Bank and Thrift Accounting and Regulatory Update

Tuesday, June 27, 2017 12:00-1:30pm

Presented by:

Robert F. Storch, Chief Accountant Federal Deposit Insurance Corporation [email protected] Jeffrey J. Geer, Associate Chief Accountant Office of the Comptroller of the Currency [email protected] Sydney K. Garmong, Partner Crowe Horwath LLP [email protected]

Agenda

• Major Standards • Credit Losses

• Revenue Recognition

• Recognition & Measurement

• Leases

• Call Report Streamlining

• Other Final Standards of Interest to Financial Institutions

• Coming Soon and On the Horizon

2

Major Standards

Major Standard Effective Dates for PBEs Effective Dates for non-PBEs

Revenue Recognition ASU No. 2014-09

•Fiscal years beg. after Dec. 15, 2017, including interims •March 31, 2018 interim F/S

• Fiscal years beg. after Dec. 15, 2018, interims beg. after Dec. 15, 2019

• Dec. 31, 2019 annual F/S

Recognition & Measurement ASU No. 2016-01

•Fiscal years beg. after Dec. 15, 2017, including interims •March 31, 2018 interim F/S

• Fiscal years beg. after Dec. 15, 2018, interims beg. after Dec. 15, 2019

• Dec. 31, 2019 annual F/S

Leases ASU No. 2016-02

•Fiscal years beg. after Dec. 15, 2018, including interims •March 31, 2019 interim F/S

• Fiscal years beg. after Dec. 15, 2019, interims beg. after Dec. 15, 2020

• Dec. 31, 2020 annual F/S

Credit Losses ASU No. 2016-13

•Fiscal years beg. after Dec. 15, 2019, including interims (SEC filers) •March 31, 2020 interim F/S •Fiscal years beg. after Dec. 15, 2020, including interims (PBE non-SEC filers) •March 31, 2021 interim F/S

• Fiscal years beg. after Dec. 15, 2020, interims beg. after Dec. 15, 2021

• Dec. 31, 2021 annual F/S

PBE = Public Business Entities

Non-PBEs typically receive

an additional year

3

Public Business Entities (PBE): Why Does It Matter?

•Effective dates • Almost every ASU has delayed effective dates for non-PBEs

• Especially important given the adoption of FASB’s major standards

•Private Company Council (PCC) alternatives • PBEs cannot elect PCC alternatives • Goodwill

• Intangibles

• Consolidation

•Disclosures • Fair value of financial instruments table (FAS 107) was removed for non-

PBEs with the issuance of ASU 2016-01, “Recognition and Measurement”

• Vintage disclosures optional in ASU 2016-13, “Credit Losses”

• Scaled disclosures available in ASU 2014-09, “Revenue Recognition”

4

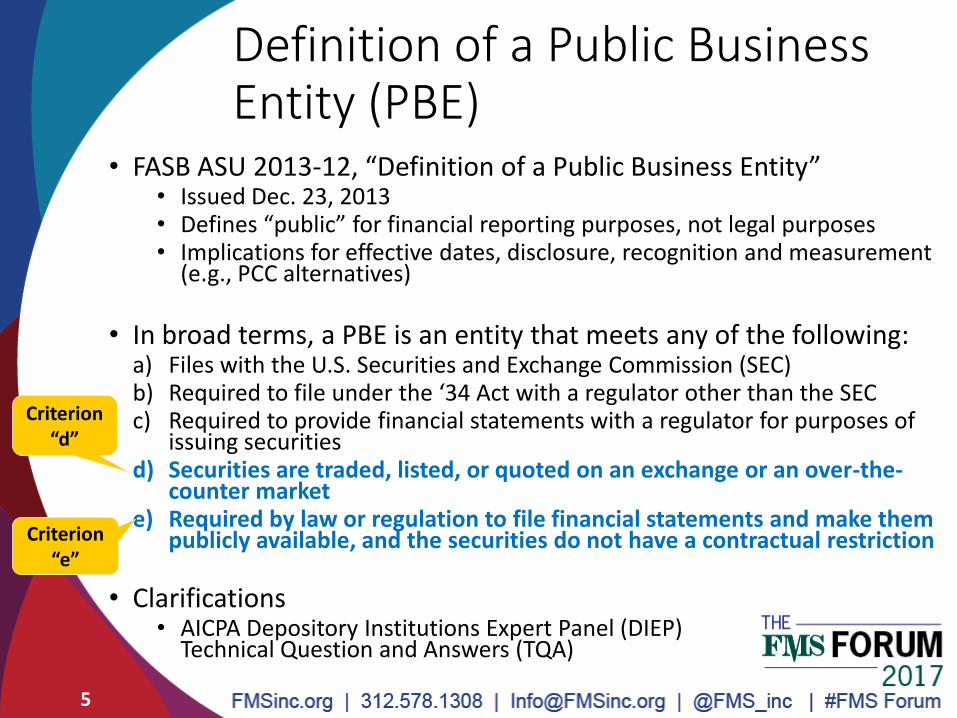

Definition of a Public Business Entity (PBE)

• FASB ASU 2013-12, “Definition of a Public Business Entity” • Issued Dec. 23, 2013 • Defines “public” for financial reporting purposes, not legal purposes • Implications for effective dates, disclosure, recognition and measurement

(e.g., PCC alternatives)

• In broad terms, a PBE is an entity that meets any of the following: a) Files with the U.S. Securities and Exchange Commission (SEC) b) Required to file under the ‘34 Act with a regulator other than the SEC c) Required to provide financial statements with a regulator for purposes of

issuing securities d) Securities are traded, listed, or quoted on an exchange or an over-the-

counter market e) Required by law or regulation to file financial statements and make them

publicly available, and the securities do not have a contractual restriction

• Clarifications • AICPA Depository Institutions Expert Panel (DIEP)

Technical Question and Answers (TQA)

5

Criterion “e”

Criterion “d”

5

6

June Birthday Celebrations!!

6

CECL June 16, 2016

Jeff June 27

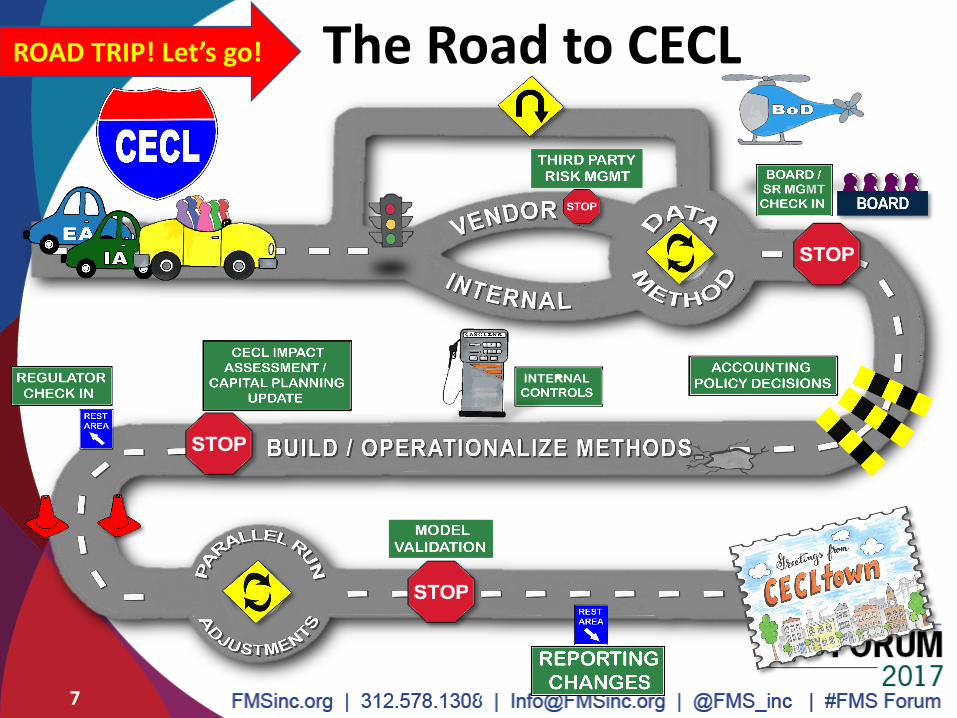

The Road to CECL

7 7 7

ROAD TRIP! Let’s go!

