Basel 3 and Solvency 2Perspective and Consequences

Eric Boyer de la Giroday

May 2015

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

2

“The farther backward you can look, the farther forward you are likely to see.”

Winston Churchill

Foreword

As a result of deregulation from 1980 onwards and creativity of the financial sector, leverage and financial innovation have been the main drivers for economic expansion in the Western world supported by private consumption and public deficits.

By 2007, the financial system broke down generating a major financial, economic and Western European sovereign crisis not yet resolved.

Drawing the lessons from the excesses, governments agreed to strengthen regulations with the Basel 3 (banks) and Solvency 2 (insurers in the EU only).

These new regulations will have direct effects not only on operators but much beyond on society itself. They may also have unintended consequences which will have to be assessed during the regulatory implementation period and possibly adapted to mitigate negative impacts.

3Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

4

Agenda

1. Financial Crises Integral Part of Model

2. The Regulatory Answers : Basel 3 and Solvency 2

3. Consequences of Regulations

4. Banks : more to come …

5. And now …

6. How does Basel 3 impact banks’ strategy ?

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

5

1. Financial Crises Integral Part of Model

The long view on financial crises…

Recent past …1980: South American Crisis1987: Black Monday1989: Junk Bonds crisis; US S&L bankruptcies1992: £ and ERM crisis 1995: Mexico / Tequila crisis1998: Asian and LTCM crisis2002: Technology bubble burst2007: Sub-Prime Loans crisis2010: Euroland sovereign crisis

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

6

1. Financial Crises Integral Part of Model

The long view on financial crises…

More distant past…

Very long list, some examples :

-600 : Greece / Solon

1637: Netherlands / Tulip crisis

1720: France / John Law, paper money

and Compagnie des Indes

1826: UK / South American crisis and

stock exchange crash

1907: USA / NYSE crash /

« Knickerbocker Trust Co. » crisis

1929: USA / The great crisis

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

7

1. Financial Crises Integral Part of ModelBefore 1980…

• Cash• Bonds• Equities• Spot and forward FX

(max. 1 year maturity)• On exchange options on

shares and (some) commodities (short term and limited volumes)

Since then…

• Over-the-counter (mainly) and on exchange, short and long term linear and non linear derivatives on :• Interest rates and inflation• FX• Equities• Credits• Commodities• Precious metals

• Repos• Hedge funds / Shadow Banking• Securitizations• SPVAs (insurances)

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

8

1. Financial Crises Integral Part of Model

Direct causes of the 2007 crisis :• Shareholders’ and managers’ greed• Politicians• Over indebtedness• Public finances drift• Accounting rules• Bank regulation (Basel 2)• Banks control deficit• Rating agencies• Hedge funds / Shadow Banking• Globalization

…and financial deregulation

as from 1980…

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

9

1. Financial Crises Integral Part of Model

Human nature and structural causes…

Determination to consume and over indebtedness…

… of individuals

… of States

EU / Euroland governance

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

10

1. Financial Crises Integral Part of Model

Quantifying the immediate financial consequences of the 2007 crisis …

Required capital infusions in the financial sector essentially funded by States…

* : including Fannie Mae and Freddie MacSource : Bloomberg

(€ bn) Banks Insurers Total

USA 492 * 120 612

Europe 463 10 473

R of W 96 0 96

1.051 130 1.181

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

0

3000

6000

9000

12000

15000

18000

1995 2000 2005 2010

Eurozone (€bn)

GDP debt

1. Financial Crises Integral Part of Model

Debt and GDP levels: USA Debt and GDP levels: Eurozone

11

($ bn) (€ bn)

Source : Thomson Reuters Datastream

0

10000

20000

30000

40000

50000

60000

1950 1960 1970 1980 1990 2000 2010

United States ($bn)

GDP debt

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

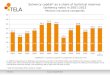

72 79 112 12753 84 62 66 85

178

340 221109

323327 400

274

70

62

66

56

58

88102

123

107

94

0

100

200

300

400

500

600

700

800

DE FR IT GR ES PT IR UK US

2009

Government debt Corporate debt Household debt

1. Financial Crises Integral Part of Model

Debt levels in % of GDP

12

Source : Thomson Reuters Datastream

*

* : Carmen Reinhart and Kenneth Rogoff critical level of total indebtedness (This Time is Different – Princeton University Press)

79 89 122 15784 125 122 86 105

184

380219 148 314

335

551

268

67

56

64

5769

81

97

102

95

79

0

100

200

300

400

500

600

700

800

DE FR IT GR ES PT IR UK US

2013

Government debt Corporate debt Household debt

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

0

5000

10000

15000

20000

25000

30000

35000

40000

1995 2000 2005 2010

Eurozone (€bn)

GDP bank assets

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

1970 1975 1980 1985 1990 1995 2000 2005 2010

United States ($bn)

