafnes, Norway and Grangemouth, Scotland crackers, as well as a greenfield 750,000 tons/year PDH unit in an undisclosed location.

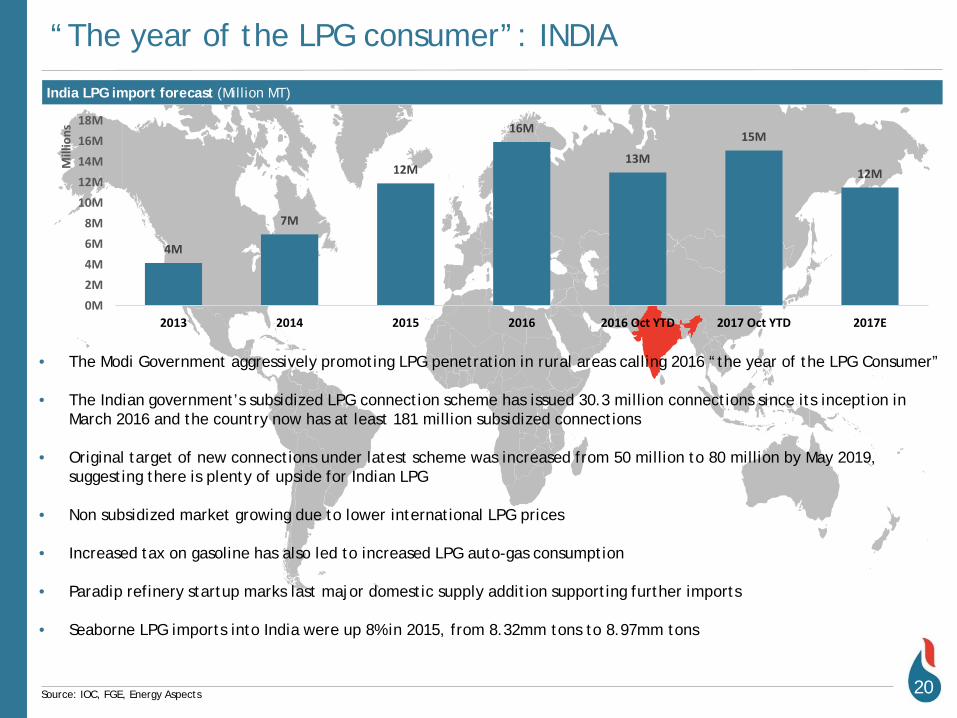

“The year of the LPG consumer”: INDIA

• Power conversion

project with Vitol

• By April, LPG will be

used as primary fuel

source

India LPG import forecast (Million MT)

• The Modi Government aggressively promoting LPG penetration in rural areas calling 2016 “the year of the LPG Consumer”

• The Indian government’s subsidized LPG connection scheme has issued 30.3 million connections since its inception in March 2016 and the country now has at least 181 million subsidized connections

• Original target of new connections under latest scheme was increased from 50 million to 80 million by May 2019, suggesting there is plenty of upside for Indian LPG

• Non subsidized market growing due to lower international LPG prices

• Increased tax on gasoline has also led to increased LPG auto-gas consumption

• Paradip refinery startup marks last major domestic supply addition supporting further imports

• Seaborne LPG imports into India were up 8% in 2015, from 8.32mm tons to 8.97mm tons

20Source: IOC, FGE, Energy Aspects

4M

7M

12M

16M

13M

15M

12M

0M2M4M6M8M

10M12M14M16M18M

2013 2014 2015 2016 2016 Oct YTD 2017 Oct YTD 2017E

Mill

ions

0

2

4

6

8

10

12

14

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Industry Commercial and Public Services Residential

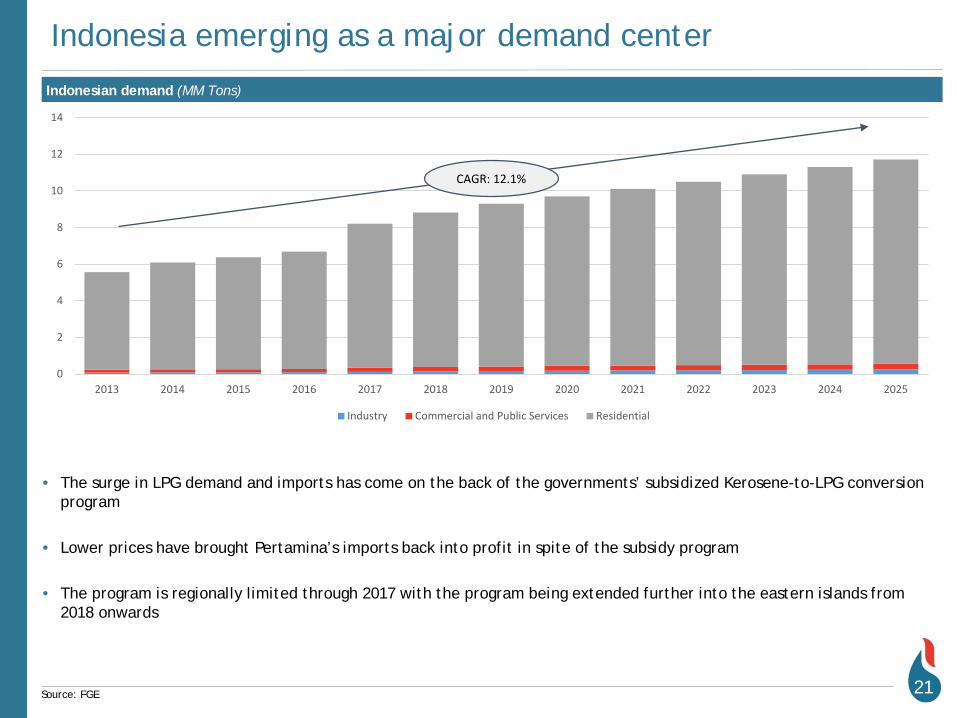

Indonesia emerging as a major demand center

21Source: FGE

• The surge in LPG demand and imports has come on the back of the governments’ subsidized Kerosene-to-LPG conversion program

