Does Private Equity have a role in Superannuation

Portfolios?

Kar Mei TangAVCAL

18th Melbourne Money & Finance Conference1 & 2 July 2013

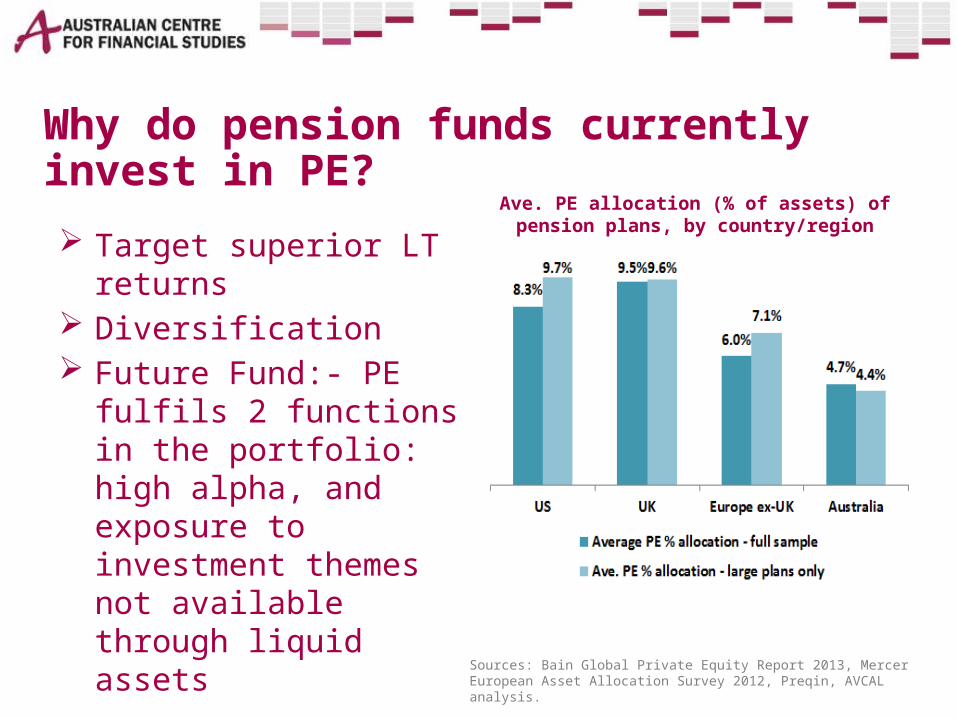

Why do pension funds currently invest in PE?

Target superior LT returns

Diversification Future Fund:- PE fulfils

2 functions in the portfolio: high alpha, and exposure to investment themes not available through liquid assets

Ave. PE allocation (% of assets) of pension plans, by country/region

Sources: Bain Global Private Equity Report 2013, Mercer European Asset Allocation Survey 2012, Preqin, AVCAL analysis.

Meeting the returns challenge

Source: Cambridge Associates, returns as of 31 Dec 2012. C|A Australian PE Index returns are net of management fees, expenses, and carried interest.

Australian PE vs ASX 300 returns (31 Dec 2012)

1 year 3 year 5 year 10 yearsC |A Australian PE Index (AUD terms) 6.77 8.19 3.96 9.67S&P/ASX 300 Acc. Index 19.74 2.8 -1.81 9.05S&P/ASX 300 Acc. PME 20.12 2.89 0.66 4.17

Source: Commonwealth Superannuation Corporation

-4

0

4

8

12

16

%

Manager selection is important too

Australian PE vs super returns

1-yr 3-yr 5-yr 10-yr returns returns returns returns

Sources: Cambridge Associates, Chant West, AVCAL analysis. Returns as of 31 Dec 2012. Super funds data for Growth options only. All returns are net of investment fees and tax.

