8/15/2019 Broker Note, Acambis, 15/09/2005 (Evolution)

http://slidepdf.com/reader/full/broker-note-acambis-15092005-evolution 1/6

Evolution Securities 100 Wood Street, London, EC2V 7AN 020 7071 4300

Evolution

SECURITIES

www.evosecurities.com 14 September 2005

BN’s complaint indicated that it believes Acambis had unlawful access to the

‘grandfather’ strain which is the ‘ancestor’ for the viruses used in both

companies’ MVA vaccines. Moreover, BN accuses Acambis of using information it

gained at a meeting in 2002 with BN, which was subject to a confidentiality

agreement. These legal proceedings are separate to the patent infringement

case that has been filed with the International Trade Commission. In terms of the

misappropriation case, BN is seeking up to triple damages as recompense.

In the complaint, BN stated it exclusively licensed for commercial use all strains of

MVA, including one known as MVA-572, from a Professor Mayr. This is despite

the fact that MVA-572 was used as the basis of a vaccine in the seventies.Acambis denies that BN holds an exclusive license for commercialisation of all

MVA strains. In fact, even BN concedes that it only holds a license (in its eyes) for

MVA strains developed by Prof. Mayr (which are not necessarily all strains).

The fact that BN entered into a secrecy agreement with Acambis in February

2002 is acknowledged by Acambis. However, Acambis denies that this was in

relation to a potential licensing agreement relating to MVA-BN (which is alleged

by BN). According to BN, at a meeting in June 2002, data relating to the

development and production of MVA-BN was disclosed to Acambis personnel,

including the Chief Scientific Officer at the time, Tom Monath. Acambis agrees

this meeting took place, but denies any confidential or proprietary information

was handed over. The fact that a draft agreement was sent to Acambis from BN

is agreed upon by both companies. However, while BN states that discussions

continued until Acambis terminated talks when the first Request for Proposal for

the development of an MVA vaccine was released, this is denied by Acambis.

It is well known that Acambis did get the strain of MVA used as the basis for its

MVA 3000 from the NIAID and this is acknowledged by Acambis in its ‘answer’.

In fact, separate documentation suggests that Acambis used a version of MVA

572 that had further been attenuated at the NIAID by Dr. Moss. MVA 3000

appears to be MVA 580, a third generation version of the stock received from

the NIAID. As far we know, Acambis did not have a development programme for

an MVA based vaccine until it was given material by the NIAID. However,

Acambis denies that it had not undertaken research into MVA prior to the

publication of the first RFP.

BN claims exclusive license to MVA

strains

Meetings with Acambis

Acambis’ strain did come from NIAID

Acambis versus Bavarian Nordic: Round II

Acambis’ ‘answer’ to the complaint filed by Bavarian Nordic in Delaware has

been published and, as might be expected, almost everything is denied.

However, a meeting between the companies in 2002 is acknowledged.

Mkt Cap £263m Net Cash £94m

Acambis (ACM.L)

Price/Target: 245p/270p

210

234

258

282

306

330

S O N D J F M A M J J A

Source: JCF

Add (remains as)

8/15/2019 Broker Note, Acambis, 15/09/2005 (Evolution)

http://slidepdf.com/reader/full/broker-note-acambis-15092005-evolution 2/6

14 September 2005

Evolution Securities 100 Wood Street, London, EC2V 7AN 020 7071 4300

On the basis of the above ‘facts’, BN made certain accusations, all of which are

denied by Acambis in its ‘Answer’:

• False representation: Acambis failed to advise its potential customer, the

NIAID (and other government agencies) that the strains in its possession werenot available for distribution for non-research purposes. In fact, BN goes further,

stating that Acambis has engaged in ‘deceptive trade practices’ by ‘passing off’

MVA 3000 as a product of its own R&D.

• Acambis received MVA-572 (or its derivatives) in the knowledge that the

virus was the property of BN (through the exclusive license with Prof. Mayr).

Furthermore, Acambis has no right to possess MVA-572 as it violated the

agreement between NIAID and Prof. Mayr.

• Misappropriation of secrets, that is, using BN’s technology to commercial

advantage without BN’s consent. In addition, Acambis should have known that

any attenuated MVA strain provided by the NIAID was given without the consent

of BN.