• Become familiar with the map: http://www.fasb.org/jsp/FASB/Document_C/DocumentPage?cid=1176168232528&acceptedDisclaimer=true

• Regulatory Resources to help along the way • FAQs

https://www.occ.gov/topics/bank-operations/accounting/cecl/cecl-faqs.html

• Joint Statement https://www.occ.gov/news-issuances/news-releases/2016/nr-ia-2016-69a.pdf

8

Where are we going?

8

72

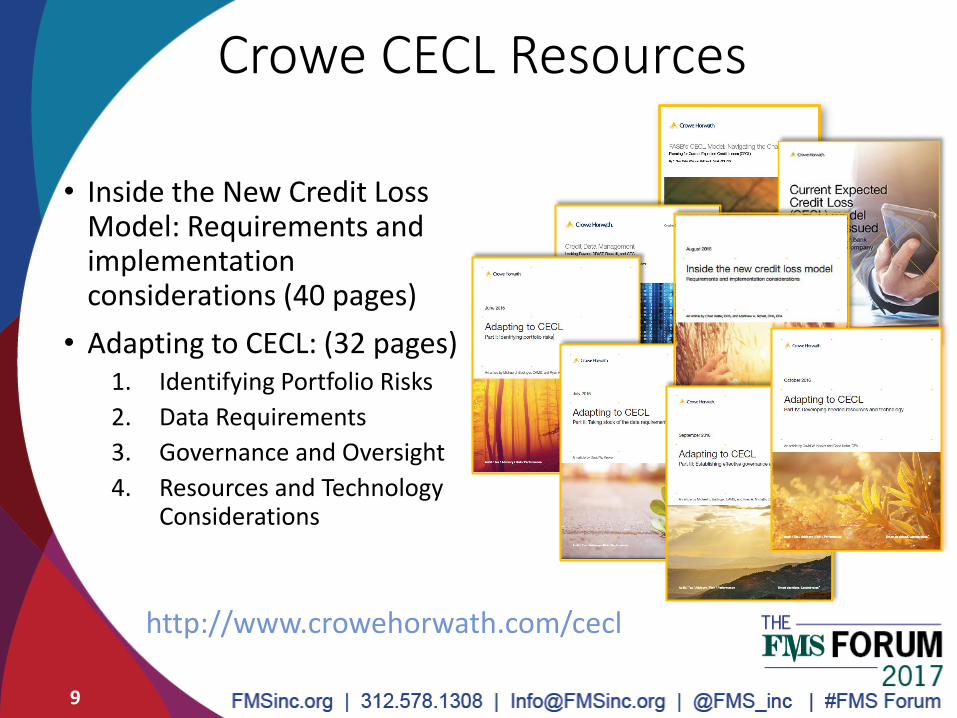

Crowe CECL Resources

• Inside the New Credit Loss Model: Requirements and implementation considerations (40 pages)

• Adapting to CECL: (32 pages) 1. Identifying Portfolio Risks

2. Data Requirements

3. Governance and Oversight

4. Resources and Technology Considerations

http://www.crowehorwath.com/cecl

9

Entity

Type

U.S. GAAP

Effective Date

Call Report

Effective Date*

Public Business

Entities (PBEs) that

are SEC Filers

Fiscal years beginning after 15 December 2019, including

interim periods within those fiscal years

Q1 2020

(31 March 2020)

Other PBEs**

(Non-SEC Filers)

Fiscal years beginning after 15 December 2020, including

interim periods within those fiscal years

Q1 2021

(31 March 2021)

Non-PBEs Fiscal years beginning after 15 December 2020, including

interim periods beginning after 15 December 2021

Q4 2021

(31 Dec 2021)

Early Application Early application permitted for fiscal years beginning after 15

December 2018, including interim periods within those fiscal

years

Permissible

no earlier than

31 March 2019

* For institutions with calendar year ends. ** A public business entity that is not an SEC filer would include (1) an entity that has issued securities that are traded, listed, or quoted on an over-the-counter market, or (2) an entity that has issued one or more securities that are not subject to contractual restrictions on transfer and is required by law, contract, or regulation to prepare U.S. GAAP financial statements and make them publicly available periodically (e.g., pursuant to Section 36 of the Federal Deposit Insurance Act and Part 363 of the FDIC’s regulations).

10

When do we need to get there?

10 10

11 11

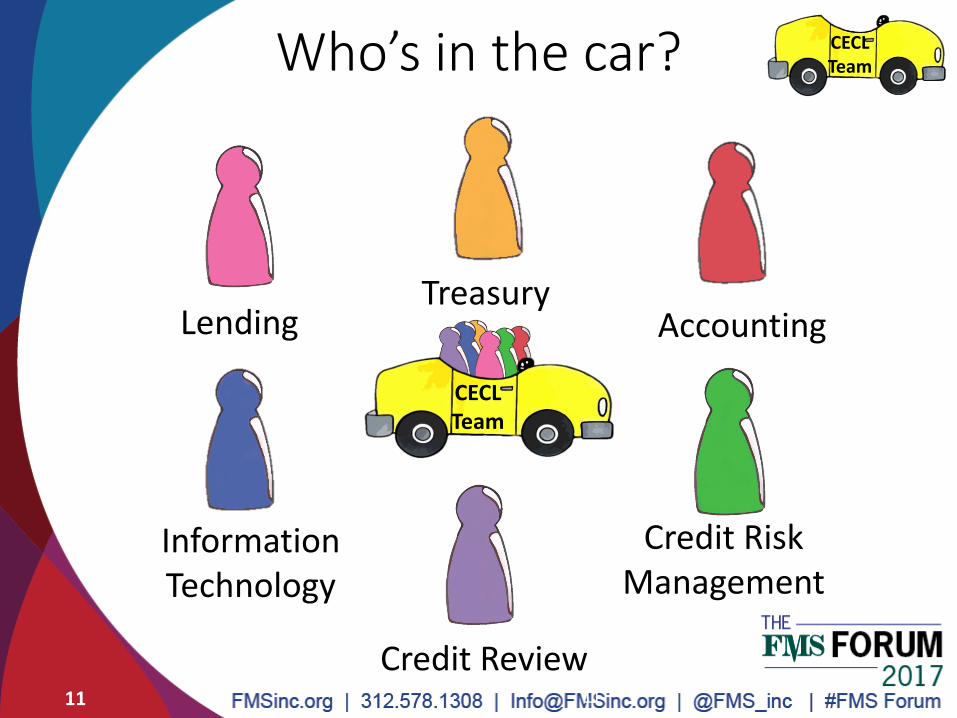

Lending Accounting Treasury

Credit Risk Management

Information Technology

Credit Review

Who’s in the car?

