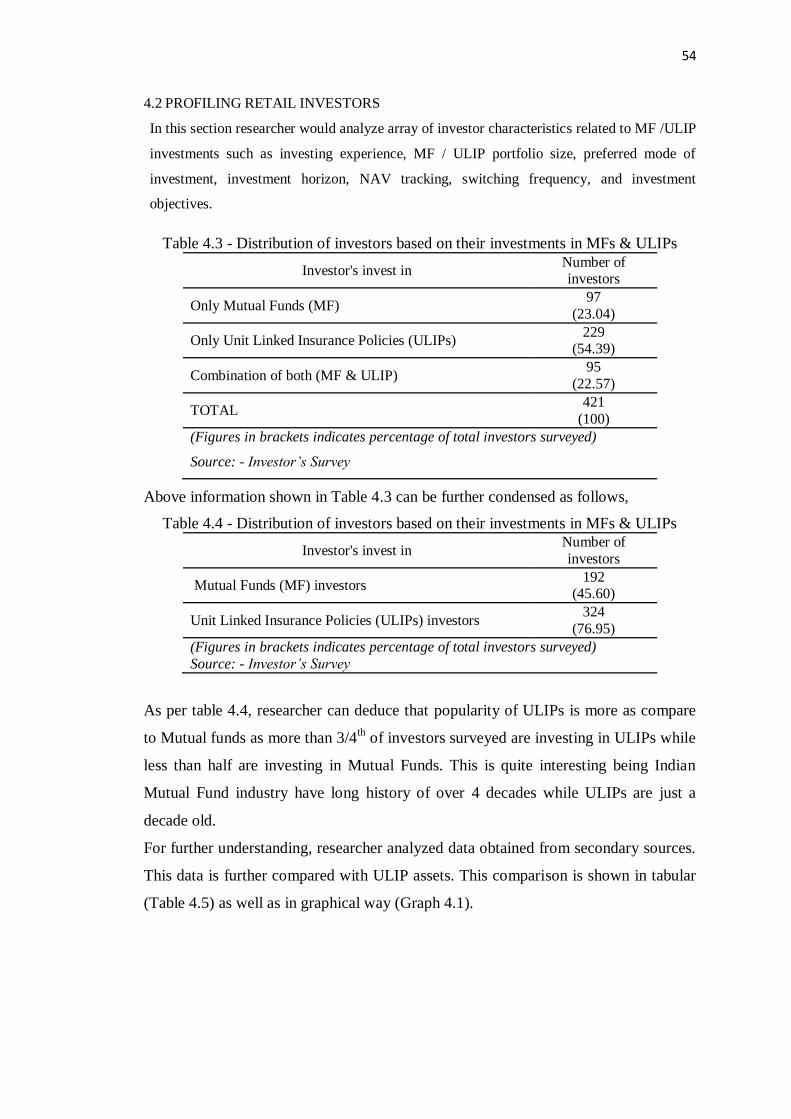

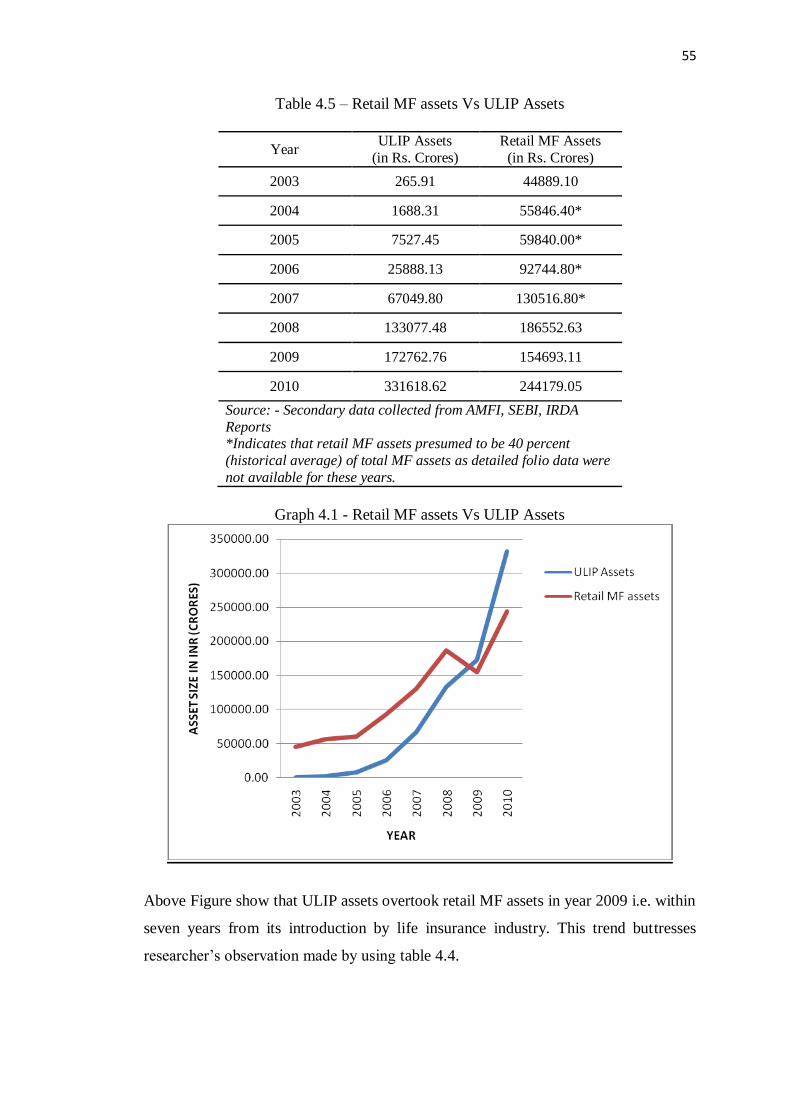

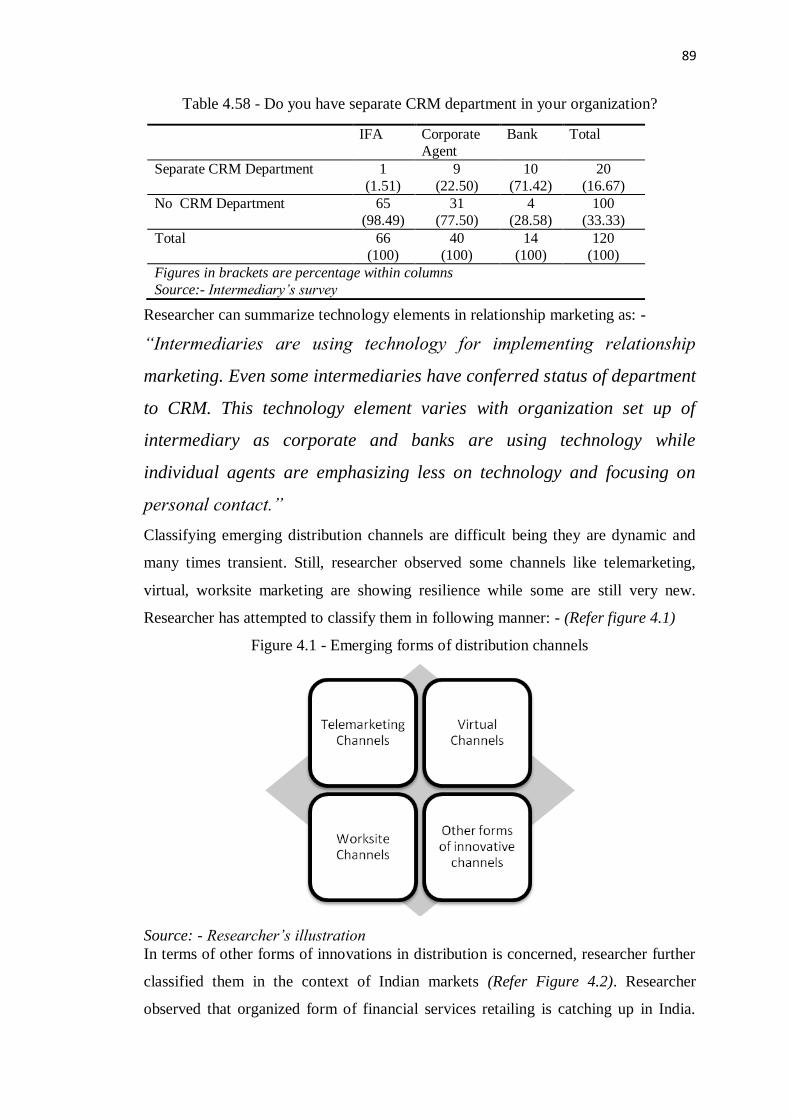

1

CHAPTER I

OVERVIEW OF THE

STUDY

2

“Healthy small investor – wealthy nation” – Dr.Kirit Somaiya

Saving is defined as excess of current income over current expenditure. Savings are

closely linked with nation’s economic growth. Being developing nation, importance

of savings to Indian economy is vital. High level of savings help the economy to

progress on a continuous growth path as investment is mainly financed out of savings.

Savings rate of our country is phenomenal. Gross domestic savings have increased

continuously from an average of 9.6 percent of GDP (Gross Domestic Product) during

the 1950s to 36.9 per cent of GDP in year 2007 -08. Savings are made via three

sectors i.e. public sector, private sector and household sector. Contribution of public

sector is erratic and hovering around 2 percent. Rather during 1998 -2003, public

sector’s contribution turned negative. Private sector savings are relatively better as it

had risen from 3.1 percent in 1990-91 to 8.1 percent currently. Contribution of private

sector towards capital accumulation is negative as their credit off take is larger than

their savings. Star saver and capital accumulator of our economy is household or retail

sector. A remarkable feature of the Indian macroeconomic story since independence

has been the continuous rise in her household savings over the decades, Mohan,

Rakesh (2008)1.

1.1 Composition of Household sector’s savings

Household / retail sector is consistently & increasingly contributing towards national

savings. Currently, household savings are 22.5 percent to the India’s GDP.

Considering household credit figures, researcher can easily state that Indian investors

understand the merits of saving over consumption. Thus, the widening of savings -

investment gaps of the public and private corporate sectors combined was financed

from household financial savings and partly from foreign savings. So any study

related to Household sector savings has importance.

After independence, Indian household’s savings in physical assets constituted the

largest portion as compared to the financial assets in the initial years of the planning

periods as Indian financial system was characterized by poor infrastructure and low

level of financial deepening. Rural households were keen on acquiring farm assets

while the portfolio of urban households constituted consumer durables, gold, jewelry

and house property. However, with the development of the financial infrastructure,

strengthening of the cooperative credit institutions, taking over of the banks

3

associated with the former princely states and transferring them into the public sector

(1954), strengthening and consolidation of the banking system in India (1950s and

1960s), nationalization of the insurance companies, establishment of Unit Trust of

India (1964), major term lending institutions for agriculture and industry (1964) and

nationalization of the major scheduled commercial banks (1969/1970), had a

cascading effect in raising the financial savings in our country . During 1980’s, the

financial savings overtook physical savings and became larger component of

household savings.

