Rabo Securities1

Sintercafé 2017

Jim Watson – Senior Beverages Analyst

Coffee Consolidation Accelerates

2 Rabo Securities

Rabobank: The World’s Leading F&A Bank

Note 1: Ranking as per Global Finance 2015

EUR

426bnoutstanding capital with

EUR 98bncommitted to the F&A sector

Active in all segments in the Netherlands with a F&A focus worldwide

Located in

43countries

ranked amongst the

Top 25safest banks globally

(1)

3 Rabo Securities

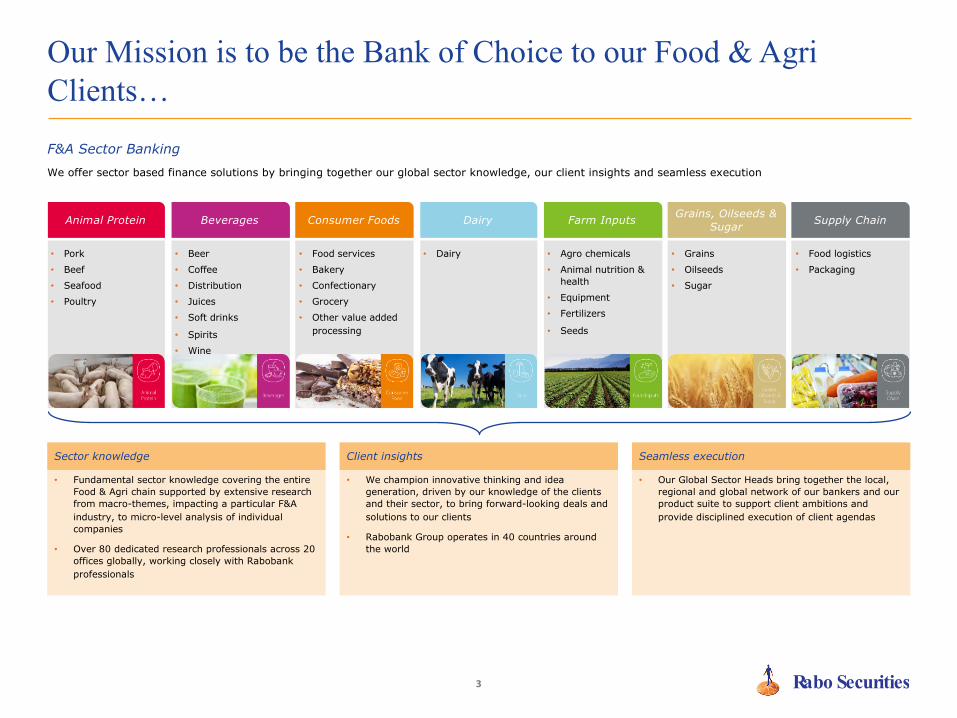

Our Mission is to be the Bank of Choice to our Food & AgriClients…

F&A Sector Banking

We offer sector based finance solutions by bringing together our global sector knowledge, our client insights and seamless execution

Sector knowledge

• Fundamental sector knowledge covering the entire Food & Agri chain supported by extensive research from macro-themes, impacting a particular F&A industry, to micro-level analysis of individual companies

• Over 80 dedicated research professionals across 20 offices globally, working closely with Rabobank professionals

Client insights

• We champion innovative thinking and idea generation, driven by our knowledge of the clients and their sector, to bring forward-looking deals and solutions to our clients

• Rabobank Group operates in 40 countries around the world

Seamless execution

• Our Global Sector Heads bring together the local, regional and global network of our bankers and our product suite to support client ambitions and provide disciplined execution of client agendas

• Pork

• Beef

• Seafood

• Poultry

• Food services

• Bakery

• Confectionary

• Grocery

• Other value added processing

• Dairy • Agro chemicals

• Animal nutrition & health

• Equipment

• Fertilizers

• Seeds

• Grains

• Oilseeds

• Sugar

• Food logistics

• Packaging

Animal Protein Consumer Foods Farm InputsDairy Supply ChainGrains, Oilseeds & Sugar

