The Future Roles of NRENs

SEPTEMBER 2012

ASPIRE

2 | ASPIRE NRENS STUDY

IntroductionASPIRE - A Study on the Prospects of the Internet for Research and Education

The ASPIRE foresight study has been exploring the implications of potential developments of the Internet up until

2020 and assessing their impact for the Research and Education (R&E) networking community.

In May 2011, a consultative workshop was held to ascertain what the community considers to be the four topics

that are most likely to have a significant impact on the sector.

The topics chosen as a result of the workshop were:

› Middleware and Managing Data and Knowledge in a Data-rich World

› Cloud Services

› Adoption of Mobile Services

› The Future Roles of NRENs

Four panels of experts were convened during the latter part of 2011, and worked until the spring of 2012,

gathering material and reaching a consensus on the major issues.

This document is the work ASPIRE panel on:

The Future Roles of NRENs

The conclusions and recommendations from each of the panels will be discussed in a second ASPIRE workshop in

September 2012. The workshop will validate the work of the panels and determine a community strategy for the

future.

The ASPIRE study team at TERENA wish to express their sincere thanks and appreciation for the work undertaken

by the panel members and leaders.

John Dyer Magda Haver

The ASPIRE foresight Study was funded from the European Community’s Seventh Framework Programme (FP7/2007-2013) under grant agreement n° 238875, relating to the project ‘Multi-Gigabit European Research and Education Network and Associated Services (GN3)’.TERENA is solely responsible for this publication, which does not represent the opinion of the European Community; nor is the European Community responsible for any use that may be made of this report.

back

to c

onte

nts

page

3 | ASPIRE NRENS STUDY

Contents1 ExECuTIvE SuMMARy ________________________________________________________________________ 6

2 INTRoDuCTIoN To THE NREN FuTuRES STuDy oF ASPIRE __________________________ 7

2.1 NREN Futures Panel ______________________________________________________________________ 7

2.2 Data Collection and SWoT Analysis ___________________________________________________ 7

2.3 Survey Analysis ___________________________________________________________________________ 9

2.4 Conclusions from the NREN Client Questionnaire ________________________________ 10

2.4.1 Respondent Group: _____________________________________________________________ 10

2.5 Summary of the Analysis ______________________________________________________________ 10

2.5.1 Important Current NREN Services ____________________________________________ 10

2.5.2 Most Important Future Services ______________________________________________ 10

2.5.3 Services Bought on the Market by Clients even though the

NREN Provides Them __________________________________________________________________ 11

2.5.4 Relations between the NRENs and their Client Communities ___________ 11

2.5.5 Perception of the NREN by their Client Communities _____________________ 11

2.5.6 Service Requests to the NRENs by their Client Communities ____________ 11

back

to c

onte

nts

page

4 | ASPIRE NRENS STUDY

3 THE CuRRENT PoSITIoN oF NRENS______________________________________________________ 12

3.1 Competition _____________________________________________________________________________ 12

3.2 Aggregation _____________________________________________________________________________ 13

3.3 Neutrality and Trust ____________________________________________________________________ 13

3.4 Competitive Advantages ______________________________________________________________ 14

3.5 Industry and NRENs ____________________________________________________________________ 14

3.6 Likely Developments for NRENs ______________________________________________________ 15

3.6.1 Commodity Services ____________________________________________________________ 15

3.6.2 Connectivity ______________________________________________________________________ 15

3.6.3 Services ___________________________________________________________________________ 16

3.6.4 Capacity Building and Collaboration _________________________________________ 16

3.7 Policy Issues _____________________________________________________________________________ 16

3.7.1 The NRENs as a Common Good ______________________________________________ 18

3.7.2 Connectivity beyond National Boundaries _________________________________ 18

3.7.3 The Global Economic Crisis ____________________________________________________ 19

3.7.4 European R&E Network Policy _________________________________________________ 20

3.7.5 Addressing Policy Issues _______________________________________________________ 20

4 FuTuRE PoSITIoNING ______________________________________________________________________ 21

4.1 Governance of the NREN Community ______________________________________________ 22

4.2 Governance of NRENs __________________________________________________________________ 22

4.3 Collaboration between NRENs _______________________________________________________ 23

4.4 NREN Services ___________________________________________________________________________ 23

4.5 NREN Markets ___________________________________________________________________________ 23

4.6 NRENs in a National Environment ___________________________________________________ 24

back

to c

onte

nts

page

5 | ASPIRE NRENS STUDY

5 ISSuES & RECoMMENDATIoNS ___________________________________________________________ 25

6 GLoSSARy _____________________________________________________________________________________ 27

7 CoNTRIBuToRS ______________________________________________________________________________ 32

Appendix 1: Terms of Reference of ASPIRE NREN Futures Panel ________________________ 34

Appendix 2: Detailed Results of NREN SWoT Analysis ___________________________________ 35

Appendix 3: Summary Results of the NREN Managers’ Questionnaire ________________ 38

back

to c

onte

nts

page

6 | ASPIRE NRENS STUDY

1 ExECuTIvE SuMMARyThe NREN Futures study is a sub-study of the ASPIRE project and was set up to look at the current state of NRENs

in Europe. From this, recommendations can be made as to how the NRENs should develop to take advantage of

developments in technology and business practice in the next five to ten years.

The study used a variety of methods: questionnaires, surveys, interviews and the expertise of the panel members,

to collect and analyse the current status, and then to predict how the NREN environment is likely to change in the

future. A remarkably consistent view of future developments emerged from the different parts of the study and a

range of recommendations and findings are detailed in the study.

Because the state of development of the NRENs differs widely, the list of recommendations will be applicable to

individual NRENs in different ways and should be adapted and adopted by the NRENs, as they deem appropriate.

The recommendations are:

› The European Research and Education (R&E) Networking Community (NRENs, DANTE, TERENA, and user

stakeholders) need an efficient, strategic management body to act as a single point of contact, capable of

responding quickly and with authority.

› under the auspices of this body, a high-level task force should be created in which decision-makers can work

together to define a single, strategic vision for pan-European R&E Networking. Failure to achieve this may lead

to fragmentation of services.

› NRENs should re-consider their funding models and move to more diversified and sustainable models.

This could embrace close collaboration with Public Service Networks but may require re-framing of some

regulatory positions, connection policies, and acceptable use policies. A major goal should be to increase

inter-institutional collaboration, aggregation of demand for joint procurement, and sharing of services.

› NRENs will need to take a strategic approach to their business planning and delivery of services, and develop a

comprehensive understanding of their own user-base, including the needs of their international users and the

external operating environment.

› It is recommended that a European user-requirements compendium be developed by TERENA so that the R&E

network providers have a strategic view of the demand-side of the sector.

› NRENs should not compete with the commercial providers, particularly on price, but should act as a trusted

broker that is an integral part of the community. They should provide expertise, aggregate demand, and add

value through negotiation, including the integration of support for community AAI systems.

back

to c

onte

nts

page

7 | ASPIRE NRENS STUDY

2 INTRoDuCTIoN To THE NREN FuTuRES STuDy oF ASPIRE2.1 NREN Futures Panel

The work-plan was designed with three major phases: data collection, analysis, and reporting, although there

were areas of common interest between the different phases.

The work was carried out by email, on the TERENA Wiki, and by video Conference (vC). Several meetings were

held by video Conference in December 2011, as well as in the first three months of 2012. 1

Email would appear to be the medium of choice for communications amongst the panel, which may reflect on the

age and background of the panel members. The fact that email is a ‘push technology’ may also be a contributory

factor.

2.2 Data Collection and SWOT AnalysisThe early part of the data-collection phase was intended to identify suitable sources of information and to look at

what the NRENs actually do on a day-to-day basis. Sources of information, such as the TERENA Compendium 2, the

GÉANT Expert Group report 3 and some internal TERENA surveys were used to determine what extra information

was required and what was generally available, in order to avoid ‘survey-fatigue’.

Part of the data collection included a SWoT (Strengths, Weaknesses, opportunities, and Threats) analysis on the

concept of an NREN. This produced some interesting results and involved some major brainstorming amongst the

panel. The SWoT analysis laid the groundwork for the various sub-topics in the data-collection phase. The results

of the SWoT analysis can be found in Appendix 2: Detailed Results of NREN SWoT Analysis.

A questionnaire was constructed and sent to the NREN managers through the TERENA GA mailing list. This was

to elicit their strategic views on what was likely to happen to NRENs in the next five to ten years. At the same

time, they were asked if they would allow their clients to be interviewed through a questionnaire about their

relationship with the NREN. Approximately 50% of the NREN managers responded to the NREN Managers’

Questionnaire and most of these did not want their clients interviewed through a questionnaire. This is significant,

reflecting on the relationships between the NRENs and their clients.

