BCOR 1020Business Statistics

Lecture 11 – February 21, 2008

Overview

• Chapter 6 – Discrete Distributions– Poisson Distribution– Linear Transformations

Chapter 6 – Poisson Distribution

Poisson Processes:• If the number of “occurrences” of interest on a given

continuous interval (of time, length, etc.) are being counted, we say we have an approximate Poisson Process with parameter > 0 (occurrences per unit length/time) if the following conditions are satisfied…

1) The number of “occurrences” in non-overlapping intervals are independent.

2) The probability of exactly one “occurrences” in a sufficiently short interval of length h is h. (i.e. If the interval is scaled by h, we also scale the parameter by h.)

3) The probability of two or more “occurrences” in a sufficiently short interval is essentially zero. (i.e. there are no simultaneous “occurrences”.)

Chapter 6 – Poisson Distribution

Poisson Distribution:• The Poisson distribution describes the number of

occurrences within a randomly chosen unit of time or space.

• For example, within a minute, hour, day, square foot, or linear mile.

If X denotes the number of “occurrences” of interest observed on a given interval of length 1 unit of a Poisson Process with parameter > 0, then we say that X has the Poisson distribution with parameter .

Chapter 6 – Poisson DistributionPoisson Distribution:• Called the model of arrivals, most Poisson applications

model arrivals per unit of time.• The events occur randomly and independently

over a continuum of time or space:

One Unit One Unit One Unit of Time of Time of Time |---| |---| |---|• • •• • • • •••• • • • •• • • ••• • • •

Flow of Time

• Each dot (•) is an occurrence of the event of interest.

Chapter 6 – Poisson Distribution• Let X = the number of events per unit of time.• X is a random variable that depends on when the

unit of time is observed.• For example, we could get X = 3 or X = 1 or

X = 5 events, depending on where the randomly chosen unit of time happens to fall.

One Unit One Unit One Unit of Time of Time of Time |---| |---| |---|• • •• • • • •••• • • • •• • • ••• • • •

Flow of Time

Chapter 6 – Poisson Distribution• Arrivals (e.g., customers, defects, accidents) must

be independent of each other.• Some examples of Poisson models in which

assumptions are sufficiently met are:

• X = number of customers arriving at a bank ATM in a given minute.

• X = number of file server virus infections at a data center during a 24-hour period.

• X = number of blemishes per sheet of white bond paper.

Chapter 6 – Poisson Distribution

Poisson Processes:

represents the mean number of events (occurrences) per unit of time or space.

• The unit of time should be short enough that the mean arrival rate is not large (< 20).

• To make smaller, convert to a smaller time unit (e.g., convert hours to minutes).

• The Poisson model’s only parameter is (Greek letter “lambda”).

Chapter 6 – Poisson Distribution

Poisson Processes:

• The number of events that can occur in a given unit of time is not bounded, therefore X has no obvious limit.

• However, Poisson probabilities taper off toward zero as X increases.

• The Poisson distribution is sometimes called the model of rare events.

