© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013

BAUER AG

Group Presentation

First quarter 2013

Bauma 2013 – Munich, Germany

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 2

Total Group revenues

1,600

1,200

800

400

0

Orders in hand

800

600

400

200

0

Net profit

60

45

30

15

0

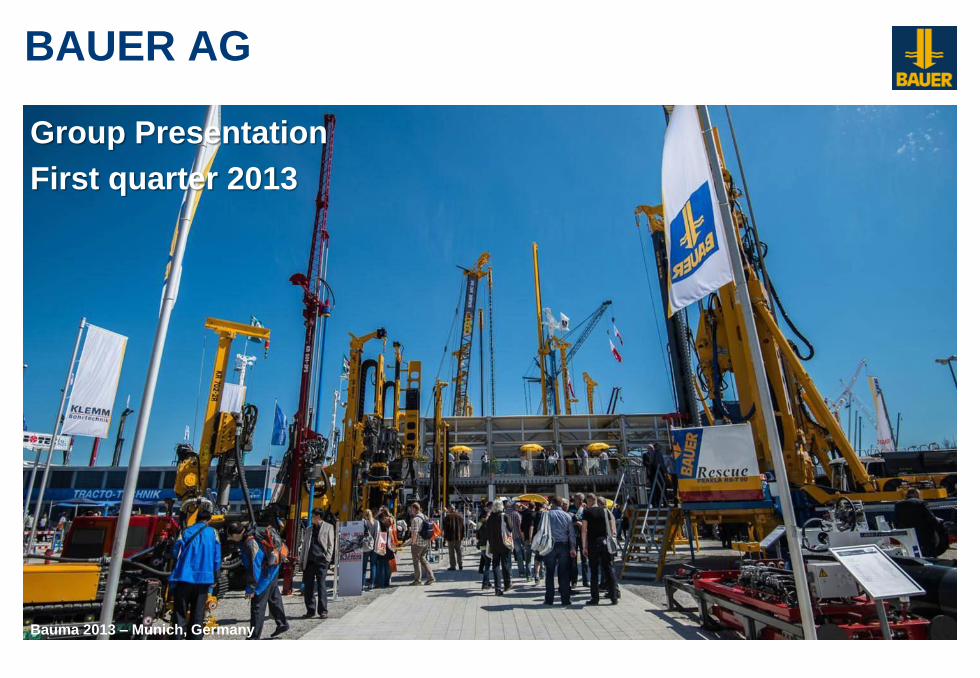

Key Figures FY 2012

Employees

12,000

9,000

6,000

3,000

0

in EUR million in EUR million

in EUR million in average

1,276 1,304 1,372

2009 2010 2011 2012

1,446 42.0 39.8 34.1

2009 2010 2011 2012*

25.8

2009 2010 2011 2012

508.9 614.9 750.0 785.0

2009 2010 2011 2012

8,872 9,094 9,646 10,253

*adjusted because of IAS 19 R

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 3

Mission & Strategy

Services, equipment & products dealing with ground

and groundwater

Our mission

Our strategy

The world is our market.

World market leadership for foundation technology.

Powerful development of drilling applications and related

services for resources, water and energy markets.

Optimizing worldwide organizational networks and self

controlling structures for the Group.

Growth 5 to 10 % per year.

BG 42 PremiumLine – Munich, Germany

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 4

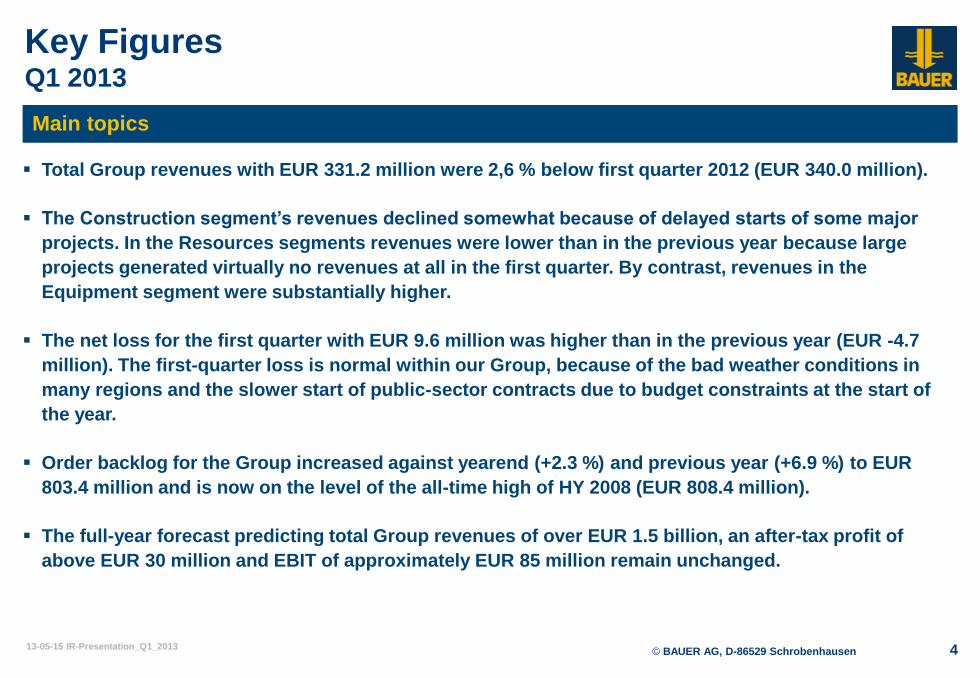

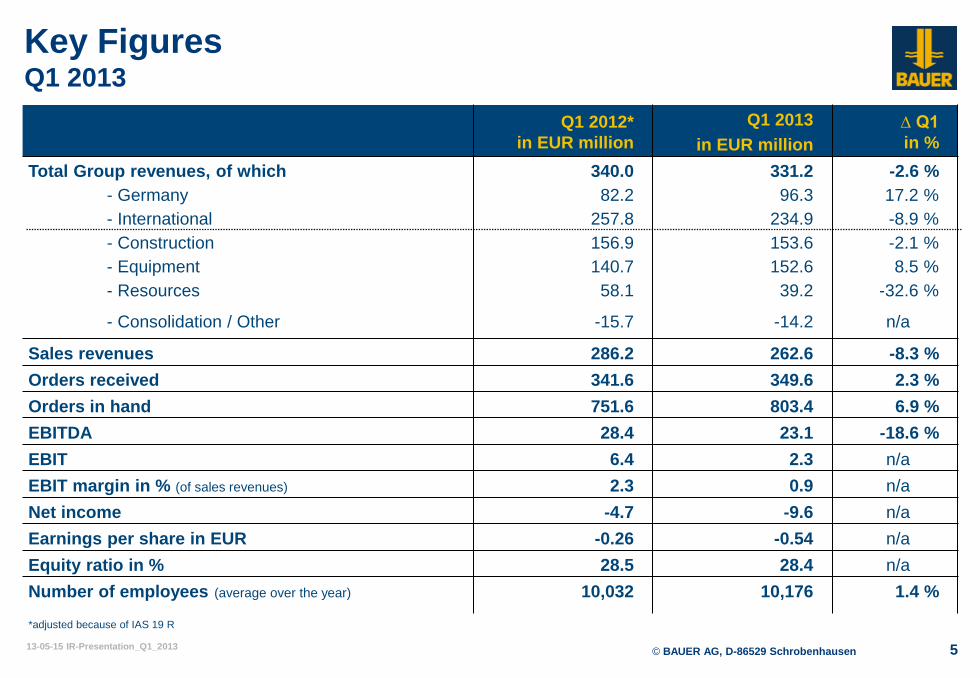

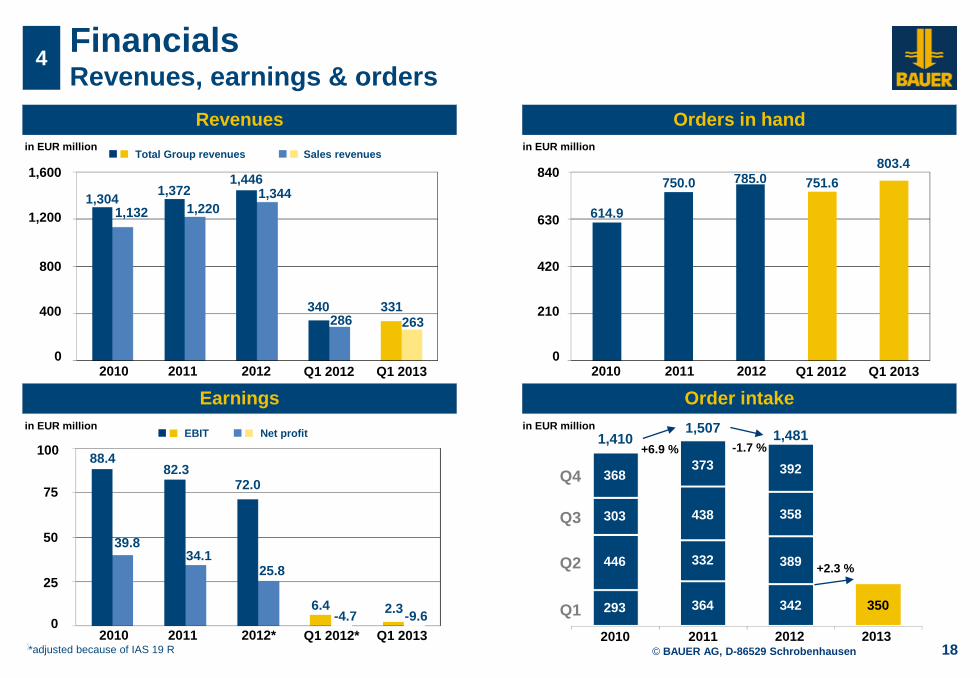

Total Group revenues with EUR 331.2 million were 2,6 % below first quarter 2012 (EUR 340.0 million).

The Construction segment’s revenues declined somewhat because of delayed starts of some major

projects. In the Resources segments revenues were lower than in the previous year because large

projects generated virtually no revenues at all in the first quarter. By contrast, revenues in the

Equipment segment were substantially higher.

The net loss for the first quarter with EUR 9.6 million was higher than in the previous year (EUR -4.7

million). The first-quarter loss is normal within our Group, because of the bad weather conditions in

many regions and the slower start of public-sector contracts due to budget constraints at the start of

the year.

Order backlog for the Group increased against yearend (+2.3 %) and previous year (+6.9 %) to EUR

803.4 million and is now on the level of the all-time high of HY 2008 (EUR 808.4 million).

The full-year forecast predicting total Group revenues of over EUR 1.5 billion, an after-tax profit of

above EUR 30 million and EBIT of approximately EUR 85 million remain unchanged.