• Lower prices have brought Pertamina’s imports back into profit in spite of the subsidy program

• The program is regionally limited through 2017 with the program being extended further into the eastern islands from 2018 onwards

Indonesian demand (MM Tons)

CAGR: 12.1%

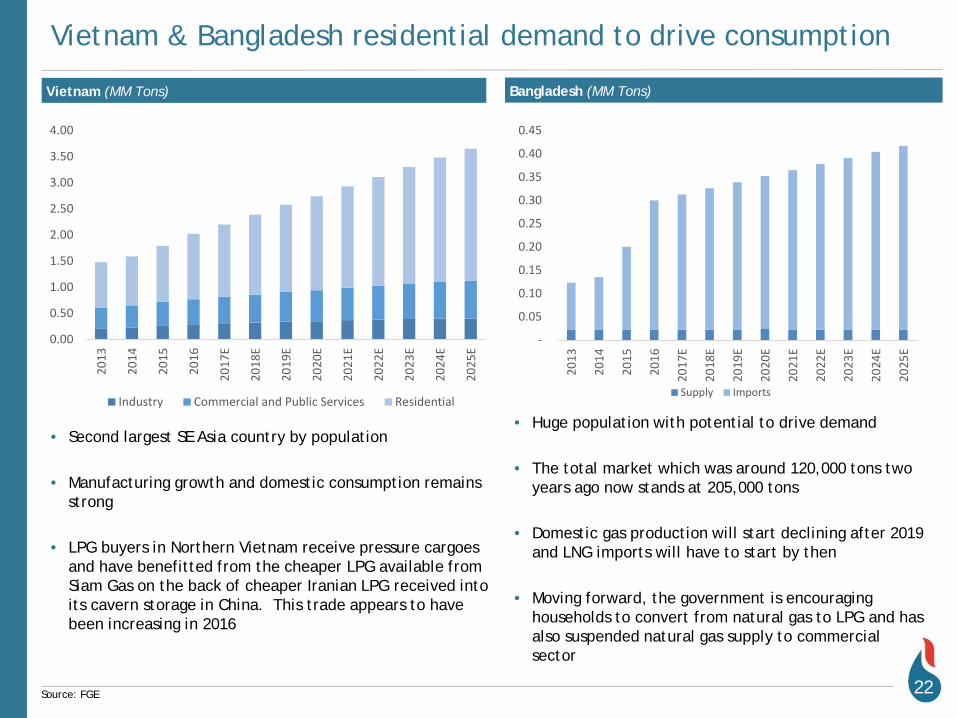

Vietnam & Bangladesh residential demand to drive consumption

22Source: FGE

• Second largest SE Asia country by population

• Manufacturing growth and domestic consumption remains strong

• LPG buyers in Northern Vietnam receive pressure cargoes and have benefitted from the cheaper LPG available from Siam Gas on the back of cheaper Iranian LPG received into its cavern storage in China. This trade appears to have been increasing in 2016

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

2013

2014

2015

2016

2017

E

2018

E

2019

E

2020

E

2021

E

2022

E

2023

E

2024

E

2025

E

Industry Commercial and Public Services Residential

• Huge population with potential to drive demand

• The total market which was around 120,000 tons two years ago now stands at 205,000 tons

• Domestic gas production will start declining after 2019 and LNG imports will have to start by then

• Moving forward, the government is encouraging households to convert from natural gas to LPG and has also suspended natural gas supply to commercial sector

-

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

2013

2014

2015

2016

2017

E

2018

E

2019

E

2020

E

2021

E

2022

E

2023

E

2024

E

2025

E

Supply Imports

Vietnam (MM Tons) Bangladesh (MM Tons)

