COMPREHENSIVE ANNUAL

FINANCIAL REPORT

OF

UPPER DEERFIELD TOWNSHIP

BOARD OF EDUCATION

UPPER DEERFIELD TOWNSHIP, NEW JERSEY

FOR THE FISCAL YEAR ENDED JUNE 30, 2016

Prepared by

Township of Upper Deerfield Township Board of Education

Finance Department

UPPER DEERFIELD TOWNSHIP SCHOOL DISTRICT

OUTLINE OF CAFR

INTRODUCTORY SECTION

Page

Letter of Transmittal

Roster of Officials

Consultants and Advisors

Organizational Chart

FINANCIAL SECTION

Independent Auditor’s Report 1-3

Required Supplementary Information - Part 1

Management’s Discussion and Analysis

Basic Financial Statements

A. District/Charter School-Wide Financial Statements:

A-1 Statement of Net Position 4

A-2 Statement of Activities 5

B. Fund Financial Statements:

Governmental Funds:

B-1 Balance Sheet 6

B-2 Statement of Revenues, Expenditures and Changes in Fund Balances 7

B-3 Reconciliation of the Statement of Revenues, Expenditures and Changes

In Fund Balances of Governmental Funds to the Statement of

Activities 8

Proprietary Funds:

B-4 Statement of Net Position 9

B-5 Statement of Revenues, Expenses and Changes in Fund Net Position 10

B-6 Statement of Cash Flows 11

Fiduciary Funds:

B-7 Statement of Fiduciary Net Position

12

B-8 Statement of Changes in Fiduciary Net Position 13

Notes to Financial Statements 14-37

Required Supplementary Information – Part II

C. Budgetary Comparison Schedules:

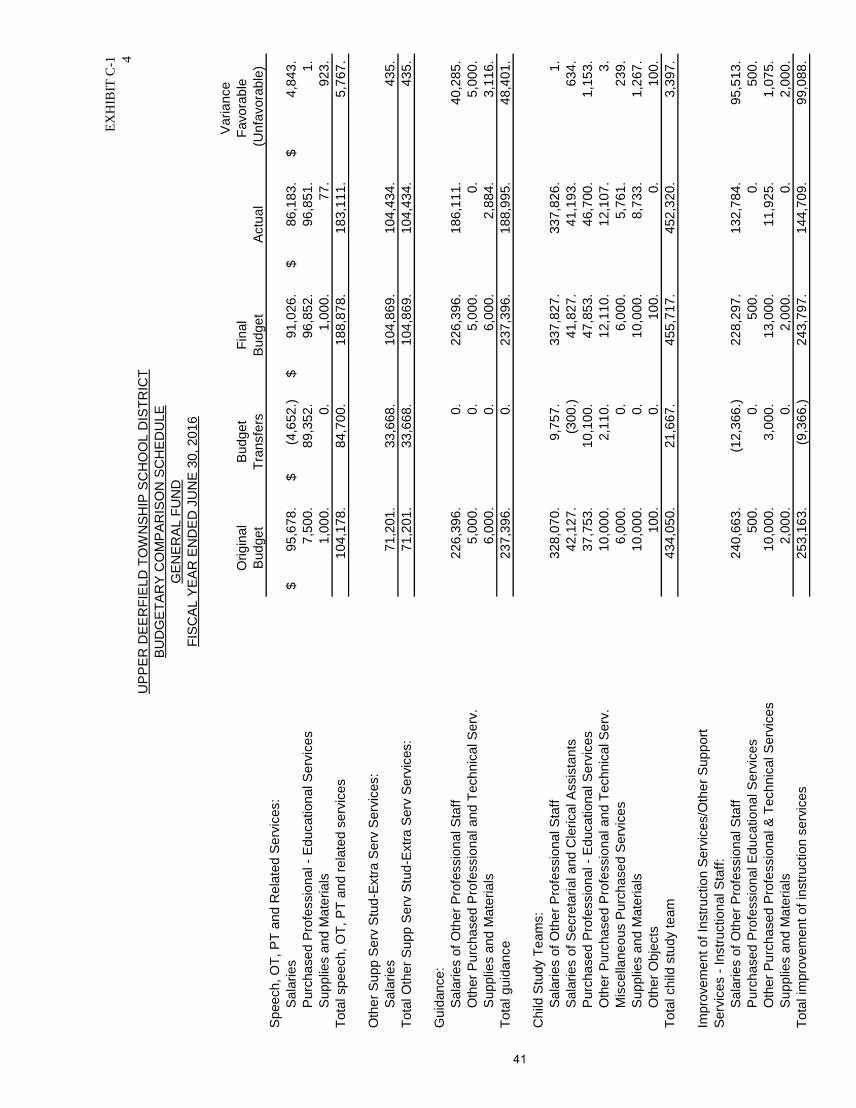

C-1 Budgetary Comparison Schedule – General Fund 38-46

C-1a Combining Schedule of Revenues, Expenditures, and Changes in Fund

Balance – Budget and Actual N/A

C-1b Education Jobs Fund Program – Budget and Actual N/A

C-2 Budgetary Comparison Schedule – Special Revenue Fund 47

UPPER DEERFIELD TOWNSHIP SCHOOL DISTRICT

OUTLINE OF CAFR

(Continued)

Page

Notes to the Required Supplementary Information – Part II

C-3 Budget-to-GAAP Reconciliations 48

Required Supplementary Information – Part III

L. Schedules Related to Accounting and Reporting for Pensions (GASB 68)

L-1 Schedule of the District’s Proportionate Share of the Net Pension 49

Liability – PERS

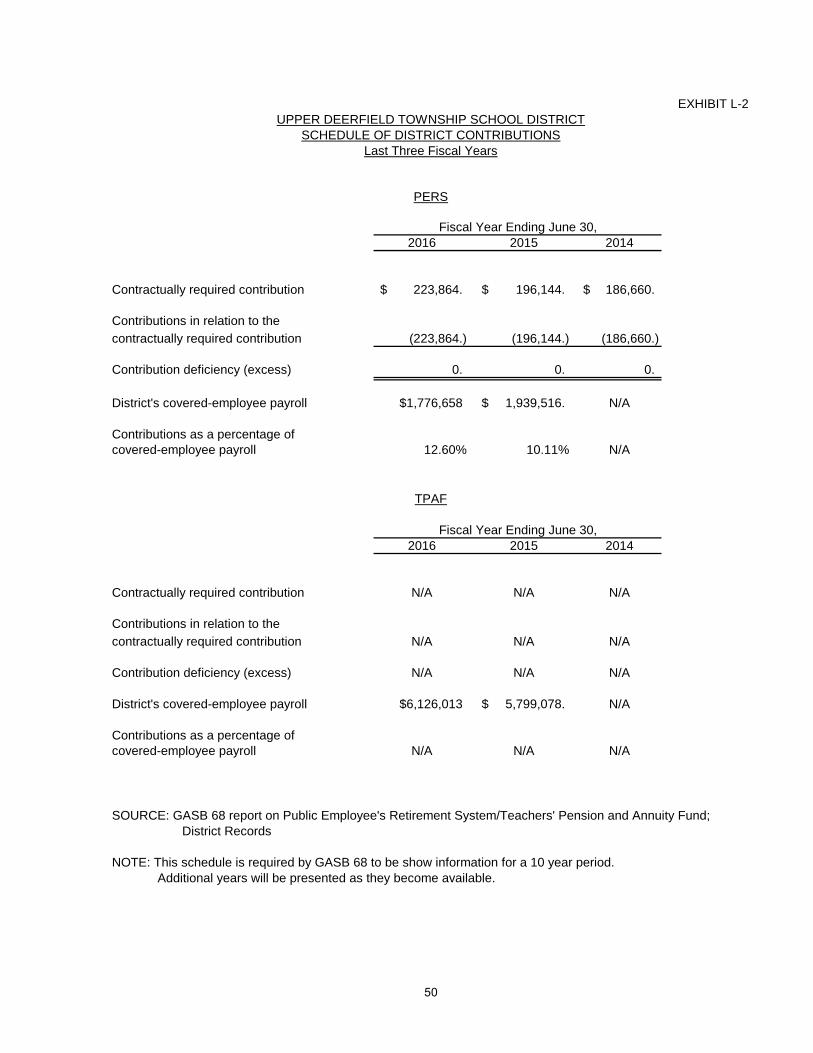

L-2 Schedule of District Contribution – PERS & TPAF 50

L-3 Schedule of the District’s Proportionate Share of the Net Pension

Liability – TPAF 51

Note to the Required Supplementary Information – Part III 52

Other Supplementary Information

D. School Based Budget Schedules:

D-1 Combining Balance Sheet N/A

D-2 Blended Resource Fund – Schedule of Expenditures Allocated

By Resource Type – Actual N/A

D-3 Blended Resource Fund – Schedule of Blended Expenditures –

Budget and Actual N/A

E. Special Revenue Fund:

E-1 Combining Schedule of Program Revenues and Expenditures Special

Revenue Fund – Budgetary Basis 53

E-2 Pre-School Education Aid Schedule(s) of Expenditures – Budgetary Basis 54

F. Capital Projects Fund:

F-1 Summary Schedule of Project Expenditures 55

F-2 Summary Schedule of Revenues, Expenditures, and Changes in Fund Balance –

Budgetary Basis 56

F-2a Schedule of Project Revenues, Expenditures, Project Balance, and Project

Status – Budgetary Basis – Charles F. Seabrook Elementary School: HVAC,

Roof, Security 57

F-2b Schedule of Project Revenues, Expenditures, Project Balance and Project

Status – Budgetary Basis – Elizabeth F. Moore School: HVAC, Roof,

Security 58

F-2c Schedule of Project Revenues, Expenditures, Project Balance, and Project

Status - Budgetary Basis – Woodruff Elementary School: HVAC, Roof,

Door/Window Replacement 59

G. Proprietary Funds:

Enterprise Fund:

G-1 Combining Schedule of Net Position 60

G-2 Combining Schedule of Revenues, Expenses and Changes in Fund Net Position 61

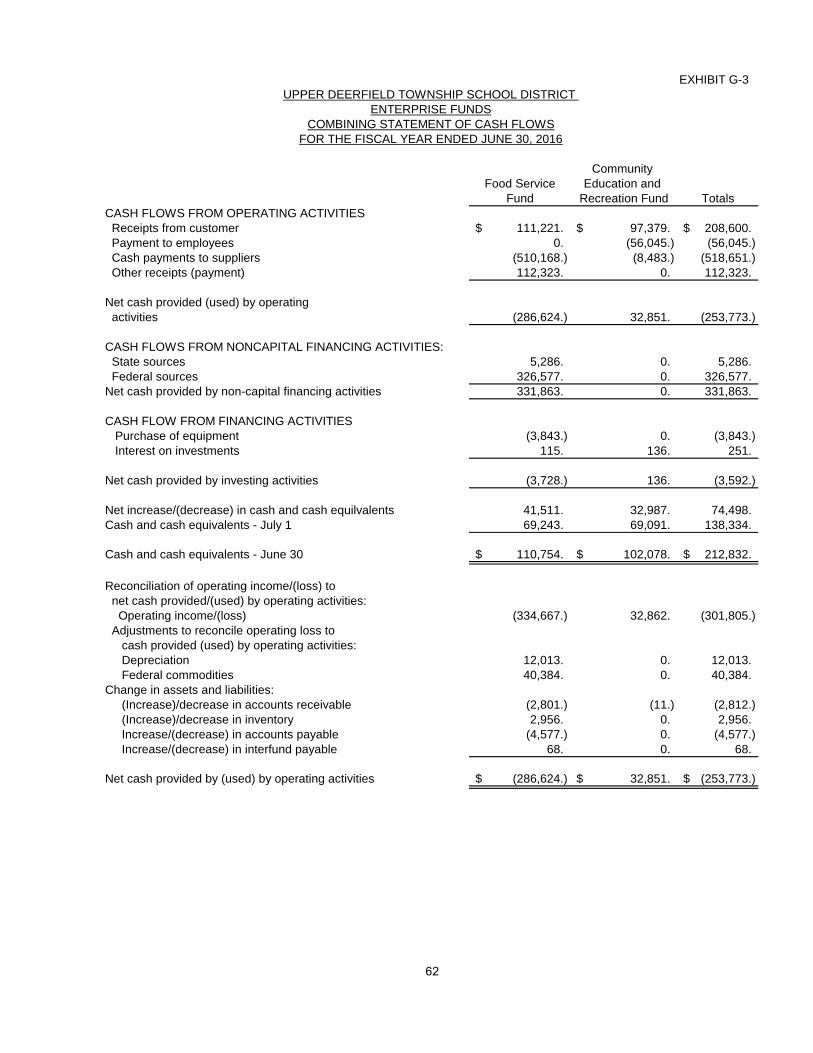

G-3 Combining Schedule of Cash Flows 62

UPPER DEERFIELD TOWNSHIP SCHOOL DISTRICT

OUTLINE OF CAFR

(Continued)