1 It is interesting to note that, despite VC being a mature technology, there were numerous problems in the video conference meetings. Most of these related to person computer based solutions, but if the experts from the NRENs cannot manage these processes, how are the end users in the universities and research institutions?

2 TERENA Compendium of NRENs: www.terena.org/compendium3 GÉANT Expert Group Report Knowledge without Borders: http://cordis.europa.eu/fp7/ict/e-infrastructure/docs/geg-report.pdf

back

to c

onte

nts

page

8 | ASPIRE NRENS STUDY

The results of the client questionnaire were consequently very disappointing, even though the EuNIS mailing list

was also used to circulate the request. Due to the low numbers that responded, it was not possible to draw any

significant conclusions. Despite this, the responses that were received were very much in line with the responses

from other feedback

A number of visionary leaders in the NREN community, in the region and beyond were consulted on their views of

the future of NRENs in Europe. A list of questions was prepared to steer the conversation in a coherent direction,

and while these questions have been answered, for the most part, the interviews ended up being quite wide

ranging, as was to be expected.

The final component of the data-collection phase was the collection of the views of the panel members,

themselves, and several sessions were held to gather their views. As expected, their views were in line with the

general information collected from other sources.

back

to c

onte

nts

page

9 | ASPIRE NRENS STUDY

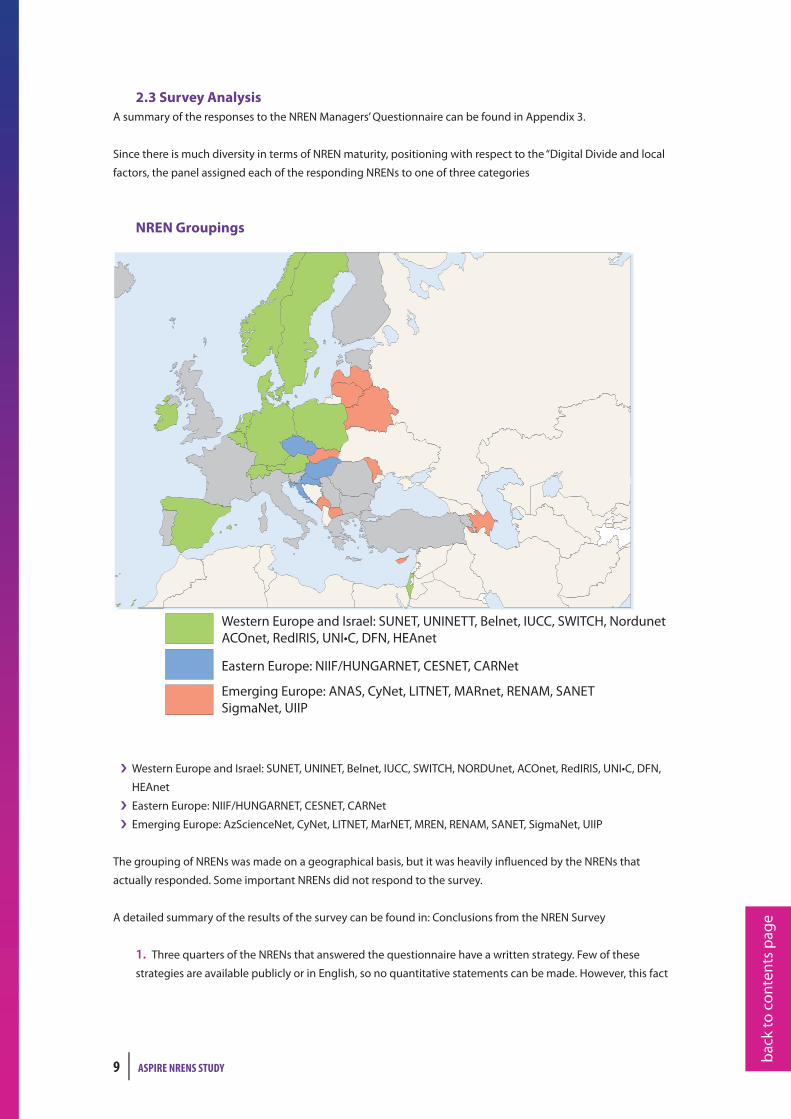

2.3 Survey AnalysisA summary of the responses to the NREN Managers’ Questionnaire can be found in Appendix 3.

Since there is much diversity in terms of NREN maturity, positioning with respect to the “Digital Divide and local

factors, the panel assigned each of the responding NRENs to one of three categories

NREN Groupings

CAzScienceAAyNet

Western Europe and Israel: SUNET, UNINETT, Belnet, IUCC, SWITCH, NordunetACOnet, RedIRIS, UNI•C, DFN, HEAnet

Eastern Europe: NIIF/HUNGARNET, CESNET, CARNet

Emerging Europe: ANAS, CyNet, LITNET, MARnet, RENAM, SANETSigmaNet, UIIP

› Western Europe and Israel: SUNET, UNINET, Belnet, IUCC, SWITCH, NORDUnet, ACOnet, RedIRIS, UNI•C, DFN,

HEAnet

› Eastern Europe: NIIF/HuNGARNET, CESNET, CARNet

› Emerging Europe: AzScienceNet, CyNet, LITNET, MarNET, MREN, RENAM, SANET, SigmaNet, uIIP

The grouping of NRENs was made on a geographical basis, but it was heavily influenced by the NRENs that

actually responded. Some important NRENs did not respond to the survey.

A detailed summary of the results of the survey can be found in: Conclusions from the NREN Survey

1. Three quarters of the NRENs that answered the questionnaire have a written strategy. Few of these

strategies are available publicly or in English, so no quantitative statements can be made. However, this fact

back

to c

onte

nts

page

10 | ASPIRE NRENS STUDY

may indicate that strategic thinking and its dissemination may not have been given sufficient priority by the

NRENs and that the level of detail of these strategies may vary significantly between NRENs.

2. Today, connectivity is considered as the common strategic service provided by all NRENs, followed by

higher-level services such as PKI and AAI. Most NRENs see cloud services as a key service in the future.

However, none gave specifics of which services should be offered through cloud technology.

3. The environment that NRENs face varies between the different countries (“all NRENs are local”) and no

common NREN vision for future services has emerged. As a sign of this diversity, 50% of NRENs do not expect

to target new markets in the next five years, twenty per cent thought they might move into the public sector,

and thirty per cent planned to grow their market-base in educational establishments.

4. The formulation and execution of a successful strategy is of great importance to NRENs, given the fact that

connectivity alone may not be sufficient to guarantee their sustainability.

5. NRENs tend to be firmly established and trusted within their community: they are considered to be a part

of the community and not just a service provider. This gives them a significant competitive advantage in

intermediation between other suppliers and users, and it separates them from commercial operators.

2.4 Conclusions from the NREN Client Questionnaire

2.4.1 Respondent Group:unlike the responses to the NREN Managers’ Questionnaire, which are well distributed over NRENs in North, East,

West, and South Europe, the twenty-nine responses to the NREN Client Questionnaire show a heavy bias toward

only a few areas, in particular, Spain and Cyprus. Most likely, this has to do with the lack of direct ties between

TERENA and the NREN clients, with the exception of those that are involved in TERENA activities or whose NREN

took an active role in finding respondents. Many NRENs are hesitant to “bother” their clients with questionnaires

too often. Therefore, it is impossible to infer strong, general conclusions from the answers to the questionnaire, let

alone analyse the differences across Europe. However, some commonalities can be found. In addition, responses

to an in-depth client questionnaire from HEAnet have been analysed to validate the findings of the NREN Client

Questionnaire.

2.5 Summary of the Analysis

2.5.1 Important Current NREN ServicesThe majority of the respondents identify connectivity (IP, lightpaths, or point-to-point connections) as the main

service offered by the NREN. Services, such as server certificates, federation, and CERT are also mentioned as

being core. Managed access to services like Gmail, and Amazon Cloud Services are not identified as critical by the

responding users.

2.5.2 Most Important Future ServicesIn contrast with the previous item, the majority of clients named cloud services as the most important future

service. This probably means that the NRENs do not offer cloud services, but their clients would like them to do so.

Federation services and mobility are also mentioned frequently. In general, NREN clients expect their NREN to act

as a trusted party for many services where it is advantageous for them to join forces. Brokering, coordination, legal

support, and joint procurement are explicitly mentioned.

back

to c

onte

nts

page

11 | ASPIRE NRENS STUDY

2.5.3 Services Bought on the Market by Clients even though the NREN Provides ThemInstitutions in the R&E community buy their services through their national NREN, if at all possible. The exceptions

to this are the few institutions that use cloud services that are offered by, for example, Amazon. Interestingly

enough, in the next five years none of the respondents expect to bypass the NREN in order to obtain services that

are offered by the market.

