International Workshop on Enhancing Access to Formal Financial

Services in Indonesia

December 9th 2009. Jakarta.

Directorat of Banking Research and Regulation

Beyond Credit; Financial Inclusion &Broader Access to FinancePresented by: Halim Alamsyah

1. Introduction;

– Access to finance (current conditions)

– G-20 Leader’s Statement

– Financial system in Indonesia

2. Indonesian Approach to Access to Finance

3. Problems in Building Financial Inclusion

4. Programs for Broader Access to Finance

(How to Reduce Asymmetric Information + Participating Guarantee

Scheme)

– The importance of financial education

– Financial identity database

– Saving account for basic saver

– Micro financial institutions (MFI’s) development & capacity building

– Building Strategic Network Among Related Institutions

Table of Contents

1. Introduction;

– Access to finance (current conditions)

– G-20 Leader’s Statement

– Financial system in Indonesia

2. Indonesian Approach to Access to Finance

3. Problems in Building Financial Inclusion

4. Programs for Broader Access to Finance

(How to Reduce Asymmetric Information + Participating Guarantee

Scheme)

– The importance of financial education

– Financial identity database

– Saving account for basic saver

– Micro financial institutions (MFI’s) development & capacity building

– Building Strategic Network Among Related Institutions

Table of Contents

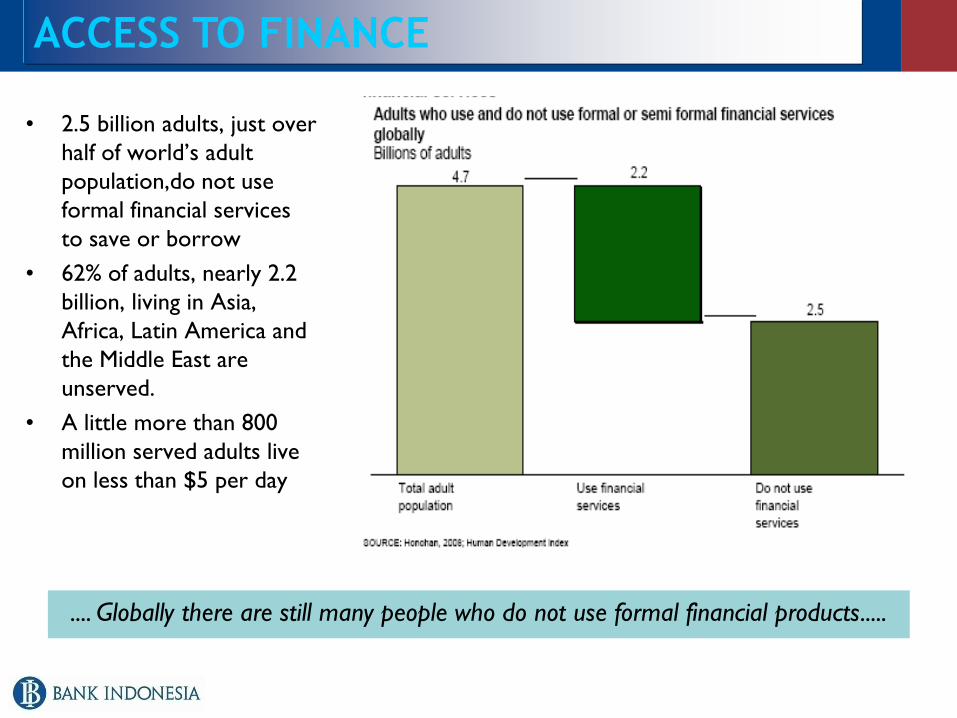

• 2.5 billion adults, just over

half of world’s adult

population,do not use

formal financial services

to save or borrow

• 62% of adults, nearly 2.2

billion, living in Asia,

Africa, Latin America and

the Middle East are

unserved.

• A little more than 800

million served adults live

on less than $5 per day

ACCESS TO FINANCE

.... Globally there are still many people who do not use formal financial products.....

