Classes 11-12Classes 11-12 Regulation policy

St-Petersburg State University Graduate School of Management

Master of International Business Program Business-government relations

Discussion questions

• Regulation of natural monopolies • Tax policy, tax classifications and

effects • Subsidies• Entry / Exit barriers • Regulatory burden and it’s economic

impact

Economic regulation of natural monopoly

Price regulation

Monopoly power

• Entrance barriers

• High price

• Low output

• Quality issues

Incentives:

• Rent-seeking behavior

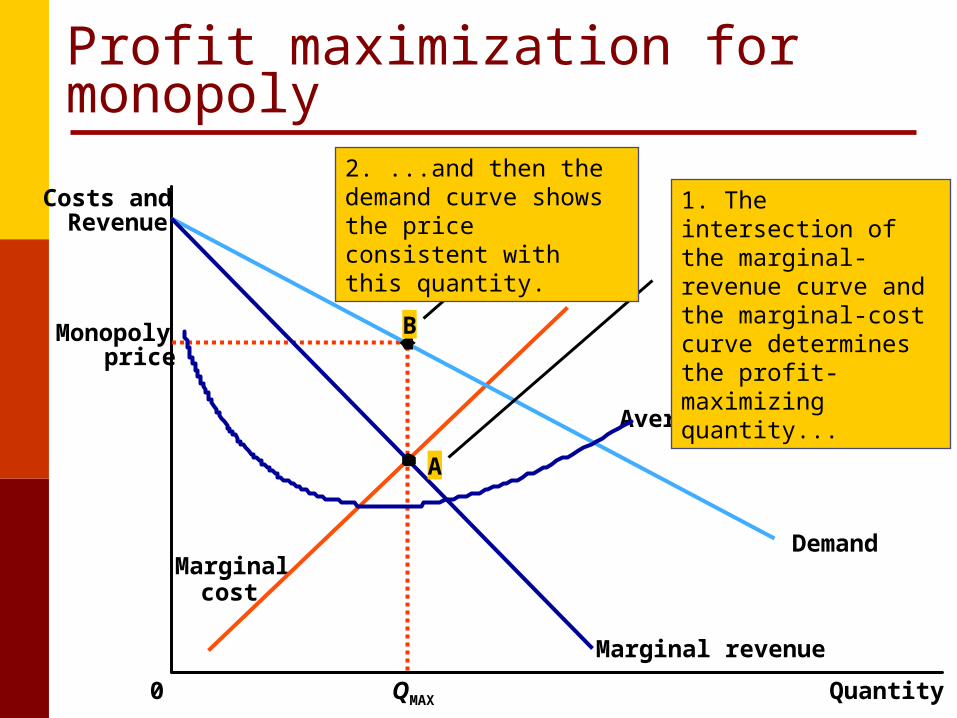

Profit maximization for monopoly

Monopolyprice

QuantityQMAX0

Costs andRevenue

Demand

Average total cost

Marginal revenue

Marginalcost

A

1. The intersection of the marginal-revenue curve and the marginal-cost curve determines the profit-maximizing quantity...

B

2. ...and then the demand curve shows the price consistent with this quantity.

Government’s role

Antitrust law F3 (or F4) Index (< 45%: low level of

concentration; 45 – 70%: high level of concentration; > 70%: very high level of concentration)

HHI (Herfindahl-Hirschman Index) Antimonopoly committees in structure of

the government and their activity

Natural monopoly

High fixed cost, low marginal cost High entrance barriers Growing economy on scale

• All volume of a product can be made with the least expenses by unique firm

Natural monopoly (examples)

Majority of activity kinds which production is «a subject of public using», - cable industry, communications, electric mains, oil-and gas mains, railway transportation, systems of water supply and water drain etc.

Monopoly power and its regulation

• Like a competitive firm, a monopoly maximizes profit by producing the quantity at which marginal cost and marginal revenue are equal

• Unlike a competitive firm, its price exceeds its marginal revenue, so its price exceeds marginal cost

• Government may regulate the prices that the monopoly charges. The allocation of resources will be efficient if

price is set to equal marginal cost.

