Copyright ©2004 Pearson Education, Inc. All rights reserved.

Chapter 19

Retirement Planning

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-2

Chapter Objectives

• Describe the role of Social Security

• Explain the difference between defined-benefit and defined-contribution retirement plans

• Present the key decisions you must make regarding retirement plans

• Introduce the retirement plans available for self-employed individuals

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-3

Chapter Objectives

• Describe types of individual retirement accounts

• Illustrate how to estimate the savings you will have in your retirement account at the time you retire

• Show how to measure the tax benefits from contributing to a retirement plan

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-4

Social Security

• Social Security is a federal program that taxes you during your working years and uses the funds to make payments to you upon retirement

• It does not provide adequate income to solely support most people

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-5

Social Security

• Qualifying for Social Security– You need to accumulate 40 credits from

contributing to Social Security• One credit for each $780 in income per year,

maximum 4 per year

– Social Security also available for disabled

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-6

Social Security

– Survivor’s benefits are also provided

• A one-time income payment to the spouse

• Monthly income payments if spouse is older than 60 or has a child under the age of 16

• Monthly income payments to children under age 18

• Social Security Taxes

– Collected from both employees and employers

• 6.2% for Social Security

• 1.45% for Medicare

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-7

Social Security

Exhibit 19.1: FICA Taxes on Various Income Levels

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-8

Financial Planning Online: Request a Social Security Statement

• Go to: http://www.ssa.gov/top10.html

• This Web site provides a form that you can use to request that a statement of your lifetime earnings and an estimate of your benefits be mailed to you.

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-9

Social Security

• Retirement benefits– Depends on your income and the number

of years you earned income

– Provides about 42% of your annual income

– Eligible for full retirement benefits at age 65

– You can earn limited income while receiving Social Security

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-10

Social Security

• Concern about retirement benefits in the future– Retirees are living longer which costs

the program more in benefits

– The number of retirees continues to grow

– Many people are relying less on Social Security and establishing their own retirement programs

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-11

Employer-Sponsored Retirement Plans

• Designed to help you save for retirement

• Employees and/or employers contribute

• A penalty is imposed for early withdrawal

• Your contributions are tax-deferred

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-12

Employer-Sponsored Retirement Plans• Defined-benefit plan: an employee-sponsored

retirement plan that guarantees you a specific amount of income when you retire based on your salary and years of employment

– Vested: having a claim to a portion of the money in an employer-sponsored retirement account that has been reserved for you upon your retirement even if you leave the company

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-13

Employer-Sponsored Retirement Plans

• Defined-contribution plan: an employer-sponsored retirement plan that specifies guidelines under which you and/or your employer can contribute to your retirement account and that allows you to invest the funds as you wish

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-14

Employer-Sponsored Retirement Plans

– Benefits of a defined-contribution plan• Money contributed by employer is like extra

income

• Encourages employees to save

• Offers tax deferred income

– Investing funds in your retirement account• Employer can usually choose from a number

of different funds

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-15

Your Retirement Planning Decisions• Which retirement plan should you pursue?

– An employer-sponsored plan is usually the best choice if your employer contributes

• How much to contribute?– As much as you can as early as you can!

– How much to save?• How many people will you be supporting?

• What do you expect prices to be?

• What is your estimated life expectancy?

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-16

Financial Planning Online: Retirement Expense Calculator

• Go to: http://moneycentral.msn.com/investor/calcs/n_retireq/main.asp

• This Web site provides an estimate of your expenses at retirement based on your current salary and expenses.