CECL Team

CECL Team

12 12

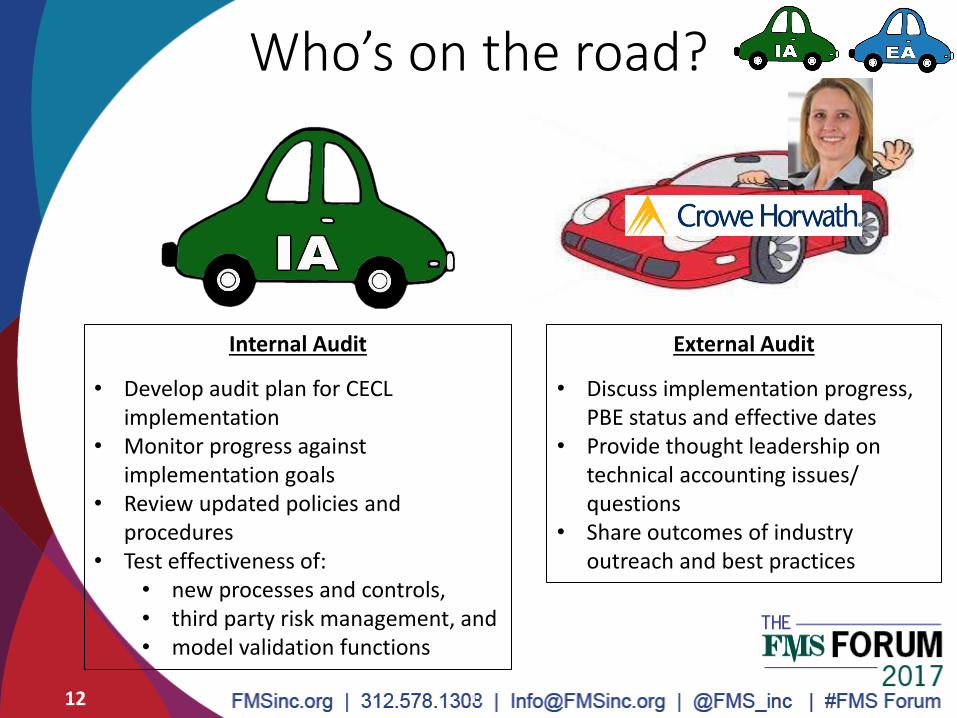

Who’s on the road?

Internal Audit

• Develop audit plan for CECL implementation

• Monitor progress against implementation goals

• Review updated policies and procedures

• Test effectiveness of: • new processes and controls, • third party risk management, and • model validation functions

External Audit

• Discuss implementation progress, PBE status and effective dates

• Provide thought leadership on technical accounting issues/ questions

• Share outcomes of industry outreach and best practices

13 13

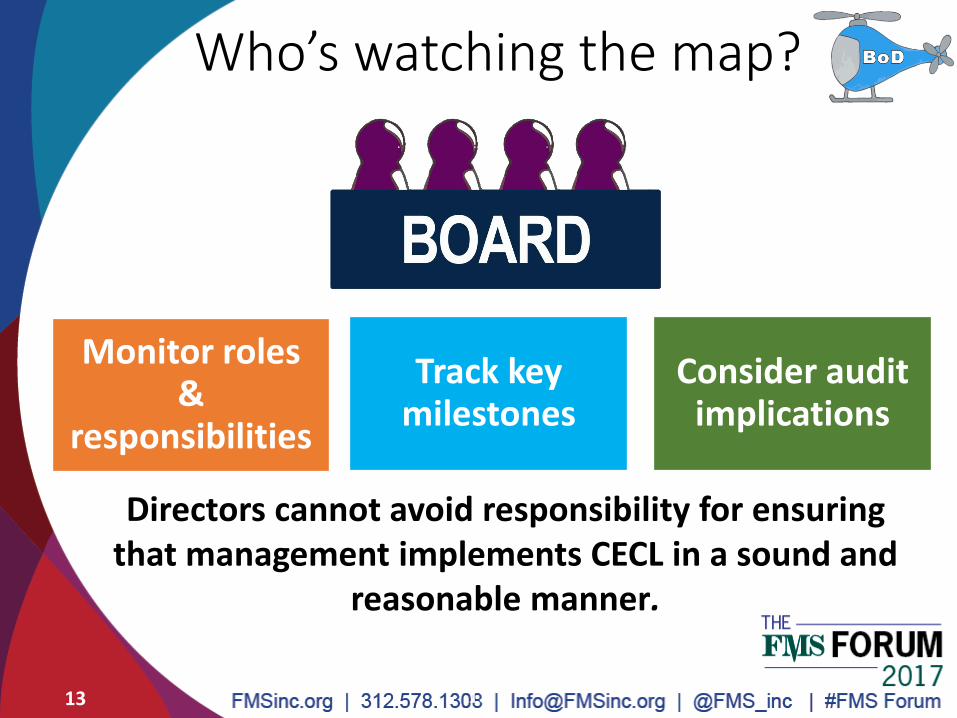

Who’s watching the map?

Monitor roles &

responsibilities

Track key milestones

Consider audit implications

Directors cannot avoid responsibility for ensuring that management implements CECL in a sound and

reasonable manner.

The Road to CECL

14 14 14

15

OCC Bulletin

2013-29

FDIC FIL-

44-2008

Oversight and Accountability

Third-Party

Life Cycle

15

The Road to CECL

16 16 16 16

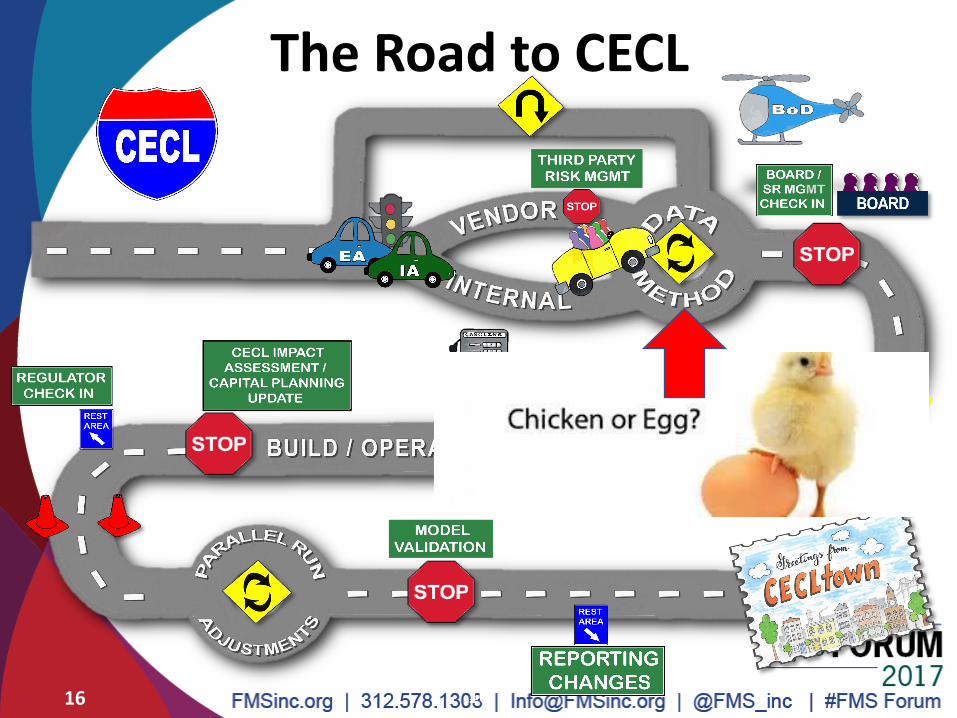

Data & Methods

Maturity

Dates

Recovery amounts

and dates

17

Origination

Dates

Initial charge-off amounts and dates

Subsequent charge-off amounts and dates

Types of data that may be needed to implement CECL:

Cumulative loss

amounts

Renewal and modification

dates

Origination par amount

17

18

Data & Methods

Lending Credit Risk Management

Credit Review

DSCR DTI LTV

Historical Risk

Ratings

Policy exceptions

Consider capturing and leveraging existing data in your credit risk functions for use in CECL estimates

18

Additional considerations • Quality of historical data

• Data archiving improvements and/or system changes

• Absence of historical loss data

• Segmentation – Significant risk characteristics

19

Data & Methods

A U-turn to the Vendor/Internal stoplight may be needed depending on

the data available to your institution and the planned estimation method(s).

19

The Road to CECL

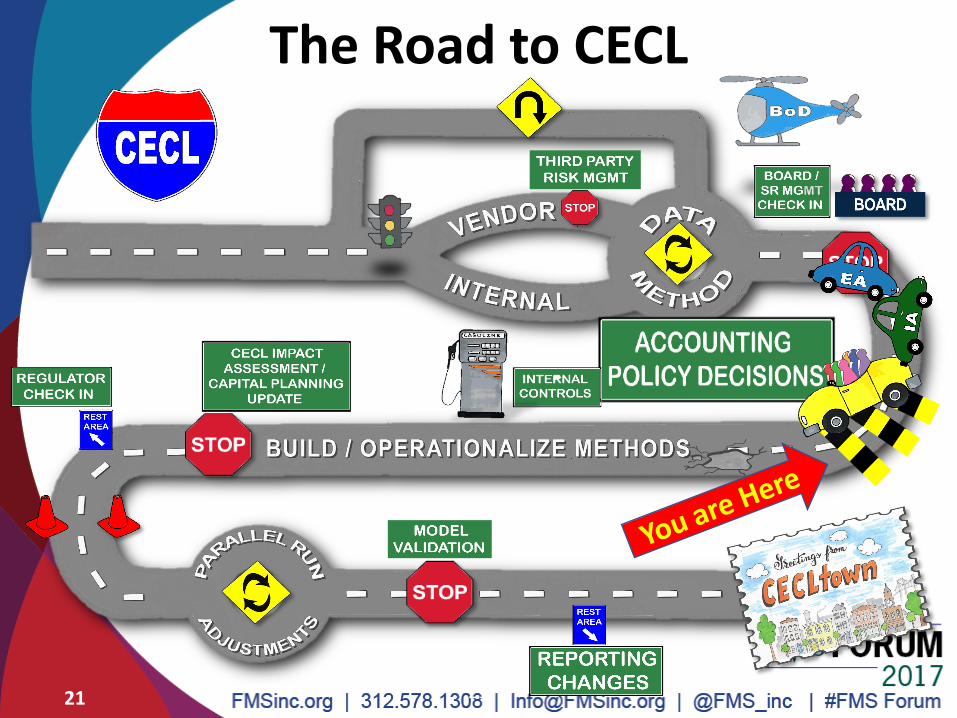

20

The Road to CECL

20

• Progress • Challenges/obstacles • Decisions made • Early capital impact

estimate

21

The Road to CECL

21

The Road to CECL

22 22

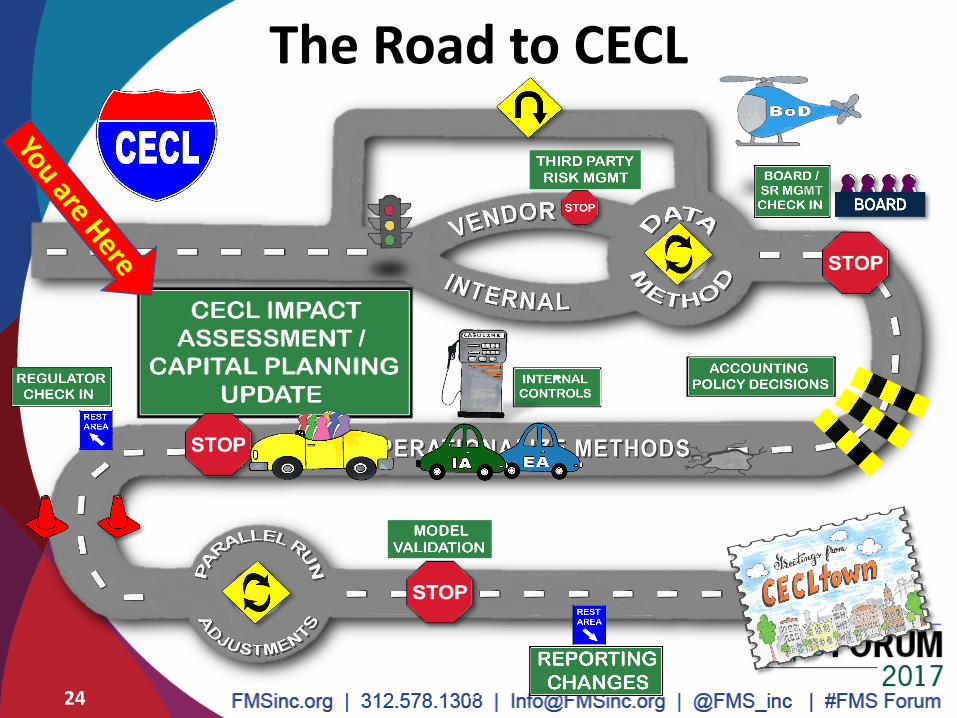

23

Take inventory of existing

controls in your allowance

estimation process and over

data used in the allowance

Think about what you are

changing in your allowance

estimation process and

what data you may be

adding

23

SOX: Recommend using Supreme for maximum performance

Fill up on

controls as you

design your

CECL process

24

The Road to CECL

24

25 25

• Update assessment of allowance change due to CECL and impact to regulatory capital

• No early incorporation of “expected loss” concepts or “soft adoption”

• No artificial inflation of the ALLL before effective date to smooth impact

• Don’t overload at adoption

– Record initial effect of CECL adoption on the effective date through retained earnings, not P&L

26

The Road to CECL

26

The Road to CECL

27 27

What is a parallel run?

28

Parallel Run

For a period of time, you run your incurred loss allowance process for financial reporting and also run your CECL process to test that your CECL process is functioning as intended. During the parallel run, you may identify that adjustments to data, systems or methods are needed in your CECL process.

Incurred Loss Process

CECL Process

CECL

Effective Date Start of parallel

run period

28

29

The Road to CECL

OCC Bulletin 2011-12 FDIC FIL 22-2017

29

30

The Road to CECL

30

31

• FFIEC Call Report • Forms and instructions will be updated for CECL

• Federal register notice expected mid-2018

• Consider updates to process and system(s) for regulatory reporting

• US GAAP Financial Statement Disclosures • For PBEs, credit quality indicators disaggregated by

year of origination (vintage)

• Discussion of reasonable and supportable forecasts and method of reversion

31

32

The Road to CECL

32

What is the TRG?

33

To ensure a smooth transition . . .

FASB formed a CECL Transition Resource Group (TRG)

Initially convened in early 2016, before final standard issued

Effort to replace confusing words and phrases before issuance

Purpose of the TRG is to . . .

Solicit, analyze, and discuss stakeholder issues arising from

implementation of new guidance

Inform the FASB about those implementation issues to determine what, if

any, action will be needed to address those issues

Provide forum for stakeholders to learn about new guidance from others

involved with implementation

33

Who’s on the TRG?

34

Preparers, including large and small banks

Auditors, with various client bases

Users / Investors

Regulators (observers)

TRG comprises experts across the spectrum of stakeholders:

34

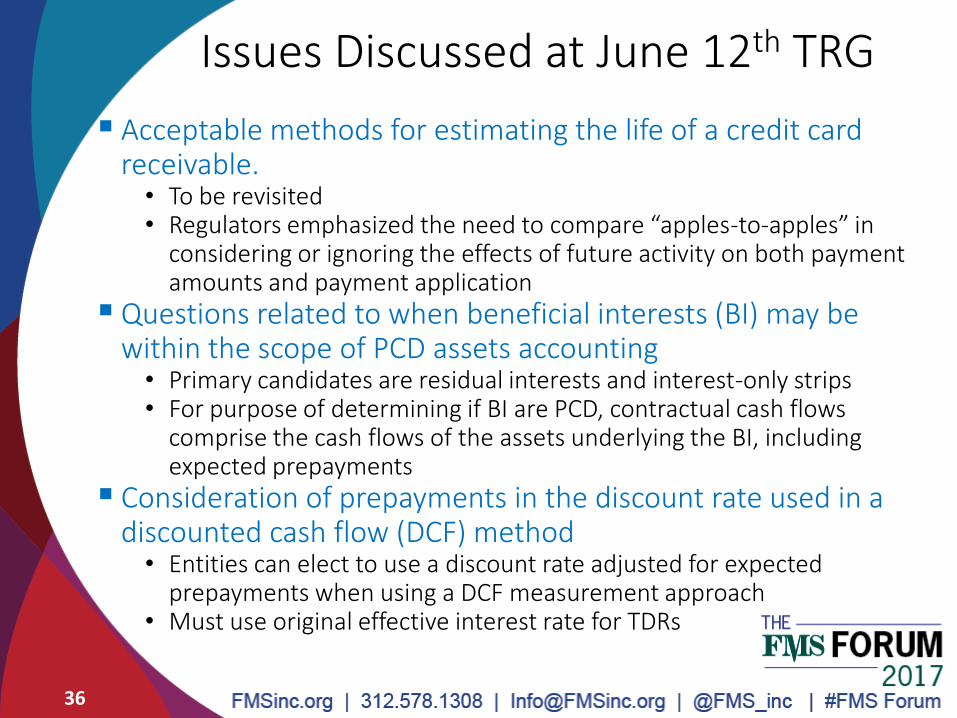

Issues Discussed at June 12th TRG

Implementation questions related to reasonably expected troubled debt restructurings (TDRs) • To be revisited

• Regulators emphasized need to consider all reasonably expected increases in credit risk, including forecasting TDRs at the portfolio level

Especially important to consider re-finance risk for pools of loans with bullet maturities (e.g., renewals of both commercial real estate loans with payments based on amortization periods exceeding contractual maturity & short-term commercial loans)

Transitioning pools of purchased credit-impaired (PCI) assets to purchased financial assets with credit deterioration (PCD) • Can elect to maintain existing pools of PCI assets either just at adoption

or also on an ongoing basis

35 35

Most relevant to community banks

Issues Discussed at June 12th TRG

Acceptable methods for estimating the life of a credit card receivable. • To be revisited • Regulators emphasized the need to compare “apples-to-apples” in

considering or ignoring the effects of future activity on both payment amounts and payment application

Questions related to when beneficial interests (BI) may be within the scope of PCD assets accounting • Primary candidates are residual interests and interest-only strips • For purpose of determining if BI are PCD, contractual cash flows

comprise the cash flows of the assets underlying the BI, including expected prepayments

Consideration of prepayments in the discount rate used in a discounted cash flow (DCF) method • Entities can elect to use a discount rate adjusted for expected

prepayments when using a DCF measurement approach • Must use original effective interest rate for TDRs

36

36

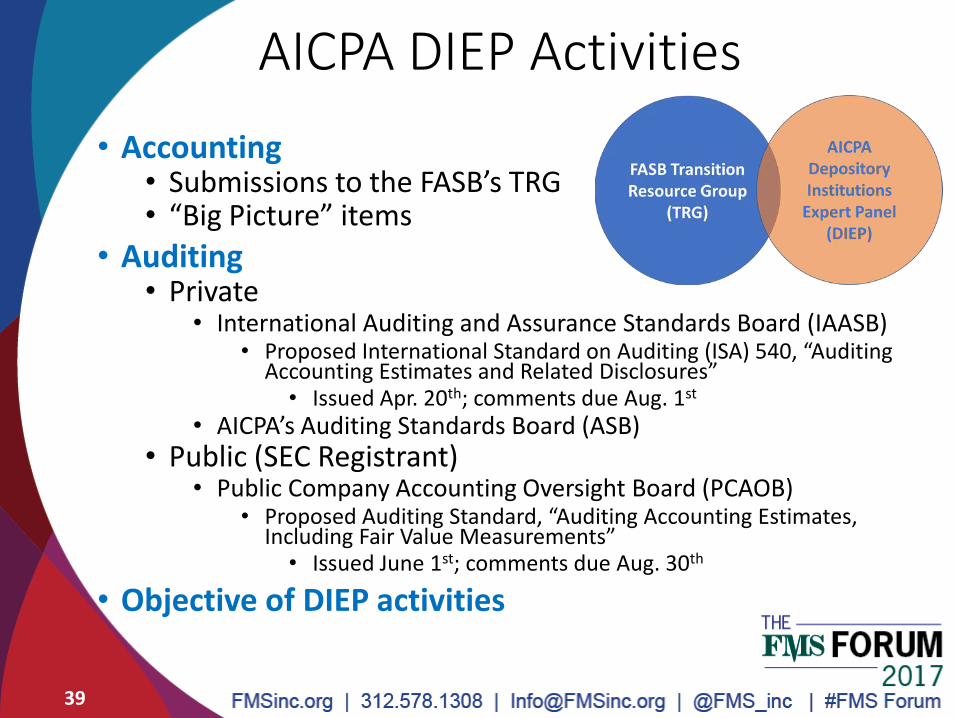

Credit Losses: AICPA Update

FASB Transition Resource Group

(TRG)

AICPA Depository Institutions

Expert Panel (DIEP)

38

AICPA DIEP Activities

• Accounting • Submissions to the FASB’s TRG • “Big Picture” items

• Auditing • Private

• International Auditing and Assurance Standards Board (IAASB) • Proposed International Standard on Auditing (ISA) 540, “Auditing

Accounting Estimates and Related Disclosures” • Issued Apr. 20th; comments due Aug. 1st

• AICPA’s Auditing Standards Board (ASB) • Public (SEC Registrant)

• Public Company Accounting Oversight Board (PCAOB) • Proposed Auditing Standard, “Auditing Accounting Estimates,

Including Fair Value Measurements” • Issued June 1st; comments due Aug. 30th

• Objective of DIEP activities

39

Revenue Recognition

• Landscape • Comments from the SEC, including disclosures

• Industry discussions

• AICPA discussions

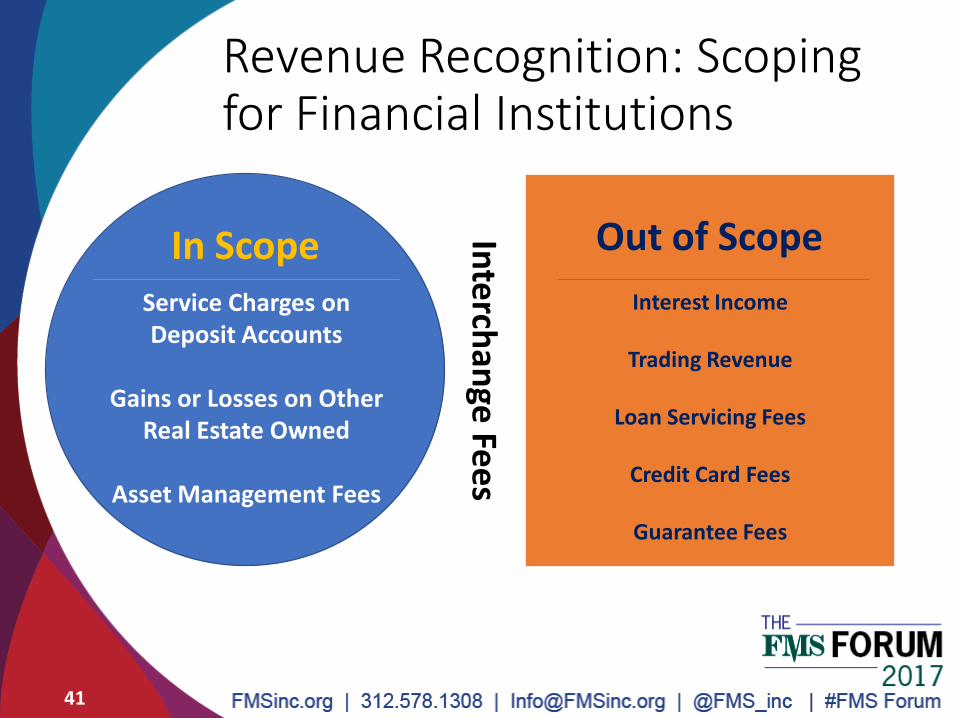

• Challenges for financial institutions • Scoping – what is in? what is out?

• Contract reviews

• Other • Internal control over financial reporting

• Disclosures

40

Revenue Recognition: Scoping for Financial Institutions

Interest Income

Trading Revenue

Loan Servicing Fees

Credit Card Fees

Guarantee Fees

In Scope Service Charges on Deposit Accounts

Gains or Losses on Other

Real Estate Owned

Asset Management Fees

Out of Scope Inte

rchan

ge Fe

es

41

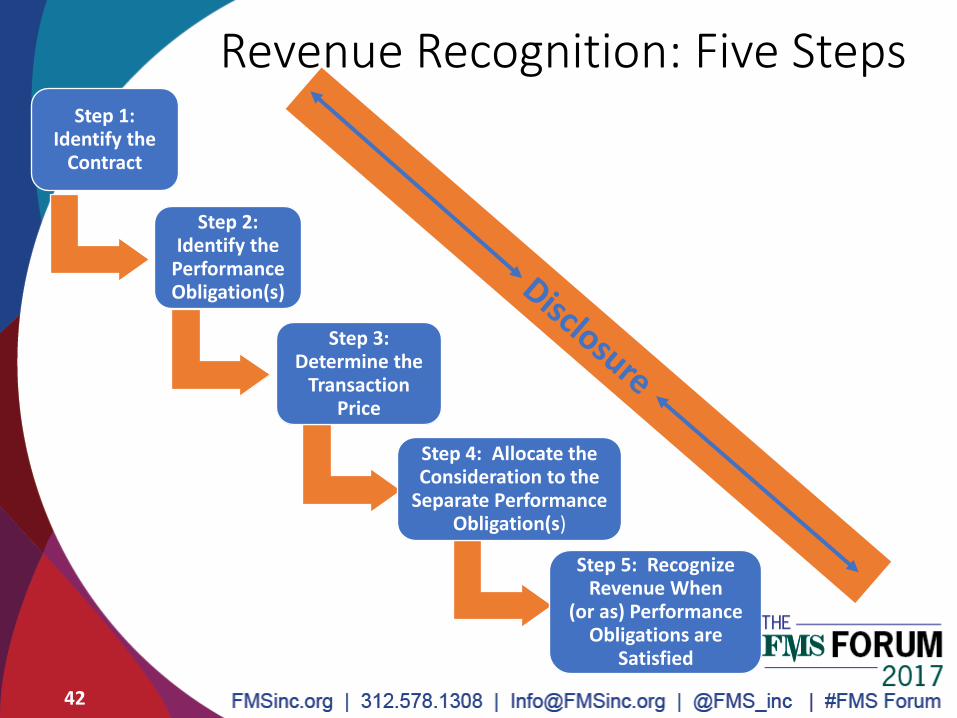

Revenue Recognition: Five Steps Step 1:

Identify the Contract

Step 2: Identify the

Performance Obligation(s)

Step 3: Determine the

Transaction Price

Step 4: Allocate the Consideration to the

Separate Performance Obligation(s)

Step 5: Recognize Revenue When

(or as) Performance Obligations are

Satisfied

42

Seller-Financed OREO Sales • Glossary entry for “Foreclosed Assets” in Call Report

instructions updated in March 2017 to incorporate the effect of the revenue recognition standard • See also March 2017 Call Report Supplemental Instructions

• Both available at https://www.ffiec.gov/ffiec_report_forms.htm

• Amended ASC 610-20 eliminates prescriptive criteria and methods for sale accounting and gain recognition for disposals of OREO in ASC 360-20 (FAS 66)

• Applying ASC 610-20 • Does selling institution have a controlling financial interest in

legal entity buying the OREO under ASC 810, Consolidation

• If yes, do not derecognize the OREO

• If no, does transaction meet ASC 606 requirements? • Does the transaction meet the ASC 606 definition of a contract?

• Has seller transferred control of the OREO to the buyer?

43

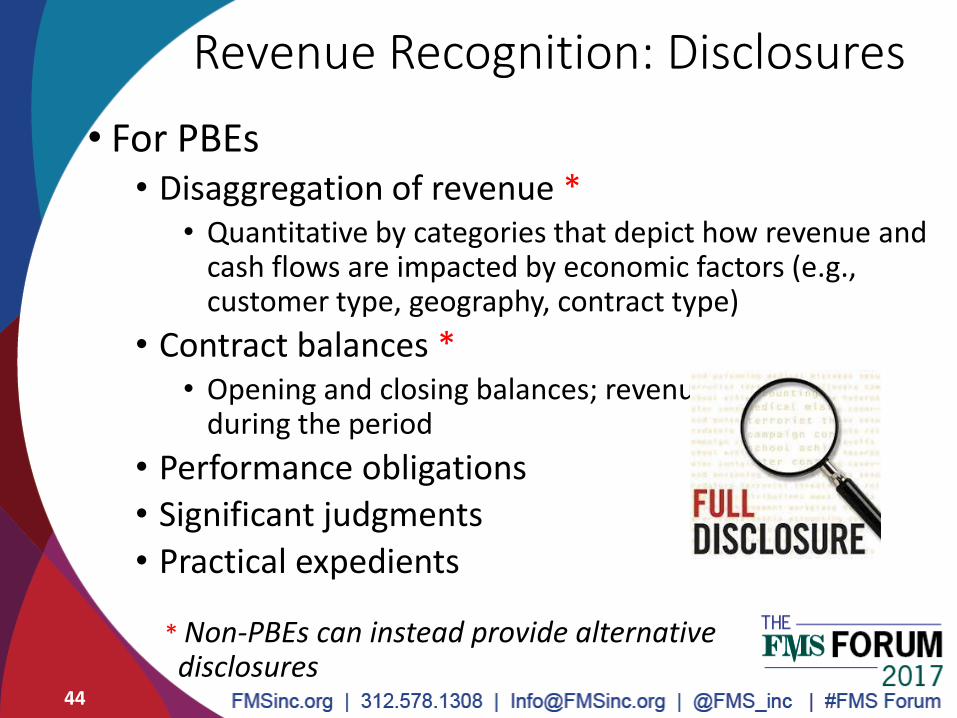

Revenue Recognition: Disclosures

• For PBEs • Disaggregation of revenue *

• Quantitative by categories that depict how revenue and cash flows are impacted by economic factors (e.g., customer type, geography, contract type)

• Contract balances * • Opening and closing balances; revenue recognized

during the period

• Performance obligations

• Significant judgments

• Practical expedients

* Non-PBEs can instead provide alternative disclosures

44

Change in Accounting for Equity Securities

• ASU 2016-01 issued in January 2016 covering the classification and measurement of financial instruments • Takes effect in 2018 (PBE) or 2019 (non-PBE)

• Makes targeted improvements to U.S. GAAP;

the most significant change is to the accounting for investments in equity securities

45

Change in Accounting for Equity Securities

• All equity investments within the scope of ASU 2016-01 will be measured at fair value through earnings (like trading assets) • Eliminates available-for-sale (AFS) category for investments in equity

securities with readily determinable fair values • Eliminates cost method for investments in equity securities without

readily determinable fair values, but a practical expedient may be elected • If elected, such investments are accounted for at cost, less

impairment, plus or minus subsequent adjustments for observable price changes, which must be reported in earnings

• Effect of elimination of AFS equity securities • On effective date, net unrealized gains (losses) on AFS equity securities in

AOCI are reclassified into retained earnings (RE) and, hence, CET1 capital • Thereafter, fair value changes are recognized in earnings, RE, and CET1

46

Change in Accounting for Leases

• ASU 2016-02, Leases (Topic 842) • Issued in February 2016 • Takes effect in 2019 (PBE) or 2020 (non-PBE) • Early application permitted

• ASU’s most significant change is to require a lessee to recognize assets & liabilities for all leases with a term more than 12 months • Operating leases would no longer be off-balance sheet items for lessees • Instead, a lessee would recognize a right-of-use (ROU) asset and a lease

liability on the balance sheet • Lessee’s income statement expense pattern and geography would differ

depending on whether a lease is: • A “finance lease” (front-loaded; ROU amortization + interest expense) or • An “operating lease” (straight-line; rent expense)