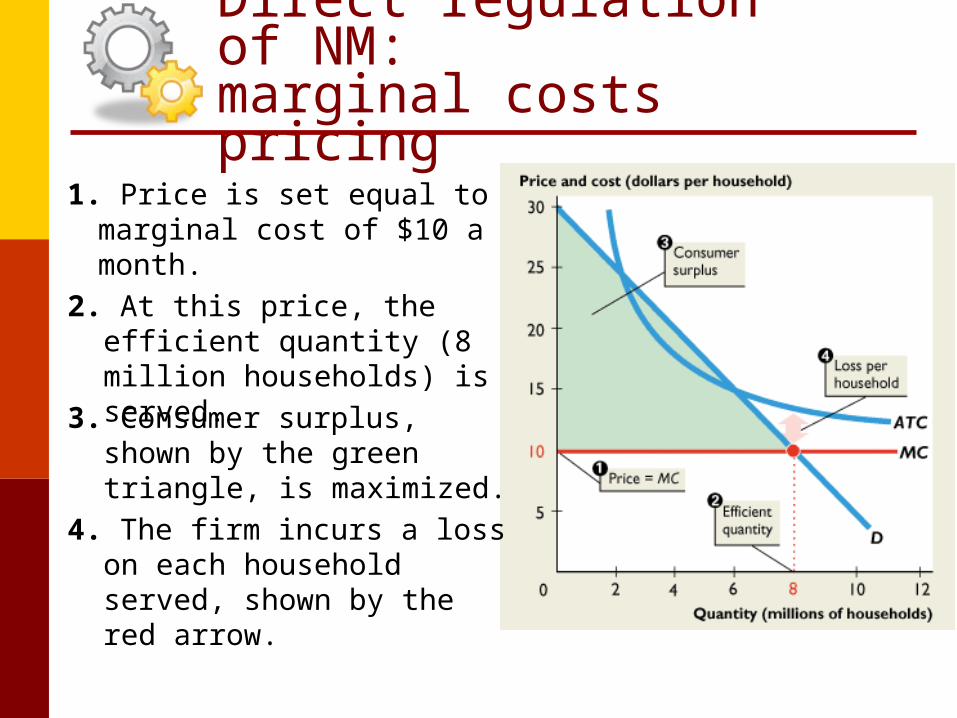

Direct regulation of NM:marginal costs pricing

2. At this price, the efficient quantity (8 million households) is served.

1. Price is set equal to marginal cost of $10 a month.

3. Consumer surplus, shown by the green triangle, is maximized.

4. The firm incurs a loss on each household served, shown by the red arrow.

Price discrimination

Price discrimination is the practice of selling the same good at different prices to different customers, even though the costs for producing for the two customers are the same.

• Price discrimination is not possible when a good is sold in a competitive market since there are many firms all selling at the market price. In order to price discriminate, the firm must have some market power.

Perfect price discrimination

Perfect price discrimination refers to the situation when the monopolist knows exactly the willingness to pay of each customer and can charge each customer a different price

Two important effects of price discrimination: It can increase the monopolist’s profits It can reduce deadweight loss

Examples of price discrimination

• Movie tickets

• Airline prices

• Discount coupons

• Financial aid

• Quantity discounts

Indirect regulation of NM:rate of return regulation

• Under rate of return regulation, a regulated firm must set its price at a level that enables it to earn a specified target percent return on its capital.• If the regulator could observe the firm’s true

costs and be sure that the firm was minimizing cost, this type of regulation would be like average cost pricing.

• But a firm might mislead the regulator and get close to maximum monopoly profit under this regulation.

Indirect regulation of NM:price cap regulation

A price cap regulation is a price ceiling—a rule that specifies the highest price the firm is permitted to charge.

A price cap regulation can be combined with earnings sharing regulation—a regulation that requires a firm to make refunds to customers if its profit rises above a target rate.

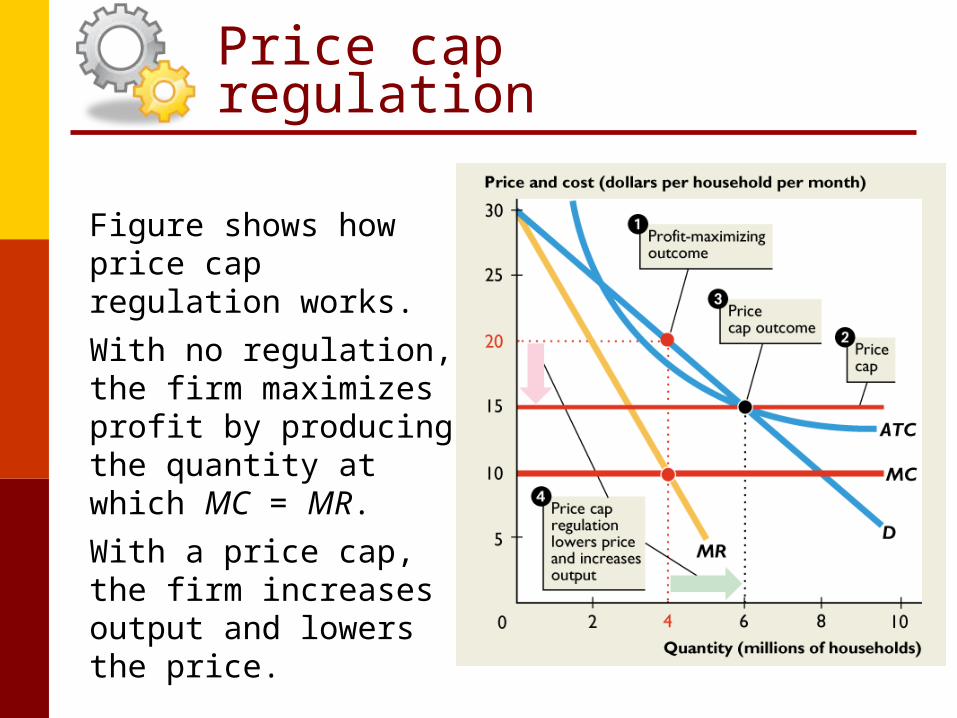

Price cap regulation

Figure shows how price cap regulation works.

With no regulation, the firm maximizes profit by producing the quantity at which MC = MR.

With a price cap, the firm increases output and lowers the price.

Why deregulation?

A. Transportation regulation failed to solve the problems it was supposed to address: industry unprofitability and service.

B. Communications-monopoly regulation resulted in blocking both customer choice and the spread of advanced technology.

C. Because it was based on cost reimbursement, Utility-monopoly regulation lacked full incentives for efficient (or, in some cases, adequate) supply

D. To the extent that the agenda of any kind of regulation was the elimination of price discrimination, the elimination of true price discrimination became impossible. Worse, in the name of “fairness,” regulators required cross-subsidization of some markets, which both discriminated in favor of high-cost or small-market customers and left the profitable markets open to entry—unless that, too, could be policed.