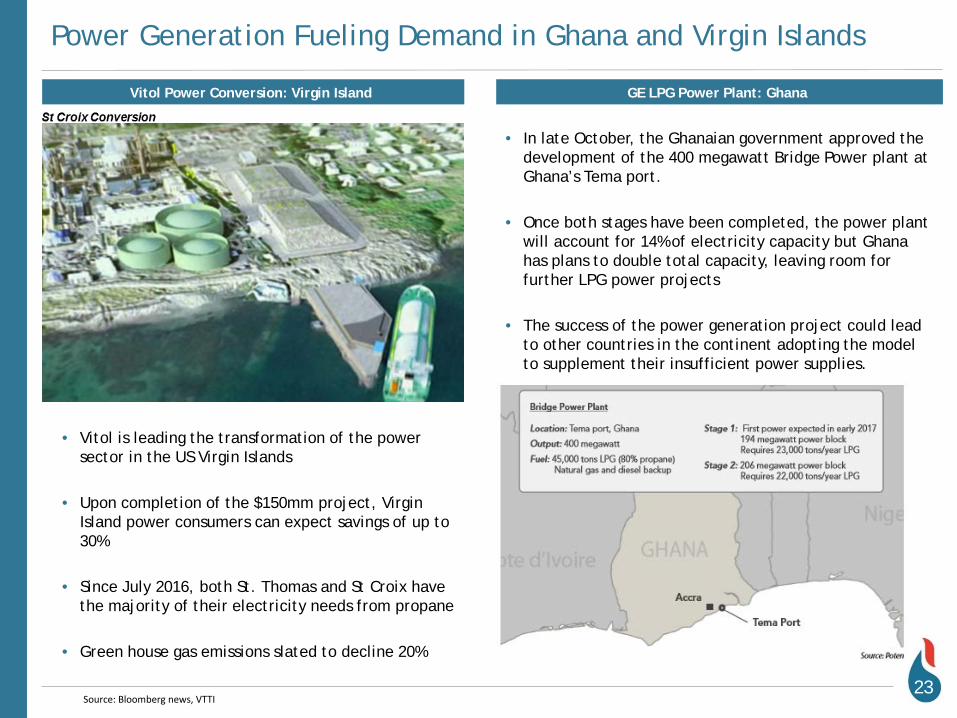

Power Generation Fueling Demand in Ghana and Virgin Islands

23

Vitol Power Conversion: Virgin Island GE LPG Power Plant: Ghana

• In late October, the Ghanaian government approved the development of the 400 megawatt Bridge Power plant at Ghana’s Tema port.

• Once both stages have been completed, the power plant will account for 14% of electricity capacity but Ghana has plans to double total capacity, leaving room for further LPG power projects

• The success of the power generation project could lead to other countries in the continent adopting the model to supplement their insufficient power supplies.

• Vitol is leading the transformation of the power sector in the US Virgin Islands

• Upon completion of the $150mm project, Virgin Island power consumers can expect savings of up to 30%

• Since July 2016, both St. Thomas and St Croix have the majority of their electricity needs from propane

• Green house gas emissions slated to decline 20%

Source: Bloomberg news, VTTI

24

Established production hubs

Global supply base

Maritime and land transport options

Price competitive product

Low cost “last mile” infrastructure

Lower greenhouse gas emissions

20% less CO2 than heating oil

50% less CO2 than coal

Safe fuel source

Avoids harmful and dangerous waste

LPG should be the fuel of choice for emerging economies

Source: ExceptionalEnergy.com

Key Factors Favoring LPG Adoption for Power Generation and Retail Consumption

Strong Fundamentals for Continued LPG Adoption

Each year, around 3.5 million premature deaths can be attributed to household air pollution resulting from the traditional use of solid fuels, such as fuelwood and charcoal.

Four out of five people in sub-Saharan Africa rely on the traditional use of solid biomass, mainly fuelwood, for cooking.

Nearly 3.1 billion people, or 43% of the global population, still rely on polluting fuels (i.e. biomass, coal, kerosene) and technologies for cooking - a major source of household air pollution.

Source: World Health Organization

Economic

Environmental

VLGC Shipping Market Dynamics

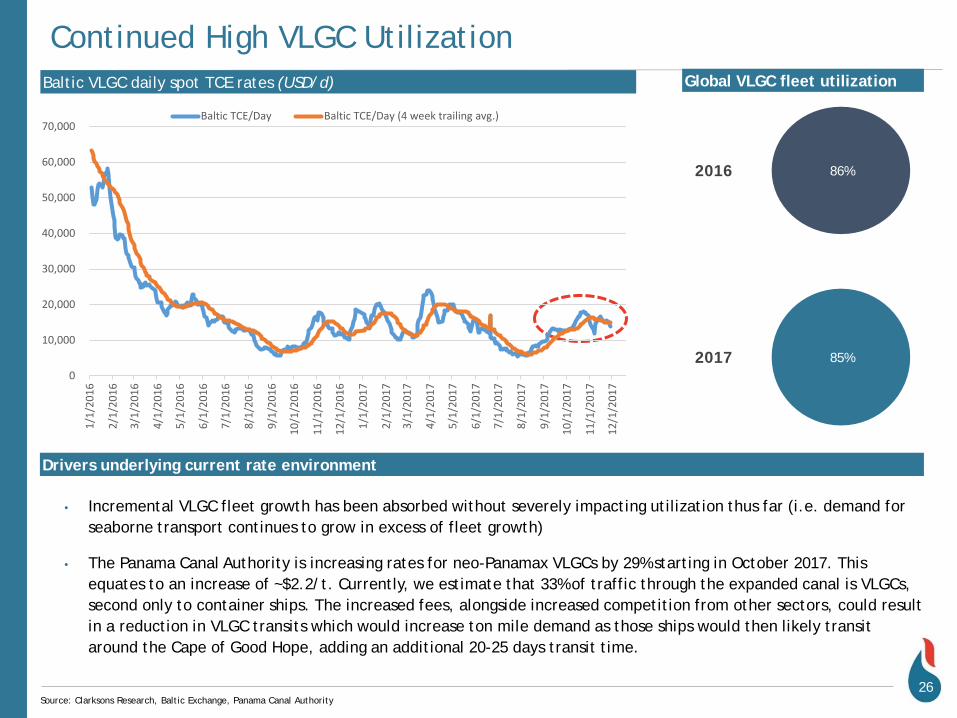

Continued High VLGC Utilization

Drivers underlying current rate environment

26Source: Clarksons Research, Baltic Exchange, Panama Canal Authority

Baltic VLGC daily spot TCE rates (USD/d) Global VLGC fleet utilization

86%

85%

2016

2017

• Incremental VLGC fleet growth has been absorbed without severely impacting utilization thus far (i.e. demand for seaborne transport continues to grow in excess of fleet growth)

