TAUMATA PLANTATIONS LIMITED

Group of Companies

Annual Report

For the Year Ended 30 June 2017

TAUMATA PLANTATIONS LIMITED

General Information

Directors

Michael N Allen

Stephen J Baldwin

Anthony J Cascio

John L Herbohn

Angeleen D Jenkins

Brenton J Keefer

Roger L Lloyd (Alternate)

William K J McCallum

A Justin Ourso IV

William E Peressini

Thomas G Sarno

Wilfred Steiner

Courtland L Washburn

Julian J Widdup

Registered Office

C/- Russell McVeagh

Level30

Vero Centre

48 Shortland Street

Auckland

New Zealand

Head Office

Appointed

28 June 2016

31 July 2011

7 March 2017

1 January2016

28 November 2016

1 May2015

14 August 2012

7 March 2017

8July2016

1 April 2011

31 March 2014

1 July2014

1 March 2007

14 August 2012

Cl- Hancock Forest Management (NZ) Limited

Unit 5

1 ?O H;:imilton StrnP.t

PO Box 13404

Tauranga 3141

New Zealand

Solicitors

Russell McVeagh

Level 30

Vero Centre

48 Shortland Street

Auckland

New Zealand

Auditors

Ernst & Young

2 Takutai Square

Britomart

Auckland

New Zealand

Resigned

21 October 2016

7 March 2017

21 October 2016

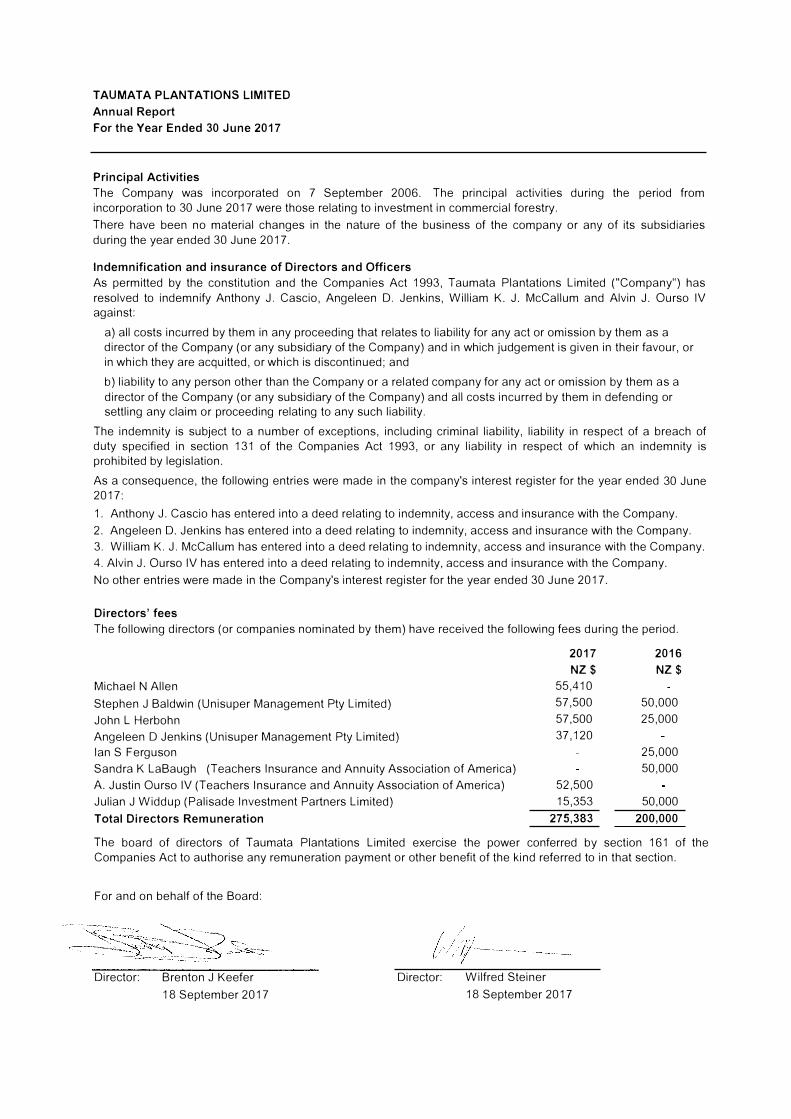

TAUMATA PLANTATIONS LIMITED

Annual Report

For the Year Ended 30 June 2017

Principal Activities

The Company was incorporated on 7 September 2006. The principal activities during the period from

incorporation to 30 June 2017 were those relating to investment in commercial forestry.

There have been no material changes in the nature of the business of the company or any of its subsidiaries

during the year ended 30 June 2017.

Indemnification and insurance of Directors and Officers

As permitted by the constitution and the Companies Act 1993, Taumata Plantations Limited ("Company") has

resolved to indemnify Anthony J. Cascio, Angeleen D. Jenkins, William K. J. McCallum and Alvin J. Ourso IV

against:

a) all costs incurred by them in any proceeding that relates to liability for any act or omission by them as a

director of the Company ( or any subsidiary of the Company) and in which judgement is given in their favour, or

in which they are acquitted, or which is discontinued; and

b) liability to any person other than the Company or a related company for any act or omission by them as a

director of the Company ( or any subsidiary of the Company) and all costs incurred by them in defending or

settling any claim or proceeding relating to any such liability.

The indemnity is subject to a number of exceptions, including criminal liability, liability in respect of a breach of

duty specified in section 131 of the Companies Act 1993, or any liability in respect of which an indemnity is

prohibited by legislation.

As a consequence, the following entries were made in the company's interest register for the year ended 30 June 2017:

1. Anthony J. Cascio has entered into a deed relating to indemnity, access and insurance with the Company.

2. Angeleen D. Jenkins has entered into a deed relating to indemnity, access and insurance with the Company.

3. William K. J. McCallum has entered into a deed relating to indemnity, access and insurance with the Company.

4. Alvin J. Ourso IV has entered into a deed relating to indemnity, access and insurance with the Company.

No other entries were made in the Company's interest register for the year ended 30 June 2017.

Directors' fees

The following directors (or companies nominated by them) have received the following fees during the period.

Michael N Allen

Stephen J Baldwin (Unisuper Management Ply Limited)

John L Herbohn

Angeleen D Jenkins (Unisuper Management Pty Limited)

Ian S Ferguson

Sandra K LaBaugh (Teachers Insurance and Annuity Association of America)

A. Justin Ourso IV (Teachers Insurance and Annuity Association of America)

Julian J Widdup (Palisade Investment Partners Limited)

Total Directors Remuneration

2017

NZ$

55,410

57,500

57,500

37,120

52,500

15,353

275,383

2016

NZ$

50,000

25,000

25,000

50,000

50,000

200,000

The board of directors of Taumata Plantations Limited exercise the power conferred by section 161 of the

Companies Act to authorise any remuneration payment or other benefit of the kind referred to in that section.

For and on behalf of the Board:

Director: Brenton J Keefer

18 September 2017

Director: Wilfred Steiner

18 September 2017

TAUMATA PLANTATIONS LIMITED

Annual Report

For the Year Ended 30 June 2017

Contents

Income Statement

Statement of Comprehensive Income

Statement of Financial Position

Statement of Changes in Equity

Statement of Cash Flows

Notes to the Financial Statements

Auditors' Report

Page

2

3

4

5

6 - 25

26 - 27

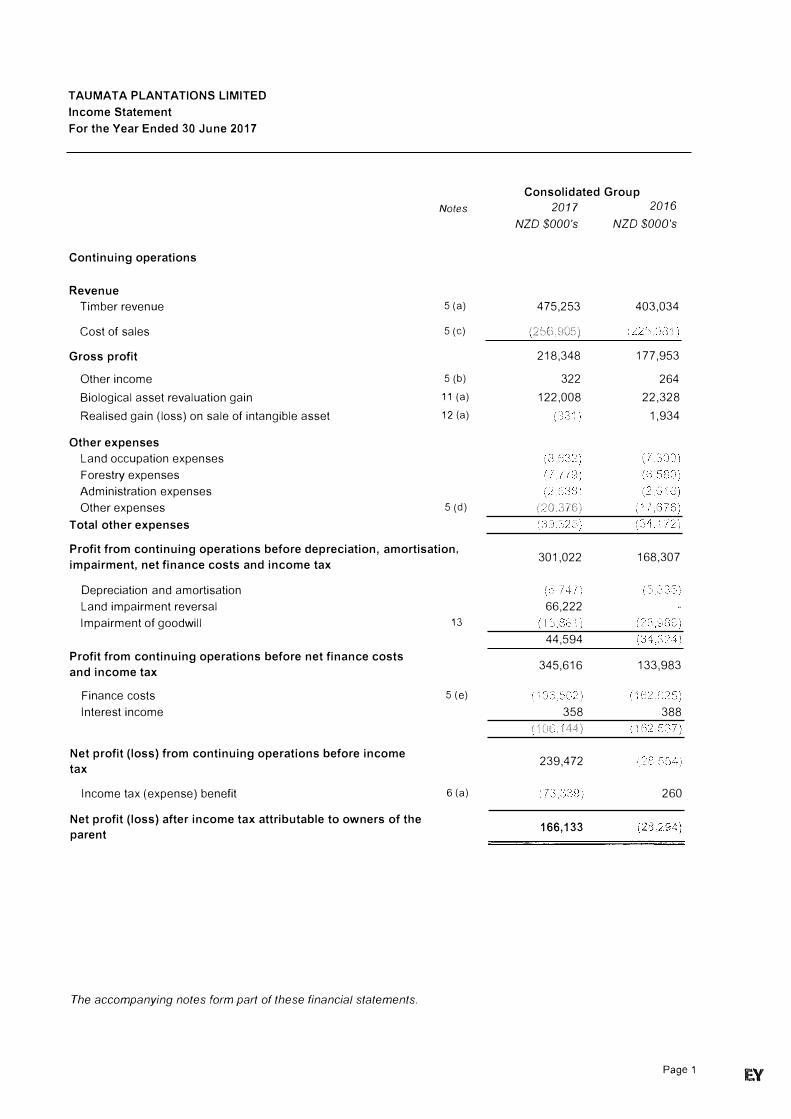

TAUMATA PLANTATIONS LIMITED

Income Statement

For the Year Ended 30 June 2017

Continuing operations

Revenue

Timber revenue

Cost of sales

Gross profit

Other income

Biological asset revaluation gain

Realised gain (loss) on sale of intangible asset

Other expenses

Land occupation expenses

Forestry expenses

Administration expenses

Other expenses

Total other expenses

Consolidated Group

Notes 2017 2016

NZO $000's NZO $000's

5 (a) 475,253 403,034

5 (c) ! '.2 '.1(-Ulu=i)

218,348 177,953

5 (b) 322 264

11 (a) 122,008 22,328

12 (a) 1,934

5 (d) (:.20,3'/C)

Profit from continuing operations before depreciation, amortisation,

impairment, net finance costs and income tax 301,022 168,307

Depreciation and amortisation

Land impairment reversal

Impairment of goodwill

Profit from continuing operations before net finance costs

and income tax

Finance costs

Interest income

Net profit (loss) from continuing operations before income

tax

Income tax (expense) benefit

Net profit (loss) after income tax attributable to owners of the

parent

The accompanying notes form part of these financial statements,

13

5 (e)

6 (a)

66,222

44,594

345,616

358

!Wl,I4'1)

239,472

166,133

133,983

388

260

Page 1 E.Y

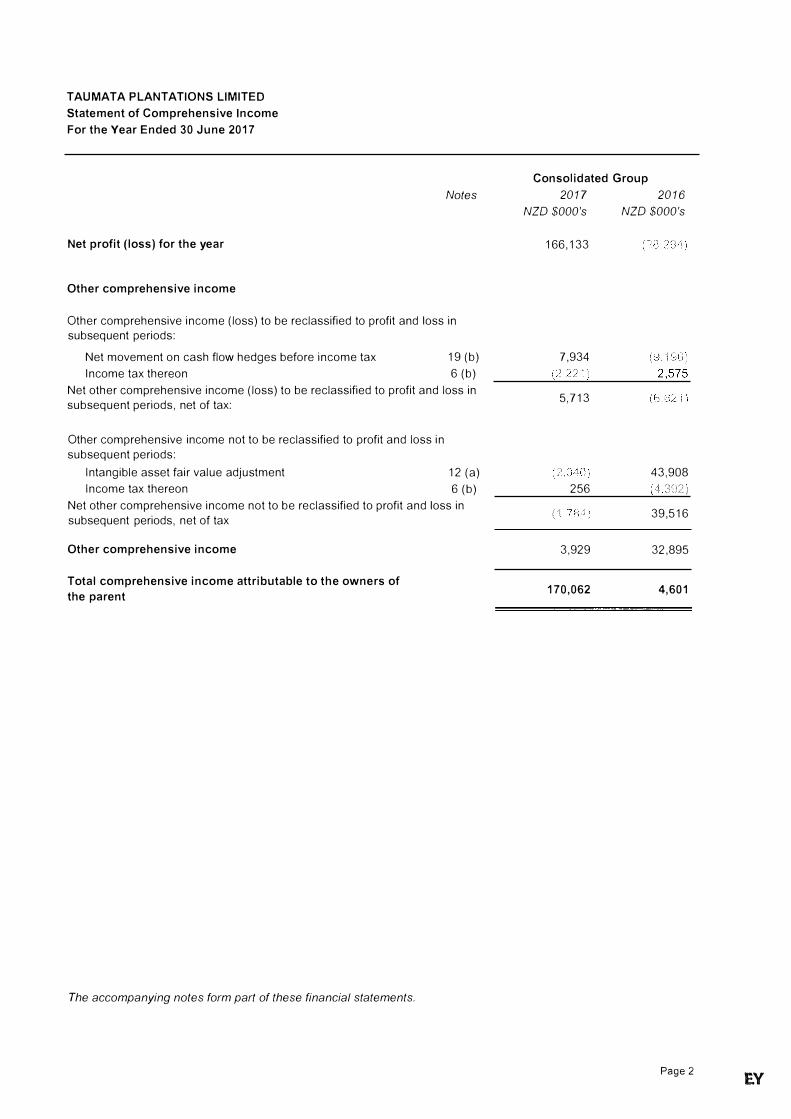

TAUMATA PLANTATIONS LIMITED

Statement of Comprehensive Income

For the Year Ended 30 June 2017

Net profit (loss) for the year

Other comprehensive income

Notes

Other comprehensive income (loss) to be reclassified to profit and loss in

subsequent periods:

Net movement on cash flow hedges before income tax 19 (b)

Income tax thereon 6 (b)

Net other comprehensive income (loss) to be reclassified to profit and loss in

subsequent periods, net of tax:

Other comprehensive income not to be reclassified to profit and loss in

subsequent periods:

Intangible asset fair value adjustment

Income tax thereon

12 (a)

6 (b)

Net other comprehensive income not to be reclassified to profit and loss in

subsequent periods, net of tax

Other comprehensive income

Total comprehensive income attributable to the owners of

the parent

The accompanying notes form part of these financial statements.

Consolidated Group

2017 2016

NZD $000's NZD $000's

166,133

7,934

5,713

43,908

256 3(())

