CEO ConferenceBTG Pactual

March 09, 2010

Disclaimer

This presentation may contain forward-looking statements. Such forward-looking statements are

and will be subject to many risks and uncertainties relating to factors that are beyond the

Direcional’s ability to control or estimate precisely, such as future market conditions,

competitive environment, currency and inflation fluctuations, changes in governmental and

regulatory policies and other factors relating to the operations of Direcional, which may cause

actual future results of Direcional to differ materially from those expressed or implied in such

forward-looking statements

You are cautioned not to place undue reliance on these forward-looking statements, which

speak only as of the date of this presentation. Such forward-looking statements shall not be

construed as guarantee of future performance. Direcional does not undertake to publicly review

or update these forward-looking statements in view of events or circumstances occurring after

the date of this presentation

This presentation does not constitute an offer, or invitation, or solicitation of an offer, to

subscribe for or purchase any securities. Neither this presentation nor anything contained

herein shall form the basis of any contract or commitment whatsoever

This presentation and its contents are proprietary information and may not be reproduced or

otherwise disseminated in whole or in part without Direcional’s prior written consent.

Agenda

Overview

Company Strengths

“Minha Casa, Minha Vida” Housing Program

Operating and Financial Highlights

Appendix

Company Overview

Background

Founded in 1981, based in Belo Horizonte, Direcional has consolidated itself as one of

the most important companies in the segment of development and construction of

residential properties in Brazil

Experience as developer and homebuilder

More than 120 projects launched

In the 9M09: 17 projects (8,492 units and a R$702 million PSV)

Focus on low-income segment

Units below R$ 130 thousand represent 85% of the Landbank

Large scale projects (+1.000 units) represent 91% of the land bank

Strong footprint in underpenetrated markets with high growth potential

Strong presence in the North and Center-West, which represented 73% of

launches in 9M09

Verticalized business model

Own team of employees

Performance based compensation

Standardized and industrialized processes

Operational Efficiency

Management focused on value creation

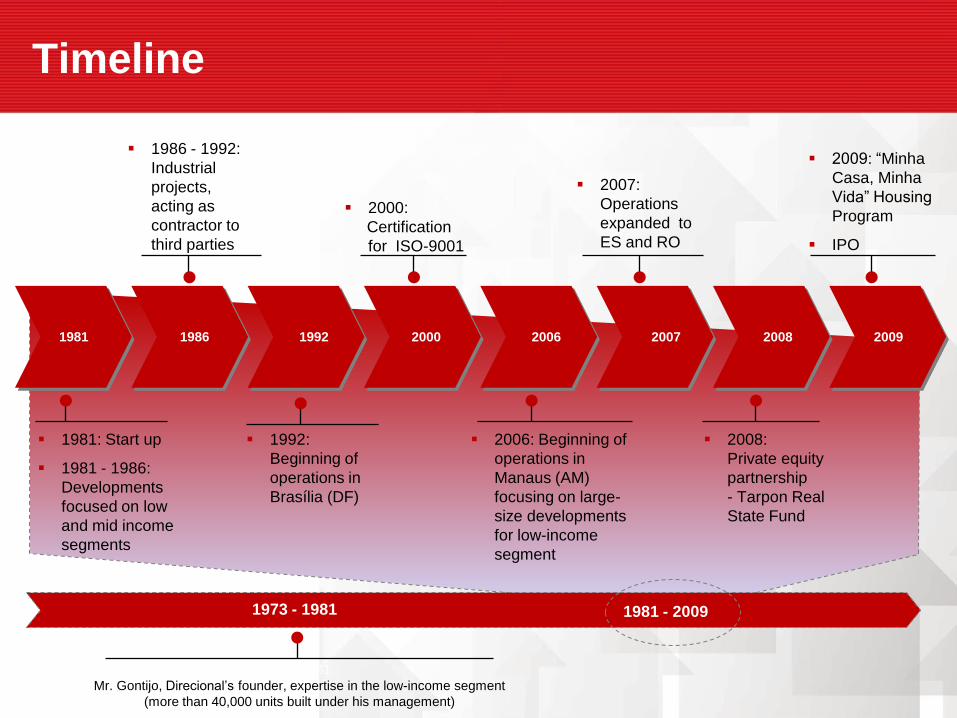

Timeline

1973 - 1981

1973 -1981:

Mr. Gontijo, Direcional’s founder, expertise in the low-income segment

(more than 40,000 units built under his management)

1981 - 2009

2000 2006 2007 200819921981 1986 2009

1986 - 1992:

Industrial

projects,

acting as

contractor to

third parties

2000:

Certification

for ISO-9001

2007:

Operations

expanded to

ES and RO

2009: “Minha

Casa, Minha

Vida” Housing

Program

IPO

1992:

Beginning of

operations in

Brasília (DF)

1981: Start up

1981 - 1986:

Developments

focused on low

and mid income

segments

2006: Beginning of

operations in

Manaus (AM)

focusing on large-

size developments

for low-income

segment

2008:

Private equity

partnership

- Tarpon Real

State Fund

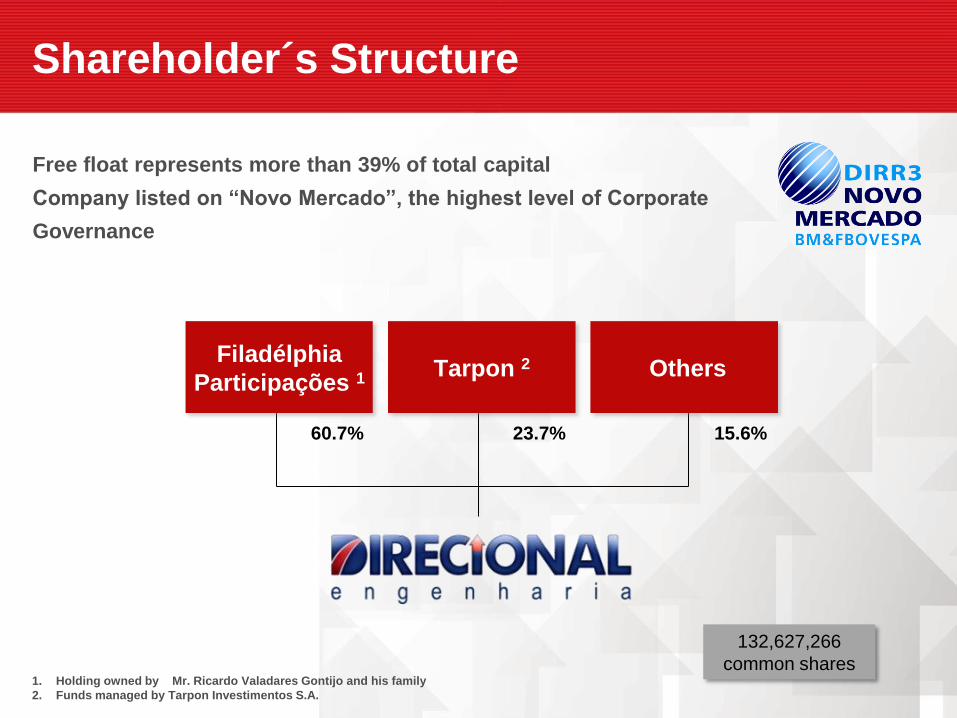

Shareholder´s Structure

60.7% 23.7% 15.6%

Free float represents more than 39% of total capital

Company listed on “Novo Mercado”, the highest level of Corporate

Governance

1. Holding owned by Mr. Ricardo Valadares Gontijo and his family

2. Funds managed by Tarpon Investimentos S.A.

Filadélphia

Participações 1 Tarpon 2 Others

132,627,266

common shares

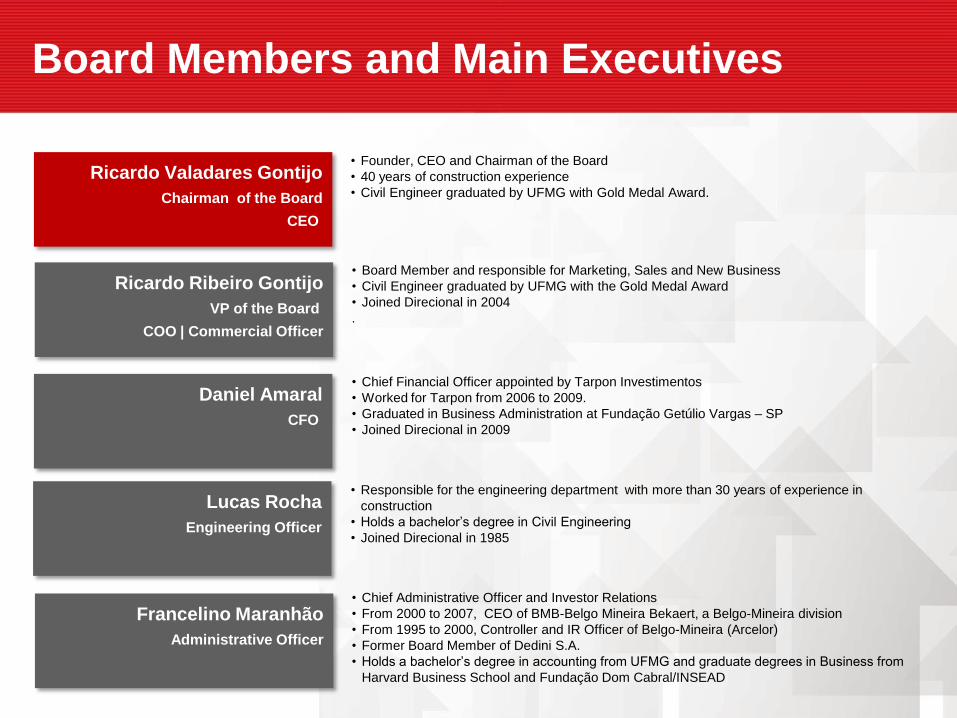

Board Members and Main Executives

Ricardo Valadares Gontijo

Chairman of the Board

CEO

Ricardo Ribeiro Gontijo

VP of the Board

COO | Commercial Officer

Francelino Maranhão

Administrative Officer

Daniel Amaral

CFO

Lucas Rocha

Engineering Officer

• Founder, CEO and Chairman of the Board

• 40 years of construction experience

• Civil Engineer graduated by UFMG with Gold Medal Award.

• Board Member and responsible for Marketing, Sales and New Business

• Civil Engineer graduated by UFMG with the Gold Medal Award

• Joined Direcional in 2004

.

• Chief Administrative Officer and Investor Relations

• From 2000 to 2007, CEO of BMB-Belgo Mineira Bekaert, a Belgo-Mineira division

• From 1995 to 2000, Controller and IR Officer of Belgo-Mineira (Arcelor)

• Former Board Member of Dedini S.A.

• Holds a bachelor’s degree in accounting from UFMG and graduate degrees in Business from

Harvard Business School and Fundação Dom Cabral/INSEAD

• Chief Financial Officer appointed by Tarpon Investimentos

• Worked for Tarpon from 2006 to 2009.

• Graduated in Business Administration at Fundação Getúlio Vargas – SP

• Joined Direcional in 2009

• Responsible for the engineering department with more than 30 years of experience in

construction

• Holds a bachelor’s degree in Civil Engineering

• Joined Direcional in 1985

Company Strengths

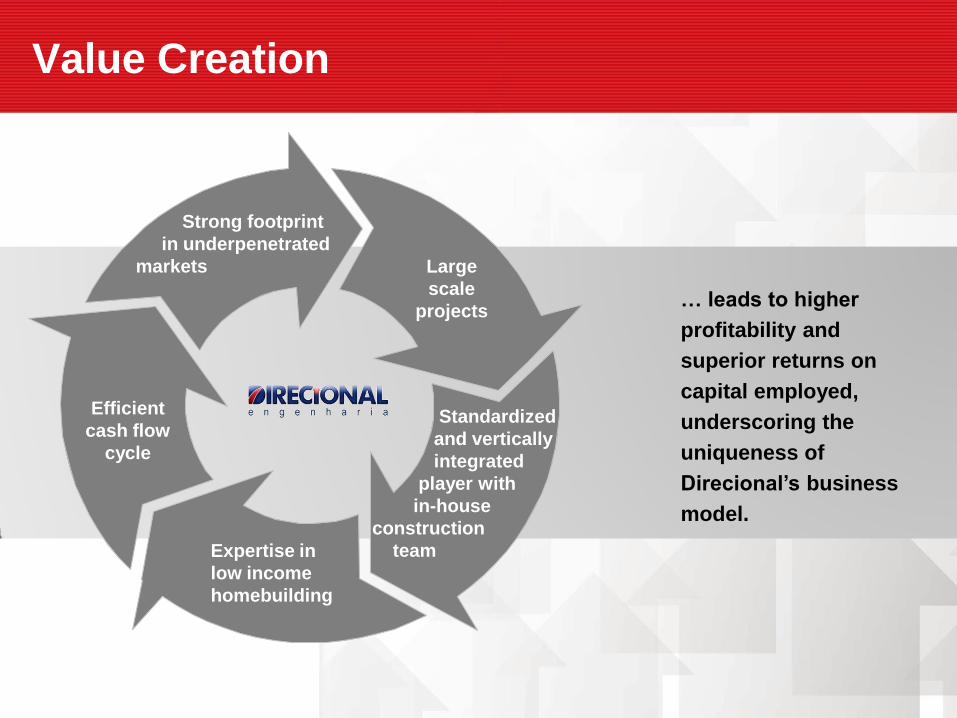

Value Creation

Efficient

cash flow

cycle

Strong footprint

in underpenetrated

markets

Expertise in

low income

homebuilding

Large

scale

projects

Standardized

and vertically

integrated

player with

in-house

construction

team

… leads to higher

profitability and

superior returns on

capital employed,

underscoring the

uniqueness of

Direcional’s business

model.

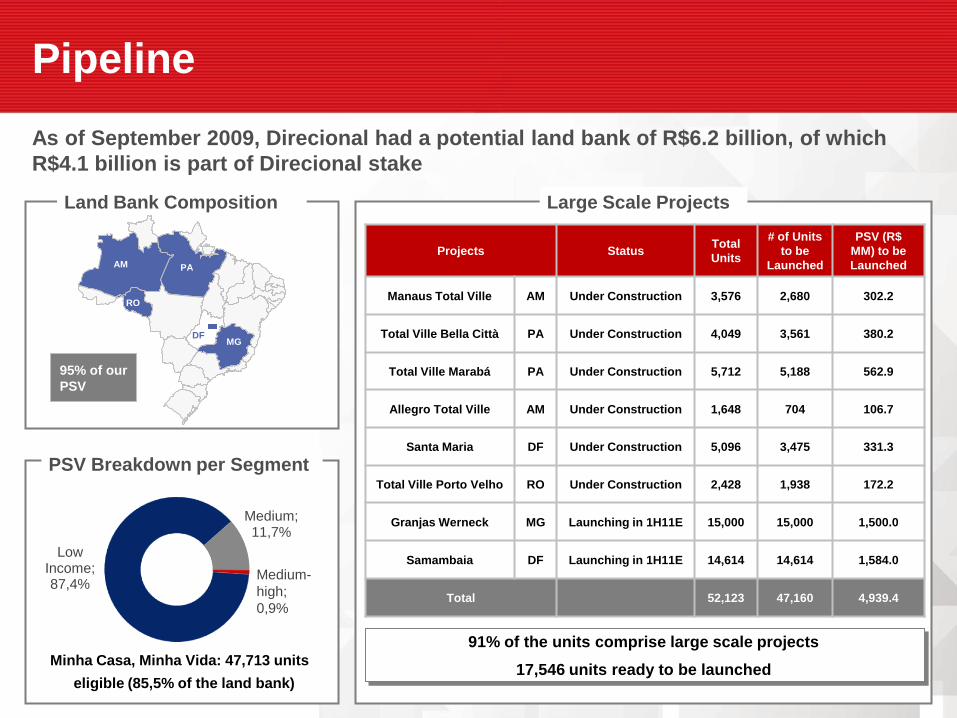

Pipeline

As of September 2009, Direcional had a potential land bank of R$6.2 billion, of which