• Beer

• Coffee

• Distribution

• Juices

• Soft drinks

• Spirits

• Wine

Beverages

4 Rabo Securities

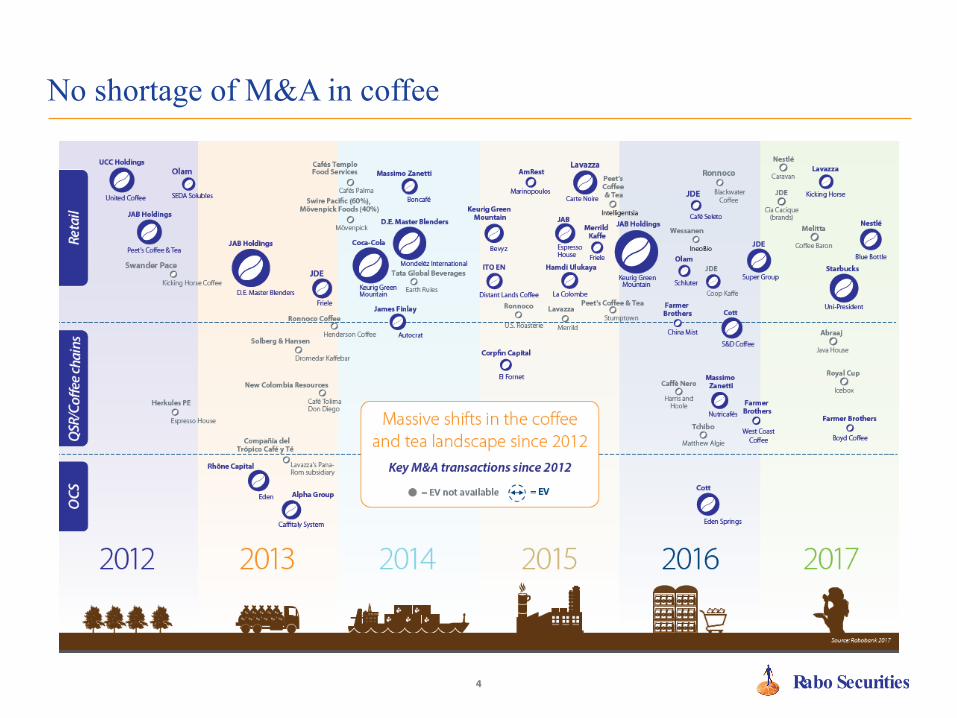

No shortage of M&A in coffee

5 Rabo Securities

Themes from the ABI model that will impact coffee

A path of aggressive M&A can take a regional company to global sector leadership very quickly

This kind of aggressive M&A is contagious

Increased financial pressure on suppliers will drive a separate wave of consolidation upstream

Best practices of the ABI/3G model spread rapidly

Local platforms become a base for distribution of select regional/global premium brands.