(1 39,516

3,929 32,895

170,062 4,601

Page 2 EV

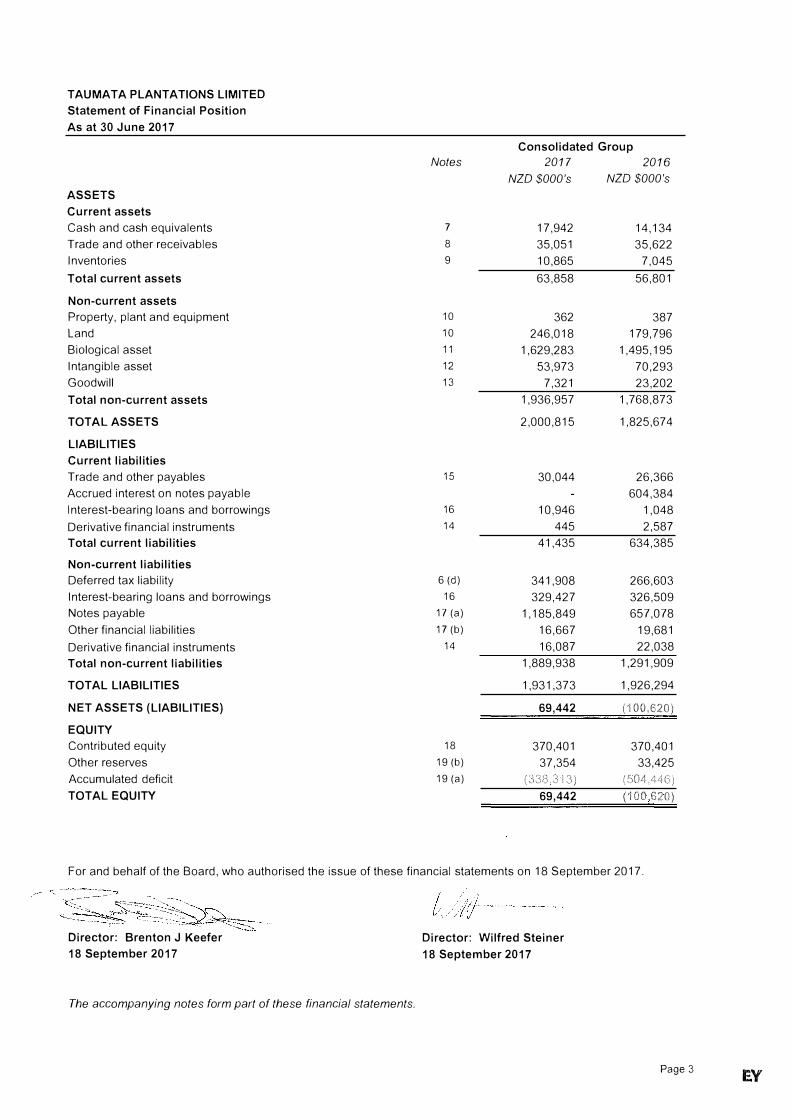

TAUMATA PLANTATIONS LIMITED

Statement of Financial Position

As at 30 June 2017

Consolidated Group

Notes 2017 2016

NZD $000's NZD $000's

ASSETS

Current assets

Cash and cash equivalents 7 17,942 14,134

Trade and other receivables 8 35,051 35,622

Inventories 9 10,865 7,045

Total current assets 63,858 56,801

Non-current assets

Property, plant and equipment 10 362 387

Land 10 246,018 179,796

Biological asset 11 1,629,283 1,495,195

Intangible asset 12 53,973 70,293

Goodwill 13 7,321 23,202

Total non-current assets 1,936,957 1,768,873

TOT AL ASSETS 2,000,815 1,825,674

LIABILITIES

Current liabilities

Trade and other payables 15 30,044 26,366

Accrued interest on notes payable 604,384

Interest-bearing loans and borrowings 16 10,946 1,048

Derivative financial instruments 14 445 2,587

Total current liabilities 41,435 634,385

Non-current liabilities

Deferred tax liability 6 (d) 341,908 266,603

Interest-bearing loans and borrowings 16 329,427 326,509

Notes payable 17 (a) 1,185,849 657,078

Other financial liabilities 17 (b) 16,667 19,681

Derivative financial instruments 14 16,087 22,038

Total non-current liabilities 1,889,938 1,291,909

TOTAL LIABILITIES 1,931,373 1,926,294

NET ASSETS (LIABILITIES) 69,442 (100,620)

EQUITY

Contributed equity 18 370,401 370,401

Other reserves 19 (b) 37,354 33,425

Accumulated deficit 19 (a) (33d.3··1J) (E)04)4l�1.3)

TOTAL EQUITY 69,442 (100 620)

For and behalf of the Board, who authorised the issue of these financial statements on 18 September 2017.

Director: Brenton J Keefer

18 September 2017

The accompanying notes form part of these financial statements.

Director: Wilfred Steiner

18 September 2017

Page 3 E.Y

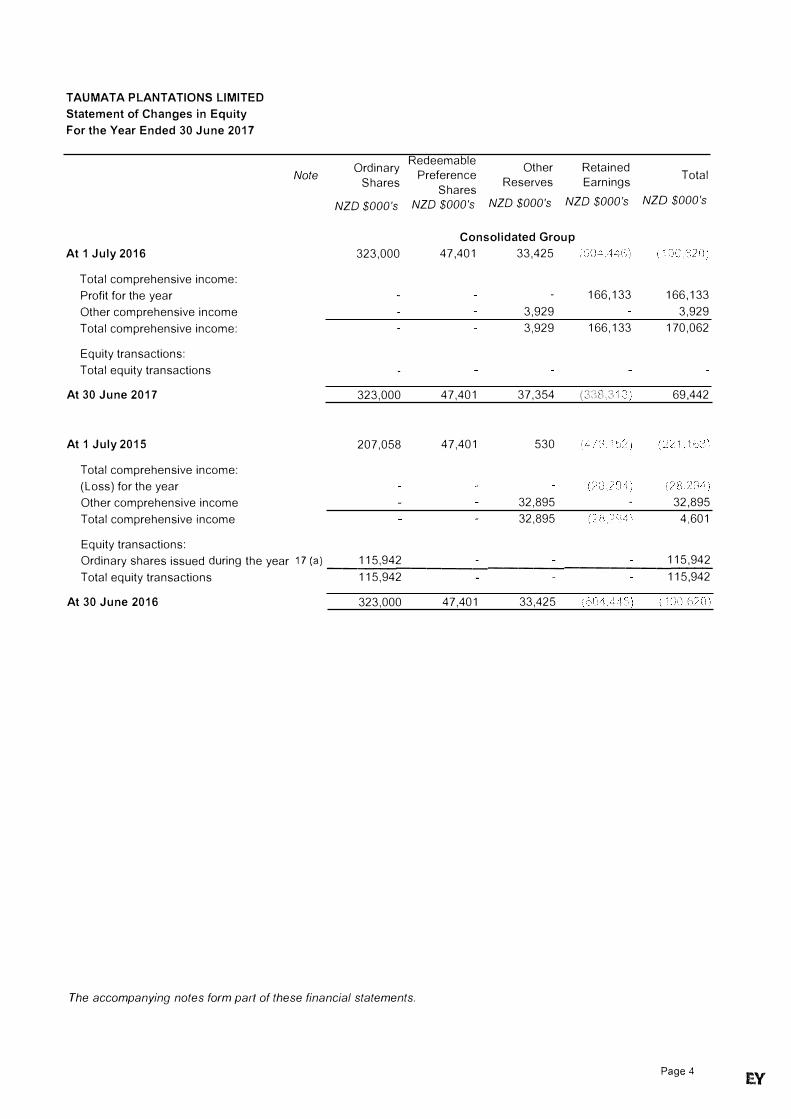

TAUMATA PLANTATIONS LIMITED

Statement of Changes in Equity

For the Year Ended 30 June 2017

At 1 July 2016

Total comprehensive income:

Profit for the year

Other comprehensive income

Total comprehensive income:

Equity transactions:

Total equity transactions

At 30 June 2017

At 1 July 2015

Total comprehensive income:

(Loss) for the year

Other comprehensive income

Total comprehensive income

Equity transactions:

Note Ordinary

Shares

Redeemable Preference

Shares

Other Reserves

Retained Earnings

Total

NZO $000's NZO $000's NZO $000's NZO $000's NZO $000's

323,000

323,000

207,058

Consolidated Group

47,401 33,425

3,929

3,929

47,401 37,354

47,401 530

32,895

32,895

166,133

166,133

(3'.',8.31

166,133

3,929

170,062

69,442

32,895

4,601

Ordinary shares issued during the year 17 (a) ___ 1 _15--', _9 _42 __________________ 1_1 _5 _,9_4_2

Total equity transactions 115,942 115,942

At 30 June 2016 323,000 47,401 33,425

The accompanying notes form pa,1 of these financial statements.

Page 4 EV

TAUMATA PLANTATIONS LIMITED

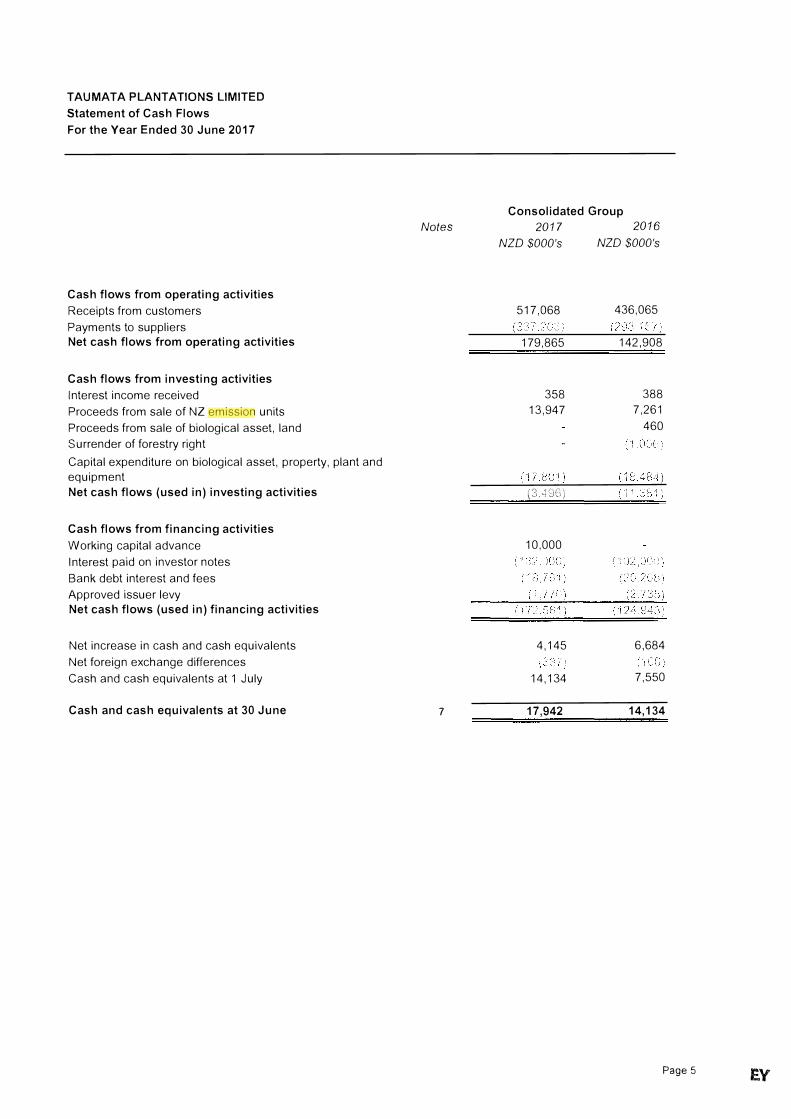

Statement of Cash Flows

For the Year Ended 30 June 2017

Cash flows from operating activities

Receipts from customers

Payments to suppliers

Net cash flows from operating activities

Cash flows from investing activities

Interest income received

Proceeds from sale of NZ emission units

Proceeds from sale of biological asset, land

Surrender of forestry right

Capital expenditure on biological asset, property, plant and

equipment

Net cash flows (used in) investing activities

Cash flows from financing activities

Working capital advance

Interest paid on investor notes

Bank debt interest and fees

Approved issuer levy

Net cash flows (used in) financing activities

Net increase in cash and cash equivalents

Net foreign exchange differences

Cash and cash equivalents at 1 July

Cash and cash equivalents at 30 June

Notes

7

Consolidated Group

2017 2016

NZD $000's

517,068

179,865

358

13,947

(3. H16)