Main topics

Key Figures Q1 2013

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 5

Key Figures Q1 2013

Q1 2012*

in EUR million

Q1 2013

in EUR million

∆ Q1

in %

Total Group revenues, of which

- Germany

- International

- Construction

- Equipment

- Resources

- Consolidation / Other

340.0

82.2

257.8

156.9

140.7

58.1

-15.7

331.2

96.3

234.9

153.6

152.6

39.2

-14.2

-2.6 %

17.2 %

-8.9 %

-2.1 %

8.5 %

-32.6 %

n/a

Sales revenues 286.2 262.6 -8.3 %

Orders received 341.6 349.6 2.3 %

Orders in hand 751.6 803.4 6.9 %

EBITDA 28.4 23.1 -18.6 %

EBIT 6.4 2.3 n/a

EBIT margin in % (of sales revenues) 2.3 0.9 n/a

Net income -4.7 -9.6 n/a

Earnings per share in EUR -0.26 -0.54 n/a

Equity ratio in % 28.5 28.4 n/a

Number of employees (average over the year) 10,032 10,176 1.4 %

*adjusted because of IAS 19 R

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 6

Contents

Regional breakdown of revenues 3

Financials 4

Overview BAUER Group 1

BAUER market environment 2

p. 7

p. 14

p. 16

p. 18

5 Guidance 2013

6 Appendix

p. 25

p. 26

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 7

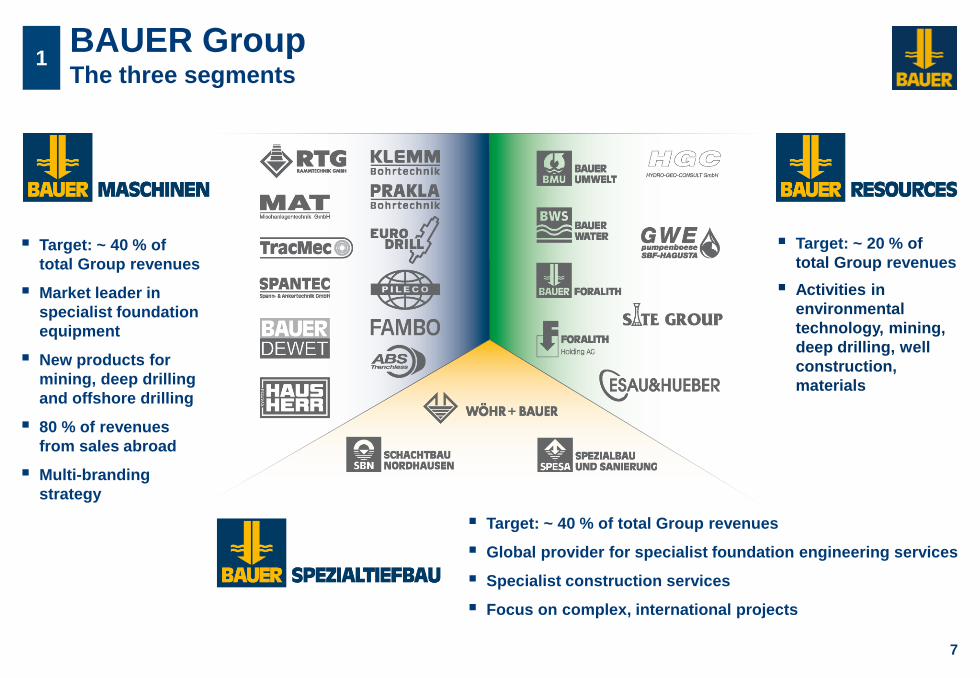

1 BAUER Group The three segments

Target: ~ 40 % of

total Group revenues

Market leader in

specialist foundation

equipment

New products for

mining, deep drilling

and offshore drilling

80 % of revenues

from sales abroad

Multi-branding

strategy

Target: ~ 40 % of total Group revenues

Global provider for specialist foundation engineering services

Specialist construction services

Focus on complex, international projects

Target: ~ 20 % of

total Group revenues

Activities in

environmental

technology, mining,

deep drilling, well

construction,

materials

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 8

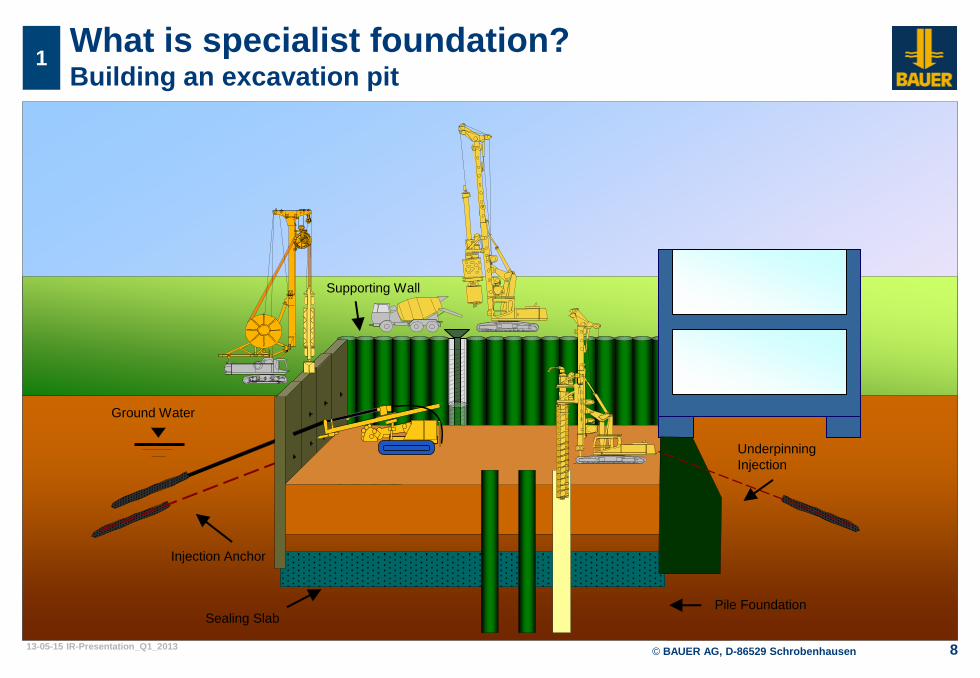

What is specialist foundation? Building an excavation pit

1

Ground Water

Injection Anchor

Sealing Slab

Supporting Wall

Underpinning

Injection

Pile Foundation

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 9

What is specialist foundation used for? Applications for projects

1

Foundations Cut-off walls Excavation pits

Buildings Infrastructure Water – Energy Industry

Ground improvement

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 10

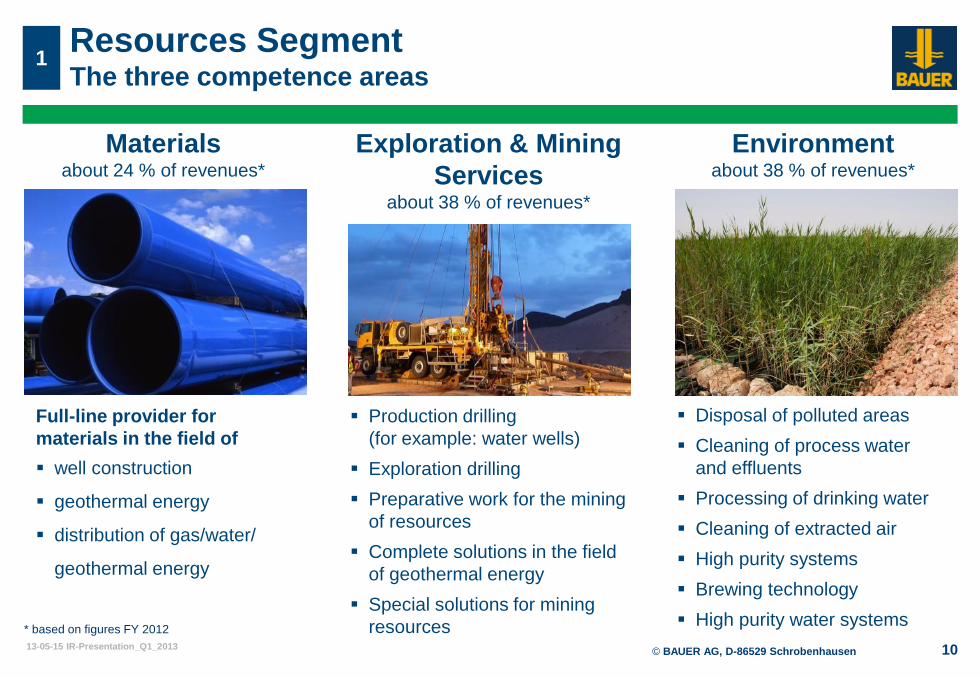

Resources Segment The three competence areas

1

Environment about 38 % of revenues*

Exploration & Mining

Services about 38 % of revenues*

Materials about 24 % of revenues*

Full-line provider for

materials in the field of

well construction

geothermal energy

distribution of gas/water/

geothermal energy

Production drilling

(for example: water wells)

Exploration drilling

Preparative work for the mining

of resources

Complete solutions in the field

of geothermal energy

Special solutions for mining

resources

Disposal of polluted areas

Cleaning of process water

and effluents

Processing of drinking water

Cleaning of extracted air

High purity systems

Brewing technology

High purity water systems * based on figures FY 2012

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013

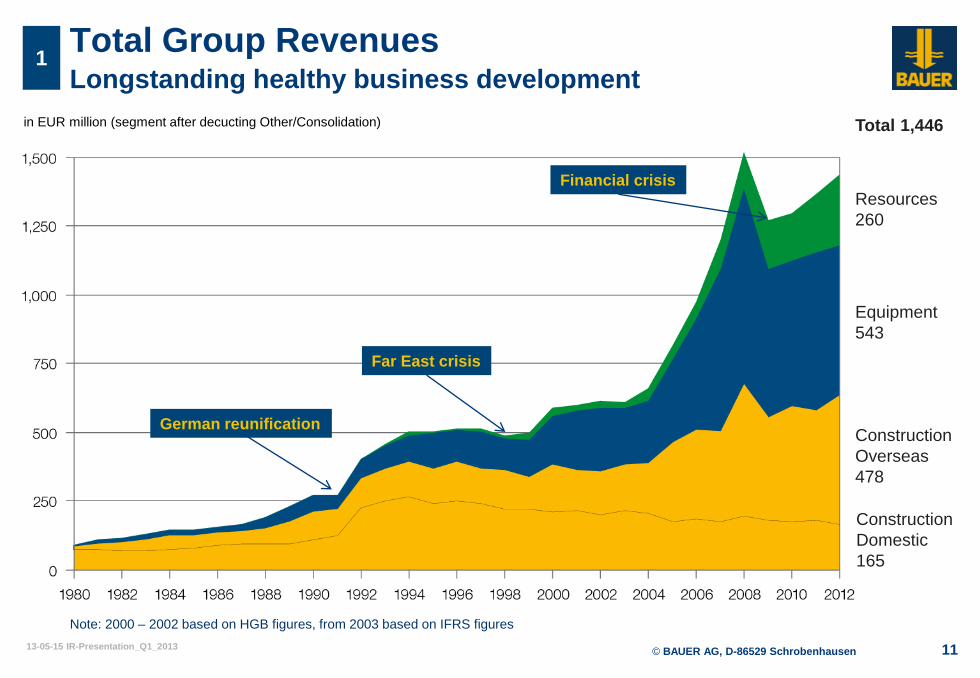

in EUR million (segment after decucting Other/Consolidation)

11

1

Note: 2000 – 2002 based on HGB figures, from 2003 based on IFRS figures

Resources

260

Equipment

543

Construction

Overseas

478

Total 1,446

Construction

Domestic

165

Total Group Revenues Longstanding healthy business development

German reunification

Far East crisis

Financial crisis

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 12

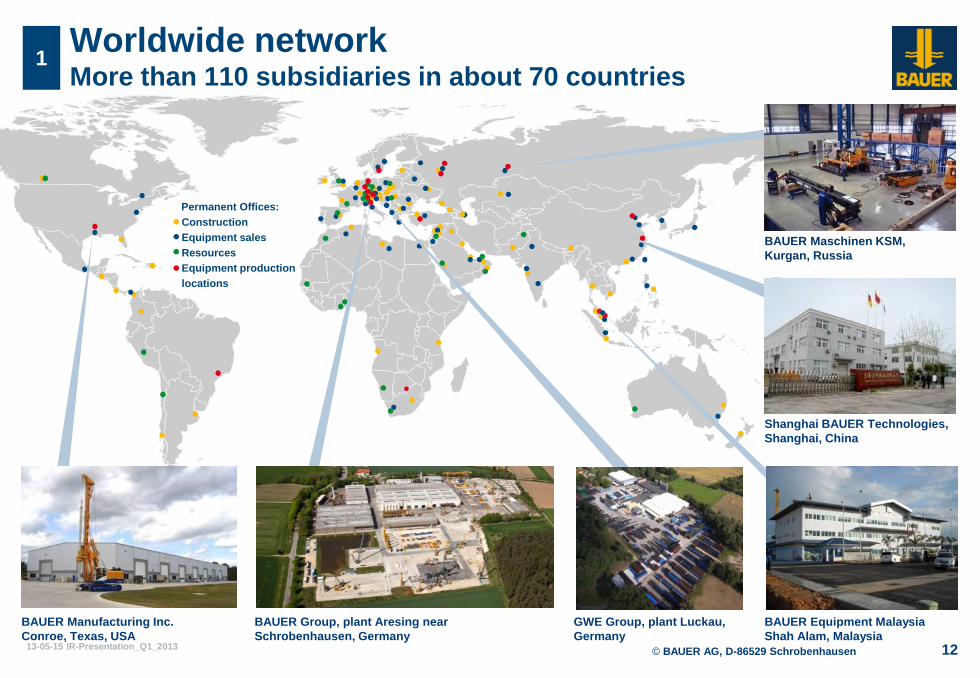

Worldwide network More than 110 subsidiaries in about 70 countries

1

BAUER Manufacturing Inc.