Page

H. Internal Service Fund:

G-4 Combining Schedule of Net Position 63

G-5 Combining Schedule of Revenues, Expenses and Changes in Fund Net Position 64

G-6 Combining Schedule of Cash Flows 65

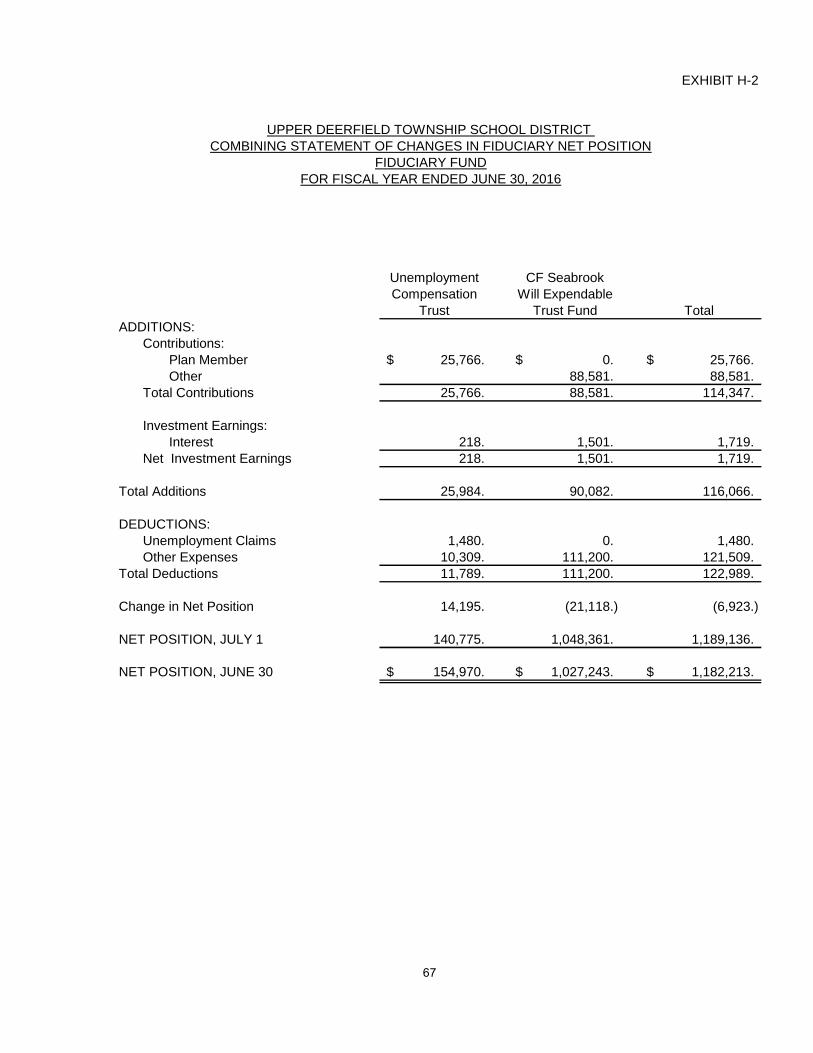

I. Fiduciary Fund:

H-1 Combining Statement of Fiduciary Net Position 66

H-2 Combining Statement of Changes in Fiduciary Net Position 67

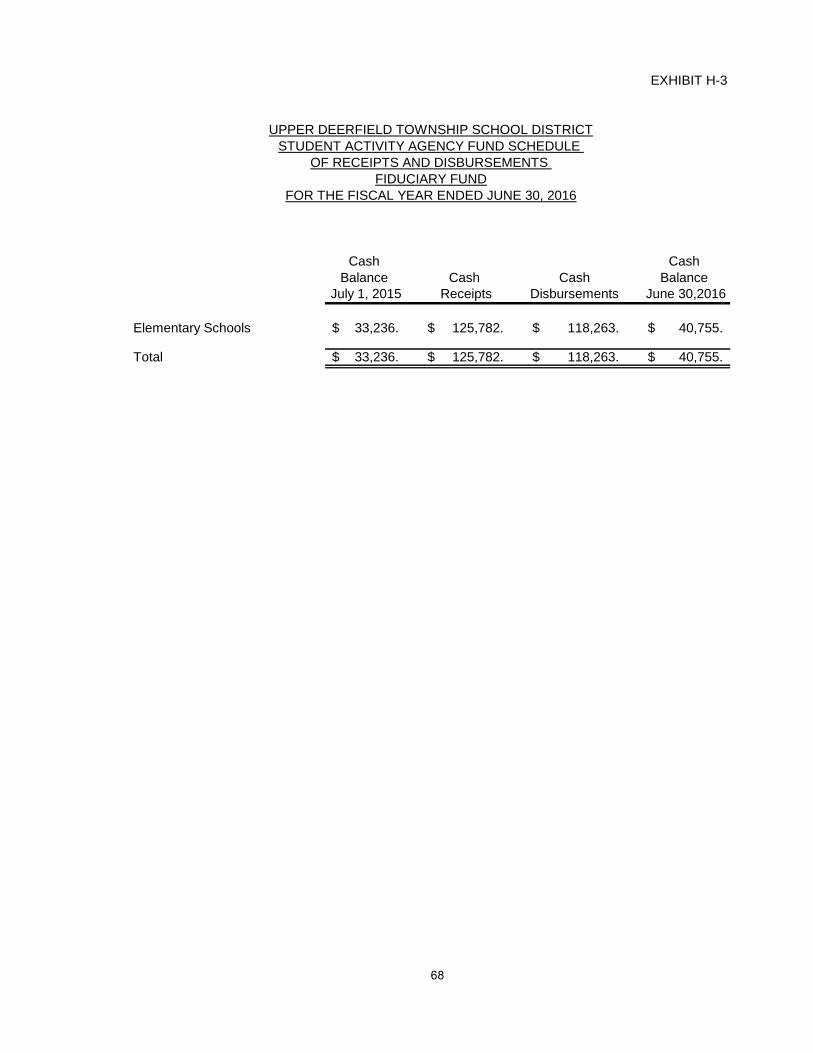

H-3 Student Activity Agency Fund Schedule of Receipts and Disbursements 68

H-4 Payroll Agency Fund Schedule of Receipts and Disbursements 69

J. Long-Term Debt:

I-1 Schedule of Serial Bonds 70

I-2 Schedule of Obligations Under Capital Leases N/A

I-3 Debt Service Fund Budgetary Comparison Schedule 71

Statistical Section

Financial Trends

J-1 Net Position by Component 72

J-2 Changes in Net Position 73-74

J-3 Fund Balances – Governmental Funds 75

J-4 Changes in Fund Balances – Governmental Funds 76-77

J-5 General Fund Other Local Revenue by Source 78

Revenue Capacity

J-6 Assessed Value and Estimated Actual Value of Taxable Property 79

J-7 Direct and Overlapping Property Tax Rates 80

J-8 Principal Property Taxpayers* 81

J-9 Property Tax Levies and Collections 82

Debt Capacity

J-10 Ratios of Outstanding Debt by Type 83

J-11 Ratios of Net General Bonded Debt Outstanding 84

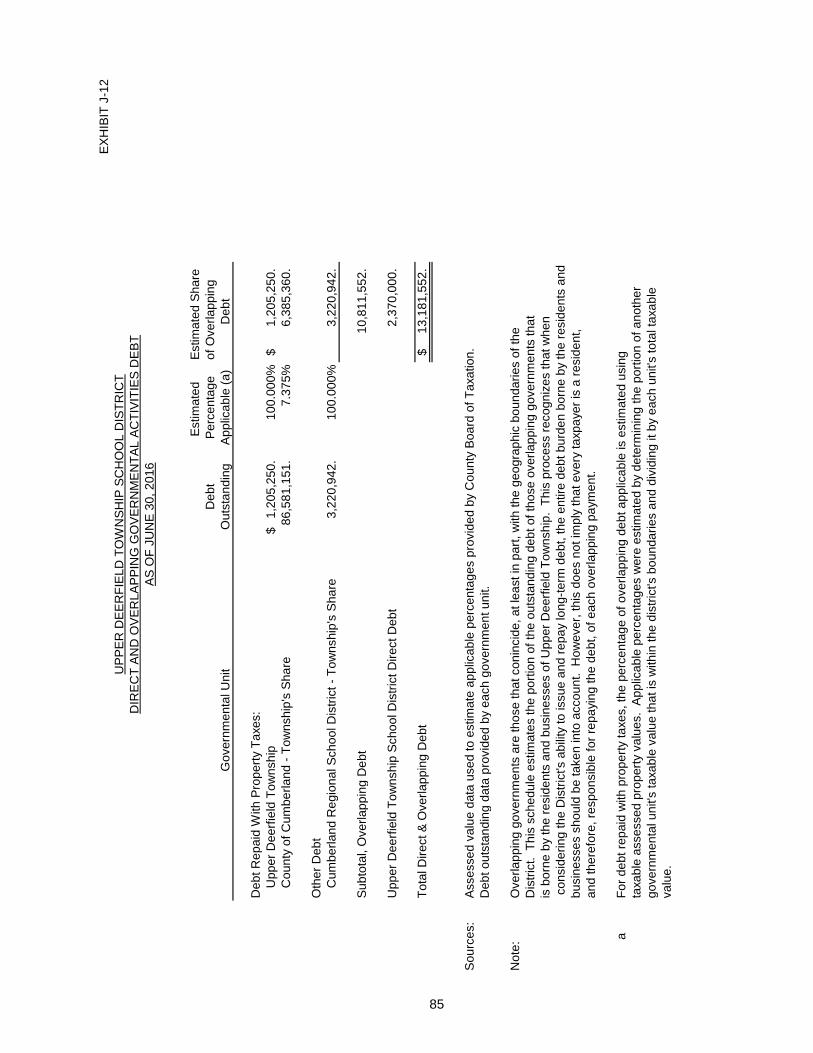

J-12 Direct and Overlapping Governmental Activities Debt 85

J-13 Legal Debt Margin Information 86

Demographic and Economic Information

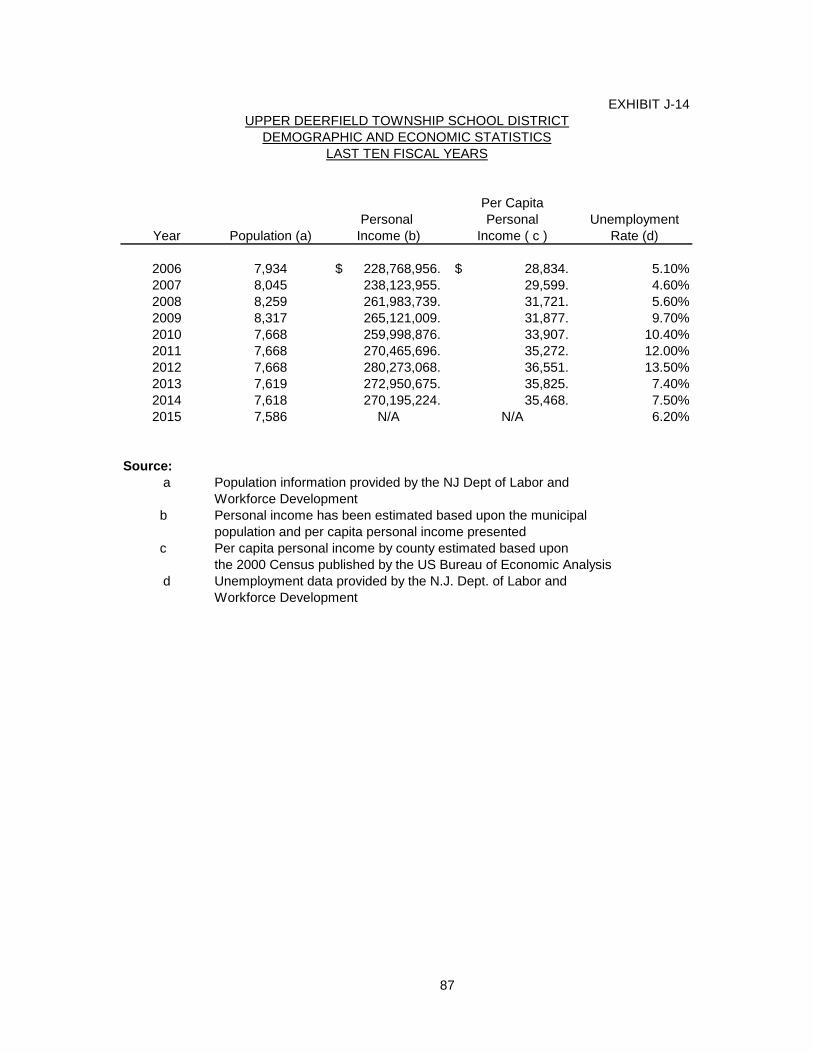

J-14 Demographic and Economic Statistics 87

J-15 Principal Employers 88

Operating Information

J-16 Full-Time Equivalent District/Charter School Employees by

Function/Program 89

J-17 Operating Statistics 90

J-18 School Building Information 91

J-19 Schedule of Required Maintenance Expenditures by School Facility 92

J-20 Insurance Schedule 93-94

UPPER DEERFIELD TOWNSHIP SCHOOL DISTRICT

OUTLINE OF CAFR

(Continued)

SINGLE AUDIT SECTION

K-1 Report on Internal Control over Financial Reporting and on Compliance

And Other Matters Based on an Audit of Financial Statements

Performed in Accordance with Government Auditing Standards 95-96

K-2 Report on Compliance For Each Major Program; Report on Internal Control

Over Compliance 97-99

K-3 Schedule of Expenditures of Federal Awards, Schedule A 100-101

K-4 Schedule of Expenditures of State Financial Assistance, Schedule B 102-103

K-5 Notes to the Schedules of Awards and Financial Assistance 104-105

K-6 Schedule of Findings and Questioned Costs 106-109

K-7 Summary Schedule of Prior Audit Findings 110

INTRODUCTORY SECTION

November 18, 2016

Honorable President and

Members of the Board of Education

Upper Deerfield Township School District

Seabrook, NJ 08302

Dear Board Members:

The comprehensive annual financial report of the Upper Deerfield Township School District for

the fiscal year ended June 30, 2016, is hereby submitted. Responsibility for both the accuracy of the data

and completeness and fairness of the presentation, including all disclosures, rests with the management of

the Upper Deerfield Township Board of Education. To the best of our knowledge and belief, the data

presented in this report is accurate in all material respects and is reported in a manner designated to

present fairly the financial position and results of operations of the various funds and account groups of

the District. All disclosures necessary to enable the reader to gain an understanding of the District’s

financial activities have been included.

The comprehensive annual financial report is presented in four sections: introductory, financial,

statistical and single audit. The introductory section includes this transmittal letter, the District’s

organizational chart and a list of principal officials. The financial section includes the general-purpose

financial statements and schedules, as well as the auditor’s report thereon. The statistical section includes

selected financial and demographic information, generally presented on a multi-year basis. The District is

required to undergo an annual single audit in conformity with the provisions of the Single Audit Act

Revisions of 1996 and the U.S. Office of Management and Budget, the Uniform Administrative

Requirements for Federal Awards 2 CFR 200 and NJ Treasury Circular OMB 15-08 OMB, “Single Audit

Policy for Recipients of Federal Grants, State Grants and State Aid Payments”. Information related to

this single audit, including the auditor’s report on the internal control structure and compliance with

applicable laws and regulations and findings and recommendations, are included in the single audit

section of this report.

1) REPORTING ENTITY AND ITS SERVICES: Upper Deerfield Township School District is an

independent reporting entity within the criteria adopted by the GASB as established by GASB

Statement No. 14. All funds and account groups of the District are included in this report. The

Upper Deerfield Township Board of Education and all its schools constitute the District’s reporting

entity.

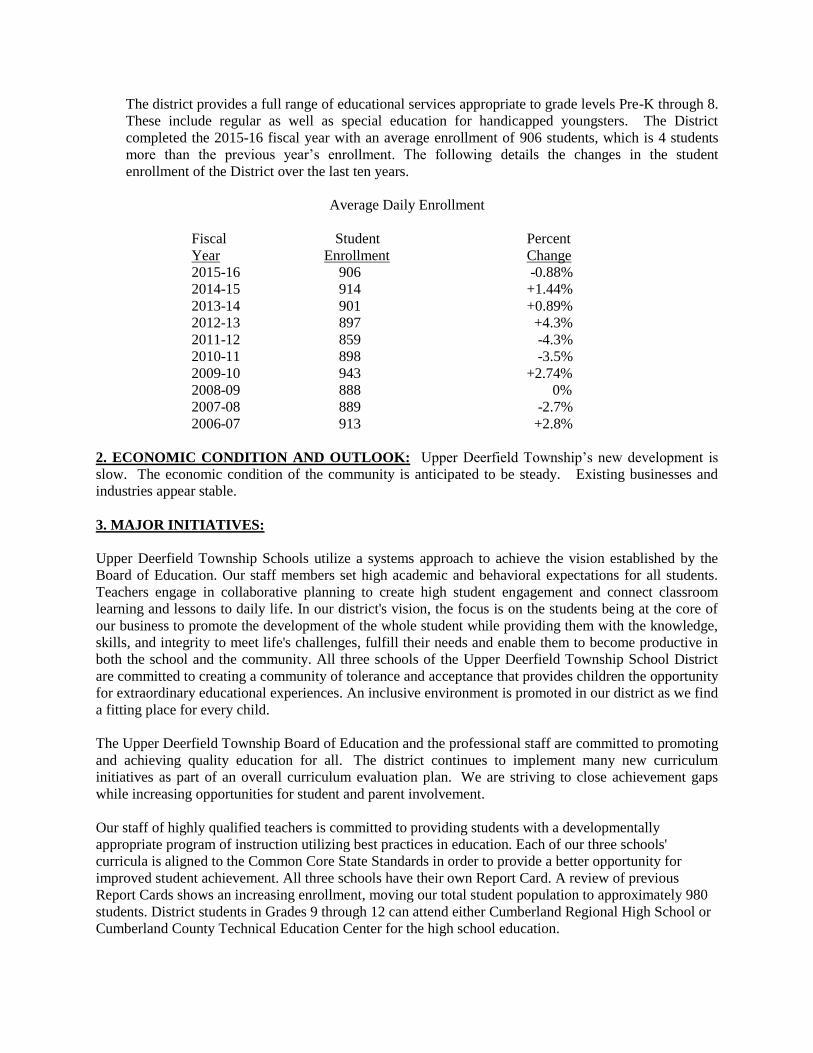

The district provides a full range of educational services appropriate to grade levels Pre-K through 8.

These include regular as well as special education for handicapped youngsters. The District

completed the 2015-16 fiscal year with an average enrollment of 906 students, which is 4 students

more than the previous year’s enrollment. The following details the changes in the student

