Solving Efeso © 2014

Closure – Summary Presentation

Cairo, February 2014

Developing Export Strategyfor

Egypt’s Engineering Industries

- 2 -EEC-EG Report Phase 5 Solving Efeso © 2014

Contents

Project OverviewProject Overview

Phase 1 – Thrust ProductsPhase 1 – Thrust Products

Phase 3 – Export Strategy DevelopmentPhase 3 – Export Strategy Development

Phase 2 – Thrust MarketsPhase 2 – Thrust Markets

Phase 4 – Implementation / Action PlanPhase 4 – Implementation / Action Plan

ConclusionConclusion

- 3 -EEC-EG Report Phase 5 Solving Efeso © 2014

Project Overview(Implemented Approach)

- 4 -EEC-EG Report Phase 5 Solving Efeso © 2014

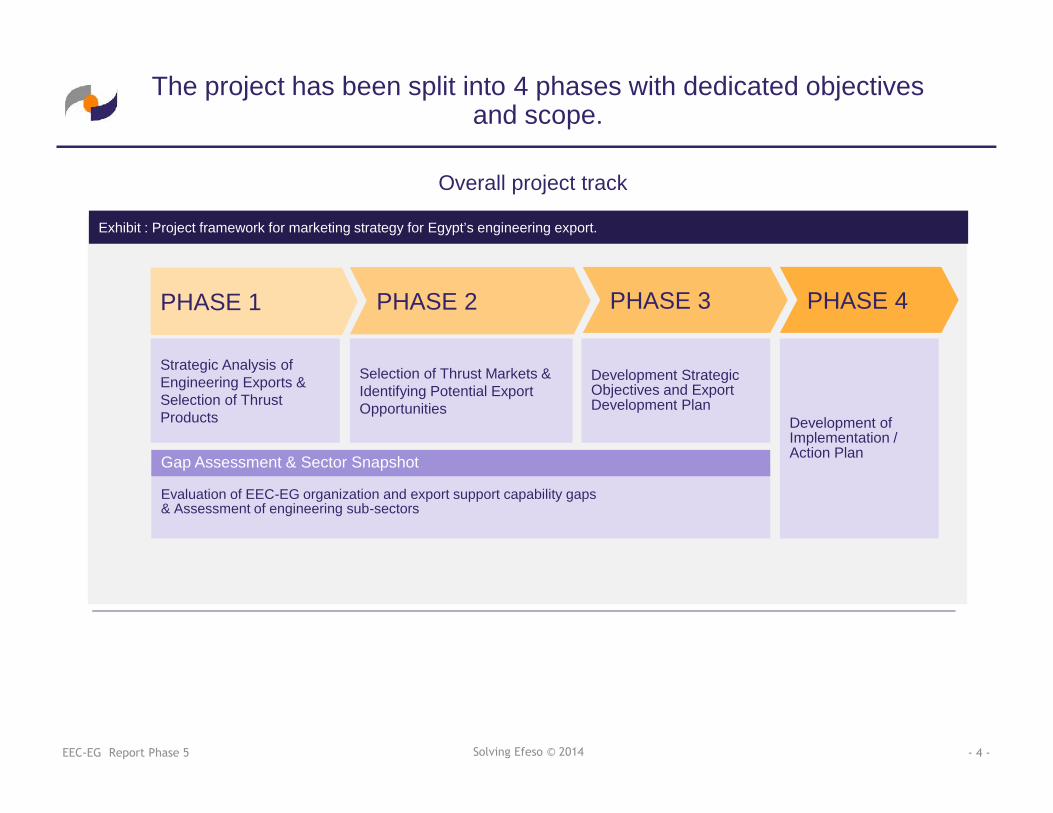

Exhibit : Project framework for marketing strategy for Egypt’s engineering export.

PHASE 1 PHASE 2 PHASE 3 PHASE 4

Strategic Analysis ofEngineering Exports &Selection of ThrustProducts

Selection of Thrust Markets &Identifying Potential ExportOpportunities

Development StrategicObjectives and ExportDevelopment Plan

Development ofImplementation /Action Plan

Overall project track

Evaluation of EEC-EG organization and export support capability gaps& Assessment of engineering sub-sectors

Gap Assessment & Sector Snapshot

The project has been split into 4 phases with dedicated objectivesand scope.

- 5 -EEC-EG Report Phase 4 Solving Efeso © 2013

PHASE 1 PHASE 2 PHASE 3 PHASE 4

Strategic Analysis ofEngineering Exports &

Selection of ThrustProducts

Selection of Thrust Markets &Identifying Potential Export

Opportunities

Development StrategicObjectives and Export

Development PlanDevelopment ofImplementation /

Action Plan

Where we are now

Evaluation of EEC-EG organization and export support capability gaps& Assessment of engineering sub-sectors

Gap Assessment & Sector Snapshot

PRO

GR

ESS

100%

Exhibit : Project framework for marketing strategy for Egypt’s engineering export & progress made to date.

100% project completion rate has been achieved

- 6 -EEC-EG Report Phase 5 Solving Efeso © 2014

Phase 1: Thrust Products

- 7 -EEC-EG Report Phase 2 Solving Efeso © 2013

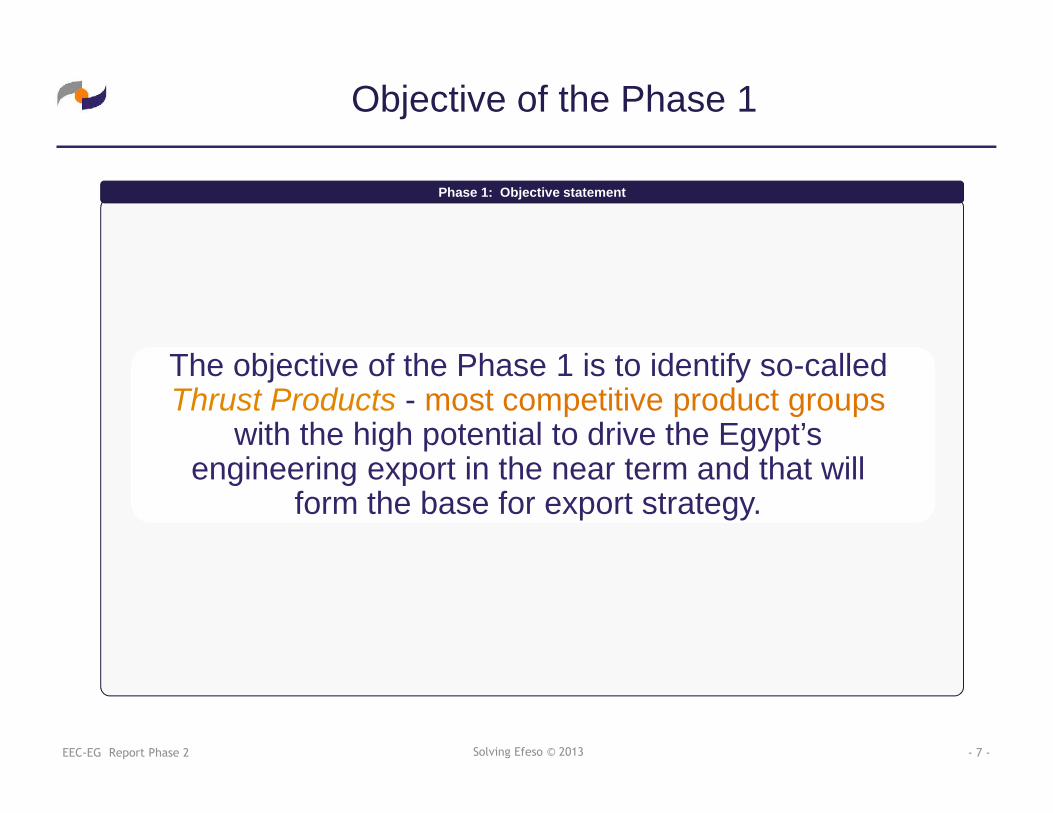

Objective of the Phase 1

The objective of the Phase 1 is to identify so-calledThrust Products - most competitive product groups

with the high potential to drive the Egypt’sengineering export in the near term and that will

form the base for export strategy.

Phase 1: Objective statement

- 8 -EEC-EG Report Phase 1 Solving Efeso © 2013

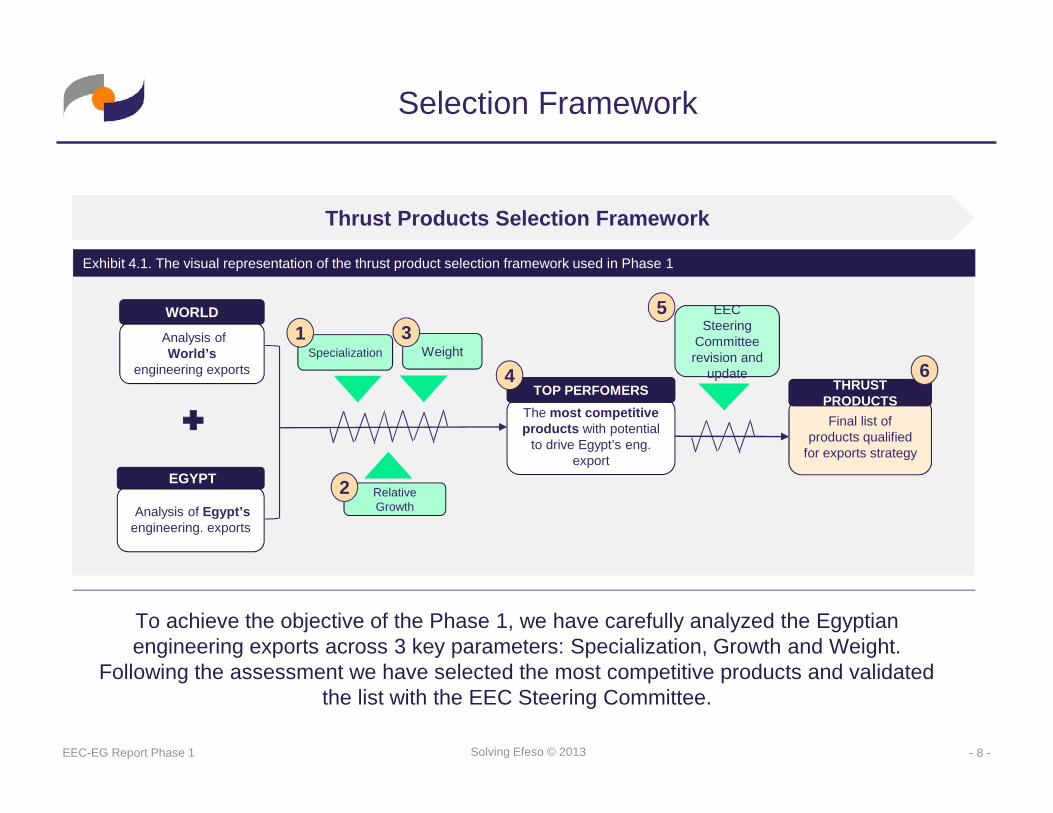

Thrust Products Selection Framework

Selection Framework

Analysis of Egypt’sengineering. exports

Analysis ofWorld’s

engineering exports

The most competitiveproducts with potential

to drive Egypt’s eng.export

Final list ofproducts qualified

for exports strategy

EGYPT

WORLD

TOP PERFOMERS THRUSTPRODUCTS

EECSteering

Committeerevision and

update

Exhibit 4.1. The visual representation of the thrust product selection framework used in Phase 1

4

5

Specialization

RelativeGrowth

Weight1

2

3

6

To achieve the objective of the Phase 1, we have carefully analyzed the Egyptianengineering exports across 3 key parameters: Specialization, Growth and Weight.