6 Rabo Securities

A three-headed acquisition monster

AB-InBev JAB HoldingsKraft Heinz

7 Rabo Securities

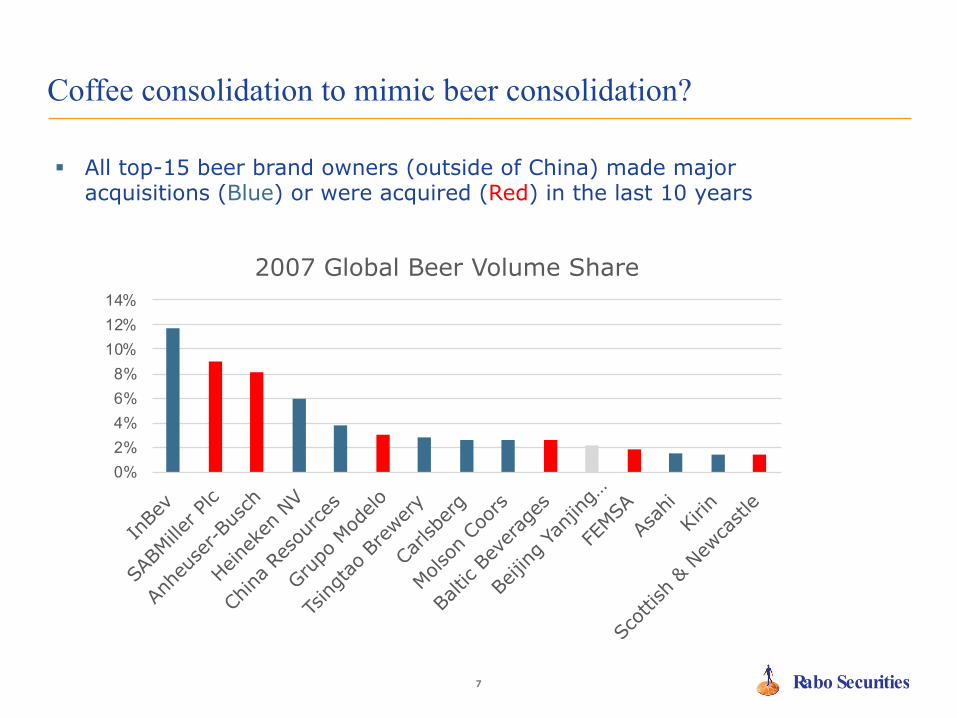

Coffee consolidation to mimic beer consolidation?

0%2%4%6%8%10%12%14%

2007 Global Beer Volume Share

§ All top-15 beer brand owners (outside of China) made major acquisitions (Blue) or were acquired (Red) in the last 10 years

8 Rabo Securities

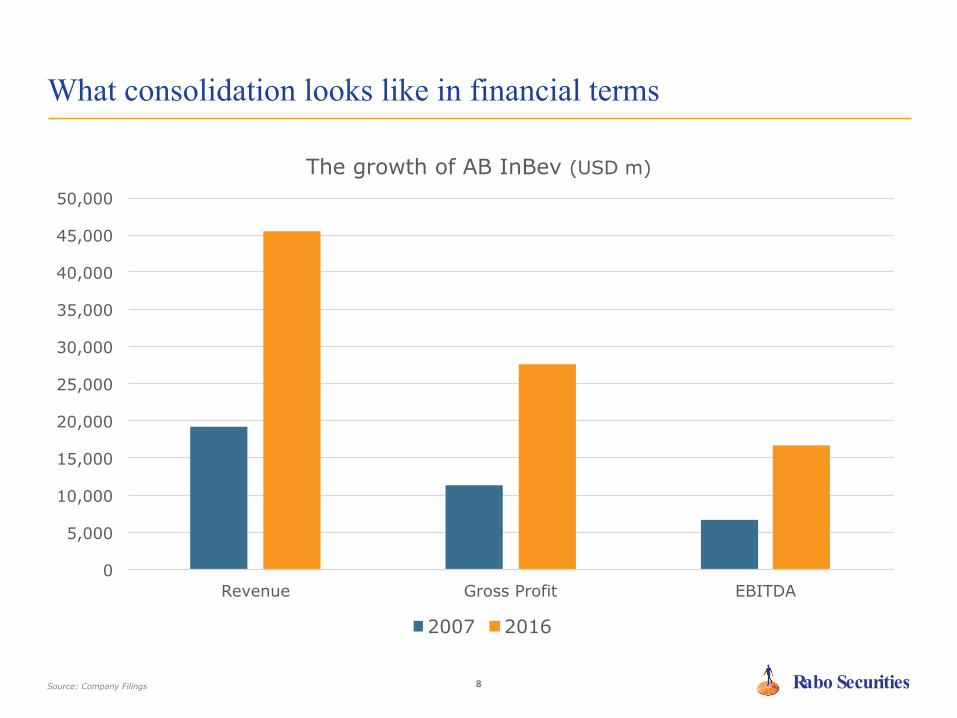

What consolidation looks like in financial terms

Source: Company Filings

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Revenue Gross Profit EBITDA

The growth of AB InBev (USD m)

2007 2016

9 Rabo Securities

Numerous coffee players between 1-3% share

Source: Euromonitor

0%

5%

10%

15%

20%

25%

Hot Coffee World Value Share

§ A “buy or be bought” environment is coming to coffee – and those with 1-3% retail share won’t be able to stay on the sidelines