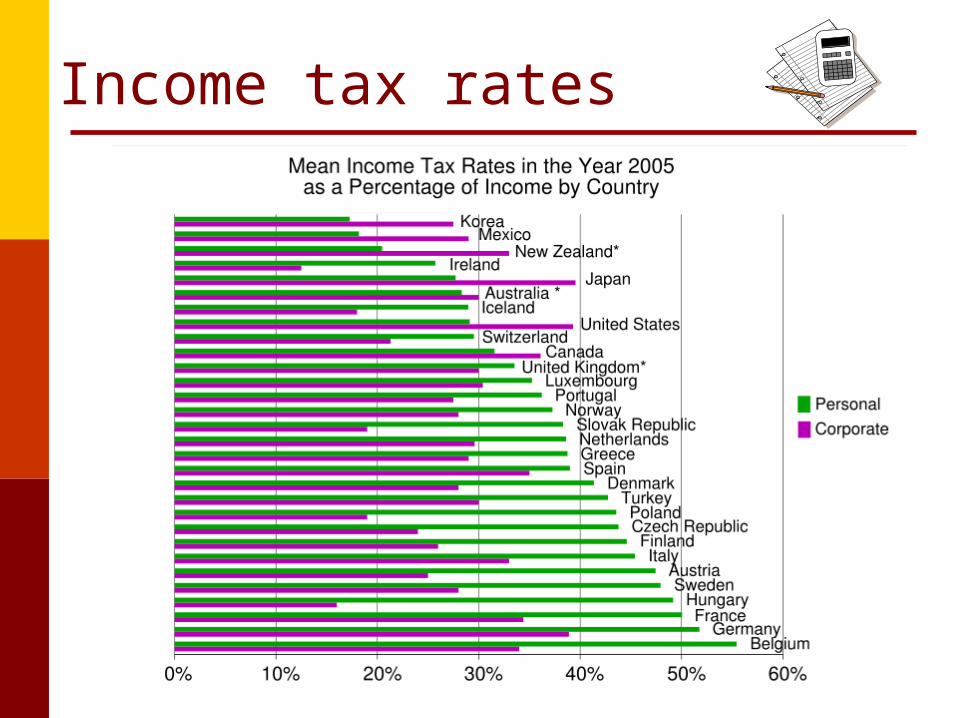

Tax policy

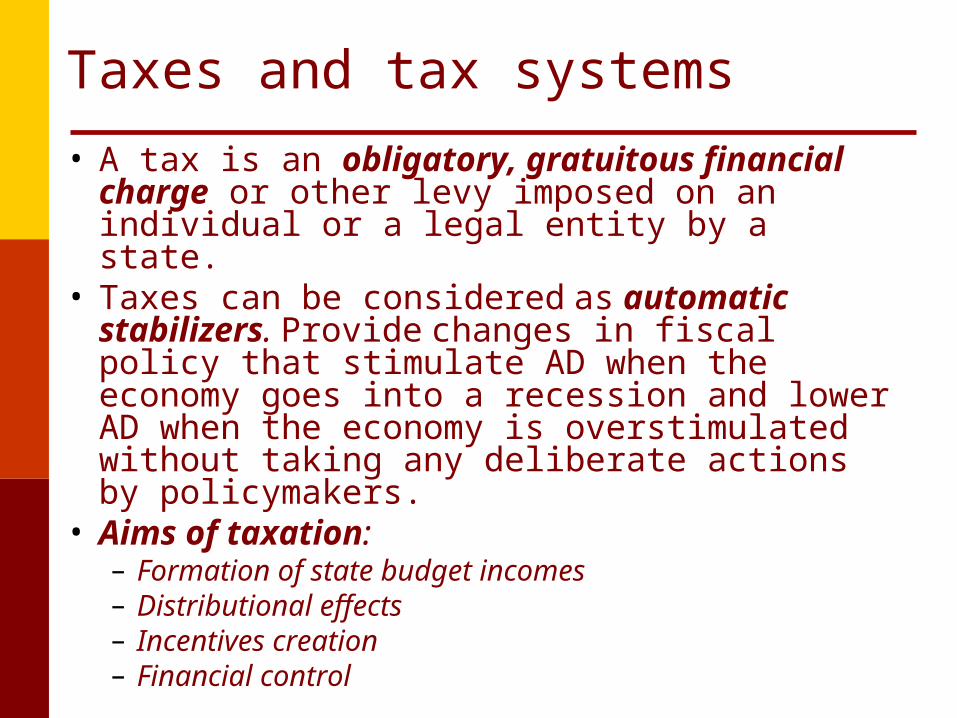

Taxes and tax systems

• A tax is an obligatory, gratuitous financial charge or other levy imposed on an individual or a legal entity by a state.

• Taxes can be considered as automatic stabilizers. Provide changes in fiscal policy that stimulate AD when the economy goes into a recession and lower AD when the economy is overstimulated without taking any deliberate actions by policymakers.

