PIAGGIO S.p.A.Politecnico Student Research

Global Investment Research Challenge 2011

Automobiles & Parts

Company Overview

Why investin Piaggio

Financial Analysis

Valuation RiskAnalysis

Data and Charts

• Wide brand portfolio• Wide brand portfolio• Premiumisation strategy

Company Overview

Young

• Largest European producer of 2w and LCVs by revenues

Company Overview

Financial Analysis

Valuation RiskAnalysis

Data and Charts

Why investin Piaggio

Company Overview

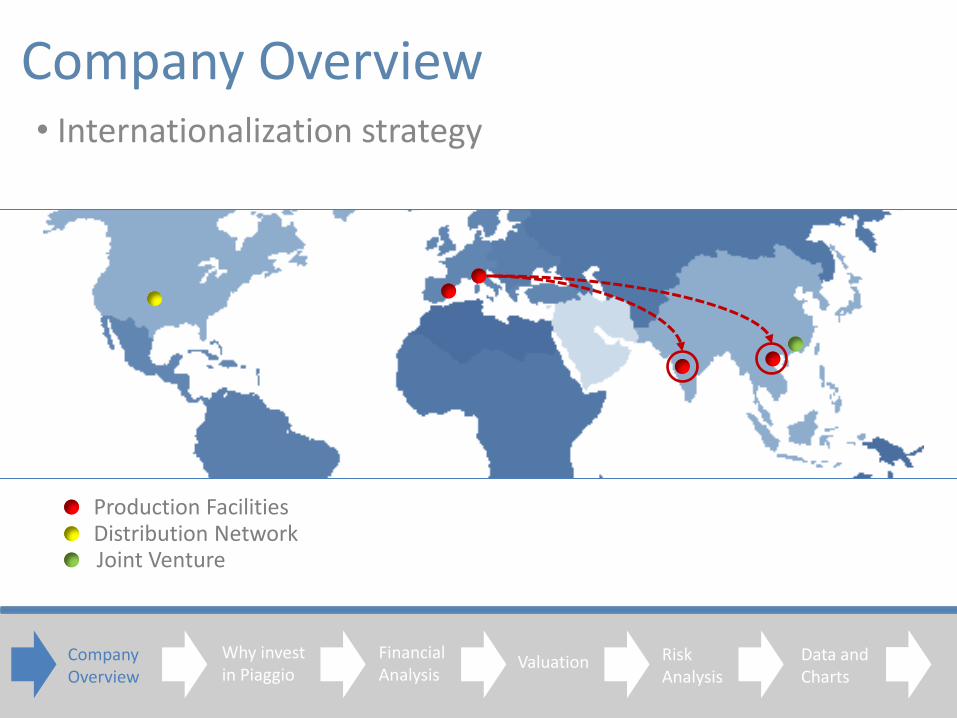

Production FacilitiesDistribution NetworkJoint Venture

• Internationalization strategy

Company Overview

Financial Analysis

Valuation RiskAnalysis

Data and Charts

Why investin Piaggio

Company Overview• Latest results

Company Overview

Financial Analysis

Valuation RiskAnalysis

Data and Charts

Europe India Vietnam

335,0002Ws

220,000LCVs 60,000

2Ws

360,0002Ws 197,000

LCVs 48,0002Ws

-7.5% +11.7% +25%

Unit Sold Vs Management Guidelines:

European Revenues (€’000)Revenues Breakdown

Source: Company Data, Politecnico EstimatesSource: Company Data

Actual Guidelines Delta

Revenues €1,485M €1,500M -1%1

Ebitda Margin 13.3% 13.3% 0%

EPS €0.115 €0.118 -2.5%

From Revenues to Earnings:

Why investin Piaggio

Company Overview• Latest results

Company Overview

Financial Analysis

Valuation RiskAnalysis

Data and Charts

• Efficiency Improvements

• Financial Savings

• Higher Materials Costs

• One-off Fiscal Items

From Revenues to Earnings:

Why investin Piaggio

Company Overview• Our Rating

Company Overview

Financial Analysis

Valuation RiskAnalysis

Data and Charts

BUY

HOLD

Price (03/31/11): €2.4112 M Target Price: €2.8Upside: 16.2%Rating: BUY

Why investin Piaggio

Indian sales report 2010 financial results

Company Overview

Why investin Piaggio

Financial Analysis

Valuation RiskAnalysis

Data and Charts

1. Launch of new products in India

2. Expansion in South-Eastern Asia

3. Consolidation in Europe

Why invest in Piaggio

Company Overview

Financial Analysis

Valuation RiskAnalysis

Data and Charts

Why investin Piaggio

Market volumes : 1M u (2010)Market growth: 8% (2011E)

Piaggio volumes: 220,000 u (2010)Piaggio growth: 13.5% (2011E)

Why invest in Piaggio: New products in India

3w

4w

Launch of Vespa: 2012EPiaggio volumes: 75,000 u (2013E)

Company Overview

Financial Analysis

Valuation RiskAnalysis

Data and Charts

25%

24%23%

18%

10%

Why investin Piaggio

Why invest in Piaggio: Expansion in Asia

Vietnam

Malaysia Indonesia

Thailand Taiwan

Potential Market: 3M vehiclesPotential Market:

11M vehicles

Company Overview

Financial Analysis

Valuation RiskAnalysis

Data and Charts

Why investin Piaggio

Why invest in Piaggio: Consolidation in Europe

EuropeanEBITDA Margin

+155bpsby 2013

• Improvement of global sourcing position

• Production plants rationalisation

• Synergies in the distribution network

Company Overview

Financial Analysis

Valuation RiskAnalysis

Data and Charts

Eco Friendly Solutions:

Piaggio Market Share: 20%

Piaggio Volumes: 335,000 units (2010)

Why investin Piaggio

Company Overview

Financial Analysis

Valuation RiskAnalysis

Data and Charts

Why investin Piaggio

€1485M €1615M €1745M €1850M7.6% Revenue CAGR 10-13Balance Sheet

Income Statement

Cash Flow Statement

+ 160bps EBITDA margin

€0.11 €0.14 €0.18 €0.22

8.8% OCF CAGR 10-13

14.8% From EMs11.9% EBITDA CAGR 10-13

Lower D&A and Financial Charges CAGR

24.3% EPS CAGR 10-13

~ €65M

~ €140M

OCF Capex ∆NWC ∆NFP Div. &Buy Back3.3% From DMs

Financial Analysis

2010 2013

Higher than Revenue CAGR

Source: Politecnico Estimates

2010 E 2011 E 2012 E 2013 E

€197M €218M €249M €276M

€153M €155M €181M €197M

2010 2011 E 2012 E 2013 E

NFP €350M €342M €318M €288M

Debt €528M €500M €470M €440M

Cash&other €155M €148M €147M €147M

Equity €443M €467M €499M €537M

Ability to meet short and long term obligations

~ €15M

~ €310M

~€530MDeleveraging while Improving ROE

Company Overview

Why investin Piaggio

Financial Analysis

Valuation RiskAnalysis

Data and Charts

Company Overview

Why investin Piaggio

Financial Analysis

Valuation RiskAnalysis

Data and Charts

• Sum-of-the-part approach

Two-Stage model Three-Stage model Analytical Period + Perpetuity Analytical Period + Convergence Stage + Perpetuity

Valuation: Discounted Cash Flow

Source: Politecnico Estimates

Company Overview

Why investin Piaggio

Financial Analysis

Valuation RiskAnalysis

Data and Charts

€963M

2.5%

9.75%

30%

€33M

7.63%

Sales 2010

Sales CAGR 10-15

EBITDA margin 2010

Tax Rate

FCFF 2010

WACC

Valuation: Discounted Cash Flow

€389M

12.9%

19.5%

42%

€13M

9.31%

€133M

13.5%

20.5%

7.5%

€10M

10.72%

Source: Politecnico Estimates

€963M

2.5%

9.75%

30%

€33M

7.63%

€133M

13.5%

20.5%

7.5%

€10M

10.72%

€2.90

€0.95

€1.30

€0.65

TP DCF EU + US India Vietnam

Company Overview

Why investin Piaggio

Financial Analysis

Valuation RiskAnalysis

Data and Charts

Median Hero Mahindra Bajaj Tata

2011 E 9.35 x 10.60 x 8.10 x 11.12 x 5.46 x

• Piaggio’s Indian and Vietnamese businesses are comparable to its Indian peers

• Using the median EV/EBITDA multiple

EV Piaggio Asia

€ 1,114M

DCF EV

€ 970.5M13% discount

Valuation: Multiple Analysis

InitiationCoverage

Why Investin Piaggio

Financial Analysis

Valuation RiskAnalysis

CompanyOverview

0%

5%

10%

15%

20%

25%

30%

35%

Piaggio-Asia Hero Honda Mahindra & Mahindra

Bajaj Auto Tata Motors

Sales growth rate (2009-11E)

Company Overview

Why investin Piaggio

Financial Analysis

Valuation RiskAnalysis

Data and Charts

Piaggio-Asia Hero HondaMahindra & MahindraBajaj Auto Tata Motors

Average EBITDA% (2010E-11E)

0%

33%

67%

100%Geographical exposure to EMs

Valuation: Multiple Analysis

As regards the whole Piaggio Group (EV/EBITDA multiple):

0%

10%

20%

30%

Sales growth rate (2009-2011)

0%

10%

20%

30%

Average EBITDA % (2010-11)EMs multiple

- for the Asian Business:

DMs multiple

- for the non-Asian Business:

9.3x 4.4x

Target Price: € 2.620%

33%

67%

100%

Business exposure to 2w market to LCVs market

Company Overview

Why investin Piaggio

Financial Analysis

Valuation RiskAnalysis

Data and Charts

• DCF Analysis:

• Multiple Analysis:

• Year-end Target Price:(upside > 15%)