10 Rabo Securities

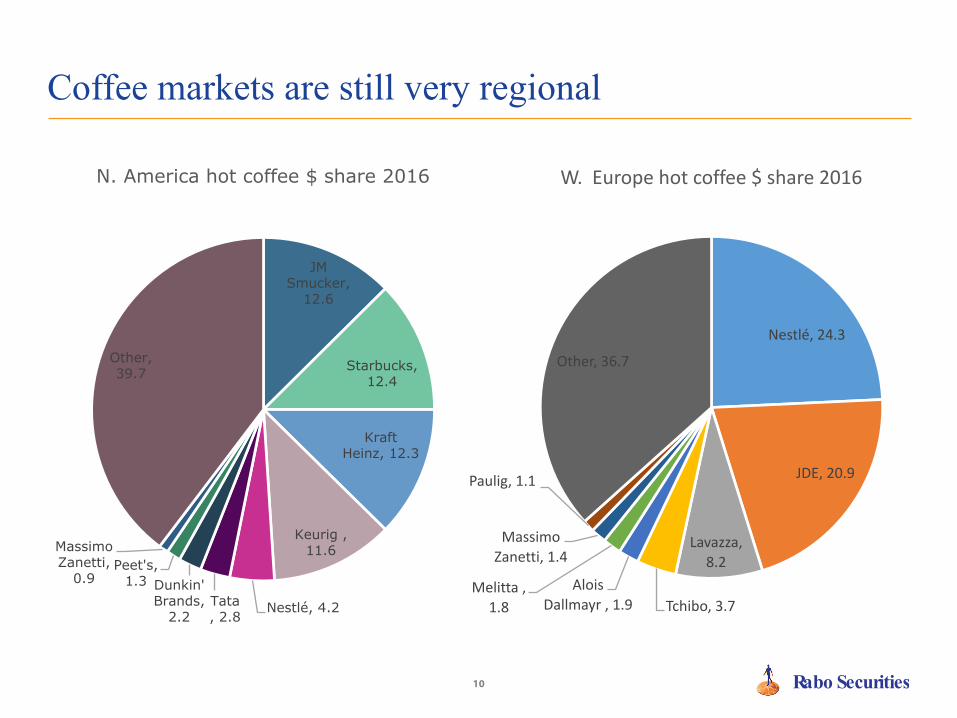

Coffee markets are still very regional

JM Smucker,

12.6

Starbucks, 12.4

Kraft Heinz, 12.3

Keurig , 11.6

Nestlé, 4.2Tata , 2.8

Dunkin' Brands,

2.2

Peet's, 1.3

Massimo Zanetti,

0.9

Other, 39.7

N. America hot coffee $ share 2016

Nestlé,24.3

JDE,20.9

Lavazza,8.2

Tchibo,3.7Alois

Dallmayr,1.9Melitta,

1.8

MassimoZanetti,1.4

Paulig,1.1

Other,36.7

W.Europehotcoffee$share2016

11 Rabo Securities

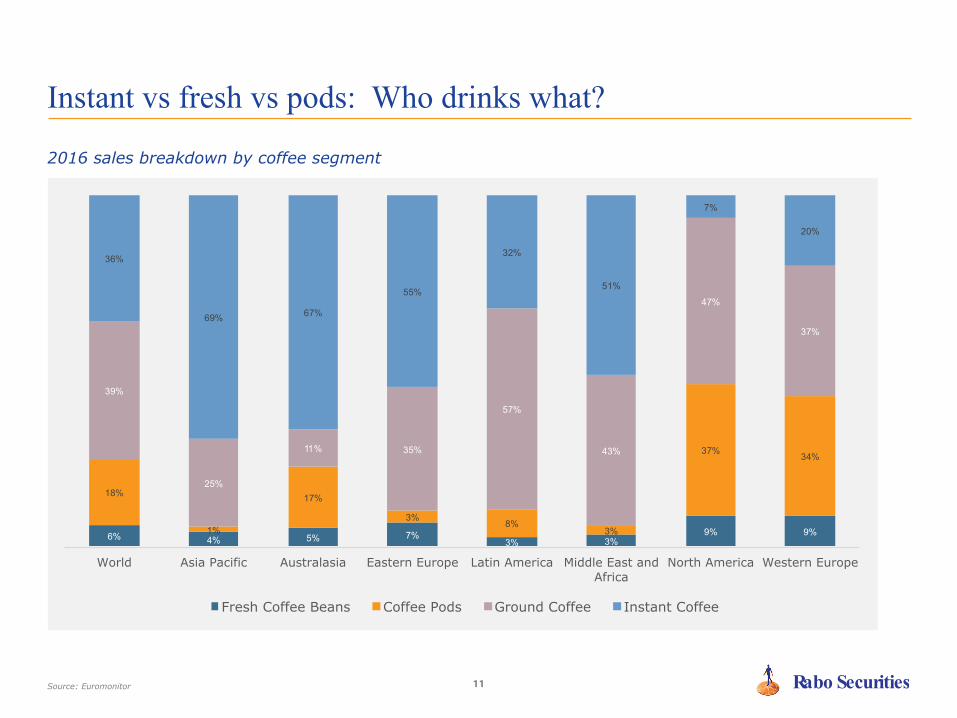

2016 sales breakdown by coffee segment

Instant vs fresh vs pods: Who drinks what?

