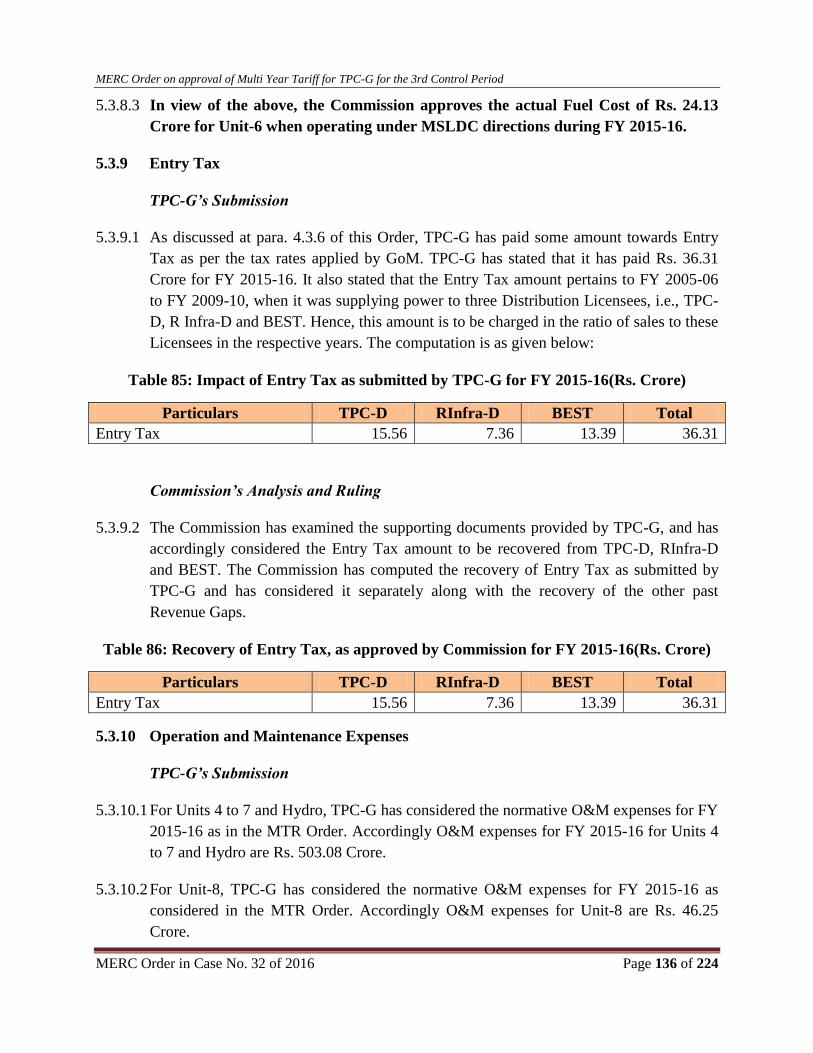

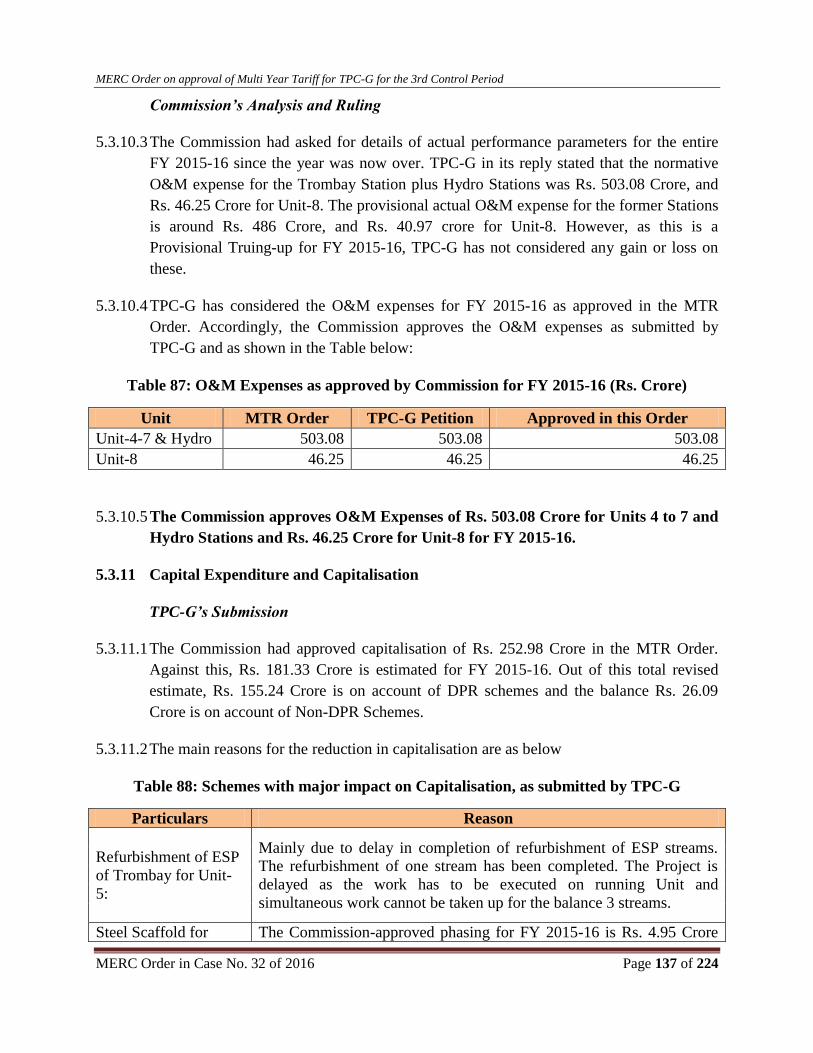

MERC Order in Case No. 32 of 2016 Page 1 of 224

Before the

MAHARASHTRA ELECTRICITY REGULATORY COMMISSION

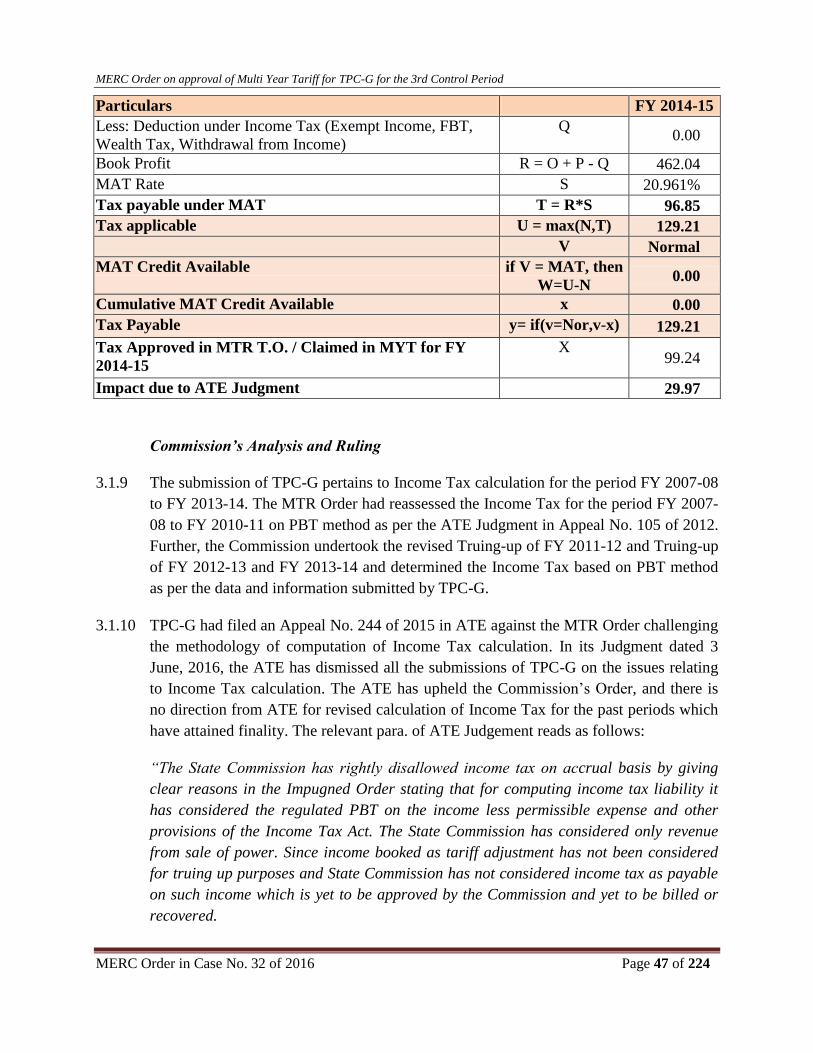

13th Floor, Centre No.1, World Trade Centre, Cuffe Parade, Mumbai- 400 005

Tel: 022 - 22163964/65/69 Fax: 022 - 22163976

E-mail: [email protected]

Website: www.merc.gov.in / www.mercindia.org.in

CASE No. 32 of 2016

In the matter of

Petition of Tata Power Company Ltd. (Generation) for Truing-up of FY 2014-15,

Provisional Truing-up for FY 2015-16 and ARR and Tariff for the 3rd Control

Period FY 2016-17 to FY 2019-20

CORAM

Shri Azeez M. Khan, Member

Shri Deepak Lad, Member

ORDER

Date: 8 August, 2016

The Tata Power Company Limited (Generation Business) (TPC-G) has, under Regulation 5 of

the MERC (Multi Year Tariff (MYT)) Regulations (‘MYT Regulations’), 2015, filed its Petition

for Truing-up of FY 2014-15, Provisional Truing-up of FY 2015-16 and Aggregate Revenue

Requirement (ARR) and Tariff for the 3rd

Control Period from FY 2016-17 to FY 2019-20. The

Truing-up for FY 2014-15 and Provisional Truing-up for FY 2015-16 is approved under the

MYT Regulations, 2011, while the ARR forecast and Tariff for FY 2016-17 to FY 2019-20 are

as per MYT Regulations, 2015. The original Petition was filed on 11 February, 2016. TPC-G

filed a revised Petition on 24 March, 2016.

The Commission, in exercise of its powers under Sections 61 and 62 of the Electricity Act (EA),

2003 and all other powers enabling it in this behalf, and after considering the submissions made

by TPC-G, suggestions and objections received, issues raised during the Public Hearing and

other relevant material, issues the following Order.

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 2 of 224

TABLE OF CONTENTS

1 BACKGROUND AND REGULATORY PROCEEDINGS .............................................................. 16

1.1. Background ................................................................................................................................. 16

1.2. MYT Regulations, 2011 .............................................................................................................. 16

1.3. Business Plan Order for MYT 2nd

Control Period ...................................................................... 16

1.4. Truing-up of FY 2011-12 and ARR for 2nd

Control Period FY 2012-13 to FY 2015-16 ........... 16

1.5. Truing-up of FY 2012-13 and FY 2013-14, Provisional Truing-up of FY 2014-15 and

Projection of ARR and Tariff for FY 2015-16 ........................................................................................ 17

1.6. MYT Regulations, 2015 .............................................................................................................. 17

1.7. Admission of the Petition and Public Consultation Process ....................................................... 17

1.8. Organisation of the Order ........................................................................................................... 19

2 SUGGESTIONS/ OBJECTIONS RECEIVED, TPC-G’S RESPONSE AND COMMISSION’S

VIEW .......................................................................................................................................................... 21

2.1 Fuel Prices ................................................................................................................................... 21

2.2 Competitive Bidding for Power Purchase ................................................................................... 24

2.3 Blended Tariff for Unit-7 ............................................................................................................ 26

2.4 GT Losses ................................................................................................................................... 27

2.5 Colony Consumption .................................................................................................................. 28

2.6 Unit-7 PLF for 3rd

Control Period ............................................................................................... 29

2.7 Foreign Exchange Loss ............................................................................................................... 29

2.8 Income Tax ................................................................................................................................. 30

2.9 Capital Expenditure and Capitalisation ....................................................................................... 31

2.10 O&M Expenses ........................................................................................................................... 33

2.11 Sharing of Unit-6 Fixed Cost ...................................................................................................... 34

2.12 Delayed Payment Charges .......................................................................................................... 35

2.13 Force Majeure in case of Units 7 and 8....................................................................................... 35

2.14 Incentive for Backing Down of Units ......................................................................................... 37

2.15 Property Tax ................................................................................................................................ 37

2.16 Recovery of Fixed Cost for Bhira Hydro Station ........................................................................ 38

2.17 Submissions for 3rd

Control Period ............................................................................................. 39

2.18 Shortcomings in Petition Filing .................................................................................................. 41

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 3 of 224

3 IMPACT OF ATE JUDGMENTS ON PREVIOUS YEARS’ TRUE-UP ......................................... 42

3.1 Appeal challenging MTR Order dated 26 June, 2015 in Case 6 of 2015 ................................... 42

4 TRUING-UP FOR FY 2014-15 .......................................................................................................... 49

4.1 Background ................................................................................................................................. 49

4.2 Performance Parameters ............................................................................................................. 49

4.3 Performance of Units-4 to 7 and Hydro Stations ........................................................................ 49

4.3.1 Availability and Gross Generation ...................................................................................... 49

4.3.2 Auxiliary Energy Consumption .......................................................................................... 52

4.3.3 Gross Station Heat Rate ...................................................................................................... 61

4.3.4 Fuel Cost ............................................................................................................................. 63

4.3.5 Fuel Cost of Unit-6 under MSLDC Directions ................................................................... 66

4.3.6 Entry Tax ............................................................................................................................ 67

4.3.7 Operation and Maintenance Expenses ................................................................................ 68

4.3.8 Capital Expenditure and Capitalisation ............................................................................... 73

4.3.9 Non-DPR Capitalisation for FY 2010-11 to FY 2013-14 ................................................... 75

4.3.10 Depreciation ........................................................................................................................ 79

4.3.11 Interest on Long-term Loans ............................................................................................... 81

4.3.12 Return on Equity ................................................................................................................. 83

4.3.13 Interest on Working Capital ................................................................................................ 84

4.3.14 Income Tax ......................................................................................................................... 85

4.3.15 Non-Tariff Income .............................................................................................................. 87

4.3.16 Revenue from Sale of Power .............................................................................................. 87

4.3.17 PLF Incentive for Thermal Station and Hydro Incentive for Hydro Stations ..................... 88

4.3.18 Reduction of Fixed Charges on account of lower Availability of Unit-7 ........................... 89

4.3.19 Sharing of Gains / Losses for FY 2014-15.......................................................................... 93

4.3.20 Gains / Losses on account of fuel costs .............................................................................. 93

4.3.21 Gains / Losses on account of Auxiliary Consumption ........................................................ 94

4.3.22 Gains / Losses on account of O&M Expenses .................................................................... 95

4.3.23 Net Entitlement, and resultant Gap/ Surplus for Units 4 to 7 and Hydro Stations .............. 97

4.4 Performance of Unit-8 ................................................................................................................ 99

4.4.1 Gross Generation................................................................................................................. 99

4.4.2 Auxiliary Energy Consumption ........................................................................................ 100

4.4.3 Gross Station Heat Rate .................................................................................................... 100

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 4 of 224

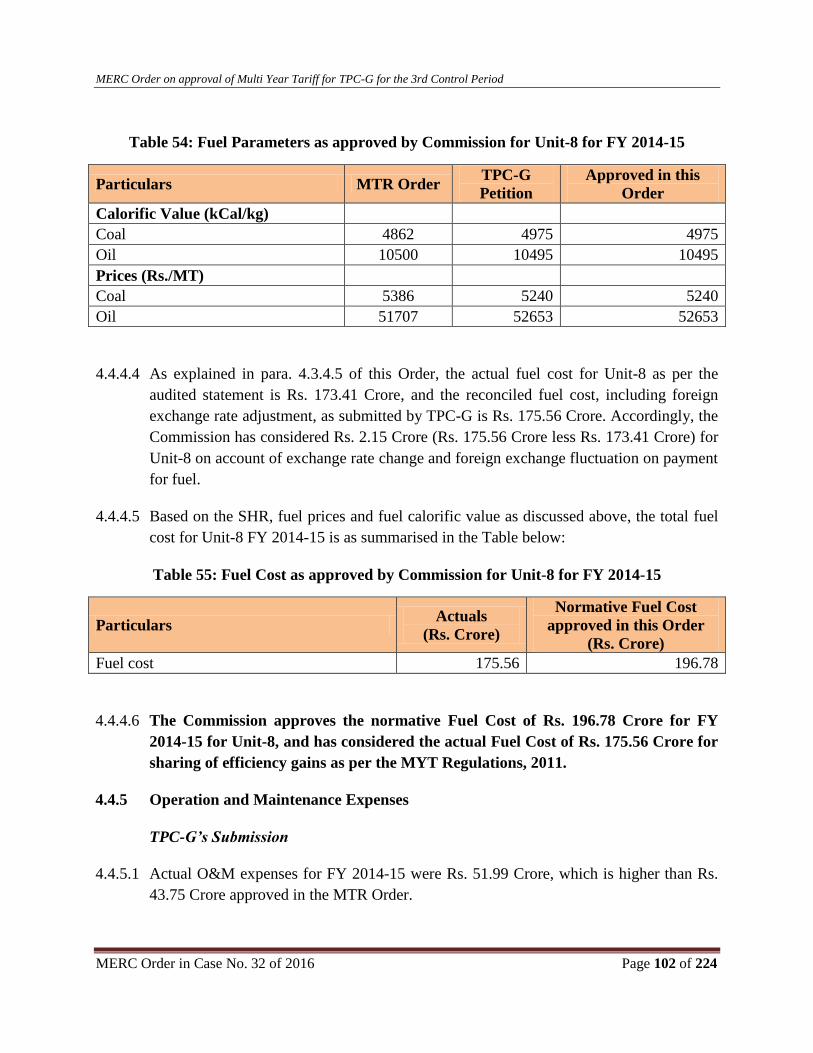

4.4.4 Fuel Cost ........................................................................................................................... 101

4.4.5 Operation and Maintenance Expenses .............................................................................. 102

4.4.6 Capital Expenditure and Capitalisation ............................................................................. 103

4.4.7 Non-DPR Capitalisation for FY 2011-12 to FY 2013-14 ................................................. 104

4.4.8 Depreciation ...................................................................................................................... 106

4.4.9 Interest on Long-term Loan .............................................................................................. 107

4.4.10 Return on Equity ............................................................................................................... 109

4.4.11 Interest on Working Capital .............................................................................................. 110

4.4.12 Income Tax ....................................................................................................................... 110

4.4.13 Non-Tariff Income ............................................................................................................ 111

4.4.14 Revenue from Sale of Power ............................................................................................ 111

4.4.15 Reduction of Fixed Charges on account of lower Availability of Unit-8 ......................... 112

4.4.16 Sharing of Gains / Losses for FY 2014-15........................................................................ 119

4.4.17 Gains / Losses on account of fuel cost .............................................................................. 119

4.4.18 Efficiency Gains / Losses on account of Auxiliary Energy Consumption ........................ 119

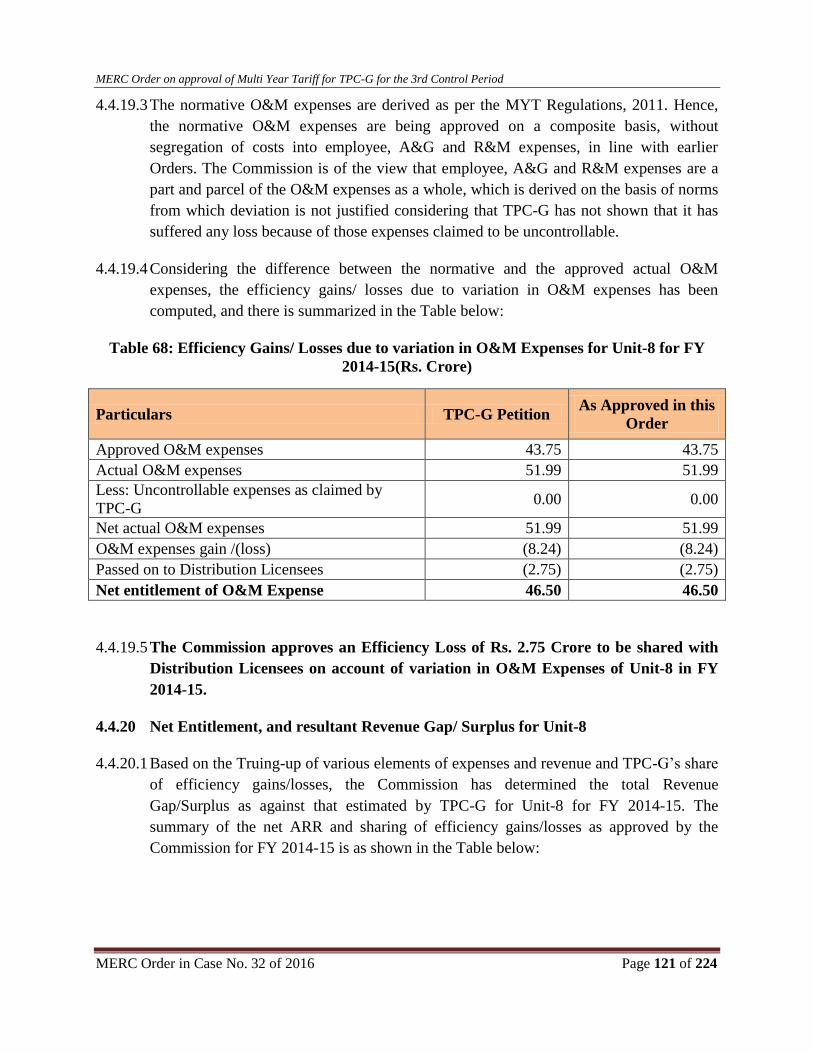

4.4.19 Efficiency Gains / Losses on account of O&M Expenses ................................................ 120

4.4.20 Net Entitlement, and resultant Revenue Gap/ Surplus for Unit-8 ..................................... 121

5. PROVISIONAL TRUE-UP OF ARR FOR FY 2015-16 .................................................................. 124

5.1 Background ........................................................................................................................... 124

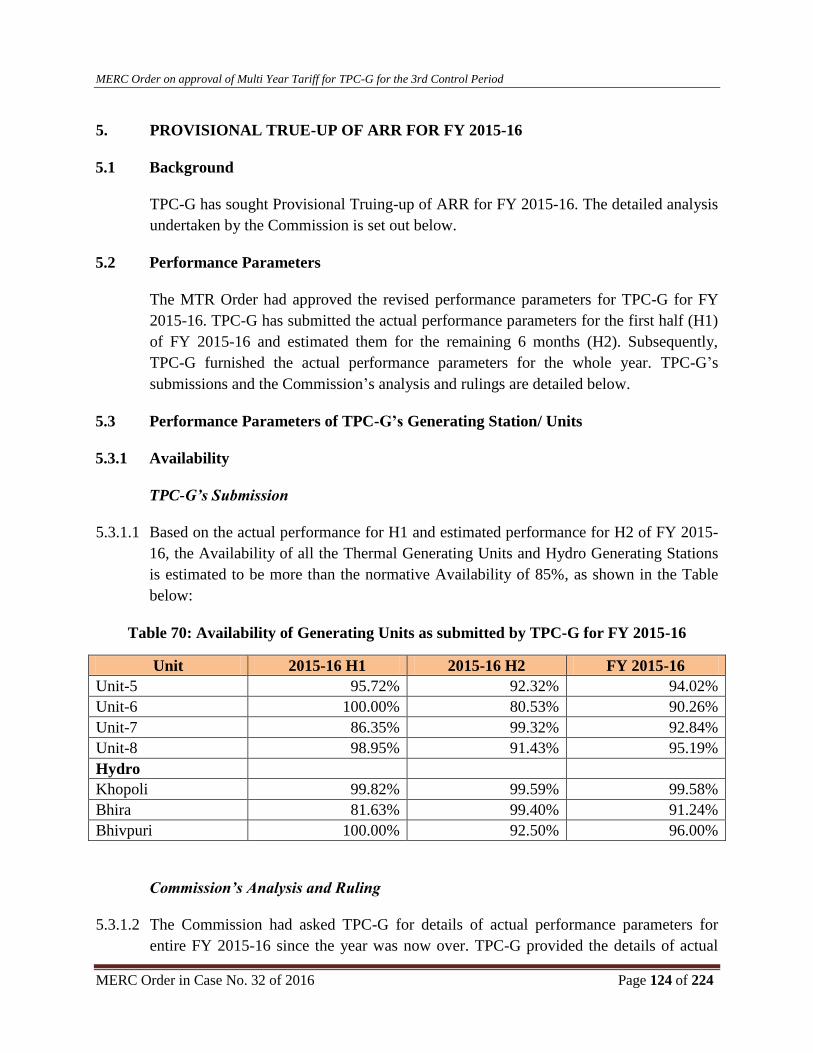

5.2 Performance Parameters ....................................................................................................... 124

5.3 Performance Parameters of TPC-G’s Generating Station/ Units .......................................... 124

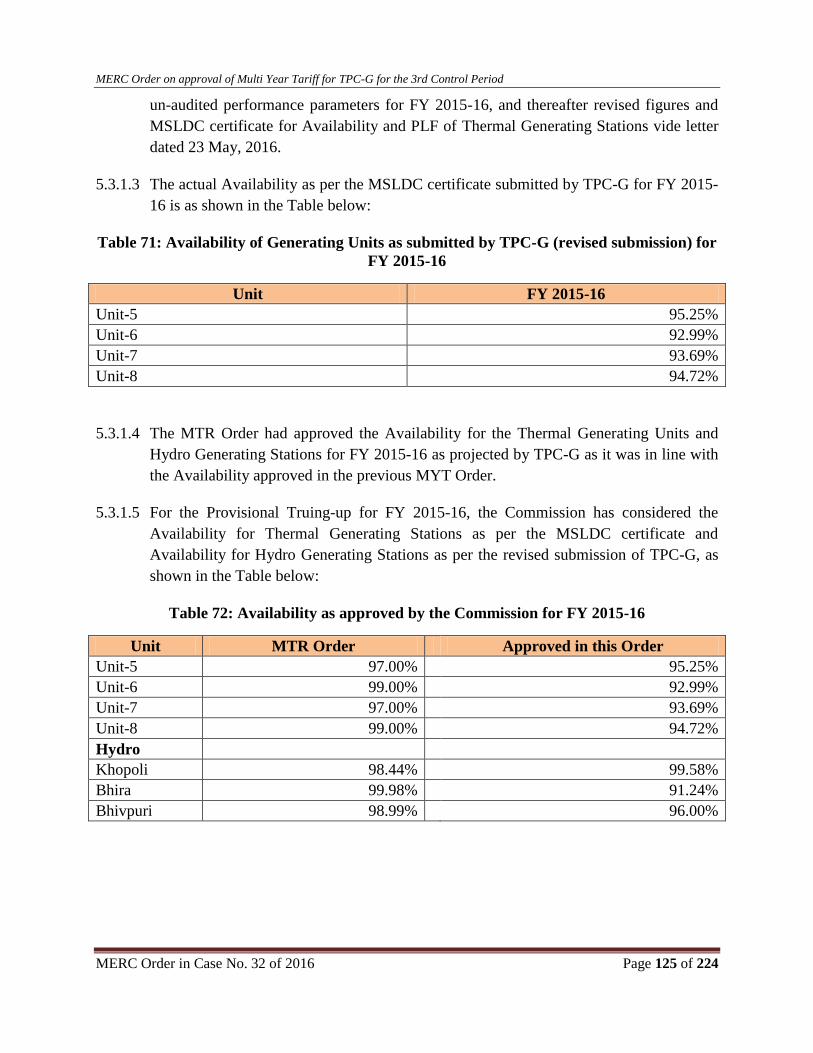

5.3.1 Availability ....................................................................................................................... 124

5.3.2 Gross Generation............................................................................................................... 126

5.3.3 Auxiliary Energy Consumption ........................................................................................ 128

5.3.4 Gross Station Heat Rate .................................................................................................... 130

