Fabio Meneghin

BRAZILIAN SUGAR / ETHANOL

MARKETSTefla´s India Sugar Summit

Feb 2nd 2018

• Brazil´s macroeconomic current situation

• Petrobras new fuel policy and the new federal taxation

• Basics scenarios for ethanol/sugar

• Costs and Margins

• The indebtedness and real value of sugar/ethanol Assets

• Forecast for brazilian season 18/19

SUMMARY | TOPICS

4,0%

1,9%

3,0%

0,5%

-3,8% -3,6%

1,1%

2,6%3,0%

2011 2012 2013 2014 2015 2016 2017 2018 2019

6,5%5,8% 5,9%

6,4%

10,7%

6,3%

2,9%

3,8%4,3%

2011 2012 2013 2014 2015 2016 2017 2018 2019

Brazil | Main Economic Indicators

GDP Evolution and Forecast (%) Official Inflation Evolution and Forecast (%)

Source: IBGE (GDP and IPCA Inflation index). Forecast: Focus Report from BACEN

Brazil | Main Economic Indicators

Interest Rate – SELIC (%) Net of Jobs creation and forecast (million)

Source: IBGE (GDP and IPCA Inflation index). Forecast: Focus Report from BACEN

14,2%

7,0%

1,94

1,15

1,49

0,40

-1,54-1,32

-0,02

0,50

2011 2012 2013 2014 2015 2016 2017 2018

Exchange Rate – REAL x Dollar

4,0

3,7

3,5

3,3 3,33,3

3,23,1

3,2 3,23,1

3,33,2

Brazil | Main Economic Indicators

Main Questions for

2018:

• Pension Reform

• Congress Renewal

• Presidential Election

• Privatization Agenda

• Tax Reform

Dollar lost 20% value against Real in the last 24 months

Source: BACEN

Brazil | New Policy and taxes for Wholesale Gasoline PricesB

RL

/ L

ite

r

Source: EIA, Petrobras and B3 (PETR4)

1,60

1,49

Jan

-16

Feb

-16

Mar

-16

Ap

r-16

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

De

c-1

6

Jan

-17

Feb

-17

Mar

-17

Ap

r-17

May

-17

Jun

-17

Jul-

17

Au

g-1

7

Sep

-17

Oct

-17

No

v-1

7

CIDE + PIS/COFINS Gasoline BR Gasoline NYFederal Tax

0.48

0.89

Gasoline Prices at refiners and Federal Tax

4,5

19,0

Petrobras´ Shares at B3 (PETR4) - BRL

New taxes on gasoline are favoring

ethanol consumptionIPO of Petrobras subsidiary “BR

Distribuidora” BRDT3 in December 2017

OIL/ETHANOL | Brent prices and E100 Market Share in

Brazil

Source: ICE NY. ANP Brazil

94 9893

4943

51

65,0

US$

/ B

arri

l 23%

20%22% 23%

30%

25% 26,0%28,0%

BRENT OIL Prices Ethanol E100 Market Share in Brazil

3,63 3,583,33

2,48

1,992,17

2,38

2012 2013 2014 2015 2016 2017 2018

24 23 23

23 23 23 22

4345

48 50 51 52 53

1619

22

25 27 29 31

2012 2013 2014 2015 2016 2017 2018

Somente Gasolina Frota Total Leves Frota Flex

Sales of New Cars Fleet by type of Fuel

Brazil | Sales of New Cars and Total Fleet

Source: Anfavea and Denatran

Million of Cars

+9,4%+10%

10,1 9,911,3

13,0

17,9

14,615,8

18,0

8,2 8,010,4 11,0 11,1 11,6 11,7 11,5

28,5

31,9 31,9 33,3

30,031,4 31,6 31,0

Gasoline A

“pure”

Ethanol

Hydrous

Ethanol

Anhydrous

25%20%20% 25%Blend on

Gasoline27%

Brazil | Fuel Consumption

Fonte: ANP e Agroconsult.

