- Anup P. Shah20th February, 2015

2nd Youth RRC @ Goa

Tax Free Govt. Bonds

© PRAVIN P. SHAH & CO. 2

Increasing

Returns

Reducing

Returns

Increasing

Risk

Reducing

Risk

REITS: MID-RISK & MID-RETURN

AIF: HIGH-RISK & HIGH-RETURNS

© PRAVIN P. SHAH & CO. 3

© PRAVIN P. SHAH & CO. 4

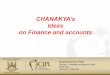

◦ Established in 1960

◦ 300+ REITs in USA

◦ Market Cap of 216 Listed REITs = $816 bn.

◦ Own $1.7 tn of Commercial RE

Over 40,000 Commercial Properties owned by REITs

◦ Paid $34 bn in Dividends in 2013

◦ Avg. Debt Ratio : 46%

◦ Raised $35 bn from Public in 2014

© PRAVIN P. SHAH & CO. 5

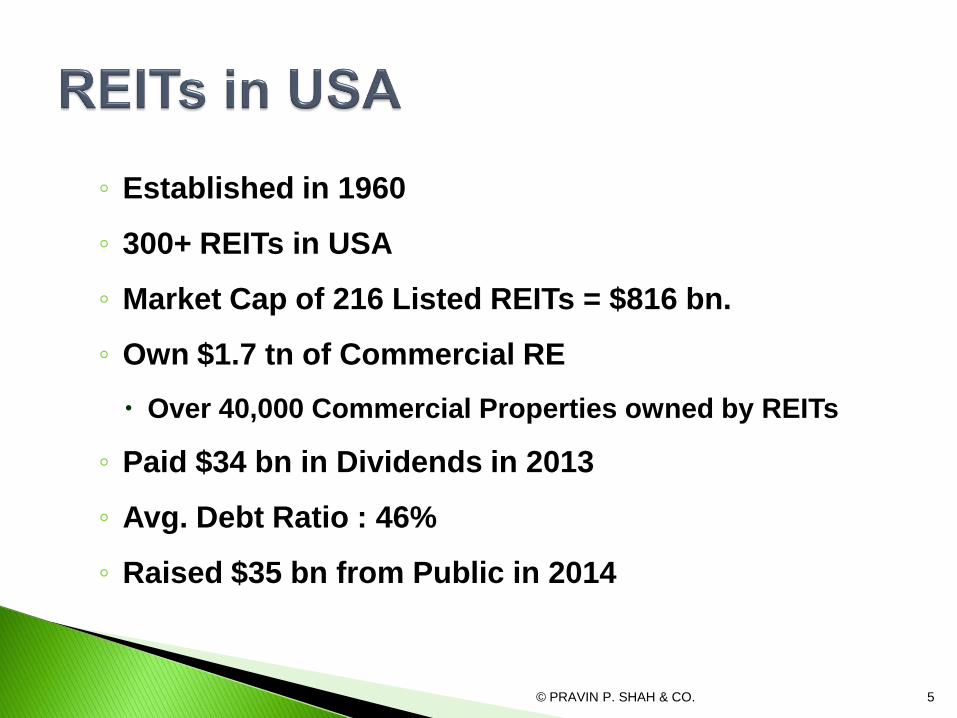

◦ Popular way of monetising commercial real estate

◦ Excellent value unlocking tool for Developers, esp. In Retail

& Commercial space.

◦ India has over 350 million sq.ft. of Grade A leased offices

which can be monetised through REITs

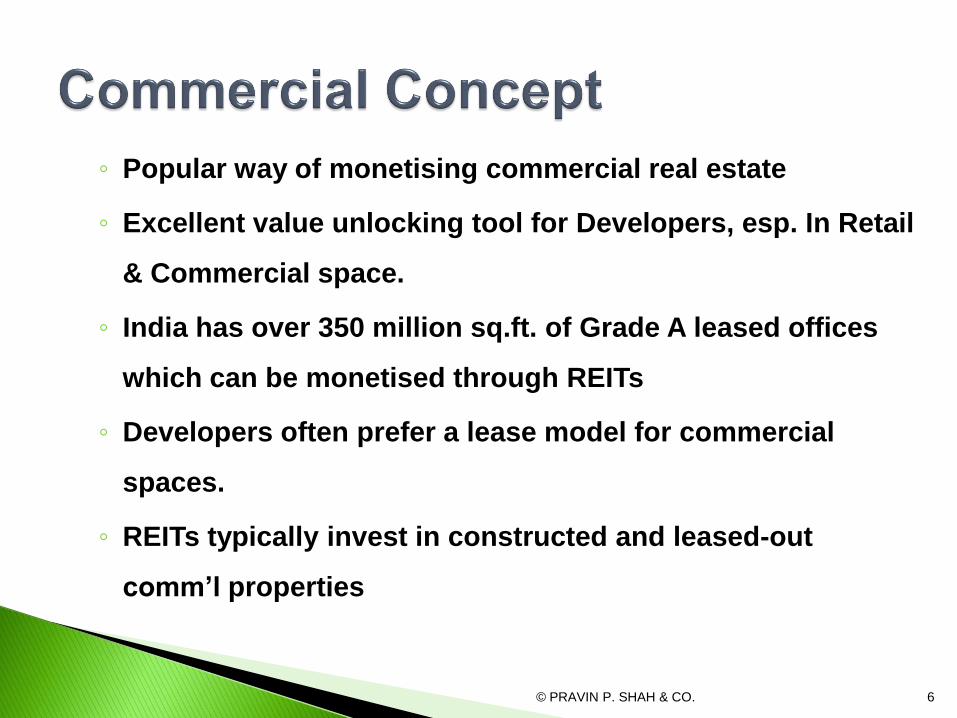

◦ Developers often prefer a lease model for commercial

spaces.

◦ REITs typically invest in constructed and leased-out

comm’l properties

© PRAVIN P. SHAH & CO. 6

◦ Developers often prefer a lease model for commercial

spaces

◦ REIT makes IPO to various investors and raises funds

◦ REIT acquires the leased assets from developers or shares

in the company (SPV) owning such assets

◦ Risk element associated with real estate of investing in

under construction properties is substantially done away

with

© PRAVIN P. SHAH & CO. 7

© PRAVIN P. SHAH & CO. 8

© PRAVIN P. SHAH & CO. 9

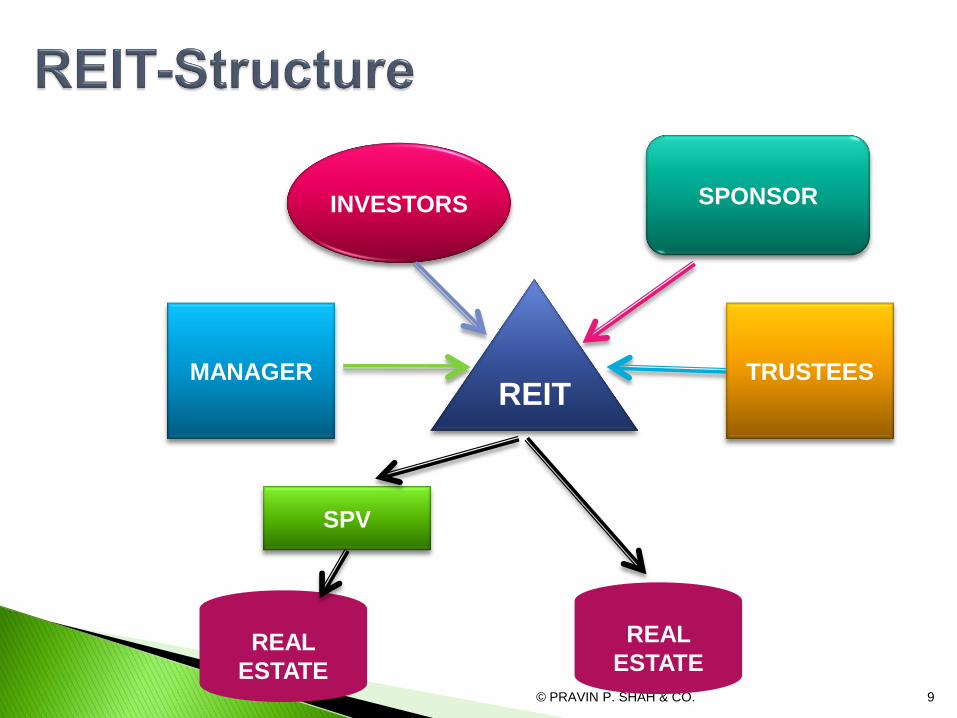

REIT

INVESTORS SPONSOR

TRUSTEES

REAL

ESTATE

SPV

REAL

ESTATE

MANAGER

Concept similar to a MF

◦ REIT – A Trust

◦ Sponsor – Developer who sets up the Trust

Introduces his Yield Portfolio in the REIT

◦ Trustees – of the REIT

◦ Manager – Professional Manager (AMC)