10,000

4,145

14,134

17,942

NZD $000's

436,065

142,908

388

7,261

460

6,684

7,550

14,134

Page 5 EY

TAUMATA PLANTATIONS LIMITED

Notes to the Financial Statements

For the Year Ended 30 June 2017

1. CORPORATE INFORMATION

The financial statements of Taumata Plantations Limited and its subsidiaries ( collectively, the Group) for the year ended

30 June 2017 were authorised for issue in accordance with a resolution of the directors on 18 September 2017.

2.1 STATEMENT OF COMPLIANCE

The consolidated financial statements of the Group comply with New Zealand Equivalents to International Financial

Reporting Standards (NZ IFRS) with reduced disclosure requirements (RDR).

2.2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(a) Basis of preparation

The financial statements have been prepared in accordance with generally accepted accounting practice in New Zealand (NZ GAAP). For the purposes of complying with NZ GAAP the entity is a for-profit entity.

The Group is a Tier 2 for-profit entity and has elected to report in accordance with Tier 2 For-profit Accounting

Standards. The Group is eligible to report in accordance with Tier 2 For-profit Accounting Standards on the basis that it

does not have public accountability and is not a large for-profit public sector entity.

The consolidated financial statements have been prepared on a historical cost basis, except for biological asset,

intangible asset, derivative financial instruments and 2006 convertible preference shares which have been measured at

fair value.The consolidated financial statements are presented in New Zealand dollars and all values are rounded to the

nearest thousand dollars ($000), except when otherwise indicated.

The financial statements provide comparative information in respect of the previous period.

(b) Basis of consolidation

The consolidated financial statements comprise the financial statements of Taumata Plantations Limited and its

subsidiaries (the Group) as at 30 June 2017. Control is achieved when the Group is exposed, or has rights, to variable

returns from the involvement with the investee and has the ability to affect those returns through its power over the investee.

The Group re-assesses whether or not it controls an investee if facts and circumstances indicate that there are changes

to one or more of the three elements of control. Consolidation of a subsidiary begins when the Group obtains control

over the subsidiary and ceases when the Group loses control of the subsidiary. Assets, liabilities, income and expenses

of a subsidiary acquired or disposed of during the year are included in the statement of comprehensive income from the

date the Group gains control until the date the Group ceases to control the subsidiary.

Profit or loss and each component of other comprehensive income (OCI) are attributed to the equity holders of the

parent of the Group. All intra-group assets and liabilities, equity, income, expenses and cash flows relating to

transactions between members of the Group are eliminated in full on consolidation.

(c) Business combinations and goodwill

Business combinations are accounted for using the acquisition method. The cost of an acquisition is measured as theaggregate of the consideration transferred measured at acquisition date fair value and the amount of any non

controlling interests in the Group.

Goodwill is initially measured at cost, being the excess of the aggregate of the consideration transferred and the

amount recognised for non-controlling interests, and any previous interest held, over the net identifiable assets acquired

and liabilities assumed.

After initial recognition, goodwill is measured at cost less any accumulated impairment losses.

For the purpose of impairment testing, goodwill acquired in a business combination is, from the acquisition date,

allocated to each of the Group's cash-generating units that are expected to benefit from the combination, irrespective of

whether other assets or liabilities of the Group are assigned to those units. Each unit or group of units to which the

goodwill is so allocated represents the lowest level within the Group at which the goodwill is monitored for internal

management purposes.

Impairment is determined by assessing the recoverable amount of the cash-generating unit (or group of cashgenerating units), to which the goodwill relates. When the recoverable amount of the cash-generating unit (or group of

cash generating units) is less than the carrying amount, an impairment loss is recognised. When goodwill forms part of a cash-generating unit ( or group of cash-generating units) it is included in the carrying amount of the operation when

determining the gain or loss on disposal of the operation. Goodwill disposed of in this manner is measured based on

the relative values of the operation disposed of and the portion of the cash-generating unit retained.

Impairment losses recognised for goodwill are not subsequently reversed.

Page 6

EY

TAUMATA PLANTATIONS LIMITED

Notes to the Financial Statements

For the Year Ended 30 June 2017

2.2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

(d) Foreign currency translation

Both the functional and presentation currency of Taumata Plantations Limited is New Zealand dollars($).

Transactions in foreign currencies are initially recorded in the functional currency at the exchange rates ruling at the date of the transaction. Monetary assets and liabilities denominated in foreign currencies are retranslated at the rate of

exchange ruling at the balance sheet date.

(e) Property, plant and equipment

Following initial recognition at cost, land is carried at cost less any subsequent accumulated impairment losses.

Plant and equipment is stated at cost, net of accumulated depreciation and accumulated impairment losses, if any.

Depreciation is calculated on a diminishing value basis dependent upon the estimated useful life of the specific asset.

Depreciation rates are as follows:

Land Not depreciated

Buildings

Plant and equipment

Furniture & fittings

Computers

Derecognition and disposal

9.5%

22%

22%

50%

An item of property, plant and equipment is derecognised upon disposal or when no further future economic benefits are expected from its use or disposal. Gains and losses on disposals which are included in the income statement are

determined by comparing proceeds with the carrying amount.

(f) Leases

The determination of whether an arrangement is or contains a lease is based on the substance of the arrangement andrequires an assessment of whether the fulfillment of the arrangement is dependent on the use of a specific asset or

assets and the arrangement conveys a right to use the asset.

Operating lease payments are recognised as an expense in the income statement on a straight-line basis over the lease term. The Group has not entered into any finance lease arrangements.

(g) Impairment of non-current assets

At each reporting date, the Group assesses whether there is any indication that an asset may be impaired. If anyindication of impairment exists, an estimate of the asset's recoverable amount is calculated. An impairment loss is recognised when the asset's carrying amount exceeds its recoverable amount.

Recoverable amount is the higher of an asset's fair value less costs to sell and value in use. For the purposes of assessing impairment, assets are grouped at the lowest levels for which there are separately identifiable cash inflows

that are largely independent of the cash inflows from other assets or groups of assets ( cash-generating units).

In assessing value in use, the estimated cash inflows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset.

(h) Inventories

Log inventories are valued at the lower of cost and net realisable value. Net realisable value is the estimated selling

price in the ordinary course of business, less the estimated costs necessary to make the sale.

(i) Trade and other receivables

Trade receivables, which generally have 30 day terms, are recognised and carried at original invoice amount less anallowance for impairment.

Collectibility of trade receivables is reviewed on an ongoing basis. Individual debts that are known to be uncollectible are written off when identified. An impairment provision is recognised when there is objective evidence that the Group will not be able to collect the receivable. Financial difficulties of the debtor, default payments or debts more than 60 days overdue are considered objective evidence of impairment subject to management review and consideration of all available information.

Page 7 EV

TAUMATA PLANTATIONS LIMITED

Notes to the Financial Statements

For the Year Ended 30 June 2017

2.2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

(j) Cash

Cash and cash equivalents in the statement of financial position comprise cash at bank and short term deposits that are

readily convertible to known amounts of cash and which are subject to an insignificant risk of change in value.

Interest income on the New Zealand dollar cash account, is calculated at the New Zealand Official Cash Rate (OCR),

calculated on a daily basis and paid to the account on the last business day of each month. The interest rate as at 30

June 2017 is 1.65% (2016: 2.25%).

(k) Intangible asset - carbon emission reduction units

Carbon emission reduction units ("units") are recognised when the Group controls the units, provided that it is probable

that economic benefits will flow to the Group and the fair value of the units can be measured reliably. Control of the

units arises when the Group has an entitlement to the units.

Carbon emission reduction units are initially measured at fair value on entitlement as an intangible asset unless the

Board of Directors have determined they are held for sale, in which case they would be recorded at the lower of cost or

net realisable value as inventory.