5.3.5 Design Energy for Hydro Generating Stations ................................................................. 132

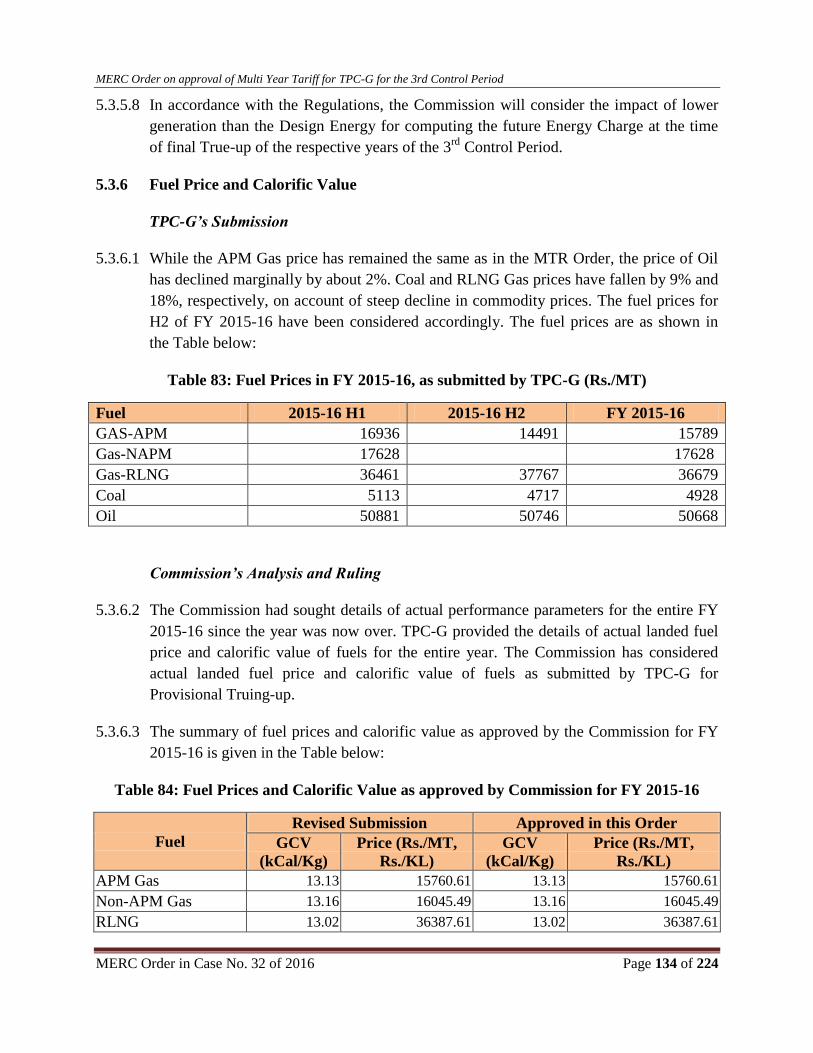

5.3.6 Fuel Price and Calorific Value .......................................................................................... 134

5.3.7 Fuel Cost ........................................................................................................................... 135

5.3.8 Fuel Cost of Unit-6 operating under MSLDC Directions ................................................. 135

5.3.9 Entry Tax .......................................................................................................................... 136

5.3.10 Operation and Maintenance Expenses .............................................................................. 136

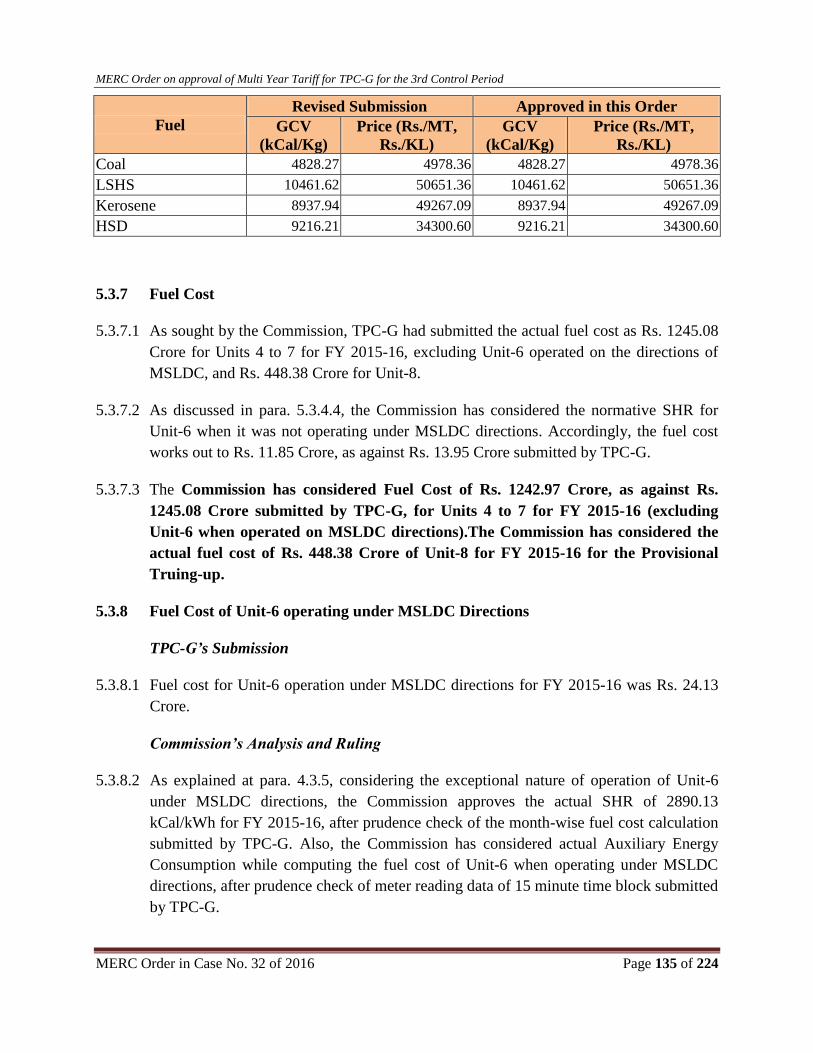

5.3.11 Capital Expenditure and Capitalisation ............................................................................. 137

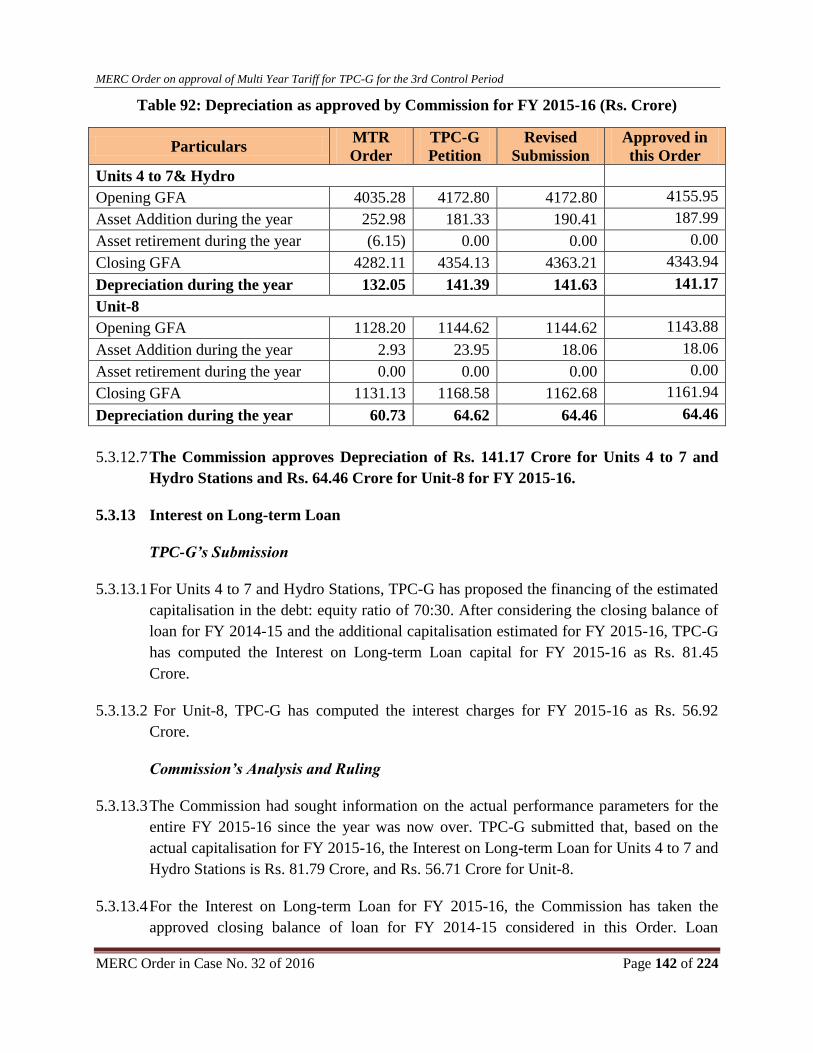

5.3.12 Depreciation ...................................................................................................................... 141

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 5 of 224

5.3.13 Interest on Long-term Loan .............................................................................................. 142

5.3.14 Return on Equity ............................................................................................................... 144

5.3.15 Interest on Working Capital .............................................................................................. 145

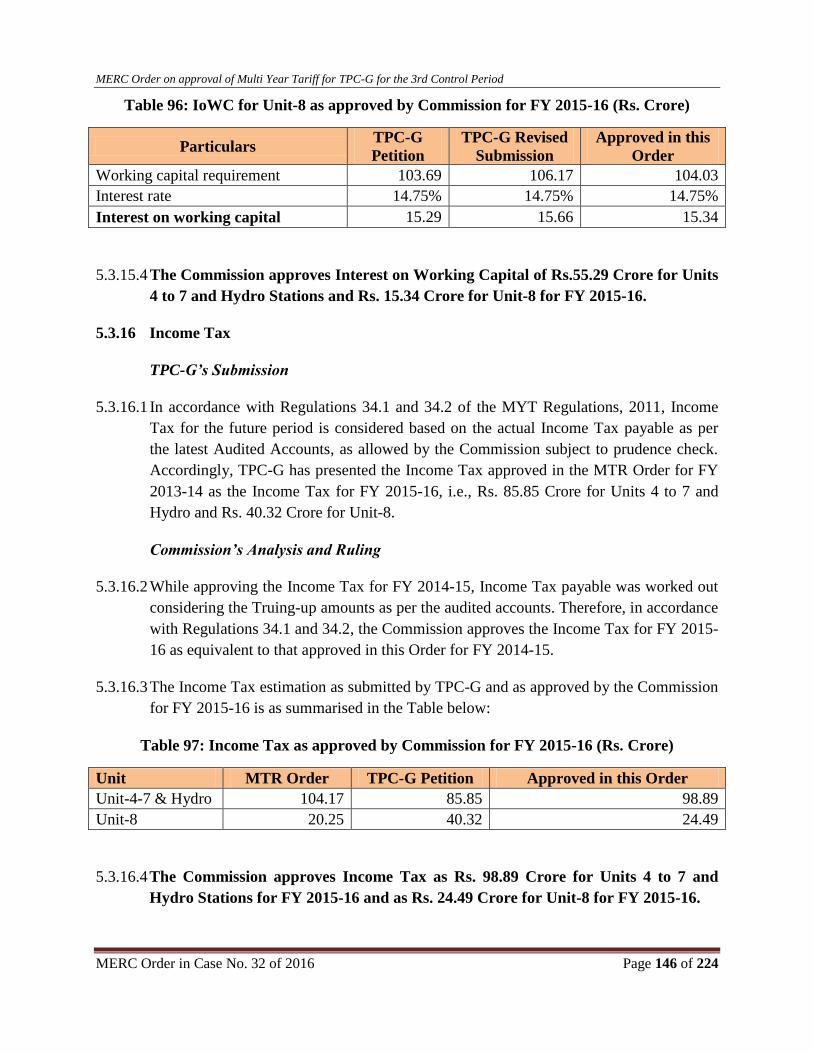

5.3.16 Income Tax ....................................................................................................................... 146

5.3.17 Non-Tariff Income ............................................................................................................ 147

5.3.18 PLF Incentive for Thermal Station ................................................................................... 147

5.3.19 Provisional Truing-up for FY 2015-16 ............................................................................. 148

5.4 Past Recoveries from Distribution Licensees ....................................................................... 149

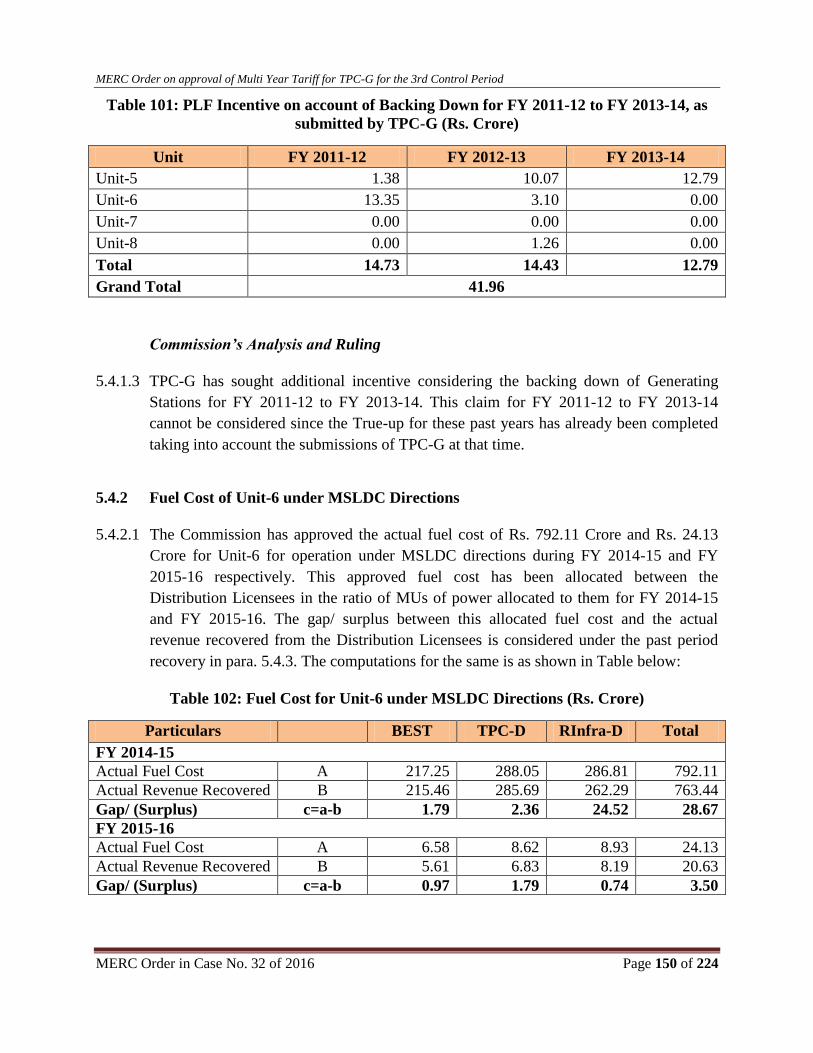

5.4.1 Incentive for backing down instructions from MSLDC for FY 2011-12 to FY 2013-14 . 149

5.4.2 Fuel Cost of Unit-6 under MSLDC Directions ................................................................. 150

5.4.3 Other Past Recoveries from Distribution Licensees ......................................................... 151

6. ARR FOR 3RD CONTROL PERIOD FROM FY 2016-17 TO FY 2019-20 .................................. 158

6.1 Background ............................................................................................................................... 158

6.2 Performance Parameters ........................................................................................................... 158

6.3 Generating Stations ................................................................................................................... 158

6.4 Performance Parameters ........................................................................................................... 159

6.4.1 Availability ....................................................................................................................... 159

6.4.2 Gross Generation............................................................................................................... 160

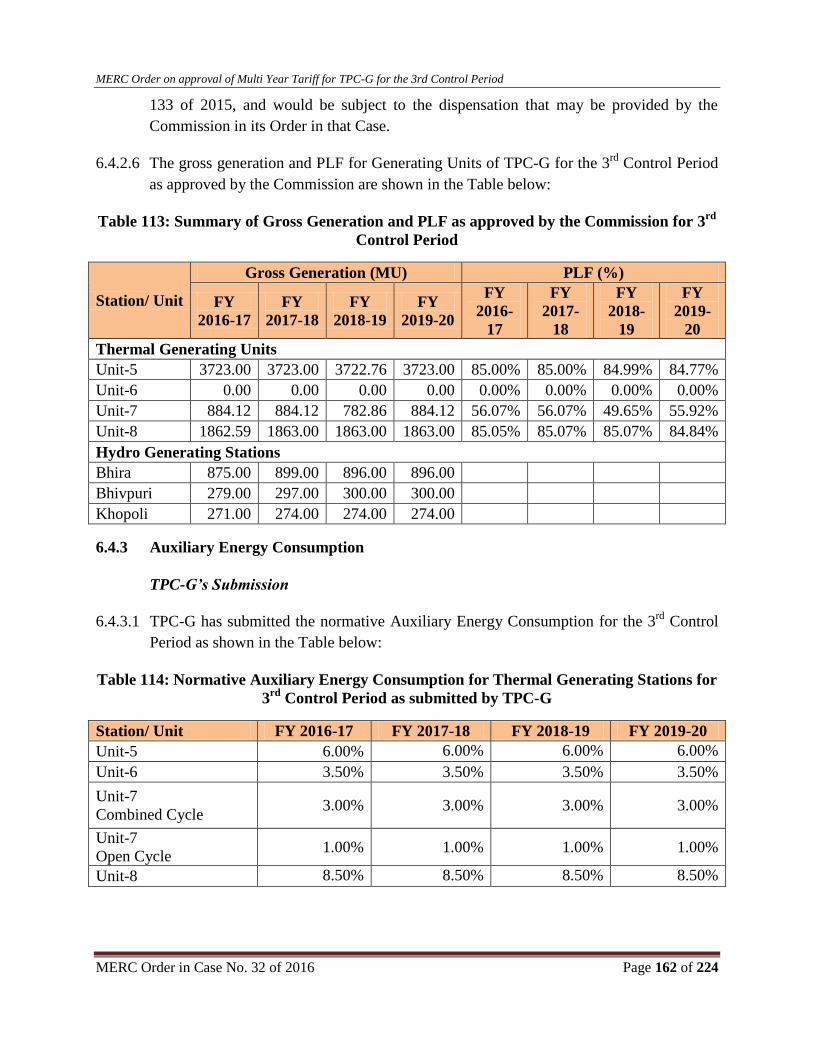

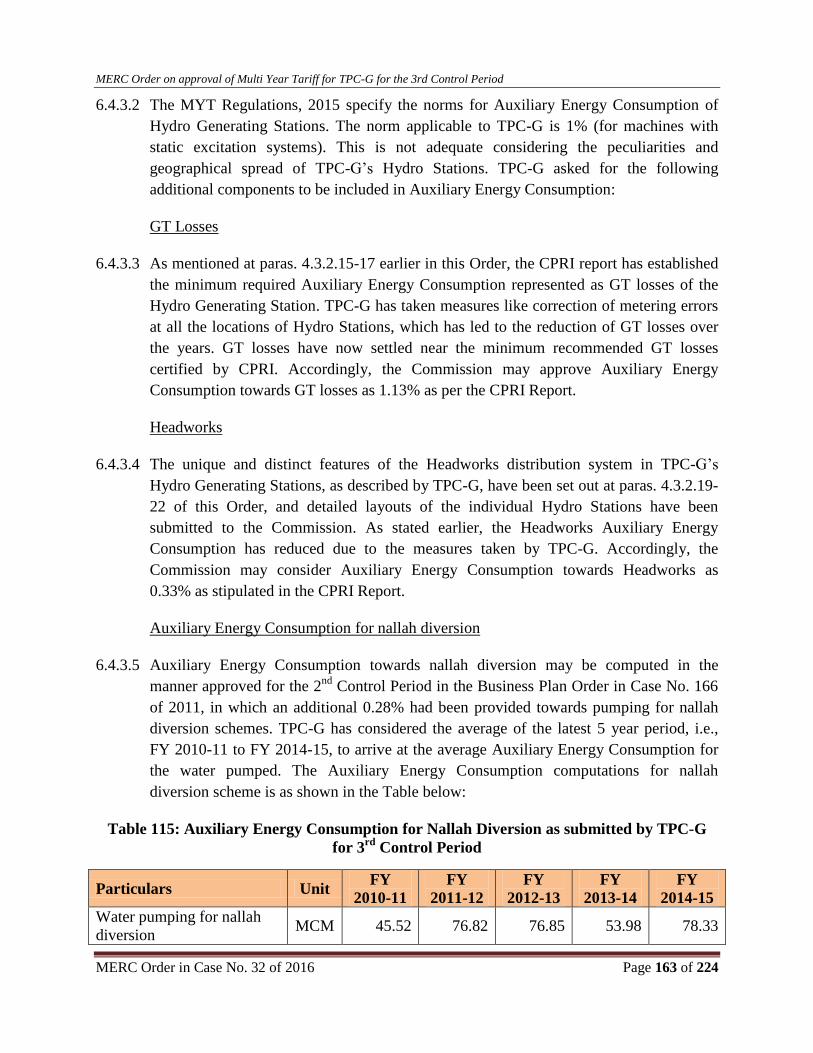

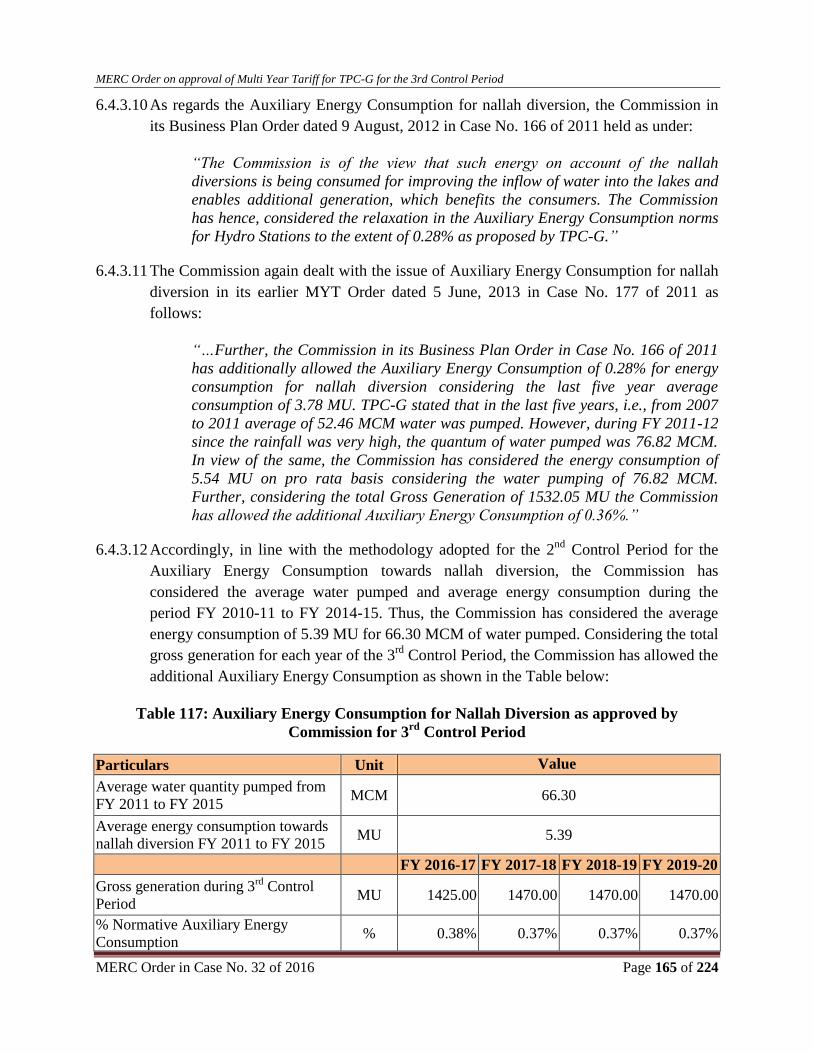

6.4.3 Auxiliary Energy Consumption ........................................................................................ 162

6.4.4 Gross Station Heat Rate .................................................................................................... 166

6.4.5 Fuel Cost ........................................................................................................................... 168

6.4.6 Operation and Maintenance Expenses .............................................................................. 172

6.4.7 Capital Expenditure and Capitalisation ............................................................................. 176

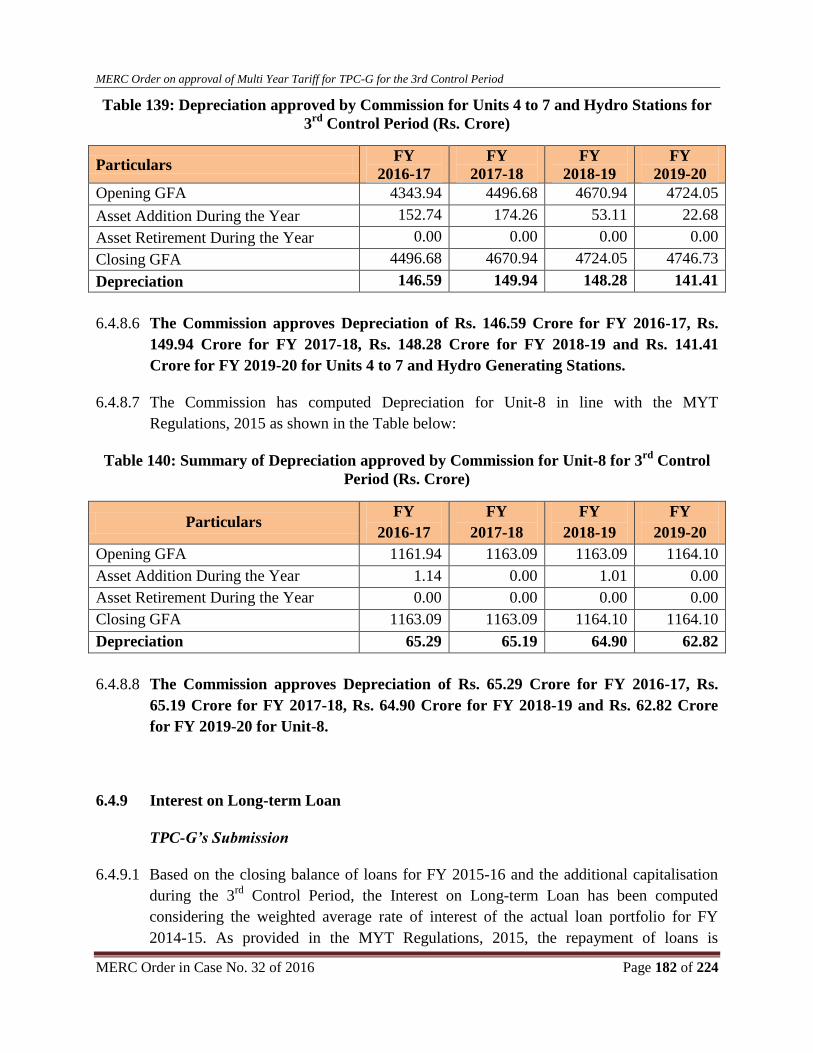

6.4.8 Depreciation ...................................................................................................................... 180