The reasons that are mentioned are the price/quality ratio, the strategic fit with the NREN, and solidarity (“club-

NREN”).

Conversely, the NREN clients do not expect to offer their own customers more autonomy in selecting service

providers. It is unlikely that the NRENs will be able to have much influence on the use of “free” cloud services, such

as Gmail, Dropbox, and Box.

2.5.4 Relations between the NRENs and their Client CommunitiesAlmost all respondents report that they participate in NREN activities or are represented on the NREN board. This

questions how selective the sample for the questionnaire was. Since respondents were approached through ties

with the NRENs, it is very likely that the only active participants were those that participate in NREN activities.

2.5.5 Perception of the NREN by their Client CommunitiesAlmost all respondents emphasize the role of the NREN as the hub for collaboration. Even though connectivity is

identified as the most important service that the NREN offers, it is, at the same time, a service that often can be

acquired for a competitive price on the market. Therefore, it seems logical that in order to remain successful, the

NRENs need to focus on their collaboration activities and, indeed, expand this area of activity.

Some of the challenges facing the clients and their needs are worth enumerating:

› budget and resource constraints (grant reduction, recruitment embargo, value for money);

› mobility-related aspects (how to cater for mobile devices, security, number of devices and their types,

ubiquitous access, coverage);

› cloud services (external to institute, integration in local services, storage, virtual machine services), and

demand for new services;

› managing data;

› multimedia services (steaming, conferencing).

2.5.6 Service Requests to the NRENs by their Client CommunitiesBoth the ASPIRE and HEAnet surveys identified the following as services that users would like their NRENs to

provide:

› cloud services (personal and group academic services, integration with local services, storage);

› resilience of connectivity (the strategic importance of connectivity, disaster recovery);

› workshops on third-party systems and services;

› hosting of virtual machines;

› 24/7 monitoring of critical LAN infrastructure;

› framework agreements (software), voIP (SIP trunks), virtualisation of desktops, video Conferencing on more

devices (including web-based), mobile applications (shared development of mobile application);

› security services (certificates, MAN/WAN, firewalling).

back

to c

onte

nts

page

12 | ASPIRE NRENS STUDY

3 THE CuRRENT PoSITIoN oF NRENSSeveral European NRENs have been in business, in one form or another, for over twenty-five years. The NRENs

have grown from best-efforts projects that serve a limited community, to highly professional providers of reliable

networks that are capable of supporting mission-critical services. In the 1980’s, it was unusual for the network to

be “at-risk” for several hours each week in order to carry out essential maintenance and upgrades. Today, users

demand availability in excess of 99.99%, with millisecond fallback to redundant backup. During the lifetime of the

oldest NRENs, network capacity has increased over 1,000,000 fold (from 9.6kps to 100Gbps).

During the late 1980’s, NRENs sprang up to satisfy the growing desire of researchers and educators to

communicate, and to share and exchange resources with their colleagues and students, irrespective of

geographic location. At the time, the incumbent network owners and operators did not focus on data-

transmission as a major traffic component of what they regarded as their “telephone networks”.

For most of their evolution, NRENs have been innovative, and have made themselves into a useful resource for

the R&E community by taking existing equipment and resources, using them in novel ways, and developing the

things that were needed.

Liberalisation of the telecommunications market, the increasing commoditisation of ISP services, pressure on

NRENs to reduce costs and nature of the research required, have contributed to a shift in balance of innovation

to the commercial sector. There is a common feeling that the NRENs are currently falling behind as an engine of

innovation. This raises several challenges to the future of NRENs.

3.1 CompetitionWhich other organisations are currently supplying or are able to offer services to the institutions that make up the

NRENs’ traditional constituency?

Commercial Internet Service Providers (ISPs) have portfolios of services that include basic IP connectivity at

speeds between 1 and 100 Gbps. ISPs can offer services, such as email services, webhosting, collaborative

document production, and storage. Similarly, cloud service providers 4 provide a wide range of on-line services

that can satisfy the computing, data processing, and storage requirements of many users in the R&E community.

A major issue currently facing all NRENs is what they can offer that is technically and/or economically equal to or

better than the services offered by commercial ISPs or cloud service providers?

The biggest difference between NRENs and commercial ISPs is that of the NREN is part of the R&E community, has

an in-depth understanding of its users’ requirements and expectations, and is not motivated by profit. In itself,

this is insufficient to differentiate the NREN from the commercial ISP. However, ISPs seem to be generally unable

or unwilling to tailor their standard service offerings to meet the non-standard requirements of the academic

community. While commodity services from a commercial supplier may be cheaper than those provided by the

NREN, the inflexibility in the commodity offering may be seen as either an advantage or a disadvantage.

4 Wikipedia lists over 100 cloud service providers at: http://en.wikipedia.org/wiki/Category:Cloud_computing_providers

back

to c

onte

nts

page

13 | ASPIRE NRENS STUDY

A Finding of the Study: NRENs are able to work with community users to pilot and develop services that meet the

specific needs of particular sectors of the community.

Recommendations:

› make sure that NRENs pursue constant interaction with clients. If possible, include communications with the

end-users (students, lecturers/teachers and researchers);

› try to know the clients and their working plans in order to meet their needs;

› react quickly to new developments (e.g., client mergers and service sharing by clients);

› pilot possible new services with clients and users to make sure the NREN is pro-active with regard delivery of

services;

› try to let the clients take an active part in your plans and developments.

3.2 AggregationIt is a common feature of markets that bulk buying brings with it economies of scale, both for the supplier and the

customer. NRENs are in a position to procure pervasive national backbone network services on behalf of a group

of NREN clients – often many hundreds. Hence, NRENs can make a saving by the procurement of a single network,

rather than the have clients or groups of clients procure their own connections to the Internet. Not only does this

offer an immediate saving on direct costs, but it also allows for the concentration of technical, procurement, and

operational expertise, freeing individual institutions from these burdens.

A Finding of the Study: There is strong evidence 5 that the benefits of aggregation-obtained procurement of network

infrastructure by the NREN can be replicated in other related areas.

Recommendations:

› NRENs should explore additional areas where aggregation can bring savings in costs, and improvements in

services and support within their own constituencies;

› NRENs should explore the opportunities for procurement by pan-European, joint NREN consortia and inter-

NREN service development and delivery;

› NREN networks and services are directly or indirectly funded, to a large extent, from the public purse and can

be regarded a common good, albeit with a specific, well-bounded role. Public Service Networks have similar

characteristics. Synergies for sharing expertise and costs should be explored.

3.3 Neutrality and TrustNRENs have generally emerged from projects or initiatives of the community and for the community. Most have

transformed into standalone, not-for-profit organisations, which are inherently regarded as part of the community

that they serve. The advantage of this is that NRENs work for and on behalf of their community in a neutral

manner, without obligations to one supplier or another. Although constrained by finite budgets, this has allowed

the NRENs to “do the right thing” - to provide the best possible outcome for their clients rather than satisfy

proprietary commercial demands.

European NRENs have served their communities, in some cases, for more than twenty-five years and have

consequently earned the respect and trust of their network users.

5 Some examples include: RedIRIS spam suppression, JANET PSN collaboration savings, SURFdiensten software deals, HEANET 3G services, TERENA Certificate Service and the SWITCHpki

back

to c

onte

nts

page

14 | ASPIRE NRENS STUDY

A Finding of the Study: In most cases, the relationship between client and NREN has developed into a partnership of

collaboration rather than that of consumer and supplier.

Recommendation: NRENs should continue to strengthen their position as integral partners with their community.

3.4 Competitive AdvantagesPossible key factors:

› extensive knowledge of how academia works and the real requirements of the academic community;

› established relationships with key decision-takers (national and international funding bodies, government

entities, Eu, other academic institutions);

› established relationships across all customer segments (e.g., from networking personnel to university

management);

› trusted, neutral stakeholder and considered “part of the academic club”;

› number of income sources; diversity of sources of income, and independent of a few customers or funding

bodies;

› economies of scale (of markets and products);

› leadership in technology, innovation, and markets;

› price of products;

› combined offerings of service chains: offering services in combinations that are important for the academic

sector, e.g., eduroam®, AAI, and broadband connectivity together with functionalities not provided by

commercial providers;

› services that are custom-tailored to the requirements of the academic sector.

The study has shown that NRENs have a competitive advantage in client relationships in the academic and

research environment. They are also able to target services that are specific to the needs of their current clients

and that cannot be bought easily in the market place.

However, they are at a disadvantage with respect to their dependence on one, relatively small market segment,

economies of scale, technological innovation, and price.