Conroe, Texas, USA

GWE Group, plant Luckau,

Germany

BAUER Maschinen KSM,

Kurgan, Russia

BAUER Equipment Malaysia

Shah Alam, Malaysia

Shanghai BAUER Technologies,

Shanghai, China

BAUER Group, plant Aresing near

Schrobenhausen, Germany

Permanent Offices:

Construction

Equipment sales

Resources

Equipment production

locations

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 13

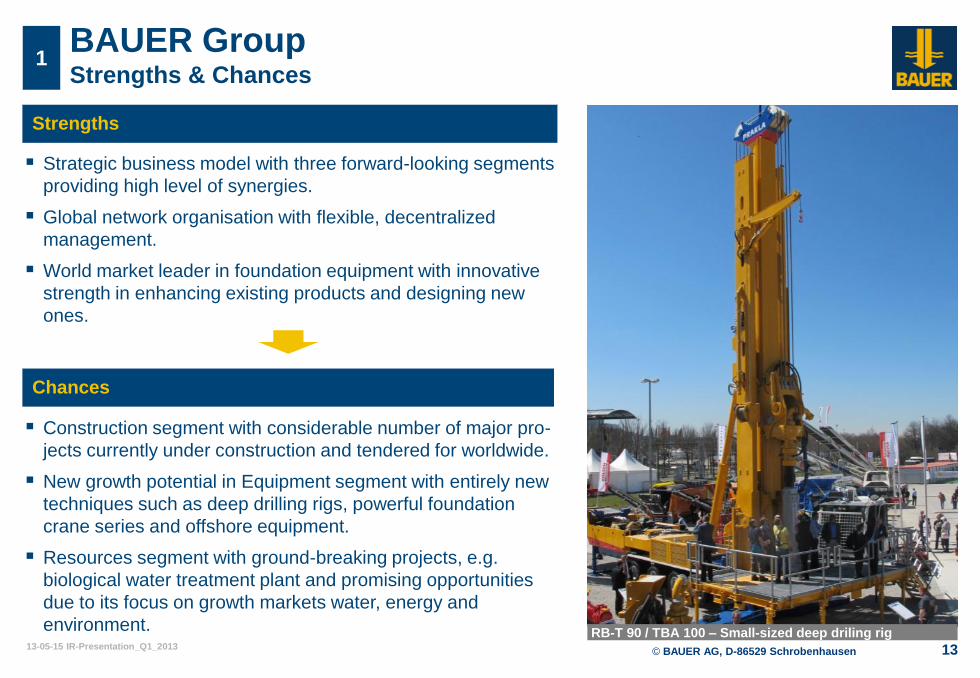

1 BAUER Group Strengths & Chances

Strategic business model with three forward-looking segments

providing high level of synergies.

Global network organisation with flexible, decentralized

management.

World market leader in foundation equipment with innovative

strength in enhancing existing products and designing new

ones.

Strengths

Chances

Construction segment with considerable number of major pro-

jects currently under construction and tendered for worldwide.

New growth potential in Equipment segment with entirely new

techniques such as deep drilling rigs, powerful foundation

crane series and offshore equipment.

Resources segment with ground-breaking projects, e.g.

biological water treatment plant and promising opportunities

due to its focus on growth markets water, energy and

environment. RB-T 90 / TBA 100 – Small-sized deep driling rig

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013

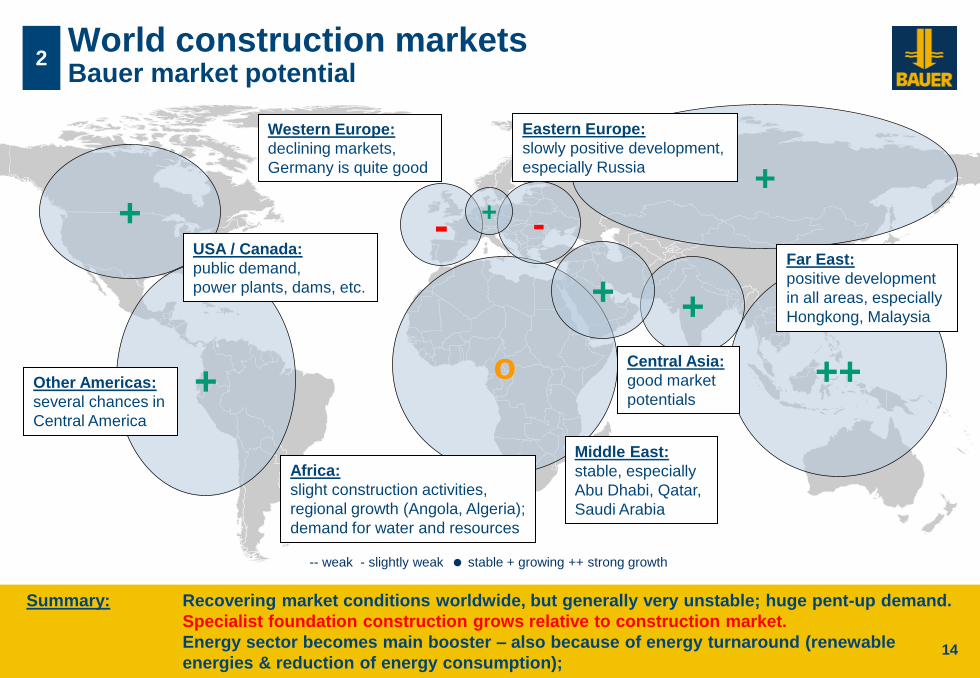

+

World construction markets Bauer market potential

2

14

-

Western Europe:

declining markets,

Germany is quite good +

+

++

Far East:

positive development

in all areas, especially

Hongkong, Malaysia

+ Other Americas:

several chances in

Central America

o

Africa:

slight construction activities,

regional growth (Angola, Algeria);

demand for water and resources

Summary: Recovering market conditions worldwide, but generally very unstable; huge pent-up demand.

Specialist foundation construction grows relative to construction market.

Energy sector becomes main booster – also because of energy turnaround (renewable

energies & reduction of energy consumption);

Middle East:

stable, especially

Abu Dhabi, Qatar,

Saudi Arabia

Eastern Europe:

slowly positive development,

especially Russia

Central Asia:

good market

potentials

USA / Canada:

public demand,

power plants, dams, etc.

14

-- weak - slightly weak stable + growing ++ strong growth

-

+

+

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 15

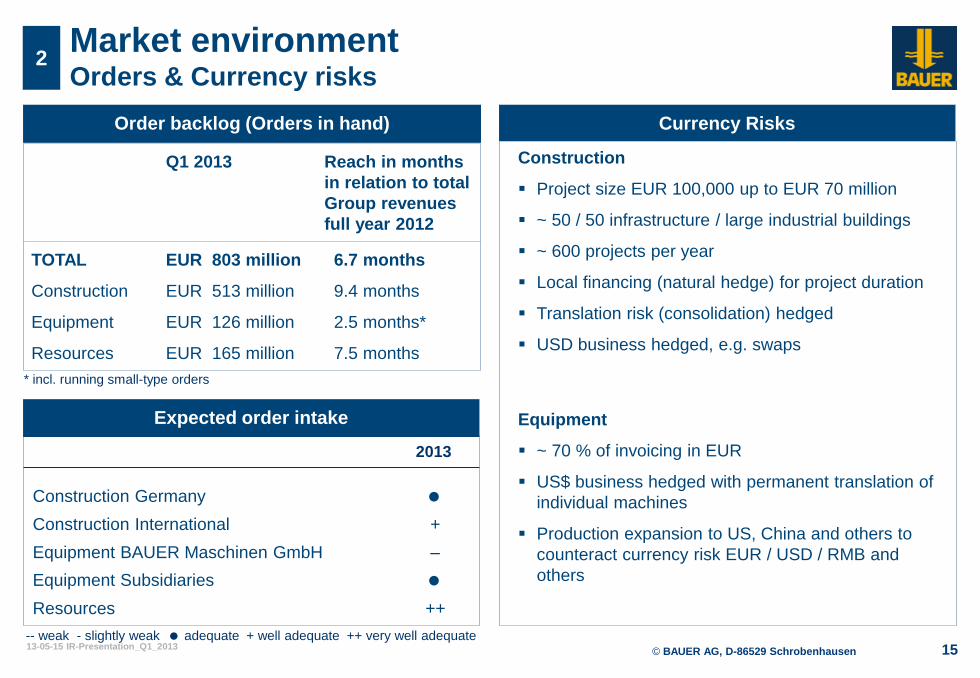

Market environment Orders & Currency risks

2

Order backlog (Orders in hand) Currency Risks

Expected order intake

2013

Construction Germany

Construction International +

Equipment BAUER Maschinen GmbH –

Equipment Subsidiaries

Resources ++

-- weak - slightly weak adequate + well adequate ++ very well adequate

Q1 2013 Reach in months

in relation to total

Group revenues

full year 2012

TOTAL

Construction

Equipment

Resources

EUR 803 million

EUR 513 million

EUR 126 million

EUR 165 million

6.7 months

9.4 months

2.5 months*

7.5 months

* incl. running small-type orders

Construction

Project size EUR 100,000 up to EUR 70 million

~ 50 / 50 infrastructure / large industrial buildings

~ 600 projects per year

Local financing (natural hedge) for project duration

Translation risk (consolidation) hedged

USD business hedged, e.g. swaps

Equipment

~ 70 % of invoicing in EUR

US$ business hedged with permanent translation of

individual machines

Production expansion to US, China and others to

counteract currency risk EUR / USD / RMB and

others

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 16

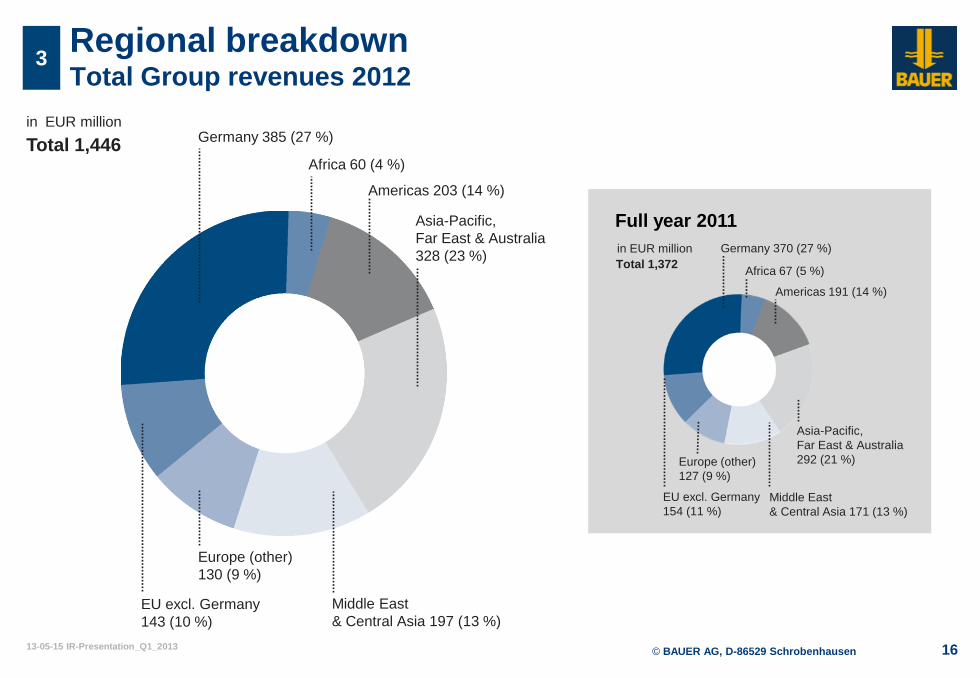

3 Regional breakdown Total Group revenues 2012

in EUR million

Total 1,446

in EUR million

Africa 67 (5 %)

Americas 191 (14 %)

Asia-Pacific,

Far East & Australia

292 (21 %)

Middle East

& Central Asia 171 (13 %)

Germany 370 (27 %)

EU excl. Germany

154 (11 %)

Europe (other)

127 (9 %)

Total 1,372

Full year 2011

Africa 60 (4 %)

Americas 203 (14 %)

Asia-Pacific,

Far East & Australia

328 (23 %)

Middle East

& Central Asia 197 (13 %)

Germany 385 (27 %)

EU excl. Germany

143 (10 %)

Europe (other)

130 (9 %)

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 17

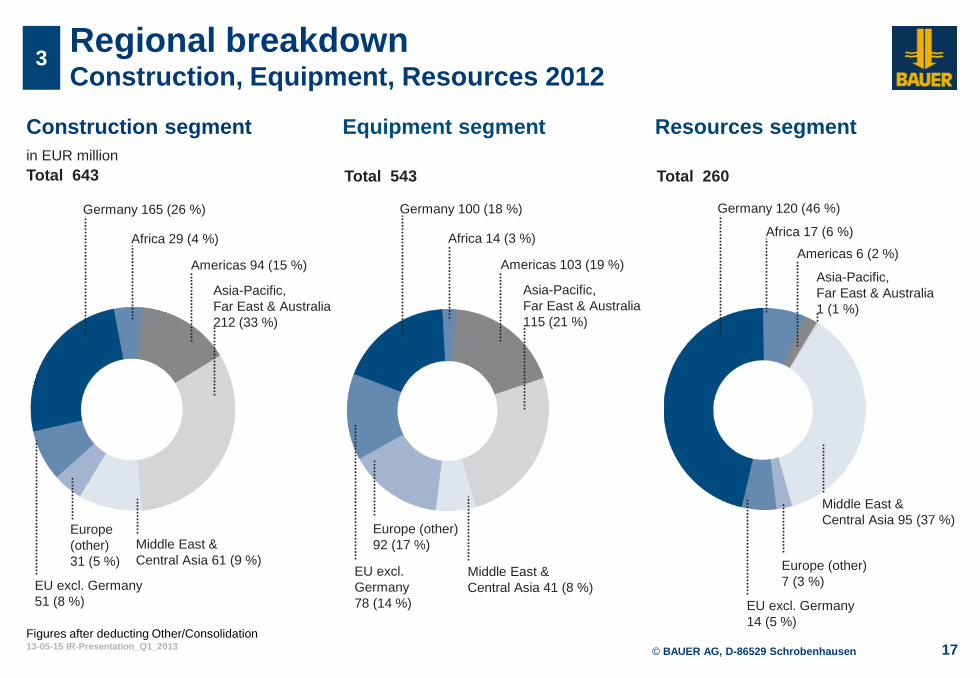

3 Regional breakdown Construction, Equipment, Resources 2012

Figures after deducting Other/Consolidation

in EUR million

Total 643 Total 543 Total 260

Construction segment Equipment segment Resources segment

Africa 29 (4 %)

Americas 94 (15 %)

Asia-Pacific,

Far East & Australia

212 (33 %)

Middle East &

Central Asia 61 (9 %)

Germany 165 (26 %)

EU excl. Germany

51 (8 %)

Europe

(other)

31 (5 %)

Africa 14 (3 %)

Americas 103 (19 %)

Asia-Pacific,

Far East & Australia

115 (21 %)

Middle East &

Central Asia 41 (8 %)

Germany 100 (18 %)

EU excl.