Chapter 6 – Poisson Distribution

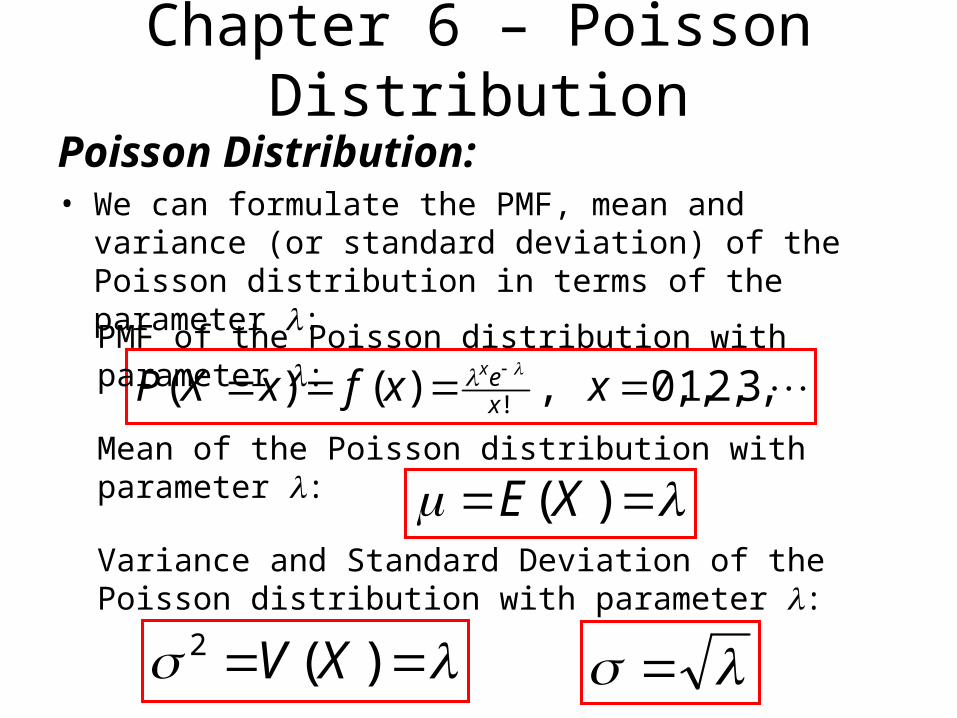

Poisson Distribution:• We can formulate the PMF, mean and variance (or

standard deviation) of the Poisson distribution in terms of the parameter :

,3,2,1,0,)()( ! xxfxXP x

ex PMF of the Poisson distribution with parameter :

)(XE

)(2 XV

Mean of the Poisson distribution with parameter :

Variance and Standard Deviation of the Poisson distribution with parameter :

Chapter 6 – Poisson Distribution

Parameters = mean arrivals per unit of time or space

Range X = 0, 1, 2, ... (no obvious upper limit)

Mean

St. Dev.

Random data Use Excel’s Tools | Data Analysis | Random Number Generation

Comments Always right-skewed, but less so for larger .

( )!

xeP x

x

Chapter 6 – Poisson Distribution

• Poisson Processes:

Poisson distributions are always right-skewed but become less skewed and more bell-shaped as increases.

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

0 4 8 12 16

Number of Calls

= 0.8

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0 4 8 12 16

Number of Calls

= 1.6

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.14

0.16

0.18

0 4 8 12 16

Number of Calls

= 6.4

Chapter 6 – Poisson Distribution

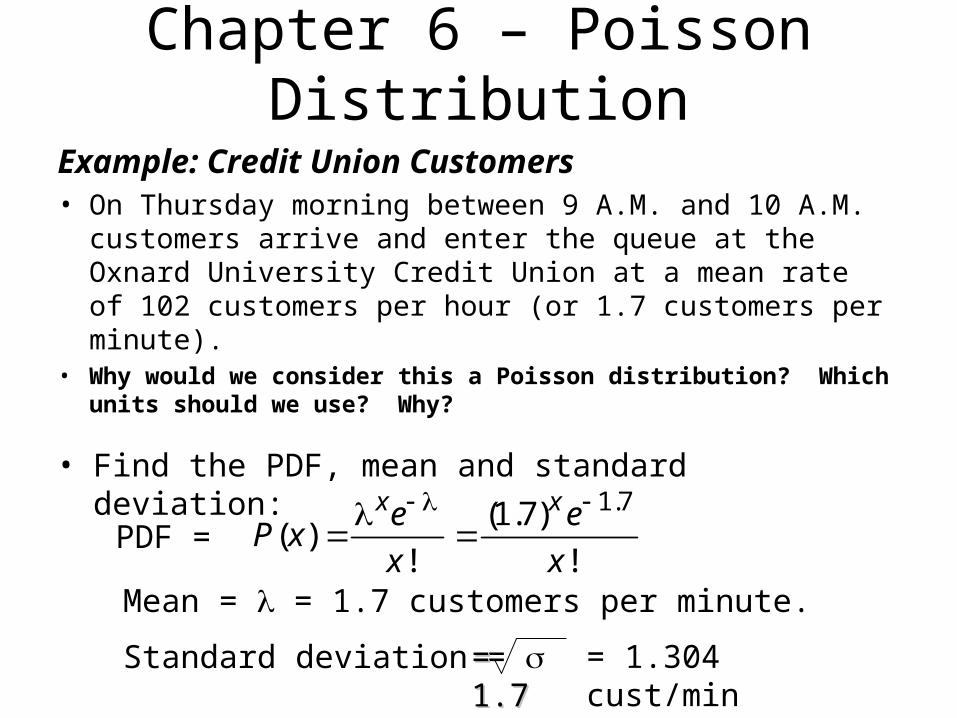

Example: Credit Union Customers• On Thursday morning between 9 A.M. and 10 A.M.

customers arrive and enter the queue at the Oxnard University Credit Union at a mean rate of 102 customers per hour (or 1.7 customers per minute).