• The proprietary information gained at the June 2002 meeting was subject

to a secrecy agreement, but was actually used to initiate Acambis’ own MVA

programme.

As we pointed out two weeks ago, one slightly bizarre element is that while the

NIAID could actually be a co-defendant in the case (as, according to BN, it

handed over MVA-572 or its derivatives to Acambis), BN is accusing Acambis of

failing to advise its potential customer of the proprietary position of the MVA

3000 strain. However, the customer is of course the NIAID! This point is

highlighted by Acambis and is used as the ‘Fourth Defense [sic]’, which states

that the case should be dismissed because of the failure to cite the US

government in the legal action.

EVO Securities makes markets in Acambis

BN’s accusations

US government accused?

Year Sales EBITDA PBT adj Tax EPS CFPS Net Cash Net Cash Cash Burn R&D R&D Chg EV/Sales DCF Sensitivity

End £m £m £m % p p £m p p £m % x WACC % Fair Value £

12/04A 85.5 27.4 16.8 28 11.4 -25.4 101.8 95.8 -30.4 -29.4 -47.7 1.9 18.0 389

12/05E 56.6 -11.8 -14.1 - -13.2 -27.5 74.7 70.3 -32.2 -29.7 -1.0 3.3 19.0 379

12/06E 47.3 -17.9 -21.0 - -19.8 -18.0 55.7 52.4 -22.3 -30.9 -4.0 4.4 20.0 369

Dr Jonathan Senior +44 (0) 20 7071 4355 [email protected]

8/15/2019 Broker Note, Acambis, 15/09/2005 (Evolution)

http://slidepdf.com/reader/full/broker-note-acambis-15092005-evolution 3/6

8/15/2019 Broker Note, Acambis, 15/09/2005 (Evolution)

http://slidepdf.com/reader/full/broker-note-acambis-15092005-evolution 4/6

8/15/2019 Broker Note, Acambis, 15/09/2005 (Evolution)

http://slidepdf.com/reader/full/broker-note-acambis-15092005-evolution 5/6

14 September 2005

Evolution Securities 100 Wood Street, London, EC2V 7AN 020 7071 4300 2

Analyst details

Dr Jonathan Senior Acambis GW Pharmaceuticals Provalis Xenova

Life Science Research Analyst Alizyme Huntleigh Technology Shire Pharmaceuticals

Ark Therapeutics Oxford BioMedica Skyepharma

Cambridge Antibody Tech Proteome Sciences Vernalis

Key: = Analyst has f inancial interest = Analyst has material interest = Analyst is a director = Analyst has a business interest