Source: Euromonitor

6% 4% 5% 7%3% 3%

9% 9%

18%

1%

17%

3%8%

3%

37% 34%

39%

25%

11% 35%

57%

43%

47%

37%

36%

69% 67%

55%

32%

51%

7%

20%

World Asia Pacific Australasia Eastern Europe Latin America Middle East and Africa

North America Western Europe

Fresh Coffee Beans Coffee Pods Ground Coffee Instant Coffee

12 Rabo Securities

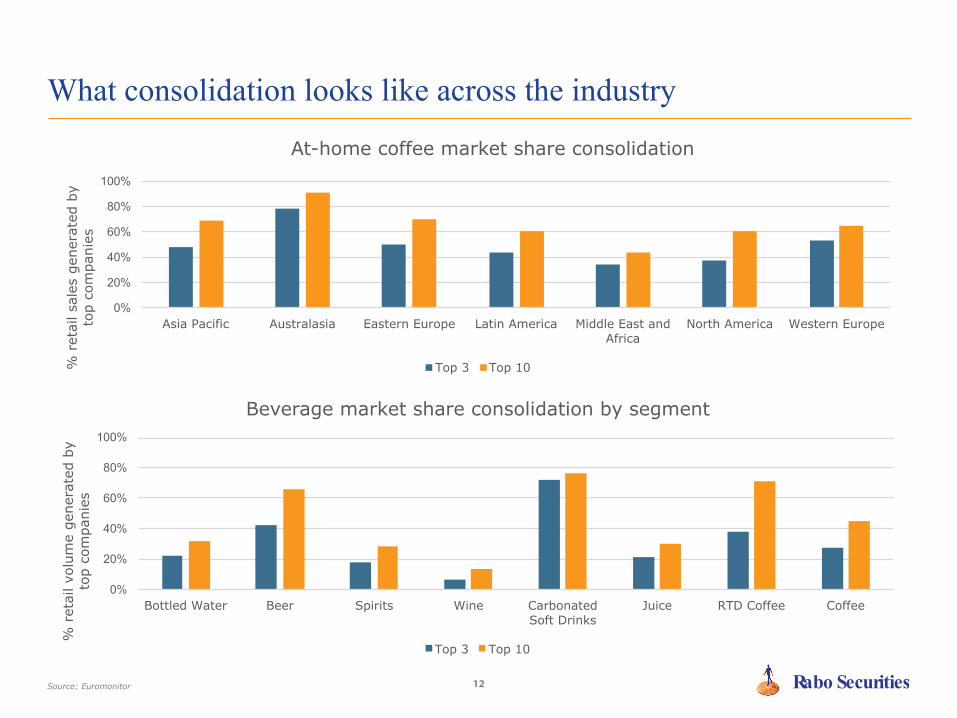

What consolidation looks like across the industry

Source: Euromonitor

0%

20%

40%

60%

80%

100%

Asia Pacific Australasia Eastern Europe Latin America Middle East and Africa

North America Western Europe

% r

etai

l sal

es g

ener

ated

by

top

com

pani

es

At-home coffee market share consolidation

Top 3 Top 10

0%

20%

40%

60%

80%

100%

Bottled Water Beer Spirits Wine Carbonated Soft Drinks

Juice RTD Coffee Coffee

% r

etai

l vol

ume

gene

rate

d by

to

p co

mpa

nies

Beverage market share consolidation by segment

Top 3 Top 10

13 Rabo Securities

Roasters will be under pressure to increase efficiency and scale

As third wave roasters take ownership of premium coffee, mainstream roasting becomes increasingly commoditized

Premium brands with the potential for regional/global expansion will become increasingly valued

“Kicking Horse Coffee represents one of the ‘local jewels’ the Lavazza Group continues to seek as part of its globalization and premium positioning strategy,” Antonio Baravalle, CEO of the Lavazza Group

