Student LoanDebt ManagementBROWN SCHOOL OFFICE OF FINANCIAL AID

Fall 2015

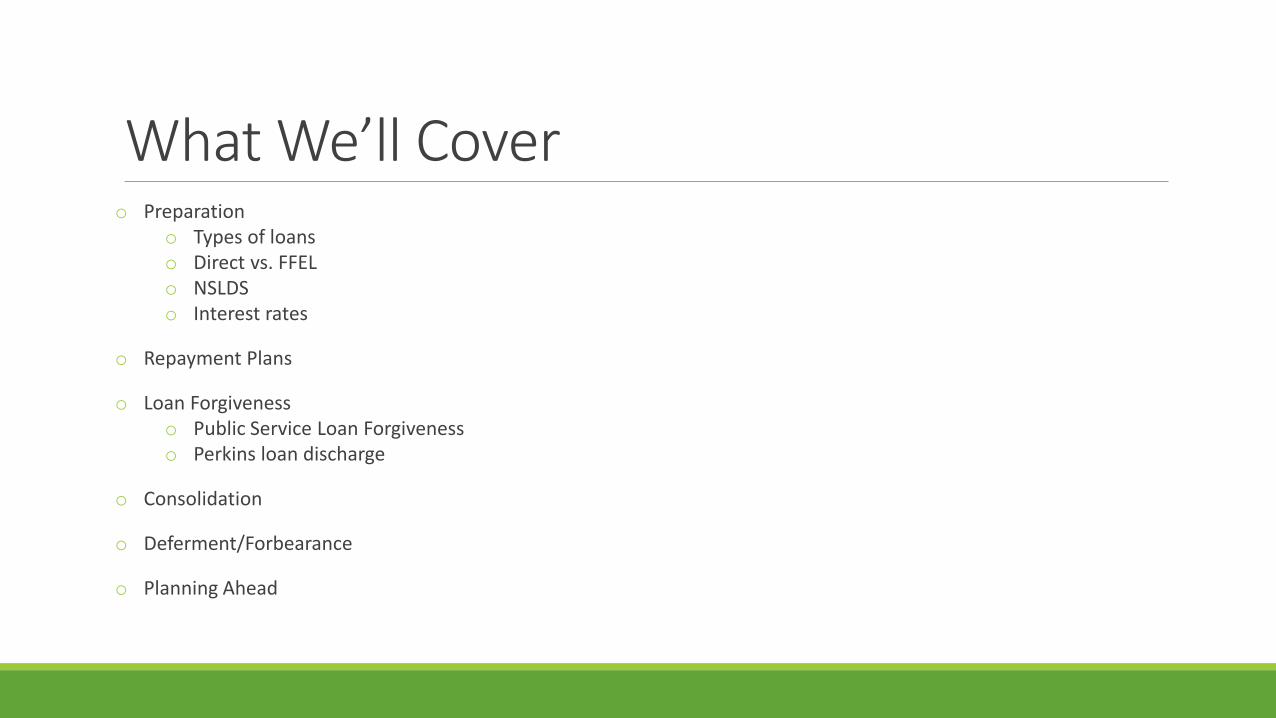

What We’ll Covero Preparation

o Types of loanso Direct vs. FFELo NSLDSo Interest rates

o Repayment Plans

o Loan Forgivenesso Public Service Loan Forgivenesso Perkins loan discharge

o Consolidation

o Deferment/Forbearance

o Planning Ahead

Preparation: Before You Leave School

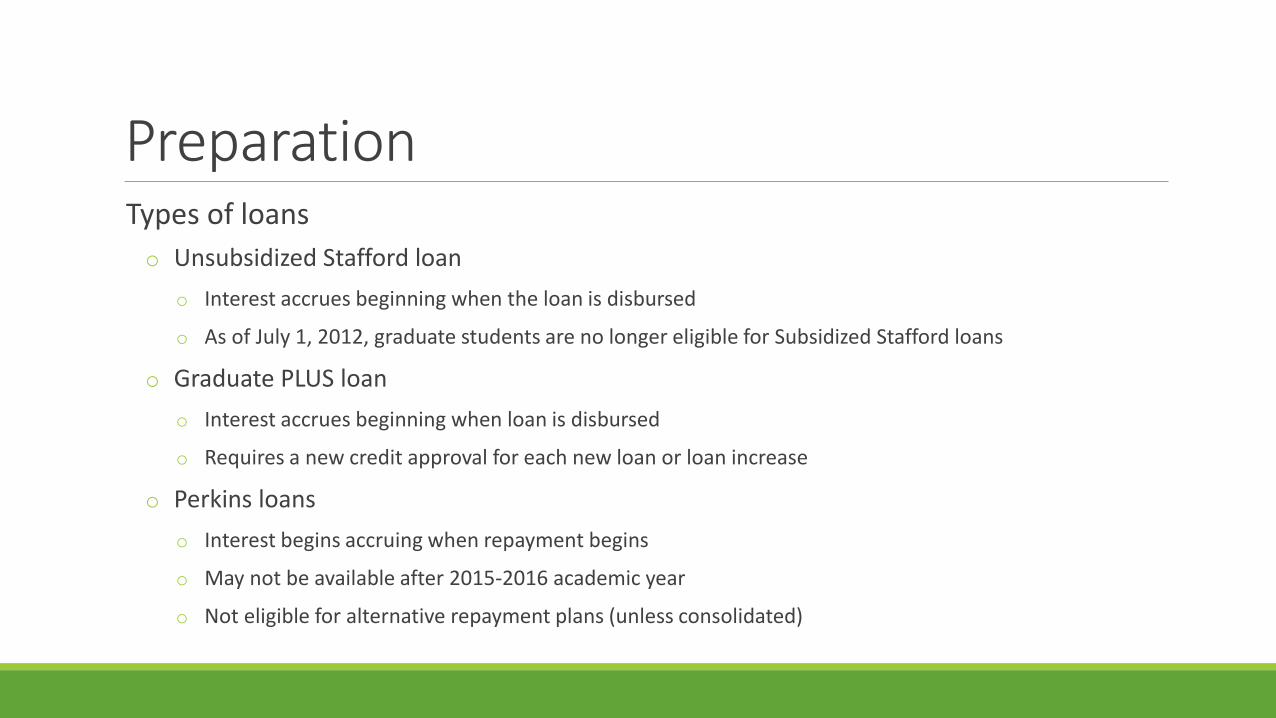

PreparationTypes of loans

o Unsubsidized Stafford loan

o Interest accrues beginning when the loan is disbursed

o As of July 1, 2012, graduate students are no longer eligible for Subsidized Stafford loans

o Graduate PLUS loan

o Interest accrues beginning when loan is disbursed

o Requires a new credit approval for each new loan or loan increase

o Perkins loans

o Interest begins accruing when repayment begins

o May not be available after 2015-2016 academic year

o Not eligible for alternative repayment plans (unless consolidated)

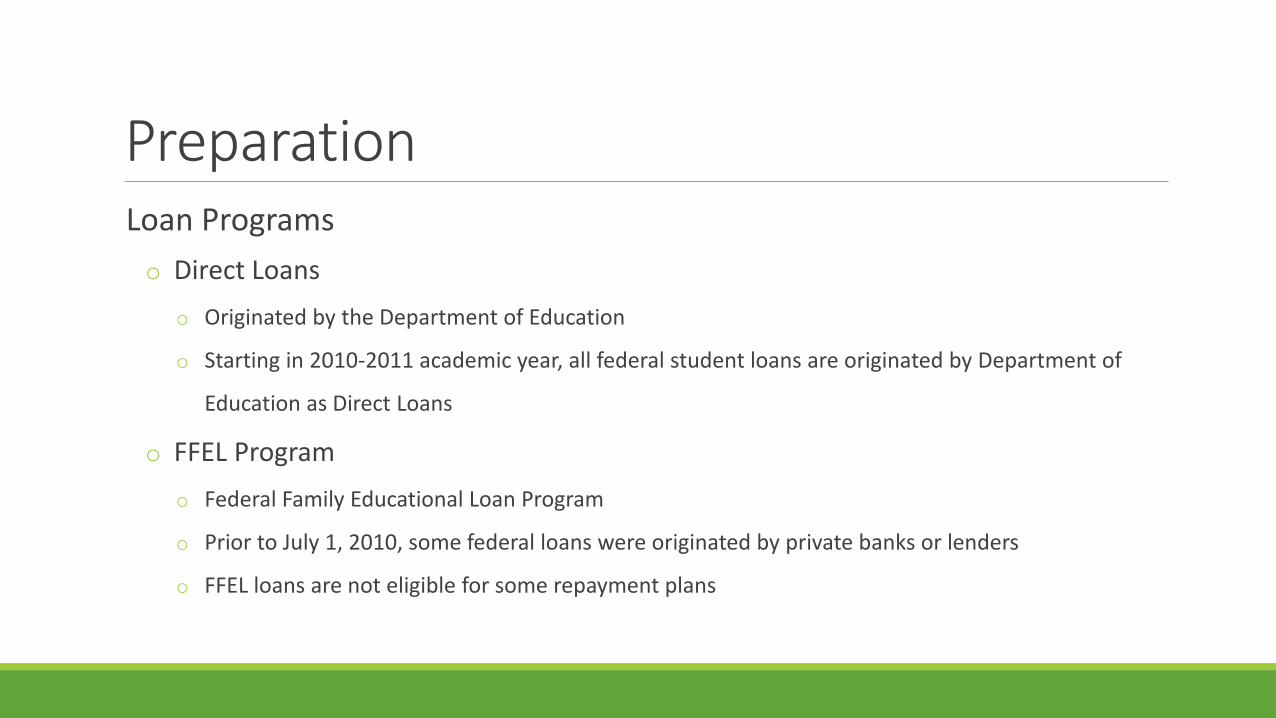

PreparationLoan Programs

o Direct Loans

o Originated by the Department of Education

o Starting in 2010-2011 academic year, all federal student loans are originated by Department of