R$4.1 billion is part of Direcional stake

Land Bank Composition Large Scale Projects

Projects StatusTotal

Units

# of Units

to be

Launched

PSV (R$

MM) to be

Launched

Manaus Total Ville AM Under Construction 3,576 2,680 302.2

Total Ville Bella Città PA Under Construction 4,049 3,561 380.2

Total Ville Marabá PA Under Construction 5,712 5,188 562.9

Allegro Total Ville AM Under Construction 1,648 704 106.7

Santa Maria DF Under Construction 5,096 3,475 331.3

Total Ville Porto Velho RO Under Construction 2,428 1,938 172.2

Granjas Werneck MG Launching in 1H11E 15,000 15,000 1,500.0

Samambaia DF Launching in 1H11E 14,614 14,614 1,584.0

Total 52,123 47,160 4,939.4

MGDF

PAAM

RO

95% of our

PSV

PSV Breakdown per Segment

Low Income; 87,4%

Medium; 11,7%

Medium-

high;

0,9%

Minha Casa, Minha Vida: 47,713 units

eligible (85,5% of the land bank)

91% of the units comprise large scale projects

17,546 units ready to be launched

Large-Scale Projects

Buildings with 4 floors, garage floor, without elevator

Complete leisure: swimming pools, barbecue area,

parks, ballroom, walking track, soccer field, bike

lanes

Large projects, with more than 1,000 units, located

in areas of severe housing shortage like Porto Velho

(Rondônia) and Manaus (Amazonas)

Apartments of 50 sq.m - 80 sq.m with selling price

around R$ 1.500 / sq.m

Green Area: balanced distribution of wide avenues,

residential towers and other facilities

Commercial area

Prime Location: few minutes from downtown

Easy access by major roads

Public transportation available

Safety: vehicle patrols

Planned neighborhood with shopping center

“Total Ville” concept: A large-scale product designed to offer housing, leisure, safety,

functionality and convenience. Direcional is a pioneer in offering all these features in

one place, close to urban centers and in accordance with the economic reality of the

market.

Own Building Team

More than 4,000 exclusive workers assuring quality, commitment, efficiency and cost

control

A Key Competitive Advantage

Independence

Direcional does not depend on contractor´s workforce

Cost Reductions

Lower labor risks and higher productivity

Higher Quality

Better quality control, reducing maintenance levels

All employes are booked in Direcional’s payroll

Reduction of labor risks

Constant training programs/ Standardization

Experienced workers = teachers

Processes standardization

Constant performance evaluation

Clear and objective task assessment

Monitoring and training of low-productive workers

Rework almost inexistent

Performance Based Compensation

Linked to targets

Lower turnover

Standardized Process

Standardized Building Process

Leads to:

Waste reduction

Low rework levels

Higher efficiency per worker

It also contributes to:

Higher building quality/control

Easy identification and

correction of building

problems

Embedded electric

fittings that minimize

the need of cutting

walls

Standardization Examples

Concrete blocks

produced in jobsite

pre-molding station

Standardized processes instead of standardized projects

Direcional adopts similar procedures in all its construction sites

Standardized processes diminishes wastes and post-sales issues

Problems in previous projects can be avoided in the new ones and general solutions can be created and

shared among teams

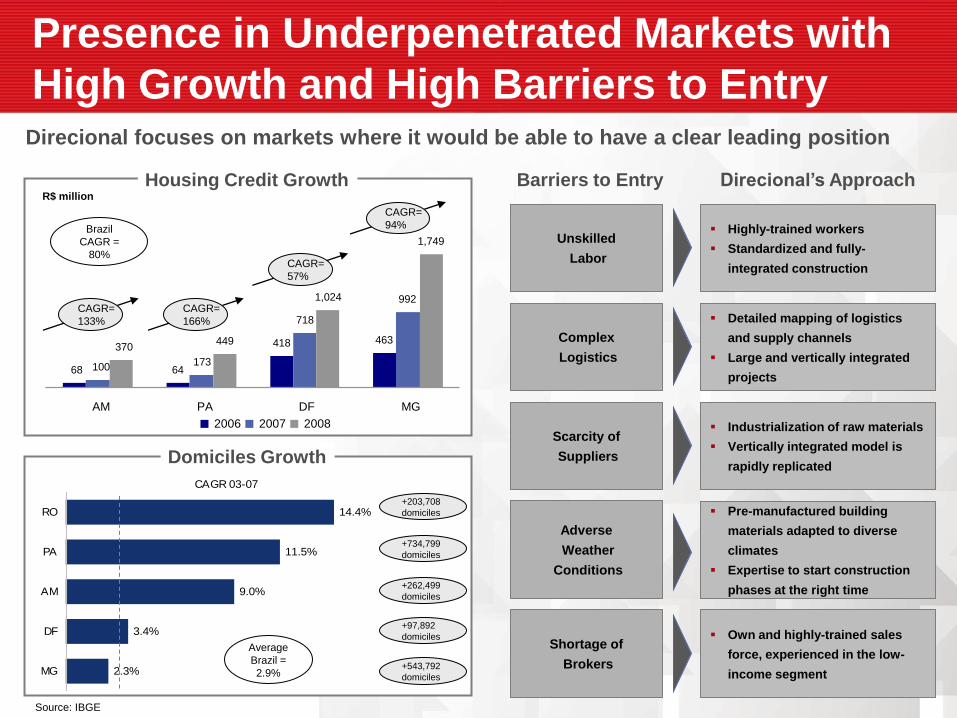

Presence in Underpenetrated Markets with

High Growth and High Barriers to EntryDirecional focuses on markets where it would be able to have a clear leading position