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-17

Your Retirement Planning Decisions

• How to invest your contributions?– Use a diversified set of investments

– Consider the number of years to retirement

– Consider your level of risk tolerance

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-18

Your Retirement Planning Decisions

Exhibit 19.2: Typical Composition of a Retirement Account Portfolio

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-19

Your Retirement Planning Decisions

Exhibit 19.2: Typical Composition of a Retirement Account Portfolio

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-20

Retirement Plans Offered by Employers• 401(k) plan: a defined-contribution plan

that allows employees to contribute a maximum of $10,500 per year or 15 percent of their salary on a pre-tax basis– Amount of contribution gradually increasing

to $15,000 under Tax Relief Act of 2001

– Matching contributions by some employers

– Tax on money withdrawn from the account• Tax and penalty for withdrawals before age 59½

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-21

Retirement Plans Offered by Employers

• Focus on Ethics: 401(k) investment alternatives– Plans requiring employees to invest their

401(k) contributions in their employer’s stock is unethical

– These contributions should be diversified

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-22

Retirement Plans Offered by Employers

• 403-b plan: a defined-contribution plan allowing employees of non-profit organizations to invest up to $10,000 of their income on a tax-deferred basis– Gradually increasing to $15,000 under Tax

Relief Act of 2001

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-23

Retirement Plans Offered by Employers

• Simplified Employee Plan (SEP): a defined-contribution plan commonly offered by firms with 1 to 10 employees or used by self-employed people– Employee cannot contribute to this plan

– Tax and penalty for withdrawals before age 59

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-24

Retirement Plans Offered by Employers

• SIMPLE (Savings Incentive Match Plan for Employees) Plan: a defined-contribution plan intended for firms with 100 or fewer employees– Employee can contribute up to $6,000

annually and the employer can match

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-25

Retirement Plans Offered by Employers

• Profit sharing: a defined-contribution plan in which the employer makes contributions to employee retirement accounts based on a specified formula– Up to 15% of employee’s salary, maximum

$24,000 per year

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-26

Retirement Plans Offered by Employers

• Employee Stock Ownership Plan (ESOP): a retirement plan in which the employer contributes some of its own stock to the employee’s retirement account– More risky because it is not diversified

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-27

Retirement Plans Offered by Employers

• Managing your retirement account after leaving your employer– Rollover IRA: an individual retirement

account into which you can transfer your assets from your company retirement plan tax-free while avoiding penalties

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-28

Retirement Plans for Self-Employed Individuals

• Keogh Plan: a retirement plan that enables self-employed individuals to contribute part of their pre-tax income to a retirement account– Up to 25% to a maximum of $30,000

annually

– Individual determines how funds are invested

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-29

Retirement Plans for Self-Employed Individuals

• Simplified Employee Plan (SEP)– Also available for self-employed who can

contribute up to 15% of annual income to a maximum of $24,000 annually

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-30

Individual Retirement Accounts

• Traditional IRA: a retirement plan that enables individuals to invest $2,000 per year– Gradually increasing to $5000 under Tax Relief

Act of 2001

– Contributions may or may not be tax-deductible

– Interest earned is tax-deferred

– Tax and penalty on withdrawals before age 59

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-31

Individual Retirement Accounts

• Roth IRA: a retirement plan that enables individuals who are under specific income limits to invest $2,000 per year– Gradually increasing to $5000 under Tax

Relief Act of 2001

– Income taxed at time of contribution, but not when withdrawn

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-32

Individual Retirement Accounts

• Comparison of the Roth IRA and Traditional IRA– Advantage of traditional IRA over Roth IRA

• Contributions are sheltered from taxes until withdrawn

– Advantage of Roth IRA over traditional IRA• Investment income accumulates tax-free

in a Roth IRA

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-33

Individual Retirement Accounts

– Factors that affect your choice• Marginal tax rates at time of contribution

and withdrawal

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-34

Financial Planning Online: Traditional IRA or Roth IRA?• Go to: http://www.financenter

.com/products/sellingtools/calculators/ira/

• Click on: “Should I convert my IRA into a Roth IRA?”

• This Web site provides an analysis of whether a Traditional or a Roth IRA is better suited to you.