Education as Direct Loans

o FFEL Program

o Federal Family Educational Loan Program

o Prior to July 1, 2010, some federal loans were originated by private banks or lenders

o FFEL loans are not eligible for some repayment plans

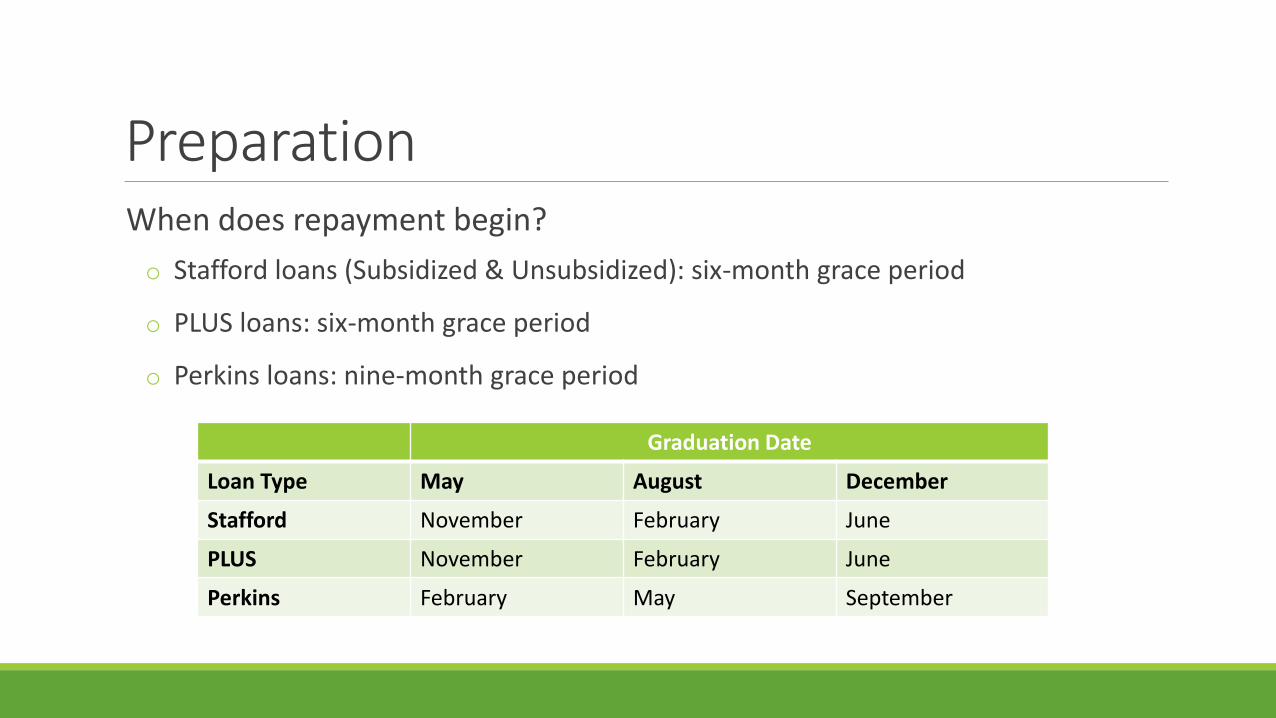

PreparationWhen does repayment begin?

o Stafford loans (Subsidized & Unsubsidized): six-month grace period

o PLUS loans: six-month grace period

o Perkins loans: nine-month grace period

Graduation Date

Loan Type May August December

Stafford November February June

PLUS November February June

Perkins February May September

PreparationNational Student Loan Data System (NSLDS)

o Comprehensive overview of all federal student loans

o Includes undergraduate and graduate borrowing history

o Lists each loan individually, including servicer contact information & interest rates