Source: IBGE

Barriers to Entry

Unskilled

Labor

Highly-trained workers

Standardized and fully-

integrated construction

Complex

Logistics

Detailed mapping of logistics

and supply channels

Large and vertically integrated

projects

Scarcity of

Suppliers

Industrialization of raw materials

Vertically integrated model is

rapidly replicated

Adverse

Weather

Conditions

Pre-manufactured building

materials adapted to diverse

climates

Expertise to start construction

phases at the right time

Shortage of

Brokers

Own and highly-trained sales

force, experienced in the low-

income segment

Direcional’s Approach

CAGR=

94%

Housing Credit GrowthR$ million

CAGR=

57%

CAGR=

133%

Brazil

CAGR =

80%

CAGR=

166%

68 64

418 463

100 173

718

992

370449

1,024

1,749

AM PA DF MG

2006 2007 2008

Average

Brazil =

2.9%

+203,708

domiciles

+734,799

domiciles

+262,499

domiciles

+97,892

domiciles

+543,792

domiciles

CAGR 03-07

14.4%

11.5%

9.0%

3.4%

2.3%MG

DF

AM

PA

RO

Domiciles Growth

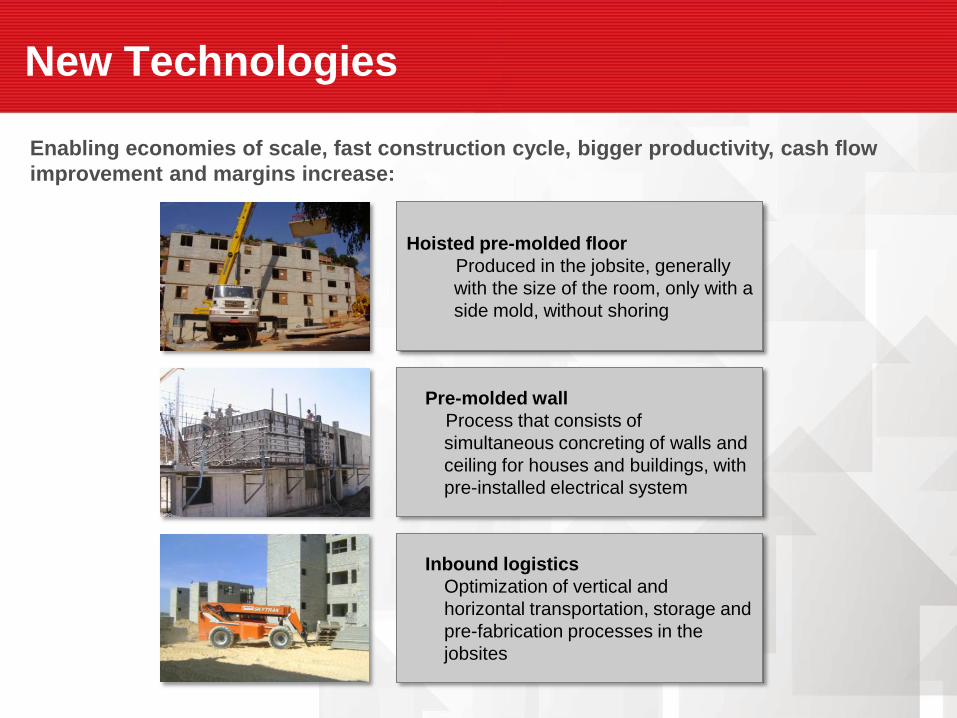

New Technologies

Enabling economies of scale, fast construction cycle, bigger productivity, cash flow

improvement and margins increase:

Hoisted pre-molded floor

Produced in the jobsite, generally

with the size of the room, only with a

side mold, without shoring

Pre-molded wall

Process that consists of

simultaneous concreting of walls and

ceiling for houses and buildings, with

pre-installed electrical system

Inbound logistics

Optimization of vertical and

horizontal transportation, storage and

pre-fabrication processes in the

jobsites

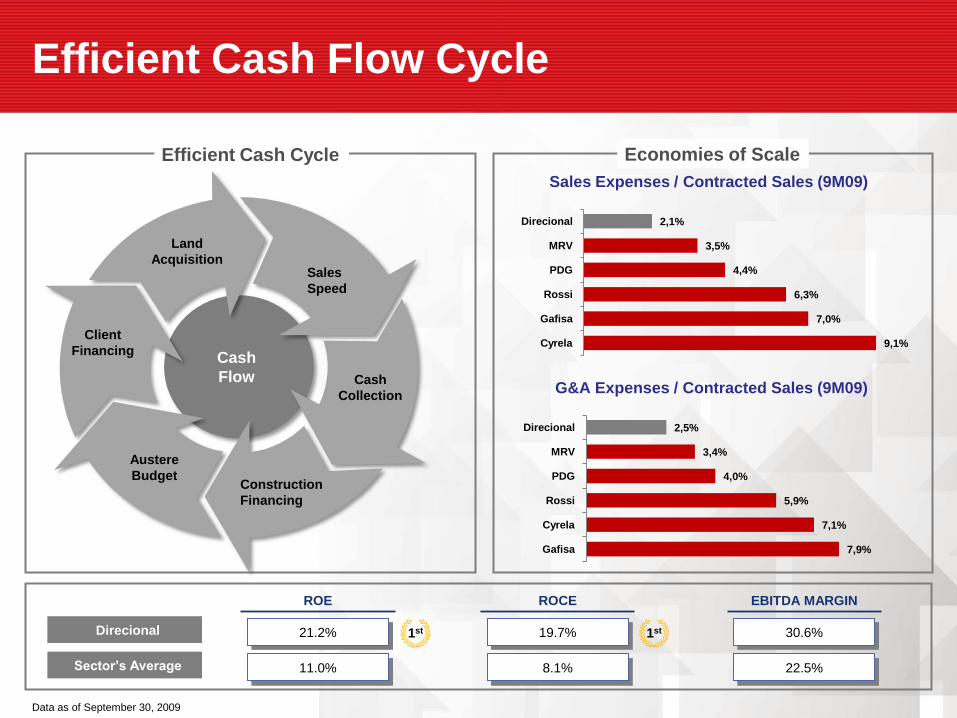

Efficient Cash Flow Cycle

Cash

Flow

Land

AcquisitionSales

Speed

Cash

Collection

Austere

Budget

Client

Financing

Construction

Financing

Efficient Cash Cycle Economies of Scale

Sales Expenses / Contracted Sales (9M09)

G&A Expenses / Contracted Sales (9M09)

Direcional

Sector’s Average

ROE

21.2%

11.0%

1st 19.7%

8.1%

ROCE

1st

Data as of September 30, 2009

2,1%

3,5%

4,4%

6,3%

7,0%

9,1%

Direcional

MRV

PDG

Rossi

Gafisa

Cyrela

2,5%

3,4%

4,0%

5,9%

7,1%

7,9%

Direcional

MRV

PDG

Rossi

Cyrela

Gafisa

30.6%

22.5%

EBITDA MARGIN

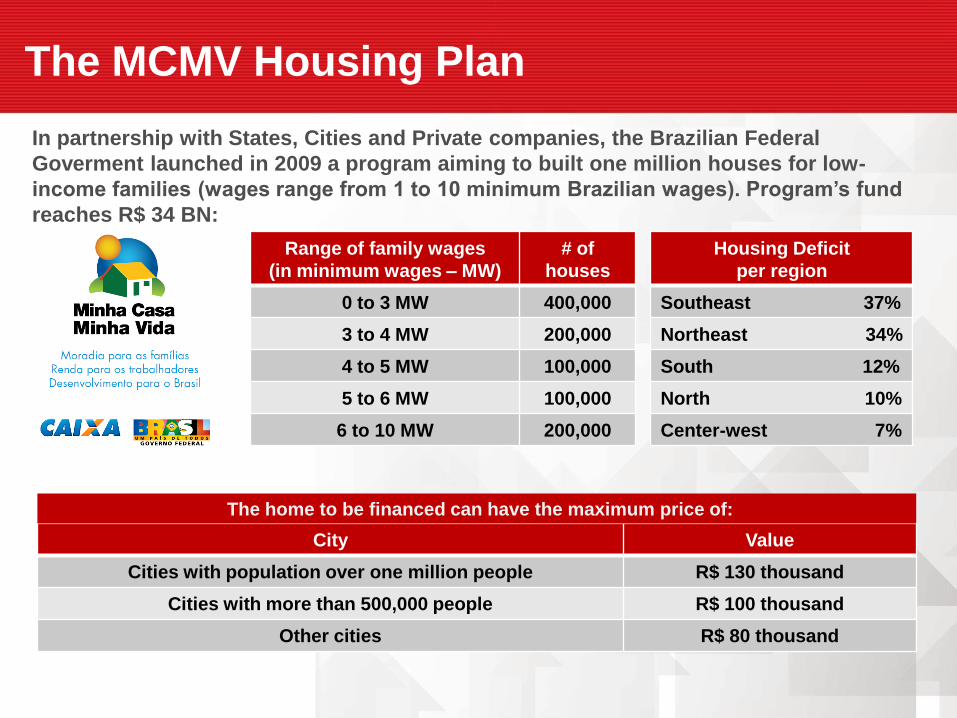

Minha Casa, Minha Vida

The MCMV Housing Plan

Range of family wages

(in minimum wages – MW)

# of

houses

0 to 3 MW 400,000

3 to 4 MW 200,000

4 to 5 MW 100,000

5 to 6 MW 100,000

6 to 10 MW 200,000

Housing Deficit

per region

Southeast 37%

Northeast 34%

South 12%

North 10%

Center-west 7%

City Value

Cities with population over one million people R$ 130 thousand

Cities with more than 500,000 people R$ 100 thousand

Other cities R$ 80 thousand

The home to be financed can have the maximum price of:

In partnership with States, Cities and Private companies, the Brazilian Federal

Goverment launched in 2009 a program aiming to built one million houses for low-

income families (wages range from 1 to 10 minimum Brazilian wages). Program’s fund

reaches R$ 34 BN:

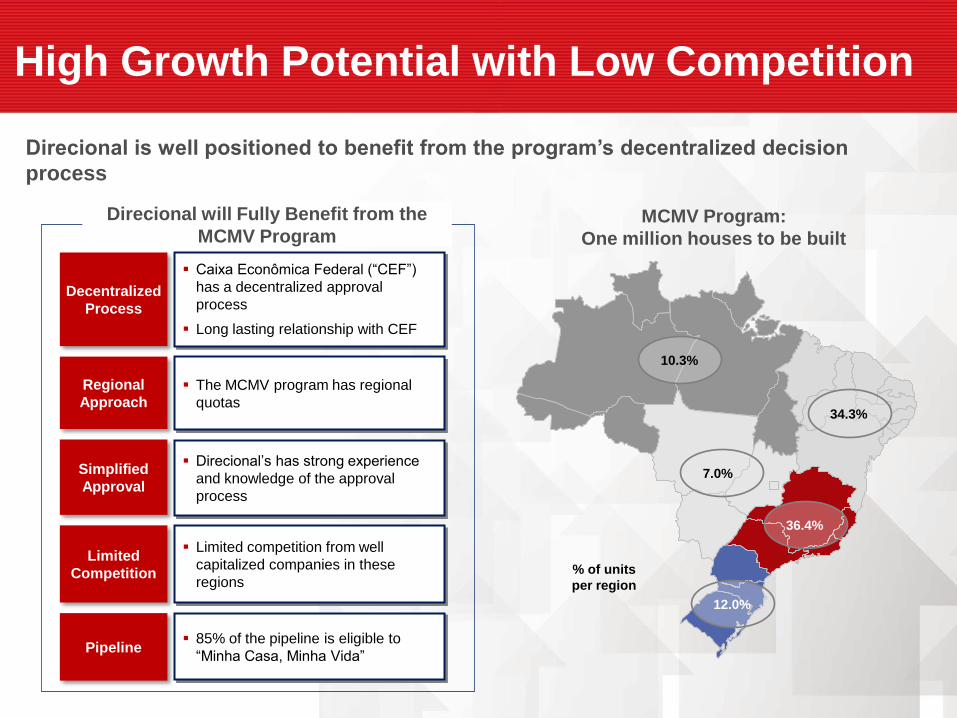

High Growth Potential with Low Competition

Direcional will Fully Benefit from the

MCMV Program

Direcional is well positioned to benefit from the program’s decentralized decision

process

10.3%

34.3%

36.4%

7.0%

12.0%

MCMV Program:

One million houses to be built

% of units

per region

Decentralized

Process

Regional

Approach

Simplified

Approval

Limited

Competition

Pipeline

Caixa Econômica Federal (“CEF”)

has a decentralized approval

process

Long lasting relationship with CEF

The MCMV program has regional

quotas

Direcional’s has strong experience

and knowledge of the approval

process

Limited competition from well

capitalized companies in these

regions

85% of the pipeline is eligible to

“Minha Casa, Minha Vida”

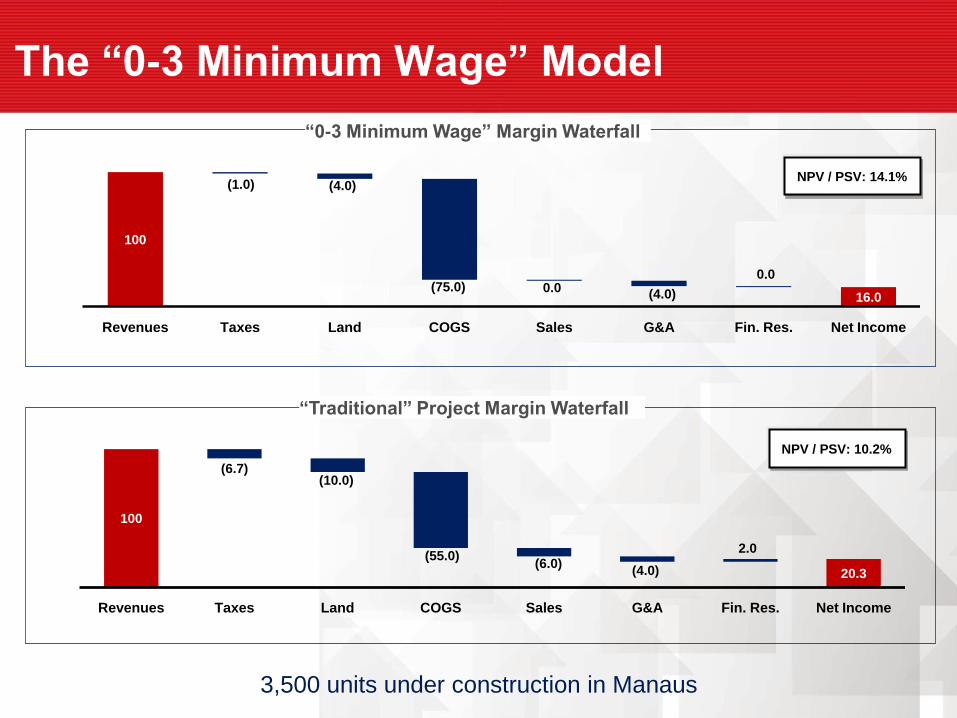

100

16.0

(1.0) (4.0)

(75.0) 0.0(4.0)

0.0

Revenues Taxes Land COGS Sales G&A Fin. Res. Net Income

The “0-3 Minimum Wage” Model

100

20.3

(6.7)(10.0)

(55.0)(6.0)

(4.0)