• At the end of 2008 the number of loans accounts / financing in

bank accounts reached 29,464,202 and the number of savings

accounts reached 73,832,779 accounts.

• While the Indonesian population is 228,523,300 persons, and with

assumption that 70% of the population are productive age

population, means in 2008 only 18% have access to credit and 46%

have access to savings accounts

• This shows that the existing financial institutions (in this case the

bank) has not utilized optimally because there is still large enough

population that do not have access to financial institutions/banks.

ACCESS TO FINANCE IN INDONESIA

.... In Indonesian, existing financial institutions (in this case the bank) has not

utilized optimally.....

6

• To take new steps to increase access to finance among

the world’s poorest

• Commit to improve access to financial services to the

poor such as micro finance

• Will launch a G-20 financial inclusion experts groups

• Commit to launch a G-20 SME finance challenge

G-20 Leaders’ Statement in The Pittsburg Summit

on September 2009

.... Commitment of G-20 Leaders to improve access to financial services to the poor.....

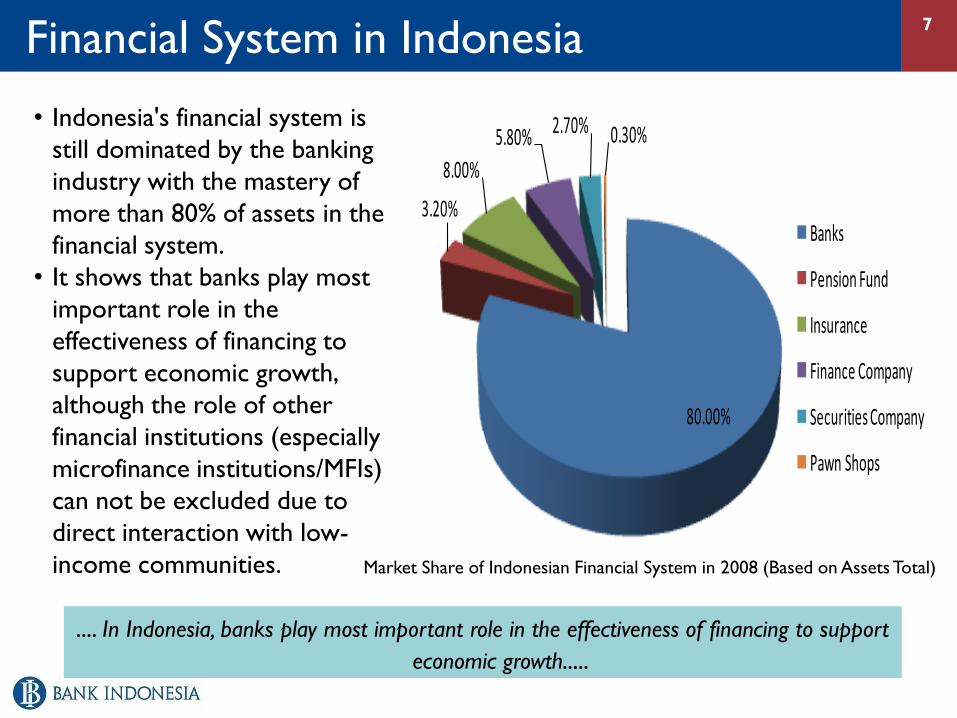

Financial System in Indonesia7

80.00%

3.20%

8.00%

5.80% 2.70% 0.30%

Banks

Pension Fund

Insurance

Finance Company

Securities Company

Pawn Shops

• Indonesia's financial system is

still dominated by the banking

industry with the mastery of

more than 80% of assets in the

financial system.

• It shows that banks play most

important role in the

effectiveness of financing to

support economic growth,

although the role of other

financial institutions (especially

microfinance institutions/MFIs)

can not be excluded due to

direct interaction with low-

income communities. Market Share of Indonesian Financial System in 2008 (Based on Assets Total)

.... In Indonesia, banks play most important role in the effectiveness of financing to support

economic growth.....