3.5 Industry and NRENsHistorically, NRENs and the main commercial players in the Internet industry were a natural fit for the evolving

Internet. The industry players were challenging the status quo dominated by the incumbent operators, and the

NRENs were trying to establish a global network for R&E, not tied to those incumbents. Today this relationship

is under pressure. The Internet has become big business and the challengers of yesterday have become the

incumbents of today. At the same time, the NRENs have developed into, or must develop into, professionally run

organisations that can guarantee the required service levels for their clients.

A few challenges can be observed in this changed relationship:

› NRENs have an innovation cycle of five to ten years for their core infrastructure. At the time of an upgrade

of the network, significant amounts of money are invested. However, a relatively low amount of on-going

investment is committed after such an upgrade. often the suppliers disband the teams dedicated to the

NREN, because of their revenue-driven models. They do not stay up-to-date with the requirements of the

NRENs and this potentially results in less than optimal offers.

› Another challenge is that in an attempt to stay ‘vendor neutral’, the NRENs purchase services individually from

suppliers and may have to ignore bundles of integrated services that might be available.

back

to c

onte

nts

page

15 | ASPIRE NRENS STUDY

Pricing models that are successful in the enterprise- and service provider-markets are based on the bundling

of a number of services, to provide the costs savings of integration to both the supplier and the customer.

Perhaps the main problem is that industry no longer perceives NRENs as cutting-edge customers, at least, for

network connectivity. In the past, industry did early field trials and developments with the NREN community,

but now the perception is that the often complex arrangements (“special needs”) that the NRENs request are

not worth the effort, because of the one-off nature of such requirements. This, in turn, leads to the offering of

“standard” products and a resulting lack of involvement with the commercial developers.

Lastly, unlike the relations in the enterprise and service provider markets, which last for many years, the NREN

market is relatively volatile. In addition, the required public procurement procedures are often lengthy and

intricate. This requirement makes a large investment by an industry player in an NREN a risky business.

Possible steps

Whereas shorter innovation cycles of the network are neither realistic nor possible, the same does not hold true

for other services. It would be useful for industry if the NRENs could generate a more continuous procurement

stream, making it easier for industry players to invest in a longer-term relationship. It is also advisable to focus on

collaboration with industry in other services, and not just on connectivity. The NREN community is leading edge

in mobility and federation. It may be advisable to invest, at board level, in relationships with the vendors of these

technologies.

3.6 Likely Developments for NRENs

3.6.1 Commodity ServicesA product or service becomes a commodity when it is available from a large number of sources as an essentially

undifferentiated offering, and at a highly competitive price. Staples, such as grain, milk, and memory chips are

examples of commodities.

In common with other products and services, data network connectivity and application-level services, such as

email and remote storage were initially only available to specialists, either on an experimental or restricted basis.

In the twenty-first century, broadband access to the Internet is available to a large percentage of the citizens

of Europe (but with significant differences in quality of coverage, depending upon geographic location). Email,

storage, and applications including calendaring, collaborative document production, and social networking are

commonly available at no charge with other paid services, which are available at commodity prices. Even national

mobile data connectivity is becoming affordable for the average citizen in some places.

It is likely that the range and availability of such services will grow rather than contract over time.

The difficult question that has to be answered is that if this plethora of services is available at commodity prices,

what is the role of the NREN?

3.6.2 ConnectivityBasic commercial Internet services are not a viable option for most institutions; ISPs can typically only offer

Mbps of bandwidth and may often suffer from congestion due to high contention ratios. Connections of higher

capacities (Gbps) are available on the market for short-term lease (which is expensive), for long-term lease,

exclusive long-term right of use (IRu), or for ownership.

NRENs have the expertise to procure, operate, and manage national networks, and can obtain bulk-purchasing

deals by operating as a single procurement agent on behalf of all of their clients. various procurement

back

to c

onte

nts

page

16 | ASPIRE NRENS STUDY

instruments, such as framework agreements, can satisfy the local requirements of individual clients at an

advantageous, nationally negotiated price.

At the international level, NRENs collaborate through DANTE to provide the pan-European GÉANT network, with

its associated intercontinental links. Additionally, some NRENs procure their own, dedicated international links,

sometimes by the provisioning of cross border fibres.

3.6.3 ServicesNRENs do not routinely provide email services to end users (although there are some exceptions). The end-user

institutions usually run their own mail servers and administer the access rights. It is not unusual for new users

that are entering the R&E sector to already have some experience and a preference for a particular mail service.

It seems unreasonable to force these users to use an institutional email system if they prefer to use other facilities.

The NREN can provide added-value to the community by negotiating preferential terms and performance from

the commodity suppliers, and indeed, can mandate the use of community-compatible AAI systems that manage

access control.

The increasing need for commodity storage and computing power is an area in which some NRENs are already

taking an active lead. Some NRENs are creating value for their users by brokering deals with commercial suppliers

on behalf of the whole community of users and putting middleware solutions in place to provide transparent

access to private or public cloud services.

The NRENs could provide value for their customers through the deployment or brokering of SaaS applications

such as spam-filtering, on-line collaboration, customer relations management, and analytics.

3.6.4 Capacity Building and CollaborationSome NRENs have developed pools of world class, technical expertise in the increasingly complex field of

delivering advanced network services. Some smaller NRENs rely on the collaborative nature of the NREN

community to assist them. Smaller end-user institutions often have difficulty in providing a sufficient level of

technical and management skills to deliver a comprehensive range of on-line services for their users. Formally

building technical capacity and expertise is a valuable role for the NRENs and their community. Activities could

include the exchange of expertise, training, provision of best practice guides, or the provision of services by

NRENs for one another. With its reputation and position of trust, TERENA is an ideal organisation to facilitate

growth in such collaboration.

3.7 Policy IssuesMany NRENS started life during the 1980’s as best-effort projects to serve a very limited constituency of users that

were centred in universities and publicly funded research centres. As NRENs grew and matured, some of them

began connecting a wider community, including commercial research centres, publishers, content providers,

museums, and in some cases, government departments.

back

to c

onte

nts

page

17 | ASPIRE NRENS STUDY

Who may and who may not be connected to these restricted communities has been enshrined in policy

documents that define the NRENs.These include:

› Connection Policy (CP) 6, 7

› Acceptable use Policy (AuP) 8, 9, 10, 11, 12

› Statues and Articles of Association 13

This rigid definition of the limits of service has enabled NRENs to operate as network providers to a closed user

group that does not offer services to the general public.

Some NRENs provide service to a wider community of clients, but still within the constraints of their governing

rules and regulations. This expanding use of the NREN networks has brought with it many advantages. This

should not be a problem for the commercial providers of these services because the NRENs usually procure

their underlying infrastructure on the open market. NRENs, such as DFN in Germany, have chosen to stick very

close to their original remit to provide connectivity and service to their original constituency of universities and

publicly-funded research institutes.

Potential areas for collaboration include interoperability and improved connectivity to a wider group of related

users. The established and neutrally minded expertise of the NREN can be utilised to support a larger community

of clients. Not least, the advantages of aggregation of demand brings with it economic benefits that help counter

the effects of the current global economic crisis, which deserves special mention here.

6 http://webarchive.ja.net/services/publications/policy/connection-policy.html7 http://www.surfnet.nl/en/organisatie/instellingen/Pages/default.aspx8 http://www.ja.net/documents/publications/policy/aup.pdf9 http://www.renater.fr/IMG/pdf/charte_en.pdf10 http://www.sigmanet.lv/usepolicy/en/11 https://openwiki.uninett.no/norstore:acceptable_use_policy12 http://www.heanet.ie/about/aup13 http://www.dfn.de/en/association/

back

to c

onte

nts

page

18 | ASPIRE NRENS STUDY

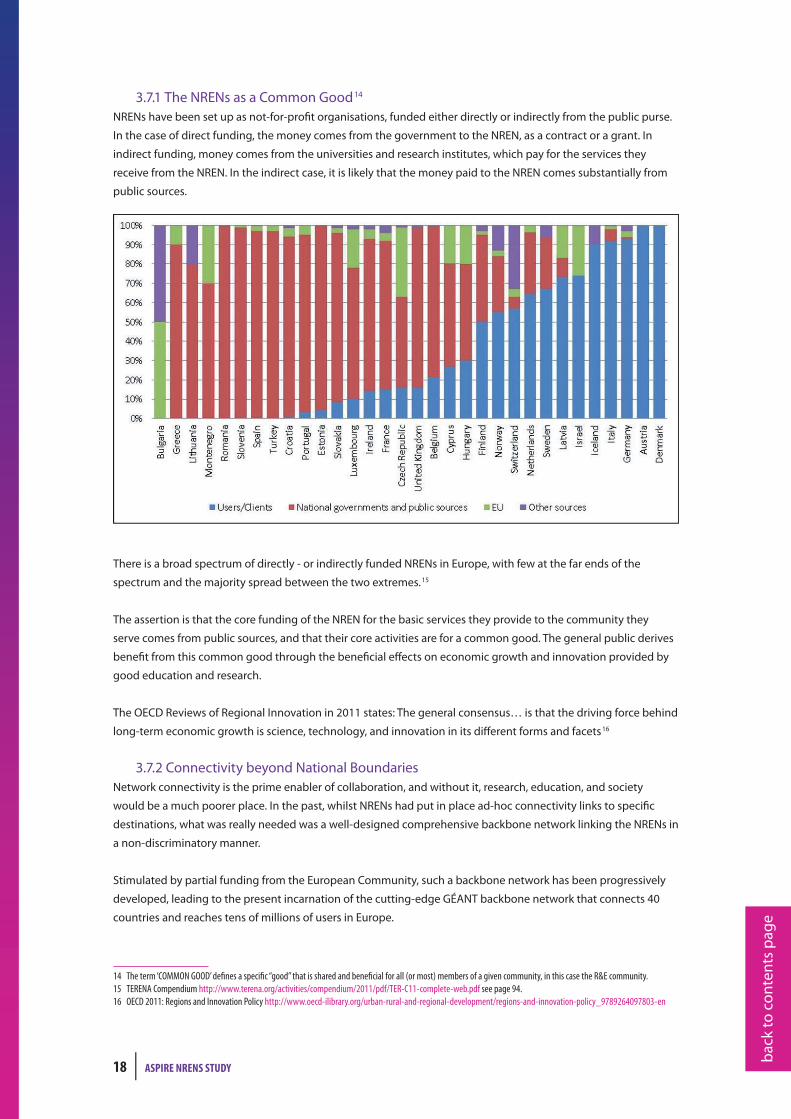

3.7.1 The NRENs as a Common Good 14 NRENs have been set up as not-for-profit organisations, funded either directly or indirectly from the public purse.

In the case of direct funding, the money comes from the government to the NREN, as a contract or a grant. In

indirect funding, money comes from the universities and research institutes, which pay for the services they

receive from the NREN. In the indirect case, it is likely that the money paid to the NREN comes substantially from

public sources.

There is a broad spectrum of directly - or indirectly funded NRENs in Europe, with few at the far ends of the

spectrum and the majority spread between the two extremes. 15

The assertion is that the core funding of the NREN for the basic services they provide to the community they

serve comes from public sources, and that their core activities are for a common good. The general public derives

benefit from this common good through the beneficial effects on economic growth and innovation provided by

good education and research.

The oECD Reviews of Regional Innovation in 2011 states: The general consensus… is that the driving force behind

long-term economic growth is science, technology, and innovation in its different forms and facets 16

3.7.2 Connectivity beyond National BoundariesNetwork connectivity is the prime enabler of collaboration, and without it, research, education, and society

would be a much poorer place. In the past, whilst NRENs had put in place ad-hoc connectivity links to specific

destinations, what was really needed was a well-designed comprehensive backbone network linking the NRENs in

a non-discriminatory manner.

Stimulated by partial funding from the European Community, such a backbone network has been progressively

developed, leading to the present incarnation of the cutting-edge GÉANT backbone network that connects 40

countries and reaches tens of millions of users in Europe.

14 The term ‘COMMON GOOD’ defines a specific “good” that is shared and beneficial for all (or most) members of a given community, in this case the R&E community.15 TERENA Compendium http://www.terena.org/activities/compendium/2011/pdf/TER-C11-complete-web.pdf see page 94.16 OECD 2011: Regions and Innovation Policy http://www.oecd-ilibrary.org/urban-rural-and-regional-development/regions-and-innovation-policy_9789264097803-en

back

to c

onte

nts

page

19 | ASPIRE NRENS STUDY

As the report of the GÉANT Expert Group 17 remarks, “GÉANT has become not just an infrastructure for e-Science

but an in-silico realisation of European integration”.

The panel agree that GÉANT has helped Europe become a world leader in many areas. GÉANT is an innovation-

environment and ideas-generator that drives the development of new networking technologies and services.

3.7.3 The Global Economic CrisisMost people are personally aware of the effects of the Global Economic Crisis, with its origins in 2007-2008. The

consequences for governments have been severe and have resulted in an increased search for savings, while at

the same time preserving or improving the level of services that they can deliver to their citizens. The idea that

improving services while cutting costs might seem impossible to achieve, the paradigm of online information and

self-service associated with e-Government, e-Health and, indeed, e-Society makes it achievable.

Some National Responses to the Economic Crisis

Greece – The Greek government has identified cloud computing as a way of reducing costs for the provision of

computing and storage facilities for publicly-funded institutions in Greece. The Greek government has asked

GRNET (The Greek NREN) to put in place and manage an Infrastructure as a Service (IaaS) system, which they have

done. The okeanos 18 system is currently in alpha test phase.

France – The French government has asked RENATER (the French NREN) to provide optical network connectivity

to government departments.

united Kingdom – JANET (the British NREN) has been working collaboratively with several uK Public Service

Networks to improve service and reduce costs.

Ireland – The higher education funding body has decided to increase the economies of scale of the educational

systems by merging educational institutes and supporting organisations. Furthermore, it recognises that use of

shared services is a way to reduce costs. HEAnet (the Irish NREN) can play a role in this sharing of services.

united States of America – The uS Recovery Act 19 is putting billions of taxpayers’ money into stimulating

investment and into pushing public and private network service and connectivity into the twenty-first century.

u.S. uCAN 20 is a project established to ensure that the advanced applications and national networking

requirements of community anchor institutions (CAIs) - including K-12 schools, libraries, community colleges,

health centres, hospitals, and public safety organisations - are understood, coordinated, and fulfilled. u.S. uCAN

will leverage the upgraded Internet2 network to deliver network services to CAIs, and will provide support

services to CAI sectors similar to those Internet2 provides to its research and higher education members, but

tailored to the specific needs of CAIs.

The European union – At a press conference on 19 october 2011, the President of the European Commission

announced 21 the Commission’s proposal for connecting Europe. The proposal for the 50 billion euro Connecting

Europe Facility (CEF) includes an investment of over nine billion euro in broadband connectivity 22, of which

two billion euro is earmarked to improve the Digital Service Infrastructure (DSI). The major component of the

proposed DSI will be a Trans-European high-speed backbone connecting public administrations serving the Eu27

countries.

17 http://cordis.europa.eu/fp7/ict/e-infrastructure/docs/geg-report.pdf18 https://cms.okeanos.grnet.gr/about/what/19 http://www.whitehouse.gov/recovery/innovations/building-platform-private-sector-innovation20 http://www.usucan.org/21 http://europa.eu/rapid/pressReleasesAction.do?reference=SPEECH/11/688&format=PDF&aged=1&language=EN&guiLanguage=en22 http://europa.eu/rapid/pressReleasesAction.do?reference=MEMO/11/709&format=PDF&aged=1&language=EN&guiLanguage=en

back

to c

onte

nts

page

20 | ASPIRE NRENS STUDY

3.7.4 European R&E Network PolicyAt the national level, NRENs provide services to their clients, many of whom are represented on the NREN

governance bodies. In theory, this gives these users of the networks a voice in how the network is managed and

developed. Mature NRENs undertake extensive customer relations work using account managers and product

managers to ensure a good two-way flow of information and to provide an opportunity for the users to influence

NREN policy – for instance, the Connection Policy and Acceptable use Policy.

For the most part, GÉANT provides pan-European connectivity although bi-lateral, cross-border fibres,

national/regional transcontinental links. other dedicated connectivity is quite common. GÉANT is operated by

DANTE - Delivery of Advanced Network Technology to Europe. DANTE is a limited liability “not for profit” company,

registered in the united Kingdom, and owned by a subset of European NRENs.

From an external perspective, the precise decision-making roles between the governing bodies of DANTE (the

company) and GÉANT (the project) appear blurred.

DANTE is governed by the DANTE Board of Directors and by its shareholders, and is managed by its DANTE

management team. The GÉANT project is governed and managed by the GÉANT Executive Committee, the NREN-

PC, the GÉANT Project Management Team, and the Project office.

To complicate things further, DANTE’s sister organisation, TERENA, also provides a forum in which NREN managers

meet and discuss issues, including policy. TERENA has its own governance structure, including the TERENA

General Assembly and the TERENA Executive Committee.

To complicate the situation even more, additional groups that make or recommend policy operate in this space

such as e-IRG 23 and EGI 24.