• Aims of taxation:– Formation of state budget incomes– Distributional effects– Incentives creation – Financial control

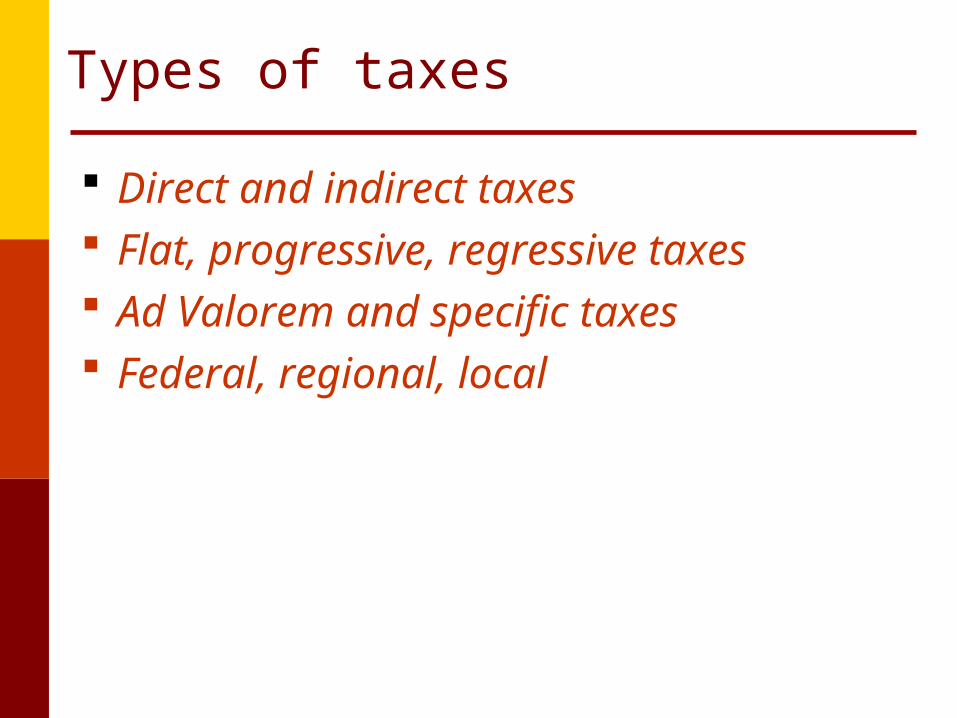

Types of taxes

Direct and indirect taxes Flat, progressive, regressive taxes Ad Valorem and specific taxes Federal, regional, local

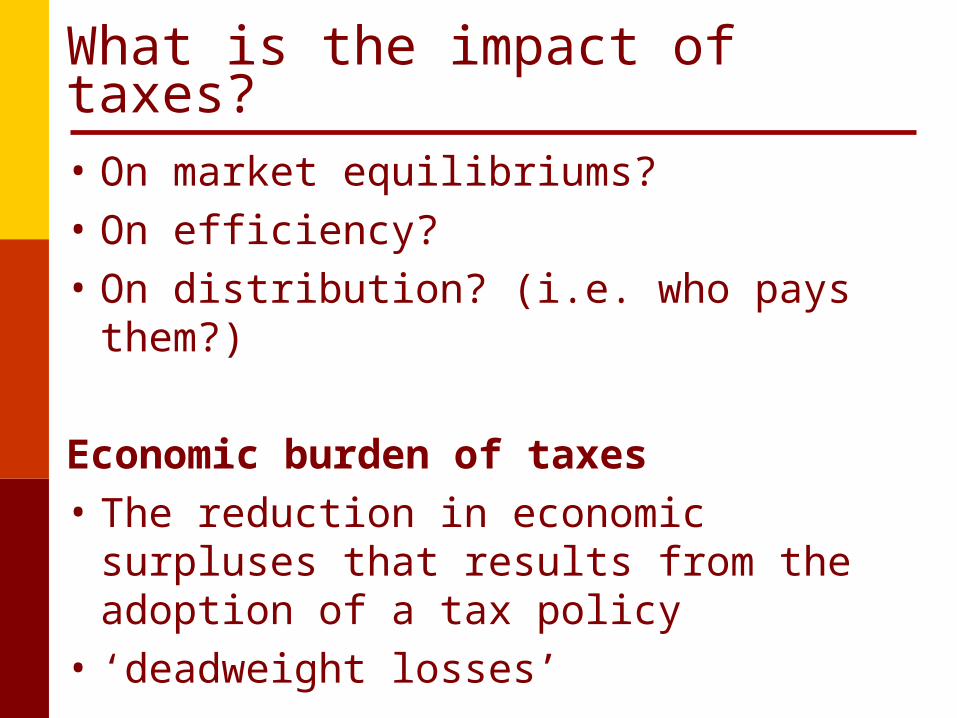

What is the impact of taxes?

• On market equilibriums?

• On efficiency?

• On distribution? (i.e. who pays them?)

Economic burden of taxes

• The reduction in economic surpluses that results from the adoption of a tax policy

• ‘deadweight losses’