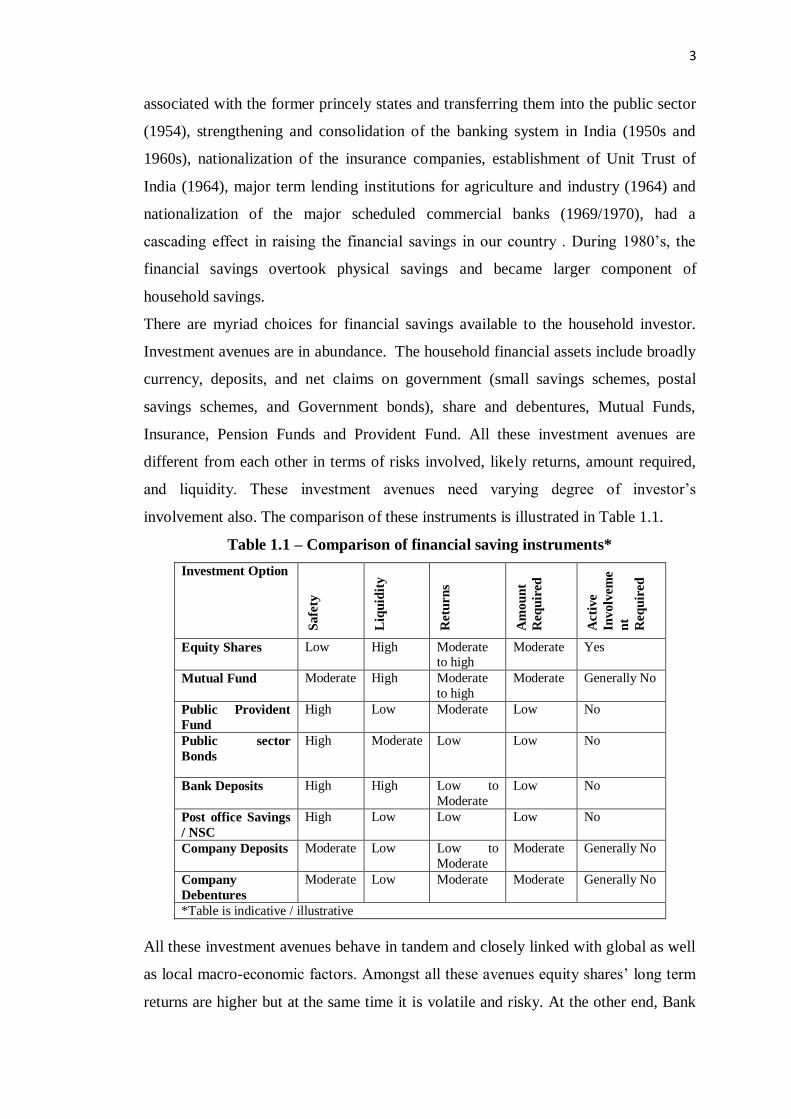

There are myriad choices for financial savings available to the household investor.

Investment avenues are in abundance. The household financial assets include broadly

currency, deposits, and net claims on government (small savings schemes, postal

savings schemes, and Government bonds), share and debentures, Mutual Funds,

Insurance, Pension Funds and Provident Fund. All these investment avenues are

different from each other in terms of risks involved, likely returns, amount required,

and liquidity. These investment avenues need varying degree of investor’s

involvement also. The comparison of these instruments is illustrated in Table 1.1.

Table 1.1 – Comparison of financial saving instruments*

Investment Option

Sa

fety

Liq

uid

ity

Retu

rn

s

Am

ou

nt

Req

uir

ed

Acti

ve

Inv

olv

em

e

nt

Req

uir

ed

Equity Shares Low High Moderate

to high Moderate Yes

Mutual Fund Moderate High Moderate

to high

Moderate Generally No

Public Provident

Fund

High Low Moderate Low No

Public sector

Bonds

High Moderate Low Low No

Bank Deposits High High Low to

Moderate

Low No

Post office Savings

/ NSC

High Low Low Low No

Company Deposits Moderate Low Low to

Moderate

Moderate Generally No

Company

Debentures

Moderate Low Moderate Moderate Generally No

*Table is indicative / illustrative

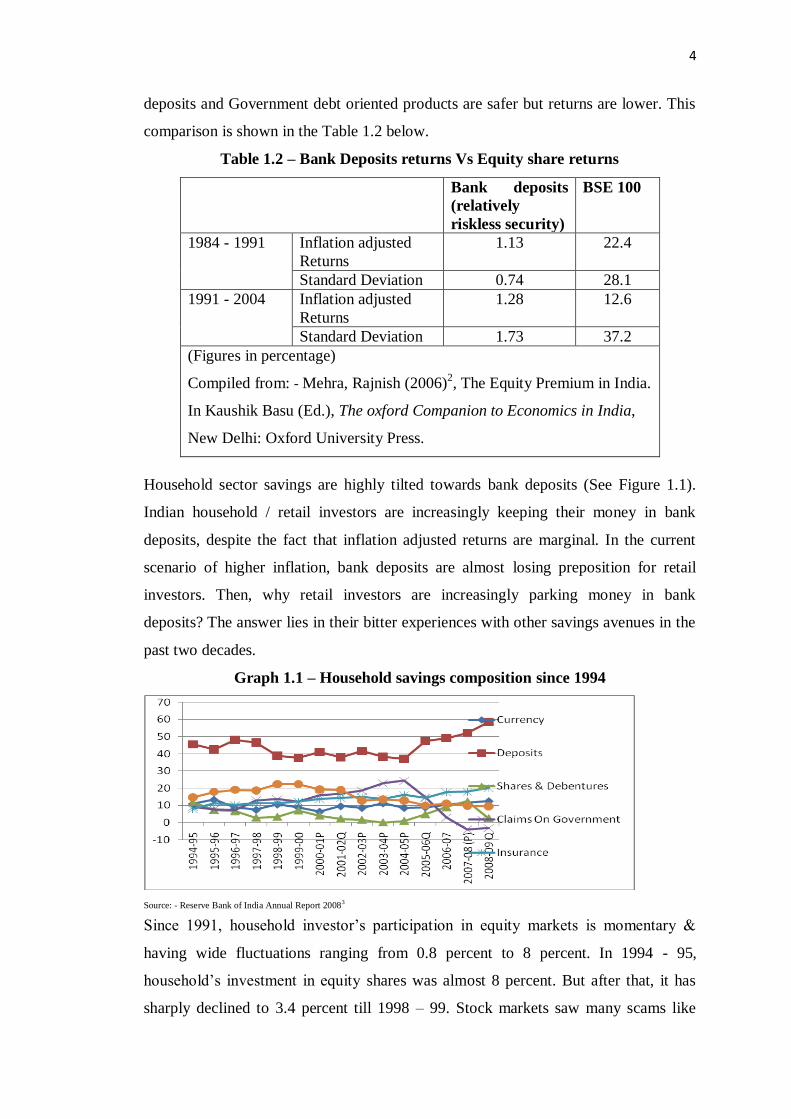

All these investment avenues behave in tandem and closely linked with global as well

as local macro-economic factors. Amongst all these avenues equity shares’ long term

returns are higher but at the same time it is volatile and risky. At the other end, Bank

4

deposits and Government debt oriented products are safer but returns are lower. This

comparison is shown in the Table 1.2 below.

Table 1.2 – Bank Deposits returns Vs Equity share returns

Bank deposits

(relatively

riskless security)

BSE 100

1984 - 1991 Inflation adjusted

Returns

1.13 22.4

Standard Deviation 0.74 28.1

1991 - 2004 Inflation adjusted

Returns

1.28 12.6

Standard Deviation 1.73 37.2

(Figures in percentage)

Compiled from: - Mehra, Rajnish (2006)2, The Equity Premium in India.

In Kaushik Basu (Ed.), The oxford Companion to Economics in India,

New Delhi: Oxford University Press.

Household sector savings are highly tilted towards bank deposits (See Figure 1.1).

Indian household / retail investors are increasingly keeping their money in bank

deposits, despite the fact that inflation adjusted returns are marginal. In the current

scenario of higher inflation, bank deposits are almost losing preposition for retail

investors. Then, why retail investors are increasingly parking money in bank

deposits? The answer lies in their bitter experiences with other savings avenues in the

past two decades.

Graph 1.1 – Household savings composition since 1994

Source: - Reserve Bank of India Annual Report 20083

Since 1991, household investor’s participation in equity markets is momentary &

having wide fluctuations ranging from 0.8 percent to 8 percent. In 1994 - 95,

household’s investment in equity shares was almost 8 percent. But after that, it has

sharply declined to 3.4 percent till 1998 – 99. Stock markets saw many scams like

5

Harshad Mehta Scam (1992), Vanishing Company Scam (1995 - 99), Name changing

scam (1999 - 00), dotcom scam (1999 - 00), Ketan Parekh Scam (1999 - 2001). These

scams shattered household investor’s confidence in equity share investment.

The three most important and persistent worries of household investors have been

identified during Indian household investor’s survey in 20044, as (a) too much

volatility of stock market prices, (b) too much price manipulation and (c) deficient

corporate governance.

This shattered confidence is evident as on average 1.13 percent household savings

were channelized in equity markets during 2000 -2006. During this period stock

markets were booming. Observing this phenomenal growth, lot of retail investors

were attracted towards equity markets, that is why equity savings has increased to 4

percent. In this return chasing behavior, lot of retail investor burnt their fingers as our

markets crashed towards end of 2007. The retail investors who had invested in

plantation companies, chit funds, non bank finance companies (NBFC) like CRB

finance during 1990s had lost their money. This made retail investor cautious about

private or corporate sector savings avenues; this may have pushed them to keep their

hard earned money into safe instruments like bank deposits, government schemes.

But, retail investors are in sticky situation as bank deposits returns are marginal and

their experiences in equity markets & other financial markets are disappointing. Again

markets for equity shares, derivatives and other assets have increasingly become

complex, mature and information-driven. A typical individual investor especially

Indian is not likely to have the knowledge, skills, and time to keep track of and

understand the causes and implications of the price changes and trends. So, mutual

funds being the combiner of various savings instruments are regarded as the ideal

investment vehicle for today’s complex and modern financial scenario.

1.2 Concept of Mutual Fund

A Mutual Fund is a trust that pools the savings of a number of investors who share a

common financial goal. Anyone with an investible surplus as little as a few hundred

rupees can invest in Mutual Funds. These investors buy units of a particular Mutual

Fund scheme which has a defined investment objective and strategy. The money thus

collected is then invested by the fund manager in different types of securities, ranging

from shares to debentures to money market instruments, depending upon the scheme’s

stated objectives. Fund manager a professionally qualified and experienced manager

6

who manages the funds in a way to increase the returns on the money invested by the

people. Thereby, the investor avoids direct involvement with the financial markets

and avoids any disadvantage that may accrue to him because of asymmetric

information or any other reason.

