BULGARIAN ECONOMY ON THE ROAD TO EUROPEAN UNION AND ECONOMIC

AND MONETARY UNION

IVAN ISKROV

GOVERNORBULGARIAN NATIONAL BANK

14 July 2006Athens

2

OUTLINE

• INITIAL CONDITIONS AND TRANSITION PROCESS

• MACROECONOMIC AND FINANCIAL FRAMEWORK

• ECONOMIC DEVELOPMENTS AND POLICY CHALLENGES

• EU AND EMU PERSPECTIVES

• REGIONAL PERSPECTIVES

3

INITIAL CONDITIONS AND TRANSITION PROCESS

• Planning economy with lack of functioning markets

• Bulgarian economy was highly integrated within Council for Mutual Economic Assistance

• Economy was not subject to competitive pressure

• Distorted incentives

• Transition was a unique process without historical experience to draw from

• Political consensus on society’s priorities was a key prerequisite for successful transition

4

MACROECONOMIC AND FINANCIAL FRAMEWORK

• Euro-based currency board since mid 1997

• Prudent and predictable fiscal policy oriented towards balanced budget or surplus

• Withdrawal of the state from the business through large scale privatization of the state owned enterprises

• Liberalization of the markets – free movement of goods, services and capital

• Government policy oriented towards improvement of investment climate

5

GENERAL GOVERNMENT BALANCE

-4

-3

-2

-1

0

1

2

3

4

1999 2000 2001 2002 2003 2004 2005

% o

f G

DP

Maastricht criterion

6

GOVERNMENT DEBT

0

10

20

30

40

50

60

70

80

90

1999 2000 2001 2002 2003 2004 2005

% o

f G

DP

Maastricht criterion

7

BULGARIAN SOVEREIGN SPREAD

0

200

400

600

800

1000

1200

14/4

/00

14/7

/00

14/1

0/0

0

14/1

/01

14/4

/01

14/7

/01

14/1

0/0

1

14/1

/02

14/4

/02

14/7

/02

14/1

0/0

2

14/1

/03

14/4

/03

14/7

/03

14/1

0/0

3

14/1

/04

14/4

/04

14/7

/04

14/1

0/0

4

14/1

/05

14/4

/05

14/7

/05

14/1

0/0

5

14/1

/06

14/4

/06

b.p.