GDP bank assets

1. Financial Crises Integral Part of Model

Bank assets and GDP evolution

13

Source : Thomson Reuters Datastream

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

14

1. Financial Crises Integral Part of Model

And now ? Cautious optimism…

The « technical » appraisal of crisis

management…

Keynes, von Hayek and the others…

Animal spirits and confidence…

Media time frame and content :

Reuter, Bloomberg, WSJ…

It’s a long way to Tipperary…

Splitting the banks… Volcker, Vickers and Liikanen…

Financial regulation and its risks…

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

15

1. Financial Crises Integral Part of Model

Lessons from the recent crisis from a political/regulatory perspective :

• Too much leverage• Too short liquidity• Too little capital• Too big to fail• Procyclicality of regulation

This is the judgment on and for banks triggering the Basel 3 new regulation. For insurers, similar considerations reinforced the Solvency 2 regulation already in discussion since several years.

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

16

2. The Regulatory Answers : Basel 3 and Solvency 2

Why are banks and insurances regulated / supervised ?

• Concern to the public• Protection of public interest• Economies sensitive to interconnectedness of and reliance on

banks• Systemic risk of failure

(Refer to field studies papers for the description of both set of rules)

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

17

3. Consequences of Regulations

Related to Banks

• Robustness : enhanced capital, liquidity and deleveraging• Capital and funding shortfall : shortfall of € 70 billion equity

and € 225 billion of liquid assets…• Cost of credit up• Lending capacity down during adjustment period• Deleveraging : retrenchment out of developing markets• Maturity of credit• Balance sheet : mortgages, consumer credit, midcorps• RWA models : exponential and procyclical…

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

18

3. Consequences of Regulations

Related to Insurers

• Assets : lower risk profile or higher capital…• Contradiction in principles : short term measurement of long-term

perspective…• Methodology bias : S2 standard formula pushes towards 3 to 5-

year strong rated sovereign bonds (mitigants introduced under Omnibus II : volatility and matching adjustment, 16-year period for implementation…)

• Competitive level playing field : Europe vs. US and the rest of the world

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

19

3. Consequences of Regulations

Related to the Joint Implementation

• Interdependence :

Independent development processes, collateral interference and coincident implementation…

• Cost of capital :

Increase of the cost of capital of banks relative to the cost of capital of insurers : banks benefit more from debt interest deductibility to reduce cost of capital because they are more leveraged than insurers.

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

20

3. Consequences of Regulations

• Asset allocation paradigm :

Insurers, traditional subscribers of debt (senior and subordinated) issued by banks, will shift more toward short / high quality / senior and sovereign type of paper.

Basel 3 and Solvency 2 both give preferential treatment to bonds / loans with good credit ratings and short maturities as this minimizes the level of capital to hold. It also best suits the composition of liquidity buffers for banks specifically.

• Preferential treatment :

Government bonds of the EU require no (or little) capital and covered bonds receive a preferential treatment. This creates incentive for banks and insurers to allocate their capital accordingly to the detriment of other issuers.

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

21

3. Consequences of Regulations

• Models induced arbitrages :

Sectors internal models may be different and a source of arbitrage between the use of internal models. Regulators should talk and align views remembering the collapse of AIG in 2008.

Risk/product transfer across the two sectors could take place in business lines where banks and insurers compete directly for example annuities (in insurance requiring higher capital requirement) vs. term deposits (in banks requiring less).

• Control vacuum :

Risk could migrate away from both sectors through use of securitization, reinsurance and shadow banking. If so, and like before the crisis, this could result in more interconnected financial systems, opaque distribution of risk and migration towards less regulated / supervised areas.

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

22

3. Consequences of Regulations

• Diminished secondary markets liquidity :

Rules on capital, liquidity but also compliance make it difficult for banks to generate a satisfactory profit from warehousing and trading financial assets.

As a consequence, banks have considerably reduced their inventories in bonds, shares, commodities, currencies and related market making activities. This explains events like “flash crashes” recently and happens as the value of outstanding bonds is at record high level as a consequence of banks pushing borrowers to the bond market.

The result is a much reduced secondary markets liquidity and price volatility. This has indeed made markets riskier and an additional challenge for insurers in the implementation of Solvency 2.

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

23

4. Banks : more to come …

• Basel Committee for Bank Supervision

Revised standardized approaches to measure RWAs

New capital floors / impose standardized approach to all

Fundamental review of the Trading Book and Interest rate risk in Banking Books

Regulatory treatment of sovereign risk

Pillar 3 : additional and harmonized disclosures to enable better comparison

… Leading to further requirements in capital beyond the already decided upon adapted solvency ratios …

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

24

4. Banks : more to come …• European Banking Authority

LCR and leverage : reporting requirements

Supervisory convergence in Pillar 2, stress testing

Harmonized Resolution rules, Recovery and Resolution, bail-in and MREL

Implementation of the DGS• ECB

25 banks (out of 123) failed the 2014 stress test (CET1 less than 5.5%); 12 have now raised necessary funds; 13 left still have a €9.5 bn shortage of capital. That is the quantitative lesson from the test.

Qualitative lessons were also drawn : requirement for better quality management and enhanced reporting capabilities.

… Leading to more requirements in data aggregation and reporting capabilities …

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

25

4. Banks : more to come …

• EU Commission and European Parliament

Implementation of the Bank Recovery & Resolution Directive.

This, amongst others, will define precisely the requirements of the Minimum Requirement for own funds and Eligible Liabilities (MREL) and the Total Loss Absorption Capacity (TLAC) in the broader international context for the European Global Systemically Important Banks (G-SIBs)

… Leading to additional requirements in (quasi) capital …

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

26

5. And now ?

“There are known knowns; there are things we know that we know. There are known unknowns; that is to say, there are things that we now know we don’t know. But there are also unknown unknowns – there are things we do not know we don’t know.”

Donald Rumsfeld, United States Secretary of Defense

The two accords have not been completely finalized. There are still moving parts and potential source of arbitrage can only be identified until the regulations are finalized.

Hopefully, Quantitative Impact Studies (QIS) and delayed timing in implementation will enable to smoothen the challenging transition.

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

27

6. How does Basel 3 impact banks’ strategy ?

• What does Basel 3 discourage ?

Over exposure to mortgages (leverage ratio and additional RWA)

Over reliance on wholesale funding (Liquidity ratios)

Financial Markets activities (Capital ratio)

Pressure on return of liquid assets portfolio (sovereign rating)

• What does Basel 3 encourage ?

Consumer lending (low balance sheet impact – leverage; high spread, short duration)

Structured Finance (high spread, short duration)

Retail deposits (liquidity)

Non-interest income

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

28

6. How does Basel 3 impact banks’ strategy ?

• Leading to a revised Business Model

Focus on a universal bank model (balanced B/S)

Profitability under severe pressure due to new regulations : banks need to review their business revenue mix and structurally lower operating costs

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

29

6. How does Basel 3 impact banks’ strategy ?

• What is an appropriate ROE for a Bank in this environment ?

Based on Market Returns ?

Return over * 20 years 10 years

S&P 500 9,7% 7,9%

Nikkei na 5,6%

Eurostoxx na 6,5%

MSCI World 7,8% 6,9%

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

30

6. How does Basel 3 impact banks’ strategy ?

Based on RoE of US/EU/Asian Banks ?

That may be answered with Basel … 4 ?

Reinforcement of an RWA floor, normalization of risk models across banks, increased required capital level/buffers, further restrictions on the size of banking groups and the nature of their activities …

Return of * Q2 2014 2007-2012

US Banks 9,1% 5,5%

€ Zone Banks 3,1% 6,8%

Asian Banks na 14,6%

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

31

Bibliography

Many articles have been published by the IMF, the BIS, consulting firms, equity sector analysts and rating agencies.

They are most of the time freely downloadable and I recommend particularly those published by McKinsey, KPMG, EY, Deloitte, Deutsche Bank, Nomura, Barclays, Exane BNP Paribas, HSBC, Goldman Sachs, Keefe Bruyette & Woods, Credit Suisse,Jefferies, UBS, Société Générale, Mood’ys and S&P.

Two references of interest :

Basel Accords vs. Solvency 2 :

Regulatory Adequacy and Consistency under the Postcrisis Capital Standards

University of St. Gallen

Daniela Laas and Caroline Siegel

Possible Unintended Consequences of Basel III and Solvency 2

IMF Working Paper

Ahmed- Al-Darwish et al.

And the following books :

This Time is Different

Eight centuries of financial folly

(Princeton)

Carmen Reinhart

Kenneth Rogoff

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

32

DebtThe First 5.000 Years(Melville House Publishing)David Graeber

Why Nations FailThe origins of power, prosperity and poverty(Profile Books)Daron AcemogluJames Robinson

Too Big to FailInside the battle to save Wall Street(Allen Lane)Andrew Sorkin Fool’s Gold(Little Brown)Gillian Tett Money and PowerHow Goldman Sachs came to rule the world(Penguin)William Cohan

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

33

Lords of FinanceThe Bankers who broke the world(Penguin)Liaquat Ahamed

Keynes HayekThe clash that defined modern economics(Norton)Nicholas Wapshott Théories du Bordel Economique2007 – 2013(JC Lattès)Pierre-Henri de MenthonAiry RoutierRisk & Other Four-Letter Words(Harper & Row)Walter Wriston The Big Short(Penguin)Michael Lewis

Basel 3 and Solvency 2 : Perspective and Consequences - May 2015

34

Fooled by Randomnes

The hidden role of chance in life and in the markets

Antifragile

The Black Swan

(Penguin)

Nassim Taleb

Against the Gods

The remarkable story of risk

(Wiley)

Peter L. Bernstein

Recommended