Following the assessment we have selected the most competitive products and validatedthe list with the EEC Steering Committee.

- 9 -EEC-EG Report Phase 1 Solving Efeso © 2013

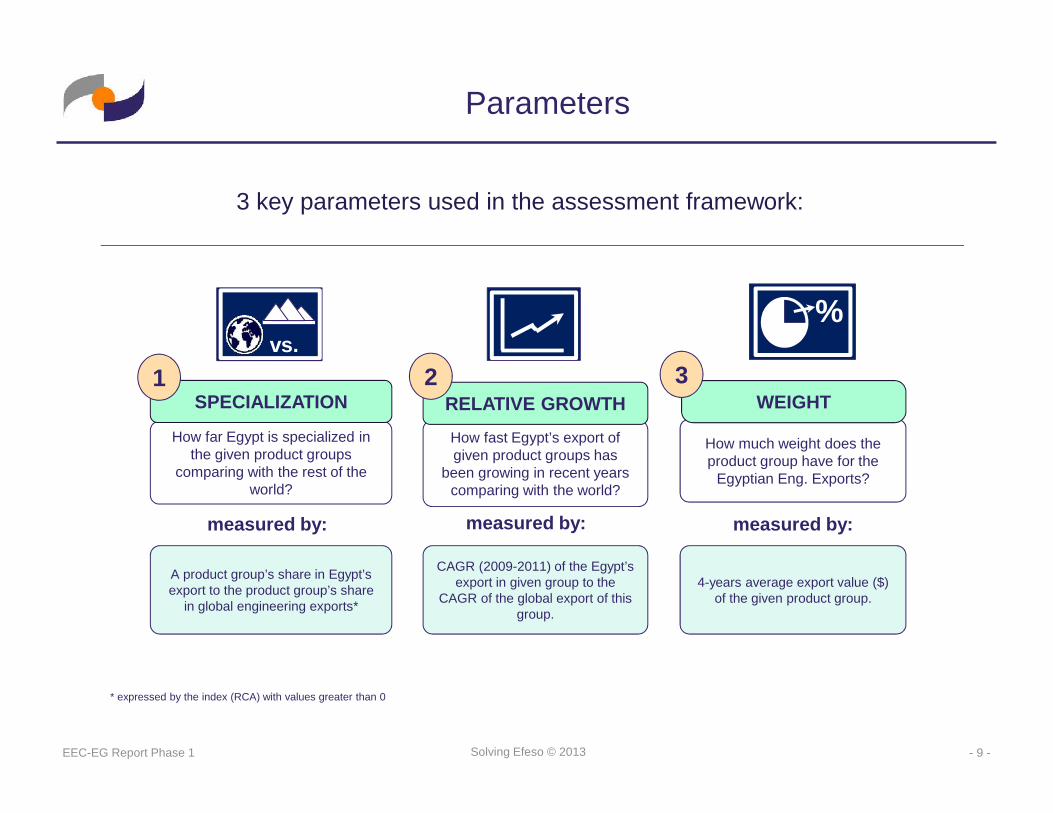

How much weight does theproduct group have for the

Egyptian Eng. Exports?

3 key parameters used in the assessment framework:

Parameters

WEIGHT

%vs.

3

How far Egypt is specialized inthe given product groups

comparing with the rest of theworld?

How fast Egypt’s export ofgiven product groups has

been growing in recent yearscomparing with the world?

measured by:

4-years average export value ($)of the given product group.

A product group’s share in Egypt’sexport to the product group’s share

in global engineering exports*

CAGR (2009-2011) of the Egypt’sexport in given group to the

CAGR of the global export of thisgroup.

measured by: measured by:

* expressed by the index (RCA) with values greater than 0

RELATIVE GROWTHSPECIALIZATION1 2

- 10 -EEC-EG Report Phase 1 Solving Efeso © 2013

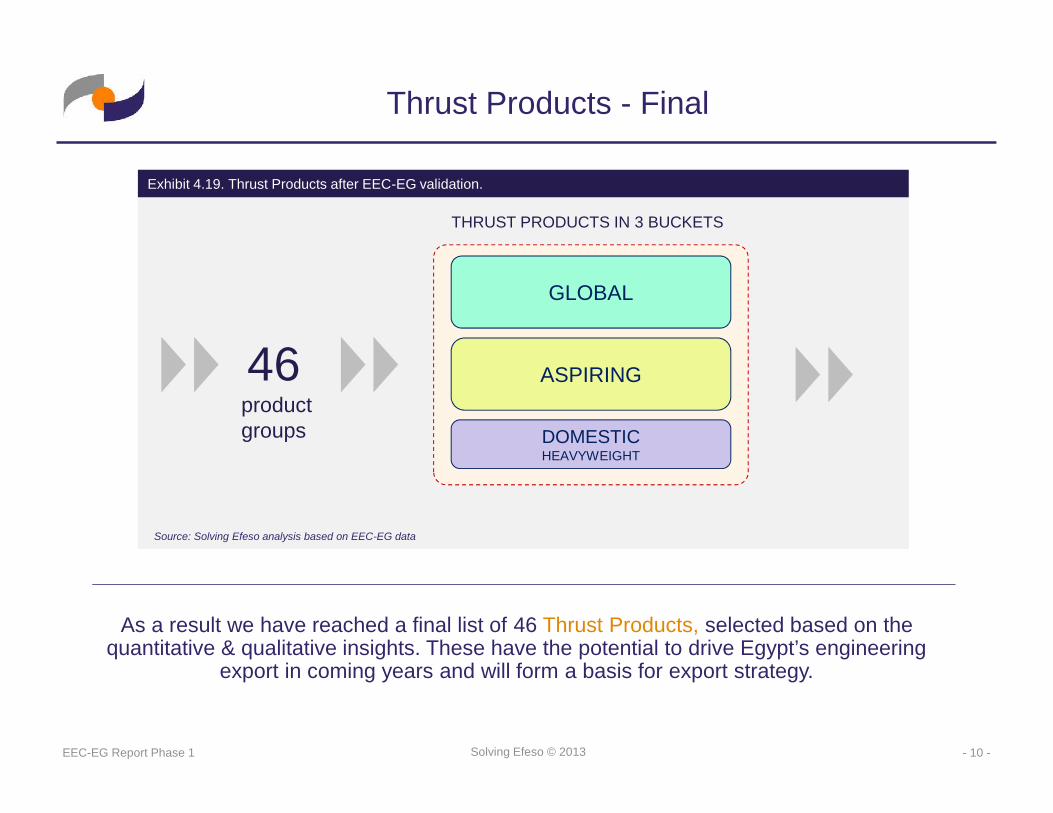

Thrust Products - Final

ASPIRING

GLOBAL

THRUST PRODUCTS IN 3 BUCKETS

Source: Solving Efeso analysis based on EEC-EG data

46productgroups

Exhibit 4.19. Thrust Products after EEC-EG validation.

DOMESTICHEAVYWEIGHT

As a result we have reached a final list of 46 Thrust Products, selected based on thequantitative & qualitative insights. These have the potential to drive Egypt’s engineering

export in coming years and will form a basis for export strategy.

- 11 -EEC-EG Report Phase 1 Solving Efeso © 2013

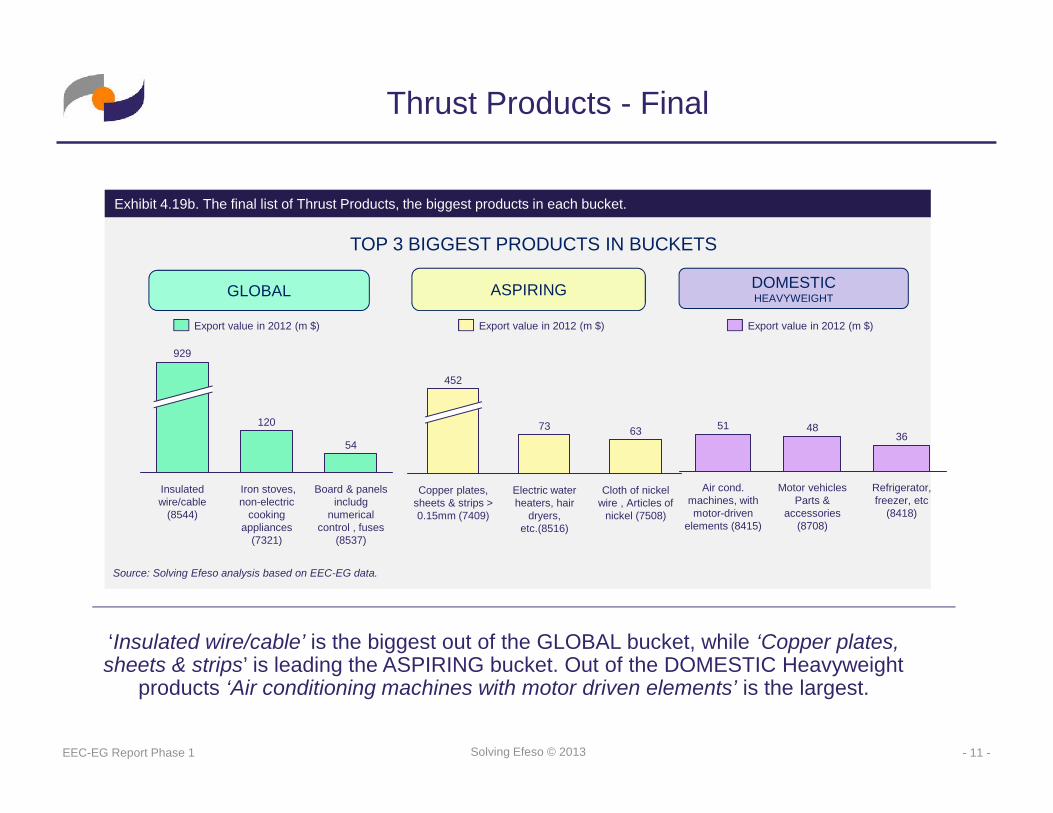

Exhibit 4.19b. The final list of Thrust Products, the biggest products in each bucket.

Source: Solving Efeso analysis based on EEC-EG data.