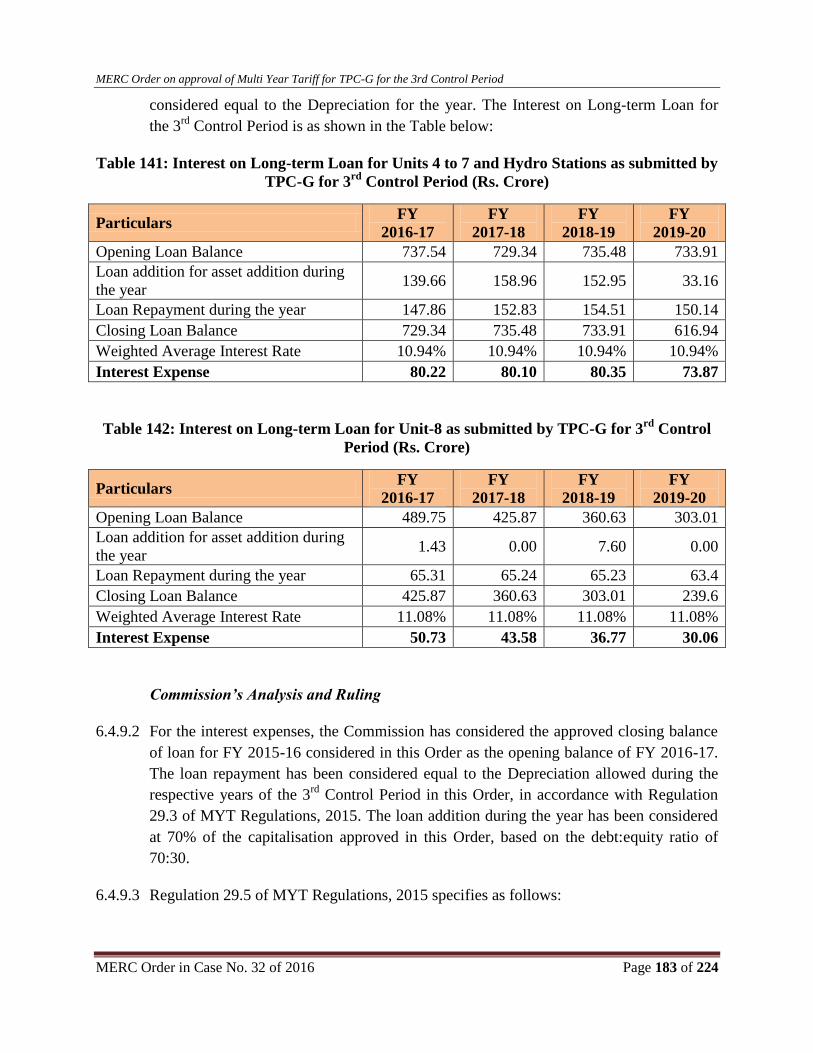

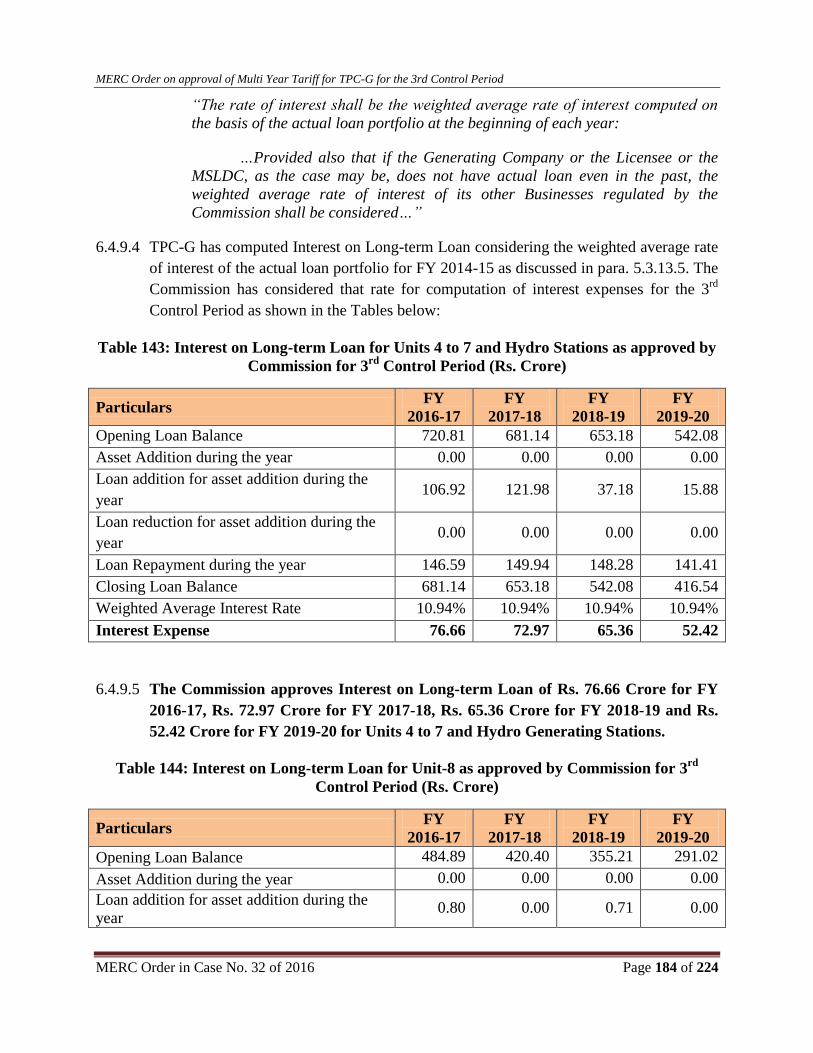

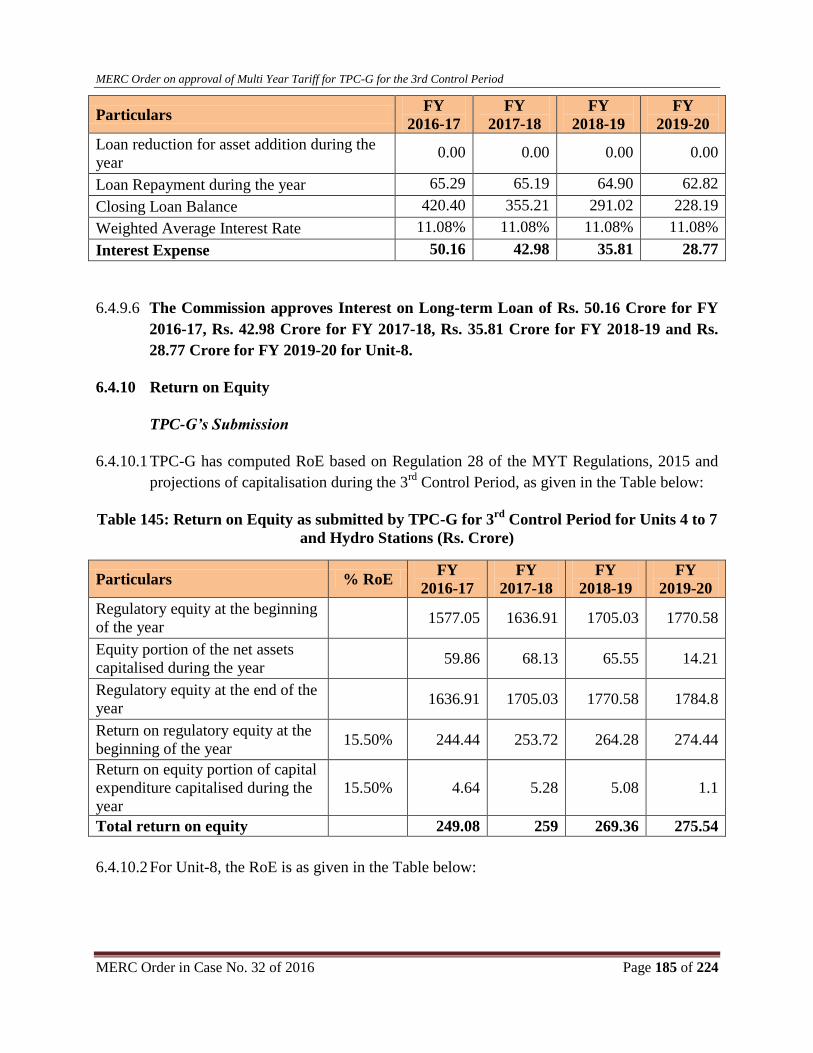

6.4.9 Interest on Long-term Loan .............................................................................................. 182

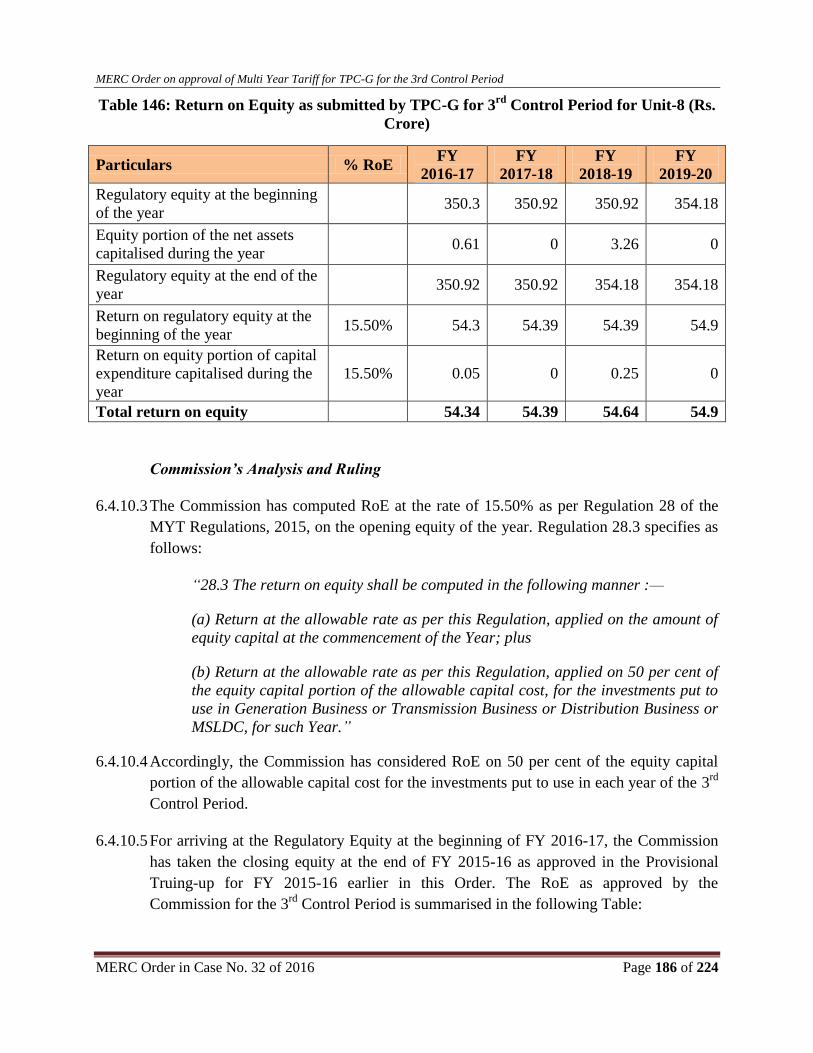

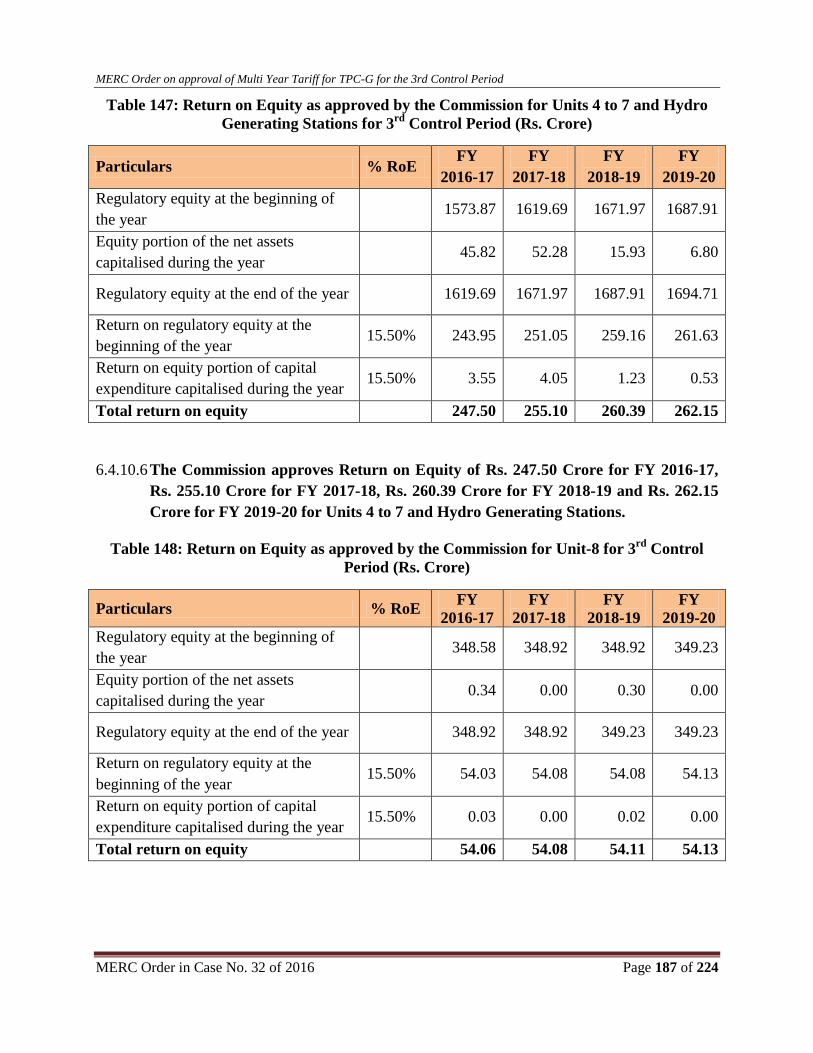

6.4.10 Return on Equity ............................................................................................................... 185

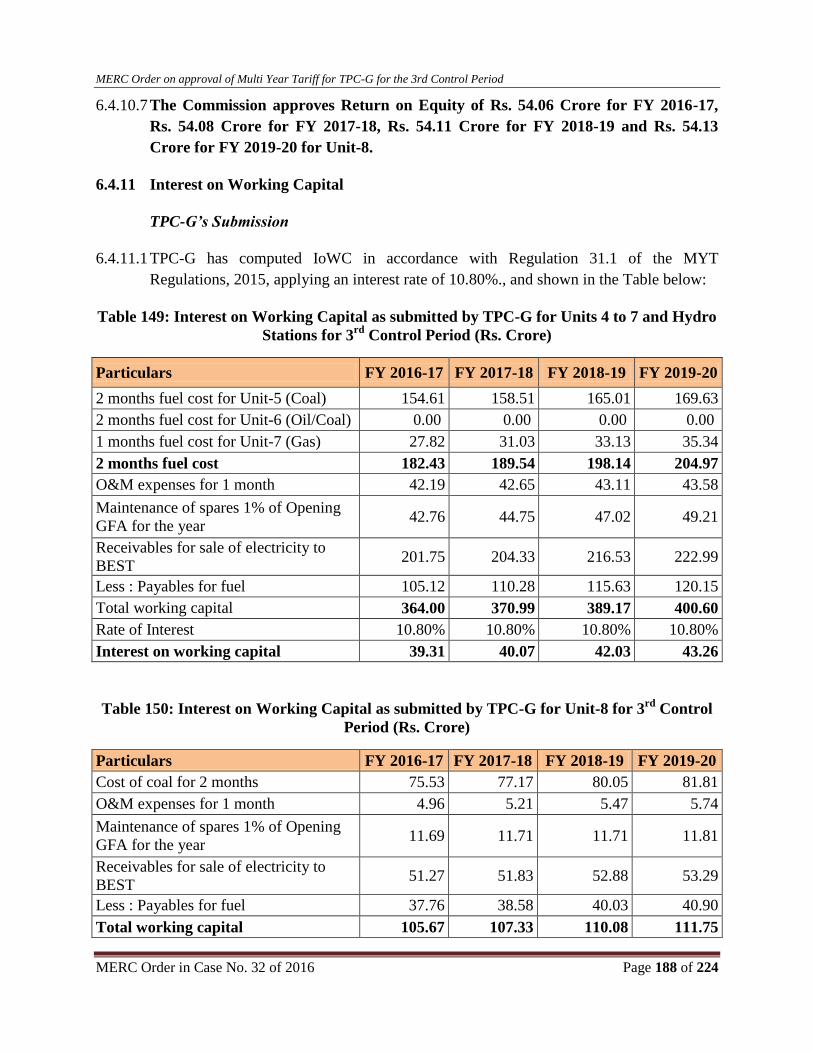

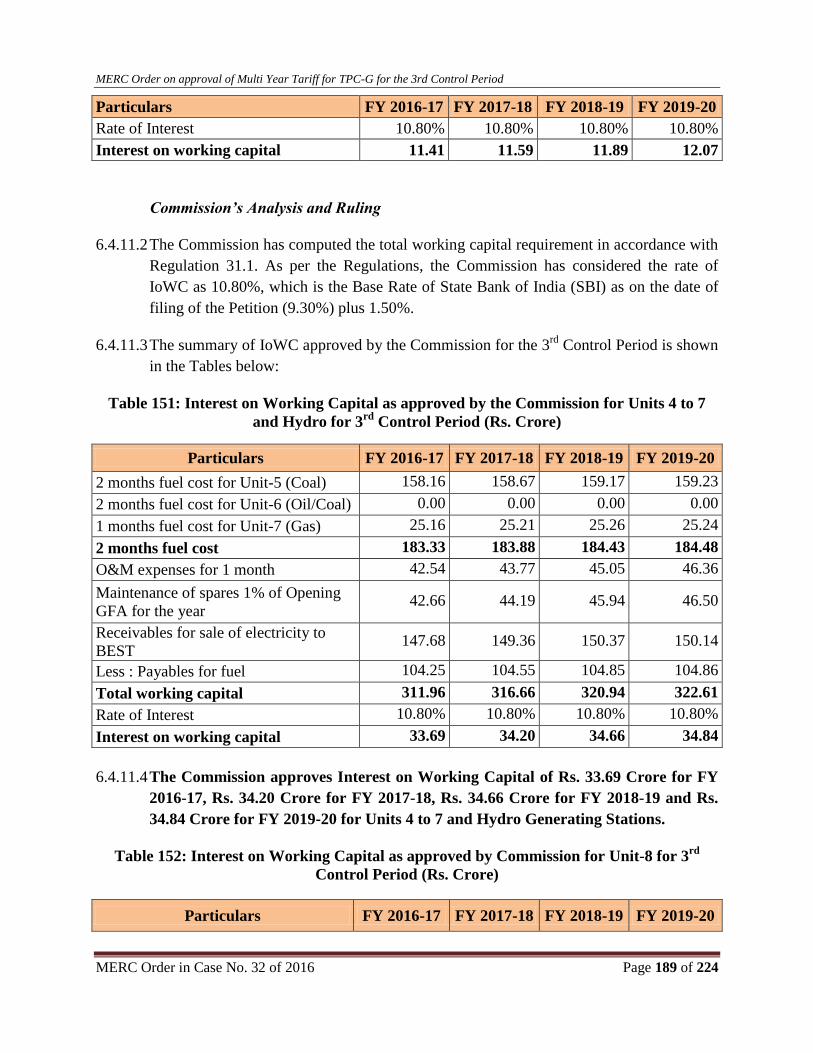

6.4.11 Interest on Working Capital .............................................................................................. 188

6.4.12 Income Tax ....................................................................................................................... 190

6.4.13 Non-Tariff Income ............................................................................................................ 191

6.4.14 Fixed Cost of Unit-4 ......................................................................................................... 193

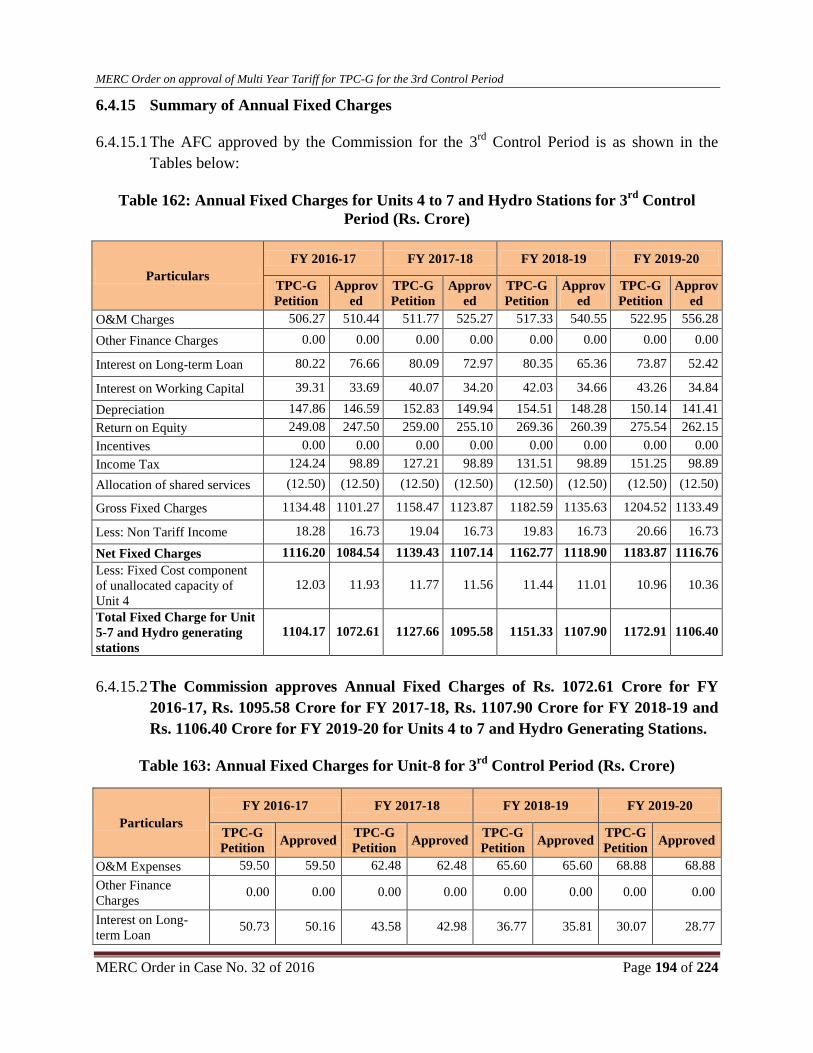

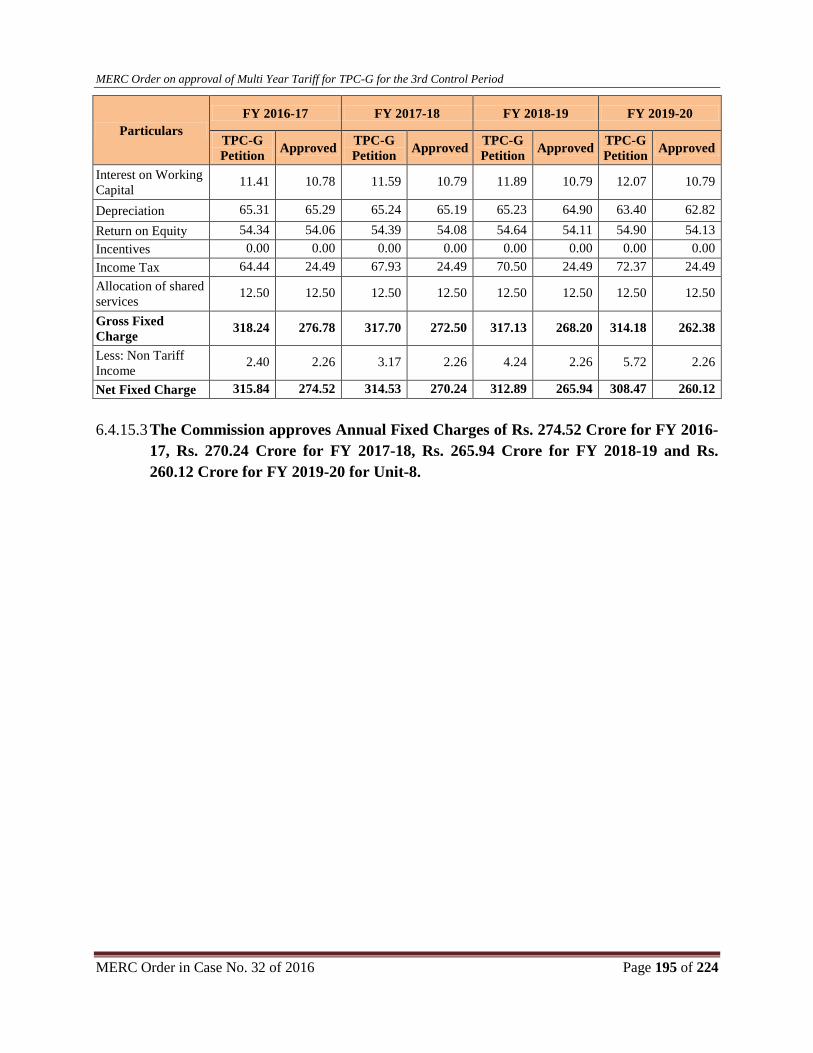

6.4.15 Summary of Annual Fixed Charges .................................................................................. 194

7. MULTI-YEAR TARIFF FOR 3RD CONTROL PERIOD FROM FY 2016-17 TO FY 2019-20 ... 196

7.1 AFC for TPC-G ......................................................................................................................... 196

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 6 of 224

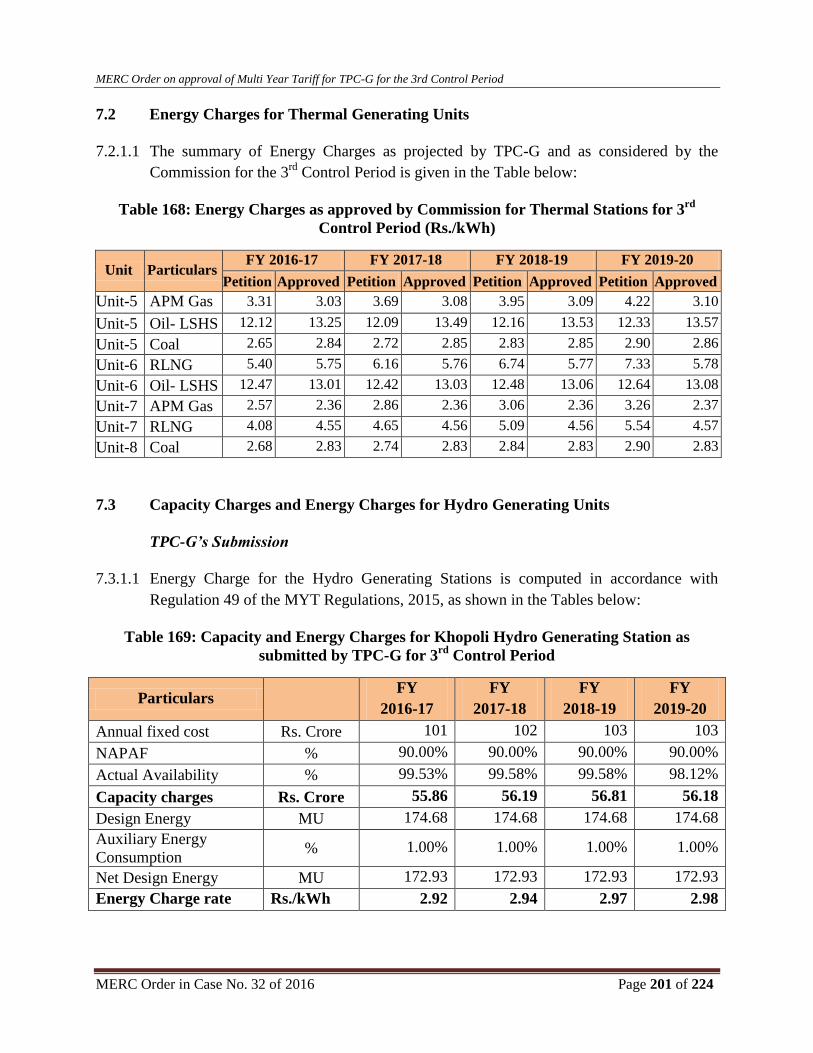

7.2 Energy Charges for Thermal Generating Units ........................................................................ 201

