Data Centre Connectivity Nice 30th of June 2016

Rev A

Per Larsson, Executive Network Architect

• Group HQ in Copenhagen, Denmark • 8 600 employees • Turnover: 23,3 billion DKK (2014) • One of the largest Nordic Networks • Covers 80 % of the business

areas in the region • 1 800 points of presence • Subsidiaries in Sweden and Norway • Extended reach

• Finland • Baltics, Iceland, Faeroe Islands,

Greenland • Continental Europe & the UK

TDC in the Nordic region

2

3

Why is the Telco interested in DC?

?

4

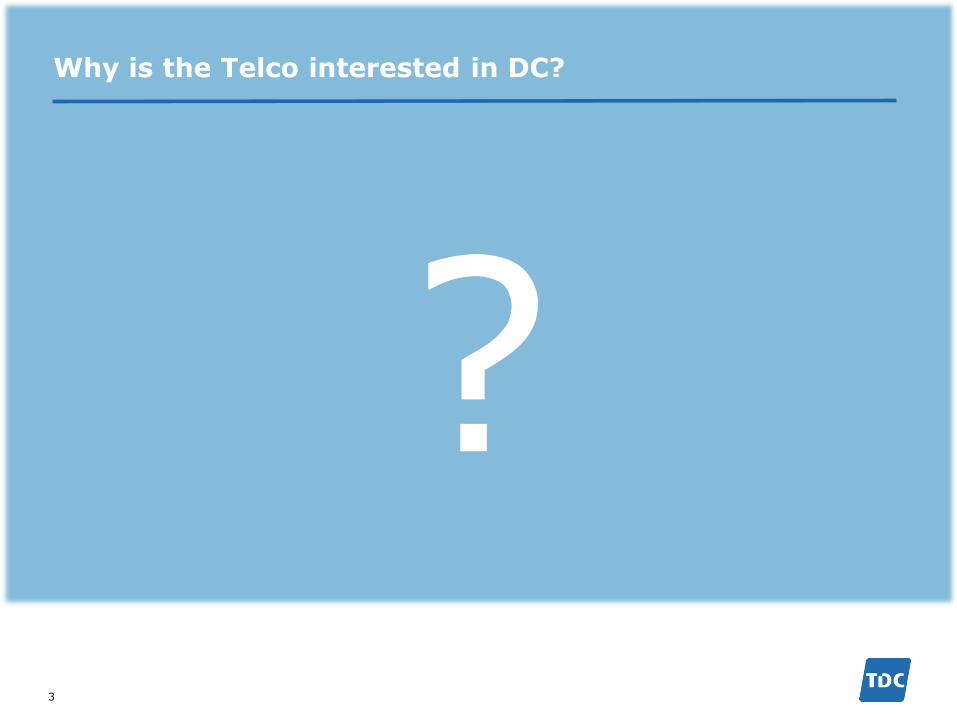

Global IP-traffic 2014 – 2019, Exabytes

2023

2629

324048

58

72

161172417

112

90

2019 2018 2015 2014

+24%

2016 2017

60

4

72

3

88

109

135

168

Managed IP

Fixed Internet

Mobile data