€ 2.62

€ 2.90

€ 2.80

70% weight

30% weight

Valuation: Target Price

Company Overview

Why investin Piaggio

Financial Analysis

Valuation RiskAnalysis

Data and Charts

Company Overview

Why investin Piaggio

Financial Analysis

Valuation RiskAnalysis

Data and Charts

Pro

bab

lePo

ssib

le

•Instable Vietnam •Labour market

•Supply Chain risk

•Tighter regulations

•Credit risk

•Increase in interest rates

Un

likel

y

•Strikes •Intellectual Property

•Liquidity risk•De-premiumisation

Rar

e

•Machinary failure •Vehicles defects

Marginal Minor Intermediate Major

Risk analysis: Risk matrix

Impact

Like

liho

od

Source: Politecnico Estimates

• Unsuccessfulproduct launches

• Stronger competition

• Exchange rate risk

• Increase in energy,raw materials andcomponents costs

• GDP growth rates

Risk analysis: Risks from Asia

• Stronger competition

• Exchange rate risk

• Unsuccessfulproduct launches

Company Overview

Why investin Piaggio

Financial Analysis

Valuation RiskAnalysis

Data and Charts

• Exchange rate risk

• Stronger competition

• Unsuccessfulproduct launches

• Exchange rate risk

• Stronger competition

• Unsuccessfulproduct launches

Source: Politecnico Estimates

Risk analysis: Risk matrixRisk analysis: Risks from Asia

Source: Pacific Exchange Rate Service

Company Overview

Why investin Piaggio

Financial Analysis

Valuation RiskAnalysis

Data and Charts

Pro

bab

lePo

ssib

le

•Instable Vietnam •Labour market

•Supply Chain risk

•Tighter regulations

•Credit risk

•Increase in interest rates

Un

likel

y

•Strikes •Intellectual Property

•Liquidity risk•De-premiumisation

Rar

e

•Machinary failure •Vehicles defects

Marginal Minor Intermediate Major

Risk analysis: Risk matrix

Impact

Like

liho

od

Source: Politecnico Estimates

• Unsuccessfulproduct launches

• Stronger competition

• Exchange rate risk

• GDP growth rates

Risk analysis: Global risks

• GDP growth rates

• Increase in energy, raw materials andcomponents costs• Increase in energy,

raw materials andcomponents costs

Company Overview

Why investin Piaggio

Financial Analysis

Valuation RiskAnalysis

Data and Charts

• Increase in energy, raw materials andcomponents costs

• GDP growth rates

• Increase in energy, raw materials andcomponent costs

• GDP growth rates

-4

-2

0

2

4

6

8

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Real GDP growth rates

World Major advanced economies (G7) ASEAN-5

Source: International Monetary Fund, World Economic Outlook Database

Risk analysis: Risk matrixRisk analysis: Global risks

Source: Company data

Company Overview

Why investin Piaggio

Financial Analysis

Valuation RiskAnalysis

Data and Charts

• Price Confidence Interval: (€ 2.70 ; € 2.90)

Risk analysis: Montecarlo Simulation

Source: Politecnico Estimates

Company Overview

Why investin Piaggio

Financial Analysis

Valuation RiskAnalysis

Data and Charts

P = 80%

€2

.80

€2

.82

€2

.85

€2

.87

€2

.90

€2

.92

€2

.95

€2

.97

€2

.77

€2

.75

€2

.72

€2

.70

€2

.67

€2

.65

€2

.62

0

50

100

150

200

250

300

350

400

Nu

mb

ers

of

iter

atio

ns

Price of ASEAN operations Price of European operations Price of Indian operations

• 74% of volatility comes from Asia

Risk analysis: Montecarlo Simulation

Source: Politecnico Estimates

Company Overview

Why investin Piaggio

Financial Analysis

Valuation RiskAnalysis

Data and Charts

QuestionsCompany Overview

Why investin Piaggio

Financial Analysis

Valuation RiskAnalysis

Data and Charts

Questions

PIAGGIO S.p.A.Politecnico Student Research

ICFAS Investment Research Challenge 2011

Automobiles & Parts

• Hedging Policy• Costs Breakdown• Corr. Oil , Rub, All.• Sensitivity on Oil Price• Sensitivity India• Sensitivity ASEAN• Sensitivity Europe• Political risk – India 1• Political risk – India 2• Japan’s earthquake• Interest Rates Risk• MS: Assumptions• MS: Impact• MS: Results• Sensitivity on steel

• India• Vietnam• Indonesia• Malaysia• Thailand• Summary• GDP growth rates

• On The Stock Market• 2010 Results• OWC• Stock Options Plan• Tax Rate• Sales’ Seasonality• Spare Parts• Aprilia and Moto Guzzi

• Main Competitors• EU Scenario• India Scenario• US Scenario• Vietnam Scenario

• CG Snapshot• Board of Directors• CG and CSR Valuation

• EMs and DMs Multiples• Piaggio Peers• Historical P/E• P/E Future Evolution

• Assumpt. Macro Scenario• Assumpt. Cost Inflation• Terminal Value• WACC

• Debt Structure• Altman Z-Score

• Balance Sheet• Income Statement• Cash Flow Statement India• Cash Flow Statement EU• Cash Flow Statement ASEAN• Ratios• ROE

Data and Charts

Data and ElaborationsFinancial Statements:

Strategy:

Company: Competitive Scenario:

• Strategic Levers• Premiumisation• Brand Diversification• Launch of Vespa• New Urban Vehicles

Macro Scenario:

Market:• From 3w to 4w• Electric and Hybrid• Indian 4w• Margins in 2w•Motorcycle IndustryOutlook

Debt:

Acquisitions:

• Piaggio as a Prey• Potential Buyers• Piaggio’s Acquisitions

DCF Model:

Multiples:

Risks:

CG and CSR:

Company Overview

Why investin Piaggio

Financial Analysis

Valuation RiskAnalysis

Data and Charts

Data and ChartsData and Charts

Piaggio on the stock market

-

1

2

3

4

5

6

7

8

9

10

1/2

/…

2/2

/…

3/2

/…

4/2

/…

5/2

/…

6/2

/…

7/2

/…

8/2

/…

9/2

/…

10

/2…

11

/2…

12

/2…

1/2

/…

2/2

/…

3/2

/…

4/2

/…

5/2

/…

6/2

/…

7/2

/…

8/2

/…

9/2

/…

10

/2…

11

/2…

12

/2…

1/2

/…

2/2

/…

3/2

/…

Mill

ion

s

Source: Bloomberg, Politecnico Estimates

TTM Daily Average: 1.18 millions shares

(equal to 2.5-3 €M)

MARKET CAP:€ 923.98 M

FTSE Italia Mid Cap

2010 ResultsSlightly below consensus, but positive underlying trends.

• Volumes:

• Ebit Margin:

• Interests:

• Tax Rate:

• EPS:

335k Actual Vs355k Expected

220k Actual Vs195k Expected

60k Actual Vs48k Expected

7.5%. In line with consensus (+50bps from 2009)

48.9%. Higher than consensun (+12.9% from 2009)

€27.3M. In line with consensus (- €3M from 2009)

€0.115. In line with consensus (substantially in line with 2009)

European 2Ws: Indian LCVs: ASEAN 2Ws:

Data and Charts

XXX

Operating Working Capital:

Source: Bloomberg, Politecnico Estimates

€ (700)

€ (500)

€ (300)

€ (100)

€ 100

€ 300

€ 500

€ 700

2008 2009 2010 2011 E 2012 E 2013 E

Payables

Receivables

Inventories

€ (10)

€ -

€ 10

€ 20

€ 30

2008 2009 2010 2011 E 2012 E 2013 E

NWC

Mill

ion

sM

illio

ns

Data and Charts

Data and Charts

Piaggio’s Stock Option Plan

Stock Option Plan approved on 07 May 2007 and updated on 25 January 2010

The Board of Directors is responsible of the Stock Option Plan

Max 10,000,000 of granted Stock Options equal to 2.52% of the share capital

The Stock Options are European style options

Grant Date/Commencement Date

0 5

Expiration Date

3

Vesting Date

EXERCISE PERIOD

Grant Date (GD) BeneficiariesStock Options

Number

Expected

Liabiliy

Stock market

price at GDStrike Price

31 July 20083 Directors and

16 Executives 2,435,000 €1,600,000 €1.391 €1.216

03 October 2008 1 Executive 300,000 €186,600 €1.512 €1.570

15 January 2009 1 Director 390,000 €220,000 €1.1569 €1.2218

11 May 2009 2 Executives 250,000 €125,000 €1.2238 €1.2237

18 December

2009

3 Directors and

29 Executives4,720,000 €3,000,000 €1.8818 €1.826

04 January 2010 1 Executive 500,000 €350,000 €2.004 €1.892

Data and Charts

Source: Politecnico Estimates

Tax Rates

Piaggio’s tax rates by region:

Piaggio’s aggregate tax rate:

Country Tax rate

Italy 27.5%

Europe ~30%

US 35%

India 43%

Vietnam 7.5%

ASEAN ~25%

44%

Piaggio’s taxes not based on taxable income:

IRAP

Indian Dividend Distribution Tax

Data and Charts

Data and Charts

Seasonality in Piaggio’s sales

Seasonal fixed-term contracts.

Peaks’ impact on OWC is:

0

100

200

300

400

500

600

700

0

100

200

300

400

500

600

700

FQ1

20

06

FQ2

20

06

FQ3

20

06

FQ4

20

06

FQ1

20

07

FQ2

20

07

FQ3

20

07

FQ4

20

07

FQ1

20

08

FQ2

20

08

FQ3

20

08

FQ4

20

08

FQ1

20

09

FQ2

20

09

FQ3

20

09

FQ4

20

09

FQ1

20

10

FQ2

20

10

FQ3

20

10

FQ4

20

10

REVENUES from 2006 to 2010

Peak in the European

springtime.