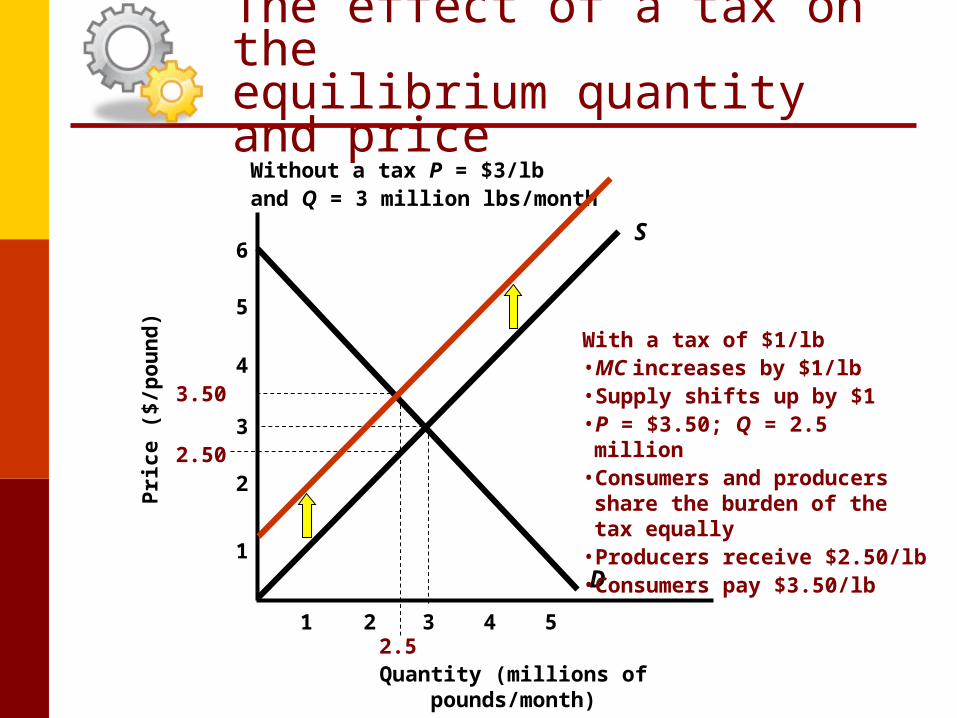

The effect of a tax on the equilibrium quantity and price

6

Quantity (millions of pounds/month)

Pri

ce (

$/p

ou

nd

)

1 2 3 4 5

5

4

2

1D

S

3

Without a tax P = $3/lband Q = 3 million lbs/month

2.50

3.50

S + tax

2.5

With a tax of $1/lb• MC increases by $1/lb• Supply shifts up by $1• P = $3.50; Q = 2.5 million• Consumers and producers share

the burden of the tax equally• Producers receive $2.50/lb• Consumers pay $3.50/lb

Tax burden and its allocation

• Elasticity– A measure of the extent to which quantity demanded

and quantity supplied respond to variations in price, income, and other factors.

• The less elastic the demand, the greater share of the tax paid by the consumer.– How effective are cigarette taxes at reducing

smoking?– How effective are cigarette taxes for earning

revenue?– What are the distributional implications of taxes on

necessities?

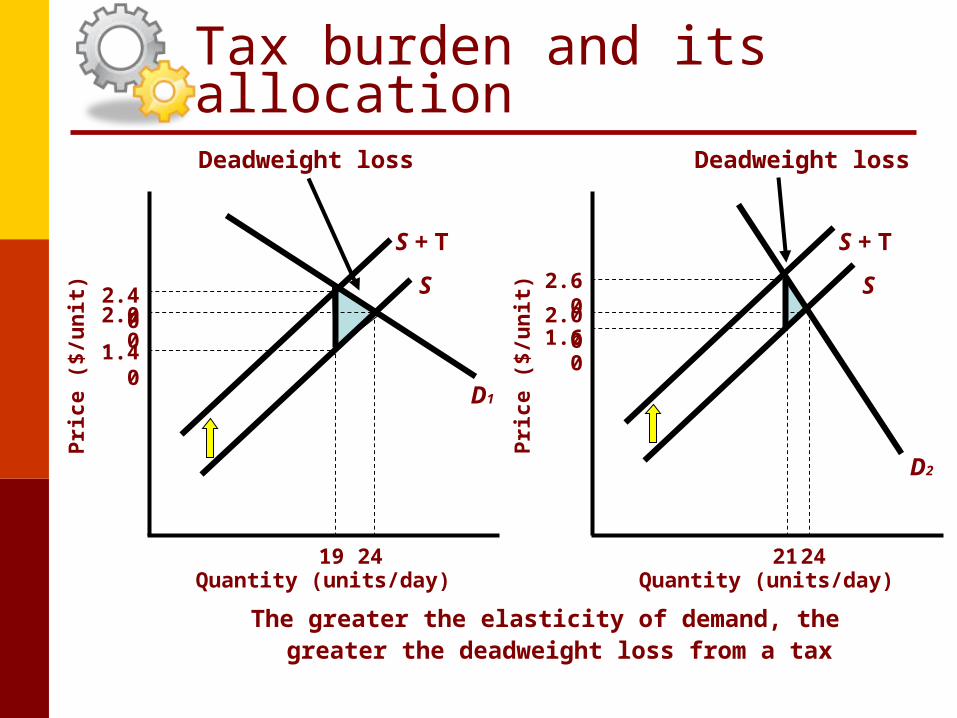

Tax burden and its allocation

Quantity (units/day)

Pri

ce (

$/u

nit

)

21

2.60

1.60

S + T

19

2.40

1.40

S + T

Deadweight loss Deadweight loss

Quantity (units/day)

Pri

ce (

$/u

nit

)