enrollment of the District over the last ten years.

Average Daily Enrollment

Fiscal Student Percent

Year Enrollment Change

2015-16 906 -0.88%

2014-15 914 +1.44%

2013-14 901 +0.89%

2012-13 897 +4.3%

2011-12 859 -4.3%

2010-11 898 -3.5%

2009-10 943 +2.74%

2008-09 888 0%

2007-08 889 -2.7%

2006-07 913 +2.8%

2. ECONOMIC CONDITION AND OUTLOOK: Upper Deerfield Township’s new development is

slow. The economic condition of the community is anticipated to be steady. Existing businesses and

industries appear stable.

3. MAJOR INITIATIVES:

Upper Deerfield Township Schools utilize a systems approach to achieve the vision established by the

Board of Education. Our staff members set high academic and behavioral expectations for all students.

Teachers engage in collaborative planning to create high student engagement and connect classroom

learning and lessons to daily life. In our district's vision, the focus is on the students being at the core of

our business to promote the development of the whole student while providing them with the knowledge,

skills, and integrity to meet life's challenges, fulfill their needs and enable them to become productive in

both the school and the community. All three schools of the Upper Deerfield Township School District

are committed to creating a community of tolerance and acceptance that provides children the opportunity

for extraordinary educational experiences. An inclusive environment is promoted in our district as we find

a fitting place for every child.

The Upper Deerfield Township Board of Education and the professional staff are committed to promoting

and achieving quality education for all. The district continues to implement many new curriculum

initiatives as part of an overall curriculum evaluation plan. We are striving to close achievement gaps

while increasing opportunities for student and parent involvement.

Our staff of highly qualified teachers is committed to providing students with a developmentally

appropriate program of instruction utilizing best practices in education. Each of our three schools'

curricula is aligned to the Common Core State Standards in order to provide a better opportunity for

improved student achievement. All three schools have their own Report Card. A review of previous

Report Cards shows an increasing enrollment, moving our total student population to approximately 980

students. District students in Grades 9 through 12 can attend either Cumberland Regional High School or

Cumberland County Technical Education Center for the high school education.

Once again in the classrooms this year there is an across-the-board initiative to enhance student

engagement and responsibility for learning. The staff is committed to finding ways to continue to improve

student learning as evidenced by the work of several Professional Learning Communities (PLC) focusing

on this topic. The Common Core has been embraced and is being implemented on all levels, supported by

our ever expanding technology initiatives.

In grades three through eight students have individual chromebooks while the pre-k through grade two

students are working with iPads in the classroom which will be expanded for individual iPads in the next

year. There is access to computers in each building in a personal computer lab. The Common Core is

supplemented by an opportunity to participate in Spanish in grades four through eight and all students are

exposed to a rich experience in visual and performing arts and vocal and instrumental music.

Our community of Upper Deerfield has much to be proud of because of our three schools. The entire

School District "family" maintains a great sense of pride in all that has been and continues to be

accomplished in our district and our three schools both individually and collectively. Each school

collaborates with all of its stakeholders to continue a tradition of providing our students with an excellent,

challenging education in an environment promoting and cultivating lifelong skills. Our faculty, staff, and

parents dedicate their time and energy to our schools in order to provide each student with a rewarding

and enriching educational experience. The PTO is very involved in the successful operation of the District

as they work tirelessly not only to support, but also enhance the District both financially and in helping

provide assistance to staff in a variety of activities. The Board of Education continues to provide support

of the District leadership and staff through support of programs, policy and governance.

The educational programs are designed to ensure all students are provided with opportunities to prepare

themselves for the future of their choice. We recognize that not all children learn at the same rate.

Accordingly, our three schools are structured to provide diverse learning environments which actively

engage students in critical thinking, strategic planning, hands-on learning and problem solving. All

students are active partners in their learning experience and equally accepting of their responsibility to

challenge themselves to meet with success.

Upper Deerfield Township School District is reaching out into the community and continues to develop

partnerships with various businesses and other districts to share services. This provides additional

positive support in various ways and strengthens the educational effort of the school district.