3.7.5 Addressing Policy IssuesThere are large differences between the European NRENs in terms of funding, staffing, national policy, existing

client base, and outlook. The NRENs would be best served by being able to express themselves to the external

world (international customers, the Commission, and networkers on other continents) with a single voice. The

first step in achieving this is to constitute a neutral forum in which a strategic vision of the future can be framed

in such a way that it addresses the varying needs of the constituent NRENs. This strategic vision may or may not

embrace full participation in the Connecting Europe Facility/Digital Service Infrastructure (CEF/DSI) proposals.

However, it should ensure that the NRENs contribute their technical and managerial expertise as an input to the

CEF/DSI readiness study.

23 The e-Infrastructure Reflection Group http://www.e-irg.eu/24 European Grid Infrastructure http://www.egi.eu/

back

to c

onte

nts

page

21 | ASPIRE NRENS STUDY

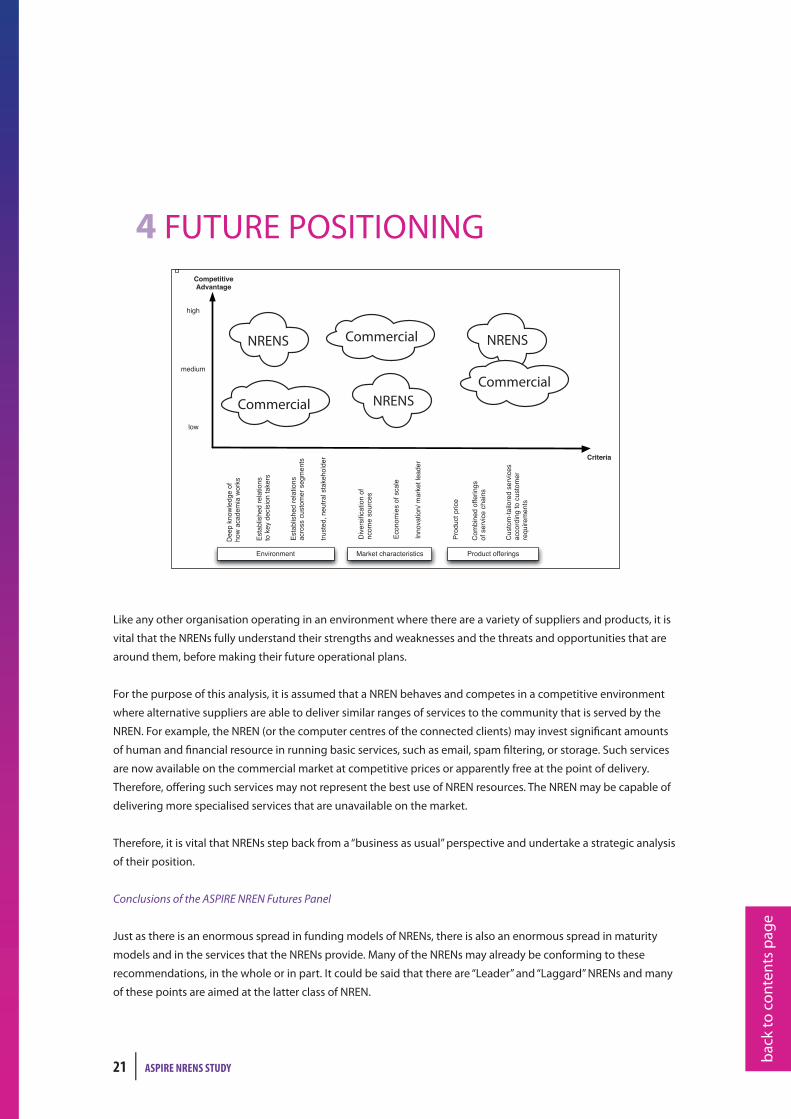

4 FuTuRE PoSITIoNING!""#$%&'()"*+"$',

-'($./.*"01.$('2%3

435.6)13-"*$2").51'&3

5'$%"7$*"/131'&$5.%"23$

435.6)13-"*$2").51'&3

./2'33$/835'0"2$3"+0"&53

52835"*9$&"852.)$35.%"-')*"2

4/'&'01"3$',$3/.)"

!1:"231!/.51'&$',$

&/'0"$3'82/"3

;&&':.51'&<$0.2%"5$)".*"2

=2'*8/5$#21/"

>'061&"*$',,"21&+3$

',$3"2:1/"$/-.1&3

>835'0?5.1)'2"*$3"2:1/"3

.//'2*1&+$5'$/835'0"2$

2"@812"0"&53

4&:12'&0"&5 A.2%"5$/-.2./5"21351/3 =2'*8/5$',,"21&+3

)'(

0"*180

-1+-

$%&.'/*/*5'9:5+6/+;'

$(*/'(*+

NRENS

NRENS

NRENS

Commercial

Commercial

Commercial

Like any other organisation operating in an environment where there are a variety of suppliers and products, it is

vital that the NRENs fully understand their strengths and weaknesses and the threats and opportunities that are

around them, before making their future operational plans.

For the purpose of this analysis, it is assumed that a NREN behaves and competes in a competitive environment

where alternative suppliers are able to deliver similar ranges of services to the community that is served by the

NREN. For example, the NREN (or the computer centres of the connected clients) may invest significant amounts

of human and financial resource in running basic services, such as email, spam filtering, or storage. Such services

are now available on the commercial market at competitive prices or apparently free at the point of delivery.

Therefore, offering such services may not represent the best use of NREN resources. The NREN may be capable of

delivering more specialised services that are unavailable on the market.

Therefore, it is vital that NRENs step back from a “business as usual” perspective and undertake a strategic analysis

of their position.

Conclusions of the ASPIRE NREN Futures Panel

Just as there is an enormous spread in funding models of NRENs, there is also an enormous spread in maturity

models and in the services that the NRENs provide. Many of the NRENs may already be conforming to these

recommendations, in the whole or in part. It could be said that there are “Leader” and “Laggard” NRENs and many

of these points are aimed at the latter class of NREN.

back

to c

onte

nts

page

22 | ASPIRE NRENS STUDY

Some of the advanced NRENs have adopted modern, agile business processes and are led by enlightened

management teams and staff. These will lead the NREN into the future, ready to embrace the rapid changes that

occur in the telecommunications world.

The panel reached a number of general conclusions regarding the European NRENs

4.1 Governance of the NREN Community1. The NRENs should present a unified front when making bids to large funding organisations such as

the European Commission. Irrespective of how NRENs are organised or grouped, they should speak with

one voice to the major funding organisations and to major multinational service providers. The current

representation by DANTE, TERENA and the various governance committees presents a fragmented face to the

EC and the large suppliers.

2. NRENs must cooperate on service provision. Many of the services supplied to the NREN clients are

common across the community, and there is unnecessary duplication of effort in re-building common

services.

4.2 Governance of NRENs3. NRENs must act as partners to the community they serve and must ensure that the current and future

services can be provided through the NREN. Increasingly, the clients will be looking at their IT/networking

budgets and will not be slow about changing providers. NRENs need to adopt modern, “agile” processes

in their business strategies and processes. Just because services have been provided by the NRENs for the

last twenty years does not guarantee that they are sustainable into the future. With the increasing squeeze

on funding in the higher education sector, the client institutions will expect increasing value for their

expenditure and will require their suppliers to respond appropriately. NRENs that have restrictive statutes

and/or attitudes, will find it difficult to compete in an increasingly open market.

4. Existing NREN statutes may prevent an NREN from expanding its customer base beyond the R&E

community. Therefore, it may therefore be necessary to seek changes in the statutes and adopt different

pricing models and conditions appropriate to each sector.

5. The concept of brokered aggregation of services has been adopted by a number of NRENs and would

appear to be a financially viable solution that does not require major investments in infrastructure or

in software development. Aggregation can occur at either the physical or the logical level and multiple

aggregation contracts can be made by an NREN to allow for the diverse requirements of its clients. Many

commercial service providers will adopt a divide and conquer approach to the clients, but with the

appropriate levels of NREN-client cooperation, the extra purchasing power of the NREN can ensure that

”best value for money” deals can be made. In a similar manner, NRENs should be able to aggregate services

with other NRENs, where the law allows this. once again, the commercial suppliers can act as a single

supplier across a whole region. It should be possible for NRENs, or a single regional NREN, to act as a regional

aggregator.

6. NRENs need to examine their funding basis. Too much reliance on project-based funding can result in

instability by causing a rise in staff turnover, with its associated costs. The provision of basic services should

be on a self-sustaining basis, with funding for advanced developments coming from grant aid from central

or regional governments. In some cases, this is probably a longer-term objective, but some NRENs need to

examine and revise their processes to ensure that the NREN is operating on a sustainable funding basis.

back

to c

onte

nts

page

23 | ASPIRE NRENS STUDY

4.3 Collaboration between NRENs7. NRENs should consider forming links with other NRENs to share expertise. This would be especially

relevant where a mature NREN links up with a developing NREN in order to fast track their development of

services. This model has been used in some regional networks in the developing world.