D1

S

24

2.00

D2

S

24

2.00

The greater the elasticity of demand, the greater the deadweight loss from a tax

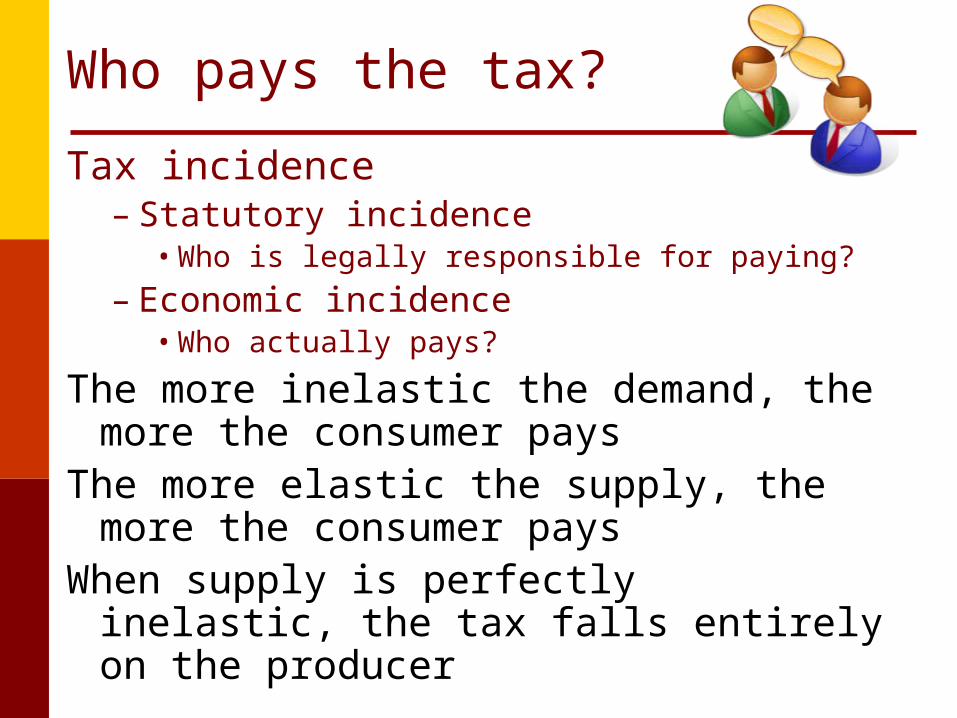

Who pays the tax?

Tax incidence– Statutory incidence

• Who is legally responsible for paying?

– Economic incidence• Who actually pays?

The more inelastic the demand, the more the consumer pays

The more elastic the supply, the more the consumer pays

When supply is perfectly inelastic, the tax falls entirely on the producer

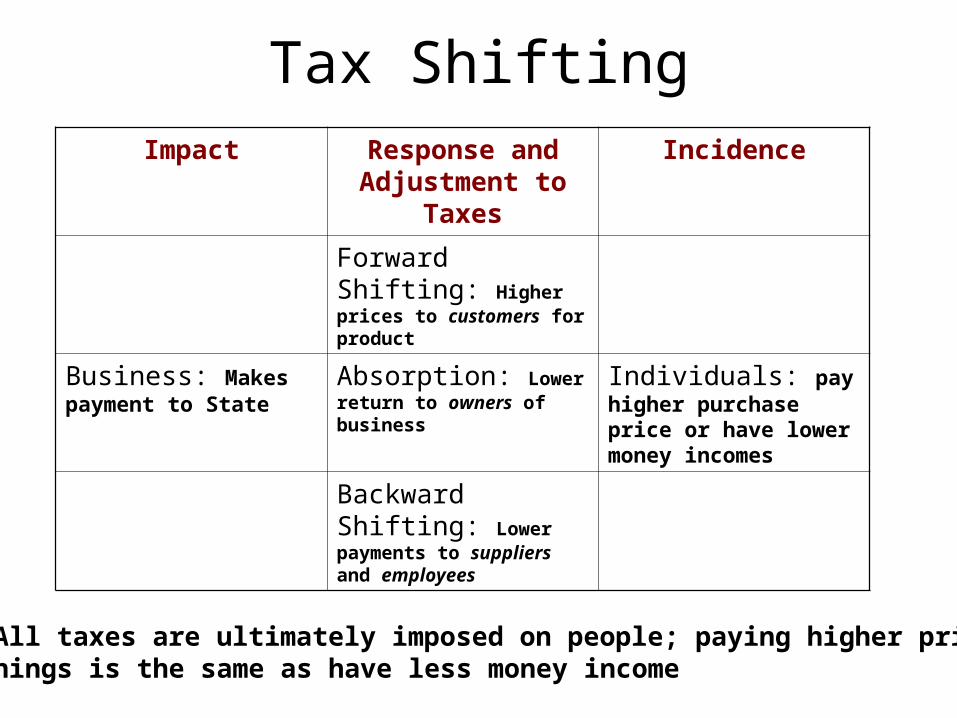

Tax ShiftingImpact Response and

Adjustment to TaxesIncidence

Forward Shifting: Higher prices to customers for product

Business: Makes payment to State

Absorption: Lower return to owners of business

Individuals: pay higher purchase price or have lower money incomes

Backward Shifting: Lower payments to suppliers and employees

Note: All taxes are ultimately imposed on people; paying higher prices for things is the same as have less money income