• Why would we consider this a Poisson distribution? Which units should we use? Why?

• Find the PDF, mean and standard deviation:

PDF = 1.7(1.7)

( )! !

x xe eP x

x x

Mean = = 1.7 customers per minute.

Standard deviation = = 1.7= 1.7 = 1.304 cust/min

Chapter 6 – Poisson Distribution

• Example: Credit Union Customers• Here is the Poisson probability

distribution for = 1.7 customers per minute on average.

xPDF

P(X = x)CDF

P(X x)

0 .1827 .1827

1 .3106 .4932

2 .2640 .7572

3 .1496 .9068

4 .0636 .9704

5 .0216 .9920

6 .0061 .9981

7 .0015 .9996

8 .0003 .9999

9 .0001 1.0000

• Note that x represents the number of customers.

• For example, P(X=4) is the probability that there are exactly 4 customers in the bank.

Chapter 6 – Poisson Distribution

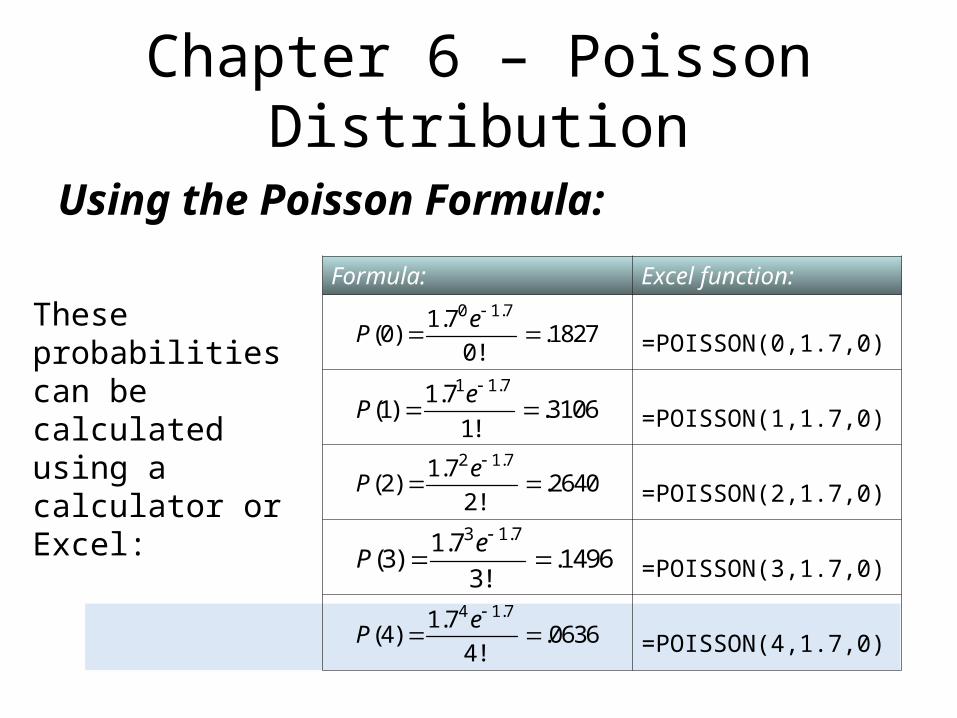

Using the Poisson Formula:

These probabilities can be calculated using a calculator or Excel:

Formula: Excel function:

=POISSON(0,1.7,0)

=POISSON(1,1.7,0)

=POISSON(2,1.7,0)

=POISSON(3,1.7,0)

=POISSON(4,1.7,0)

3 1.71.7(3) .1496

3!

eP

4 1.71.7(4) .0636

4!

eP

2 1.71.7(2) .2640

2!

eP

1 1.71.7(1) .3106

1!

eP

0 1.71.7(0) .1827

0!

eP

Chapter 6 – Poisson Distribution

• Here are the graphs of the distributions:

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0 1 2 3 4 5 6 7 8 9

Number of Customer Arrivals

Pro

bab

ility

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

0 1 2 3 4 5 6 7 8 9

Number of Customer Arrivals

Pro

bab

ility

Poisson PDF for = 1.7 Poisson CDF for = 1.7

• The most likely event is 1 arrival (P(1)=.3106 or 31.1% chance).