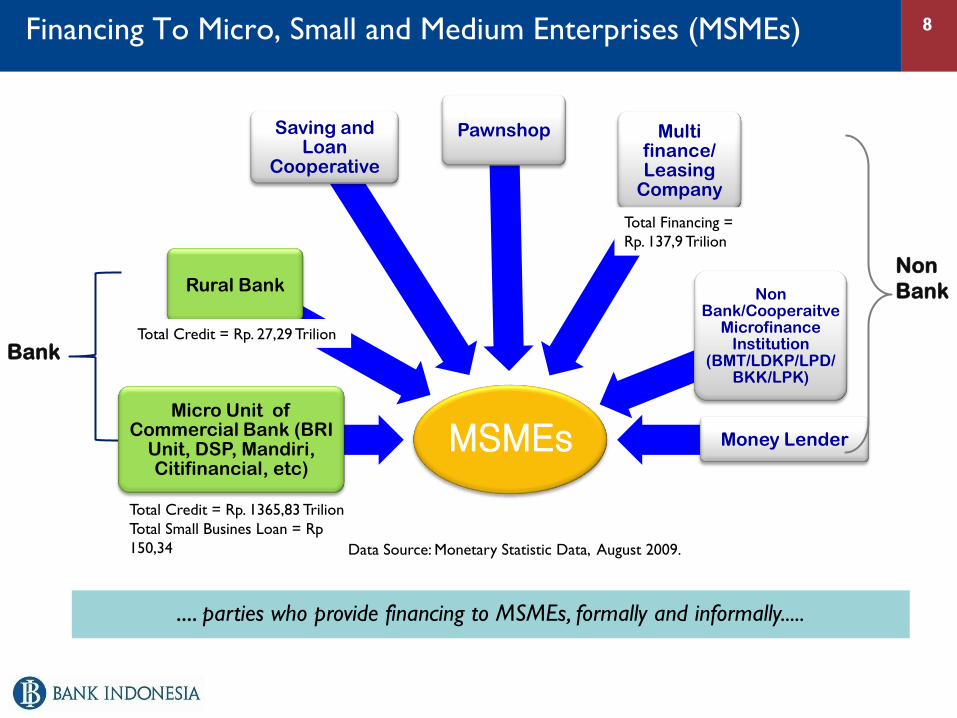

Financing To Micro, Small and Medium Enterprises (MSMEs) 8

MSMEs Micro Unit of

Commercial Bank (BRI Unit, DSP, Mandiri, Citifinancial, etc)

Rural Bank

Saving and Loan

Cooperative

Pawnshop Multi finance/ Leasing

Company

Non Bank/Cooperaitve

MicrofinanceInstitution

(BMT/LDKP/LPD/BKK/LPK)

Money Lender

Bank

Non

Bank

Total Credit = Rp. 1365,83 Trilion

Total Small Busines Loan = Rp

150,34

Total Credit = Rp. 27,29 Trilion

Total Financing =

Rp. 137,9 Trilion

Data Source: Monetary Statistic Data, August 2009.

.... parties who provide financing to MSMEs, formally and informally.....

1. Introduction;

– Access to finance (current conditions)

– G-20 Leader’s Statement

– Financial system in Indonesia

2. Indonesian Approach to Access to Finance

3. Problems in Building Financial Inclusion

4. Programs for Broader Access to Finance

(How to Reduce Asymmetric Information + Participating Guarantee

Scheme)