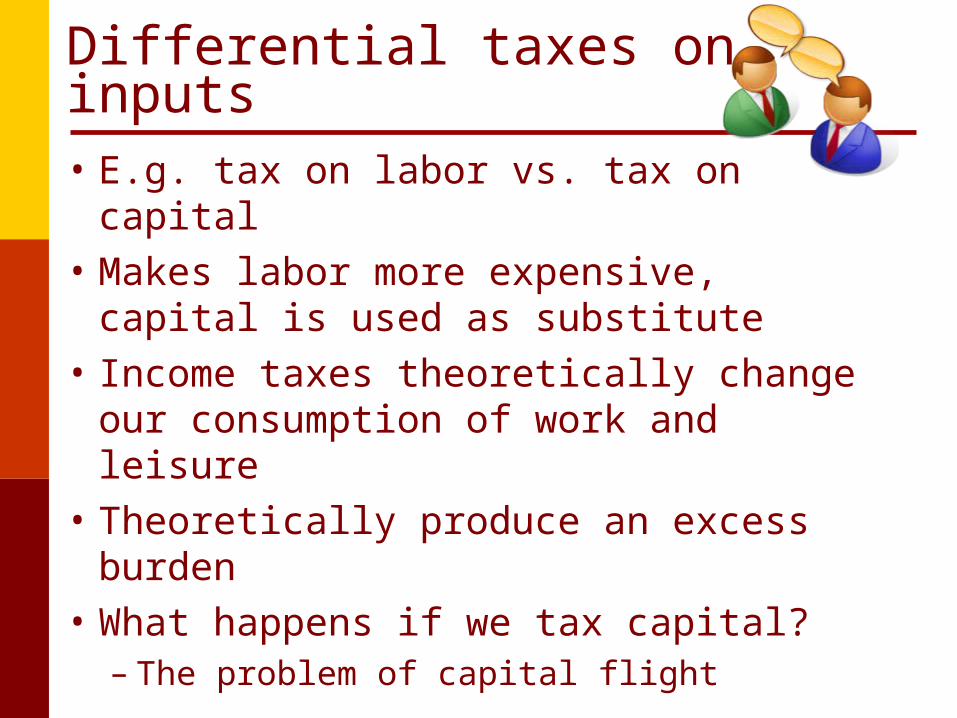

Differential taxes on inputs

• E.g. tax on labor vs. tax on capital

• Makes labor more expensive, capital is used as substitute

• Income taxes theoretically change our consumption of work and leisure

• Theoretically produce an excess burden

• What happens if we tax capital?– The problem of capital flight

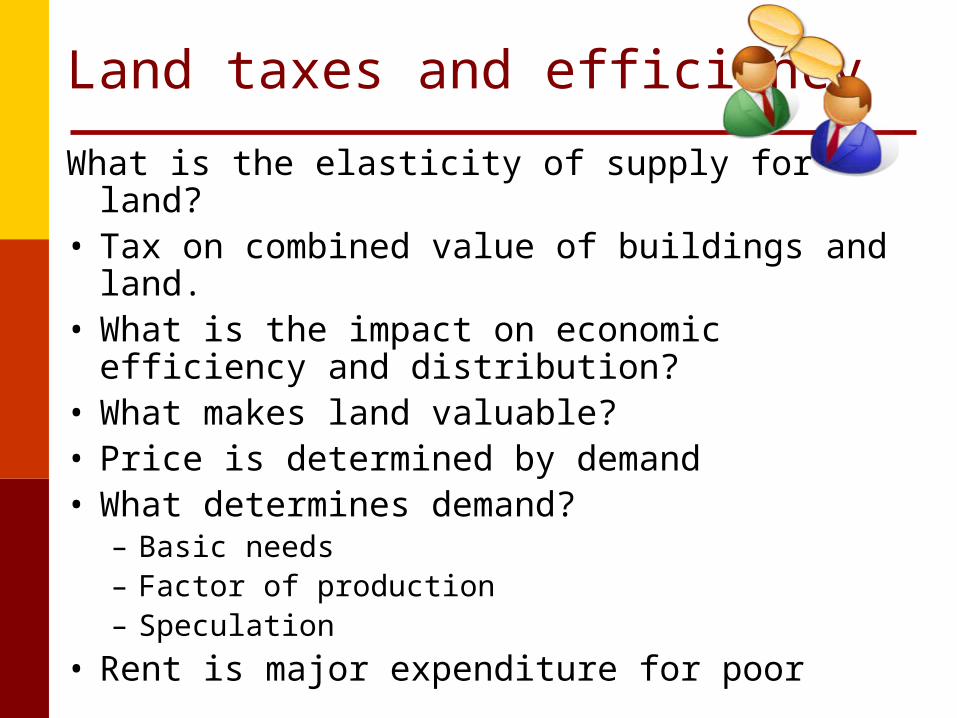

Land taxes and efficiency

What is the elasticity of supply for land?• Tax on combined value of buildings and land.• What is the impact on economic efficiency and

distribution?• What makes land valuable?• Price is determined by demand• What determines demand?

– Basic needs– Factor of production– Speculation

• Rent is major expenditure for poor

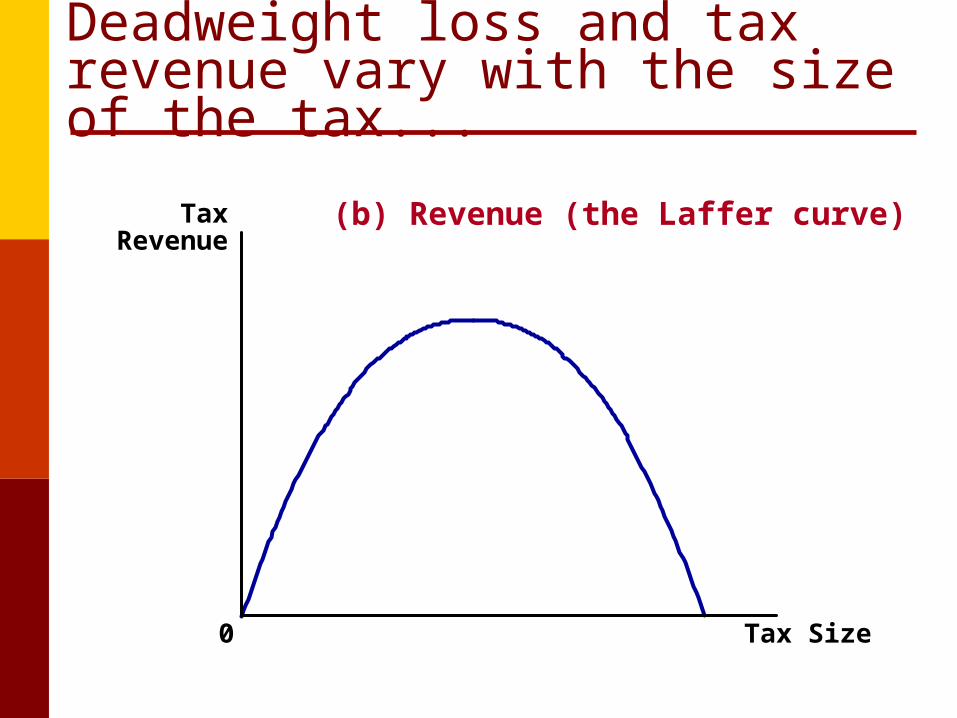

Deadweight loss and tax revenue vary with the size of the tax...