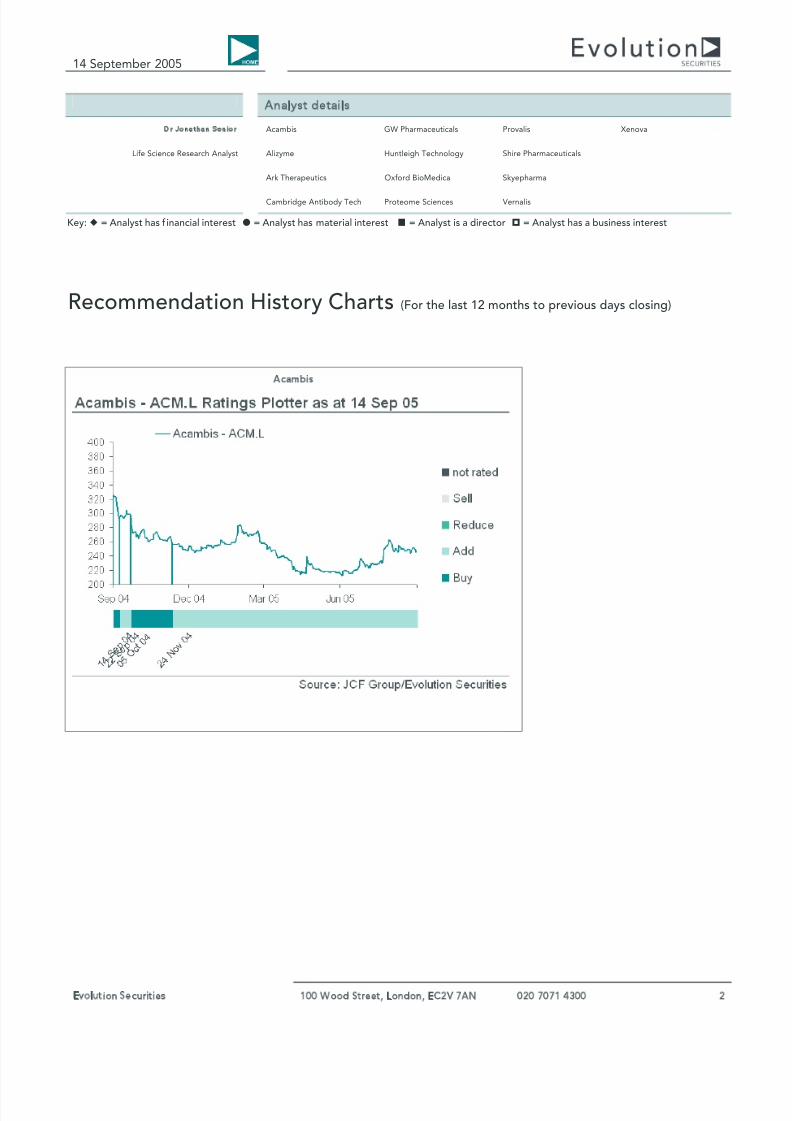

Recommendation History Charts (For the last 12 months to previous days closing)

Acambis

8/15/2019 Broker Note, Acambis, 15/09/2005 (Evolution)

http://slidepdf.com/reader/full/broker-note-acambis-15092005-evolution 6/6

14 September 2005

Evolution Securities 100 Wood Street, London, EC2V 7AN 020 7071 4300 3

% of recommendations(all stocks)

% of recommendations(corporate stocks)

% of recommendations(non corporate stocks)

Evolution Securities – Recommendation Guide

This document is issued by Evolution Securities Ltd (ESL) (Incorporated in England No. 2316630), which is authorised and regulated in the United Kingdom bythe Financial Services Authority (FSA) for designated investment business and is a member of the London Stock Exchange.

This document is for information purposes only and should not be regarded as an offer or solicitation to buy the securities or other instruments mentioned init. Expressions of opinions are those of the research department of ESL only and are subject to change without notice. No representation or warranty, eitherexpressed or implied, is made nor responsibility of any kind is accepted by any Evolution Group company, its directors or employees either as to the accuracyor completeness of any information stated in this document. There is no regular update series for research issued by ESL.

ESL and/or its officers, directors and employees may have or take positions in securities mentioned in this document (or in any related investment) and mayfrom time to time dispose of any such securities (or instrument). ESL may act as a market maker in the securities of companies discussed in this document (orrelated investments), and may sell them or buy them from customers on a principal basis and may also perform underwriting services for or relating to thosecompanies.

ESL or persons connected with it may provide or may have provided corporate services to the issuers of securities mentioned in this material andrecipients of this document should not therefore rely on this report as being an impartial document. Accordingly, information may be known to ESLor persons connected with it which is not reflected in this material.

ESL has a conflicts management policy in relation to its investment research activities, this is available at:http://www.research.evosecurities.com/conflicts.pdf

The stated price of any securities mentioned herein is as at the end of the business day immediately prior to the publication date on this document unlessotherwise stated and is not a representation that any transaction can be effected at this price. No personal recommendation is being made to you; thesecurities referred to may not be suitable for you and should not be relied upon in substitution for the exercise of independent judgement.

ESL shall not be liable for any direct or indirect damages, including lost profits arising in any way from the information contained in this material. This materialis for the use of intended recipients only and only for distribution to professional and institutional investors, i.e. persons who are authorised persons orexempted persons within the meaning of the Financial Services and Markets Act 2000 of the United Kingdom, or persons who have been categorised by ESLas intermediate customers under the rules of the FSA.

This document is being supplied to you solely for your information and may not be reproduced, re-distributed or passed to any other person or published inwhole or in part for any purpose.

The material in this document is not intended for distribution or use outside the United Kingdom. This material is not directed at you if ESL isprohibited or restricted by any legislation or regulation in any jurisdiction from making it available to you.

Recommended