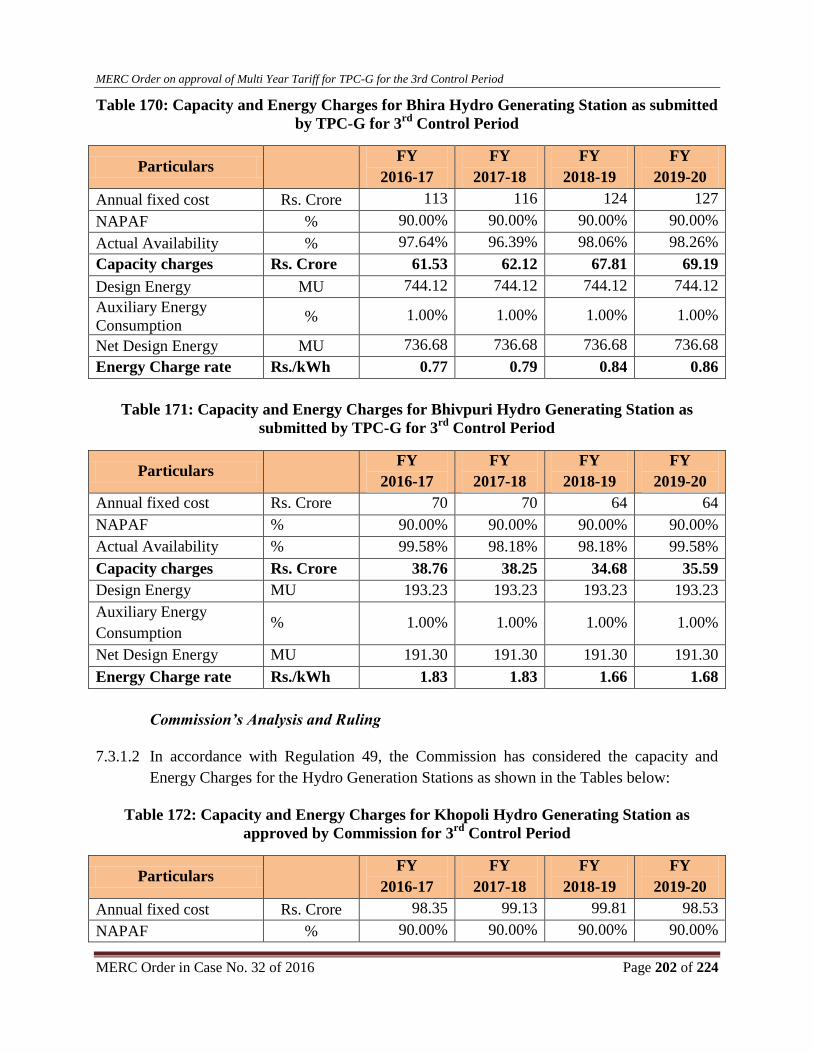

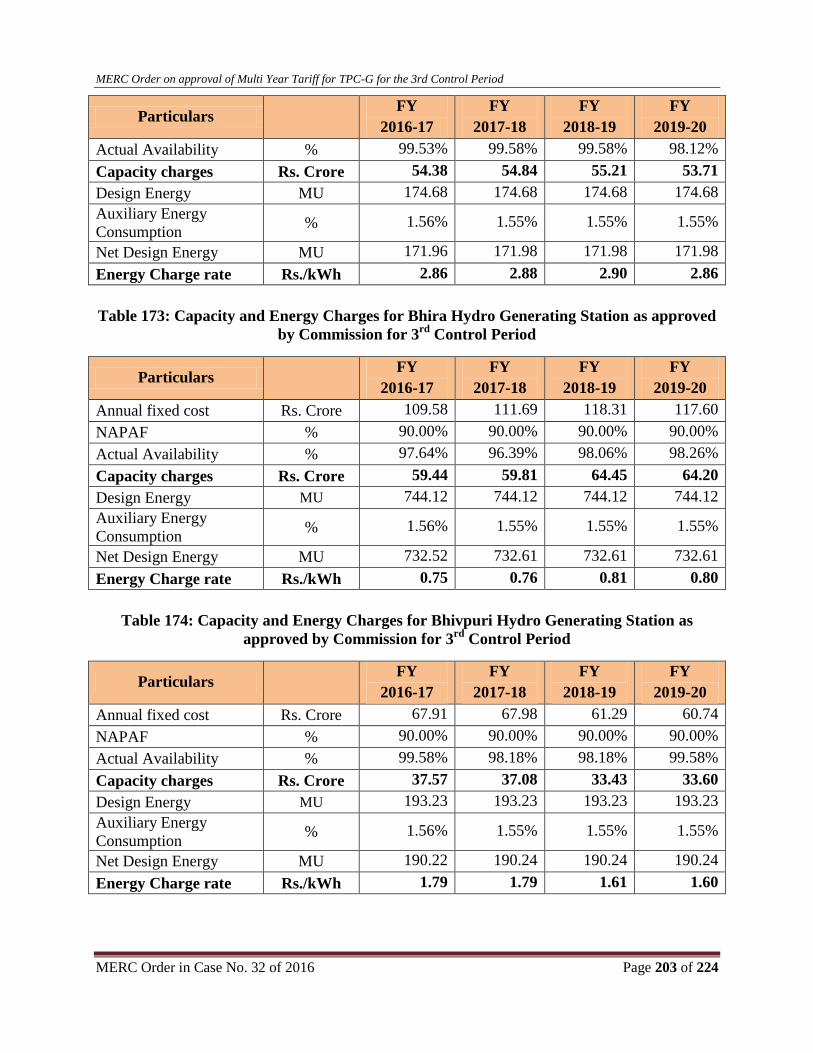

7.3 Capacity Charges and Energy Charges for Hydro Generating Units ........................................ 201

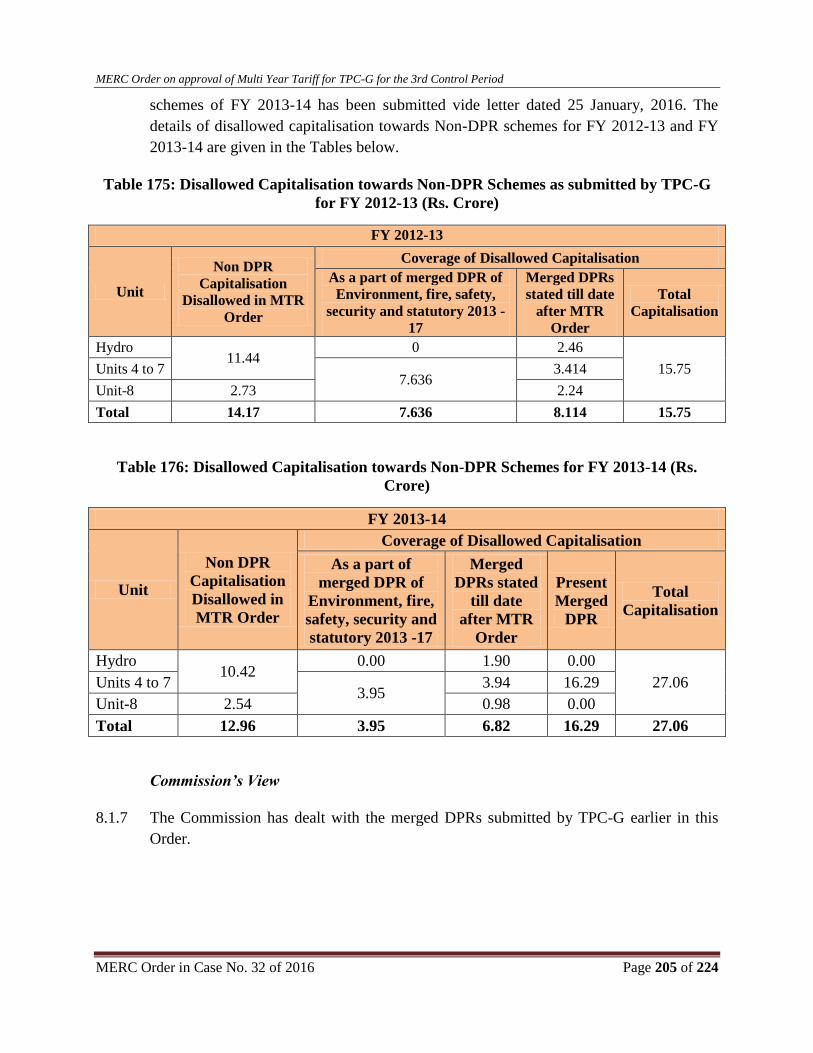

8. COMPLIANCE OF DIRECTIVES IN MTR ORDER ..................................................................... 204

8.1 Non-DPR Capitalisation ........................................................................................................... 204

8.2 Section 80 IA of Income Tax Act ............................................................................................. 206

8.3 BHEL Circular .......................................................................................................................... 206

8.4 Replacement of Blades.............................................................................................................. 207

8.5 Operating Conditions ................................................................................................................ 209

9. SUMMARY OF THE RULINGS ..................................................................................................... 212

9.1 Carrying Cost on impact of ATE Judgment .............................................................................. 212

9.2 True-up For FY 2014-15 ........................................................................................................... 212

9.2.1 Performance of Unit-8 ...................................................................................................... 213

9.3 Provisional True-up for FY 2015-16 ........................................................................................ 215

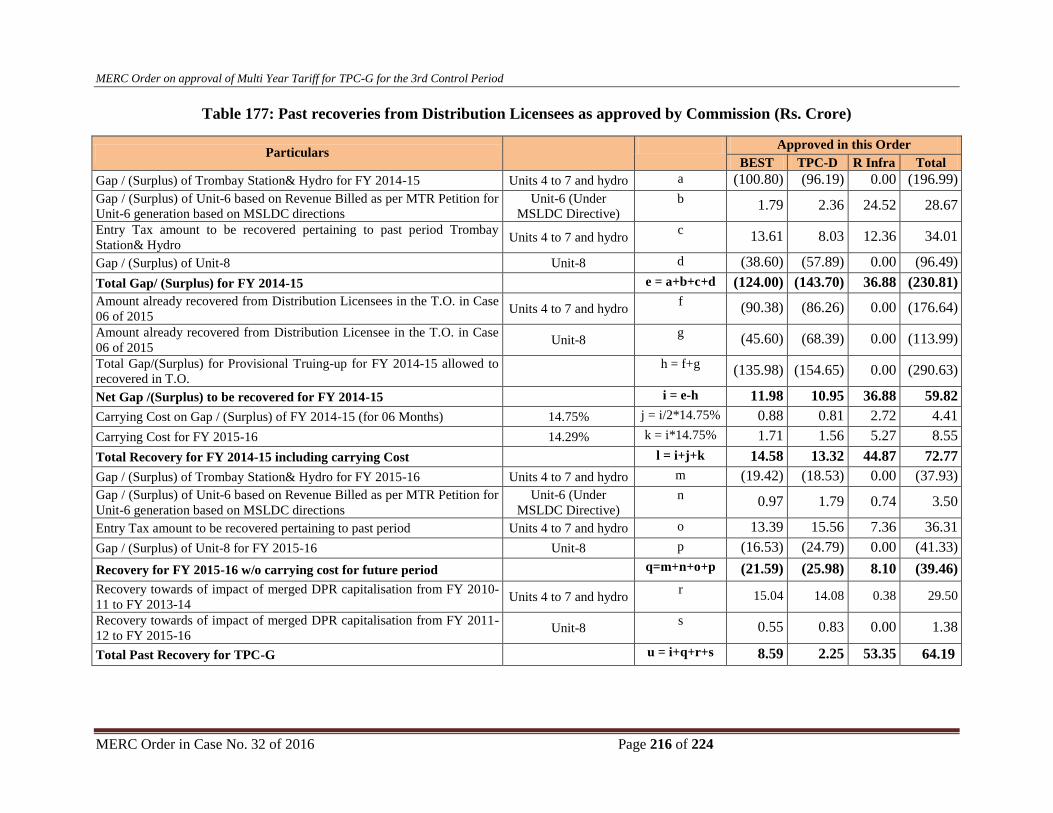

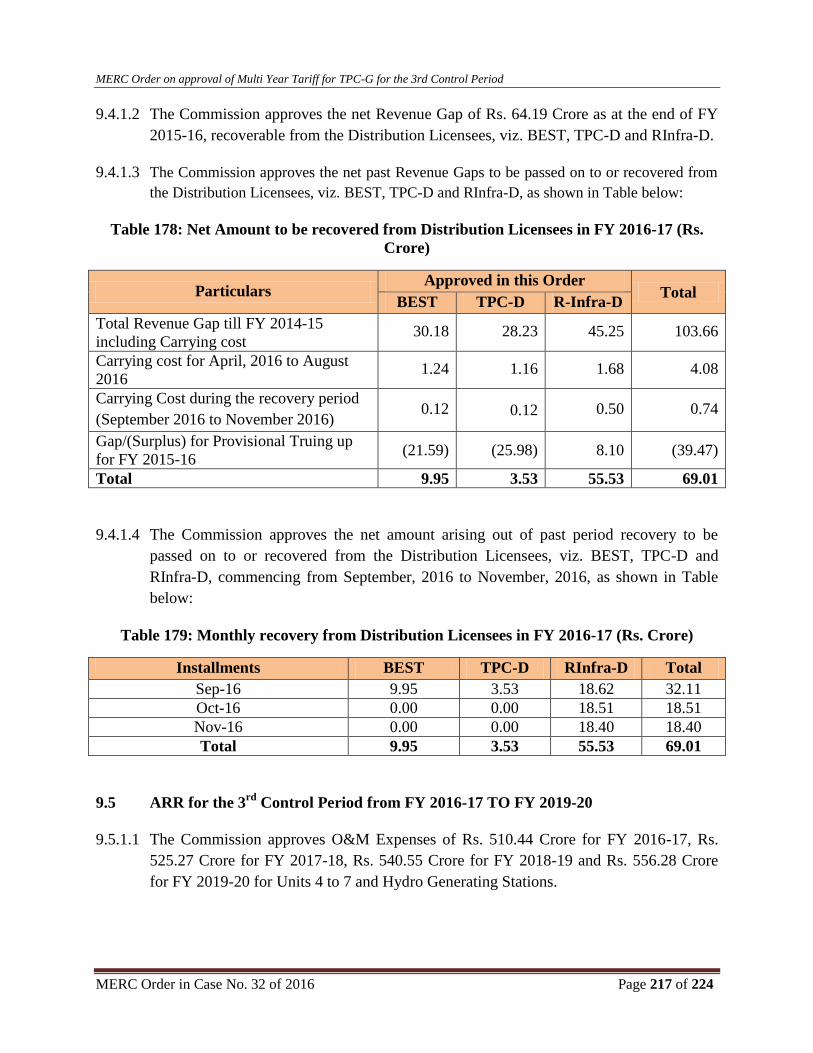

9.4 Past Recoveries from Distribution Licensees ........................................................................... 215

9.5 ARR for the 3RD

Control Period from FY 2016-17 TO FY 2019-20 ........................................ 217

10. DIRECTIVES ................................................................................................................................... 220

10.1 Imported Coal Purchase ............................................................................................................ 220

10.2 Expiry of PPA ........................................................................................................................... 220

11. APPLICABILITY OF ORDER ........................................................................................................ 221

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 7 of 224

LIST OF TABLES

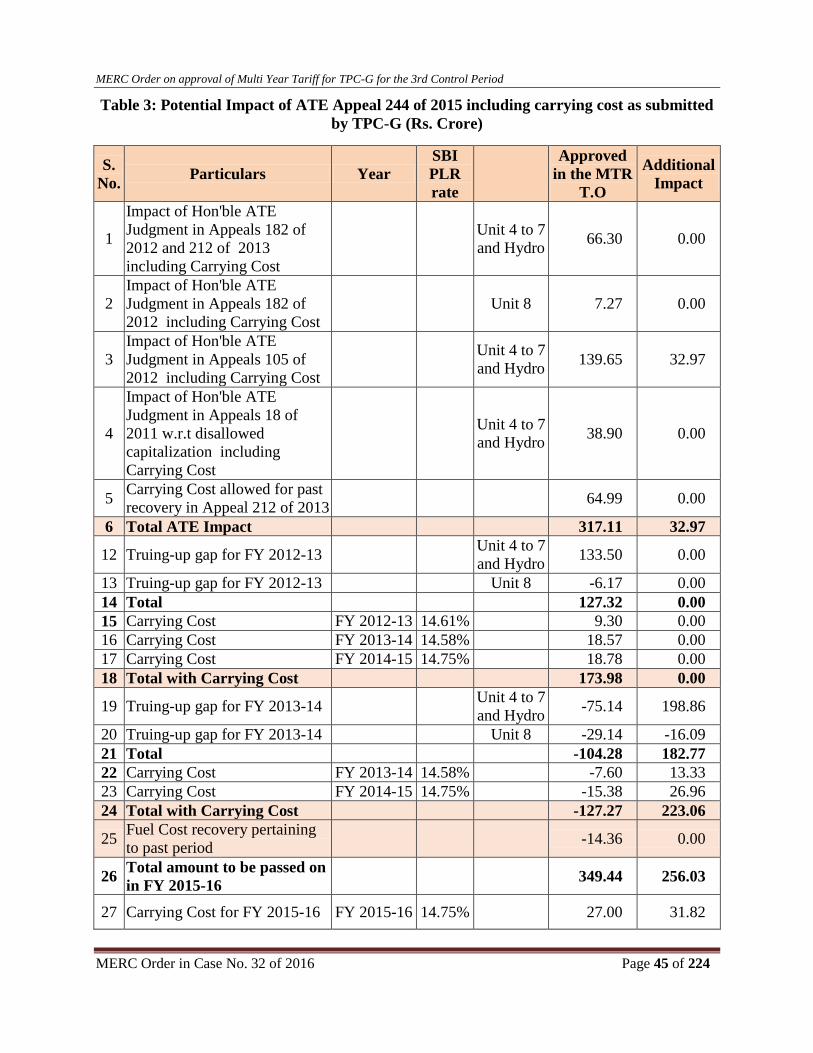

Table 1: Potential Impact of ATE Appeal 244 of 2015 as submitted by TPC-G ........................................ 42

Table 2: Potential Impact of ATE Appeal 244 of 2015 as submitted by TPC-G ....................................... 43

Table 3: Potential Impact of ATE Appeal 244 of 2015 including carrying cost as submitted by TPC-G . 45

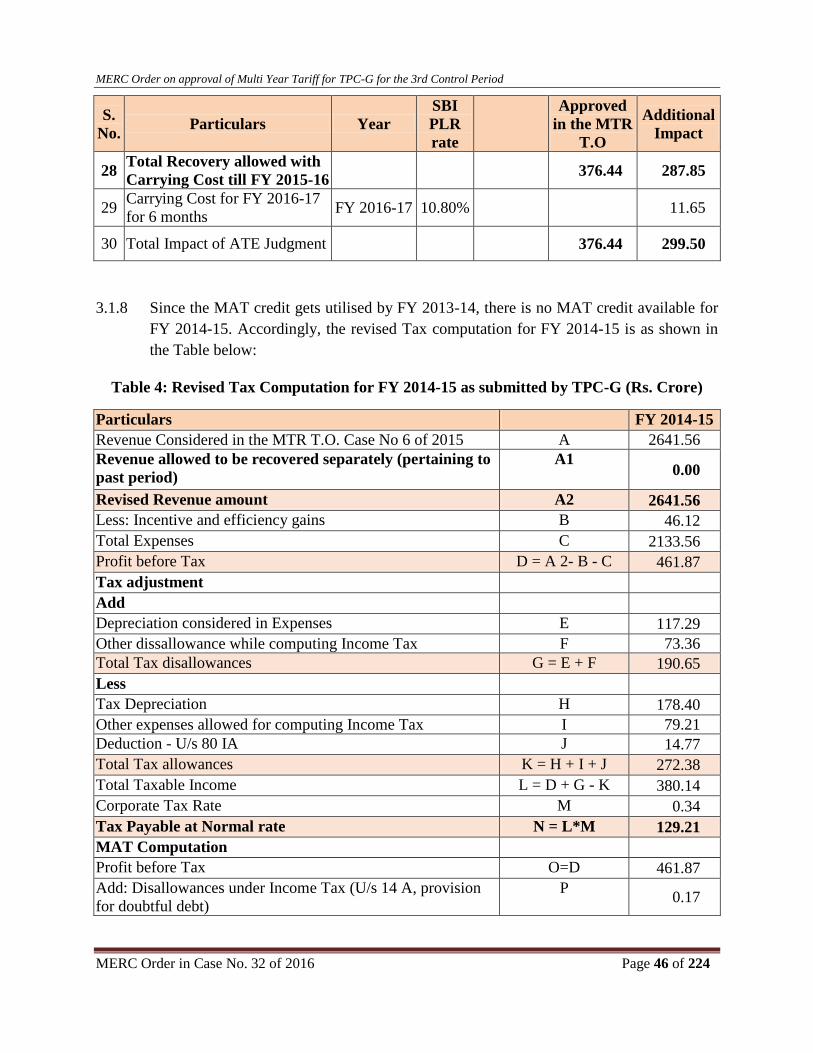

Table 4: Revised Tax Computation for FY 20-14-15 as submitted by TPC-G .......................................... 46

Table 5: Gross Generation and Availability certified by MSLDC for FY 2014-15 ................................... 50

Table 6: Summary of Availability for Units 4 to 7 and Hydro Stations for FY 2014-15 as approved by

Commission ................................................................................................................................................ 51

Table 7: Summary of Gross Generation for Units 4 to 7 and Hydro Stations for FY 2014-15 as approved

by Commission ........................................................................................................................................... 51

Table 8: Auxiliary Energy Consumption for FY 2014-15 as submitted by TPC-G ................................... 52

Table 9: Unit-4Auxiliary Energy Consumption for FY 2014-15 as submitted by TPC-G ......................... 52

Table 10: Auxiliary Energy Consumption of Hydro Stations for FY 2014-15 as submitted by TPC-G .... 54

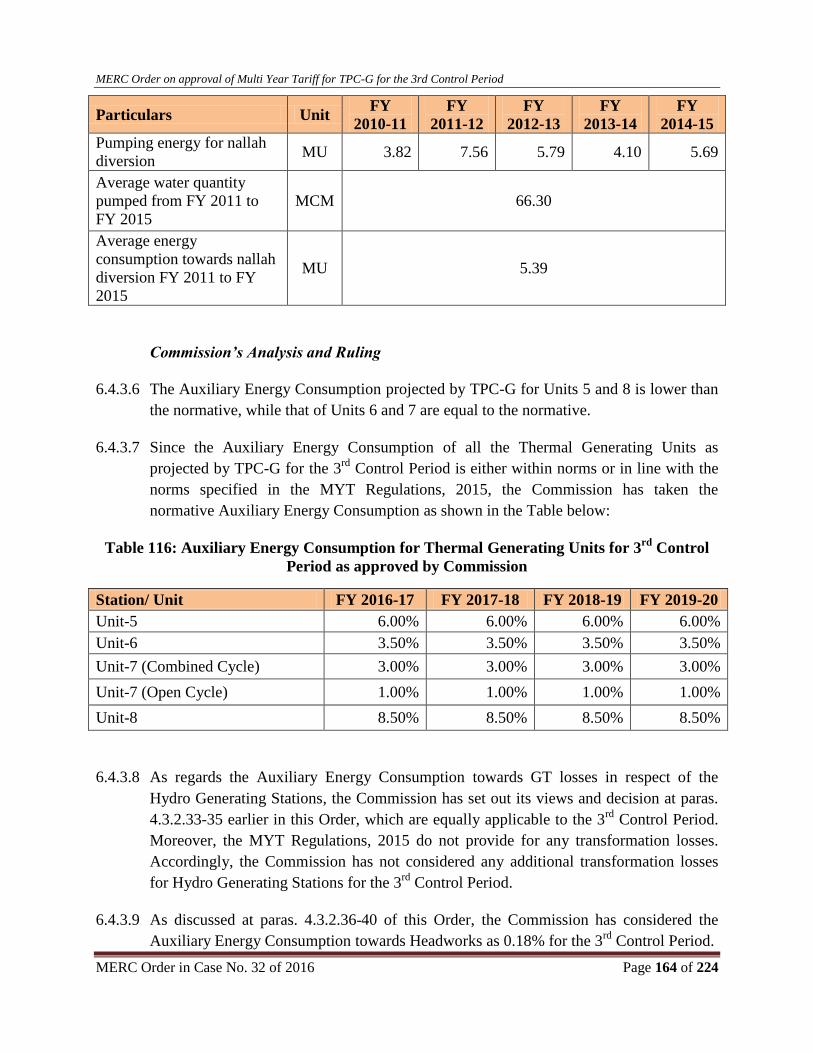

Table 11: Auxiliary Energy Consumption for nallah diversion as submitted by TPC-G for FY 2014-15 . 54

Table 12: Actual GT Losses for FY 2014-15 as submitted by TPC-G ....................................................... 55

Table 13: Headworks consumption as submitted by TPC-G ...................................................................... 56

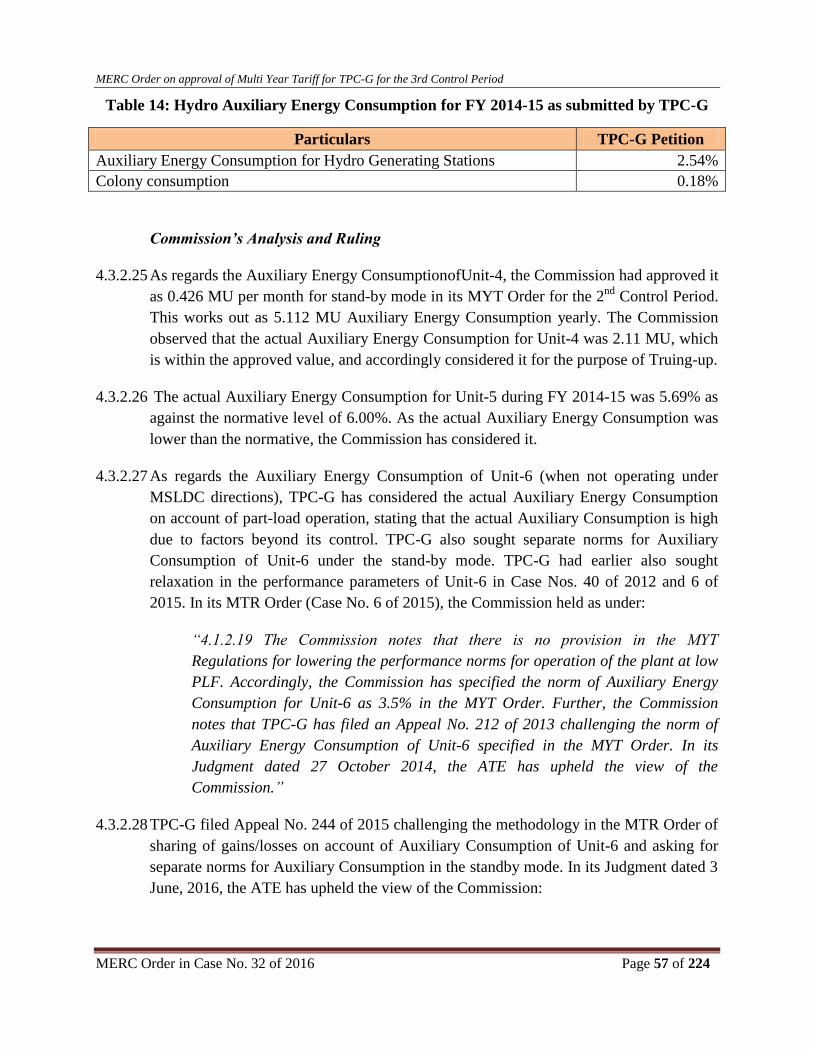

Table 14: Hydro Auxiliary Energy Consumption for FY 2014-15 as submitted by TPC-G ...................... 57

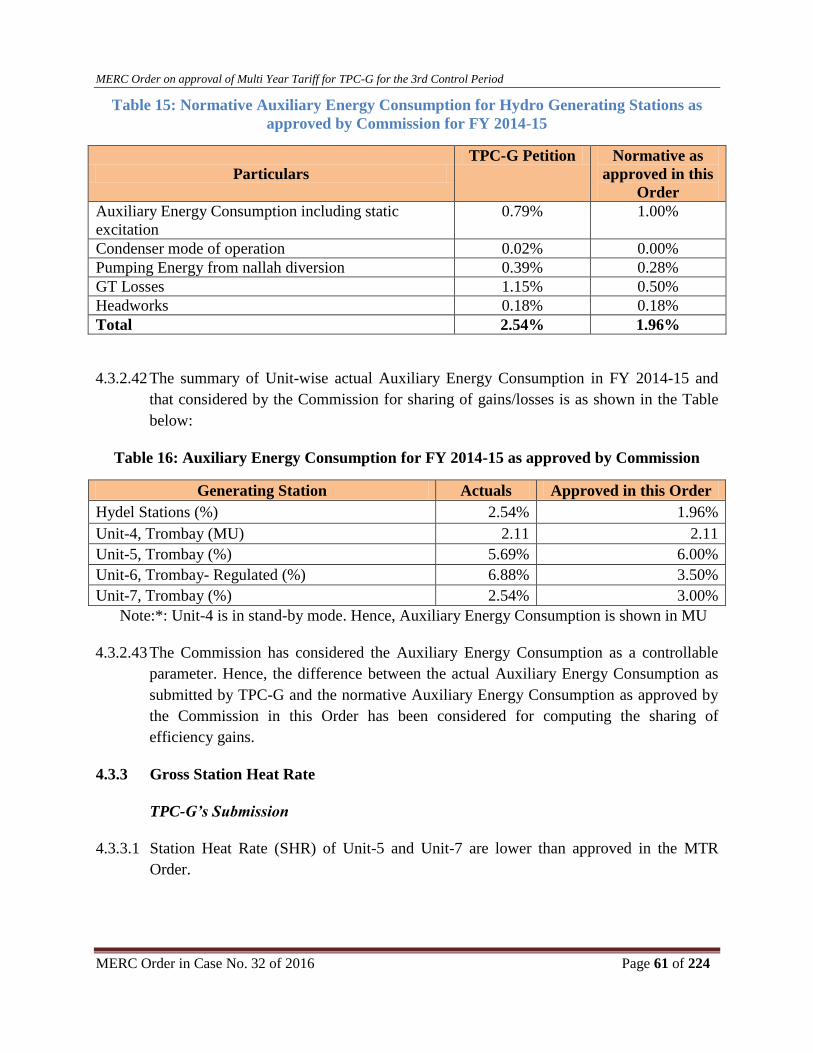

Table 15: Normative Auxiliary Energy Consumption for Hydro Generating Stations as approved by

Commission for FY 2014-15 ...................................................................................................................... 61

Table 16: Auxiliary Energy Consumption for FY 2014-15 as approved by Commission .......................... 61

Table 17: SHR for Unit-6 for FY 2014-15 as submitted by TPC-G ........................................................... 62

Table 18: Actual SHR for Unit-6 under different modes of operation, as submitted by TPC-G for FY

2014-15 ....................................................................................................................................................... 62

Table 19: Unit-wise SHR for 2014-15 approved by Commission .............................................................. 63

Table 20: Break-up of Fuel Cost, as submitted by TPC-G for FY 2014-15 ............................................... 63

Table 21: Fuel Parameters as approved by Commission for FY 2014-15 .................................................. 64

Table 22: Fuel Cost Reconciliation as submitted by TPC-G for FY 2014-15 ........................................... 65

Table 23: Fuel Cost for Units 4 to 7 for FY 2014-15 as approved by Commission .................................. 65

Table 24: Impact of Entry Tax as submitted by TPC-G for FY 2014-15 ................................................... 68

Table 25: Recovery of Entry Tax, as approved by Commission ................................................................ 68