• For leases with a term of 12 months or less, a lessee may elect for each class of underlying asset not to recognize lease assets and lease liabilities

47

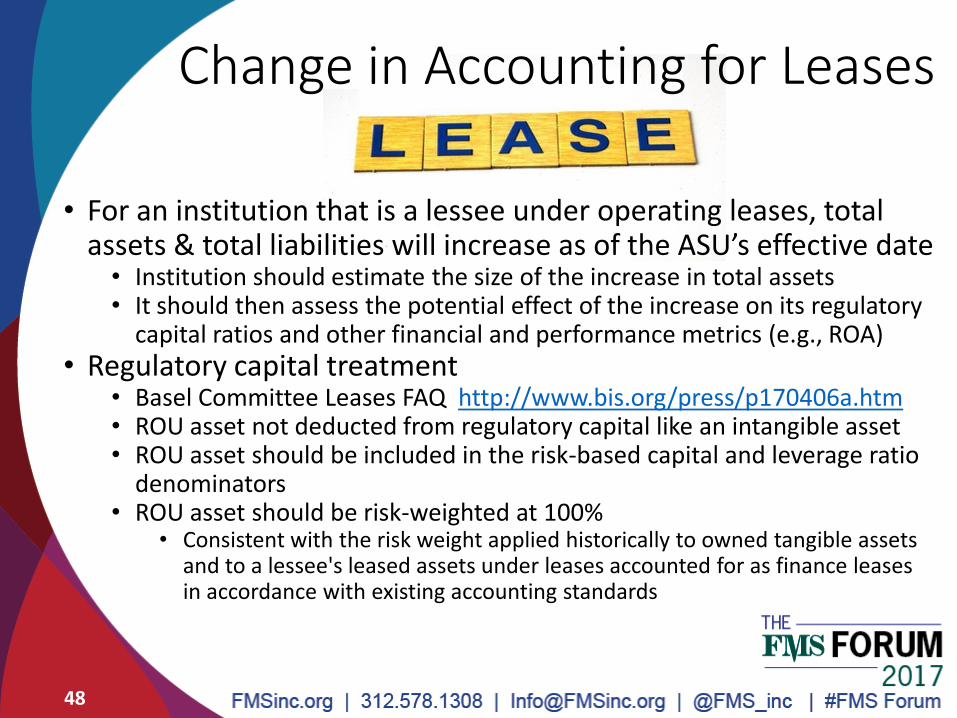

Change in Accounting for Leases

• For an institution that is a lessee under operating leases, total assets & total liabilities will increase as of the ASU’s effective date • Institution should estimate the size of the increase in total assets • It should then assess the potential effect of the increase on its regulatory

capital ratios and other financial and performance metrics (e.g., ROA) • Regulatory capital treatment

• Basel Committee Leases FAQ http://www.bis.org/press/p170406a.htm • ROU asset not deducted from regulatory capital like an intangible asset • ROU asset should be included in the risk-based capital and leverage ratio

denominators • ROU asset should be risk-weighted at 100%

• Consistent with the risk weight applied historically to owned tangible assets and to a lessee's leased assets under leases accounted for as finance leases in accordance with existing accounting standards

48

Community Bank Call Report Burden-Reduction Initiative

• New streamlined FFIEC 051 Call Report for eligible small institutions took effect on March 31, 2017 (FIL-82-2016 and FIL-14-2017) • Applicable to institutions with domestic offices only and less than $1 billion in

assets (except advanced approaches institutions) • Other burden-reducing revisions were made to the existing FFIEC 031 and 041

• Changes to the FFIEC 041 to create the new FFIEC 051 • Addition of a Supplemental Schedule of nine indicator questions and related

indicator data items on certain complex and specialized activities • Replaces all or part of six schedules currently included in the FFIEC 041

• Removal of data items identified as no longer necessary for collection from institutions with domestic offices only and total assets less than $1 billion

• Reduction in the reporting frequency for certain data items identified as needed less often than quarterly from such institutions

• Removal of all items currently subject to a $1 billion asset reporting threshold • Webinar to introduce the new FFIEC 051 took place on March 8, 2017

(FIL-10-2017) • Further burden-reducing changes to the Call Reports, including the new

FFIEC 051, will be proposed in future Federal Register notices

49

Other Final Standards of Interest to Financial Institutions

• Acquisitions, including Business Combinations • Simplifying Measurement-Period Adjustments (ASU 2015-16) • Clarifying the Definition of a Business (ASU 2017-01) • Goodwill Impairment Testing (ASU 2017-04)

• Compensation • Share-Based Payments (ASU 2016-09) • Topic 718: Scope of Modification Accounting (ASU 2017-09) • Presentation of Net Periodic Pension and Postretirement Benefit Costs

(ASU 2017-07)

• Other • Breakage for Prepaid Cards (ASU 2016-04) • Statement of Cash Flows

• Certain Clarifications (ASU 2016-15)

• Restricted Cash (ASU 2016-18)

• Income Taxes for Intra-Entity Asset Transfers (ASU 2016-16) • Premium Amortization on Purchased Callable Debt Securities

(ASU 2017-08)

50

Final Standards: Acquisitions

ASUs for Acquisitions PBE Non-PBE

Simplifying Measurement-Period Adjustments (ASU 2015-16) Eliminates retroactive revisions as a result of measurement-period adjustments, but requires disclosure of measurement period adjustments recorded in the current period.

1Q16 12/31/17

Definition of a Business (ASU 2017-01) Provides guidance to determine whether an acquisition is an asset (no goodwill) or business combination (goodwill)

1Q18 12/31/19

Goodwill Impairment Testing (ASU 2017-04) Removes step two (hypothetical purchase price allocation when the carrying value of a reporting unit exceeds its fair value) of the goodwill impairment test.

1Q20 (SEC) 1Q21 (non-SEC)

1Q22

Calendar Year-ends

51

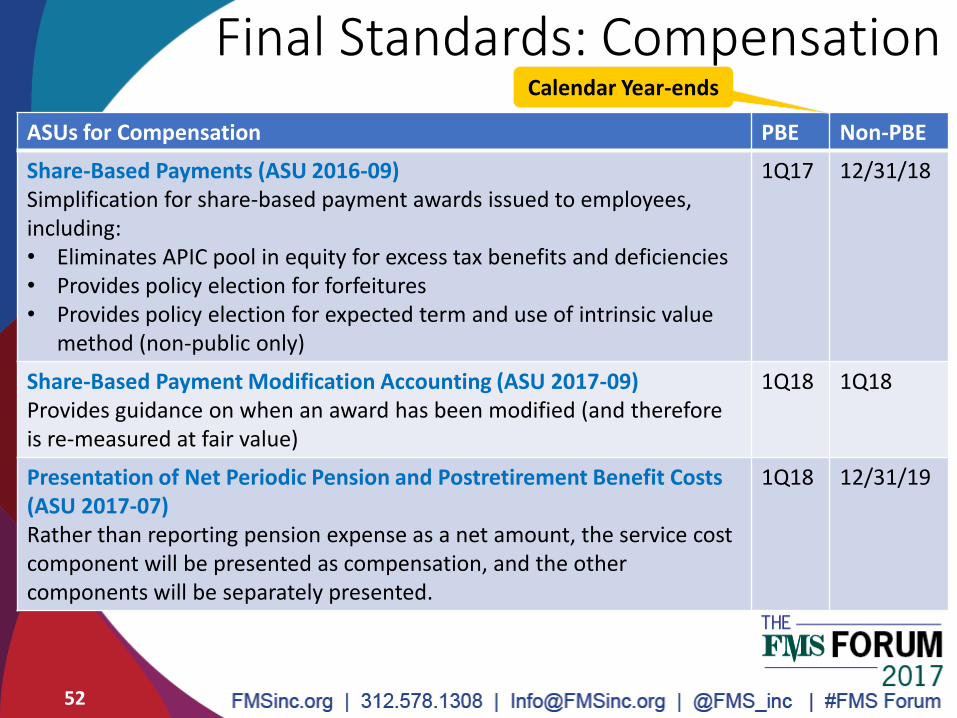

Final Standards: Compensation

ASUs for Compensation PBE Non-PBE

Share-Based Payments (ASU 2016-09) Simplification for share-based payment awards issued to employees, including: • Eliminates APIC pool in equity for excess tax benefits and deficiencies • Provides policy election for forfeitures • Provides policy election for expected term and use of intrinsic value

method (non-public only)

1Q17 12/31/18

Share-Based Payment Modification Accounting (ASU 2017-09) Provides guidance on when an award has been modified (and therefore is re-measured at fair value)

1Q18 1Q18

Presentation of Net Periodic Pension and Postretirement Benefit Costs (ASU 2017-07) Rather than reporting pension expense as a net amount, the service cost component will be presented as compensation, and the other components will be separately presented.