Board & panelsincludg

numericalcontrol , fuses

(8537)

54

Iron stoves,non-electric

cookingappliances

(7321)

120

Insulatedwire/cable

(8544)

929

Cloth of nickelwire , Articles of

nickel (7508)

63

Electric waterheaters, hair

dryers,etc.(8516)

73

Copper plates,sheets & strips >0.15mm (7409)

452

Refrigerator,freezer, etc

(8418)

36

Motor vehiclesParts &

accessories(8708)

48

Air cond.machines, withmotor-driven

elements (8415)

51

ASPIRINGGLOBAL DOMESTICHEAVYWEIGHT

TOP 3 BIGGEST PRODUCTS IN BUCKETS

Export value in 2012 (m $) Export value in 2012 (m $)Export value in 2012 (m $)

Thrust Products - Final

‘Insulated wire/cable’ is the biggest out of the GLOBAL bucket, while ‘Copper plates,sheets & strips’ is leading the ASPIRING bucket. Out of the DOMESTIC Heavyweight

products ‘Air conditioning machines with motor driven elements’ is the largest.

- 12 -EEC-EG Report Phase 1 Solving Efeso © 2013

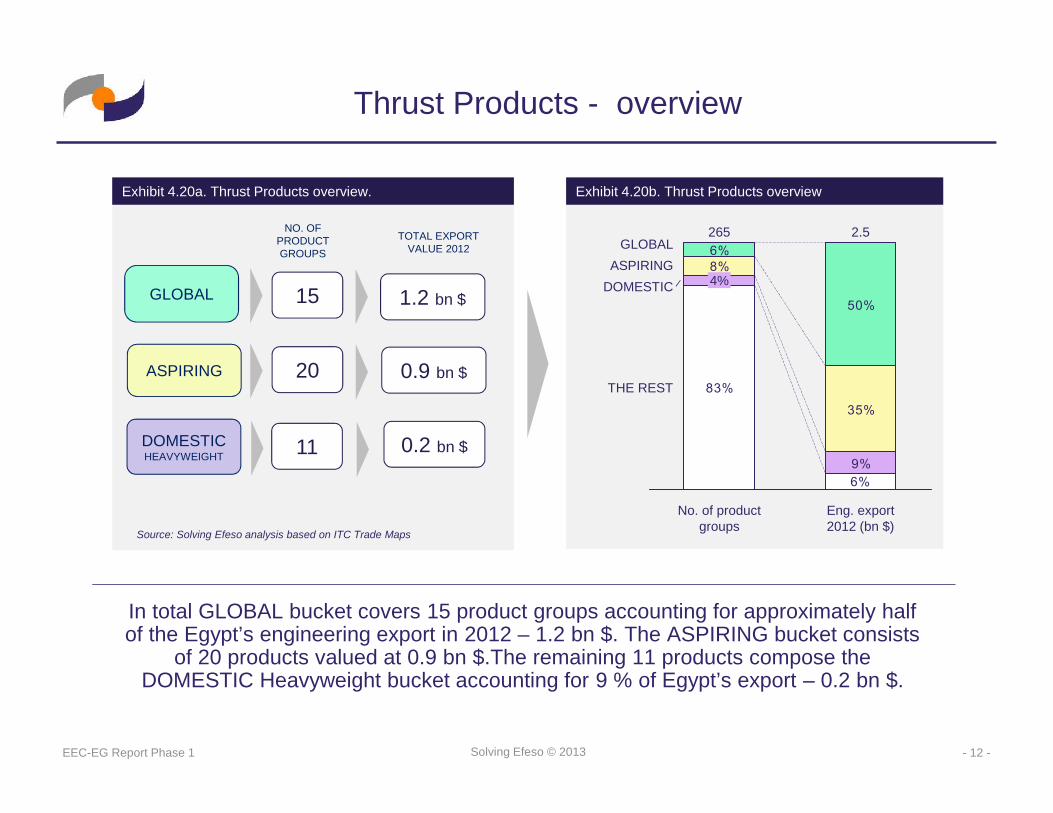

In total GLOBAL bucket covers 15 product groups accounting for approximately halfof the Egypt’s engineering export in 2012 – 1.2 bn $. The ASPIRING bucket consists

of 20 products valued at 0.9 bn $.The remaining 11 products compose theDOMESTIC Heavyweight bucket accounting for 9 % of Egypt’s export – 0.2 bn $.

Thrust Products - overview

ASPIRING

GLOBAL

DOMESTICHEAVYWEIGHT

Source: Solving Efeso analysis based on ITC Trade Maps

Exhibit 4.20a. Thrust Products overview.

NO. OFPRODUCTGROUPS

TOTAL EXPORTVALUE 2012

15

20

11

1.2 bn $

0.9 bn $

0.2 bn $

Exhibit 4.20b. Thrust Products overview

83%

8%

35%

6%

50%

6%9%

THE REST

DOMESTICASPIRING

GLOBAL

Eng. export2012 (bn $)

2.5

No. of productgroups

265

4%

- 13 -EEC-EG Report Phase 3 Solving Efeso © 2013

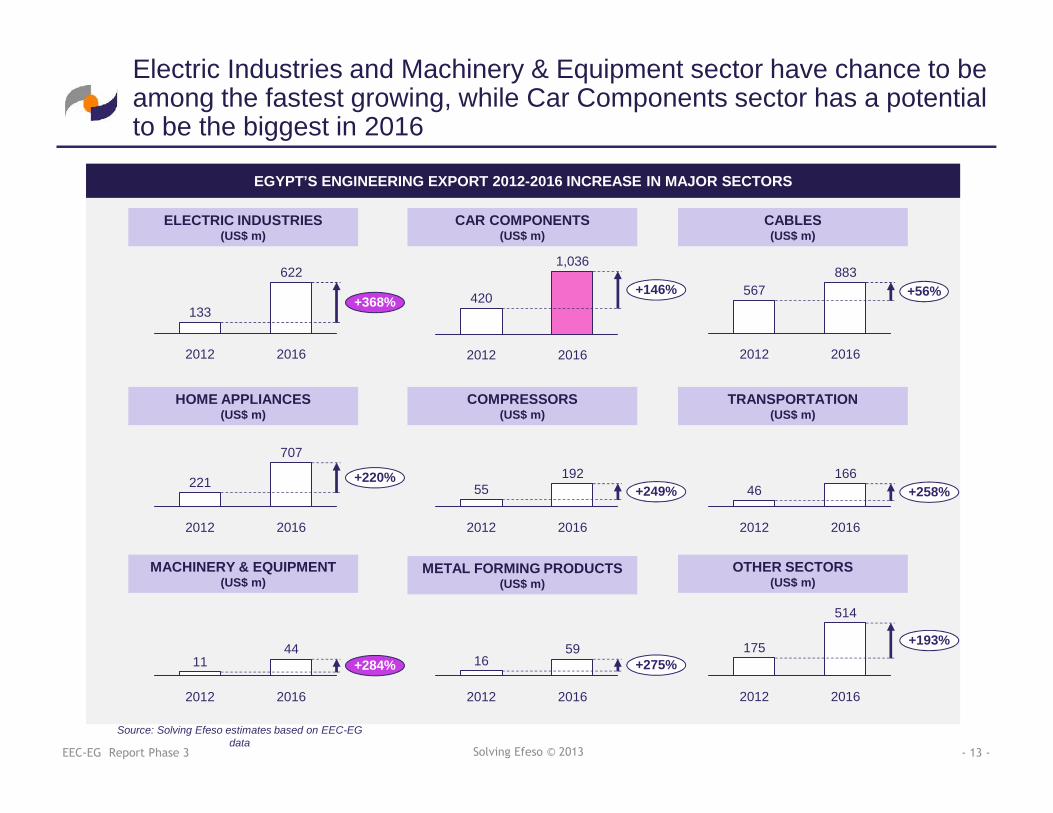

Electric Industries and Machinery & Equipment sector have chance to beamong the fastest growing, while Car Components sector has a potentialto be the biggest in 2016

EGYPT’S ENGINEERING EXPORT 2012-2016 INCREASE IN MAJOR SECTORS

Source: Solving Efeso estimates based on EEC-EGdata

622

+368%

20162012

133

ELECTRIC INDUSTRIES(US$ m)

1,036

+146%

20162012

420

CAR COMPONENTS(US$ m)

883+56%

20162012

567

CABLES(US$ m)

707

+220%

20162012

221

HOME APPLIANCES(US$ m)

192+249%

20162012

55

COMPRESSORS(US$ m)

166+258%

20162012

46

TRANSPORTATION(US$ m)

44+284%

20162012

11

MACHINERY & EQUIPMENT(US$ m)

59+275%

20162012

16

METAL FORMING PRODUCTS(US$ m)

514

+193%

20162012

175

OTHER SECTORS(US$ m)

- 14 -EEC-EG Report Phase 3 Solving Efeso © 2013

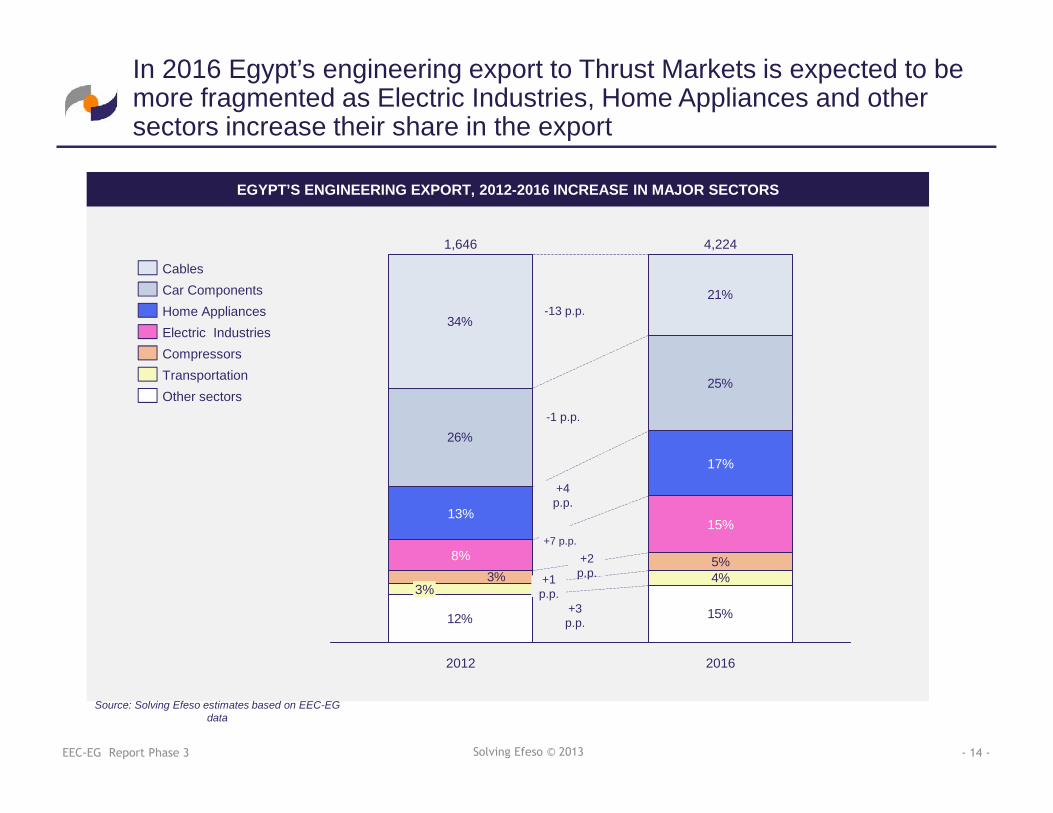

In 2016 Egypt’s engineering export to Thrust Markets is expected to bemore fragmented as Electric Industries, Home Appliances and othersectors increase their share in the export

EGYPT’S ENGINEERING EXPORT, 2012-2016 INCREASE IN MAJOR SECTORS

Source: Solving Efeso estimates based on EEC-EGdata

12% 15%

5%

26%

25%

34%

21%

4%3%

2012 2016

4,224

15%

17%

1,646

3%

8%

13%

Other sectorsTransportation

Home AppliancesElectric Industries

Car Components

Compressors

Cables

-13 p.p.