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-35

Annuities

• Annuity: a financial contract that provides annual payments over a specified period

• Contributions taxable but gains are tax-deferred

• Fixed versus variable annuities– Fixed annuity: an annuity that provides a specified

return on your investment, so you know exactly how much you will receive at a future time

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-36

Annuities

– Variable annuity: an annuity in which the return is based on the performance of the selected investment vehicles

• Annuity fees– High fees is a disadvantage of annuities

– Surrender charge: a fee that may be imposed on any money withdrawn from an annuity

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-37

Annuities

– Also commissions to salespeople

– Look for no-load annuities that do not charge commissions and have low management fees

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-38

Estimating Your Future Retirement Savings• Estimating the future value of one investment

• Example:

– You consider investing $5,000 this year, and this

investment will remain in your account until 40

years from now when you retire. You believe that

you can earn a return of 10% per year on your

investment. Using FVIF, you expect the value of

your investment in 40 years to be:

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-39

Estimating Your Future Retirement Savings

Value in 40 years = Investment FVIF(I=10,

n=40)

= $5,000 45.259

= $226,295

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-40

Estimating Your Future Retirement Savings

• Estimating the future value of one investment– Relationship between amount saved now

and retirement savings• If you invested $10,000 instead of $5,000,

your savings would grow to $452,590 in 40 years

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-41

Estimating Your Future Retirement Savings

– Relationship between years of saving and your retirement savings

• If you invested $5,000 for 25 years instead of 40 years, your savings would be only $54,175

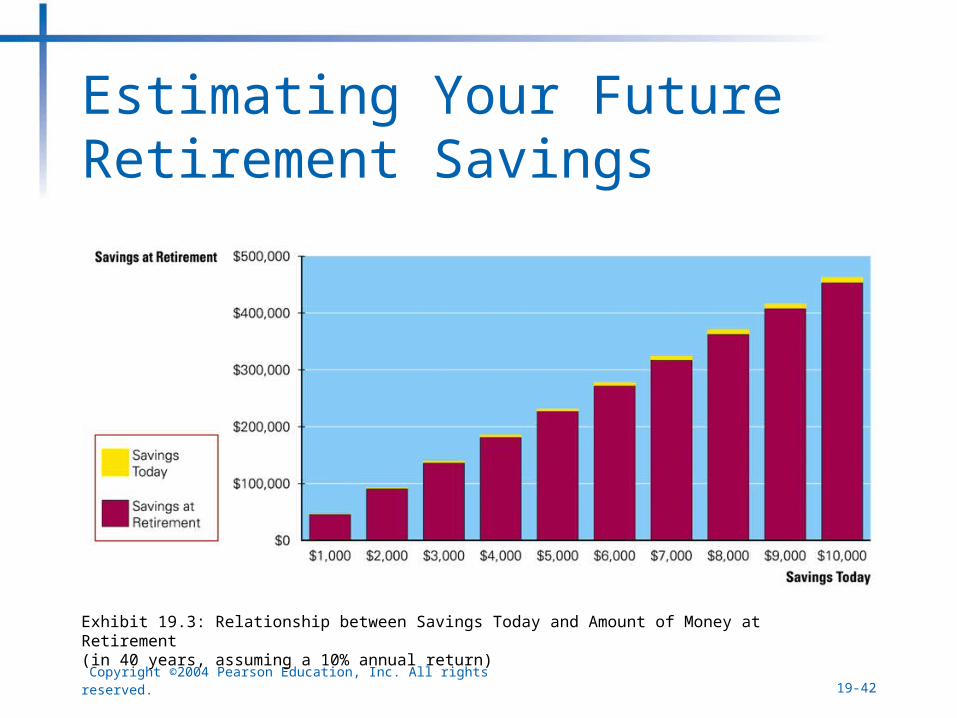

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-42

Estimating Your Future Retirement Savings

Exhibit 19.3: Relationship between Savings Today and Amount of Money at Retirement (in 40 years, assuming a 10% annual return)