• This will help the credit union schedule tellers.

Clickers

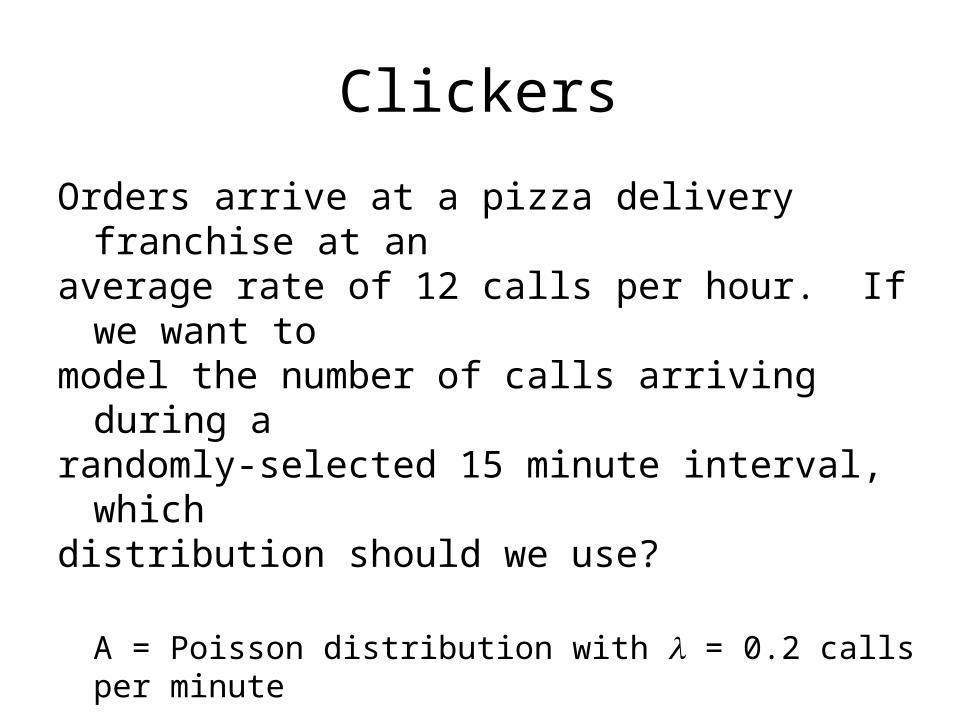

Orders arrive at a pizza delivery franchise at an average rate of 12 calls per hour. If we want to model the number of calls arriving during a randomly-selected 15 minute interval, which distribution should we use?

A = Poisson distribution with = 0.2 calls per minute

B = Poisson distribution with = 0.8 calls per 15 minutes

C = Poisson distribution with = 3 calls per 15 min.

D = Poisson distribution with = 12 calls per hour

Clickers

Orders arrive at a pizza delivery franchise at an average rate of 12 calls per hour. What are the mean and standard deviation of the number of calls arriving during a randomly-selected 15 minute interval?

A = = 3 and = 1.73

B = = 3 and = 3

C = = 12 and = 3.46

D = = 12 and = 12

Clickers

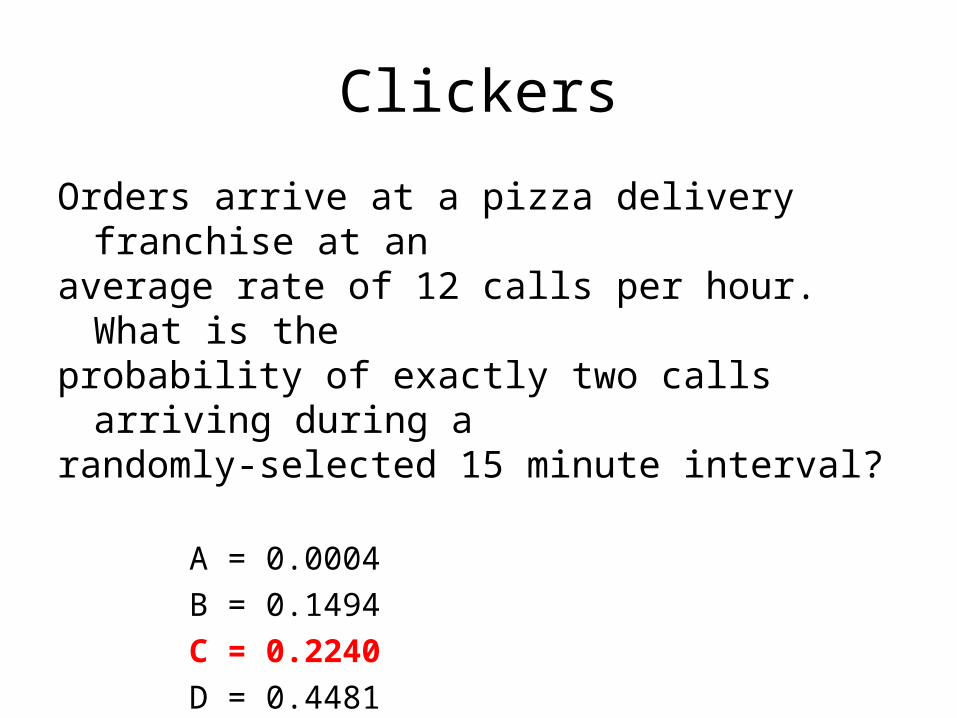

Orders arrive at a pizza delivery franchise at an average rate of 12 calls per hour. What is the probability of exactly two calls arriving during a randomly-selected 15 minute interval?

A = 0.0004

B = 0.1494

C = 0.2240

D = 0.4481

Chapter 6 – Poisson Distribution

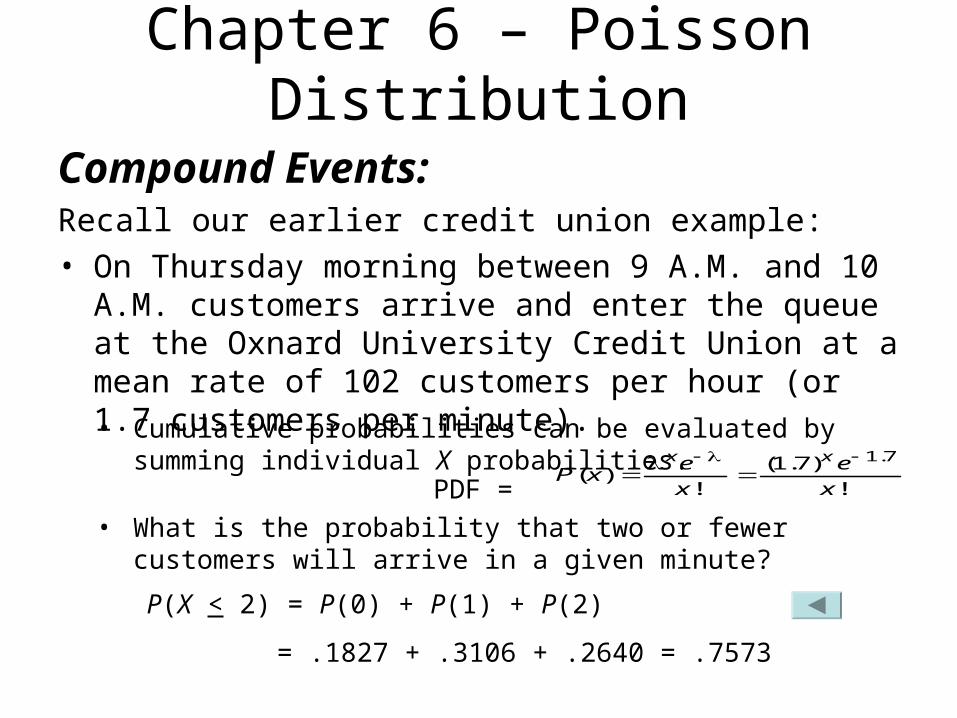

Compound Events: Recall our earlier credit union example: • On Thursday morning between 9 A.M. and 10 A.M.

customers arrive and enter the queue at the Oxnard University Credit Union at a mean rate of 102 customers per hour (or 1.7 customers per minute). • Cumulative probabilities can be evaluated by summing

individual X probabilities.

• What is the probability that two or fewer customers will arrive in a given minute?