Payables BEFORE the peak

Receivables AFTER the peak

Inventories BEFORE the peak

Data and Charts

Data and Charts

Spare parts segment

Higher marginality

PIAGGIO’S Business Units

2Ws

Scooters

Motorcycles

Spare Parts

LCVs

Spare Parts

10% of Total Revenues in 2010

Strategic for LCVs in India

New logistics center in Pontendera (Italy)

Data and Charts

Data and Charts

Aprilia and Moto Guzzi

Source: Acem

Substitution trend in Europe (‘000 units)

Two significant brands for Piaggio linked to:

increasing importance of motorbikes in the European market: a trend that has begun since the early ‘90

need to enrich and complete Piaggio’s brand diversification

Piaggio’s large investments in 2010 for them

synergies with Piaggio distribution network

Data and Charts

Piaggio Strategic Levers

Internationalization Premiumization• Design

• Environment• Safety

• Innovation• Robustness

• New markets• New products• New plants

Cost Efficiency• Improvement of global sourcing position

• Production Plants Rationalization• Sinergies in Distribution Network

Outsourcing and SCM• Production of engines

• Centralized logistic center for the spareparts business

Data and Charts

Data and Charts

Premiumisation strategy

Piaggio’s prices are higher than itscompetitors:

customersrecognize higher

quality and uniquesolutions.

Revenues COGs R&D

Premiumisation’s impact

Data and Charts

Data and Charts

Brand diversification

Wide BrandPortfolio

Wide Range ofCustomers

Data and Charts

Distribution network already present…

…but for LCVs distribution

Larger organizational structure (Piaggio India has its own CEO)

Piaggio’s R&D department improved Vespa to better target the Indian’s customers

Vespa gained a successful commercial presence in India:

..in 1960, Rahul Bajaj obtained the license to produce the Vespa in India, till 1970 when the Indian government

revoked the license. Now Piaggio has better fundamentals to compete in Indiain respect to the ‘80s and ‘90s.

XXX

Launch of Vespa: India vs Vietnam

Source: Indian news, Politecnico Estimates

Data and Charts

Scooter MP3:

- launched in October 2007- 72,000 units sold so far- hybrid models since 2009

Car prototype NT3:

- November 2010 (Milan Motor Show)- launch expected in 2012-13- three-seat city car

XXX

New types of vehicles: urban mobility

Source: News, Politecnico Estimates

Data and Charts

Piaggio as a Prey

WHAT DOES A PREDATOR GET?

•Business: 2W and LCV in Europe. 2W, 3W and 4W in India. 2W in ASEAN.

•Market Share: 20% in 2W Europe40% in 3W, 4% in 4W India Niche player in 2W ASEAN

•Revenues: €1,485M in 2010 (~$2,065M)

•Leverage: 1.2x

AT WHAT PRICE?

• Market Cap: ~€895M (~ $1,245M)

• Ownership: Immsi S.p.a. (53% share)

~€470M

~€220M • Premium to pay for the deal (+25%)

Best Case: €600M Worst Case: €1,130M

• Market Value of the Control Stake

~€420M • Pubblic Offer to Minority Shareholders(compulsory in the Italian order in case ofacquisition of the control stake)

~€20M • Fees

Data and Charts

Potential BuyersINDIAN CONGLOMERATE COMPANIES:

Automotive Business: Commercial Vehicles and Personal Vehicles. Market Share: 1% in Indian 3W LCVs and 31% in 4W.Revenues: Rs184,520 M (~$4,095M)Market Cap: $7,740MLeverage: 0.14x

Automotive Business: Commercial Vehicles and Personal Vehicles.Market Share: 57% in indian 4W LCVs.Revenues: Rs918,934 M (~$20,390M)Market Cap: $14,803MLeverage: 1.0x

Recent acquisitions: Ssangyong Motors (Korean Premium SUV manufacturer )

Recent acquisitions: Jaguar and Land Rover (2008)

BENEFITS FROM ACQUIRING PIAGGIO:

• Entry in Western Markets• Consolidation in Indian Market

• Premium Brands + Technology Transfer• Entry in 2W

Data and Charts

Data and Charts

Leader in motorbikes

Large brand portfolio

Piaggio’s acquisitionsPiaggio’s past acquisitions:

In the future Piaggio will not make acquisitions:

according to its strategy;

there are not potential takeover targets. For example:

Company Positive Negative

Ducati• High margin (18%)

• Strong distribution network• Insignificant share in

emerging markets

Scooters India• High annual capacity

• Highly cost effective product• It hasn’t a strong brand

position in 3W as Ape

Data and Charts

Data and Charts

Piaggio’s main competitorsEUROPEAN COMPETITORS INDIAN COMPETITORS

2W 2W

LCVs LCVs

Auto Auto

DRIVER PIAGGIO MAHINDRA BAJAJ TATA GM NISSAN

PRODUCT DESIGN QUALITY

PRODUCTION PROCESS QUALITY

PRICE

DISTRIBUTION NETWORK

DRIVER PIAGGIO HONDA YAMAHA BMW KYMCO SUZUKI

BRAND

DESIGN

ENGINE INNOVATION

QUALITY

PRICE

Data and Charts

Data and Charts

Competitive scenarios: EUSegment Total market

sales (2010)Piaggio’s Market

share (2010)

Motorcycles total 1,548,000 20%

Scooters 970,000 27%

Motorbikes 578,000 7%

LCVs 1,500,000 0.92%

Data and Charts

Data and Charts

Competitive scenarios: India

Data and Charts

Data and Charts

Competitive scenarios: the US

€82 €79

€95

€61

€22

$103 $109

$140

$85

$29

20

70

120

2006 2007 2008 2009 2010

Mill

ion

s

US net sales Euro (€) USD ($)

March 8°, 2011, Piaggio US changed its CEO: Paolo Timoni > Miguel Martinez

Market with very peculiarrequirements and customer needs.

Data and Charts

Strong impact of the economiccrisis. 60% reduction in volumes

Scooter segment: 5% of total in 2010, down from 12% in 2007

Piaggio’s market share in scooter market: 30% (6,700 vehicles)

700

800

900

1000

1100

1200

1300

1400

1500

2006 2007 2008 2009 2010 2011 2012

GDP per capita (US $)

India

Vietnam

Data and Charts

Competitive scenarios: Vietnam

90% of total vehicles in Vietnam are scooters(motorbike segment: absent)

0

5

10

15

20

25

2006 2007 2008 2009 2010 2011 2012

CPI Inflation (%)

India

Vietnam

Vietnamese market accounts2,800,000 vehicles sold in 2010

Source: IMF Source: IMF

Data and Charts

Macroeconomic data 2009 2010 2011 2012 2015

Real GDP growth (%) 5.678 9.668 8.373 7.976 8.128

GDP per capita (US $) 1,031.59 1,176.06 1,296.68 1,410.64 1,856.76

Inflation CPI (%) 10.882 13.187 6.668 4.693 4.033

Population (Millions) 1,199.06 1,215.94 1,232.68 1,249.28 1,299.24

Industry data 2009 2010 2011 2012 2015

2w total sales 7,437,619 9,371,231 10,148,600 10,990,000 13,959,500

3w total sales 349,727 440,368 468,500 498,000 600,500

4w LCVs total sales 384,194 531,395 584,500 642,000 855,800

Macro scenario: India

Data and Charts

Macroeconomic data 2009 2010 2011 2012 2015

Real GDP growth (%) 5.323 6.468 6.817 7.044 7.485

GDP per capita (US $) 1,068.26 1,155.57 1,272.18 1,387.16 1,771.85

Inflation CPI (%) 6.717 8.4 8 6.05 5

Unemployment rate (%) 6 5 5 5 5

Population (Millions) 87.211 88.257 89.316 90.388 93.681

Macro scenario: Vietnam

Data and Charts

Macroeconomic data 2009 2010 2011 2012 2015

Real GDP growth (%) 4.546 6 6.2 6.5 7

GDP per capita (US $) 2,329.45 2,963.28 3,270.01 3,532.00 4,440.58

Inflation CPI (%) 4.814 5.066 5.5 5.357 3.714

Unemployment rate (%) 8 7.5 7 6.5 7

Population (Millions) 231.547 234.557 237.606 240.695 250.205

Macro scenario: Indonesia

Data and Charts

Macroeconomic data 2009 2010 2011 2012 2015

Real GDP growth (%) -1.714 6.716 5.3 5.2 5

GDP per capita (US $) 6,950.47 7,754.99 8,238.51 8,748.81 10,455.22

Inflation CPI (%) 0.6 2.2 2.1 2.3 2.5

Unemployment rate (%) 3.7 3.5 3.2 3.1 3

Population (Millions) 27.761 28.233 28.713 29.201 30.716

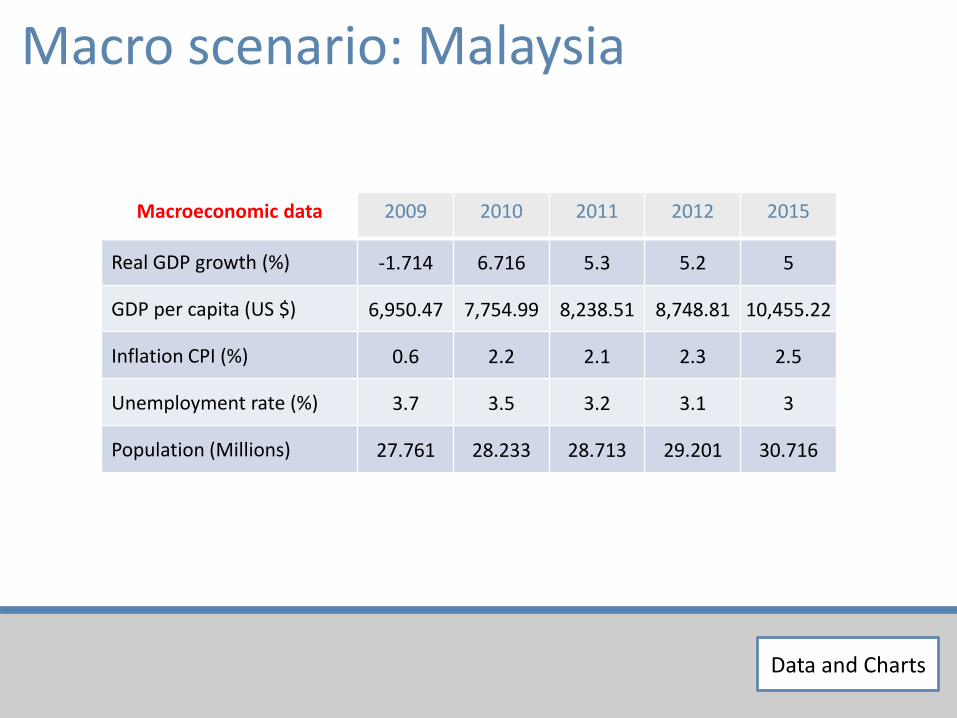

Macro scenario: Malaysia

Data and Charts

Macroeconomic data 2009 2010 2011 2012 2015

Real GDP growth (%) -2.248 7.522 4.001 4.25 5

GDP per capita (US $) 3,940.97 4,620.71 4,888.46 5,161.49 6,268.62

Inflation CPI (%) -0.846 3.047 2.755 2.53 1.954

Unemployment rate (%) 1.39 1.39 1.39 1.39 1.39

Population (Millions) 66.983 67.653 68.33 69.013 71.104

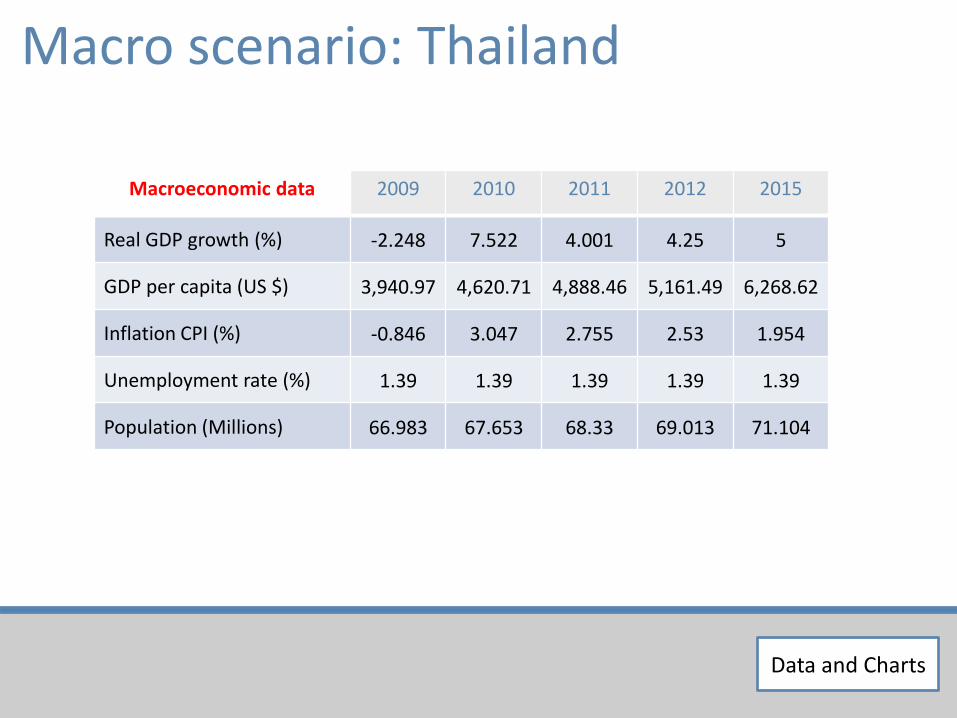

Macro scenario: Thailand

Data and Charts

0.00

2,000.00

4,000.00

6,000.00

8,000.00

10,000.00

India Indonesia Malaysia Thailand Vietnam

GDP per capita (US $)

2009

2010

2011

2012

2015

-2

0

2

4

6

8

10

12

14

India Indonesia Malaysia Thailand Vietnam

Inflation, CPI (%)

2009

2010

2011

2012

2015

1,215.94

234.557

28.233

67.653 88.257

Population (Millions, 2010)

India

Indonesia

Malaysia

Thailand

Vietnam

Population CAGR 2010-15

India 1.33%

Indonesia 1.30%

Malaysia 1.70%

Thailand 1.00%

Vietnam 1.20%

Macro scenario: Summary

Data and Charts

Shift from 3 to 4 wheel LCVs

Market segment

2003-2010CAGR

2010 Volumes

Piaggio’s market

share (2010)

3W 6.46% 500,000 40%

4W 10.74% 350,000 4%

Piaggio’s Productlaunches (4W)

Quargo Ape Truck

Data and Charts

Electric and hybrid markets

MP3 Hybrid Electric Porter Bifuel Porter

Max speed 62 miles/h 34 miles/h 80 miles/h

GHGs reduction 60% 100% 20%

Range (electric) 12 miles 66 miles -

Full-charge time 3 hours 8 hours -

Cost 11,000 $ 30,000 $ 16,500 $

India Europe USA

Presence ofPiaggio’s Eco line

No Yes Yes

Competitors TVS, HeroElectric

Yamaha (2011E),Honda (2011E)

KTM (2011E), EVTAmerica, ZEV, etc.

5,000 electric Porter sold in 10 years, leader in the

niche “Green” Market

MP3 Hybrid

Porter

Data and Charts

XXXWe do not believe margins will suffer in the next years

Source: Company’s financial statements, Politecnico Estimates

Indian market of 4w LCV’s: growing 10% YoY Price competition is not a rational strategy

Piaggio’s strategic positioning: quality leadership vs. cost leadership Piaggio’s products have a higher fuel efficiency in respect to competitors’ products

GM and Nissan start from scratch, while Piaggio is operating in India since 1999with 560 dealers across the country

Indian 4w market

Data and Charts

Europe and U.S. Low margins, but on the way to

increase, due to:- plant rationalization (elimination

of the factories in Spain)- the market will slowly recover

Vietnam and ASEAN: Higher margins, slightly decreasing

(conservative forecasting)- lower cost of labor;- advanced know-how in respect to

emerging markets’ based companies

XXX

20.0%

20.5%

21.0%

21.5%

22.0%

22.5%

23.0%

2011 E 2012 E 2013 E 2014 E 2015 E

ASEAN EBITDA %

10.0%

10.5%

11.0%

11.5%

12.0%

2011 E 2012 E 2013 E 2014 E 2015 E

EU and US EBITDA %

Margins in the 2w market

Source: Bloomberg, Politecnico Estimates

Data and Charts

Data and Charts

Motorcycle industry: world outlookCountry 2010 2009 Growth

Italy 294,000 389,000 -24.42%France 210,000 226,000 -7.08%Spain 106,000 106,500 -0.47%

Germany 89,000 113,000 -21.24%UK 29,000 31,868 -9.00%

USA 27,000 30,337 -11.00%Brasil 375,000 277,778 35.00%India 2,600,000 2,460,377 5.67%

Indonesia 6,700,000 5,321,684 25.90%Vietnam 2,700,000 2,263,202 19.30%

Thailandia 1,500,000 1,247,920 20.20%Malesia 428,000 407,619 5.00%

Philippine 402,000 328,969 22.20%

Country 2010 2009 Growth

India 11,300,000 9,300,000 21.51%China 16,000,000 17,391,304 -8.00%

Indonesia 7,600,000 5,801,527 31.00%Vietnam 2,750,000 2,305,113 19.30%

Thailandia 1,850,000 1,537,822 20.30%Philippine 768,000 619,355 24.00%Malesia 451,000 429,524 5.00%Taiwan 541,000 477,915 13.20%

USA 496,000 520,000 -4.62%Brasil 1,800,000 1,563,858 15.10%Italy 393,000 504,116 -22.04%

France 343,000 370,565 -7.44%Spain 167,000 174,278 -4.18%

Germany 181,000 213,000 -15.02%UK 96,000 111,630 -14.00%

Motorcycles Scooters

Country 2010 2009 Growth

Italy 99,000 115,116 -14.00%France 133,000 144,565 -8.00%Spain 61,000 67,778 -10.00%

Germany 92,000 100,000 -8.00%UK 67,000 79,762 -16.00%

USA 412,000 489,000 -15.75%Brasil 1,400,000 1,262,399 10.90%India 8,700,000 6,839,623 27.20%

Indonesia 648,000 514,286 26.00%Vietnam - - -

Thailandia 366,000 290,476 26.00%Malesia 73,000 60,331 21.00%

Philippine 22,000 20,952 5.00%

Data and Charts

Source: Company Data, Politecnico Estimates

Data and Charts

Balance Sheet2008 2009 2010 2011 E 2012 E 2013 E

FIXED ASSETS 899,186 892,251 909,909 917,080 920,218 923,412

Intangible assets 648,234 641,254 652,622 655,611 656,929 658,271

Tangible assets 250,354 250,415 256,759 260,887 262,707 264,559

Financial assets 598 582 528 582 582 582

NET WORKING CAPITAL (3,726) 17,212 30,553 52,103 72,844 92,798

Current trade receivables 90,278 103,164 90,421 103,292 116,800 129,597

Other current receivables 21,380 24,198 23,300 25,823 27,893 29,622

Other non-current receivables 12,587 12,914 12,655 13,718 14,818 15,737

Inventories 257,961 252,496 240,066 264,685 289,385 309,182

Trade payables (362,224) (345,987) (352,627) (377,660) (402,699) (425,820)

Short term Tax receivables 27,772 23,979 44,200 40,200 39,400 37,000

Long term Tax receivables 8,166 4,990 967 4,708 4,708 4,708

Deferred tax assets 36,227 46,462 46,294 42,994 42,994 42,994

Short term Tax payables (19,065) (18,952) (19,290) (19,102) (19,102) (19,102)

Long term Tax payables (166) - (3,361) - - -

Other short term payables (70,677) (79,567) (69,503) (75,855) (87,164) (92,569)

Other long term payables (5,965) (6,485) (5,961) (6,294) (6,799) (7,220)

PROVISIONS (137,531) (133,685) (131,100) (124,680) (123,807) (122,733)

NET CAPITAL EMPLOYED 757,929 775,778 785,970 808,645 816,645 824,808

NET FINANCIAL POSITION 359,708 351,976 349,938 341,645 317,957 287,535

Short term debt 140,691 113,178 156,800 140,000 110,000 90,000

Long term debt 264,789 443,164 371,048 360,000 360,000 350,000

Other liquid assets 5,787 4,127 23,051 10,000 5,000 5,000

Cash 39,985 200,239 154,859 148,355 147,043 147,465

TOTAL SHAREHOLDER’S EQUITY 398,221 423,802 442,890 467,000 498,688 537,273

SOURCES OF FUNDS 757,929 775,778 785,970 808,645 816,645 824,808

Data and Charts

Source: Company data, Politecnico Estimates

2008 2009 2010 2011 E 2012 E 2013 ENet Sales 1,570,060 1,486,882 1,485,304 1,613,932 1,743,286 1,851,390

Reported Growth -7.2% -5.3% -0.1% 8.7% 8.0% 6.2%

Business Units

Two Wheeler Vehicles 1,180,666 1,065,417 988,015 1,063,383 1,154,554 1,224,789

Reported Growth -8.8% -9.8% -7.3% 7.6% 8.6% 6.1%

Commercial Vehicles 389,394 421,465 497,289 550,549 588,732 626,600

Reported Growth 2.4% 8.2% 18.0% 10.7% 6.9% 6.4%

Geographical Area

Europe and America 1,280,932 1,116,191 963,253 1,008,187 1,038,362 1,060,882

Reported Growth -8.6% -12.9% -13.7% 4.7% 3.0% 2.2%

India 243,972 286,753 388,890 448,934 527,477 590,348

Reported Growth 2.5% 17.5% 35.6% 15.4% 17.5% 11.9%

ASEAN 45,156 83,938 133,161 156,810 177,447 188,000

Reported Growth -13.2% 85.9% 58.6% 17.8% 13.2% 5.9%

Other operating income 133,474 135,938 121,128 130,728 134,233 140,706

Cost for materials (936,603) (871,653) (881,075) (963,517) (1,040,742) (1,107,131)

Cost for services (292,920) (272,065) (258,358) (279,210) (294,615) (307,331)

Employee costs (250,967) (242,916) (240,115) (251,773) (256,263) (262,897)

Other operating costs (33,993) (35,387) (29,821) (32,279) (36,609) (38,879)

EBITDA 189,051 200,799 197,063 217,881 249,290 275,857 EBITDA margin 12.04% 13.50% 13.27% 13.50% 14.30% 14.90%

D&A 94,540 96,378 86,006 94,560 101,459 103,261

% Capex 91.85% 102.76% 89.50% 93.00% 97.00% 97.00%

EBIT 94,511 104,421 111,057 123,321 147,831 172,596 EBIT margin 6.02% 7.02% 7.48% 7.64% 8.48% 9.32%

Financial charges (41,288) (33,275) (33,905) (32,725) (32,548) (31,570)

% Tot Financial Liabilities 10.18% 5.98% 6.42% 6.55% 6.93% 7.18%

Other Financials 6,410 2,947 6,625 3,000 3,000 3,000

Earnings before tax 59,633 74,093 83,777 93,596 118,283 144,026 Taxation for the period 16,302 26,674 40,983 41,182 50,862 61,931

Actual tax rate (%) 27.34% 36.00% 48.92% 44.00% 43.00% 43.00%

Consolidated net income 43,331 47,419 42,794 52,413 67,421 82,095 Profit margin 2.76% 3.19% 2.88% 3.25% 3.87% 4.43%

Minority Shareholders 330 1,388 30 262 337 410

Earnings per share (€) 0.11 0.116 0.115 0.14 0.18 0.22 Avg. number of Ordinary Shares 396,041 396,041 371,793 371,793 371,793 371,793

Dividend per share (€) 0.06 0.07 0.07 0.08 0.10 0.12 Earnings paid as dividends 22,120 25,795 26,000 28,303 35,733 43,510

Payout Ratio 51% 56% 61% 54% 53% 53%

Income Statement

Data and Charts

Source: Politecnico Estimates

Data and Charts

Cash Flow Statement IndiaINDIA 2011 E 2012 E 2013 E 2014 E 2015 E

LCV volumes (units) 243,756 258,381 271,817 285,408 299,393

LCV ARPU (€) 1,842 1,910 1,977 2,036 2,097

2w volumes (units) 50,000 75,000 95,000 110,000

2w ARPU (€) 680 707 735 765

Sales from India 448,934 527,477 590,348 650,970 712,000

% tot sales 27.82% 30.26% 31.89% 33.38% 34.71%

% growth 15.44% 17.50% 11.92% 10.27% 9.38%

EBITDA from India 87,542 102,331 114,528 124,986 134,568

EBITDA margin India 19.50% 19.40% 19.40% 19.20% 18.90%

D&A India 22,877 24,580 25,017 25,206 25,309

% Capex India 90.00% 94.00% 94.00% 94.00% 94.00%

EBIT from India 64,665 77,750 89,511 99,780 109,259

EBIT margin India 14.40% 14.74% 15.16% 15.33% 15.35%

Tax Rate India 42.00% 42.00% 42.00% 42.00% 42.00%

Op. Tax India 27,159 32,655 37,594 41,908 45,889

Adj. Op. Tax India 34,713 40,725 47,069 52,582 57,556

Adj. Tax Rate India 53.68% 52.38% 52.58% 52.70% 52.68%

D&A India 22,877 24,580 25,017 25,206 25,309

Change in NWC India (4,363) (2,262) (2,265) (1,005) (84)

Cash Flow From Indian Operations 48,466 59,343 65,194 71,399 76,928

Capex India 25,419 26,149 26,614 26,815 26,924

% Capex 25.00% 25.00% 25.00% 25.00% 25.00%

FCFF India 23,046 33,194 38,580 44,585 50,004

% growth 44.03% 16.23% 15.56% 12.15%

Data and Charts

Source: Politecnico Estimates

Data and Charts

Cash Flow Statement Europe and USEUROPE and US 2011 E 2012 E 2013 E 2014 E 2015 E

2W volumes (units) 352,275 362,843 370,100 373,801 377,539

2W ARPU (€) 2,573 2,599 2,625 2,651 2,678

LCV volumes (units) 13,165 12,560 11,982 11,431 10,905

LCV ARPU (€) 7,718 7,584 7,452 7,323 7,195

Sales from Europe and US 1,008,187 1,038,362 1,060,882 1,074,822 1,089,504

% tot sales 62.47% 59.56% 57.30% 55.11% 53.11%

% growth 4.66% 2.99% 2.17% 1.31% 1.37%

EBITDA from Europe and US 98,802 110,066 119,880 121,455 123,114

EBITDA margin Europe and US 9.80% 10.60% 11.30% 11.30% 11.30%

D&A Europe and US 61,007 63,386 64,512 64,999 65,264

% Capex Europe and US 100.00% 101.00% 101.00% 101.00% 101.00%

EBIT from Europe and US 37,796 46,680 55,368 56,456 57,850

EBIT margin Europe and US 3.75% 4.50% 5.22% 5.25% 5.31%

Tax Rate Europe and US 30.00% 30.00% 30.00% 30.00% 30.00%

Op. Tax Europe and US 11,339 14,004 16,610 16,937 17,355

Adj. Op. Tax Europe and US 15,754 18,849 22,471 22,976 23,532

Adj. Tax Rate Europe and US 41.68% 40.38% 40.58% 40.70% 40.68%

D&A Europe and US 61,007 63,386 64,512 64,999 65,264

Change in NWC Europe and US (3,265) (869) (811) (231) (20)

Cash Flow From EU Operations 79,783 90,348 96,597 98,248 99,562

Capex Europe 61,007 62,758 63,873 64,356 64,618

% Capex 60.00% 60.00% 60.00% 60.00% 60.00%

FCFF Europe 18,777 27,590 32,725 33,892 34,943

% growth 17.54% 12.71% 5.53% 1.42%

Data and Charts

Source: Politecnico Estimates

Data and Charts

Cash Flow Statement ASEANASEAN 2011 E 2012 E 2013 E 2014 E 2015 E

2W volumes (units) 76,160 93,677 112,412 132,646 153,870

2W ARPU (€) 2,059 1,894 1,781 1,692 1,624

Sales from ASEAN 156,810 177,447 200,160 224,379 249,869

% tot sales 9.72% 10.18% 10.81% 11.51% 12.18%

% growth 17.76% 13.16% 12.80% 12.10% 11.36%

EBITDA from ASEAN 31,676 35,667 40,232 44,651 49,224

EBITDA margin ASEAN 20.20% 20.10% 20.10% 19.90% 19.70%

D&A ASEAN 11,896 13,336 14,371 14,480 14,539

% Capex ASEAN 78.00% 85.00% 90.00% 90.00% 90.00%

EBIT from ASEAN 19,779 22,331 25,861 30,171 34,685

EBIT margin ASEAN 12.61% 12.58% 12.92% 13.45% 13.88%

Tax Rate ASEAN 7.50% 7.50% 7.50% 7.50% 7.50%

Op. Tax ASEAN 1,483 1,675 1,940 2,263 2,601

Adj. Op. Tax ASEAN 3,794 3,993 4,677 5,490 6,305

Adj. Tax Rate ASEAN 19.18% 17.88% 18.08% 18.20% 18.18%

D&A ASEAN 11,896 13,336 14,371 14,480 14,539

Change in NWC ASEAN (1,211) (504) (675) (335) (29)

Cash Flow From ASEAN Operations 26,671 31,170 34,880 38,826 42,890

Capex ASEAN 15,252 15,690 15,968 16,089 16,155

% Capex 15.00% 15.00% 15.00% 15.00% 15.00%

FCFF ASEAN 11,419 15,480 18,912 22,737 26,735

% growth 35.56% 22.17% 20.22% 17.59%

Data and Charts

Source: Company data, Politecnico Estimates

RatiosKey Financial Ratios 2009 2010 2011E 2012E 2013E 2009 2010 2011E 2012E 2013E

Profitability ratios

EBITDA margin 13.50% 13.27% 13.50% 14.30% 14.90% ROI 6.67% 7.18% 7.85% 9.19% 10.49%

EBIT margin 7.02% 7.48% 7.64% 8.48% 9.32% ROA 3.03% 2.77% 3.34% 4.19% 4.99%

EBT margin 4.98% 5.64% 5.80% 6.79% 7.78% ROE 11.19% 9.66% 11.22% 13.52% 15.28%

Cost structure Du Pont Analysis

Labor Cost / Sales 16.34% 16.17% 15.60% 14.70% 14.20% Profit Margin 3.19% 2.88% 3.25% 3.87% 4.43%

Materials Cost / Sales 58.62% 59.32% 59.70% 59.70% 59.80% Asset Turnover 0.95x 0.96x 1.03x 1.08x 1.13x

Services Cost / Sales 18.30% 17.39% 17.30% 16.90% 16.60% Total Assets/Equity 3.69x 3.49x 3.36x 3.22x 3.06x

Gearing ratios Debt ratios

Net Debt to Equity 0.83x 0.79x 0.73x 0.64x 0.54x Interest coverage ratio 3.44x 4.07x 4.15x 5.00x 6.04x

Total Debt to Equity 1.31x 1.19x 1.07x 0.94x 0.82x Net Debt / EBITDA 0.57x 0.56x 0.64x 0.78x 0.96x

Liquidity ratios Cash flow ratios

Current ratio 1.05x 0.93x 0.94x 0.99x 1.02x OCF / Sales 10.93% 10.28% 9.60% 10.37% 10.62%

Solvency ratio 0.26x 0.24x 0.29x 0.36x 0.42x OCF / Earnings 3.43x 3.57x 2.96x 2.68x 2.40x

Market Ratios Capex

EPS €0.116 €0.115 €0.141 €0.181 €0.221 Capex / Sales 6.31% 6.30% 6.00% 5.85% 5.75%

DPS €0.07 €0.07 €0.08 €0.10 €0.12 D&A / Capex 6.48% 5.79% 5.86% 5.82% 5.58%

Data and Charts

Source: Starmine Smart Income Statements, Politecnico Estimates

ROE Piaggio and its competitors

Expectations and Du Pont analysis

Yamaha Suzuki Honda Piaggio Harley Mahindra Tata Bajaj Hero

2010 (2.0%) 3.6% 6.4% 9.7% 12% 31.9% 35.6% N.A. 61.4%

2011E 2.4% 5.4% 12.1% 11.2% 22.9% 28.2% 57.2% 66.8% 48.8%

ROE Earnings / EBT EBT / EBIT EBIT / Sales Sales / Assets Assets/ Equity

2010 9.66% 0.51 0.75 0.075 0.96 3.49

2011E 11.22% 0.56 0.76 0.076 1.03 3.36

2012E 13.52% 0.57 0.80 0.085 1.08 3.22

2013E 15.28% 0.57 0.83 0.093 1.13 3.06

Source: Politecnico Estimates

TaxBurden

Interest Burden

EbitMargin

AssetTurnover

Leverage(Proxy)

Data and Charts

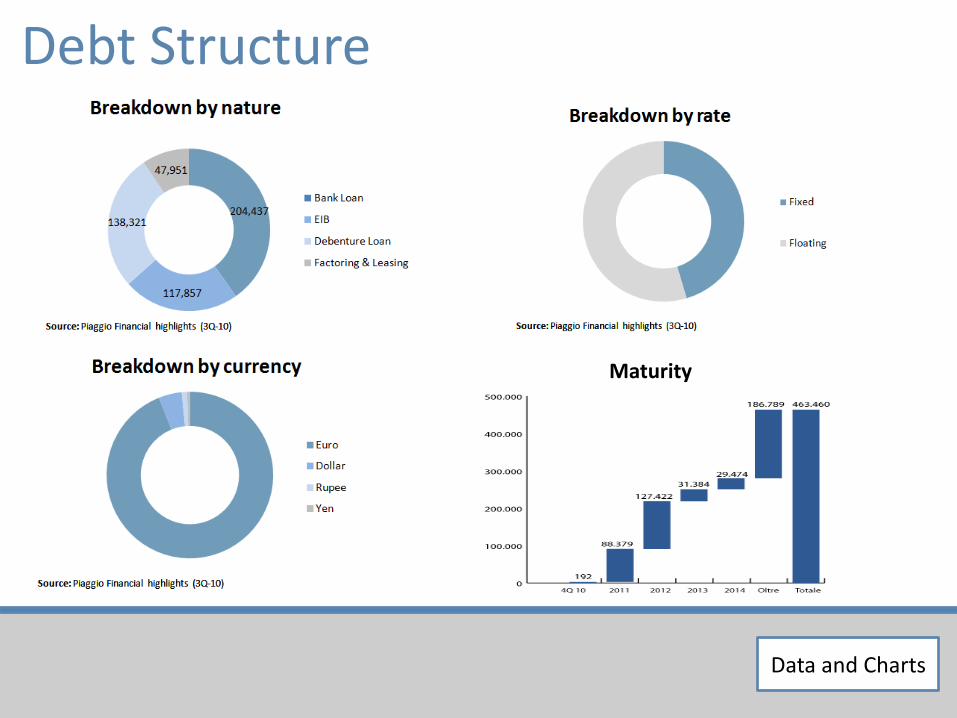

Debt Structure

Maturity

Data and Charts

Altman Z-Score

Time series of Piaggio’s Z-Score Competitors’ Z-score (2010)

Source: Bloomberg

Automotive players Indian PlayersExpectation

Data and Charts

Assumptions on Macro Scenario

Raising interest rates Raising Cost of DebtRaising commodities’prices Raising Cost of Materials

Global recovery stronger in EMs than in DMs Increasing revenues from EMs

∆=5.5%∆=4.5%

Source: Politecnico Estimates, www.economywatch.com Source: Bank or America Estimates , Politecnico Estimates

Data and Charts

Assumptions on Cost Inflation

• Decreasing cost of labour

• Increasing cost of materials

• Decreasing G&A Costs

• Cost structure:

• Increasing Ebitda Margin:

Data and Charts

Terminal Value

Two-Stage model Three-Stage model Analytical Period + Perpetuity

Ability of the company to generate cash flow

• Convergence Stage: Exponential Decay of FCFF Growth Rates

• Perpetuity: Long Term FCFF Growth Rate = 0.5%

• Sum-of-the-Parts Approach:

High Medium Low

Strongly developing 3-5% 2-3% 0-1%

Moderately developing 1.5 - 2.5% 1-2% 0%

Stable 0-1% 0% 0%

Decadent 0% 0% 0%

Industry

Source: Guatri (1998)

Analytical Period + Convergence Stage + Perpetuity

+

Source: Politecnico Estimates

Data and Charts

XXX

Source: Company’s financial statements, Bloomberg, (1) Damodaran, Politecnico Estimates

• NWC Historical evolution

EU & US

INDIA Asean Notes:

7.63% 9.31% 10.72%

Gearing Ratio (D/E) 0.7Target declared by the company

Cost of Debt 5.58%

Marginal tax rate 43% Corporate tax rate

Gross cost of debt 9.79%1/3 of debt is indexed to Euribor

Cost of Equity 10.76% 13.61% 16.01%

Beta ß 1.00Measured on 5Y of weekly returns

Risk free rate 4.81%Yield on Italian Gov. Debt (21.01.11)

Equity market premium 5.20%Implied market premium (1) (01.01.11)

Country risk premium 0.75% 3.60% 6.00% Country’s default spread adjusted by 1.5 times (1)

WACC

Data and Charts

Basic Assumptions:• EBITDA margin is 50% higher in EMs• Markets’ exposure is equal to the percentage of

Sales in EMs

EV/EBITDA multiple for the whole Company:

EMs multiple:• Equal to the Indian peers’ multiple = 9.3 x

DMs multiple:• Mkt_Multiple = (EBITDA_DMs x Multiple_DMs) + (EBITDA_EMs x Multiple_EMs)

known estimated estimated 9.3 x4.4 x

EMs and DMs Multiples.

Data and Charts

Data and Charts

Piaggio's currentmarket multiple

MedianHero

HondaMahindra & Mahindra

BajajAuto

Tata Motors

Yamaha Motor

Harley-Davidson

KtmAG

Honda Motor

SuzukiPeugeot Citroen

EV/EBITDA 2011E median = 9.3 2011E median = 7.2

2011E 5.75 8.31 10.6 8.1 11.1 5.5 5.5 13.2 9.4 8.5 3.5 5.8

2012E 5.10 6.51 9.5 N/A 10.3 4.7 4.8 10.7 N/A 7.8 3.1 5.3

Price/Earnings 2011E median = 12.9 2011E median = 16.1

2011E 16.7 13.04 12.8 13.1 14.8 8.0 13.0 19.2 35.3 11.6 18.7 5.9

2011E (1) 13.92 12.8 13.1 14.8 - 13.0 19.2 35.3 - - -

2012E 13.3 10.89 11.5 11.4 12.9 6.6 10.2 15.3 24.5 10.2 15.8 4.3

Price/Book Value2011E 1.93 2.65 4.9 2.9 7.1 2.9 1.5 3.9 2.4 1.3 1.1 0.5

2011E (1) 3.39 4.9 2.9 7.1 - 1.5 3.9 2.4 - - -

2012E 1.81 2.10 4.0 N/A 5.1 2.1 1.3 4.3 2.1 1.1 1.0 0.4

Piaggio MedianHero

HondaMahindra & Mahindra

BajajAuto

Tata Motors

Yamaha Motor

Harley-Davidson

KtmAG

Honda Motor

SuzukiPeugeot Citroen

Sales’ CAGR 2008-11E 4.1% -1% 14% 17% 21% 20% -3% -6% -4% -3% -3% 1%

EBITDA margin (2) 13.5% 12% 15% 18% 20% 13% 8% 23% 12% 11% 9% 9%

EBITDA growth (3) 10.0% 11% 9.5% 12.1% 16.7% 26.4% 18.6% 32.2% 8.2% 7.7% 9.7% 3.5%

EBIT margin (2) 8.0% 8% 14% 15% 20% 10% 5% 17% 5% 6% 4% 3%

Profit margin (2) 3.2% 6% 12.1% 8.9% 15.0% 6.5% 2.5% 8.8% 2.1% 5.5% 1.9% 1.9%

EPS growth (3)