– The importance of financial education

– Financial identity database

– Saving account for basic saver

– Micro financial institutions (MFI’s) development & capacity building

– Building Strategic Network Among Related Institutions

Table of Contents

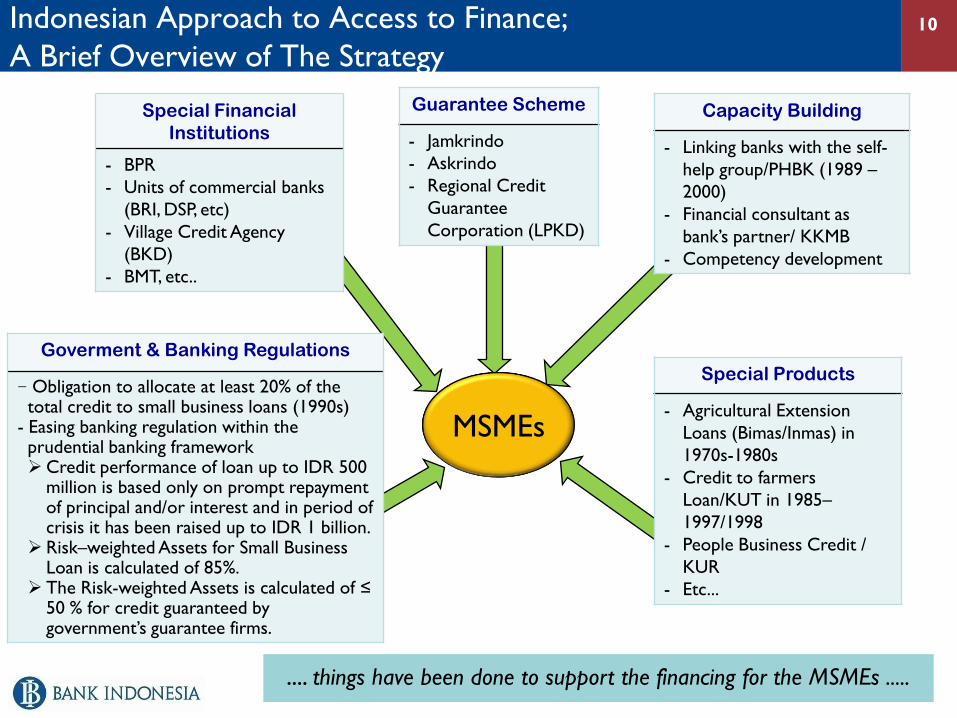

Indonesian Approach to Access to Finance;

A Brief Overview of The Strategy10

MSMEs

Special Financial

Institutions

- BPR

- Units of commercial banks

(BRI, DSP, etc)

- Village Credit Agency

(BKD)

- BMT, etc..

Guarantee Scheme

- Jamkrindo

- Askrindo

- Regional Credit

Guarantee

Corporation (LPKD)

Capacity Building

- Linking banks with the self-

help group/PHBK (1989 –

2000)

- Financial consultant as

bank’s partner/ KKMB

- Competency development

Goverment & Banking Regulations

- Obligation to allocate at least 20% of the total credit to small business loans (1990s)

- Easing banking regulation within the prudential banking frameworkCredit performance of loan up to IDR 500

million is based only on prompt repayment of principal and/or interest and in period of crisis it has been raised up to IDR 1 billion.

Risk–weighted Assets for Small Business Loan is calculated of 85%.

The Risk-weighted Assets is calculated of ≤50 % for credit guaranteed by government’s guarantee firms.

Special Products

- Agricultural Extension

Loans (Bimas/Inmas) in

1970s-1980s

- Credit to farmers

Loan/KUT in 1985–

1997/1998

- People Business Credit /

KUR

- Etc...

.... things have been done to support the financing for the MSMEs .....

1. Introduction;

– Access to finance (current conditions)

– G-20 Leader’s Statement

– Financial system in Indonesia

2. Indonesian Approach to Access to Finance

3. Problems in Building Financial Inclusion

4. Programs for Broader Access to Finance

(How to Reduce Asymmetric Information + Participating Guarantee

Scheme)