2.0

Revenues Taxes Land COGS Sales G&A Fin. Res. Net Income

“0-3 Minimum Wage” Margin Waterfall

“Traditional” Project Margin Waterfall

NPV / PSV: 14.1%

NPV / PSV: 10.2%

3,500 units under construction in Manaus

Operating and

Financial Highlights

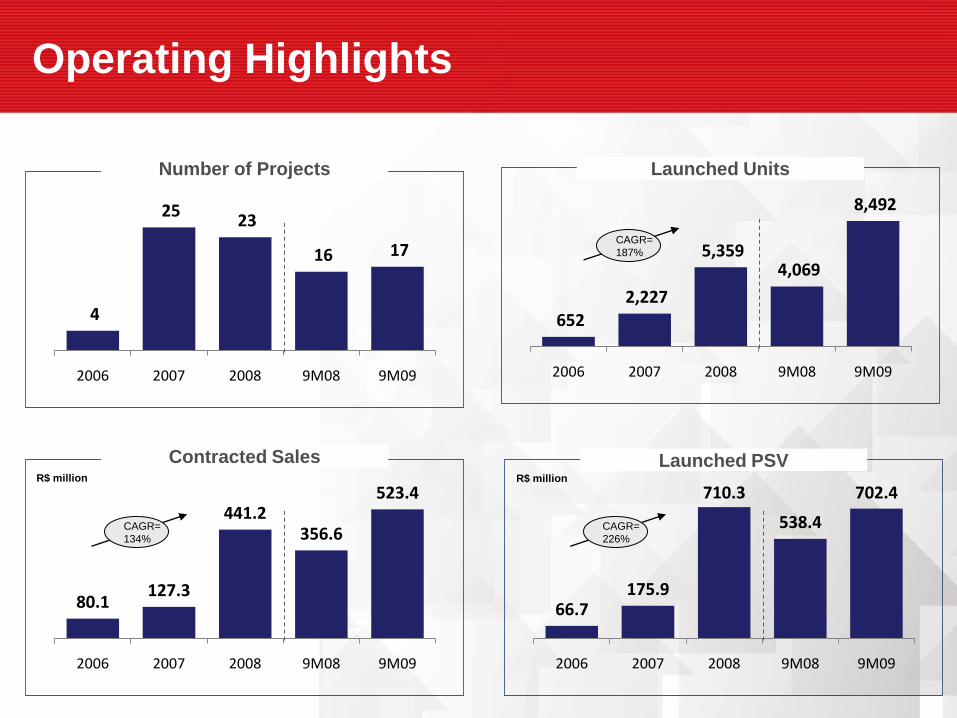

Operating Highlights

4

25 23

16 17

2006 2007 2008 9M08 9M09

Number of Projects

652 2,227

5,359 4,069

8,492

2006 2007 2008 9M08 9M09

Launched Units

80.1 127.3

441.2 356.6

523.4

2006 2007 2008 9M08 9M09

Contracted Sales

66.7 175.9

710.3

538.4

702.4

2006 2007 2008 9M08 9M09

Launched PSV

CAGR=

187%

CAGR=

226%

CAGR=

134%

R$ million R$ million

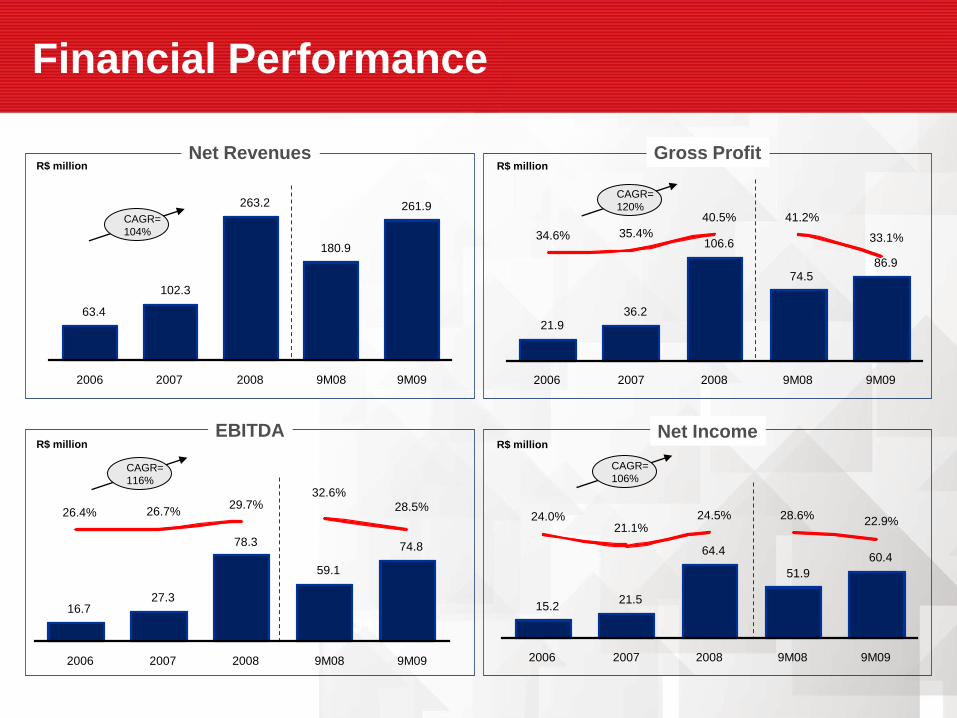

Financial Performance

R$ million R$ million

R$ million R$ million

Net Revenues Gross Profit

Net IncomeEBITDA

CAGR=

120%CAGR=

104%

CAGR=

106%CAGR=

116%

21.936.2

106.6

74.586.9

34.6% 35.4%

40.5% 41.2%

33.1%

2006 2007 2008 9M08 9M09

15.2 21.5

64.4

51.9

60.4

24.0%21.1%

24.5% 28.6%22.9%

2006 2007 2008 9M08 9M09

16.7 27.3

78.3

59.1

74.8

26.4% 26.7%29.7%

32.6%

28.5%

2006 2007 2008 9M08 9M09

63.4

102.3

263.2

180.9

261.9

2006 2007 2008 9M08 9M09

Direcional At-a-Glance

Standardized

and Vertically

Integrated

Operations

Large Scale

Projects

Underpenetrated

Markets with High

Growth Potential

and Barriers to

Entry

In-house

Construction

Team

Expertise in Low

Income

Homebuilding

Efficient Cash

Flow Cycle

Appendix

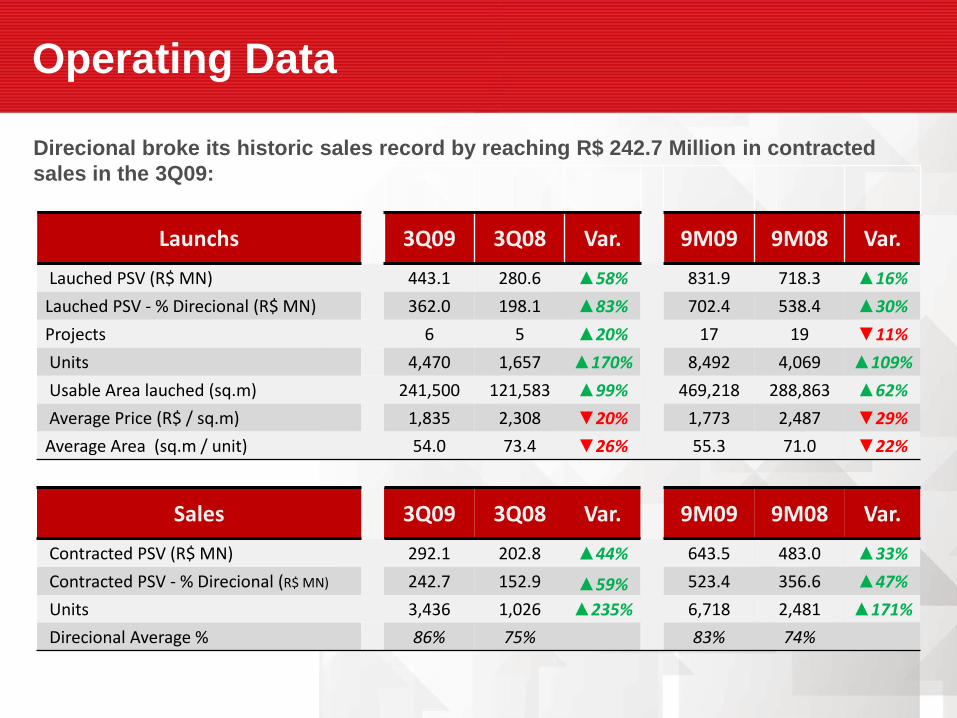

Launchs 3Q09 3Q08 Var. 9M09 9M08 Var.

Lauched PSV (R$ MN) 443.1 280.6 ▲58% 831.9 718.3 ▲16%

Lauched PSV - % Direcional (R$ MN) 362.0 198.1 ▲83% 702.4 538.4 ▲30%

Projects 6 5 ▲20% 17 19 ▼11%

Units 4,470 1,657 ▲170% 8,492 4,069 ▲109%

Usable Area lauched (sq.m) 241,500 121,583 ▲99% 469,218 288,863 ▲62%

Average Price (R$ / sq.m) 1,835 2,308 ▼20% 1,773 2,487 ▼29%

Average Area (sq.m / unit) 54.0 73.4 ▼26% 55.3 71.0 ▼22%

Sales 3Q09 3Q08 Var. 9M09 9M08 Var.

