SEBI GUIDELINES FOR

CORPORATE GOVERNANCE

PRESENTED BY :

SUMEET DUBEY

JENIE MEHTA

VISHAL MISHRA

DISHA SHROFF

SHAILY BAVISHI

Corporate governance is….

A means whereby society can be sure that large corporations are well-run institutions to which investors and lenders can confidently commit their funds.

Safeguards against corruption and mismanagement, while promoting fundamental values of a market economy in democratic society.

(Considering the ethical failures in the last several years and the resulting crisis in confidence)..A sincere commitment to creating and sustaining an ethical business culture in public and private sectors..(has never been so important).

Why Corporate Governance?

TRANSPARENCY

ACCOUNTABILITY

CONTROL

TRUSTEESHIP

ETHICS

Securities and Exchange BOARD of India {SEBI}

The Government of India's securities watchdog, the Securities Board of India, announced strict corporate governance norms for publicly listed companies in India.

The Indian Economy was liberalized in 1991. In order to achieve the full potential of liberalization and enable the Indian Stock Market to attract huge investments from foreign institutional investors (FIIs), it was necessary to introduce a series of stock market reforms.

SEBI, established in 1988 and became a fully autonomous body by the year 1992 with defined responsibilities to cover both development and regulation of the market.

EMERGENCE OF CORPORATE GOVERNANCE IN INDIA

1997

• Formation of Kumar Mangalam Birla committee on Corporate Governance

2000

• Companies Amendment Act 2000 introduced ;• Setting up Audit Committee• Director’s Responsibility Statement

2005

• Clause 49 introduced in listing agreement• Narayan Murthy committee revised Clause 49

2012

• Companies Bill 2012• Major Highlights : Independent Director, Auditor & CSR

Clause 49

II. Board of Directors: A. Composition of Board of Directors:• BOD should have optimum combination of

Executive and Non- Executive Director• At least 50% of directors should be Non-

Executive Director• At least A *WOMEN Director.

INDEPENDENT DIRECTOR

Independent Director:All Qualification As per section 149 (6) of Companies Act, 2013 Except Below 2•Should attain age of 21 year•Who, neither himself nor any of his relatives ) is a material supplier, service provider or customer or a lessor or lessee of the company.

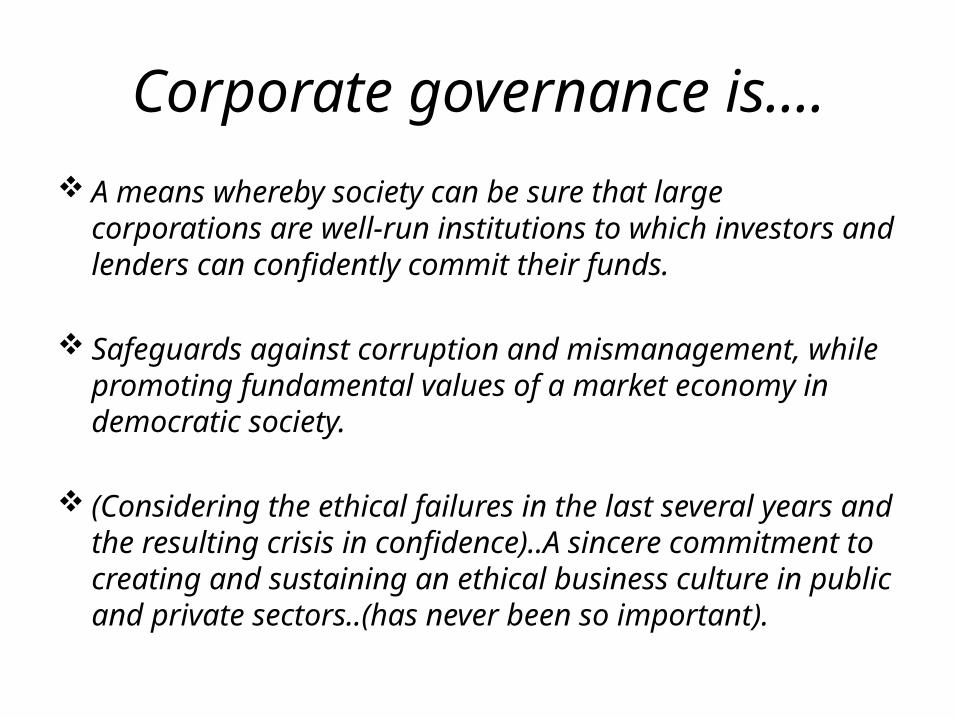

Old CG norms

Fraud

Loop Holes

New CG

norms

The Corporate Governance Cycle

US ScandalsoEnron oMCI Inc (Worldcom)

Fed passes the Sarkanes-Oxley Act (2002)

Australia ScandalsoHIHoOne.Tel

Aus passes CLERP 9 (Corporate Law Economic Reform Program) Act in 2004

The Big Bull

The Stock Market Scam

o 1980 – Started working in a brokerage firm.o 1990 – Started his own firm.o Traded heavily in ACC (Associated Cement Company)o Prices of ACC rose from Rs 200 to 9000.o Mr. Mehta said “ Stock was undervalued , the market simply corrected , I identified it”o Replacement Cost Theory : Revaluing a company at price equivalent to cost of building similar enterprise.o People started Trusting Mr. Mehta’s instinct.