4) INTERNAL ACCOUNTING CONTROLS: Management of the District is responsible for

establishing and maintaining an internal control structure designed to ensure that the assets of the District

are protected from loss, theft or misuse and to ensure that adequate accounting data are compiled to allow

for the preparation of financial statements in conformity with generally accepted accounting principles

(GAAP). The internal control structure is designed to provide reasonable, but not absolute, assurance that

these objectives are met. The concept of reasonable assurance recognizes that: (1) the cost of a control

should not exceed the benefits likely to be derived; and (2) the valuation of costs and benefits requires

estimates and judgments by management.

As a recipient of federal and state financial assistance, the District also is responsible for ensuring that an

adequate internal control structure is in place to ensure compliance with applicable laws and regulations

related to those programs. This internal control structure is also subject to periodic evaluation by the

District management.

As part of the District’s single audit described earlier, tests are made to determine the adequacy of the

internal control structure, including that portion related to federal and state financial assistance programs,

as well as to determine that the District has complied with applicable laws and regulations.

5)_ BUDGETARY CONTROLS: In addition to internal accounting controls, the District maintains

budgetary controls. The objective of these budgetary controls is to ensure compliance with legal

provisions embodied in the annual appropriation budget approved by the voters of the municipality.

Annual appropriation budgets are adopted for the general fund, the special revenue fund, and the debt

service fund. Project-length budgets are approved for the capital improvements accounted for in the

capital projects fund. The final budget amount as amended for the fiscal year is reflected in the financial

section.

An encumbrance accounting system is used to record outstanding purchase commitments on a line item

basis. Open encumbrances at year-end are either canceled or are included as reappropriation of fund

balance in the subsequent year. Those amounts to be reappropriated are reported as reservations of fund

balances at June 30, 2016.

6) ACCOUNTING SYSTEM AND REPORTS: The District’s accounting records reflect generally

accepted accounting principles, as promulgated by the Governmental Accounting Standards Board

(GASB). The accounting system of the District is organized on the basis of funds and account groups.

These funds and account groups are explained in “Notes to the Financial Statements”, Note 1.

7) FINANCIAL INFORMATION AT FISCAL YEAR-END: As demonstrated by the various

statements and schedules included in the financial section of this report, the District continues to meet its

responsibility for sound financial management. The following schedule presents a summary of the

general fund, special revenue fund and debt service fund revenues for the fiscal year ended June 30, 2016

and the amount and percentage of increases in relation to prior year revenues.

PERCENT INCREASE PERCENT OF

OF (DECREASE) INCREASE

REVENUE AMOUNT TOTAL FROM 2015 (DECREASE)

Local Sources $ 7,320,632. 44.37% $ 26,285. 0.36%

State Sources 7,964,013. 47.72% 119,282. 1.50%

Federal Sources 1,155,012. 4.75% 374,854. 32.45%

Total $ 16,439,657. 100.00% $ 520,421. 2.73%

The following schedule presents a summary of general fund, special revenue fund and debt service fund

expenditures for the fiscal year ended June 30, 2016 and the percentage of increases and decreases in

relation to prior year amounts.

PERCENT INCREASE PERCENT OF

OF (DECREASE) INCREASE

EXPENDITURES AMOUNT TOTAL FROM 2015 (DECREASE)

Current Expense:

Instruction $6,383,580. 39.16% $ 252,288. 3.95%

Undistributed

Expenditures: 9,072,729. 55.65% 769,787. 8.48%

Capital Outlay 326,682. 2.00% 156,156. 47.80%

Debt Service 518,976. 3.18% (16,072.) (3.10%)

Total $16,301,967. 100.00% $ 1,162,159. 7.13%

UPPER DEERFIELD TOWNSHIP BOARD OF EDUCATION

SEABROOK, NEW JERSEY

ROSTER OF OFFICIALS

JUNE 30, 2016

Members of the Board of Education Term Expires

Greg Peterson, President 2017

Mark Evans, Vice President 2015

Robert Atha 2015

Peter Ballinger 2016

Samuel Elwell 2017

Joseph Lee 2016

Anthony Buono 2015

Other Officials

Dr. Peter L. Koza, Superintendent

Cherie Ludy, School Business Administrator

Susan Robostello, Treasurer

FINANCIAL SECTION

INDEPENDENT AUDITOR’S REPORT

The Honorable President and

Members of the Board of Education

Upper Deerfield Township School District

County of Cumberland, New Jersey

Report on Financial Statements

We have audited the accompanying financial statements of the governmental activities, the business-type

activities, each major fund and the aggregate remaining fund information of the Board of Education of the

Upper Deerfield Township School District in the County of Cumberland, in the State of New Jersey, as of

and for the fiscal year ended June 30, 2016, and the related notes to the financial statements, which

collectively comprise the Board of Education’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in

accordance with accounting principles generally accepted in the United States of America; this includes the

design, implementation, and maintenance of internal control relevant to the preparation and fair

presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted

our audit in accordance with auditing standards generally accepted in the United States of America and the

standards applicable to financial audits contained in Government Auditing Standards, issued by the

Comptroller General of the United States; and audit requirements as prescribed by the Office of School

Finance, Department of Education, State of New Jersey. Those standards require that we plan and perform

the audit to obtain reasonable assurance about whether the financial statements are free from material

misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the

financial statements. The procedures selected depend on the auditor’s judgment, including the assessment

of the risks of material misstatement of the financial statements, whether due to fraud or error. In making

those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair

presentation of the financial statements in order to design audit procedures that are appropriate in the

circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal

control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness

of accounting policies used and the reasonableness of significant accounting estimates made by

management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our

audit opinions.

1

INDEPENDENT AUDITOR’S REPORT

(Continued)

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the

respective financial position of the governmental activities, the business-type activities, each major fund

and the aggregate remaining fund information of the Upper Deerfield Township Board of Education in the

County of Cumberland, State of New Jersey, as of June 30, 2016, and the respective changes in financial

position and, where applicable, cash flows thereof for the year then ended in accordance with accounting

principles generally accepted in the United States of America.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the Management’s

Discussion and Analysis, Budgetary Comparison Information, Schedules Related to Accounting and

Reporting for Pension, and Notes to the Required Supplemental Information on pages 38 through 51 and

52 be presented to supplement the basic financial statements. Such information, although not part of the

basic financial statements, is required by the Governmental Accounting Standards Board who considers it

to be an essential part of financial reporting for placing the basic financial statements in an appropriate

operational, economic, or historical context. We have applied certain limited procedures to the required

supplementary information in accordance with auditing standards generally accepted in the United States of

America, which consisted of inquiries of management about the methods of preparing the information and

comparing the information for consistency with management’s response to our inquiries, the basic financial

statements, and other knowledge we obtained during our audit of the basic financial statements. We do not

express an opinion or provide any assurance on the information because the limited procedures do not

provide us with sufficient evidence to express an opinion or provide any assurance.

Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively

comprise the Upper Deerfield Township Board of Education’s basic financial statements The

accompanying schedule of expenditures of federal awards as required by Title 2 U.S Code of Federal

Regulations Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements

for Federal Awards, (Uniform Guidance), and schedule of expenditures of state awards as required by

New Jersey OMB’s Circular 15-08, Single Audit Policy for Recipients of Federal Grants, State Grants,

and State Aid are presented for purposes of additional analysis and are not a required part of the basic

financial statements. The accompanying introductory information, statistical sections, combining and

individual non-major fund financial statements are also presented for purposes of additional analysis and

are not a required part of the basic financial statements.

The accompanying combining and individual non-major fund financial statements, schedule of expenditures

of federal awards, and schedule of expenditure of state awards are the responsibility of management and

were derived from and relate directly to the underlying accounting and other records used to prepare the

basic financial statements. Such information has been subjected to the auditing procedures applied in the

audit of the basic financial statements and certain additional procedures, including comparing and

reconciling such information directly to the underlying accounting and other records used to prepare the

basic financial statements or to the basic financial statements themselves, and other additional procedures

in accordance with auditing standards generally accepted in the United States of America. In our opinion,

the accompanying combining and individual non-major fund financial statements, schedule of expenditures

of federal awards, and schedule expenditures of state awards are fairly stated, in all material respects, in

relation to the basic financial statements as a whole.

2

INDEPENDENT AUDITOR’S REPORT

(Continued)

The introductory informational and statistical section have not been subjected to the auditing procedures

applied in the audit of the basic financial statements, and accordingly, we do not express an opinion or

provide any assurance on them.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated November 18,

2016 on our consideration of the Upper Deerfield Township Board of Education’s internal control over

financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts,

and grant agreements and other matters. The purpose of that report is to describe the scope of our testing

of internal control over financial reporting and compliance and the results of that testing, and not to provide

an opinion on internal control over financial reporting or on compliance. That report is an integral part of

an audit performed in accordance with Government Auditing Standards in considering Upper Deerfield

Township Board of Education’s internal control over financial reporting and compliance.

Respectfully submitted,

Samuel A. Delp, Jr.

Public School Accountant, #745

Triantos & Delp

Certified Public Accountants, LLC

November 18, 2016

3

REQUIRED SUPPLEMENTARY INFORMATION–PART I

MANAGEMENT’S DECISION AND ANALYSIS

Management Discussion and Analysis

This section of the Upper Deerfield Township School District’s Comprehensive Annual Financial

Report presents our discussion and analysis of the District’s financial performance during the fiscal

year ending on June 30, 2016. Please read it in conjunction with the transmittal letter at the front of this

report and the District’s financial statements, which immediately follow this section.

Overview of the Financial Statements

This annual report consists of three parts: management’s discussion and analysis (this section), the

basic financial statements, and required supplementary information. The basic financial statements

include two kinds of statements that present different views of the District:

The first two statements are district-wide financial statements that provide both short-term and

long-term information about the District’s overall financial status.

The remaining statements are fund financial statements that focus on individual parts of the

District, reporting the District’s operations in more detail than the District-wide statements.

The governmental funds statements tell how basic services such as regular and special

education were financed in the short term as well as what remains for future spending.

Proprietary funds statements offer short- and long-term financial information about activities

the District operates like businesses.

Fiduciary funds statements provide information about the financial relationships in which the

District acts solely as a trustee or agent for the benefit of others.

The financial statements also include notes that explain some of the information in the statements and

provide more detailed data. The statements are followed by a section of required supplementary

information that further explains and supports the financial statements with a comparison of the

District’s budget for the year.

Figure A-1 below summarizes the major features of the District’s financial statements, including the

portion of the District’s activities that cover and the types of information they contain. The remainder

of this overview section of management’s discussion and analysis highlights the structure and contents

of each of the statements.