-1 p.p.

+4p.p.

+7 p.p.

+3p.p.

+2p.p.+1

p.p.

- 15 -EEC-EG Report Phase 5 Solving Efeso © 2014

Phase 2: Thrust Markets

- 16 -EEC-EG Report Phase 2 Solving Efeso © 2013

Objective of the Phase 2

The main objective of Phase 2 is to identify ThrustMarkets - the most attractive markets for selected

Thrust Products that will form the basis for astrategy for Egypt’s engineering export.

Phase 2 Objective statement

- 17 -EEC-EG Report Phase 2 Solving Efeso © 2013

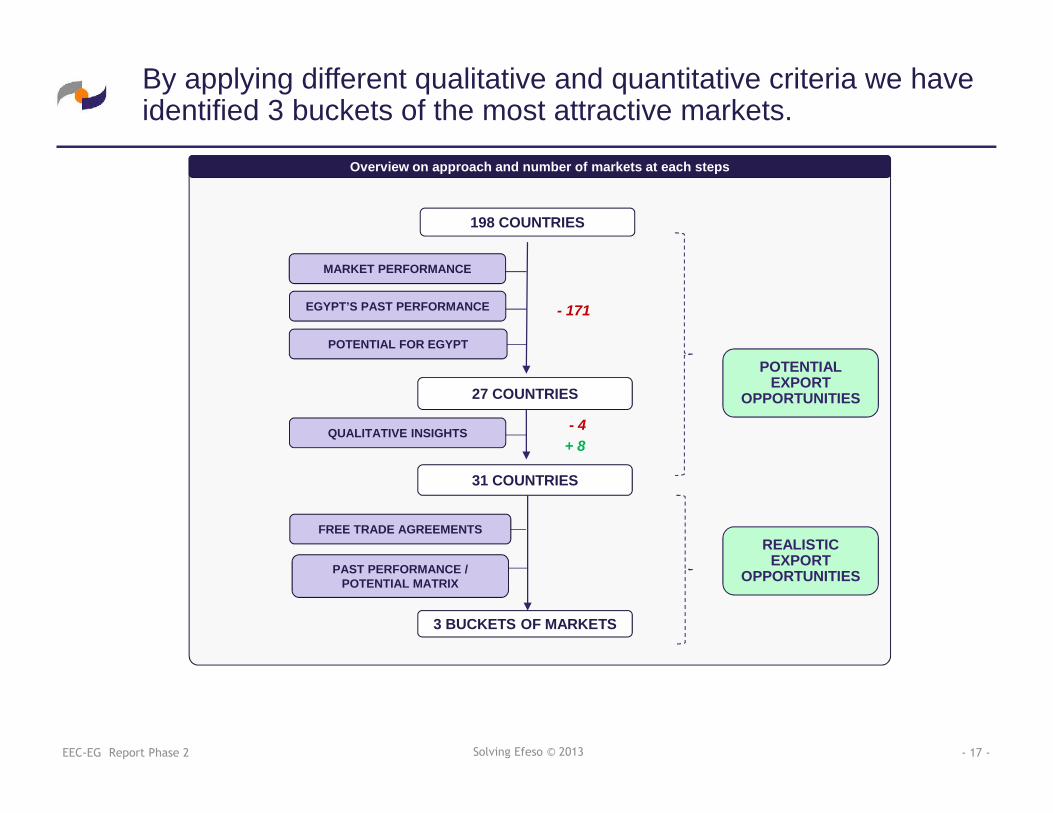

198 COUNTRIES

31 COUNTRIES

Overview on approach and number of markets at each steps

EGYPT’S PAST PERFORMANCE

POTENTIAL FOR EGYPT

QUALITATIVE INSIGHTS

FREE TRADE AGREEMENTS

27 COUNTRIES

- 171

- 4+ 8

3 BUCKETS OF MARKETS

POTENTIALEXPORT

OPPORTUNITIES

REALISTICEXPORT

OPPORTUNITIES

MARKET PERFORMANCE

PAST PERFORMANCE /POTENTIAL MATRIX

By applying different qualitative and quantitative criteria we haveidentified 3 buckets of the most attractive markets.

- 18 -EEC-EG Report Phase 2 Solving Efeso © 2013

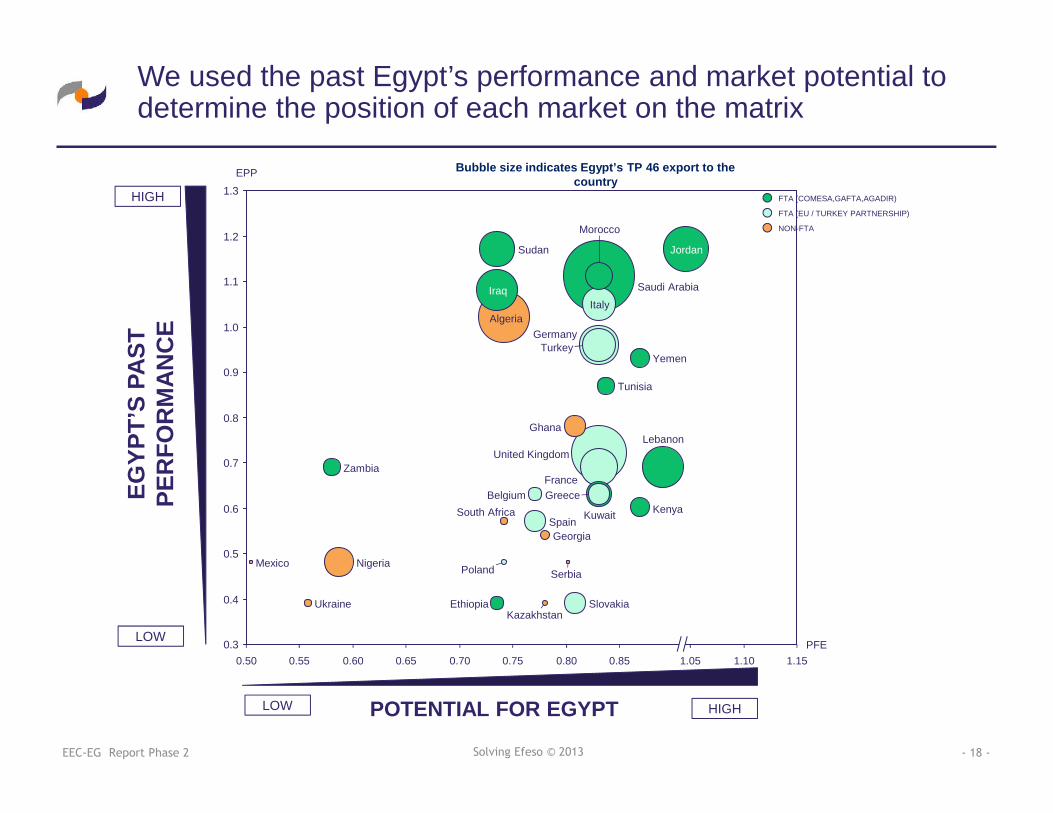

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3EPP

Slovakia

Poland

Kenya

Ghana

Spain Kuwait

GreeceSouth Africa

Lebanon

Belgium

Yemen

Sudan

Iraq

France

United Kingdom

Algeria

Tunisia

TurkeyGermany

Italy

Morocco

Saudi Arabia

Jordan

0.650.600.550.50

EthiopiaUkraine

Zambia

Nigeria

Kazakhstan

Mexico

Georgia

Serbia

PFE1.151.101.050.850.800.750.70

HIGH

HIGHLOW

LOW

POTENTIAL FOR EGYPT

EGYP

T’S

PAST

PER

FOR

MAN

CE

NON-FTA

FTA (EU / TURKEY PARTNERSHIP)

FTA (COMESA,GAFTA,AGADIR)

Bubble size indicates Egypt’s TP 46 export to thecountry

We used the past Egypt’s performance and market potential todetermine the position of each market on the matrix

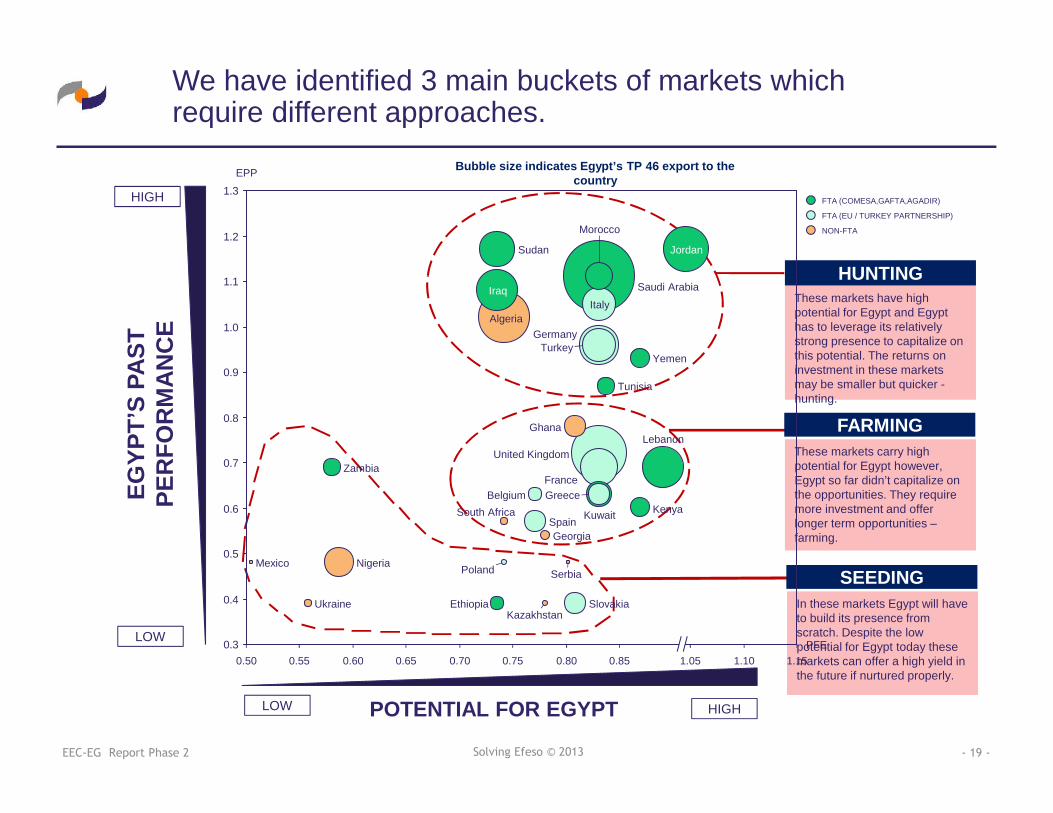

- 19 -EEC-EG Report Phase 2 Solving Efeso © 2013

HIGH

HIGHLOW

LOW

POTENTIAL FOR EGYPT

EGYP

T’S

PAST

PER

FOR

MAN

CE

Bubble size indicates Egypt’s TP 46 export to thecountry

We have identified 3 main buckets of markets whichrequire different approaches.

These markets have highpotential for Egypt and Egypthas to leverage its relativelystrong presence to capitalize onthis potential. The returns oninvestment in these marketsmay be smaller but quicker -hunting.

These markets carry highpotential for Egypt however,Egypt so far didn’t capitalize onthe opportunities. They requiremore investment and offerlonger term opportunities –farming.

FARMING

HUNTING

In these markets Egypt will haveto build its presence fromscratch. Despite the lowpotential for Egypt today thesemarkets can offer a high yield inthe future if nurtured properly.

SEEDING

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.151.101.050.850.800.700.650.60 0.750.550.50

EthiopiaUkraine

Zambia

Nigeria

Kazakhstan

Mexico

Georgia

Serbia

Slovakia

Poland

Kenya

Ghana

Spain Kuwait

GreeceSouth Africa

EPP

Belgium

Yemen

Sudan

Iraq

France

United Kingdom

Algeria

Lebanon

TurkeyGermany

Italy

Morocco

Saudi Arabia

Jordan

PFE

Tunisia

NON-FTA

FTA (EU / TURKEY PARTNERSHIP)

FTA (COMESA,GAFTA,AGADIR)

- 20 -EEC-EG Report Phase 2 Solving Efeso © 2013

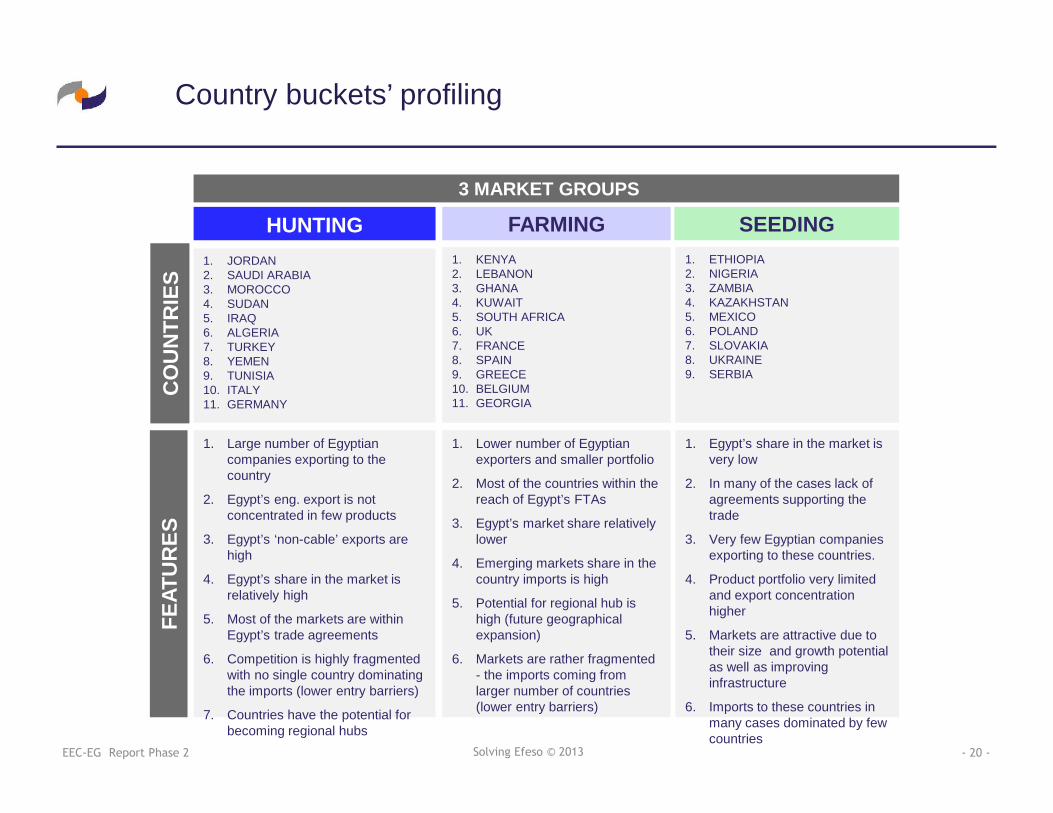

Country buckets’ profiling

FARMINGHUNTING SEEDING

CO

UN

TRIE

SFE

ATU

RES

1. JORDAN2. SAUDI ARABIA3. MOROCCO4. SUDAN5. IRAQ6. ALGERIA7. TURKEY8. YEMEN9. TUNISIA10. ITALY11. GERMANY

1. KENYA2. LEBANON3. GHANA4. KUWAIT5. SOUTH AFRICA6. UK7. FRANCE8. SPAIN9. GREECE10. BELGIUM11. GEORGIA

1. ETHIOPIA2. NIGERIA3. ZAMBIA4. KAZAKHSTAN5. MEXICO6. POLAND7. SLOVAKIA8. UKRAINE9. SERBIA

1. Large number of Egyptiancompanies exporting to thecountry

2. Egypt’s eng. export is notconcentrated in few products

3. Egypt’s ‘non-cable’ exports arehigh

4. Egypt’s share in the market isrelatively high

5. Most of the markets are withinEgypt’s trade agreements

6. Competition is highly fragmentedwith no single country dominatingthe imports (lower entry barriers)

7. Countries have the potential forbecoming regional hubs

1. Lower number of Egyptianexporters and smaller portfolio

2. Most of the countries within thereach of Egypt’s FTAs

3. Egypt’s market share relativelylower

4. Emerging markets share in thecountry imports is high

5. Potential for regional hub ishigh (future geographicalexpansion)

6. Markets are rather fragmented- the imports coming fromlarger number of countries(lower entry barriers)

1. Egypt’s share in the market isvery low

2. In many of the cases lack ofagreements supporting thetrade

3. Very few Egyptian companiesexporting to these countries.

4. Product portfolio very limitedand export concentrationhigher

5. Markets are attractive due totheir size and growth potentialas well as improvinginfrastructure

6. Imports to these countries inmany cases dominated by fewcountries

3 MARKET GROUPS

- 21 -EEC-EG Report Phase 2 Solving Efeso © 2013

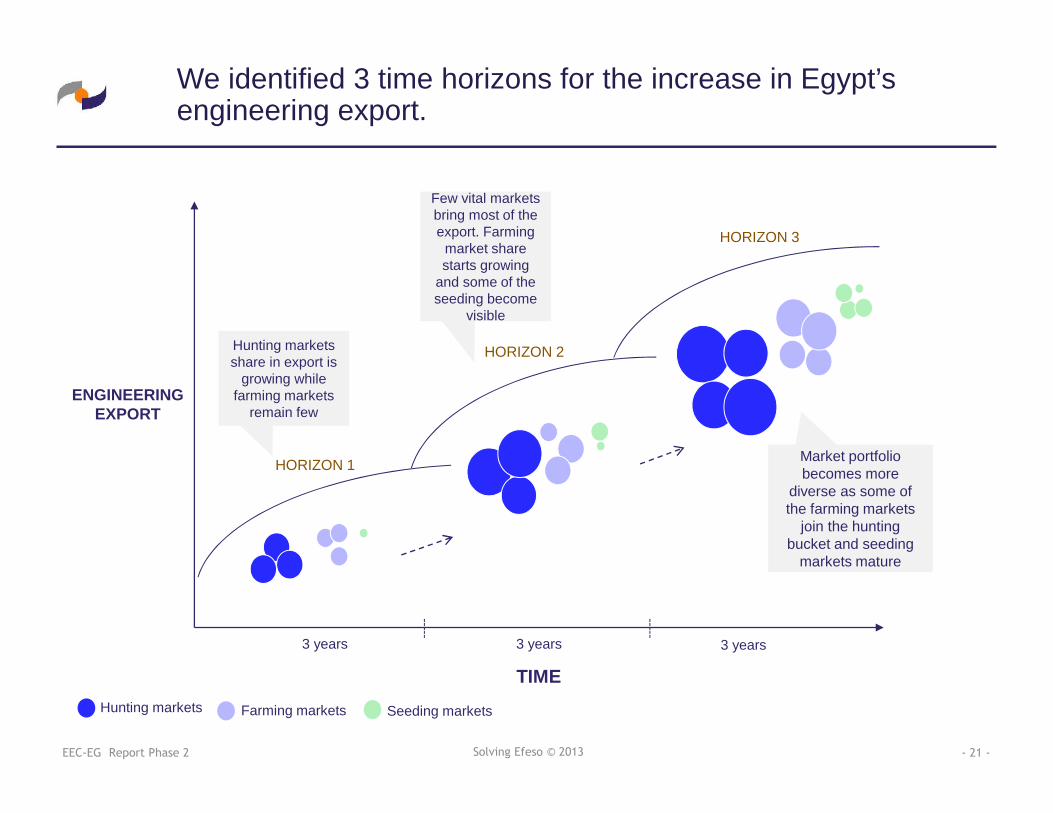

We identified 3 time horizons for the increase in Egypt’sengineering export.