o Exit Interview process prior to graduation

o Financial Aid Review

Preparation

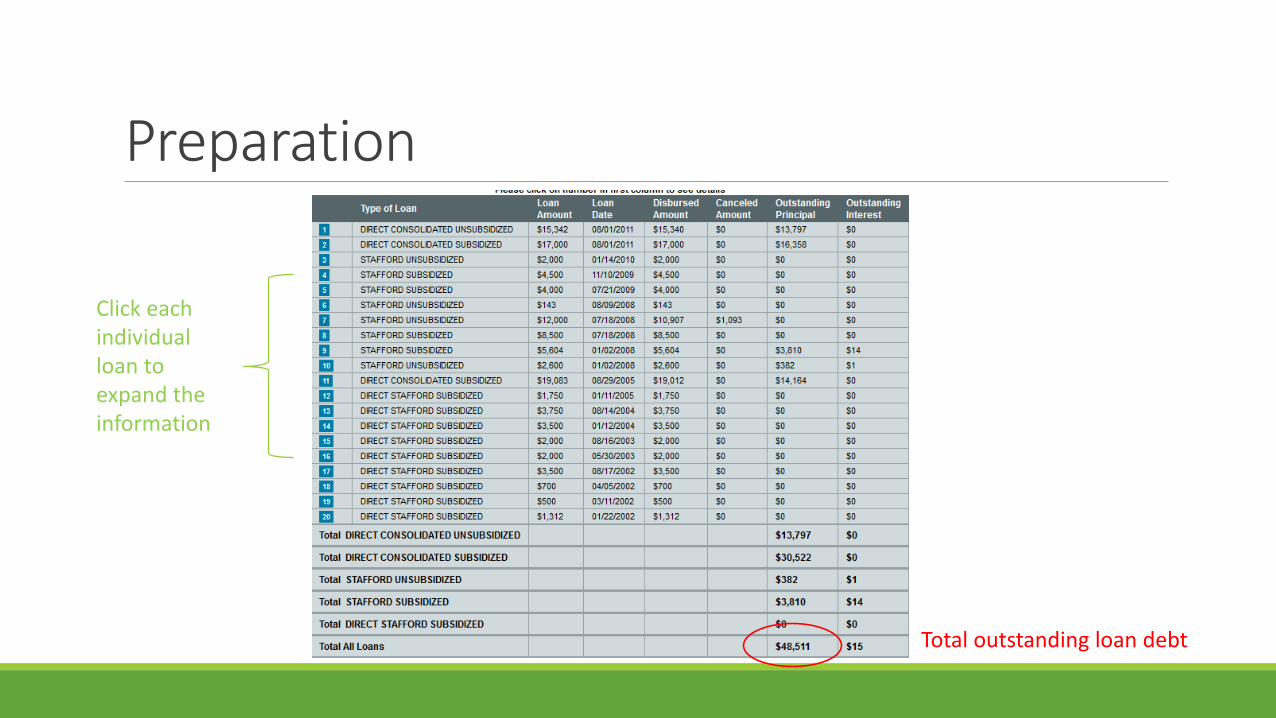

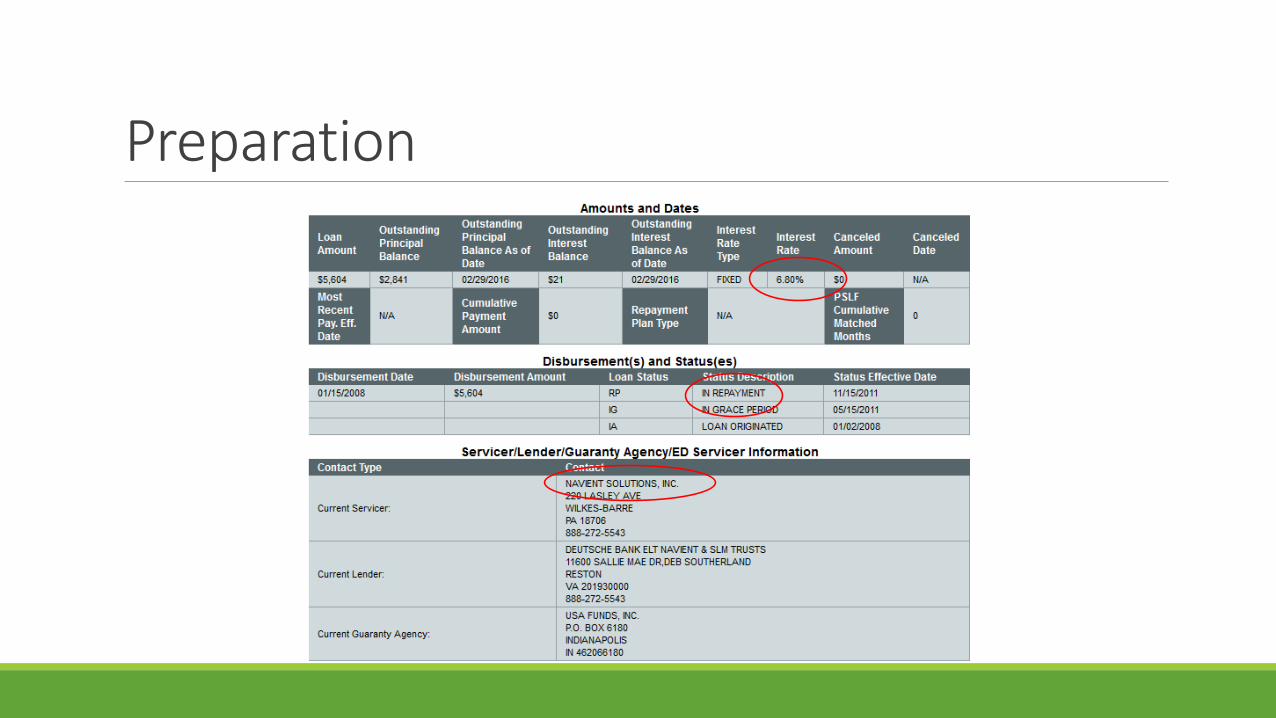

Click each individual loan to expand the information

Total outstanding loan debt

Preparation

Preparation

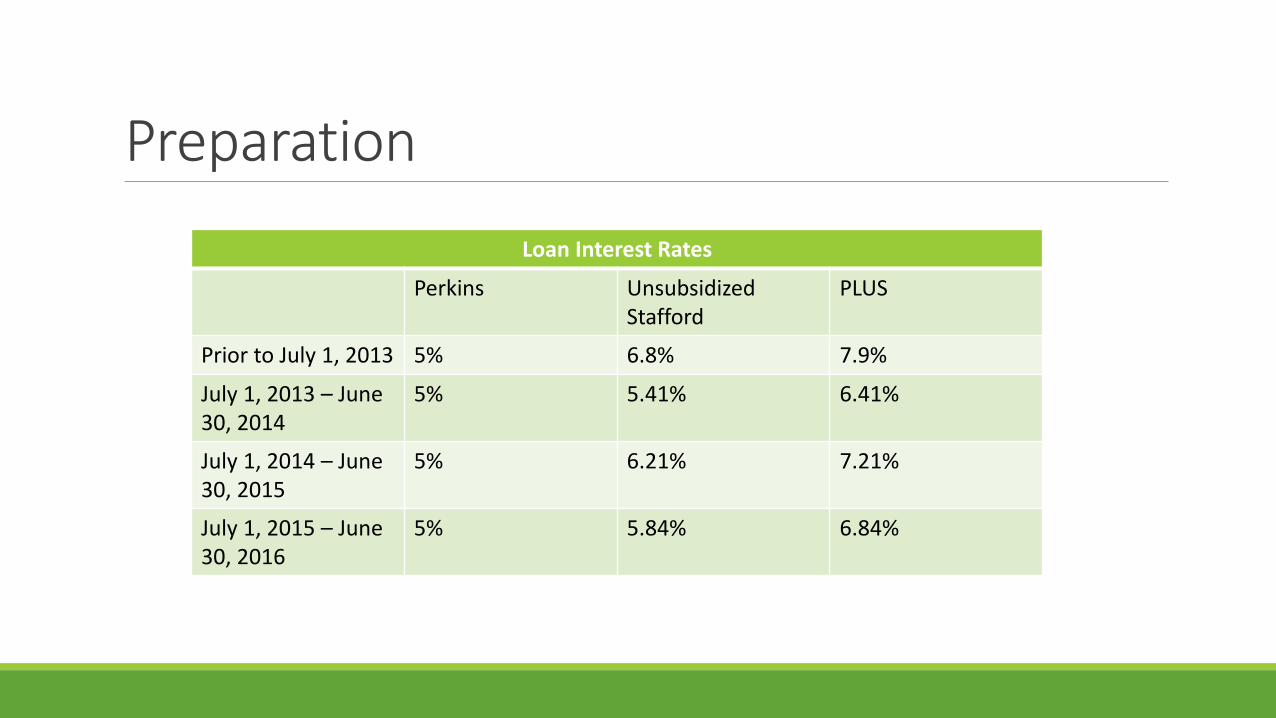

Loan Interest Rates

Perkins UnsubsidizedStafford

PLUS

Prior to July 1, 2013 5% 6.8% 7.9%

July 1, 2013 – June 30, 2014

5% 5.41% 6.41%

July 1, 2014 – June 30, 2015

5% 6.21% 7.21%

July 1, 2015 – June 30, 2016

5% 5.84% 6.84%

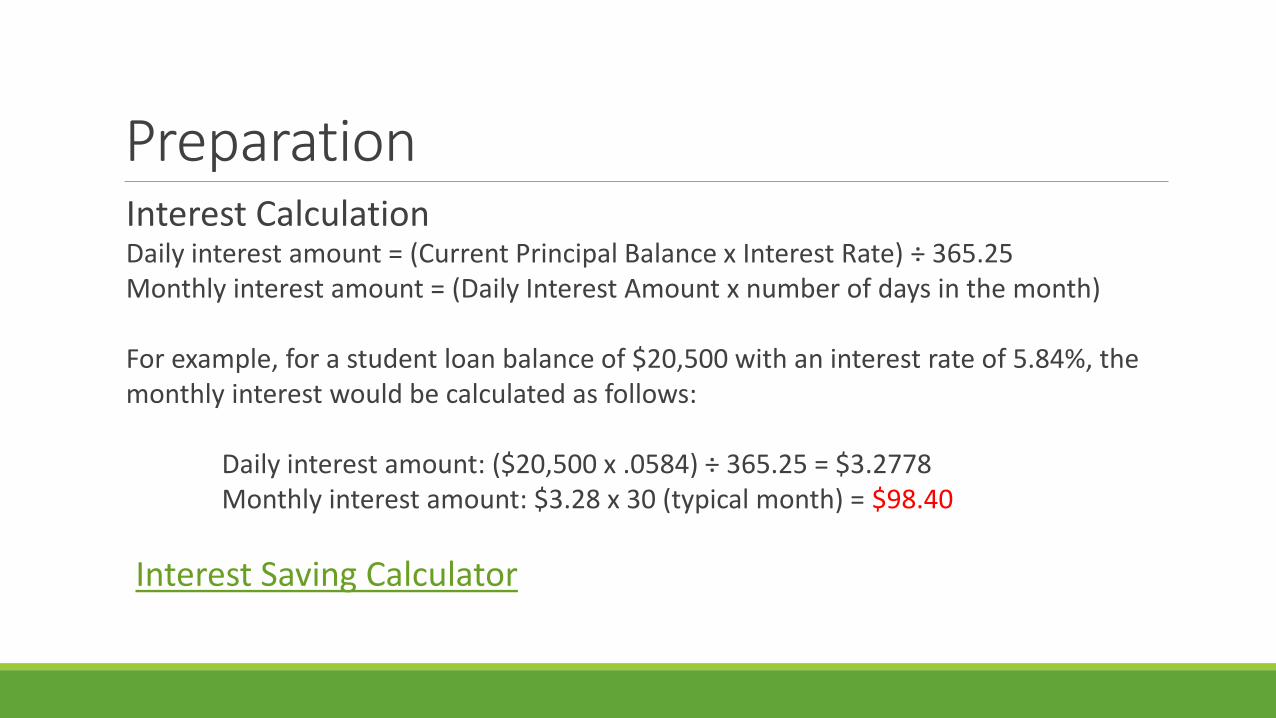

PreparationInterest CalculationDaily interest amount = (Current Principal Balance x Interest Rate) ÷ 365.25Monthly interest amount = (Daily Interest Amount x number of days in the month)

For example, for a student loan balance of $20,500 with an interest rate of 5.84%, the monthly interest would be calculated as follows:

Daily interest amount: ($20,500 x .0584) ÷ 365.25 = $3.2778Monthly interest amount: $3.28 x 30 (typical month) = $98.40