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-43

Estimating Your Future Retirement Savings

– Relationship between your annual return and your retirement savings

• If you earned a return of 14% instead of 10%, your $5,000 would be worth $944,400 in 40 years

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-44

Estimating Your Future Retirement Savings

Exhibit 19.4: Relationship between the Investment Period and Your Savings at Retirement (assuming a $5,000 investment and a 10% annual return)

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-45

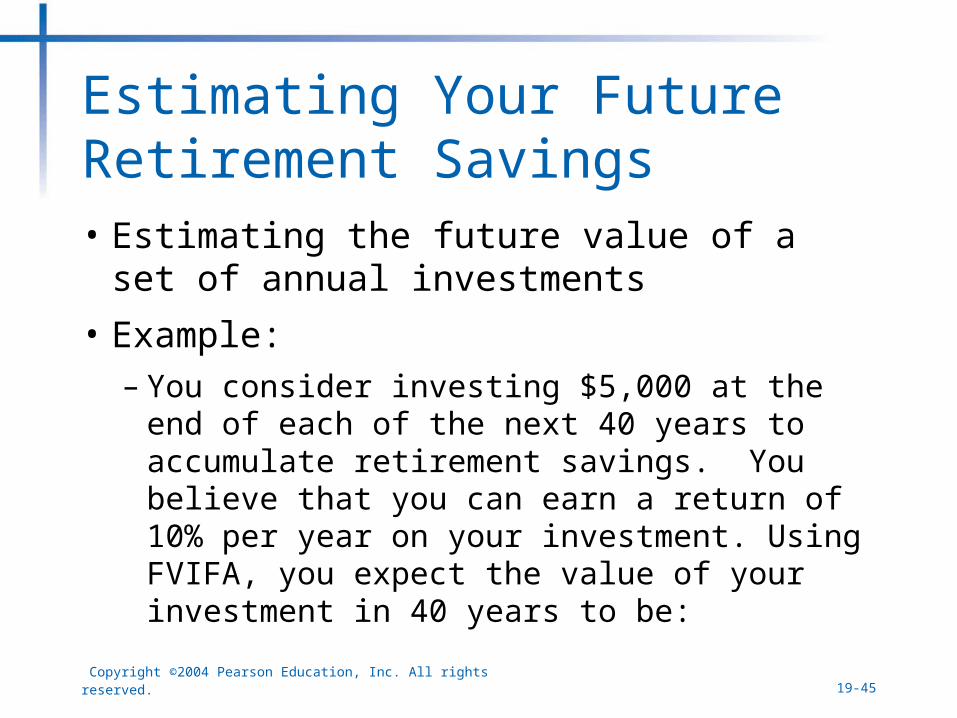

Estimating Your Future Retirement Savings• Estimating the future value of a set of

annual investments

• Example: – You consider investing $5,000 at the end of

each of the next 40 years to accumulate retirement savings. You believe that you can earn a return of 10% per year on your investment. Using FVIFA, you expect the value of your investment in 40 years to be:

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-46

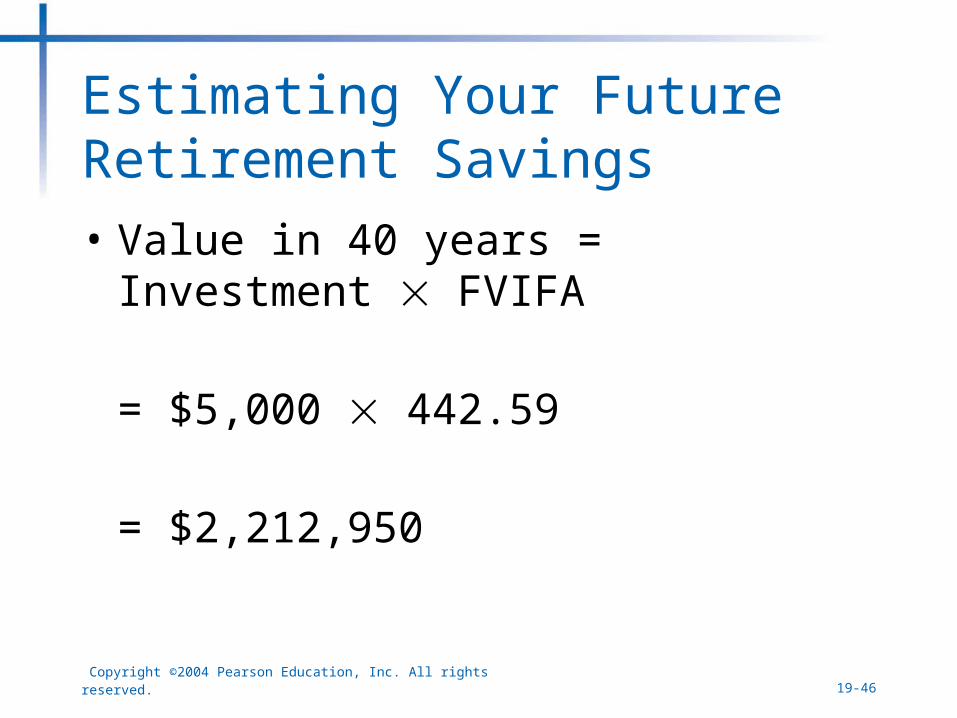

Estimating Your Future Retirement Savings

• Value in 40 years = Investment FVIFA

= $5,000 442.59

= $2,212,950

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-47

Estimating Your Future Retirement Savings

– Relationship between size of annuity and retirement savings

• For every extra $1,000 you can save by the end of each year, you will accumulate an additional $442,590

– Relationship between years of saving and retirement savings

• If you start saving $5,000 per year at age 25 instead of age 30 (saving until age 65), you will save an additional $857,850

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-48

Estimating Your Future Retirement Savings

Exhibit 19.6: Relationship between the Amount Saved per Year and Amount of Savings at Retirement(in 40 years, assuming a 10% annual return)

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-49

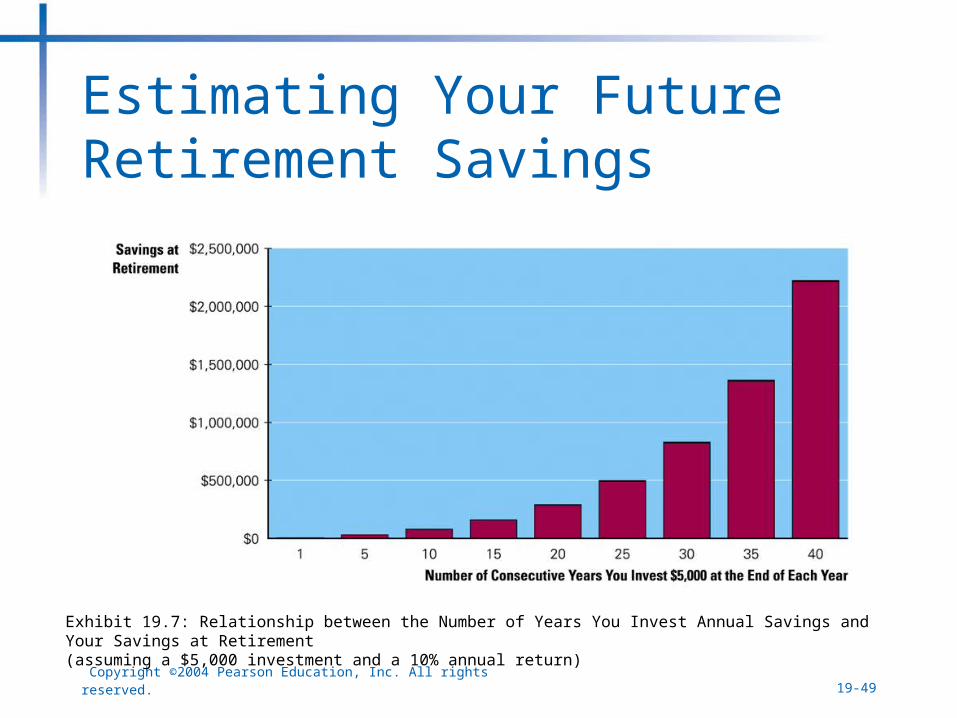

Estimating Your Future Retirement Savings

Exhibit 19.7: Relationship between the Number of Years You Invest Annual Savings and Your Savings at Retirement (assuming a $5,000 investment and a 10% annual return)