– The importance of financial education

– Financial identity database

– Saving account for basic saver

– Micro financial institutions (MFI’s) development & capacity building

– Building Strategic Network Among Related Institutions

Table of Contents

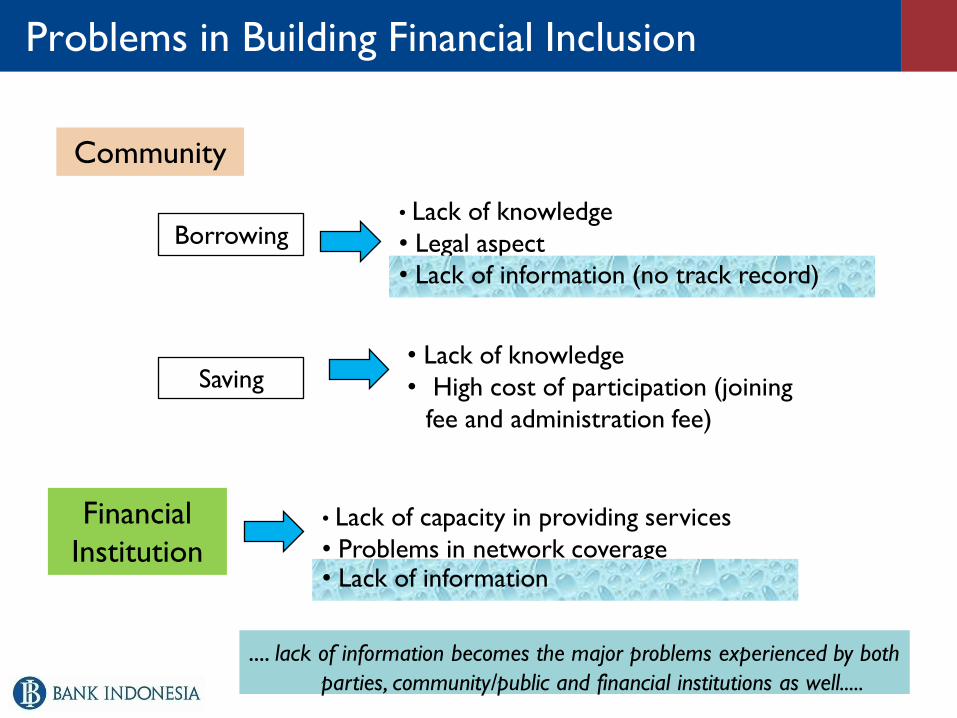

Problems in Building Financial Inclusion

Community

Financial

Institution

Borrowing

Saving• Lack of knowledge

• High cost of participation (joining

fee and administration fee)

• Lack of knowledge

• Legal aspect

• Lack of capacity in providing services

• Problems in network coverage

• Lack of information (no track record)

• Lack of information

.... lack of information becomes the major problems experienced by both

parties, community/public and financial institutions as well.....

1. Introduction;

– Access to finance (current conditions)

– G-20 Leader’s Statement

– Financial system in Indonesia

2. Indonesian Approach to Access to Finance

3. Problems in Building Financial Inclusion

4. Programs for Broader Access to Finance

(How to Reduce Asymmetric Information + Participating Guarantee

Scheme)

– The importance of financial education

– Financial identity database

– Saving account for basic saver

– Micro financial institutions (MFI’s) development & capacity building

– Building Strategic Network Among Related Institutions

Table of Contents

The Importance of Financial Education14

• Financial education is something that can not be ruled out to establish the

financial literated community; good understanding in financial institutions,

financial products and services, as well as financial management to achieve a

better living in the future.

• Financial education is an effort to change public behavior. Therefore, financial

education is a long-term program (more than 5 years).

• Because of the financial institutions are still dominated by banks, the financial

education begins with implementing banking education programs.

• Bank Indonesia in this regard have been initiated implementing banking

education since 2007 and intensified starting in 2008 with the declaration of

banking education year .

.... financial education needs to be done to improve the financial knowledge of the community .....