Following initial recognition, the intangible asset has been measured at fair value since the Board of Directors consider

there is an active market for the sale of units. Where it is considered there is no active market for the sale of the units,

the intangible asset is recorded at cost less accumulated impairment losses, if any. Units determined as held for sale at

recognition and recorded as inventory are subsequently measured at cost (less amortisation and impairment, if any}, or

net realisable value.

The intangible asset is tested for impairment annually. The liability arising from the deforestation of eligible land is

measured using the market value approach. A liability exists on pre-1990 forests if the land use changes from forestry.

On land holdings of post-1989 forests the Group has deregistered from the emissions trading scheme and has met all

obligations.

(I) Derivative financial instruments, hedging and risk management

The Group's principal financial instruments, other than derivatives, comprise a syndicated bank loan, a working capital

facility, convertible notes and preference shares with a contractual redemption date. The main purpose of these

financial instruments is to raise finance for the Group's operations.

The Group has various other financial assets and liabilities such as cash and cash equivalents, trade receivables and

trade payables, which arise directly from its operations.

The Group uses derivative financial instruments, principally interest rate swaps, for the purpose of managing interest

rate risk on the Group's syndicated bank loan. The Group has no intention to trade derivative financial instruments.

The Group has issued promissory notes payable, the terms of which contain an option for the Group to repay or redeem

the notes at any time before expiration. The terms of the notes also contain an option for the Group to convert the

promissory notes payable into newly issued preference shares of the Group at any time before expiration at the rate of one New Zealand dollar of principal and accrued and unpaid interest for each New Zealand dollar of redemption

amount of preferred shares.

The main risks arising from the Group's financial instruments are interest rate risk, credit risk, fair value risk and liquidity

risk. The Board reviews and agrees policies for managing each of these risks as summarised below.

Details of the significant accounting policies and methods adopted, including the criteria for recognition, the basis for

measurement and the basis on which income and expenses are recognised, in respect of each class of financial asset,

financial liability and equity instrument are disclosed in this note.

Interest rate risk

The Group's exposure to market interest rates relates primarily to the Group's syndicated bank loan with a floating

interest rate.

The Group's policy is to manage its finance costs using a mix of fixed and variable rate debt. To manage this risk in a

cost-efficient manner, the Group enters into interest rate swaps, in which the Group agrees to exchange, at specified

intervals, the difference between fixed and variable rate interest amounts calculated by reference to an agreed-upon

notional principal amount. These swaps are designated to hedge underlying debt obligations. At 30 June 2017, after

taking into account the effect of interest rate swaps, approximately 81% (2016: 81%) of the Group's borrowings in

relation to the syndicated bank loan are at a fixed rate of interest.

Page 8 EV

TAUMATA PLANTATIONS LIMITED

Notes to the Financial Statements

For the Year Ended 30 June 2017

2.2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

(I) Derivative financial instruments, hedging and risk management (continued)

Fair value interest rate risk

The Group enters into interest rate swaps which are measured in the statement of financial position at fair value. Fair value of the interest rate swap depends on fluctuations in market interest rates. As the Group's intention is to hold the interest rate swaps until expiry as a cash flow hedge, fluctuations in fair value are not expected to impact the Group's commercial operations or its capacity to attract adequate operating finance.

The fair value of the Group's preferred shares redemption liability is also subject to fluctuations in market interest rates. The fluctuations in fair value will impact the income statement and equity but is not expected to impact the Group's cash flow, commercial operations or the ability of the Group to secure adequate finance.

Credit risk

Credit risk arises from the financial assets of the Group, which comprise cash and cash equivalents, and trade and other receivables. The Group's exposure to credit risk arises from potential default of the counter party, with a maximum exposure equal to the carrying amount of these instruments.

The Group seeks to trade only with recognised, creditworthy third parties. It is the Group's policy that all customers who wish to trade on credit terms are subject to credit verification procedures. In addition, receivable balances are monitored on an ongoing basis with the result that the Group's exposure to bad debts is not significant.

Interest rate swaps have been transacted separately with three financial institutions thus reducing the concentration of credit risk with respect to any one counterparty. Cash and cash equivalents are held with Westpac Banking Corporation.

Liquidity risk

Liquidity risk arises from meeting obligations associated with financial liabilities.

The Group's objective is to maintain a balance between continuity of funding and flexibility through the use of a syndicated bank loan, a syndicated bank working capital facility, convertible notes and preference shares with a contractual redemption date.

Interest rate swap and hedging

The Group uses interest rate swaps to hedge its risks associated with interest rate fluctuations on the bank loan. Interest rate swaps are initially recognised at fair value (usually $nil) when entered into and are subsequently remeasured to fair value at each reporting date. Interest rate swaps are carried as assets when their fair value is positive and as liabilities when their fair value is negative.

For the purpose of hedge accounting, the interest rate swap is classified as a cash flow hedge as it hedges the Group's exposure to variability in cash flows attributable to the payment of interest on the bank loan.

At inception of an interest rate swap, the Group formally designates the swap as a hedging instrument and documents the hedge relationship and risk management objectives for undertaking the hedge. The documentation includes identification of the hedging instrument and the hedged item, the nature of the risk being hedged and how the Group will assess the hedging instrument's effectiveness in offsetting exposure to variability in cash flows attributable to variable interest rates on the bank loan. The cash flow hedge is expected to be highly effective in offsetting cash flow variability and it is assessed on an ongoing basis to determine that it actually has been highly effective throughout the financial reporting periods for which it was designated.

A cash flow hedge that meets the strict criteria of hedge accounting is accounted for as follows:

Cash flow hedges are hedges of the Group's exposure to variability in cash flows that is attributable to a particular risk associated with a recognised asset or liability or a highly probable forecast transaction that could affect the income statement. The effective portion of the gain or loss on the hedging instruments is recognised in other comprehensive income, net of income tax, while the ineffective portion is recognised in the income statement.

Amounts taken to equity are subsequently transferred to the income statement when the hedge transaction affects the income statement, such as when interest expense on the bank loan is recognised in the income statement.

If the forecast transaction is no longer expected to occur, amounts previously recognised in equity are transferred to the income statement. If the hedging instrument expires or is sold, terminated or exercised without replacement or rollover, amounts previously recognised in equity are transferred to the income statement.

If the hedged instrument ceases to qualify for hedge accounting and the forecast transaction is still expected to occur, then all amounts previously taken directly to equity are transferred to the income statement. In addition, all future gains and losses on the hedging instrument will be taken to the income statement when the forecast transaction occurs.

Page 9 EV

TAUMATA PLANTATIONS LIMITED

Notes to the Financial Statements

For the Year Ended 30 June 2017

2.2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

(m) Interest-bearing loans and borrowings

All loans and borrowings are initially recognised at the fair value of the consideration received less directly attributable

transaction costs.

After initial recognition, interest-bearing loans and borrowings are subsequently measured at amortised cost using the

effective interest method. Amortised cost is calculated by including issue costs and any discount or premium on initial

issue; and estimating cash flows over the term of the loan, including interest payments and other costs to maintain the

loan, to determine the effective interest rate on the loan. The Group considers that the carrying amount of interest

bearing loans and borrowings is a reasonable approximation of the fair value, however the carrying amount does not

represent the amount repayable on early termination.

Borrowings are classified as current liabilities unless the Group has an unconditional right to defer settlement of the

liability for at least 12 months after the balance sheet date.

(n) Notes payable

Notes payable are initially recognised at the fair value of the consideration received less directly attributable transaction

costs.

After initial recognition, notes payable are subsequently measured at amortised cost using the effective interest method.

Amortised cost is calculated by including issue costs and any discount or premium on issue; and estimating cash flows

over the term of the notes, including interest payments, to determine the effective interest rate on the notes payable.

Interest expense is calculated by applying the effective interest rate to the amortised balance and is taken to the income

statement. Gains and losses on derecognition of notes payable are taken to the income statement in the period the

notes are derecognised.

(o) Trade and other payables

Trade and other payables are carried at invoice amount. They represent liabilities for goods and services provided to

the Group prior to the end of the financial year that are unpaid and arise when the Group becomes obliged to make

future payments in respect of the purchase of these goods and services. The amounts are unsecured and are usually

paid within 30 days of recognition. Due to the short term nature of trade payables, their carrying amount is considered

a close approximation of their fair value.

(p) Provisions

Provisions are recognised when the Group has a present obligation (legal or constructive) as a result of a past event, it

is probable that an outflow of resources embodying economic benefits will be required to settle the obligation and a

reliable estimate can be made of the amount of the obligation.

When the Group expects some or all of a provision to be reimbursed, for example under an insurance contract, the

reimbursement is recognised as a separate asset but only when the reimbursement is virtually certain. The expense

relating to a provision is presented in the income statement net of any reimbursement.

If the effect of the time value of money is material, provisions are discounted using a current pre-tax rate that reflects,

when appropriate, the risks specific to the liability. The increase in the provision resulting from the passage of time is

recognised as a finance cost.

