Arvid Kjellberg- Jakub Lawik - Juan Mojica - Xiaodong Xu

Hull & White Trinomial Trees

The outline of our Project

by Journal of Derivatives in Fall 1994

Where to use it? if there is a function x = f(r) of the short rate r that follows a mean reverting arithmetic process

Our project: Hull and White trinomial tree building procedure Excel Implementation

Theoretical background

Short Rate (or instantaneous rate) The interest rate charged (usually in some particular market) for

short term loans.

Bonds, option & derivative prices can depend only on the process followed by r (in risk neutral world)

t - t+Δt investor earn on average r(t) Δt

Payoff:

ttTr feE )(ˆˆ

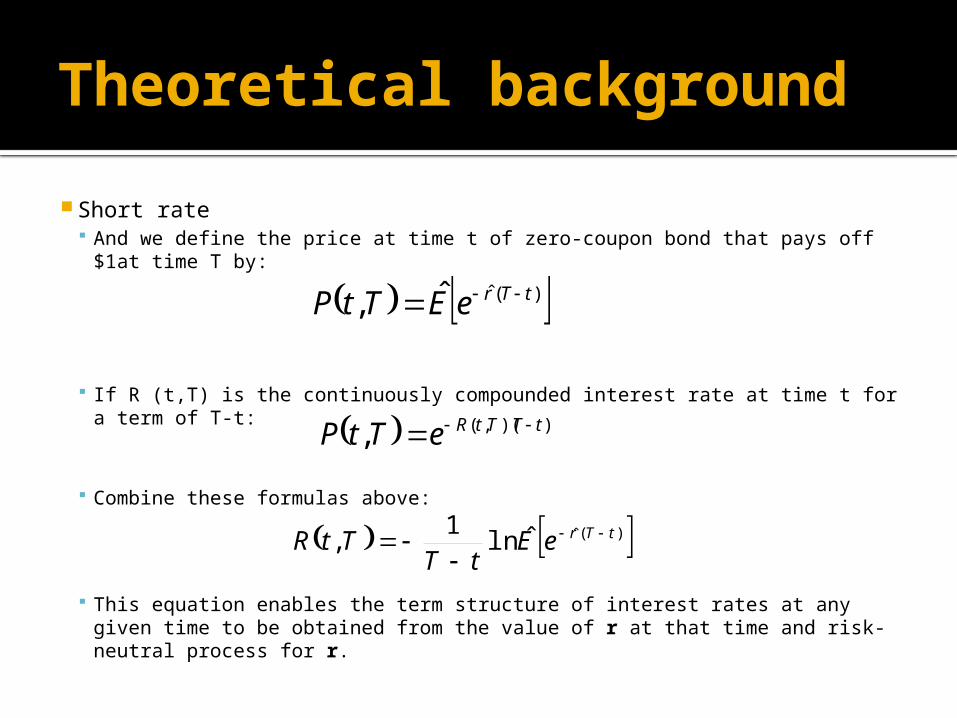

Theoretical background

Short rate And we define the price at time t of zero-coupon bond that pays off $1at time T

by:

If R (t,T) is the continuously compounded interest rate at time t for a term of T-t:

Combine these formulas above:

This equation enables the term structure of interest rates at any given time to be obtained from the value of r at that time and risk-neutral process for r.

And we define the price at time t of zero-coupon bond that pays off $1at time T by:

This equation enables the term structure of interest rates at any given time to be obtained from the value of r at that time and risk-neutral process for r.

)(ˆˆ, tTreETtP

))(,(, tTTtReTtP

)(ˆˆln1

, tTreEtT

TtR

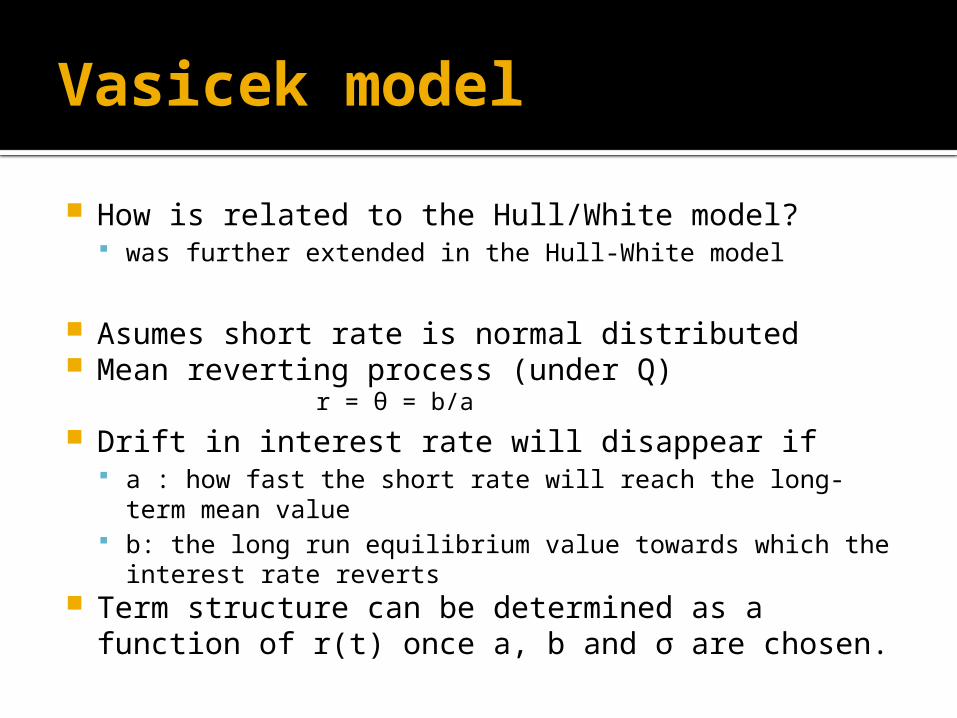

Vasicek model

How is related to the Hull/White model? was further extended in the Hull-White model

Asumes short rate is normal distributed Mean reverting process (under Q)

Drift in interest rate will disappear if a : how fast the short rate will reach the long-term mean value b: the long run equilibrium value towards which the interest rate

reverts Term structure can be determined as a function of r(t)

once a, b and σ are chosen.

r = θ = b/a

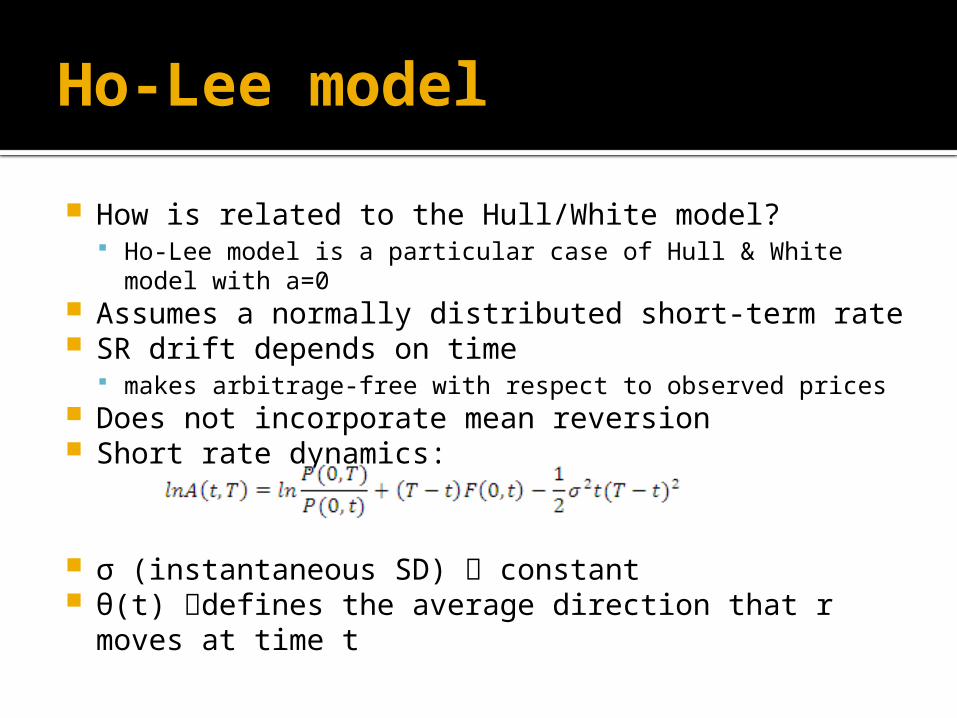

Ho-Lee model

How is related to the Hull/White model? Ho-Lee model is a particular case of Hull & White model with a=0

Assumes a normally distributed short-term rate SR drift depends on time

makes arbitrage-free with respect to observed prices Does not incorporate mean reversion Short rate dynamics:

σ (instantaneous SD) constant θ(t) defines the average direction that r moves at time t

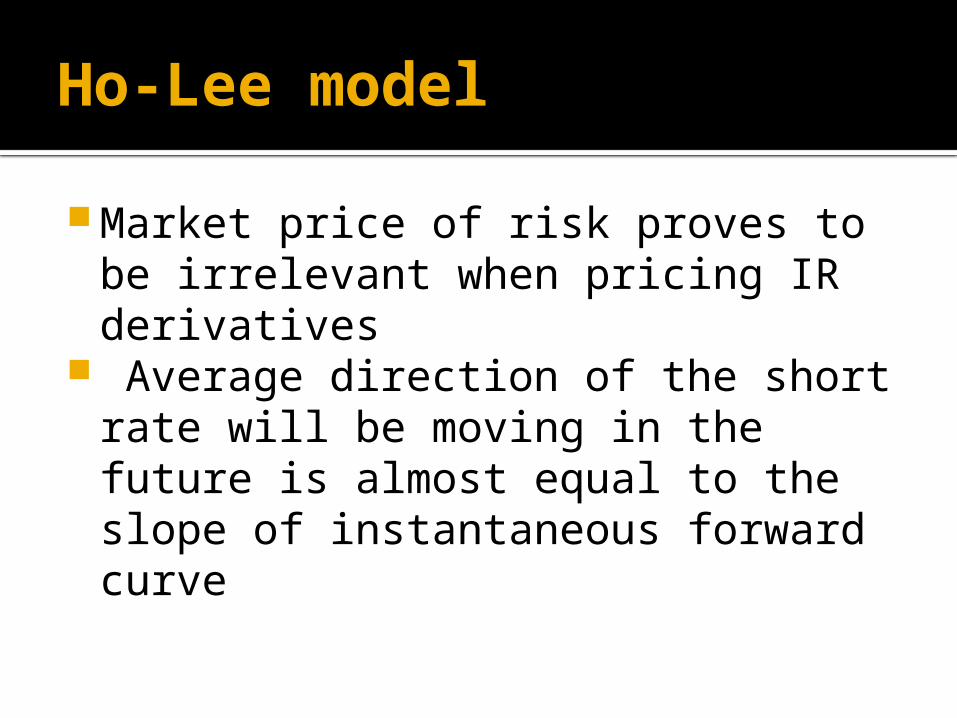

Ho-Lee model

Market price of risk proves to be irrelevant when pricing IR derivatives

Average direction of the short rate will be moving in the future is almost equal to the slope of instantaneous forward curve

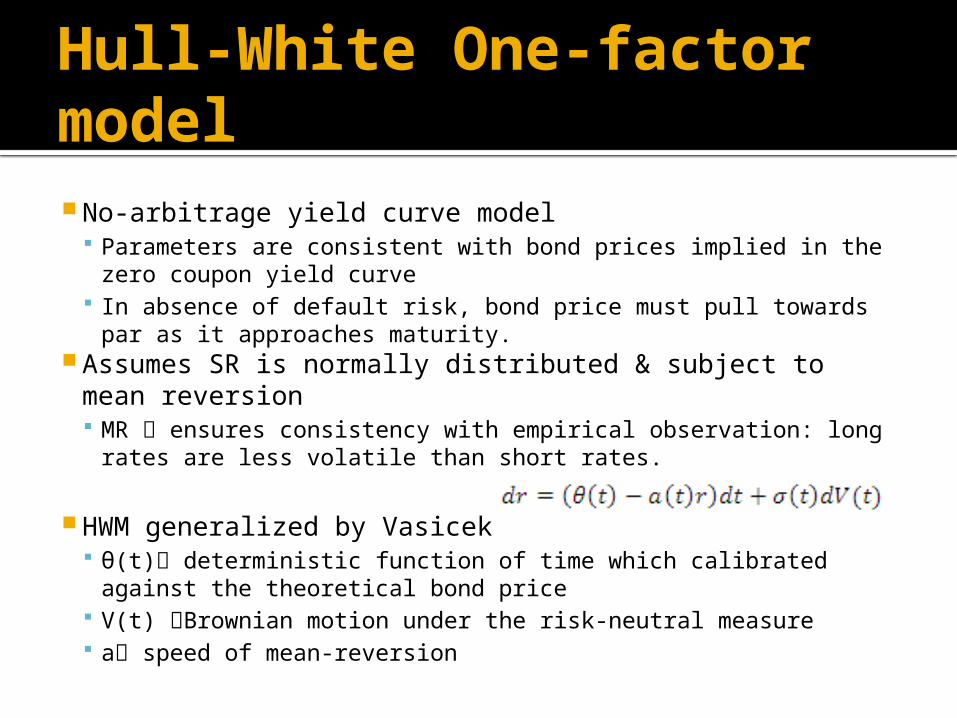

Hull-White One-factor model

No-arbitrage yield curve model Parameters are consistent with bond prices implied in the zero coupon

yield curve In absence of default risk, bond price must pull towards par as it

approaches maturity. Assumes SR is normally distributed & subject to mean reversion

MR ensures consistency with empirical observation: long rates are less volatile than short rates.

HWM generalized by Vasicek θ(t) deterministic function of time which calibrated against the

theoretical bond price V(t) Brownian motion under the risk-neutral measure a speed of mean-reversion

Volatility (estimation and structure)

Input parameters for HWM a : relative volatility of LR and SR σ : volatility of the short rate

Not directly provided by the market (inferred from data of IR derivatives)

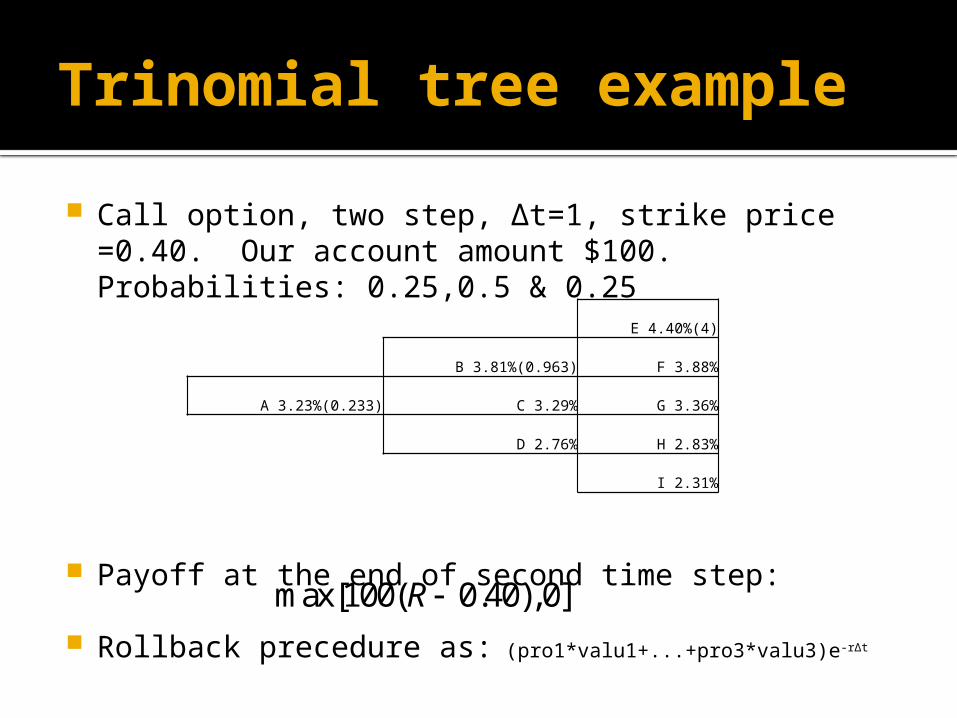

Trinomial tree example

Call option, two step, Δt=1, strike price =0.40. Our account amount $100. Probabilities: 0.25,0.5 & 0.25

Payoff at the end of second time step:

Rollback precedure as: (pro1*valu1+...+pro3*valu3)e-rΔt

max[100( 0.40),0]R

0.00% 0.00% E 4.40%(4)

0.00% B 3.81%(0.963) F 3.88%

A 3.23%(0.233) C 3.29% G 3.36%

0.00% D 2.76% H 2.83%

0.00% 0.00% I 2.31%

0.00% 0.00% 0.00%

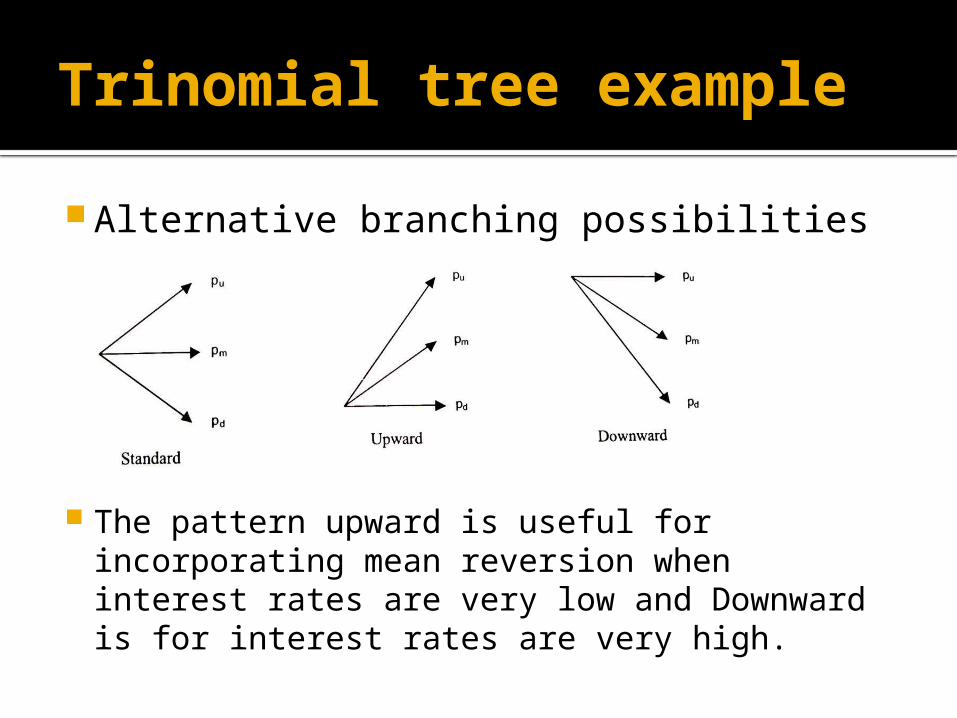

Trinomial tree example

Alternative branching possibilities

The pattern upward is useful for incorporating mean reversion when interest rates are very low and Downward is for interest rates are very high.

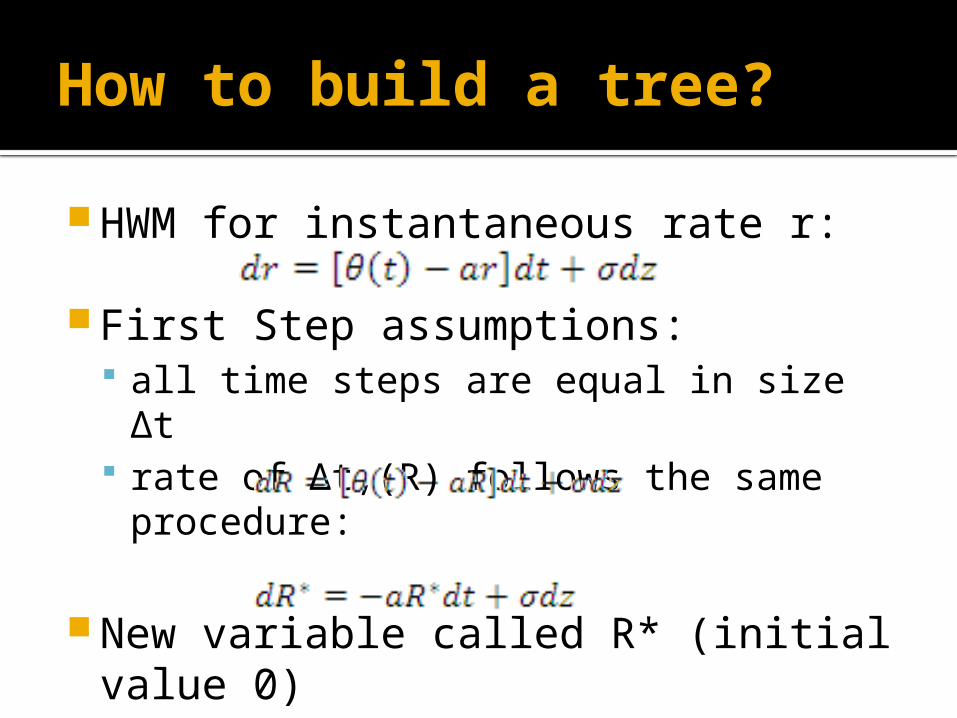

How to build a tree?

HWM for instantaneous rate r:

First Step assumptions: all time steps are equal in size Δt rate of Δt,(R) follows the same procedure:

New variable called R* (initial value 0)

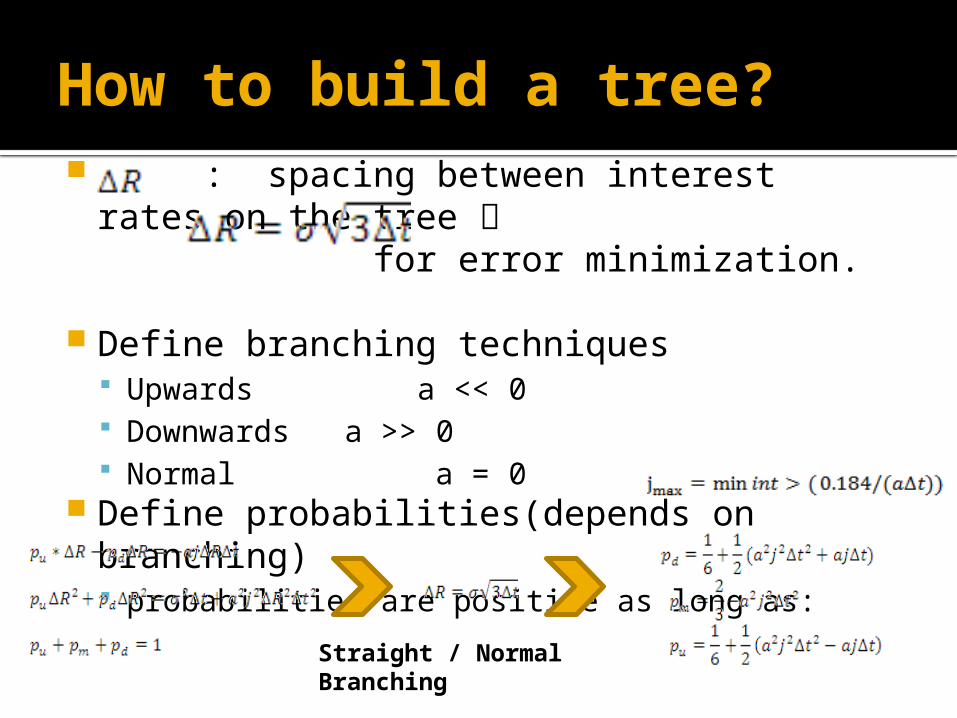

How to build a tree? : spacing between interest rates on the tree

for error minimization.

Define branching techniques Upwards a << 0 Downwards a >> 0 Normal a = 0

Define probabilities(depends on branching) probabilities are positive as long as:

Straight / Normal Branching

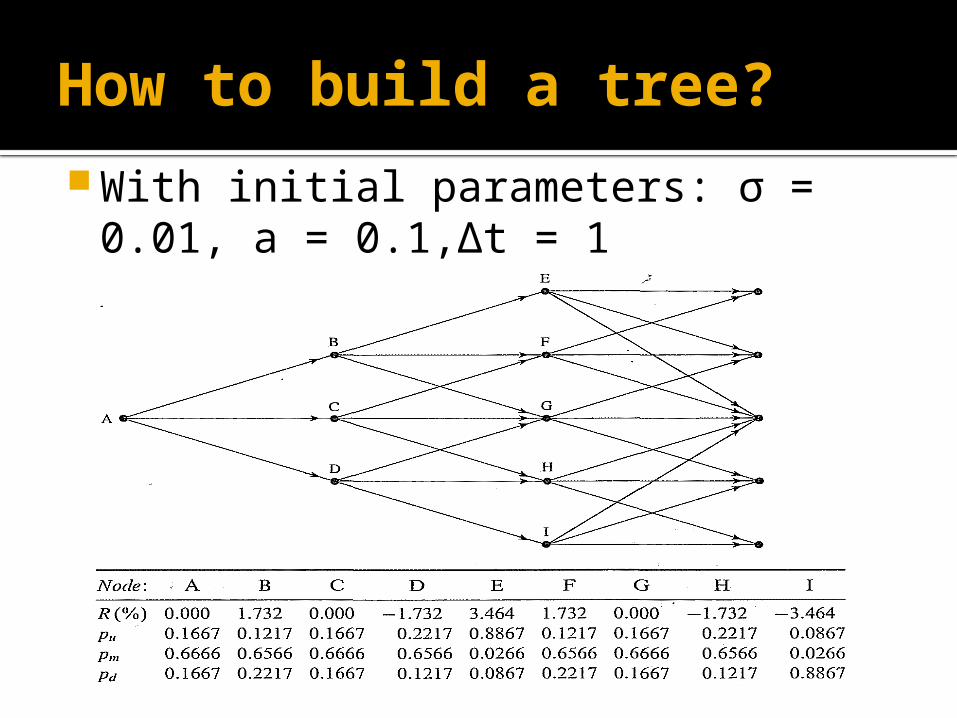

How to build a tree?

With initial parameters: σ = 0.01, a = 0.1,Δt = 1 ΔR=0.0173,jmax=2,we get:

How to build a tree?

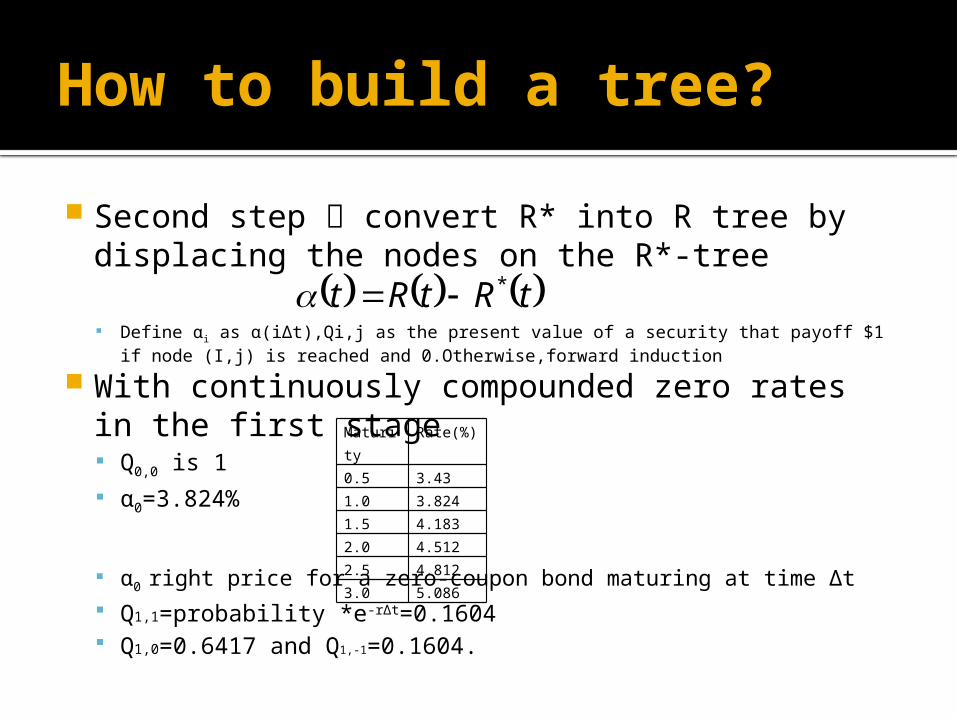

Second step convert R* into R tree by displacing the nodes on the R*-tree

Define αi as α(iΔt),Qi,j as the present value of a security that payoff $1 if node (I,j) is reached and 0.Otherwise,forward induction

With continuously compounded zero rates in the first stage Q0,0 is 1

α0=3.824%

α0 right price for a zero-coupon bond maturing at time Δt

Q1,1=probability *e-rΔt=0.1604 Q1,0=0.6417 and Q1,-1=0.1604.

Maturity Rate(%)0.5 3.431.0 3.8241.5 4.1832.0 4.5122.5 4.8123.0 5.086

tRtRt *

How to build a tree?

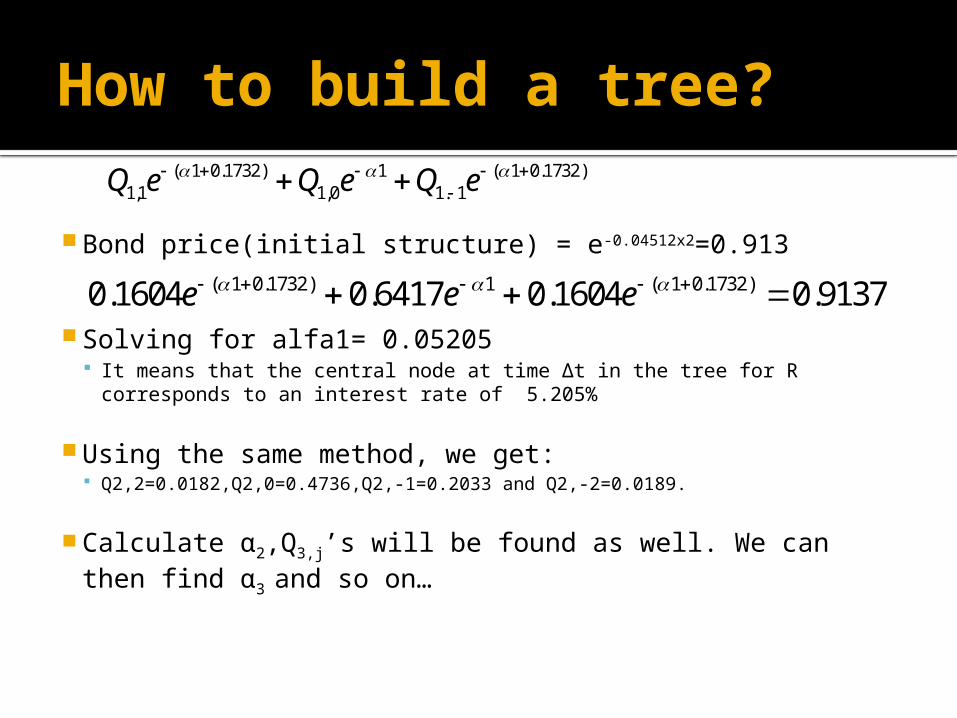

Bond price(initial structure) = e-0.04512x2=0.913

Solving for alfa1= 0.05205 It means that the central node at time Δt in the tree for R corresponds to an interest

rate of 5.205%

Using the same method, we get: Q2,2=0.0182,Q2,0=0.4736,Q2,-1=0.2033 and Q2,-2=0.0189.

Calculate α2,Q3,j’s will be found as well. We can then find α3 and so on…

( 1 0.1732) 1 ( 1 0.1732)1,1 1,0 1. 1Q e Q e Q e

( 1 0.1732) 1 ( 1 0.1732)0.1604 0.6417 0.1604 0.9137e e e

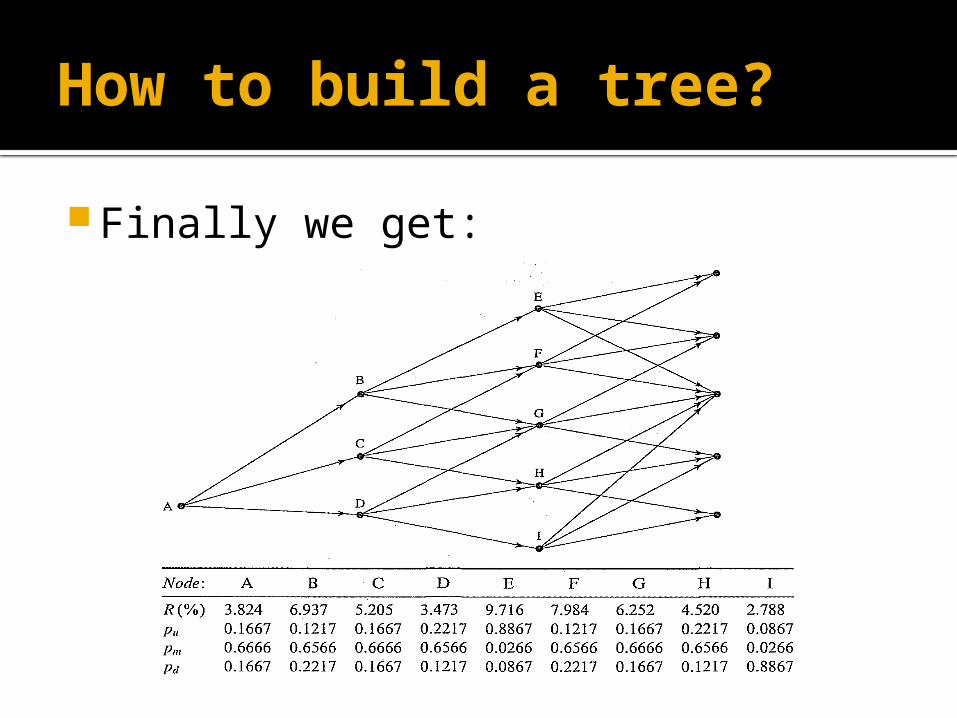

How to build a tree?

Finally we get:

Model presentation (excel)

Option valuation issues

Underlying interest rate

Payoff date

American options

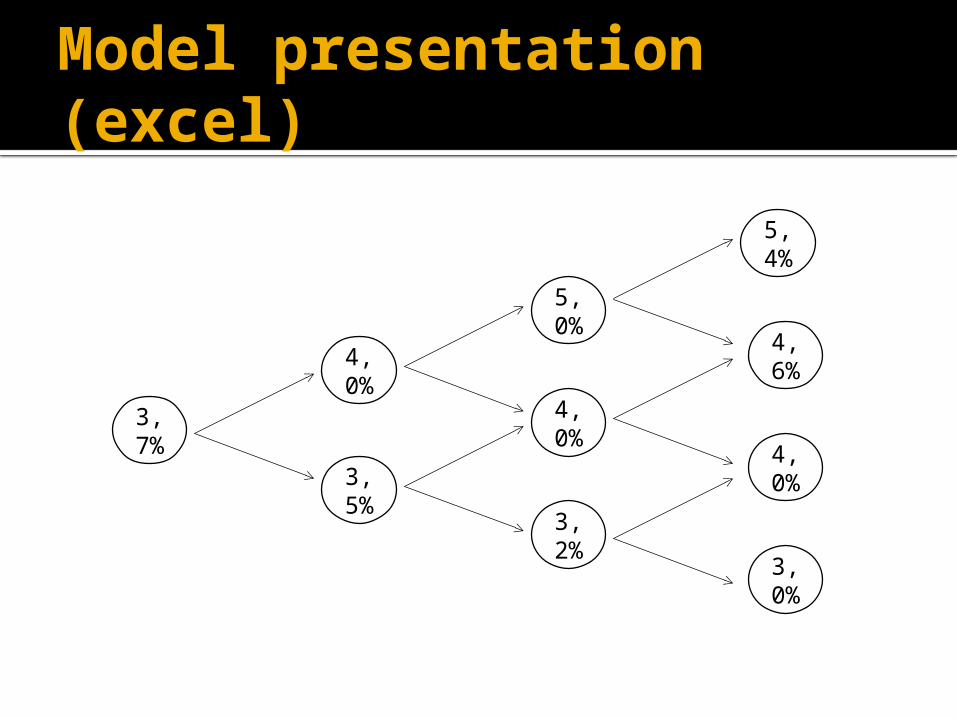

Model presentation (excel)

4,0%

3,5%

3,2%

4,0%

5,0%

5,4%

4,0%

4,6%

3,0%

3,7%

Thank You!!!

Recommended