(b) Revenue (the Laffer curve)TaxRevenue

0 Tax Size

Tax avoidance and tax evasion

Tax evasion: The intentional misrepresentation or concealment of a person's tax obligations. Tax evasion is clearly illegal.Tax avoidance: Taking advantage of legal or arguably legal tax loopholes. Tax avoidance falls into 2 categories:

•Intentional relaxation of regulations to offer incentives•Legal exploitation of weakness in the legal system to reduce tax liability

Types of taxes

• Income taxes (salary, interest, rent, dividends)• Corporate tax (profit)• Property taxes• Land taxes • Excises (alcohol, tobacco, gas) • Sales• Transport • Inheritance • Social contributions to employees (Medicare,

social security, pension fund) • VAT

Taxes as main instrument of incentives type of regulatory strategyTax HavensVery low or zero tax offshore companies incorporated in jurisdictions often described as tax haven islands, such as the differing types of offshore company that can be formed in offshore company formation centres such as the BVI or British Virgin Islands, Belize or the SeychellesTerritorial TaxationOperate/Register in countries with favourable tax rates (Eg Hong Kong)

How to assess tax system?

• Fairness criteria:– Horizontal and vertical relative equality – Principle of ability to pay– Principle of received benefits

• Effectiveness criteria:– Economic neutrality – Flexibility – Organizational simplicity– Transparency

Subsidies

Subsidies

• In economics, a subsidy is a kind of financial government assistance, such as a grant, tax break, or trade barrier, in order to encourage the production or purchase of a good. The term subsidy may also refer to assistance granted by others, such as individuals or non-government institutions, although this is more commonly described as charity.

Subsidies

• Same basic concept as a tax

• Distort production incentives

• Must be paid for, so a subsidy in one place implies a tax in another

Types of subsidies

• Direct subsidies • Indirect Subsidies • Labor subsidies • Tax Subsidy • Production subsidies• Regulatory advantages • Infrastructure subsidies • Trade protection (Import) • Export subsidies (trade promotion) • Procurement subsidies• Consumption subsidies

Entry/exit barriers

Barriers

• Barriers to entry or exit are obstacles in the path of a firm which wants to enter or exit a given market.

• The term refers to hindrances that an individual may face while trying to gain entrance into (or exit out of) a profession or trade. It also, more commonly, refers to hindrances that a firm may face (or even a country) while trying to enter or exit an industry or trade grouping.

Classification of barriers

• Investment• Government regulation• Predatory pricing• Patents• Economy of scale• Customer loyalty• Advertising• Research and development• Sunk costs• Network effect• Restrictive practices• Distributor agreements• Supplier agreements

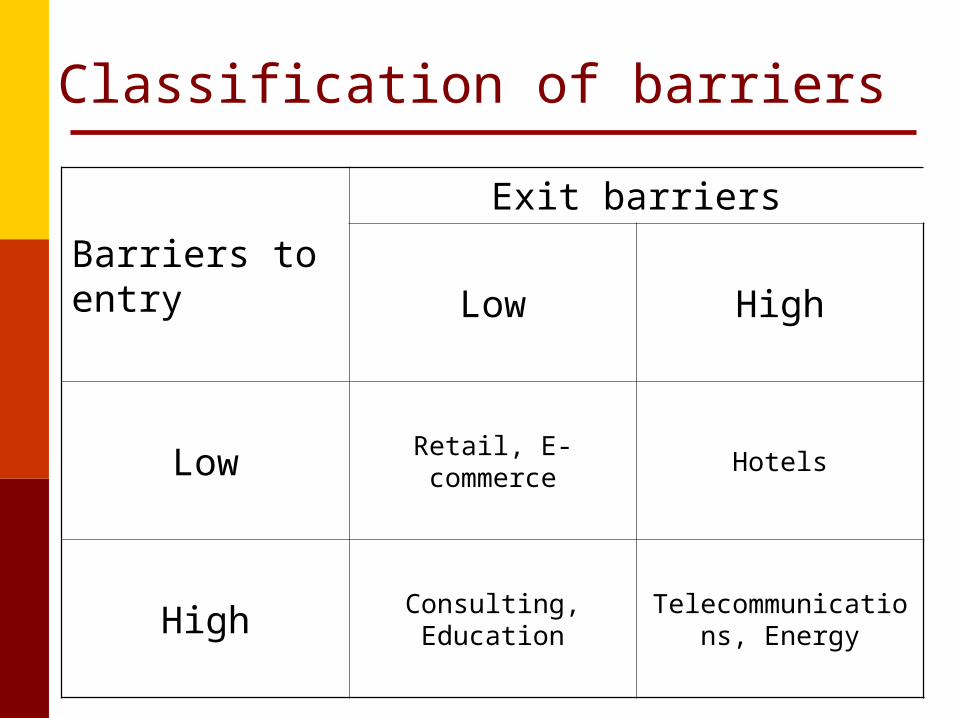

Classification of barriers

Barriers to entry

Exit barriers

Low High

Low Retail, E-commerce Hotels

High Consulting, EducationTelecommunications,

Energy

Recommended