Source: Cisco VNI 2015

All words ever spoken by

humans ~ 5 EB

5

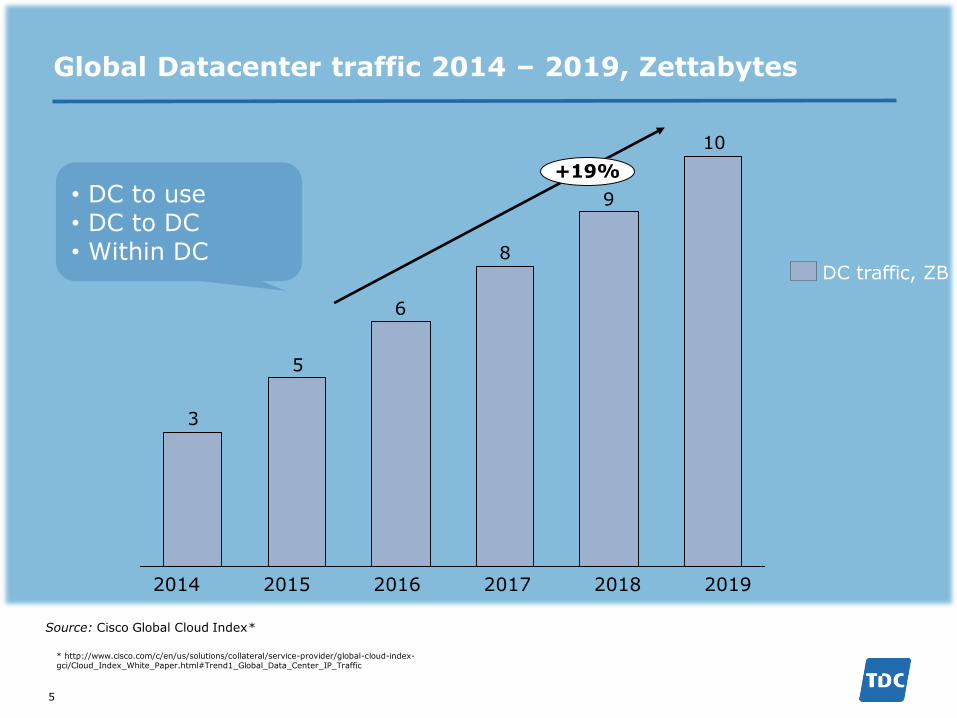

Global Datacenter traffic 2014 – 2019, Zettabytes

Source: Cisco Global Cloud Index*

* http://www.cisco.com/c/en/us/solutions/collateral/service-provider/global-cloud-index-gci/Cloud_Index_White_Paper.html#Trend1_Global_Data_Center_IP_Traffic

10

9

8

6

5

3

2016 2014 2015

+19%

2017 2018 2019

DC traffic, ZB

• DC to use • DC to DC • Within DC

6

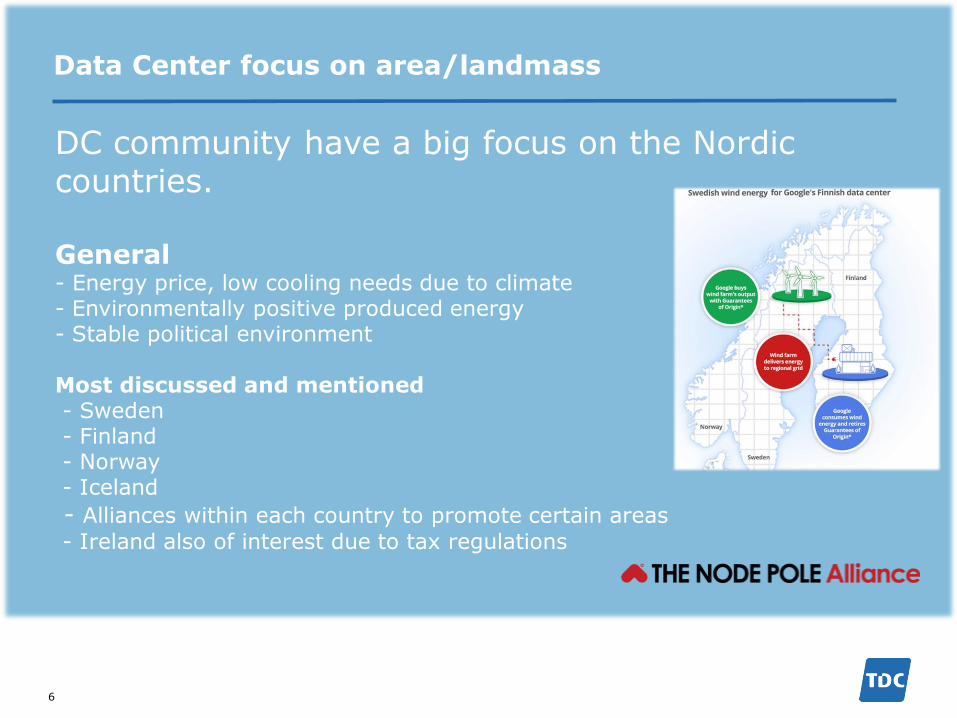

DC community have a big focus on the Nordic countries. General - Energy price, low cooling needs due to climate - Environmentally positive produced energy - Stable political environment Most discussed and mentioned - Sweden - Finland - Norway - Iceland

