Building Innovation Clusters

Innovation Heatmap

André AndonianMarch 14, 2010

CONFIDENTIAL AND PROPRIETARYAny use of this material without specific permission of McKinsey & Company is strictly prohibited

McKinsey & Company | 2

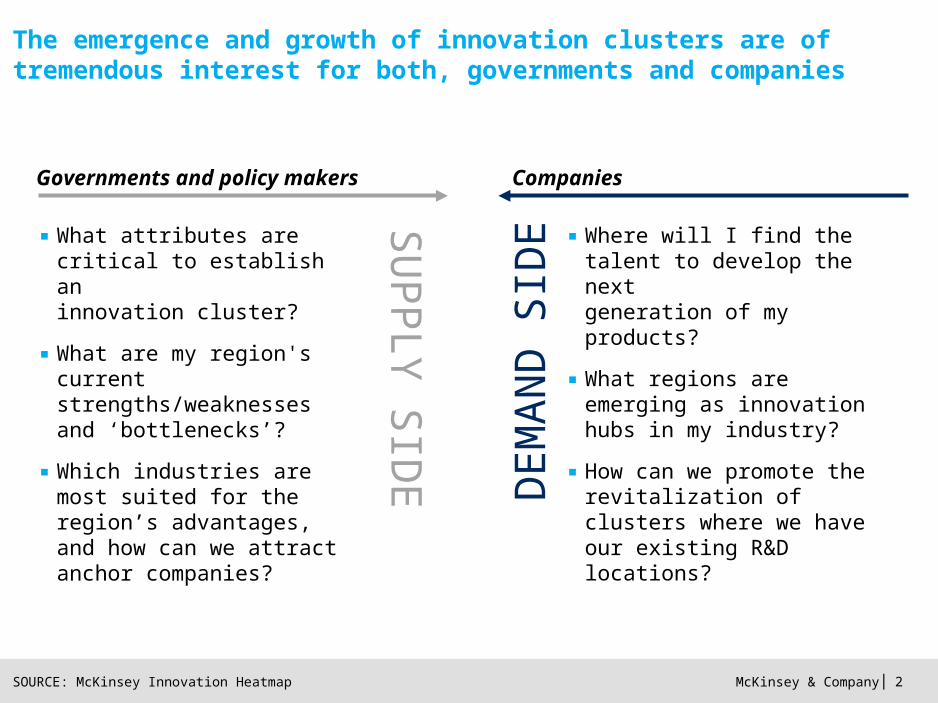

The emergence and growth of innovation clusters are of tremendous interest for both, governments and companies

SOURCE: McKinsey Innovation Heatmap

SU

PP

LY S

IDE

DE

MA

ND

SID

E

Governments and policy makers Companies

▪ What attributes are critical to establish an innovation cluster?

▪ What are my region'scurrent strengths/weaknesses and ‘bottlenecks’?

▪ Which industries are most suited for the region’s advantages, and how can we attract anchor companies?

▪ Where will I find the talent to develop the next generation of my products?

▪ What regions are emerging as innovation hubs in my industry?

▪ How can we promote the revitalization of clusters where we have our existing R&D locations?

McKinsey & Company | 3

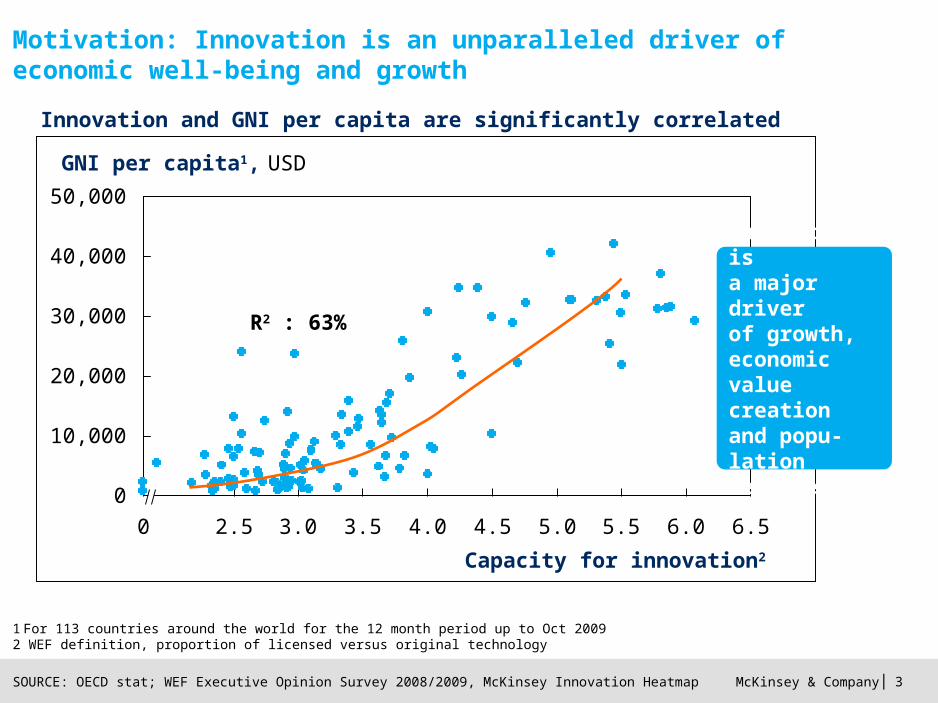

Motivation: Innovation is an unparalleled driver of economic well-being and growth

SOURCE: OECD stat; WEF Executive Opinion Survey 2008/2009, McKinsey Innovation Heatmap

1 For 113 countries around the world for the 12 month period up to Oct 20092 WEF definition, proportion of licensed versus original technology

GNI per capita1, USD

50,000

40,000

30,000

20,000

10,000

0

Capacity for innovation2

6.56.05.55.04.54.03.53.02.50

Innovation and GNI per capita are significantly correlated

R2 : 63%

Innovation is a major driver of growth, economic value creation and popu-lation well-being

McKinsey & Company | 4

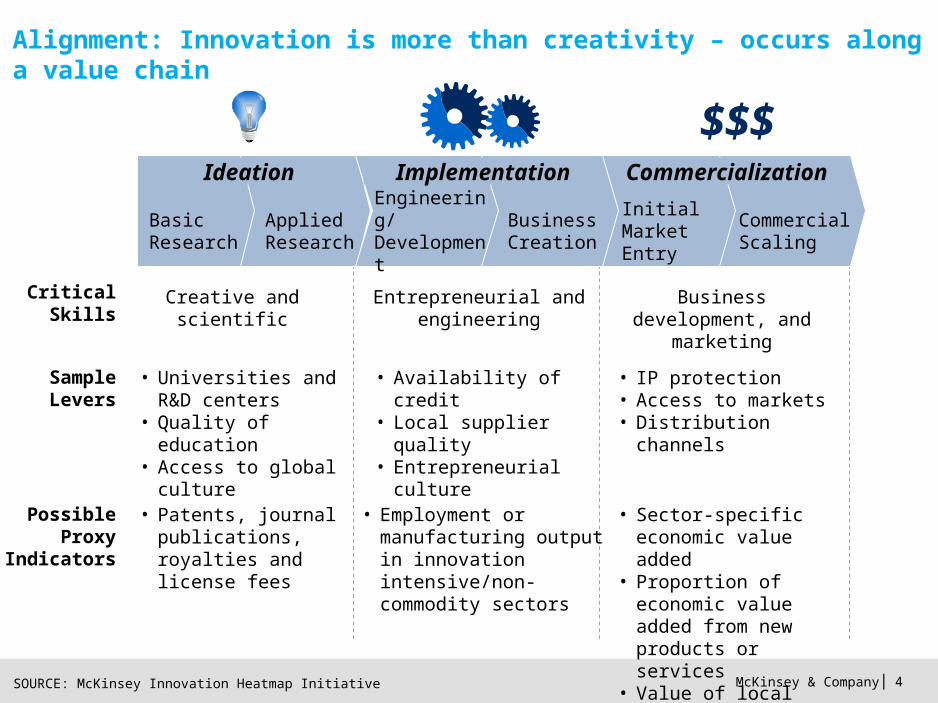

Critical Skills

SampleLevers

PossibleProxy

Indicators

• Universities and R&D centers

• Quality of education• Access to global

culture

• IP protection• Access to markets• Distribution channels

• Availability of credit• Local supplier quality• Entrepreneurial culture

• Patents, journal publications, royalties and license fees

• Sector-specific economic value added

• Proportion of economic value added from new products or services

• Value of local brands

• Employment or manufacturing output in innovation intensive/non-commodity sectors

Creative and scientific

Business development, and marketing

Entrepreneurial and engineering

Alignment: Innovation is more than creativity – occurs along a value chain

SOURCE: McKinsey Innovation Heatmap Initiative

Ideation Implementation Commercialization

Basic Research

Applied Research

Initial Market Entry

Commercial Scaling

Business Creation

Engineering/ Development

$$$

McKinsey & Company | 5 SOURCE: McKinsey

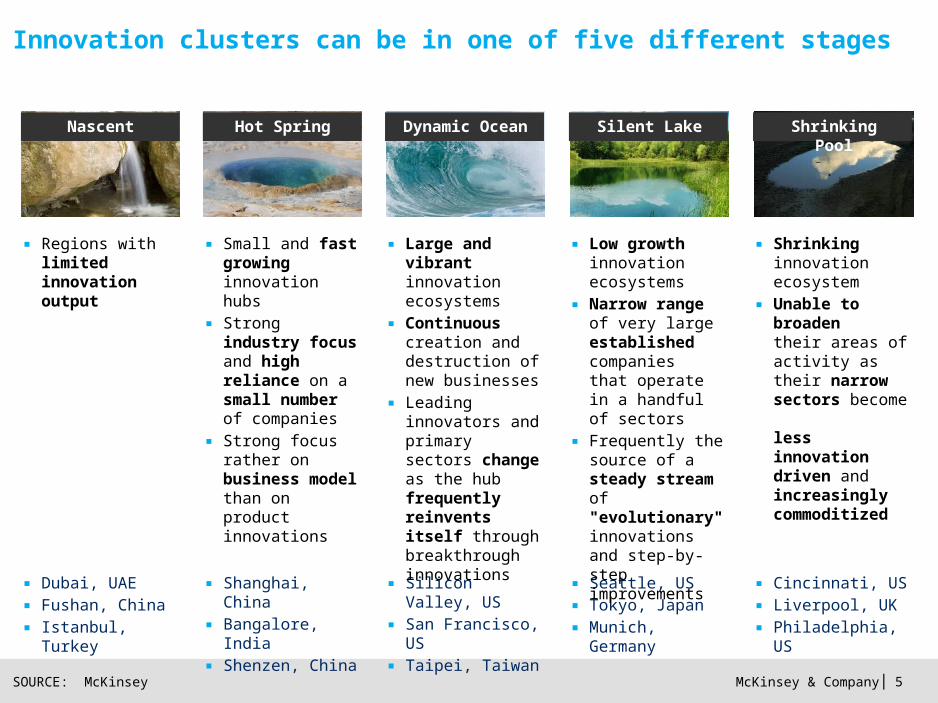

Innovation clusters can be in one of five different stages

▪ Dubai, UAE

▪ Fushan, China

▪ Istanbul, Turkey

Nascent Hot Spring

▪ Shanghai, China

▪ Bangalore, India

▪ Shenzen, China

Dynamic Ocean

▪ Silicon Valley, US

▪ San Francisco, US

▪ Taipei, Taiwan

Silent Lake

▪ Seattle, US

▪ Tokyo, Japan

▪ Munich, Germany

Shrinking Pool

▪ Cincinnati, US

▪ Liverpool, UK

▪ Philadelphia, US

▪ Regions with limited innovation output

▪ Small and fast growing innovation hubs

▪ Strong industry focus and high reliance on a small number of companies

▪ Strong focus rather on business model than on product innovations

▪ Large and vibrant innovation ecosystems

▪ Continuous creation and destruction of new businesses

▪ Leading innovators and primary sectors change as the hub frequently reinvents itself through breakthrough innovations

▪ Low growth innovation ecosystems

▪ Narrow range of very large established companies that operate in a handful of sectors

▪ Frequently the source of a steady stream of "evolutionary" innovations and step-by-step improvements

▪ Shrinking innovation ecosystem

▪ Unable to broaden their areas of activity as their narrow sectors become less innovation driven and increasingly commoditized

McKinsey & Company | 6

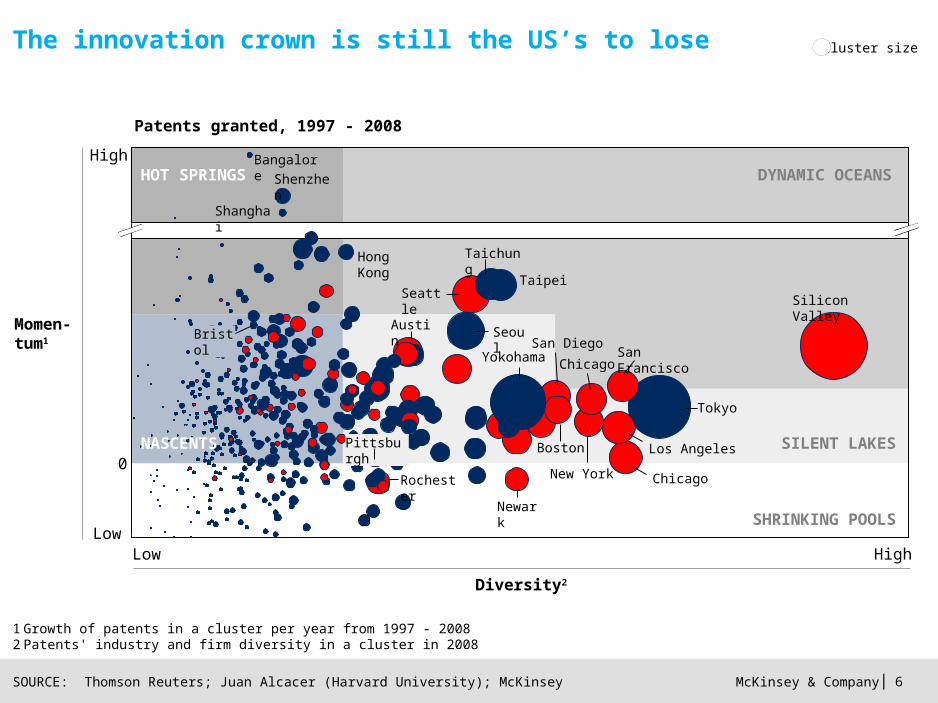

The innovation crown is still the US’s to lose

1 Growth of patents in a cluster per year from 1997 - 20082 Patents' industry and firm diversity in a cluster in 2008

SOURCE: Thomson Reuters; Juan Alcacer (Harvard University); McKinsey

Cluster size

Patents granted, 1997 - 2008

High

Diversity2

High

Momen-tum1

LowLow

0

Bangalore

Shenzhen

Shanghai

Silicon Valley

Tokyo

San Francisco

Taichung

Seattle

Seoul

Chicago

Los Angeles

Hong Kong

Rochester

Newark

Pittsburgh

San Diego

New York

Bristol

SILENT LAKES

DYNAMIC OCEANSHOT SPRINGS

SHRINKING POOLS

NASCENTS

Yokohama

Austin

Taipei

Chicago

Boston

McKinsey & Company | 7

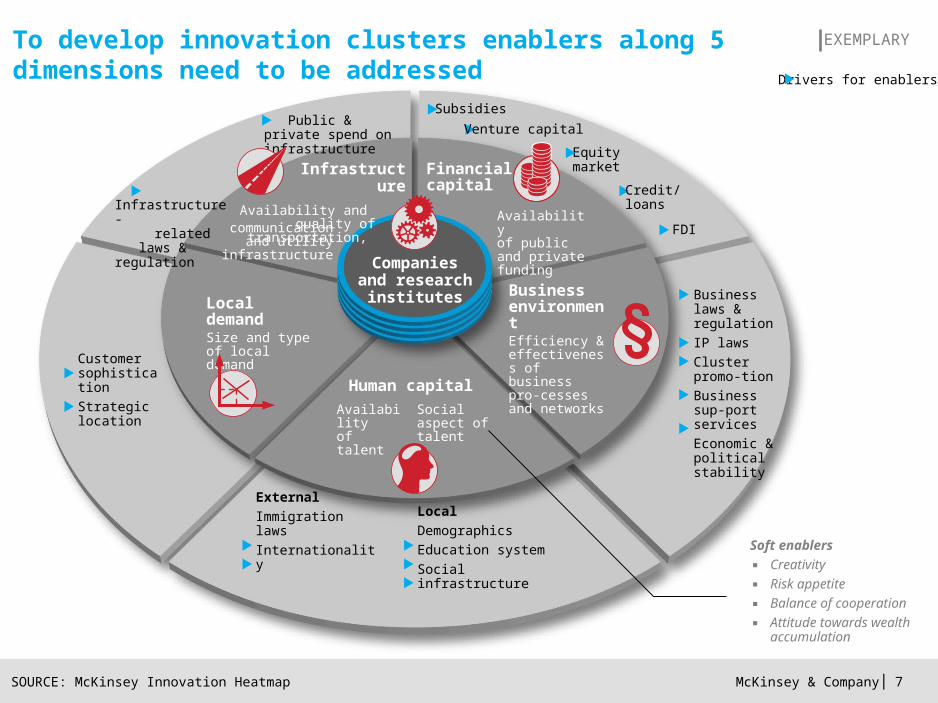

To develop innovation clusters enablers along 5 dimensions need to be addressed

SOURCE: McKinsey Innovation Heatmap

Drivers for enablers

EXEMPLARY

Financial capital

Infrastructure

Local demandSize and type of local demand

Business environmentEfficiency & effectiveness of business pro-cesses and networks

Public & private spend on infrastructure

Customer sophistication

Strategic location

Business laws & regulation

IP laws

Cluster promo-tion

Business sup-port services

Economic & political stability

Human capital

Availability of talent

Social aspect of talent

Soft enablers

▪ Creativity

▪ Risk appetite

▪ Balance of cooperation

▪ Attitude towards wealth accumulation

Local

Demographics

Education system

Social infrastructure

External

Immigration laws

Internationality

Companiesand research

institutes

Equity market

Infrastructure- related laws & regulation

Availability and quality of transportation, Availability

of public and private funding

Credit/loans

FDI

Subsidies

Venture capital

communication and utility infrastructure

McKinsey & Company | 8

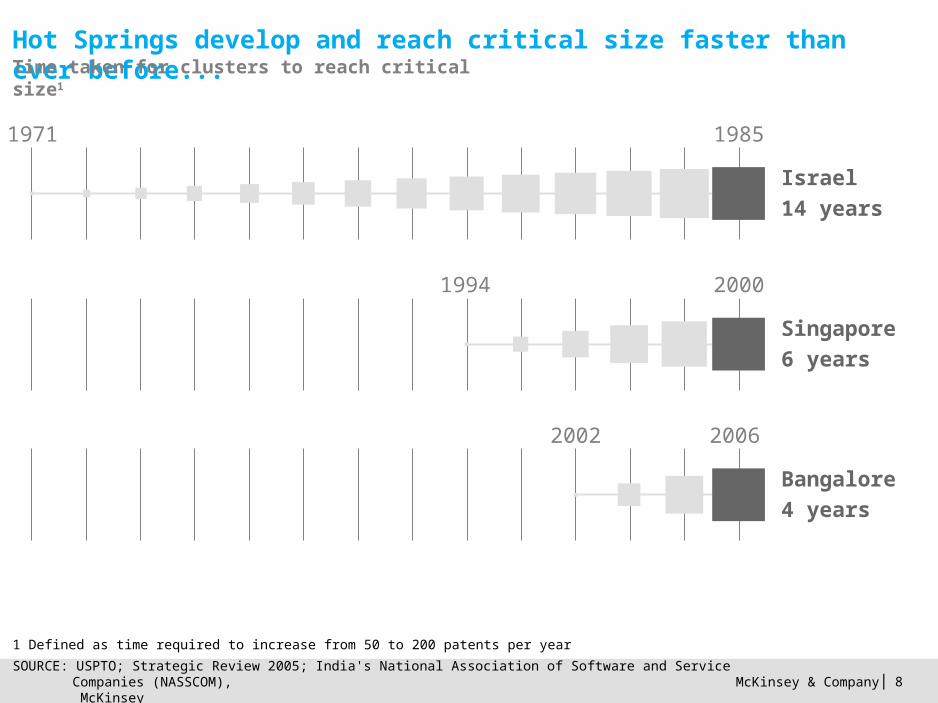

Hot Springs develop and reach critical size faster than ever before...

1 Defined as time required to increase from 50 to 200 patents per year

SOURCE: USPTO; Strategic Review 2005; India's National Association of Software and Service Companies (NASSCOM), McKinsey

Israel

14 years

1971 1985

Singapore

6 years

1994 2000

Bangalore

4 years

2002 2006

Time taken for clusters to reach critical size1

McKinsey & Company | 9 N

asc

en

t

Ho

t S

prin

gs

Dyn

am

ic

Oce

an

s

Sile

nt

La

kes

Sh

rinki

ng

Po

ols

0

20

40

60

80

100

SOURCE: Prequin; Shanghai University; Mastercard; Worldwide Centers of Commerce Index; US Census Bureau; Statistics of US Business (SUSB); McKinsey & Company

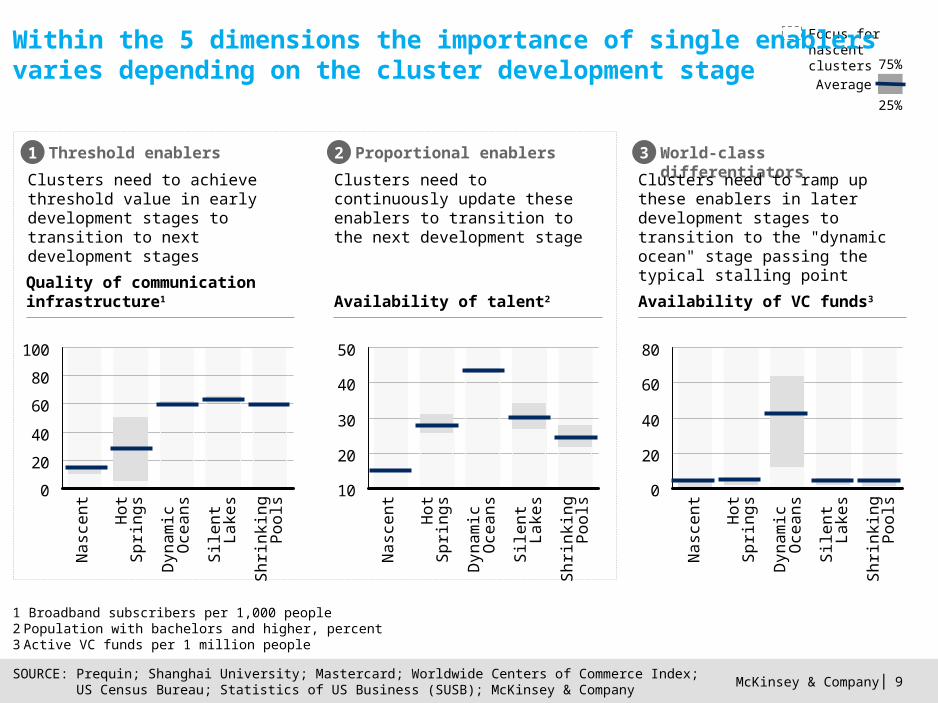

Focus for nascent clusters

Threshold enablers1

Clusters need to achieve threshold value in early development stages to transition to next development stages

World-class differentiators3

Clusters need to ramp up these enablers in later development stages to transition to the "dynamic ocean" stage passing the typical stalling point

Proportional enablers2

Clusters need to continuously update these enablers to transition to the next development stage

10

20

30

40

50

0

20

40

60

80

Na

sce

nt

Ho

t S

prin

gs

Dyn

am

ic

Oce

an

s

Sile

nt

La

kes

Sh

rinki

ng

Po

ols

Na

sce

nt

Ho

t S

prin

gs

Dyn

am

ic

Oce

an

s

Sile

nt

La

kes

Sh

rinki

ng

Po

ols

1 Broadband subscribers per 1,000 people2 Population with bachelors and higher, percent3 Active VC funds per 1 million people

Within the 5 dimensions the importance of single enablers varies depending on the cluster development stage

Quality of communication infrastructure1 Availability of VC funds3Availability of talent2

75%

25%

Average

McKinsey & Company | 10

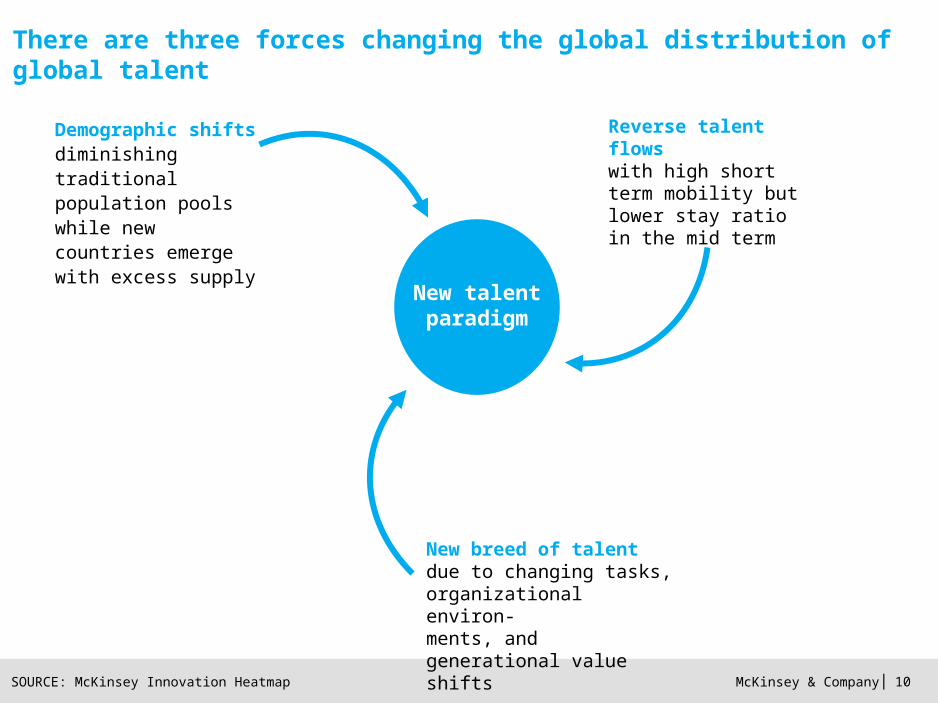

New talent paradigm

Demographic shiftsdiminishing traditional population pools while new countries emerge with excess supply

New breed of talent due to changing tasks, organizational environ-ments, and generational value shifts

Reverse talent flowswith high short term mobility but lower stay ratio in the mid term

There are three forces changing the global distribution of global talent

SOURCE: McKinsey Innovation Heatmap

McKinsey & Company | 11

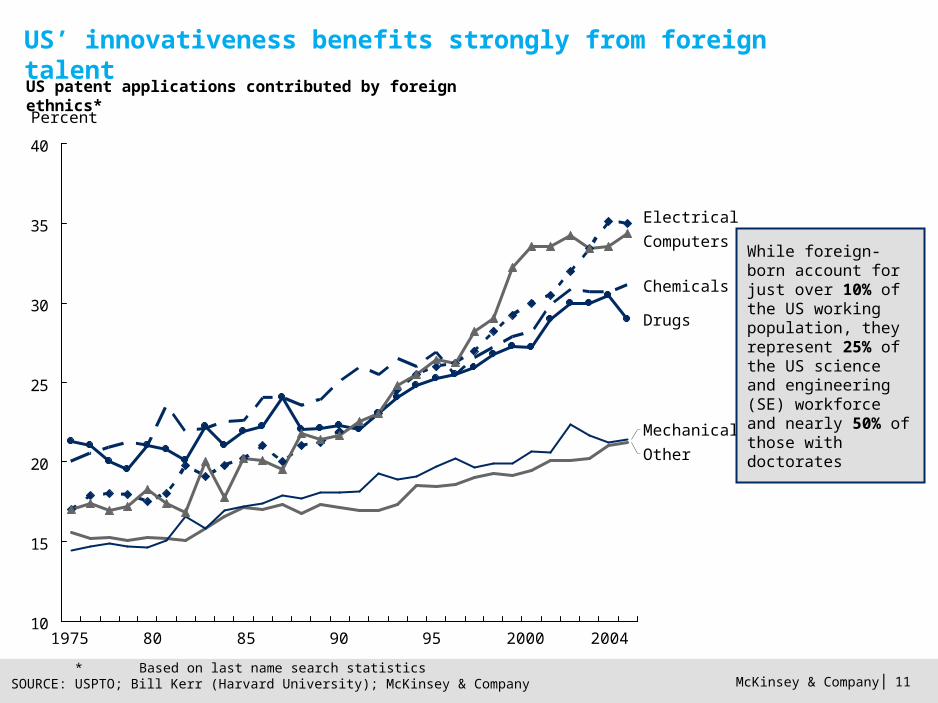

US’ innovativeness benefits strongly from foreign talent

10

15

20

25

30

35

40

Percent

Mechanical

Other

Computers

Electrical

Chemicals

Drugs

US patent applications contributed by foreign ethnics*

While foreign-born account for just over 10% of the US working population, they represent 25% of the US science and engineering (SE) workforce and nearly 50% of those with doctorates

1975 80 85 90 95 2000 2004

* Based on last name search statisticsSOURCE: USPTO; Bill Kerr (Harvard University); McKinsey & Company

McKinsey & Company | 12

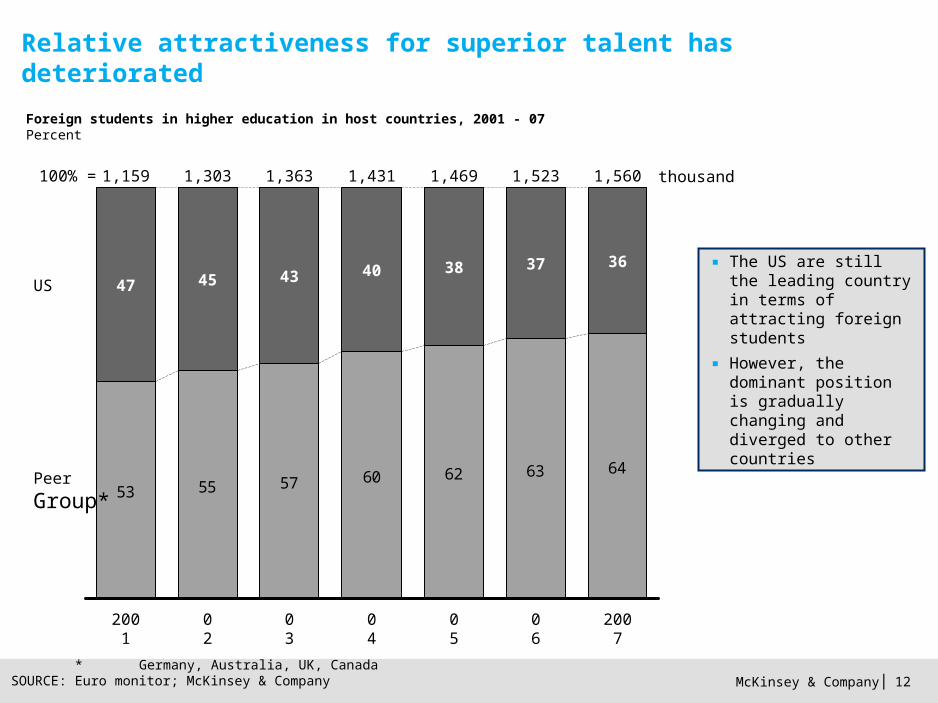

Relative attractiveness for superior talent has deteriorated

Foreign students in higher education in host countries, 2001 - 07Percent

▪ The US are still the leading country in terms of attracting foreign students

▪ However, the dominant position is gradually changing and diverged to other countries

53 55 57 60 62 63 64

1,560

36

06

1,523

37

05

1,469

38

04

1,431

40

03

1,363

43

02

1,303100% =

Peer

Group*

US

2007

45

2001

1,159

47

thousand

* Germany, Australia, UK, CanadaSOURCE: Euro monitor; McKinsey & Company

McKinsey & Company | 13

BACKUP

McKinsey & Company | 14

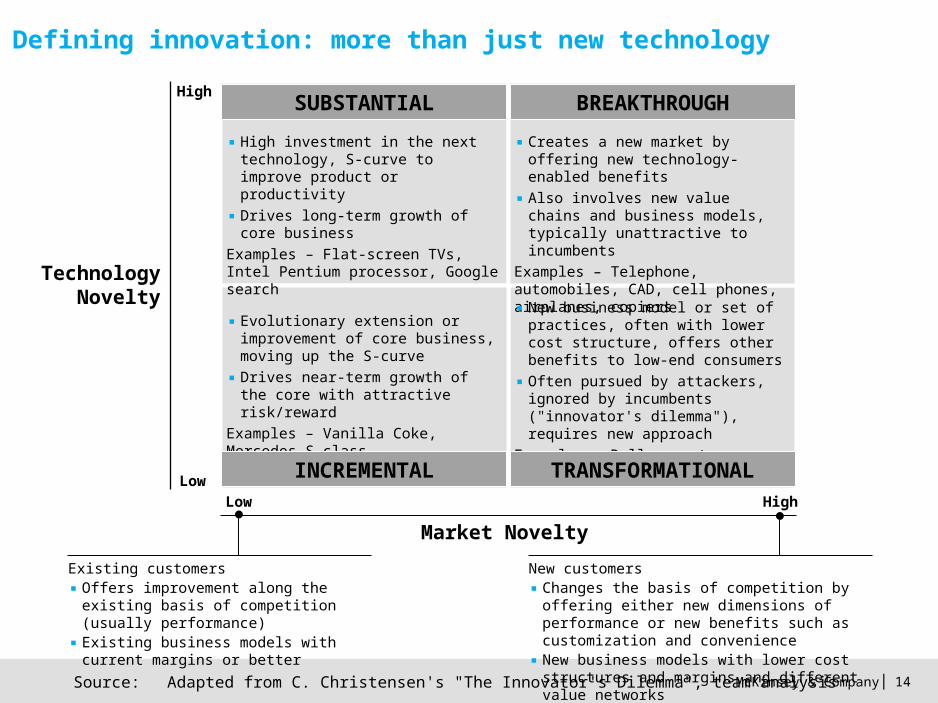

Defining innovation: more than just new technology

Existing customers▪ Offers improvement along the existing basis

of competition (usually performance) ▪ Existing business models with current

margins or better

Technology Novelty

High

Low

Market Novelty

Low High

▪ High investment in the next technology, S-curve to improve product or productivity

▪ Drives long-term growth of core business

Examples – Flat-screen TVs, Intel Pentium processor, Google search

▪ Creates a new market by offering new technology-enabled benefits

▪ Also involves new value chains and business models, typically unattractive to incumbents

Examples – Telephone, automobiles, CAD, cell phones, airplanes, copiers

▪ Evolutionary extension or improvement of core business, moving up the S-curve

▪ Drives near-term growth of the core with attractive risk/reward

Examples – Vanilla Coke, Mercedes S class

▪ New business model or set of practices, often with lower cost structure, offers other benefits to low-end consumers

▪ Often pursued by attackers, ignored by incumbents ("innovator's dilemma"), requires new approach

Examples – Dell computer, Southwest Airlines, Wal-Mart

New customers▪ Changes the basis of competition by offering

either new dimensions of performance or new benefits such as customization and convenience

▪ New business models with lower cost structures and margins and different value networks