Contracted PSV (R$ MN) 292.1 202.8 ▲44% 643.5 483.0 ▲33%

Contracted PSV - % Direcional (R$ MN) 242.7 152.9 ▲59% 523.4 356.6 ▲47%

Units 3,436 1,026 ▲235% 6,718 2,481 ▲171%

Direcional Average % 86% 75% 83% 74%

Operating Data

Direcional broke its historic sales record by reaching R$ 242.7 Million in contracted

sales in the 3Q09:

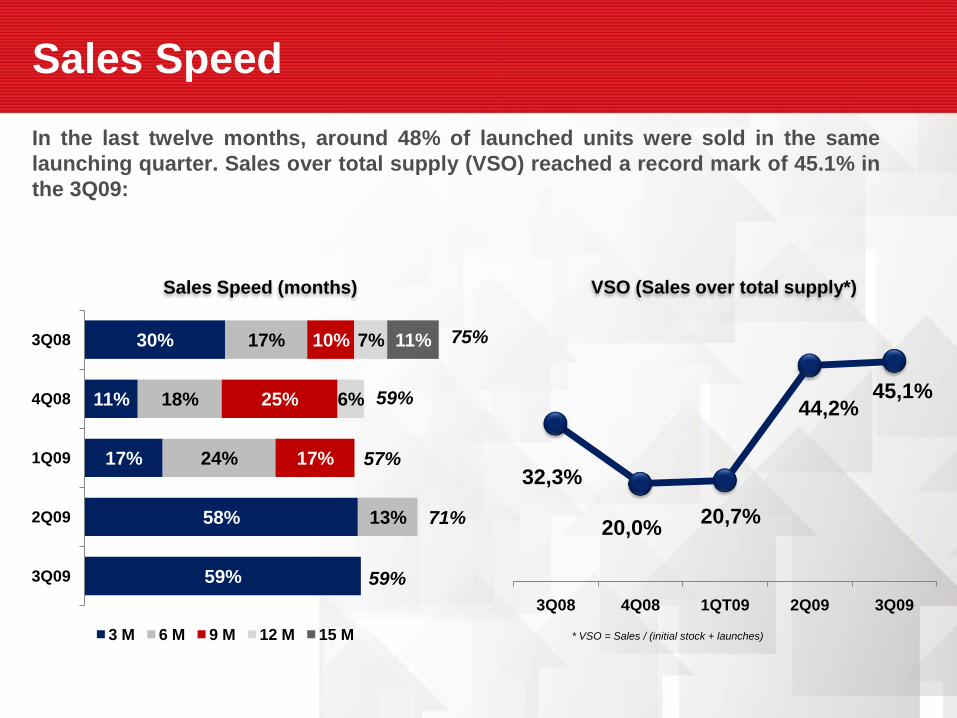

Sales Speed

In the last twelve months, around 48% of launched units were sold in the same

launching quarter. Sales over total supply (VSO) reached a record mark of 45.1% in

the 3Q09:

59%

58%

17%

11%

30%

13%

24%

18%

17%

17%

25%

10%

6%

7% 11%

3Q09

2Q09

1Q09

4Q08

3Q08

3 M 6 M 9 M 12 M 15 M

32,3%

20,0%20,7%

44,2%45,1%

3Q08 4Q08 1QT09 2Q09 3Q09

VSO (Sales over total supply*)

* VSO = Sales / (initial stock + launches)

Sales Speed (months)

75%

59%

57%

71%

59%

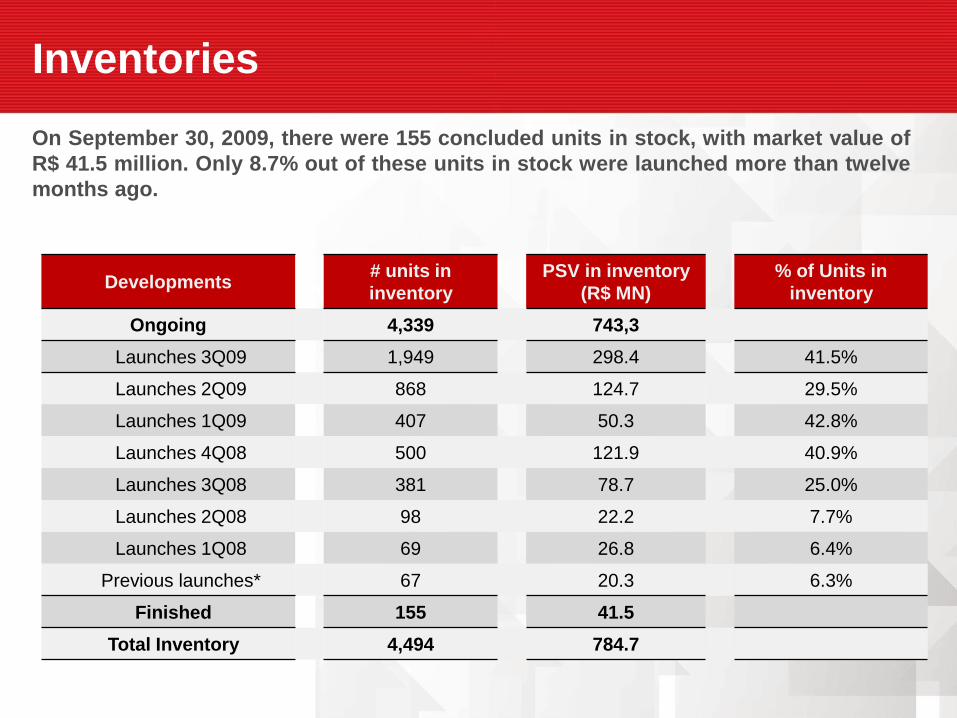

Inventories

On September 30, 2009, there were 155 concluded units in stock, with market value of

R$ 41.5 million. Only 8.7% out of these units in stock were launched more than twelve

months ago.

Developments# units in

inventory

PSV in inventory

(R$ MN)

% of Units in

inventory

Ongoing 4,339 743,3

Launches 3Q09 1,949 298.4 41.5%

Launches 2Q09 868 124.7 29.5%

Launches 1Q09 407 50.3 42.8%

Launches 4Q08 500 121.9 40.9%

Launches 3Q08 381 78.7 25.0%

Launches 2Q08 98 22.2 7.7%

Launches 1Q08 69 26.8 6.4%

Previous launches* 67 20.3 6.3%

Finished 155 41.5

Total Inventory 4,494 784.7

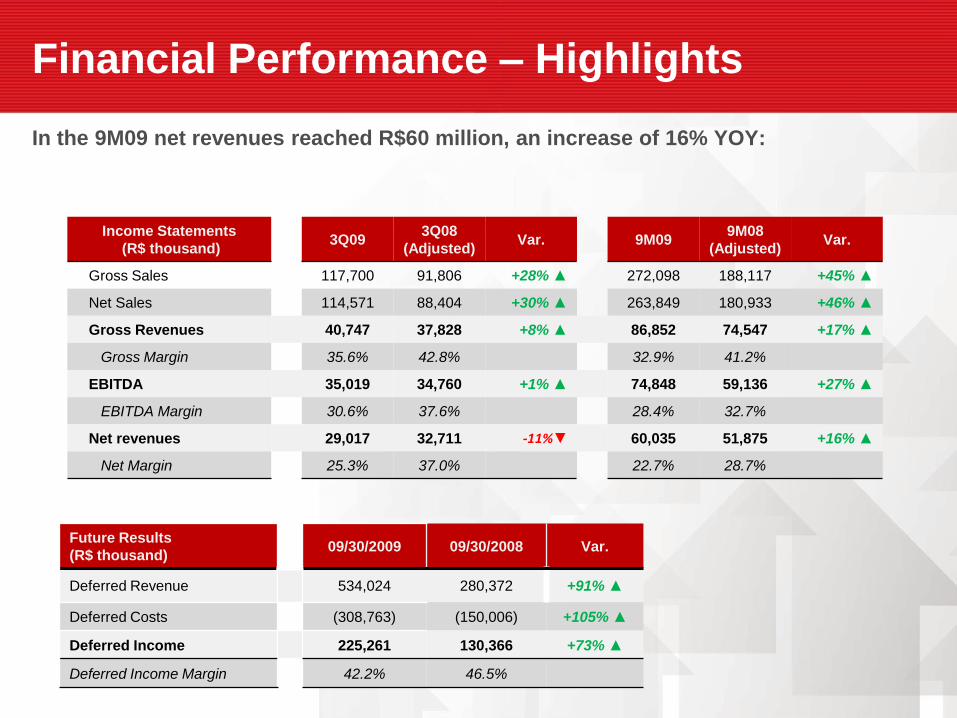

Financial Performance – Highlights

In the 9M09 net revenues reached R$60 million, an increase of 16% YOY:

Income Statements

(R$ thousand)3Q09

3Q08

(Adjusted)Var. 9M09

9M08

(Adjusted)Var.