- Alliances within each country to promote certain areas

- Ireland also of interest due to tax regulations

Data Center focus on area/landmass

7

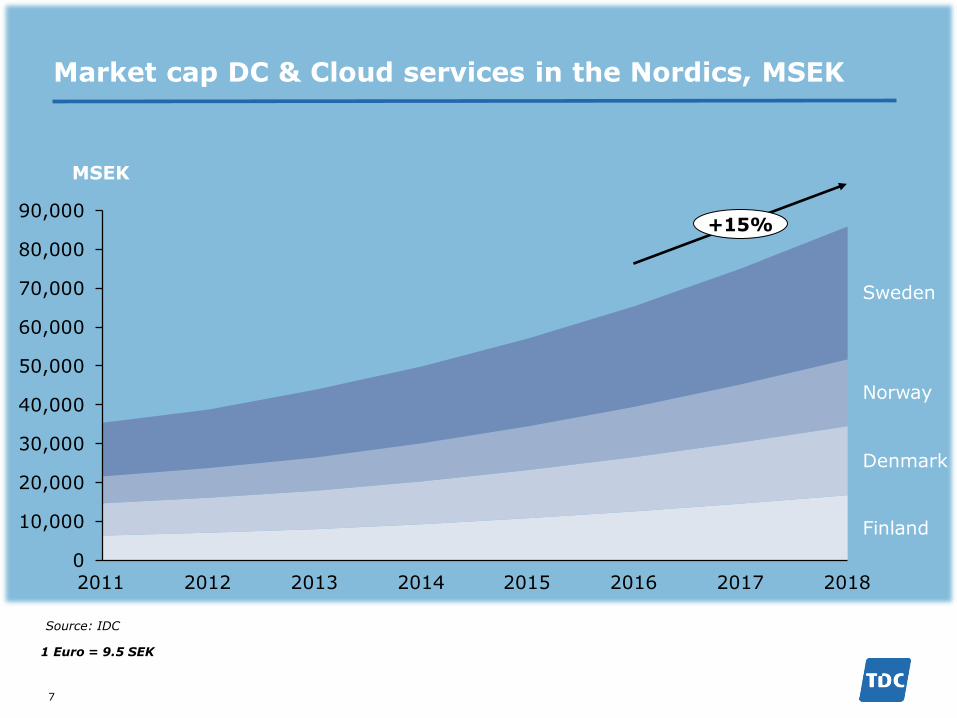

Market cap DC & Cloud services in the Nordics, MSEK

Source: IDC

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

MSEK

Denmark

+15%

Norway

Finland

Sweden

2012 2011 2015 2017 2014 2016 2013 2018

1 Euro = 9.5 SEK

8

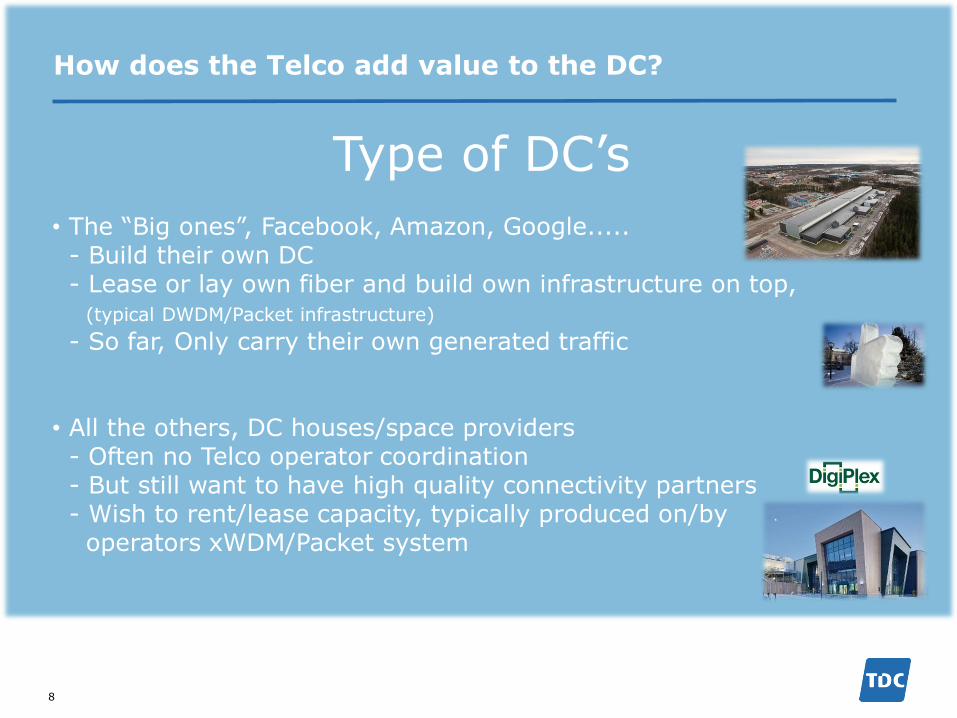

How does the Telco add value to the DC?