TIME

ENGINEERINGEXPORT

3 years 3 years 3 years

HORIZON 1

HORIZON 2

HORIZON 3

Hunting markets Farming markets Seeding markets

Hunting marketsshare in export is

growing whilefarming markets

remain few

Few vital marketsbring most of theexport. Farming

market sharestarts growing

and some of theseeding become

visible

Market portfoliobecomes more

diverse as some ofthe farming markets

join the huntingbucket and seeding

markets mature

- 22 -EEC-EG Report Phase 2 Solving Efeso © 2013

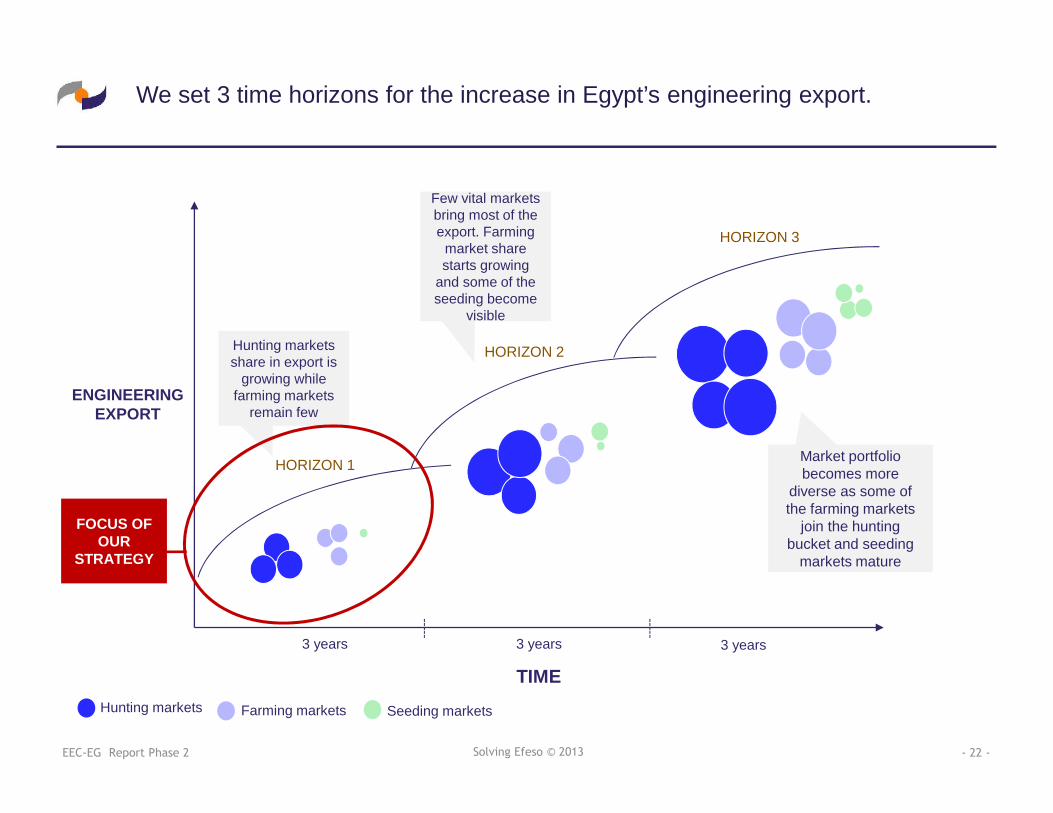

We set 3 time horizons for the increase in Egypt’s engineering export.

TIME

ENGINEERINGEXPORT

3 years 3 years 3 years

HORIZON 1

HORIZON 2

HORIZON 3

Hunting markets Farming markets Seeding markets

Hunting marketsshare in export is

growing whilefarming markets

remain few

Few vital marketsbring most of theexport. Farming

market sharestarts growing

and some of theseeding become

visible

Market portfoliobecomes more

diverse as some ofthe farming markets

join the huntingbucket and seeding

markets mature

FOCUS OFOUR

STRATEGY

- 23 -Solving Efeso © 2013

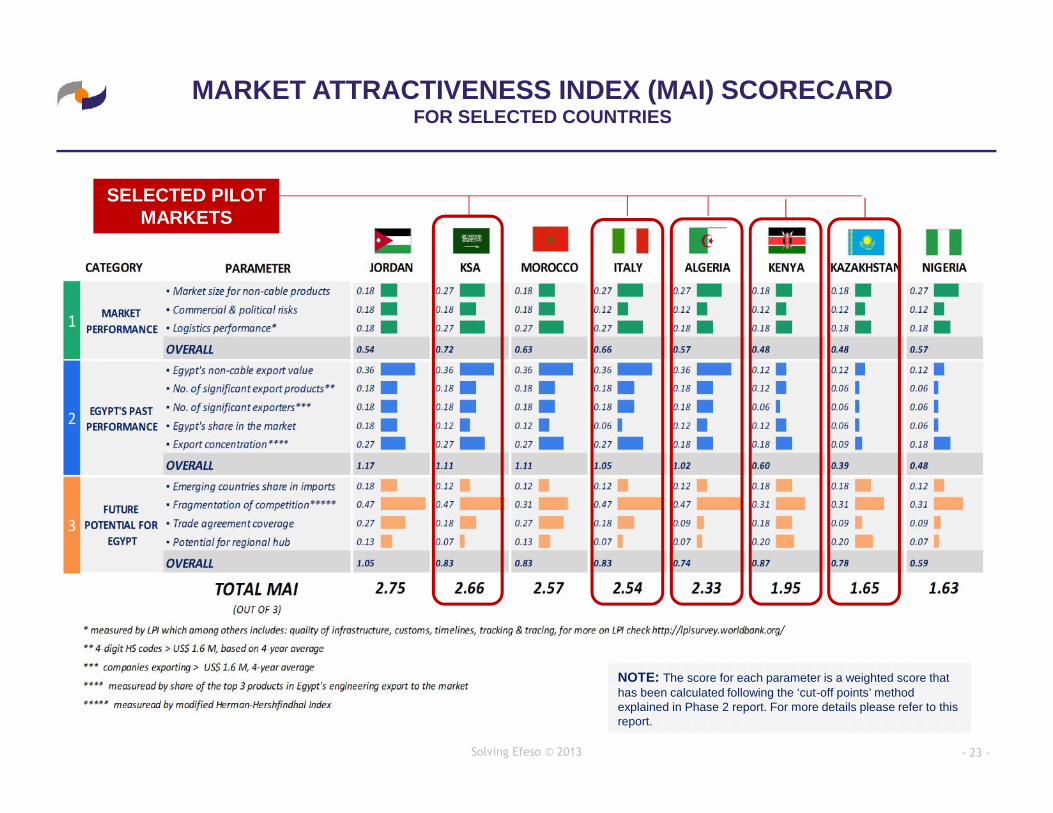

MARKET ATTRACTIVENESS INDEX (MAI) SCORECARDFOR SELECTED COUNTRIES

NOTE: The score for each parameter is a weighted score thathas been calculated following the ‘cut-off points’ methodexplained in Phase 2 report. For more details please refer to thisreport.

SELECTED PILOTMARKETS

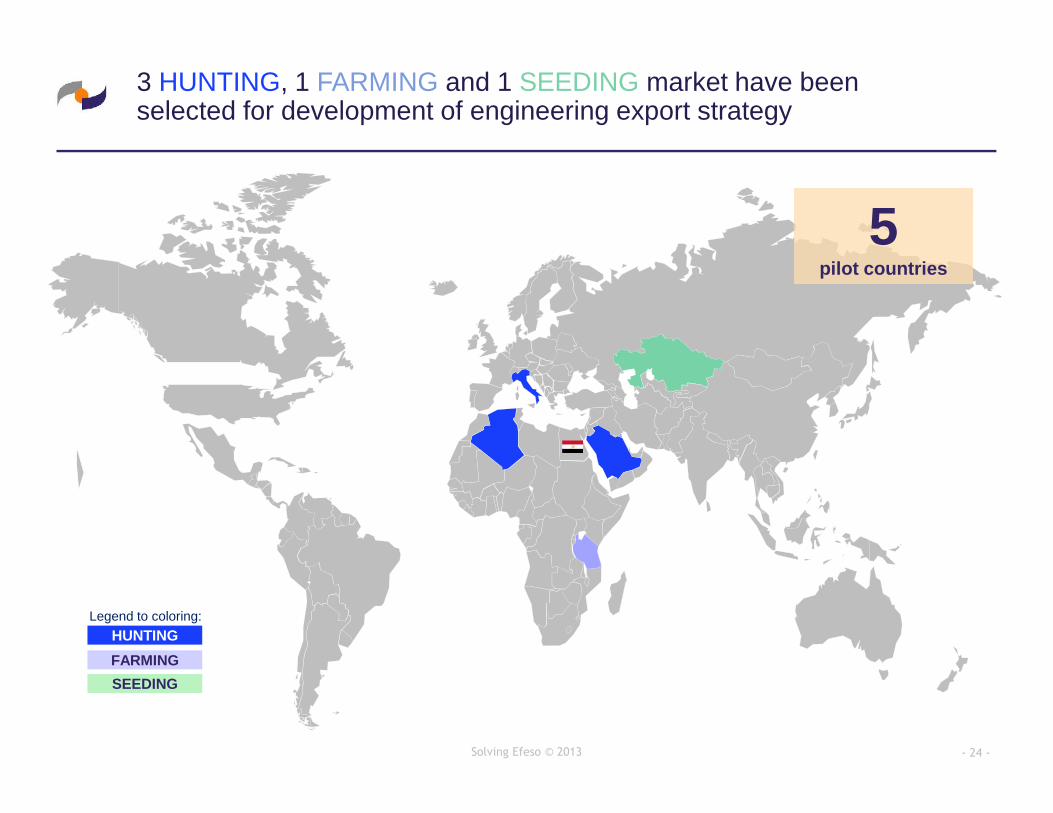

- 24 -Solving Efeso © 2013

3 HUNTING, 1 FARMING and 1 SEEDING market have beenselected for development of engineering export strategy

FARMINGHUNTING

SEEDING

Legend to coloring:

5pilot countries

- 25 -Solving Efeso © 2013

SAUDI ARABIA KENYA

RATIONALE BEHIND THE SELECTION

• Historically one of the topmarkets for Egypt

• Steady growth fuelled bythe oil revenues

• After the events of ‘ArabSpring’ Saudi Arabiaembarked on a majordomestic investmentprogram

• The government hasbegun establishing six"economic cities" indifferent regions of thecountry to promote foreigninvestment and plans tospend $373 billion in 4years on socialdevelopment andinfrastructure projects.

• Large number ofEgyptians living in thecountry

• Excellent connectionbetween Egypt and SaudiArabia through the RedSea

• One of the mostpromising markets inAfrica

• Stable economy andpolitical climate

• Kenya is emerging as ahub for East Africa 300 mpeople makret.

• This role will increasefurther as the LAPPSETcorridor project (linkingKenya with Ethiopia andSouth Sudan) kicks off.

• It includes constructingnew port in Lamu that willsurpass the capacity ofMombasa

• Good sea connectionbetween Egypt and Kenya

• Egypt has alreadyundertook trade missions/ visits to Kenya what haslaid the foundation forfurther efforts

These 5 markets have been considered ‘pilot markets’ for exportstrategy development. Further research will be done for these

countries to forge country-specific recommendation.*

ALGERIA• Large value of

engineering productsexports over last 4 years

• Nearly 40 m people andpopulation is expected togrow in coming years

• Consistently investing inthe infrastructure upgrade

• Optimistic GDP forecast

• Good access through theMediterranean Sea ports

• Large number ofEgyptians exporterspresent

• Arabic speaking countryalthough some minordifferences in dialect exist

• Country importsengineering products ofnearly US$ 6 bn, morethan Morocco and Jordantogether

ITALY• One of the top markets for

Egyptian engineeringproducts in Europe

• Very diverse portfolio ofEgyptian engineeringproducts exported to thecountry

• Significant number ofEgyptian exportersexporting to the country

• The engineering importsto Italy very high, nearlyUS$ 50 bn in 2012

• Very good access acrossthe Mediterranean Sea

• Recent economicdownturn may forceItalian companies andconsumers to seekcheaper substitutes for itscurrent components andproducts, what createsopportunity for Egypt.

