Cost Management Cost Management

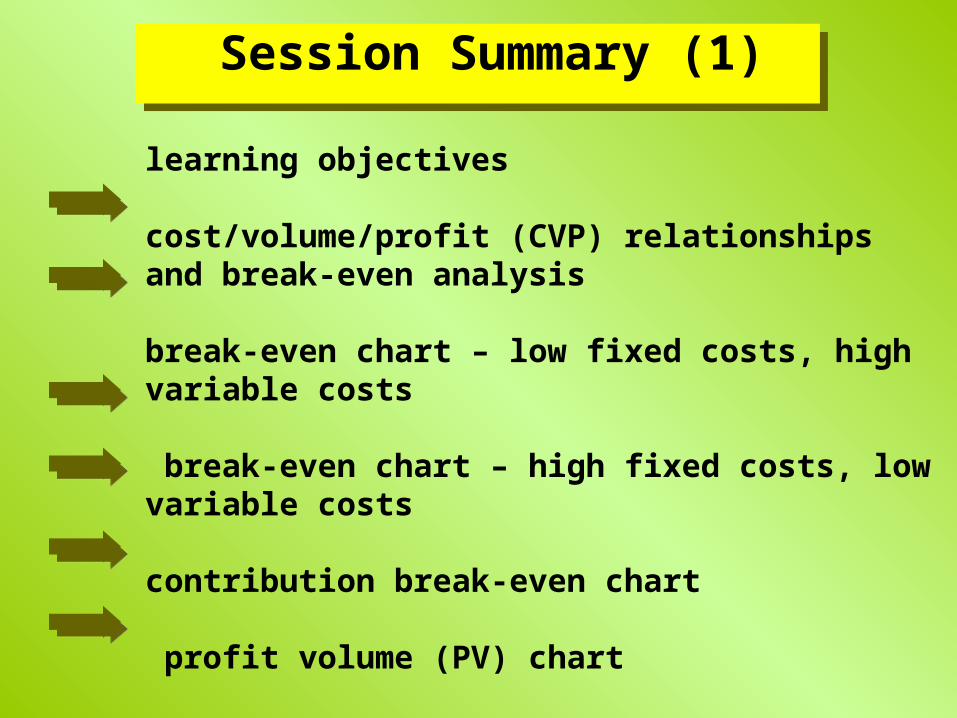

learning objectives

cost/volume/profit (CVP) relationships and break-even analysis

break-even chart – low fixed costs, high variable costs

break-even chart – high fixed costs, low variable costs

contribution break-even chart

profit volume (PV) chart

Session Summary (1) Session Summary (1)

CVP and break-even analysis

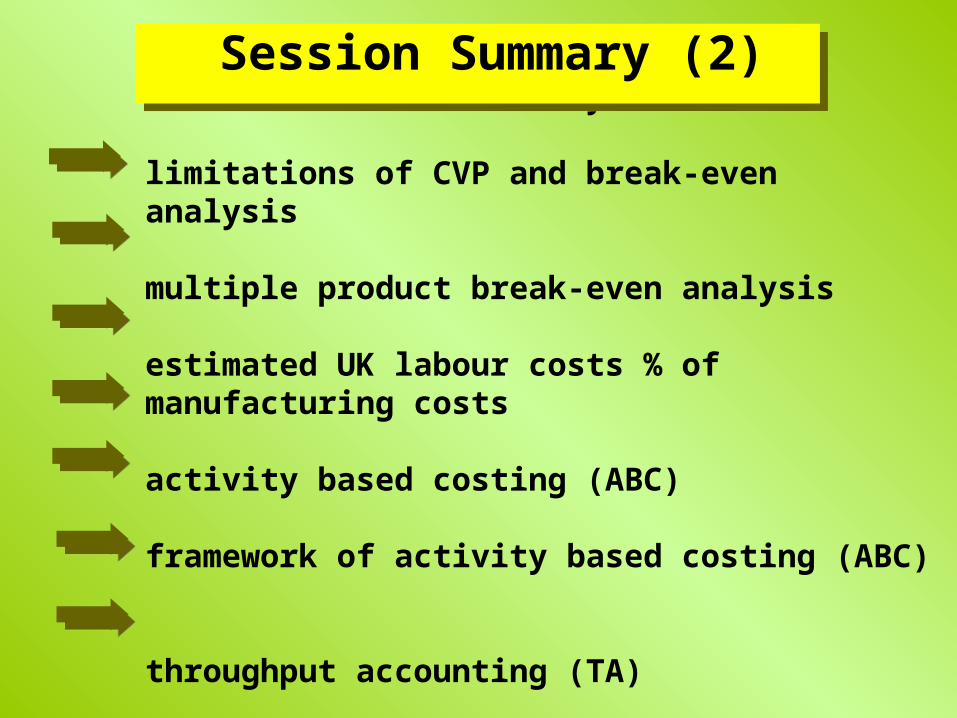

limitations of CVP and break-even analysis

multiple product break-even analysis

estimated UK labour costs % of manufacturing costs activity based costing (ABC)

framework of activity based costing (ABC) throughput accounting (TA)

Session Summary (2) Session Summary (2)

throughput report

life cycle costing

target costing

benchmarking

kaizen

cost of quality (COQ)

non financial indicators

balanced scorecard

Session Summary (3) Session Summary (3)

explain cost/volume/profit (CVP) relationships andbreak-even analysis

identify the limitations of CVP analysis

outline the more recently developed techniques of activity based costing (ABC), and throughput accounting (TA)

identify the conditions appropriate to the use of life cycle costing

Learning Objectives (1) Learning Objectives (1)

apply the principles of target costing

consider benchmarking as a technique to identify best practice and enable the introduction of appropriate performance improvement targets outline kaizen as technique for continuous improvementof all aspects of business performance

explain the types of information and measurements used in lean accounting

Learning Objectives (2) Learning Objectives (2)

use cost of quality (COQ) to identify areas for improvement and cost reduction within each of the processes throughout the business

appreciate the importance of, and consider the use of both financial and non-financial indicators in the evaluation of business performance

consider the use of both financial and non-financial measures incorporated into performance measurement systems such as the balanced scorecard

Learning Objectives (3) Learning Objectives (3)

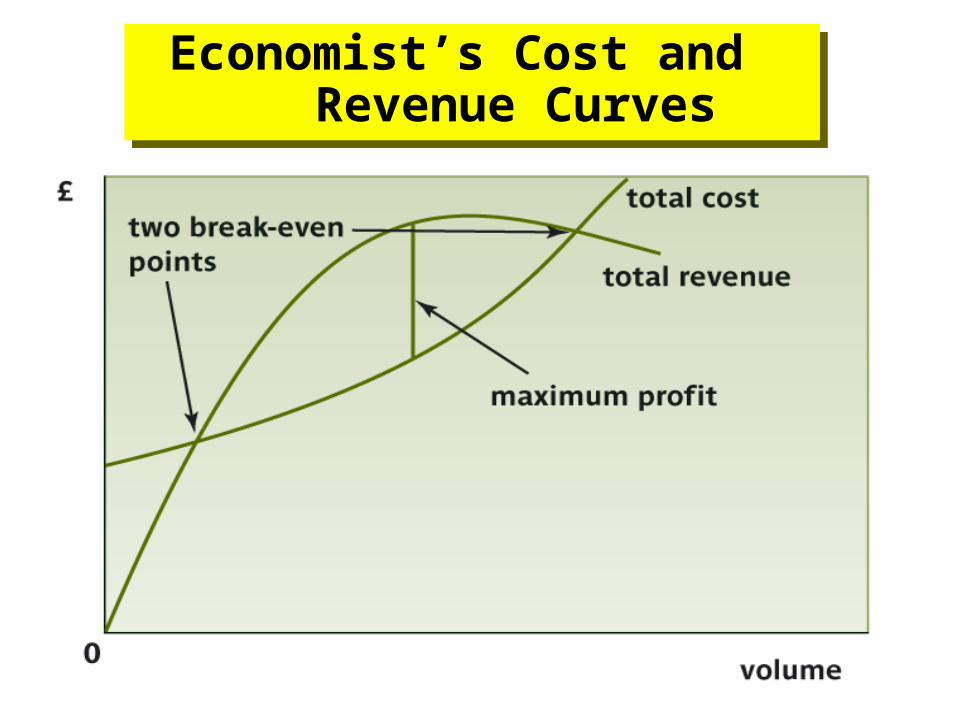

Economist’s Cost and Revenue Curves

Economist’s Cost and Revenue Curves

Cost/volume/profit (CVP) analysis may be used

to determine the break-even position of a business

to provide sensitivity analyses on the impact on the business of changes to any of the variables used to calculate break-even the break-even point is the level of activity at whichthere is neither profit nor loss

Cost/Volume/Profit (CVP) Relationships

and Break-Even Analysis (1)

Cost/Volume/Profit (CVP) Relationships

and Break-Even Analysis (1)

There are three fundamental cost/revenue relationships that form the basis of CVP analysis

total costs = variable costs + fixed costs contribution = total revenue - variable costs profit (or operating income) = total revenue - total costs