INCREMENTAL TRANSFORMATIONAL

SUBSTANTIAL BREAKTHROUGH

Source:Adapted from C. Christensen's "The Innovator's Dilemma", team analysis

McKinsey & Company | 15

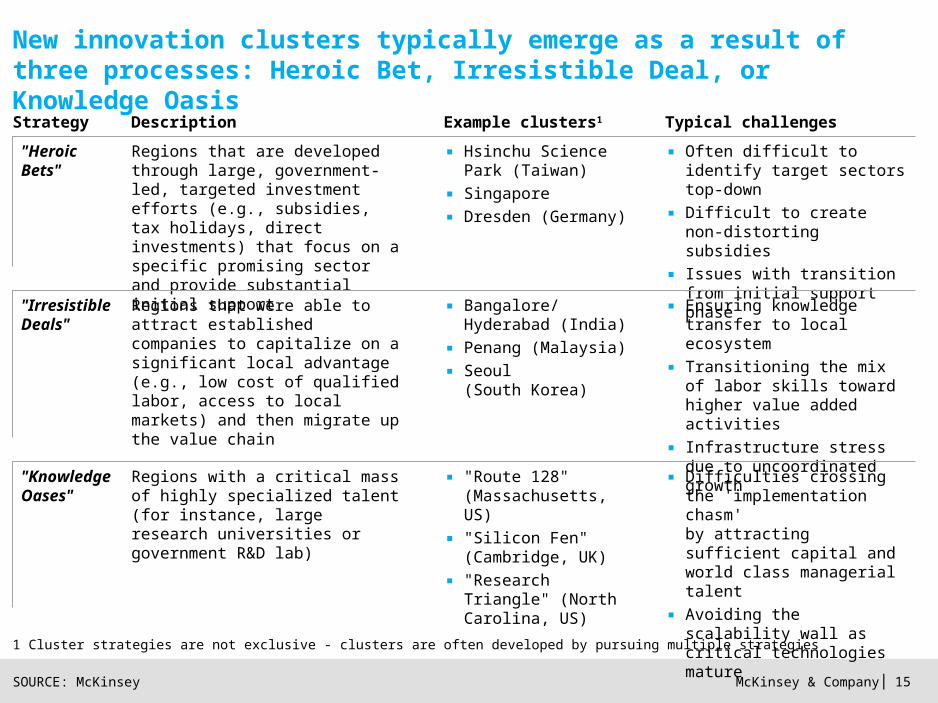

New innovation clusters typically emerge as a result of three processes: Heroic Bet, Irresistible Deal, or Knowledge Oasis

1 Cluster strategies are not exclusive - clusters are often developed by pursuing multiple strategies

SOURCE: McKinsey

Strategy Description Example clusters1 Typical challenges

"Heroic Bets"

Regions that are developed through large, government-led, targeted investment efforts (e.g., subsidies, tax holidays, direct investments) that focus on a specific promising sector and provide substantial initial support

▪ Hsinchu Science Park (Taiwan)

▪ Singapore

▪ Dresden (Germany)

▪ Often difficult to identify target sectors top-down

▪ Difficult to create non-distorting subsidies

▪ Issues with transition from initial support phase

"Irresistible Deals"

Regions that were able to attract established companies to capitalize on a significant local advantage (e.g., low cost of qualified labor, access to local markets) and then migrate up the value chain

▪ Bangalore/ Hyderabad (India)

▪ Penang (Malaysia)

▪ Seoul (South Korea)

▪ Ensuring knowledge transfer to local ecosystem

▪ Transitioning the mix of labor skills toward higher value added activities

▪ Infrastructure stress due to uncoordinated growth

Regions with a critical mass of highly specialized talent (for instance, large research universities or government R&D lab)

"Knowledge Oases"

▪ "Route 128" (Massachusetts, US)

▪ "Silicon Fen" (Cambridge, UK)

▪ "Research Triangle" (North Carolina, US)

▪ Difficulties crossing the 'implementation chasm' by attracting sufficient capital and world class managerial talent

▪ Avoiding the scalability wall as critical technologies mature

McKinsey & Company | 16

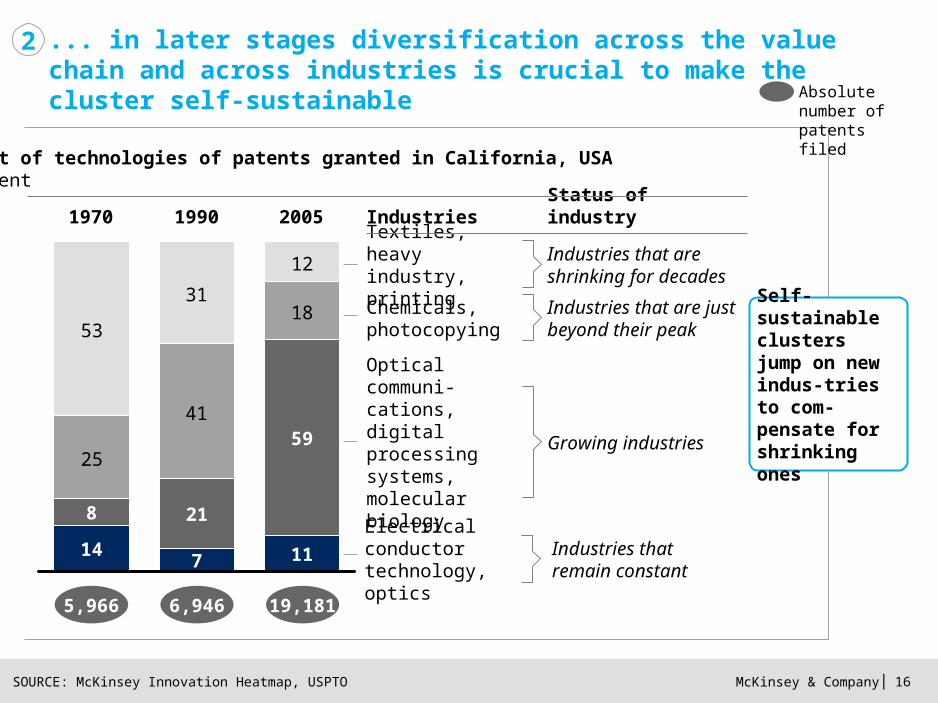

... in later stages diversification across the value chain and across industries is crucial to make the cluster self-sustainable

Absolute number of patents filed

SOURCE: McKinsey Innovation Heatmap, USPTO

5,966 6,946 19,181

200519901970

Textiles, heavy industry, printing

Chemicals, photocopying

Optical communi-cations, digital processing systems, molecular biology

Electrical conductor technology, optics

Industries Status of industry

Industries that are shrinking for decades

Industries that are just beyond their peak

Growing industries

Industries that remain constant

Split of technologies of patents granted in California, USAPercent

Self-sustainable clusters jump on new indus-tries to com-pensate for shrinking ones

2

25

41

1853

12

31

11

59

7

21

14

8

Recommended