Interest Saving Calculator

Repayment Plans

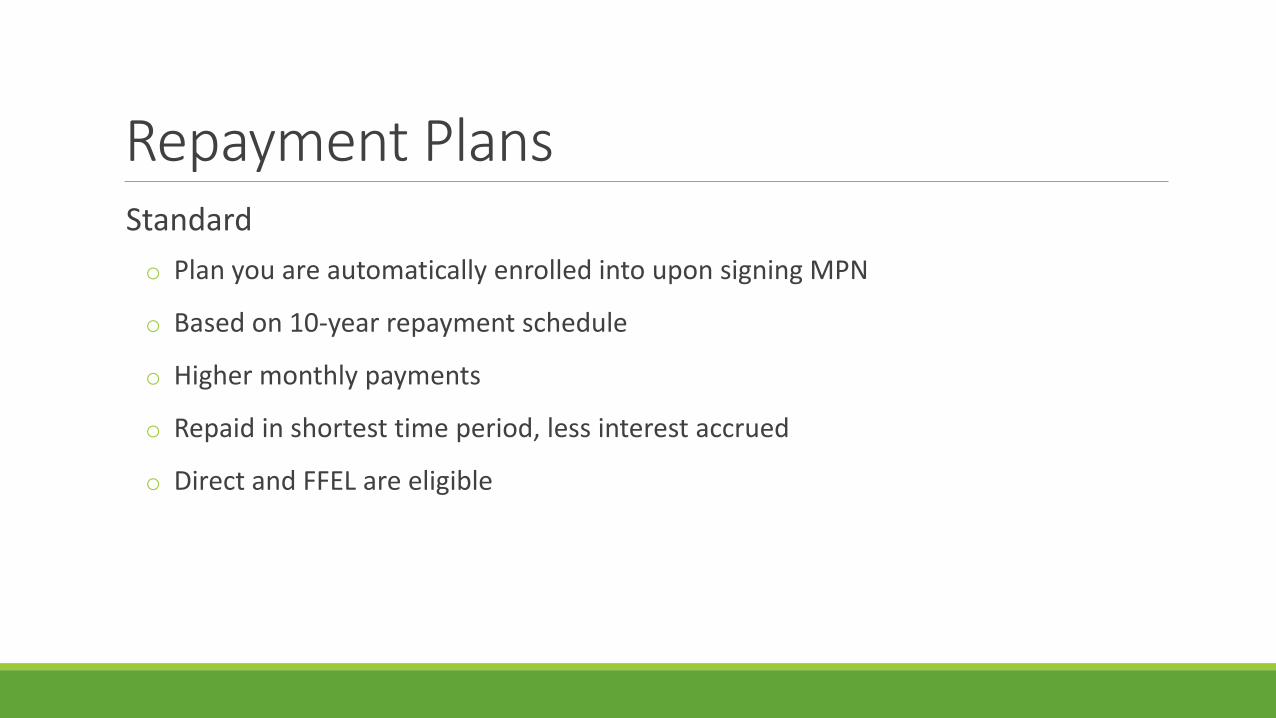

Repayment PlansStandard

o Plan you are automatically enrolled into upon signing MPN

o Based on 10-year repayment schedule

o Higher monthly payments

o Repaid in shortest time period, less interest accrued

o Direct and FFEL are eligible

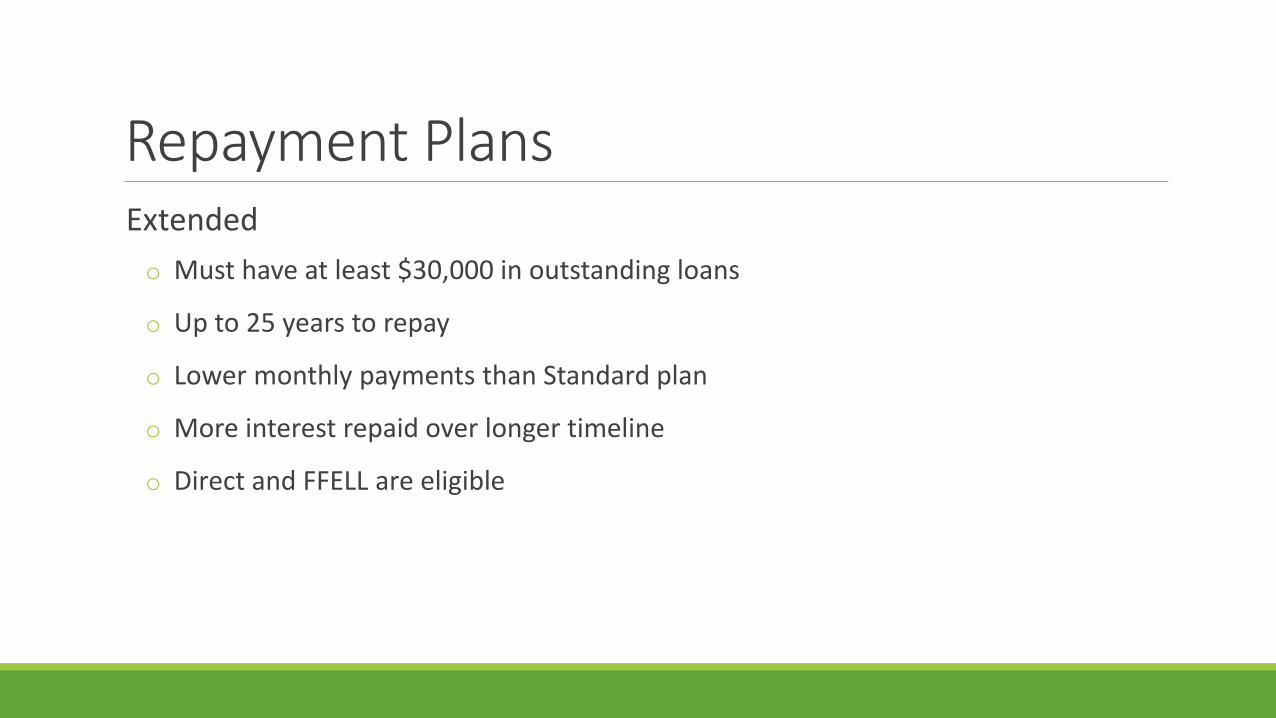

Repayment PlansExtended

o Must have at least $30,000 in outstanding loans

o Up to 25 years to repay

o Lower monthly payments than Standard plan

o More interest repaid over longer timeline

o Direct and FFELL are eligible

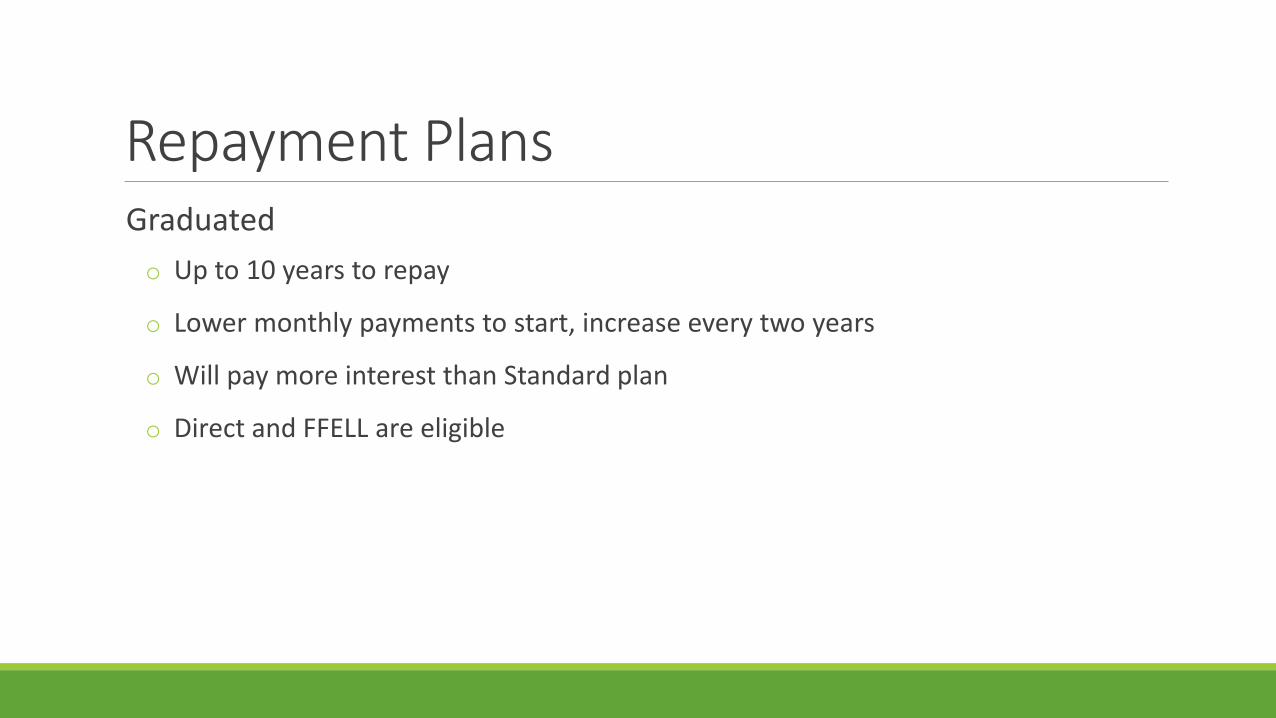

Repayment PlansGraduated

o Up to 10 years to repay

o Lower monthly payments to start, increase every two years