-4

0

4

8

12

16

%

1-yr 3-yr 5-yr 10-yr returns returns returns returns

Australian Top 2-quartile PE vs Top 2-quartile super returns

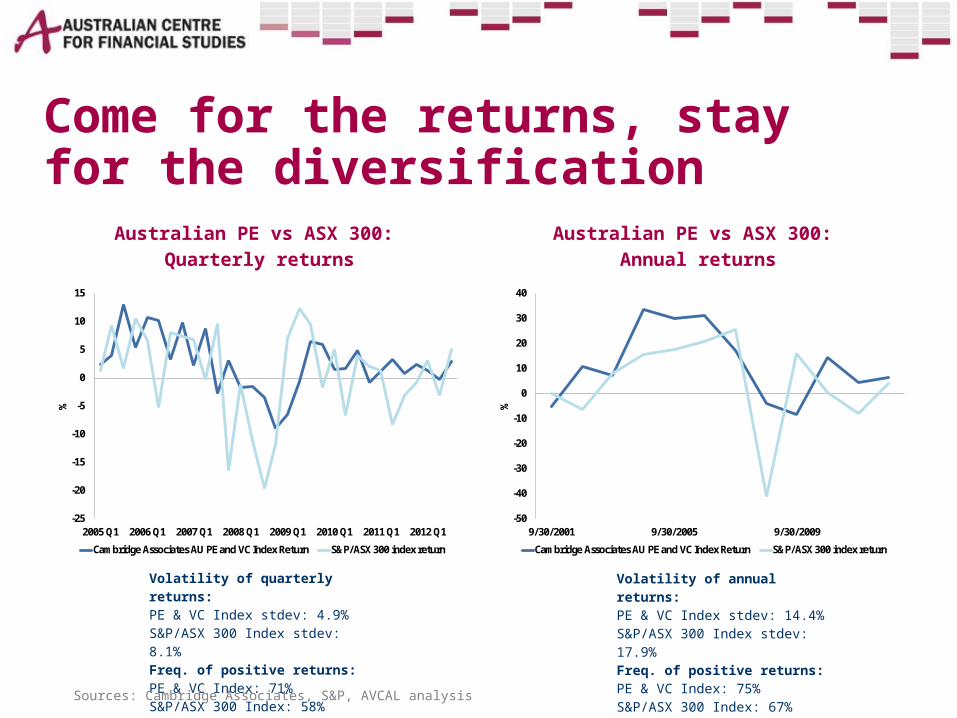

Come for the returns, stay for the diversification

-25

-20

-15

-10

-5

0

5

10

15

2005 Q1 2006 Q1 2007 Q1 2008 Q1 2009 Q1 2010 Q1 2011 Q1 2012 Q1

%

Cambridge Associates AU PE and VC Index Return S&P/ASX 300 index return

-50

-40

-30

-20

-10

0

10

20

30

40

9/30/2001 9/30/2005 9/30/2009

%

Cambridge Associates AU PE and VC Index Return S&P/ASX 300 index return

Volatility of quarterly returns:PE & VC Index stdev: 4.9% S&P/ASX 300 Index stdev: 8.1% Freq. of positive returns:PE & VC Index: 71% S&P/ASX 300 Index: 58%

Volatility of annual returns:PE & VC Index stdev: 14.4% S&P/ASX 300 Index stdev: 17.9% Freq. of positive returns:PE & VC Index: 75% S&P/ASX 300 Index: 67% Sources: Cambridge Associates, S&P, AVCAL analysis

Australian PE vs ASX 300: Quarterly returns

Australian PE vs ASX 300: Annual returns

But…

LiquidityFees

Liquidity

Managing liquidity risk: APRA guidance ASFA, FSC guidance Stronger Super reforms Internal controls

An allocation to illiquid assets does have a risk-adjusted return payoff Cummings & Ellis (2011) looks

at Australian DC investments in illiquid assets

Funds with moderate (below 30%) allocations to illiquid investments have higher risk-adjusted returns

Illiquid asset allocations linked to higher

Source: Cummings and Ellis (2011)

Fees MySuper trustees have “a

specific duty to deliver value for money as measured by long-term net returns, and to actively consider whether the fund has sufficient scale”

Delivering better LT net returns through Asset allocation decisions Cost reductions

Defined Contribution Inst. Investment Association (2013): Asset allocation, not fees, is

the key reason behind the DB/DC returns differential

Productive vs unproductive fee components?

PE investment managers generally earn their fees through higher returns Robinson and Sensoy (2012),

Cummings and Ellis (2011), Higson and Stucke (2012), Harris et al (2012), Acharya et al (2013)

Costs can be reduced through fee negotiations and economies of scale Dyck and Pomorski (2012) Cummings (2012)

Unintended consequences Are policy levers moving default super funds away from

optimal asset allocations? Dollar cost driving asset allocation decisions At some point: tradeoff between low cost and returns/diversification Myners Review (2001) Broadbent, Palumbo and Woodman (2006)

What are the choices available to members seeking more returns/diversification through super investment options? Fund performance tends to converge in narrow range in LT.

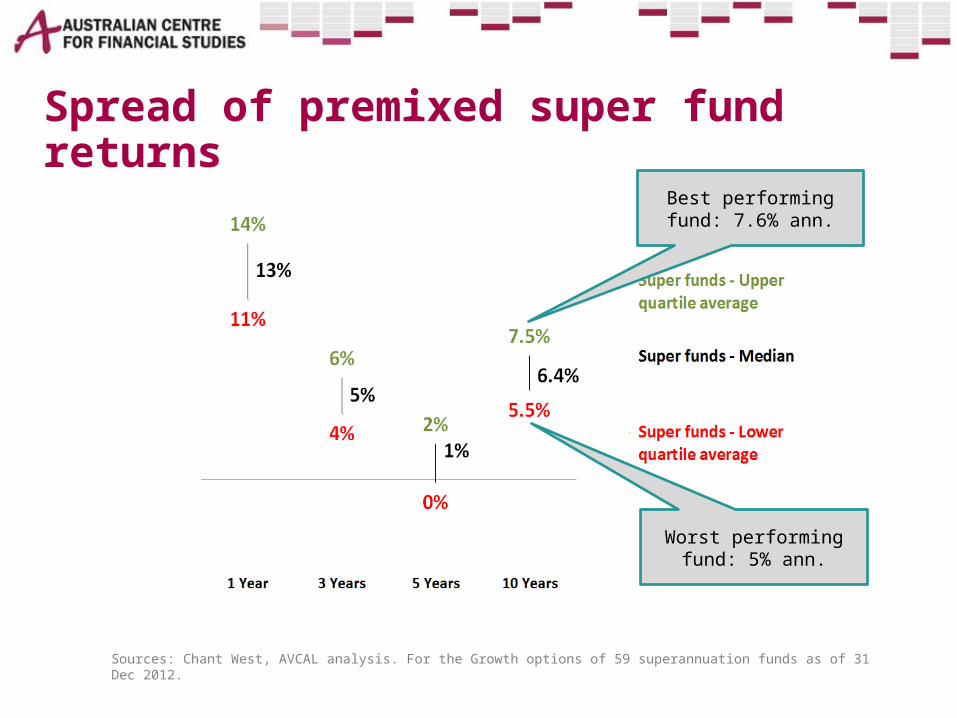

Spread of premixed super fund returns

Sources: Chant West, AVCAL analysis. For the Growth options of 59 superannuation funds as of 31 Dec 2012.

Best performing fund: 7.6% ann.

Worst performing fund: 5% ann.

Summary

Retirement savings adequacy a looming problem

PE has historically delivered, but good manager selection and a LT focus needed

Room for more diversity in: asset allocations options available to

members wanting access to high-performing asset classes through super

Further work: getting members more

engaged policy levers with

unintended LT consequences

look at global best practice: how mature pension PE programmes approach the asset class to deliver value

THANK YOU

Recommended