• The Panama Canal Authority is increasing rates for neo-Panamax VLGCs by 29% starting in October 2017. This equates to an increase of ~$2.2/t. Currently, we estimate that 33% of traffic through the expanded canal is VLGCs, second only to container ships. The increased fees, alongside increased competition from other sectors, could result in a reduction in VLGC transits which would increase ton mile demand as those ships would then likely transit around the Cape of Good Hope, adding an additional 20-25 days transit time.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1/1/

2016

2/1/

2016

3/1/

2016

4/1/

2016

5/1/

2016

6/1/

2016

7/1/

2016

8/1/

2016

9/1/

2016

10/1

/201

6

11/1

/201

6

12/1

/201

6

1/1/

2017

2/1/

2017

3/1/

2017

4/1/

2017

5/1/

2017

6/1/

2017

7/1/

2017

8/1/

2017

9/1/

2017

10/1

/201

7

11/1

/201

7

12/1

/201

7

Baltic TCE/Day Baltic TCE/Day (4 week trailing avg.)

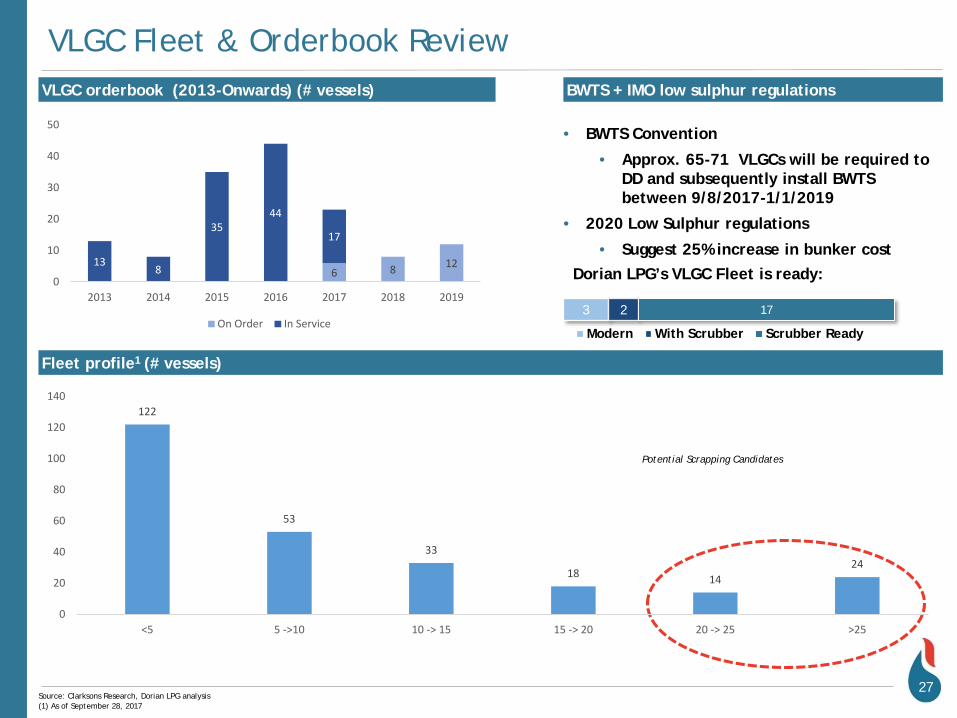

VLGC Fleet & Orderbook ReviewVLGC orderbook (2013-Onwards) (# vessels)

27Source: Clarksons Research, Dorian LPG analysis

Fleet profile1 (# vessels)

3 2 17

Modern With Scrubber Scrubber Ready

BWTS + IMO low sulphur regulations

• BWTS Convention

• Approx. 65-71 VLGCs will be required to DD and subsequently install BWTS between 9/8/2017-1/1/2019

• 2020 Low Sulphur regulations

• Suggest 25% increase in bunker costDorian LPG’s VLGC Fleet is ready:

Potential Scrapping Candidates

122

53

33

18 1424

0

20

40

60

80

100

120

140

<5 5 ->10 10 -> 15 15 -> 20 20 -> 25 >25

6 8 12138

3544

17

0

10

20

30

40

50

2013 2014 2015 2016 2017 2018 2019

On Order In Service

(1) As of September 28, 2017

Financials

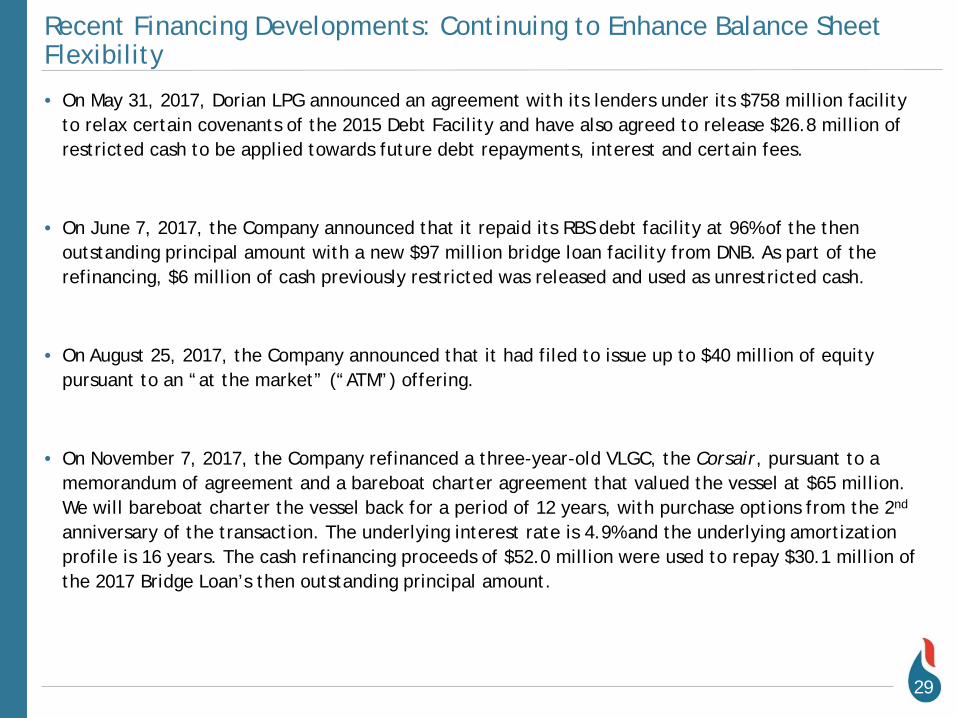

Recent Financing Developments: Continuing to Enhance Balance Sheet Flexibility

29

• On May 31, 2017, Dorian LPG announced an agreement with its lenders under its $758 million facility to relax certain covenants of the 2015 Debt Facility and have also agreed to release $26.8 million of restricted cash to be applied towards future debt repayments, interest and certain fees.

• On June 7, 2017, the Company announced that it repaid its RBS debt facility at 96% of the then outstanding principal amount with a new $97 million bridge loan facility from DNB. As part of the refinancing, $6 million of cash previously restricted was released and used as unrestricted cash.

• On August 25, 2017, the Company announced that it had filed to issue up to $40 million of equity pursuant to an “at the market” (“ATM”) offering.

• On November 7, 2017, the Company refinanced a three-year-old VLGC, the Corsair, pursuant to a memorandum of agreement and a bareboat charter agreement that valued the vessel at $65 million. We will bareboat charter the vessel back for a period of 12 years, with purchase options from the 2nd

anniversary of the transaction. The underlying interest rate is 4.9% and the underlying amortization profile is 16 years. The cash refinancing proceeds of $52.0 million were used to repay $30.1 million of the 2017 Bridge Loan’s then outstanding principal amount.

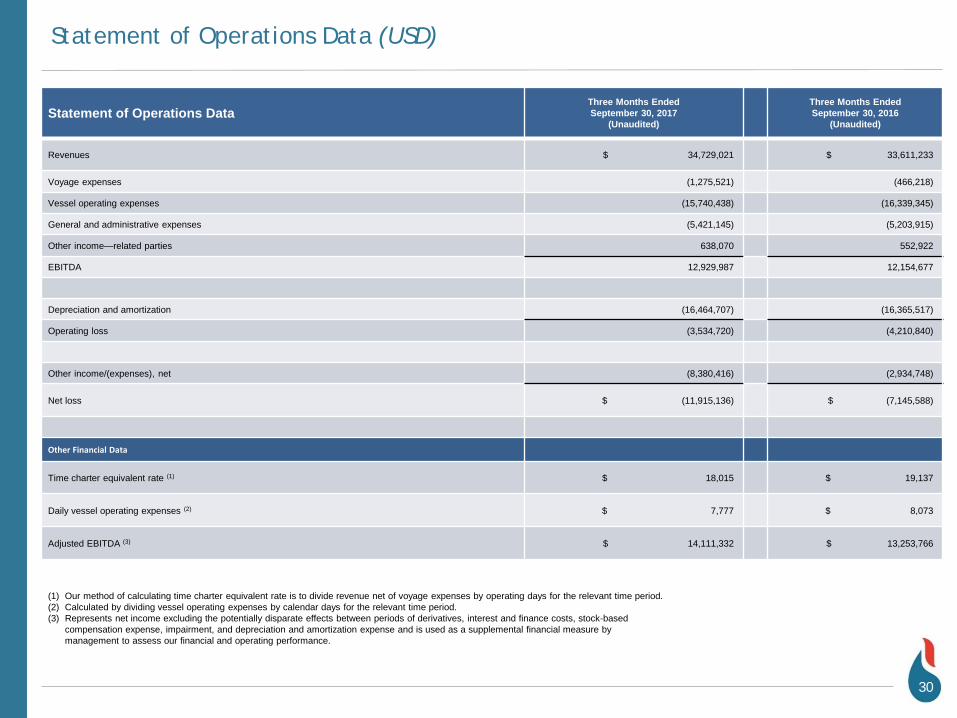

Statement of Operations Data (USD)