o Will pay more interest than Standard plan

o Direct and FFELL are eligible

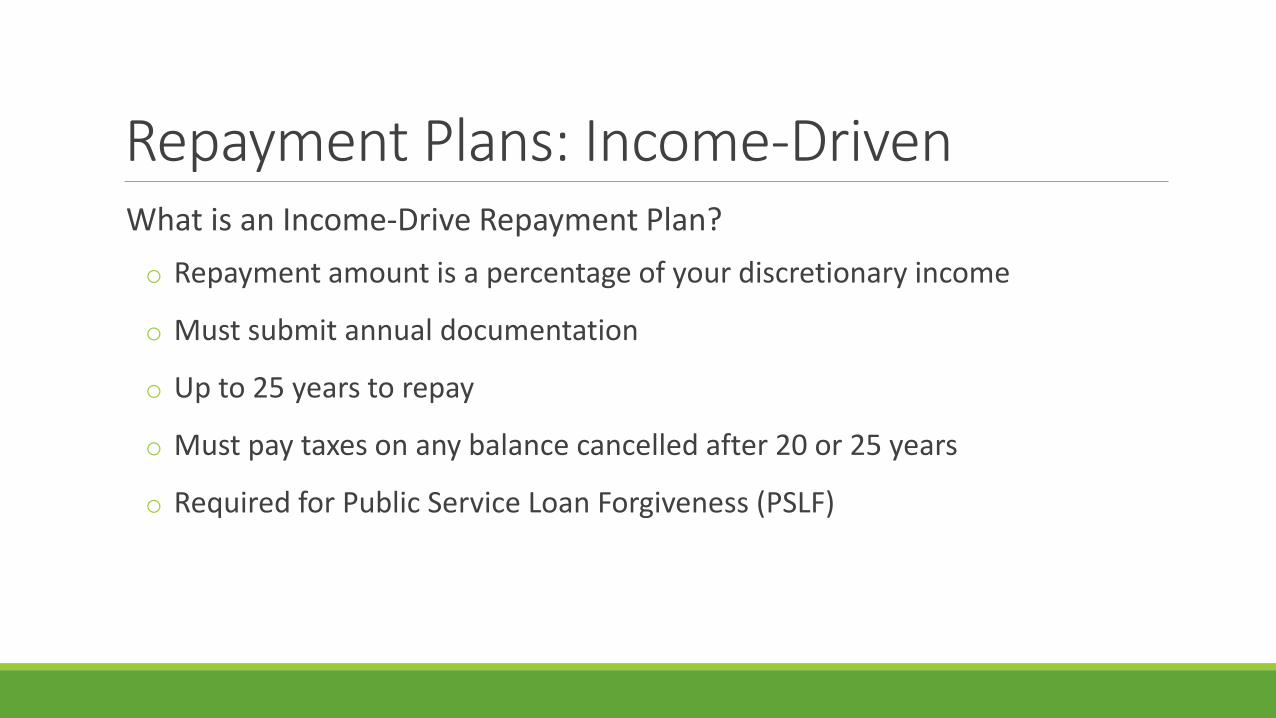

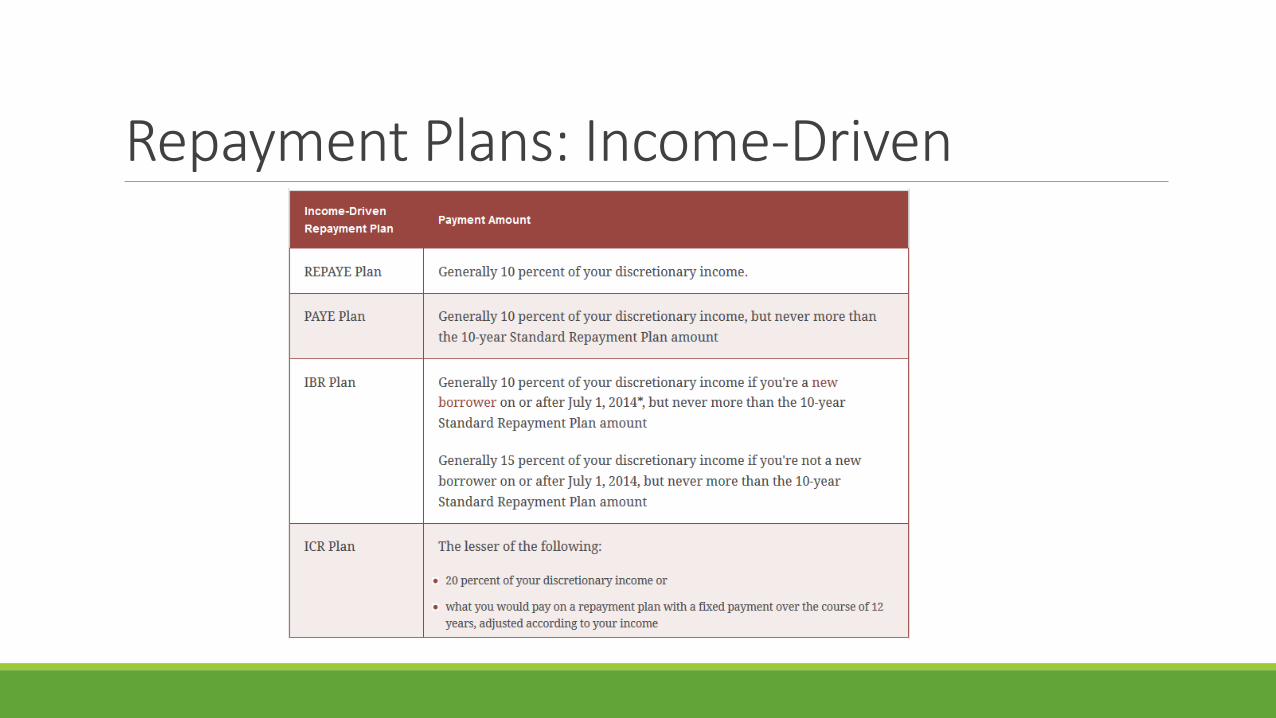

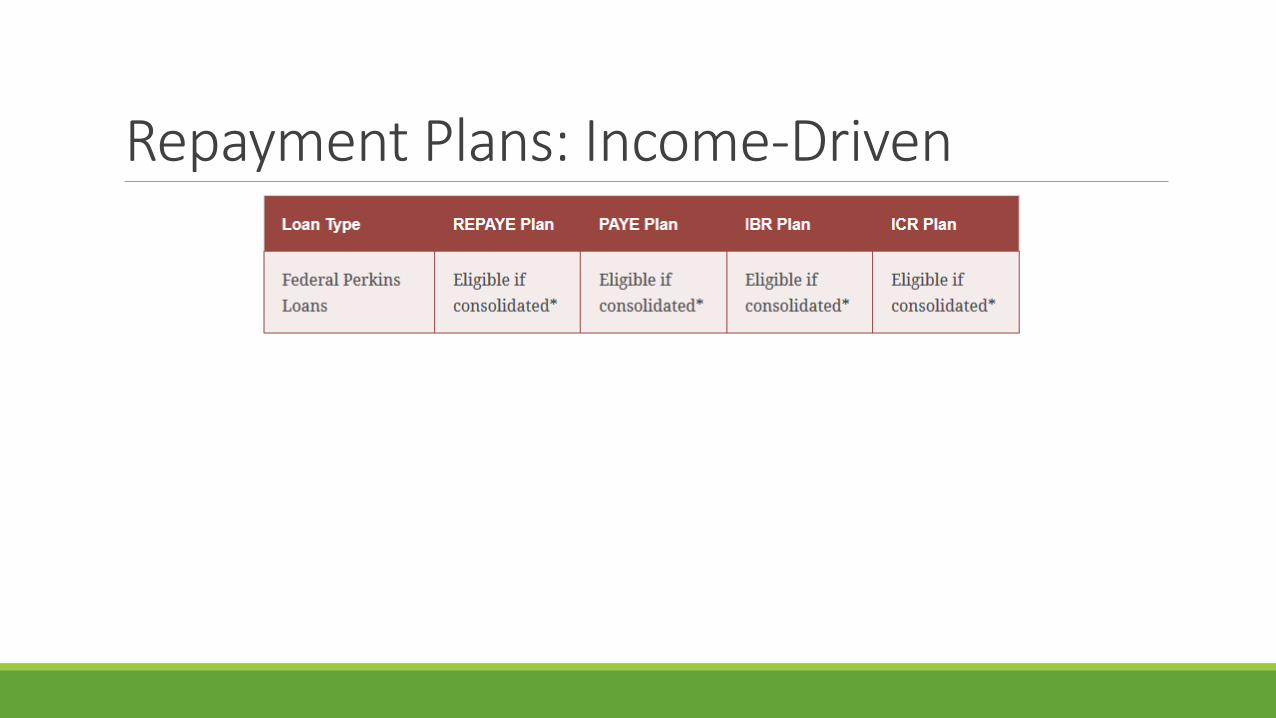

Repayment Plans: Income-DrivenWhat is an Income-Drive Repayment Plan?

o Repayment amount is a percentage of your discretionary income

o Must submit annual documentation

o Up to 25 years to repay

o Must pay taxes on any balance cancelled after 20 or 25 years

o Required for Public Service Loan Forgiveness (PSLF)

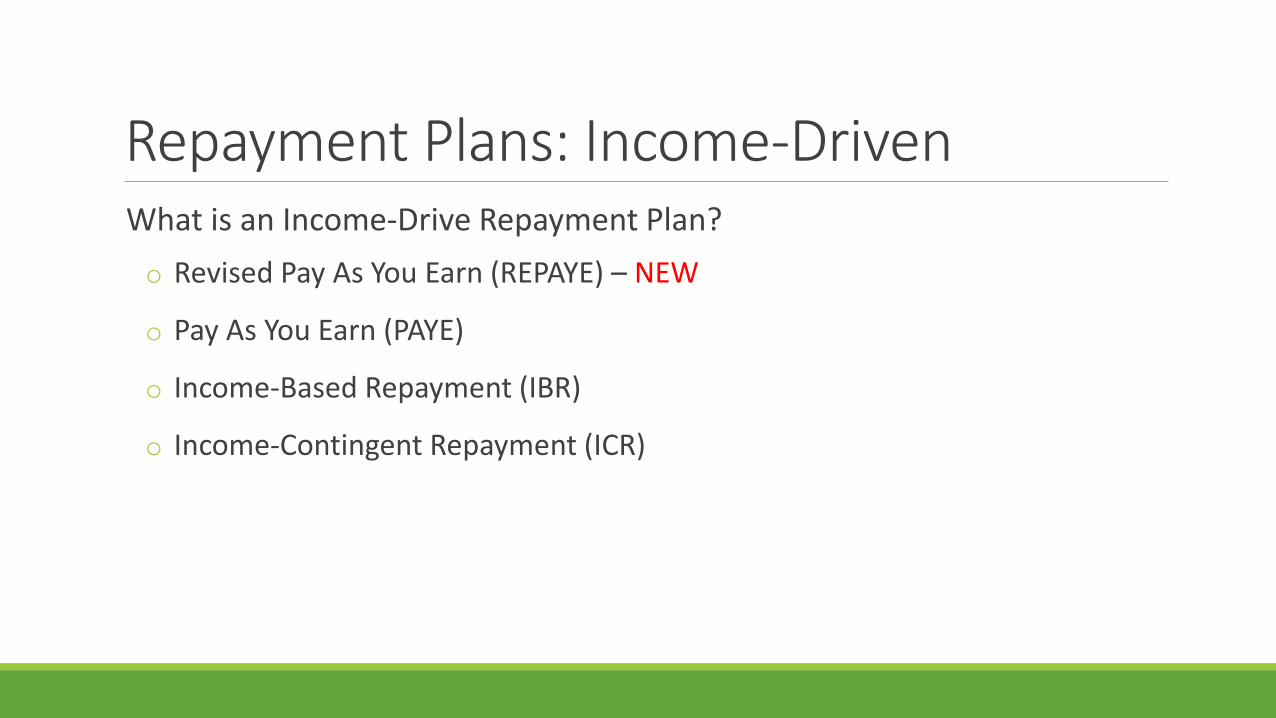

Repayment Plans: Income-DrivenWhat is an Income-Drive Repayment Plan?

o Revised Pay As You Earn (REPAYE) – NEW

o Pay As You Earn (PAYE)

o Income-Based Repayment (IBR)

o Income-Contingent Repayment (ICR)