EMBI+ Bulgarian Sovereign Spread EMBI+ Emerging Market Spread

8

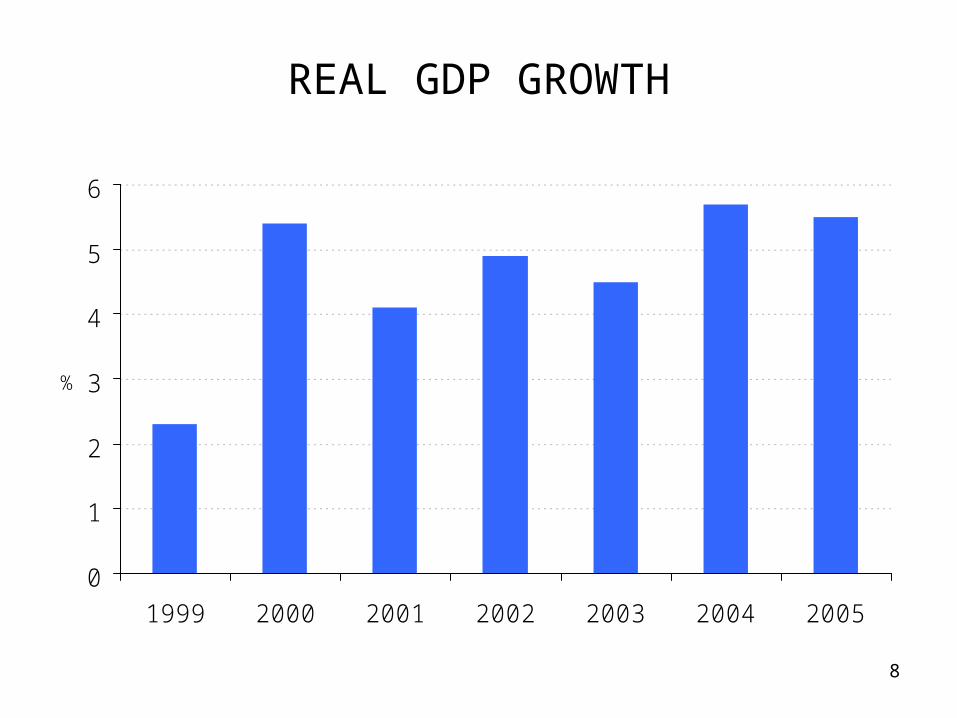

REAL GDP GROWTH

0

1

2

3

4

5

6

1999 2000 2001 2002 2003 2004 2005

%

9

FOREIGN DIRECT INVESTMENTS IN BULGARIA

0

2

4

6

8

10

12

14

16

1999 2000 2001 2002 2003 2004 2005

% o

f G

DP

10

REAL GROWTH OF GROSS FIXED CAPITAL FORMATION

0

5

10

15

20

25

1999 2000 2001 2002 2003 2004 2005

%

11

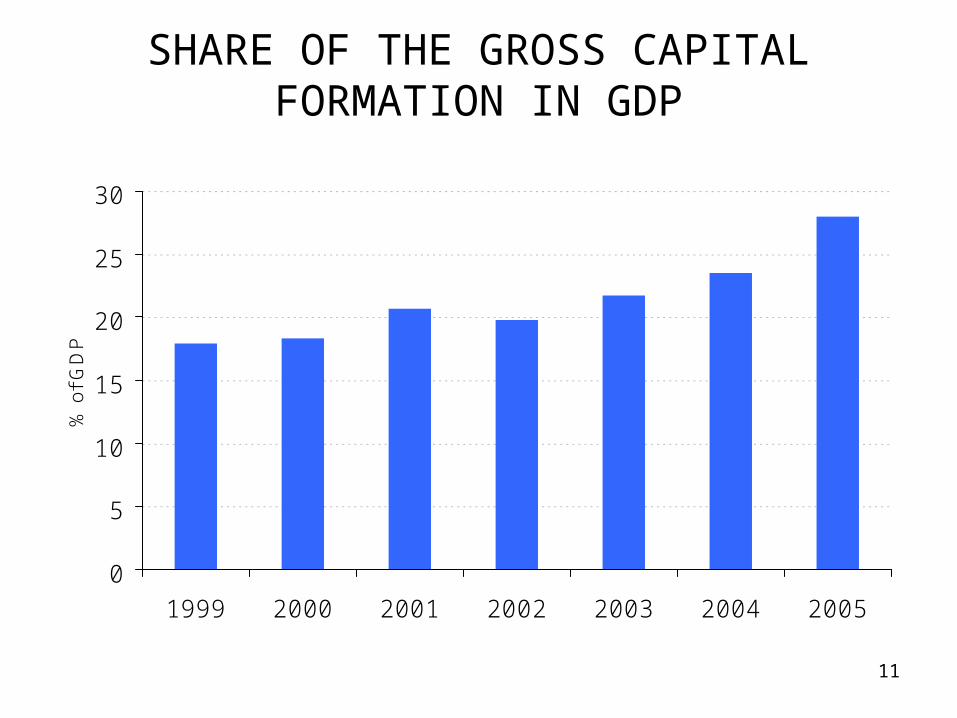

SHARE OF THE GROSS CAPITAL FORMATION IN GDP

0

5

10

15

20

25

30

1999 2000 2001 2002 2003 2004 2005

% o

f G

DP

12

GROWTH OF THE REAL GDP PER PERSON EMPLOYED

-4

-2

0

2

4

6

8

10

1999 2000 2001 2002 2003 2004 2005

%

13

GROWTH OF THE UNIT LABOUR COSTS

-8

-6

-4

-2

0

2

4

6

8

10

1999 2000 2001 2002 2003 2004 2005

%

Nominal Unit Labour Costs Real Unit Labour Costs

14

EMPLOYMENT GROWTH

-4

-2

0

2

4

6

8

1999 2000 2001 2002 2003 2004 2005

%

15

UNEMPLOYMENT RATE

0

5

10

15

20

25

1999 2000 2001 2002 2003 2004 2005

%

16

ECONOMIC DEVELOPMENTS AND POLICY CHALLENGES

• High consumption and investment growth

• Dynamic credit growth

• External imbalances

• Limited scope for policy reaction of the central bank

• Limits of conservative fiscal policy

17

REAL GROWTH OF CONSUMPTION

0

1

2

3

4

5

6

7

8

9

10

1999 2000 2001 2002 2003 2004 2005

%

18

SAVINGS AND INVESTMENTS BALANCE

-20

-15

-10

-5

0

5

1999 2000 2001 2002 2003 2004 2005

% o

f G

DP

Current Account Government "S-I" Balance Private Sector "S-I" Balance

19

EXTERNAL POSITION

-25

-20

-15

-10

-5

0

1999 2000 2001 2002 2003 2004 2005

% o

f G

DP

Current Account Balance Trade Balance

20

CREDIT TO THE PRIVATE SECTOR

0

5

10

15

20

25

30

35

40

45

50

1999 2000 2001 2002 2003 2004 2005

% o

f GD

P

21

