[email protected] www.e-mfp.eu

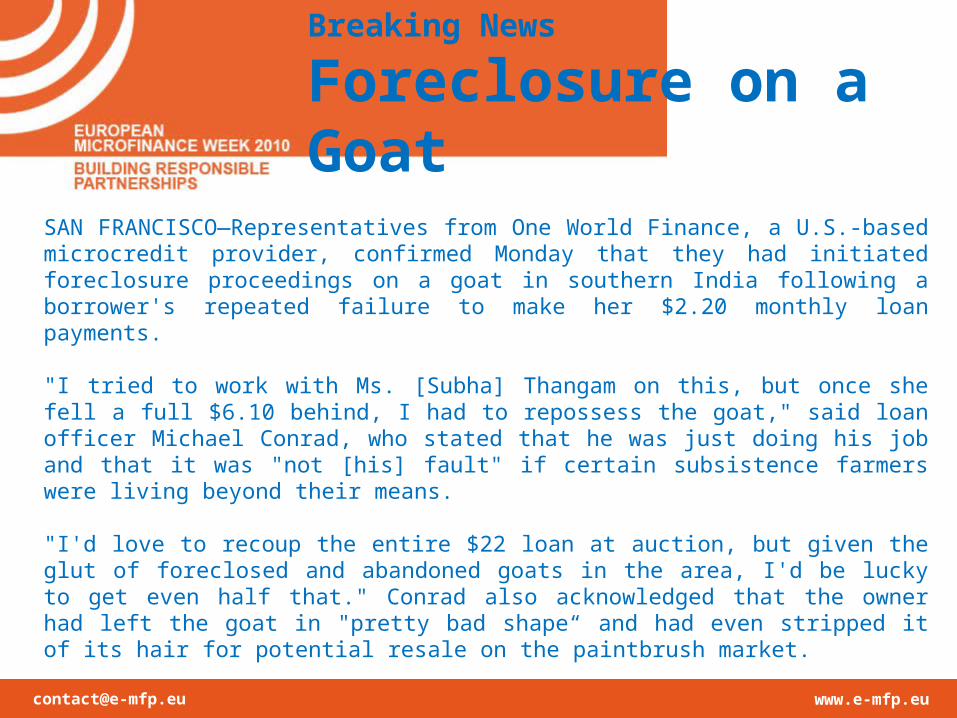

Breaking News

Foreclosure on a Goat

SAN FRANCISCO—Representatives from One World Finance, a U.S.-based microcredit provider, confirmed Monday that they had initiated foreclosure proceedings on a goat in southern India following a borrower's repeated failure to make her $2.20 monthly loan payments.

"I tried to work with Ms. [Subha] Thangam on this, but once she fell a full $6.10 behind, I had to repossess the goat," said loan officer Michael Conrad, who stated that he was just doing his job and that it was "not [his] fault" if certain subsistence farmers were living beyond their means.

"I'd love to recoup the entire $22 loan at auction, but given the glut of foreclosed and abandoned goats in the area, I'd be lucky to get even half that." Conrad also acknowledged that the owner had left the goat in "pretty bad shape“ and had even stripped it of its hair for potential resale on the paintbrush market.

[email protected] www.e-mfp.eu

The Blame Game

So Mrs Thangam and her goat are in bad shape. The loan did not work out well for them. Who is to be blamed for that?

Is it the MFI: lending too easily, charging excessively?Is it the customer: overstretching herself?Is it the investor: demanding too high a return?Is it the regulator: not installing price controls?Is it the market: allowing for exploiting vulnerabilities? Or is it just tough luck: collateral damage?

[email protected] www.e-mfp.eu

Basically a Good Mix

Microfinance applies both market and social objectives

From the market approach we take Laissez fair market development Limited regulation Insistence on full commercial prizing

And from the social approach we adopt The poverty alleviation drive The “access for all” paradigm: inclusive finance

[email protected] www.e-mfp.eu

Convincingly Applied?