8. While there is a great range of different NREN models in use across the region, many of the basic services

are common and will become increasingly commoditised. NRENs need to collaborate to optimise the

deployment of resources and to avoid inadvertent competition by the duplication of services. Similarly,

NRENs are at different levels of maturity in their development, and there should be closer collaboration to

ensure that the less-mature NRENs can benefit from the expertise and experience of the more developed

NRENs.

An example of such a regional network is NoRDunet, which is probably unique in Europe in that it is

governed by a treaty that formed the Nordic Council. However, there are many other “logical” groupings

across the region where de-facto cooperation exists that could be built upon to ensure better economies of

scale and reduction of duplication without interfering in national sovereignty issues.

9. NRENs should try to work together on service provision. Some of the work they do is very country-specific,

but some services span regions or even continents. There are obvious successful collaborations, such as

eduroam®, AAI, certificate services and the GÉANT network, where the concept of a regional NREN has

worked very successfully.

10. NRENs should not engage in the development of services readily available on the market. Development

of new services by the NRENs should be on a pilot basis and should be driven by the client community. It

should preferably be undertaken after consultation with other NRENs so as to avoid duplication of effort. This

may foster collaborative development, spreading the cost and risk or lead to a common service offered to

other NRENs.

There are many examples of services that the NREN community have pioneered that are unlikely to be

available on the market because they were developed to fulfil specific requirements of the R&E community.

However, once a specific service does become readily available on the commercial market, NRENs should

broker a migration of users to that service and withdraw the running of their own service.

4.4 NREN Services11. NRENs should not compete on price alone. If the market can provide the service cheaper, then the NREN

should move to act as an aggregator or broker of the commercial service.

4.5 NREN Markets12. NRENs should concentrate on the broad R&E markets in their region. This could include the full spectrum

of education, including public libraries and teaching hospitals as well as the broad range of schools. Where

questions arise as to the suitability of a particular sector, then a test of whether the new sector would be of a

benefit to the existing organisation should be applied.

13. NRENs should understand the needs of a broad and diverse community of users and then articulate

those requirements in a clear and coherent way to the market.

back

to c

onte

nts

page

24 | ASPIRE NRENS STUDY

4.6 NRENs in a National Environment14. NRENs should work with other public sector providers in their country and for interconnections between

adjacent countries. The clients on the NRENs are largely funded by the public sector and there is much to be

gained by the different components of the public sector working together. Similarly, there is much to be lost

by having multiple competing bids from one country for funding.

back

to c

onte

nts

page

25 | ASPIRE NRENS STUDY

5 ISSuES & RECoMMENDATIoNSIssue: The number of bodies and committees involved in discussing policy and management of the NREN/

European R&E networking sector is large. Although there is some cross membership and liaison, the consequence

is too many meetings, resulting in inefficiency and duplication.

Recommendation 1

The European R&E Networking Community (NRENs, DANTE, TERENA, and user stakeholders) need an efficient

strategic management body that is able to act as a single point of contact and is able to respond quickly and with

authority.

Recommendation 2

under the auspices of this body, a high-level task force should be created in which decision-makers work together

to define a single strategic vision for pan-European R&E Networking. Failure to achieve this may lead to the

fragmentation of services.

Issue: For many NRENs, the global economic crisis has intensified the issue of ensuring the sustainability of

funding. Governments and the institutions that fund them are seeking ways to cut their expenditure. In some

European countries, this is leading to the development of Public Service Networks (PSNs), intended to serve a

range of publicly-funded institutions.

NRENs dependence on periodic funding injections and money from short-term projects can be problematic for

NRENs, and can hinder them in running reliable, long-term, stable services.

Recommendation 3

NRENs should re-consider their funding models and move to more diversified and sustainable models. This

could embrace close collaboration with Public Service Networks but may require re-framing of some regulatory

positions: Connection Policies and Acceptable use Policies. A major goal should be to increase inter-institutional

collaboration, aggregation of demand, joint procurement, and sharing of services.

Issue: NRENs will find themselves operating in a harsher world than in the past. Commercial providers are

becoming capable of providing many of the basic services once provided by the community. It is vital for NRENs

to fully understand their operating environment and to adapt if necessary, if they are to survive - and indeed, to

thrive.

NRENs should review the makeup of senior management to ensure that there is suitable succession-planning

in place, and that new managers have suitable management skills and vision. To compete with the commercial

world, NRENs need to adopt commercial skills and policies.

back

to c

onte

nts

page

26 | ASPIRE NRENS STUDY

Recommendation 4

NRENs need to take a strategic approach to their business planning and service delivery, and develop a thorough

understanding of their own user base, including the needs of their international users and the external operating

environment.

Recommendation 5

A European user-requirements compendium should be developed by TERENA, so that the R&E network providers

have a strategic view of the demand side of the sector.

Recommendation 6

NRENS should not compete with the commercial providers, particularly on price. They should act as a trusted

broker that is an integral part of the community by providing expertise, aggregating demand, and adding value

through negotiation - including the integration of support for community AAI systems.

back

to c

onte

nts

page

27 | ASPIRE NRENS STUDY

3G 3rd Generation (mobile telecommunications technology)

3GPP 3rd Generation Partnership Project

AAI Authentication and Authorisation Infrastructure

AKA Authentication and Key Agreement

ALMA Atacama Millimetre Array

API Application Programming Interface

APN Access Point Network

ARC ALMA Regional Centre

ASDM ALMA Science Data Model

ASKAP Australian SKA Precursor

ASPIRE A Study on the Prospects of the Internet for Research and Education

ATLAS A particle physics experiment at the Large Hadron Collider at CERN

AUP Acceptable use Policy

AWS Amazon Web Service

BYOD Bring your own Device

CA Certification Authority

CAD Computer Aided Design

CAI Community Anchor Institutions

CAPEX Capital Expenditure

CEF Connecting Europe Facility

CEF/DSI Connecting Europe Facility/Digital Service Infrastructure

CERN European organisation for Nuclear Research

CERT Computer Emergency Response Teams

CIDOC-CRM International Committee for Documentation - Conceptual Reference Model

CP Connection Policy

CPU Central Processing unit

DANTE Delivery of Advanced Network Technology to Europe

DARIAH Digital Research Architecture for the Arts and Humanities

DC Dublin Core

DCH Digital Cultural Heritage

DCH-RP Digital Cultural Heritage Roadmap for Preservation

DC-NET Digital Cultural heritage NETwork

6 GLoSSARy

back

to c

onte

nts

page

28 | ASPIRE NRENS STUDY

DEAS Delegate eduroam® Authentication System

DL Distance Learning

DNA Deoxyribonucleic acid

DRDB Distributed Replicated Block Device (software)

DSI Digital Service Infrastructure

DVTS Digital video Transport System

EAP Extensible Authentication Protocol

EC2 Elastic Compute Cloud (Amazon)

ECDD&S ELIxIR Core Data Collections and Services

eduGAIN Education GÉANT Authorisation Infrastructure

eduroam Education Roaming

EEA European Economic Area

EGI European Grid Infrastructure

EIRO European Industrial Relations observatory

ELIXIR A sustainable infrastructure for biological information in Europe

ELSI Ethical, Legal and Social Implications

EMBL-EBI European Molecular Biology Laboratory - European Bioinformatics Institute

e-MERLIN vLBI National Radio Astronomy Facility

EMI European Middleware Initiative

ESD Event Summary Data

ESFRI BMS RI European Strategy Forum - Biological and Medical Sciences Research Infrastructure

EU European union

EUDAT European Data Infrastructure

FITS Flexible Image Transport System

FTP File Transfer Protocol

FTS File Transfer Service

GA General Assembly

GB Gigabyte

Gbps Gigabits per second

GÉANT Gigabit European Academic Network Technology

GN3 Multi-Gigabit European Academic Network

GPRS General Packet Radio Service

GPS Global Positioning System

GUI Graphical user Interface

HDF5 Hierarchical Data Format

HEP High Energy Physics

HG Human Genome Project

HPC High Performance Computing

HPC/Grid High Performance Computing and Grid

HTTPS HyperText Transfer Protocol Secure

IaaS Infrastructure as a Service

back

to c

onte

nts

page

29 | ASPIRE NRENS STUDY

ICFA Study Group on Data Preservation and Long Term Analysis in High Energy Physics

ICRAR a science archive facility in Australia

ICT Information and Communication Technologies

IEEE 802.1X e Institute of Electrical and Electronics Engineers – standard for port-based Network Access Control