Germany

78 (14 %)

Europe (other)

92 (17 %)

Africa 17 (6 %)

Americas 6 (2 %)

Asia-Pacific,

Far East & Australia

1 (1 %)

Middle East &

Central Asia 95 (37 %)

Germany 120 (46 %)

EU excl. Germany

14 (5 %)

Europe (other)

7 (3 %)

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 18

Revenues

Earnings

Financials Revenues, earnings & orders

4

2012 Q1 2012

1,600

1,200

800

400

0

1,304 1,132

100

75

50

25

0

88.4

39.8

Orders in hand

840

630

420

210

0

614.9

Order intake

2012 2013

303

446

293

2011

2011

2010

2010

368

1,410

1,372

1,220

750.0

82.3

34.1

364

332

438

373

1,507

+6.9 %

Q1

Q2

Q3

Q4

1,446 1,344

Q1 2013

2012* Q1 2012* 2011 2010 Q1 2013

72.0

25.8

2012 Q1 2012 2011 2010 Q1 2013

785.0 751.6

350

Total Group revenues Sales revenues

EBIT Net profit

in EUR million

in EUR million in EUR million

in EUR million

340 286

331 263

803.4

6.4 -4.7

2.3 -9.6

342

389

358

392

1,481 -1.7 %

+2.3 %

*adjusted because of IAS 19 R

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 19

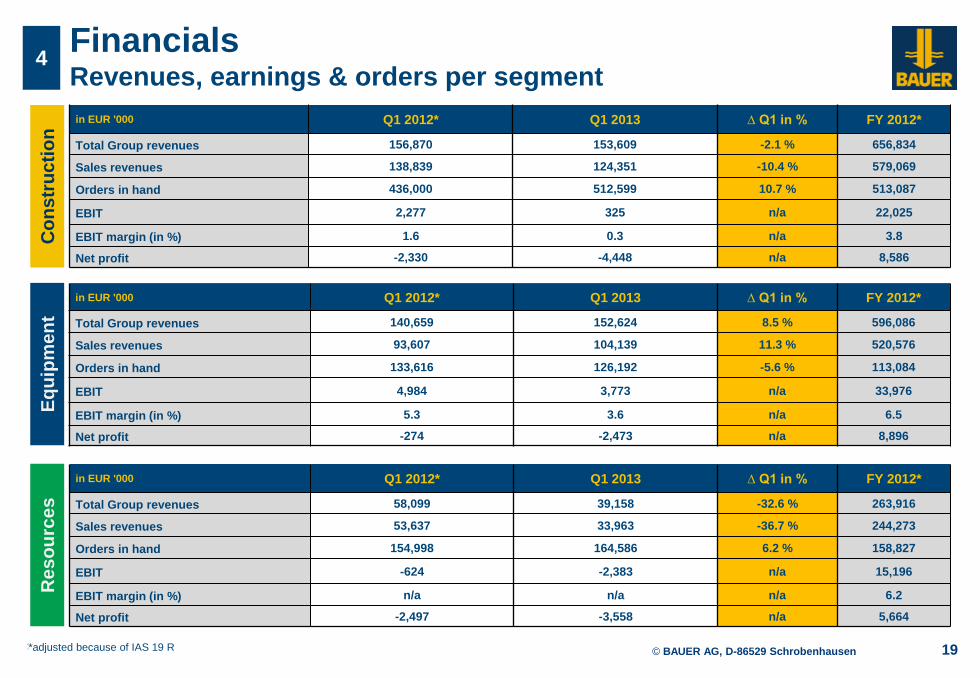

Financials Revenues, earnings & orders per segment

4 C

on

str

uc

tio

n

Eq

uip

me

nt

in EUR '000 Q1 2012* Q1 2013 ∆ Q1 in % FY 2012*

Total Group revenues 140,659 152,624 8.5 % 596,086

Sales revenues 93,607 104,139 11.3 % 520,576

Orders in hand 133,616 126,192 -5.6 % 113,084

EBIT 4,984 3,773 n/a 33,976

EBIT margin (in %) 5.3 3.6 n/a 6.5

Net profit -274 -2,473 n/a 8,896

Re

so

urc

es

in EUR '000 Q1 2012* Q1 2013 ∆ Q1 in % FY 2012*

Total Group revenues 156,870 153,609 -2.1 % 656,834

Sales revenues 138,839 124,351 -10.4 % 579,069

Orders in hand 436,000 512,599 10.7 % 513,087

EBIT 2,277 325 n/a 22,025

EBIT margin (in %) 1.6 0.3 n/a 3.8

Net profit -2,330 -4,448 n/a 8,586

in EUR '000 Q1 2012* Q1 2013 ∆ Q1 in % FY 2012*

Total Group revenues 58,099 39,158 -32.6 % 263,916

Sales revenues 53,637 33,963 -36.7 % 244,273

Orders in hand 154,998 164,586 6.2 % 158,827

EBIT -624 -2,383 n/a 15,196

EBIT margin (in %) n/a n/a n/a 6.2

Net profit -2,497 -3,558 n/a 5,664

*adjusted because of IAS 19 R

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 20

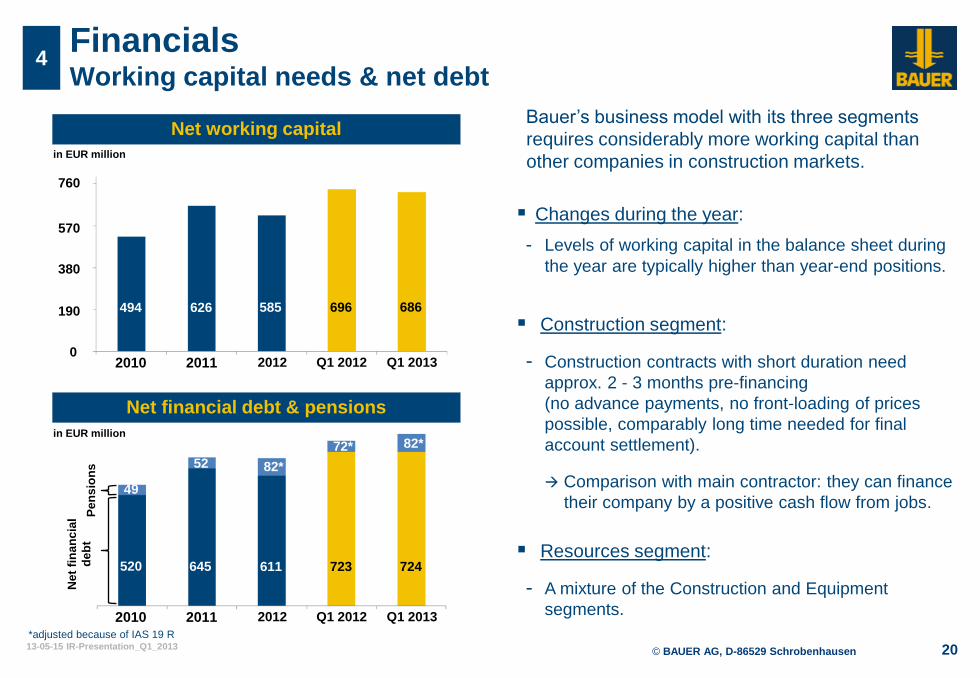

Financials Working capital needs & net debt

4

Net financial debt & pensions

Net

fin

an

cia

l

de

bt

Pe

ns

ion

s

520

49

Net working capital

2010 2011

494

760

570

380

190

0

626

645

52

2012 Q1 2012 Q1 2013

585 696

2010 2011 2012 Q1 2012 Q1 2013

82*

72*

611 723

Bauer’s business model with its three segments

requires considerably more working capital than

other companies in construction markets.

Changes during the year:

- Levels of working capital in the balance sheet during

the year are typically higher than year-end positions.

Construction segment:

- Construction contracts with short duration need

approx. 2 - 3 months pre-financing

(no advance payments, no front-loading of prices

possible, comparably long time needed for final

account settlement).

Comparison with main contractor: they can finance

their company by a positive cash flow from jobs.

Resources segment:

- A mixture of the Construction and Equipment

segments.

724

82*

*adjusted because of IAS 19 R

in EUR million

in EUR million

686

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 21

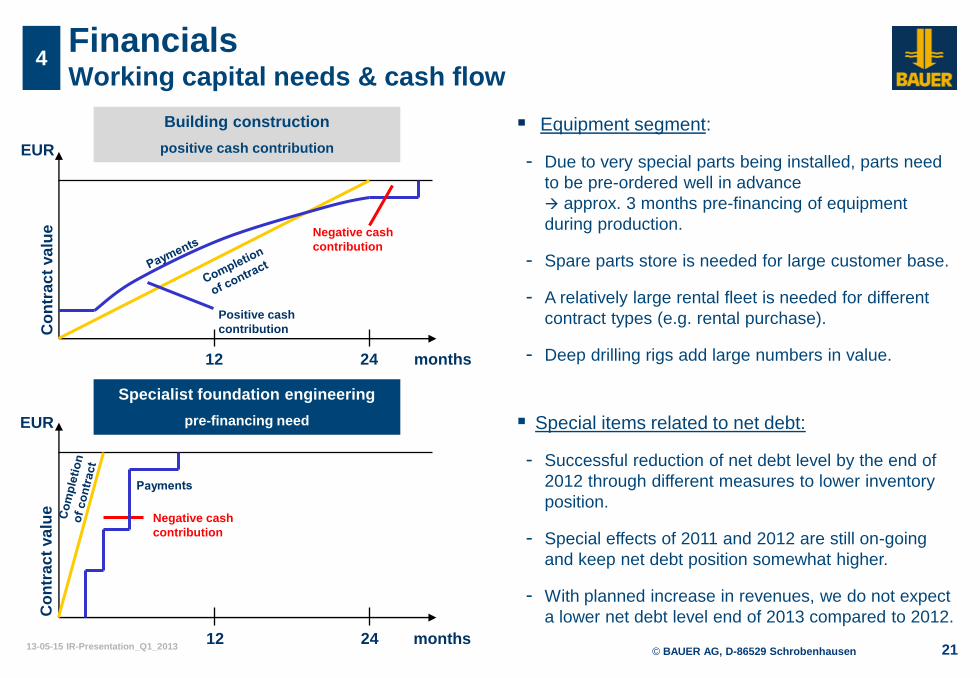

Building construction

positive cash contribution

Specialist foundation engineering

pre-financing need

Financials Working capital needs & cash flow

4

EUR

12 24 months

Positive cash

contribution

Negative cash

contribution

Co

ntr

ac

t va

lue

EUR

Negative cash

contribution

12 24 months

Co

ntr

ac

t va

lue

Equipment segment:

- Due to very special parts being installed, parts need

to be pre-ordered well in advance

approx. 3 months pre-financing of equipment

during production.

- Spare parts store is needed for large customer base.