KAZAKHSTAN• Booming economy driven by

oil & gas revenue andinfrastructure projects.Engineering importsexceeded US$ 5 bn in 2012

• No major export toKazakhstan from Egypt -except the transport. sector

• Apart from being a bigmarket itself Kazakhstanshows growing importanceas regional hub for CentralAsia growing markets

• The most stable politicallycountry in Central Asia andCaucasus. Commercial risksare low comparing to otherseeding markets.

• Due to its locationKazakhstan may be difficultmarket to compete in, butonce enter the marketEgyptian exporters mayenjoy long-term profits andaccess to much largermarket

*Country-specific recommendations will complement the generic ones

- 26 -EEC-EG Report Phase 5 Solving Efeso © 2014

Phase 3: Export Strategy

- 27 -EEC-EG Report Phase 2 Solving Efeso © 2013

Recommended Export Strategy

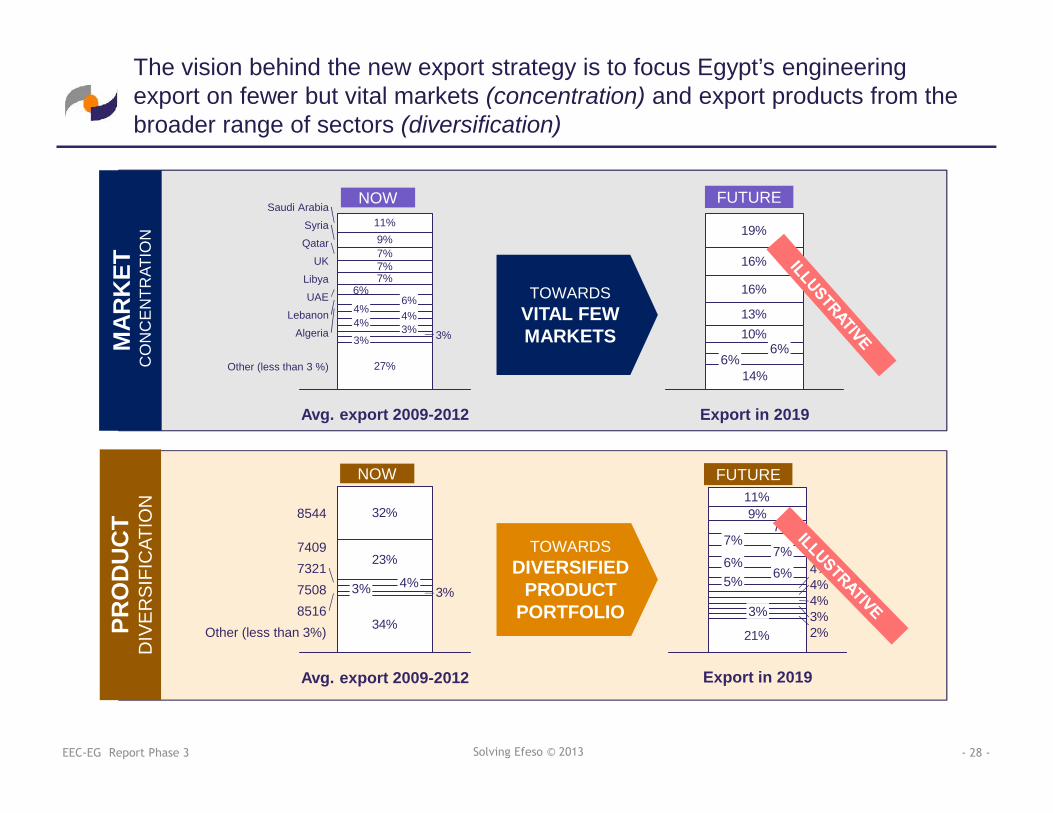

The vision behind the new export strategy is tofocus Egypt’s engineering export on fewer but vitalmarkets (concentration) and export products fromthe broader range of sectors (diversification)

Recommended Export Strategy

- 28 -EEC-EG Report Phase 3 Solving Efeso © 2013

The vision behind the new export strategy is to focus Egypt’s engineeringexport on fewer but vital markets (concentration) and export products from thebroader range of sectors (diversification)

27%

3%

6%7%7%7%9%11%

Other (less than 3 %)

3%4% 4%4%6%

Algeria

Lebanon

UAE

Libya

UK

Qatar

Syria

Saudi Arabia

Avg. export 2009-2012

3%

14%

10%13%

16%

16%

19%

Export in 2019

6%6%

TOWARDSVITAL FEWMARKETS

34%

3%

23%

32%

Other (less than 3%)8516750873217409

8544

Avg. export 2009-2012

3% 4%

21% 2%3%4%4%4%

7%9%

11%

Export in 2019

3%

5% 6%6%

7%7%TOWARDS

DIVERSIFIEDPRODUCT

PORTFOLIOPRO

DU

CT

DIV

ER

SIF

ICAT

ION

MAR

KET

CO

NC

EN

TRAT

ION

NOW FUTURE

NOW FUTURE

- 29 -EEC-EG Report Phase 4 Solving Efeso © 2013

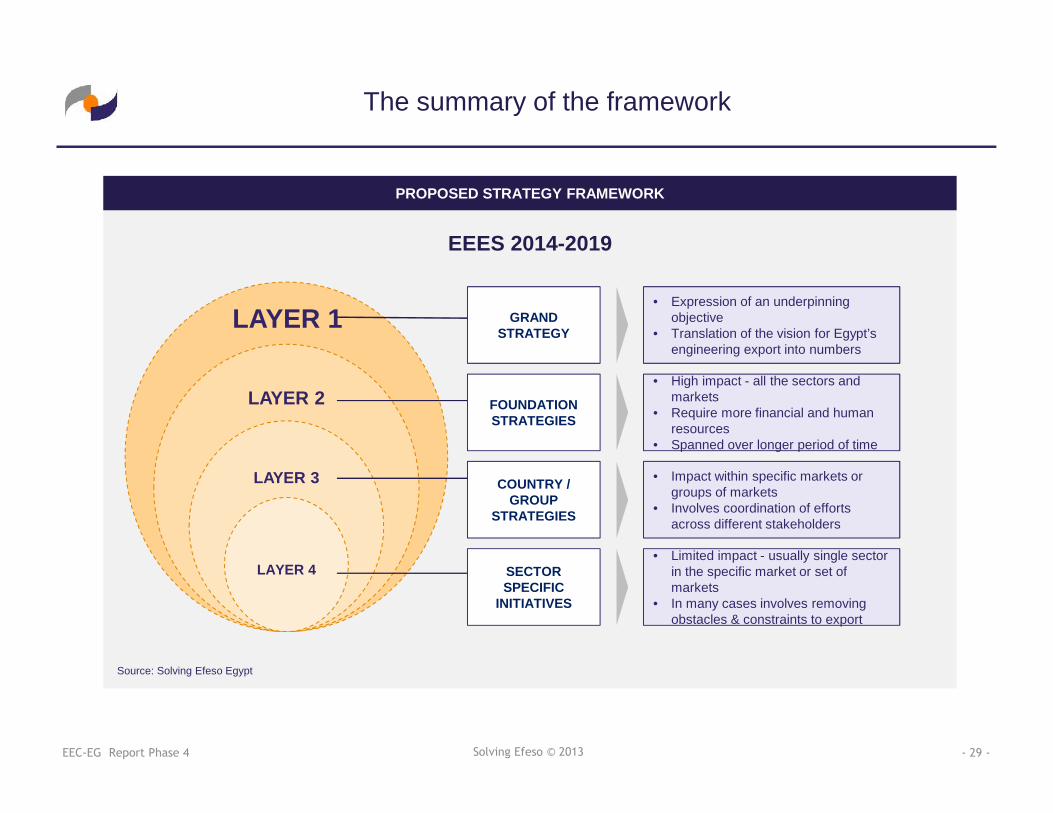

The summary of the framework

PROPOSED STRATEGY FRAMEWORK

LAYER 2

LAYER 3

LAYER 4

FOUNDATIONSTRATEGIES

COUNTRY /GROUP

STRATEGIES

SECTORSPECIFIC

INITIATIVES

• High impact - all the sectors andmarkets

• Require more financial and humanresources

• Spanned over longer period of time

• Impact within specific markets orgroups of markets

• Involves coordination of effortsacross different stakeholders

• Limited impact - usually single sectorin the specific market or set ofmarkets

• In many cases involves removingobstacles & constraints to export

EEES 2014-2019

Source: Solving Efeso Egypt

LAYER 1 GRANDSTRATEGY

• Expression of an underpinningobjective

• Translation of the vision for Egypt’sengineering export into numbers

- 30 -EEC-EG Report Phase 4 Solving Efeso © 2013

GRAND STRATEGY

PROPOSED STRATEGY FRAMEWORK

FOUNDATIONSTRATEGIES

COUNTRY /GROUP

STRATEGIES

SECTORSPECIFIC

INITIATIVES

Source: Solving Efeso Egypt

GRANDSTRATEGY

“Increase Egypt’s engineering export toUS$ 5 bn by 2016, and US$ 7.5 bn by

2019, while focusing the now-termefforts on fewer vital markets and by

taking a diverse portfolio of competitiveproducts”

EEES 2014-2019

- 31 -EEC-EG Report Phase 4 Solving Efeso © 2013

We identified 4 main constraints that will have to be addressed inorder to reach the targets stated in the grand strategy