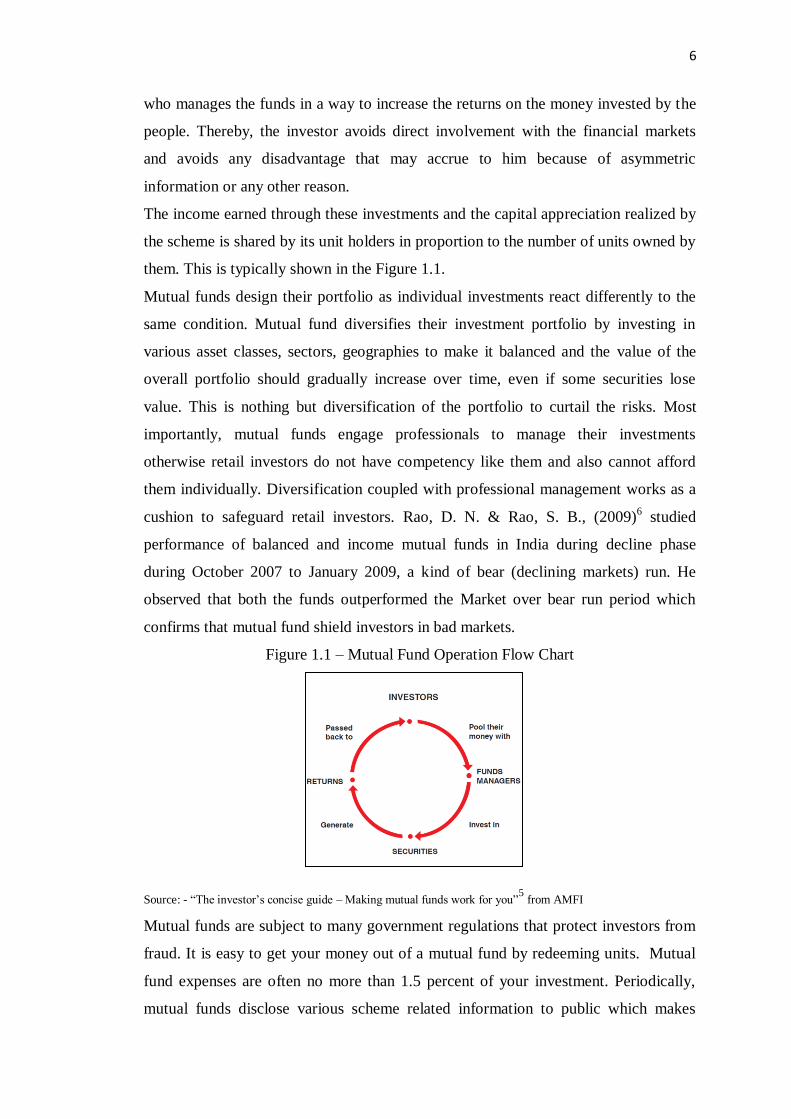

The income earned through these investments and the capital appreciation realized by

the scheme is shared by its unit holders in proportion to the number of units owned by

them. This is typically shown in the Figure 1.1.

Mutual funds design their portfolio as individual investments react differently to the

same condition. Mutual fund diversifies their investment portfolio by investing in

various asset classes, sectors, geographies to make it balanced and the value of the

overall portfolio should gradually increase over time, even if some securities lose

value. This is nothing but diversification of the portfolio to curtail the risks. Most

importantly, mutual funds engage professionals to manage their investments

otherwise retail investors do not have competency like them and also cannot afford

them individually. Diversification coupled with professional management works as a

cushion to safeguard retail investors. Rao, D. N. & Rao, S. B., (2009)6 studied

performance of balanced and income mutual funds in India during decline phase

during October 2007 to January 2009, a kind of bear (declining markets) run. He

observed that both the funds outperformed the Market over bear run period which

confirms that mutual fund shield investors in bad markets.

Figure 1.1 – Mutual Fund Operation Flow Chart

Source: - “The investor’s concise guide – Making mutual funds work for you”5 from AMFI

Mutual funds are subject to many government regulations that protect investors from

fraud. It is easy to get your money out of a mutual fund by redeeming units. Mutual

fund expenses are often no more than 1.5 percent of your investment. Periodically,

mutual funds disclose various scheme related information to public which makes

7

them transparent. Lot of mutual fund schemes comes with tax benefits also. Most

importantly mutual funds offer wide variety of schemes to the investors. This fact

makes mutual fund an ideal investment product for masses. Mutual funds cater to the

wide range of needs of different classes of investors.

In short, mutual funds possess several advantages like diversification, professional

management, tight regulation, liquidity, low cost, transparency, flexibility, wide

variety of choice, tax benefits. Thus, Mutual Funds can be the most suitable

investment for small or retail investors as it offers an opportunity to invest in a

diversified, professionally managed basket of securities.

1.3 Global Evolution of Mutual Fund

Historians may differ on the exact origin of mutual funds Rachana, Baid (2007)7. As

per Rouwenhorst, K. G. (2004)8, Mutual funds emerged early in the second half of the

18th century in The Netherlands. In 1774, the Dutch merchant and broker Abraham

Van Ketwich invited subscriptions from investors to form a trust named Eendragt

Maakt Magt—the maxim of the Dutch Republic, “Unity Creates Strength.” It was a

closed end Mutual fund aimed to provide small investors an opportunity to diversify

by investing in Austria, Denmark, Germany, Spain, Sweden, Russia, and a variety of

colonial plantations in Central and South America.

Consequently, this concept has travelled across countries but it really flourished and

blossomed into the world’s largest Mutual Fund industry in United States of America

(USA). The first USA based mutual fund was formed when three executives dealing

in securities in Boston came together & put their money for investment purposes in

1924 and created a mutual fund i.e. fund for the mutual benefit of the three members.

However, the first recognized US based mutual fund was instituted on 21st

March

1924 that was called the ‘Massachusetts Investors Trust’ that grew from a $50,000 to

$392000 in a year with 200 shareholders. Subsequently ‘Massachusetts Investors

Trust’ went public in 1928. In a brief period of five years there were around 19 open-

end mutual fund schemes and 700 closed-end mutual fund schemes operating in the

American financial market, till the stock market crashed in 1929 that resulted in

‘Great Depression’ in the economy.

The great depression compelled the authorities in USA to take steps to regulate the

mutual fund industry. This led to the enactment of the Securities Act of 1933 and the

establishment of the Securities Exchange Commission (SEC) that necessitated

8

registration of all mutual funds operating in the US market to be registered with the

Securities Exchange Commission (SEC) and made various rules for the mutual fund

industry like drafting a prospectus that would contain detailed information about the

fund, the securities and the fund manager managing the mutual fund. It also drafted

the Investment Company Act of 1940 whose guidelines the mutual funds had to

comply. This act regulates the organization and functioning of mutual funds and

other companies. The act primarily tries to minimize the conflict of interest that arises

in investing, reinvesting and trading in securities and simultaneously offer the

securities to public for investment. According to this act, the companies operating in

this sector have to reveal their financial condition to the investing public and the

investment policies during the initial sale of stock and continue to do on a regular

basis along with other information relating to the investment objectives, company

structure and operations. Falling short of any compliance to the act, the Securities

Exchange Commission can directly supervise the investment operations or judge the

merits of their investment schemes. Today, almost this model is followed across all

the countries of the world.

From above discussion, researcher can straightforwardly deduce that though the

concept of mutual fund is rooted in Netherlands but the modern concept of

mutual fund is originated in USA.

As Fernando, Deepthi; Klapper, Leora; Sulla, Víctor Sulla & Vittas Dimitri (2003)9

observed the global growth of Mutual funds were explosive one during 1990s, now

the mutual fund concept is reached to all the continents and regarded as one of the

crucial part of financial services sector of any country.

1.4 Evolution of Mutual Fund Industry in India

Many researchers viz Kamiyama, Tetsuya (2007)10

;Agrawal, Deepak (2011)11

; Mitra,

Anupam (2009)12

; Acharya, D & Sidana, Gajendra (2007)13

; Kumar, Raj and Sharma,

Priyanka (2009)14

have traced the evolution cum history of mutual funds India.

The development of India's mutual fund industry can be divided into four distinct

phases. The first phase was spanned from 1964 until 1987. In 1963, India's central

bank, the Reserve Bank of India (RBI), established the Unit Trust of India (UTI);

subsequently its control was passed from the RBI to the Industrial Development Bank

of India in 1978. The first fund launched by the UTI was the Unit Scheme 1964 (US -

64), which had assets worth of Rs 67 billion, at the end of 1988.

9

The second phase was from 1987 until 1993, known for entry of public sector banks

in Mutual Fund Industry. SBI Mutual Fund was established by the State Bank of India

in June 1987. This was followed by several other funds introduced by public sector

banks and insurance companies. At the end of 1993, India's mutual fund industry

assets had grown to Rs 470 billion.

The third phase was from 1993 to 2003. This phase is known for spate of regulations

and emergence of private players in this industry. In 1993, the Securities and

Exchange Board of India (SEBI) introduced a comprehensive set of regulations

governing mutual funds, known as SEBI (Mutual Fund) Regulation 1993, to regulate,

and require the registration of, all non-UTI funds. These regulations were further

completely overhauled in 1996, and now it is the SEBI (Mutual Funds) Regulation

1996 that regulates mutual funds. Since 1993, private-sector asset management

companies have been actively involved in the Indian mutual fund industry. In July

1993, the first private-sector fund was registered named Kothari Pioneer, later it was

merged with Franklin Templeton. The number of asset management companies has

continued to grow. This phase also saw number of mergers and acquisitions in the

sector. At the end of January 2003, India's mutual fund industry had 33 asset

management companies managing assets totaling Rs 1.218 trillion, and the largest of

them was UTI, with assets of Rs. 445.4 billion. UTI saw its “almost death” when

fiasco came to light in the form of two big blows in 1997 and 2001.

The fourth phase began in 2003. On the backdrop of US – 64 fiasco, UTI is demerged

by repealing The Unit Trust of India Act 1963 in February 2003. The first was the

Specified Undertaking of the Unit Trust of India (SUUTI), which was made up of

UTI's flagship fund Unit Scheme 1964 and closed-end funds, and managed assets as

of the end of January 2003 totaling Rs 298.3 billion. The other entity was UTI Mutual

Fund, the major shareholders of which were four public-sector financial institutions,

including the State Bank of India. These funds were registered with the SEBI and

subject to SEBI's mutual fund regulations. This split up of UTI, along with mergers

and acquisitions within India's mutual fund industry propelled the industry into a new

era of growth and restructuring. The buzzword is globalization and achieving growth

by penetrating in the market through various distribution channels.

As shown in the figure 1.2, mutual fund growth is exponential after year 2003. This

phenomenal growth is attributed to various factors. One of the important recent

developments in the Mutual Fund Industry has been the aggressive explosion of the

10

private players. The recent years have seen a private sector wave in the opening up of

the sector, as the large number of private sector companies has entered in the Indian

Mutual Fund Industry.

Another major change in the last few years has been the globalization of the industry

as lot of foreign companies entered by way of mergers, acquisitions, stake sale; etc .

Currently, there is a general restructuring going on in the industry. An increased

foreign participation and competition in the Mutual Fund industry paved way for

many new practices such as product innovation, sharp improvements in the service

standards and disclosures, usage of technology, broker education and support, advent

of new distribution channels, etc.