- A relatively large rental fleet is needed for different

contract types (e.g. rental purchase).

- Deep drilling rigs add large numbers in value.

Special items related to net debt:

- Successful reduction of net debt level by the end of

2012 through different measures to lower inventory

position.

- Special effects of 2011 and 2012 are still on-going

and keep net debt position somewhat higher.

- With planned increase in revenues, we do not expect

a lower net debt level end of 2013 compared to 2012.

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 22

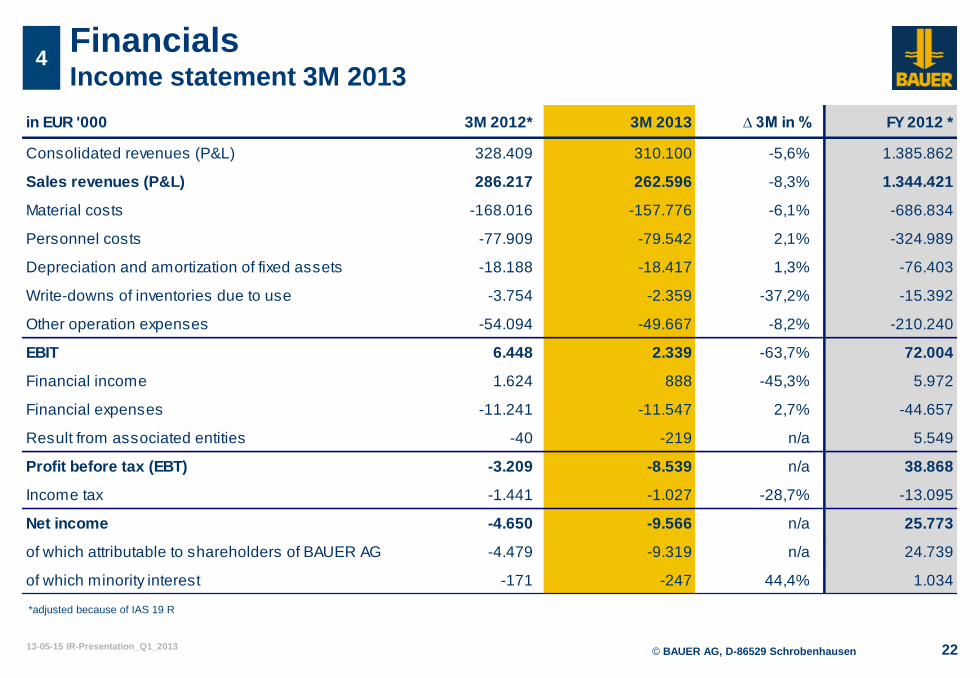

Financials Income statement 3M 2013

4

*adjusted because of IAS 19 R

in EUR '000 3M 2012* 3M 2013 ∆ 3M in % FY 2012 *

Consolidated revenues (P&L) 328.409 310.100 -5,6% 1.385.862

Sales revenues (P&L) 286.217 262.596 -8,3% 1.344.421

Material costs -168.016 -157.776 -6,1% -686.834

Personnel costs -77.909 -79.542 2,1% -324.989

Depreciation and amortization of fixed assets -18.188 -18.417 1,3% -76.403

Write-downs of inventories due to use -3.754 -2.359 -37,2% -15.392

Other operation expenses -54.094 -49.667 -8,2% -210.240

EBIT 6.448 2.339 -63,7% 72.004

Financial income 1.624 888 -45,3% 5.972

Financial expenses -11.241 -11.547 2,7% -44.657

Result from associated entities -40 -219 n/a 5.549

Profit before tax (EBT) -3.209 -8.539 n/a 38.868

Income tax -1.441 -1.027 -28,7% -13.095

Net income -4.650 -9.566 n/a 25.773

of which attributable to shareholders of BAUER AG -4.479 -9.319 n/a 24.739

of which minority interest -171 -247 44,4% 1.034

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 23

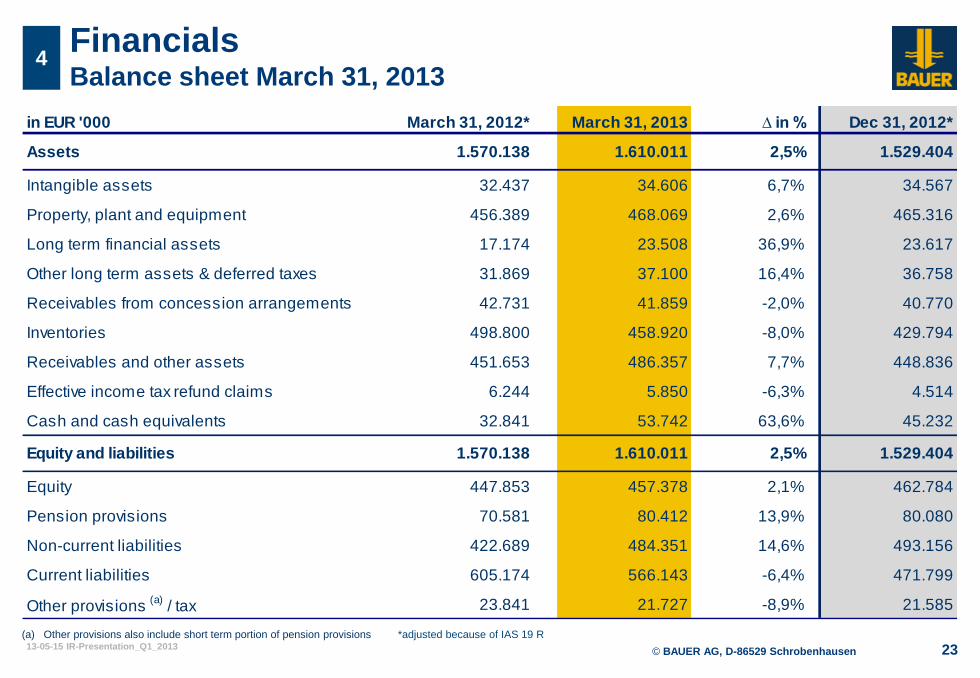

Financials Balance sheet March 31, 2013

4

(a) Other provisions also include short term portion of pension provisions *adjusted because of IAS 19 R

in EUR '000 March 31, 2012* March 31, 2013 ∆ in % Dec 31, 2012*

Assets 1.570.138 1.610.011 2,5% 1.529.404

Intangible assets 32.437 34.606 6,7% 34.567

Property, plant and equipment 456.389 468.069 2,6% 465.316

Long term financial assets 17.174 23.508 36,9% 23.617

Other long term assets & deferred taxes 31.869 37.100 16,4% 36.758

Receivables from concession arrangements 42.731 41.859 -2,0% 40.770

Inventories 498.800 458.920 -8,0% 429.794

Receivables and other assets 451.653 486.357 7,7% 448.836

Effective income tax refund claims 6.244 5.850 -6,3% 4.514

Cash and cash equivalents 32.841 53.742 63,6% 45.232

Equity and liabilities 1.570.138 1.610.011 2,5% 1.529.404

Equity 447.853 457.378 2,1% 462.784

Pension provisions 70.581 80.412 13,9% 80.080

Non-current liabilities 422.689 484.351 14,6% 493.156

Current liabilities 605.174 566.143 -6,4% 471.799

Other provisions (a)

/ tax 23.841 21.727 -8,9% 21.585

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 24

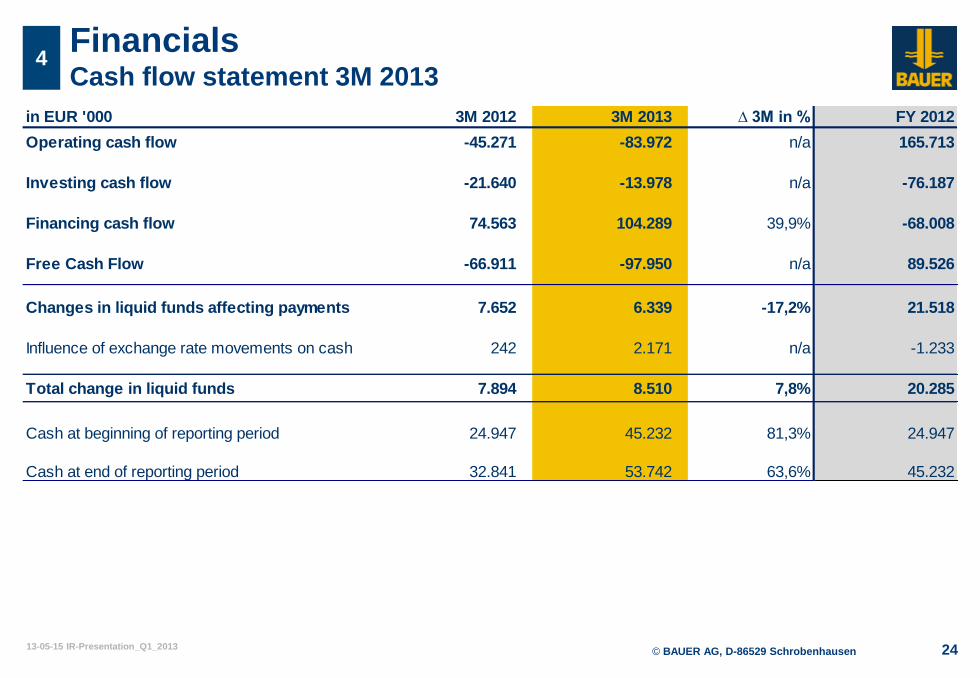

Financials Cash flow statement 3M 2013

4

in EUR '000 3M 2012 3M 2013 ∆ 3M in % FY 2012

Operating cash flow -45.271 -83.972 n/a 165.713

Investing cash flow -21.640 -13.978 n/a -76.187

Financing cash flow 74.563 104.289 39,9% -68.008

Free Cash Flow -66.911 -97.950 n/a 89.526

Changes in liquid funds affecting payments 7.652 6.339 -17,2% 21.518

Influence of exchange rate movements on cash 242 2.171 n/a -1.233

Total change in liquid funds 7.894 8.510 7,8% 20.285

Cash at beginning of reporting period 24.947 45.232 81,3% 24.947

Cash at end of reporting period 32.841 53.742 63,6% 45.232

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 25

Guidance 2013 Top-line growth with an increase in profitability

5

2012e* 2012 final 2013e

Total Group Revenues ~ 1,450 EUR million 1,446 EUR million > 1,500 EUR million

EBIT ~ 76 EUR million 71.4 EUR million ~ 85 EUR million

Net profit 25 - 30 EUR million 25.3 EUR million > 30 EUR million

Merdeka station – Kuala Lumpur, Malaysia In-house exhibition, Schrobenhausen Water treatment plant – Nimr, Oman

* Guidance published November 14, 2012

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 26

Appendix

Equipment programme C

Resources projects D

History of Bauer A

E Market environment Germany

F BAUER share

Construction projects B

p. 27

p. 29

p. 34

p. 38

p. 41

p. 42

G Key Figures Time Line p. 44

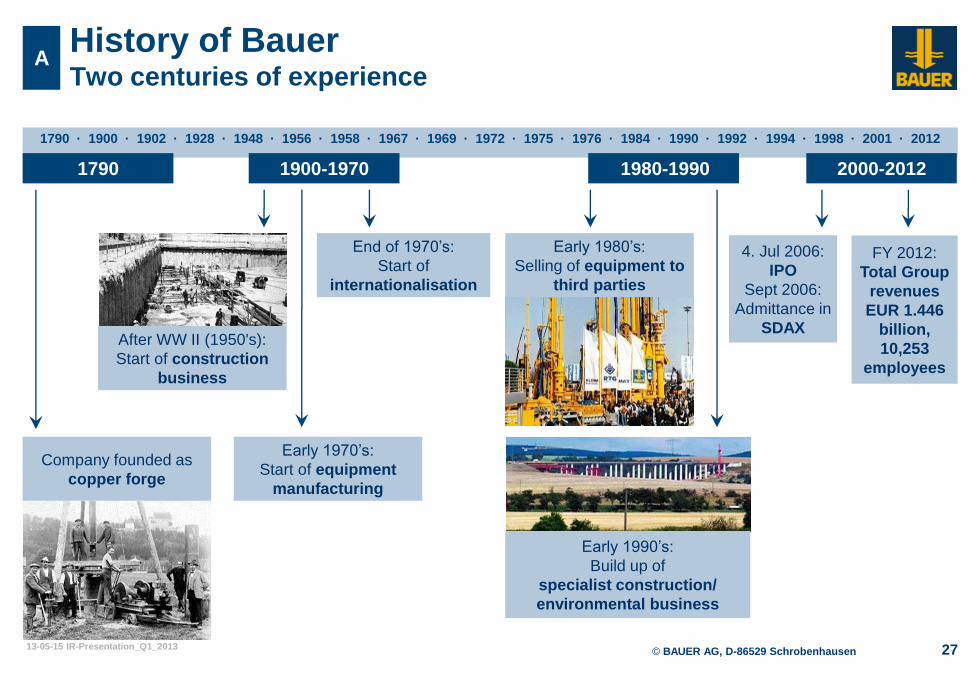

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 27

1790 · 1900 · 1902 · 1928 · 1948 · 1956 · 1958 · 1967 · 1969 · 1972 · 1975 · 1976 · 1984 · 1990 · 1992 · 1994 · 1998 · 2001 · 2012