Table 26: Employee Expenses for Trombay Units 4-7 &Hydro Stations for FY 2014-15 ........................ 69

Table 27: Summary of O&M Expenses for FY 2014-15 as approved by Commission ............................. 72

Table 28: Non-DPR Schemes not considered for Capitalisation ............................................................... 74

Table 29: Capitalisation approved by Commission for FY 2014-15 ......................................................... 75

Table 30: Summary of Merged DPRs, as submitted by TPC-G ................................................................ 76

Table 31: Summary of Merged Non-DPR Capitalisation now approved by Commission for Units 4 to 7

and Hydro Generating Stations .................................................................................................................. 78

Table 32: Non-DPR Capitalisation for Units 4 to 7 and Hydro Generating Stations as approved by

Commission for FY 2010-11 to FY 2013-14 ............................................................................................. 78

Table 33: Depreciation as approved by Commission for FY 2014-15 ...................................................... 80

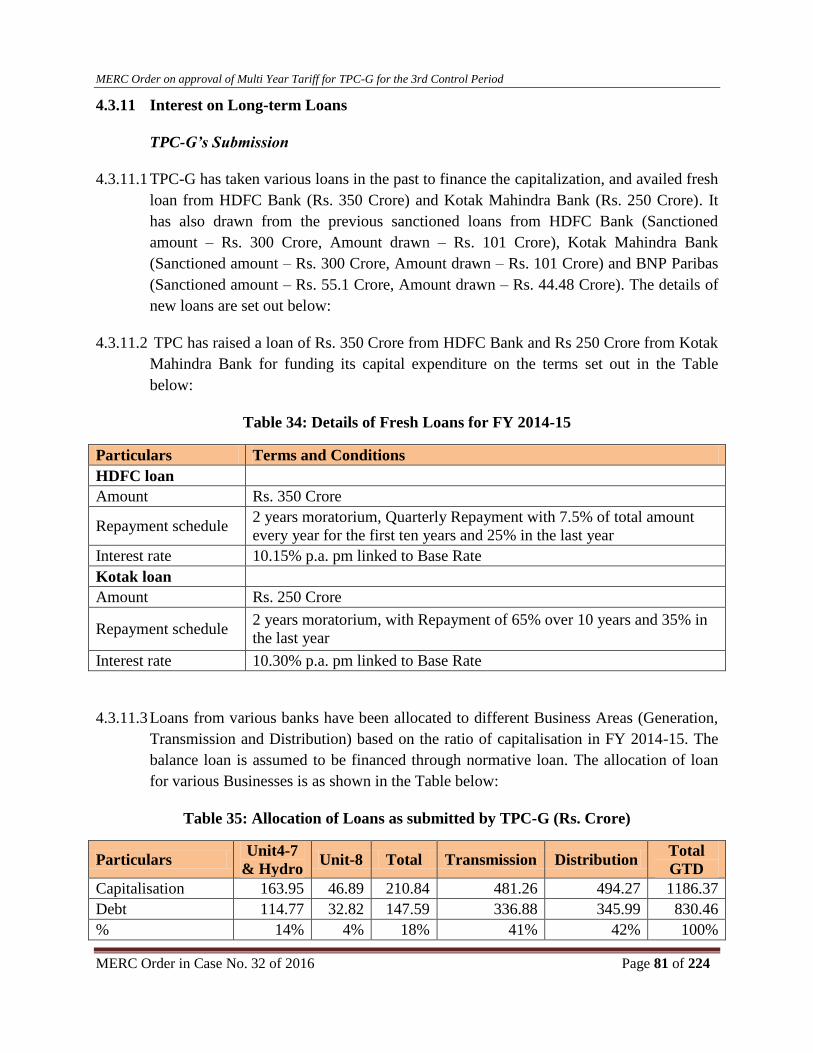

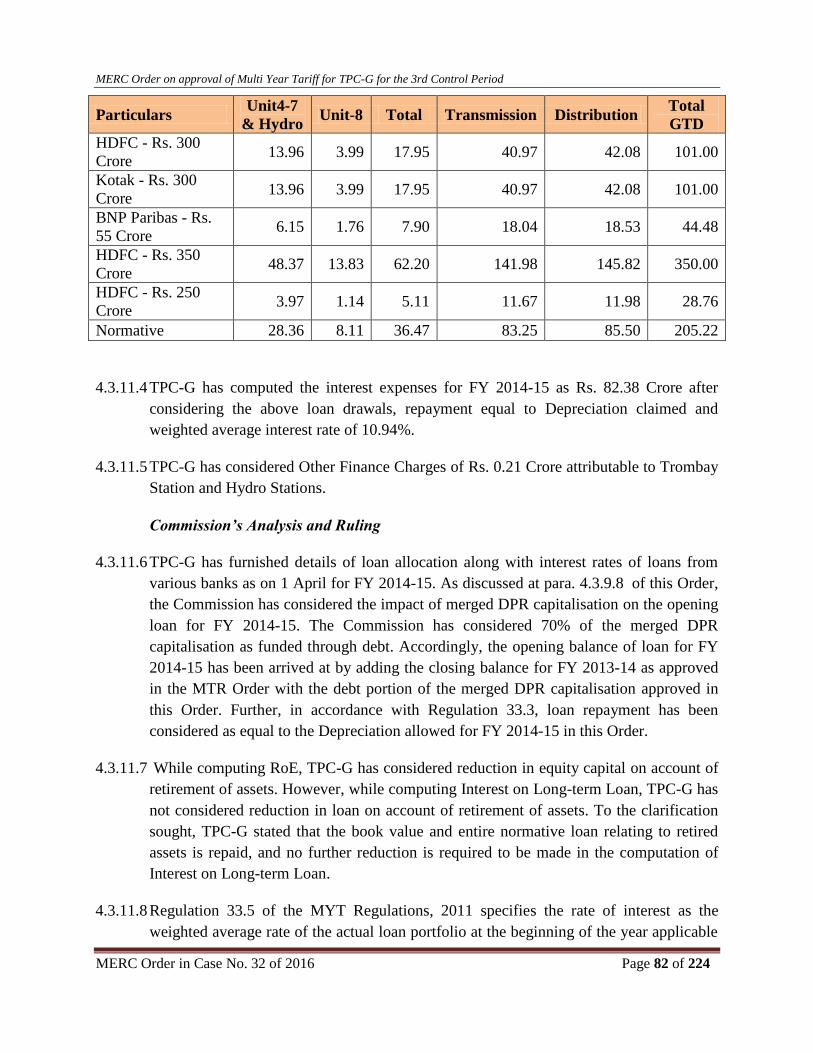

Table 34: Details of Fresh Loans for FY 2014-15 ...................................................................................... 81

Table 35: Allocation of Loans as submitted by TPC-G ............................................................................. 81

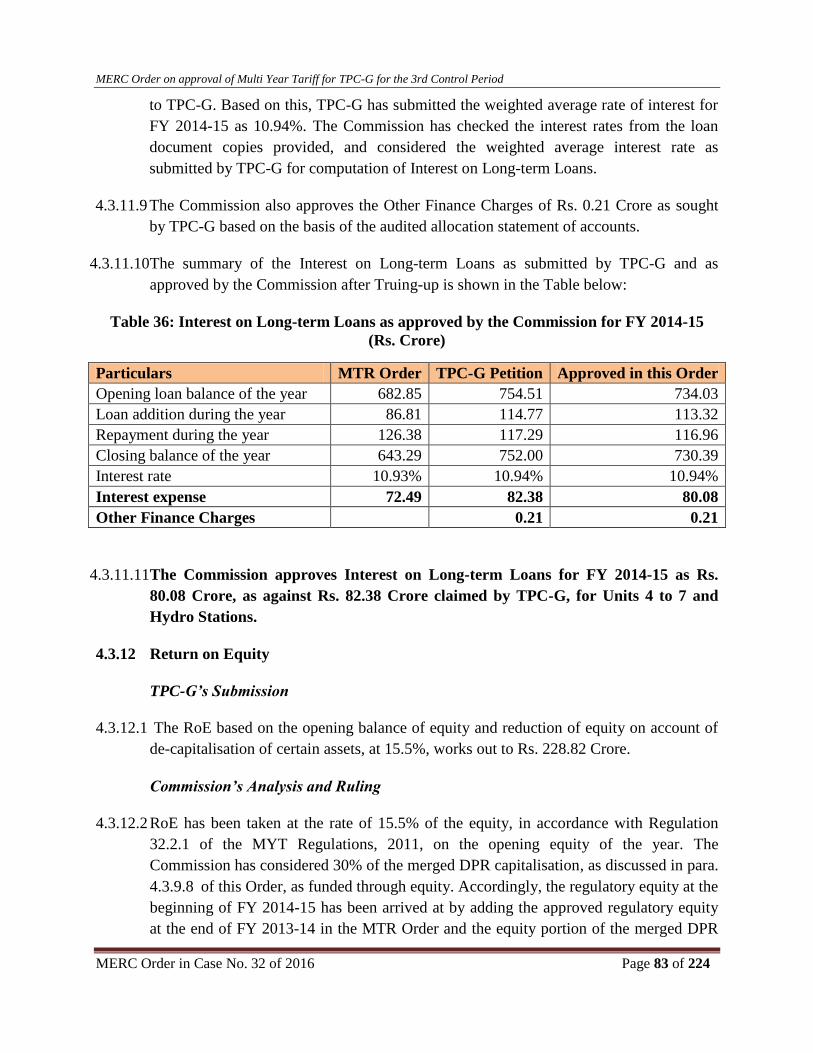

Table 36: Interest on Long-term Loans as approved by the Commission for FY 2014-15 ....................... 83

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 8 of 224

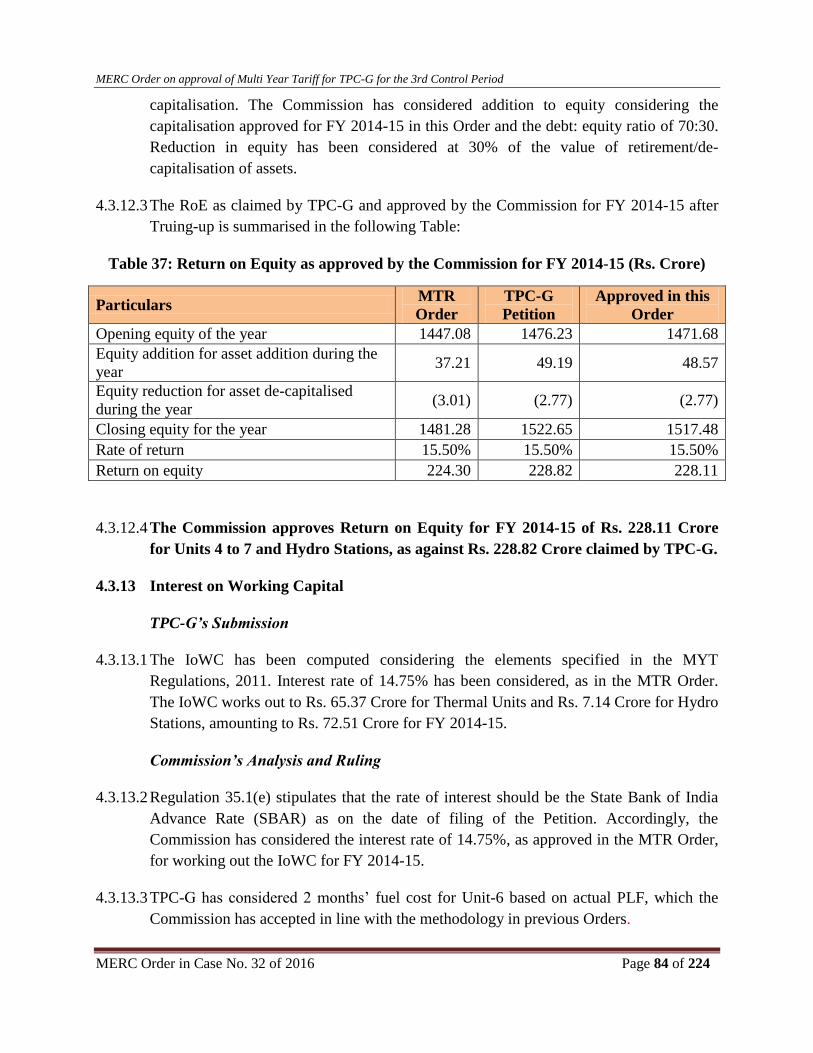

Table 37: Return on Equity as approved by the Commission for FY 2014-15 .......................................... 84

Table 38: Interest on Working Capital as approved by Commission for FY 2014-15 .............................. 85

Table 39: Income Tax as approved by Commission for FY 2014-15 ........................................................ 86

Table 40: Non-Tariff Income as approved by Commission for FY 2014-15 ............................................. 87

Table 41: Revenue from Sale of Power for FY 2014-15 ............................................................................ 87

Table 42: Approved Reduction in AFC for Unit-7 for FY 2014-15 ........................................................... 92

Table 43: Gains and Losses due to variation in Fuel Cost, as approved by Commission for FY 2014-15 94

Table 44: Gain/Loss due to variation in Auxiliary Energy Consumption as approved by Commission for

FY 2014-15 ................................................................................................................................................ 95

Table 45: Property Tax Summary as submitted by TPC-G for FY 2014-15 ............................................. 96

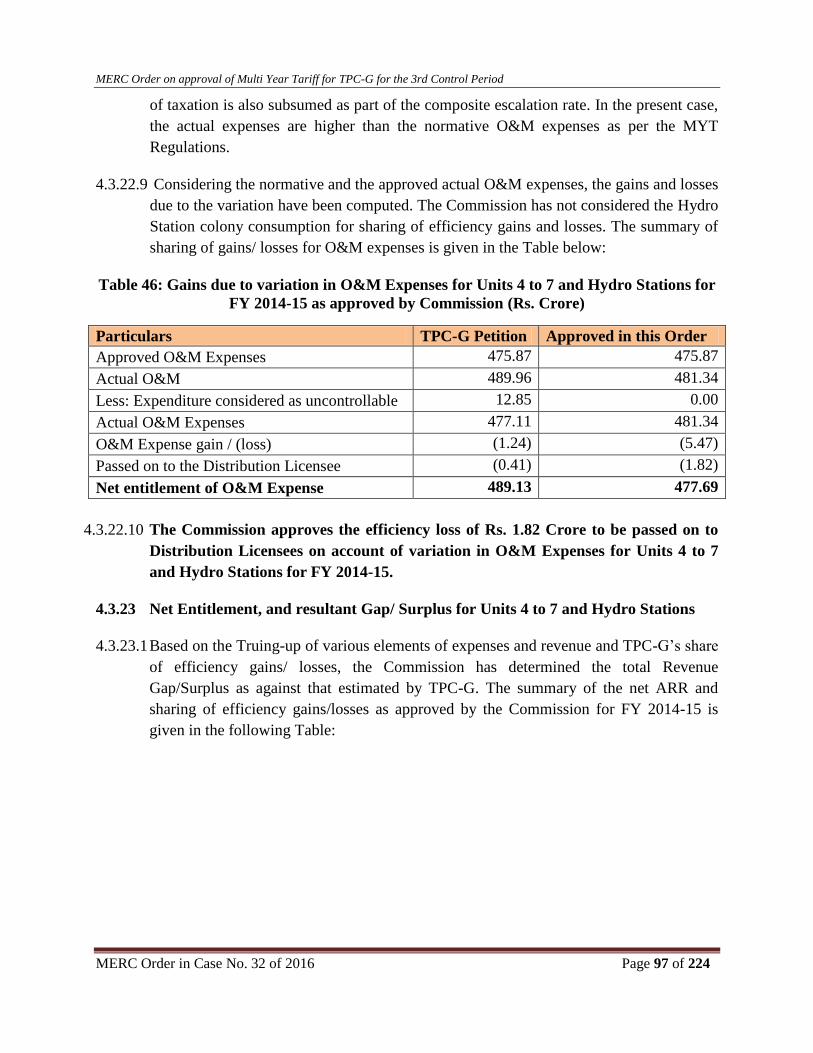

Table 46: Gains due to variation in O&M Expenses for Units 4 to 7 and Hydro Stations for FY 2014-15

as approved by Commission ...................................................................................................................... 97

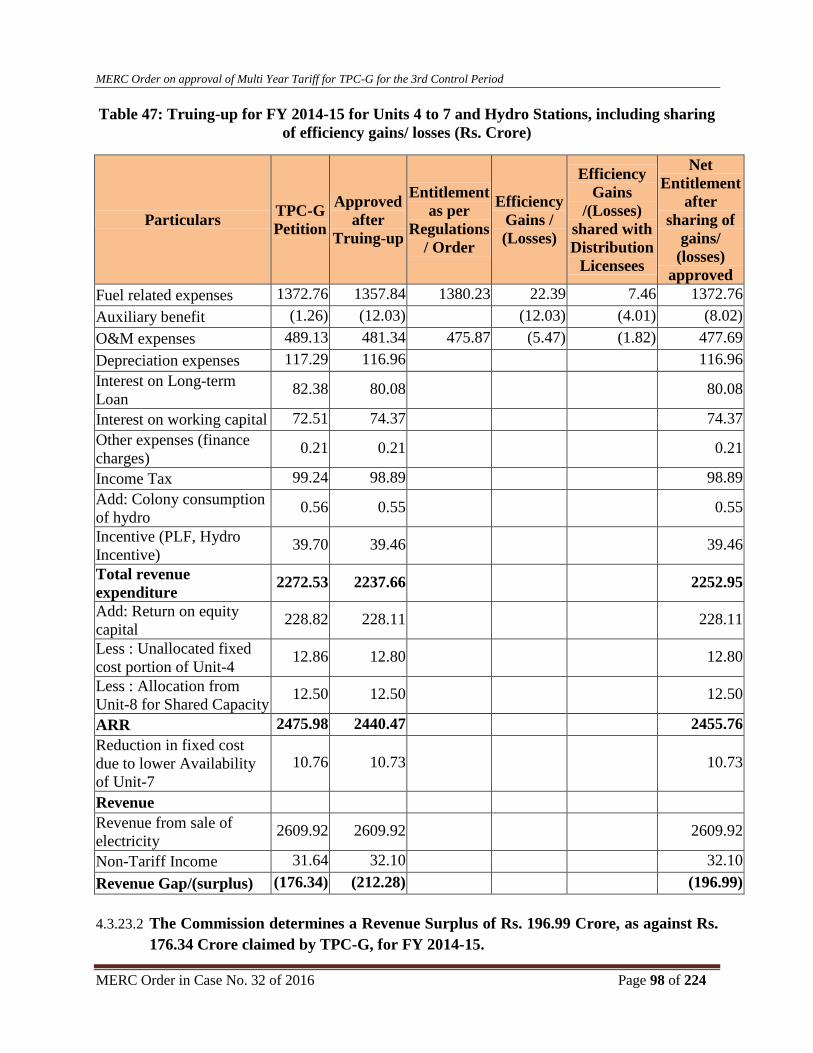

Table 47: Truing-up for FY 2014-15 for Units 4 to 7 and Hydro Stations, including sharing of efficiency

gains/ losses ............................................................................................................................................... 98

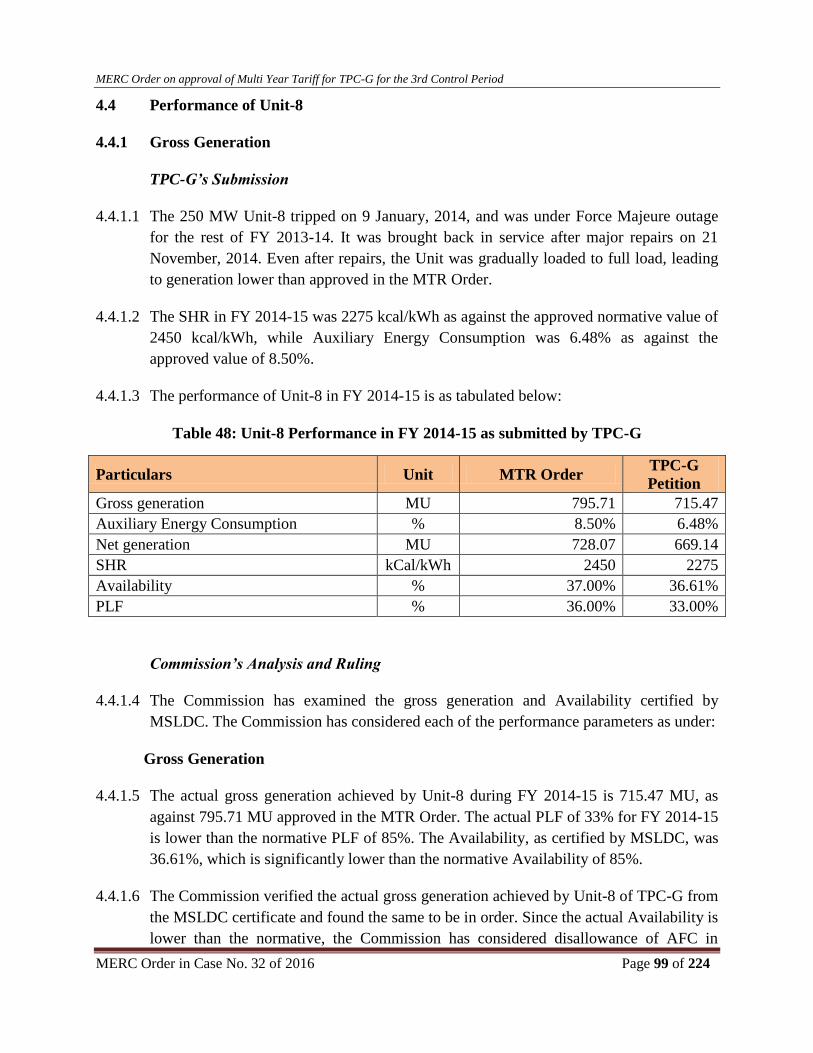

Table 48: Unit-8 Performance in FY 2014-15 as submitted by TPC-G...................................................... 99

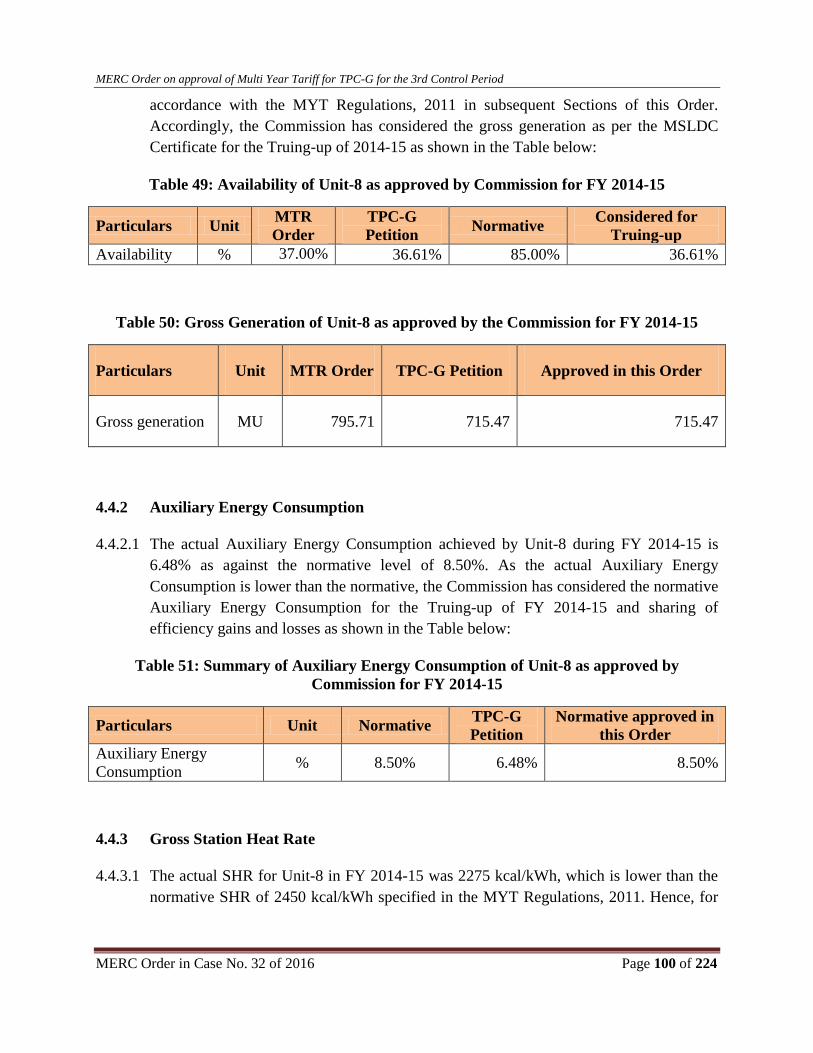

Table 49: Availability of Unit-8 as approved by Commission for FY 2014-15 ....................................... 100

Table 50: Gross Generation of Unit-8 as approved by the Commission for FY 2014-15 ........................ 100

Table 51: Summary of Auxiliary Energy Consumption of Unit-8 as approved by Commission for FY

2014-15 ..................................................................................................................................................... 100

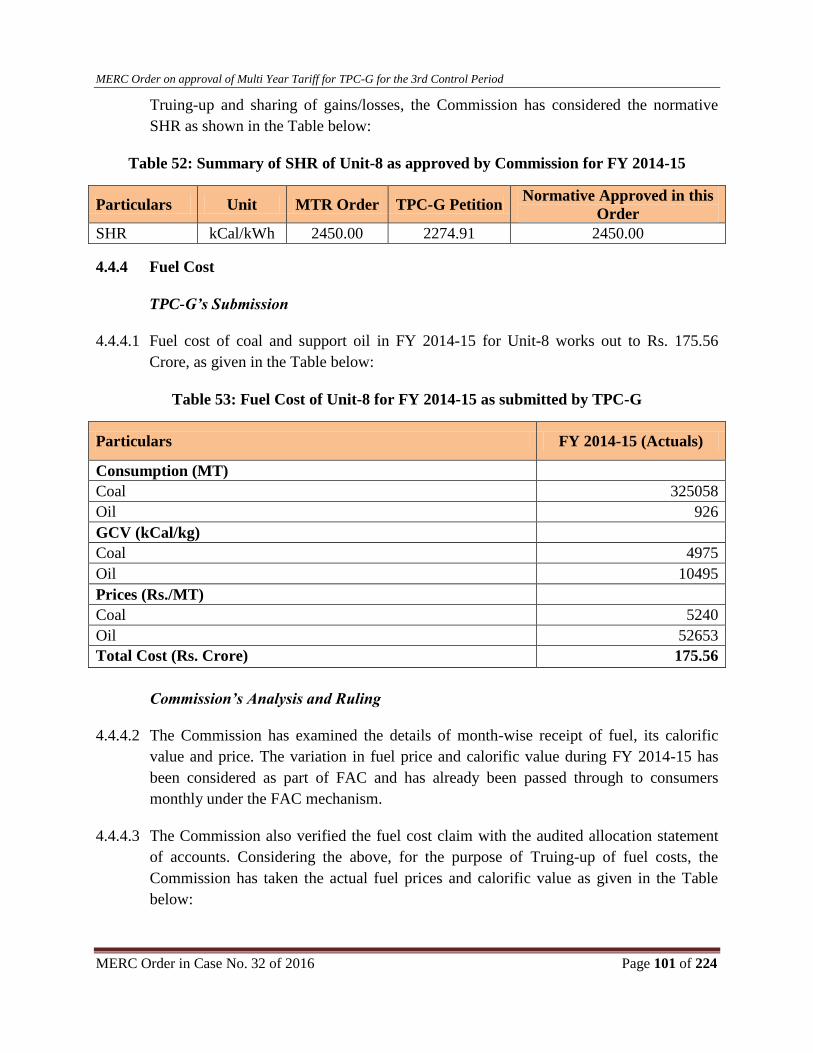

Table 52: Summary of SHR of Unit-8 as approved by Commission for FY 2014-15 .............................. 101

Table 53: Fuel Cost of Unit-8 for FY 2014-15 as submitted by TPC-G ................................................... 101

Table 54: Fuel Parameters as approved by Commission for Unit-8 for FY 2014-15 ............................... 102

Table 55: Fuel Cost as approved by Commission for Unit-8 for FY 2014-15.......................................... 102