(q) Revenue recognition

Revenue is recognised to the extent that it is probable that the economic benefits will flow to the Group and the revenue

can be reliably measured, regardless of when the payment is being made. The following specific recognition criteria

must also be met before revenue is recognised:

Timber revenue

Timber revenue is recognised when the Group has ensured delivery of the product according to the terms and

conditions of the contract, the customer has assumed the risks and rewards of ownership and collection of the related

receivables is reasonably assured. Generally this occurs for sales in domestic markets after the shipment of the goods

to customers. In the case of goods sold to export customers this is dependent on the nature of the contract, but no

earlier than the goods are loaded on the vessel.

Interest revenue

Interest revenue on bank and short term cash deposits is recognised using the effective interest rate method.

Page 10 EY

TAUMATA PLANTATIONS LIMITED

Notes to the Financial Statements

For the Year Ended 30 June 2017

2.2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

(q) Revenue recognition (continued)

Other income

Other Income is recognised when the Group has ensured delivery of the product, such as by product wastes, where the

customer has assumed the risks and rewards of ownership. Management fees are recognised according to the terms

and conditions of the contract.

(r) Income tax

Current income tax assets and liabilities for the current and prior periods are measured at the amount expected to be

recovered from or paid to the taxation authorities. The tax rates and tax laws used to compute the amount are those

that are enacted or substantively enacted by the balance sheet date in New Zealand.

Deferred tax is provided using the liability method on temporary differences at the balance sheet date between the tax

bases of assets and liabilities and their carrying amounts for financial reporting purposes.

Deferred income tax liabilities are recognised for all taxable temporary differences except:

- when the deferred income tax liability arises from the initial recognition of goodwill; or

- when the deferred income tax liability arises from the initial recognition of an asset or liability in a transaction that is

not a business combination and that, at the time of the transaction, affects neither the accounting profit nor taxable

profit or loss; or

- when the taxable temporary difference is associated with investments in subsidiaries, and the timing of the reversal of

the temporary differences can be controlled and it is probable that the temporary difference will not reverse in the

foreseeable future.

Deferred income tax assets are recognised for all deductible temporary differences, the carry forward of unused tax

credits and unused tax losses, to the extent that it is probable that future taxable profit will be available against which

the deductible temporary differences, and the carry forward of unused tax credits and unused tax losses can be utilised,

except:

- when the deferred income tax asset relating to the deductible temporary differences arises from the initial recognition

of an asset or liability in a transaction that is not a business combination and, at the time of the transaction, affects

neither the accounting profit nor taxable profit or loss; or

- when the deductible temporary differences are associated with investment in subsidiaries, deferred tax assets are

only recognised to the extent that it is probable that the temporary differences will reverse in the foreseeable future and

future taxable profits will be available against which the temporary differences can be utilised.

The carrying amount of deferred income tax assets is reviewed at each balance sheet date and reduced to the extent

that it is no longer probable that sufficient future taxable profits will be available to allow all or part of the deferred

income tax asset to be utilised.

Deferred tax assets and deferred tax liabilities are offset only if a legally enforceable right exists to set off current tax

assets against current tax liabilities and the deferred tax assets and liabilities relate to the same taxable entity and the

same taxation authority.

Income tax relating to items recognised in equity are recognised in equity and not in the income statement.

(s) Other taxes

Revenues, expenses, assets and liabilities are recognised net of the amount of GST except:

- when the GST incurred on a purchase of goods and services is not recoverable from the taxation authority, in which

case the GST is recognised as part of the cost of acquisition of the asset or as part of the expense item as applicable;

and

- receivables and payables, which are stated with the amount of GST included.

The net amount of GST recoverable from, or payable to, the taxation authority is included as part of the receivables or payables in the statement of financial position.

Cash flows are included in the statement of cash flows on a gross basis and the GST component of cash flows arising

from investing and financing activities, which is recoverable from, or payable to, the taxation authority is classified as

part of operating cash flows.

Commitments and contingencies are disclosed net of the amount of GST recoverable from, or payable to, the taxation

authority.

Page 11

EY

TAUMATA PLANTATIONS LIMITED

Notes to the Financial Statements

For the Year Ended 30 June 2017

2.2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

(t) Biological assets

Biological assets are predominantly standing trees which are managed by the company on a sustainable-yield basis.

These are shown in the statement of financial position at fair value. The costs to establish and maintain the forest

assets are included in the income statement together with the change in fair value for each accounting period.

The determination of fair value, as assessed annually by an independent forest valuer, is based on the before tax value

of net revenue from projected woodflows by product and destination. Projected woodflows, which are derived from the

forest estate model, correspond to the expected volumes of merchantable timber that could be harvested from existing stands given current management strategy and projected customer demand.

The forests can be summarised into three main regions based on geographic locations being Northland, Central North

Island and Eastern Bay of Plenty.

Capitalised harvest roads are stated at cost less accumulated depreciation and any impairment in value. Harvest roads

are built to facilitate timber harvesting planned to commence within 12 months following the completion of the road, and

in use for greater than a 12 month period. Roads are included as part of the biological asset.

Depreciation on harvest roads is calculated on a diminishing value basis using the rates over the estimated useful life of

the specific asset. Depreciation rates are as follows:

Harvest Roads (Sealed)

Harvest Roads (Partially or Unsealed)

(u) Derecognition of financial instruments

Acquired prior Acquired post

2013 2013

6%

24%

5%

20%

The derecognition of a financial instrument takes place when the Group no longer controls the contractual rights that

comprise the financial instrument, which is normally the case when the instrument is sold, or all the cash flows

attributable to the instrument are passed through to an independent third party.

(v) Redeemable preference shares

On initial recognition, the component of the preference shares that exhibits characteristics of a liability is recognised as

a liability on the statement of financial position, net of transaction costs.

After initial recognition, the liability component of the preference shares issued in 2006 is subsequently measured at fair

value through the income statement using a discount rate based on a long term bond plus an appropriate credit margin.

The Group's risk management policy requires it to manage various alternative sources of long term capital requirements

in order to minimise the cost of capital to the Group and maximise shareholders' returns. The designation of the 2006

preference shares redemption liability at fair value through the income statement is consistent with this policy as

changes in fair value provide additional information on the cost of capital inherent in the preference shares liability

relative to alternative sources of long term capital.

After initial recognition, the liability component of the preference shares issued in 2009 is subsequently measured at

amortised cost using the effective interest method. As the number of preference shares issued in 2009 is only a small

portion of various long term capital sources and they were issued for nil consideration, the Group considers that in

terms of its risk management policy it was not necessary to subsequently measure this preference share issue at fair

value through the income statement.

The increase in the liability due to the passage of time is recognised as a finance cost using the effective interest rate

method. Changes in fair value attributable to changes in the discount rate are recognised as a finance cost. The

carrying amount of the liability component does not represent the amount that would be contractually repayable if the

shares were redeemed early.

The remainder of the proceeds net of tax is allocated to the residual right to receive future dividends and is recognised

and included in shareholders' equity, net of transaction costs. The carrying amount of the equity component is not

remeasured in subsequent years.

Dividend distribution on the preference shares would be recognised as an equity distribution.

Transaction costs are apportioned between the liability and equity components of the redeemable preference shares

based on the allocation of proceeds between the liability and equity components on initial recognition.

Page 12 E.Y

TAUMATA PLANTATIONS LIMITED

Notes to the Financial Statements

For the Year Ended 30 June 2017

2.2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

(w) Contributed equity

Ordinary shares are classified as equity.

Incremental costs directly attributable to the issue of new shares are shown in equity as a deduction, net of tax, from the

proceeds.

(x) Dividend distribution

Dividend distribution to the company's shareholders would be recognised as a liability in the Group's financial

statements in the year in which the dividends are declared.

2.3 CHANGES IN ACCOUNTING POLICIES AND DISCLOSURES

New and amended standards and interpretations

Certain standards and interpretations apply for the first time in 2017. However, they do not impact the annual

consolidated financial statements of the Group.

The accounting policies adopted are consistent with those of the previous year.

3. SIGNIFICANT ACCOUNTING JUDGEMENTS, ESTIMATES AND ASSUMPTIONS

In the process of applying the Group's accounting policies, the manager makes estimates and assumptions concerning

the future. Estimates and assumptions are continually evaluated and are based on historical experience and other

factors, including expectations of future events that are believed to be reasonable under the circumstances.

The estimates and assumptions are reviewed for reasonableness on an ongoing basis. Revisions to accounting estimates are recognised in the period in which the estimate is revised if the revision effects only that period, or in the

period of revision and future periods if the revision affects both current and future periods.

The estimates and assumptions that have a reasonable risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year are discussed below:

Fair value of the biological asset

The fair value of the biological asset is determined by an independent appraiser which requires the appraiser to make

judgments and assumptions in relation to the discount rate, future log prices and costs, foreign exchange rates and

other key inputs.

Recovery of deferred tax assets

Deferred tax assets are recognised for deductible temporary differences, primarily accumulated income tax losses, as

management considers it is probable that the Group will generate sufficient future taxable profits to utilise the temporary

differences.