= .1827 + .3106 + .2640 = .7573

P(X < 2) = P(0) + P(1) + P(2)

PDF =

1.7(1.7)( )

! !

x xe eP x

x x

Chapter 6 – Poisson Distribution

Compound Events:

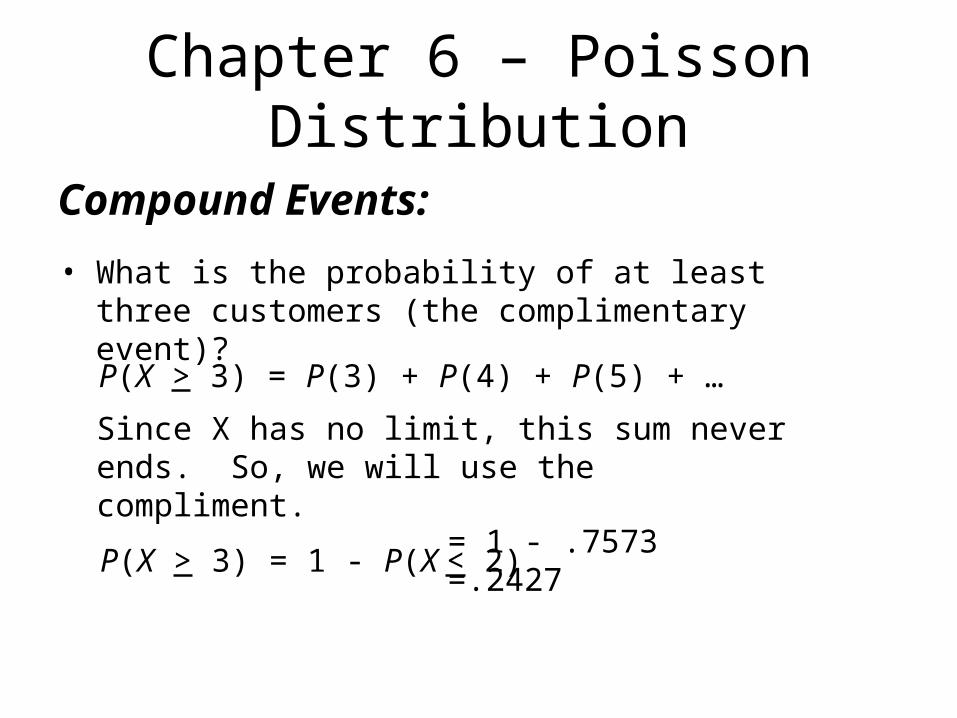

• What is the probability of at least three customers (the complimentary event)?

= 1 - .7573 =.2427 P(X > 3) = 1 - P(X < 2)

P(X > 3) = P(3) + P(4) + P(5) + …

Since X has no limit, this sum never ends. So, we will use the compliment.

Clickers

Orders arrive at a pizza delivery franchise at an average rate of 12 calls per hour. What is the probability that more than two calls arrive during a randomly-selected 15 minute interval?

A = 0.0498

B = 0.1494

C = 0.2240

D = 0.4232

E = 0.5768

Chapter 6 – Poisson Distribution

Recognizing Poisson Applications:• Can you recognize a Poisson situation?

• Look for arrivals of “rare” independent events with no obvious upper limit.

• In the last week, how many credit card applications did you receive by mail?

• In the last week, how many checks did you write?

• In the last week, how many e-mail viruses did your firewall detect?

Chapter 6 – Linear Transformations

Linear Transformations:• A linear transformation of a random variable X is

performed by adding a constant or multiplying by a constant.

Rule 1: aX+b = aX + b (mean of a transformed variable)Rule 2: aX+b = |a|X (standard deviation of a transformed variable)

• For example, consider defining a random variable Y in terms of the random variable X as follows:

baXY Where a and b are any two constants.

Chapter 6 – Linear Transformations

Example: Total Cost• The total cost of many goods is often modeled as a

function of the good produced, Q (a random variable).

Fv QC

Specifically, if there is a variable cost per unit v and a fixed cost F, then the total cost of the good, C, is given by …

where v and F are constant values.

For given values of Q, Q, v, and F, we can determine the mean and standard deviation of the total cost…

QC v

FvQC

ClickersIf Q is a random variable with mean Q = 500 units and standard deviation Q = 40 units, the variable cost is v = $35 per unit, and the fixed cost is F = $24,000, the mean of the total cost is

Determine the standard deviation of the total cost.

A) C = $35

B) C = $40

C) C = $1,400

D) C = $25,400

500,41$24000)50035( Fv QC

Recommended