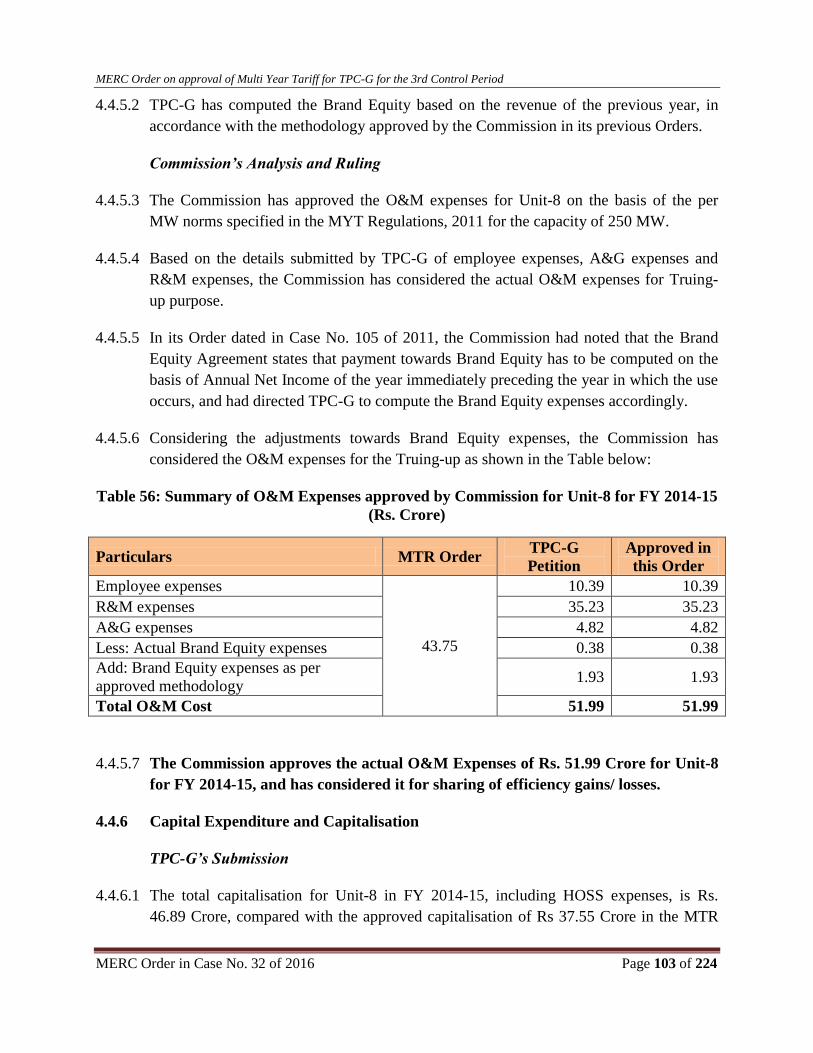

Table 56: Summary of O&M Expenses approved by Commission for Unit-8 for FY 2014-15 .............. 103

Table 57: Capitalisation of Unit-8 as approved by Commission for FY 2014-15 ................................... 104

Table 58: Summary of Non-DPR Capitalisation now approved by Commission for Unit-8 ................... 105

Table 59: Non-DPR Capitalisation for Unit-8 as approved by Commission for FY 2011-12 to FY 2013-14

.................................................................................................................................................................. 106

Table 60: Depreciation for Unit-8 as approved by Commission for FY 2014-15 ................................... 107

Table 61: Interest on Long-term Loan as approved by Commission for FY 2014-15 ............................. 108

Table 62: Return on Equity for Unit-8 as approved by Commission for FY 2014-15 ............................ 109

Table 63: Income Tax for Unit-8 for FY 2014-15 as approved by Commission ..................................... 110

Table 64: Revenue from GenerationofUnit-8 for FY 2014-15, as submitted by TPC-G .......................... 112

Table 65: Summary of Reduction of AFC for Unit-8 for FY 2014-15 as approved by Commission ....... 118

Table 66: Gains/Losses in Fuel Cost as approved by Commission for FY 2014-15 ................................ 119

Table 67: Efficiency Gains/ Losses due to variation in Auxiliary Energy Consumption of Unit-8 in FY

2014-15, as approved by Commission ...................................................................................................... 120

Table 68: Efficiency Gains/ Losses due to variation in O&M Expenses for Unit-8 for FY 2014-15 ....... 121

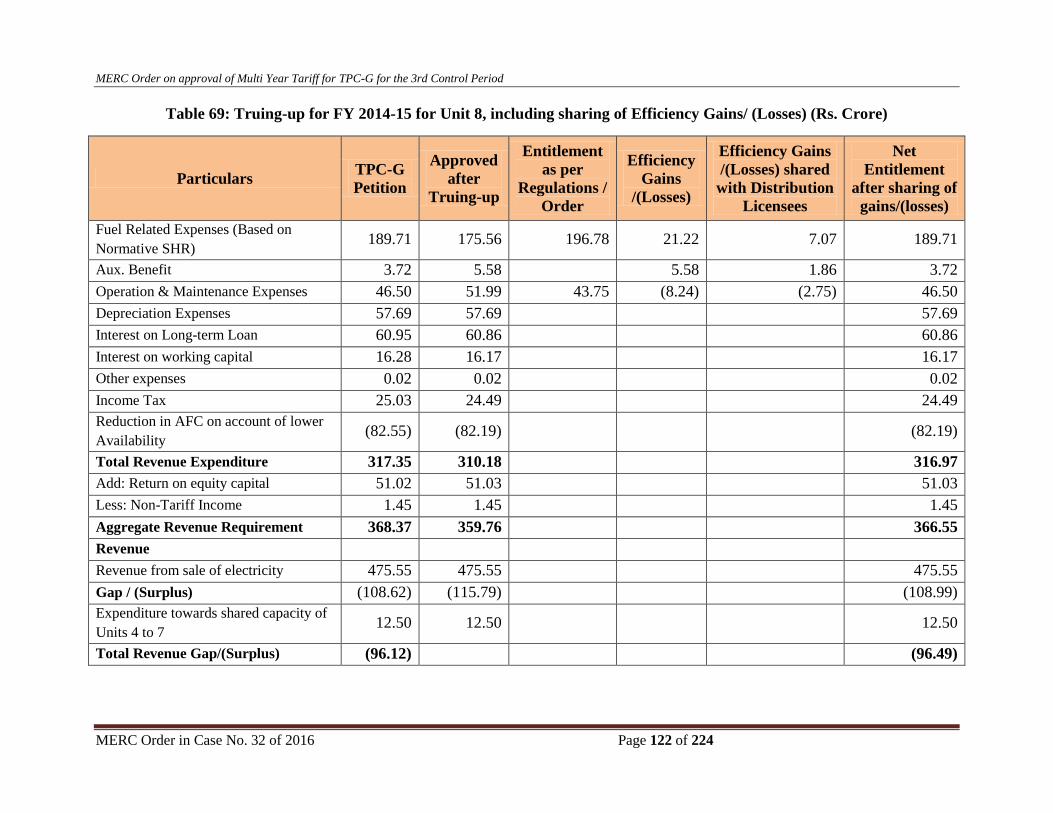

Table 69: Truing-up for FY 2014-15 for Unit 8, including sharing of Efficiency Gains/ (Losses) ......... 122

Table 70: Availability of Generating Units as submitted by TPC-G for FY 2015-16 .............................. 124

Table 71: Availability of Generating Units as submitted by TPC-G (revised submission) for FY 2015-16

.................................................................................................................................................................. 125

Table 72: Availability as approved by the Commission for FY 2015-16 ................................................. 125

Table 73: Gross Generation and PLF as submitted by TPC-G for FY 2015-16 ...................................... 127

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 9 of 224

Table 74: Gross Generation and PLF as submitted by TPC-G in revised submission for FY 2015-16 .... 127

Table 75: Gross Generation and PLF as approved by Commission for FY 2015-16 ............................... 128

Table 76: Auxiliary Energy Consumption as submitted by TPC-G for FY 2015-16 ............................... 128

Table 77: Auxiliary Energy Consumption as submitted by TPC-G in its revised submission for FY 2015-

16 .............................................................................................................................................................. 129

Table 78: Auxiliary Energy Consumption as approved by Commission for FY 2015-16 ........................ 130

Table 79: SHR for FY 2015-16 as submitted by TPC-G .......................................................................... 130

Table 80: SHR as submitted by TPC-G in its revised submission for FY 2015-16 .................................. 130

Table 81: Revised Normative SHR for Unit-6 for FY 2015-16 ................................................................ 131

Table 82: SHR as approved by the Commission for FY 2015-16 ............................................................ 131

Table 83: Fuel Prices in FY 2015-16, as submitted by TPC-G ................................................................ 134

Table 84: Fuel Prices and Calorific Value as approved by Commission for FY 2015-16 ........................ 134

Table 85: Impact of Entry Tax as submitted by TPC-G for FY 2015-16 ................................................. 136

Table 86: Recovery of Entry Tax, as approved by Commission for FY 2015-16 .................................... 136

Table 87: O&M Expenses as approved by Commission for FY 2015-16 ............................................... 137

Table 88: Schemes with major impact on Capitalisation, as submitted by TPC-G .................................. 137

Table 89: Summary of disallowed DPR Capitalisation for restricted cumulative Capitalisation ............ 139

Table 90: Summary of Capitalisation disallowed by Commission for FY 2015-16 ................................ 140

Table 91: Capitalisation as approved by Commission for FY 2015-16 ................................................... 140

Table 92: Depreciation as approved by Commission for FY 2015-16 .................................................... 142

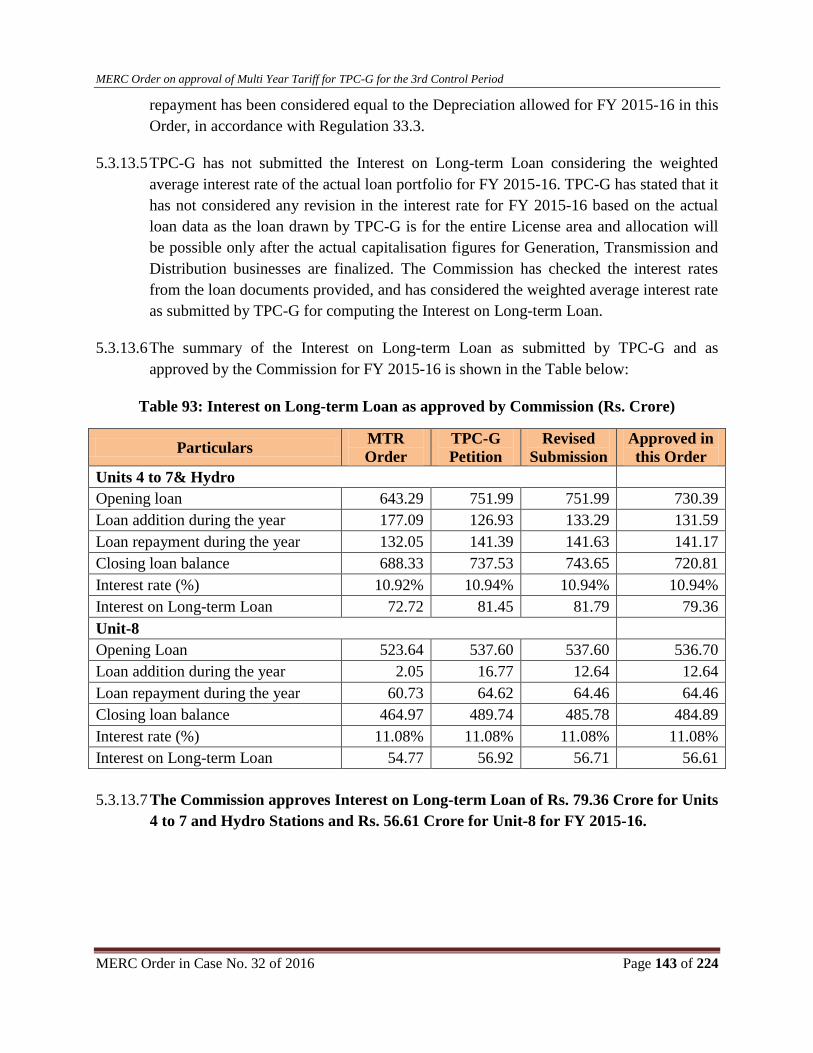

Table 93: Interest on Long-term Loan as approved by Commission ....................................................... 143

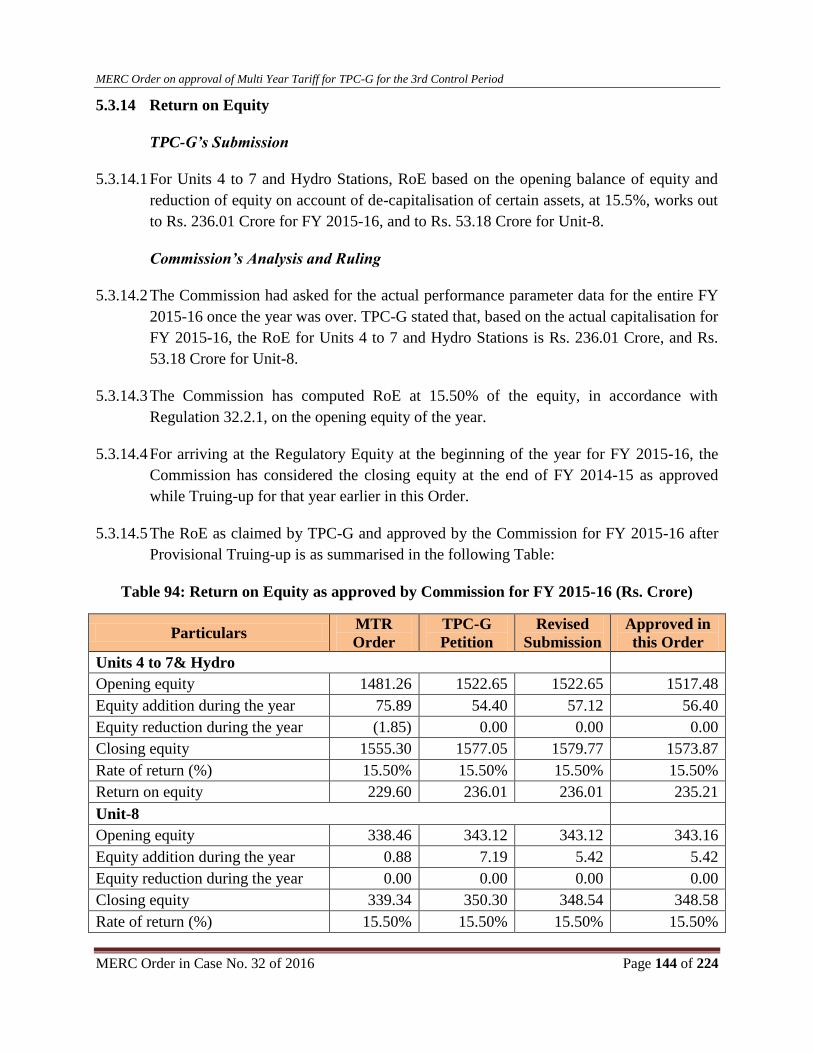

Table 94: Return on Equity as approved by Commission for FY 2015-16 .............................................. 144

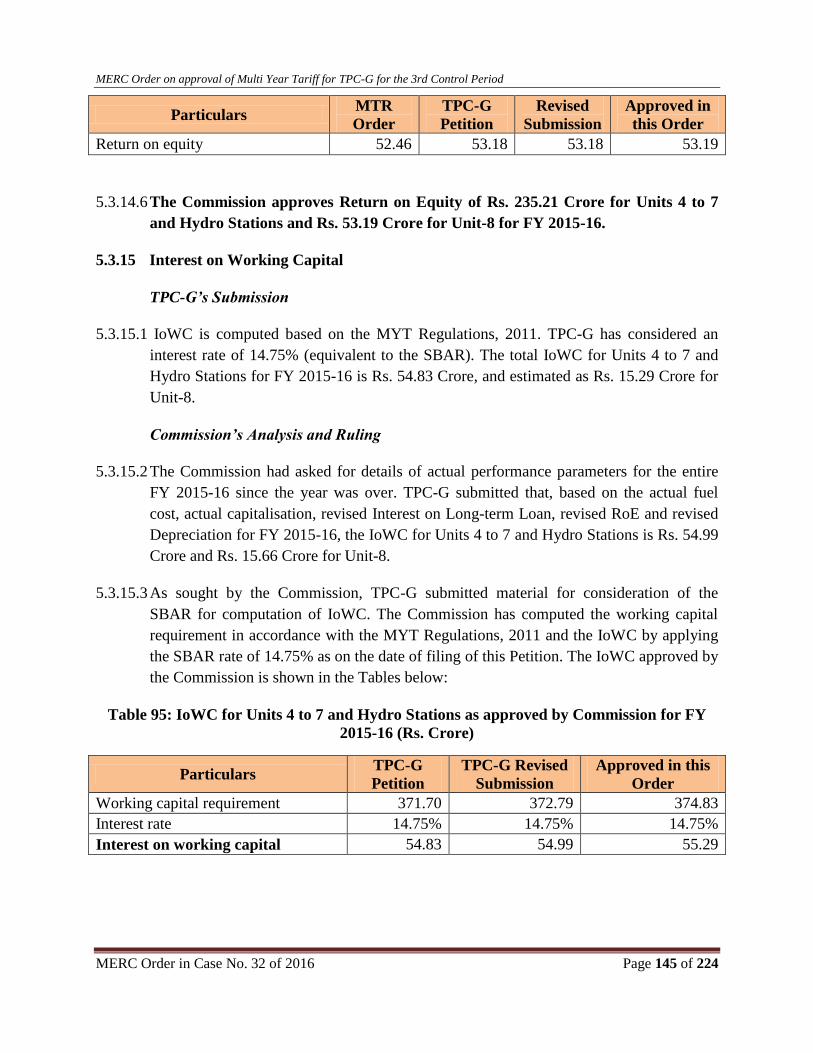

Table 95: IoWC for Units 4 to 7 and Hydro Stations as approved by Commission for FY 2015-16 ...... 145

Table 96: IoWC for Unit-8 as approved by Commission for FY 2015-16 .............................................. 146

Table 97: Income Tax as approved by Commission for FY 2015-16 ...................................................... 146

Table 98: Non-Tariff Income as approved by Commission for FY 2015-16 ........................................... 147

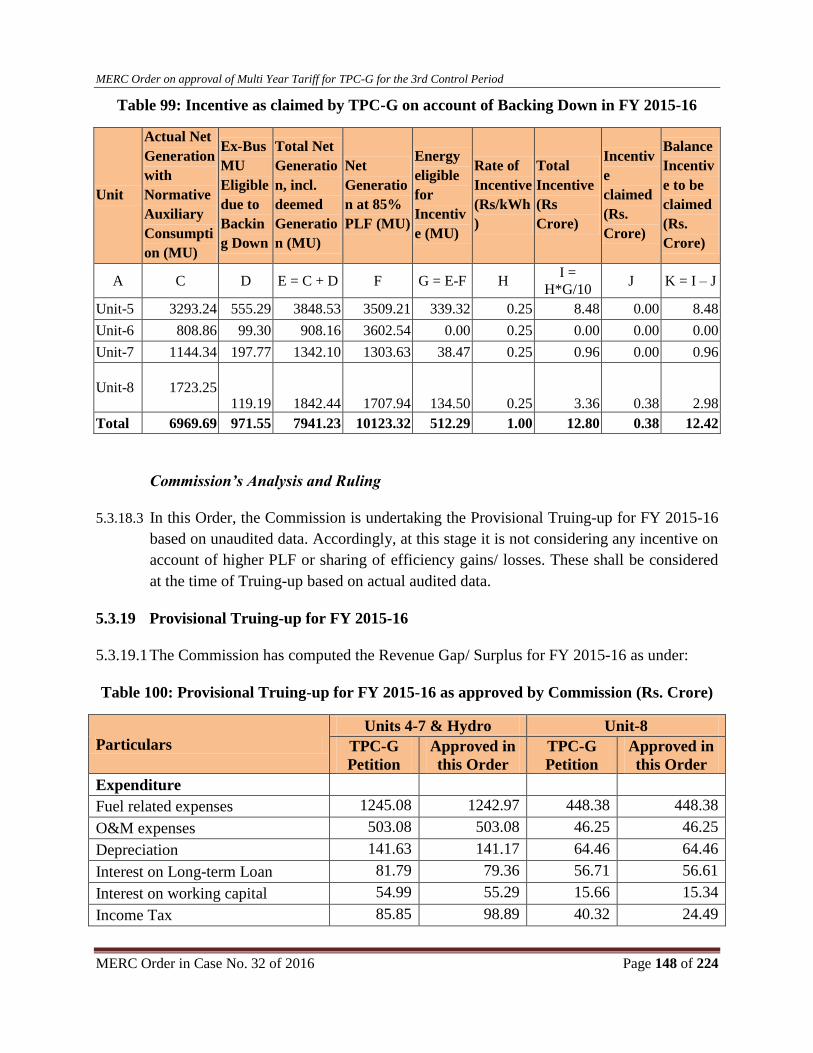

Table 99: Incentive as claimed by TPC-G on account of Backing Down in FY 2015-16 ........................ 148

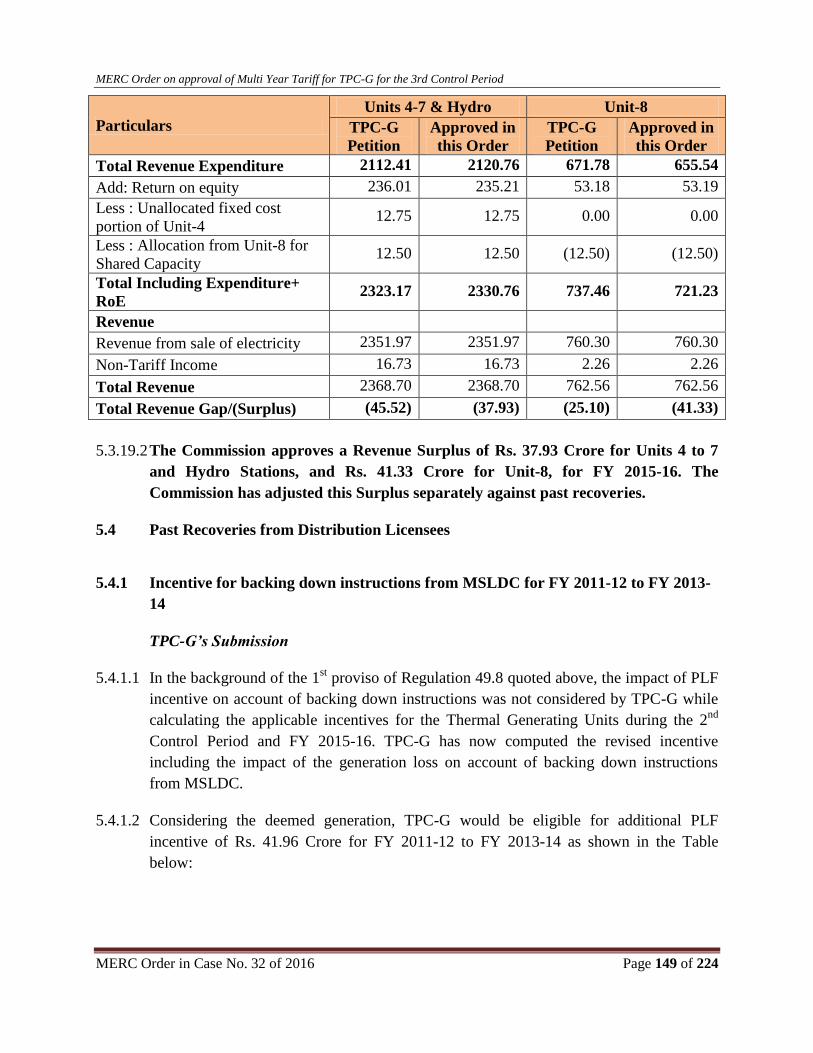

Table 100: Provisional Truing-up for FY 2015-16 as approved by Commission .................................... 148

Table 101: PLF Incentive on account of Backing Down for FY 2011-12 to FY 2013-14, as submitted by

TPC-G ...................................................................................................................................................... 150

Table 102: Fuel Cost for Unit-6 under MSLDC Directions .................................................................... 150

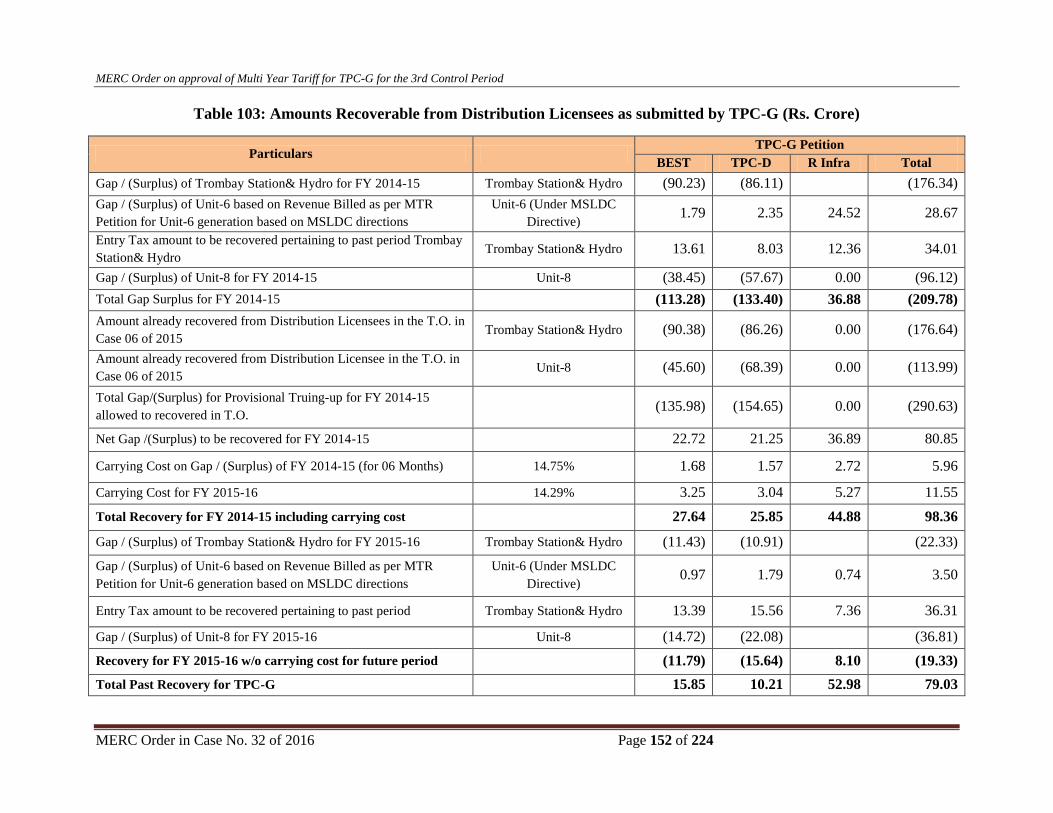

Table 103: Amounts Recoverable from Distribution Licensees as submitted by TPC-G ........................ 152

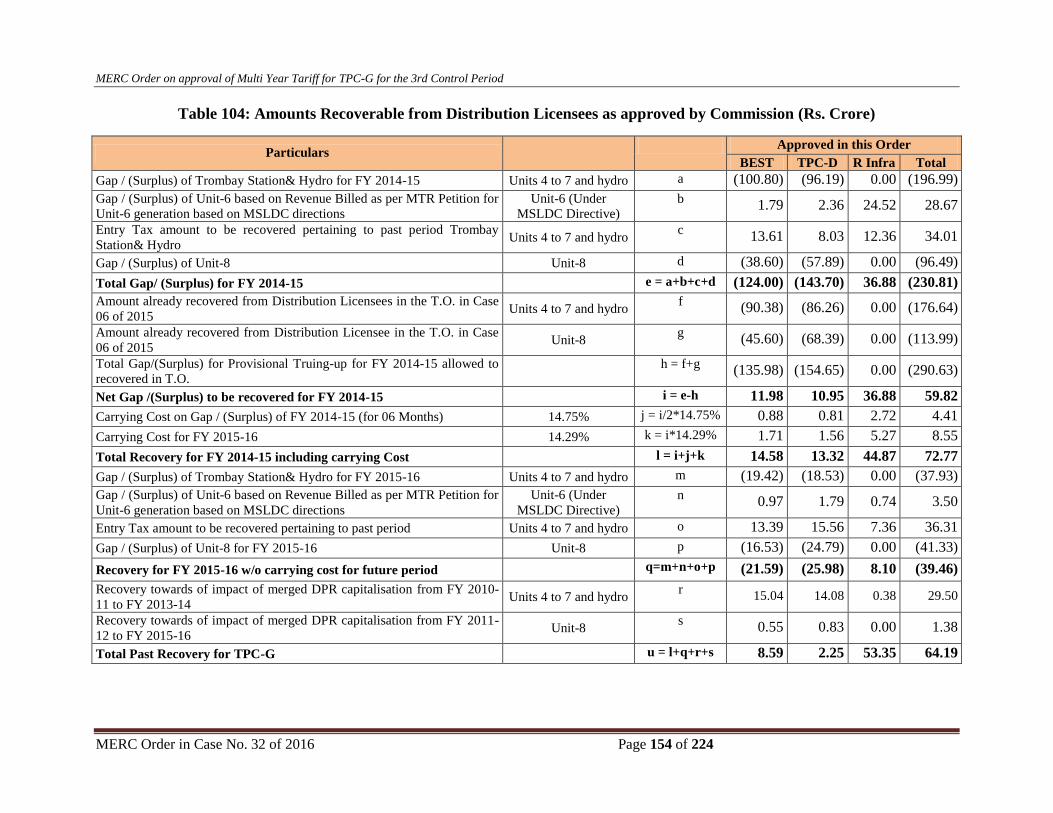

Table 104: Amounts Recoverable from Distribution Licensees as approved by Commission ................ 154