Fair value of preference shares

The fair value of the preference shares (issued in 2006) is calculated by discounting the contractual redemption liability

using a market discount rate for a long term treasury bond plus an appropriate credit margin based on market

determined credit margins for similar corporate debt issues.

Estimation of useful lives of depreciable plant and equipment

The estimation of useful lives of depreciable plant and equipment is based on historical experience and also other

factors such as manufacturers· warranties. The condition of assets is assessed each year and considered against the

remaining useful life. Adjustments are made to the estimate of remaining useful life where appropriate.

Assessment of active market for intangible asset

Intangible asset of carbon emission units are valued at fair value when there is an active market for these units. This assessment is based on the frequency and volumes of sales and consistency of quoted prices for sale of the units.

Fair value measurement

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction

between market participants at the measurement date. The fair value measurement is based on the presumption that

the transaction to sell the asset or transfer the liability takes place either:

- In the principal market for the asset or liability, or

- In the absence of a principal market, in the most advantageous market for the asset or liability

- The principal or the most advantageous market must be accessible to by the Group.

Page 13 EV

TAUMATA PLANTATIONS LIMITED

Notes to the Financial Statements

For the Year Ended 30 June 2017

3. SIGNIFICANT ACCOUNTING JUDGEMENTS, ESTIMATES AND ASSUMPTIONS (continued)

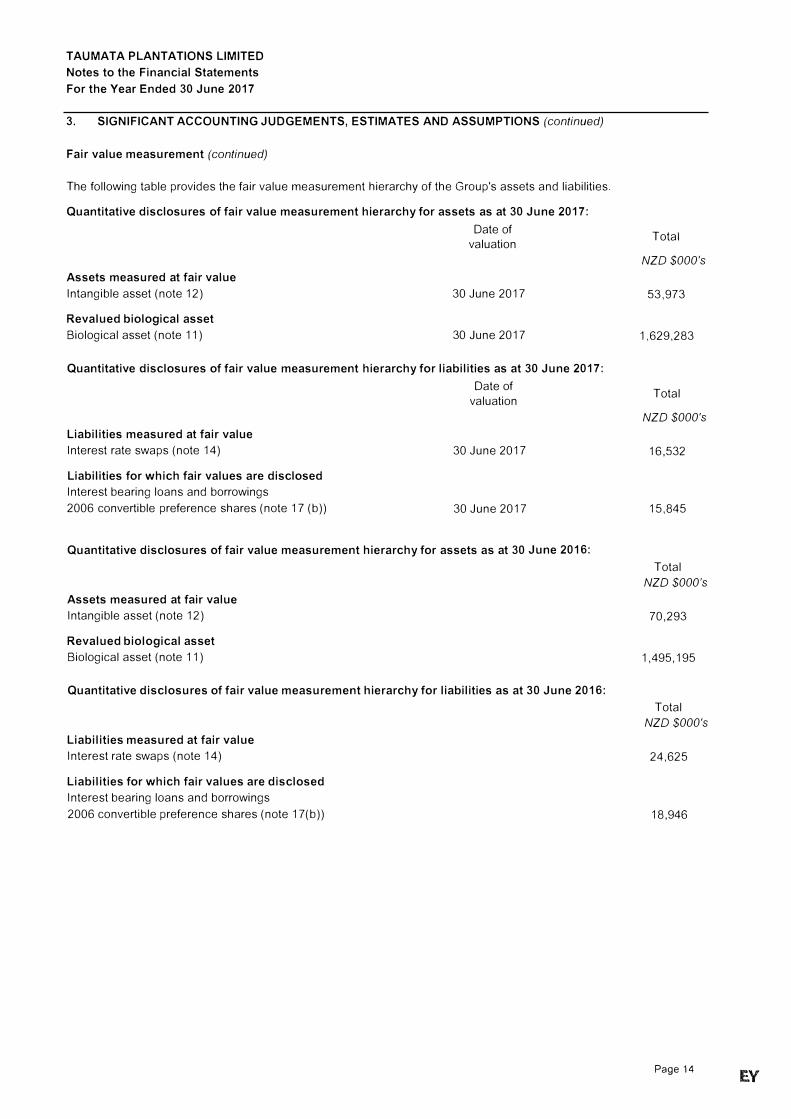

Fair value measurement (continued)

The following table provides the fair value measurement hierarchy of the Group's assets and liabilities.

Quantitative disclosures of fair value measurement hierarchy for assets as at 30 June 2017:

Assets measured at fair value

Intangible asset (note 12)

Revalued biological asset

Biological asset (note 11)

Date of

valuation

30 June 2017

30 June 2017

Quantitative disclosures of fair value measurement hierarchy for liabilities as at 30 June 2017:

Liabilities measured at fair value

Interest rate swaps (note 14)

Liabilities for which fair values are disclosed

Interest bearing loans and borrowings

2006 convertible preference shares (note 17 (b))

Date of

valuation

30 June 2017

30 June 2017

Quantitative disclosures of fair value measurement hierarchy for assets as at 30 June 2016:

Assets measured at fair value

Intangible asset (note 12)

Revalued biological asset

Biological asset (note 11)

Quantitative disclosures of fair value measurement hierarchy for liabilities as at 30 June 2016:

Liabilities measured at fair value

Interest rate swaps (note 14)

Liabilities for which fair values are disclosed

Interest bearing loans and borrowings

2006 convertible preference shares (note 17(b))

Total

NZD $000's

53,973

1,629,283

Total

NZD $000's

16,532

15,845

Total

NZD $000's

70,293

1,495,195

Total

NZD $000's

24,625

18,946

Page 14 EY

TAUMATA PLANTATIONS LIMITED

Notes to the Financial Statements

For the Year Ended 30 June 2017

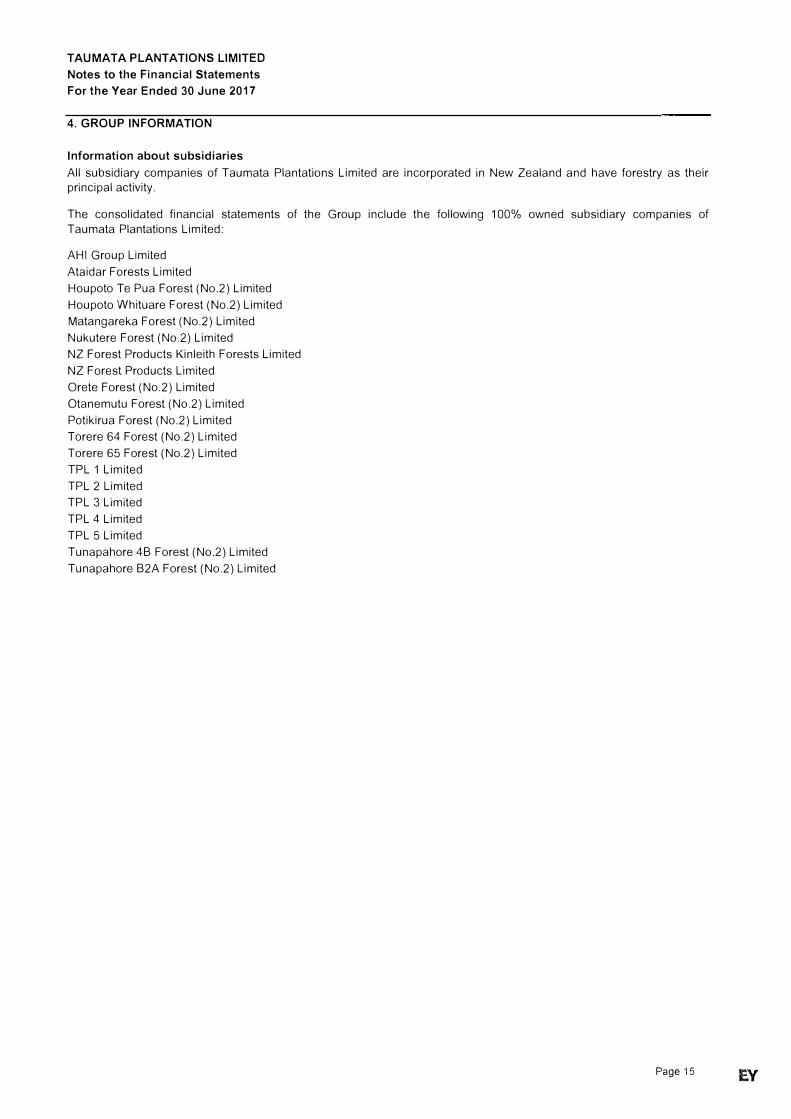

4. GROUP INFORMATION

Information about subsidiaries

All subsidiary companies of Taumata Plantations Limited are incorporated in New Zealand and have forestry as their

principal activity.

