1

Chapter 11 : Agri-Food Sector (Alan Matthews)

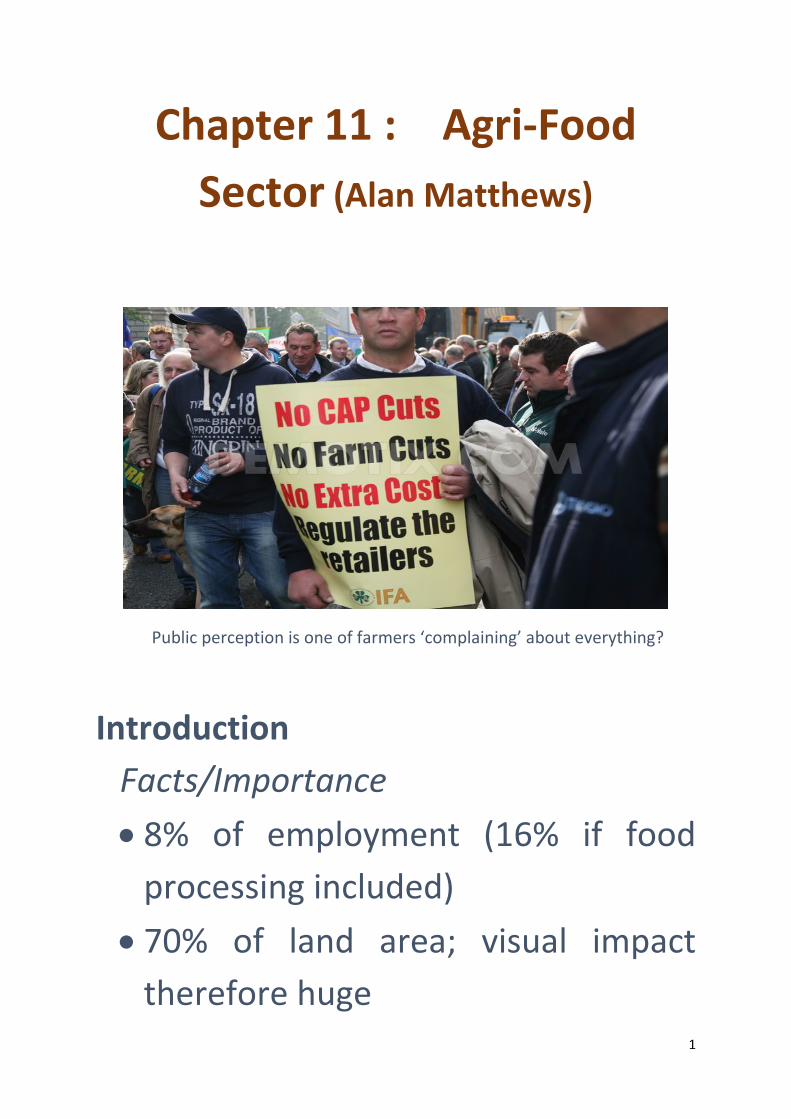

Public perception is one of farmers ‘complaining’ about everything?

Introduction

Facts/Importance • 8% of employment (16% if food

processing included) • 70% of land area; visual impact

therefore huge

2

• Exports: book at NET figures • Also R-based, implies not mobile • 30% of greenhouse gas emissions • food and drink: 18% of C • Huge government intervention;

regulation and subsidies • Central to WTO talks, environment

and health • Cannot exist without food and

water 2 Characteristics of Agricultural Sector

Unique Considerations (not in book) • Supply factors: disease, weather,

storage costs, and safety. Means

3

sudden and dramatic shifts in supply possible.

• Inelastic demand: cannot increase D by reducing price because those who can afford food reached limit of demand

• Large number of producers, implies weak bargaining power of farmers without strong farmer organisation

• Immobile factors of production: land has ‘cosmic’ attachment. Huge change for farmers to move to other job.

• Small shopkeeper analogy: market forces allowed to apply there.

• Anthony Hopkins, ‘Field’ and other stories.

4

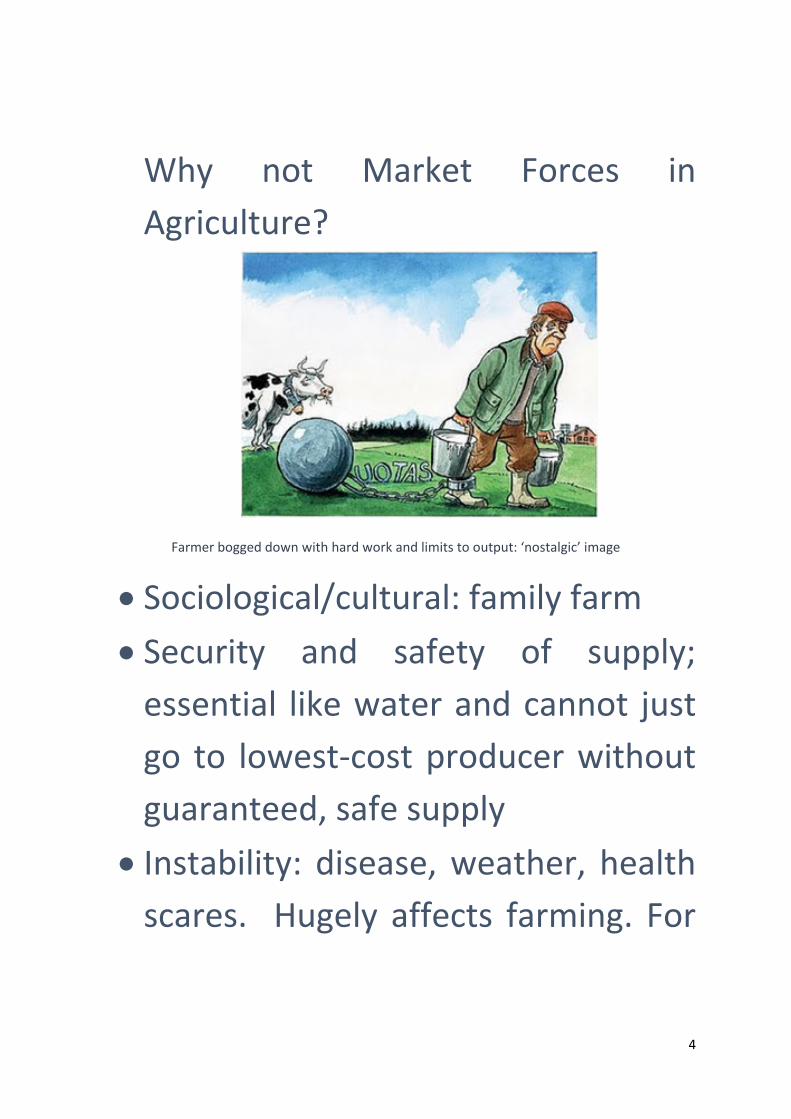

Why not Market Forces in Agriculture?

Farmer bogged down with hard work and limits to output: ‘nostalgic’ image

• Sociological/cultural: family farm • Security and safety of supply;

essential like water and cannot just go to lowest-cost producer without guaranteed, safe supply

• Instability: disease, weather, health scares. Hugely affects farming. For

5

example, flooding, drought, and so on.

Incomes/Production • 30% farm income from market: rest

subsidies • Emphasis on livestock, Table 11.1

(72% of total); beef and milk • Export orientation; 80% of beef and

dairy output rely on access to export markets

6

• Real price falling for 20 years • Volatility of prices a real problem;

huge swings and uncertainty that few other industries could cope with

• Much fewer produce same output; 20% farmers product 80% of output

• Number of farms falling steadily • Income from farming v farm

household income. Former accounts now for just 27% of latter

• Very uneven distribution of incomes in farming: destitute bachelor to very well-off farmers

• Wealth v income; farmers often rich in former and very poor in latter

7

3 Agricultural Policy Common Agricultural Policy (CAP)

• French/German ‘deal’ • Objectives:

- increased Q -fair standard of living - stabilize markets: weather, disease, health scare issues again - guarantee supply

8

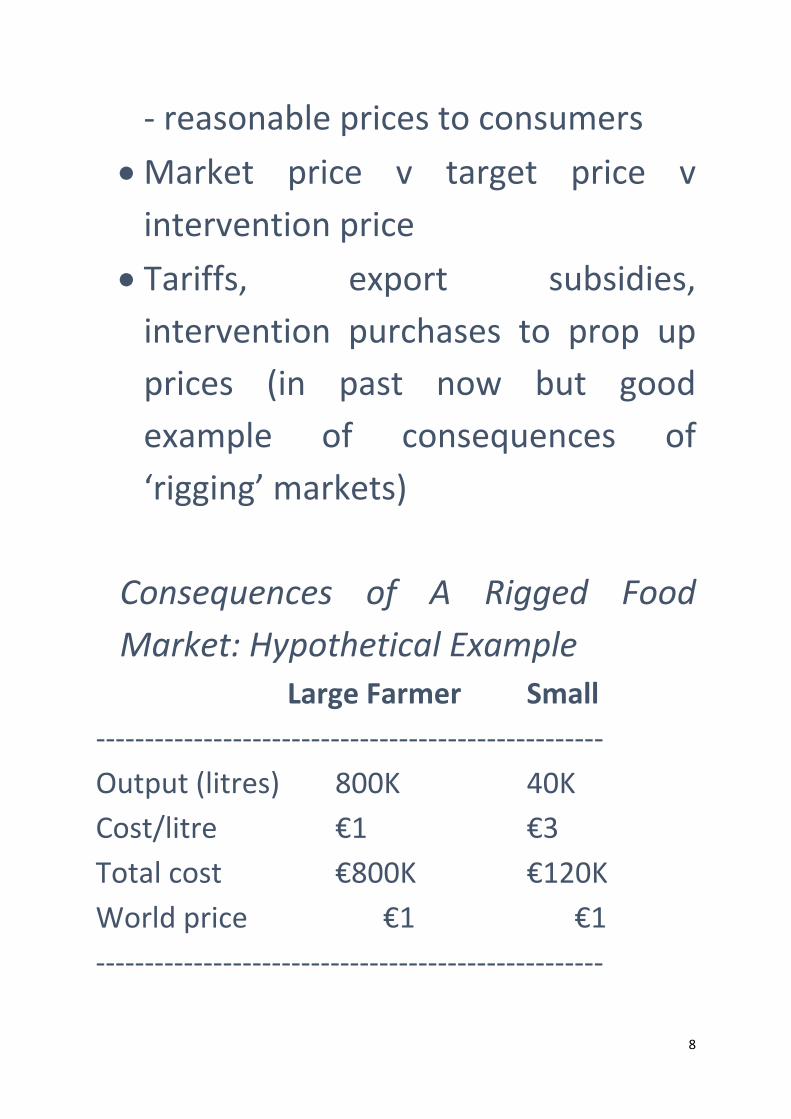

- reasonable prices to consumers • Market price v target price v

intervention price • Tariffs, export subsidies,

intervention purchases to prop up prices (in past now but good example of consequences of ‘rigging’ markets)

Consequences of A Rigged Food Market: Hypothetical Example

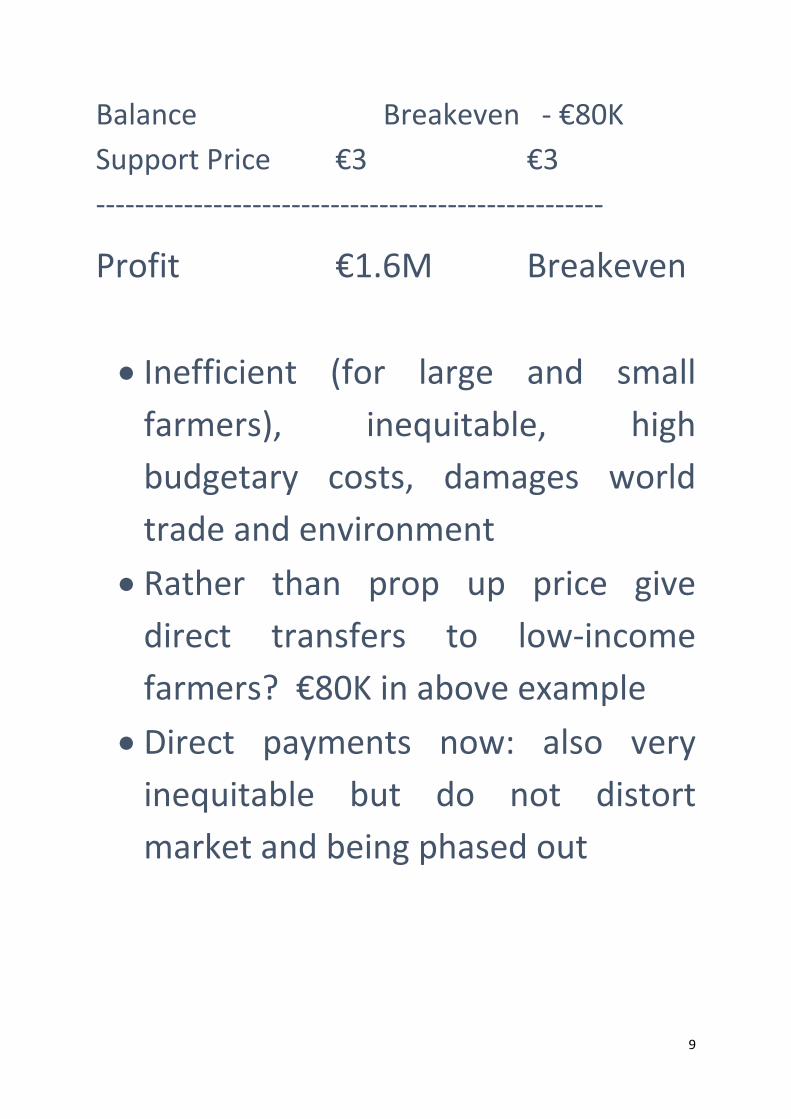

Large Farmer Small ---------------------------------------------------- Output (litres) 800K 40K Cost/litre €1 €3 Total cost €800K €120K World price €1 €1 ----------------------------------------------------

9

Balance Breakeven - €80K Support Price €3 €3 ----------------------------------------------------

Profit €1.6M Breakeven • Inefficient (for large and small

farmers), inequitable, high budgetary costs, damages world trade and environment

• Rather than prop up price give direct transfers to low-income farmers? €80K in above example

• Direct payments now: also very inequitable but do not distort market and being phased out

10

• Does world price take account of safety/health issues and sustainability though?

Reform of CAP • Mansholt 1968: recognised all of

problems of price support • McSharry (Irish Commissioner)

1992: introduced direct payments • EU enlargement : agreed in 1993

and happened in 2004: addition of 10 agricultural states changed dynamic

• Luxembourg Agreement 2003 - payments (de-coupled)

11

- ‘cross compliance’ - payments to be ‘modulated’ - rural development emphasis

• WTO and Doha Accord - US v EU (proposed EU/US trade

accord) • Ireland a substantial net gainer • Safety, reliability and sustainability:

new emphases • Energy from agriculture; e.g. wind,

biomass • CAP today and after 2013 • Changed in last 10 years

- Lower payments to some countries still

- Increased role of European Parliament

12

- Emphasis on rural development: small industry, forestry, sustaining rural communities

4 Food Processing and Distribution

Food Industry (food needs to be processed, treated, packaged and delivered) • Few products sold directly to

consumer; potatoes and strawberries mainly in summer or local markets

• For example milk: cow to farmer to creamery to wholesalers to retailers to customers

• Food industry value (Table 11.2): huge industry, e.g. Glanbia,

13

Greencore, Kerry Group, Danone, etc

Distribution • Wholesale franchisors • Retail sector; e.g Tesco, Supervalu,

Aldi, Lidl • Concentration of market power, in

both wholesale and retail sectors, the policy issue • Changing consumer lifestyles

14

- 50% of food in US consumed outside home, 30% here

- Easy to prepare food/take-away food

- Safety, health, ‘fair trade’ issues • Exports to UK: exchange rate issue

5 Food Policy Growing Concern over Food Safety

• Always a concern; e.g. water in 18th century, and indeed today

• Huge variety of issues

15

- diseased animals posing threat to human health (BSE and ‘bird flu’)

- to other animals (‘foot and mouth’ and ‘bird flu’)

- sanitary conditions for animals; e.g. battery hens, veal ‘story’

- labelling (e.g. horsemeat issue) - pesticides/hormone residues - food additives, e.g. to make

salmon pink - GM food, etc

• Can lead to drops in demand: e.g. listeria in soft cheeses, salmonella in eggs

• Obesity (the next health crisis after smoking)

16

• Not too little food (as 100 years ago, and much of world today) but too much and of wrong type the issues today

• Common eating areas (greater danger of rapid spread of viruses etc)

Economic Considerations • Need state agency for food safety • asymmetry of information

(customer cannot tell quality) • reputational issues, implies self

regulation? • danger of fatalities: irreversible

• Zero risk not possible: not just in eating but also ‘living’

17

• Perceived v actual risk: former all that matters for people

• Mass production : efficiency v safety. Farm of 2m cows maybe much more efficient but disease spread very difficult to control

EU Framework • New General Food Law 2002 • New legislation. Key Principles:

- whole food chain approach: ‘farm to fork’

- risk analysis: zero risk not possible - operator liability - enforcement

18

• New Food Safety Authority created (but will they ‘miss ball’ like banking regulators did)?

• Food quality the big issue now also

Irish Responses • Food Safety Authority 1999

Market Power in Food Chain

19

• Wholesalers • Supermarkets (top 3 account for 50

per cent of sales) • Farmer share of retail price • South v N Ireland comparison: lower

costs in former and economies of scale because part of large UK chains

6 Conclusions • See summary in book: time of major

change - EU budget (2014-2020) - WTO negotiations and proposed

US/EU trade deal - food safety - environmental issues and

sustainability

20

• Less price intervention but increased regulation

• Growth sector of future in Ireland?

• • Special access for Irish beef to US

and Russia, and lifting of milk quotes big boost

• Changing composition of food demand in China to more European patterns

• Also remember food industry is R based

21

Recommended