We see pressure on trading houses to expand outward

M&A is clearer path (vs organic growth)

Only limited options to get closer to production

What 2017 deals show us across the supply chainSucafina takes minority stake in Brazil farm JV

Farmer Brothers grows with West Coast Coffee acquisition

Lavazza acquires 80% stake in Kicking Horse Coffee

14 Rabo Securities

Consumers will accept large scale third-party roasting

For consumers - the brand story matters more than production ownership

For brand owners - the flexibility, scale, QC of third-parties are the benefit

15 Rabo Securities

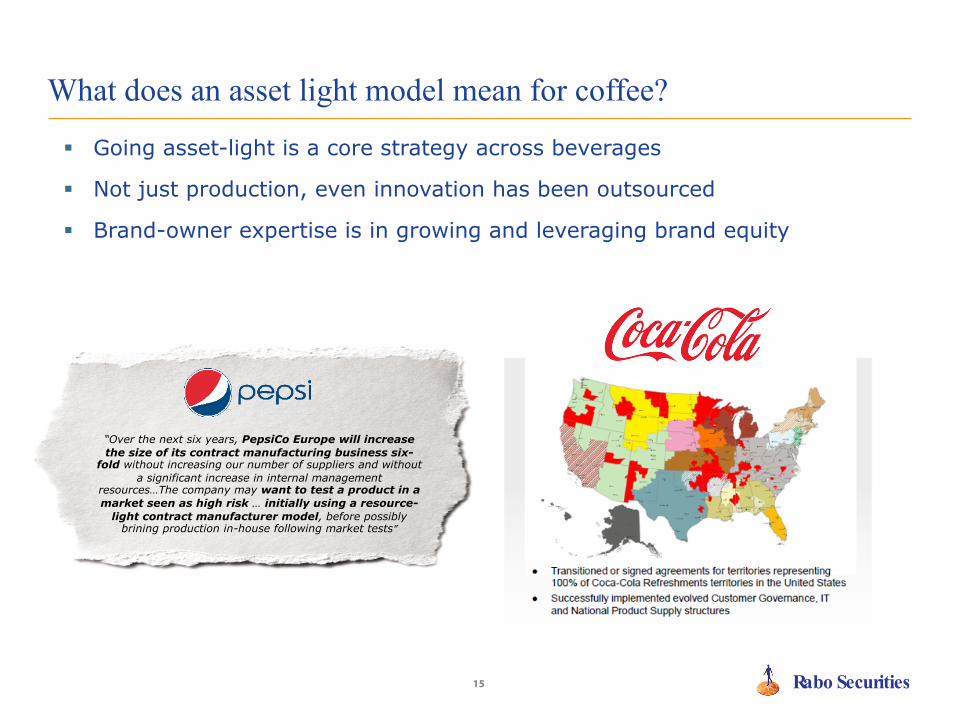

What does an asset light model mean for coffee?

“Over the next six years, PepsiCo Europe will increase the size of its contract manufacturing business six-

fold without increasing our number of suppliers and without a significant increase in internal management

resources…The company may want to test a product in a market seen as high risk … initially using a resource-

light contract manufacturer model, before possibly brining production in-house following market tests”

§ Going asset-light is a core strategy across beverages

§ Not just production, even innovation has been outsourced

§ Brand-owner expertise is in growing and leveraging brand equity

16 Rabo Securities

Global brands: Blue Bottle already has a bit of international presence with a few shops in Japan – but, like Kicking Horse, see themselves as a global brand eventually.

Build out a portfolio: Blue Bottle slots in very nicely with Nestle as a true ultra-premium brand to sit at the top of the portfolio.

RTD coffee is a young category: is so small relatively, that paying a big premium now will likely seem very reasonable if the category takes off. Buying a top player early in the game gives a lot of upside.

An e-commerce play?: Blue Bottle had previously bought Tonx(subscription coffee start-up) and Perfect Coffee (start-up focused on grinding and preserving coffee). Every beverage company (coffee through spirits) is trying to figure how to get an edge in online shipping. Or more accurately – they are all investing money to prevent missing the boat and getting left behind.

We didn’t forget about Nestle – Blue Bottle

The drivers behind the deal

17 Rabo Securities

The power of global brands (AB-InBev version)

18 Rabo Securities

Final thought: It takes two to tango

Source: Reuters, Bloomberg

Recommended