Inside Story

o Mehta and his associates were manipulating the rise.

o The whole scheme was financed by supposedly “Collateralized” Bank Receipts (BR) which were actually “Uncollateralized”.

o BR (Bank Receipts) are used in short term Bank-to-Bank lending known as “Ready Forward” (RF) deals.

Mechanism of SCAMSecurity

Lending Bank Borrowing Bank

Government Securities

This is a Ready Forward Deal

Mechanism of SCAM

Lending BankBuyer of Security Broker

Borrowing BankSeller of Security

o Normally the Broker just Brings together both the parties and doesn’t handle cash or security.o This is exactly where the SCAM started.

o Now the Buyer and sellers wont even know each other.o Mr. Mehta and associates had become Big enough to be able to do this.o However to make it look “LEGAL” they pretended to be undertaking the transaction on Behalf of a Bank.

Another Instrument (BR)

Lending BankBuyer of Security Broker

Borrowing BankSeller of Security

o In a Ready Forward (RF) Deal “Securities” were not allowed to move forward and Backward.o BR (Bank Receipts)o BR confirms sales of security and acts as a receipt for money.o Promises delivery of securities to buyer’s Bank.o Seller holds the Security in Trust of Buyer.

Execution

o Banks which issue Fake BRs (not backed by any government securities)

Two Small Banks1. Bank of Karad (BOK)2. Metropolitan Co-operative Bank (MCB)

o Issued Fake BR for a Fee.

BOK and MCB

Fake BR Mr. MehtaOther Banks

Execution

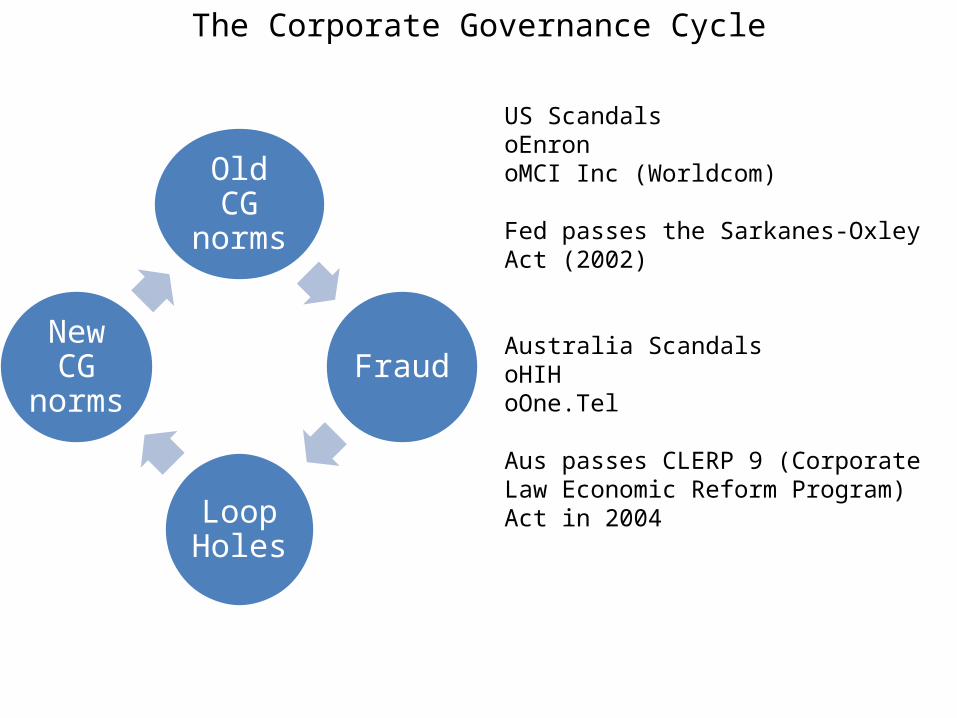

o So Banks kept lending Money.o When actually they were not lending against government securities.

o And when time came shares were sold at High Profit and money was returned to Banks.

Exposureo On April 23rd 1992 Sucheta Dalal (The Times of India) exposed Mr. Mehta’s SCAM.o When exposed Banks came running demanding their money causing Collapse.o Mr. Mehta Charged with 72 criminal offences and more than 600 civil action suit.o Arrested on 9th November 1992 and banished from Stock market.o Also was in allegation of misappropriation of 2.8 million shares of about 90 companies.

Implicationso This Scam is estimated to be of around 4000-5000 cr.o It pointed out a major Loop hole in the Banking system.

Interesting Facts and Allegationso Of the 27 criminal charges against him was convicted of only one before his death in 2001.o In the Supreme court hearing 1 out of the 3 Justice acquitted him.o On June 16 1993 he made public announcement of Bribing the then PM Mr. PV Narasimha Rao as donation to his party to get him out of this Scandal.o For More Watch the movie “Gafla”.