The market and social mix shows various inconveniences

Development grants do not directly benefit end-usersRarely factored into retail pricesRather benefit supply side players

The development notion applied is restrainedDevelopment impacts are not convincingly proven

Resulting in growing disconnectsSocially with civil societyPolitically with local governments

[email protected] www.e-mfp.eu

A Creative Approach

Modifies the mix and creates equitability

Borrowers need protection against Over-indebtedness Usurious and unsustainable interest rates Harsh or semi-illegal repossession practices

Practitioners need to be able To sustain and grow their institutions

And investors need to be able to Earn a decent return on investment

[email protected] www.e-mfp.eu

Equitability Explained

Markets need full regulation

Which goes beyond self-regulation Or principles of client protection And is to be installed and enforced by governments

Borrowers have a right to be protected By their own governments Not to be left at the goodwill of supply side players As the only way to create a level playing field Need for access not to overrule client rights

[email protected] www.e-mfp.eu

Full Regulation

Unavoidable and necessary to deal with the main evils

That will damage the industry if not controlled Lending beyond borrower’s handling capacity Charging usurious or unaffordable rates Multiple lending to the same borrower

There is growing need for industry consolidation Entirely focusing on quality of service delivery Putting quantitative goals on the backburner And full acceptance of governments as stakeholders

[email protected] www.e-mfp.eu

Market Segmentation

This requires carving up the market in segments

What can be left to the market, leave to the market Withdrawal of development aid from that segment Autonomous growth, local capitalization Regulation driving innovation and price reduction

For the unfeasible segments, alternative concepts apply Using public and donor support Creating client and system sustainability over time As legitimate proxies for ‘inclusiveness’

[email protected] www.e-mfp.eu

Creating Feasibility

How to make unfeasible market segments feasible?

Taking into account Borrowers’ limited earning capacity Investors’ need for decent return on investment And practitioners’ need for sustainability

The answer is in strengthening earning capacity By dedicated BDS, VCF and other interventions

And in wholesale risk deduction Allowing for modest but adequate returns

[email protected] www.e-mfp.eu

Earning Capacity

Essentially to be achieved by moving beyond microfinance

Microloans do no trigger rural development What does is rural enterprise development In combination with infrastructure development Removal of institutional barriers And adequate (long-term, affordable) finance

Microloans do not trigger urban development What does is formalizing the urban economy With job creation through SME development

[email protected] www.e-mfp.eu

Risk Reduction

To be achieved at both the supply and demand side

By offering local investors near risk-free returns As alternative to massive T-bill buying And tapping into liquidity of domestic markets Thus lowering cost of capital for (M)FIs

Clients can be offered much lower rates By offering longer-term, larger business loans And business support reducing project risk Through (M)FIs, reducing operational costs