15.2 % 21% 9.7% 13.0% 21.8% 32.9% 20.4% 119.4%-

11.5% 11.5% 25.7% 24.4%

Leverage (D/E) 0.4 0.3 0.0 0.2 0.0 0.4 0.2 0.5 0.3 0.5 0.0 3.5

(1) no automotive peers(2) 2010-11E Average(3) 2011E

Piaggio and its peers (CY 2011E):Global playersIndian based players

Source: Bloomberg, Politecnico Estimates (03.25.2011)

Data and Charts

25.8

8.5

7.1

19.2

16.7

19.2

0.0

5.0

10.0

15.0

20.0

25.0

30.0 forward P/E ratio

Historical P/E:

Average: 15.7

Source: Bloomberg, Politecnico Estimates (03.25.2011)

Data and Charts

0.18

0.15

0.11 0.12 0.12

0.14

0.18

0.22

0.25

0.27

0.03

0.06 0.06 0.07 0.07

0.08

0.10

0.12 0.13

0.14

2006 2007 2008 2009 2010 2011 E 2012 E 2013 E 2014 E 2015 E

Earnings per share (figures in €)

Dividend per share (figures in €)

XXX

Source: Bloomberg, Politecnico Estimates (03.25.2011)

(1) FTM P/E ratio

EPS P/E (1)

2010 € 0.12 20.1

2011 E € 0.14 16.7

2012 E € 0.18 13.3

2013 E € 0.22 11.0

2014 E € 0.25 9.8

2015 E € 0.27 9.3

P/E future evolution:CAGR EPS

PEG ratio

2010-13E 24.5% 0.68

2010-15E 18.3% 0.91

2006-10 -14.4%

Data and Charts

Piaggio’s Hedging PolicyRisk area Risk Hedging Policy

Strategicrisks

Unsuccessful product launches Local R&D departments, continuous investment, frequentintroduction of innovative products.

Stronger competition Focus on premiumisation and differentiation; frequentintroduction of innovative products.

GDP growth rates Flexible structure, fixed term employment contracts and CIGO funds to align production capacity with demand.

Operative risks

Increase in energy, row mat. and components costs

Multi-year supply contracts, premiumisation strategy, bargain power.

IP and brand plagiarism risk Legal protection (patents), with exception to India, wherelaws are not strict enough.

Vehicles defects Strict quality controls both on finished products and on inbound components.

Financial risks

Exchange rate risk Derivatives purchase and sell operations on 100% of the transaction risk and on 66% of the translation risk. Fluctuations are also mitigated with natural hedging.

Liquidity risk Strong cash generation and committed lines available (€150mln unrevocable, €125 mln revocable).

Interest rate risk Half debt is fixed rate. Derivatives for variable rate debt.

Credit risk Low concentration (17,500 dealers); agreements for the transfer of trade recievables without recourse.

Complian. Tighter regulations CSR policy, R&D investments, auditing by indep. auditors.

Data and ChartsSource: Company annual report

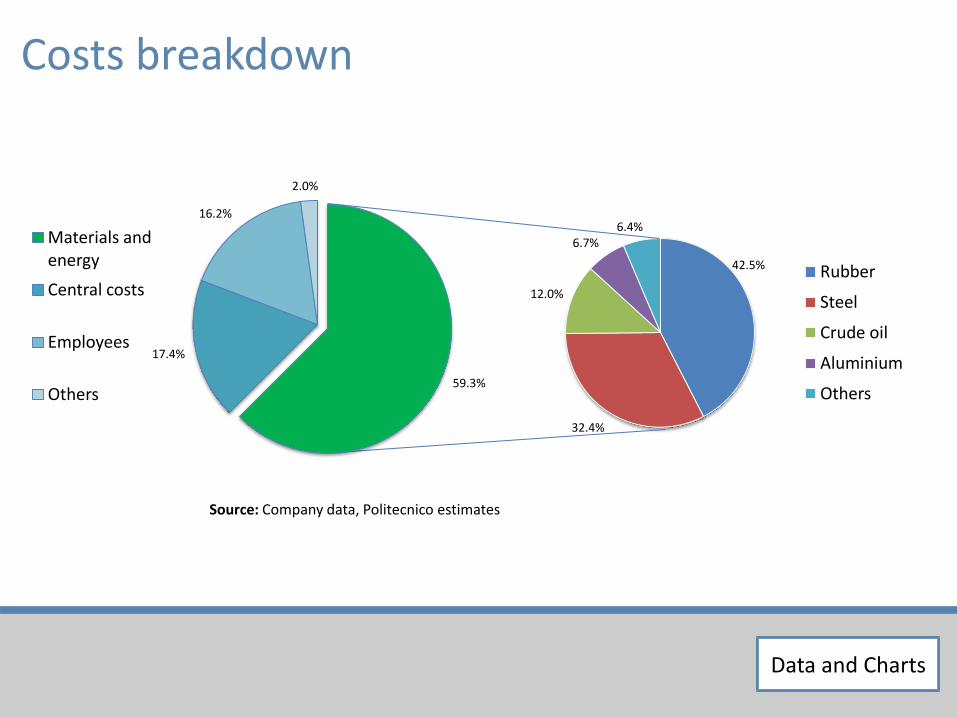

42.5%

32.4%

12.0%

6.7%6.4%

Rubber

Steel

Crude oil

Aluminium

Others

Data and Charts

Costs breakdown

59.3%

17.4%

16.2%

2.0%

Materials and energy

Central costs

Employees

Others

Data and Charts

Source: Company data, Politecnico estimates

0.020.040.060.080.0

100.0120.0140.0160.0180.0

Sep

-06

Jan

-07

May

-07

Sep

-07

Jan

-08

May

-08

Sep

-08

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

Jan

-11

USD/bbl USD/tonCrude oil Aluminium

4000

3500

3000

2500

2000

1500

Data and Charts

Oil price impact on Rubber and Alluminium

0.020.040.060.080.0

100.0120.0140.0160.0180.0

Sep

-06

Jan

-07

May

-07

Sep

-07

Jan

-08

May

-08

Sep

-08

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

Jan

-11

USD/bbl USD/kgCrude oil Rubber

Crude oil and Rubber priceRUBBER ALLUM.

Actual price 5,5 USD/kg 2.600 USD/ton

Correlationindex withoil price

91% (strong) 83% (strong)

Rationale More than 75% of synteticrubber raw materials are derived on petroleum.

Alluminiumproduction is energy intensive

Price increseestimation

+0.5 $/kg foreach +10 $/bbloil increase

+300 $/ton for each +10 $/bbl oil increase

Source: World Bank Community price data

Crude oil and Aluminium price

Data and Charts

Sensitivity on Oil PriceRESULTS: KEY DRIVERS TO PROTECT EPS:

EPS

2011 E 2012 E

CR

UD

EO

IL P

RIC

E ($

/BB

L)

70.0 €0.186 €0.192

80.0 €0.171 €0.181

90.0 €0.156 €0.163

100.0

(base case)€0.141 €0.141

110.0 €0.141 €0.136

120.0 €0.135 €0.129

130.0 €0.130 €0.119

140.0 €0.125 €0.109

Oil Oil , Rubber, Alluminium

Data and Charts

Bargaining power: Improving Global Sourcing

Pricing power:Premiumization

SUPPLIERS CUSTOMERS

Source: Politecnico estimates

Sensitivity on Indian Business

16.9% 17.4% 17.9% 18.4% 18.9% 19.4% 19.9% 20.4% 20.9%

4.4% €2.52 €2.55 €2.58 €2.61 €2.65 €2.68 €2.72 €2.75 €2.79

4.8% €2.54 €2.57 €2.61 €2.64 €2.68 €2.71 €2.75 €2.78 €2.82

5.2% €2.57 €2.60 €2.64 €2.67 €2.71 €2.74 €2.78 €2.82 €2.85

5.6% €2.59 €2.63 €2.66 €2.70 €2.74 €2.77 €2.81 €2.85 €2.89

6.0% €2.62 €2.66 €2.69 €2.73 €2.77 €2.80 €2.84 €2.88 €2.92

6.4% €2.65 €2.68 €2.72 €2.76 €2.80 €2.84 €2.88 €2.92 €2.96

6.8% €2.68 €2.71 €2.75 €2.79 €2.83 €2.87 €2.91 €2.95 €2.99

7.2% €2.70 €2.74 €2.78 €2.82 €2.86 €2.90 €2.94 €2.99 €3.03

7.6% €2.73 €2.77 €2.81 €2.85 €2.89 €2.94 €2.98 €3.02 €3.06

8.0% €2.76 €2.80 €2.85 €2.89 €2.93 €2.97 €3.01 €3.06 €3.10

8.4% €2.79 €2.84 €2.88 €2.92 €2.96 €3.01 €3.05 €3.10 €3.14

Indian 2015 Ebitda Margin

Indian LCV Volume CAGR 10-15

According to our DCF, Indian business is worth €1.3

Data and Charts

Data and Charts

Sensitivity on ASEAN BusinessAccording to our DCF, ASEAN business is worth €0.65

18.9% 19.1% 19.3% 19.5% 19.7% 19.9% 20.1% 20.3% 20.5%

18.9% €2.71 €2.71 €2.72 €2.72 €2.73 €2.73 €2.74 €2.74 €2.75

19.3% €2.72 €2.73 €2.73 €2.74 €2.74 €2.75 €2.75 €2.76 €2.76

19.7% €2.73 €2.74 €2.74 €2.75 €2.75 €2.76 €2.76 €2.77 €2.77

20.1% €2.75 €2.75 €2.76 €2.76 €2.77 €2.77 €2.78 €2.78 €2.79

20.5% €2.76 €2.77 €2.77 €2.78 €2.78 €2.79 €2.79 €2.80 €2.80

20.9% €2.77 €2.78 €2.78 €2.79 €2.80 €2.80 €2.81 €2.81 €2.82

21.3% €2.79 €2.79 €2.80 €2.80 €2.81 €2.82 €2.82 €2.83 €2.83

21.7% €2.80 €2.81 €2.81 €2.82 €2.82 €2.83 €2.84 €2.84 €2.85

22.1% €2.82 €2.82 €2.83 €2.83 €2.84 €2.84 €2.85 €2.85 €2.85

22.5% €2.83 €2.84 €2.84 €2.85 €2.85 €2.86 €2.87 €2.87 €2.88

22.9% €2.84 €2.85 €2.86 €2.86 €2.87 €2.87 €2.88 €2.89 €2.89

ASEAN 2015 Ebitda Margin

ASEAN 2W Volume CAGR 10-15

Data and Charts

Data and Charts

Sensitivity on European BusinessAccording to our DCF, European business is worth €0.95