Case study

Stock prices in 2011• Shree Ashtavinayak Cine Vision Ltd is a film production and distribution company.

• On 14th January 2011, the stock price touched a 52-week low of Rs 4.86 during trading, but closed a notch higher at Rs5.36. This was the first upward move since 25 November 2010.

• On 19 January 2011 the volume of shares traded on the stock exchange was 11,40,68,280 shares, up from merely 364,547 shares a day earlier.

• The average volume traded for the six trading sessions since 14th January is up to over 428 lakh shares compared to the average in the two months 14 lakh.

•On 31 March 2014, the shares of Shree Ashtavinayak Cine Vision Ltd, (Shree Ashtavinayak) hit a 52-week low at Rs0.46. After this, it started moving up ferociously and in just eight trading days the stock has gained 128%.

Stock Prices in 2014• On 31st March, the volume of shares traded was 2.93 lakh shares, which kept on

increasing and on 10th March, volumes grew more than 10 times to 33.86 lakh.

• The company is making large losses. During December 2013 quarter, Shree Ashtavinayak recorded net loss of Rs4.27 crore compared with Rs3.26 crore of loss a year ago. In the September 2013 quarter, it recorded a humongous Rs43.19 crore of loss.

Allegations on SEBI• Operators can rig stock prices at will in India. There is no investigation.

• The FII route has long been suspected of money laundering and round-tripping. This case almost proves it. Why would “FIIs” be holding 7.93% shares in a penny stock, where “promoters” hold just 0.54%?

• The market regulator SEBI is getting more powers and money to act like the police – search, seize, detain, freeze assets etc but has been found to be failing to monitor obvious cases of price manipulation.

• SEBI has blown up over Rs40 crore in installing Intermarket Surveillance System under successive chairmen from M Damodaran to Mr UK Sinha but can be bothered by such obvious cases of price rigging.

Other CG Models

CG Model in Continental Europe

• Germany and the Netherlands have two-tiered Board of Directors

• Company Executive runs operations• Non executive directors:– Hire and fire– Determine compensation– Review business decisions

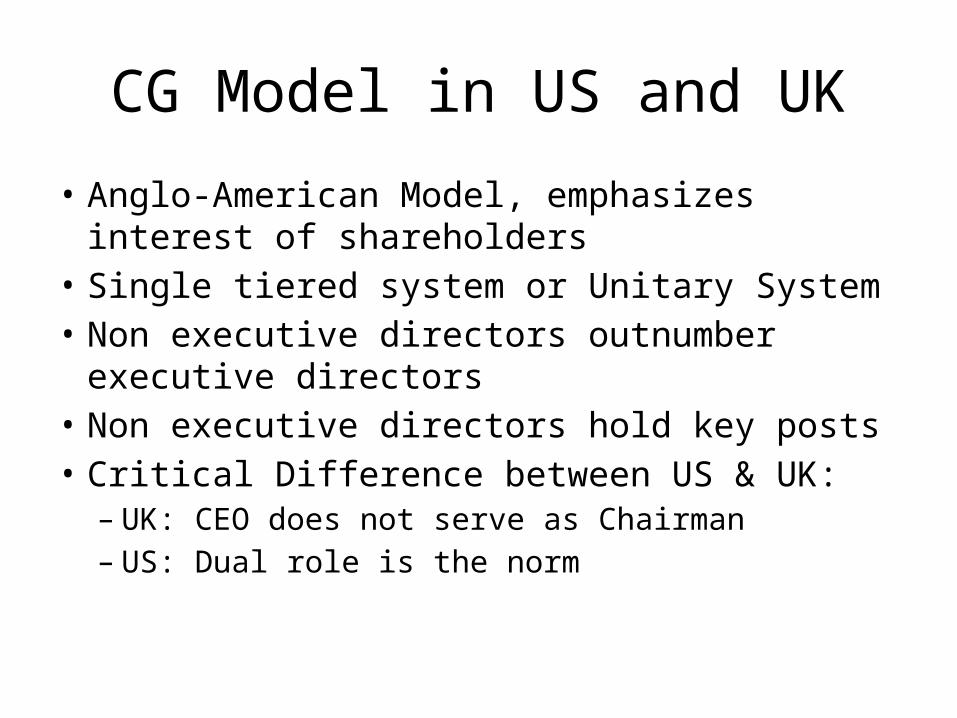

CG Model in US and UK

• Anglo-American Model, emphasizes interest of shareholders

• Single tiered system or Unitary System• Non executive directors outnumber executive

directors• Non executive directors hold key posts• Critical Difference between US & UK:– UK: CEO does not serve as Chairman– US: Dual role is the norm

Suggestions

• More development programs should be conducted to improve the awareness level of Investors

• Implementation of current norms should be made efficient

• Company should appoint internal auditors for audit committee

• Stakeholders value enhancement steps should be considered at large

• More programs should be arranged to educate shareholder about corporate governance

THANK YOU!

Recommended