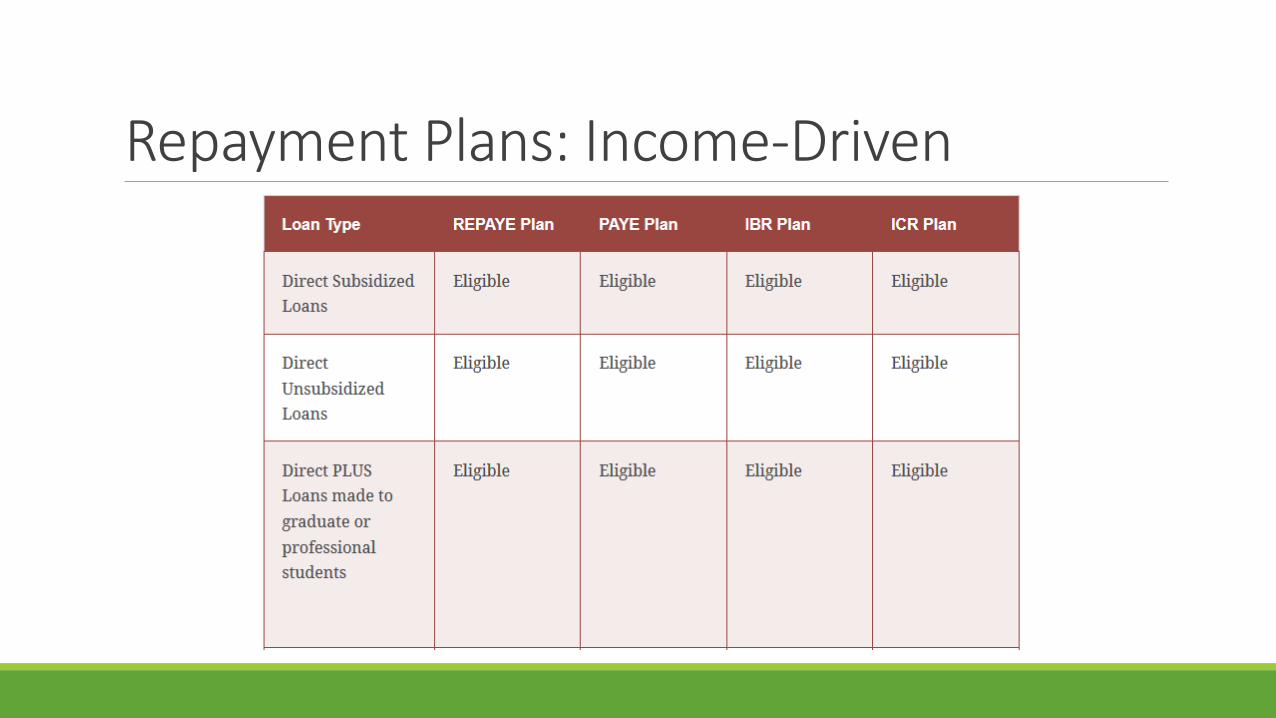

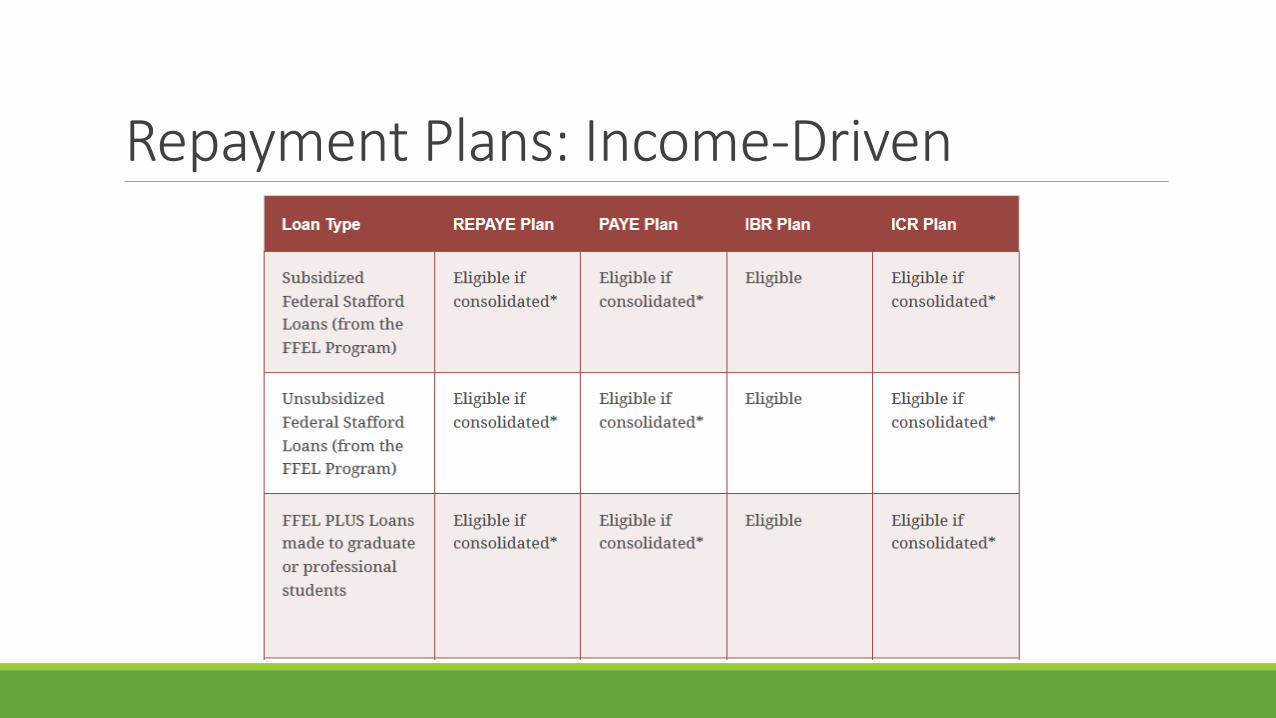

Repayment Plans: Income-Driven

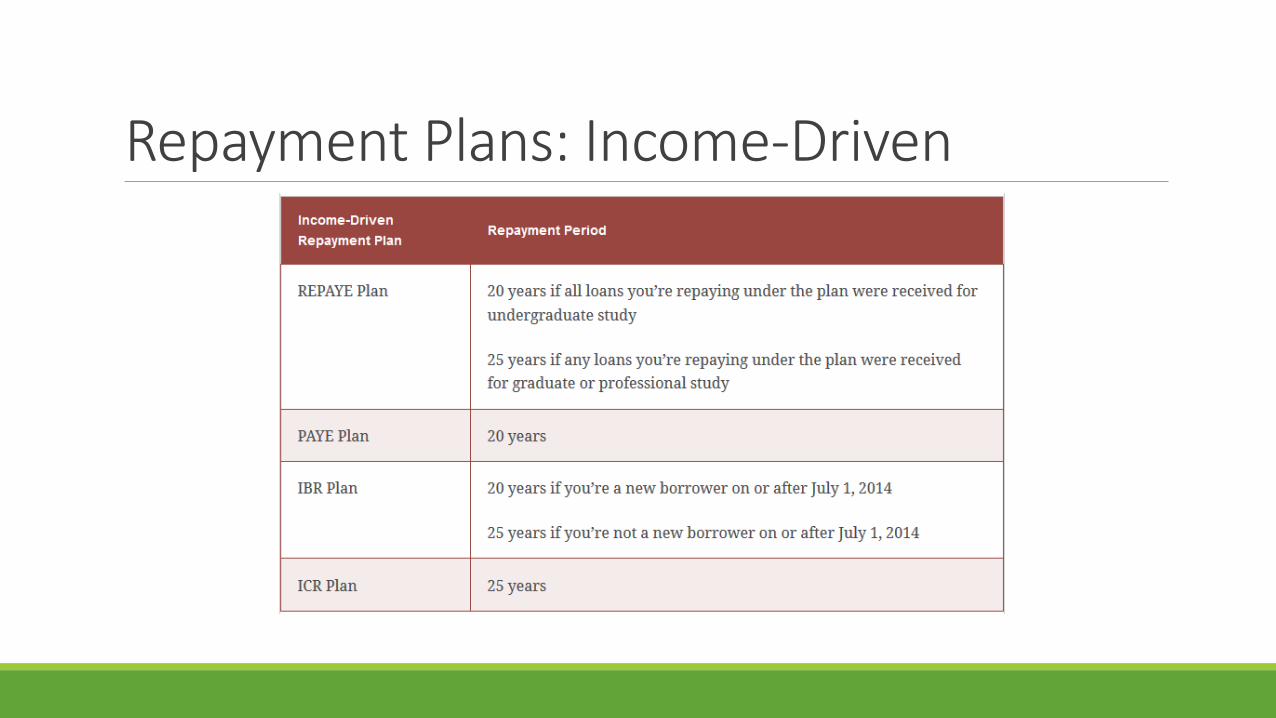

Repayment Plans: Income-Driven

Repayment Plans: Income-Driven

Repayment Plans: Income-Driven

Repayment Plans: Income-Driven

Repayment Plans: Income-Driven

Repayment Plans: Income-Driven

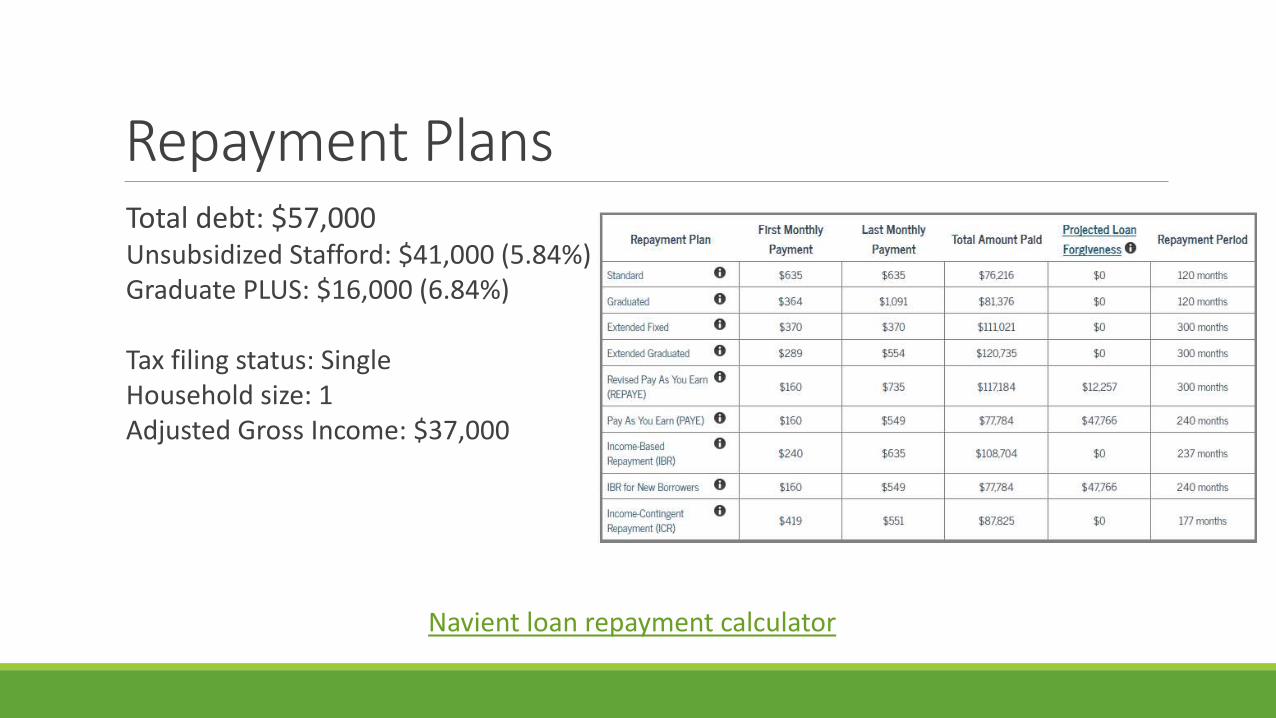

Repayment PlansTotal debt: $57,000Unsubsidized Stafford: $41,000 (5.84%)Graduate PLUS: $16,000 (6.84%)

Tax filing status: SingleHousehold size: 1Adjusted Gross Income: $37,000

Navient loan repayment calculator

Loan Forgiveness

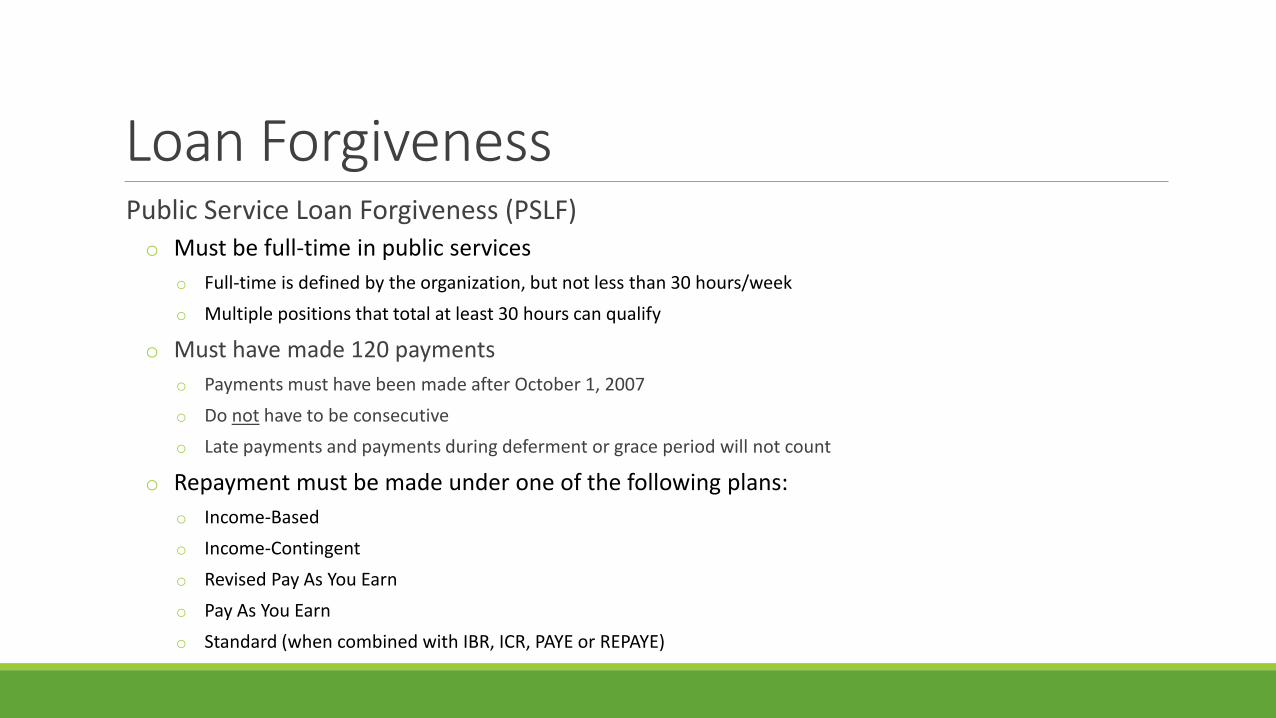

Loan ForgivenessPublic Service Loan Forgiveness (PSLF)

o Must be full-time in public services

o Full-time is defined by the organization, but not less than 30 hours/week

o Multiple positions that total at least 30 hours can qualify

o Must have made 120 payments

o Payments must have been made after October 1, 2007

o Do not have to be consecutive

o Late payments and payments during deferment or grace period will not count

o Repayment must be made under one of the following plans:

o Income-Based

o Income-Contingent

o Revised Pay As You Earn

o Pay As You Earn

o Standard (when combined with IBR, ICR, PAYE or REPAYE)

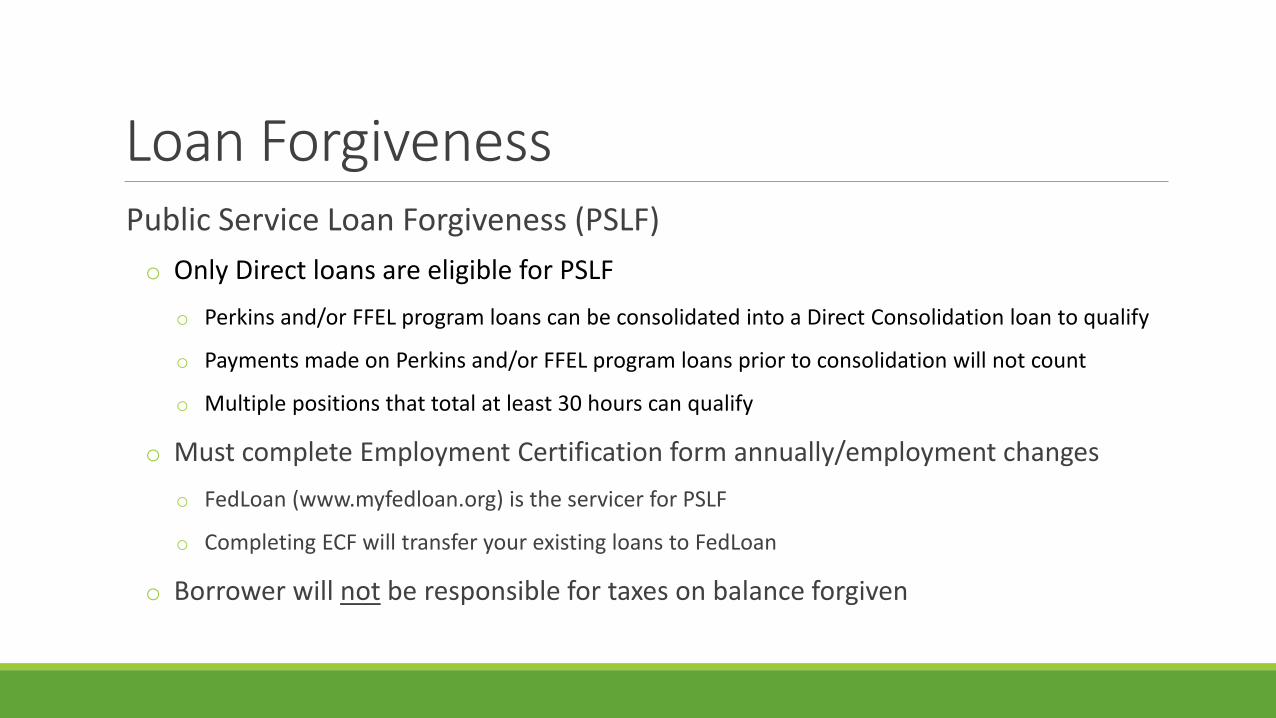

Loan ForgivenessPublic Service Loan Forgiveness (PSLF)

o Only Direct loans are eligible for PSLF

o Perkins and/or FFEL program loans can be consolidated into a Direct Consolidation loan to qualify

o Payments made on Perkins and/or FFEL program loans prior to consolidation will not count

o Multiple positions that total at least 30 hours can qualify

o Must complete Employment Certification form annually/employment changes

o FedLoan (www.myfedloan.org) is the servicer for PSLF

o Completing ECF will transfer your existing loans to FedLoan

o Borrower will not be responsible for taxes on balance forgiven

Eligible public service positions

o Federal, state or local government agency or entity

o Non-profit categorized as 501(c)(3)

o Qualifying employment may include:

o The organization must not be a labor union or partisan political organization

Loan Forgiveness

o Military Serviceo Public safetyo Law enforcemento Public health serviceso Public educationo Tribal agency/organization

or tribal college/university

o Public library serviceso School library serviceso Public interest law serviceso Early childhood educationo Public services for elderly or

individuals with disabilities

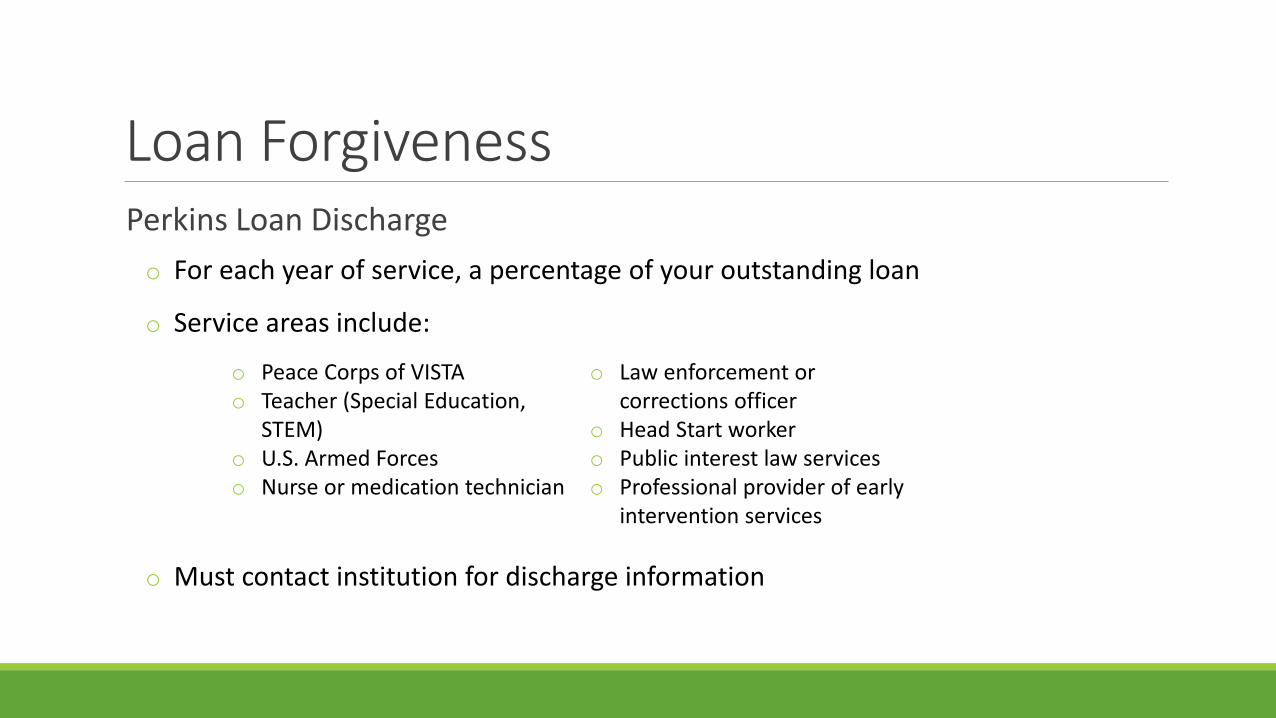

Perkins Loan Discharge

o For each year of service, a percentage of your outstanding loan

o Service areas include:

o Must contact institution for discharge information

Loan Forgiveness

o Peace Corps of VISTAo Teacher (Special Education,

STEM)o U.S. Armed Forceso Nurse or medication technician

o Law enforcement or corrections officer

o Head Start workero Public interest law serviceso Professional provider of early

intervention services

Consolidation

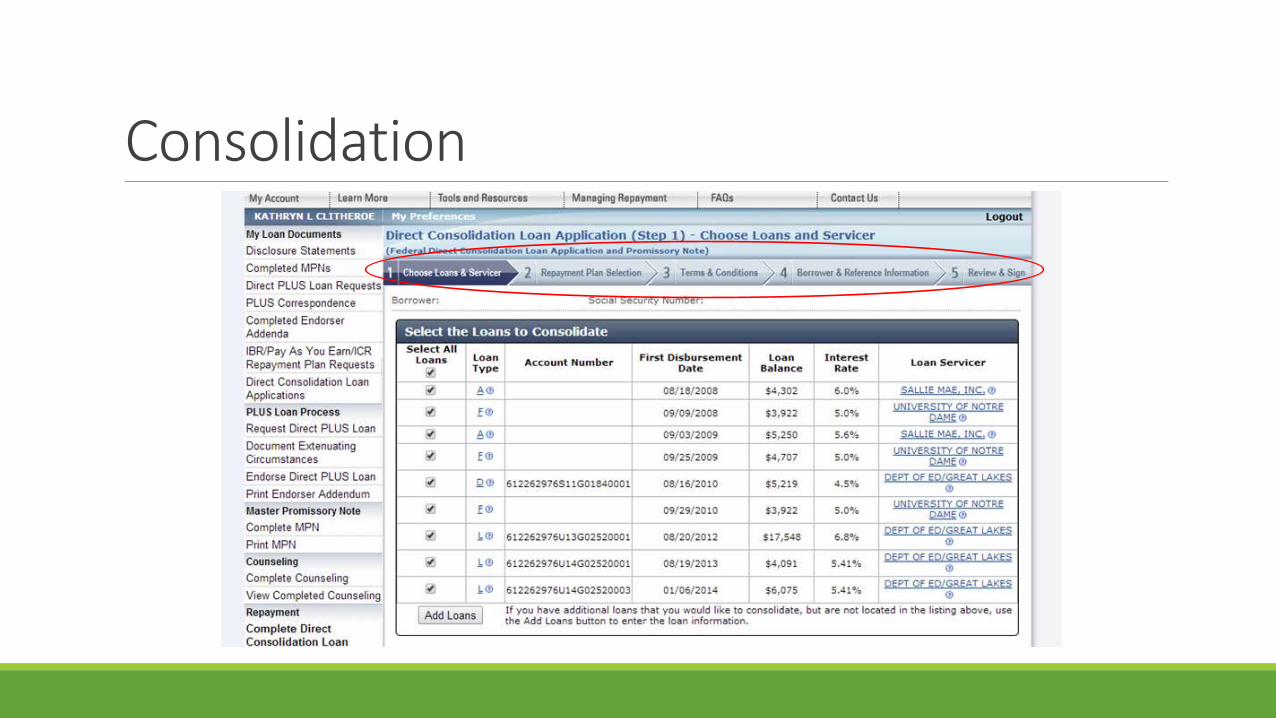

ConsolidationDirect Consolidation Loan

o Combines multiple federal loans, pays off individual balances

o One interest rate, one lender, one payment

o Eligible loans:

o Stafford

o Graduate PLUS

o Perkins

o Interest rate is a weighted average of all loans

o Up to 30 years to repay depending on loan balance

Consolidation

Repayment Plans: Income-Driven

Consolidation

Deferment & Forbearance

Deferment & ForbearanceDeferment

o Temporary suspension of loan payments

o Interest does not accrue on Subsidized Stafford or Perkins loans

o Unsubsidized and PLUS loans will accrue interest

o Qualifying situations

o Reenrollment in school

o Military service

o Unemployment

o Economic hardship (up to three years)