FIGURE 1.2 - GROWTH OF MUTUAL FUND ASSETS UNDER

MANAGEMENT

Source: www.amfi.org.in15

With the industry of more than four decades, Mutual Fund industry must have

respectable presence in global Mutual Fund industry. An important criterion, which is

used by the analysts to judge any country’s mutual fund industry, is amount of MF

11

assets to GDP (PPP basis) ratio. Let me compare Indian mutual fund industry vis-a-

vis to some other nations in terms to mutual fund assets under management as

compare to Gross Domestic Product – purchasing power parity basis (GDP) that

country. The table 1.3 shows how Indian mutual fund industry is placed against other

countries: -

Table 1.3 – Global comparison in terms of Mutual Fund asset size in terms of

country’s GDP

Country Mutual Fund

asset size in terms

of country’s GDP

Country Mutual Fund asset

size in terms of

country’s GDP

Bahrain** 44% Luxemburg More than 100%

Egypt* 13% Hong Kong More than 100%

Kuwait* 8.2% Australia** 133.4 %

Morocco* 32.1% USA++ 78.6%

Saudi Arabia* 31.9% Japan++ 14.3%

United Kingdom++ 34.9% Russia++ 26%

India++ 1.3% Brazil++ 23.1%

*Figures are for the year 2009, **Figures are for the year 2010,

++ Figures are for the year 2006

Source: - Macko, Willam & Sourrouille, Diego (2010), “Investment Funds in

MENA”, Financial Flagship series of World Bank,16

Indian economy is ranked amongst the top 10 globally (in terms of GDP), and placed

fourth-largest [in terms of purchasing power parity (PPP)]. However, when it comes

to MF assets under management (AUM), Rao, P. H., & Mishra, V. K, (2007)17

observed that India’s rank is twenty fifth in year 2006 which is not very satisfactory,

rather dismal. Add to this, out of total mutual fund assets in India only 36% are owned

by retail investors while rest is by corporate / institutional investors. This further

underlines that retail or household investors’ participation in Indian mutual fund

industry is well below the global standards.

While comparing Indian mutual fund industry and studying global evolution of

mutual funds, researcher came across with phenomenon of integration or

convergence. As this phenomenon does have strong linkage with mutual funds so we

will further explain the same in the next section.

12

1.5 Defining mutual funds on the backdrop of financial integration /

convergence

The drivers behind financial service integration and financial convergence are

customer demand as well as the pressure on institutions to find new growth

opportunities and revenue streams.

Berghe, Van den; Verweire, K; Carchon, S.W.M. (1999)18

, Financial Convergence

includes all possible interfaces between different categories of financial service

providers. Financial services integration occurs when firms in one sector create and

sell products containing significant elements traditionally associated with products of

another sector. Kist, Ewald (2001)19

found that the banking, insurance, asset

management, investment and pension industry is converging into each other to form

integrated financial services.

It is necessary to understand this convergence especially related with mutual funds.

Professional asset management is central aspect of mutual funds (that is why it

referred as a part of asset management industry). Importantly professional asset

management is also vital aspect for other financial services like pension / retirement

products, insurance, etc. Understanding these overlaps will facilitate us to understand

the concept of mutual fund in this modernised world of financial markets.

Walter, Ingo (1999)20

observes that the structure of the asset management industry in

European union encompasses significant overlaps amongst the three types of asset

pools i.e. mutual funds, portfolio services & pension funds, to the point that they are

sometimes difficult to differentiate. He further noted the linkage between defined-

contribution pension funds and the mutual fund industry, and the association of the

disproportionate growth in the former with the expansion of mutual fund assets under

management. There is a similar but perhaps more limited linkage between private

clients’ assets or (known as Portfolio Management services i.e. PMS in India) and

mutual funds.

In US, There is considerable overlap between Mutual Funds and retirement (pension)

assets as various retirement plans like DC (Defined contribution) Plans, IRA

(Individual Retirement Account), 401(K) Plans, 403(B) Plans, Private retirement

plans are increasingly mobilizing funds into Mutual Fund industry.

Due to this complex interfaces amongst various financial services, even Fernando,

Deepthi & et al (2003)21

faced difficulty in setting the boundaries for mutual funds as

“Annual mutual fund report” of ICI (Investment Company Institute, USA) publishes a

13

table with aggregate data on mutual funds around the world but also includes a strong

warning which is as follows: -

………….because of differences in definitions and coverage, the published data

lacks comparability. These differences are due to the inclusion, or exclusion, of

closed end funds, unit-linked funds (popularly known as ULIPs in India)

operated by life insurance companies, and retirement funds that operate on

mutual fund principles (such as the AFP system of Chile or the defined-

contribution pension plans prevailing in Australia, New Zealand, South Africa

and the United States).

In the UK, nexus between ULIPs and mutual fund is stronger as insurance companies

invest fund raised under ULIPs in Mutual Funds, Aneel Keswani and David Stolin

(2010)22

.

Even, Chakrabarti, Rajesh (2009)23

clustered various financial products like mutual

funds, unit-linked insurance plans, and Venture Capital Funds both domestic and

foreign as a part of Asset management Industry in India. Internationally, he also found

“professional management of assets” is the common factor amongst all these

products. Further he said pooling of funds is not prerequisite, even professional

management of the assets of high net worth individuals (HNI) may also be considered

part of this asset management industry. As both Mutual Funds and Unit Linked

Insurance Policies (ULIPs) are pooling money from investors this similarity has even

enticed Das, Bhagaban; Mohanty, Sangeeta and Shil, N.C., (2008)24

to compare

investor’s behavior towards both the products.

This increased convergence is mainly responsible for spat between two Indian

regulators pertaining to regulations of Mutual funds & ULIPs.

Both the Mutual Funds and ULIPs resembles due to following two reasons: -

a) Products are similar in terms of its composition & features.

b) Similar Companies / Corporate houses / brands involved in offering both the

products

a) Products are similar in terms of its composition & features.

As far as similarities between mutual fund and Unit Linked Insurance Products are

concerned one would found an ample discussion in the Securities exchange board of

India (SEBI) order passed against insurers offering ULIPs issued on 6th

April 2010.

This 11 page order discusses the features of ULIPs. It was found that ULIPs are

predominantly Mutual Funds with small component of life insurance. It will be

14

interesting to pluck out some text from this order to establish point No. 1. Order

observes,

From the examination of the product documents of the ULIPs and the investment

options offered therein by the entities it is noted that:

a. the contributions or payments made by the investor are pooled;

b. the contributions or payments are made to such ULIPs by the investor

with a view to receive profits, income;

c. the investment made by the investor in the ULIPs is managed on behalf

of the investor;

d. the investor does not have day to day control over the management and

operation of the ULIPs.

The aforementioned attributes are those of a collective investment scheme and

also of the mutual funds.

Again Insurance companies themselves consider ULIPs differently as compare to

traditional insurance policies. It is also found that in their product brochure for ULIPs,

the entities have under the heading “risks of investments”, inter alia, disclosed and

declared that:

a. unit linked life insurance products are different from traditional

insurance products and are subject to risk factors.

b. the premium paid in unit linked life insurance policies are subject to

investment risks associated with capital markets and the unit price of the

units may go up or down based on the performance of the fund and factors

influencing the capital market and the insured/policyholder is responsible

for his/her decisions.

…………….direct the entities mentioned in paragraph 1 of this order not to issue

any offer document, advertisement, brochure soliciting money from investors or

raise money from investors by way of new and/or additional subscription for any

product (including ULIPs) having an investment component in the nature of

mutual funds, till they obtain the requisite certificate of registration from SEBI.

This order paved the way for one of the most talked regulatory tussle between

Insurance Regulatory Development Authority (IRDA) & Securities Exchange Board

of India (SEBI). The matter was referred to various apex bodies and at the last SEBI’s

order is set aside and ULIPs remained under the regulations of IRDA. This entire

regulatory battle was intensely discussed in electronic as well as print media. Lots of

15

articles were written and published about how the ULIP charges are irrationally

higher as compare to Mutual Funds. Due to this, investors became increasingly aware

about hidden charges in ULIPs. Therefore, IRDA understood this trend and took

some immediate steps and issued new ULIP guidelines. ULIPs under the new set of

the guidelines were re-launched by the life insurers. New ULIPs become more similar

to the Mutual Funds as the cost structure is completely changed to make it comparable

with MF. Still in terms of hidden expenses, ULIPs are dearer as compare to Mutual

Funds. As far as this cost structure is concerned an innovation in the form of life style

wrap was earlier suggested by Korivi, Sunder Ram & Venkatesh, B.S., (2007)25

to

reduce management expenses ratio, by introducing Life-Style Wraps. These are

essentially index funds (type of mutual fund) that will have a term insurance wrapped

around it. They call it Life-Style Wraps because these products can satisfy the cash

flow requirements to support investors’ life-style needs.

From Investor’s perspective, both products are similar in terms various decisions one

has to take while investing in these products. Both the products are investing in

various asset classes like equity, debt, money market, etc. Investor has to decide the

type of fund he or she should invest; again he has to decide the combination of asset

classes and weightage for each one. It is not only one time decision but he or she has

to take periodic review to see whether the allocation is fitting to the prevailing

situation in the financial markets.

b) Similar Companies / Corporate houses / brands involved in offering both the

products

A close & detailed look over various organizations offering Mutual funds and life

insurance products (including unit Linked Insurance Plans i.e. ULIPs) will reveal that

both the industries are similar in terms of members involved in it.

The table 1.4 & 1.5 shows that almost seventy percent life insurers are involved in

mutual fund industry while almost forty percent mutual fund companies are also

operating in life insurance industry.

Researcher has seen how the overlap amongst pension funds, insurance and mutual

funds are globally. Researcher has also examined the similarities between some

insurance products (mainly ULIPs) and mutual fund on the backdrop of recent

regulatory tangle between two regulators (SEBI & IRDA).

16

Table 1.4 - Mutual Fund Companies’ participation into Life Insurance Industry

Year

Total Number of

Mutual fund

Companies

(Column I)

Pure Mutual

Fund companies

(Column II)

MF Companies

or their JV

partners

offering life

insurance

(Column III)

As on

31st March

2010

38

(100)

22

(57.89)

16

(42.11)

As on

31st March

2011

43

(100)

25

(58.13)

18

(41.87)

Figures in the brackets indicate percentage within row

Table 1.5 - Life Insurance Companies’ participation into Mutual Fund Industry

Year

Total Number of

Life Insurance

Companies

(Column I)

Pure Life

Insurance

companies

(Column II)

Insurance

Companies or their

JV partners offering

Mutual Funds

(Column III)

As on

31st March

2010

23

(100)

9

(39.13)

14

(60.87)

As on

31st March

2011

23

(100)

7

(30.43)

16

(69.57)

Figures in the brackets indicate percentage within row (Technically, third column should be same for table 3.2 and table 3.3 but there are four

Mutual Fund companies came together and formed two insurance companies Canara Robeco

+ HSBC = CanaraHSBC, Tata + AIG = Tata AIG)

Importantly, there is close similarity amongst distribution intermediaries involved in

both MF and ULIPs. As this study is focusing on “role of distribution intermediaries”

pertaining to Mutual Funds. These similarities are giving birth to question,

“Should researcher treat ULIP as a mutual fund for the purpose of our study?”

This question has compelled researcher to define mutual funds, specifically for the

purpose our study.

The situation currently in India is summed up in the latest statement made by Mr.

Yogesh Agarwal, chairman, Pension Fund Regulatory and Development Authority

(PFRDA). He spoke to Business standard Reporter on 19th April 2011, “……….

entities, not products, are regulated in India under the current regulatory framework”

17

He also said pension products offered by insurance companies would continue to be

regulated by the Insurance Regulatory and Development Authority (IRDA), while

those offered by mutual funds would be regulated by the Securities and Exchange

Board of India (SEBI).