[email protected] www.e-mfp.eu

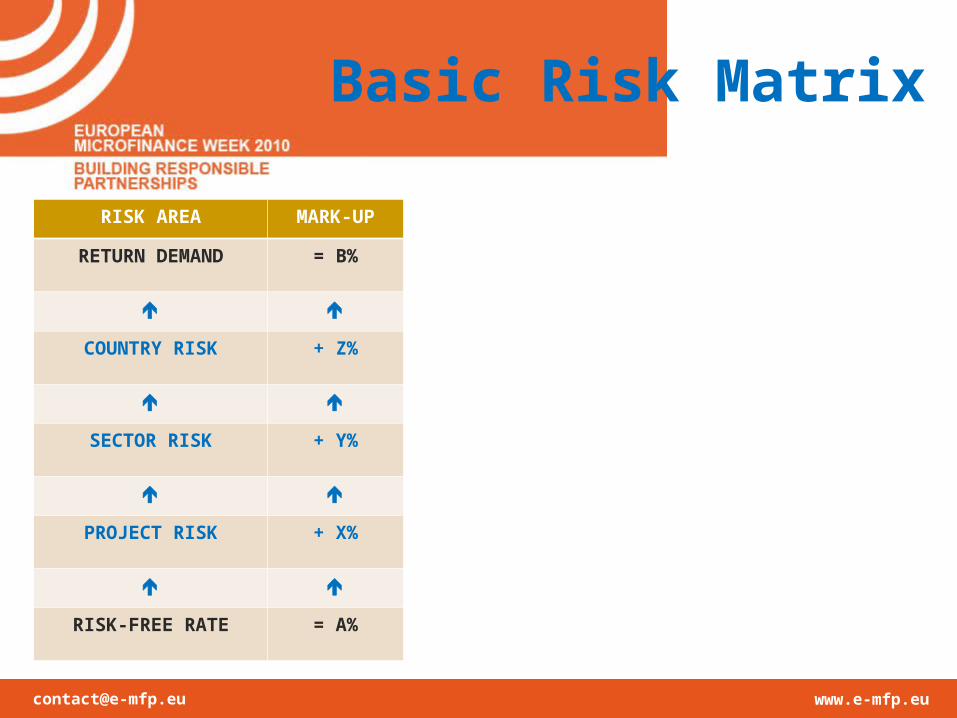

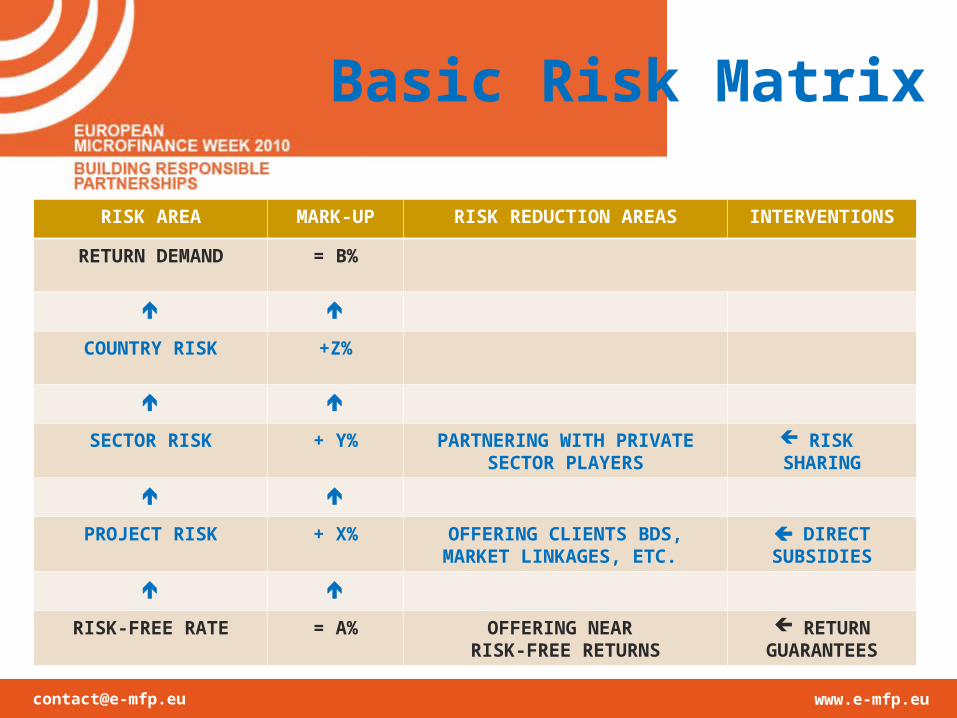

Basic Risk Matrix

RISK AREA

RETURN DEMAND

COUNTRY RISK

SECTOR RISK

PROJECT RISK

RISK-FREE RATE

[email protected] www.e-mfp.eu

Basic Risk Matrix

RISK AREA MARK-UP

RETURN DEMAND = B%

COUNTRY RISK + Z%

SECTOR RISK + Y%

PROJECT RISK + X%

RISK-FREE RATE = A%

[email protected] www.e-mfp.eu

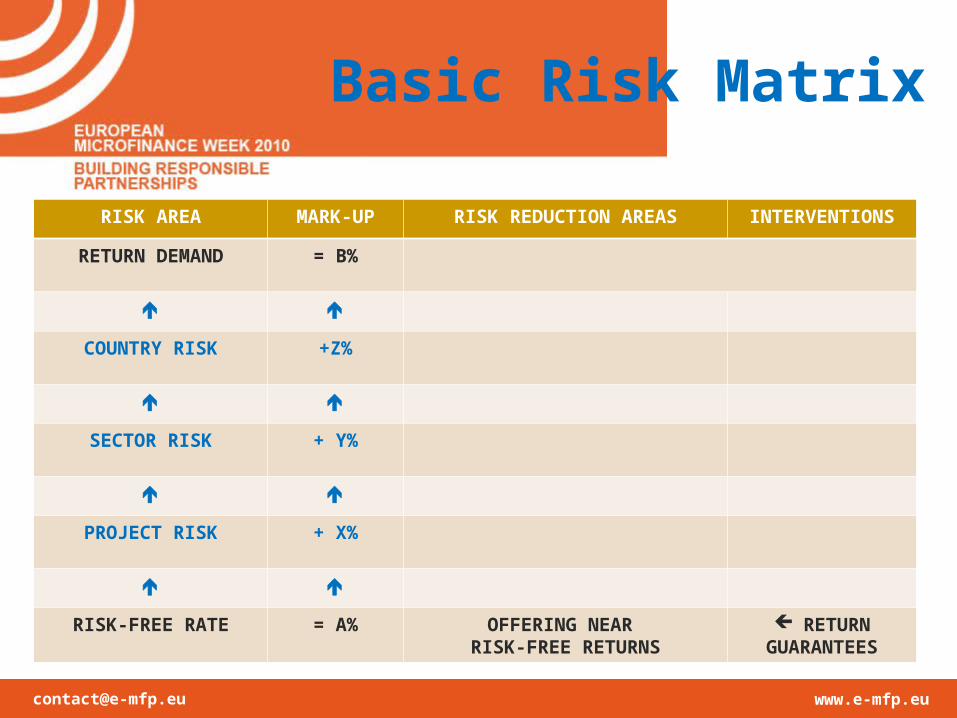

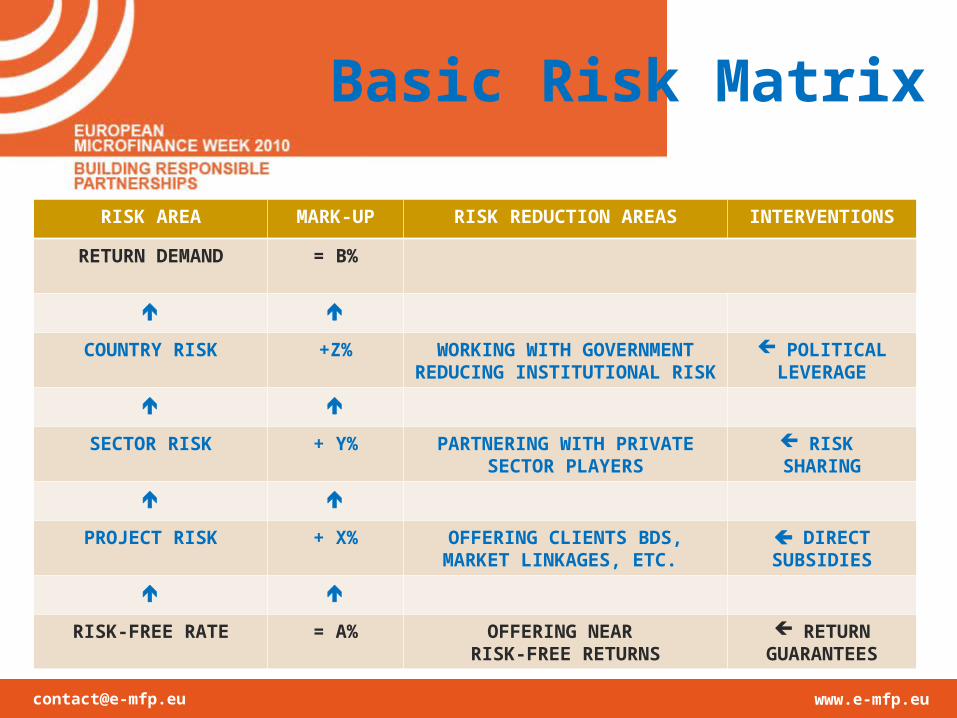

Basic Risk Matrix

RISK AREA MARK-UP RISK REDUCTION AREAS INTERVENTIONS

RETURN DEMAND = B%