Figure A-1: Major Features of the District wide and Fund Financial Statements

Fund Financial Statements

District-wide

Statements

Governmental Funds

Proprietary Funds

Fiduciary Funds

Scope Entire district

(except fiduciary

funds)

The activities of the

district that are not

proprietary or fiduciary,

such as special education and building

maintenance

Activities the district

operates similar to private

businesses: food services

is included here

Instances in which

the district

administers resources

on behalf of someone else, such as

scholarship programs

and student activities monies

Required

Financial

Statements

Statement

of net assets

Statement

of activities

Balance Sheet

Statement of

revenues,

expenditures,

and changes in fund balances

Statement of net

assets

Statement of

revenues,

expenses, and changes in fund

net assets

Statement of cash

flows

Statement of

fiduciary net

assets

Statement of

changes in fiduciary net

assets

Accounting

Basis and

Measurement

Focus

Accrual accounting

and economic

resources focus

Modified accrual

accounting and current

financial focus

Accrual accounting and

economic resources focus

Accrual accounting

and economic

resources focus

Type of

Asset/Liability

All assets and liabilities, both

financial and capital,

short-term and long-term

Generally assets expected to be used up

and liabilities that come

due during the year or soon thereafter; no

capital assets or long-

term liabilities included

All assets and liabilities, both financial and capital,

and short-term and long-

term

All assets and liabilities, both short-

term and long-term;

funds do not currently contain

capital assets,

although they can

Type of

Inflow/Outflow

Information

All revenues and expenses during the

year, regardless

of when cash is received or paid

Revenues for which cash is received during

or soon after the end of

the year; expenditures when goods or services

have been received and

the related liability is due and payable

All revenues and expenses during the year,

regardless of when cash

is received or paid

All additions and deductions during the

year, regardless of

when cash is received or paid

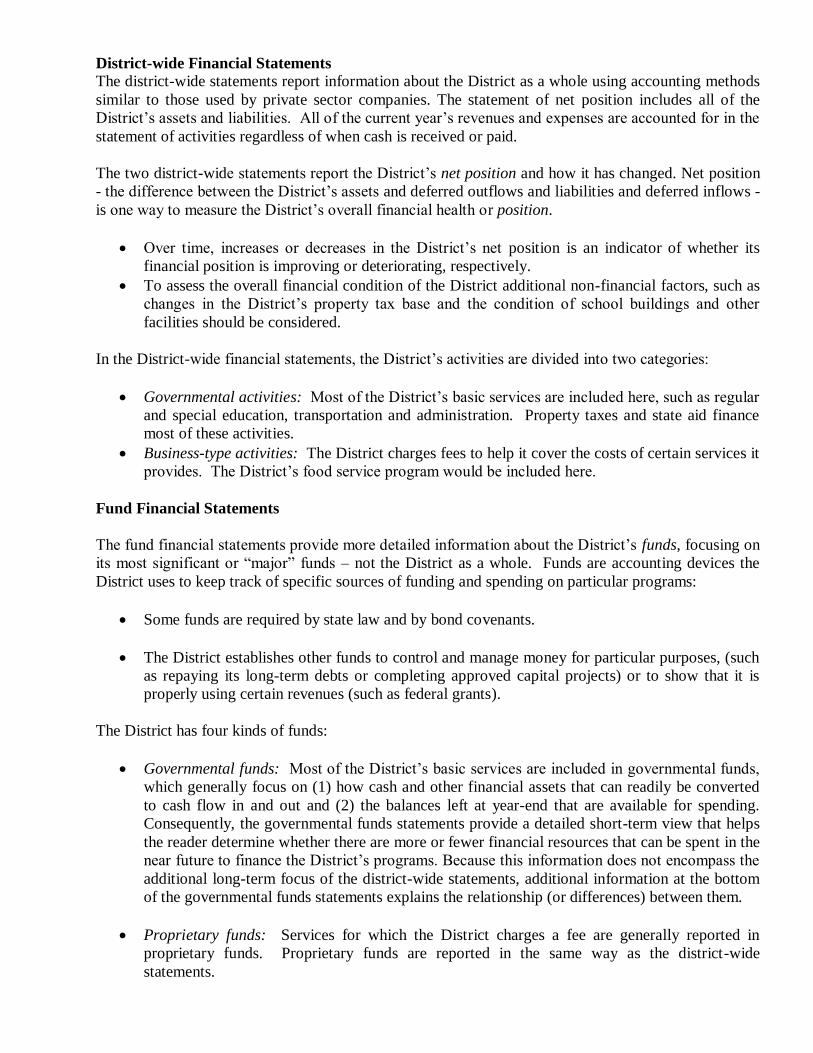

District-wide Financial Statements

The district-wide statements report information about the District as a whole using accounting methods

similar to those used by private sector companies. The statement of net position includes all of the

District’s assets and liabilities. All of the current year’s revenues and expenses are accounted for in the

statement of activities regardless of when cash is received or paid.

The two district-wide statements report the District’s net position and how it has changed. Net position

- the difference between the District’s assets and deferred outflows and liabilities and deferred inflows -

is one way to measure the District’s overall financial health or position.

Over time, increases or decreases in the District’s net position is an indicator of whether its

financial position is improving or deteriorating, respectively.

To assess the overall financial condition of the District additional non-financial factors, such as

changes in the District’s property tax base and the condition of school buildings and other

facilities should be considered.

In the District-wide financial statements, the District’s activities are divided into two categories:

Governmental activities: Most of the District’s basic services are included here, such as regular

and special education, transportation and administration. Property taxes and state aid finance

most of these activities.

Business-type activities: The District charges fees to help it cover the costs of certain services it

provides. The District’s food service program would be included here.

Fund Financial Statements

The fund financial statements provide more detailed information about the District’s funds, focusing on

its most significant or “major” funds – not the District as a whole. Funds are accounting devices the

District uses to keep track of specific sources of funding and spending on particular programs:

Some funds are required by state law and by bond covenants.

The District establishes other funds to control and manage money for particular purposes, (such

as repaying its long-term debts or completing approved capital projects) or to show that it is

properly using certain revenues (such as federal grants).

The District has four kinds of funds:

Governmental funds: Most of the District’s basic services are included in governmental funds,

which generally focus on (1) how cash and other financial assets that can readily be converted

to cash flow in and out and (2) the balances left at year-end that are available for spending.

Consequently, the governmental funds statements provide a detailed short-term view that helps

the reader determine whether there are more or fewer financial resources that can be spent in the

near future to finance the District’s programs. Because this information does not encompass the

additional long-term focus of the district-wide statements, additional information at the bottom

of the governmental funds statements explains the relationship (or differences) between them.

Proprietary funds: Services for which the District charges a fee are generally reported in

proprietary funds. Proprietary funds are reported in the same way as the district-wide

statements.

In fact, the District’s enterprise funds (one type of proprietary fund) are the same as its

business-type activities, but provide more detail and additional information, such as cash flow.

Internal service funds: (the other kind of proprietary fund) are optional and utilized to report

activities that provide supplies and services for other District programs and activities.

Fiduciary funds: The District is the trustee, or fiduciary, for assets that belong to others, such as

the student activity fund. The District is responsible for ensuring that the assets reported in

these funds are used only for their intended purposes and by those to whom the assets belong.

The District excludes these activities from the district-wide financial statements because the

District cannot use these assets to finance its operations.

Financial Analysis of the District as a Whole

(in thousands)

Net assets. The District’s combined net assets are $9,852 on June 30, 2016 (see Table A-1). Less than

3% of the total net assets are from business-type activities. The balance of the total net assets, which is

in excess of 97%, attributable to governmental activities.

Changes in net assets. The District’s total revenues are $21,185 for the fiscal period ended June 30,

2016 (see Table A-2). Property taxes and state formula aid accounted for 72% of the District’s

revenue. 15% is derived from state and federal aid for specific programs, and the remainder, 13% from

fees charged for services and miscellaneous resources.

The District’s predominant expenses are related to educating and caring for students 44%. The purely

administrative activities of the District accounted for 6% of total costs. Salary increases due to

contractual agreements for teachers and other educational staff are included in the instruction-related

costs. Total revenues surpassed expenses increasing net assets approximately $159 last year, primarily

in governmental activities.

Governmental Activities.

Revenues for governmental activities were $20,492. Total expenses amounted to $20,400. The

increase in net position in governmental activities of $92 for 2016.

Business-Type Activities.

Revenues of the District’s business-type activities amounted to $693 and expenses were $626. Factors

contributing to these results included:

The community school had revenue in excess of expenses of approximately $35.

Food service revenue in excess of expenses of approximately $33.

Financial Analysis of the District’s Funds

(in thousands)

The strong financial performance of the District as a whole is primarily reflected in its governmental funds.

As the district completed the year, its governmental funds reported combined balances of $2,359 of which

$26 was reserved per capital improvements in the capital project fund. Miscellaneous revenue exceeded the

amounts anticipated in the 2016 budget.

General Fund Budgetary Highlights

Over the course of the year, the District revised the annual operating budget several times. These

budget amendments were due to:

Transfers between budgetary line accounts to prevent overruns.

The District’s final budget anticipated utilizing $680 in fund balance and $205 of prior year

encumbrances to fund the appropriation plan for this fiscal period. The actual result of operations was

an increase in the general fund balance of $135.

Actual expenditures for capital outlay amounted to $327 in the Operating Fund and $119 in the Capital

Projects Fund.

Capital Asset and Debt Administration

(in thousands)

Capital Assets

By the end of 2016, the District had invested $22,843 in a broad range of capital assets, including

school buildings, athletic facilities, computer and audiovisual equipment, and administrative offices.

(See Table A-3) (More detailed information about capital assets can be found in Note 5 to the financial

statements.) Total depreciation expenses for the year was $565 while building improvements and

additions to equipment and furniture and land amounted to $342.

Long-Term Debt

The state limits the amount of general obligation debt the District can issue to 3 percent of the

equalized valuation of all taxable property within the District. The current limit is $18,708 of which

$16,338 is available for the issuance of debt.

Factors Bearing on the District’s Future

At the time these financial statements were prepared and audited, the District was aware of the

following existing circumstances that could significantly affect its financial health in the future:

State Formula Aid for the fiscal year 2015-2016 was flat funded to the previous year. It is the

District’s hope the State will apply the CEIFA formula resulting in the distribution of aid on the

formula’s enrollment basis. By including the District in the litigation regarding the effect of not

being funded by the SFRA, the District hopes to obtain financial award in the future. The

District’s special revenue is an unpredictable revenue source. The District avails itself of every

grant opportunity to increase educational opportunities for the students.

Contacting the District’s Financial Management

This financial report is designed to provide the District’s citizens, taxpayers, customers, investors and

creditors with a general overview of the District’s finances and to demonstrate the District’s

accountability of the money it receives. If you have questions about this report or need additional

financial information, contact Cherie Bratty Assistant Superintendent for Business/Board Secretary,

Upper Deerfield Township School District, 1385 Highway 77, Seabrook, NJ 08302.

To

tal

Per

cen

tage

Ch

ange

2015

2016

2015

2016

2015

2016

2015-2

016

Curr

ent

and O

ther

Ass

ets

2,6

66.

$

2,7

16.

$

197.

$

368.

$

2

,86

3.

$

3

,08

4.

$

7

.7%

Cap

ital

Ass

ets

14,9

38.

14,7

15.

89.

81.

15

,02

7.

14

,79

6.

-1.5

%

To

tal A

ssets

17,6

04.

$

17,4

31.

$

286.

$

449.

$

1

7,8

90

.$

1

7,8

80

.$

-0

.1%

Defe

rred

Ou

tflo

ws o

f R

eso

urc

es

560.

$

1,5

72.

$

0.

$

0.

$

0

.$

1,5

72

.$

0.0

%

Curr

ent

Lia

bil

itie

s1,0

71.

$

1,0

35.

$

33.

$

28.

$

1,1

04

.$

1,0

63

.$

-3.7

%

Noncu

rren

t L

iab

ilit

ies

7,2

30.

8,2

14.

0.

0.

7

,23

0.

8

,21

4.

1

3.6

%

To

tal L

iab

ilit

ies

8,3

01.

$

9,2

49.

$

33.

$

28.

$

8,3

34

.$

9,2

77

.$

11

.3%

Defe

rred

In

flo

ws o

f R

eso

urc

es

424.

$

223.

$

0.

$

0.

$

0

.$

22

3.

$

0

.0%

Net P

ositio

n

Inves

ted i

n C

apit

al A

sset

s

Net

of

Rel

ated

Deb

t12,1

13.

$

12,3

45.

$

89.

$

81.

$

12

,20

2.

$

12

,42

6.

$

1.8

%

Res

tric

ted

2,4

19.

2,7

16.

0.

0.

2

,41

9.

2

,71

6.

1

2.3

%

Unre

stri

cted

(5,0

93.)

(5,5

30.)

164.

240.

(4

,92

9.)

(5,2

90

.)

7.3

%

To

tal N

et

Po

sit

ion

9,4

39.

$

9,5

31.

$

253.

$

321.

$

9

,69

2.

$

9

,85

2.