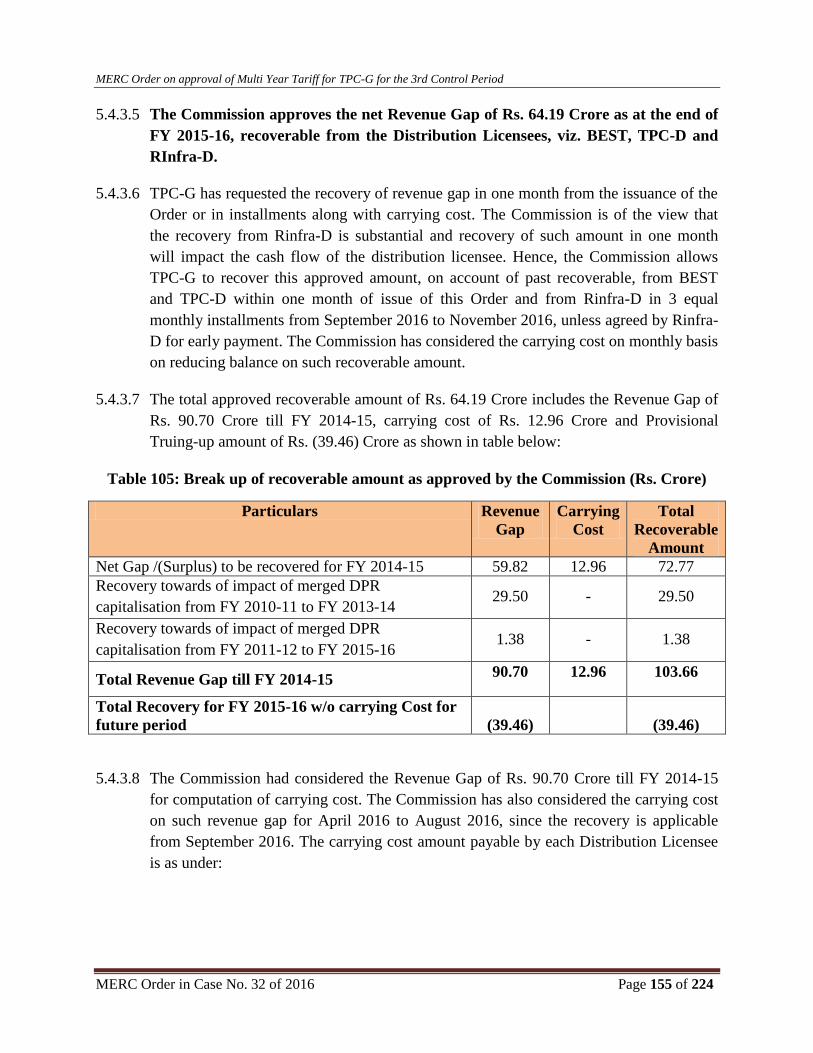

Table 105: Break up of recoverable amount as approved by the Commission ........................................ 155

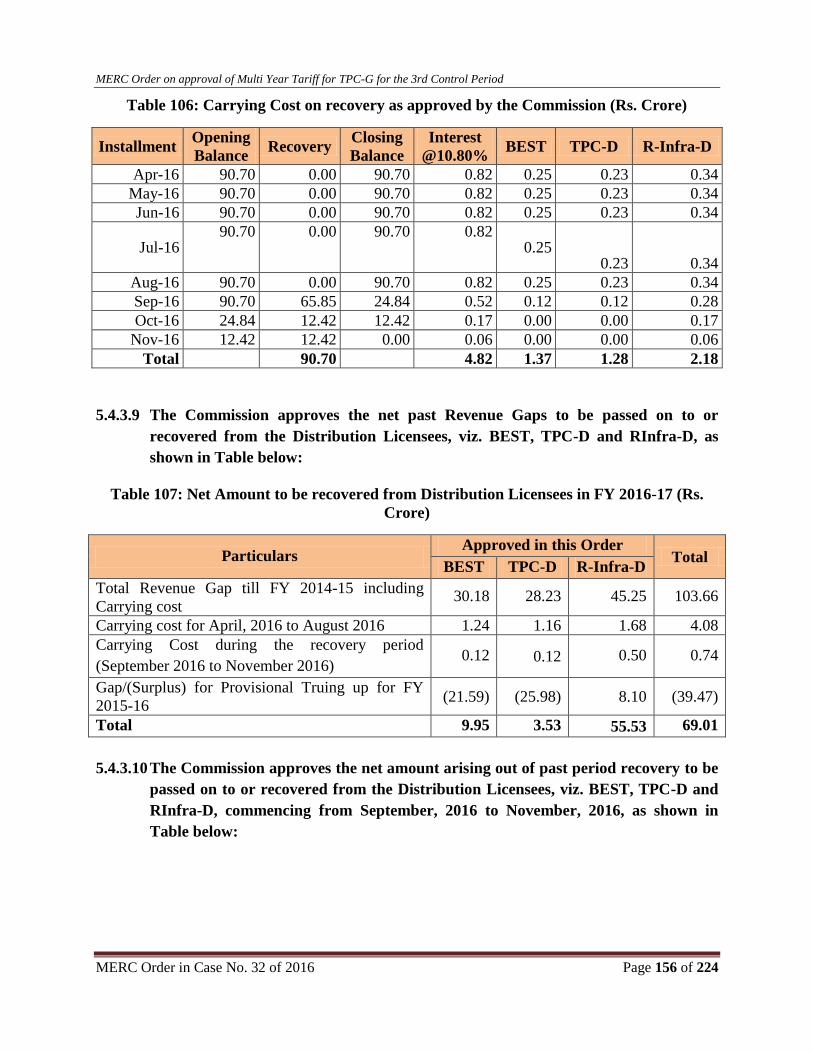

Table 106: Carrying Cost on recovery as approved by the Commission ................................................. 156

Table 107: Net Amount to be recovered from Distribution Licensees in FY 2016-17 ............................ 156

Table 108: Monthly recovery from Distribution Licensees in FY 2016-17 ............................................ 157

Table 109: Existing Generation Capacity of TPC-G ................................................................................ 159

Table 110: Availability of Generating Units in 3rd

Control Period as submitted by TPC-G .................... 159

Table 111: Availability of Generating Units in 3rd

Control Period as approved by Commission............. 160

Table 112: Summary of Gross Generation and PLF as submitted by TPC-G for 3rd

Control Period ....... 161

Table 113: Summary of Gross Generation and PLF as approved by the Commission for 3rd

Control Period

.................................................................................................................................................................. 162

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 10 of 224

Table 114: Normative Auxiliary Energy Consumption for Thermal Generating Stations for 3rd

Control

Period as submitted by TPC-G ................................................................................................................. 162

Table 115: Auxiliary Energy Consumption for Nallah Diversion as submitted by TPC-G for 3rd

Control

Period ........................................................................................................................................................ 163

Table 116: Auxiliary Energy Consumption for Thermal Generating Units for 3rd

Control Period as

approved by Commission ......................................................................................................................... 164

Table 117: Auxiliary Energy Consumption for Nallah Diversion as approved by Commission for 3rd

Control Period ........................................................................................................................................... 165

Table 118: Auxiliary Energy Consumption for Hydro Generating Stations as approved by Commission

for 3rd

Control Period ................................................................................................................................ 166

Table 119: Normative SHR for Thermal Generating Stations for 3rd

Control Period as submitted by TPC-

G ................................................................................................................................................................ 166

Table 120: SHR as approved by Commission for 3rd

Control Period ....................................................... 168

Table 121: Fuel proposed for Thermal Generating Stations in 3rd

Control Period as submitted by TPC-G

.................................................................................................................................................................. 168

Table 122: Existing Contracts for APM Gas as submitted by TPC-G ...................................................... 169

Table 123: Fuel Parameters as projected by TPC-G for 3rd

Control Period.............................................. 170

Table 124: Summary of Fuel Parameters as approved by Commission for 3rd

Control Period ................ 171

Table 125: Summary of Energy Charges as approved by Commission for 3rd

Control Period ................ 172

Table 126: O&M Expenses for Base Year as submitted by TPC-G for 3rd

Control Period ..................... 172

Table 127: O&M Expenses as submitted by TPC-G for Units 4 to 7 and Hydro for 3rd

Control Period . 173

Table 128: O&M Expenses as submitted by TPC-G for Unit-8 for 3rd

Control Period ............................ 173

Table 129: Summary of O&M Expense escalation computation for 3rd

Control Period .......................... 175

Table 130: Summary of O&M Expense escalation computation for 3rd

Control Period .......................... 175

Table 131: O&M Expenses as approved by Commission for Units 4 to 7 and Hydro Generating Stations

for 3rd

Control Period ............................................................................................................................... 176

Table 132: O&M Expenses as approved by Commission for 3rd

Control Period for Unit-8 ................... 176

Table 133: Capitalisation for Units 4 to 7 and Hydro Generating Stations for 3rd

Control Period as

submitted by TPC-G ................................................................................................................................ 177

Table 134: Capital Expenditure and Capitalisation as submitted by TPC-G for Unit-8 during 3rd

Control

Period ....................................................................................................................................................... 178

Table 135: Capitalisation disallowed by Commission for FY 2015-16 ................................................... 179

Table 136: Capitalisation approved by Commission for 3rd

Control Period ............................................ 179

Table 137: Depreciation for Units 4 to 7 and Hydro Stations as submitted by TPC-G for 3rd

Control

Period ....................................................................................................................................................... 180

Table 138: Depreciation for Unit-8 as submitted by TPC-G for 3rd

Control Period ................................ 181

Table 139: Depreciation approved by Commission for Units 4 to 7 and Hydro Stations for 3rd

Control

Period ....................................................................................................................................................... 182

Table 140: Summary of Depreciation approved by Commission for Unit-8 for 3rd

Control Period ........ 182

Table 141: Interest on Long-term Loan for Units 4 to 7 and Hydro Stations as submitted by TPC-G for 3rd

Control Period .......................................................................................................................................... 183

Table 142: Interest on Long-term Loan for Unit-8 as submitted by TPC-G for 3rd

Control Period ........ 183

Table 143: Interest on Long-term Loan for Units 4 to 7 and Hydro Stations as approved by Commission

for 3rd

Control Period ............................................................................................................................... 184

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 11 of 224

Table 144: Interest on Long-term Loan for Unit-8 as approved by Commission for 3rd

Control Period 184

Table 145: Return on Equity as submitted by TPC-G for 3rd

Control Period for Units 4 to 7 and Hydro

Stations ..................................................................................................................................................... 185

Table 146: Return on Equity as submitted by TPC-G for 3rd

Control Period for Unit-8 ......................... 186

Table 147: Return on Equity as approved by the Commission for Units 4 to 7 and Hydro Generating

Stations for 3rd

Control Period ................................................................................................................. 187

Table 148: Return on Equity as approved by the Commission for Unit-8 for 3rd

Control Period ........... 187

Table 149: Interest on Working Capital as submitted by TPC-G for Units 4 to 7 and Hydro Stations for 3rd

Control Period .......................................................................................................................................... 188

Table 150: Interest on Working Capital as submitted by TPC-G for Unit-8 for 3rd

Control Period ........ 188

Table 151: Interest on Working Capital as approved by the Commission for Units 4 to 7 and Hydro for 3rd

Control Period .......................................................................................................................................... 189

Table 152: Interest on Working Capital as approved by Commission for Unit-8 for 3rd

Control Period 189

Table 153: Income Tax for Units 4 to 7 and Hydro Stations as submitted by TPC-G for 3rd

Control Period

.................................................................................................................................................................. 190

Table 154: Income Tax for Unit-8 as submitted by TPC-G for 3rd

Control Period ................................. 190

Table 155: Income Tax for Units 4 to 7 and Hydro Stations as approved by TPC-G for 3rd

Control Period

.................................................................................................................................................................. 191

Table 156: Income Tax for Unit-8 as approved by TPC-G for 3rd

Control Period .................................. 191

Table 157: Non-Tariff Income as submitted by TPC-G for Units 4 to 7 and Hydro Stations for 3rd

Control

Period ....................................................................................................................................................... 192

Table 158: Non-Tariff Income as submitted by TPC-G for Units 4 to 7 and Hydro Stations for 3rd

Control

Period ....................................................................................................................................................... 192

Table 159: Non-Tariff Income as submitted by TPC-G for Unit-8 for 3rd

Control Period ...................... 192

Table 160: Non-Tariff Income as approved by the Commission for Units 4 to 7 and Hydro Stations for 3rd

Control Period .......................................................................................................................................... 193

Table 161: Non-Tariff Income as approved by the Commission for Unit-8 for 3rd

Control Period ........ 193

Table 162: Annual Fixed Charges for Units 4 to 7 and Hydro Stations for 3rd

Control Period ............... 194

Table 163: Annual Fixed Charges for Unit-8 for 3rd

Control Period ....................................................... 194

Table 164: Annual Fixed Charges as approved by Commission for FY 2016-17 ................................... 197

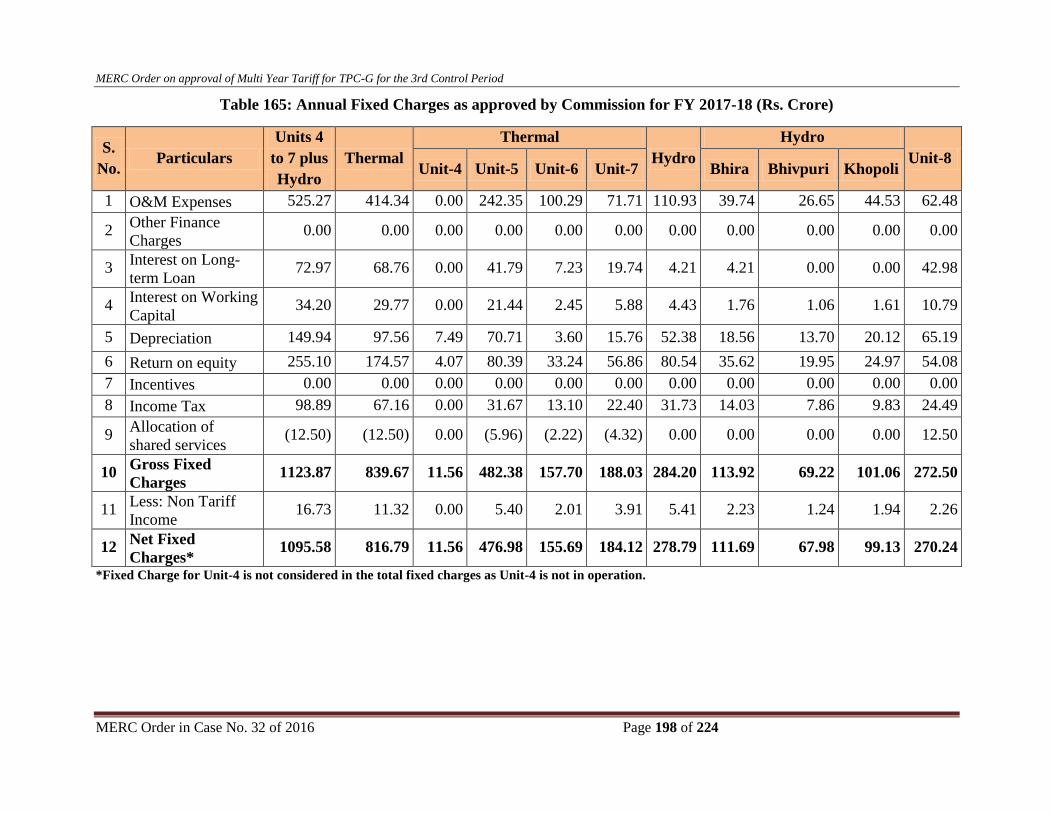

Table 165: Annual Fixed Charges as approved by Commission for FY 2017-18 ................................... 198

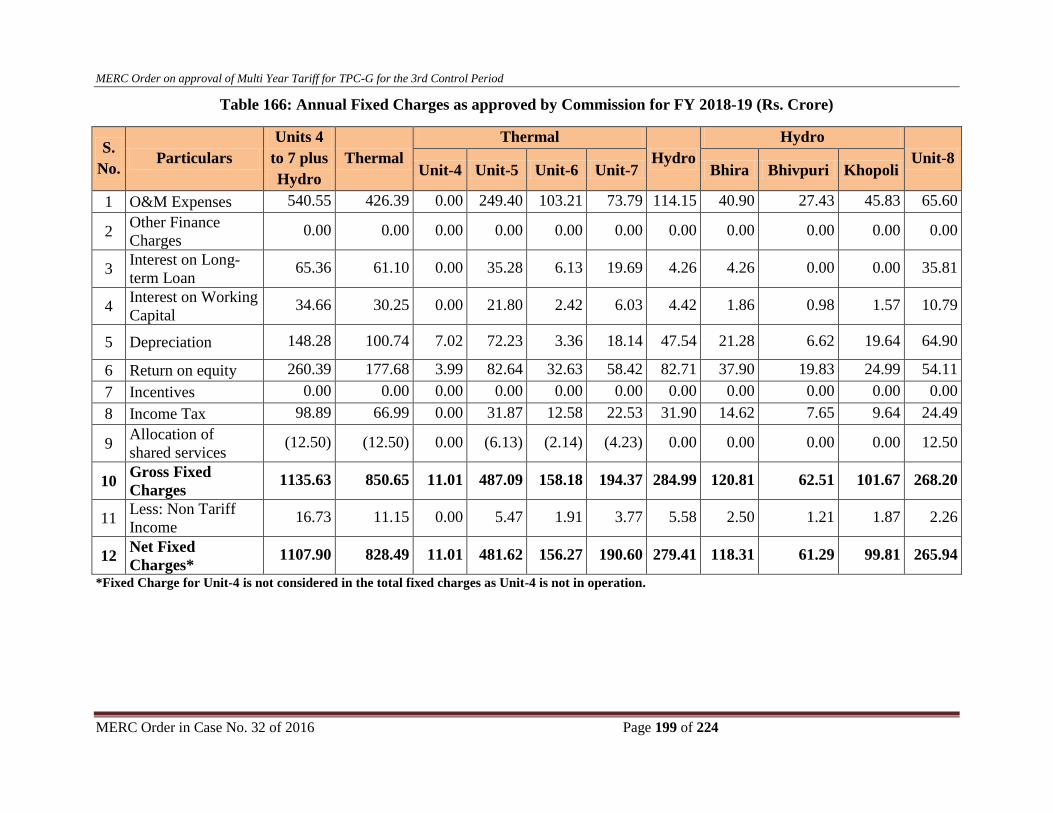

Table 166: Annual Fixed Charges as approved by Commission for FY 2018-19 ................................... 199

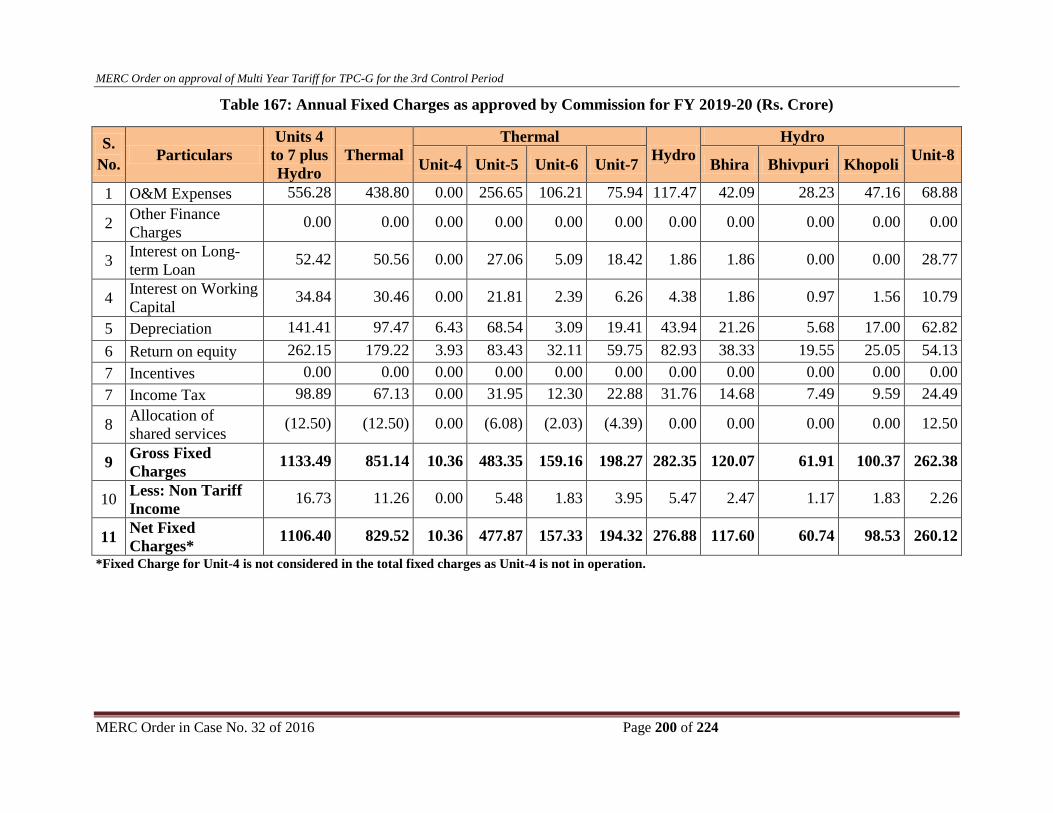

Table 167: Annual Fixed Charges as approved by Commission for FY 2019-20 ................................... 200

Table 168: Energy Charges as approved by Commission for Thermal Stations for 3rd

Control Period ... 201

Table 169: Capacity and Energy Charges for Khopoli Hydro Generating Station as submitted by TPC-G

for 3rd

Control Period ................................................................................................................................ 201

Table 170: Capacity and Energy Charges for Bhira Hydro Generating Station as submitted by TPC-G for

3rd

Control Period ...................................................................................................................................... 202

Table 171: Capacity and Energy Charges for Bhivpuri Hydro Generating Station as submitted by TPC-G

for 3rd

Control Period ................................................................................................................................ 202

Table 172: Capacity and Energy Charges for Khopoli Hydro Generating Station as approved by

Commission for 3rd

Control Period ........................................................................................................... 202

Table 173: Capacity and Energy Charges for Bhira Hydro Generating Station as approved by

Commission for 3rd

Control Period ........................................................................................................... 203

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 12 of 224

Table 174: Capacity and Energy Charges for Bhivpuri Hydro Generating Station as approved by

Commission for 3rd

Control Period ........................................................................................................... 203

Table 175: Disallowed Capitalisation towards Non-DPR Schemes as submitted by TPC-G for FY 2012-

13 ............................................................................................................................................................. 205

Table 176: Disallowed Capitalisation towards Non-DPR Schemes for FY 2013-14 .............................. 205

Table 177: Past recoveries from Distribution Licensees as approved by Commission ........................... 216

Table 178: Net Amount to be recovered from Distribution Licensees in FY 2016-17 ............................ 217

Table 179: Monthly recovery from Distribution Licensees in FY 2016-17 ............................................. 217

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 13 of 224

List of Abbreviations

Abbreviations Definitions

A&G Administrative and General

AFC Annual Fixed Charges

APR Annual Performance Review

ARR Aggregate Revenue Requirement

ATE Appellate Tribunal for Electricity

BEST BEST Undertaking

BHEL Bharat Heavy Electricals Limited

BPCL Bharat Petroleum Corporation Limited

CAGR Compounded Annual Growth Rate

CAPEX Capital Expenditure

CAT Conservation Action Trust

CERC Central Electricity Regulatory Commission

CFR Cost and Freight

COD Commercial Operation Date

CPI Consumer Price Index

CPRI Central Power Research Institute

CRZ Coastal Regulation Zone

Cu. M Cubic meter

GCV Gross Calorific Value

DPC Delayed Payment Charges

DPR Detailed Project Report

EA Electricity Act

FAC Fuel Adjustment Charge

FCCB Foreign Currency Convertible Bond

FGD Flue Gas De-sulphurisation

FOB Free On Board

FY Financial Year

GAIL Gas Authority India Limited

GFA Gross Fixed Assets

GoI Government of India

GoM Government of Maharashtra

GT Generator Transformer

HBA Index Harga Patokan Batubara Index

HOSS Head Office and Support Services

HPCL Hindustan Petroleum Corporation Limited

IDC Interest During Construction

IOC Indian Oil Corporation Limited

IWC Interest on Working Capital

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 14 of 224

Abbreviations Definitions

IDBI Industrial Development Bank of India Limited

IDFC Infrastructure Development Finance Company Limited

kCal kilo Calories

kW kilo Watt

kWh kilo Watt hour

LCC Load Control Centre

LSHS Low Sulphur Heavy Stock

MAT Minimum Alternative Tax

MbPT Mumbai Port Trust

MCGM Municipal Corporation of Greater Mumbai

MCM Million Cubic Meters

MERC or the Commission Maharashtra Electricity Regulatory Commission

MoD Merit Order Despatch

MoEF Ministry of Environment & Forest

MoPNG Ministry of Petroleum and Natural Gas

MPCB Maharashtra Pollution Control Board

MT Metric Tonnes

MTR Mid-Term Review

MU Million Units

MW Mega Watt

MWRRA Maharashtra Water Resources Regulatory Authority

MYT Multi Year Tariff

NAPAF Normative Annual Plant Availability Factor

NGT National Green Tribunal

OEM Original Equipment Manufacturer

O&M Operation and Maintenance

ONGC Oil and Natural Gas Corporation Limited

PLF Plant Load Factor

PPA Power Purchase Agreement

RBI Reserve Bank of India

RLNG Re-gasified Liquefied Natural Gas

RTL Rupee Term Loan

RoE Return on Equity

RPM Rotations Per Minute

R&M Repair and Maintenance

SBAR State Bank of India Advance Rate

SBI State Bank of India

SBI-PLR State Bank of India-Prime Lending Rate

SHR Station Heat Rate

SLP Special Leave Petition

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 15 of 224

Abbreviations Definitions

STU State Transmission Utility

SBAR State Bank Advance Rate

TPC The Tata Power Company Ltd.

TPC-D Tata Power Company-Distribution

TPC-G Tata Power Company-Generation

TPC-T Tata Power Company-Transmission

TVS Technical Validation Session

UMPP Ultra Mega Power Project

USD US Dollar

WPI Wholesale Price Index

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 16 of 224

1 BACKGROUND AND REGULATORY PROCEEDINGS

1.1. Background

1.1.1 TPC is a Company with its registered office at Bombay House, 24, Homi Mody Street,

Fort, Mumbai. TPC has various regulated and non-regulated business verticals. TPC

(Distribution Business) (TPC-D), TPC (Transmission Business) (TPC-T) and TPC-G

(Generation Business) are regulated businesses under the provisions of the EA, 2003.

TPC-G’s installed generation capacity is 2027 MW, comprising 447 MW of Hydro

Generation and 1580 MW of Thermal Generation. However, the 150 MW Unit-4

Generating Capacity is no longer in use, and hence the operational Thermal Generation

Capacity is 1430 MW. The entire generation capacity of TPC-G is tied up on a long-

term basis with two Distribution Licensees of Mumbai, namely TPC-D and

Brihanmumbai Electric Supply and Transport Undertaking (BEST).

1.1.2 This Order relates to TPC-G’s Petition for Truing-up of FY 2014-15, Provisional

Truing-up of FY 2015-16 and approval of ARR and determination of Tariff for the 3rd

Control Period from FY 2016-17 to FY 2019-20.

1.2. MYT Regulations, 2011

The Commission notified its MYT Regulations, 2011 on 4 February, 2011, applicable

for determination of Tariff for the 2nd

Control Period from FY 2011-12 to FY 2015-16.

1.3. Business Plan Order for MYT 2nd

Control Period

In its Order dated 9 August, 2012 in Case No. 166 of 2011 on TPC-G’s Business Plan

Petition, the Commission directed TPC-G to file a MYT Petition for the 2nd

Control

Period from FY 2012-13 to FY 2015-16. However, for FY 2011-12, the Commission

directed it to file the ARR as per the Tariff Regulations, 2005. On TPC-G’s Appeal

against that directive, the Appellate Tribunal for Electricity (ATE), in its Order dated 28

November, 2013, entitled it to claim ARR based on the MYT Regulations, 2011 for FY

2011-12.