◦ Unitholders – Investors of the REIT

◦ Valuer – Values the REIT’s portfolio

© PRAVIN P. SHAH & CO. 10

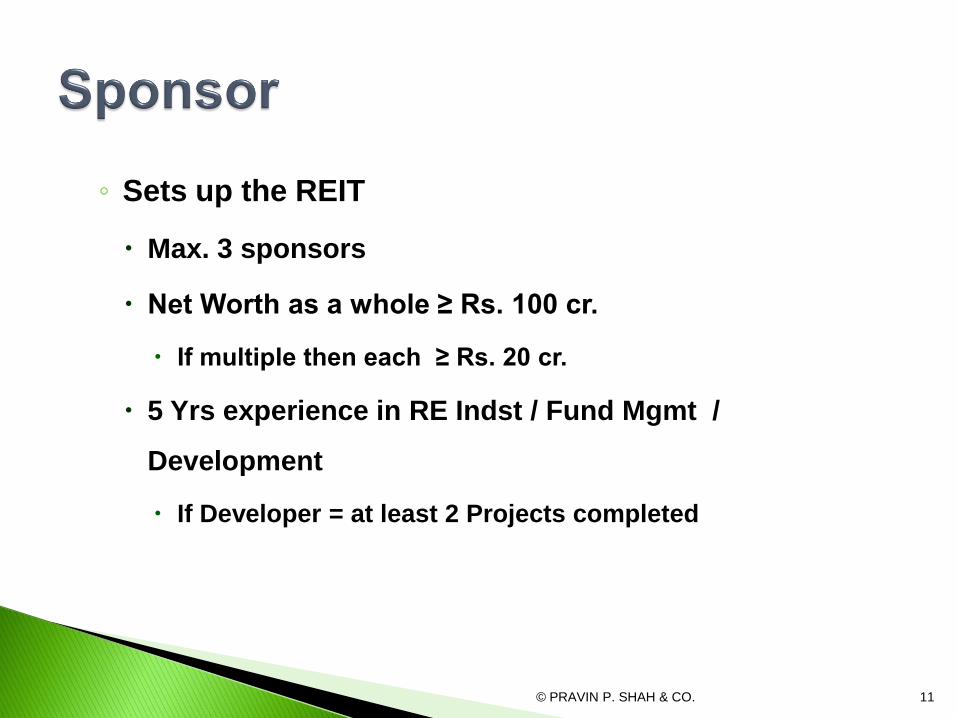

◦ Sets up the REIT

Max. 3 sponsors

Net Worth as a whole ≥ Rs. 100 cr.

If multiple then each ≥ Rs. 20 cr.

5 Yrs experience in RE Indst / Fund Mgmt /

Development

If Developer = at least 2 Projects completed

© PRAVIN P. SHAH & CO. 11

◦ Manages the REIT = similar to AMC in MF

Net Worth ≥ Rs. 10 cr. If Co. Or Net Assets ≥ Rs. 10 cr. if

LLP

5 Yrs experience in Advisory / Fund Mgmt / Property

Mgmt in in RE Ind or Development

At least 2 key personnel with 5 Yrs exp.

50% of Board is Independent & Not on Other REITs

© PRAVIN P. SHAH & CO. 12

◦ Must within 3 yrs of Regn. else cancellation

Min. Value ≥ Rs. 500 cr.

IPO Size ≥ 25% to Public

Offer Size ≥ Rs. 250 cr.

Subsequent: FPOs, Pref. QIP, Bonus, Rights, OFS, etc.

◦ Sponsor:

Must hold 25% of Total units post IPO

Must hold 15% of Units in aggregate at all times

Individually 5% at all times

3 Yrs lock-in from listing + Re-designate New Sponsor

© PRAVIN P. SHAH & CO. 13

REIT can allot units to both residents and non-residents.

Investment by non-residents shall be subject to FEMA

Regulations

REITs should have a minimum of 200 public unit holders

at any point in time

Minimum subscription – Rs 200,000 with minimum

tradable lots of Rs 100,000

© PRAVIN P. SHAH & CO. 14

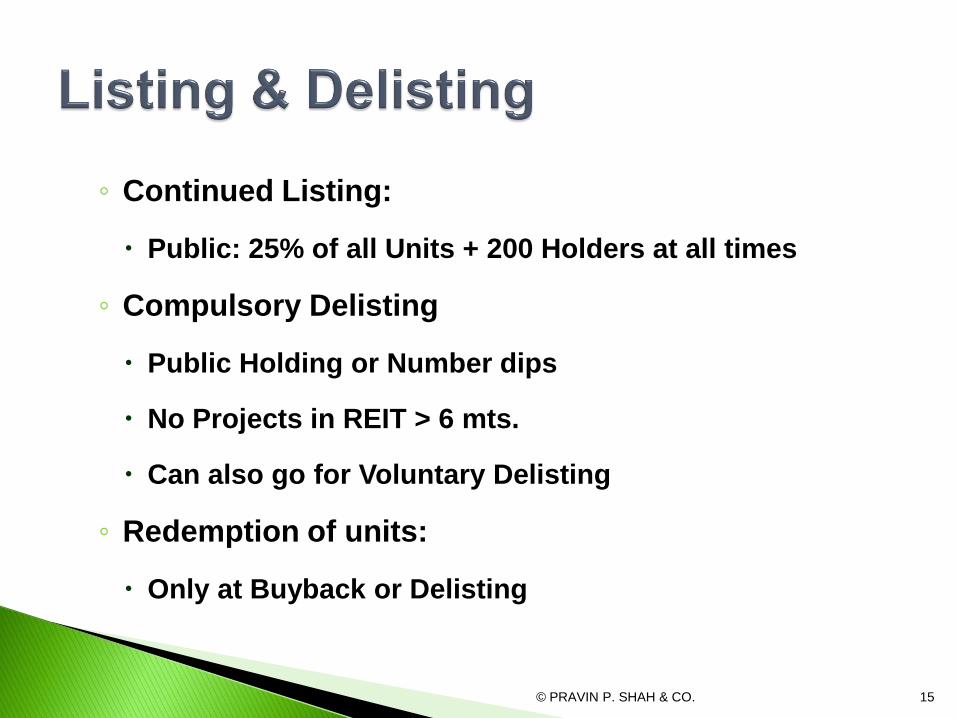

◦ Continued Listing:

Public: 25% of all Units + 200 Holders at all times

◦ Compulsory Delisting

Public Holding or Number dips

No Projects in REIT > 6 mts.

Can also go for Voluntary Delisting

◦ Redemption of units:

Only at Buyback or Delisting

© PRAVIN P. SHAH & CO. 15

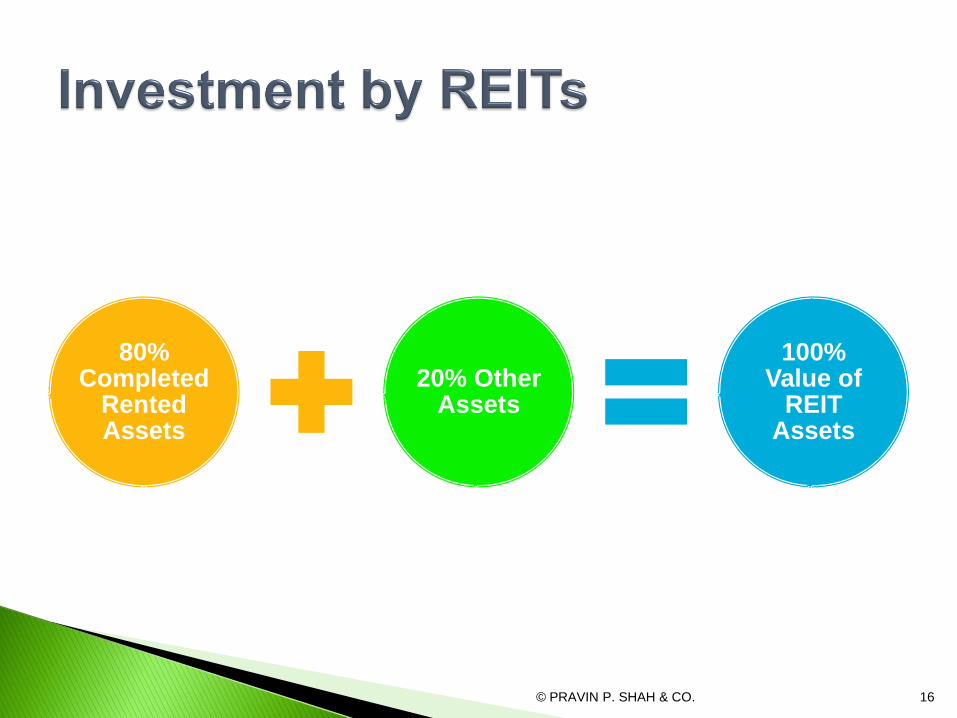

80% Completed

Rented Assets

20% Other Assets

100% Value of

REIT Assets

© PRAVIN P. SHAH & CO. 16

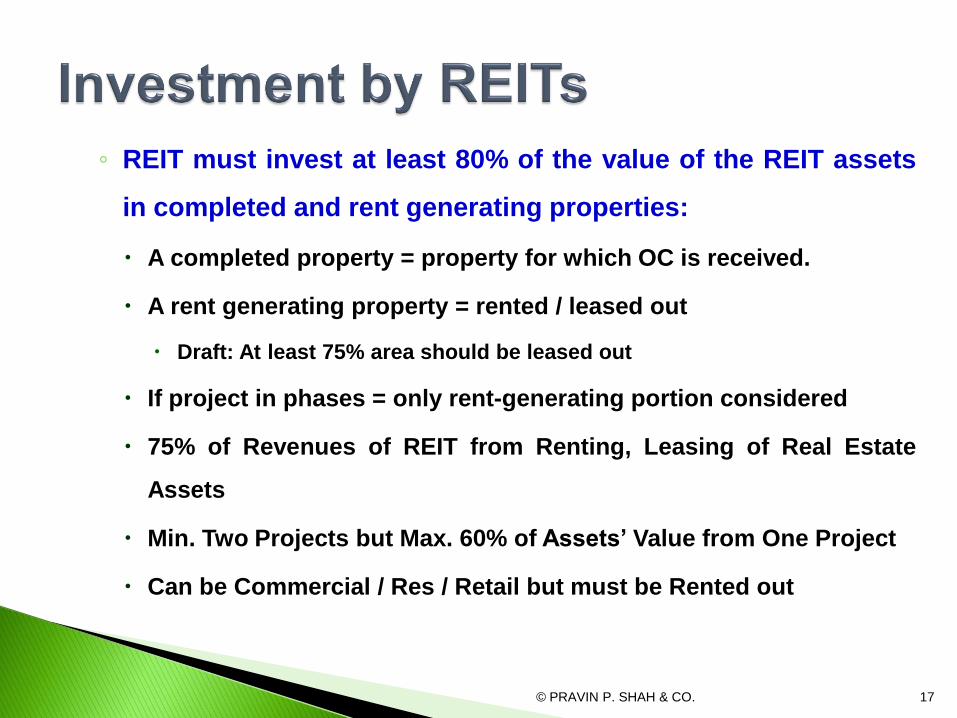

◦ REIT must invest at least 80% of the value of the REIT assets

in completed and rent generating properties:

A completed property = property for which OC is received.

A rent generating property = rented / leased out

Draft: At least 75% area should be leased out

If project in phases = only rent-generating portion considered

75% of Revenues of REIT from Renting, Leasing of Real Estate

Assets

Min. Two Projects but Max. 60% of Assets’ Value from One Project

Can be Commercial / Res / Retail but must be Rented out

© PRAVIN P. SHAH & CO. 17

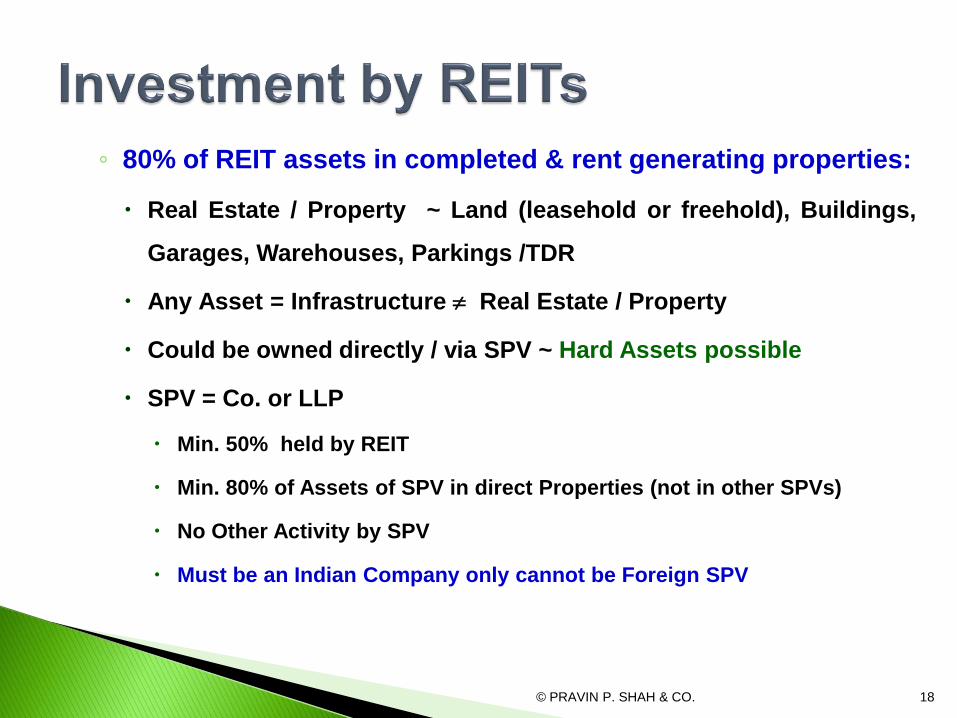

◦ 80% of REIT assets in completed & rent generating properties:

Real Estate / Property ~ Land (leasehold or freehold), Buildings,

Garages, Warehouses, Parkings /TDR

Any Asset = Infrastructure Real Estate / Property

Could be owned directly / via SPV ~ Hard Assets possible

SPV = Co. or LLP

Min. 50% held by REIT

Min. 80% of Assets of SPV in direct Properties (not in other SPVs)

No Other Activity by SPV

Must be an Indian Company only cannot be Foreign SPV

© PRAVIN P. SHAH & CO. 18

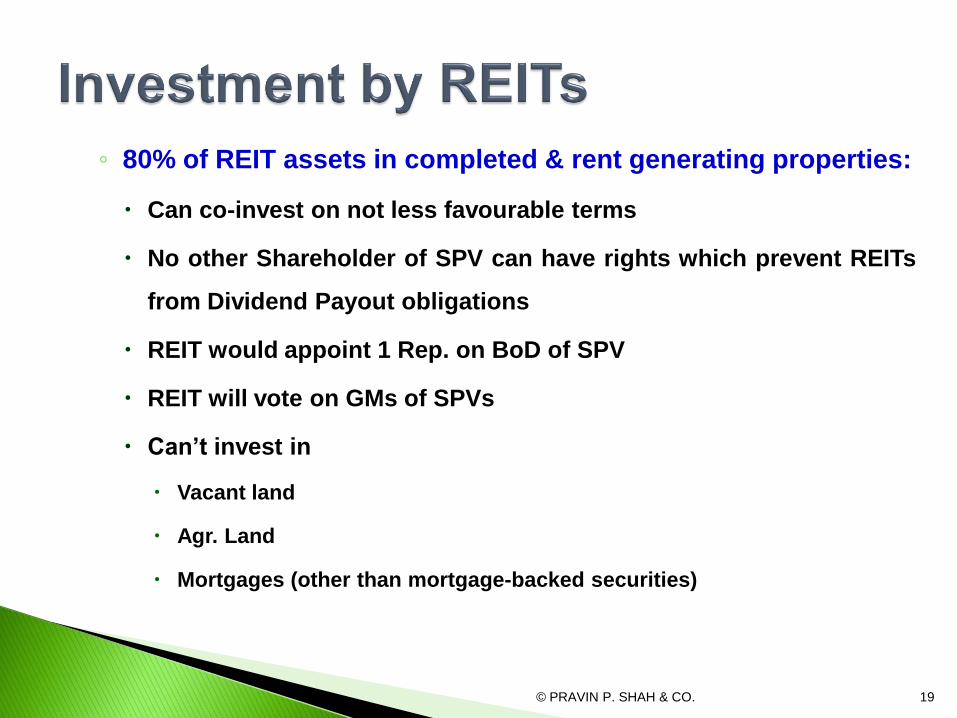

◦ 80% of REIT assets in completed & rent generating properties:

Can co-invest on not less favourable terms

No other Shareholder of SPV can have rights which prevent REITs

from Dividend Payout obligations

REIT would appoint 1 Rep. on BoD of SPV

REIT will vote on GMs of SPVs

Can’t invest in

Vacant land

Agr. Land

Mortgages (other than mortgage-backed securities)

© PRAVIN P. SHAH & CO. 19

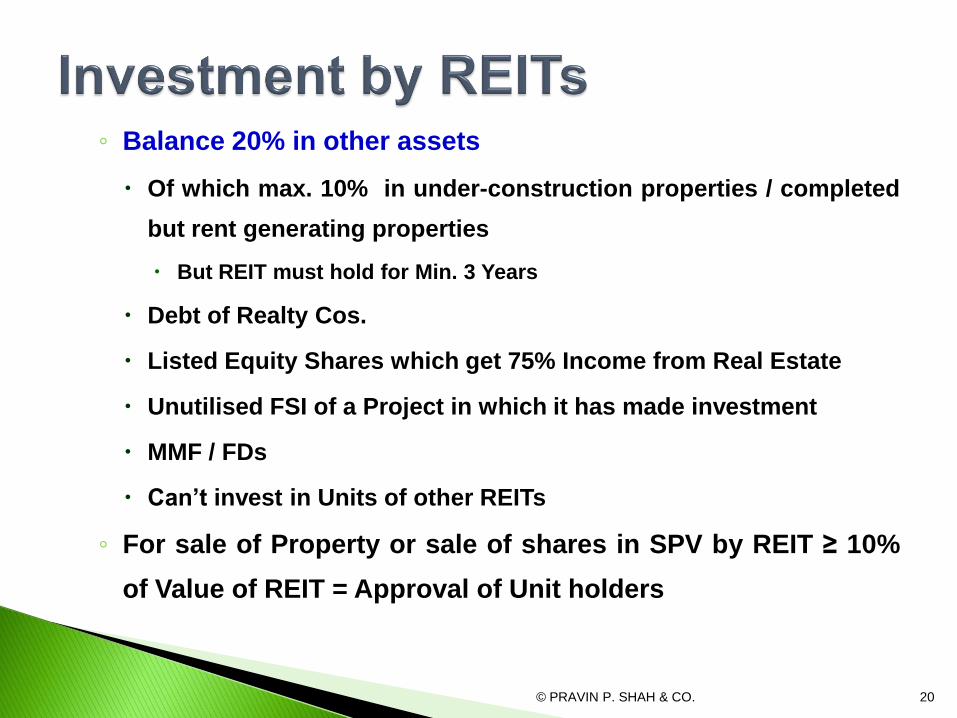

◦ Balance 20% in other assets

Of which max. 10% in under-construction properties / completed

but rent generating properties

But REIT must hold for Min. 3 Years

Debt of Realty Cos.