1Q18 12/31/19

Calendar Year-ends

52

Final Standards: Other

ASU PBE Non-PBE

Breakage for Prepaid Cards (ASU 2016-04) Applies to prepaid stored-value products redeemable for goods, services or cash (e.g., certain prepaid gift & telecomm cards, and traveler’s checks). If breakage is expected, de-recognize in proportion to pattern of rights; otherwise, derecognize which exercise is remote.

1Q18 12/31/19

Statement of Cash Flows: Certain Clarifications (ASU 2016-15) Provides guidance for 8 specific cash flows, including: • Debt prepayment or debt extinguishment costs • Contingent consideration payments after a business combination • Proceeds from insurance claim settlements • Proceeds from BOLI & COLI settlements • Distributions from equity method investees

1Q18 12/31/19

Statement of Cash Flows: Restricted Cash (ASU 2016-18) Restricted cash should be included in cash & cash equivalents

1Q18 12/31/19

Calendar Year-ends

53

Final Standards: Other

ASU PBE Non-PBE

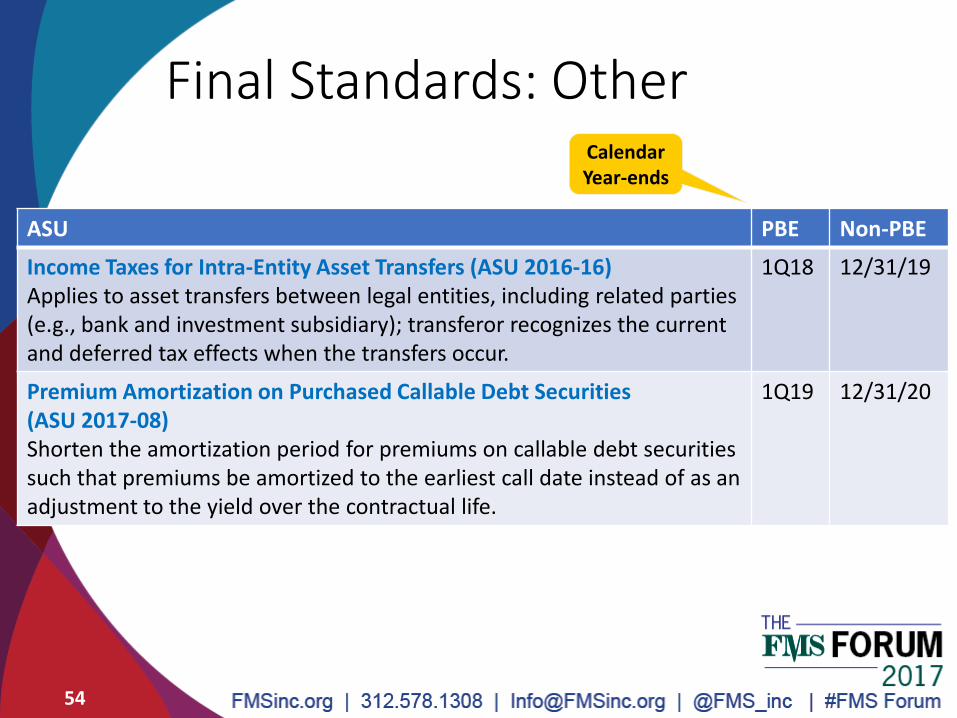

Income Taxes for Intra-Entity Asset Transfers (ASU 2016-16) Applies to asset transfers between legal entities, including related parties (e.g., bank and investment subsidiary); transferor recognizes the current and deferred tax effects when the transfers occur.

1Q18 12/31/19

Premium Amortization on Purchased Callable Debt Securities (ASU 2017-08) Shorten the amortization period for premiums on callable debt securities such that premiums be amortized to the earliest call date instead of as an adjustment to the yield over the contractual life.

1Q19 12/31/20

Calendar Year-ends

54

Purchased Callable Debt Securities

• FASB issued ASU No. 2017-08, “Premium Amortization on Purchased Callable Debt Securities,” in March 2017 • Under existing GAAP, a premium on a purchased callable debt

security generally must be amortized as a yield adjustment over the contractual life of the security

• Under the ASU, the premium will be amortized to the earliest call date, consistent with typical pricing in the market

• Effective dates • For public business entities, fiscal years, and interim periods within

those fiscal years, beginning after 12/15/2018

• For all other entities, fiscal years beginning after 12/15/2019 (and interim periods within fiscal years beginning after 12/15/2020)

• Early adoption permitted, including in an interim period

55

55

Coming Soon

• Hedging • FASB voted to issue a final standard on June 7th

• Final standard expected in August

• Forthcoming standard will better align the accounting rules with a company’s risk management activities, better reflect the economic results of hedging in the financial statements, and simplify hedge accounting treatment.

• Effective dates • Public - fiscal years beginning after Dec. 15, 2018, and interim

period within

• Private – fiscal years beginning after Dec. 15, 2019 (and interim periods for fiscal years beginning after Dec. 15, 2020)

• Early adoption will be permitted

56

On The Horizon

• Implementation Costs Incurred in a Cloud Computing Arrangement That is Considered a Service Contract • ASU 2015-05, Fees Paid in a Cloud Computing Arrangement

• Evaluate cloud computing arrangement to determine whether the arrangement provides the entity control of a license to internal-use software

• Control defined as right to take possession of software without significant cost and the ability to run software on own hardware (or contract elsewhere)

• If do not control, arrangement is a service contract and costs are expensed

• FASB added a project to address implementation costs • Include setup and other upfront fees to get the arrangement ready

for use. Other costs can include training, creating or installing an interface, reconfiguring existing systems, and reformatting data.

57

Thank you! Questions? Note: Resources Available on Following Pages……

58

Resource

• “Just Around the Corner: Apply the ‘New’ Revenue Recognition Standard to Financial Institutions”

• Issued May 25, 2017 (24 pages)

• Contents • Standardizing Revenue Recognition Practices

• Evaluating a Financial Institution’s Revenue Streams: What Is In and What Is Out?

• For Revenue in Scope: Now What?

• Disclosures

• Effective Date and Transition

https://www.crowehorwath.com/folio-pdf/Applying-the-New-Revenue-Recognition-Standard-to-Financial-Institution-FS-18200-024A.pdf

59

Audit Committee Tool for Revenue Recognition

Center for Audit Quality (CAQ) Audit Committee Tool

• Issued Dec. 13, 2016 (8 pages)

• Assists audit committees in assessing a company’s implementation status • Understanding the New Revenue Recognition

Standard – What Is It?

• Evaluating the Company’s Impact Assessment – How Will Revenue Recognition Change?

• Evaluating the Implementation Project Plan – How Do We Need to Prepare?

• Other Implementation Considerations – What Else Do We Need to Consider?

http://thecaq.org/preparing-new-revenue-recognition-standard-tool-audit-committees

60

Recommended