In this scenario of financial convergence, we will treat ULIPs as well as NPS as

mutual fund. So our definition of the mutual funds is as follows: -

Mutual funds include all those investment services where investors’ money is pooled

(making it collective investment) and it is invested in various securities including

financial and physical so that benefits of diversification & risk sharing will happen

with the help of professionals.

In a nutshell the following features are standards to term a financial product as

mutual Fund: -

1) Investors money is pooled

2) Money is invested in various securities

3) Professional management

Mutual funds includes all Unit Linked Insurance Products (including retirement

products), Pension Products from Pension Fund Regulatory Development Authority

i.e. PFRDA e.g. New Pension Schemes.

Pension sector reforms are on cards and some steps has been taken in the recent past.

One of the prominent developments in this regard is setting up of Pension fund

Regulatory Authority (PFRDA). PFRDA was established by Government of India on

23rd

August, 2003. The Government has, through an executive order dated 10th

October 2003, mandated PFRDA to act as a regulator for the pension sector. The

mandate of PFRDA is development and regulation of pension sector in India.

PFRDA constituted and launched a product named New pension Scheme (NPS) in

2004 for Government employees & after this PFRDA has allowed every citizen to

invest in NPS from 1st April, 2009 on a voluntary basis. After almost two years,

there are only 38857 accounts (as on 5th

February 2011) are opened, even though

8894 offices are distributing the product. This means still NPS as product has not

gained any presence in country till date & it is in very nascent stage. As a result,

researcher dropped the NPS (though it resembles with Mutual Fund) from the

working definition of mutual funds. Rather this study will be useful to PFRDA to

strengthen NPS distribution. In given situation, there is need to redefine the definition

18

of mutual fund in the context of our study. So the final definition of mutual fund is as

follows: -

Mutual funds include all those investment services where investors’ money is

pooled (making it collective investment) and it is invested in various securities

including financial and physical so that benefits of diversification & risk sharing

will happen with the help of professionals. In a nutshell, the following features

are essential to term a financial product as Mutual Fund: -

1) Investors money is pooled

2) Money is invested in various securities

3) Professional management

Mutual funds includes the all Unit Linked Insurance Products offered by life

insurance companies.

1.6 Statement of Research problem

Thus Indian MF industry has long history. In the last decade, ULIPs became popular.

As discussed earlier mutual fund & ULIP investments have many merits over other

investment avenues. Considering this, mutual fund & ULIP investments should be

popular and widespread in our country. But in reality, at the end of March 2009, there

are only 4,60,75,763 individual investors30

investing in mutual funds. As per IRDA’s

annual report, by the end of year 2007 – 08, total number of ULIP policies in India

issued was 5611400031

. For a nation with billion plus population, these figures seem

to be small. MF /ULIP penetration will be in single digit.

Also the same concern has been endorsed by erstwhile SEBI chairman Mr. C. B.

Bhave while addressing to Mutual fund industry in Mutual Fund Summit 2009 on 17th

June 2009,

“The importance of the individual investors is tremendous and that lesson we

will take home not because somebody tells us that you need to go to retail and

you need to go the individual investors but because it is in industry’s interest

from the interest of a stability of scheme that we want more individual

participation. Thus, I would urge the industry to shed this idea from their mind

that they are going to retail investor in order to fulfill what the regulator wants

or the government wants. They must go to the retail investor because that is

what they need. It is in their interest that retail investors have a larger portion

of their scheme.”

19

Mutual funds/ ULIPs and retail investors are like “made for each other”,

therefore, the poor participation of retail investors in them is a curious and

surprising phenomenon. It contradicts the theory underlying these products.

In marketing, when a quality product or service is not able to reach the consumers

then the onus is on marketing mix elements other than product. Distribution

intermediaries act as a link between manufacturer of the product i.e. mutual fund /

insurance company in our case and the investor. There are diverse set of Mutual fund /

ULIP distribution Intermediaries like individual agents, corporate agents, brokers,

distribution houses, banks, non-banking financial companies (NBFCs). The scenario

in which distribution intermediaries are working is rapidly changing. These changes

are spelled out as below: -

1) Changing Indian investors - Changing socio - economic environment

paves way for more demanding investors. New work culture, and growing

number of working couples created need of convenient, quick and doorstep

delivery of financial services. Disposable income of Indian middle class has

increased due to rise in salary levels of both public (especially after sixth pay

commission) as well as corporate sector employees. This makes the task MF

distribution intermediaries more important and challenging.

2) Changing Regulatory framework – Currently, regulators are making

stricter regulations for mutual fund industry. AMFI (Association of mutual

funds in India) has taken the initiative for developing a cadre of trained

professional intermediaries. AMFI launched the certification programme in

association with NSE’s Certification in Financial Markets (NCFM) in July

2000. SEBI has made AMFI Certification compulsory in a phased manner.

Regulators want to bring element of advice while selling financial products.

3) Increased use of technology in financial services - In addition to tough

regulatory environment, technological changes are also affecting the Indian

mutual fund / ULIP distribution. Today Information Technology has changed

the nature of financial markets and financial transactions. The pace and reach

of change are unlikely to slowdown in the foreseeable future. Banks and

capital markets are forerunner in adopting technology. Technologies such as

smart cards, bank accounts with biometric identification, mobile ATMs,

electronic payments networks, branchless banking services through mobile

phones, telephone are making financial inclusion possible. These technologies

20

are helping financial services organization to penetrate deep in the market. In

near future, may be technology will bring new ways of MF distribution.

Distribution Intermediation itself has undergone a change over the past few decades.

Mutual fund / ULIP distribution business has been going through lot of changes.

Rather, researcher is observing new distribution paradigm in Indian mutual fund /

insurance industry. Just look at the two statements made by industry insiders.

Jaideep Bhattacharya, chief marketing officer of UTI Asset Management Co.

Ltd. spoke during MF summit 2009 “It’s a new environment. People (Mutual

fund distribution intermediaries) will have to move from distribution to

advisory model,”

Mr. Avinash Ramnath, national sales head of Canara Robeco Asset

Management Ltd. said in same event “The writing is on the wall. The onus is

on the distributors to create an ownership of customers by improving the

quality of services. Platforms can be one way of doing it,”

As per the report titled “Asset management outlook in India”33

by Indian Chamber of

commerce & Ernst & Young in 2008, 90 percent executives working in the industry

kept distribution on their agenda for the next two years.

Though the industry is recognizing significance of distribution, but recent articles

written in print media and various discussions taking place in electronic media about

rampant “mis-selling” of mutual fund, insurance products (especially unit linked

insurance products) and other financial services compel the researcher to enquire

more. Again, the cost of financial services distribution is enormous as Indian investor

pays large amount of money to intermediaries under various heads such as fee,

commission or expenses, either directly or indirectly. Just to buttress this fact, as per

IRDA Annual Report 2007 -0834

, Indian insurance industry had paid whooping INR

14704 crore as a commission to distribution intermediaries. Even, Mutual Fund

industry pays around 2 percent as a commission to their intermediaries.

Are our investors getting back something from distribution intermediaries? If yes,

then what and how much? Are these commissions justified in terms of what they offer

to retail investors? This entire context has made researcher more curious. This has

further enticed researcher to undertake research study with following research

problem.

What is the present role of mutual fund intermediaries & what will be the role

in near future in the backdrop of changing environment?

21

1.7 Significance of the Study

Mutual Fund Company acts as non bank financial company and fund lot of business

activities. Mutual fund companies are important institutional investors as they are

pooling money from both retail and corporate savers to form capital for business

activities. Our study endeavors to help mutual fund industry to spruce up their

distribution channels. This will make mutual fund industry stronger. This is good

news for those businesses that depends on MF companies as a funding source.

Again mutual fund being strong domestic institutional investors, their role in

corporate governance is large. Mutual fund companies being significant shareholder

can directly influence corporate decisions by voting against management at

shareholder meetings. Thus stronger mutual fund industry will be strong crusader for

corporate governance. Currently, our stock markets are mainly influenced by foreign

institutional investors (FIIs) as they bring lot of liquidity in the market. As our

markets more volatile (Refer Table 1.2), stronger MF industry will act as a buffer

against these FIIs and volatility in our stock markets may be reduced.

So anything which will help in making MF industry stronger does have spillover

effect on Indian corporate and stock markets.

Financial markets are integrating, lot of financial services are bundled together to

create convenience for customers. Even financial services distribution is also

integrated. More and more distribution intermediaries are involved in selling multiple

financial products. This means though our study is focused on MF distribution but its

result do have some sort of implications for other financial services also. As

mentioned earlier, pension reforms are ongoing and soon lot of pension products will

be introduced. This study will definitely useful for pension industry as pension

products are similar to mutual funds in terms of product composition and features.

Thus, this study is significant for Indian pension industry.

This study is significant from regulators’ perspective also. Lot of government bodies

and regulators like SEBI, AMFI, IRDA, and FPSB are working towards investor

education, investor protection or rather investor empowerment per se. This study will

also give vital cues for further research in this regard.

Lot of economists like Adam Smith, David Ricardo, J. S. Mill, Keynes recognized the

causal nexus between income, saving, investment and economic development and

growth of the nation even from earlier times. Our study is focused on household

22

savings towards mutual funds. Indirectly, this study becomes significant from

economic development of our country.

In a nutshell this study does have larger ramifications for retail investors, corporate

companies, stock markets, regulators & policy makers.

1.8 Chapter scheme

The study comprises of seven chapters. Apart from background or overview of the

problem, Chapter I outline research problem, its significance. Chapter II will focus

distribution intermediaries prevailing in global as well as Indian markets. Research

methods and methodology will be spelled out in Chapter III. Chapter IV analyzes the

data while Chapter V will summarize the main findings and will offer some

suggestions also.

23

References:

1) Mohan, Rakesh (2008), “Growth Record of the Indian Economy, 1950-2008: A Story of

Sustained Savings and Investment”, Based on the keynote address at the conference on

“Growth and Macroeconomic Issues and Challenges in India” organized by the Institute of

Economic Growth, New Delhi, on February 14, 2008 also published Economic & Political

Weekly, May 2008, pp. 61-71

2) Mehra, Rajnish (2006), The Equity Premium in India. In Kaushik Basu (Ed.), The oxford

Companion to Economics in India, New Delhi: Oxford University Press.

3) Reserve Bank of India (2008), Annual Report, Mumbai

4) Society of Capital Market Research & Development (2004), Indian household investor’s

survey – 2004, New Delhi : Author

5) Association of Mutual Funds in India (2008), The investor’s concise guide – Making mutual funds work for you (3rd Edition), Mumbai : Author

6) Rao, D. N. & Rao, S. B., (2009), “Can Balanced and Income Mutual Funds Outperform the

Stock Market? An Empirical Study in the Indian Context” Retrieved March 23, 2011, from

SSRN: http://ssrn.com/abstract=1367032

7) Baid, Rachana (2007), “Mutual Funds Products & services” New Delhi: Taxmann

Publications Pvt. Ltd.

8) Rouwenhorst, K. G., (2004), “The origins of Mutual Fund”, In William N. Goetzmann and

K.Geert Rouwenhorst (Ed,), Origins of Value - The Financial Innovations that Created

Modern Capital Markets, New York : Oxford University Press

9) Fernando, Deepthi; Klapper, Leora; Sulla, Víctor Sulla & Vittas Dimitri (2003), “The

Global Growth of Mutual Funds”, World Bank Policy Research Working Paper 3055, The

world Bank Development Research Group Finance 10) Kamiyama, Tetsuya (2007), “India's Mutual Fund Industry”, Nomura Capital Market

Review Vol.10 No.4, pp 58 – 72.

11) Agrawal, Deepak (2011),“Measuring Performance of Indian Mutual funds”, Finance India ,

June 2011, Electronic copy available at: http://ssrn.com/abstract=1311761

12) Mitra, Anupam (2009), “Mutual funds– are they for mutual benefit?”, NSE Newsletter, Sept

2009

13) Acharya, D & Sidana, Gajendra (2007), “Classifying Mutual Funds in India: some results

from clustering”, Indian journal of business & economics, Vol. 6, No.1, 2007, pp 71-79

14) Kumar, Raj & Sharma Priyanka (2009), “Mutual funds: expanding horizons”, SCMS

Journal of Indian Management, January - March, 2009, pp 100 – 118

15) “History of Indian Mutual Fund industry” (n.d.) retrieved July 11, 2009, from http://www.amfiindia.com

16) Macko, Willam & Sourrouille, Diego (2010), “Investment Funds in MENA”, Financial

Flagship series of World Bank, Retrieved from

http://siteresources.worldbank.org/INTMNAREGTOPPOVRED/Resources/MENAFlagshipM

utualFund12_20_10s.pdf

17) Rao, P. H., & Mishra, V. K, (2007), “MUTUAL FUND: A RESOURCE MOBILIZER IN

FINANCIAL MARKET”, Vidyasagar University Journal of Commerce, Vol. 12, March 2007,

pp 109 -115

18) Berghe, Van den; Verweire, K; Carchon, S.W.M. (1999), “Convergence in the financial

service industry”, Tokyo : OECD 19) Kist, Ewald (2001), “Integrated Financial services – A framework for success: synergies in

insurance, banking, and asset management”, The Geneva papers on risk and insurance Vol.

26, No. 3, pp 311 – 322.

20) Walter, Ingo (1999) “The Asset Management Industry in Europe: Competitive Structure

and Performance under EMU” In Jean Dermine & Pierre Hillion (Eds.) European Capital

Markets with a Single Currency, Oxford: Oxford University Press

21) ibid

22) Keswani, Aneel & Stolin, David (2010), “Investor reaction to past performance : Evidence

from UK distribution channels”, retrieved on January 12 2011, from

http://www.cassknowledge.com/sites/default/files/article-

attachments/482~~aneel_kewani_investor_reaction_to_mutual_fund_performance.pdf

23) Chakrabarti Rajesh (2009), “Asset Management Industry In India” retrieved on April 23, 2009, from http://ssrn.com/abstract=1428473

24

24) Das, Bhagaban; Mohanty, Sangeeta and Shil, N.C., (2008) “Mutual Fund vs. Life

Insurance: Behavioral Analysis of Retail Investors”, International Journal of Business and

Management, Vol. 3, No. 10, pp 89-103

25) Korivi, Sunder Ram & Venkatesh, B.S., (2007), “Life-style Wraps: Cost-efficient

Alternative to ULIPs”, Proceedings of 11th APRIA Conference, Taipei : National Chengchi

University 26) Insurance Regulatory Development Authority (2008), IRDA Annual Report 2007 – 08,

Hyderabad : Author

27) Higher exit load in mutual fund with insurance (2008), retrieved March 21, 2010, from

http://www.business-standard.com/india/news/higher-exit-load-in-mutual

fundinsurance/327901/

28) Product Details (2008), retrieved December 11, 2008, from

http://www.sbimf.com/Product_Details.asp?ProductId=27

29) Anand, Abhishek; Verma, Shruti & Khare, (2009), Fund schemes with insurance cover a

big draw for investors, retrieved March 21, 2010, from http://www.mydigitalfc.com/mutual-

funds/fund-schemes-insurance-cover-a-big-draw-investors-827

30) Rao,C.S.,(2007), “Indian Insurance Industry Since 2000 – A Remarkable Journey”, A.D.

Shroff Memorial Lecture on 10th August, 2007 at Bombay House Auditorium, Mumbai 31) Securities Exchange Board of India (2009), “Annual Report 2008-09”, Mumbai : Author

32) ibid

33) Ernst & Young (2008), “Asset management outlook in India”, Mumbai : Author

34) Ibid

35) Kotler, Keller. (2005). Marketing Management (12th ed.). New Delhi: Prentice Hall India

Private Limited

36) Pune per capita income higher than India's (2008), Retrieved October, 11, 2011, from

http://articles.timesofindia.indiatimes.com/2008-08-05/pune/27945189_1_esr-capita-income-

pune-district

25

CHAPTER II

MUTUAL FUND / INSURANCE

DISTRIBUTION

INTERMEDIARIES

& RETAIL INVESTORS

26

2.1 Importance of distribution channels for Financial Services

The financial services refer to services provided by the financial industry. Thus the

financial industry comprises of a broad range of organizations that deal with the

management of money. Among these organizations are banks, insurance companies,

consumer finance companies, investment funds and stock broking companies.

Lovelock (1983)1 classified services based on various criterions like nature of service

acts, who receives the service, nature of service delivery, type of relationship, need

for customization, need for judgment by customer contact staff, demand – supply

fluctuations, availability of service outlet, customer – service provider interaction.

Researcher applied these bases to financial services and the scenario emerged is as

follows: -

- Financial services are intangible and they are directed towards things.

- Continuous nature of service delivery.

- Formal relationship between service provider and customer

- High level of customization is needed.

- High level of judgment is needed from customer contact staff

- Low demand fluctuations. Demand is met without major delay.

- Service availability at multiple outlets

- Mainly organization comes to customer but increasingly even customer

goes to organization. Due to technology both i.e. buyer and seller transact

at arm’s length.

These all characteristics of financial services make distribution channels very

significant. Mutual funds and insurance are those modern financial services which

are needed by corporate as well as retail customers. This entire chapter will portray

various retail distribution channels prevailing in both insurance and mutual fund

industry.

2.2 Mutual Fund / Insurance Distribution Channels worldwide

There are wide differences across the countries in terms of how mutual funds are

distributed. Let us start with mutual fund distribution channels prevalent in USA.

Mutual Fund distribution structure prevailing in USA is well described in various

literatures. An official source for classifying Mutual Fund distribution intermediaries

27

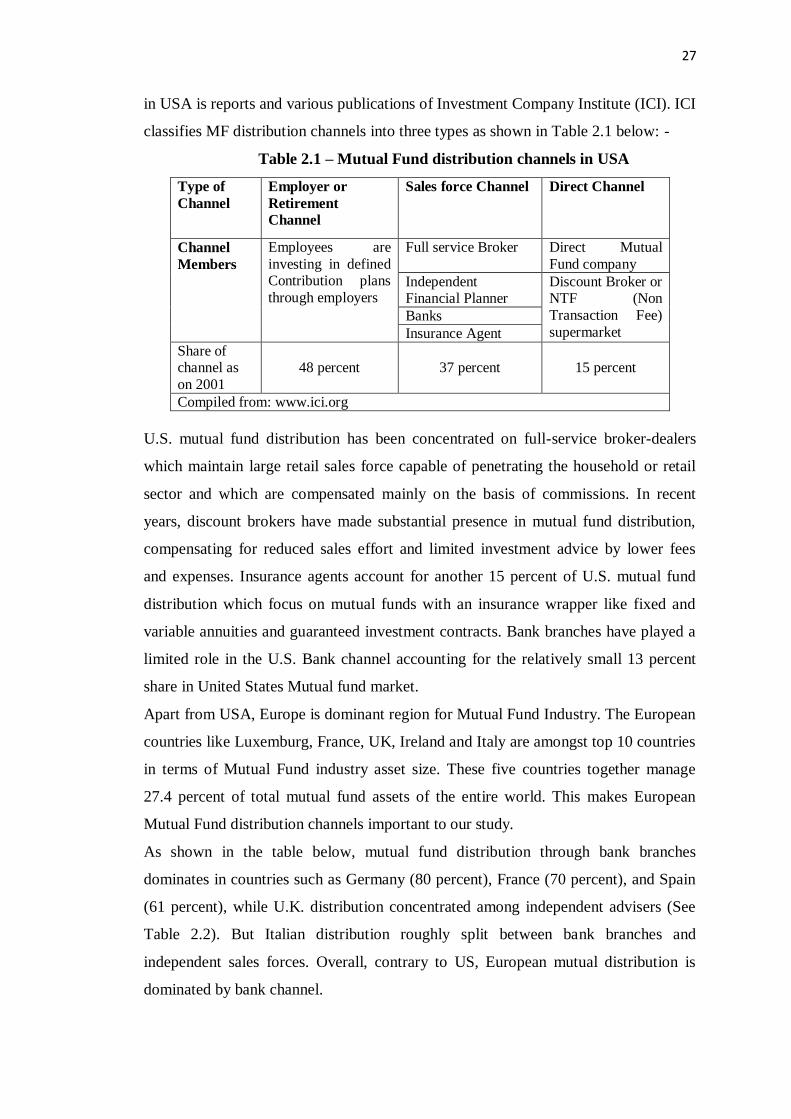

in USA is reports and various publications of Investment Company Institute (ICI). ICI

classifies MF distribution channels into three types as shown in Table 2.1 below: -

Table 2.1 – Mutual Fund distribution channels in USA

Type of

Channel

Employer or

Retirement

Channel

Sales force Channel Direct Channel

Channel

Members

Employees are

investing in defined Contribution plans

through employers

Full service Broker Direct Mutual

Fund company

Independent Financial Planner

Discount Broker or NTF (Non

Transaction Fee)

supermarket Banks

Insurance Agent

Share of channel as

on 2001

48 percent 37 percent 15 percent

Compiled from: www.ici.org

U.S. mutual fund distribution has been concentrated on full-service broker-dealers

which maintain large retail sales force capable of penetrating the household or retail

sector and which are compensated mainly on the basis of commissions. In recent

years, discount brokers have made substantial presence in mutual fund distribution,

compensating for reduced sales effort and limited investment advice by lower fees

and expenses. Insurance agents account for another 15 percent of U.S. mutual fund

distribution which focus on mutual funds with an insurance wrapper like fixed and

variable annuities and guaranteed investment contracts. Bank branches have played a

limited role in the U.S. Bank channel accounting for the relatively small 13 percent

share in United States Mutual fund market.

Apart from USA, Europe is dominant region for Mutual Fund Industry. The European

countries like Luxemburg, France, UK, Ireland and Italy are amongst top 10 countries

in terms of Mutual Fund industry asset size. These five countries together manage

27.4 percent of total mutual fund assets of the entire world. This makes European

Mutual Fund distribution channels important to our study.

As shown in the table below, mutual fund distribution through bank branches

dominates in countries such as Germany (80 percent), France (70 percent), and Spain

(61 percent), while U.K. distribution concentrated among independent advisers (See

Table 2.2). But Italian distribution roughly split between bank branches and

independent sales forces. Overall, contrary to US, European mutual distribution is

dominated by bank channel.

28

Table 2.2 – Share of various Mutual Fund /Insurance distribution channels in

European Union

USA Germany United

Kingdom France Italy Spain

Bank 8 80 10 70 43 71

Full service brokers 31.2

Dedicated Sales Force 25

Independent Sales force 20.3 14 50 44.1

Discount Brokers 8.6 6

Direct Channels 31.9 15 1.1

Others 30 11.8 29

Compiled from: Ingo Walter (1999)2 “The Asset Management Industry in Europe:

Competitive Structure and Performance Under EMU”

A closer look at United Kingdom shows that Investment Management Association

(IMA) disaggregates Mutual Fund (referred as Unit Trusts) flow data by investor type

and distribution channel into the seven Categories. From retail investor’s perspective,

IMA classifies distribution channels into four types.

1) Direct investment from Mutual Fund Company

2) Independent Financial Advisor;

3) Tied sales force;

4) Private clients - refers to portfolio management services offered by banks,

stockbrokers and law firms

The table 2.3 below describes each channel in detail.

Table 2.3 – Mutual Fund distribution prevalent in United Kingdom

Channel Description

Direct

investment

All sales and repurchases where the unit holder places the deal directly with the

Mutual fund company. This type of business is likely to arise as a result of "off

the page" advertising, direct mail-shots or spontaneous customer response to

newspaper editorial coverage or fund performance rankings.

Independent

Financial

Advisor

All sales and repurchases of unit trusts where the order is placed through an

Independent Financial Adviser / Intermediary. Such advisers will normally be

members of a recognized professional body

Tied sales force

All sales and repurchases of units in question where the order is placed through a company's Direct Sales Force or tied agents. It is important to remember that tied

agents could, for instance, include a bank or building society branch selling units

on behalf of a unit trust management company from a different parent group.

Private clients All sales and repurchases of units arising as a result of orders from an in-house

private client discretionary portfolio management service. . These could be

execution-only or advisory services, or they could even take the form of

discretionary services whereby the provider may trade on behalf of the individual

investor.

29

Aslam, John (2010)3 has classified Mutual fund distribution channel as a direct &

indirect distribution channel. Lakshmikutty Sreedevi and Baskar Sridharan (2003)4

also observed distinction of channels in the developed markets as personal

distribution systems and direct response systems. Personal distribution systems

include all channels like agencies of different models and brokerages, bancassurance,

and work site marketing. Direct response distribution systems are the method

whereby the client purchases the insurance directly. This segment, which utilizes

various media such as the Internet, telemarketing, direct mail, call centers, etc., is just

beginning to grow.

In a nutshell, when it comes to insurance distribution channels one-size does not fit all

Dumm & Hoyt (2002)

5. Multiple distribution channels are the key feature of

insurance as well as mutual fund distribution.

2.3 Mutual Fund / Insurance Distribution Channels in India

Categorizing distributions channels in India is a difficult task, in particular given the

relatively poor disclosure by AMFI & SEBI of distribution activity in the mutual fund

as well as life insurance industry (as compared with disclosure of performance data).

Daniel Bergstresser, et al (2004)6 has also encountered with this problem while

conducting study on Mutual Fund industry in USA.

As per IRDA, Insurance (ULIPs) products are sold in India through various channels

like agents, corporate agents (including banks), brokers, referral & direct channels. As

per AMFI, mutual fund distribution channels are classified as corporate agents

(including banks) and individual agents. As far as direct channels are concerned,

mutual fund companies are exploring various ways to reach directly. Direct channels

like mutual fund company’s offices, websites, telephone, mobile, ATM kiosks are

evolved in the recent past. All these channels and channel intermediaries are common

for both insurance (ULIPs) and mutual funds. Again distribution structure is changing

and embracing newer and newer ideas increasingly. Both the industries are observing

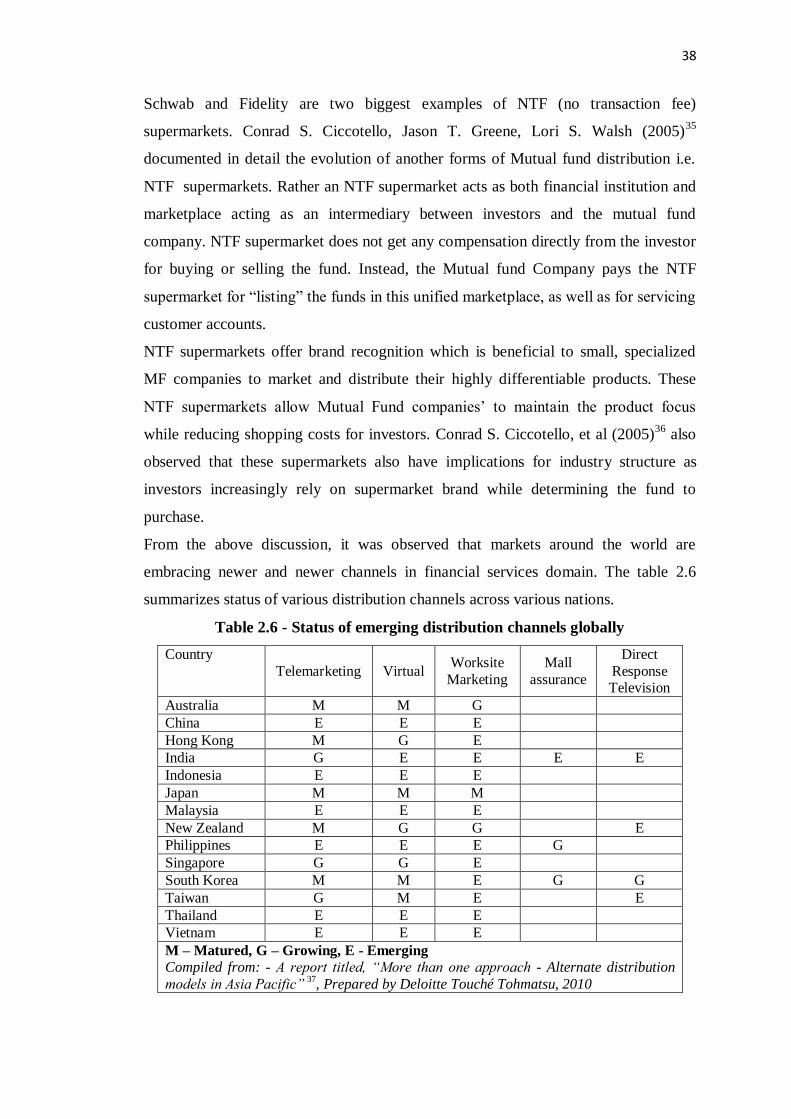

emergence of innovative distribution channels. A prominent channel has emerged in

the form of banks. Both AMFI and IRDA do not report data separately for the bank.

They have included banks as a corporate channel.

As researcher has already discussed how bank as a distribution channel is evolving

worldwide. This phenomenon is gaining its importance in India also. Karunagaran

(2006)7 concludes that going by the present pace, bancassurance would turn out to be

30

a norm rather than an exception in future in India and it would be a ‘win-win

situation’ for all the parties involved - the customer, the insurance companies and the

banks. Syed Shahabuddin (2008)8 bank channel has slowly realized its own potential

and is now emerging as a big player for mutual fund industry. Considering this, one

should accord bank as a separate distribution channel.

In a nutshell, need for multiple distribution channels is obvious for both Mutual funds

and ULIPs as low level of penetration of both the products, diverse needs of

customers, low level of awareness amongst the customers, increasing number

customers emphasizing service.

But the way Distribution intermediaries as classified by the regulators are increasingly

becoming obsolete as newer and newer distribution channels are emerging.

In this dynamic set up, researcher would classify Mutual Fund distribution

intermediaries for the purpose of study as below: -

1) Individual Mutual Fund agents / Individual financial advisor / Brokers.

2) Institutional or Corporate Agents (Group of people working together as a

company or partnership firm, Mutual fund branch offices, National or

regional level organizations operating through branches, Distribution

houses, etc)

3) Banks.

4) Emerging distribution intermediaries (all those channels which are not

covered by Sr. No. 1, 2, 3)

After classifying Mutual Fund / Insurance distribution intermediaries in India,

researcher will now define the term “Retail investors” in next section.

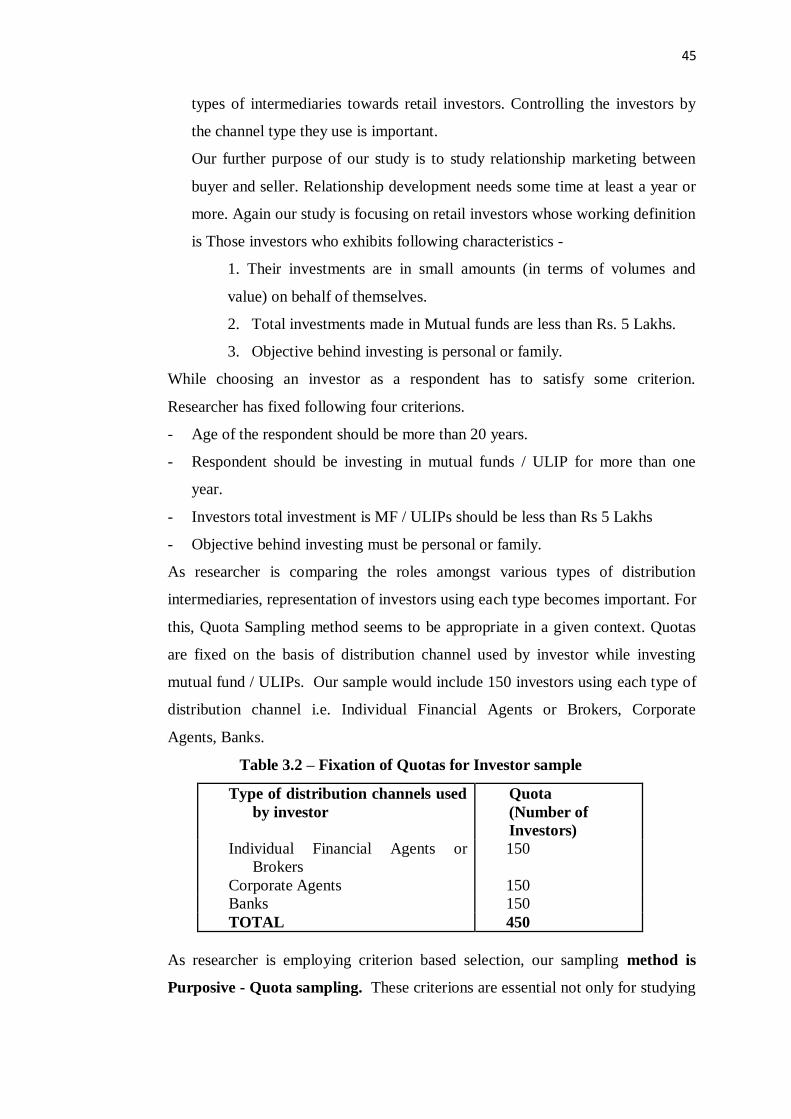

2.4 Definition of Retail Investors

Retail investors are referred in various ways like non institutional investors, small

investors, individual investors, non professional investors, household investors.