1.4. Truing-up of FY 2011-12 and ARR for 2nd

Control Period FY 2012-13 to FY 2015-

16

In its Order dated 5 June, 2013 in Case No. 177 of 2011 (‘previous MYT Order’), the

Commission undertook the Truing-up of FY 2011-12 and approved the Tariff for FY

2012-13 to FY 2015-16. Aggrieved on issues relating to wrongful computation of

Operation and Maintenance (O&M) expenses, considering income from gain/losses on

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 17 of 224

Foreign Exchange as a part of Non-Tariff Income, disallowance of Auxiliary Energy

Consumption of Unit-6 and non-allowance of carrying cost on past recovery, TPC-G

filed an Appeal No. 212 of 2013. In its Judgment dated 27 October, 2014, the ATE

entitled TPC-G to claim some of the earlier disallowed expenditure.

1.5. Truing-up of FY 2012-13 and FY 2013-14, Provisional Truing-up of FY 2014-15

and Projection of ARR and Tariff for FY 2015-16

On TPC-G’s Mid-Term Review (MTR) Petition for the 2nd

Control Period (Case No. 6

of 2015) for Truing-up of FY 2012-13 and FY 2013-14, Provisional Truing-up of FY

2014-15 and projection of ARR and Tariff for FY 2015-16, the Commission issued its

Order on 26 June, 2015 (‘MTR Order’).

1.6. MYT Regulations, 2015

1.6.1 The Commission notified the MYT Regulations, 2015 on 8 December, 2015. These

Regulations are applicable for determination of Tariff for the 3rd

Control Period, i.e., FY

2016-17 to FY 2019-20.

1.6.2 TPC-G requested the Commission to extend the time for filing of MYT Petition stating

its difficulties in collecting the data and preparation of MYT Petition within the due

date. Considering the requests of various Generating Companies and Licensees,

including TPC-G, vide Order dated 15 January, 2016 the Commission allowed TPC-G to

file its Petition by 31 January, 2016.

1.7. Admission of the Petition and Public Consultation Process

1.7.1 TPC-G filed its MYT Petition on 11 February, 2016. Preliminary data gaps were

forwarded to TPC-G on 24 and 29 February and 4 March, 2016. TPC-G stated its replies

on 3 March, 2016.

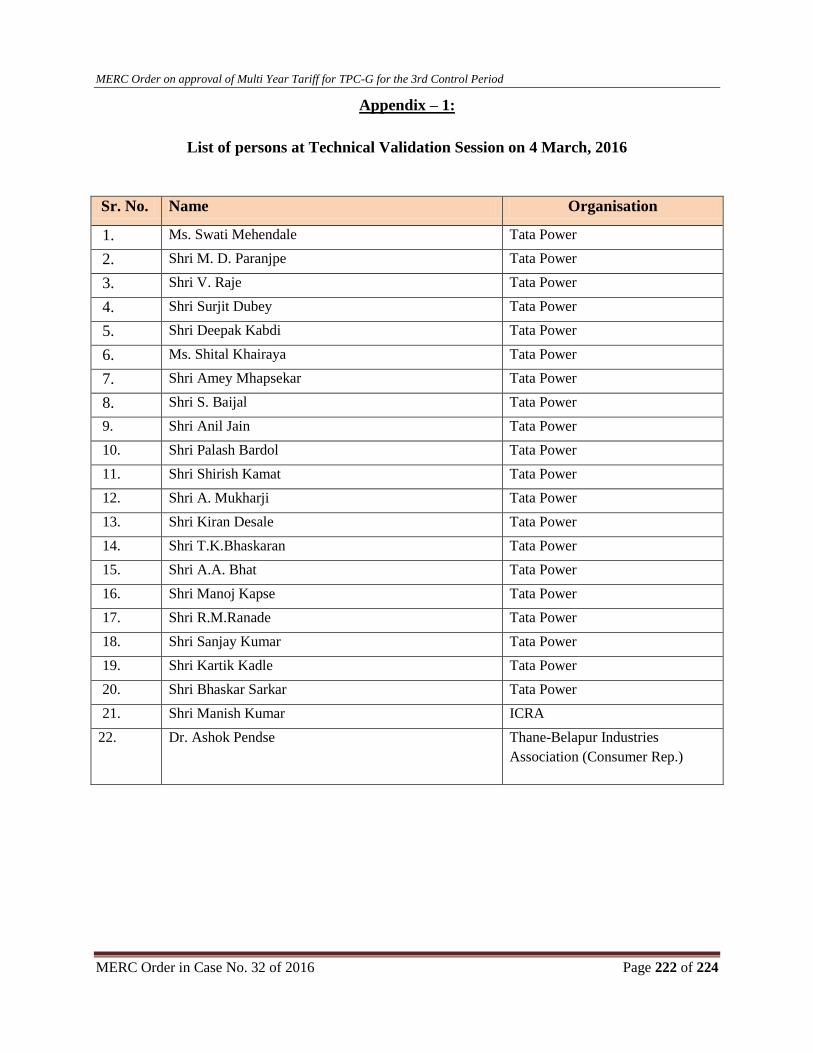

1.7.2 The Commission conducted a Technical Validation Session (TVS) on 4 March, 2016.

The list of persons who participated in the TVS is at Appendix - 1. TPC-G made a

presentation on the salient features of the Petition.

1.7.3 The Commission sought additional information and clarifications on the issues raised

during the TVS. TPC-G stated replies to the pending data gaps and issues raised during

the TVS vide its letters dated 10, 17, and 18 March 2016. Thereafter, TPC-G filed a

revised Petition on 24 March, 2016 incorporating the changes pointed out through data

gaps.

1.7.4 TPC-G’s prayers are as follows:

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 18 of 224

“

I. Accept the Truing-up for FY 2014-15, Provisional Truing-up of FY 2015-16 and past

Gap / (Surplus) thereof in accordance with the guidelines & principles outlined in

MYT Regulations, 2011;

II. Accept the Projections for FY 2016-17 to FY 2019-20 in accordance with the

guidelines & principles outlined in MYT Regulations, 2015;

III. Allow determination of normative Auxiliary Energy Consumption in Standby Mode

for Unit 6.

IV. Allow Heat Rate and Auxiliary Energy Consumption for Unit 6 under Technical

Minimum operation.

V. Allow Heat Rate and Auxiliary Energy Consumption for Unit 7 in open cycle mode

for the Third Control Period, similar to that approved in the Business Plan Order in

Case 166 of 2011 for the Second Control Period.

VI. To treat the release of 30 MCM water from Mulshi dam for drinking water purpose

as uncontrollable over and above that of low rainfall during FY 2015-16 and allow us

to apply the appropriate regulatory mechanisms provided in the Regulations in the

future years to enable the recovery of the entire fixed cost of the Generating Stations.

VII. Condone any inadvertent omissions / errors / rounding off differences / shortcomings

and permit Tata Power- G to add / change / modify / alter this filing and make further

submissions as may be required at a future date;

VIII. Pass such further and other orders, as the Hon’ble Commission may deem fit and

proper, keeping in view the facts and circumstances of the case.”

1.7.5 The Commission admitted the revised Petition on 29 March, 2016, directed TPC-G to

publish it Petition in an abridged form by 1 April, 2016, and to reply expeditiously to all

suggestions and objections received on its Petition.

1.7.6 TPC-G published the Public Notice in the daily newspapers Hindustan Times and Indian

Express (English), and Loksatta and Saamna (Marathi) on 31 March, 2016. Copies of

the Petition and its Executive Summary were made available at TPC’s offices and on

TPC-G’s website (www.tatapower.com). The Public Notice and Executive Summary of

the Petition were also made available on the websites of the Commission

(www.mercindia.org.in / www.merc.gov.in) in downloadable format.

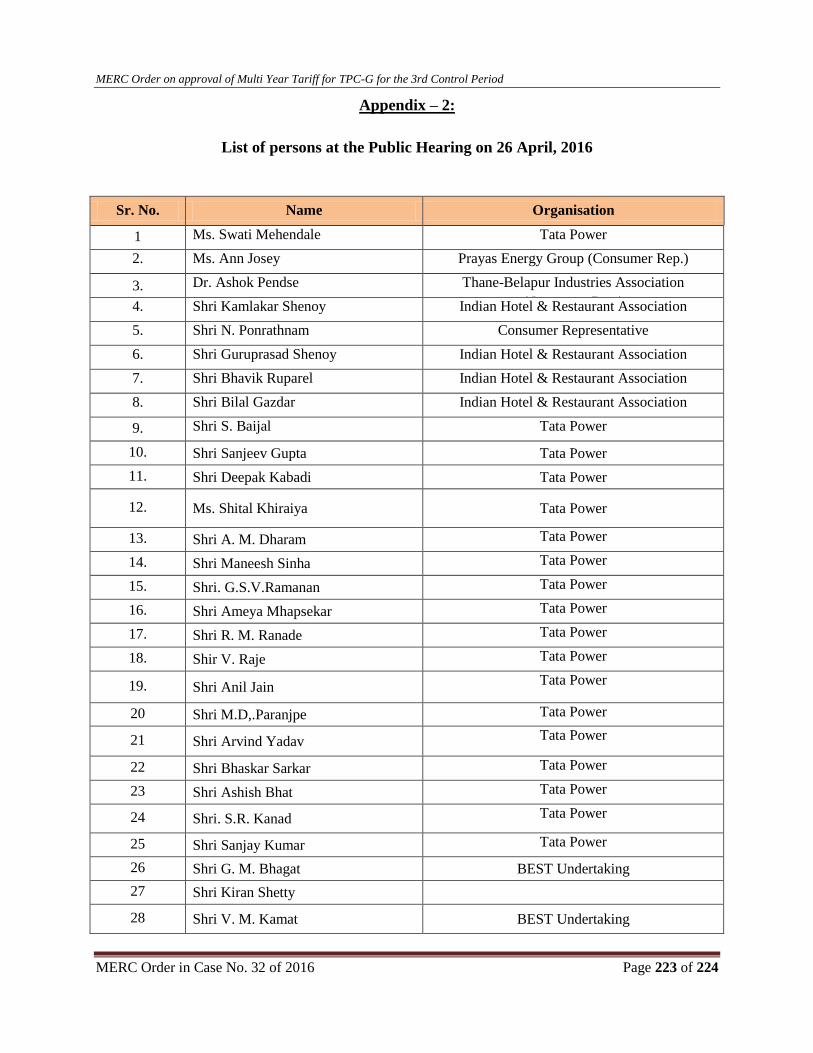

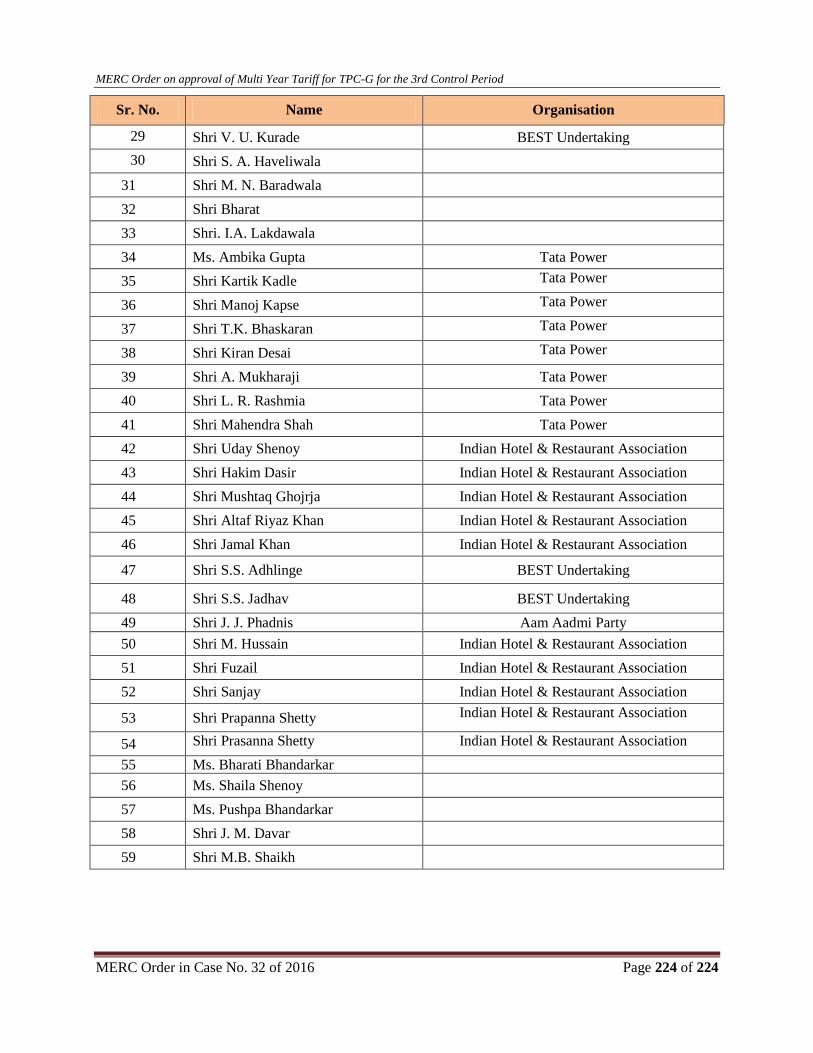

1.7.7 A Public Hearing was held on 26 April, 2016 in the Office of the Commission, 13th

Floor, Centre No. 1, World Trade Centre, Cuffe Parade, Colaba, Mumbai. The list of

persons at the Public Hearing is atAppendix-2.

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 19 of 224

1.7.8 Two more sets of data gaps were sent to TPC-G on 20 and 25 April, 2016, seeking

additional information relating to fuel purchase and revised actual unaudited data of FY

2015-16 (since the year was over). TPC-G stated its replies vide letters dated 5, 6, 10

and 13 May, 2016.

1.7.9 TPC-G made additional submission on Plant Load Factor (PLF) incentive on account of

backing down instructions for FY 2011-12 to FY 2015-16 vide letters dated 25 April and

23 May, 2016.

1.7.10 The Commission has ensured that the due process contemplated under the law to ensure

transparency and public participation was followed at every stage, and adequate

opportunity was given to all to submit their views.

1.7.11 The Commission received written suggestions and objections, and oral submissions at

the Public Hearing.

1.8. Organisation of the Order

This Order is organised in the following Sections:

Section 1 provides a brief history of the quasi-judicial regulatory process undertaken

by the Commission. A list of abbreviations with their expanded forms has been

included.

Section 2 discusses the suggestions and objections given in writing as well as those

presented during the Public Hearing. The suggestions and objections have been

summarised, followed by the response of TPC-G and the views of the Commission

on each issue.

Section 3 details the impact of ATE Judgments on the previous years' Truing-up.

Section 4 details the Truing-up of the ARR for FY 2014-15, including sharing of

efficiency gains/ losses.

Section 5 details the approval of the Provisional Truing-up for FY 2015-16.

Section 6 details the ARR and Tariff for the 3rd

Control Period.

Section 7 deals with summary of approved Tariff for the 3rd

Control Period

Section 8 covers the directives given in the MTR Order, TPC-G's responses and new

directives.

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 20 of 224

Section 9 summarises the rulings of the Commission.

Section 10 deals with Directives to TPC-G.

Section 11 sets out the applicability of this Order

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 21 of 224

2 SUGGESTIONS/ OBJECTIONS RECEIVED, TPC-G’S RESPONSE AND

COMMISSION’S VIEW

2.1 Fuel Prices

Suggestions/Objections

2.1.1 The Indian Hotel and Restaurant Association, Shri Kamlakar Shenoy, Shri Guruprasad

Shetty and Shri Lalit Vashista stated that TPC-G has inflated the purchase price of fuel.

TPC-G has projected LSHS price of Rs. 47211 per MT for the 3rd

Control Period, while

the same is sold by Bharat Petroleum at Rs. 15678 per MT. Similarly TPC-G has

projected coal purchase price as Rs. 4747 per MT, while it is being sold by Coal India

Ltd. (CIL) at Rs. 1600 per MT. TPC-G has projected purchase of Administered Pricing

Mechanism (APM) Gas at Rs. 16138 per MT, while the APM rate of Gas Authority of

India Ltd. (GAIL) is $2.32 MMBTU which works out to Rs. 6669 per MT. TPC-G has

also projected the price of imported coal as Rs 4747 per MT, which has in fact crashed

to $ 45 per MT or Rs 2992 per MT. Thus, TPC-G has inflated fuel prices by almost 3

times, thereby inflating the ARR. TPC-G is able to inflate its costs as it has the

monopoly of supplying to two major power Distribution Licensees, namely BEST and

TPC-D, who in turn charge high Tariff to their consumers.

2.1.2 Shri Kamlakar Shenoy and Shri Lalit Vashista further stated that this act of inflating the

fuel costs on affidavit filed before the Commission is a gross misrepresentation of facts,

and that such false declaration is an offence under the Indian Penal Code, IPC and hence

the Commission is duty bound to register a First Information Report (FIR) against

TPC’s Directors and concerned officials. Such deterrent actions are required to stop such

Companies from inflating expenses and thereby causing wrongful loss to consumers.

2.1.3 They also questioned why the cost of electricity has not come down as expected after the

enactment of the EA, 2003. The cost in the neighboring States is almost one third of

what is paid by electricity consumers of Mumbai. Further, verification by the

Commission of the cost of raw materials and expenses incurred was necessary before

fixing the Tariff.

TPC-G’s Response

2.1.4 TPC-G has projected the fuel prices based on its analysis of the market and to the best of

its knowledge. As per the Regulations, the fuel price gets charged at actuals by way of

the Fuel Adjustment Charge (FAC). The assumptions for fuel-wise price projections are

as below:

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 22 of 224

Oil

2.1.5 The fuel oil prices have gone down recently, and thus the projections of future prices are

in line with this trend. TPC-G uses oil in its 500 MW Unit-6, which is operated

intermittently. This intermittent operation requires it to maintain a certain inventory of

fuel oil in order to be available for generation as per requirements. As the Unit was

under economic shutdown, the fuel oil procured earlier is part of the inventory.

Accordingly, the price of fuel oil includes the weighted price of fuel oil procured earlier

at the then prevailing rates. Hence, the fuel oil price projections for the 3rd

Control

Period appear to be slightly higher.

2.1.6 As per Bharat Petroleum Corporation Ltd. (BPCL), the current price of LSHS with Low

Sulphur content of 0.5-0.65 % is Rs. 21639 per MT, which is higher than the projected

oil prices of future purchases, i.e., Rs. 20998 per MT indicated in the MYT Petition.

Coal

2.1.7 For the Trombay Generating Station, TPC-G has to abide by the stringent emission

norms on Sulphur and Ash stipulated by the Maharashtra Pollution Control Board

(MPCB). Accordingly, TPC-G has to use coal with Sulphur content below 0.3% and

Ash below 5%, which is sourced from Indonesia as Indian coal of the required

specifications is not available. Even washed domestic coal has an ash content of 34%.

2.1.8 It is not stated whether the imported coal price of USD 42 per MT cited by the objectors

is Free On Board (FOB) or Cost and Freight (CFR), and the type of coal has also not

been mentioned. Thus, TPC-G is not in a position to comment on the price of coal cited.

It appears that the price referred to is the FOB price and does not include sea freight,

local logistics, taxes and duties to arrive at the landed cost. TPC-G’s projections of FOB

price is also in the range of USD 35 to 37.5 per MT, based on the market view on

imported coal and the current FOB prices. Considering this FOB price, the landed cost

of coal works out to Rs. 4747 per MT for FY 2016-17, as stated in the Petition.

APM Gas

2.1.9 The price of APM gas is governed by the Ministry of Petroleum & Natural Gas

(MoPNG), and the gas prices indicated in the MYT Petition are based on its pricing

guidelines.

2.1.10 Thus, the projections of fuel prices are not inflated.

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 23 of 224

Commission’s View

2.1.11 The Commission has examined the data stated by TPC-G and sought additional

information, viz. imported coal contracts and bills, details of quantity, price and Gross

Calorific Value (GCV) of fuel, details of process followed for competitiveness, etc. The

GCV, price and quantity of fuel have been approved based on scrutiny, as summarized

below

a. Regarding imported coal, the Commission asked for the Letter of Award (LoA)

for contracts relating to imported coal and asked TPC-G to clarify whether the

procurement was through competitive bidding. TPC-G has provided all the bills

for imported coal for FY 2014-15 and FY 2015-16. The Commission analyzed

these contracts, bills and submissions. The Commission found that the payments

for coal-related invoices were made to the agencies with whom the LoAs were

signed. The quantity of fuel claimed in the Petition matched the totals of the

quantity in the bills for imported coal. The Commission sought details of the

process followed for entering into supply agreements for imported coal for the

Trombay Station. TPC-G stated that the annual coal requirement is about 2.70

MMT. The Trombay Station requires low sulphur, low ash and medium GCV coal

to meet the stringent environment norms. TPC-G had existing contracts for 1.3

MMT per annum with P. T Adaro, Indonesia. For the balance 1.4 MMT, global

competitive bids were invited on 25 March, 2015 in EXIM (Weekly newsletter)

and Platts International Coal Trader (Daily News Letter). In response, three

bidders submitted their interest:

i. P.T. Adaro, Indonesia

ii. Samtan Co. Ltd., Korea

iii. P.T. Mitrabara, Indonesia

b. After technical evaluation and quality checks, two bidders, viz. P.T. Adaro and

Samtan Co. were found to be technically suitable and were invited for price

negotiations. Thereafter, in order to have two sources for better operational

flexibility, the contract was awarded to both these bidders at the same negotiated

price (P.T. Adaro 0.6 MMT per annum and Samtan 0.8 MMT per annum). The

Commission noted that the negotiated price was linked the international coal

index.

c. The Commission sought details of month-wise opening stock (quantity and price),

procurement and closing stock of each fuel. The Commission has also considered

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 24 of 224

the month-wise weighted average price calculations for fuel based on existing

stock and new purchases.

d. The Commission also cross-checked the fuel cost claim for FY 2014-15 with the

audited allocation statement of accounts.

2.1.12 The Commission has approved the fuel prices and GCV for the 3rd

Control Period as per

the MYT Regulations, 2015, i.e., considering the actual weighted average fuel price as

considered above and the GCV of the past three months. The landed price of coal is also

adjusted for the variation in Clean Environment Cess (earlier known as Clean Energy

Cess). The Commission has not allowed any year-wise escalation in fuel prices as the

future variations upwards or downwards are taken into account through the FAC

charges.

2.2 Competitive Bidding for Power Purchase

Suggestions/Objections

2.2.1 The Indian Hotel and Restaurant Association and Shri Guruprasad Shetty stated that the

object of the EA, 2003 is to bring in competition. The Govt. of India (GoI) has issued

guidelines that power procured by the Distribution Licensees should be through

competitive bidding. Many Licensees, i.e., from Gujarat, Goa, Madhya Pradesh,

Karnataka, etc. have benefited by competitive bidding, lowering their power purchase

cost. M/s Torrent, Adani, National Thermal Power Corporation (NTPC), Videocon,

Reliance Infrastructure Ltd. (RInfra) and TPC have opted for competitive bidding and

have obtained at lower cost. RInfra’s Sasan Ultra Mega Power Project (UMPP) has

publicized the cost of Rs 1.19/ kWh. To be fair to the consumers, TPC-G should not be

given the comfort of monopoly supply and Distribution Utilities should undertake

transparent competitive bidding for price discovery. Further, if electricity generation and

distribution are two separate businesses of the same Company, it should be ensured that

there is no conflict of interest.

2.2.2 Shri Guruprasad Shetty further stated that, in the recent past, the prices of raw material

required for power generation have substantially decreased. Coal, oil and gas are now

amply available at rates which are one third of the rates prevailing a few years back. The

electricity prices in the open market have crashed, and electricity in the open market is

now available at around Rs. 2.00 per Unit whereas the Tariff proposed by TPC-G is

nearly double that. As TPC-G’s cost of generation is more than the rates at which power

is being sold through competitive bidding and in the open market, TPC should buy

power from the open market instead of generating itself. Alternatively, the Distribution

Licensee can buy power through competitive bidding from the open market. Further,

Comptroller & Auditor General (CAG) audits have revealed that some of the biggest

MERC Order on approval of Multi Year Tariff for TPC-G for the 3rd Control Period

MERC Order in Case No. 32 of 2016 Page 25 of 224

scams occurred when competitive bidding was bypassed. Even the Supreme Court has

reprimanded the authorities for not calling for competitive tenders.

2.2.3 Shri Kamlakar Shenoy and Shri Lalit Vashista also stated that Sections 61(c) and (d) of

the EA, 2003 regarding encouraging competition and safeguarding of consumers'

interest have not been complied with while determining Tariff in the past. The final cost

borne by electricity consumers in neighboring States is around Rs. 4.00/kWh to Rs.

5.00/kWh whereas it is around Rs. 17.00/kWh for Mumbai consumers. Hence, gross

injustice is caused to the electricity consumers of Mumbai due to non-compliance of

Section 61.

TPC-G’s Response

2.2.4 The objections pertain to the Distribution Business, and hence no response is required

from TPC-G.

Commission’s View

2.2.5 The issues raised relate to the procurement modalities of the Mumbai Distribution

Licensees in general and TPC-D in particular, and whether at all they should buy

apparently costly power from TPC-G. TPC-D and BEST, both Mumbai Distribution

Licensees, have entered into a long-term Power Purchase Agreements (PPA) for power

procurement from TPC-G (in addition to sourcing a smaller quantum from elsewhere).

This PPA procurement is at Tariffs approved by the Commission from time to time after

examination and in accordance with Section 62 and other provisions of the EA, 2003

and the MYT Regulations.

2.2.6 Long-term power procurement through PPA and short-term power procurement from the

open market both have certain merits and demerits. While short-term power

procurement from the open market appears to be beneficial and cheaper at present (and

is, indeed, being resorted to from time to time), Distribution Licensees cannot depend

upon it for the bulk of their requirements considering variations in availability and price

(which is also influenced by the extent of their purchases), and stable long-term

arrangements are required which also enable better transmission system planning.

2.2.7 Moreover, sourcing of power from outside for Mumbai, in particular, is still constrained

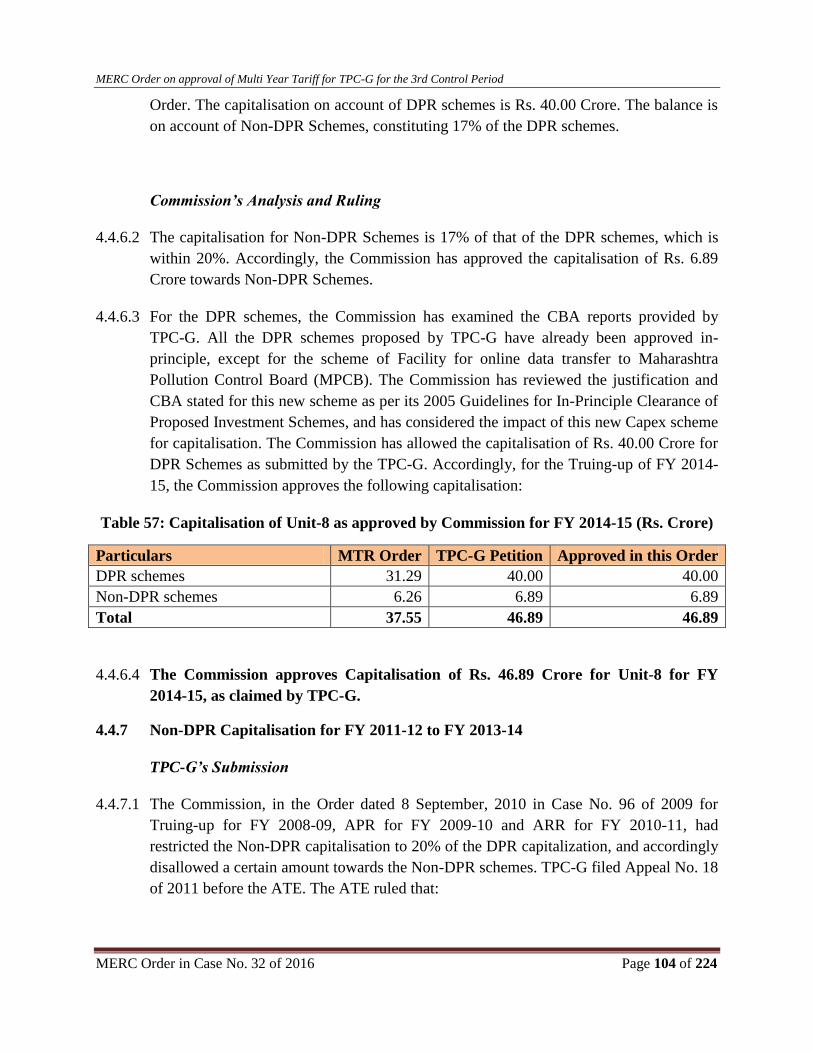

by transmission availability. This also limits the quantum of power which can be