$

0

.$

To

tal

Sch

oo

l D

istr

ict

Tab

le A

-1

Upper

Deerf

ield

Tow

nship

Board

of

Education's

Net P

ositio

n

(in

thousa

nds

of

doll

ars)

Gover

nm

enta

l

Act

ivit

ies

Busi

nes

s-ty

pe

Act

ivit

ies

To

tal

Per

cen

tage

Ch

ange

2015

2016

2015

2016

2015

2016

2015-2

016

Rev

en

ues

Pro

gra

m R

evenues

Charg

es f

or

Serv

ices

2,1

00.

$

2,0

93.

$

318.

$

324.

$

2,4

18

.$

2,4

17

.$

0

.0%

Federa

l &

Sta

te C

ate

gorical G

rants

2,7

21.

2,9

11.

365.

369.

3,0

86

.

3,2

80

.

6

.3%

Genera

l R

evenues

Pro

pert

y T

axes

7,0

48.

7,1

62.

0.

0.

7

,04

8.

7

,16

2.

1

.6%

Sta

te F

orm

ula

Aid

7,4

03.

8,1

68.

0.

0.

7

,40

3.

8

,16

8.

1

0.3

%

Oth

er

285.

158.

0.

0.

2

85

.

15

8.

-44

.6%

To

tal R

ev

en

ues

19,5

57.

$

20,4

92.

$

683.

$

693.

$

20

,24

0.

$

21

,18

5.

$

4.7

%

Exp

en

ses

Instr

uction -

Rela

ted

6,4

94.

$

6,7

51.

$

60.

$

65.

$

6,5

54

.$

6,8

16

.$

4

.0%

Stu

dent S

upport

Serv

ices

1,4

62.

1,8

19.

576.

561.

2,0

38

.

2,3

80

.

1

6.8

%

Main

tenance &

Opera

tions

1,3

15.

1,4

75.

0.

0.

1

,31

5.

1

,47

5.

1

2.2

%

Tra

nsport

ation

861.

776.

0.

0.

8

61

.

77

6.

-9.9

%

Adm

inis

tration

1,1

65.

1,1

87.

0.

0.

1

,16

5.

1

,18

7.

1

.9%

Oth

er

7,5

99.

8,3

92.

0.

0.

7

,59

9.

8

,39

2.

1

0.4

%

To

tal E

xp

en

ses

18,8

96.

$

20,4

00.

$

636.

$

626.

$

19

,53

2.

$

21

,02

6.

$

0.

$

Inc

rease/

(de

cre

ase)

in N

et

Po

sit

ion

661.

$

92.

$

47.

$

67.

$

70

8.

$

15

9.

$

(0.)

$

Tab

le A

-2

To

tal

Sch

oo

l D

istr

ict

Changes in N

et P

ositio

n

Upper

Deerf

ield

Tow

nship

Board

of

Education's

(in

thousa

nds

of

doll

ars)

Gover

nm

enta

l

Act

ivit

ies

Busi

nes

s-ty

pe

Act

ivit

ies

To

tal

Per

cen

tage

Ch

ange

2015

2016

2015

2016

2015

2016

2015-2

016

Land

312.

$

312.

$

0.

$

0.

$

3

12

.$

3

12

.$

0

.0%

Constr

uction in P

rogre

ss

12.

0.

0.

0.

1

2.

0

.

0

.0%

Site Im

pro

vem

ents

60.

55.

0.

0.

6

0.

5

5.

-8.3

%

Build

ings &

Im

pro

vem

ents

14,3

07.

14,1

33.

0.

0.

14,3

07

.

14

,13

3.

-1.2

%

Machin

ery

& E

quip

ment

247.

215.

81.

81.

32

8.

29

6.

-9

.8%

To

tal

14,9

38.

$

14,7

15.

$

81.

$

81.

$

15,0

19

.$

14

,79

6.

$

-1.5

%

Tab

le A

-3

To

tal

Sch

oo

l D

istr

ict

Upper

Deerf

ield

Tow

nship

Board

of

Education's

Capital A

ssets

(in t

housa

nds

of

doll

ars)

Gover

nm

enta

l

Act

ivit

ies

Busi

nes

s-ty

pe

Act

ivit

ies

(Net

of

Dep

reci

atio

n)

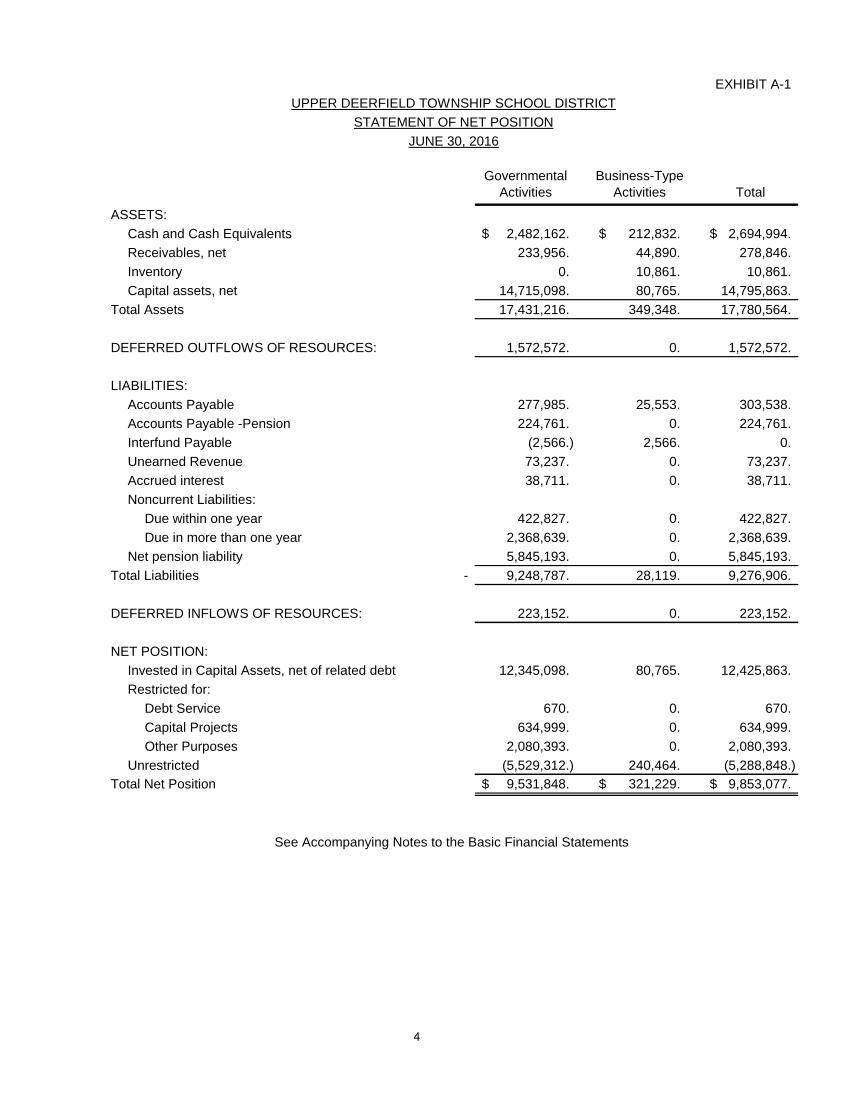

BASIC FINANCIAL STATEMENTS

DISTRICT-WIDE FINANCIAL STATEMENTS

EXHIBIT A-1

Governmental

Activities

Business-Type

Activities Total

ASSETS:

Cash and Cash Equivalents 2,482,162.$ 212,832.$ 2,694,994.$

Receivables, net 233,956. 44,890. 278,846.

Inventory 0. 10,861. 10,861.

Capital assets, net 14,715,098. 80,765. 14,795,863.

Total Assets 17,431,216. 349,348. 17,780,564.

DEFERRED OUTFLOWS OF RESOURCES: 1,572,572. 0. 1,572,572.

LIABILITIES:

Accounts Payable 277,985. 25,553. 303,538.

Accounts Payable -Pension 224,761. 0. 224,761.

Interfund Payable (2,566.) 2,566. 0.

Unearned Revenue 73,237. 0. 73,237.

Accrued interest 38,711. 0. 38,711.

Noncurrent Liabilities:

Due within one year 422,827. 0. 422,827.

Due in more than one year 2,368,639. 0. 2,368,639.

Net pension liability 5,845,193. 0. 5,845,193.

Total Liabilities - 9,248,787. 28,119. 9,276,906.

DEFERRED INFLOWS OF RESOURCES: 223,152. 0. 223,152.

NET POSITION:

Invested in Capital Assets, net of related debt 12,345,098. 80,765. 12,425,863.

Restricted for:

Debt Service 670. 0. 670.

Capital Projects 634,999. 0. 634,999.

Other Purposes 2,080,393. 0. 2,080,393.

Unrestricted (5,529,312.) 240,464. (5,288,848.)

Total Net Position 9,531,848.$ 321,229.$ 9,853,077.$

JUNE 30, 2016

STATEMENT OF NET POSITION

UPPER DEERFIELD TOWNSHIP SCHOOL DISTRICT

See Accompanying Notes to the Basic Financial Statements

4

EX

HIB

IT A

-2

Ne

t (E

xpe

nse

) R

eve

nue

S a

nd

Cha

nge

s in N

et A

sse

ts

Cha

rge

s f

or

Ope

rating G

rants

C

apita

l G

rants

G

ove

rnm

enta

lB

usin

ess-t

ype

Functio

ns/P

rogra

ms

Expe

nse

sS

erv

ice

sa

nd

Co

ntr

ibutio

ns

and

Co

ntr

ibutio

ns

Activitie

sA

ctivitie

sT

ota

l

G

ove

rnm

enta

l a

ctivitie

s:

In

str

uctio

n:

R

egula

r4

,22

2,2

25

.$

0.

$

0.

$

0.

$

(4,2

22

,22

5.)

$

0.

$

(4,2

22

,22

5.)

$

S

pe

cia

l ed

uca

tion

2,3

54

,41

6.

(2,3

54

,41

6.)

(2,3

54

,41

6.)

O

the

r spe

cia

l in

str

uction

17

4,0

65

.

(17

4,0

65

.)

(17

4,0

65

.)

S

uppo

rt s

erv

ice

s:

T

uitio

n2

03

,94

9.

(20

3,9

49

.)

(20

3,9

49

.)

S

tud

ent &

instr

uction r

ela

ted

se

rvic

es

1,6

14

,57

4.

(1,6

14

,57

4.)

(1,6

14

,57

4.)

S

cho

ol ad

min

istr

ative

se

rvic

es

50

7,4

46

.

(50

7,4

46

.)

(50

7,4

46

.)

G

ene

ral and

busin

ess a

dm

inis

tra

tive

se

rvic

es

31

5,9

93

.

(31

5,9

93

.)

(31

5,9

93

.)

C

entr

al se

rvic

es

25

0,0

54

.

(25

0,0

54

.)

(25

0,0

54

.)

A

dm

in info

te

chce

s1

13

,72

0.

(11

3,7

20

.)

(11

3,7

20

.)

P

lant o

pe

rations a

nd

ma

inte

na

nce

1,4

74

,66

1.

(1,4

74

,66

1.)

(1,4

74

,66

1.)

P

upil

tra

nspo

rta

tion

77

5,6

24

.

(77

5,6

24

.)

(77

5,6

24

.)

E

mplo

ye

e b

ene

fits

6,0

72

,73

7.

2,9

10

,86

5.

(3,1

61

,87

2.)

(3,1

61

,87

2.)

In

tere

st o

n lo

ng-t

erm

de

bt

10

2,2

80

.

(10

2,2

80

.)

(10

2,2

80

.)

T

ransfe

r to

cha

rte

r scho

ol

20

,54

9.

(20

,54

9.)

(20

,54

9.)

In

tern

al se

rvic

e f

und

2,0

93

,93

9.

2,0

92

,87

8.

(1,0

61

.)

(1,0

61

.)