Deferment & ForbearanceForbearance

o Temporary postponement or reduction of payments due to financial difficulty

o Interest accrues on all loans

o Can be granted for up to 12 months at a time for no more than three years

Planning Ahead

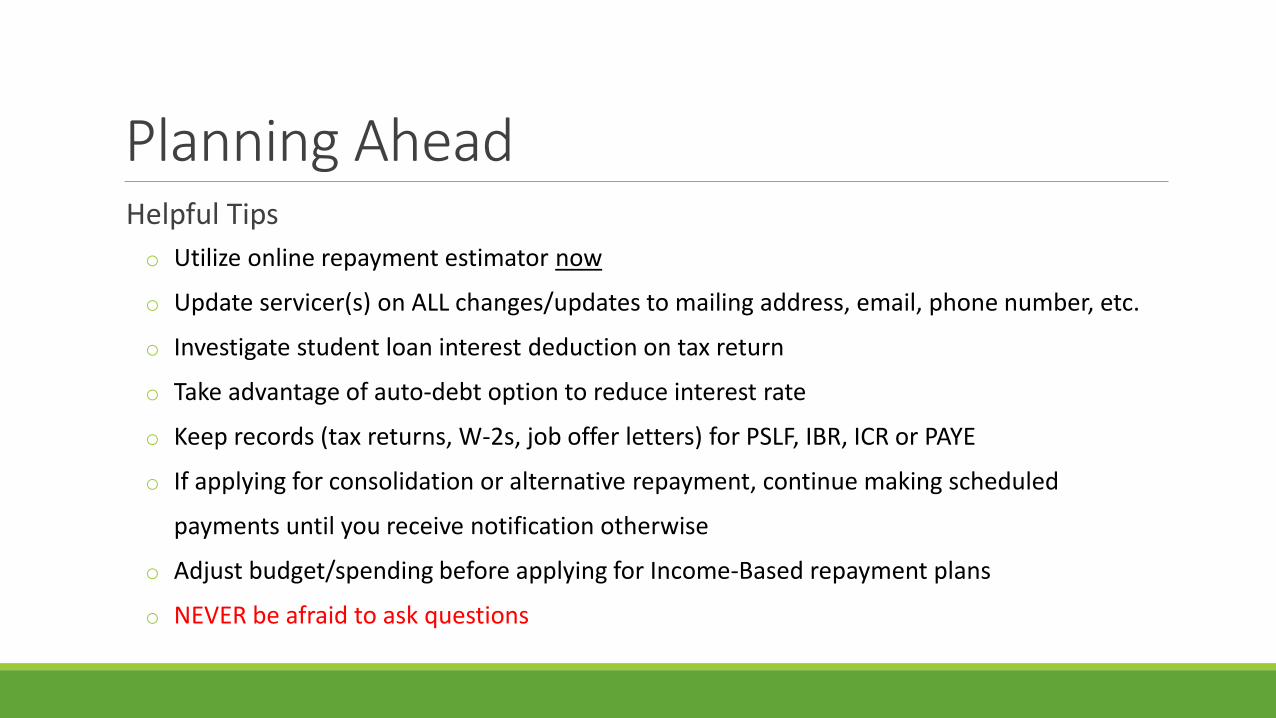

Planning AheadHelpful Tips

o Utilize online repayment estimator now

o Update servicer(s) on ALL changes/updates to mailing address, email, phone number, etc.

o Investigate student loan interest deduction on tax return

o Take advantage of auto-debt option to reduce interest rate

o Keep records (tax returns, W-2s, job offer letters) for PSLF, IBR, ICR or PAYE

o If applying for consolidation or alternative repayment, continue making scheduled

payments until you receive notification otherwise

o Adjust budget/spending before applying for Income-Based repayment plans

o NEVER be afraid to ask questions

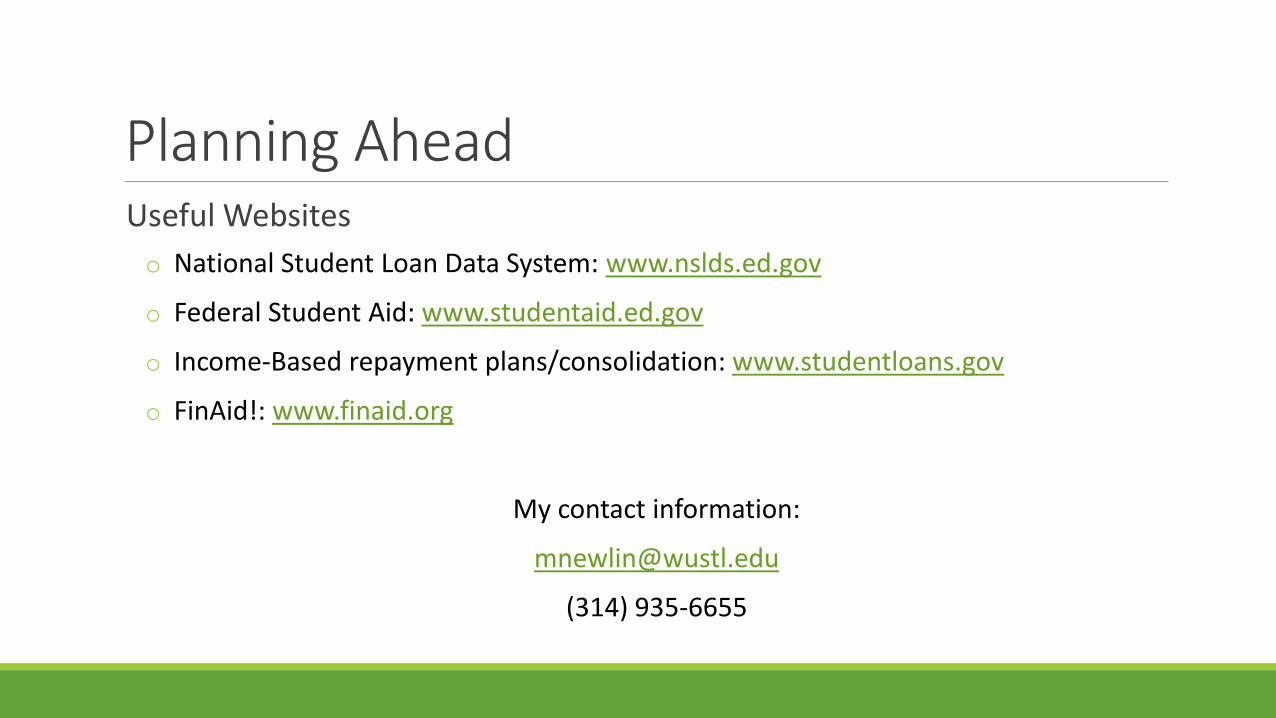

Planning AheadUseful Websites

o National Student Loan Data System: www.nslds.ed.gov

o Federal Student Aid: www.studentaid.ed.gov

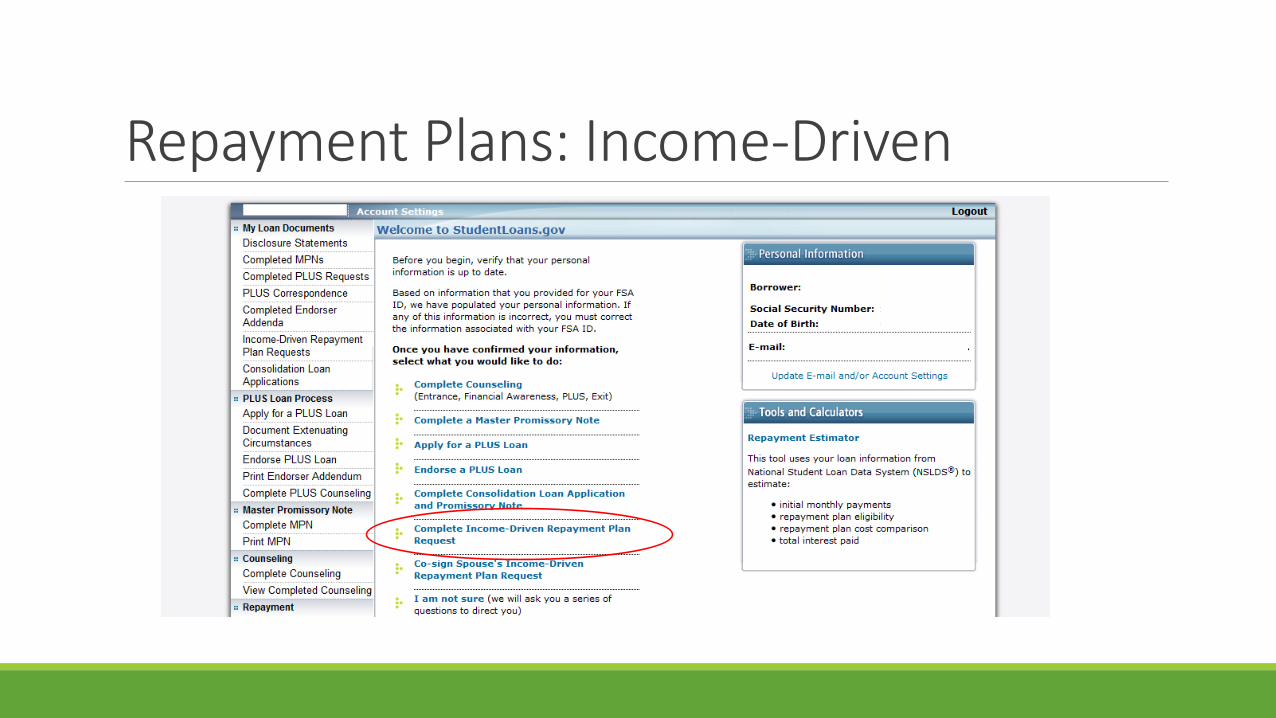

o Income-Based repayment plans/consolidation: www.studentloans.gov

o FinAid!: www.finaid.org

My contact information:

(314) 935-6655

Questions?

Recommended