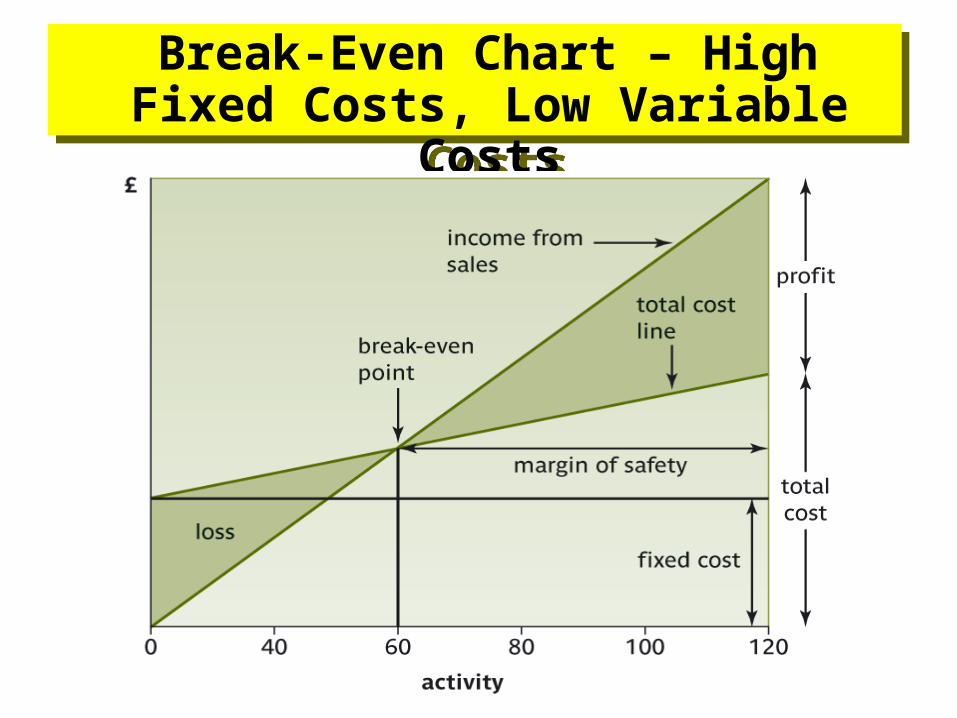

the slopes of the total cost lines in the following twocharts represent the unit variable costs

Cost/Volume/Profit (CVP) Relationships

and Break-Even Analysis (2)

Cost/Volume/Profit (CVP) Relationships

and Break-Even Analysis (2)