Gross Sales 117,700 91,806 +28% ▲ 272,098 188,117 +45% ▲

Net Sales 114,571 88,404 +30% ▲ 263,849 180,933 +46% ▲

Gross Revenues 40,747 37,828 +8% ▲ 86,852 74,547 +17% ▲

Gross Margin 35.6% 42.8% 32.9% 41.2%

EBITDA 35,019 34,760 +1% ▲ 74,848 59,136 +27% ▲

EBITDA Margin 30.6% 37.6% 28.4% 32.7%

Net revenues 29,017 32,711 -11%▼ 60,035 51,875 +16% ▲

Net Margin 25.3% 37.0% 22.7% 28.7%

Future Results

(R$ thousand)09/30/2009 09/30/2008 Var.

Deferred Revenue 534,024 280,372 +91% ▲

Deferred Costs (308,763) (150,006) +105% ▲

Deferred Income 225,261 130,366 +73% ▲

Deferred Income Margin 42.2% 46.5%

Balance Sheet

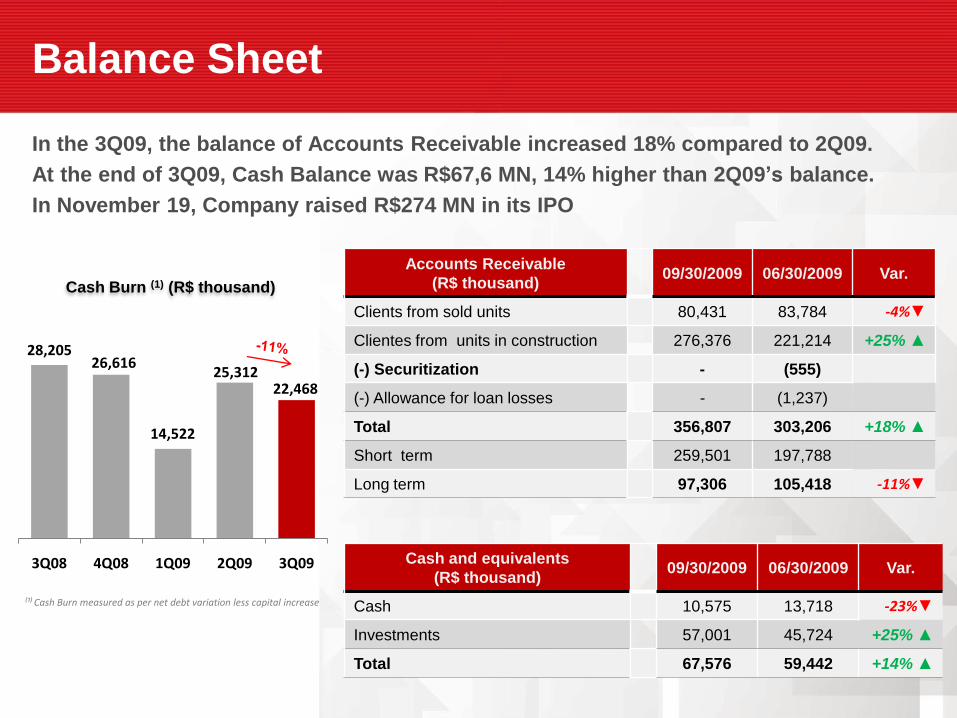

In the 3Q09, the balance of Accounts Receivable increased 18% compared to 2Q09.

At the end of 3Q09, Cash Balance was R$67,6 MN, 14% higher than 2Q09’s balance.

In November 19, Company raised R$274 MN in its IPO

Accounts Receivable

(R$ thousand)09/30/2009 06/30/2009 Var.

Clients from sold units 80,431 83,784 -4%▼

Clientes from units in construction 276,376 221,214 +25% ▲

(-) Securitization - (555)

(-) Allowance for loan losses - (1,237)

Total 356,807 303,206 +18% ▲

Short term 259,501 197,788

Long term 97,306 105,418 -11%▼

Cash and equivalents

(R$ thousand)09/30/2009 06/30/2009 Var.

Cash 10,575 13,718 -23%▼

Investments 57,001 45,724 +25% ▲

Total 67,576 59,442 +14% ▲

28,205 26,616

14,522

25,312 22,468

3Q08 4Q08 1Q09 2Q09 3Q09

Cash Burn (1) (R$ thousand)

⁽¹⁾ Cash Burn measured as per net debt variation less capital increase

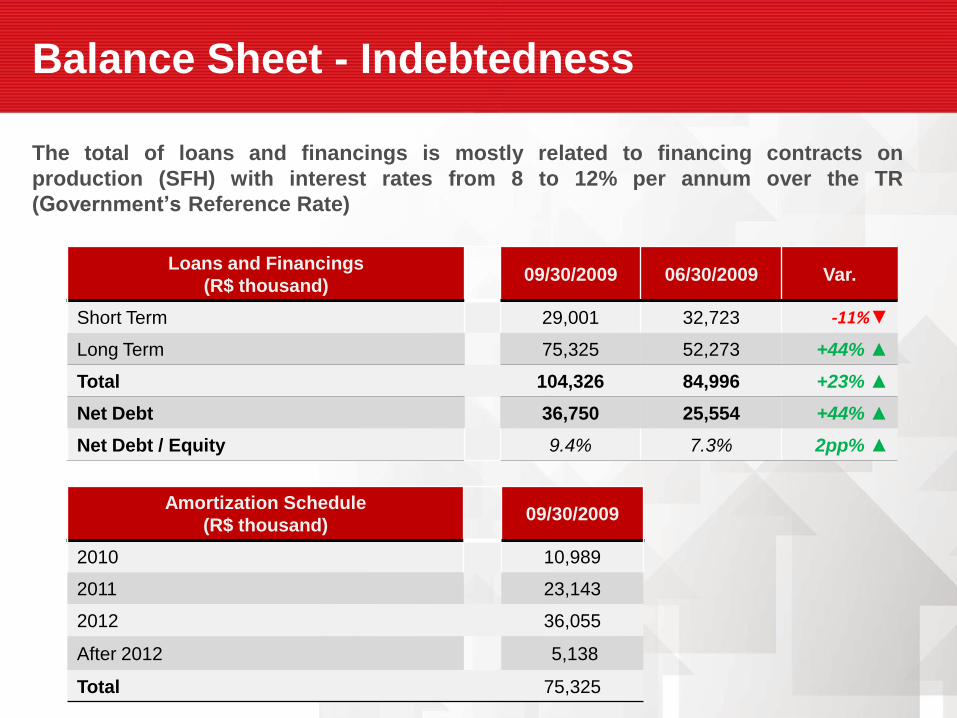

Balance Sheet - Indebtedness

The total of loans and financings is mostly related to financing contracts on

production (SFH) with interest rates from 8 to 12% per annum over the TR

(Government’s Reference Rate)

Loans and Financings

(R$ thousand)09/30/2009 06/30/2009 Var.

Short Term 29,001 32,723 -11%▼

Long Term 75,325 52,273 +44% ▲

Total 104,326 84,996 +23% ▲

Net Debt 36,750 25,554 +44% ▲

Net Debt / Equity 9.4% 7.3% 2pp% ▲

Amortization Schedule

(R$ thousand)09/30/2009

2010 10,989

2011 23,143

2012 36,055

After 2012 5,138

Total 75,325

Recommended