COUNTRY RISK +Z%

SECTOR RISK + Y%

PROJECT RISK + X%

RISK-FREE RATE = A% OFFERING NEAR RISK-FREE RETURNS

RETURNGUARANTEES

[email protected] www.e-mfp.eu

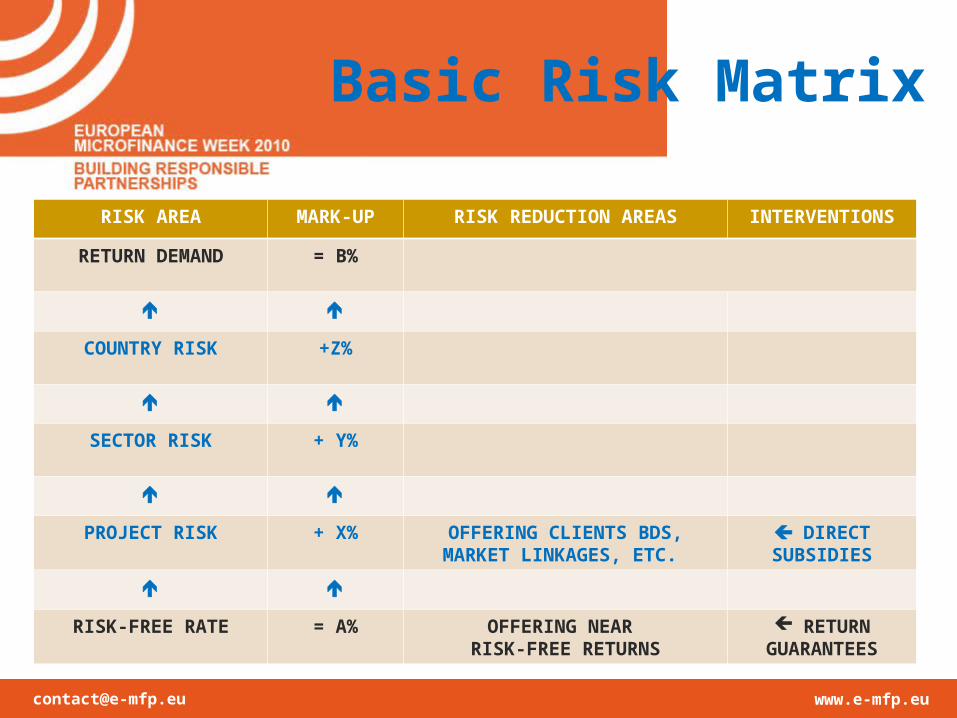

Basic Risk Matrix

RISK AREA MARK-UP RISK REDUCTION AREAS INTERVENTIONS

RETURN DEMAND = B%

COUNTRY RISK +Z%

SECTOR RISK + Y%

PROJECT RISK + X% OFFERING CLIENTS BDS,MARKET LINKAGES, ETC.

DIRECT SUBSIDIES

RISK-FREE RATE = A% OFFERING NEAR RISK-FREE RETURNS

RETURNGUARANTEES

[email protected] www.e-mfp.eu

Basic Risk Matrix

RISK AREA MARK-UP RISK REDUCTION AREAS INTERVENTIONS

RETURN DEMAND = B%

COUNTRY RISK +Z%

SECTOR RISK + Y% PARTNERING WITH PRIVATESECTOR PLAYERS

RISK SHARING

PROJECT RISK + X% OFFERING CLIENTS BDS,MARKET LINKAGES, ETC.

DIRECT SUBSIDIES

RISK-FREE RATE = A% OFFERING NEAR RISK-FREE RETURNS

RETURNGUARANTEES

[email protected] www.e-mfp.eu

Basic Risk Matrix

RISK AREA MARK-UP RISK REDUCTION AREAS INTERVENTIONS

RETURN DEMAND = B%

COUNTRY RISK +Z% WORKING WITH GOVERNMENTREDUCING INSTITUTIONAL RISK

POLITICALLEVERAGE

SECTOR RISK + Y% PARTNERING WITH PRIVATESECTOR PLAYERS

RISK SHARING

PROJECT RISK + X% OFFERING CLIENTS BDS,MARKET LINKAGES, ETC.