S

tate

de

bt se

rvic

e a

sse

ssm

ent

10

4,6

18

.

(10

4,6

18

.)

(10

4,6

18

.)

T

ota

l go

ve

rnm

enta

l activitie

s2

0,4

00

,85

0.

2,0

92

,87

8.

2,9

10

,86

5.

0.

(15

,39

7,1

07

.)

0.

(15

,39

7,1

07

.)

B

usin

ess-t

ype

activitie

s:

F

oo

d S

erv

ice

56

0,9

45

.

22

6,2

78

.

36

9,2

15

.

0.

0.

34

,54

8.

34

,54

8.

C

ER

64

,52

8.

97

,39

0.

0.

0.

0.

32

,86

2.

32

,86

2.

T

ota

l busin

ess-t

ype

activitie

s6

25

,47

3.

32

3,6

68

.

36

9,2

15

.

0.

0.

67

,41

0.

67

,41

0.

To

tal prim

ary

go

ve

rnm

ent

21

,02

6,3

23

.$

2,4

16

,54

6.

$

3,2

80

,08

0.

$

0.

$

(15

,39

7,1

07

.)$

67

,41

0.

$

(15

,32

9,6

97

.)$

Ge

ne

ral re

ve

nue

s:

Ta

xe

s:

P

rope

rty ta

xe

s, le

vie

d f

or

ge

ne

ral purp

ose

s,n

et

6,6

44

,24

8.

$

0.

$

6,6

44

,24

8.

$

T

axe

s le

vie

d f

or

de

bt se

rvic

e5

17

,95

2.

51

7,9

52

.

Fe

de

ral a

nd

Sta

te a

id n

ot re

str

icte

d

6,7

89

,15

3.

6,7

89

,15

3.

Fe

de

ral a

nd

Sta

te a

id r

estr

icte

d

1,3

79

,45

7.

1,3

79

,45

7.

Tuitio

n r

ece

ive

d7

9,2

06

.

79

,20

6.

Inve

stm

ent e

arn

ings

4,9

91

.

25

1.

5,2

42

.

Mis

ce

llane

ous inco

me

74

,48

8.

74

,48

8.

To

tal ge

ne

ral re

ve

nue

s, spe

cia

l ite

ms, e

xtr

ao

rdin

ary

ite

ms a

nd

tra

nsfe

rs1

5,4

89

,49

5.

25

1.

15

,48

9,7

46

.

C

ha

nge

in N

et P

ositio

n9

2,3

88

.

67

,66

1.

16

0,0

49

.

Ne

t P

ositio

n—

be

gin

nin

g9

,43

9,4

60

.

25

3,5

68

.

9,6

93

,02

8.

Ne

t P

ositio

n—

end

ing

9,5

31

,84

8.

$

32

1,2

29

.$

9,8

53

,07

7.

$

UP

PE

R D

EE

RF

IEL

D T

OW

NS

HIP

SC

HO

OL

DIS

TR

ICT

ST

AT

EM

EN

T O

F A

CT

IVIT

IES

FO

R T

HE

YE

AR

EN

DE

D J

UN

E 3

0, 2

01

6

Pro

gra

m R

eve

nue

s

See

Acc

om

pan

yin

g N

ote

s to

the

Bas

ic F

inan

cial

Sta

tem

ents

5

FUND FINANCIAL STATEMENTS

GOVERNMENTAL FUNDS

EXHIBIT B-1

Special Capital Debt Total

General Revenue Projects Service Permanent Governmental

Fund Fund Fund Fund Fund Funds

Assets:

Cash and cash equivalents 2,280,032.$ 0.$ 24,349.$ 1.$ 0.$ 2,304,382.$

Due from other funds 111,173. 0. 0. 670. 0. 111,843.

Receivables from other governments 42,579. 73,126. 88,086. 0. 0. 203,791.

Total assets 2,433,784.$ 73,126.$ 112,435.$ 671.$ 0.$ 2,620,016.$

Liabilities and Fund Balances:

Liabilities:

Accounts payable 79,191.$ 0.$ 0.$ 0.$ 0.$ 79,191.$

Interfund payable 0. 22,149. 86,443. 0. 0. 108,592.

Unearned revenue 0. 73,237. 0. 0. 0. 73,237.

Total liabilities 79,191. 95,386. 86,443. 0. 0. 261,020.

Fund Balances:

Restricted for:

Excess surplus-current year 760,937. 0. 0. 0. 0. 760,937.

Excess surplus -- designated for

Subsequent year's expenditures 578,289. 0. 0. 0. 0. 578,289.

Maintenance reserve 715,963. 0. 0. 0. 0. 715,963.

Capital reserve 609,007. 0. 0. 0. 609,007.

Committed to:

Other purposes 16,298. 0. 0. 0. 0. 16,298.

Assigned to:

Designated by BOE for

subsequent year's expenditures 8,906. 0. 0. 633. 0. 9,539.

Capital projects 0. 0. 25,992. 0. 0. 25,992.

Unassigned:

General fund (334,807.) 0. 0. 0. 0. (334,807.)

Special revenue fund 0. (22,260.) 0. 37. 0. (22,223.)

Total Fund balances 2,354,593. (22,260.) 25,992. 670. 0. 2,358,995.

Total liabilities and fund balances 2,433,784.$ 73,126.$ 112,435.$ 670.$ 0.$

Amounts reported for governmental activities in the statement of

net assets (A-1) are different because:

Capital assets used in governmental activities are not financial

resources and therefore are not reported in the funds. The cost

of the assets is $ 23,155,154. and the accumulated depreciation

is $ 8,440,056. (See Note 6). 14,715,098.$

Long-term liabilities, including bonds payable, are not due and

payable in the current period and therefore are not reported as

liabilities in the funds (see Note 8). (2,830,177.)

Internal service net assets (155,389.)

Pension related items in governmental funds:

Deferred outflows of resources 1,517,700.

Deferred inflows of resources (215,469.)

Pension account payable (216,962.)

Net pension liability (5,641,948.)

Total pension related items in governmental funds (4,556,679.)

Net assets of governmental activities 9,531,848.$

UPPER DEERFIELD TOWNSHIP SCHOOL DISTRICT

BALANCE SHEET

GOVERNMENTAL FUNDS

June 30, 2016

6

EXHIBIT B-2

Special Capital Debt Total

General Revenue Projects Service Permanent Governmental

Fund Fund Fund Fund Fund Funds

REVENUES:

Local sources:

Local tax levy 6,644,248.$ 0.$ 0.$ 517,952.$ 0.$ 7,162,200.$

Tuition charges 79,206. 0. 0. 0. 0. 79,206.

Interest Earned 4,738. 0. 37. 0. 0. 4,775.

Miscellaneous 74,488. 0. 0. 0. 0. 74,488.

Total - Local Sources 6,802,680. 0. 37. 517,952. 0. 7,320,669.

State sources 7,738,445. 225,568. 59,786. 0. 0. 8,023,799.

Federal sources 60,909. 1,094,103. 0. 0. 1,155,012.

Total revenues 14,602,034. 1,319,671. 59,823. 517,952. 0. 16,499,480.

EXPENDITURES:

Current:

Regular instruction 3,911,579. 0. 0. 0. 0. 3,911,579.

Special education instruction 1,061,740. 1,236,196. 0. 0. 0. 2,297,936.

Other special instruction 174,065. 0. 0. 0. 0. 174,065.

Support services:

Tuition 203,949. 0. 0. 0. 0. 203,949.

Student & instruction related services 1,427,039. 131,055. 0. 0. 0. 1,558,094.

School administrative services 445,317. 0. 0. 0. 0. 445,317.

Other administrative services 253,864. 0. 0. 0. 0. 253,864.

Central services 250,054. 0. 0. 0. 0. 250,054.

Admin info tech 113,720. 0. 0. 0. 0. 113,720.

Plant operations and maintenance 1,457,718. 0. 0. 0. 0. 1,457,718.

Pupil transportation 775,624. 0. 0. 0. 0. 775,624.

Employee benefits 3,743,912. 249,928. 0. 0. 0. 3,993,840.

Debt service:

Principal 0. 0. 0. 410,000. 0. 410,000.

Interest and other charges 0. 0. 0. 108,976. 0. 108,976.

Capital outlay 326,682. 0. 119,497. 0. 0. 446,179.

Transfer to charter schools schools 20,549. 0. 0. 0. 0. 20,549.

Total expenditures 14,165,812. 1,617,179. 119,497. 518,976. 0. 16,421,464.

Excess (deficiency) of revenues over exp. 436,222. (297,508.) (59,674.) (1,024.) 0. 78,016.

OTHER FINANCING SOURCES (USES):

Transfers in 0. 300,476. 0. 37. 0. 300,513.

Transfers out (300,476.) 0. (37.) 0. 0. (300,513.)

Total other financing sources and uses (300,476.) 300,476. (37.) 37. 0. 0.

Net change in fund balance 135,746. 2,968. (59,711.) (987.) 0. 78,016.

Fund balance—July 1 2,218,847. (25,228.) 85,703. 1,657. 0. 2,280,979.

Fund balance—June 30 2,354,593.$ (22,260.)$ 25,992.$ 670.$ 0.$ 2,358,995.$

UPPER DEERFIELD TOWNSHIP SCHOOL DISTRICT

STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES

GOVERNMENTAL FUNDS

FOR THE YEAR ENDED JUNE 30, 2016

See Accompanying Notes to the Financial Statements

7

EXHIBIT B-3

UPPER DEERFIELD TOWNSHIP SCHOOL DISTRICT

RECONCILATION OF THE STATEMENT OF REVENUES, EXPENDITURES,

AND CHANGES IN FUND BALANCES OF GOVERNMENTAL FUNDS

TO THE STATEMENT OF ACTIVITIES

FOR THE YEAR ENDED JUNE 30, 2016

Total net changes in fund balances - governmental funds (from B-2) 78,016.$

Amounts reported for governmental activities in the statement of activities (A-2)

are different because:

Capital outlays are reported in governmental funds as expenditures. However, in the statement of

activities, the cost of those assets is allocated over their estimated useful lives as depreciation

expense.

This is the amount by which capital outlays exceeded depreciation in the period.

Depreciation expense (564,807.)

Capital outlays 341,561. (223,246.)

Adjustment to fixed assets

Repayment of bond principal is an expenditure in the governmental funds, but the repayment reduces

long-term liabilities in the statement of net assets and is not reported in the statement of activities.

Principal paid on bonds 410,000.

Principal paid on lease purchase 0. 410,000.

Decrease in accrued interest 6,696.

Proceeds from debt issues are a financing source in the governmental funds. They are not revenue

in the statement of activities; issuing debt increases long-term liabilities in the statement of net assets.

Proceeds of long-term debt 0.

Capital lease proceeds 0. 0.

In the statement of activities, certain operating expenses, e.g., compensated absences (vacations) are

measured by the amounts earned during the year. In the governmental funds, however, expenditures

for these items are reported in the amount of financial resources used (paid). When the earned amount

exceeds the paid amount, the difference is reduction in the reconciliation (-); when the paid amount

exceeds the earned amount the difference is an addition to the reconciliation (+). (6,111.)

Increase in pension expense (2,072,786.)

Increase in on-behalf pension payments 1,900,664.

Increase/(decrease) in internal service fund (845.)

Change in net position of governmental activities 92,388.$

See Accompanying Notes to the Financial Statements

8

PROPRIETARY FUNDS

EXHIBIT B-4

Governmental

Activities

Food Community Education Internal

Service and Recreation Fund Total Service Funds

ASSETS:

Current Assets:

Cash and cash equivalents 110,754.$ 102,078.$ 212,832.$ 177,780.$

Accounts receivable:

State 165. 0. 165. 0.

Federal 11,590. 0. 11,590. 0.

Other 33,124. 11. 33,135. 30,165.

Inventories 10,861. 0. 10,861. 0.

Total current assets 166,494. 102,089. 268,583. 207,945.

Noncurrent assets:

Furniture, machinery & equipment 219,216. 2,810. 222,026. 2,572.