The Importance of Financial Education (continued...)15

Goals of banking education programs are:

• To build people's interest in banking (bank-minded & awareness)

• To increase public awareness in banking products and services as

well as awareness of the rights and obligations of customers

• To increase public awareness in prudential aspects of financial

transactions (risk awareness); and

• To increase awareness of the availability of complaints and dispute

settlement mechanisms to resolve problems with the bank

Financial Identitiy Database/Number16

• Financial identity database is a database contains data about the financial condition of a

person or a micro and small businesses that can be used by financial institutions as a

reference in providing financing.

• Financial identity database is more directed to those who have not been associated with

financial institutions. Datas are collected through community groups at the lower level,

such as the social gathering, farmers' groups, youth groups (karang taruna), and so on.

• The basic idea of the financial identity database is the asymmetric information

between financial institutions and small communities. In this case, the small communities

are often considered not "bankable" to save or borrow money because it can not meet

the financial institution’s requirements.

• On the other side they are who considered not "bankable" actually has great potential,

both as borrower and saver. They are generally small and micro entrepreneurs who have

good business prospects

• To reduce the information gap, both public and financial institutions can take advantage

from financial identity database as a means of clearing house of information about the

financial condition of customers/prospective customers of financial institutions.

.... Financial Identity Database needs to be provided to reduce the information gap problems

between public and financial institutions...

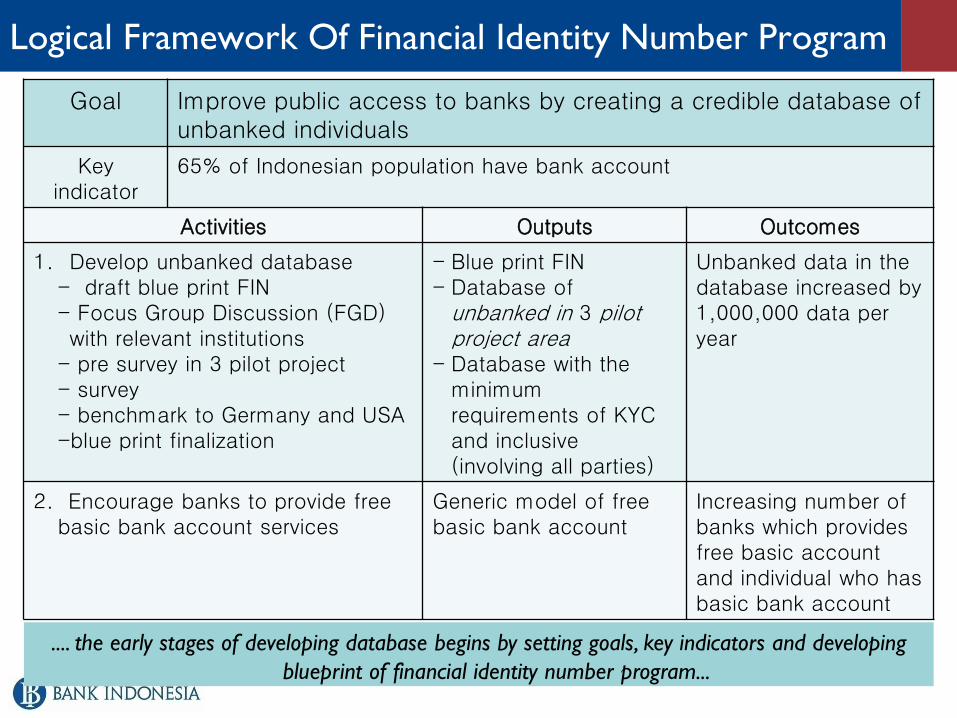

Logical Framework Of Financial Identity Number Program

Goal Improve public access to banks by creating a credible database of unbanked individuals

Keyindicator

65% of Indonesian population have bank account

Activities Outputs Outcomes

1. Develop unbanked database - draft blue print FIN- Focus Group Discussion (FGD) with relevant institutions

- pre survey in 3 pilot project- survey- benchmark to Germany and USA-blue print finalization

- Blue print FIN- Database of

unbanked in 3 pilot project area

- Database with the minimum requirements of KYC and inclusive (involving all parties)

Unbanked data in the database increased by 1,000,000 data per year

2. Encourage banks to provide free basic bank account services

Generic model of free basic bank account

Increasing number of banks which provides free basic account and individual who has basic bank account

.... the early stages of developing database begins by setting goals, key indicators and developing

blueprint of financial identity number program...