Listed Equity Shares which get 75% Income from Real Estate

Unutilised FSI of a Project in which it has made investment

MMF / FDs

Can’t invest in Units of other REITs

◦ For sale of Property or sale of shares in SPV by REIT ≥ 10%

of Value of REIT = Approval of Unit holders

© PRAVIN P. SHAH & CO. 20

◦ Aggregate Borrowings & Deferred Payments ≤ 49%

of Value of REIT Assets

Not Including Refundable Deposits of Tenants

If Borrowings > 25% of REIT Assets, then for fresh

leveraging:

Credit Rating

Approval of Unit Holders

© PRAVIN P. SHAH & CO. 21

PAYOUT

90% of Distributable Cash Flows to REIT by

SPV

Once in 6 mts. + Payout within 15

Days of decl.

90% of Distributable Cash Flows by REIT to

Unitholders

Once in 6 mts. + Payout within 15

Days of decl.

Property Sale by REIT / SPV

If Reinvested = No Payout

If Not Reinvested = Payout Rules

apply

© PRAVIN P. SHAH & CO. 22

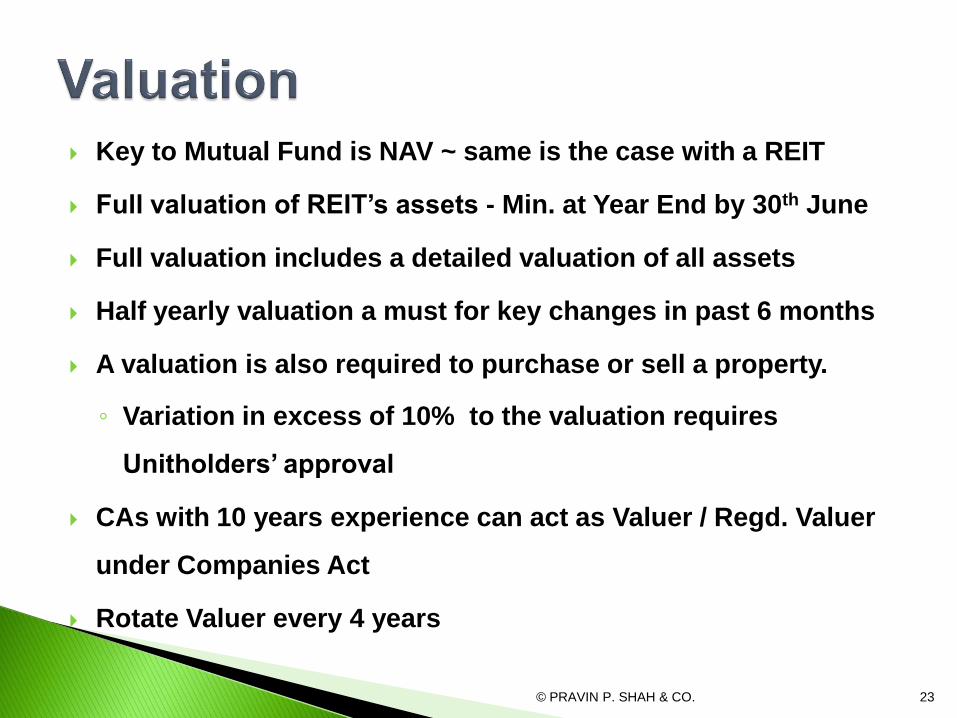

Key to Mutual Fund is NAV ~ same is the case with a REIT

Full valuation of REIT’s assets - Min. at Year End by 30th June

Full valuation includes a detailed valuation of all assets

Half yearly valuation a must for key changes in past 6 months

A valuation is also required to purchase or sell a property.

◦ Variation in excess of 10% to the valuation requires

Unitholders’ approval

CAs with 10 years experience can act as Valuer / Regd. Valuer

under Companies Act

Rotate Valuer every 4 years

© PRAVIN P. SHAH & CO. 23

RPT Compliance

Purchase / sale of

Properties at any time

Price = Avg of 2 Ind. Valn. Reports

RPT before IPO Disclosures in Prospectus + Proper Agr.

RPT after IPO Disclosures to St.Ex. + UH’s prior Approval if RPT ≥

10% Value of REITs

Lease to RPs by REIT Valuer’s Fairness Opinion if:

• Lease Area > 20% of total area

• Value of leased area > 20% of REIT Value

• Rentals > 20% of Total Rental

2 or more REITs with

Common Manager

Deemed RPT

RP has competing business

with REIT activities

Details in Prospectus

© PRAVIN P. SHAH & CO. 24

◦ Appointed for max. 5 yrs + reappoint. for another 5 years

◦ Audit Min. Twice a Yr – Sept & March

A/R within 45 days of these periods to St Ex.

◦ A/C & Auditing Standards may be specified by SEBI

◦ A/C, B/s, P&L, CF give T & F View of State of Affairs

◦ Right of access to all Books & Vouchers pertaining to REIT

Right to Info. & Expl. Pertaining to REIT as he deems fit from:

Employees of REIT

Parties to REIT / SPV

Any other person in possession of such information

© PRAVIN P. SHAH & CO. 25

© PRAVIN P. SHAH & CO. 26

Entity Income Stream

SPV • Lease Rentals from renting out property

• Capital Gains on selling the Yield Properties

REIT Dividends distributed / Interest paid by SPV

Unitholders • Distributions made by the REIT

• Sale of Units on Stock Exchange / Off-market

Sponsor Same as Unitholders

Manager AMC Fees + Carry (2-20 Model?)

Trustees Trusteeship Fees

© PRAVIN P. SHAH & CO. 27

Exchange of SPV shares for REIT Units

◦ Transfer Exempt u/s.47(xvii) No CGT

© PRAVIN P. SHAH & CO. 28

Sponsor

SPV

REIT

Sale of REIT Units: On Market OR Off-Market

◦ Taxable as Capital Gains – Exemption u/s.10(38) Not Available

Thus, gains on exchange postponed but not fully exempt

◦ Cost of REIT Units = Cost of shares of SPV

◦ Period of holding shares of SPV added to that of Units

◦ LTCG if > 36 months, else STCG

◦ STCG u/s.111A – Taxed @ Normal Slab Rates

◦ LTCG

Taxed @ 20% with Indexation or

10% without Indexation

◦ LTCL of Developer can be set-off against LTCG on Units

© PRAVIN P. SHAH & CO. 29

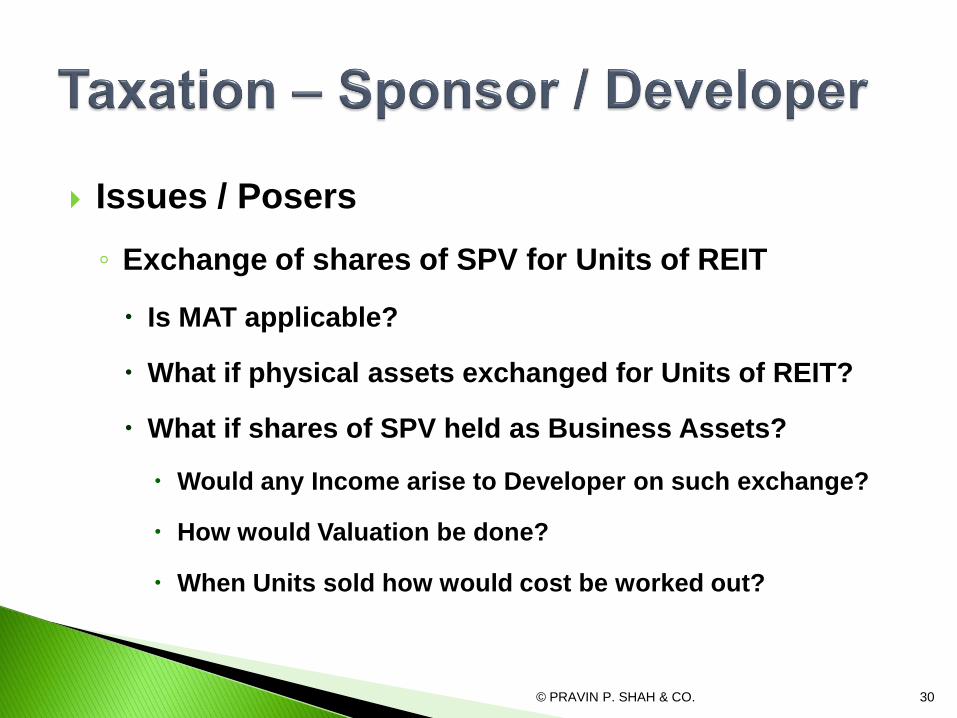

Issues / Posers

◦ Exchange of shares of SPV for Units of REIT

Is MAT applicable?

What if physical assets exchanged for Units of REIT?

What if shares of SPV held as Business Assets?

Would any Income arise to Developer on such exchange?

How would Valuation be done?

When Units sold how would cost be worked out?

© PRAVIN P. SHAH & CO. 30

Tax

◦ Normal Tax @ 30% + SC + Cess

◦ No Exemption from MAT @ 20% - Big Negative

Interest to REIT

◦ REIT is a Pass-through Vehicle

◦ No TDS @ 10% on Payment to REIT

Dividend distributed to REIT

◦ DDT u/s.115-O payable @ 20%

◦ Biggest Disadvantage of current regime

Reduces Yield to Investor drastically

© PRAVIN P. SHAH & CO. 31

Income stream of SPV

◦ What would be the Income stream for SPV?

◦ How would Tax be computed?

© PRAVIN P. SHAH & CO. 32

Interest from SPV

◦ Exempt u/s.10(23FC)

◦ No Tax in hands of REIT, i.e., REIT is a Pass-through Vehicle

◦ No TDS by SPV also

Dividend from SPV

◦ Exempt in hands of REIT

◦ SPV pays DDT @ 20%

Sale of Assets by REIT

◦ Capital Gain Taxable at applicable rates

© PRAVIN P. SHAH & CO. 33

Any Other Income

Taxable at MMR @ 30% u/s.115UA

HPI if Assets held directly by REITs

Management Fees charged from SPVs, if any?

REITs must file Return of Income

© PRAVIN P. SHAH & CO. 34

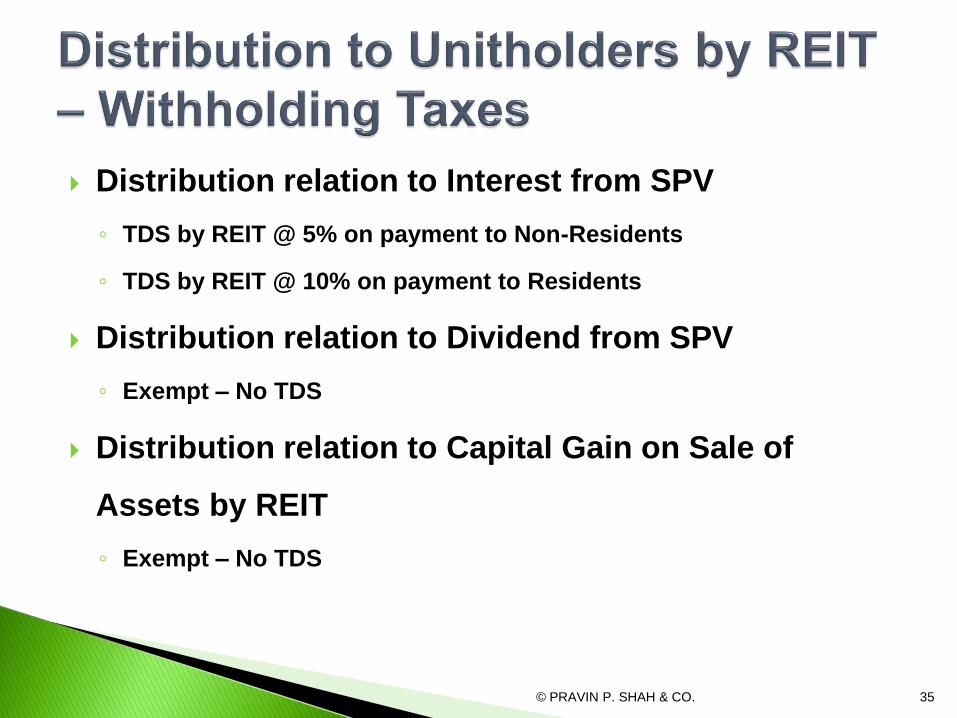

Distribution relation to Interest from SPV

◦ TDS by REIT @ 5% on payment to Non-Residents

◦ TDS by REIT @ 10% on payment to Residents

Distribution relation to Dividend from SPV

◦ Exempt – No TDS

Distribution relation to Capital Gain on Sale of

Assets by REIT

◦ Exempt – No TDS

© PRAVIN P. SHAH & CO. 35

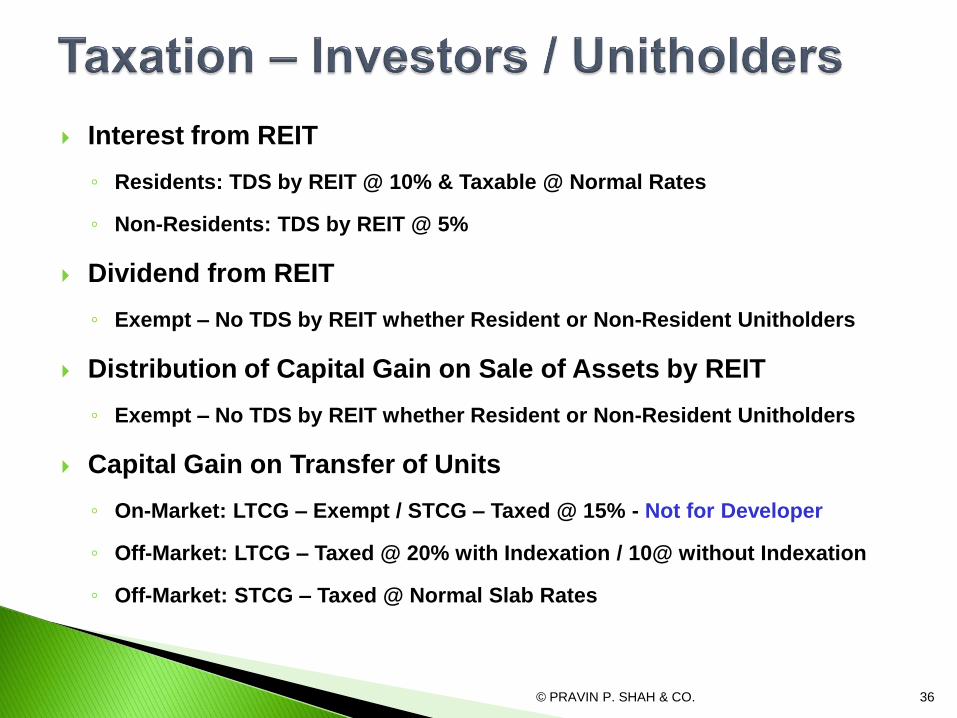

Interest from REIT

◦ Residents: TDS by REIT @ 10% & Taxable @ Normal Rates

◦ Non-Residents: TDS by REIT @ 5%

Dividend from REIT

◦ Exempt – No TDS by REIT whether Resident or Non-Resident Unitholders

Distribution of Capital Gain on Sale of Assets by REIT

◦ Exempt – No TDS by REIT whether Resident or Non-Resident Unitholders

Capital Gain on Transfer of Units

◦ On-Market: LTCG – Exempt / STCG – Taxed @ 15% - Not for Developer

◦ Off-Market: LTCG – Taxed @ 20% with Indexation / 10@ without Indexation

◦ Off-Market: STCG – Taxed @ Normal Slab Rates

© PRAVIN P. SHAH & CO. 36

© PRAVIN P. SHAH & CO. 37

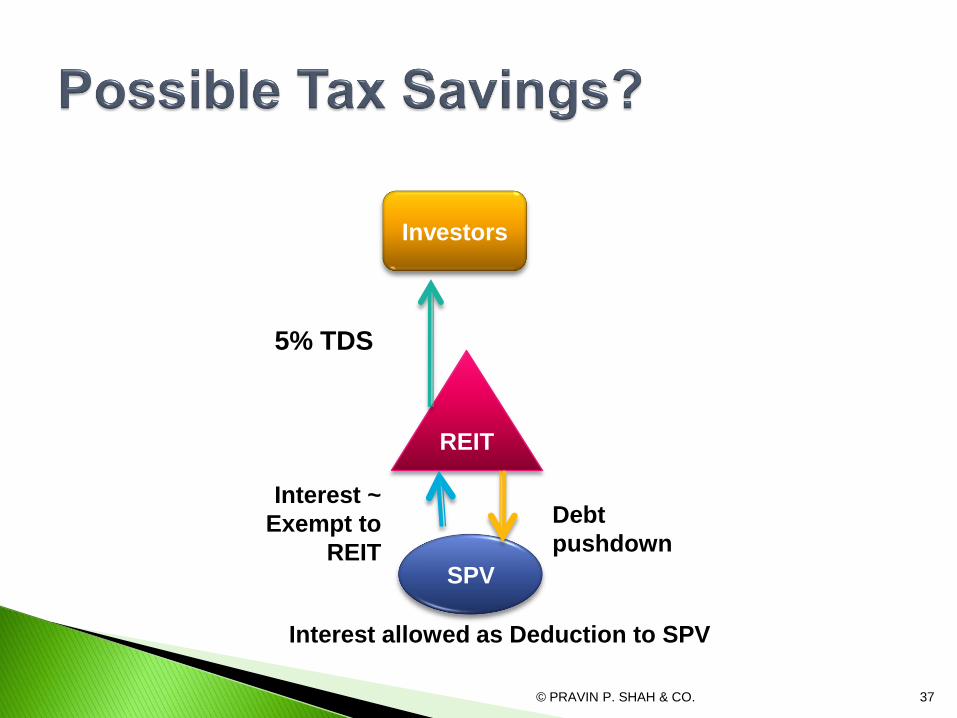

Investors

REIT

SPV

Debt

pushdown

Interest ~

Exempt to

REIT

Interest allowed as Deduction to SPV

5% TDS

◦ How would REIT acquire Debt Securities of SPV?

Exchange with Sponsor?

Invest in fresh Debt issued by SPV out of IPO proceeds

What would SPV do with this fresh debt?

© PRAVIN P. SHAH & CO. 38

◦ Poser – Can SPV be an LLP?

Positives?

Negatives?

© PRAVIN P. SHAH & CO. 39

© PRAVIN P. SHAH & CO. 40

◦ Drive with Caution!

Stamp Duty on SPVisation?

Property held in Flagship Co. or directly to SPV

SD Exemption for Transfer to 90%+ Sub?

Available in Maharashtra?

© PRAVIN P. SHAH & CO. 41

Income-tax Hurdles

Sponsor

Period of holding for Listed Units is 3 years to qualify as LT?

Investors

Availability of Foreign Tax Credit for non-resident Unit

holders of taxes paid by SPV

© PRAVIN P. SHAH & CO. 42

FEMA

Auto Route for Foreign Investment in REITs?

Auto Route for Swap by Foreign Sponsors of SPVs

FIPB Approval required?

RFPIs can Invest?

Renting of Properties ~ Is it RE Business?

ECBs by SPVs and REITs allowed?

Other

State Rent Control Laws should not be a Hindrance

Property Taxes should not be a dampener!

© PRAVIN P. SHAH & CO. 43

© PRAVIN P. SHAH & CO. 44

© PRAVIN P. SHAH & CO. 45

◦ Trust / Company / LLP

Privately Pooled Investment Vehicle

Most Important Portion of Definition

Collects Funds from Investors

Foreign or Domestic

Defined Investment Policy

Not a CIS / Not a MF

© PRAVIN P. SHAH & CO. 46

Not AIF

Gratuity Trust

Regulate Pool of Funds

RegulatSPVs

Holding Co

Family Trusts

ESOP Trust

Securitisation

Funds

© PRAVIN P. SHAH & CO. 47

© PRAVIN P. SHAH & CO. 48

AIF

INVESTORS SPONSOR

TRUSTEES /

DIRECTORS

/ DPARTNER

COMPANY

MANAGER

Concept similar to a VCF

◦ AIF – A Trust / Company / LLP

◦ Sponsor – Person who sets up the AIF (Manager can

be Sponsor also)

◦ Trustees – of the AIF if in the form of Trust

◦ Manager – Professional Manager (AMC)

◦ Investors – Investors of the AIF

© PRAVIN P. SHAH & CO. 49

◦ Sponsor Sets up the AIF / Manager Manages it

Manager or Sponsor must have:

Continuing Interest in AIF

Minimum 2.5% of Corpus or Rs. 5 cr. ~ Lower

If Cat III AIF – Min. 2.5% or Rs. 10 cr. ~ Lower

By way of Investment in AIF – monetary terms

Not in Kind – fee waiver

Must disclose their Investment in AIF to Investors

© PRAVIN P. SHAH & CO. 50

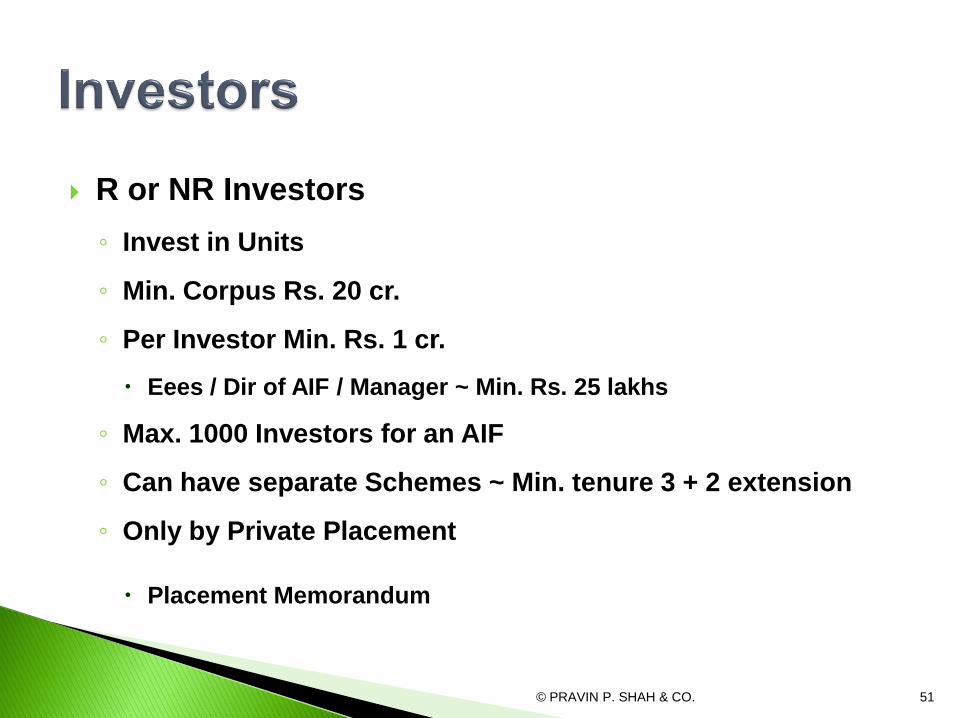

R or NR Investors

◦ Invest in Units

◦ Min. Corpus Rs. 20 cr.

◦ Per Investor Min. Rs. 1 cr.

Eees / Dir of AIF / Manager ~ Min. Rs. 25 lakhs

◦ Max. 1000 Investors for an AIF

◦ Can have separate Schemes ~ Min. tenure 3 + 2 extension

◦ Only by Private Placement

Placement Memorandum

© PRAVIN P. SHAH & CO. 51

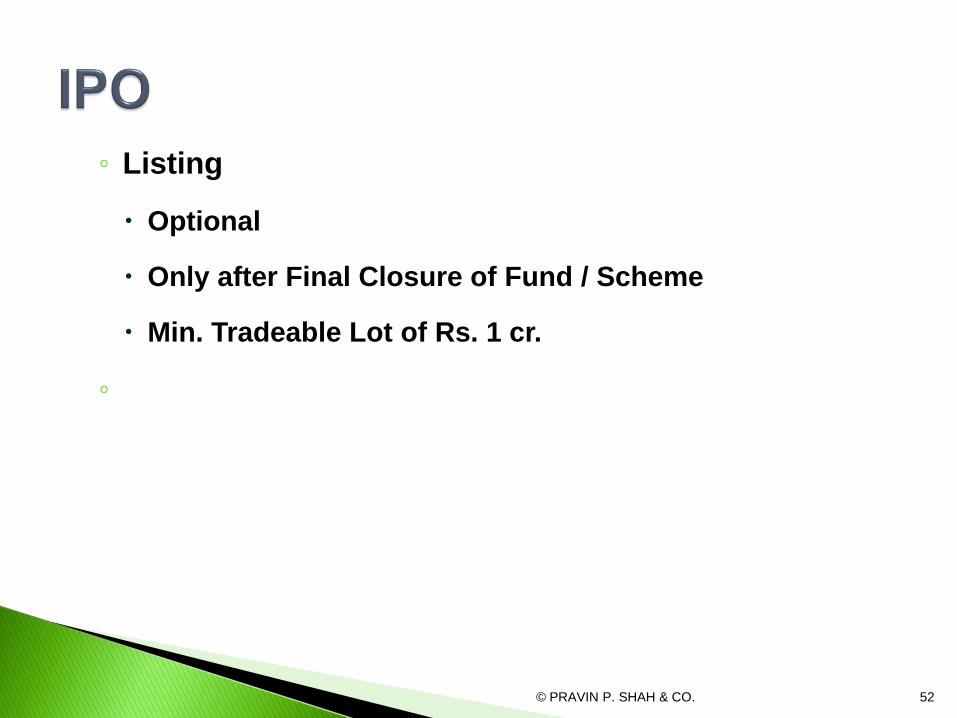

◦ Listing

Optional

Only after Final Closure of Fund / Scheme

Min. Tradeable Lot of Rs. 1 cr.

◦

© PRAVIN P. SHAH & CO. 52

Particulars AIF-I AIF-II AIF-III

Types VCF / SME /

Social Venture /

Infra Funds

Private Equity / Debt

Funds

Hedge Funds

Borrowing

Allowed

No Temporary funding ≤

30 days; 10% of

Corpus + 4 times /

Year

Yes subject to a

maximum limit to be

specified by SEBI

Investment VCU /Cos /

SPVs / LLP

Unlisted Cos. / Units of

AIF-I / II

Listed / Unlisted

Securities /

Derivatives /

Structured Products /

Units of AIF-I /II

Max

Investment in

1 Co.

25% of Corpus 25% of Corpus 10% of Corpus

© PRAVIN P. SHAH & CO. 53

AIF Category Commitments -

Sep 2014

Commitments – Dec

2014

Category I

Infrastructure 5,706.82

Social Venture 484.49

Venture Capital 645.83

SME -

Total for Category I 6,837.14 7,819

Category II 8,492.58 10,302

Category III 2,122.52 2,336

Grand Total 17,452.24 20,457

© PRAVIN P. SHAH & CO. 54

Norms VCF AIF-I SME AIF-I Infra AIF-I Social AIF-I

Primary

Invests

Startups / Early

stage / Angel

Funds but not

in NBFC / Gold

Financing

SME Startups /

listed on SME

Exchange

Sec / Listed Debt of

SPV in Infra

Projects

Securities of

Social Ventures

+ social

performance

norms

Funds Min. 66% in

Unlisted Equity

of VCU / Cos.

on SME

Exchange

Min. 75% in

Unlisted Sec /

LLP of VCU /

SME Exchange

Cos.

Min. 75% in

Unlisted Sec / LLP

of Cos. in Infra.

Projects

Min. 75% in

Unlisted Sec /

LLP of Social

ventures

Max. 33% in

IPO / Debt of

VCU / QIP by

Listed Co / Sick

listed Co.

Also Listed

Securitised Debt /

Debt of Infra Cos.

Can give grants

to Social

Ventures

© PRAVIN P. SHAH & CO. 55

© PRAVIN P. SHAH & CO. 56

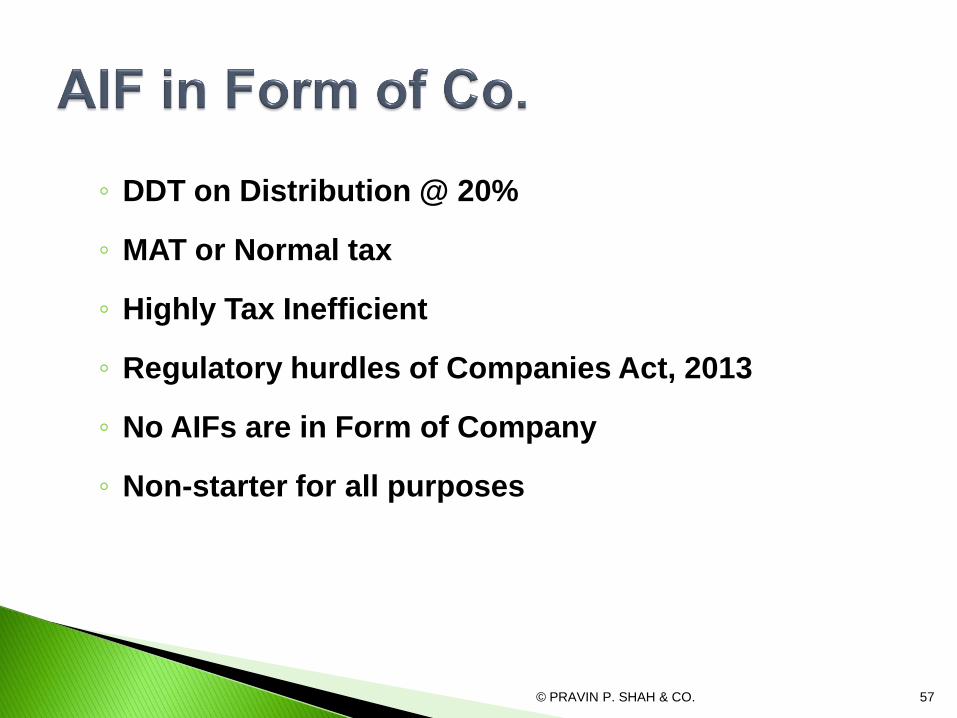

◦ DDT on Distribution @ 20%

◦ MAT or Normal tax

◦ Highly Tax Inefficient

◦ Regulatory hurdles of Companies Act, 2013

◦ No AIFs are in Form of Company

◦ Non-starter for all purposes

© PRAVIN P. SHAH & CO. 57

◦ Single Point taxation

◦ Firm Tax @ 30%

◦ No MAT

◦ Distribution to Partners Tax Free - No DDT

◦ Entry – Exit of Partners: Cumbersome

◦ Pass-through u/s. 10(23FB) for VC also for LLPs?

◦ FDI in AIF LLP: FIPB approval

◦ Several AIFs-II and III are LLPs

© PRAVIN P. SHAH & CO. 58

◦ Most popular Vehicle for Pooling of Funds

FDI in AIF Trust: FIPB Approval

Taxation of Trusts: Some Hurdles – Some Clarity

Ambiguity has retarded AIF Registration to some extent

SEBI has made representations to FM

Budget expected to present some Cheer!!

© PRAVIN P. SHAH & CO. 59

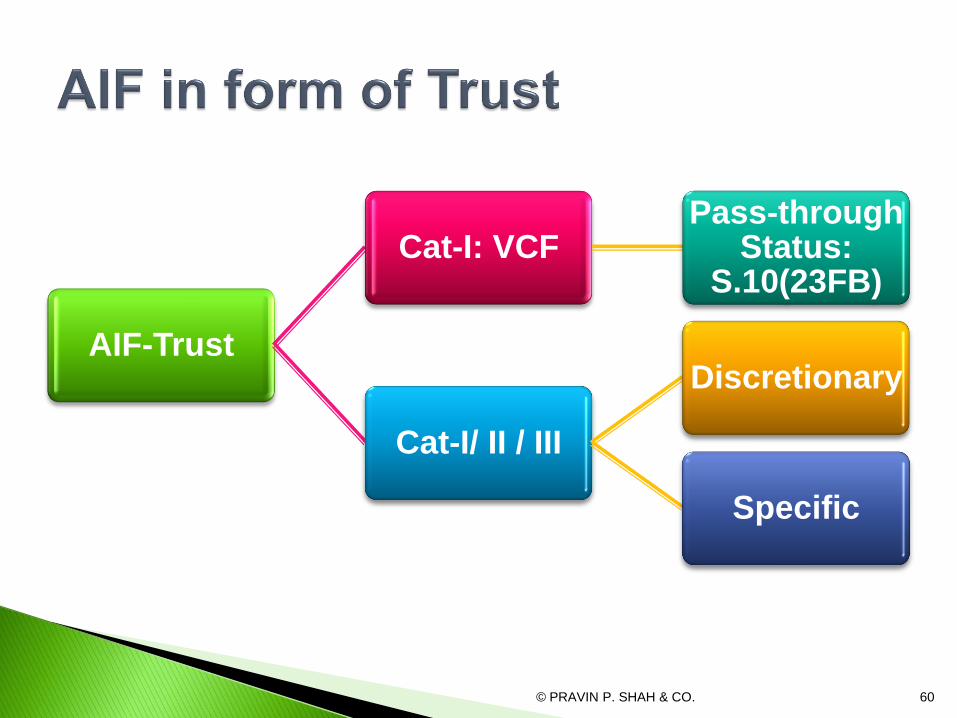

AIF-Trust

Cat-I: VCFPass-through

Status: S.10(23FB)

Cat-I/ II / III

Discretionary

Specific

© PRAVIN P. SHAH & CO. 60

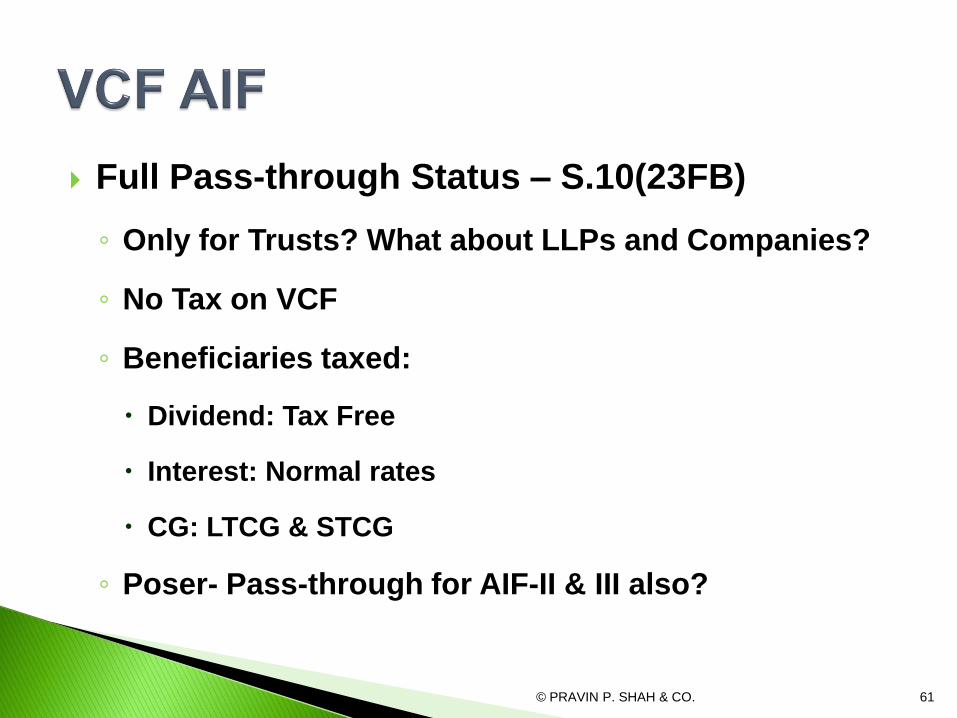

Full Pass-through Status – S.10(23FB)

◦ Only for Trusts? What about LLPs and Companies?

◦ No Tax on VCF

◦ Beneficiaries taxed:

Dividend: Tax Free

Interest: Normal rates

CG: LTCG & STCG

◦ Poser- Pass-through for AIF-II & III also?