10.5% 10.7% 10.9% 11.1% 11.3% 11.5% 11.7% 11.9% 12.1%

0.4% €2.63 €2.65 €2.67 €2.69 €2.71 €2.73 €2.74 €2.76 €2.78

0.8% €2.65 €2.67 €2.69 €2.71 €2.72 €2.74 €2.76 €2.78 €2.80

1.2% €2.67 €2.68 €2.70 €2.72 €2.74 €2.76 €2.78 €2.80 €2.82

1.6% €2.68 €2.70 €2.72 €2.74 €2.76 €2.78 €2.80 €2.82 €2.84

2.0% €2.70 €2.72 €2.74 €2.76 €2.78 €2.80 €2.82 €2.84 €2.86

2.4% €2.72 €2.74 €2.76 €2.78 €2.80 €2.82 €2.84 €2.86 €2.88

2.8% €2.73 €2.75 €2.78 €2.80 €2.82 €2.84 €2.86 €2.88 €2.90

3.2% €2.75 €2.77 €2.79 €2.82 €2.84 €2.86 €2.88 €2.90 €2.93

3.6% €2.77 €2.79 €2.81 €2.84 €2.86 €2.88 €2.90 €2.92 €2.95

4.0% €2.79 €2.81 €2.83 €2.86 €2.88 €2.90 €2.92 €2.95 €2.97

4.4% €2.81 €2.83 €2.85 €2.88 €2.90 €2.92 €2.95 €2.97 €2.99

European 2015 Ebitda Margin

European 2W Volume CAGR 10-15

Data and Charts

Independence: 15 August 1947 Republic: 26

January 1950

World’s most populous democracy Federal parliamentary democratic republic:

- INC (India National Congress),center left: liberal

- BJP (Bhartiya Janata Party), center right: conservative

Current Government: the INC party won the general elections both in 2004 and 2009, forming the government with the UPA coalition and Manmohan Singh as prime minister.

XXX

Not a major threat for Piaggio’s business

Data and Charts

Political risk - India

Source: Reuters, Politecnico Estimates

Key Political Risks:

- Inflation

- Corruption

Data and Charts

Euromoney Country Risk Score (March 2011):

XXXData and Charts

Political risk - India

Source: Reuters, Politecnico Estimates

Data and Charts

80

85

90

95

100

105

110 Piaggio

S&P500

NIKKEI 225Earthquake

4Q 2010 data release

Middle East turmoil

Data and Charts

The Japan’s earthquake:

: Peak of S&P500 02.18.2011

Bottom of Nikkei 03.15.2011

10 days later03.25.2011

Piaggio 2.31 2.41 ( + 4.3%) 2.51 ( + 8.7%)

S&P500 1,343.01 1,281.87 ( - 4.6%) 1,316.11 ( - 2.0%)

Nikkei225 10,857.53 8,605.15 ( - 20.7%) 9,536.13 ( - 12.2%)

Source: Bloomberg, Politecnico Estimates

Data and Charts

XXXData and Charts

Source: krugman.blogs.nytimes.com

How rising interest rates affect share prices:

“If fears of default were driving rates, a rise in

interest rates should be associated with a fall in stock prices. If, on the other hand, rates rise

because people think the US will emerge from the

liquidity trap sooner, stocks and rates should move in the same direction. And here’s what it looks like: It’s all about economic

optimism.”

Data and Charts

Data and Charts

Montecarlo SimulationASSUMPTIONS:

Risk Business Unit Drawn Variable Distribution Std. Dev. Comment

GDP growth rate India LCV YoY volumes growth (%) Inverted Lognormal 1% Unexpected Indian slowdown

India 2W “ Inverted Lognormal 5% “

Europe 2W “ Lognormal 1% Unexpected European recovery

Europe LCV “ Normal 0.5% Structural decline

ASEAN 2W “ Inverted Lognormal 2% Unexpected ASEAN slowdown

Success of new models India LCV Volumes (units) Normal 6000 units

India 2W “ Normal 4000 units

ASEAN 2W “ Normal 5000 units

Stronger Competition India EBITDA Margin (%) Inverted Lognormal 1%

Europe “ Inverted Lognormal 0.5%

ASEAN “ Inverted Lognormal 1%

Exchange Rate Volatility India EBIT (€) Normal 3.5% EBIT 3.5% is the avg yearly INR std dev

ASEAN “ Normal 4.5% EBIT 4.5% is the avg yearly VND std dev

Legend:

Upside risk Lognormal

Downside risk Inverted Lognormal

Data and Charts

Data and Charts

Montecarlo SimulationIMPACT ON CASH FLOW STATEMENT:

INDIA 2011 E 2012 E 2013 E 2014 E 2015 E

LCV volumes (units) 250,000 265,000 280,000 295,000 310,000

% growth 25% 18% 15% 12% 8%

LCV ARPU (€) 50,000 75,000 95,000 110,000

… 680 707 735 765

Sales from India 439,895 526,074 601,840 671,067 736,122

% growth 19.92% 19.59% 14.40% 11.50% 9.69%

EBITDA from India 89,739 107,319 122,174 134,213 144,280

EBITDA margin India 20.40% 20.40% 20.30% 20.00% 19.60%

D&A India 24,867 25,244 25,745 26,454 27,266

EBIT from India 64,871 82,075 96,429 107,759 117,013

EBIT margin India 14.75% 15.60% 16.02% 16.06% 15.90%

Tax Rate India 42.00% 42.00% 42.00% 42.00% 42.00%

… 27,246 34,471 40,500 45,259 49,146

D&A India 24,867 25,244 25,745 26,454 27,266

Change in NWC India (12,172) (12,670) (11,150) (10,914) (9,855)

Cash Flow From India 43,484 52,228 60,098 68,774 74,963

Capex India 26,454 26,856 27,388 28,143 29,007

RISKS:

• Success of new models

• GDP / Industry growth rate

• Stronger competition

• Exchange rate volatility

Data and Charts

Data and Charts

Montecarlo SimulationRESULTS:

• Target price volatility:

• Geographical breakdown:

ASEAN EUROPE + US INDIA

Piaggio India Europe ASEAN

TP DCF €2.90 €1.30 €0.95 €0.65

Std. Dev. €0.055 €0.029 €0.019 €0.025

CV 1.9% 2.26% 2% 3.67%

Data and Charts

Data and Charts

Comply Does not comply

Independence of the board of directors:

4 of 11 members are independent.

Internal Control Committee: Composed

of independent directors, convenes at least

5 times per year.

Appointment Proposals Committee: The

majority of members are non executives,

and there is a transparent procedure for

the presentation of candidate lists.

Financial disclosure and transparency:

Piaggio follows COSO Reporting guidelines.

Internal Control Supervisor: Tight relationship

between the Company and Immsi Audit S.c.ar.l. CEO undermines auditors’ autonomy.

Independence of Chairman: Chairman and

CEO are not separate.

Board of Directors members’ maximum

offices in other companies: Board has not

established a limit to the number of offices

directors can cover in other companies.

Remuneration Committee: The attendance of

the CEO by invitation creates a conflict of

interest.

Source: Politecnico Estimates

Corporate Governance Snapshot

Data and Charts

Data and Charts

Name Position In office from

Indep. % attendance

Otheroffices

Roberto Colaninno ChairmanCEO

04/16/2009 100 7

Matteo Colaninno DeputyChairman

04/16/2009 100 3

Michele Colaninno Director 04/16/2009 100 9

Livio Corghi Director 04/16/2009 100 5

Franco Debenedetti Director 04/16/2009 X 91 5

Daniele Discepolo Director 04/16/2009 X 100 9

Andrea Paroli Director 22/09/2010 - -

Giorgio Magnoni Director 04/16/2009 73 1

Luca Crespi Director 04/16/2009 X 91 5

Riccardo Varaldo Director 04/16/2009 X 82 2

Vito Varvaro Director 04/16/2009 90 2

Source: Piaggio’s 2009 CG Report

Composition of the Board of Directors

Data and Charts

Data and Charts

CG and CSR Valuation

Piaggio’s CG and CSR are under control, with improvement margins

Data and Charts

Data and Charts

Steel impact on EPSSe

p-0

6

Dec

-06

Mar

-07

Jun

-07

Sep

-07

Dec

-07

Mar

-08

Jun

-08

Sep

-08

Dec

-08

Mar

-09

Jun

-09

Sep

-09

Dec

-09

Mar

-10

Jun

-10

Sep

-10

Dec

-10

1.2

1.0

0.8

0.6

0.4

0.2

Steel price chart (USD/kg)

Source: World Bank Community price data

Data and Charts

DRIVERS WeightWhy

increasing?

Coking Coal

Accounts for 50% of steel price fluctuations

Economic recovery

Iron Ore Accounts for 30% of steel price fluctuations

Increase in demand form EMs, mainly China and India

Source: Company’s data

Worst case scenario:

-0.3% EBITDA margin

Data and ChartsData and Charts

India and Vietnam nominal GDP growth rates

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

2009 2010 2011 2012 2015

India Nominal GDP growth (%) Vietnam Nominal GDP growth (%)

Source: IMF, World Economic Outlook Database

India Vietnam

EMs nominal GDP growth rates(2011-2015)

12.29% CAGR

14.00% CAGR

Piaggio’s top line growthrate (‘11-’15)

12.86% CAGR*

13.41% CAGR*

(ASEAN)

*Source: Politecnico estimates

GDP growth rates in EMs

Recommended