DIRECT SUBSIDIES

RISK-FREE RATE = A% OFFERING NEAR RISK-FREE RETURNS

RETURNGUARANTEES

[email protected] www.e-mfp.eu

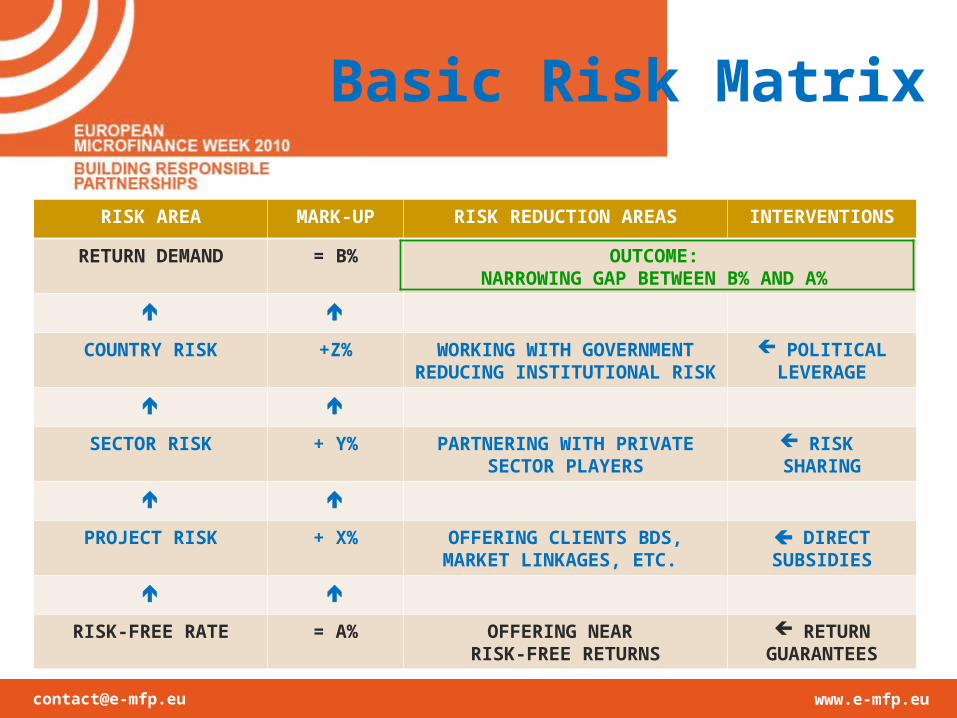

Basic Risk Matrix

RISK AREA MARK-UP RISK REDUCTION AREAS INTERVENTIONS

RETURN DEMAND = B% OUTCOME: NARROWING GAP BETWEEN B% AND A%

COUNTRY RISK +Z% WORKING WITH GOVERNMENTREDUCING INSTITUTIONAL RISK

POLITICALLEVERAGE

SECTOR RISK + Y% PARTNERING WITH PRIVATESECTOR PLAYERS

RISK SHARING

PROJECT RISK + X% OFFERING CLIENTS BDS,MARKET LINKAGES, ETC.

DIRECT SUBSIDIES

RISK-FREE RATE = A% OFFERING NEAR RISK-FREE RETURNS

RETURNGUARANTEES

[email protected] www.e-mfp.eu

Complicated?

Not really: it is how Public Private Partnerships work

The public sector decides on policy priorities Attending to market segments that are Commercially unfeasible but developmentally critical

The private sector invests and leads With risk reduction support from public sector Through performance-based contracting

And the civil society sector comes in To guard community interests and build capacities

[email protected] www.e-mfp.eu

Example?

It is how health systems work in many OECD countries

The public sector decides on policy priorities Affordable access to quality care By capping profits and offering low-risk returns

The private sector invests and leads Through accessing low-cost capital And making modest yet acceptable returns

And the civil society sector comes in By guarding patient interests

[email protected] www.e-mfp.eu

A Creative Approach

Therefore is based on multi-sector cooperation

That engineers respective roles and capabilities

Into functional PPPs that allow all sectors to make their required returns in financial and/or social terms

And makes finance really inclusive

[email protected] www.e-mfp.eu

And Ms. Thangam?

Under a creative PPP approach

She would not have borrowed beyond her means Or her loans would have been rescheduled Without destroying her marginal earning capacity

She would still have her goat, probably a few more Without having over-glutted the local market Perhaps she would have been a shareholder in a professional goat farm

And also her goat would have been in much better shape

Recommended