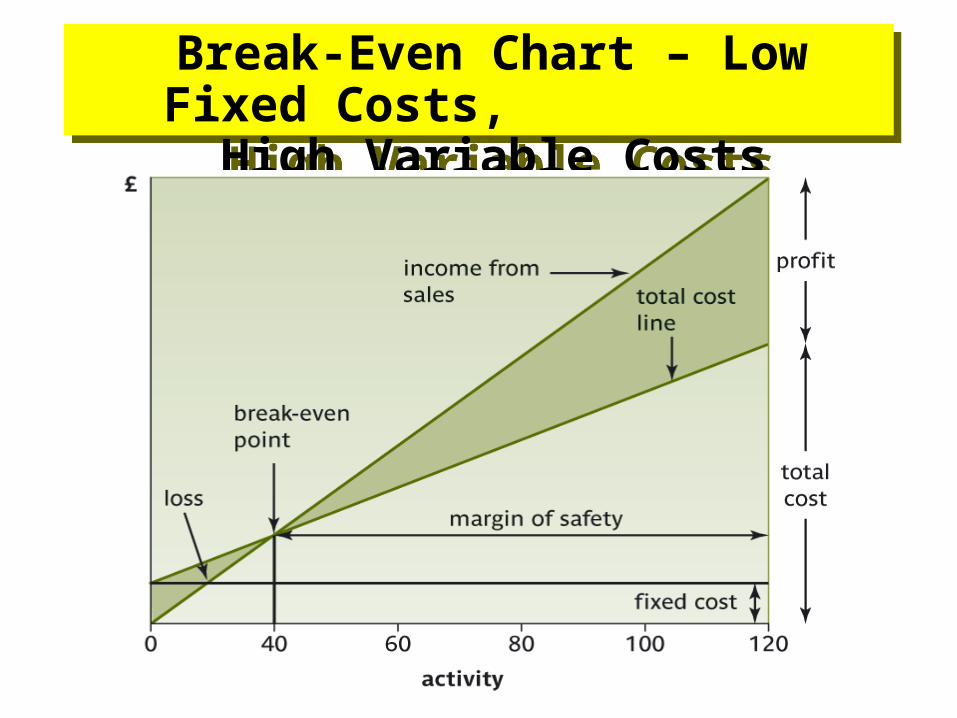

Break-Even Chart – Low Fixed Costs, High

Variable Costs

Break-Even Chart – Low Fixed Costs, High

Variable Costs

Break-Even Chart – High Fixed Costs, Low Variable

Costs

Break-Even Chart – High Fixed Costs, Low Variable

Costs

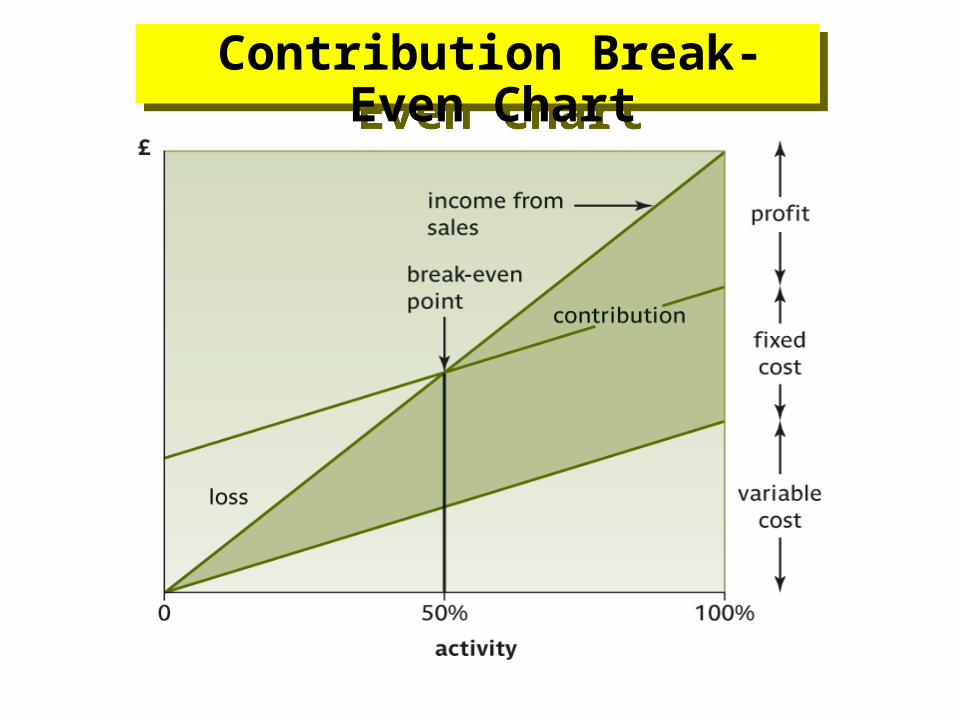

Contribution Break-Even Chart

Contribution Break-Even Chart

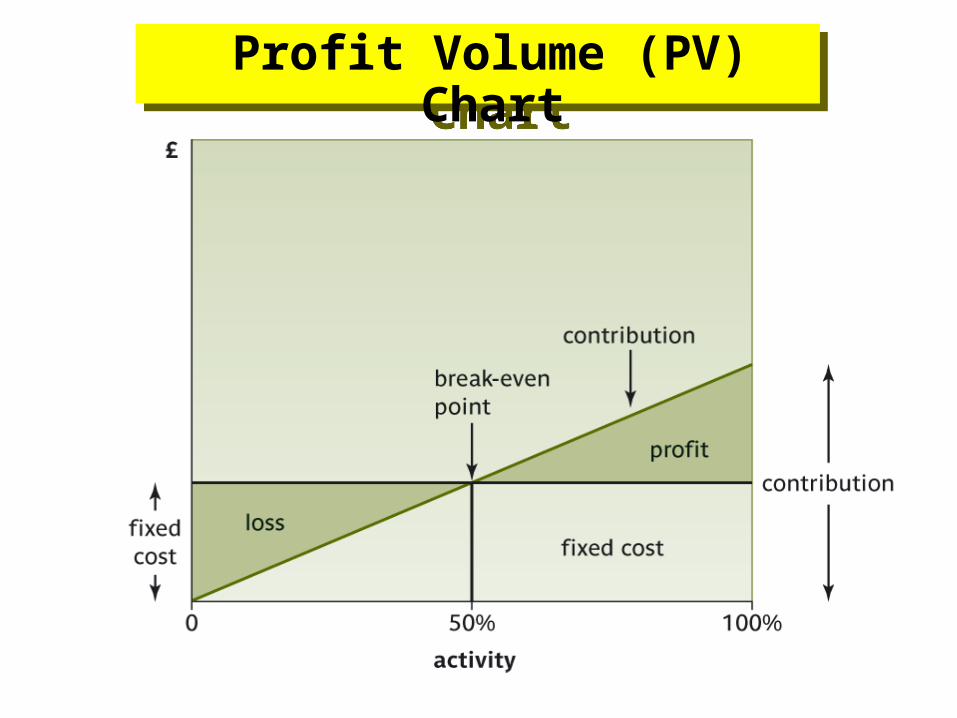

Profit Volume (PV) Chart

Profit Volume (PV) Chart

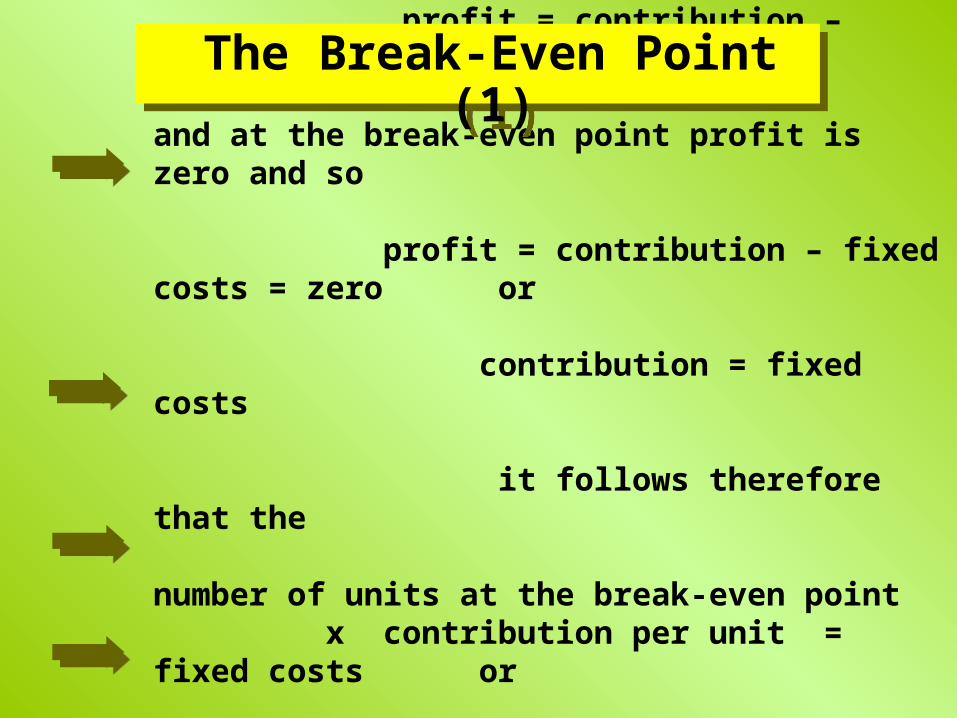

profit = contribution – fixed costs

and at the break-even point profit is zero and so profit = contribution – fixed costs = zero or

contribution = fixed costs

it follows therefore that the

number of units at the break-even point x contribution per unit = fixed costs or number of units at break-even = fixed costs contribution per unit

The Break-Even Point (1)

The Break-Even Point (1)

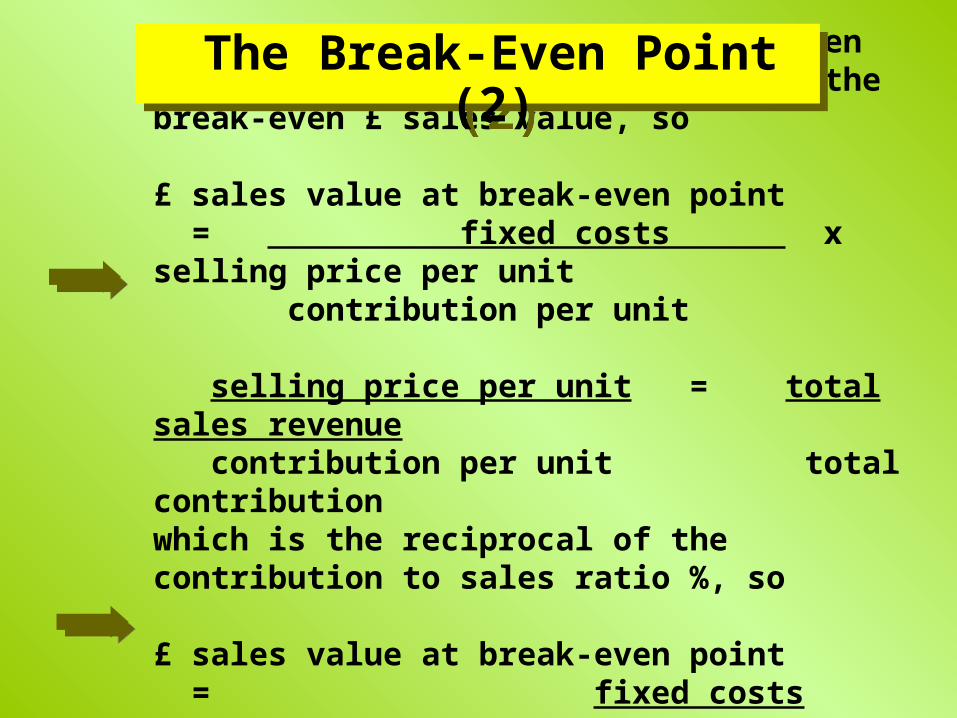

The number of units at the break-even point x selling price per unit is the break-even £ sales value, so £ sales value at break-even point = fixed costs x selling price per unit contribution per unit

selling price per unit = total sales revenue contribution per unit total contribution which is the reciprocal of the contribution to sales ratio %, so £ sales value at break-even point = fixed costs

contribution to sales ratio %

The Break-Even Point (2)

The Break-Even Point (2)

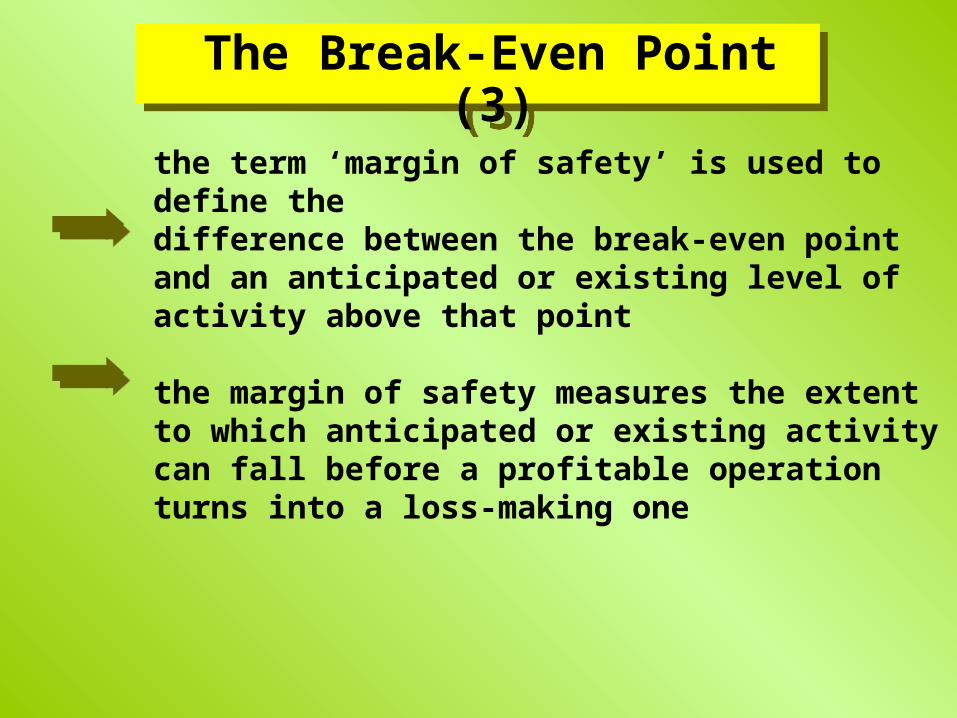

the term ‘margin of safety’ is used to define thedifference between the break-even point and an anticipated or existing level of activity above that point

the margin of safety measures the extent to which anticipated or existing activity can fall before a profitable operation turns into a loss-making one

The Break-Even Point (3)

The Break-Even Point (3)

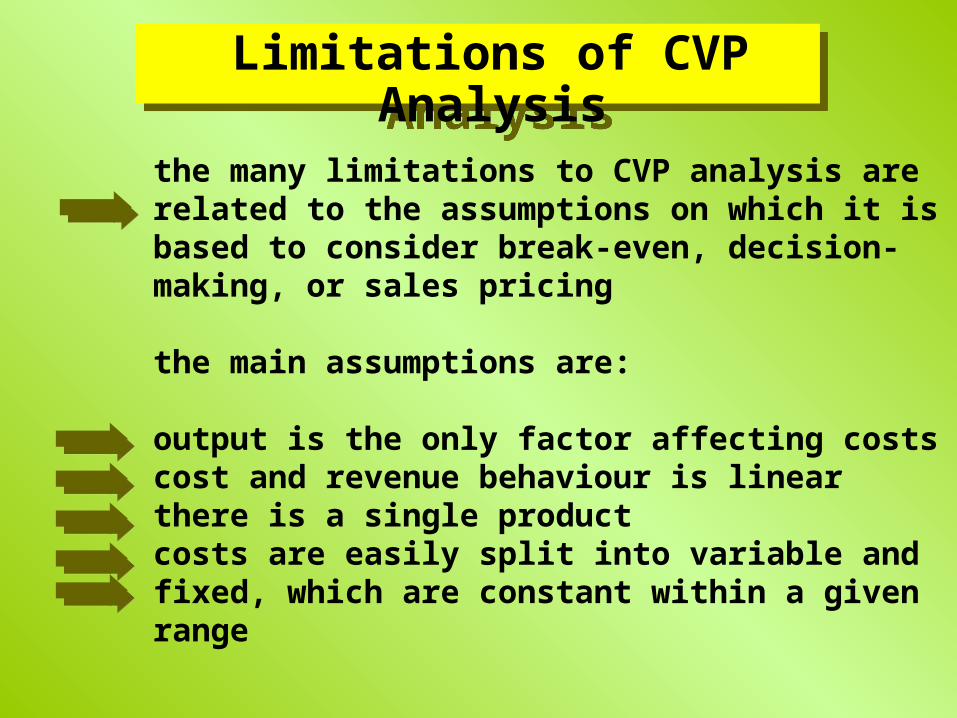

the many limitations to CVP analysis are related to the assumptions on which it is based to consider break-even, decision-making, or sales pricing

the main assumptions are:

output is the only factor affecting costscost and revenue behaviour is linearthere is a single productcosts are easily split into variable and fixed, which are constant within a given range