History of Bauer Two centuries of experience

End of 1970’s:

Start of

internationalisation

Early 1990’s:

Build up of

specialist construction/

environmental business

FY 2012:

Total Group

revenues

EUR 1.446

billion,

10,253

employees

4. Jul 2006:

IPO

Sept 2006:

Admittance in

SDAX

A

Early 1970’s:

Start of equipment

manufacturing

Company founded as

copper forge

After WW II (1950's):

Start of construction

business

Early 1980’s:

Selling of equipment to

third parties

1790 1900-1970 1980-1990 2000-2012

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 28

A Bauer’s home base Headquarters and plant Schrobenhausen, Germany

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 29

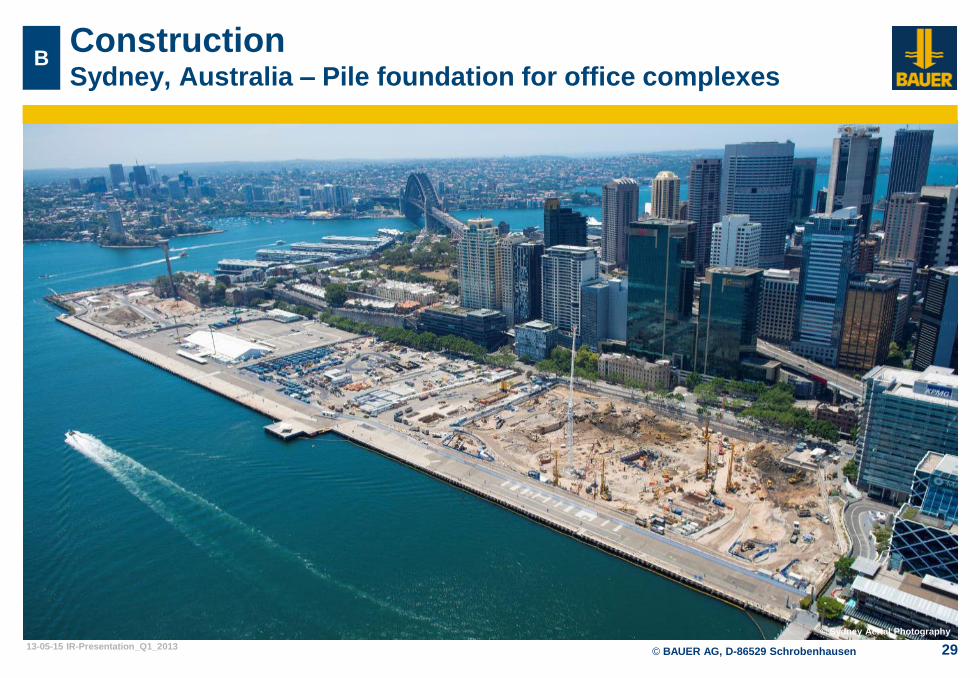

B Construction Sydney, Australia – Pile foundation for office complexes

© Sydney Aerial Photography

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 30

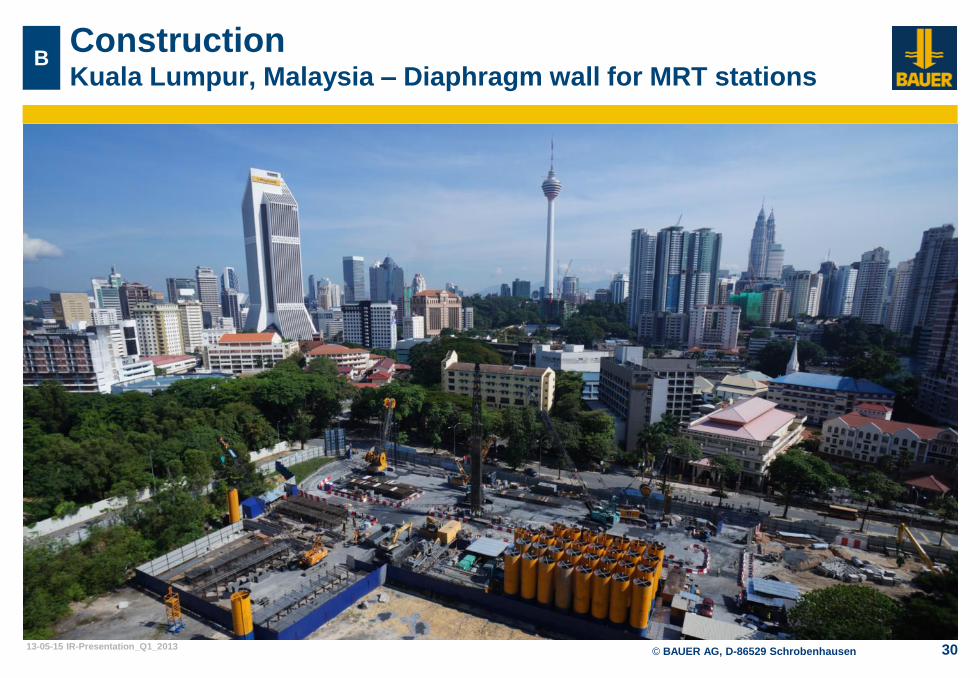

Construction Kuala Lumpur, Malaysia – Diaphragm wall for MRT stations

B

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 31

Construction Singapore – Foundation works for Market Street Tower

B

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 32

Construction Munich, Germany – Tunnel for Mittlerer Ring

B

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 33

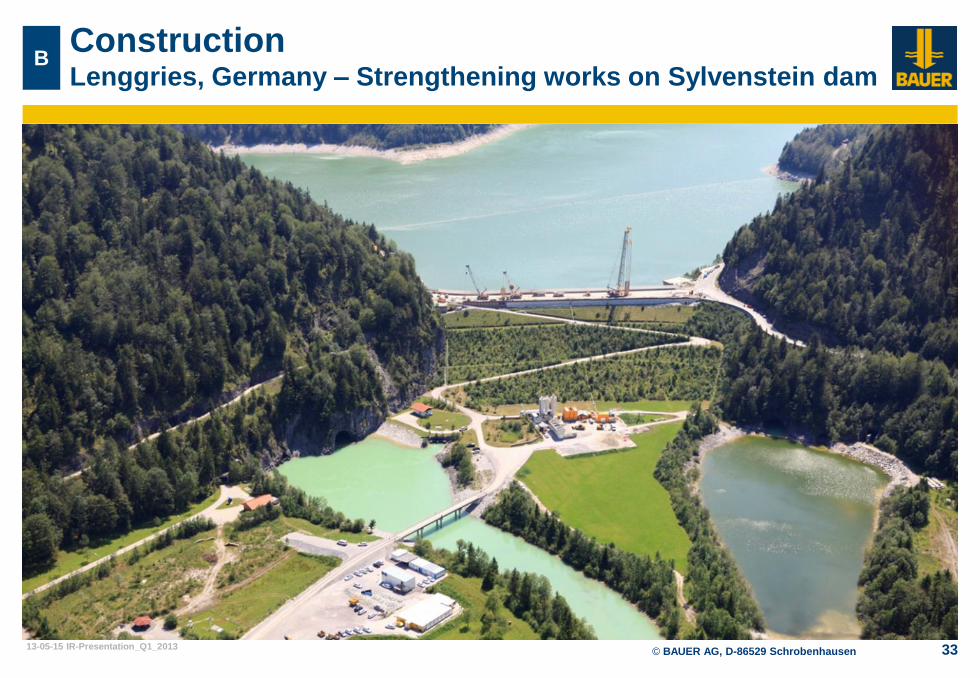

Construction Lenggries, Germany – Strengthening works on Sylvenstein dam

B

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 34

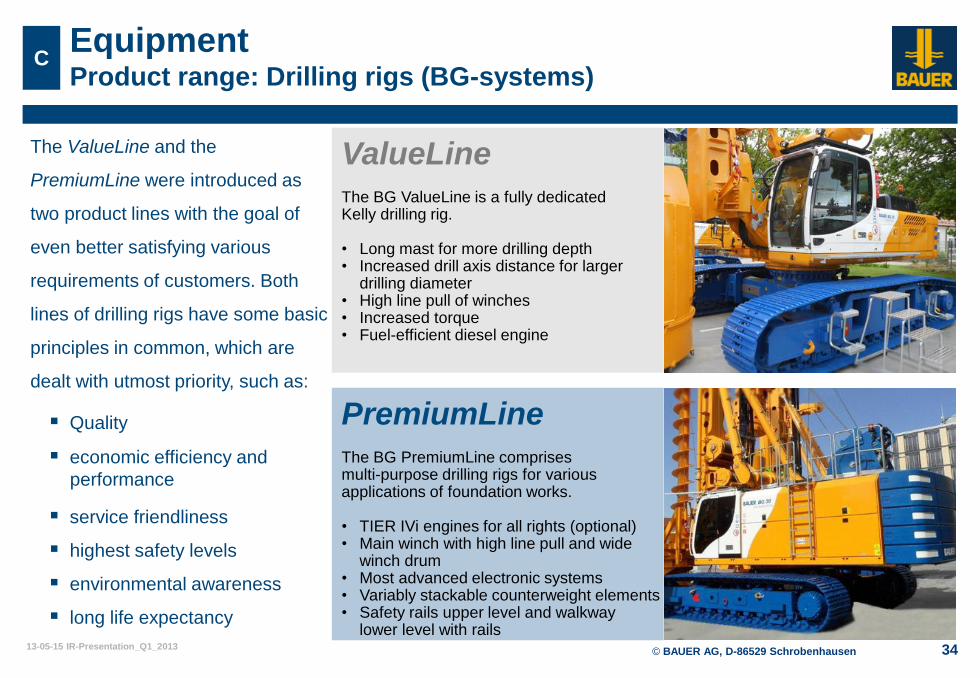

Equipment Product range: Drilling rigs (BG-systems)

C

ValueLine The BG ValueLine is a fully dedicated Kelly drilling rig. • Long mast for more drilling depth • Increased drill axis distance for larger

drilling diameter • High line pull of winches • Increased torque • Fuel-efficient diesel engine

PremiumLine The BG PremiumLine comprises multi-purpose drilling rigs for various applications of foundation works. • TIER IVi engines for all rights (optional) • Main winch with high line pull and wide

winch drum • Most advanced electronic systems • Variably stackable counterweight elements • Safety rails upper level and walkway

lower level with rails

The ValueLine and the

PremiumLine were introduced as

two product lines with the goal of

even better satisfying various

requirements of customers. Both

lines of drilling rigs have some basic

principles in common, which are

dealt with utmost priority, such as:

Quality

economic efficiency and

performance

service friendliness

highest safety levels

environmental awareness

long life expectancy

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 35

C Equipment Product range: Foundation Cranes

MC 128 MC 96 MC 32

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 36

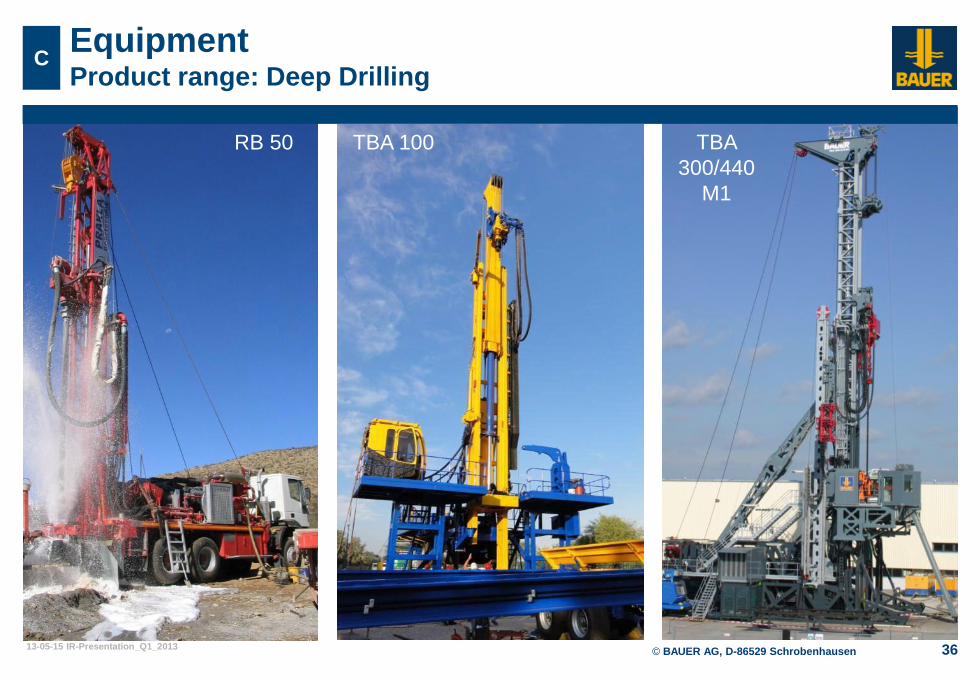

C Equipment Product range: Deep Drilling

RB 50 TBA 100 TBA

300/440

M1

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 37

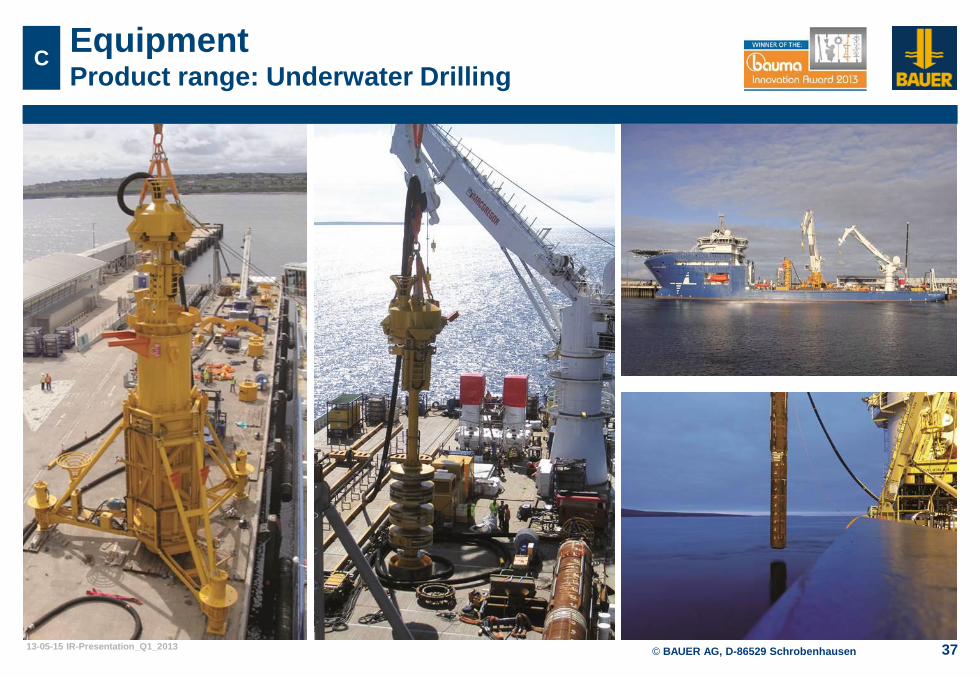

C Equipment Product range: Underwater Drilling

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 38

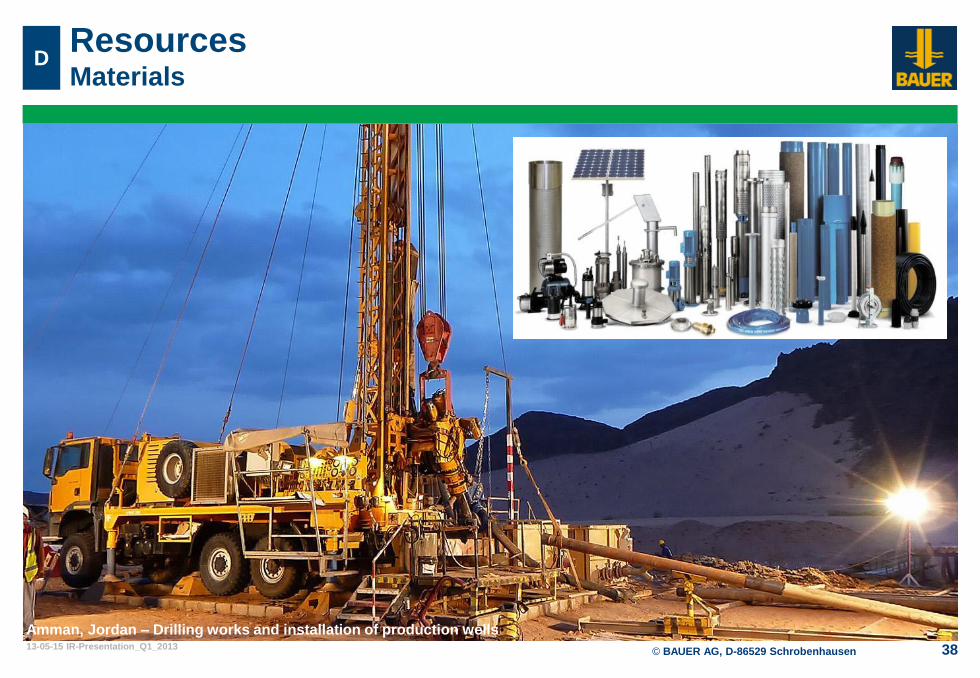

Resources Materials

D

Amman, Jordan – Drilling works and installation of production wells

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 39

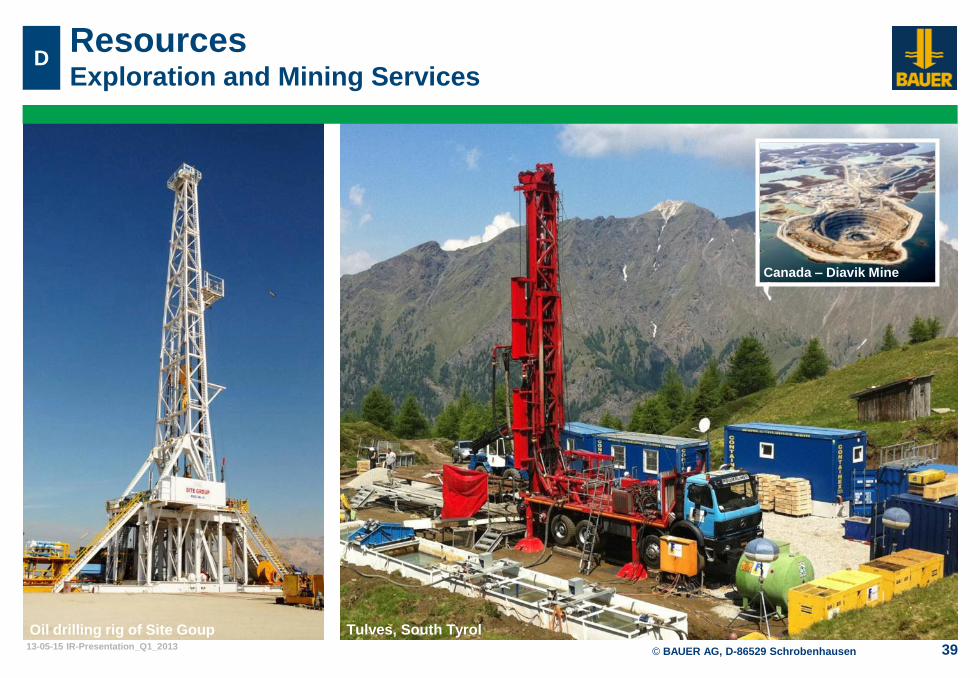

Resources Exploration and Mining Services

D

Oil drilling rig of Site Goup Tulves, South Tyrol

Canada – Diavik Mine

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 40

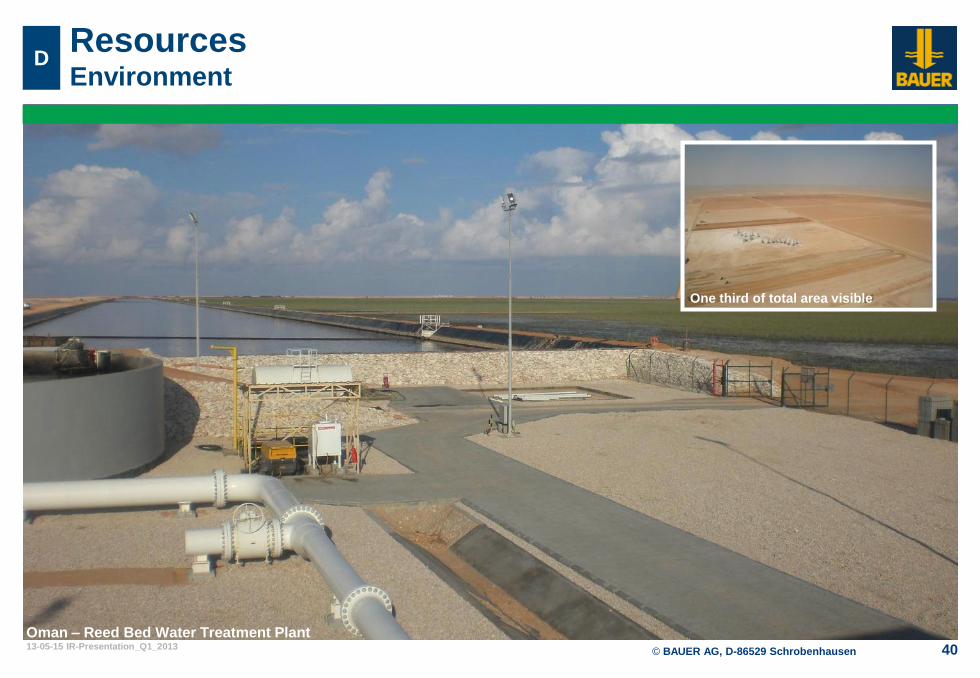

Resources Environment

D

Oman – Reed Bed Water Treatment Plant

One third of total area visible

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 41

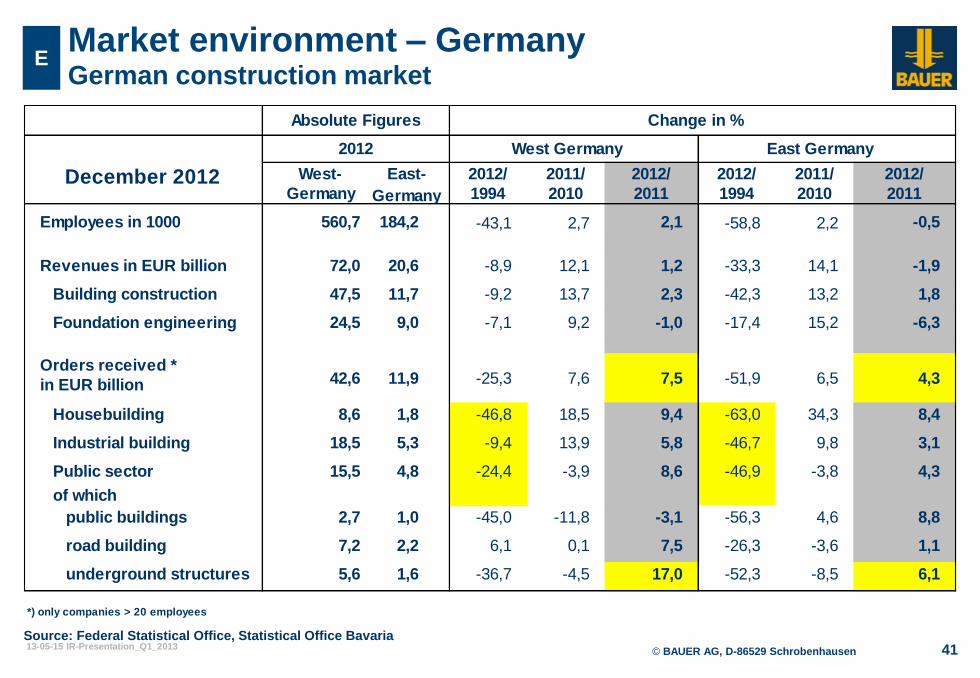

West-

Germany

Employees in 1000 560,7 184,2 -43,1 2,7 2,1 -58,8 2,2 -0,5

Revenues in EUR billion 72,0 20,6 -8,9 12,1 1,2 -33,3 14,1 -1,9

Building construction 47,5 11,7 -9,2 13,7 2,3 -42,3 13,2 1,8

Foundation engineering 24,5 9,0 -7,1 9,2 -1,0 -17,4 15,2 -6,3

Orders received *

in EUR billion

Housebuilding 8,6 1,8 -46,8 18,5 9,4 -63,0 34,3 8,4

Industrial building 18,5 5,3 -9,4 13,9 5,8 -46,7 9,8 3,1

Public sector

of which

public buildings 2,7 1,0 -45,0 -11,8 -3,1 -56,3 4,6 8,8

road building 7,2 2,2 6,1 0,1 7,5 -26,3 -3,6 1,1

underground structures 5,6 1,6 -36,7 -4,5 17,0 -52,3 -8,5 6,1

*) only companies > 20 employees

Absolute Figures

2012

8,6 -46,915,5 4,8 -3,8 4,3-24,4 -3,9

6,5

2011

4,3-25,3

1994

7,5

2010

7,6 -51,942,6 11,9

2011December 2012 2011/ 2012/

1994 2010

East-

Germany

2012/ 2012/

Change in %

West Germany East Germany

2011/2012/

Market environment – Germany German construction market

E

Source: Federal Statistical Office, Statistical Office Bavaria

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 42

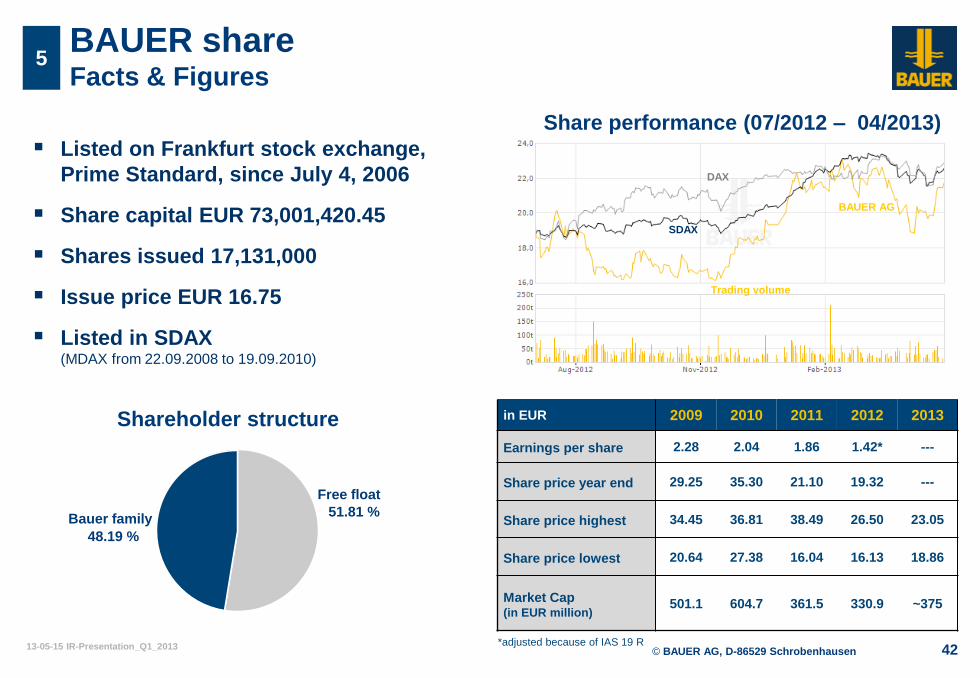

BAUER share Facts & Figures

5

Bauer family

48.19 %

Free float

51.81 %

Listed on Frankfurt stock exchange,

Prime Standard, since July 4, 2006

Share capital EUR 73,001,420.45

Shares issued 17,131,000

Issue price EUR 16.75

Listed in SDAX (MDAX from 22.09.2008 to 19.09.2010)

Shareholder structure

Share performance (07/2012 – 04/2013)

SDAX

DAX

Trading volume

BAUER AG

in EUR 2009 2010 2011 2012 2013

Earnings per share 2.28 2.04 1.86 1.42* ---

Share price year end 29.25 35.30 21.10 19.32 ---

Share price highest 34.45 36.81 38.49 26.50 23.05

Share price lowest 20.64 27.38 16.04 16.13 18.86

Market Cap (in EUR million)

501.1 604.7 361.5 330.9 ~375

*adjusted because of IAS 19 R

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 43

BAUER share Dividend policy

5

2009

Dividend payment (in EUR per share)

2010 2008 2007 2006

0.30

0.00

0.60

0.90

1.20

0.50

1.00 1.00

0.60 0.60

Dividend policy founded on a reasonable

balance between shareholders and

company

fair participation of shareholders

continuity over the years

safeguarding of the equity base

All shareholders shall participate in the

success of the business.

In turbulent times such as the financial crisis

our goal of strategic and safe growth of the

company led to slightly higher profit retention

for the last years.

To secure an adequate equity ratio is an

important aim of the company’s management.

With this we intend to safeguard the long-term

success of the Group.

2011

0.50

2012*

0.30

* Proposed; subject to the consent of the Annual General Meeting to be held on June 27, 2013

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 44

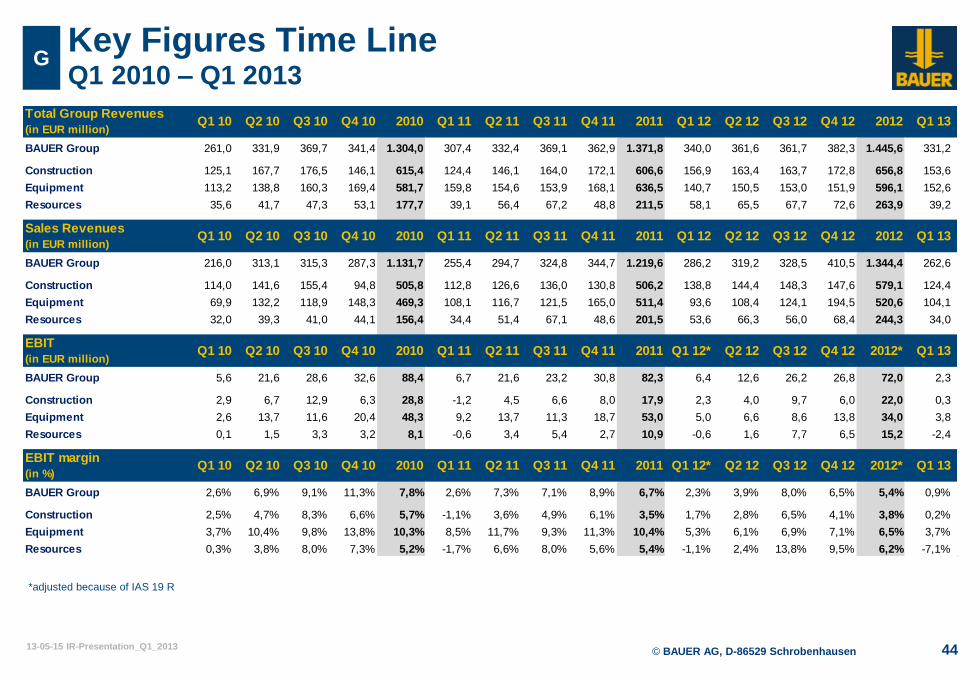

G Key Figures Time Line Q1 2010 – Q1 2013