Bill

ion

oflit

ers

27% 27% 27%

38% 36%33%

36% 36%

13,5

16,617,5

15,016,0

14/15 15/16 16/17 17/18 18/19

Estoque/Uso NY (USD. ¢/lb)

8

-3 -1

71

14

/15

15

/16

16

/17

17

/18

18

/19

176

167171

182 178

168

170 172

175 178

Produção Consumo

Supply and Demand (mmt) NY Prices (U.S. ¢/pound) and Stock/Use Ratio

Sugar/World | Scenario for 2018/19

Source: USDA. Forecast: Agroconsult. Calendar: Oct-Sep.

Output Consumption

Ratio

Center-South | Cost of Production

Source: Agroconsult.. (Exchange Rate 18/19: BRL 3.20/USD)

Sugar Costs – São Paulo

(US¢/pound)Ethanol Costs in Sugar

Equivalent (US¢/pound)

11,812,9 12,5

13,214,5 14,2

0

2

4

6

8

10

12

14

16

2016/17 2017/18 2018/19

Cost at Mills FOB Costs

13,4

14,6

14,2

12,8

13

13,2

13,4

13,6

13,8

14

14,2

14,4

14,6

14,8

2016/17 2017/18 2018/19

Center-South | Sugar Logistics Costs for Export

Source: Agroconsult..

Santos

Paranaguá

US$ cents

1.56/pound

+18%

+35%

+2%

+38%

Sugar Transportation Costs – 17/18

(US¢/pound)

1,61,6

1,0

1,1

1,2

1,3

1,4

1,5

1,6

1,7

1,8

1,9

2,0

2010 2011 2012 2013 2014 2015 2016 2017 2018

Evolution of the Transportation

Costs in São Paulo (US¢/pound)

14,4

17,5

12,0

13,0

14,0

15,0

16,0

17,0

18,0

NY 11 Anidro SP Hidratado SP

Brazil | Sugar / Ethanol Price Parity in domestic marketU

SD

ce

nts

/ pound

Hydrous

Ethanol SP Anhydrous

Ethanol SP

VHP Sugar

FOB

Source: Ice Futures, Cepea.

Higher taxation over

gasoline to consumer

Brazil | Mix of Production and Ebit Margin

Mix of Production Theoretic Ebit Margin

Source: Agroconsult.

17%14%

7%

25%

19%

24%

16%

-1%

12%

8%

23% 21%

12%

18%

12

/13

13

/14

14

/15

15

/16

16

/17

17

/18

18

/19

Açúcar EtanolSugar Ethanol

50%46%

43%

40%

46% 45%

42%

50%

54%

57%

60%

54% 55%

58%

12

/13

13

/14

14

/15

15

/16

16

/17

17

/18

18

/19

Sugar Ethanol

Sugar/Ethanol Net Revenues – Sector´s

Average

USD / t of cane crushed

EBIT – Sector´s Average

USD / t of cane crushed

Brazil | Mills Net Revenues and EBIT Margin

Source: Agroconsult. Margem Ebit: (Net Revenues / Operational Costs including depreciation)

Admnistrative, Sales and General expenses are not included. Eletric energy not included.