Less accumulated depreciation (138,451.) (2,810.) (141,261.) (2,572.)

Total noncurrent assets 80,765. 0. 80,765. 0.

Total assets 247,259.$ 102,089.$ 349,348.$ 207,945.$

DEFERRED OUTFLOW OF RESOURCES: 0.$ 0.$ 0.$ 54,872.$

LIABILITIES:

Current Liabilities:

Accounts payable 25,553.$ 0.$ 25,553.$ 198,794.$

Interfund payable 2,566. 0. 2,566. 685.

Pension account payable 0. 0. 0. 7,799.

Total current liabilities 28,119.$ 0.$ 28,119.$ 207,278.$

Noncurrent liabilities:

Net pension liability 0. 0. 0. 203,245.

Total liabilities 28,119.$ 0.$ 28,119.$ 410,523.$

DEFERRED INFLOW OF RESOURCES: 0.$ 0.$ 0.$ 7,683.$

NET ASSETS:

Invested in capital assets net of

related debt 80,765. 0. 80,765. 0.

Unrestricted 138,375. 102,089. 240,464. (155,389.)

Total net assets 219,140.$ 102,089.$ 321,229.$ (155,389.)$

See Accompanying Notes to the Basic Financial Statements

UPPER DEERFIELD TOWNSHIP SCHOOL DISTRICT

STATEMENT OF NET POSITION

PROPRIETARY FUND

JUNE 30, 2016

Business-Type Activities

Enterprise Fund

9

EXHIBIT B-5

Governmental

Activities -

Food Service Community Education Internal

Fund and Recreation Fund Total Service Fund

Operating revenues:

Changes for services:

Daily sales-reimbursable programs 70,596.$ 0.$ 70,596.$ 0.$

Daily sales-nonreimbursable pgms 40,557. 0. 40,557. 0.

Child care fees 0. 97,390. 97,390. 0.

Miscellaneous Income 76. 0. 76. 0.

Charges for services 115,049. 0. 115,049. 2,092,878.

Total operating revenues 226,278. 97,390. 323,668. 2,092,878.

Operating expenses

Cost of sales - reimbursable 181,366. 0. 181,366. 0.

Cost of sales - nonreimbursable 50,402. 0. 50,402. 0.

Salaries 188,726. 52,062. 240,788. 69,973.

Payroll taxes and fringe benefits 32,984. 3,983. 36,967. 22,733.

Pension expense 0. 0. 0. 6,242.

Supplies 21,099. 8,233. 29,332. 0.

Insurance 7,270. 0. 7,270. 0.

Office expense 1,247. 250. 1,497. 2,255.

Management fees 48,000. 0. 48,000. 0.

Depreciation 12,013. 0. 12,013. 0.

Miscellaneous 8,761. 0. 8,761. 4,789.

Repair and maintenance 9,077. 0. 9,077. 0.

Transportation costs 0. 0. 0. 1,987,947.

Total operating expenses 560,945. 64,528. 625,473. 2,093,939.

Operating income/(loss) (334,667.) 32,862. (301,805.) (1,061.)

Nonoperating revenues (expenses):

State sources:

State school lunch program 5,263. 0. 5,263. 0.

Federal sources:

National school breakfast program 82,065. 0. 82,065. 0.

National school lunch program 241,503. 0. 241,503. 0.

Food distribution program 40,384. 0. 40,384. 0.

Interest revenue 115. 136. 251. 216.

Total nonoperation revenues (expenses) 369,330. 136. 369,466. 216.

Change in net position 34,663. 32,998. 67,661. (845.)

Net position - beginning 184,477. 69,091. 253,568. (154,544.)

Net position - ending 219,140.$ 102,089.$ 321,229.$ (155,389.)$

See Accompanying Notes to the Basic Financial Statements

UPPER DEERFIELD TOWNSHIP SCHOOL DISTRICT

STATEMENT OF REVENUES, EXPENSES, AND CHANGES IN FUND NET POSITION

PROPRIETARY FUND

JUNE 30, 2016

Business-Type Activities

Enterprise Fund

10

EXHIBIT B-6

Governmental

Activities -

Food Service Community Education Internal

Fund and Recreation Fund Total Service Fund

CASH FLOWS FROM OPERATING ACT.

Receipts from customers 111,221.$ 97,379.$ 208,600.$ 2,092,681.$

Payments to employees 0. (56,045.) (56,045.) (69,973.)

Payment for employee benefits 0. 0. 0. (22,732.)

Payments to suppliers (510,168.) (8,483.) (518,651.) (1,995,908.)

Other receipts/(payments) 112,323. 0. 112,323. 0.

Net cash provided by (used for) operating activities (286,624.) 32,851. (253,773.) 4,068.

CASH FLOWS FROM NONCAPITAL FINANCING ACT.

State Sources 5,286. 0. 5,286. 0.

Federal Sources 326,577. 0. 326,577. 0.

Net cash provided by (used for) non-

capital financing activities 331,863. 0. 331,863. 0.

CASH FLOWS FROM FINANCING ACTIVITIES:

Purchase of equipment (3,843.) 0. (3,843.) 0.

Interest of investments 115. 136. 251. 216.

Net cash provided by investing activites (3,728.) 136. (3,592.) 216.

Net increase (decrease) in cash and cash equilvalents 41,511. 32,987. 74,498. 4,284.

Balances - beginning of year 69,243. 69,091. 138,334. 173,496.

Balances - end of year 110,754.$ 102,078.$ 212,832.$ 177,780.$

Reconciliation of operating income (loss)

to net cash provided (used) by operating

activities:

Operating income (loss) (334,667)$ 32,862.$ (301,805.)$ (1,061)$

Adjust to reconcile operating income

(loss) to net cash provided by (used for)

operating activities

Depreciation and net amortization 12,013. 0. 12,013. 0.

Federal commodities 40,384. 0. 40,384. 0.

(Increase)/decrease in accts receivables, net (2,801.) (11.) (2,812.) (197.)

(Increase)/decrease in inventories 2,956. 0. 2,956. 0.

Increase/(decrease) in accounts payable (4,577.) 0. (4,577.) (916.)

Increase/(decrease) in pension accounts payable 0. 0. 0. 31.

Increase/(decrease) in interfund payable 68. 0. 68. 0.

(Increase)/decrease in deferred inflow 0. 0. 0. (35,437.)

Increase/(decrease) in deferred outflow 0. 0. 0. (7,021.)

Increase/(decrease) in net pension liability 0. 0. 0. 48,669.

Total adjustments 48,043. (11.) 48,032. 5,129.

Net cash provided by (used for) oper activities (286,624)$ 32,851.$ (253,773)$ 4,068.$

See Accompanying Notes to the Basic Financial Statements

UPPER DEERFIELD TOWNSHIP SCHOOL DISTRICT

STATEMENT OF CASH FLOWS

PROPRIETARY FUND

FOR YEAR ENDED JUNE 30, 2016

Business-Type Activities

Enterprise Funds

11

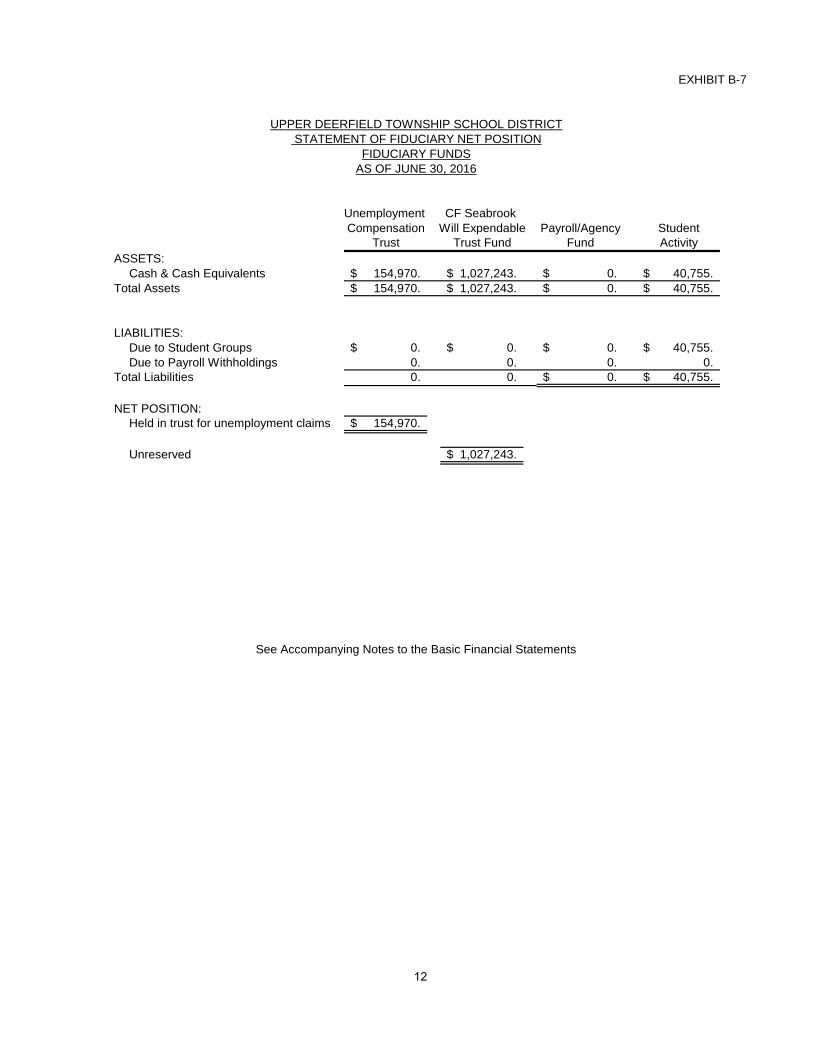

FIDUCIARY FUNDS

EXHIBIT B-7

Unemployment CF Seabrook

Compensation Will Expendable Payroll/Agency Student

Trust Trust Fund Fund Activity

ASSETS:

Cash & Cash Equivalents 154,970.$ 1,027,243.$ 0.$ 40,755.$

Total Assets 154,970.$ 1,027,243.$ 0.$ 40,755.$

LIABILITIES:

Due to Student Groups 0.$ 0.$ 0.$ 40,755.$

Due to Payroll Withholdings 0. 0. 0. 0.

Total Liabilities 0. 0. 0.$ 40,755.$

NET POSITION:

Held in trust for unemployment claims 154,970.$

Unreserved 1,027,243.$

UPPER DEERFIELD TOWNSHIP SCHOOL DISTRICT

STATEMENT OF FIDUCIARY NET POSITION

AS OF JUNE 30, 2016

See Accompanying Notes to the Basic Financial Statements

FIDUCIARY FUNDS

12

EXHIBIT B-8

Unemployment CF Seabrook

Compensation Will Expendable

ADDITIONS:

Contributions:

Plan Member 25,766.$ 0.$

Other 0. 88,581.

Total Contributions 25,766. 88,581.

Interest 218. 1,501.

Net Investment Earnings 218. 1,501.

DEDUCTIONS:

Unemployment Claims 1,480. 0.

Other Expenses 10,309. 111,200.

Total Deductions 11,789. 111,200.

Change in Net Position 14,195. (21,118.)

NET POSITION, JULY 1 140,775. 1,048,361.

NET POSITION, JUNE 30 154,970.$ 1,027,243.$

UPPER DEERFIELD TOWNSHIP SCHOOL DISTRICT

See Accompanying Notes to the Basic Financial Statements

FOR FISCAL YEAR ENDED JUNE 30, 2016

FIDUCIARY FUND

COMBINING STATEMENT OF CHANGES IN FIDUCIARY NET POSITION

13

NOTES TO FINANCIAL STATEMENTS

UPPER DEERFIELD TOWNSHIP SCHOOL DISTRICT

NOTES TO BASIC FINANCIAL STATEMENTS

FOR FISCAL YEAR ENDED JUNE 30, 2016

NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES