A i P ifi S t C d O tl kAsia Pacific Smart Card Outlook

“Secure Silicon for Smart Cards”

March 2009

Focus Points

Global Smart Cards IC Overview

Asia Pacific Smart Cards IC Overview

• APAC Smart Card IC Market Dynamics

K M k t D i & R t i tKey Market Drivers & Restraints

Smart Card IC Overview & Market Size

• Impact of Financial Crisis on the Smart Card Industry by key applicationsImpact of Financial Crisis on the Smart Card Industry by key applications

• Conclusion – Smart Cards Outlook 2009

• Key Take Away Messages

Highlights of Related and Upcoming Research & About Us

Questions & Answers

2

Global Smart Cards IC Overview

Smart Card IC Market: Market Segmentation (World), 2008

• Applications such as SIM, Banking and payment,

ICs (Integrated Circuits)

Applications such as SIM, Banking and payment, Government ID, transportation are key contributors to the total global smart card IC and smart card revenue.

• Europe and parts of Asia have been theEurope and parts of Asia have been the technological leaders in smart card application over the years. In both these regions, there are catalysts in various fields, pushing the boundaries of smart card usage year on year.

Memory Microcontroller

• France, Germany and UK are among the more progressive nations in Europe, with adoption in all key applications today.

• Asia Pacific houses the most progressive markets• Asia Pacific houses the most progressive marketslike Japan and South Korea and potential volumesfrom China and India. However at the same time, a large part of this region, in contrast, is extremely nascent, if not underdeveloped.

NorthAmerica

LatinAmerica

AsiaPacific EMEA

• North America – contactless continue to gain healthy growth

3

Global Smart Cards IC Overview

• Major applications continue to offer steady growth.

• Price continues to have an impact on the market.

• New emerging vertical markets begin to show real promise in terms of growth• New emerging vertical markets begin to show real promise in terms of growth.

• Use of biometrics increases sparked by US intervention.

• The use of contactless technology in the payment sector in all regions heightens.

MCU Smart card IC gaining Momentum thrust on security and larger memory capacity• MCU Smart card IC gaining Momentum –thrust on security and larger memory capacity

• Continued variance of market strategies used by manufacturers leading to a dynamic competitive landscapecompetitive landscape.

4

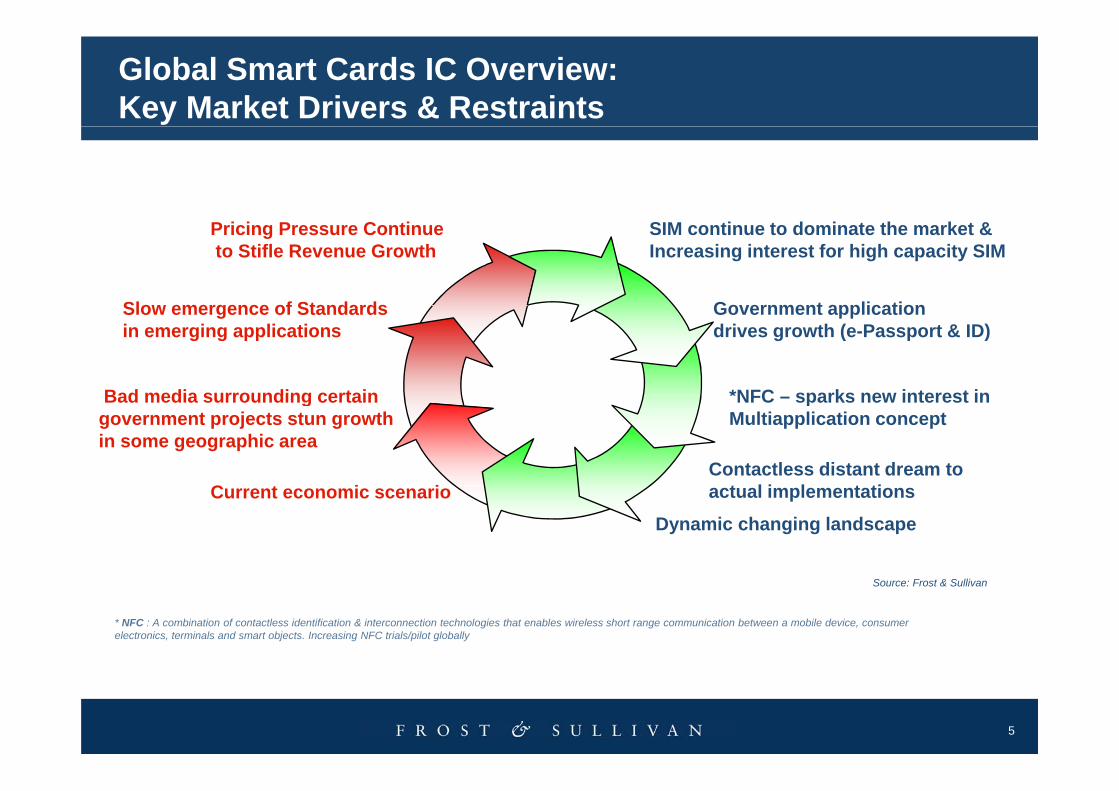

Global Smart Cards IC Overview: Key Market Drivers & Restraints

SIM continue to dominate the market & Increasing interest for high capacity SIM

Pricing Pressure Continueto Stifle Revenue Growth

Slow emergence of Standards Government application

*NFC sparks new interest in

Slow emergence of Standards in emerging applications

Government applicationdrives growth (e-Passport & ID)

Bad media surrounding certain NFC – sparks new interest inMultiapplication concept

Contactless distant dream to t l i l t tiC t i i

Bad media surrounding certain government projects stun growth in some geographic area

actual implementationsCurrent economic scenarioDynamic changing landscape

* NFC : A combination of contactless identification & interconnection technologies that enables wireless short range communication between a mobile device, consumer electronics, terminals and smart objects. Increasing NFC trials/pilot globally

Source: Frost & Sullivan

5

Global Smart Cards IC Overview: Market Size

Smart Card IC Market: Revenue Forecasts (World), 2001-20135,000.0

3,500.0

4,000.0

4,500.0

,0,

000)

2,000.0

2,500.0

30,00.0

enue

s ($

00

500.0

1,000.0

1,500.0Rev

e

0.02001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

YearNote: All figures are rounded; the base year is 2007. Source: Frost & Sullivan

• In 2007 approximately over 4.9 billion smart cards IC were shipped worldwide

• By 2013- expected to grow to over 9 billion units with CAGR of approximately 12-13% (2007-2013)

6

Percentage Split by Region 2007 & Forecast 2013

Smart Card IC Market: Unit Shipments Split by Geographic Region (World), 2007

N th d L ti A iNorth and Latin America 6.2%

Smart Card IC Market; Unit Shipments Split by Geographic Region (World) 2013Europe Middle East

Asia Pacific3 9% Geographic Region (World), 2013

North and Latin America 4.9%

Europe, Middle East and Africa

55.9%

37.9%

Europe, Middle East and Africa

53.3%Asia Pacific

41.8%

Note: All figures are rounded; the base year is 2007. Source: Frost & Sullivan

7

Partial list of Emerging Applications

Healthcare

Mobile PaymentsGaming

EmergingEmerging Applications

TourismFurther Developments in NFC

Rural BankingSource: Frost & Sullivan

8

Price War

Plummeting SIM card prices

Competition is good for driving efficiency, BUT:

Significant impact for vendors globally- more dramatic in Asianmarkets.

Vicious price war aggravated by local players is potentially damaging to the industry, as this could eat into the reserves for further R&D and

Resulted in overall revenue drops for many players in Asia.

innovation required of smart card manufacturers to further progress the industry.

When the price is too low, some of the card vendors might corrupt the quality and securityp y p y

Foreign vendors in the largest Asian market, China, loss market share to local competitors

vendors might corrupt the quality and securitystandards in order to survive. In the long run, this will affect the end users

Interesting to see developments of local vendors-competitors. g pcan live up to the expectation of 3G requirements by telcos and users alike.

9

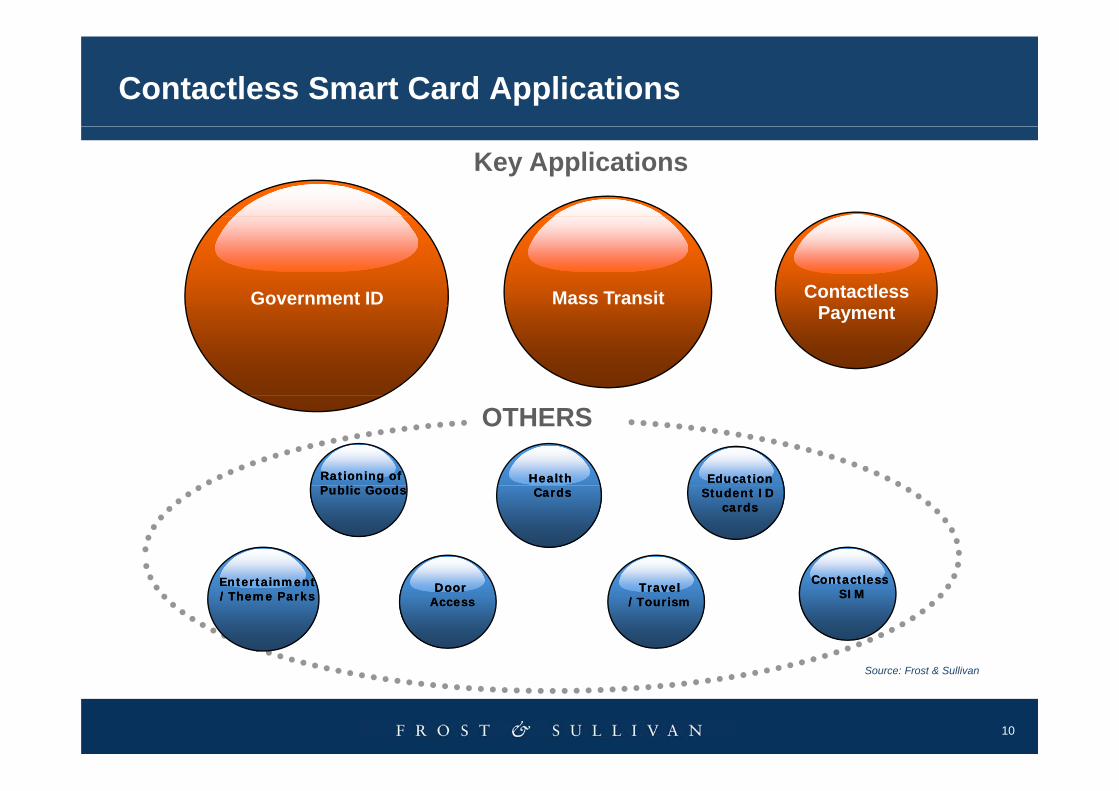

Contactless Smart Card Applications

Key Applications

Government ID Mass Transit Contactless PPayment

Rationing ofRationing ofbli dbli d

Health Health EducationEducation

OTHERS

Public GoodsPublic Goods CardsCards Student ID Student ID cardscards

C l C l TravelTravel

/Tourism/Tourism

EntertainmentEntertainment/Theme Parks/Theme Parks

Contactless Contactless SIMSIMDoor Door

AccessAccess

10

Source: Frost & Sullivan

Key Applications for Contactless-Partial List of Examples

Key Applications

Government ID Mass Transit Contactless Government ID Mass Transit Co tact essPayment &

Loyalty

e-Passport

National ID/Citizen Cards (e.g.

SUICA

T-Money

Visa Wave/Touch

MasterCard's MyKad and Second Generation ID card in China)

Driving License/Vehicle Registration

Octopus

Ez-Link

PayPass/PayWave

JCB – QUICPay/JSpeedy

Edy prepaid e walletForeign Worker Cards

Public Sector Cards

Taxation Cards

Taiwan Money Card & EasyCard

Edy – prepaid e-wallet

Moneta

11

Social Security

Contactless Market Trends

Security concerns drive business case for various applications

Flexible form factors provide opportunities forFlexible form factors provide opportunities for value-add

Upgrade and improved features in some pg papplications

Convergence of mass transit and payment – on d d bil l tfcards and mobile platform

NFC and other mobile payment technologies moves towards mass adoptionp

12

APAC Market Dynamics

High population.I di 1 1 billi

New technologyIndia = 1.1 billion

China = 1.3 billion

gyacceptance levels

highEg: Japan, Korea

Densely populated regions. Minimal legacy

systems in Tier 3

Rising Income Manufacturing Hub of

the world.

ycountries

Levels.Improvement in

standards of living

Majority of markets far from saturation

13

APAC Smart Cards IC Overview: Key Market Drivers

SIMContinues to

ContactlessProven to be

Drive Growth

A WinningBusiness Case

Growth inTransit Projects

GovernmentMandates & roll out& roll out

NFC Brings New Interest to contactless and Multi-application

Source: Frost & SullivanLargeUser base

Source: Frost & Sullivan

14

NFC Outlook

Current State Future State: Mass DeploymentO di k f

Convergence of Availability of Contactless t d

Outstanding key factors

2006 & 07: trials, acceptance

testing &standards

setting

Convergence of contactless SC

apps on 1 platform

yhandsets smart card

infrastructure

setting

U i APAC: South

Equitable business

model

TSM and support

service for multi-appsUsing

Contactless SC technology –

mobile devices

APAC: South Korea and Japan leads way with

highest usage of contactless

multi-apps

Interoperability &

standards

APAC Volume Ramp up- expected in later halff 2010

* NFC : A combination of contactless identification & interconnection technologies that enables wireless short range communication between a mobile device, consumer electronics, terminals and smart objects. Increasing NFC trials/pilot globally

15

of 2010Increasing NFC trials/pilot globally

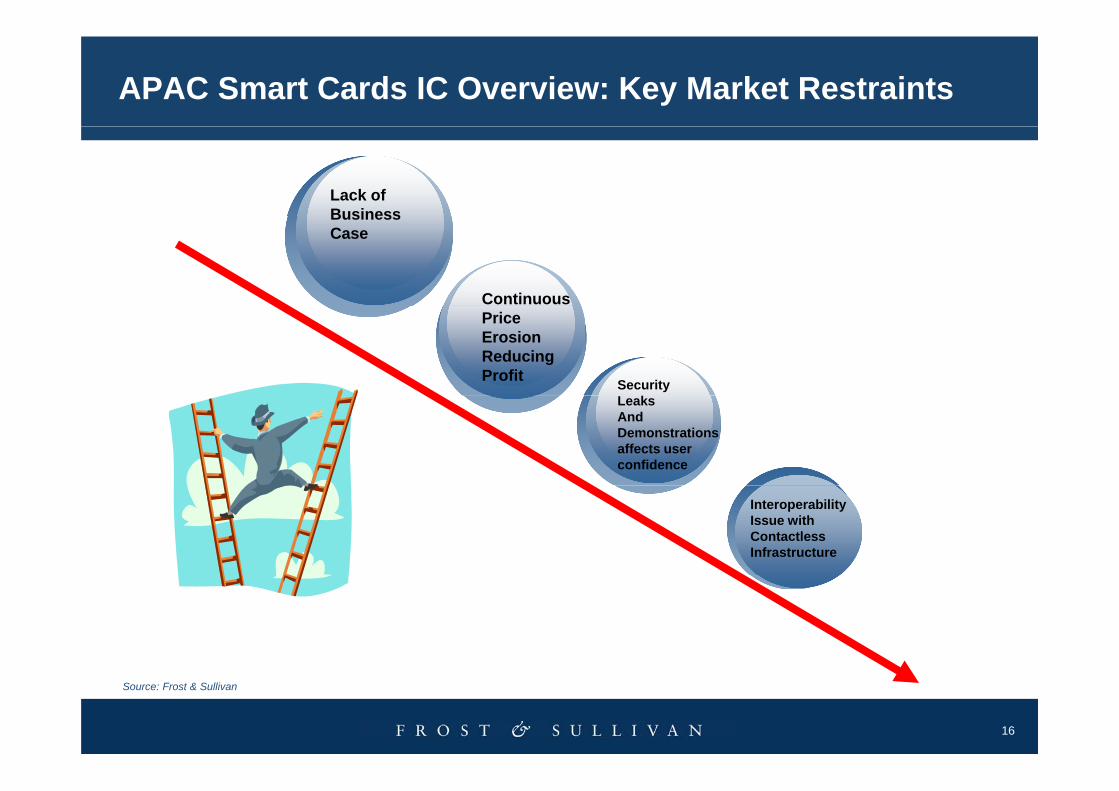

APAC Smart Cards IC Overview: Key Market Restraints

Lack of BusinessBusinessCase

ContinuousPriceErosionReducing Profit Security

LeaksAnd Demonstrations affects user confidence

InteroperabilityIssue with ContactlessInfrastructure

16

Source: Frost & Sullivan

APAC Smart Cards Overview: Market Size & Estimated Forecast

2007 APAC total smart card IC shipments = over 1.9 billion units (to grow to over 4 billion by 2013 ( with CAGR of approximately 15%)CAGR of approximately 15%)

• In 2007, SIM was still the key application with approximately 60% of total smart card volume in the region

Others SIM60%

Mobile Communication

34% 60%

Government ID Mass TransitAPAC

Key Smart Card

Others40%

2006 Total Asia Pacific Smart Card MarketCard Applications

Corporate Security

Banking/ Loyalty 2007 Total Asia Pacific Smart Card Market

SIM 60%

Others Source: Frost & Sullivan

17

Impact of Financial Crisis on the Smart Card Industry by Key Applications

2009 outlook

Corporate Security

Government ID Loyalty & Banking

GDP Growth, (World), 1970-2010

Emerging and

9.0%

Emerging and developing economies

World

3.0%

6.0% Grow

th (%)

Healthcare Telecom

Advanced economies

19 0-3.0%

0%

18

1970 1975 1980 1985 1990 1995 2000 2005 2010FSource: IMF

Corporate Security Outlook

• Irrespective of the economic scenario, security will continue to be a key issueissue.

• Companies may have reduced their budgets in terms of the type of security needed; they might prefer standard security systems, which offer good

it th th hi h d it tsecurity, rather than high-end security systems.

• Security tensions are still quite high in the Asia Pacific region (e.g. Bali, Mumbai and Pakistan)

• In order to have economic security measure, smart cards would be employed to have the biometric template on the chip, as against a database that would attract significantly higher costs. C t it th f ill ti t b f hi h i it i ti• Corporate security, therefore, will continue to be of high priority, irrespective of the economic scenario.

• Vendors can maximize on the cards ability to host multiapplications on a card – for example in addition to physical access control application –card – for example in addition to physical access control application –suggest to include cafeteria /micropayment application to ensure higher return on investment (ROI)

19

Loyalty & Banking Outlook

• The banking vertical is expected to experience a slowdown in 2009, as a direct consequence of various financial institutions having stricter regulations on the issuance ofconsequence of various financial institutions having stricter regulations on the issuance of credit cards. This scenario is, however, not expected to be a long-term effect.

• Banks would also be looking at situations where a credit card could be given to a high-risk customer, but with stricter penalties in case of defaults. Moreover, the credit limit would be

h t i t d f hi h i k tvery much restricted for high-risk customers.

• Financial institutions will be looking at having proper segmentation. As per the segmentation, users will have benefits that are apt for their credit rating. These conditions will not be binding forever as the users credit rating could increase depending on his/herwill not be binding forever, as the users credit rating could increase depending on his/her payback capacity over a period of time. In such cases of improvement in the user's credit rating scores, he/she can opt for higher, or better, privileges on the same card. The privileges may be in the form of more credit, or lower interest rates, or even the availability of loans and insurance on the card.

• Through a smart card, these conditions can be rewritten as many times as there is a change in the user's credit rating score.

• Loyalty programs are expected to continue unabated despite many of them still being inLoyalty programs are expected to continue unabated, despite many of them still being in the pilot stages. The loyalty card programs, as a matter of fact, are likely to experience a higher growth rate in 2009 than in the previous years, as a result of the economic recession. the loyalty program is expected to witness substantial growth with many of the customers wanting to take full advantages of the points accrued on their loyalty cards.

20

Telecom Outlook

• Mobile and social applications are expected to be some of the major growth areas for 2009.g

• Blogging and social applications that can be accessed from the mobile phone have all been growing since the second half of 2008, and are expected to continue to grow in 2009expected to continue to grow in 2009.

• Telecom applications will continue to grow especially in the emerging countries in Asia Pacific. Currently, mobile banking through short y, g gmessage services (SMSs) is extremely popular in the Philippines. In the current financial crisis, a rapid growth in additional subscribers in this field can be expected.

• Local participants should be able to provide quick applications that could be an addition to the payment application on these phones. The addition of these applications would be dependent on the subscriber identity

d l (SIM) d b i d d h ld th f hi hmodule (SIM) card being used and hence, could pave the way for higher capacity SIM cards in the future.

21

Healthcare

• The healthcare application is also likely to witness a slowdown in the issuance of smart cards Many of the healthcare card projects in Asiaissuance of smart cards. Many of the healthcare card projects in Asia are still in the pilot stage.

• The correct documentation and record conciliation features, which the ,smart card offers, are indispensable; however, during this time of an economic recession, many hospitals would rather concentrate their efforts on not increasing the cost to the end user.

• However for certain healthcare projects have been brought in line with the country's national ID project. Projects such as these will continue on track and other vendors such as the terminal readers can also betrack and other vendors, such as the terminal readers, can also be expected to benefit from such programs.

22

Government ID

• It is during an economic recession that individual vehicle owners would consider other more economic modes of transportation Thus will see aconsider other, more economic modes of transportation. Thus will see a steady growth in this application market.

• Transit projects in the Asia Pacific region are already quite popular and p j g y q p phave been chosen as the killer application for contactless smart cards.

• Small value payments is already an application that is being uploaded p y y pp g pon many of the transit cards. Revenues generated from this application could be used by smart card participants to invest in new applications.

• One of the first applications that is usually considered is the loyalty application, which could be added on to the transit card, that is likely to be a new and faster source of revenue generation. Retail and loyalty can also be used in conjunction with an access control applicationalso be used in conjunction with an access control application.

23

Government Application/s Outlook

• Government ID projects are expected to continue without any delays as a result of the economic recession.

• The main driver for government ID cards continues to be security threats in the Asian region, which takes precedence over the recession.

• Various governments are providing tax holidays or concessions for companies during these tough times. In line with this, various governments are bringing in more companies in the value chain for the production and issuance of smart card, which would be beneficial to the country in the final reckoning. y g

• In line with an increase in the demand for security, government agencies in the Asia Pacific region will be increasing their security, especially along border regions. This would demand fast and proper identification of citizens in these areas.p p

• The e-passport program is an example of a project that will not see any reduction in unit shipments over the years. As a matter of fact, certain new additions can be expected in the security protocols of the e passport program, in terms of other biometric parametersthe security protocols of the e passport program, in terms of other biometric parameters being added apart from facial and fingerprint.

• The e-passport program would also ensure the stable growth of high-capacity chips in the coming years with more countries being brought in under the web

24

coming years, with more countries being brought in under the web.

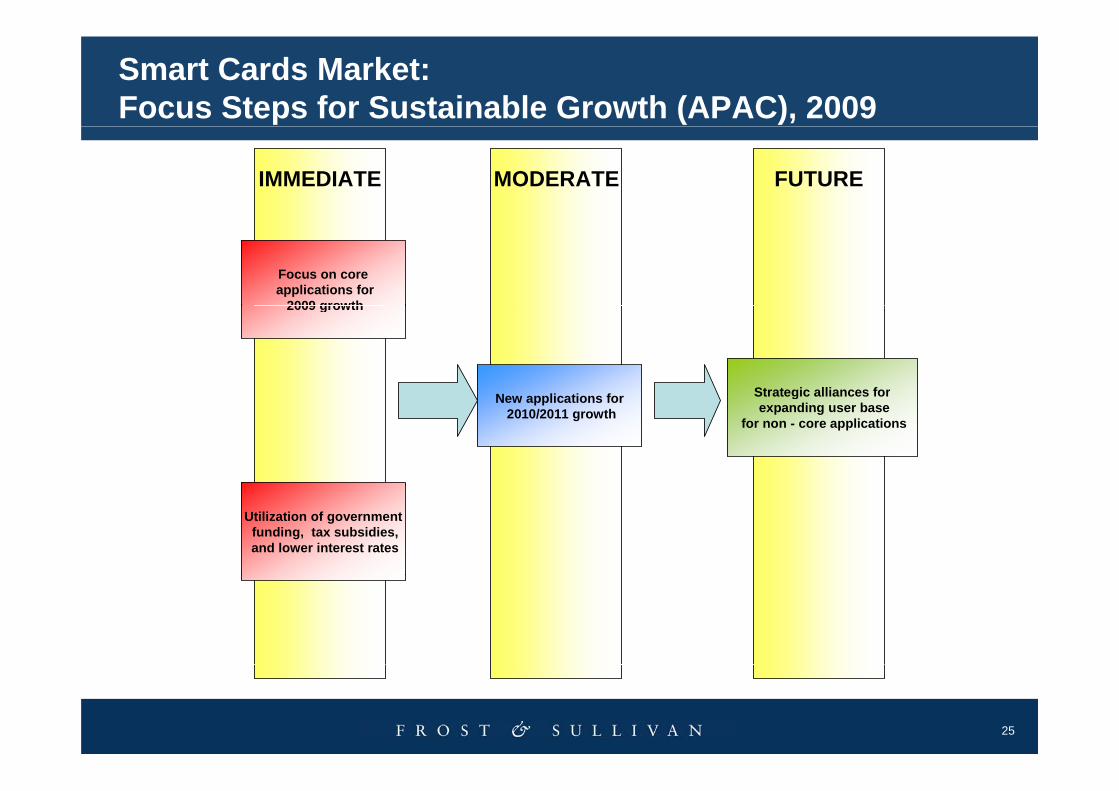

Smart Cards Market: Focus Steps for Sustainable Growth (APAC), 2009

FUTUREMODERATEIMMEDIATE

Focus on coreapplications for

2009 growth2009 growth

N li ti f Strategic alliances forNew applications for2010/2011 growth

Strategic alliances forexpanding user base

for non - core applications

Utilization of governmentfunding, tax subsidies,and lower interest rates

25

Conclusions – Global Smart Card IC Growth Recommendations

• To be a market leader in this market, strong presence in the SIM market is required.

• Focusing on new emerging applications with certainly provide manufacturers with a boost in growth and also boost average selling prices.

• Looking for new types of customers is a medium term process and one which needs to be done carefully as not to frustrate existing ones.

National ID projects expected to provide momentum in the market• National ID projects expected to provide momentum in the market.

• NFC expected to bring substantial growth to the market in the coming years.

• Contactless and dual-interface technology on the upswing with electronic passports with contactless chips being the highlight.

26

Key Take Away Messages

• On the whole, the smart card industry participants should concentrate on their core competencies for their respective applications through utilizing all the benefits fromcompetencies for their respective applications through utilizing all the benefits from government subsidies, tax cuts, and so on.

• The next stage should be in investing, or at least laying the foundation, for the next g g, y g ,year from when an economic upswing is likely to be witnessed.

• New applications should be tapped now. pp pp

• Strategic alliances should also not be ruled out. A strategic alliance would help the industry participant to expand to new markets, as well as allow it to concentrate on its core competency.

27

Who is Frost & Sullivan

• A global growth consulting company that partners with clients to support the development ofA global growth consulting company that partners with clients to support the development ofinnovative growth strategies.

• For more than 45 years, we have leveraged our comprehensive market expertise to serve anextensive clientele that includes Global 10 000 companies emerging companies and the investmentextensive clientele that includes Global 10,000 companies, emerging companies, and the investmentcommunity

• We offer industry research and market strategies, provide growth consulting and corporate training, and support clients to help grow their businessesand support clients to help grow their businesses.

28

What Makes Us Unique

•Exclusively Focused on Growth •360o PerspectiveTMGlobal thought leader exclusively focused on

addressing client growth strategies and plans –Team actively engaged in researching and developing of growth models that enable clients

Proprietary T.E.A.M.TM Methodology integrates all 6 critical research methodologies to significantly enhance the accuracy of decision making and lower the risk of implementing growth strategiesdeveloping of growth models that enable clients

to achieve aggressive growth objectives.

•Industry Breadth

lower the risk of implementing growth strategies.

•Growth Monitoring

Continuously monitor changing technologyCover the broad spectrum of industries and technologies to provide clients with the ability to look outside the box and discover new and

Continuously monitor changing technology, markets and economics and proactively address clients growth initiatives and position.

Trusted Partnerinnovative ideas.

•Global Perspective

•Trusted Partner

Working closely with client Growth Teams –helping them generate new growth initiatives and

32 global offices ensure that clients receive a global coverage/perspective based on regional expertise.

leverage all of Frost & Sullivan assets to accelerate their growth.

29

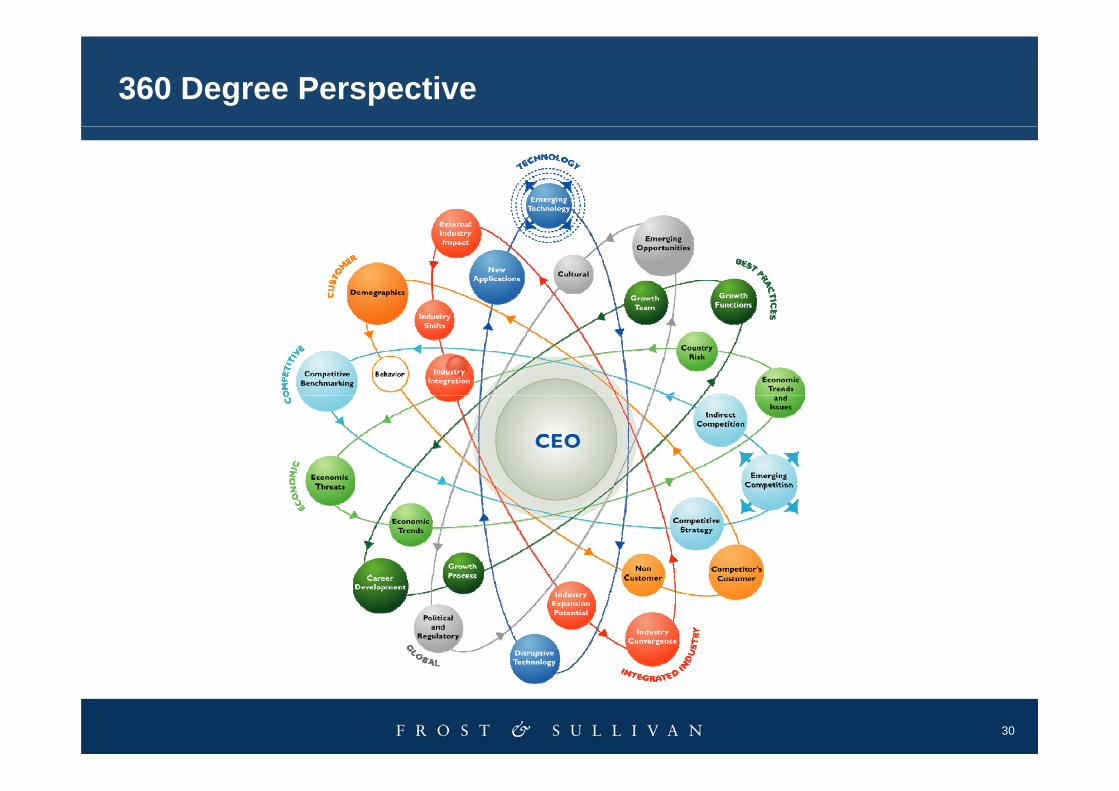

360 Degree Perspective

30

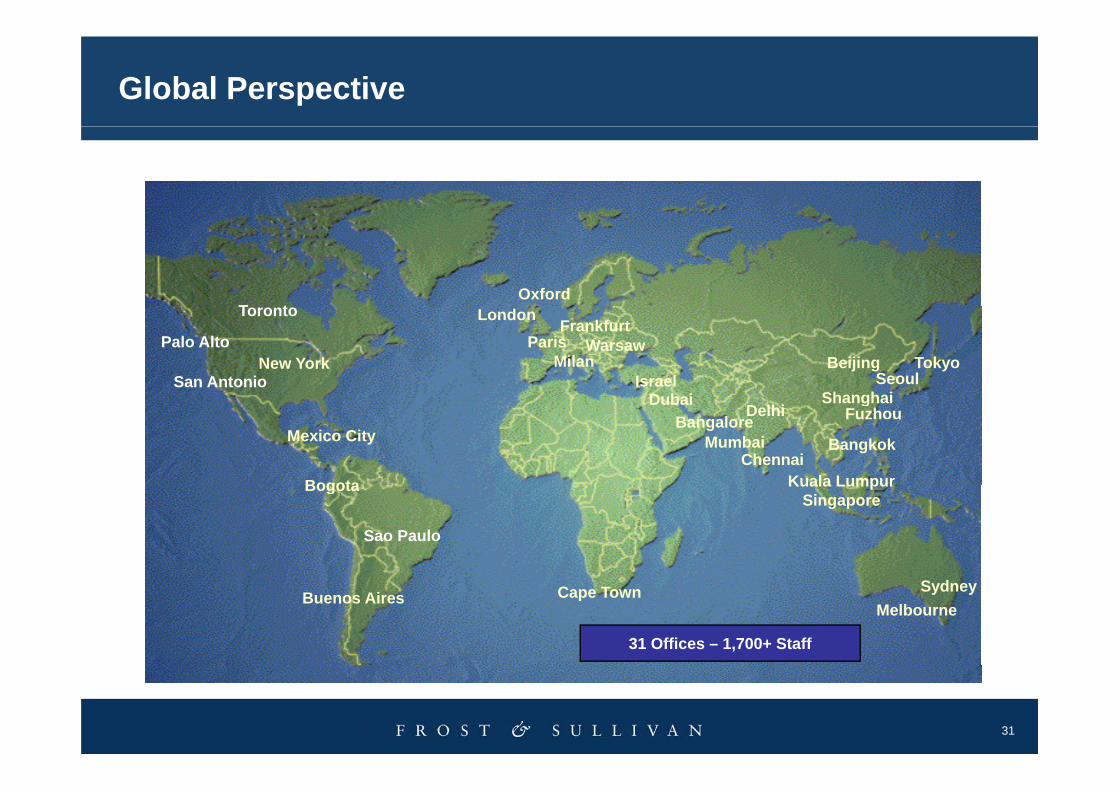

Global Perspective

T tOxford

London

Beijing Tokyo

TorontoFrankfurt

New YorkSan Antonio

Shanghai

Paris

SeoulIsraelD b i

WarsawMilan

Palo Alto

Kuala Lumpur

Mumbai

Shanghai

Mexico City

DubaiBangalore

BangkokChennai

Fuzhou

Bogota

Delhi

Kuala LumpurSingapore

Sao Paulo

Bogota

Buenos AiresSydneyCape Town

31 Offices – 1,700+ Staff

Melbourne

31

Highlights of Current & Upcoming Research

Research Titles (GLOBAL)

Draft Smart Card IC Market size

Research Titles (ASIA PACIFIC)

APAC Smart Card O tlook 2009Draft Smart Card IC Market size

Draft Smart Card Market size

Collection of Smart Card Numbers

Smart Card Market

APAC Smart Card Outlook 2009

APAC Smart Card Management System

APAC Smart Card Printers

P fil f l l C i S C d V l Smart Card Market

Smart Card SIM

Smart Cards for Banking

Smart Cards for Government

Profiles of local Companies: Smart Card Value Chain

Smart Card Third Party Testing

Chip & PIN in Asia (banking/payment)Smart Cards for Government

Smart Cards for Transportation

Smart Card IC Market

Contactless Smart Card

Chip & PIN in Asia (banking/payment)

South Korea Smart cards Market

Asia Best practices/Cases for Contactless Convergence

Readers & Chipsets

M2M

High Density SIM Cards

Asia Pacific Smart Card IC on Different Form Factors

Corporate security (inc Smart USB)

Smart Card Management Systems

Near Field Communication

32

Th kThank you

Questions & Answers

Recommended