Statement of Operations DataThree Months Ended September 30, 2017

(Unaudited)

Three Months Ended September 30, 2016

(Unaudited)

Revenues $ 34,729,021 $ 33,611,233

Voyage expenses (1,275,521) (466,218)

Vessel operating expenses (15,740,438) (16,339,345)

General and administrative expenses (5,421,145) (5,203,915)

Other income—related parties 638,070 552,922

EBITDA 12,929,987 12,154,677

Depreciation and amortization (16,464,707) (16,365,517)

Operating loss (3,534,720) (4,210,840)

Other income/(expenses), net (8,380,416) (2,934,748)

Net loss $ (11,915,136) $ (7,145,588)

Other Financial Data

Time charter equivalent rate (1) $ 18,015 $ 19,137

Daily vessel operating expenses (2) $ 7,777 $ 8,073

Adjusted EBITDA (3) $ 14,111,332 $ 13,253,766

(1) Our method of calculating time charter equivalent rate is to divide revenue net of voyage expenses by operating days for the relevant time period.(2) Calculated by dividing vessel operating expenses by calendar days for the relevant time period.(3) Represents net income excluding the potentially disparate effects between periods of derivatives, interest and finance costs, stock-based

compensation expense, impairment, and depreciation and amortization expense and is used as a supplemental financial measure by management to assess our financial and operating performance.

30

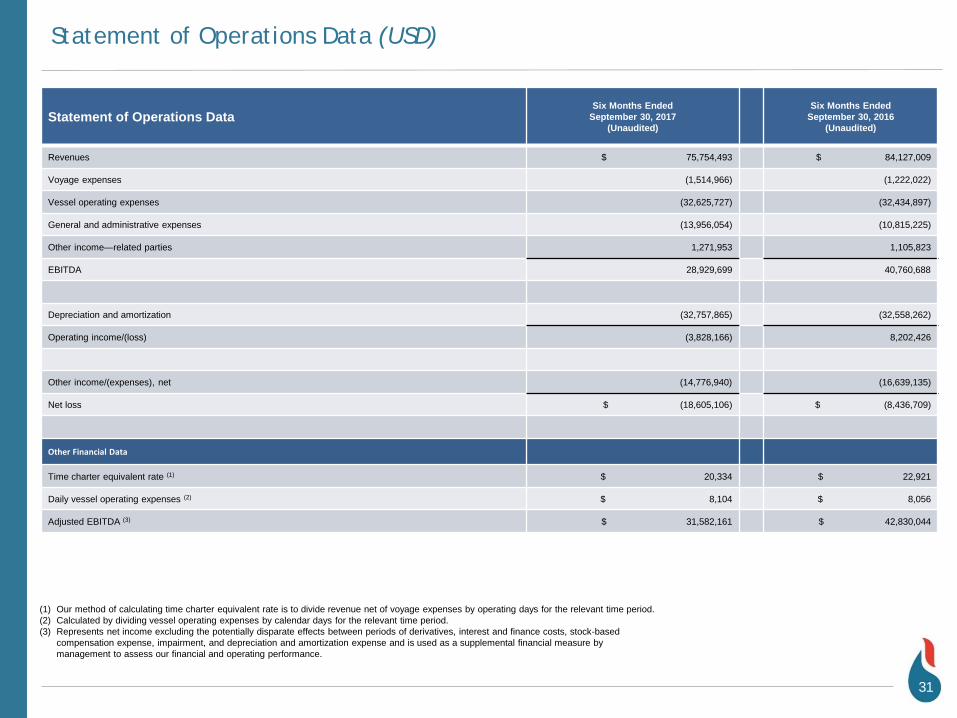

Statement of Operations Data (USD)

Statement of Operations DataSix Months Ended

September 30, 2017(Unaudited)

Six Months Ended September 30, 2016

(Unaudited)

Revenues $ 75,754,493 $ 84,127,009

Voyage expenses (1,514,966) (1,222,022)

Vessel operating expenses (32,625,727) (32,434,897)

General and administrative expenses (13,956,054) (10,815,225)

Other income—related parties 1,271,953 1,105,823

EBITDA 28,929,699 40,760,688

Depreciation and amortization (32,757,865) (32,558,262)

Operating income/(loss) (3,828,166) 8,202,426

Other income/(expenses), net (14,776,940) (16,639,135)

Net loss $ (18,605,106) $ (8,436,709)

Other Financial Data

Time charter equivalent rate (1) $ 20,334 $ 22,921

Daily vessel operating expenses (2) $ 8,104 $ 8,056

Adjusted EBITDA (3) $ 31,582,161 $ 42,830,044

(1) Our method of calculating time charter equivalent rate is to divide revenue net of voyage expenses by operating days for the relevant time period.(2) Calculated by dividing vessel operating expenses by calendar days for the relevant time period.(3) Represents net income excluding the potentially disparate effects between periods of derivatives, interest and finance costs, stock-based

compensation expense, impairment, and depreciation and amortization expense and is used as a supplemental financial measure by management to assess our financial and operating performance.

31

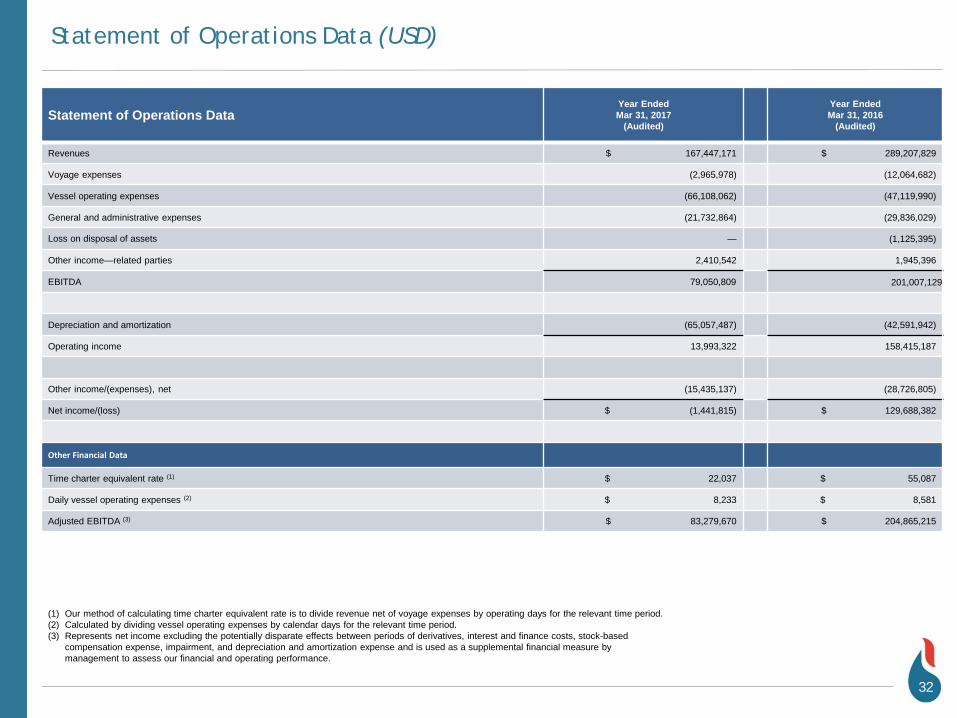

Statement of Operations Data (USD)

Statement of Operations DataYear Ended Mar 31, 2017

(Audited)

Year Ended Mar 31, 2016

(Audited)

Revenues $ 167,447,171 $ 289,207,829

Voyage expenses (2,965,978) (12,064,682)

Vessel operating expenses (66,108,062) (47,119,990)

General and administrative expenses (21,732,864) (29,836,029)

Loss on disposal of assets — (1,125,395)

Other income—related parties 2,410,542 1,945,396

EBITDA 79,050,809 201,007,129

Depreciation and amortization (65,057,487) (42,591,942)

Operating income 13,993,322 158,415,187

Other income/(expenses), net (15,435,137) (28,726,805)

Net income/(loss) $ (1,441,815) $ 129,688,382

Other Financial Data

Time charter equivalent rate (1) $ 22,037 $ 55,087

Daily vessel operating expenses (2) $ 8,233 $ 8,581

Adjusted EBITDA (3) $ 83,279,670 $ 204,865,215

(1) Our method of calculating time charter equivalent rate is to divide revenue net of voyage expenses by operating days for the relevant time period.(2) Calculated by dividing vessel operating expenses by calendar days for the relevant time period.(3) Represents net income excluding the potentially disparate effects between periods of derivatives, interest and finance costs, stock-based

compensation expense, impairment, and depreciation and amortization expense and is used as a supplemental financial measure by management to assess our financial and operating performance.

32

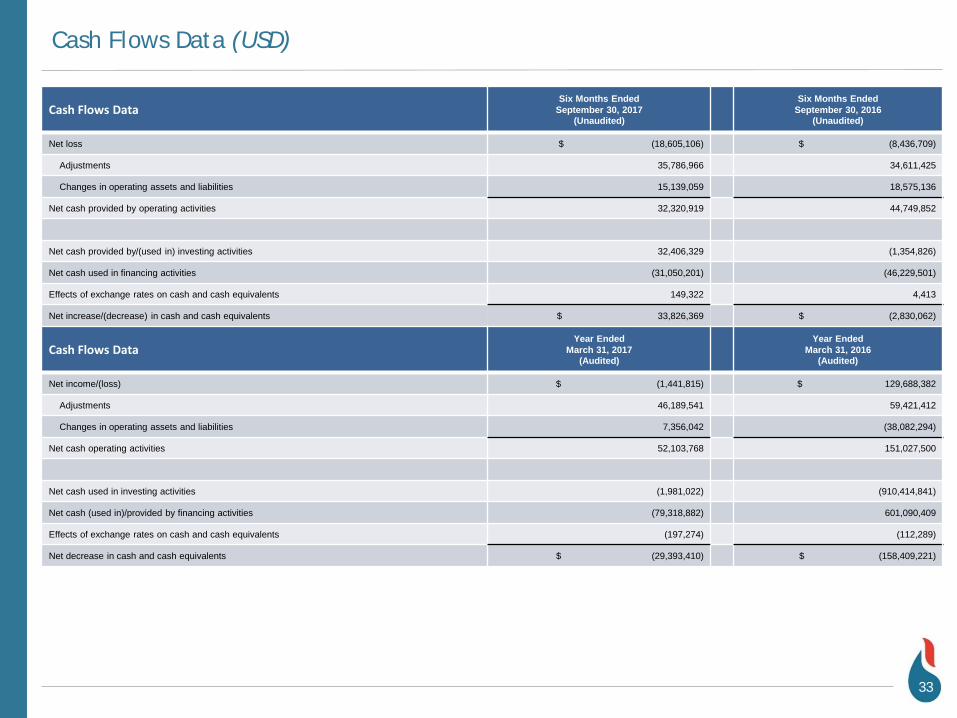

Cash Flows Data (USD)