5446

42

3440

44 40

12

/13

13

/14

14/1

5

15

/16

16

/17

17

/18

18

/19

5,16,2

3,3

8,1 8,1 8,07,0

12/1

3

13

/14

14

/15

15

/16

16/1

7

17

/18

18

/19

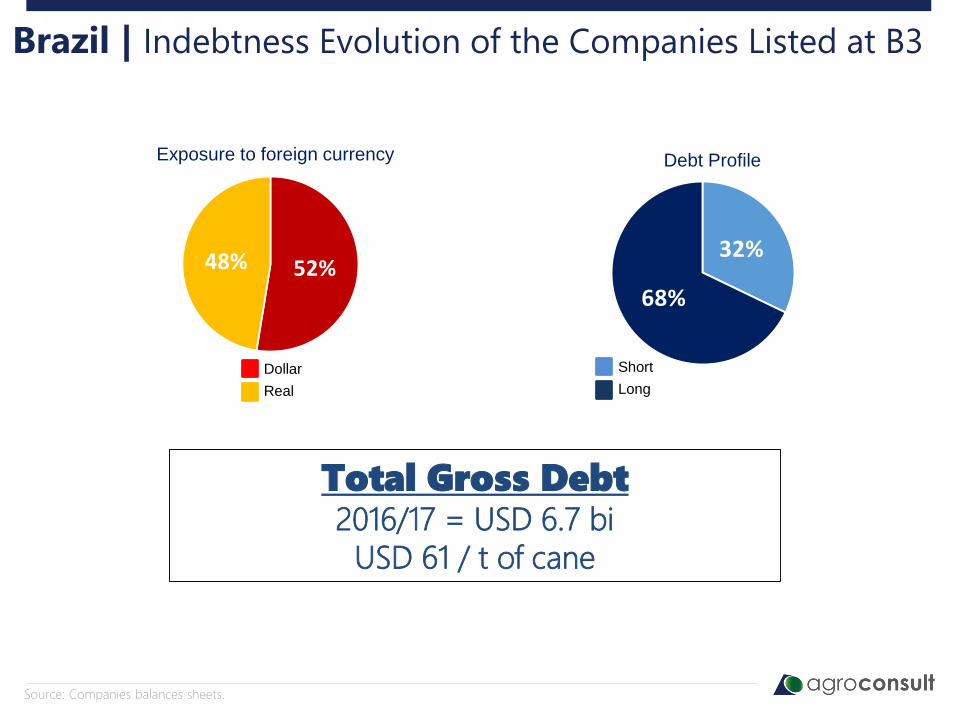

Brazil | Indebtness Evolution of the Companies Listed at B3

Source: Companies balances sheets.

Total Gross Debt2016/17 = USD 6.7 bi

USD 61 / t of cane

52%48%32%

68%

Dollar

Real

Exposure to foreign currency Debt Profile

Short

Long

86 88

49 4357

48 45

37 38

44

2013 2014 2015 2016 2017

Market Value Revenues (USD/t of cane)

Brazil | Market Value of Sugar/Ethanol ProducersCompanies listed on B3 represents 20% of the sector

Source: Agroconsult. With data from listed companies on BM&FBovespa (CSAN3, SMTO3, BSEV3).

Value of Assets under recovery with

more transparency on fuels market

Center-South | Margins of Sugarcane Suppliers

against competitors crops (R$/ha)

Source: Agroconsult

1.047

1.469

829

0

200

400

600

800

1.000

1.200

1.400

1.600

1.800

R$

/ h

ecta

re

Soja + Milho 2ª (MS) Soja + Milho 2ª (GO) Cana-de-açúcar (CS)Soybean + Corn 2nd (GO)Soybean + Corn 2nd (MS) Sugarcane (Center-South)

Sugarcane Fields | Average Age

5,4 – 6,4

5,2 – 5,4

5,0 – 5,2

4,8 – 5,0

2,9 – 4,8

n/a

Age (nº of cuts):