• The “Big ones”, Facebook, Amazon, Google..... - Build their own DC - Lease or lay own fiber and build own infrastructure on top, (typical DWDM/Packet infrastructure)

- So far, Only carry their own generated traffic • All the others, DC houses/space providers - Often no Telco operator coordination - But still want to have high quality connectivity partners - Wish to rent/lease capacity, typically produced on/by operators xWDM/Packet system

Type of DC’s

9

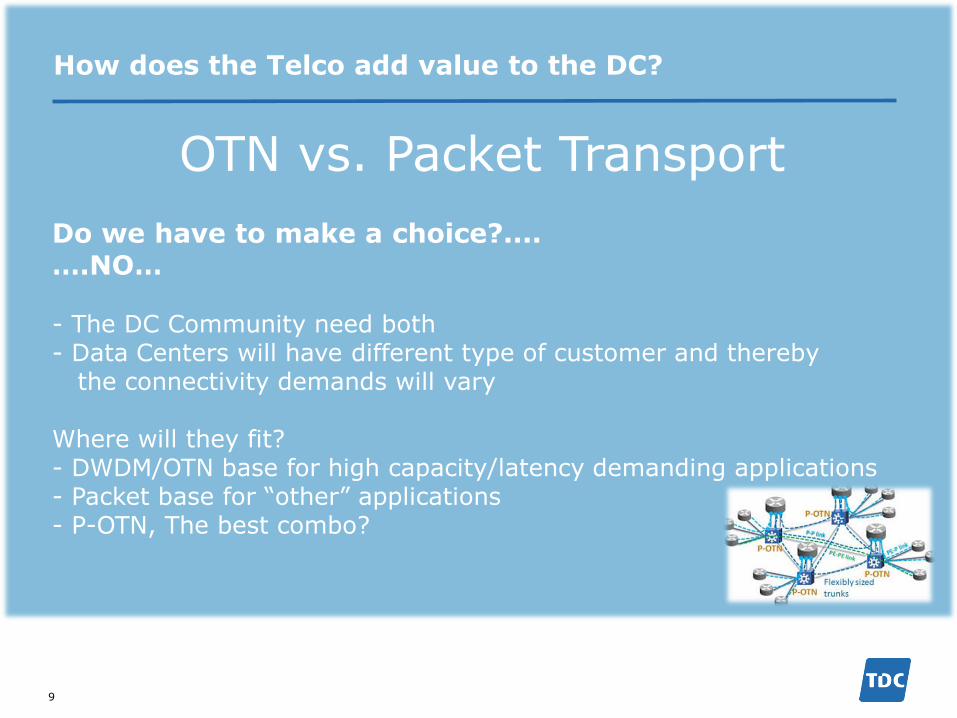

How does the Telco add value to the DC?

Do we have to make a choice?.... ….NO… - The DC Community need both - Data Centers will have different type of customer and thereby the connectivity demands will vary Where will they fit? - DWDM/OTN base for high capacity/latency demanding applications - Packet base for “other” applications - P-OTN, The best combo?

OTN vs. Packet Transport

10

How does the Telco add value to the DC?

Client 1G - > 10G- > 100G….. ->? - 10G up to 150km on black fiber from Backbone POP, or extended by xWDM metro - Relatively inexpensive

- 100G up to 40km on black fiber from Backbone POP - Expensive HW (CFPx ER)

- xWDM metro extension also expensive - Will the Customer/DC come closer the carrier’s POP? probably not

- The Carrier’s main network/POP has to come to the Customer/DC

- Expand main network are not “for free” - Are we able to build a business case here?

Connectivity challenges

11

...What about your communications capabilities...?

How does the Telco add value to the DC?

....Our DC has fiber from the local provider to the facility, even dual

entries…

12

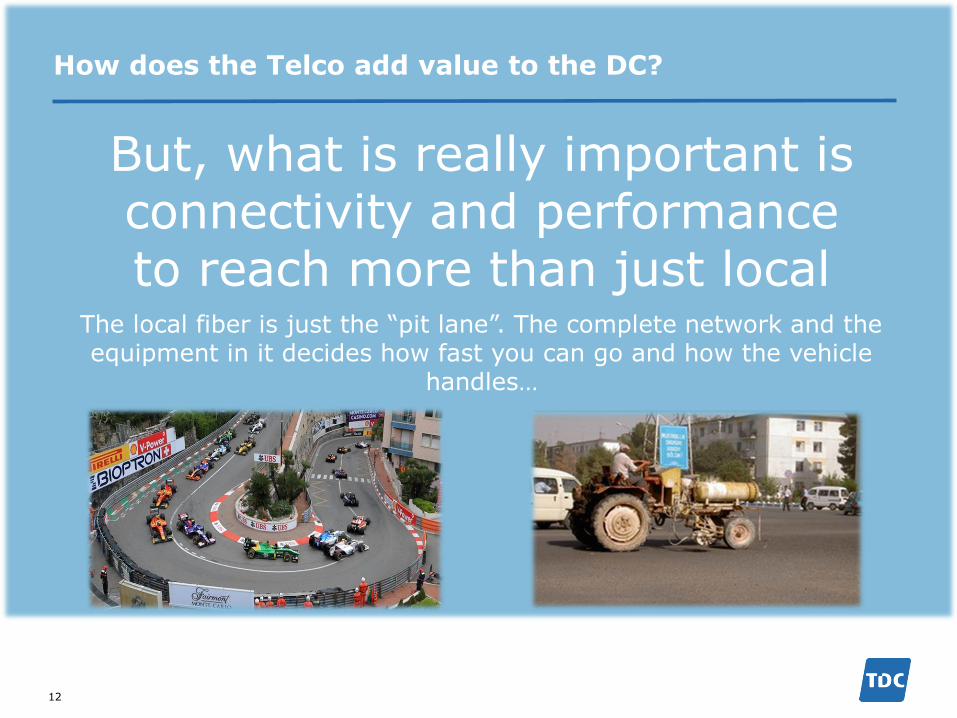

How does the Telco add value to the DC?

The local fiber is just the “pit lane”. The complete network and the equipment in it decides how fast you can go and how the vehicle

handles…

But, what is really important is connectivity and performance to reach more than just local