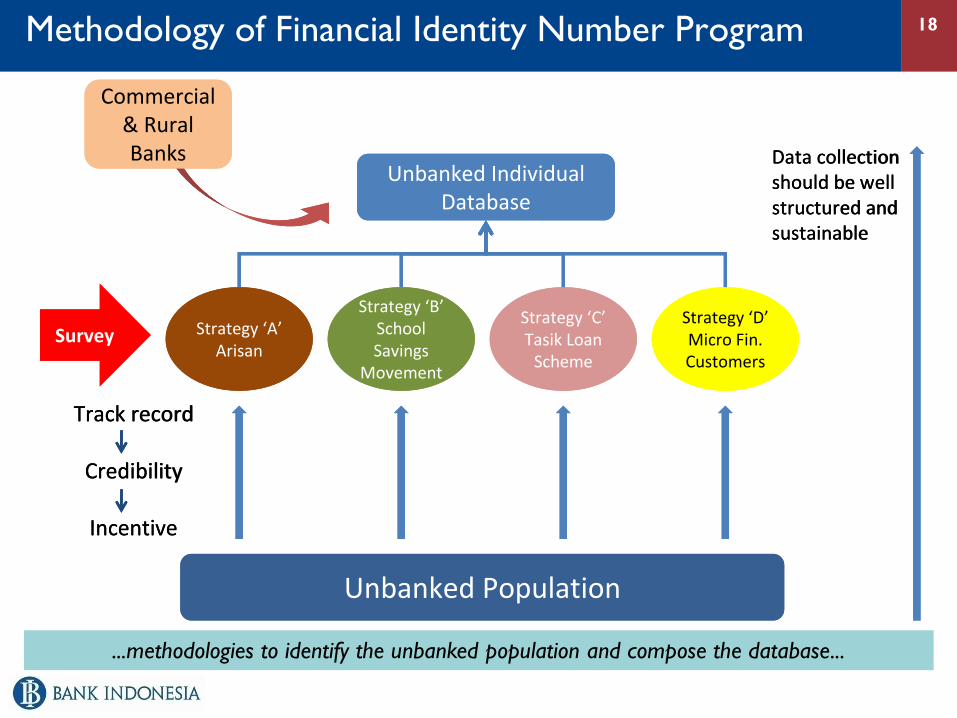

Methodology of Financial Identity Number Program 18

Unbanked Individual Database

Strategy ‘A’Arisan

Strategy ‘B’School Savings

Movement

Strategy ‘C’Tasik Loan

Scheme

Strategy ‘D’Micro Fin. Customers

Unbanked Population

Data collection should be well structured and sustainable

Commercial & Rural Banks

Track record

Credibility

Incentive

Survey

Unbanked Individual Database

Strategy ‘A’Arisan

Strategy ‘B’School Savings

Movement

Strategy ‘C’Tasik Loan

Scheme

Strategy ‘D’Micro Fin. Customers

Unbanked Population

Data collection should be well structured and sustainable

Commercial & Rural Banks

Track record

Credibility

Incentive

Survey

...methodologies to identify the unbanked population and compose the database...

Saving Account for Basic Saver

• Currently almost all financial institutions, particularly banks, charging the same monthly

administrative fee regardless of the existing balance. In addition, some banks are put

different rate/yield for a particular balance where generally low interest rates/yield will be

given to low savings balance.

• With this condition, not surprising if basic saver’s savings balance will continue eroded

because of the imposition of administrative costs that is greater than the interest/yield. If

this condition is continously allowed, then the consequence is the low-income people's

reluctance to keep money in banks and in turn will not lead the financial inclusion efforts.