PROPOSED STRATEGY FRAMEWORK

Source: Solving Efeso Egypt

EEES 2014-2019

US$

2.5bn

NOW 2019

US$

7.5bn

Inefficientbusiness

matchmaking

Lack / lowaccessibility of quality

market and exportrelated data

Discriminativefinancialincentivesystem

Weak position of instreamlining support

services

12

34

- 32 -EEC-EG Report Phase 5 Solving Efeso © 2014

Phase 4: Action Plan

- 33 -EEC-EG Report Phase 4 Solving Efeso © 2013

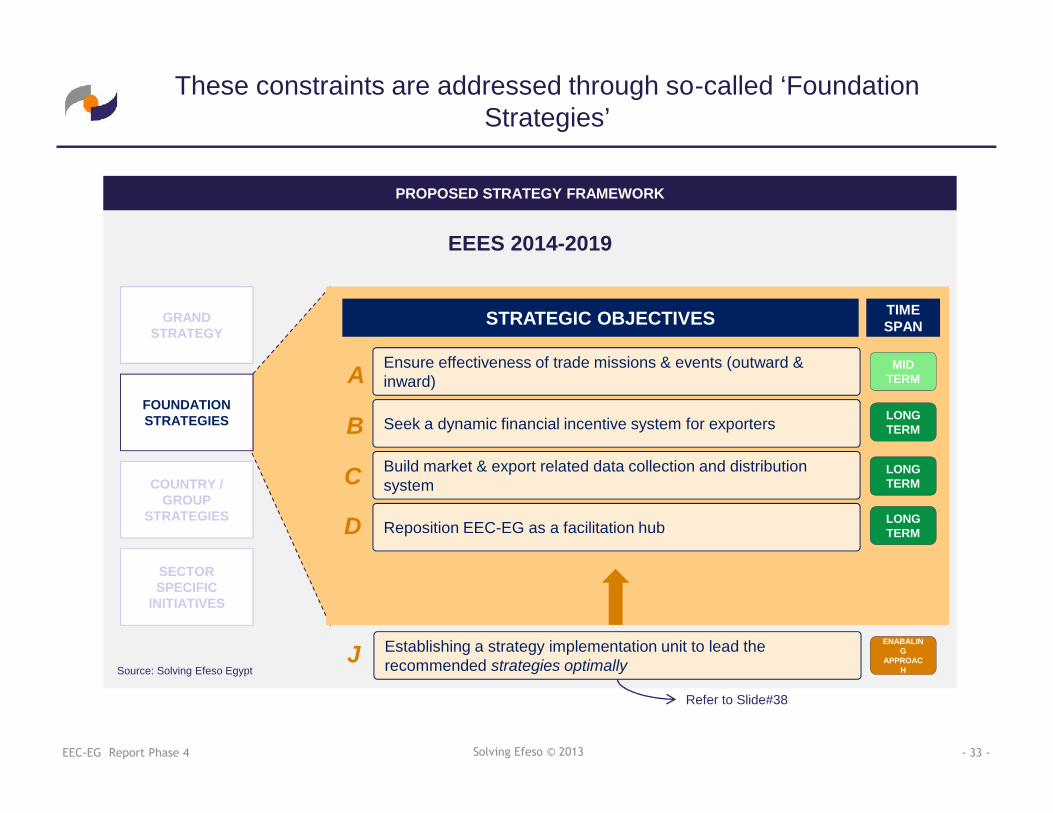

These constraints are addressed through so-called ‘FoundationStrategies’

PROPOSED STRATEGY FRAMEWORK

COUNTRY /GROUP

STRATEGIES

SECTORSPECIFIC

INITIATIVES

Source: Solving Efeso Egypt

GRANDSTRATEGY

FOUNDATIONSTRATEGIES

STRATEGIC OBJECTIVES

Ensure effectiveness of trade missions & events (outward &inward)

Build market & export related data collection and distributionsystem

Reposition EEC-EG as a facilitation hub

Seek a dynamic financial incentive system for exporters

A

B

C

D

LONGTERM

LONGTERM

TIMESPAN

LONGTERM

MIDTERM

EEES 2014-2019

Establishing a strategy implementation unit to lead therecommended strategies optimallyJ

ENABALING

APPROACH

Refer to Slide#38

- 34 -EEC-EG Report Phase 4 Solving Efeso © 2013

Apart from ‘Foundation Strategies’ we have identified a set of countryspecific strategies that can help boost engineering export

PROPOSED STRATEGY FRAMEWORK

COUNTRY /GROUP

STRATEGIES

SECTORSPECIFIC

INITIATIVES

Source: Solving Efeso Egypt

GRANDSTRATEGY

FOUNDATIONSTRATEGIES

STRATEGIC OBJECTIVES

Improve the brand image of Egyptian engineering products(KSA)

Monitor the trade agreements compliance (Algeria)

Boost know-how transfer and cooperation to grow export tocompetitive markets (Italy)

Launch ‘Go-to Africa’ export support kit (Kenya)

Develop effective financial & logistics support tools for difficult-to-access countries (Kazakhstan)

E

F

G

H

I

LONGTERM

MIDTERM

MIDTERM

MIDTERM

MIDTERM

TIMESPAN

EEES 2014-2019

- 35 -EEC-EG Report Phase 4 Solving Efeso © 2013

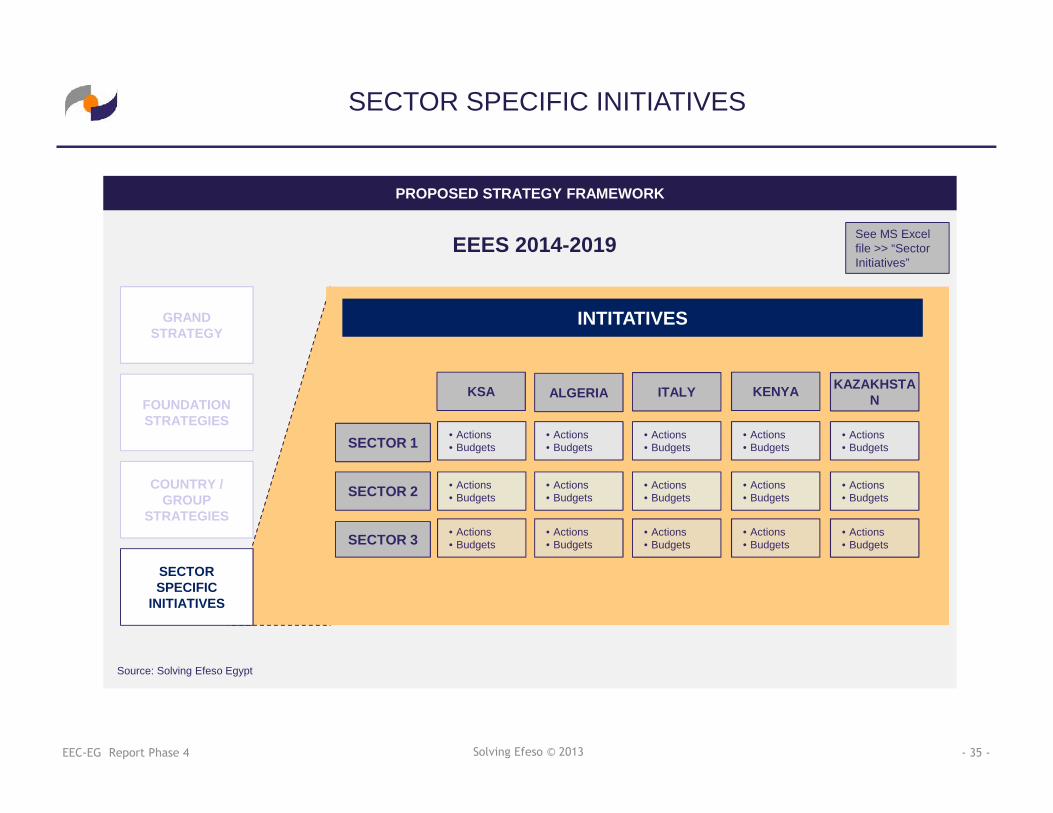

SECTOR SPECIFIC INITIATIVES

PROPOSED STRATEGY FRAMEWORK

COUNTRY /GROUP

STRATEGIES

SECTORSPECIFIC

INITIATIVES

Source: Solving Efeso Egypt

GRANDSTRATEGY

FOUNDATIONSTRATEGIES

INTITATIVES

KSA ALGERIA

SECTOR 1

SECTOR 2

SECTOR 3

ITALY KENYA KAZAKHSTAN

• Actions• Budgets

• Actions• Budgets

• Actions• Budgets

• Actions• Budgets

• Actions• Budgets

• Actions• Budgets

• Actions• Budgets

• Actions• Budgets

• Actions• Budgets

• Actions• Budgets

• Actions• Budgets

• Actions• Budgets

• Actions• Budgets

• Actions• Budgets

• Actions• Budgets

EEES 2014-2019 See MS Excelfile >> “SectorInitiatives”

- 36 -EEC-EG Report Phase 4 Solving Efeso © 2013

Key Performance Indicators(KPIs)

- 37 -EEC-EG Report Phase 4 Solving Efeso © 2013

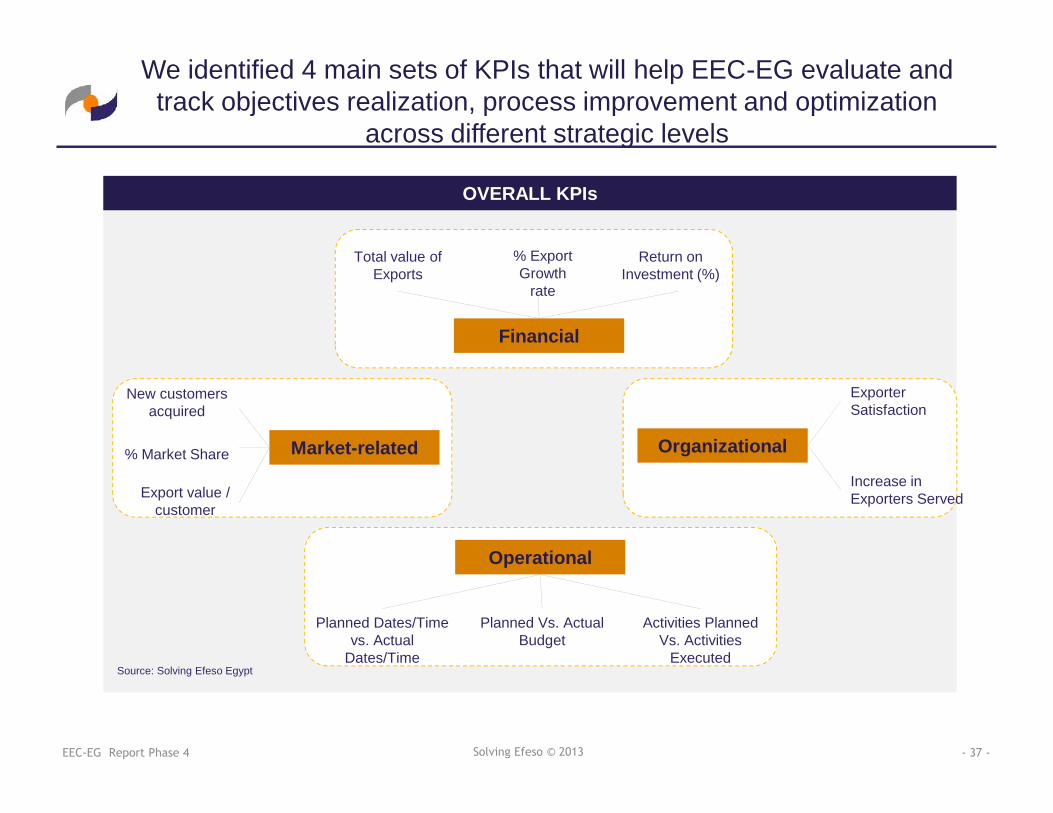

We identified 4 main sets of KPIs that will help EEC-EG evaluate andtrack objectives realization, process improvement and optimization

across different strategic levels

OVERALL KPIs

Source: Solving Efeso Egypt

% ExportGrowth

rate

Return onInvestment (%)

Total value ofExports

Financial

Operational

Planned Vs. ActualBudget

Activities PlannedVs. Activities

Executed

Planned Dates/Timevs. Actual

Dates/Time

Organizational

Increase inExporters Served

ExporterSatisfaction

Market-related

Export value /customer

% Market Share

New customersacquired

Recommended