Limitations of CVP Analysis

Limitations of CVP Analysis

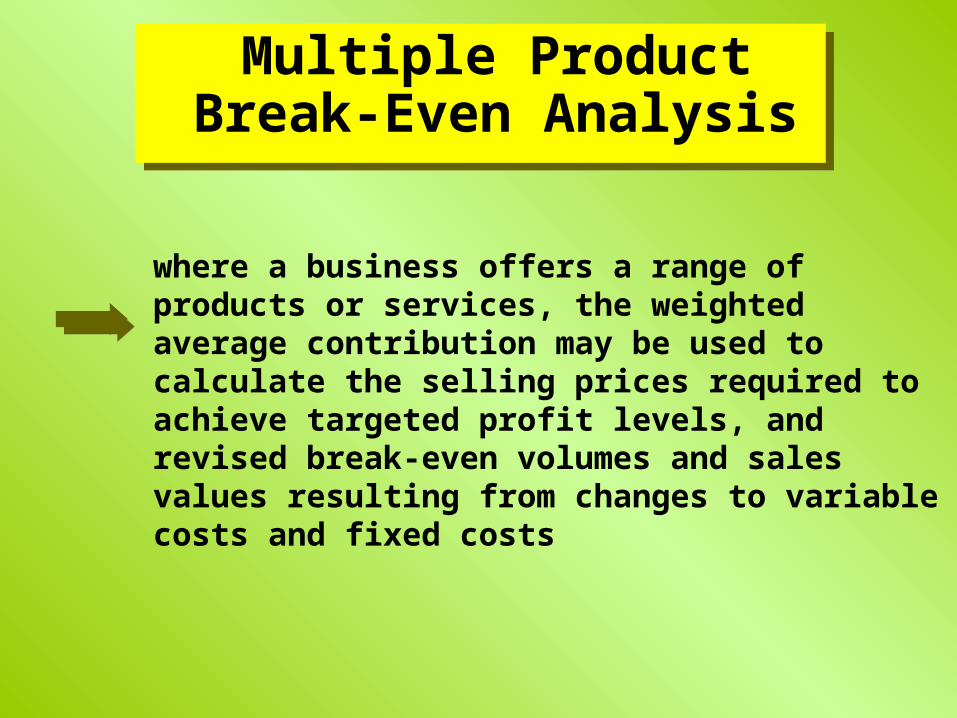

where a business offers a range of products or services, the weighted average contribution may be used to calculate the selling prices required to achieve targeted profit levels, and revised break-even volumes and sales values resulting from changes to variable costs and fixed costs

Multiple Product Break-Even Analysis Multiple Product

Break-Even Analysis

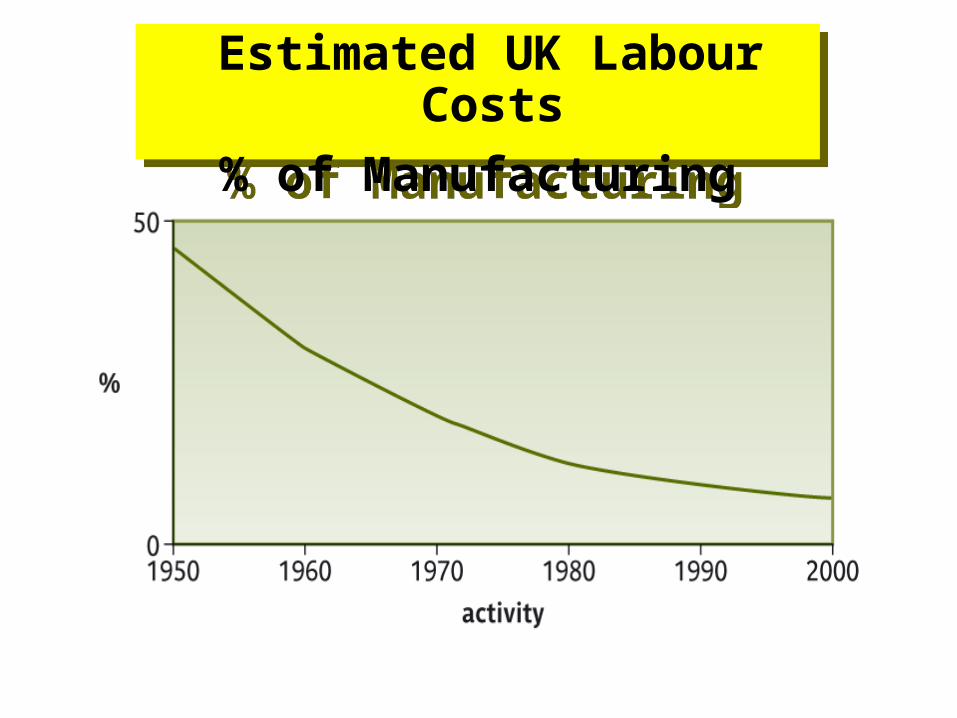

Estimated UK Labour Costs

% of Manufacturing Costs

Estimated UK Labour Costs

% of Manufacturing Costs

the more recently-developed techniques of activity based costing (ABC) and throughput accounting (TA) are approaches that attempt to overcome the problem of allocation and apportionment of overheads

Activity Based Costing (ABC)

Activity Based Costing (ABC)

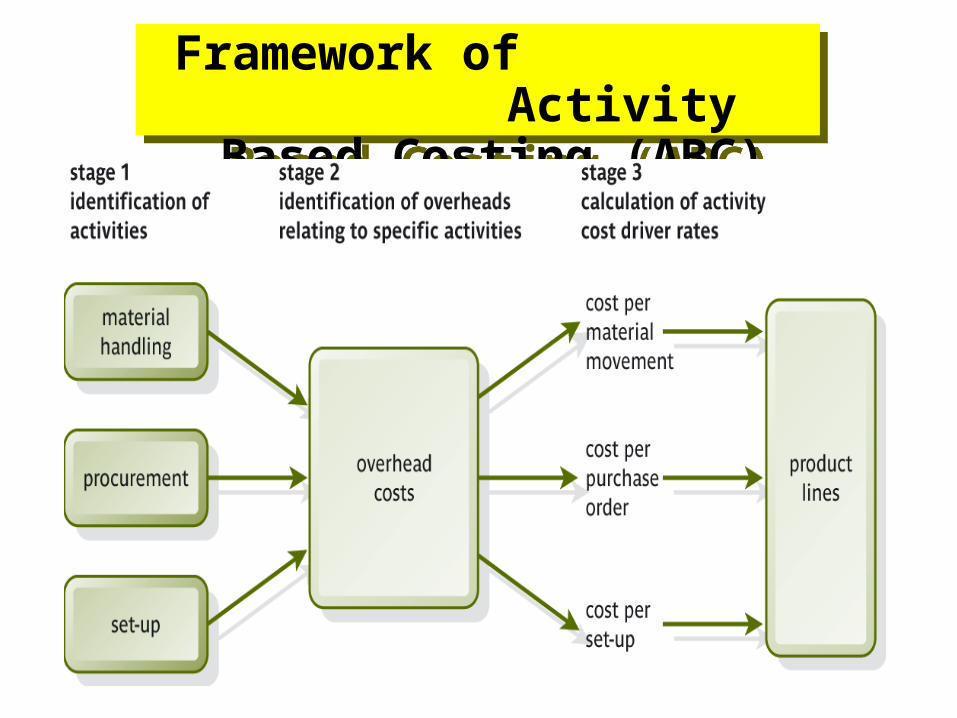

Framework of Activity Based Costing (ABC)

Framework of Activity Based Costing (ABC)