© PRAVIN P. SHAH & CO. 61

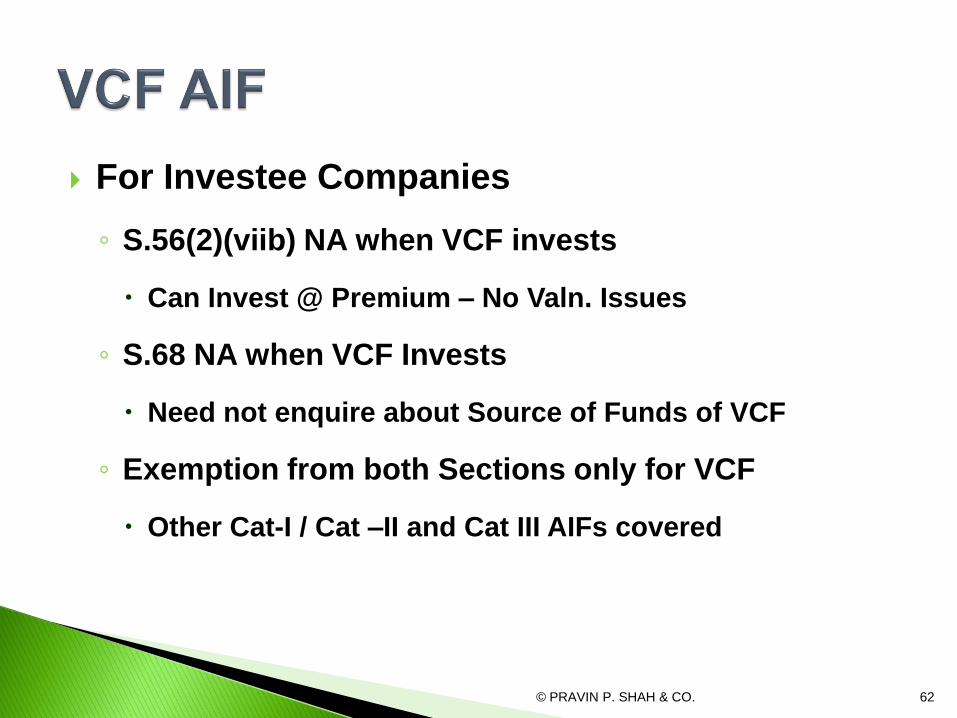

For Investee Companies

◦ S.56(2)(viib) NA when VCF invests

Can Invest @ Premium – No Valn. Issues

◦ S.68 NA when VCF Invests

Need not enquire about Source of Funds of VCF

◦ Exemption from both Sections only for VCF

Other Cat-I / Cat –II and Cat III AIFs covered

© PRAVIN P. SHAH & CO. 62

Nature

Specific

Shares Specified

Discretionary

Shares left to Discretion

© PRAVIN P. SHAH & CO. 63

◦ Posers- What is a Specific Trust?

Individual Shares specified in Deed

What if Power to Trustees to determine Shares?

What if Beneficiaries not in existence but shares

determinate?

What if Class of Beneficiaries specified in Deed and

Methodology for the determination of the shares?

© PRAVIN P. SHAH & CO. 64

Income taxed in hands of the Trustee in a like manner and

to the same extent as that of the beneficiaries

Character of the income - dividend, interest, capital gain,

etc., should be the same as it would be in the hands of the

beneficiary

Once income is taxed in the hands of the Trustee as

Representative Assessee, subsequent distribution of the

same should not attract any further income-tax in the

hands of the beneficiaries

© PRAVIN P. SHAH & CO. 65

◦ 2014 CBDT Circular

If ‘the names of the investors’ or their ‘beneficial interests’

are not specified in the trust deed on the ‘date of its

creation’, the trust will be treated as PDT ~ taxed at MMR

All Income of AIF – LTCG / Exempt LTCG taxed @ 30%

Way Out?

Cir. NA if Jurisdictional HC has taken a different position

What happens if Beneficiary position changes – Exits?

© PRAVIN P. SHAH & CO. 66

◦ Posers- Can an AIF be treated as a Revocable Trust?

Under what circumstances?

If yes, then what is the Tax Treatment?

© PRAVIN P. SHAH & CO. 67

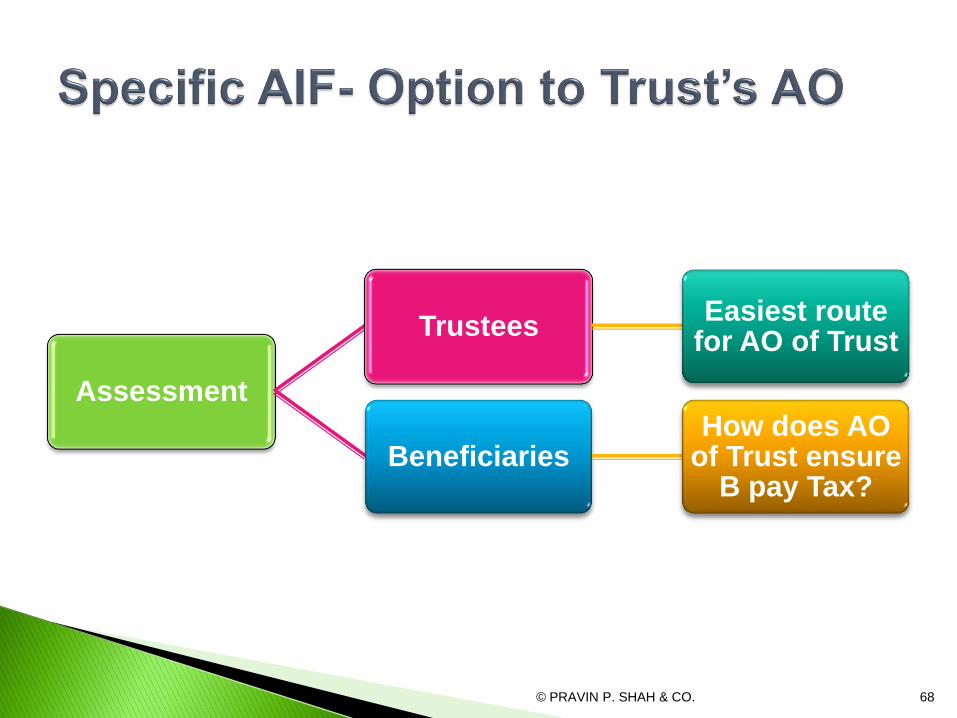

Assessment

TrusteesEasiest route

for AO of Trust

BeneficiariesHow does AO

of Trust ensure B pay Tax?

© PRAVIN P. SHAH & CO. 68

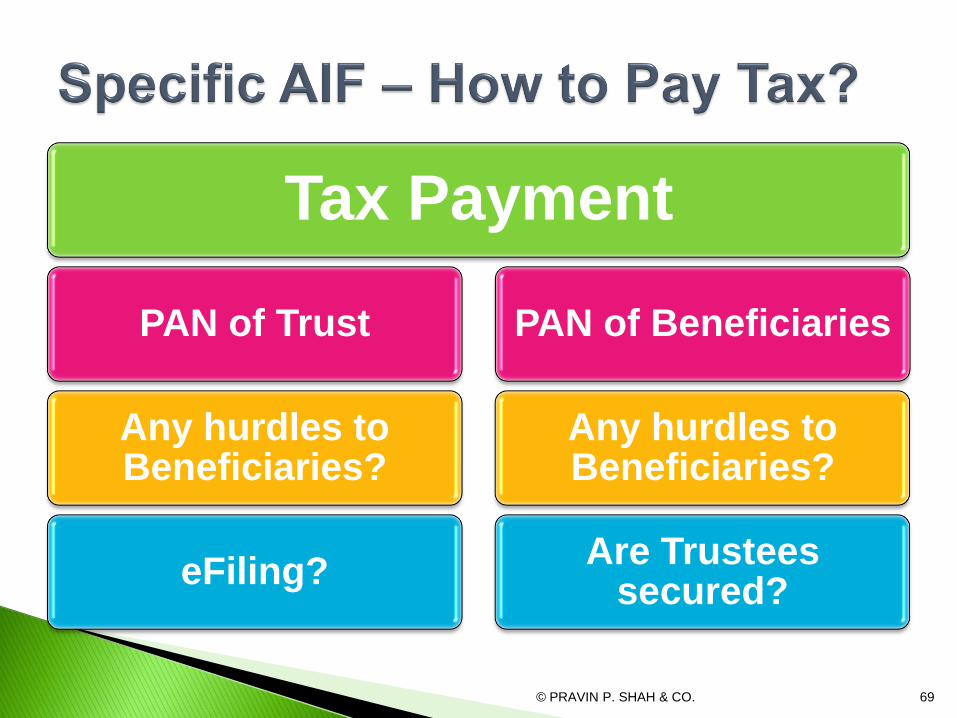

Tax Payment

PAN of Trust

Any hurdles to Beneficiaries?

eFiling?

PAN of Beneficiaries

Any hurdles to Beneficiaries?

Are Trustees secured?

© PRAVIN P. SHAH & CO. 69

◦ Entire Income taxed @ MMR – 30%

◦ No shelter for Exempt LTCG / Listed LTCG @ 11%

◦ Everything becomes Business Income

◦ Taxes paid by AIF

◦ CBDT Cir

Credit should be given to Beneficiaries for Tax paid

No such Instruction in case of Specific Trusts

© PRAVIN P. SHAH & CO. 70

◦ Poser-Is the Trust taxable as an AOP?

Have Investors come together for earning Profit

Hence, taxable as an AOP?

© PRAVIN P. SHAH & CO. 71

www.ppsco.in

© PRAVIN P. SHAH & CO. 72

Recommended