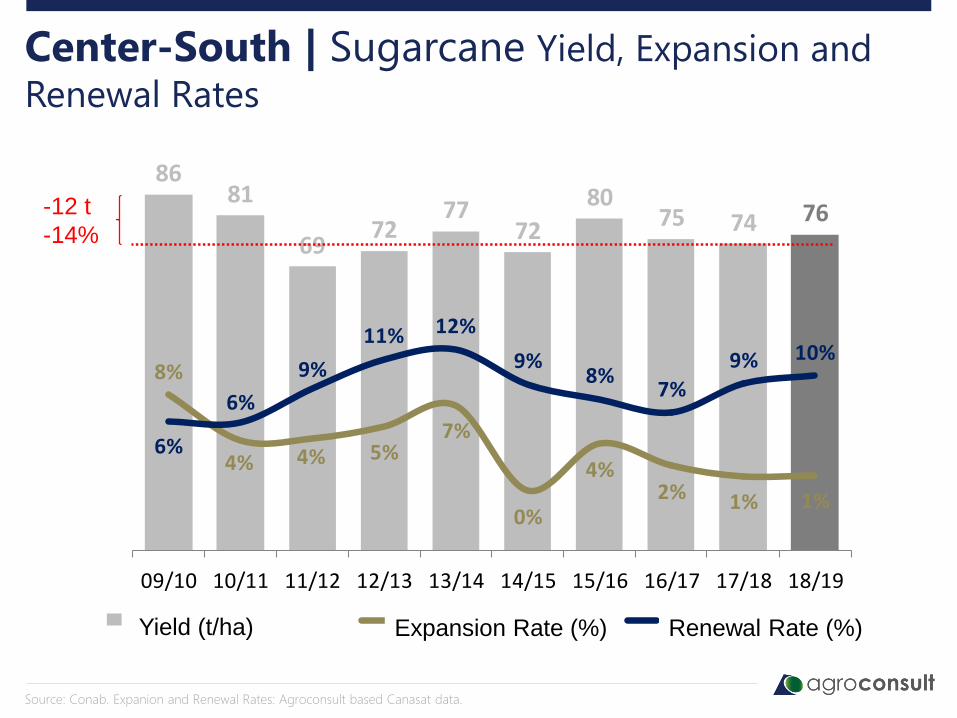

Source: Agrosatélite, based Canasat 2017/18 data. Microrregions with planted area higher than 1000 ha.

8681

6972

7772

8075 74 76

8%

4% 4% 5%7%

0%

4%2% 1% 1%

6%

6%

9%

11% 12%

9%8%

7%

9% 10%

09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18 18/19

Produtividade (t/ha) Taxa de Expansão (%) Taxa de Renovação (%)

Center-South | Sugarcane Yield, Expansion and

Renewal Rates

Source: Conab. Expanion and Renewal Rates: Agroconsult based Canasat data.

-12 t

-14%

Yield (t/ha)Yield (t/ha) Expansion Rate (%) Renewal Rate (%)

533597 575 617 612 594 601

5657 59

49 45 47 49589654 635

666 657 641 650

12/13 13/14 14/15 15/16 16/17 17/18 18/19

CS N-NE

Source: CONAB. Agroconsult. 18/19: Another 0.5 billion liters will come from corn (MT and GO states)

Brazil | Sugarcane Crushing. Sugar/Ethanol Output

35,9

32,9

2,4

2,2

38,4

35,1

2017/18 2018/19

mm

t

Centro-Sul N-NE

26,027,5

2,3

2,028,3

29,5

2017/18 2018/19

bil

hõ

es d

e li

tro

s

Centro-Sul N-NE

MM

T

Bill

ion

oflit

ers

RENOVABIO

• Long-term plan (2030) to incentive the use of renewable energy in the light

fuels market, with emphasis on ethanol.

• Brazilian commitment to the COP21 Climate Agreement, which aims to

reduce CO2 emissions by 43% (on a 2005 basis) until 2030.

• The proposal predicts the need for 54 billion ethanol by 2030.

• Plan Guidelines:

1. Maintain the gasoline price policy in line with the international market

2. Recognition of the positive externalities of ethanol with clear environmental

taxation on fossil fuels (CIDE)

3. Implementation of an emission certificate system (CDBios - Fuel Savings

Credit - Similar to US RINs)

AGROCONSULT

Agribusiness services for banks, investment funds, M&A operations.

• Market analysis and sizing

• Analysis of Investments

• Assets and Land Valuation

• Due Diligences (Agricultural and Industrial)

agroconsult.com.br+55 48 3209-1650

Recommended