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-50

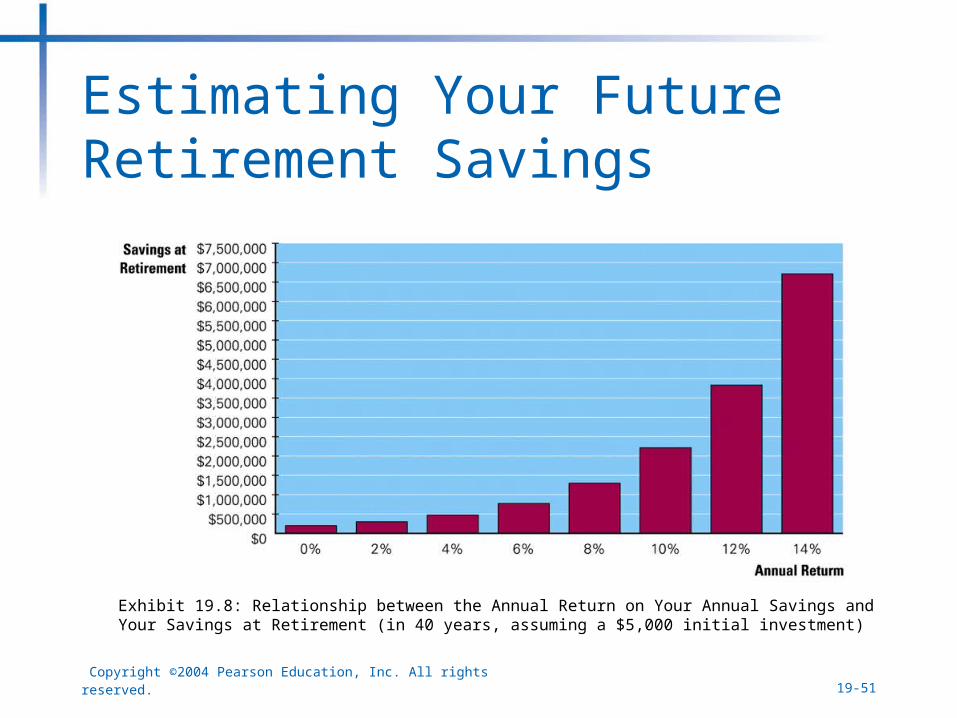

Estimating Your Future Retirement Savings

– Relationship between your annual return and your savings at retirement

• If you earn a return of 12% instead of 10% your savings will accumulate at additional $1.6 million

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-51

Estimating Your Future Retirement Savings

Exhibit 19.8: Relationship between the Annual Return on Your Annual Savings and Your Savings at Retirement (in 40 years, assuming a $5,000 initial investment)

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-52

Measuring the Tax Benefits From a Retirement Account

• Example: – You wish to invest $5,000 per year in a

retirement account for the next 40 years. You expect to earn a return of 10% per year. Using FVIFA, your savings at retirement would be:

$5,000 442.59 = $2,212,950

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-53

Measuring the Tax Benefits From a Retirement Account

– If you withdrew all of your money in one year, with a 25% tax rate, your tax would be:

$2,212,950 .25 = $553,238– Your income after taxes would be:

$2,212,950 - $553,238 = $1,659,712

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-54

Measuring the Tax Benefits From a Retirement Account

– Consider if you invest the $5,000 elsewhere, you have an additional $5,000 taxable income each year. Assuming a marginal tax rate of 30%, you have only $3,500 each year to invest. Assume a 10% return on those savings over the next 40 years. Using FVIFA, your savings would be:(cont’d on next slide)

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-55

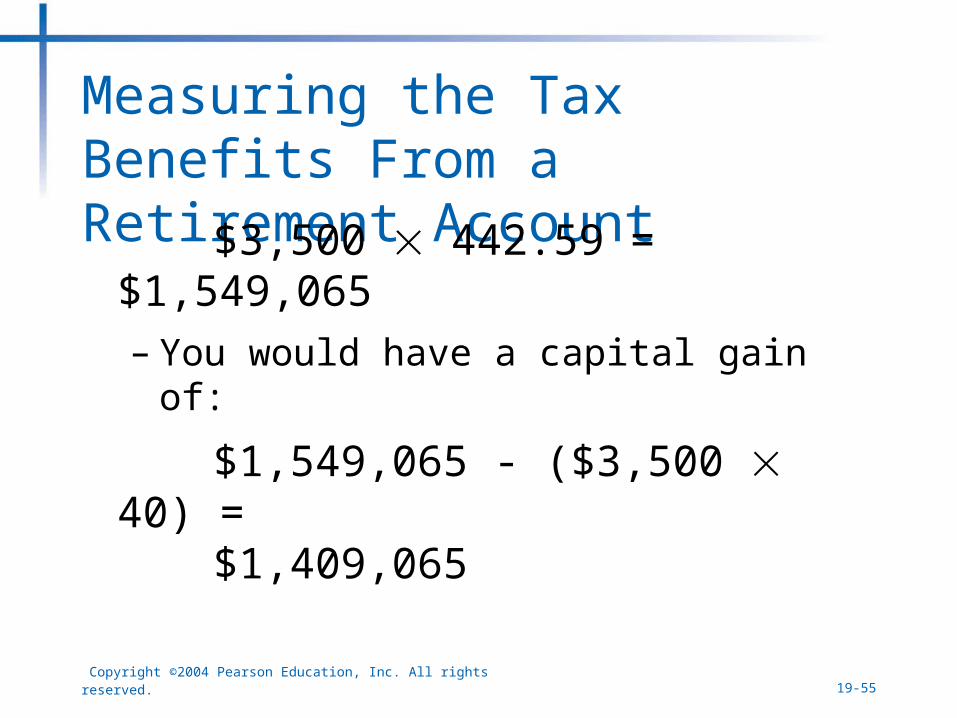

Measuring the Tax Benefits From a Retirement Account

$3,500 442.59 = $1,549,065– You would have a capital gain of:

$1,549,065 - ($3,500 40) = $1,409,065

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-56

Measuring the Tax Benefits From a Retirement Account

– Assuming a capital gains tax of 20%, your capital gains tax would be:

$1,409,065 .20 = $281,813– Therefore, after 40 years you have:

$1,409,065 - $281,813 = $1,127,252– With your IRA, your account would be

worth over $500,000 more!

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-57

Financial Planning Online: How to Build Your Retirement Plan

• Go to: http://www.quicken.com/retirement/planner/

• This Web site provides a framework for building a retirement plan based on your financial situation.

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-58

How Retirement Planning Fits within Your Financial Plan

• Key decisions about retirement planning

for your financial plan are:– Should you invest in a retirement plan?

– How much should you invest in a retirement plan?

– How should you allocate investments within your retirement plan?

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-59

Integrating Key Concepts

Copyright ©2004 Pearson Education, Inc. All rights reserved. 19-60

Integrating Key Concepts

• Part 1: Financial Planning Tools• Part 2: Liquidity Management• Part 3: Financing• Part 4: Protecting Your Assets and Income• Part 5: Investing• Part 6: Retirement and Estate Planning

– In Chapter 19 we learned about retirement planning– In Chapter 20 we will learn about estate planning

Recommended