*adjusted because of IAS 19 R

Total Group Revenues

(in EUR million)

BAUER Group 261,0 331,9 369,7 341,4 1.304,0 307,4 332,4 369,1 362,9 1.371,8 340,0 361,6 361,7 382,3 1.445,6 331,2

Construction 125,1 167,7 176,5 146,1 615,4 124,4 146,1 164,0 172,1 606,6 156,9 163,4 163,7 172,8 656,8 153,6

Equipment 113,2 138,8 160,3 169,4 581,7 159,8 154,6 153,9 168,1 636,5 140,7 150,5 153,0 151,9 596,1 152,6

Resources 35,6 41,7 47,3 53,1 177,7 39,1 56,4 67,2 48,8 211,5 58,1 65,5 67,7 72,6 263,9 39,2

Sales Revenues

(in EUR million)

BAUER Group 216,0 313,1 315,3 287,3 1.131,7 255,4 294,7 324,8 344,7 1.219,6 286,2 319,2 328,5 410,5 1.344,4 262,6

Construction 114,0 141,6 155,4 94,8 505,8 112,8 126,6 136,0 130,8 506,2 138,8 144,4 148,3 147,6 579,1 124,4

Equipment 69,9 132,2 118,9 148,3 469,3 108,1 116,7 121,5 165,0 511,4 93,6 108,4 124,1 194,5 520,6 104,1

Resources 32,0 39,3 41,0 44,1 156,4 34,4 51,4 67,1 48,6 201,5 53,6 66,3 56,0 68,4 244,3 34,0

EBIT

(in EUR million)

BAUER Group 5,6 21,6 28,6 32,6 88,4 6,7 21,6 23,2 30,8 82,3 6,4 12,6 26,2 26,8 72,0 2,3

Construction 2,9 6,7 12,9 6,3 28,8 -1,2 4,5 6,6 8,0 17,9 2,3 4,0 9,7 6,0 22,0 0,3

Equipment 2,6 13,7 11,6 20,4 48,3 9,2 13,7 11,3 18,7 53,0 5,0 6,6 8,6 13,8 34,0 3,8

Resources 0,1 1,5 3,3 3,2 8,1 -0,6 3,4 5,4 2,7 10,9 -0,6 1,6 7,7 6,5 15,2 -2,4

EBIT margin

(in %)

BAUER Group 2,6% 6,9% 9,1% 11,3% 7,8% 2,6% 7,3% 7,1% 8,9% 6,7% 2,3% 3,9% 8,0% 6,5% 5,4% 0,9%

Construction 2,5% 4,7% 8,3% 6,6% 5,7% -1,1% 3,6% 4,9% 6,1% 3,5% 1,7% 2,8% 6,5% 4,1% 3,8% 0,2%

Equipment 3,7% 10,4% 9,8% 13,8% 10,3% 8,5% 11,7% 9,3% 11,3% 10,4% 5,3% 6,1% 6,9% 7,1% 6,5% 3,7%

Resources 0,3% 3,8% 8,0% 7,3% 5,2% -1,7% 6,6% 8,0% 5,6% 5,4% -1,1% 2,4% 13,8% 9,5% 6,2% -7,1%

2012*

Q1 13

Q1 13

Q1 13

Q1 13

2012

Q4 12

Q2 12 Q3 12

Q2 12

Q2 12

Q2 12

Q4 12

Q3 12 Q4 12

Q3 12 Q4 12

2012

2012*

Q4 11

2010 Q4 11

2010 Q4 11

Q2 11

2011

Q3 10

Q3 11

Q3 11

Q3 11

Q3 112010

Q2 11Q1 11

Q1 11

Q2 11

Q3 10 Q4 10

Q1 10

Q1 10

Q1 10 Q2 10

Q1 10 Q2 10

Q1 11

Q1 11Q2 10 Q3 10 Q4 10

2011

2011

Q2 10 Q3 10 Q4 10

2011Q4 10

2010 Q4 11

Q2 11

Q1 12

Q1 12

Q1 12*

Q1 12* Q3 12

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 45

Investor Relations

BAUER Aktiengesellschaft

BAUER-Straße 1

86529 Schrobenhausen

Germany

Tel.: +49 8252 97-1218

Fax: +49 8252 97-2900

www.bauer.de

BAUER Aktiengesellschaft

Financial calendar 2013

Publication Annual Report 2012 April 11, 2013

Annual Press Conference April 11, 2013

Analyst Conference April 11, 2013

Annual General Meeting June 27, 2013

Interim Report to March 31, 2013 May 15, 2013

Half-Year Interim Report to June 30, 2013 August 14, 2013

Interim Report to September 30, 2013 November 14, 2013

Listing SDAX, CDAX, GEX,

Classic All Share

Prime All Share

DAXplus Family

Get the

BAUER App

for iPhone

and iPad

Visit us on YouTube:

http://www.youtube.com/Bauergruppe

ISIN DE0005168108

Reuters B5AG.DE

Bloomberg B5A GR

© BAUER AG, D-86529 Schrobenhausen 13-05-15 IR-Presentation_Q1_2013 46

Disclaimer

This presentation contains forward-looking statements. Forward-looking statements

are statements that are not historical facts, including statements about our beliefs,

intentions, expectations, predictions and the assumptions underlying them.

These statements are based on factors as they are currently available to the

management of BAUER AG and therefore speak only as of the date they are made.

We assume no liability to update publicly or conform any of them to future events or

future developments.

Forward-looking information is subject to various known and unknown risks and un-

certainties, which could lead to material differences between the actual future results,

financial situation, development or performance of the BAUER Group and those

factors contained in any forward-looking statement. In view of these uncertainties, no

assurance can be given that these forward-looking statements will prove accurate

and correct, or that anticipated and projected future results will be achieved and we

caution you not to place undue reliance on these forward-looking statements.

Recommended