GROWTH RATE OF THE CREDIT TO THE PRIVATE SECTOR

0

10

20

30

40

50

60

1999 2000 2001 2002 2003 2004 2005 May-06

%

22

EU AND EMU PERSPECTIVES

• BNB and Government signed in 2004 an agreement that defines the strategy for Euro adoption

• Joining Exchange Rate Mechanism II immediately after EU membership

• Maintaining unilaterally currency board at the current exchange rate – BGN 1.95583/EUR 1

• Bulgarian economy is in good position to fulfill Maastricht criteria

• Inflation criterion is a challenge

23

LONG-TERM INTEREST RATES

0

1

2

3

4

5

6

7

8

9

2002 2003 2004 2005

%

Maastricht criterion

24

AVERAGE INFLATION

-4

-2

0

2

4

6

8

10

12Jan

-99

Ju

l-99

Jan

-00

Ju

l-00

Jan

-01

Ju

l-01

Jan

-02

Ju

l-02

Jan

-03

Ju

l-03

Jan

-04

Ju

l-04

Jan

-05

Ju

l-05

Jan

-06

%

Inflation

Maastricht inflation criterion

Inflation excl Administrative Prices and Excise Tax Effects

25

REGIONAL PERSPECTIVES

• Greek business and politicians extended consistent support to economic and political reforms in Bulgaria

• Greek economy has very strong ties with Bulgarian economy through trade of goods and services and direct investments

• The accession of Bulgaria and Romania in EU opens economic opportunities for the Balkans that our region have never had in its history

26

GEOGRAPHICAL STRUCTURE OF FOREIGN TRADE (2005)

4%6%

9%

14%

15%

52%

EUROPEAN UNION BALKAN COUNTRIESOTHER EUROPEAN COUNTRIES (incl Russia)ASIAN COUNTRIESAMERICAN COUNTRIES OTHER

9%

6%

5%

4%

10%

10%

13%

19%

23%

GERMANY ITALY GREECE FRANCEBELGIUM SPAINUK OTHER OLD MEMBER STATESNEW MEMBER STATES

All EU

27

GEOGRAPHICAL STRUCTURE OF THE EU’s FDI IN BULGARIA

5%

6%

7%

7%

12%

7%

8%

12%

35%

AUSTRIA GREECE CYPRUS

GERMANY ITALY BELGIUMNETHERLANDS UK Rest of EU

18%

82%

EU REST OF THE WORLD

All EU

Recommended