Cash Flows DataSix Months Ended

September 30, 2017(Unaudited)

Six Months Ended September 30, 2016

(Unaudited)

Net loss $ (18,605,106) $ (8,436,709)

Adjustments 35,786,966 34,611,425

Changes in operating assets and liabilities 15,139,059 18,575,136

Net cash provided by operating activities 32,320,919 44,749,852

Net cash provided by/(used in) investing activities 32,406,329 (1,354,826)

Net cash used in financing activities (31,050,201) (46,229,501)

Effects of exchange rates on cash and cash equivalents 149,322 4,413

Net increase/(decrease) in cash and cash equivalents $ 33,826,369 $ (2,830,062)

Cash Flows DataYear Ended

March 31, 2017(Audited)

Year Ended March 31, 2016

(Audited)

Net income/(loss) $ (1,441,815) $ 129,688,382

Adjustments 46,189,541 59,421,412

Changes in operating assets and liabilities 7,356,042 (38,082,294)

Net cash operating activities 52,103,768 151,027,500

Net cash used in investing activities (1,981,022) (910,414,841)

Net cash (used in)/provided by financing activities (79,318,882) 601,090,409

Effects of exchange rates on cash and cash equivalents (197,274) (112,289)

Net decrease in cash and cash equivalents $ (29,393,410) $ (158,409,221)

33

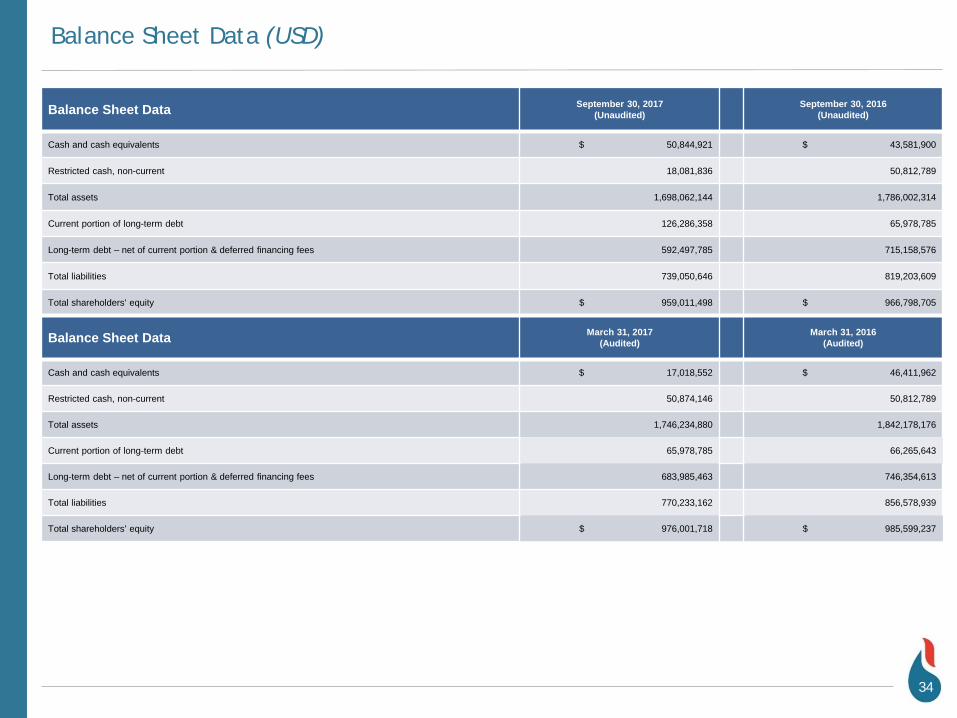

Balance Sheet Data (USD)

Balance Sheet Data September 30, 2017(Unaudited)

September 30, 2016(Unaudited)

Cash and cash equivalents $ 50,844,921 $ 43,581,900

Restricted cash, non-current 18,081,836 50,812,789

Total assets 1,698,062,144 1,786,002,314

Current portion of long-term debt 126,286,358 65,978,785

Long-term debt – net of current portion & deferred financing fees 592,497,785 715,158,576

Total liabilities 739,050,646 819,203,609

Total shareholders' equity $ 959,011,498 $ 966,798,705

Balance Sheet Data March 31, 2017(Audited)

March 31, 2016(Audited)

Cash and cash equivalents $ 17,018,552 $ 46,411,962

Restricted cash, non-current 50,874,146 50,812,789

Total assets 1,746,234,880 1,842,178,176

Current portion of long-term debt 65,978,785 66,265,643

Long-term debt – net of current portion & deferred financing fees 683,985,463 746,354,613

Total liabilities 770,233,162 856,578,939

Total shareholders' equity $ 976,001,718 $ 985,599,237

34

Our Mission is to arrange safe, reliable and trouble free transportation

Recommended