IETF Internet Engineering Task Force

IGTF International Grid Trust Federation

IN2P3 the National institute of nuclear and particle physics in France

IOS iPhone operating System

IP Internet Protocol

IP Intellectual Property

IPR Intellectual Property Right

IRCAM Institut de Recherche et Coordination Acoustique/Musique

IRG e-Infrastructure Reflection Group

IRU Indefeasible Right of use

ISO International organization for Standardization

ISP Internet Service Provider

IVOA International virtual observatory Alliance

JIVE Joint Institute for vLBI in Europe

JSPG Joint Security Policy Group

K-12 schools primary and secondary schools

km kilometre

KVM Kernel-based virtual Machine

LAN Local Area Network

LHC Large Hadron Collider

LHCOPN LHC optical Private Network

LIPA Local IP Access

LMS Learning Management Systems

LOFAR Low Frequency Array

LOLA Low LAtency audio visual streaming system

LTE Long Term Evolution - a standard for wireless communication of high-speed data

MAN Metropolitan Area Network

mID unique Identification of person per device

MiFi Mobile Broadband Wi-Fi

MMS Multimedia Messaging Service

ms millisecond

NDGF Nordic DataGrid Facility

NFC Near Field Communication

NGAS New Generation Archive System

NGI National Grid Initiatives

NIST (uS) National Institute of Standards and Technology

NOC Network operations Centre

back

to c

onte

nts

page

30 | ASPIRE NRENS STUDY

NRC National Research Council

NREN National Research and Education Network (can also refer to the operator of such a network)

NREN-PC National Research and Education Network Programme Committee

NSF National Science Foundation

OAI-MPH open Archives Initiative Protocol for Metadata Harvesting

OECD organisation for Economic Co-operation and Development

OMII open Middleware Infrastructure Institute

OPEX operating Expenditure

OSF operations Support Facility

OSG open Science Grid

OTP one Time Passwords

OWL ontology Web Language

PaaS Platform as a Service

PII Personally Identifiable Information

PKI Public Key Infrastructure

PMH Protocol for Metadata Harvesting

PoP Point of Presence

R&E Research and Education

RADIUS Remote Authentication Dial In user Service

RAM Random Access Memory

RDF Resource Description Framework

REST Representational State Transfer

RF/IF Radio Frequency/Intermediate Frequency

RNA Ribonucleic acid

RTT Round-Trip Time

S3 Simple Storage Services (Amazon)

SaaS Software-as-a-Service

SAML Security Assertion Markup Language

SIM Subscriber Identification Module

SIP Session Initiation Protocol

SIPTO Selective IP Traffic offload

SKA Square Kilometre Array

SLA Service Level Agreement

SLAC Stanford Linear Accelerator Center

SMIL Synchronized Multimedia Integration Language

SRM Storage Resource Manager

SSID Service Set Identifier

SVG Scalable vector Graphics

SWOT Strengths, Weaknesses, opportunities, Threats

TERENA Trans European Research and Education Networking Association

TLS Transport Layer Security

back

to c

onte

nts

page

31 | ASPIRE NRENS STUDY

U.S. UCAN united States unified Community Anchor Network

UMF university Modernisation Fund (Greece)

UMTS universal Mobile Telecommunications System

VLAN virtual Local Area Network

VLBI very Long Baseline Interferometry

VLE virtual Learning Environment

VM virtual Machine

VO virtual observatory

VoIP voice over Internet Protocol

VOMS vo Membership Services

WAN Wide Area Network

WAP Wireless Application Protocol

WebDAV Web Distributed Authoring and versioning

Wi-Fi Wireless exchange of data

WiMAX Worldwide Interoperability for Microwave Access

WLAN Wireless Local Area Network

WLCG Worldwide LHC Computing Grid

XML Extensible Markup Language

back

to c

onte

nts

page

David Foster, CERN, Switzerland

DAvID FoSTER has both a BSc and PHD from Durham university, Department of

Applied Physics and Electronics, and an MBA from Durham university Business

School. He has spent more than thirty years at CERN and has held many technical

and managerial roles. He currently chairs a number of international committees

on networking and supercomputing as well as representing CERN on a number of

projects with the European Commission. David is currently Deputy IT Department

Head at CERN and has particular responsibility for international network strategy

as well as infrastructure strategy in the areas of information management. He is

a Fellow of the Institute of Physics and a member of the Chartered Management

Institute and the Association of MBAs.

Michael Nowlan, Ireland

ASPIRE NRENs Study Leader

MICHAEL NoWLAN is a consultant in the higher education networking and IT

sector, especially in a European context. until 2008, he was Director of Information

Systems Services at Trinity College Dublin and was involved with HEAnet, the

Irish NREN, since its foundation in 1983.

Victor Reijs, HEANET, Ireland

After studying at the university of Twente in the Netherlands, vICToR REIJS

worked for KPN Telecom Research and SuRFnet. He was involved in CLNS/TuBA

(one of the earlier alternatives for IPv6). Experience was gained with x.25 and ATM

in a national and international environment. His last activity at SuRFnet was the

tender for SuRFnet5 (a step towards optical networking). Emigrating to Ireland,

he manages the network development team of HEAnet and is actively involved

in international activities, such as GN3 and Mantychore (IP Networks as a Service),

as well as (optical) networking, point-to-point links, virtualisation and monitoring.

32 | ASPIRE NRENS STUDY

7 CoNTRIBuToRS

back

to c

onte

nts

page

Klaas Wierenga, CISCo, The Netherlands

KLAAS WIERENGA works in the Research and Advanced Development group

of Cisco Systems. He has worked in the Dutch NREN SuRFnet for over ten years

and currently serves as chair of the TERENA Task Force on Mobility and Network

Middleware. He co-authored the Cisco Press publication “Building the Mobile

Internet” and is the inventor of eduroam. He is particularly interested in future

development of the Internet in the areas of identity and mobility.

Asher Rotkop, IuCC, Israel

ASHER RoTKoP is Director Genral of IuCC, CIo of Tel Aviv university, and Deputy

Director General for Higher Education. He is an IT expert, with wide experience

in the IT infrastructures and Information Systems of universities. He is focused

on leading IuCC (the NREN of Israel) towards fulfilling the universities’ needs by

expanding its range of activities to include added-value services such as, cloud and

DRP, data base agreements with libraries, and inter-university IT services.

Christoph Witzig, SWITCH, Switzerland

CHRISToPH WITzIG is the head of the Central ICT Providers at SWITCH, the NREN

of Switzerland. He holds a degree in High Energy Physics from ETH zurich and

worked for several years at Brookhaven National Laboratory in upton, Ny. He held

various positions in the commercial sector before joining SWITCH in spring 2005.

33 | ASPIRE NRENS STUDY

back

to c

onte

nts

page

34 | ASPIRE NRENS STUDY

Appendix 1: Terms of Reference of ASPIRE NREN Futures Panel

The future roles of NRENS 25

The NRENS and the R&E networking community exist in a rapidly evolving environment, characterised by

technological innovation, increasing numbers of service suppliers and ever demanding users.

As a result of the current global economic crisis, some NRENs have to cope with severe financial constraints.

Institutional funding is coming under closer scrutiny, and the management of institutions endeavours to extract

maximum value from the available resources. NRENs should be aware that services that they have traditionally

provided for users may now be available from commercial cloud services providers. NRENs should seek to

maximise their value to the community by brokering deals with such providers.

Meanwhile, users expect that the services available to them will include tools for real-time interaction,

collaborative working, media sharing, and social interaction, as well as traditional document-creation and email.

There is increasing globalisation in all sectors of human activity, including R&E. Many of the achievements being

made on the global scale are too large or complex to be realised through national initiatives. Therefore, it is

vital that excellent global communication and network services are available to support the growing number

of distributed and collaborative virtual organisations. The NRENs are well placed to satisfy these requirements,

acting in collaboration with industry. However, the current model of NRENs providing a full range of services by

themselves to their connected institutions is facing a disruptive challenge.

While the European NRENs have a good history of collaborating at a pan-European level through organisations

like TERENA, this collaboration should be intensified and extended globally if the community is to stay relevant to

serving the future needs of R&E.

NRENs, and possibly other organisations in the R&E networking community, should capitalise on the cohesiveness

of the community and negotiate jointly with suppliers to obtain higher levels of service and cost savings.

Several European NRENs already connect organisations involved in lifelong-learning, e-Health, e- Culture, and

e-Government, while in other countries, there are other organisations catering for those sectors. The European

Commission wishes to encourage more intensive cooperation between the R&E networking community and the

commercial sector, as part of the European union vision for a digital Europe. The NRENs can play an essential role

in developing and improving networking and related services for those sectors, capitalising on the strengths of

the European R&E networking community in areas such as security, mobility, and middleware.

This sub-study will include exploration and discussion of the following issues: