Central Bank Transparency and Independence:Updates and New Measures∗

N. Nergiz Dincera and Barry Eichengreenb

aTED University, Ankara, TurkeybUniversity of California, Berkeley

This paper reports updated measures of transparency andindependence for more than 100 central banks. The indicesshow that there has been steady movement in the direction ofgreater transparency and independence over time. In addition,we show that outcomes such as the variability of inflation aresignificantly affected by both central bank transparency andindependence. Disentangling the impact of the two dimensionsof central bank arrangements remains difficult, however.

JEL Codes: E0, E4, F0.

1. Introduction

In early 2012 the Federal Open Market Committee (FOMC) madeknown a decision to further increase the transparency of its monetarypolicy decisions.1 It announced a plan to publish the predictions ofmembers of the Board of Governors and Reserve Bank presidents ofthe level of short-term interest rates as well as having them describetheir views of the evolution of the Federal Reserve’s investment port-folio. The Federal Reserve already published their forecasts of infla-tion, unemployment, and growth. In taking this additional step, itwas following the central banks of New Zealand, Norway, and Swe-den, which have been publishing interest rate forecasts for years.More broadly, this decision to release interest rate forecasts and port-folio outlooks was another step in the trend toward greater central

∗The first author gratefully acknowledges financial support of TUBITAK(The Scientific and Technological Research Council of Turkey) under TUBITAK-BIDEP fellowship.

1The decision was contained in the minutes of the FOMC for December 2011,released on January 3, 2012.

189

190 International Journal of Central Banking March 2014

bank transparency that has not been limited to this small handfulof countries but has been under way globally for some years now.

This trend toward heightened transparency is a departure fromlong-standing central bank practice which valued confidentiality.Early central banks engaged in commercial banking business; theycloaked their lending decisions in secrecy in order to maintain anadvantage over their competitors and out of respect to their clients.As bankers to the government, they sought to avoid releasing embar-rassing information about the public finances. As they becamelenders of last resort, they sought to avoid undermining confidencein distressed financial institutions by husbanding information abouttheir emergency operations.

The rise of central bank transparency can be understood in anumber of related ways. First, it is part of a broader trend, respond-ing to popular pressure, to make government more responsive tothe public. In New Zealand, for example, the increase in centralbank transparency associated with the Reserve Bank Act of 1989,a parliamentary act that required the rationale for monetary policydecisions to be publicly disclosed, was part of a broader movementassociated with the Official Information Act of 1982 and effort of theLabour Government elected in 1984 to enhance the transparency andefficiency of government operations generally.

Second, transparency is seen as a key element of accountabil-ity in an era of central bank independence. As central banks havebecome more independent and freer to choose their tactics, trans-parency has come to be seen as a mechanism enabling the publicto assess whether the actions of central bankers are consistent withtheir mandate. Central bank independence is widely advocated asa means of insulating monetary from short-term political pressures;it is seen as an efficient means of addressing the time-consistencyproblems that plague discretionary policy.2 But “with independence,

2On these two arguments see Blinder (1998) and Rogoff (1985), respectively.Walsh (2003) emphasizes the importance of distinguishing two aspects of indepen-dence: insulation from politics when it comes to defining the objectives of mon-etary policy, and the independence to freely implement policy once those goalshave been defined. Grilli, Masciandaro, and Tabellini (1991), in an early, influ-ential article on this subject, called them political and economic independence,respectively. Debelle and Fischer (1994) refer to them as goal and instrumentindependence.

Vol. 10 No. 1 Central Bank Transparency and Independence 191

comes . . . responsibility,” as Siklos (2011, p. 929) puts it. “Democra-tic accountability for unelected officials and arm’s length institutionsnecessitates behavior that demonstrates sensitivity for the public’sneed to understand how policy is made.”3 Pressure for transparencyis more intense insofar as the mandate of central banks extendsbeyond the pursuit of easily quantifiable, independently verifiabletargets like the rate of inflation to encompass emergency lending,securities market intervention, and related financial operations. Inthe United States, for example, calls to audit the Federal Reservehave intensified as the central bank has come to rely more exten-sively on unconventional policies and expanded the range of its inter-ventions in securities markets. The FOMC’s decision to make moreinformation publicly available can thus be understood as an effort toreconcile the increased complexity of its operations with the desireto maintain and defend its independence.

Third, central bank transparency is seen as a way of enablingmarkets to respond more smoothly to policy decisions. When a cen-tral bank is more transparent about its economic outlook and abouthow that outlook is related to its policy stance, monetary policy deci-sions are less likely to come as a surprise. Investors are less likelyto be caught unawares by policy actions. Policy changes are lesslikely to cause sharp movements in asset prices that cause financialdistress.4

Fourth, transparency is a means of enhancing the credibility ofthe central bank’s commitments. A commitment to ensuring low

3There is also an argument that more independent central banks have greaterincentive to clearly communicate their policies (they will want to be more trans-parent) simply because they have more control over their own policies (Croweand Meade 2008).

4There is also the criticism that excessive transparency and informationends up confusing the markets. Clare and Cortenay (2001) argued that minutesrecounting contentious discussions among board members can heighten asset-price volatility and end up confusing investors. This is presumably why the Fed-eral Reserve trims officials’ forecasts before publishing them. It is presumablyone reason why the European Central Bank (ECB) continues to refuse to pub-lish its minutes and the votes and forecasts of board members. Mishkin (2004)similarly warns that a high degree of transparency could disrupt communicationwith the public, which might not easily understand that forecasts for the policyinstrument are conditional and which might misinterpret changes in the forecast(or deviations between forecast and realized rates) as the central bank renegingon its commitments.

192 International Journal of Central Banking March 2014

and stable inflation will be more convincing when the central bankexplains in detail how and why its policies are supposed to producethe desired inflation rate. In turn, that more credible commitmentgives the central bank more leeway to deviate from typical policysettings when atypical conditions arise, since it will be clear to thepublic that the deviation is temporary and not inconsistent withthe longer-run pursuit of the monetary policy target. Transparencyenhances not just policy credibility, in other words, but also policyflexibility.

It follows that transparency about policy is a way to manageexpectations, which can matter importantly for the effectiveness ofpolicy, in general but especially under exceptional conditions. Whilethe central bank sets certain short-term interest rates, the long-termrates on which, inter alia, fixed investment decisions depend are afunction of not just current short-term rates but also expected futureshort-term rates. Releasing forecasts of future rates, along with fore-casts of future economic conditions to make those future-rate fore-casts credible, is a way for the central bank to influence long-termrates and associated private-sector decisions. Announcements thatcreate expectations about future policy can be especially importantin periods when current policy is constrained. Thus, the FederalReserve, having cut current short-term interest rates to near zero,must now attempt to affect economic activity by creating expec-tations of low future short-term rates—by announcing that short-term rates will remain at current near-zero levels for some num-ber of quarters or years—thereby influencing the long-term rateson which the costs of borrowing for home purchases and corporatefixed investment depend. Publishing forecasts of future interest ratesand, more generally, providing more information about likely futurestance—becoming more transparent, in other words—is a means tothis end.

Understanding the extent of the trend, its motivations, and itsimplications requires measures of the transparency of central banks.In previous papers (Dincer and Eichengreen 2008, 2010) we have pro-vided estimates of the extent of transparency for central banks from1998 through 2006. Here we update those measures through 2010.We use the updated data to ask whether the trend toward greatercentral bank transparency has continued or instead plateaued, as

Vol. 10 No. 1 Central Bank Transparency and Independence 193

some have argued.5 This also allows us to ask how the global financialcrisis and central bank response affected the trend toward greatercentral bank transparency. The Federal Reserve’s response, as dis-cussed above, would suggest that the trend toward greater trans-parency should have been reinforced insofar as the crisis caused cen-tral banks to take unconventional and unprecedented actions. Butwhether the trend toward greater transparency is in fact general isan empirical question. We attempt to answer it below.

In this paper we also provide new measures of transparency fortwenty central banks, mainly those of emerging markets and devel-oped countries that we were not able to consider previously. Thisspeaks further to the question of whether the trend toward increasedcentral bank transparency is general. It helps to address the asser-tion, sometimes heard, that the trend toward greater transparencyis primarily an advanced-country phenomenon that is not equallyevident among central banks in developing economies.6

We also supplement our database with new measures of centralbank independence, building on the earlier empirical literature onthis subject. Transparency and independence are likely to be relatedattributes of central banks, as explained above. We consider theirrelationship in the analysis below.

Finally, with these new measures in hand, we reconsider thedeterminants of central bank transparency and its effects on, interalia, the dynamics of inflation.

2. Literature

An early landmark in the literature on central bank transparencyis Fry et al. (2000). A strength of the Fry et al. analysis is itswide country coverage, based on a Bank of England-administeredsurvey of ninety-four central banks. A limitation is its relativelycoarse definition of transparency. Fry et al. measured central banktransparency as an equally weighted average of three sub-indicators:whether the central bank provides prompt public explanations of itspolicy decisions; the frequency and form of forward-looking analysis

5See inter alia Siklos (2011).6 See the Crowe and Meade (2008) paper discussed below.

194 International Journal of Central Banking March 2014

provided to the public; and the frequency of bulletins, speeches, andresearch papers. Siklos (2002) then provided similar measures fortwenty OECD countries but again for only one point in time, thelate 1990s.

Eijffinger and Geraats (2006) distinguish more aspects of trans-parency and consider more than one point in time. Their indices, onwhich we build, distinguish political transparency (openness aboutpolicy objectives), economic transparency (openness about data,models, and forecasts), procedural transparency (openness aboutthe way decisions are made, achieved mainly through the release ofminutes and votes), policy transparency (openness about the policyimplications, achieved through prompt announcement and explana-tion of decisions), and operational transparency (openness aboutthe implementation of those decisions—in other words, about con-trol errors and macroeconomic disturbances affecting their magni-tude). They distinguish three sub-categories within each of these fivedimensions. Their overall index sums values across these five dimen-sions, each of which is in turn an equally weighted average of itssub-dimensions. The strength of this approach is its comprehensive,multi-dimensional definition of transparency; its limitation is thatEijffinger and Geraats construct it for just nine central banks—theReserve Bank of Australia, Bank of Canada, ECB, Bank of Japan,Reserve Bank of New Zealand, Swedish Riksbank, Swiss NationalBank, Bank of England, and Federal Reserve—and for five years(1998–2002).7 Their results point to sharp differences between moreand less transparent central banks, with the Reserve Bank of NewZealand, the Bank of England, and the Swedish Riksbank at the topin terms of transparency, and the Reserve Bank of Australia, theBank of Japan, and the Swiss National Bank at the bottom.8

7The index covers the period 1998–2002.8A related study is Bini-Smaghi and Gros (2001), who (like Eijffinger-Geraats)

consider fifteen aspects of central bank transparency. They implement their indexfor four central banks: the Federal Reserve, the Bank of England, the Bank ofJapan, and the ECB. De Haan, Amtembrink, and Waller (2004) develop a sim-ilar index for six countries. In an unpublished companion paper (De Haan andAmtembrink 2002), two of the authors apply a similar methodology to fifteencountries.

Vol. 10 No. 1 Central Bank Transparency and Independence 195

In the paper closest to ours, Crowe and Meade (2008) con-struct indices of both the transparency and independence of centralbanks. They report transparency in 1998 and 2006 using criteriasimilar to ours.9 Their measures of transparency cover thirty-sevencentral banks. Only among advanced countries do they find thattransparency rose significantly. There is no evidence of a systematicchange in emerging markets.10

To measure central bank independence, Crowe and Meade applythe criteria developed by Cukierman, Webb, and Neyapti (1992).First, a central bank is categorized as more independent if its head(the chief executive) is appointed by the board of the central bankand not by the prime minister or minister of finance, is not subjectto dismissal, and has a long term in office. These features of theappointment process are important for insulating the head of thecentral bank from political pressures. Second, independence is takenas greater when policy decisions are made without direct governmentinvolvement. Third, a central bank is classified as more independentif its charter states that price stability is the sole or primary goalof monetary policy. Finally, independence is greater when there arelimits on the ability of the government to borrow from the centralbank. The authors combine these four aspects into a single index ofindependence.

Crowe and Meade use information on central bank laws from adatabase held by the International Monetary Fund (IMF) to updatethe Cukierman et al. index. Their measure covering ninety-ninecountries in 2003 suggests that independence increased significantlyin the 1990s and continued to do so since the turn of the century.For developing and emerging economies, all components of the inde-pendence index rise significantly. In the advanced countries, how-ever, this is true only of the components capturing disputes withthe executive and lending to the government.11 Their regressionssuggest that the change in independence between the two periods is

9In some country cases, it would appear, their series end in years slightlyearlier than 2006 as a function of data availability.

10However, their data for the two years may not be directly comparable: whilethe 1998 data are self-reported—they come from the Bank of England surveyreported in Fry et al. (2000)—the 2006 data are constructed on the basis ofinformation gleaned from central bank publications and websites.

196 International Journal of Central Banking March 2014

a function of initial independence (with a negative coefficient, indi-cating that central banks that were already relatively independenthad less room for further improvement) and democracy (more checksand balances make society more amenable to delegation within thepolitical system). They find a larger increase in independence incountries with less flexible exchange rate regimes (a pegged exchangerate being an alternative to central bank independence as a way oflimiting political interference in the day-to-day conduct of monetarypolicy).

Crowe and Meade then regress the level of transparency in 2006on the level of central bank independence and a vector of controls.They find that independence affects transparency positively, as dothe flexibility of the exchange rate regime and measures of institu-tional quality.12

In Dincer and Eichengreen (2008, 2010) we provide indices oftransparency for 100 central banks from 1998 to 2005 and 2006,respectively. Siklos (2011) then updates these same transparencyindices through 2009. While finding that the degree of central banktransparency continued to rise outside the advanced countries andin Central and Eastern Europe in particular, we find little sign offurther increases in the Group of Seven countries and only a mod-est increase among developing and Asian countries. Siklos finds noimpact of the global financial crisis on trends in transparency inthese regions.

3. Trends and Determinants of Transparency

We draw our data from information on central banks’ websitesand statutes, annual reports, and other published documents.13 We

11This may reflect the fact that the other components relating to the appoint-ment of the central bank head and existence of a codified objective for monetarypolicy were already at high levels, having increased previously.

12An explanation for the exchange rate result is that flexible exchange ratestend to be associated with more transparent monetary policy strategies like infla-tion targeting. The positive association of transparency with independence plau-sibly reflects the role of the former as an accountability mechanism for centralbanks otherwise insulated from the political system.

13We draw our data in this manner rather than sending a survey instrument tothe central banks themselves and relying on the subjectivity of responding staff.

Vol. 10 No. 1 Central Bank Transparency and Independence 197

gather this information for as large a number of central banks aspossible and for every year from 1998 through 2010. Where therewas a change in some aspect of transparency over the course of acalendar year, we take the value that prevailed for the largest portionof the year.

We were able to assemble information on transparency for 120central banks. Most of the omissions are central banks of micro-states: our sample includes the central banks of all large, systemicallysignificant countries. New central banks considered here, in additionto those covered in our previous study, are those of Angola, Azer-baijan, Bosnia and Herzegovina, Botswana, Cambodia, the CaymanIslands, Curacao, Iran, Lebanon, Macao, Macedonia, Mozambique,Samoa, Seychelles, Tanzania, Tonga, Venezuela, Laos, the Maldives,and Syria.

Since we have discussed the criteria used in constructing theseindices in a series of earlier papers, we do not repeat that discussionhere. Readers can find the relevant details in appendix 1.

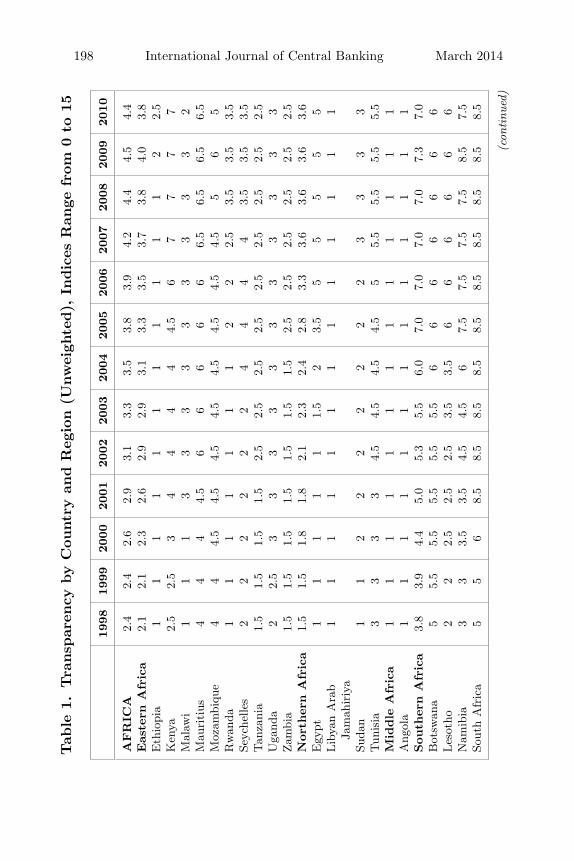

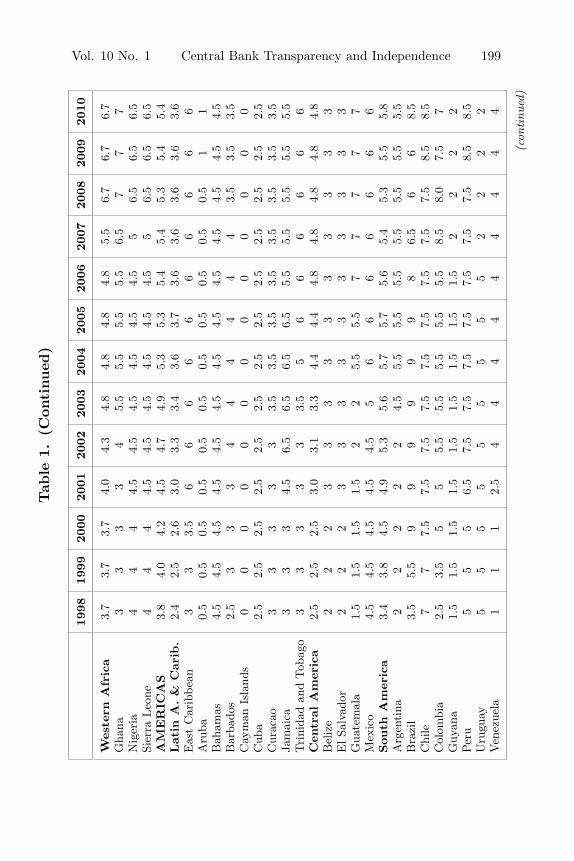

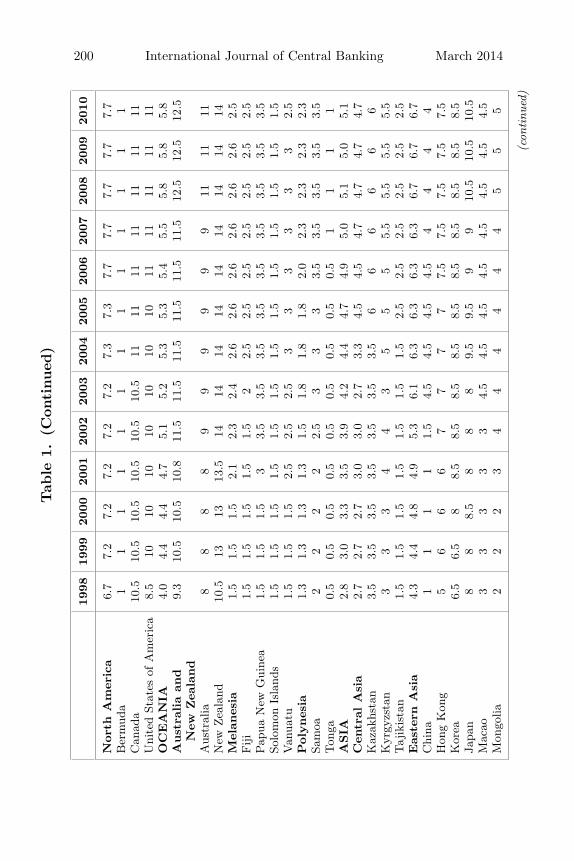

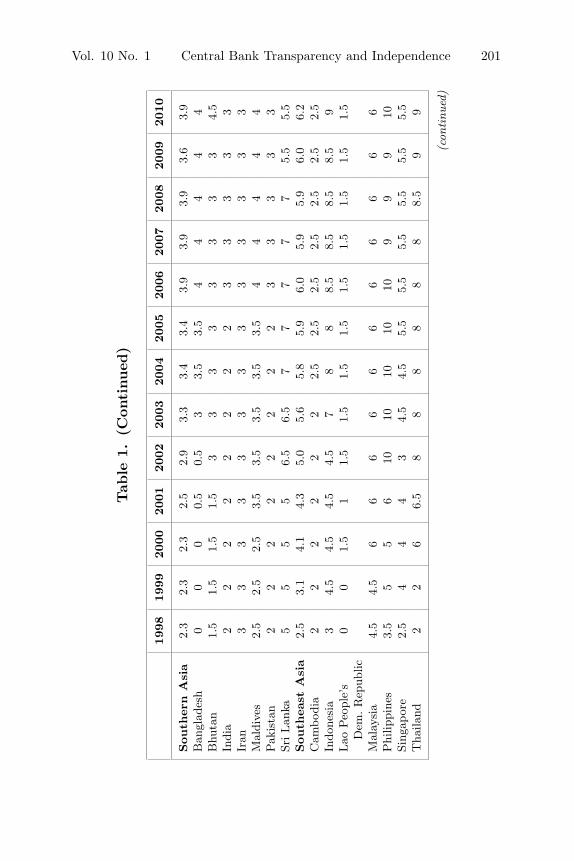

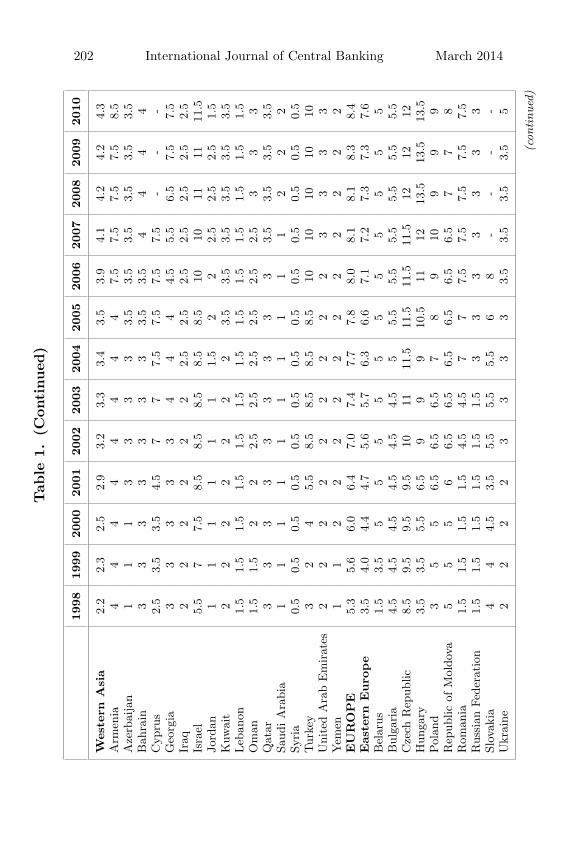

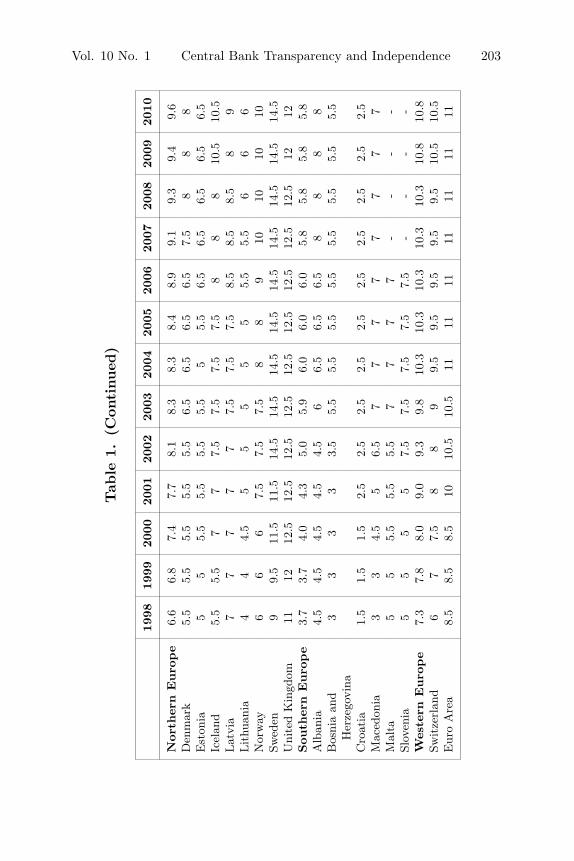

Table 1 shows the indices by country and region.14 The mosttransparent central banks in 2010 are the Swedish Riksbank, theReserve Bank of New Zealand, the Central Bank of Hungary, theCzech National Bank, the Bank of England, and the Bank of Israel.We see here a number of central banks that received high marksfor transparency in past studies (those of Sweden, New Zealand, theUnited Kingdom, and Canada) but also others that did not makethe top-ten list previously. This is a reminder of the advantages ofbroad country coverage and of the fact that a number of countrieshave been moving in the direction of greater transparency.

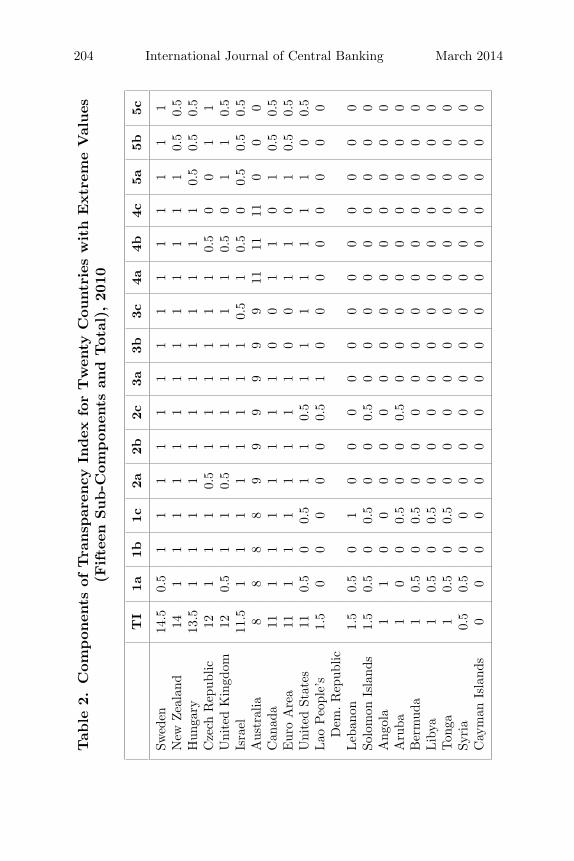

The six least transparent central banks in 2010 were those ofAngola, Aruba, Bermuda, the Cayman Islands, Libya, Syria, andTonga. In 2006, by comparison, the six least transparent bankswere those of Aruba, Bermuda, Ethiopia, Libya, Saudi Arabia, andYemen. While some of the names have changed, the categoriesremain the same; that is to say, many of the least transparent cen-tral banks remain those of offshore financial centers and autocraticregimes in North Africa and the Middle East (see table 2).15

14Regions are constructed using United Nations classifications.15It will be interesting to see what impact recent efforts to combat money

laundering and, in addition, the advent of the Arab Spring have on these patterns.

198 International Journal of Central Banking March 2014Tab

le1.

Tra

nsp

aren

cyby

Cou

ntr

yan

dR

egio

n(U

nw

eigh

ted),

Indic

esR

ange

from

0to

15

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

AFR

ICA

2.4

2.4

2.6

2.9

3.1

3.3

3.5

3.8

3.9

4.2

4.4

4.5

4.4

Eas

tern

Afr

ica

2.1

2.1

2.3

2.6

2.9

2.9

3.1

3.3

3.5

3.7

3.8

4.0

3.8

Eth

iopi

a1

11

11

11

11

11

22.

5K

enya

2.5

2.5

34

44

44.

56

77

77

Mal

awi

11

13

33

33

33

33

2M

auri

tius

44

44.

56

66

66

6.5

6.5

6.5

6.5

Moz

ambi

que

44

4.5

4.5

4.5

4.5

4.5

4.5

4.5

4.5

56

5R

wan

da1

11

11

11

22

2.5

3.5

3.5

3.5

Seyc

helle

s2

22

22

24

44

43.

53.

53.

5Tan

zani

a1.

51.

51.

51.

52.

52.

52.

52.

52.

52.

52.

52.

52.

5U

gand

a2

2.5

33

33

33

33

33

3Zam

bia

1.5

1.5

1.5

1.5

1.5

1.5

1.5

2.5

2.5

2.5

2.5

2.5

2.5

Nor

ther

nA

fric

a1.

51.

51.

81.

82.

12.

32.

42.

83.

33.

63.

63.

63.

6E

gypt

11

11

11.

52

3.5

55

55

5Lib

yan

Ara

b1

11

11

11

11

11

11

Jam

ahir

iya

Suda

n1

12

22

22

22

33

33

Tun

isia

33

33

4.5

4.5

4.5

4.5

55.

55.

55.

55.

5M

iddle

Afr

ica

11

11

11

11

11

11

1A

ngol

a1

11

11

11

11

11

11

Sou

ther

nA

fric

a3.

83.

94.

45.

05.

35.

56.

07.

07.

07.

07.

07.

37.

0B

otsw

ana

55.

55.

55.

55.

55.

56

66

66

66

Les

otho

22

2.5

2.5

2.5

3.5

3.5

66

66

66

Nam

ibia

33

3.5

3.5

4.5

4.5

67.

57.

57.

57.

58.

57.

5So

uth

Afr

ica

55

68.

58.

58.

58.

58.

58.

58.

58.

58.

58.

5

(con

tinu

ed)

Vol. 10 No. 1 Central Bank Transparency and Independence 199Tab

le1.

(Con

tinued

)

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Wes

tern

Afr

ica

3.7

3.7

3.7

4.0

4.3

4.8

4.8

4.8

4.8

5.5

6.7

6.7

6.7

Gha

na3

33

34

5.5

5.5

5.5

5.5

6.5

77

7N

iger

ia4

44

4.5

4.5

4.5

4.5

4.5

4.5

56.

56.

56.

5Si

erra

Leo

ne4

44

4.5

4.5

4.5

4.5

4.5

4.5

56.

56.

56.

5A

MER

ICA

S3.

84.

04.

24.

54.

74.

95.

35.

35.

45.

45.

35.

45.

4Lat

inA

.&

Car

ib.

2.4

2.5

2.6

3.0

3.3

3.4

3.6

3.7

3.6

3.6

3.6

3.6

3.6

Eas

tC

arib

bean

33

3.5

66

66

66

66

66

Aru

ba0.

50.

50.

50.

50.

50.

50.

50.

50.

50.

50.

51

1B

aham

as4.

54.

54.

54.

54.

54.

54.

54.

54.

54.

54.

54.

54.

5B

arba

dos

2.5

33

34

44

44

43.

53.

53.

5C

aym

anIs

land

s0

00

00

00

00

00

00

Cub

a2.

52.

52.

52.

52.

52.

52.

52.

52.

52.

52.

52.

52.

5C

urac

ao3

33

33

3.5

3.5

3.5

3.5

3.5

3.5

3.5

3.5

Jam

aica

33

34.

56.

56.

56.

56.

55.

55.

55.

55.

55.

5Tri

nida

dan

dTob

ago

33

33

33.

55

66

66

66

Cen

tral

Am

eric

a2.

52.

52.

53.

03.

13.

34.

44.

44.

84.

84.

84.

84.

8B

eliz

e2

22

33

33

33

33

33

ElSa

lvad

or2

22

33

33

33

33

33

Gua

tem

ala

1.5

1.5

1.5

1.5

22

5.5

5.5

77

77

7M

exic

o4.

54.

54.

54.

54.

55

66

66

66

6Sou

thA

mer

ica

3.4

3.8

4.5

4.9

5.3

5.6

5.7

5.7

5.6

5.4

5.3

5.5

5.8

Arg

enti

na2

22

22

4.5

5.5

5.5

5.5

5.5

5.5

5.5

5.5

Bra

zil

3.5

5.5

99

99

99

86.

56

68.

5C

hile

77

7.5

7.5

7.5

7.5

7.5

7.5

7.5

7.5

7.5

8.5

8.5

Col

ombi

a2.

53.

55

55.

55.

55.

55.

55.

58.

58.

07.

57

Guy

ana

1.5

1.5

1.5

1.5

1.5

1.5

1.5

1.5

1.5

22

22

Per

u5

55

6.5

7.5

7.5

7.5

7.5

7.5

7.5

7.5

8.5

8.5

Uru

guay

55

55

55

55

52

22

2V

enez

uela

11

12.

54

44

44

44

44

(con

tinu

ed)

200 International Journal of Central Banking March 2014Tab

le1.

(Con

tinued

)

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Nor

thA

mer

ica

6.7

7.2

7.2

7.2

7.2

7.2

7.3

7.3

7.7

7.7

7.7

7.7

7.7

Ber

mud

a1

11

11

11

11

11

11

Can

ada

10.5

10.5

10.5

10.5

10.5

10.5

1111

1111

1111

11U

nite

dSt

ates

ofA

mer

ica

8.5

1010

1010

1010

1011

1111

1111

OC

EA

NIA

4.0

4.4

4.4

4.7

5.1

5.2

5.3

5.3

5.4

5.5

5.8

5.8

5.8

Aust

ralia

and

9.3

10.5

10.5

10.8

11.5

11.5

11.5

11.5

11.5

11.5

12.5

12.5

12.5

New

Zea

land

Aus

tral

ia8

88

89

99

99

911

1111

New

Zea

land

10.5

1313

13.5

1414

1414

1414

1414

14M

elan

esia

1.5

1.5

1.5

2.1

2.3

2.4

2.6

2.6

2.6

2.6

2.6

2.6

2.5

Fiji

1.5

1.5

1.5

1.5

1.5

22.

52.

52.

52.

52.

52.

52.

5Pap

uaN

ewG

uine

a1.

51.

51.

53

3.5

3.5

3.5

3.5

3.5

3.5

3.5

3.5

3.5

Solo

mon

Isla

nds

1.5

1.5

1.5

1.5

1.5

1.5

1.5

1.5

1.5

1.5

1.5

1.5

1.5

Van

uatu

1.5

1.5

1.5

2.5

2.5

2.5

33

33

33

2.5

Pol

ynes

ia1.

31.

31.

31.

31.

51.

81.

81.

82.

02.

32.

32.

32.

3Sa

moa

22

22

2.5

33

33.

53.

53.

53.

53.

5Ton

ga0.

50.

50.

50.

50.

50.

50.

50.

50.

51

11

1A

SIA

2.8

3.0

3.3

3.5

3.9

4.2

4.4

4.7

4.9

5.0

5.1

5.0

5.1

Cen

tral

Asi

a2.

72.

72.

73.

03.

02.

73.

34.

54.

54.

74.

74.

74.

7K

azak

hsta

n3.

53.

53.

53.

53.

53.

53.

56

66

66

6K

yrgy

zsta

n3

33

44

35

55

5.5

5.5

5.5

5.5

Taj

ikis

tan

1.5

1.5

1.5

1.5

1.5

1.5

1.5

2.5

2.5

2.5

2.5

2.5

2.5

Eas

tern

Asi

a4.

34.

44.

84.

95.

36.

16.

36.

36.

36.

36.

76.

76.

7C

hina

11

11

1.5

4.5

4.5

4.5

4.5

44

44

Hon

gK

ong

56

66

77

77

7.5

7.5

7.5

7.5

7.5

Kor

ea6.

56.

58

8.5

8.5

8.5

8.5

8.5

8.5

8.5

8.5

8.5

8.5

Japa

n8

88.

58

88

9.5

9.5

99

10.5

10.5

10.5

Mac

ao3

33

33

4.5

4.5

4.5

4.5

4.5

4.5

4.5

4.5

Mon

golia

22

23

44

44

44

55

5

(con

tinu

ed)

Vol. 10 No. 1 Central Bank Transparency and Independence 201

Tab

le1.

(Con

tinued

)

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Sou

ther

nA

sia

2.3

2.3

2.3

2.5

2.9

3.3

3.4

3.4

3.9

3.9

3.9

3.6

3.9

Ban

glad

esh

00

00.

50.

53

3.5

3.5

44

44

4B

huta

n1.

51.

51.

51.

53

33

33

33

34.

5In

dia

22

22

22

22

33

33

3Ir

an3

33

33

33

33

33

33

Mal

dive

s2.

52.

52.

53.

53.

53.

53.

53.

54

44

44

Pak

ista

n2

22

22

22

23

33

33

SriLan

ka5

55

56.

56.

57

77

77

5.5

5.5

Sou

thea

stA

sia

2.5

3.1

4.1

4.3

5.0

5.6

5.8

5.9

6.0

5.9

5.9

6.0

6.2

Cam

bodi

a2

22

22

22.

52.

52.

52.

52.

52.

52.

5In

done

sia

34.

54.

54.

54.

57

88

8.5

8.5

8.5

8.5

9Lao

Peo

ple’

s0

01.

51

1.5

1.5

1.5

1.5

1.5

1.5

1.5

1.5

1.5

Dem

.R

epub

licM

alay

sia

4.5

4.5

66

66

66

66

66

6P

hilip

pine

s3.

55

56

1010

1010

109

99

10Si

ngap

ore

2.5

44

43

4.5

4.5

5.5

5.5

5.5

5.5

5.5

5.5

Tha

iland

22

66.

58

88

88

88.

59

9

(con

tinu

ed)

202 International Journal of Central Banking March 2014Tab

le1.

(Con

tinued

)

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Wes

tern

Asi

a2.

22.

32.

52.

93.

23.

33.

43.

53.

94.

14.

24.

24.

3A

rmen

ia4

44

44

44

47.

57.

57.

57.

58.

5A

zerb

aija

n1

11

33

33

3.5

3.5

3.5

3.5

3.5

3.5

Bah

rain

33

33

33

33.

53.

54

44

4C

ypru

s2.

53.

53.

54.

57

77.

57.

57.

57.

5-

--

Geo

rgia

33

33

34

44

4.5

5.5

6.5

7.5

7.5

Iraq

22

22

22

2.5

2.5

2.5

2.5

2.5

2.5

2.5

Isra

el5.

57

7.5

8.5

8.5

8.5

8.5

8.5

1010

1111

11.5

Jord

an1

11

11

11.

52

22.

52.

52.

51.

5K

uwai

t2

22

22

22

3.5

3.5

3.5

3.5

3.5

3.5

Leb

anon

1.5

1.5

1.5

1.5

1.5

1.5

1.5

1.5

1.5

1.5

1.5

1.5

1.5

Om

an1.

51.

52

22.

52.

52.

52.

52.

52.

53

33

Qat

ar3

33

33

33

33

3.5

3.5

3.5

3.5

Saud

iA

rabi

a1

11

11

11

11

12

22

Syri

a0.

50.

50.

50.

50.

50.

50.

50.

50.

50.

50.

50.

50.

5Tur

key

32

45.

58.

58.

58.

58.

510

1010

1010

Uni

ted

Ara

bE

mir

ates

22

22

22

22

23

33

3Y

emen

11

22

22

22

22

22

2EU

RO

PE

5.3

5.6

6.0

6.4

7.0

7.4

7.7

7.8

8.0

8.1

8.1

8.3

8.4

Eas

tern

Euro

pe

3.5

4.0

4.4

4.7

5.6

5.7

6.3

6.6

7.1

7.2

7.3

7.3

7.6

Bel

arus

1.5

3.5

55

55

55

55

55

5B

ulga

ria

4.5

4.5

4.5

4.5

4.5

4.5

55.

55.

55.

55.

55.

55.

5C

zech

Rep

ublic

8.5

9.5

9.5

9.5

1011

11.5

11.5

11.5

11.5

1212

12H

unga

ry3.

53.

55.

56.

59

99

10.5

1112

13.5

13.5

13.5

Pol

and

35

56.

56.

56.

57

89

109

99

Rep

ublic

ofM

oldo

va5

55

66.

56.

56.

56.

56.

56.

57

78

Rom

ania

1.5

1.5

1.5

1.5

4.5

4.5

77

7.5

7.5

7.5

7.5

7.5

Rus

sian

Fede

rati

on1.

51.

51.

51.

51.

51.

53

33

33

33

Slov

akia

44

4.5

3.5

5.5

5.5

5.5

68

--

--

Ukr

aine

22

22

33

33

3.5

3.5

3.5

3.5

5

(con

tinu

ed)

Vol. 10 No. 1 Central Bank Transparency and Independence 203

Tab

le1.

(Con

tinued

)

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Nor

ther

nEuro

pe

6.6

6.8

7.4

7.7

8.1

8.3

8.3

8.4

8.9

9.1

9.3

9.4

9.6

Den

mar

k5.

55.

55.

55.

55.

56.

56.

56.

56.

57.

58

88

Est

onia

55

5.5

5.5

5.5

5.5

55.

56.

56.

56.

56.

56.

5Ic

elan

d5.

55.

57

77.

57.

57.

57.

58

88

10.5

10.5

Lat

via

77

77

77.

57.

57.

58.

58.

58.

58

9Lit

huan

ia4

44.

55

55

55

5.5

5.5

66

6N

orw

ay6

66

7.5

7.5

7.5

88

910

1010

10Sw

eden

99.

511

.511

.514

.514

.514

.514

.514

.514

.514

.514

.514

.5U

nite

dK

ingd

om11

1212

.512

.512

.512

.512

.512

.512

.512

.512

.512

12Sou

ther

nEuro

pe

3.7

3.7

4.0

4.3

5.0

5.9

6.0

6.0

6.0

5.8

5.8

5.8

5.8

Alb

ania

4.5

4.5

4.5

4.5

4.5

66.

56.

56.

58

88

8B

osni

aan

d3

33

33.

55.

55.

55.

55.

55.

55.

55.

55.

5H

erze

govi

naC

roat

ia1.

51.

51.

52.

52.

52.

52.

52.

52.

52.

52.

52.

52.

5M

aced

onia

33

4.5

56.

57

77

77

77

7M

alta

55

5.5

5.5

5.5

77

77

--

--

Slov

enia

55

55

7.5

7.5

7.5

7.5

7.5

--

--

Wes

tern

Euro

pe

7.3

7.8

8.0

9.0

9.3

9.8

10.3

10.3

10.3

10.3

10.3

10.8

10.8

Swit

zerl

and

67

7.5

88

99.

59.

59.

59.

59.

510

.510

.5E

uro

Are

a8.

58.

58.

510

10.5

10.5

1111

1111

1111

11

204 International Journal of Central Banking March 2014

Tab

le2.

Com

pon

ents

ofTra

nsp

aren

cyIn

dex

for

Tw

enty

Cou

ntr

ies

with

Extr

eme

Val

ues

(Fifte

enSub-C

ompon

ents

and

Tot

al),

2010

TI

1a1b

1c2a

2b2c

3a3b

3c4a

4b4c

5a5b

5c

Swed

en14

.50.

51

11

11

11

11

11

11

1N

ewZea

land

141

11

11

11

11

11

11

0.5

0.5

Hun

gary

13.5

11

11

11

11

11

11

0.5

0.5

0.5

Cze

chR

epub

lic12

11

10.

51

11

11

10.

50

01

1U

nite

dK

ingd

om12

0.5

11

0.5

11

11

11

0.5

01

10.

5Is

rael

11.5

11

11

11

11

0.5

10.

50

0.5

0.5

0.5

Aus

tral

ia8

88

89

99

99

911

1111

00

0C

anad

a11

11

11

11

10

01

10

10.

50.

5E

uro

Are

a11

11

11

11

10

01

10

10.

50.

5U

nite

dSt

ates

110.

50

0.5

11

0.5

11

11

11

10

0.5

Lao

Peo

ple’

s1.

50

00

00

0.5

10

00

00

00

0D

em.R

epub

licLeb

anon

1.5

0.5

01

00

00

00

00

00

00

Solo

mon

Isla

nds

1.5

0.5

00.

50

00.

50

00

00

00

00

Ang

ola

11

00

00

00

00

00

00

00

Aru

ba1

00

0.5

00

0.5

00

00

00

00

0B

erm

uda

10.

50

0.5

00

00

00

00

00

00

Lib

ya1

0.5

00.

50

00

00

00

00

00

0Ton

ga1

0.5

00.

50

00

00

00

00

00

0Sy

ria

0.5

0.5

00

00

00

00

00

00

00

Cay

man

Isla

nds

00

00

00

00

00

00

00

00

Vol. 10 No. 1 Central Bank Transparency and Independence 205

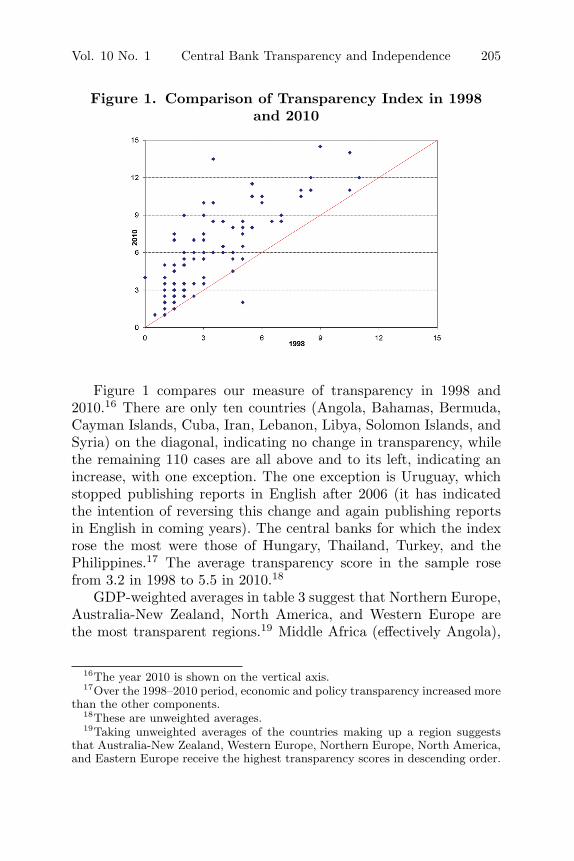

Figure 1. Comparison of Transparency Index in 1998and 2010

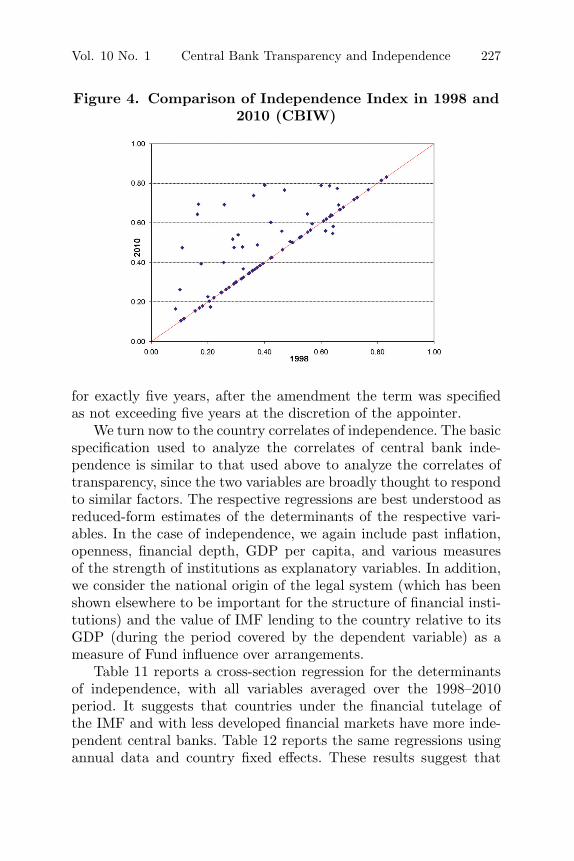

Figure 1 compares our measure of transparency in 1998 and2010.16 There are only ten countries (Angola, Bahamas, Bermuda,Cayman Islands, Cuba, Iran, Lebanon, Libya, Solomon Islands, andSyria) on the diagonal, indicating no change in transparency, whilethe remaining 110 cases are all above and to its left, indicating anincrease, with one exception. The one exception is Uruguay, whichstopped publishing reports in English after 2006 (it has indicatedthe intention of reversing this change and again publishing reportsin English in coming years). The central banks for which the indexrose the most were those of Hungary, Thailand, Turkey, and thePhilippines.17 The average transparency score in the sample rosefrom 3.2 in 1998 to 5.5 in 2010.18

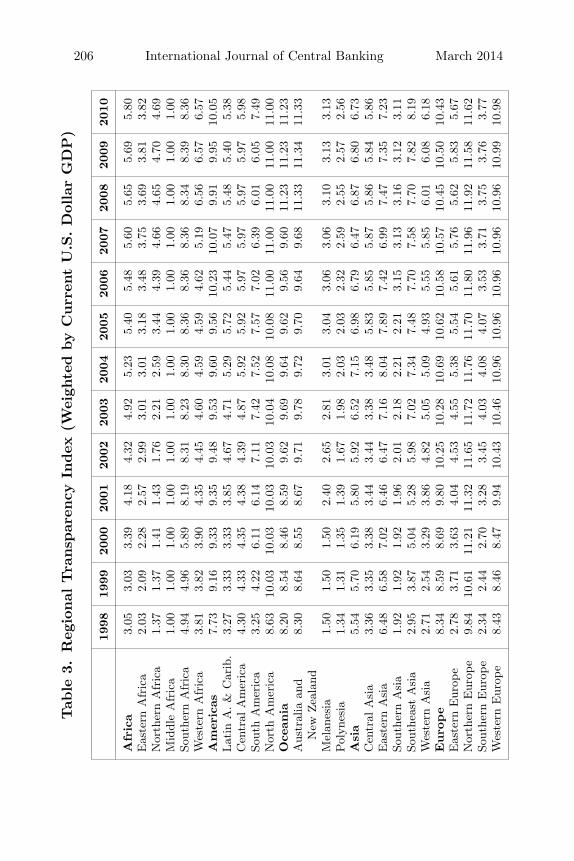

GDP-weighted averages in table 3 suggest that Northern Europe,Australia-New Zealand, North America, and Western Europe arethe most transparent regions.19 Middle Africa (effectively Angola),

16The year 2010 is shown on the vertical axis.17Over the 1998–2010 period, economic and policy transparency increased more

than the other components.18These are unweighted averages.19Taking unweighted averages of the countries making up a region suggests

that Australia-New Zealand, Western Europe, Northern Europe, North America,and Eastern Europe receive the highest transparency scores in descending order.

206 International Journal of Central Banking March 2014Tab

le3.

Reg

ional

Tra

nsp

aren

cyIn

dex

(Wei

ghte

dby

Curr

ent

U.S

.D

olla

rG

DP

)

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Afr

ica

3.05

3.03

3.39

4.18

4.32

4.92

5.23

5.40

5.48

5.60

5.65

5.69

5.80

Eas

tern

Afr

ica

2.03

2.09

2.28

2.57

2.99

3.01

3.01

3.18

3.48

3.75

3.69

3.81

3.82

Nor

ther

nA

fric

a1.

371.

371.

411.

431.

762.

212.

593.

444.

394.

664.

654.

704.

69M

iddl

eA

fric

a1.

001.

001.

001.

001.

001.

001.

001.

001.

001.

001.

001.

001.

00So

uthe

rnA

fric

a4.

944.

965.

898.

198.

318.

238.

308.

368.

368.

368.

348.

398.

36W

este

rnA

fric

a3.

813.

823.

904.

354.

454.

604.

594.

594.

625.

196.

566.

576.

57A

mer

icas

7.73

9.16

9.33

9.35

9.48

9.53

9.60

9.56

10.2

310

.07

9.91

9.95

10.0

5Lat

inA

.&

Car

ib.

3.27

3.33

3.33

3.85

4.67

4.71

5.29

5.72

5.44

5.47

5.48

5.40

5.38

Cen

tral

Am

eric

a4.

304.

334.

354.

384.

394.

875.

925.

925.

975.

975.

975.

975.

98So

uth

Am

eric

a3.

254.

226.

116.

147.

117.

427.

527.

577.

026.

396.

016.

057.

49N

orth

Am

eric

a8.

6310

.03

10.0

310

.03

10.0

310

.04

10.0

810

.08

11.0

011

.00

11.0

011

.00

11.0

0O

cean

ia8.

208.

548.

468.

599.

629.

699.

649.

629.

569.

6011

.23

11.2

311

.23

Aus

tral

iaan

d8.

308.

648.

558.

679.

719.

789.

729.

709.

649.

6811

.33

11.3

411

.33

New

Zea

land

Mel

anes

ia1.

501.

501.

502.

402.

652.

813.

013.

043.

063.

063.

103.

133.

13Pol

ynes

ia1.

341.

311.

351.

391.

671.

982.

032.

032.

322.

592.

552.

572.

56A

sia

5.54

5.70

6.19

5.80

5.92

6.52

7.15

6.98

6.79

6.47

6.87

6.80

6.73

Cen

tral

Asi

a3.

363.

353.

383.

443.

443.

383.

485.

835.

855.

875.

865.

845.

86E

aste

rnA

sia

6.48

6.58

7.02

6.46

6.47

7.16

8.04

7.89

7.42

6.99

7.47

7.35

7.23

Sout

hern

Asi

a1.

921.

921.

921.

962.

012.

182.

212.

213.

153.

133.

163.

123.

11So

uthe

ast

Asi

a2.

953.

875.

045.

285.

987.

027.

347.

487.

707.

587.

707.

828.

19W

este

rnA

sia

2.71

2.54

3.29

3.86

4.82

5.05

5.09

4.93

5.55

5.85

6.01

6.08

6.18

Euro

pe

8.34

8.59

8.69

9.80

10.2

510

.28

10.6

910

.62

10.5

810

.57

10.4

510

.50

10.4

3E

aste

rnE

urop

e2.

783.

713.

634.

044.

534.

555.

385.

545.

615.

765.

625.

835.

67N

orth

ern

Eur

ope

9.84

10.6

111

.21

11.3

211

.65

11.7

211

.76

11.7

011

.80

11.9

611

.92

11.5

811

.62

Sout

hern

Eur

ope

2.34

2.44

2.70

3.28

3.45

4.03

4.08

4.07

3.53

3.71

3.75

3.76

3.77

Wes

tern

Eur

ope

8.43

8.46

8.47

9.94

10.4

310

.46

10.9

610

.96

10.9

610

.96

10.9

610

.99

10.9

8

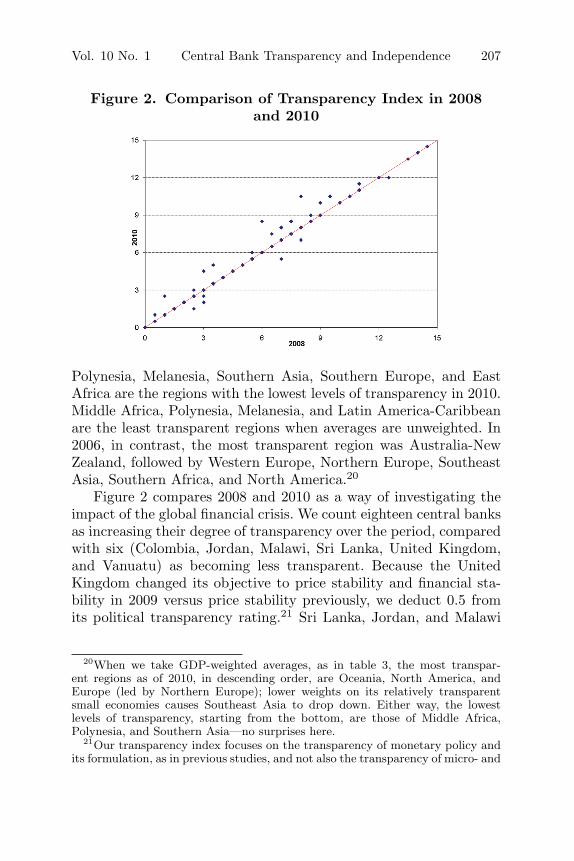

Vol. 10 No. 1 Central Bank Transparency and Independence 207

Figure 2. Comparison of Transparency Index in 2008and 2010

Polynesia, Melanesia, Southern Asia, Southern Europe, and EastAfrica are the regions with the lowest levels of transparency in 2010.Middle Africa, Polynesia, Melanesia, and Latin America-Caribbeanare the least transparent regions when averages are unweighted. In2006, in contrast, the most transparent region was Australia-NewZealand, followed by Western Europe, Northern Europe, SoutheastAsia, Southern Africa, and North America.20

Figure 2 compares 2008 and 2010 as a way of investigating theimpact of the global financial crisis. We count eighteen central banksas increasing their degree of transparency over the period, comparedwith six (Colombia, Jordan, Malawi, Sri Lanka, United Kingdom,and Vanuatu) as becoming less transparent. Because the UnitedKingdom changed its objective to price stability and financial sta-bility in 2009 versus price stability previously, we deduct 0.5 fromits political transparency rating.21 Sri Lanka, Jordan, and Malawi

20When we take GDP-weighted averages, as in table 3, the most transpar-ent regions as of 2010, in descending order, are Oceania, North America, andEurope (led by Northern Europe); lower weights on its relatively transparentsmall economies causes Southeast Asia to drop down. Either way, the lowestlevels of transparency, starting from the bottom, are those of Middle Africa,Polynesia, and Southern Asia—no surprises here.

21Our transparency index focuses on the transparency of monetary policy andits formulation, as in previous studies, and not also the transparency of micro- and

208 International Journal of Central Banking March 2014

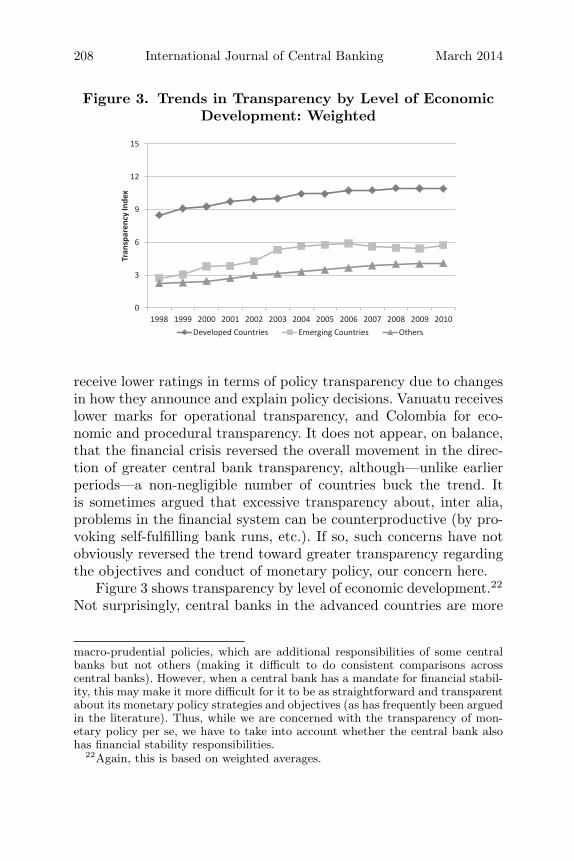

Figure 3. Trends in Transparency by Level of EconomicDevelopment: Weighted

0

3

6

9

12

15

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Tran

spar

ency

Inde

x

Developed Countries Emerging Countries Others

receive lower ratings in terms of policy transparency due to changesin how they announce and explain policy decisions. Vanuatu receiveslower marks for operational transparency, and Colombia for eco-nomic and procedural transparency. It does not appear, on balance,that the financial crisis reversed the overall movement in the direc-tion of greater central bank transparency, although—unlike earlierperiods—a non-negligible number of countries buck the trend. Itis sometimes argued that excessive transparency about, inter alia,problems in the financial system can be counterproductive (by pro-voking self-fulfilling bank runs, etc.). If so, such concerns have notobviously reversed the trend toward greater transparency regardingthe objectives and conduct of monetary policy, our concern here.

Figure 3 shows transparency by level of economic development.22

Not surprisingly, central banks in the advanced countries are more

macro-prudential policies, which are additional responsibilities of some centralbanks but not others (making it difficult to do consistent comparisons acrosscentral banks). However, when a central bank has a mandate for financial stabil-ity, this may make it more difficult for it to be as straightforward and transparentabout its monetary policy strategies and objectives (as has frequently been arguedin the literature). Thus, while we are concerned with the transparency of mon-etary policy per se, we have to take into account whether the central bank alsohas financial stability responsibilities.

22Again, this is based on weighted averages.

Vol. 10 No. 1 Central Bank Transparency and Independence 209

transparent than central banks in emerging markets (defined asmiddle-income countries with significant links to international finan-cial markets), which in turn are more transparent than central banksin developing countries.23 We see an upward trend over time in allthree categories of economies until 2006. In the case of emerging mar-kets, this is in contrast to Crowe and Meade, who find no increasebetween 1998 and 2006; it is precisely in this period and sub-groupof economies that our data show the most dramatic increase in thelevel of transparency.24

Strikingly, while transparency continues to trend upward in boththe advanced and developing countries, the same emerging marketsthat made the most dramatic strides through 2006 (the terminal dateof our earlier study) appear to give back some ground thereafter.This reflects somewhat lower rates for a number of larger emergingmarkets (Brazil and China in 2007; Brazil, Colombia, and Poland in2008).25

Tables 4 and 5 update our earlier regressions on the determinantsof transparency. Table 4 presents the cross-section results, with allvariables averaged over the 1998–2010 period. Evidently, countrieswith higher per capita incomes, deeper financial markets, more openeconomies, and stronger political institutions have more transparentcentral banks. A new result here is the positive association betweenpast inflation and current transparency. However, the inflation vari-able is not significant in all specifications; it is correlated with variousdimensions of the political regime (columns 5–7), making it hard toidentify its effects.26

23We adopt the Dow Jones classification of emerging markets throughout.24Siklos (2011) reports conclusions similar to ours. Note that no countries

moved between emerging market and developing country status over the periodaccording to our categorization.

25The People’s Bank of China announced numerical forecasts before 2007 butnot after. Brazil did not publish quarterly inflation reports starting in 2007 (theypublished all the reports for the period of 2007–11 in July 2011). Poland changedthe frequency of its inflation reports and inflation and output forecast announce-ments from four times a year to three times a year starting in 2008. Likewise,Columbia changed the frequency of inflation reports from four times a year tothree times a year starting in 2008.

26Some recent literature has suggested the existence of a positive relationshipbetween inflation and democracy, especially in the Latin American context (see,e.g., Haggard and Kaufman 1995).

210 International Journal of Central Banking March 2014Tab

le4.

Det

erm

inan

tsof

Tra

nsp

aren

cy,19

98–2

010,

Ave

rage

sa

(1)

(2)

(3)

(4)

(5)

(6)

(7)

Con

stan

t1.

41−

5.20

∗−

1.17

4.49

−2.

87−

7.33

∗−

2.80

(0.5

7)(−

2.43

)(−

0.67

)(1

.68)

(−1.

45)

(−3.

86)

(−1.

49)

Pas

tIn

flati

on8.

23∗

4.16

5.81

∗9.

71∗

−0.

554.

62−

1.28

(3.1

6)(1

.32)

(2.1

6)(4

.47)

(−0.

18)

(1.4

8)(−

0.35

)O

penn

ess

−0.

01∗

−0.

01∗

−0.

01∗

−0.

01∗

−0.

00−

0.01

∗−

0.00

(−3.

51)

(−2.

95)

(−2.

23)

(−3.

00)

(−1.

07)

(−3.

09)

(−0.

77)

Fin

anci

alD

epth

0.01

0.01

∗0.

01∗

0.00

0.01

0.01

∗0.

01(1

.13)

(2.0

6)(2

.14)

(0.6

3)(1

.18)

(2.0

6)(0

.97)

GD

Ppe

rC

apit

a0.

381.

13∗

0.64

∗0.

000.

81∗

1.14

∗0.

83∗

(1.2

5)(4

.12)

(3.0

2)(0

.00)

(2.9

8)(5

.32)

(3.5

5)R

ule

ofLaw

1.87

∗

(3.9

5)Pol

itic

alSt

abili

ty0.

17(0

.44)

Voi

cean

d1.

78∗

Acc

ount

abili

ty(6

.09)

Gov

ernm

ent

Effi

cien

cy2.

67∗

(5.2

3)D

emoc

racy

0.17

∗

(2.6

6)A

utoc

racy

−0.

13∗

(−2.

24)

Pol

ity

0.17

∗

(4.6

1)R

-Squ

ared

0.44

0.32

0.52

0.52

0.42

0.38

0.50

at-

stat

isti

csin

par

enth

eses

.N

ote

s:T

he

defi

nit

ions

ofin

dep

enden

tva

riab

les

are

asfo

llow

s:Pas

tin

flat

ion

isth

elo

gari

thm

icva

lue

of1

plu

sth

ela

gged

inflat

ion

rate

;op

ennes

sis

the

shar

eof

the

sum

ofex

por

tsan

dim

por

tsto

GD

P;finan

cial

dep

this

the

rati

oof

M2

toG

DP;G

DP

per

capit

ais

the

loga

rith

mof

const

ant

GD

Pper

capit

a;ru

leof

law

,pol

itic

alst

ability,

voic

ean

dac

count

ability,

and

gove

rnm

ent

effici

ency

are

from

the

Gov

ernan

ceIn

dic

ator

sD

atab

ase;

and

dem

ocra

cy,au

tocr

acy,

and

pol

ity

are

take

nfr

omth

ePol

ity

Dat

abas

e.∗

den

otes

sign

ifica

nce

atth

e5

per

cent

leve

l.

Vol. 10 No. 1 Central Bank Transparency and Independence 211

Tab

le5.

Det

erm

inan

tsof

Tra

nsp

aren

cy,Pan

elFix

edEffec

tsa

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

Con

stan

t−

3.08

−3.

99−

2.24

−3.

17−

1.04

−3.

28−

2.74

−3.

07(−

0.01

)(−

0.01

)(−

0.01

)(−

0.01

)(−

0.02

)(−

0.01

)(−

0.01

)(−

0.01

)Pas

tIn

flati

on−

0.60

−0.

56−

0.53

−0.

60−

0.48

−0.

61−

0.65

−0.

62(−

1.27

)(−

1.20

)(−

1.13

)(−

1.26

)(−

1.02

)(−

1.35

)(−

1.44

)(−

1.38

)O

penn

ess

−0.

01∗

−0.

01∗

−0.

01∗

−0.

01∗

−0.

01∗

−0.

00−

0.01

∗−

0.00

∗

(−3.

24)

(−2.

93)

(−3.

31)

(−3.

23(−

3.81

)(−

1.82

)(−

2.92

)(−

2.13

)Fin

anci

alD

epth

0.03

∗0.

03∗

0.03

∗0.

03∗

0.03

∗0.

02∗

0.02

∗0.

02∗

(6.7

6)(6

.66)

(6.5

8)(6

.77)

(6.8

2)(5

.75)

(5.6

1)(5

.70)

GD

Ppe

rC

apit

a0.

82∗

0.92

∗0.

73∗

0.83

∗0.

59∗

0.66

∗0.

90∗

0.75

∗

(6.9

9)(7

.81)

(6.6

3)(6

.82)

(4.9

6)(6

.02)

(8.4

0)(6

.99)

Rul

eof

Law

−0.

11(0

.85)

Pol

itic

alSt

abili

ty−

0.31

∗

(−2.

78)

(con

tinu

ed)

212 International Journal of Central Banking March 2014

Tab

le5.

(Con

tinued

)

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

Voi

cean

d0.

21A

ccou

ntab

ility

(1.7

8)G

over

nmen

t−

0.12

Effi

cien

cy(−

0.90

)R

egul

ator

yQ

ualit

y0.

48∗

(3.4

6)D

emoc

racy

0.29

∗

(9.2

9)A

utoc

racy

−0.

41∗

(−9.

30)

Pol

ity

0.19

∗

(9.8

5)H

auss

man

Tes

t18

.18∗

11.0

1∗28

.03∗

26.8

5∗26

.63∗

11.9

1∗9.

2310

.00

R-S

quar

ed0.

950.

950.

950.

950.

950.

960.

960.

96

at-

stat

isti

csin

par

enth

eses

.N

ote

s:T

he

defi

nit

ions

ofin

dep

enden

tva

riab

les

are

asfo

llow

s:Pas

tin

flat

ion

isth

elo

gari

thm

icva

lue

of1

plu

sth

ela

gged

inflat

ion

rate

;op

ennes

sis

the

shar

eof

the

sum

ofex

por

tsan

dim

por

tsto

GD

P;finan

cial

dep

this

the

rati

oof

M2

toG

DP;G

DP

per

capit

ais

the

loga

rith

mof

const

ant

GD

Pper

capit

a;ru

leof

law

,pol

itic

alst

ability,

voic

ean

dac

count

ability,

and

gove

rnm

ent

effici

ency

are

from

the

Gov

ernan

ceIn

dic

ator

sD

atab

ase;

and

dem

ocra

cy,au

tocr

acy,

and

pol

ity

are

take

nfr

omth

ePol

ity

Dat

abas

e.∗

den

otes

sign

ifica

nce

atth

e5

per

cent

leve

l.

Vol. 10 No. 1 Central Bank Transparency and Independence 213

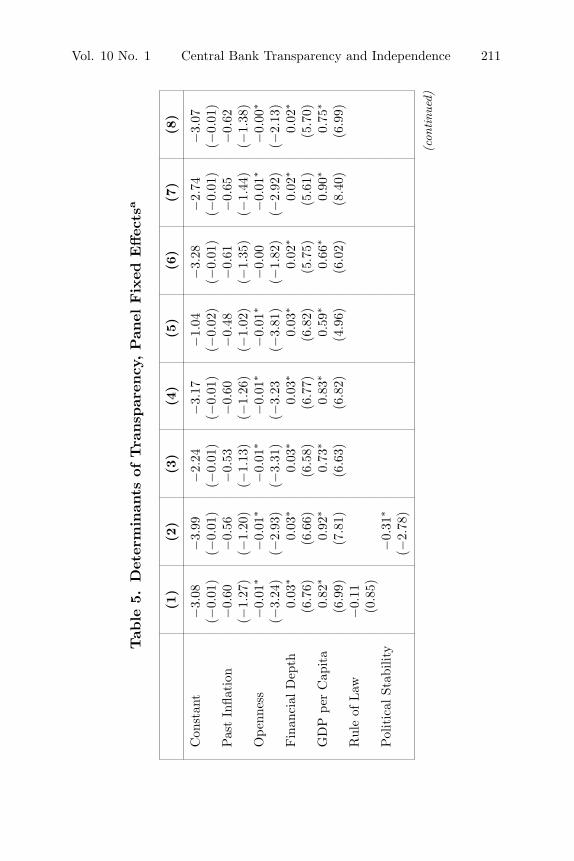

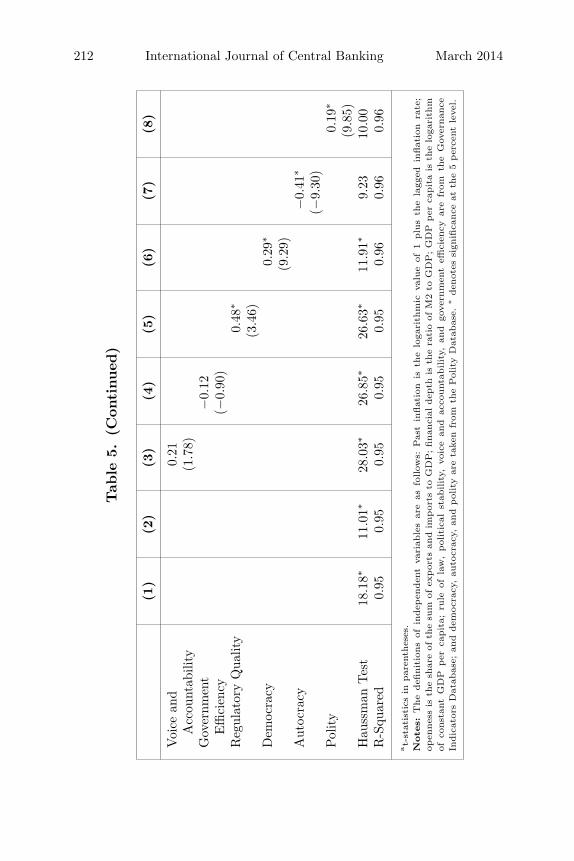

Table 5 reports the analogous panel estimates, with countryeffects included in all columns.27 Since these results eliminate time-invariant country-specific effects, they can be interpreted as ana-lyzing the determinants of changes in transparency over time. Herethe positive effects of higher per capita incomes, deeper financialmarkets, more economic openness, and stronger political institu-tions come through even more clearly than before. In contrast, pastinflation is uniformly insignificant, reinforcing our earlier skepticismabout the robustness of this variable.

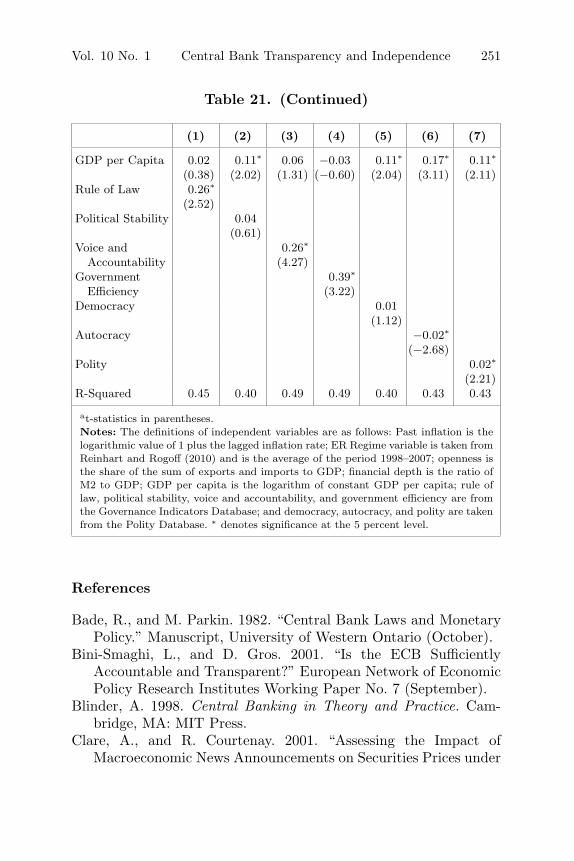

Some previous studies, including our own, have suggested thattransparency becomes more important as a mechanism of monetarypolicy accountability when countries adopt a more flexible exchangerate and success at maintaining a peg no longer suffices for verifyingthe ability of the central bank to attain its monetary policy goals.In table 21 (in appendix 2) we add a measure of the flexibility ofthe exchange rate regime. This index is based on the IMF coarse-classification data provided by Ilzetzki, Reinhart, and Rogoff (2008)and takes the score 1 to 6, where a higher score indicates a moreflexible exchange rate regime. Data on the exchange rate regime areavailable only through 2007, making for a shorter sample, which iswhy we relegate these results to an appendix. They confirm the pre-sumption that countries with more flexible exchange rate regimesalso tend to have more transparent central banks. Otherwise, thesealternative estimates are broadly consistent with those in the text.28

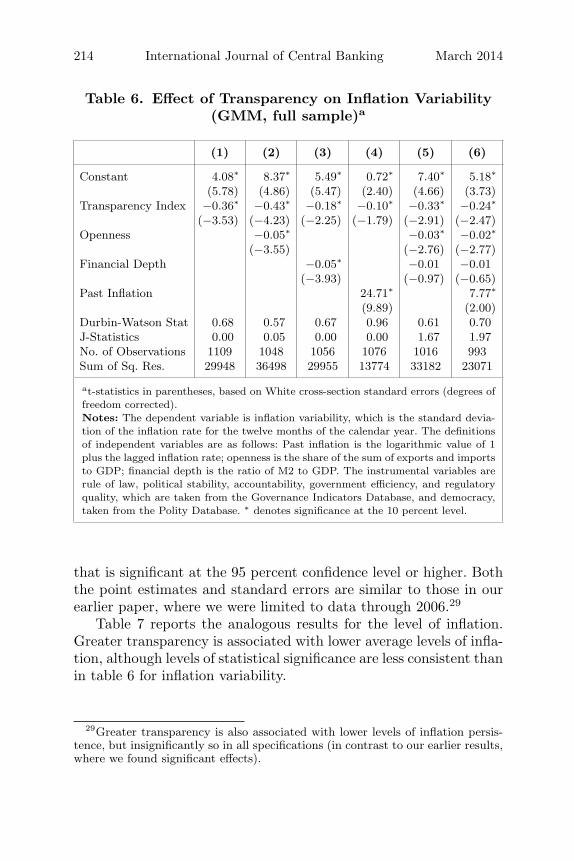

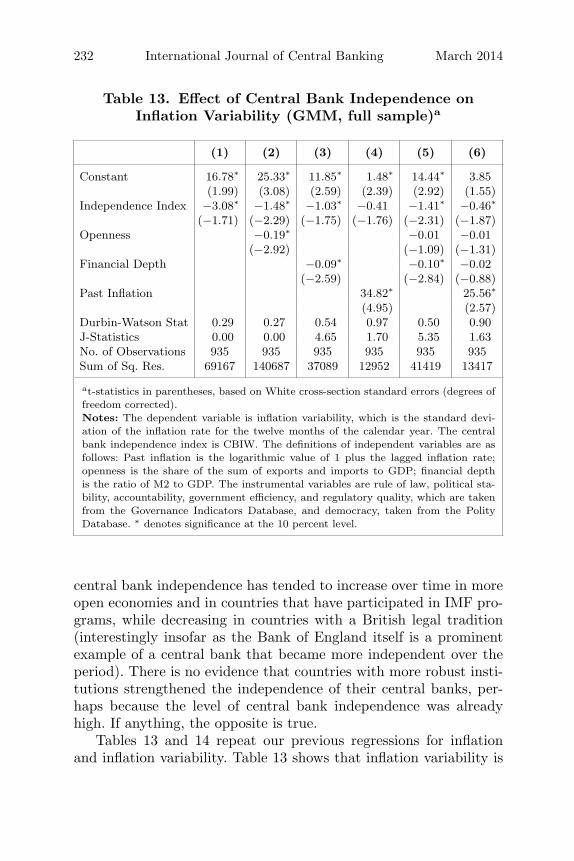

Table 6 updates our earlier analysis of the effects of transparencyon inflation variability, defined as the standard deviation of monthlyinflation in a given year. We use the independent variables in tables4 and 5 as instruments for transparency in table 6 and include asadditional determinants of inflation variability measures of open-ness, financial depth, and past inflation. According to table 6, moreopen economies have less variable inflation, while countries with apast history of inflation experience more nominal variability. Centralbank transparency consistently enters with a negative coefficient

27The variables used here are stationary and cointegrated according to thestandard augmented Dickey-Fuller tests.

28Estimates on panel data including country fixed effects are again consistentwith the just-mentioned results, although the exchange-rate-regime variable isnot consistently significant at the same high level of confidence.

214 International Journal of Central Banking March 2014

Table 6. Effect of Transparency on Inflation Variability(GMM, full sample)a

(1) (2) (3) (4) (5) (6)

Constant 4.08∗ 8.37∗ 5.49∗ 0.72∗ 7.40∗ 5.18∗

(5.78) (4.86) (5.47) (2.40) (4.66) (3.73)Transparency Index −0.36∗ −0.43∗ −0.18∗ −0.10∗ −0.33∗ −0.24∗

(−3.53) (−4.23) (−2.25) (−1.79) (−2.91) (−2.47)Openness −0.05∗ −0.03∗ −0.02∗

(−3.55) (−2.76) (−2.77)Financial Depth −0.05∗ −0.01 −0.01

(−3.93) (−0.97) (−0.65)Past Inflation 24.71∗ 7.77∗

(9.89) (2.00)Durbin-Watson Stat 0.68 0.57 0.67 0.96 0.61 0.70J-Statistics 0.00 0.05 0.00 0.00 1.67 1.97No. of Observations 1109 1048 1056 1076 1016 993Sum of Sq. Res. 29948 36498 29955 13774 33182 23071

at-statistics in parentheses, based on White cross-section standard errors (degrees offreedom corrected).Notes: The dependent variable is inflation variability, which is the standard devia-tion of the inflation rate for the twelve months of the calendar year. The definitionsof independent variables are as follows: Past inflation is the logarithmic value of 1plus the lagged inflation rate; openness is the share of the sum of exports and importsto GDP; financial depth is the ratio of M2 to GDP. The instrumental variables arerule of law, political stability, accountability, government efficiency, and regulatoryquality, which are taken from the Governance Indicators Database, and democracy,taken from the Polity Database. ∗ denotes significance at the 10 percent level.

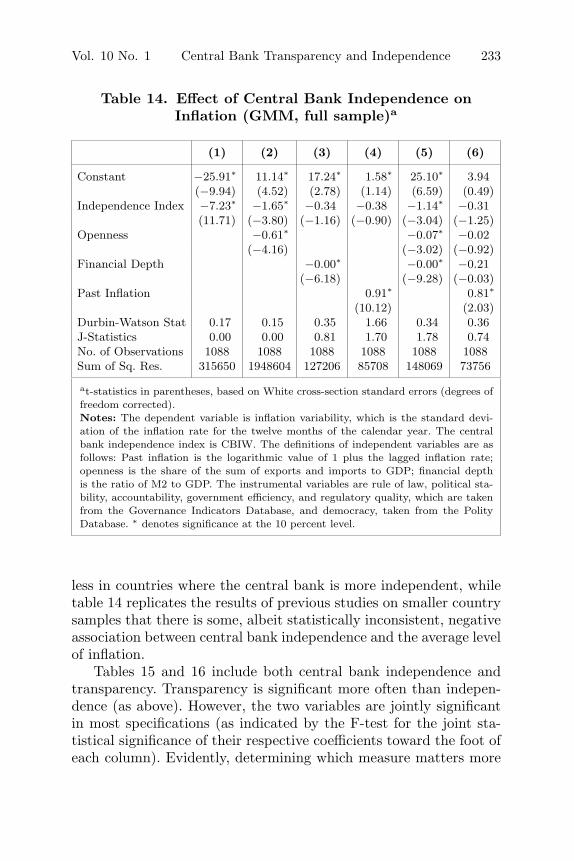

that is significant at the 95 percent confidence level or higher. Boththe point estimates and standard errors are similar to those in ourearlier paper, where we were limited to data through 2006.29

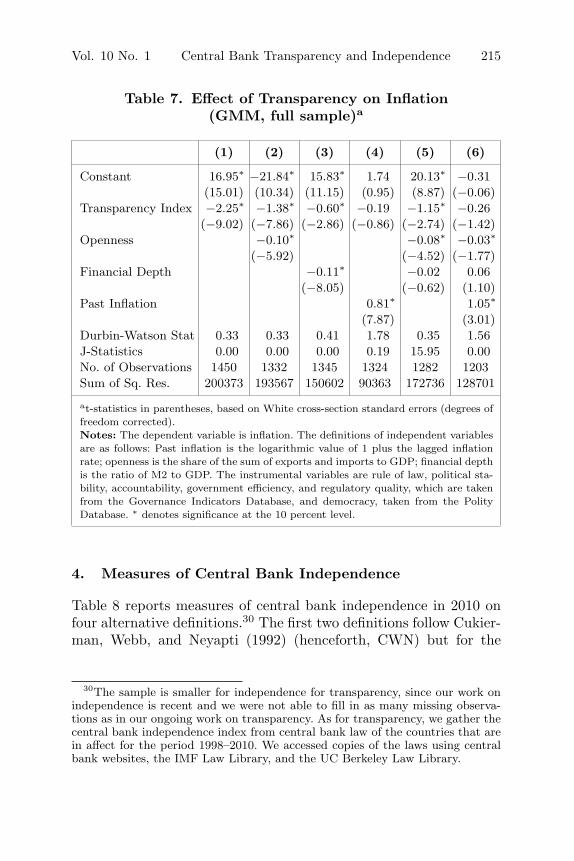

Table 7 reports the analogous results for the level of inflation.Greater transparency is associated with lower average levels of infla-tion, although levels of statistical significance are less consistent thanin table 6 for inflation variability.

29Greater transparency is also associated with lower levels of inflation persis-tence, but insignificantly so in all specifications (in contrast to our earlier results,where we found significant effects).

Vol. 10 No. 1 Central Bank Transparency and Independence 215

Table 7. Effect of Transparency on Inflation(GMM, full sample)a

(1) (2) (3) (4) (5) (6)

Constant 16.95∗ −21.84∗ 15.83∗ 1.74 20.13∗ −0.31(15.01) (10.34) (11.15) (0.95) (8.87) (−0.06)

Transparency Index −2.25∗ −1.38∗ −0.60∗ −0.19 −1.15∗ −0.26(−9.02) (−7.86) (−2.86) (−0.86) (−2.74) (−1.42)

Openness −0.10∗ −0.08∗ −0.03∗

(−5.92) (−4.52) (−1.77)Financial Depth −0.11∗ −0.02 0.06

(−8.05) (−0.62) (1.10)Past Inflation 0.81∗ 1.05∗

(7.87) (3.01)Durbin-Watson Stat 0.33 0.33 0.41 1.78 0.35 1.56J-Statistics 0.00 0.00 0.00 0.19 15.95 0.00No. of Observations 1450 1332 1345 1324 1282 1203Sum of Sq. Res. 200373 193567 150602 90363 172736 128701

at-statistics in parentheses, based on White cross-section standard errors (degrees offreedom corrected).Notes: The dependent variable is inflation. The definitions of independent variablesare as follows: Past inflation is the logarithmic value of 1 plus the lagged inflationrate; openness is the share of the sum of exports and imports to GDP; financial depthis the ratio of M2 to GDP. The instrumental variables are rule of law, political sta-bility, accountability, government efficiency, and regulatory quality, which are takenfrom the Governance Indicators Database, and democracy, taken from the PolityDatabase. ∗ denotes significance at the 10 percent level.

4. Measures of Central Bank Independence

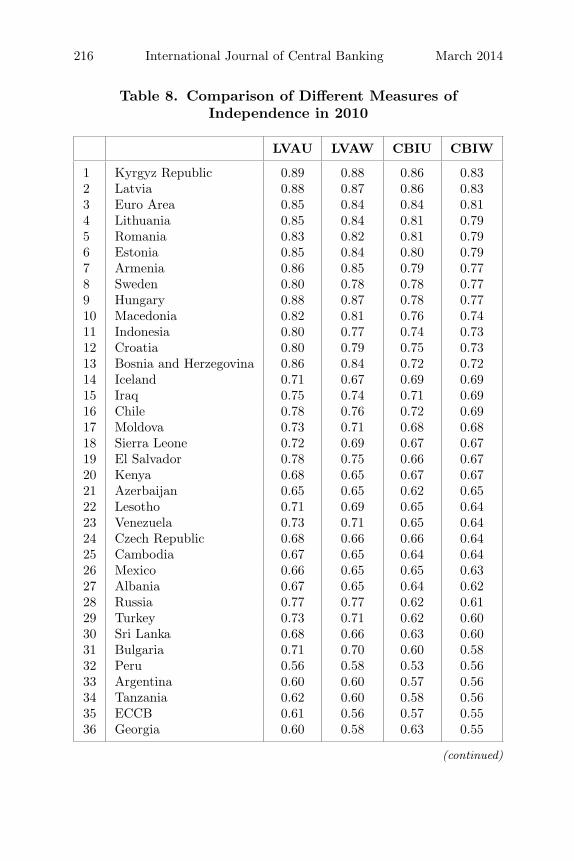

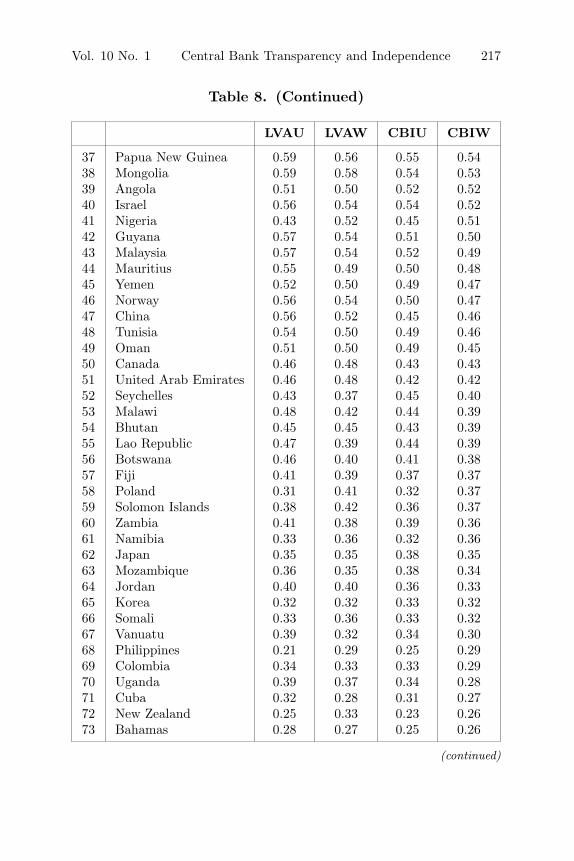

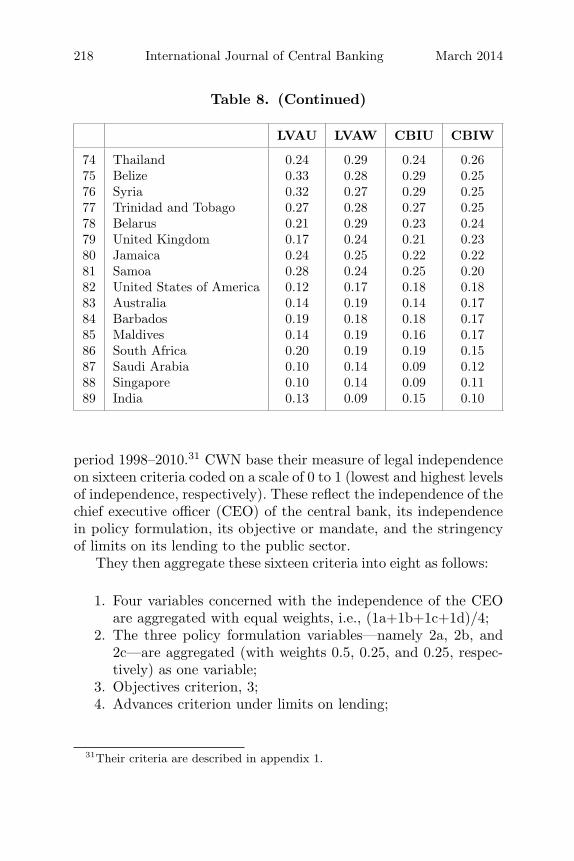

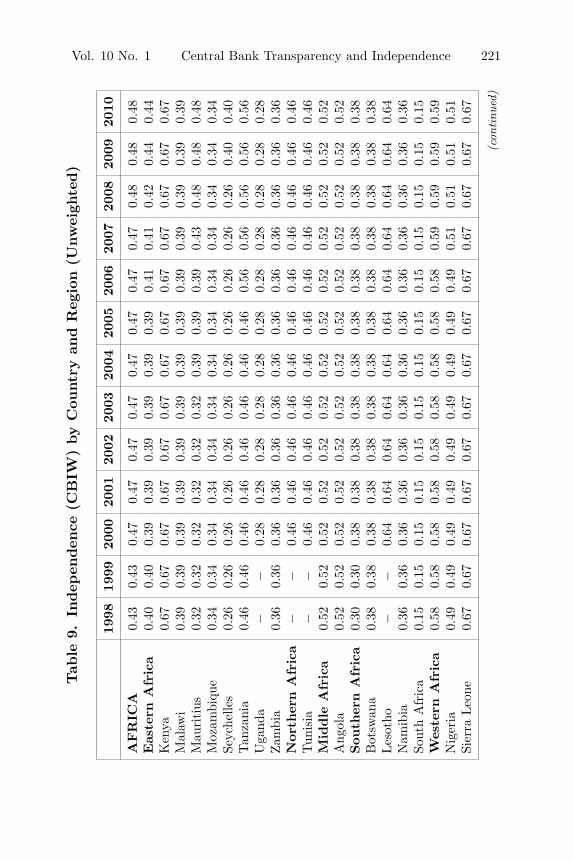

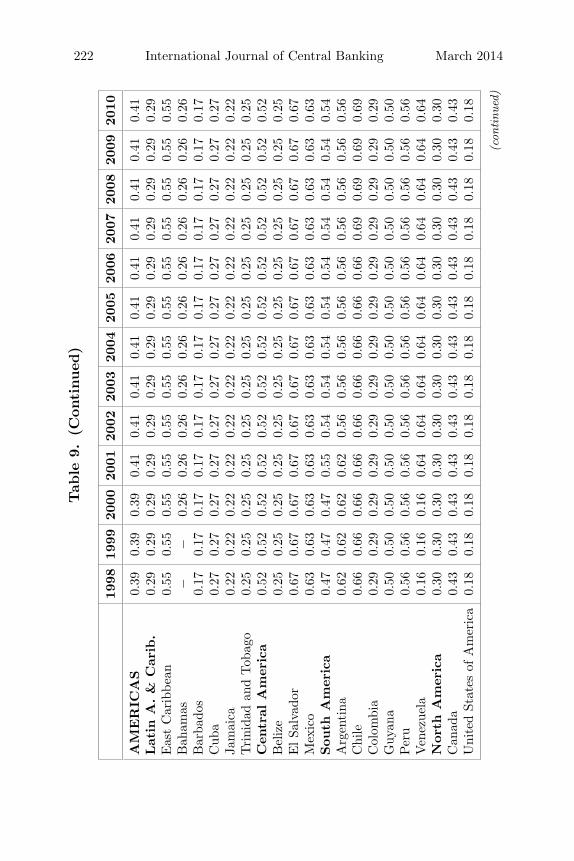

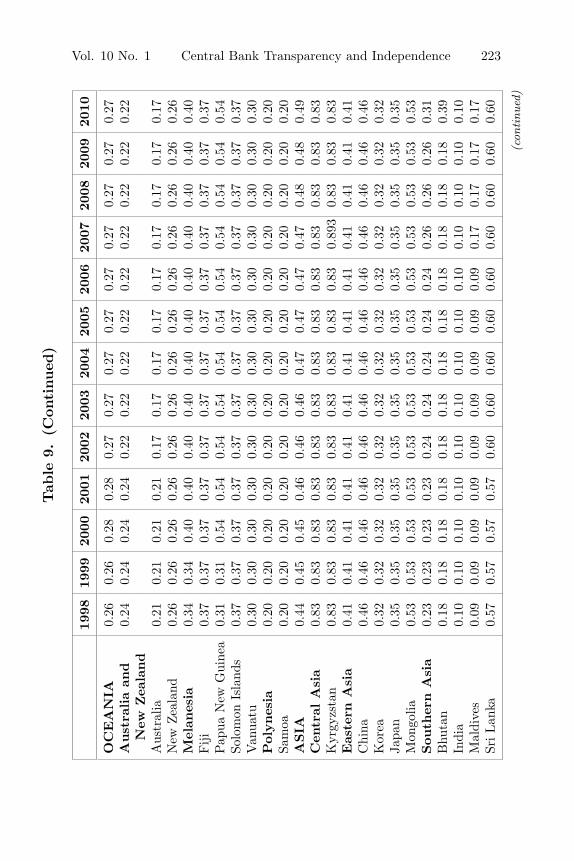

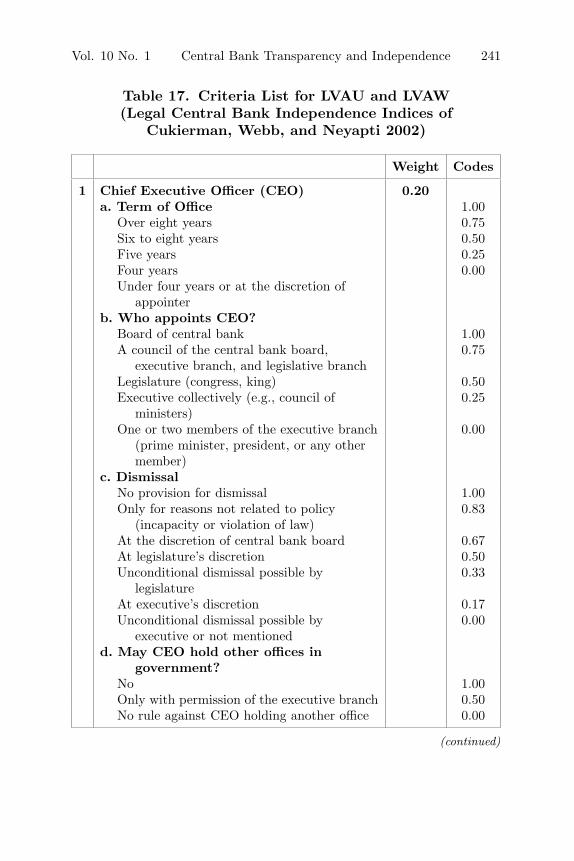

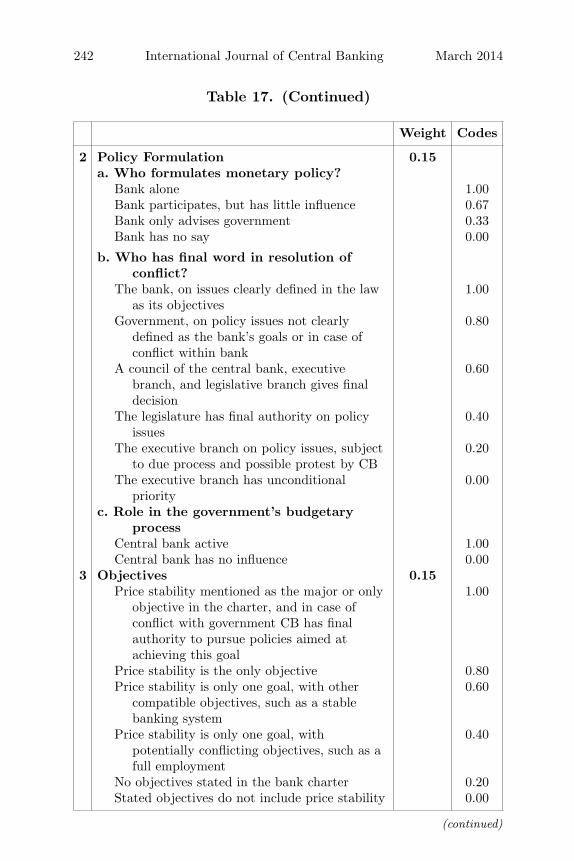

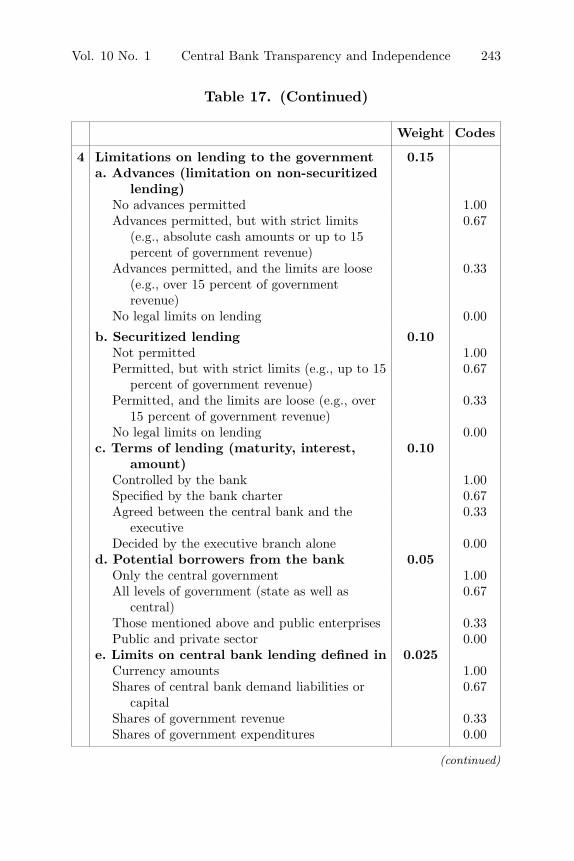

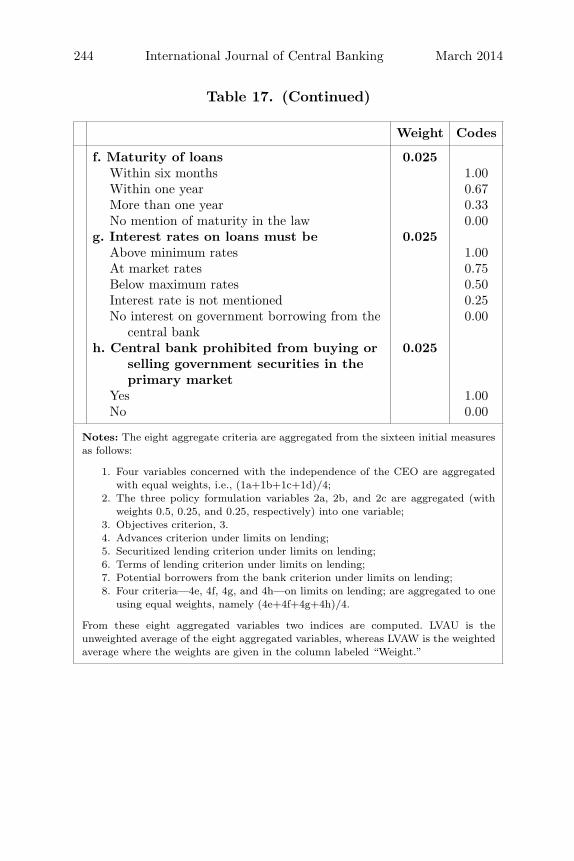

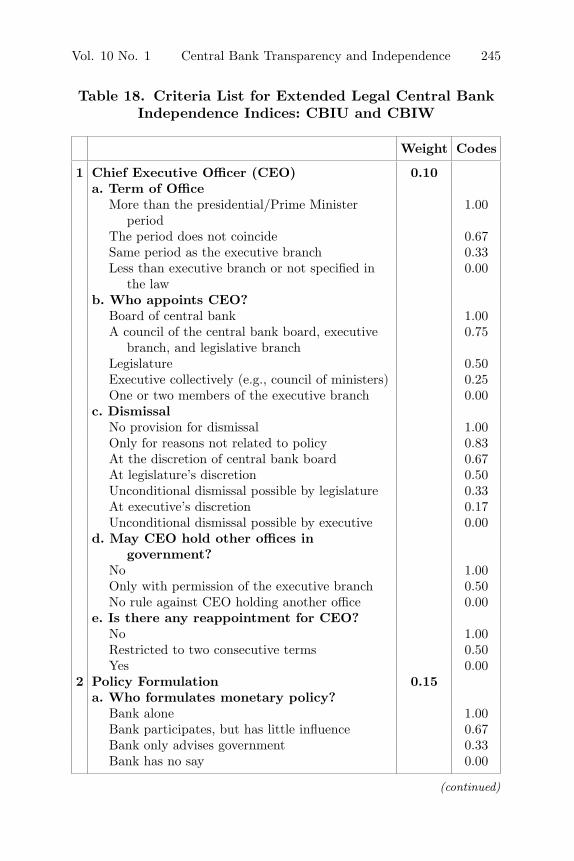

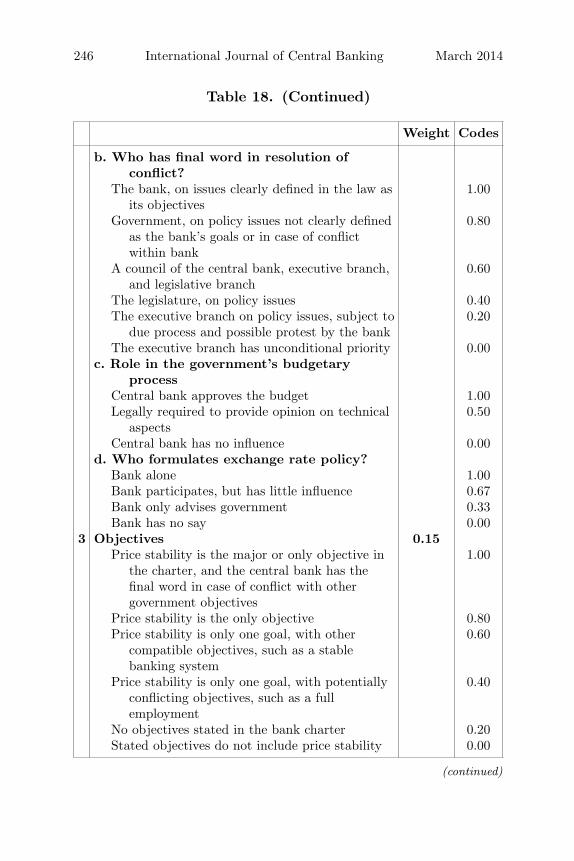

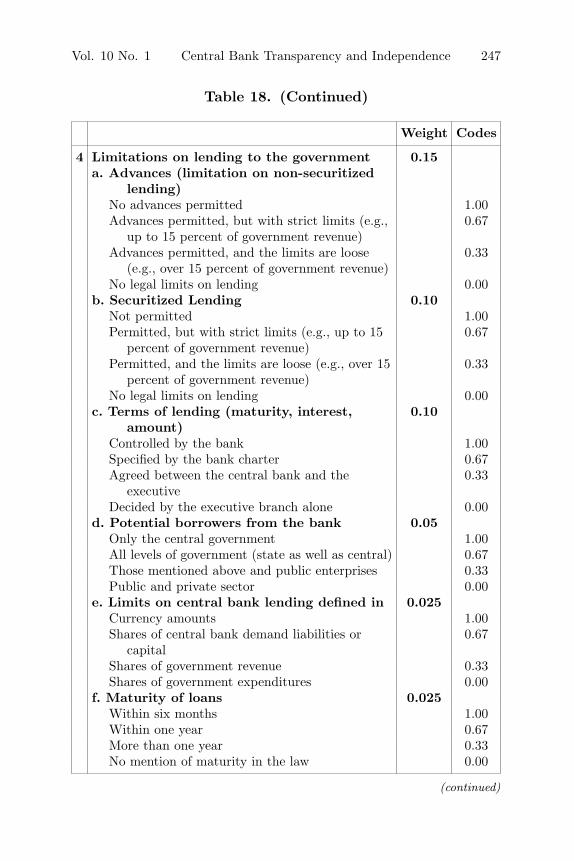

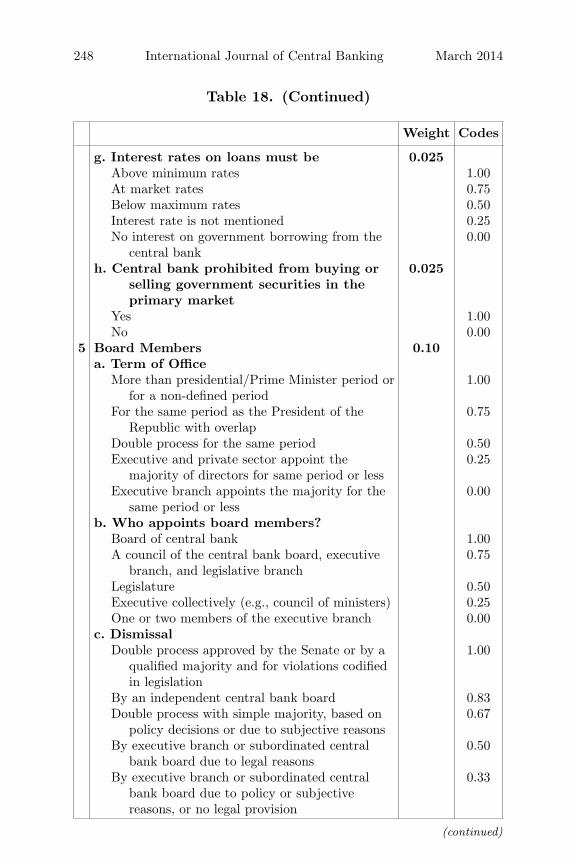

Table 8 reports measures of central bank independence in 2010 onfour alternative definitions.30 The first two definitions follow Cukier-man, Webb, and Neyapti (1992) (henceforth, CWN) but for the

30The sample is smaller for independence for transparency, since our work onindependence is recent and we were not able to fill in as many missing observa-tions as in our ongoing work on transparency. As for transparency, we gather thecentral bank independence index from central bank law of the countries that arein affect for the period 1998–2010. We accessed copies of the laws using centralbank websites, the IMF Law Library, and the UC Berkeley Law Library.

216 International Journal of Central Banking March 2014

Table 8. Comparison of Different Measures ofIndependence in 2010

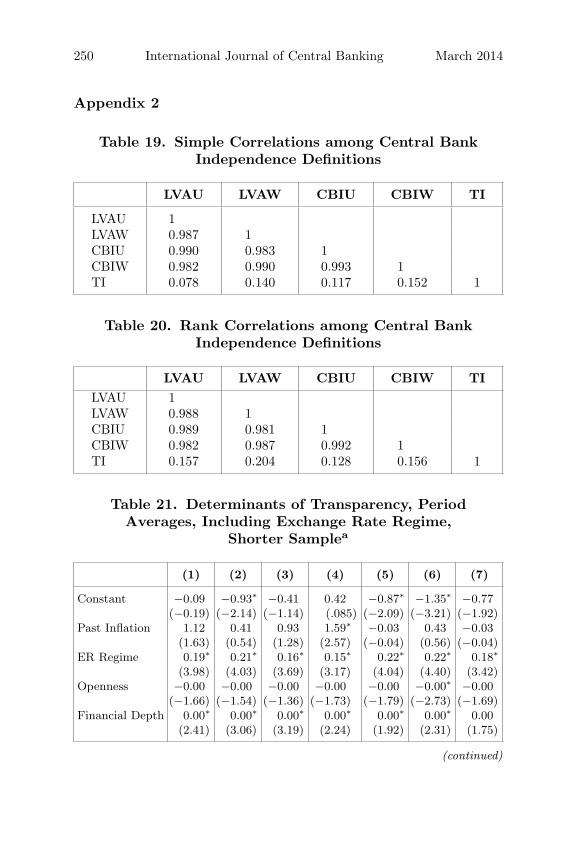

LVAU LVAW CBIU CBIW

1 Kyrgyz Republic 0.89 0.88 0.86 0.832 Latvia 0.88 0.87 0.86 0.833 Euro Area 0.85 0.84 0.84 0.814 Lithuania 0.85 0.84 0.81 0.795 Romania 0.83 0.82 0.81 0.796 Estonia 0.85 0.84 0.80 0.797 Armenia 0.86 0.85 0.79 0.778 Sweden 0.80 0.78 0.78 0.779 Hungary 0.88 0.87 0.78 0.7710 Macedonia 0.82 0.81 0.76 0.7411 Indonesia 0.80 0.77 0.74 0.7312 Croatia 0.80 0.79 0.75 0.7313 Bosnia and Herzegovina 0.86 0.84 0.72 0.7214 Iceland 0.71 0.67 0.69 0.6915 Iraq 0.75 0.74 0.71 0.6916 Chile 0.78 0.76 0.72 0.6917 Moldova 0.73 0.71 0.68 0.6818 Sierra Leone 0.72 0.69 0.67 0.6719 El Salvador 0.78 0.75 0.66 0.6720 Kenya 0.68 0.65 0.67 0.6721 Azerbaijan 0.65 0.65 0.62 0.6522 Lesotho 0.71 0.69 0.65 0.6423 Venezuela 0.73 0.71 0.65 0.6424 Czech Republic 0.68 0.66 0.66 0.6425 Cambodia 0.67 0.65 0.64 0.6426 Mexico 0.66 0.65 0.65 0.6327 Albania 0.67 0.65 0.64 0.6228 Russia 0.77 0.77 0.62 0.6129 Turkey 0.73 0.71 0.62 0.6030 Sri Lanka 0.68 0.66 0.63 0.6031 Bulgaria 0.71 0.70 0.60 0.5832 Peru 0.56 0.58 0.53 0.5633 Argentina 0.60 0.60 0.57 0.5634 Tanzania 0.62 0.60 0.58 0.5635 ECCB 0.61 0.56 0.57 0.5536 Georgia 0.60 0.58 0.63 0.55

(continued)

Vol. 10 No. 1 Central Bank Transparency and Independence 217

Table 8. (Continued)

LVAU LVAW CBIU CBIW

37 Papua New Guinea 0.59 0.56 0.55 0.5438 Mongolia 0.59 0.58 0.54 0.5339 Angola 0.51 0.50 0.52 0.5240 Israel 0.56 0.54 0.54 0.5241 Nigeria 0.43 0.52 0.45 0.5142 Guyana 0.57 0.54 0.51 0.5043 Malaysia 0.57 0.54 0.52 0.4944 Mauritius 0.55 0.49 0.50 0.4845 Yemen 0.52 0.50 0.49 0.4746 Norway 0.56 0.54 0.50 0.4747 China 0.56 0.52 0.45 0.4648 Tunisia 0.54 0.50 0.49 0.4649 Oman 0.51 0.50 0.49 0.4550 Canada 0.46 0.48 0.43 0.4351 United Arab Emirates 0.46 0.48 0.42 0.4252 Seychelles 0.43 0.37 0.45 0.4053 Malawi 0.48 0.42 0.44 0.3954 Bhutan 0.45 0.45 0.43 0.3955 Lao Republic 0.47 0.39 0.44 0.3956 Botswana 0.46 0.40 0.41 0.3857 Fiji 0.41 0.39 0.37 0.3758 Poland 0.31 0.41 0.32 0.3759 Solomon Islands 0.38 0.42 0.36 0.3760 Zambia 0.41 0.38 0.39 0.3661 Namibia 0.33 0.36 0.32 0.3662 Japan 0.35 0.35 0.38 0.3563 Mozambique 0.36 0.35 0.38 0.3464 Jordan 0.40 0.40 0.36 0.3365 Korea 0.32 0.32 0.33 0.3266 Somali 0.33 0.36 0.33 0.3267 Vanuatu 0.39 0.32 0.34 0.3068 Philippines 0.21 0.29 0.25 0.2969 Colombia 0.34 0.33 0.33 0.2970 Uganda 0.39 0.37 0.34 0.2871 Cuba 0.32 0.28 0.31 0.2772 New Zealand 0.25 0.33 0.23 0.2673 Bahamas 0.28 0.27 0.25 0.26

(continued)

218 International Journal of Central Banking March 2014

Table 8. (Continued)

LVAU LVAW CBIU CBIW

74 Thailand 0.24 0.29 0.24 0.2675 Belize 0.33 0.28 0.29 0.2576 Syria 0.32 0.27 0.29 0.2577 Trinidad and Tobago 0.27 0.28 0.27 0.2578 Belarus 0.21 0.29 0.23 0.2479 United Kingdom 0.17 0.24 0.21 0.2380 Jamaica 0.24 0.25 0.22 0.2281 Samoa 0.28 0.24 0.25 0.2082 United States of America 0.12 0.17 0.18 0.1883 Australia 0.14 0.19 0.14 0.1784 Barbados 0.19 0.18 0.18 0.1785 Maldives 0.14 0.19 0.16 0.1786 South Africa 0.20 0.19 0.19 0.1587 Saudi Arabia 0.10 0.14 0.09 0.1288 Singapore 0.10 0.14 0.09 0.1189 India 0.13 0.09 0.15 0.10

period 1998–2010.31 CWN base their measure of legal independenceon sixteen criteria coded on a scale of 0 to 1 (lowest and highest levelsof independence, respectively). These reflect the independence of thechief executive officer (CEO) of the central bank, its independencein policy formulation, its objective or mandate, and the stringencyof limits on its lending to the public sector.

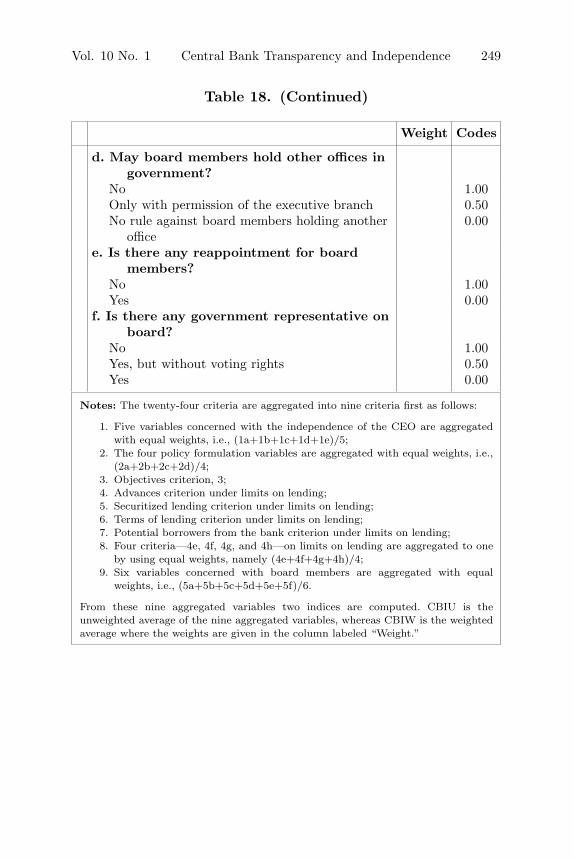

They then aggregate these sixteen criteria into eight as follows:

1. Four variables concerned with the independence of the CEOare aggregated with equal weights, i.e., (1a+1b+1c+1d)/4;

2. The three policy formulation variables—namely 2a, 2b, and2c—are aggregated (with weights 0.5, 0.25, and 0.25, respec-tively) as one variable;

3. Objectives criterion, 3;4. Advances criterion under limits on lending;

31Their criteria are described in appendix 1.

Vol. 10 No. 1 Central Bank Transparency and Independence 219

5. Securitized lending criterion under limits on lending;6. Terms of lending criterion under limits on lending;7. Potential borrowers from the bank criterion under limits on

lending;8. Four criteria—4e, 4f, 4g, and 4h—on limits on lending are

aggregated to one by using equal weights, namely (4e+4f+4g+4h)/4.