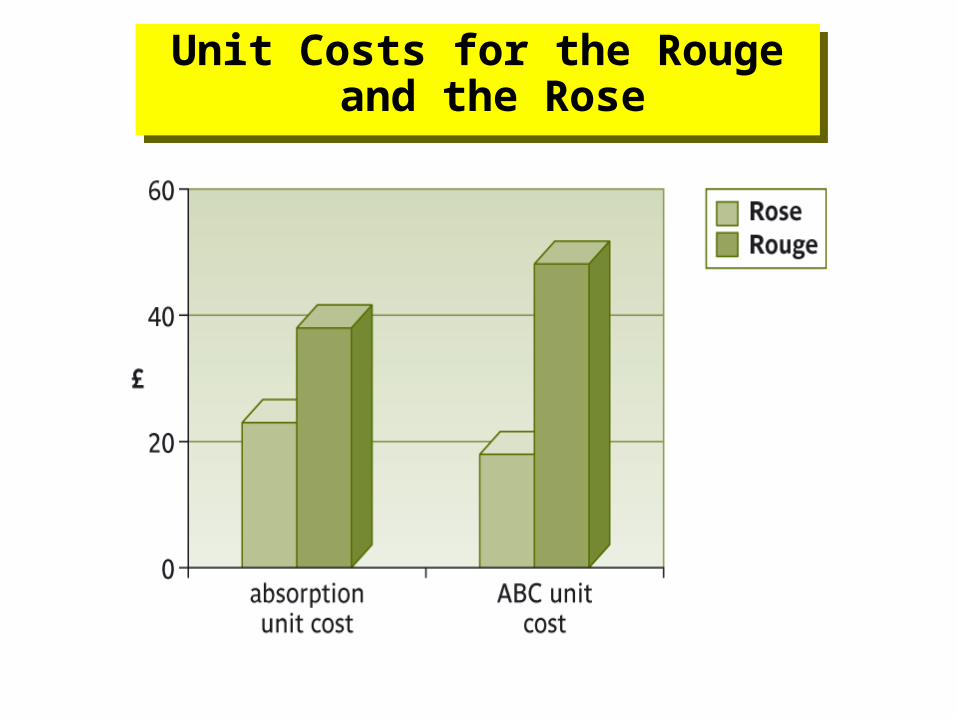

Unit Costs for the Rouge and the Rose

Unit Costs for the Rouge and the Rose

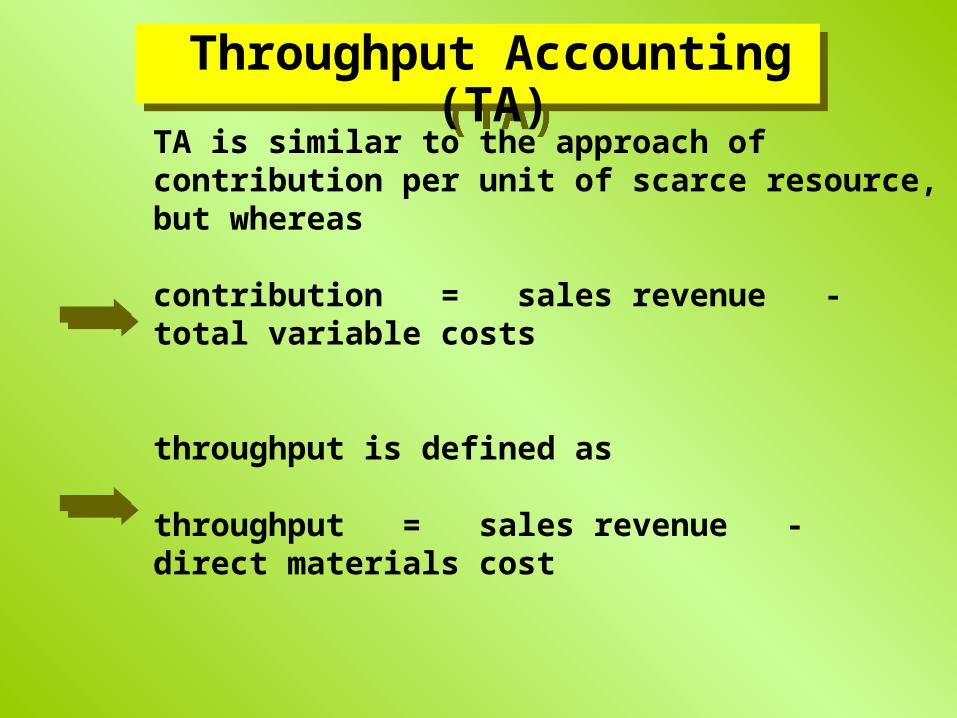

TA is similar to the approach of contribution per unit of scarce resource, but whereas contribution = sales revenue - total variable costs

throughput is defined as throughput = sales revenue - direct materials cost

Throughput Accounting (TA)

Throughput Accounting (TA)

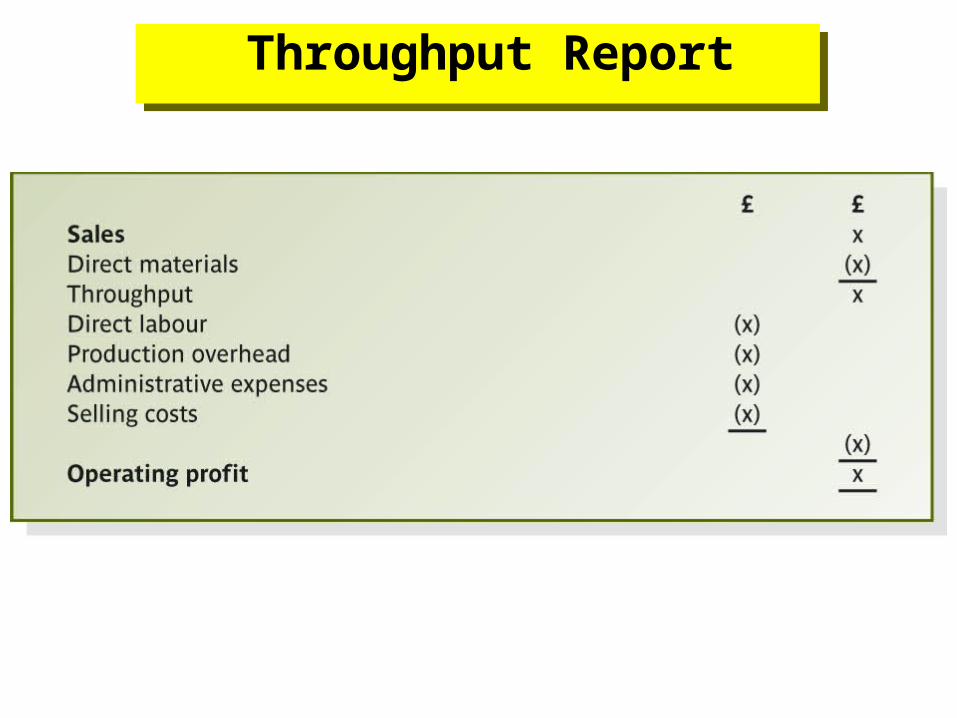

Throughput Report Throughput Report

life cycle costing uses maintenance of cost records over entire asset lives so that decisions regarding acquisitionor disposal may be made in a way that optimises asset usage at the lowest cost to the business

Life Cycle Costing Life Cycle Costing

a target cost is a product cost estimate that may be less than the planned initial product cost

the target cost will be expected to be achieved by the time the product reaches the mature production stage through

continuous improvement, and

replacement of technologies and processes

Target Costing (1) Target Costing (1)

a target cost is derived by subtracting a desired profit margin from a competitive market price, determined through

customer analysis

market research

Target Costing (2) Target Costing (2)

benchmarking processes of the best performing organisations within the industry, or within any other industry, can identify best practice, the adoption ofwhich may improve performance

Benchmarking Benchmarking

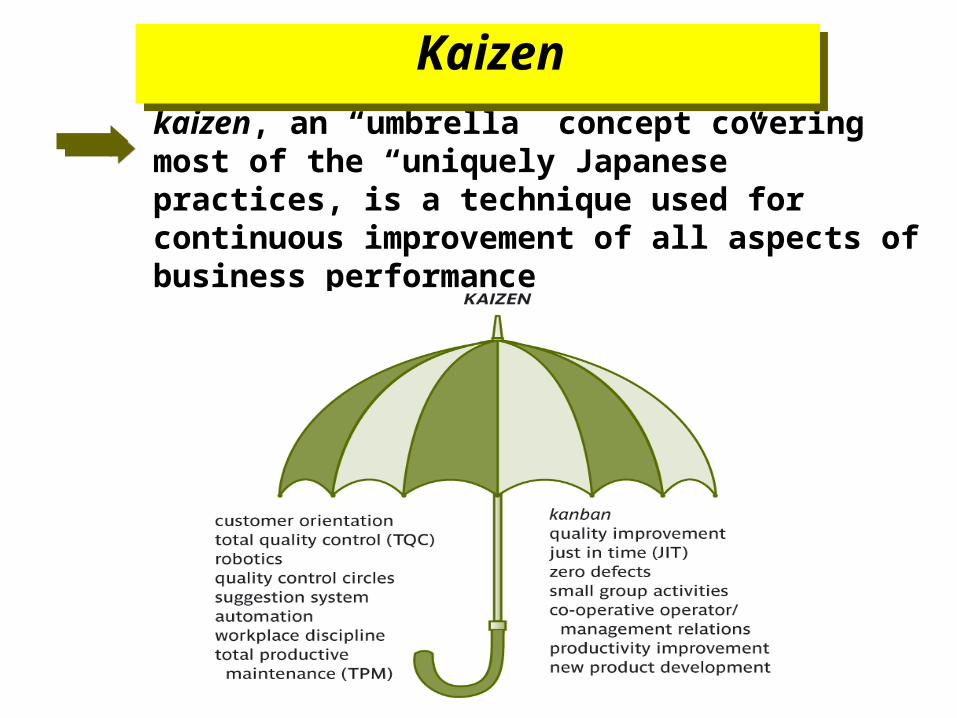

kaizen, an “umbrella” concept covering most of the “uniquely Japanese” practices, is a technique used for continuous improvement of all aspects of business performance

Kaizen Kaizen

Lean Accounting Lean Accounting

lean accounting provides the relevant information and measurements to support an organisation’s use of less resources to provide more output and in greater variety, and to encourage lean thinking throughout the organisation

lean accounting includes the use of target costing and value stream cost analysis

the strategic emphasis of lean accounting is on performance measurement that focuses on the elimination of waste and creation of capacity

cost of quality (COQ) is used to identify areas for improvement and cost reduction within each of the processes throughout the business

Cost of Quality (COQ) Cost of Quality (COQ)

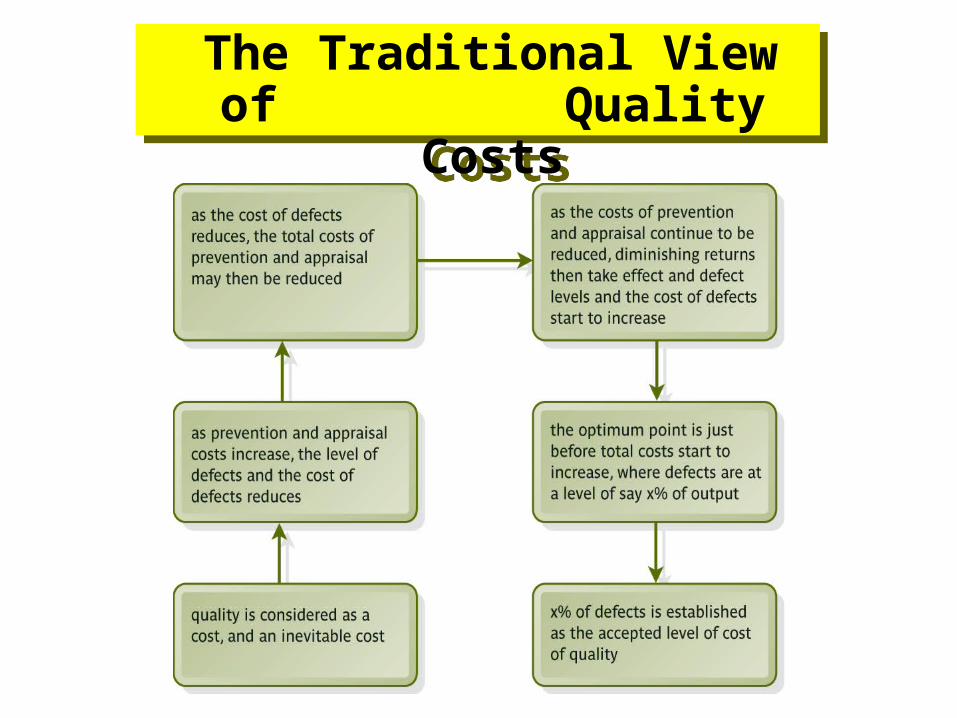

The Traditional View of Quality Costs

The Traditional View of Quality Costs

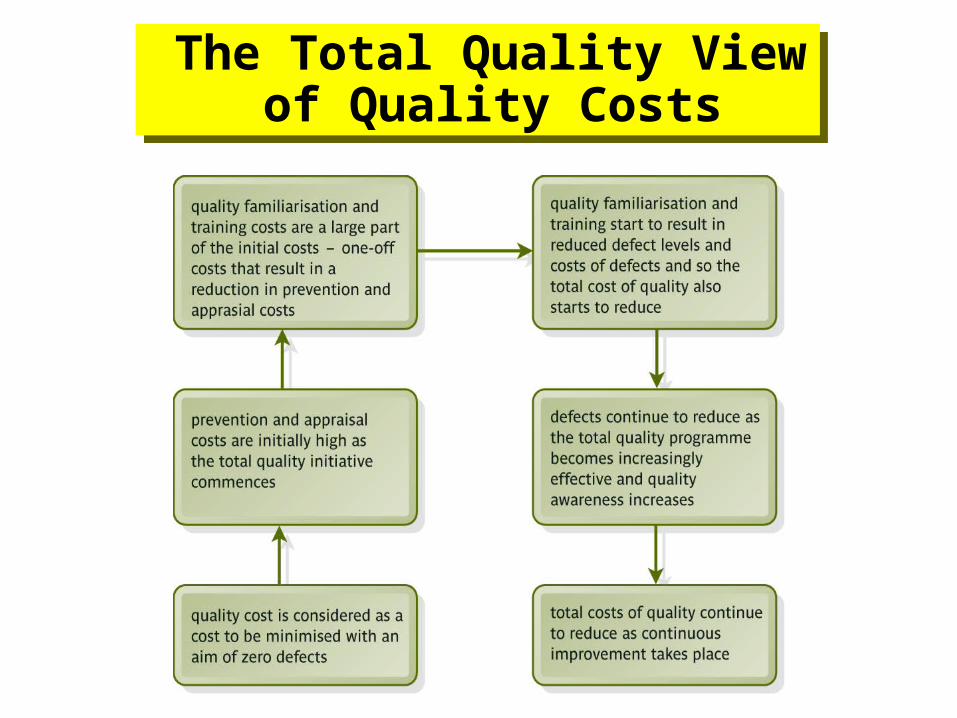

The Total Quality View of Quality Costs

The Total Quality View of Quality Costs

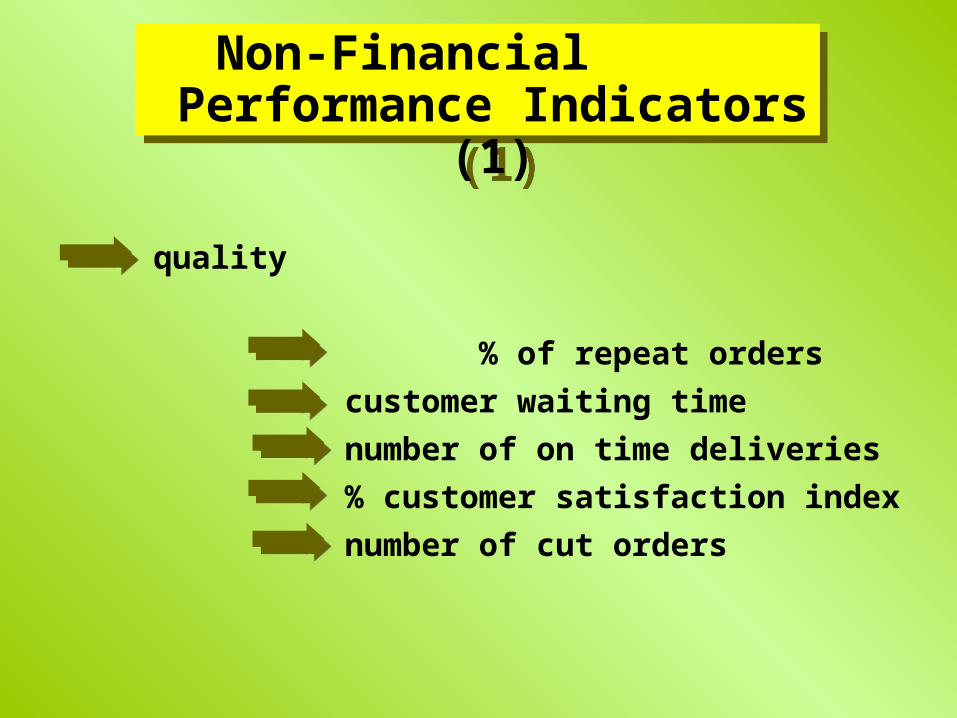

quality

% of repeat orders

customer waiting time

number of on time deliveries

% customer satisfaction index

number of cut orders

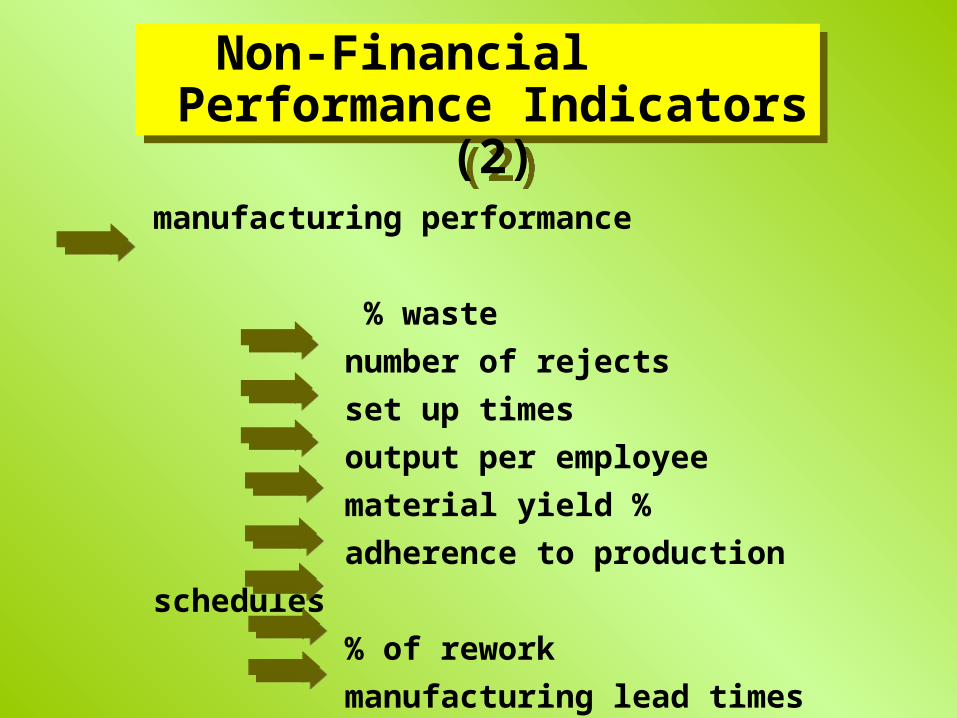

Non-Financial Performance Indicators (1)

Non-Financial Performance Indicators (1)

manufacturing performance

% waste

number of rejects

set up times

output per employee

material yield %

adherence to production

schedules

% of rework

manufacturing lead times

Non-Financial Performance Indicators (2)

Non-Financial Performance Indicators (2)

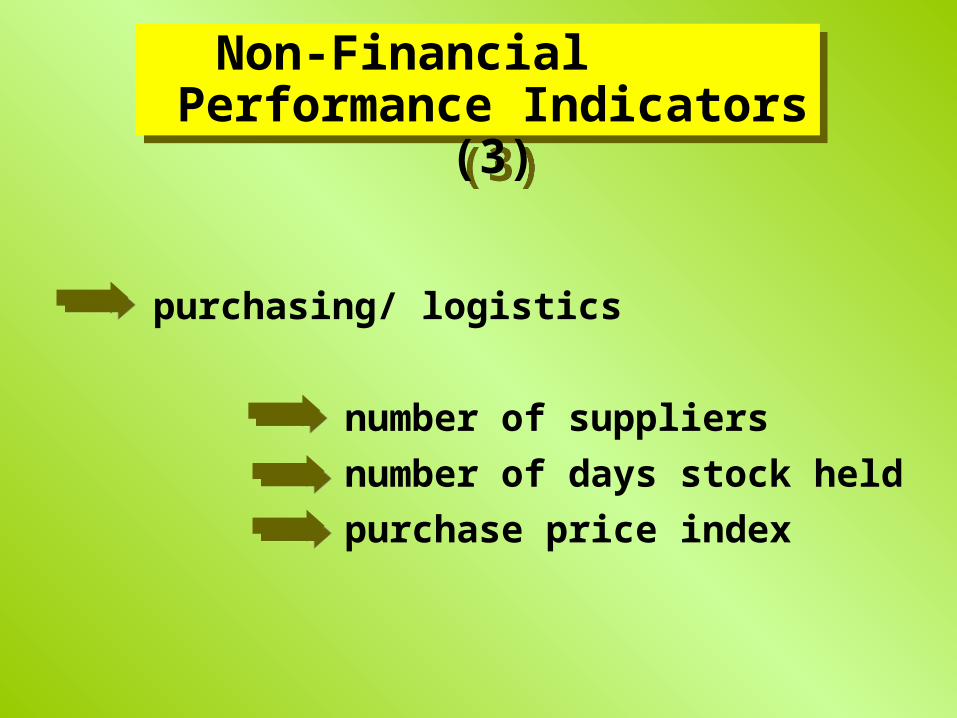

purchasing/ logistics

number of suppliers

number of days stock held

purchase price index

Non-Financial Performance Indicators (3)

Non-Financial Performance Indicators (3)

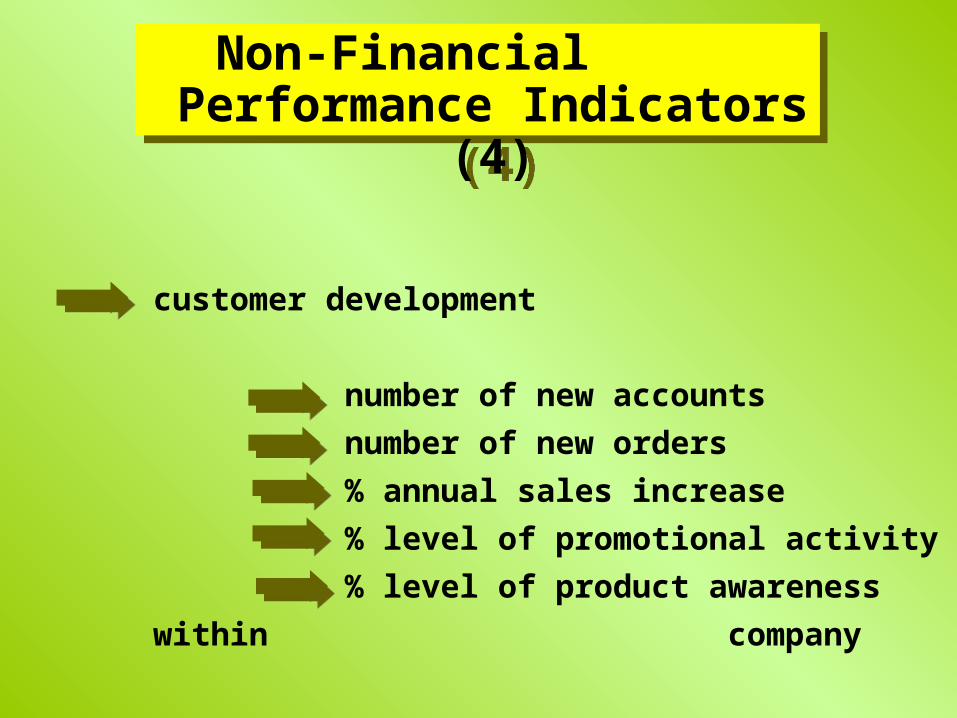

customer development

number of new accounts

number of new orders

% annual sales increase

% level of promotional activity

% level of product awareness

within company

Non-Financial Performance Indicators (4)

Non-Financial Performance Indicators (4)

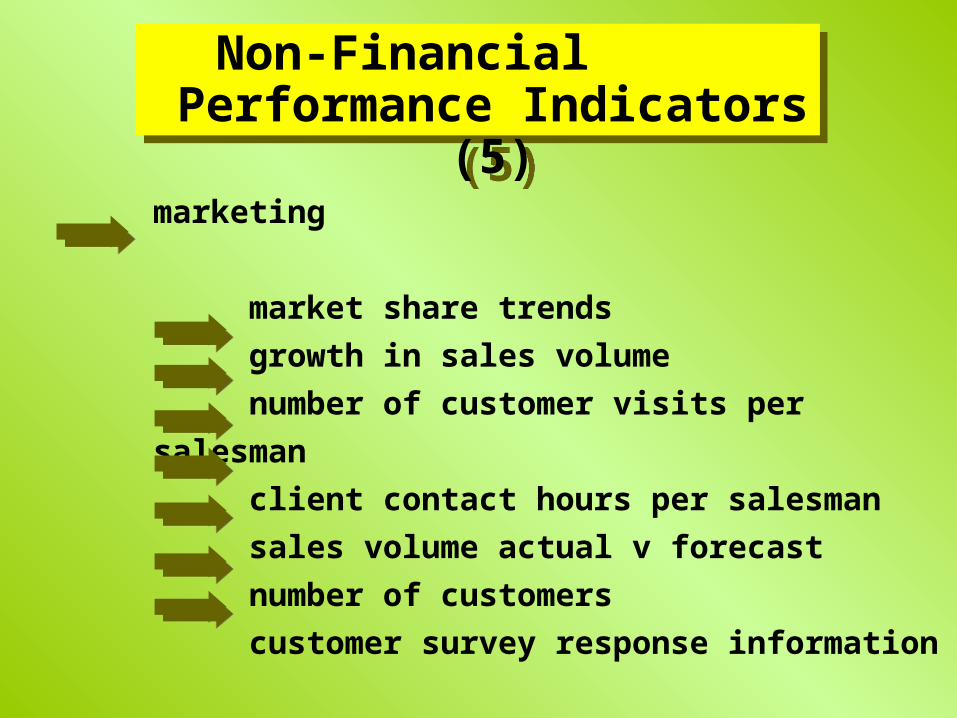

marketing

market share trends

growth in sales volume

number of customer visits per

salesman

client contact hours per salesman

sales volume actual v forecast

number of customers

customer survey response information

Non-Financial Performance Indicators (5)

Non-Financial Performance Indicators (5)

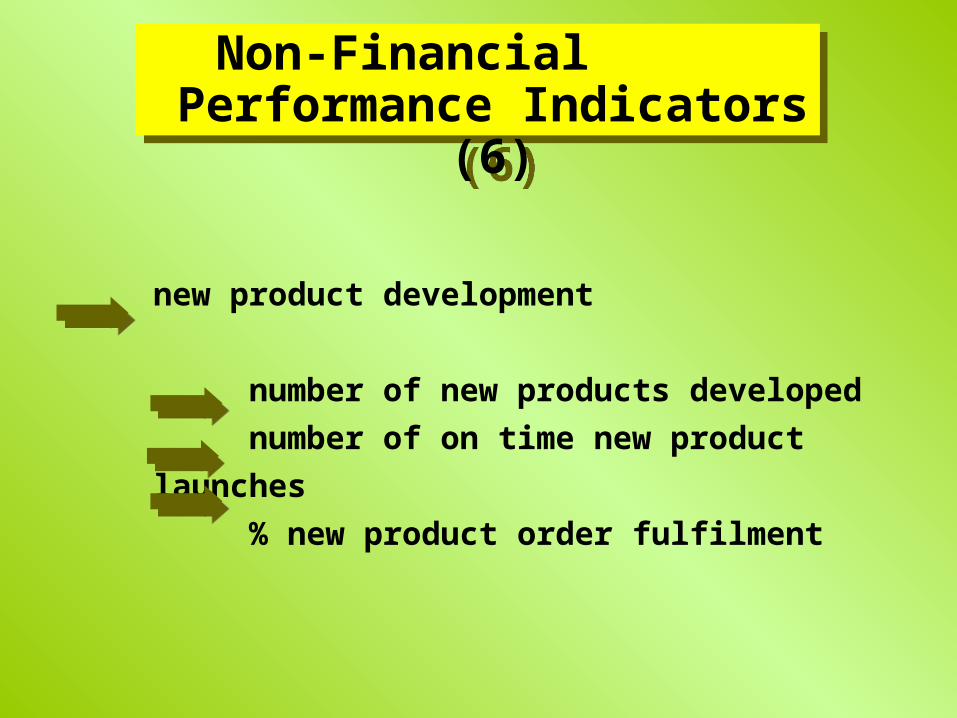

new product development

number of new products developed

number of on time new product

launches

% new product order fulfilment

Non-Financial Performance Indicators (6)

Non-Financial Performance Indicators (6)

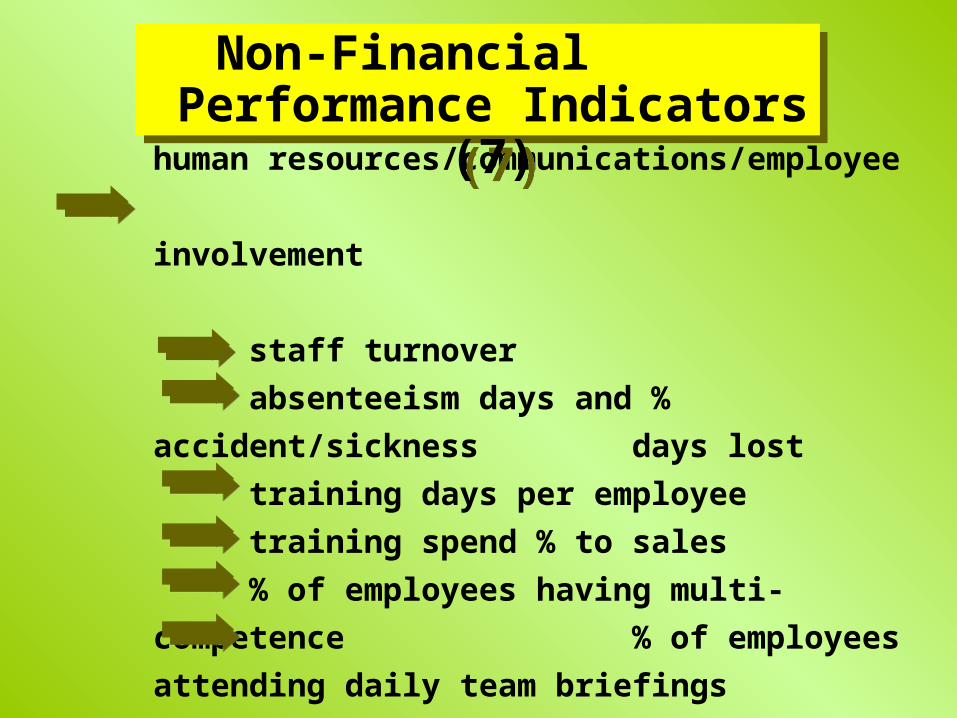

human

resources/communications/employee

involvement

staff turnover

absenteeism days and %

accident/sickness days lost

training days per employee

training spend % to sales

% of employees having multi-

competence % of employees

attending daily team briefings

Non-Financial Performance Indicators (7)

Non-Financial Performance Indicators (7)

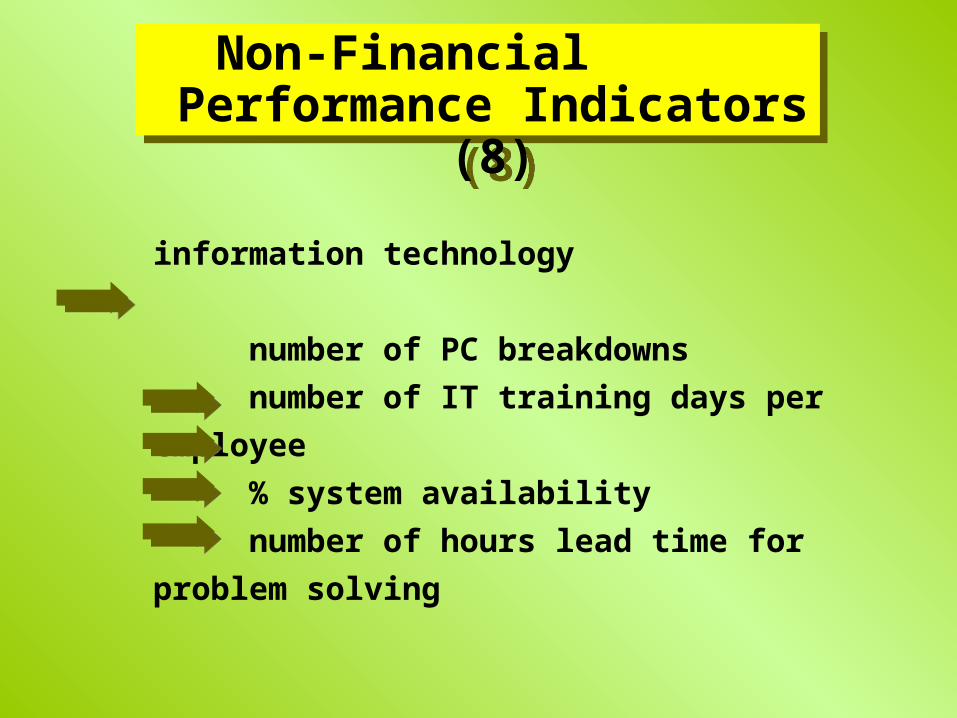

information technology

number of PC breakdowns

number of IT training days per

employee

% system availability

number of hours lead time for

problem solving

Non-Financial Performance Indicators (8)

Non-Financial Performance Indicators (8)

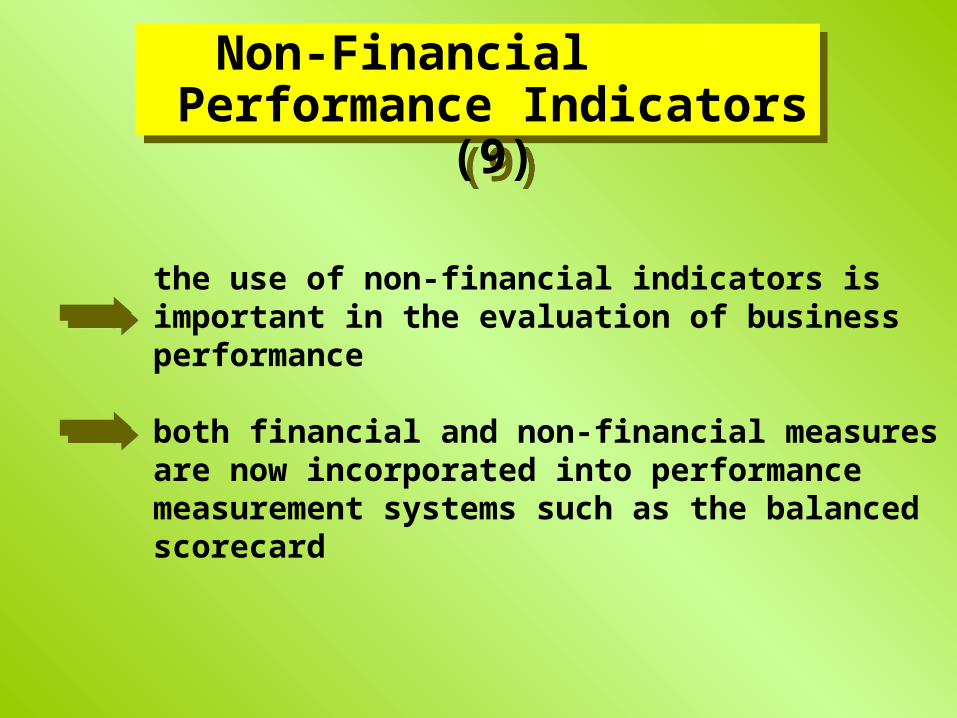

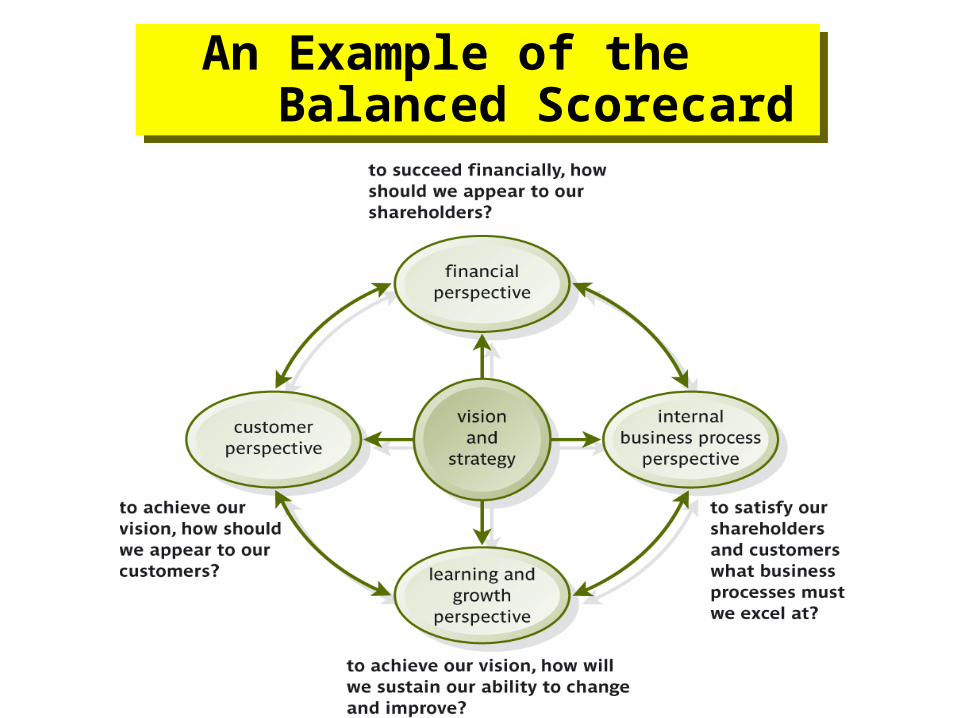

the use of non-financial indicators is important in the evaluation of business performance both financial and non-financial measures are now incorporated into performance measurement systems such as the balanced scorecard

Non-Financial Performance Indicators (9)

Non-Financial Performance Indicators (9)

An Example of the Balanced Scorecard

An Example of the Balanced Scorecard

Recommended