• To overcome this condition, we need to create a special savings scheme for small savers

with low cost. This special saving scheme will provide financial access for low-income

communities and beginner depositors.

• In the beginning of 2010, most of national banks will launch a saving product named

TabunganKu, that is a saving product for individuals with easy and light requirements

without the administrative costs. This product is a joint product issued by most national

banks to enhance the saving culture and to improve the public welfare.

... the need for special savings products for low-income communities and beginner depositors...

20Micro Financial Institutions Development and Capacity Building

1. Linkage Program

Through linkage program, commercial banks with large financing resources

but can not distribute because of the limited scope and understanding of

the characteristics of borrowers can use the network of rural banks to

distribute the funds. This considers that rural banks have advantage in

reaching remote areas and its human resources likely familiar with the

characteristics of the debtor.

Through synergic cooperation between commercial and rural banks will

help the community to meet their funding needs.

Up to now linkage program have been able to deliver approximately Rp6, 5

trillion to the public financing of low income community and micro and

small businesses

Recently, linkage program even started extended to incorporate

cooperatives in order to have further improvement of public access to

financial institutions

... linkage program between commercial banks and rural banks, to improve the capacity of rural

bank to provide financing for the MSMEs...

21Micro Financial Institutions Development and Capacity Building

2. Encouraging the Role of Credit Guarantee

Facilitating access of MSMEs to bank loan for: "Feasible“ MSMEs (have a

good prospect on business), but... Not “Bankable” (dealing with collateral

problem)

BI acts as a facilitator:

- Regional parliament : approval to place fund in the credit guarantee

corporation

- MoU between regional government and credit guarantee corporation

- MoU between credit guarantee corporation and banks

Until now, regional credit guarantee institutions have been established in 19

provinces

... Credit guarantee especially to overcome MSME’s collateral problems in

obtaining bank’s financing ...

22

3. Provide technical assisstance and competency improvement for rural banks/MFIs and

MSMEs

Certification for rural banks Directors

Technical assistance : training, research, dissemination information and MSMEs

cluster development.

Linking banks with the self-help group/PHBK (1989 – 2000)

Financial consultant as bank’s partner/ KKMB

Developing database of potential SMEs

4. Promoting the establishment of MSME center

Special unit extending services to MSMEs

Information center for MSMEs clients

5. Facilitating dialogue between banking sector, MSMEs sector and government agencies in

the form of seminar, focus group discussion or exhibition (bazaar of banking

intermediary).

6. Supporting the establishment of Credit Bureau

Center of database on all bank

Micro Financial Institutions Development and Capacity Building

Building Strategic Network Among Related Institutions

• All parties have to carry out their respective roles in order to obtain synergies in enhancing financial

access and building financial inclusion;

– Financial Authorities facilitate and build a conducive situation for financial institutions to

carry out their duties as intermediary institutions.

– Financial institutions play their main role to do intermediary function.

– Development of financial identity database, linkage program, regional credit guarantee scheme,

providing special saving scheme are some examples of programs that can and should be done

by the financial authorities and financial institutions under its supervision.

– On the other hand, community also need to be empowered to improve their understanding

in financial institutions, financial products and their characteristics (benefits, risks, fees), rights

and obligations of public and financial institutions, and gradually lead to create financial planning

behavior for a better future.

– Related to this, non-governmental self help organizations together with banking

education working group could take a major role to accelerate the process of community

empowerment through educational activities that directly touch the major financial problems

that often faced by community.

• In addition, cooperation with other agencies such as Ministry of National Education, Ministry

of Home Affairs, Ministry of Cooperatives and SMEs, Ministry of Social Affairs, needs to be done to

further expansion of financial access. Cooperation can be done with the implementation of joint

programs or to integrate financial education programs in each government agencies programs that

have relevance to the wider community.

... all stakeholders should work together and build strategic network to

improve public access to financial ...

24

End of

PresentationThank You

Recommended