Stefan Bender (2006)9 a retail investor is an individual who buys and sells securities

for their own behalf not for an organization. Retail investors (non-professional

investors) typically trade in much smaller quantities than institutional investors. Retail

customers define the end of the distribution chain.

AMFI reports mutual fund folio data periodically in which data is shown for three

types of investors i.e. corporate or institutional investors, HNI (High Net worth

Individuals), Individual (small / retail) investors. AMFI terms those individuals whose

mutual fund portfolio is more than Rs. 5 Lakhs as HNI (High Net worth Individuals).

31

From this, researcher can make out that retail mutual fund investors those investors

who invest less than Rs. 5 Lakhs in mutual funds & other similar products.

In a nutshell, retail investors are those investors who exhibits following

characteristics; -

1) Their investments are in small amounts (in terms of volumes and value)

on behalf of themselves.

2) Total investments made in Mutual funds are less than Rs. 5 Lakhs.

3) Objectives behind investing are personal or family.

2.5 Role of Mutual Fund distribution intermediaries in relation to retail investors

Taking a leaf from previous subsection one can easily classify these distribution

channels into direct and indirect channels. Indirect channels include independent

financial planners, Individual financial agents (IFAs), banks, tied agents, brokers.

Direct channels will be Mutual Fund Company itself, NTF supermarkets, etc.

In India, indirect channels (comprising individual agents, corporate agents including

banks) are the dominant channels but a lot of direct channels are emerging. Mutual

fund investors prefer indirect channel as against the direct ones. Globally, in most of

the countries investors initially use indirect channels and then slowly shifted towards

the direct channels. Even today, in the sophisticated markets like USA investors

prefer indirect as against direct channels.

John Aslam (2008)10

further studied possible reasons behind Mutual Fund investor’s

propensity to engage financial advisors and found that behavioral influences as well

as knowledge plays vital role. These influences are tabulated (Table 2.4) as follows: -

Table 2.4 – Influences for engaging advisor while purchasing Mutual Funds

Behavioral Influences Knowledge Influences

1) Investor desire for convenience rather than

low cost in fund investing; 2) Influence of fund and distributor advertising

and marketing on the investor;

3) Investor feelings of inertia rather than action;

4) Investor feels the need to combine financial

services “under one roof”

5) Investor has feelings of insecurity rather than

confidence;

6) Investor feels the need to validate fund

decisions before transacting;

7) Investor feels the need for a referee in

spousal disagreements over investing and

money; 8) Investor tries to time the market, especially

short term;

1) Investor is a novice rather than

experienced fund investor; 2) Investor has proven inability to select

high-performing funds;

3) Investor has a lack of knowledge of

and/or appropriate education in fund

investing;

4) Investor has inadequate time to do the

necessary “homework” prior to

transacting; and

5) Investor has certain knowledge of

advisor who is a successful investor to

manage his/her fund investments.

Compiled from – John Aslam (2008)9

32

In short, investors engage advisor for variety of reason like convenience, inertia, non

confidence, indecisiveness, inability, lack of knowledge, advisors’ advertising and

marketing, advisors past performance, lack of time, etc. Many of these reasons are

relatable with Indian retail investors. Victoria Leonard and Michael Bogdan (2007)11

also found two prominent reasons behind using advisors one is investment and

planning services offered by them and other is advisor’s expertise.

To explain the role of Mutual Fund distribution intermediaries in India, researcher has

to go through the fine print of the guidelines given by insurance as well as mutual

fund regulators. Association of Mutual funds in India (AMFI) made a comprehensive

guidelines and the code of conduct so that all those engaged in the business of selling

and marketing of mutual fund schemes follow professional, healthy and best practices

for the sustained benefit of all concerned – investors, intermediaries and the Mutual

Fund Industry as a whole.

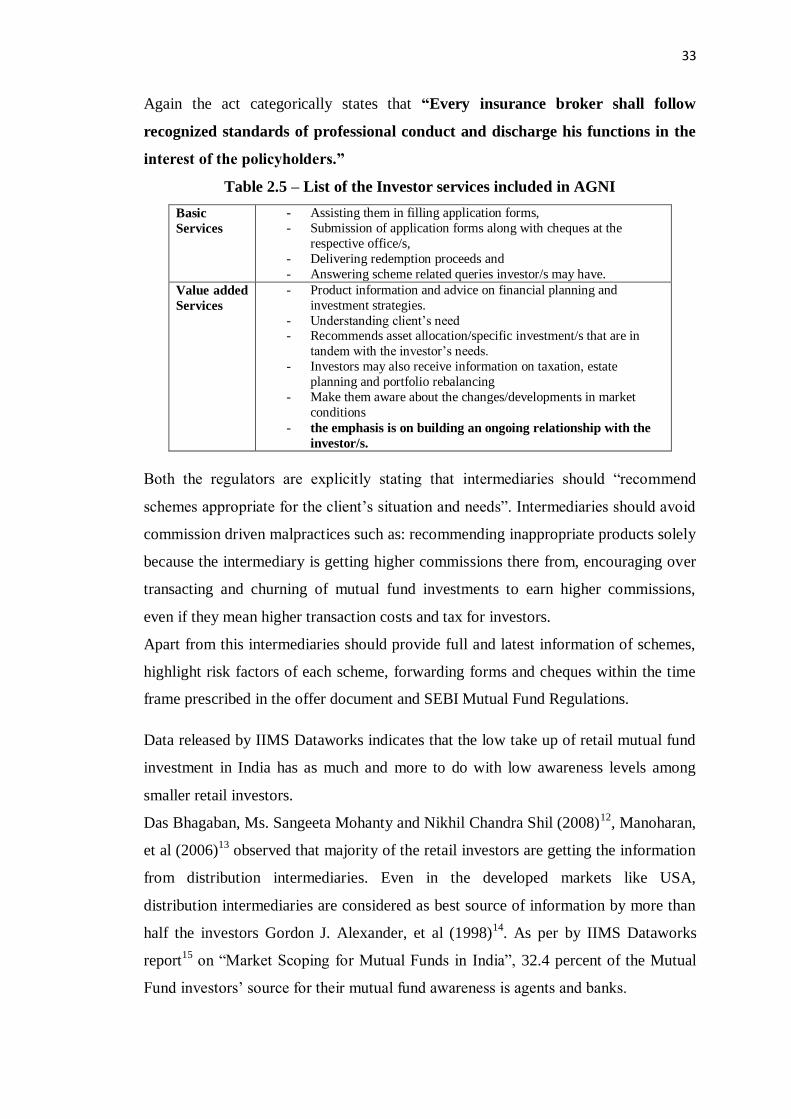

AGNI endorses that investors are diverse in terms of their needs; they can broadly be

classified in three categories:-

(i) Those who want product information, advice on financial planning and

investment strategies.

(ii) Those who require only a basic level of service and execution support i.e.

delivering and collecting application forms and cheques, and other basic

paperwork and post sale activities.

(iii) Those prefer to do it all themselves, including choice of investments as

well as the process/paperwork related to investments.

To cater these investors AGNI has listed two types of services an intermediary

should offer to their investors (See Table 2.5).

The cardinal principle of AGNI is “ensuring that the clients’ interest is

protected”.

As per our definition mutual funds includes Unit Linked insurance products, it will be

essential to study the regulation in relation to it. IRDA has stated these guidelines

under two acts i.e. Insurance Regulatory and Development Authority (Licensing of

Insurance Agents) Regulations, 2000), IRDA (Insurance brokers) Regulations 2002.

IRDA (Insurance Brokers) Regulations, 2002 laid down the comprehensive guidelines

pertaining to client’s relationship, sales practices furnishing of information

explanation of insurance contract renewal of policies claim by client, documentation.

33

Again the act categorically states that “Every insurance broker shall follow

recognized standards of professional conduct and discharge his functions in the

interest of the policyholders.”

Table 2.5 – List of the Investor services included in AGNI

Basic

Services

- Assisting them in filling application forms,

- Submission of application forms along with cheques at the

respective office/s,

- Delivering redemption proceeds and

- Answering scheme related queries investor/s may have.

Value added

Services

- Product information and advice on financial planning and

investment strategies.

- Understanding client’s need - Recommends asset allocation/specific investment/s that are in

tandem with the investor’s needs.

- Investors may also receive information on taxation, estate

planning and portfolio rebalancing

- Make them aware about the changes/developments in market

conditions

- the emphasis is on building an ongoing relationship with the

investor/s.

Both the regulators are explicitly stating that intermediaries should “recommend

schemes appropriate for the client’s situation and needs”. Intermediaries should avoid

commission driven malpractices such as: recommending inappropriate products solely

because the intermediary is getting higher commissions there from, encouraging over

transacting and churning of mutual fund investments to earn higher commissions,

even if they mean higher transaction costs and tax for investors.

Apart from this intermediaries should provide full and latest information of schemes,

highlight risk factors of each scheme, forwarding forms and cheques within the time

frame prescribed in the offer document and SEBI Mutual Fund Regulations.

Data released by IIMS Dataworks indicates that the low take up of retail mutual fund

investment in India has as much and more to do with low awareness levels among

smaller retail investors.

Das Bhagaban, Ms. Sangeeta Mohanty and Nikhil Chandra Shil (2008)12

, Manoharan,

et al (2006)13

observed that majority of the retail investors are getting the information

from distribution intermediaries. Even in the developed markets like USA,

distribution intermediaries are considered as best source of information by more than

half the investors Gordon J. Alexander, et al (1998)14

. As per by IIMS Dataworks

report15

on “Market Scoping for Mutual Funds in India”, 32.4 percent of the Mutual

Fund investors’ source for their mutual fund awareness is agents and banks.

34

Considering that distribution intermediaries are regarded as prominent source of

information, they should ideally be responsible for investor education.

Summarizing the role of distribution intermediaries

After discussing what role mutual fund intermediaries are playing worldwide and

what role is expected by regulators in India. Now researcher would define the “the

role of mutual fund distribution intermediaries” which will be focused in the study.

Researcher will split the role of mutual fund distribution intermediaries into four

components. As the scope of each component is large, researcher has set boundaries

for each component as follows: -

1) Role of intermediaries in Educating Investors / Customers - Investor education

is very broad term, researcher limits it to whether basics of investing (risk,

return, liquidity, taxation) have been explained by the intermediary or not.

Apart from this, researcher will study investors’ overall perception towards

education by intermediaries.

2) Role towards Building Relationships & Creating Loyalty – Researcher will

study perceived relationship strength and the level of loyalty towards

intermediaries. Researcher will study various relationship marketing factors

and will explore the basis of relationship development.

3) Role as a Service Provider – Apart from understanding the need hierarchy of

investors’, researcher will also study the nature of services i.e. basic /

transactional, advisory and information offered to the investor by the

intermediaries.

4) Role as Value Creator – Value is core element of any service. Value is also

one of the three pillars of relationship marketing. Researcher would explore

how these intermediaries are adding the value? What are the value additions

these intermediaries are making?

2.6 Understanding retail investors

Researcher found numerous research pertaining to behavior of mutual fund investors

like Dorn Daniel, Huberman G (2005)16

; Kenneth A. Kim and John R. Nofsinger,