13

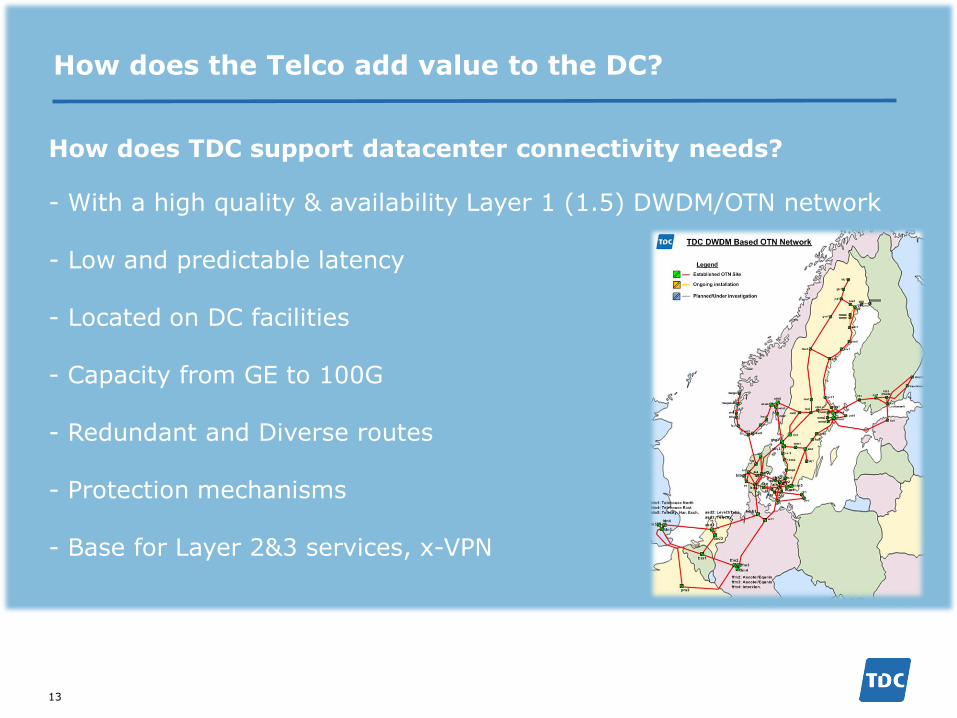

How does TDC support datacenter connectivity needs?

How does the Telco add value to the DC?

- With a high quality & availability Layer 1 (1.5) DWDM/OTN network - Low and predictable latency

- Located on DC facilities - Capacity from GE to 100G - Redundant and Diverse routes - Protection mechanisms - Base for Layer 2&3 services, x-VPN

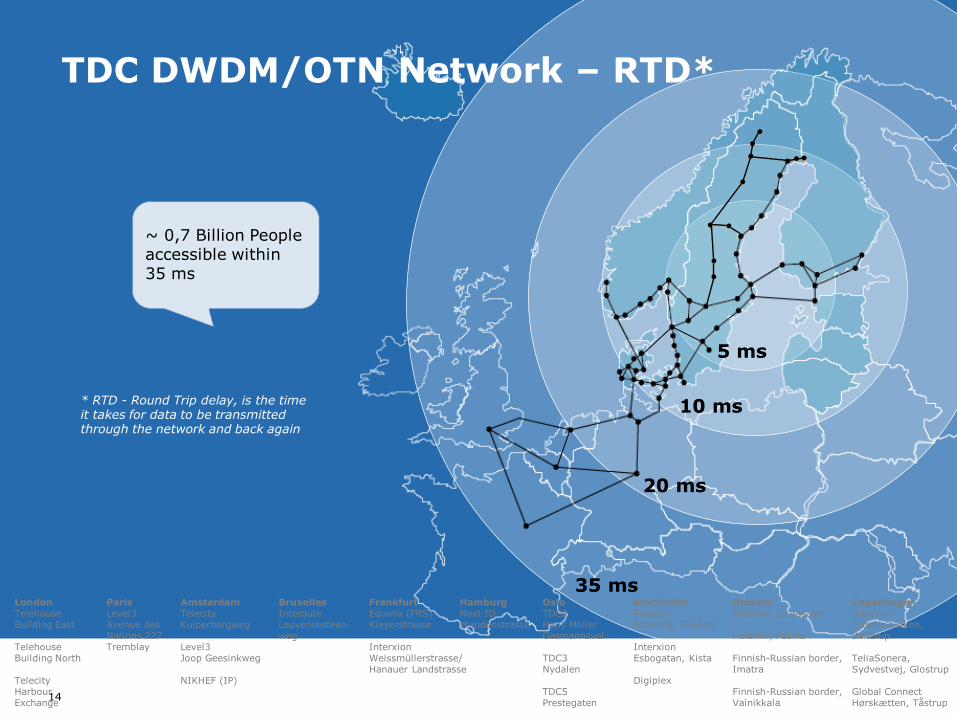

~ 0,7 Billion People accessible within 35 ms

TDC DWDM/OTN Network – RTD*

5 ms

10 ms

20 ms

35 ms

* RTD - Round Trip delay, is the time it takes for data to be transmitted through the network and back again

London Telehouse Building East Telehouse Building North Telecity Harbour Exchange

Amsterdam Telecity Kuiperbergweg Level3 Joop Geesinkweg NIKHEF (IP)

Bruxelles Interoute Leuvensesteen- weg

Frankfurt Equinix (FRS) Kleyerstrasse Interxion Weissmüllerstrasse/ Hanauer Landstrasse

Hamburg Next ID Wendenstrasse

Oslo TDC2 Hans Möller Gasmannsvei TDC3 Nydalen TDC5 Prestegaten

Helsinki Helsinki, Lautasaari Helsinki, Pasilia Finnish-Russian border, Imatra Finnish-Russian border, Vainikkala

Copenhagen Interxion Industriparken, Ballerup TeliaSonera, Sydvestvej, Glostrup Global Connect Hørskætten, Tåstrup

Paris Level3 Avenue des Nations 227 Tremblay

Stockholm Telecity Bromma, Sköndal Interxion Esbogatan, Kista Digiplex

14

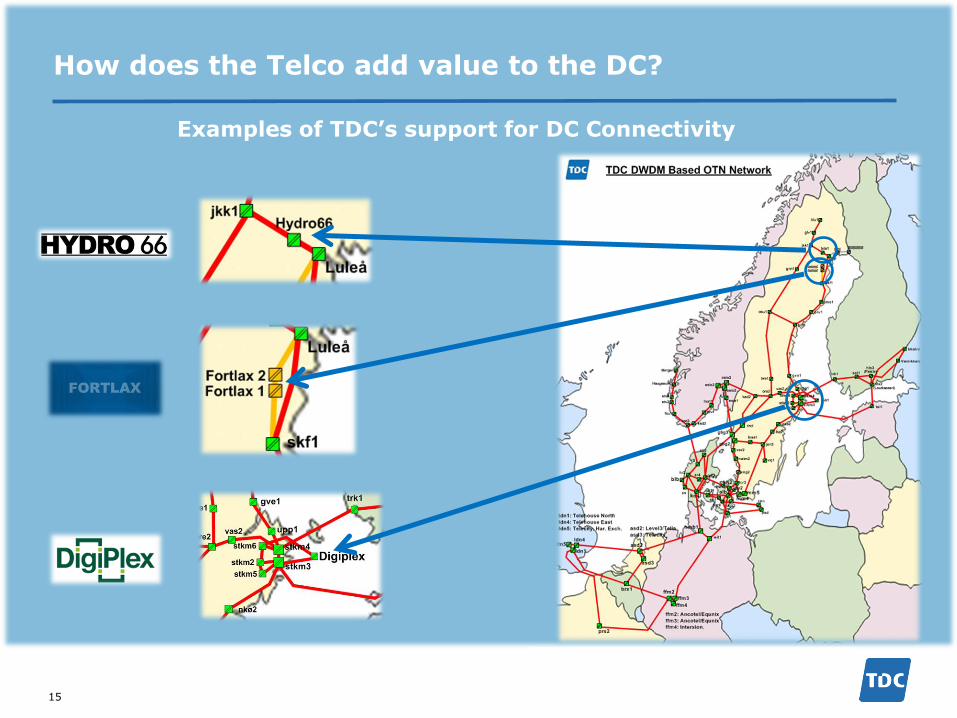

15

Examples of TDC’s support for DC Connectivity

How does the Telco add value to the DC?

Wrap-up

- Data growth drives DC and connectivity

requirements, and they co-exist

- Latency is a often “key factor” in the DC market,

where customers expect their data to be available

and at their fingertips

- The complete network gives the performance –

the chain is no stronger than its weakest link

16

Thank you!

17

Recommended