The consolidated financial statements of the Group include the following 100% owned subsidiary companies of

Taumata Plantations Limited:

AHi Group Limited

Ataidar Forests Limited

Houpoto Te Pua Forest (No.2) Limited

Houpoto Whituare Forest (No.2) Limited

Matangareka Forest (No.2) Limited

Nukutere Forest (No.2) Limited

NZ Forest Products Kinleith Forests Limited

NZ Forest Products Limited

Orete Forest (No.2) Limited

Otanemutu Forest (No.2) Limited

Potikirua Forest (No.2) Limited

Torere 64 Forest (No.2) Limited

Torere 65 Forest (No.2) Limited

TPL 1 Limited

TPL 2 Limited

TPL 3 Limited

TPL 4 Limited

TPL 5 Limited

Tunapahore 4B Forest (No.2) Limited

Tunapahore B2A Forest (No.2) Limited

Page 15 EV

TAUMATA PLANTATIONS LIMITED

Notes to the Financial Statements

For the Year Ended 30 June 2017

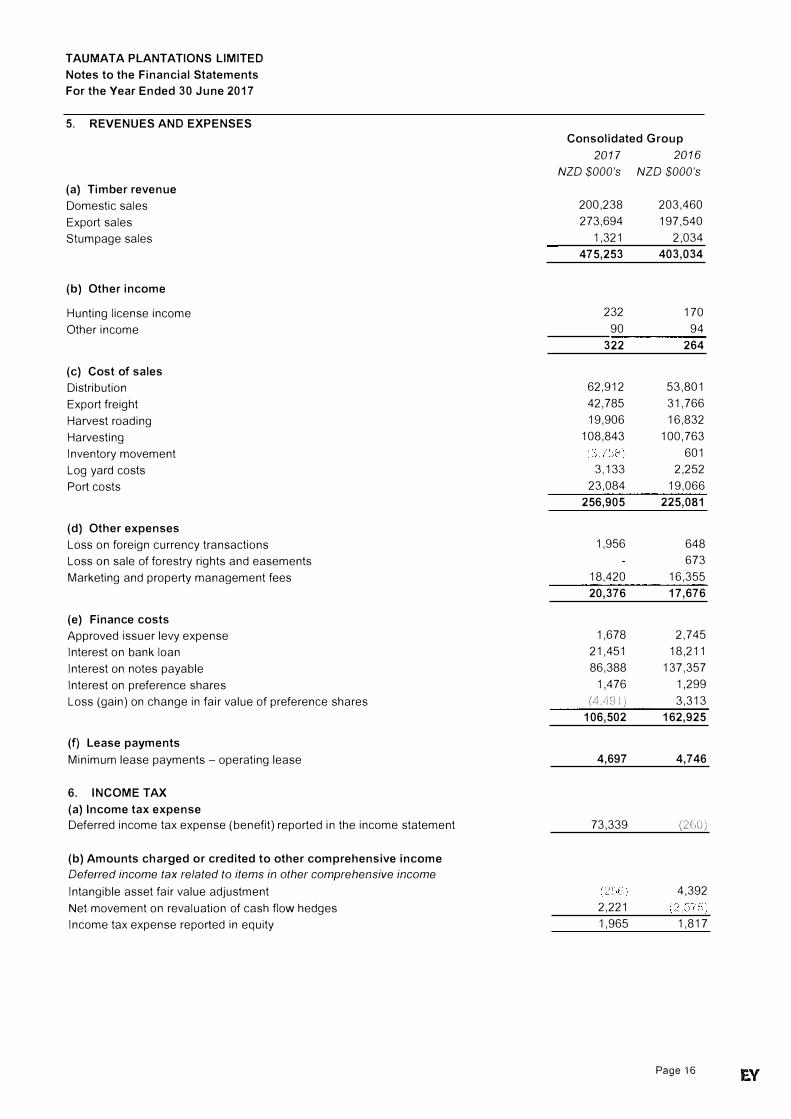

5. REVENUES AND EXPENSES

(a) Timber revenue

Domestic sales

Export sales

Stumpage sales

(b) Other income

Hunting license income

Other income

(c) Cost of sales

Distribution

Export freight

Harvest roading

Harvesting

Inventory movement

Log yard costs

Port costs

(d) Other expenses

Loss on foreign currency transactions

Loss on sale of forestry rights and easements

Marketing and property management fees

(e) Finance costs

Approved issuer levy expense

Interest on bank loan

Interest on notes payable

Interest on preference shares

Loss (gain) on change in fair value of preference shares

(f) Lease payments

Minimum lease payments - operating lease

6. INCOME TAX

(a) Income tax expense

Deferred income tax expense (benefit) reported in the income statement

(b) Amounts charged or credited to other comprehensive income

Deferred income tax related to items in other comprehensive income

Intangible asset fair value adjustment

Net movement on revaluation of cash flow hedges

Income tax expense reported in equity

Consolidated Group

2017 2016

NZD $000's NZD $000's

200,238

273,694

1,321

475,253

232

90

322

62,912

42,785

19,906

108,843

3,133

23,084

256,905

1,956

18,420

20,376

1,678

21,451

86,388

1,476

{4J�)··1)

106,502

4,697

73,339

2,221

1,965

203,460

197,540

2,034

403,034

170

94

264

53,801

31,766

16,832

100,763

601

2,252

19,066

225,081

648

673

16,355

17,676

2,745

18,211

137,357

1,299

3,313

162,925

4,746

(2(iC)

4,392

1,817

Page16 E.Y

TAUMATA PLANTATIONS LIMITED

Notes to the Financial Statements

For the Year Ended 30 June 2017

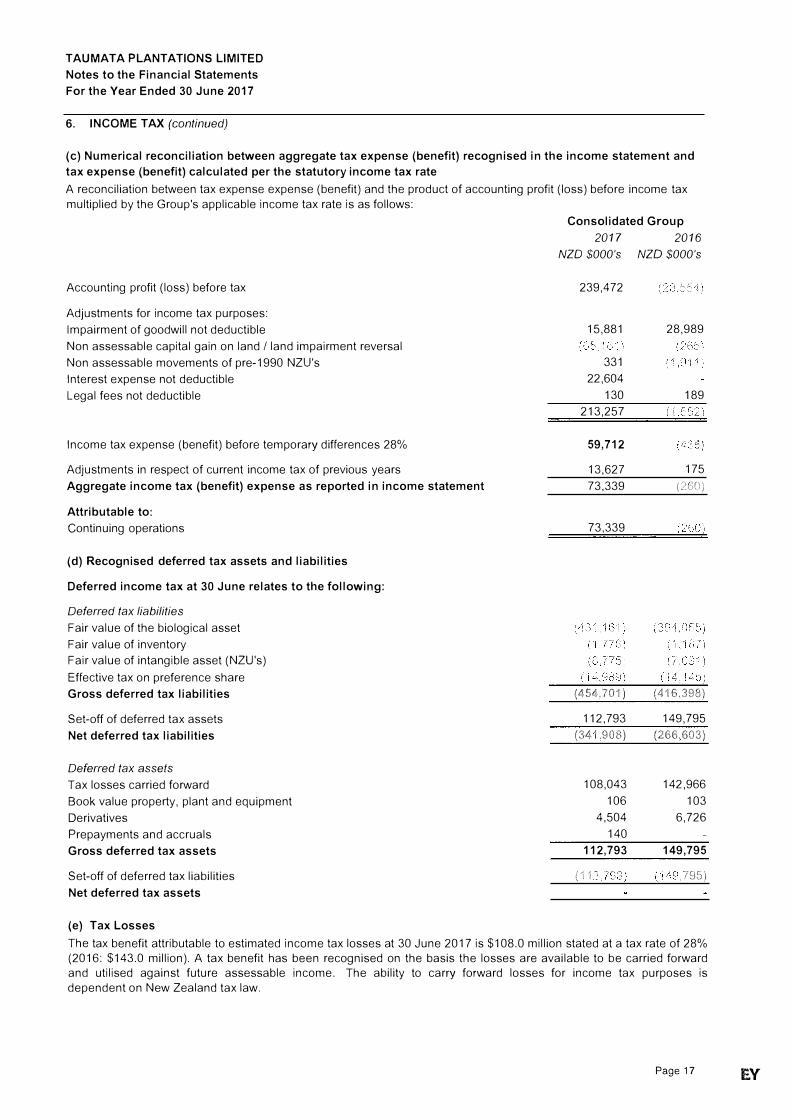

6. INCOME TAX (continued)

(c) Numerical reconciliation between aggregate tax expense (benefit) recognised in the income statement and

tax expense (benefit) calculated per the statutory income tax rate

A reconciliation between tax expense expense (benefit) and the product of accounting profit (loss) before income tax multiplied by the Group's applicable income tax rate is as follows:

Accounting profit (loss) before tax

Adjustments for income tax purposes: Impairment of goodwill not deductible Non assessable capital gain on land / land impairment reversal Non assessable movements of pre-1990 NZU's Interest expense not deductible Legal fees not deductible

Income tax expense (benefit) before temporary differences 28%

Adjustments in respect of current income tax of previous years Aggregate income tax (benefit) expense as reported in income statement

Attributable to:

Continuing operations

(d) Recognised deferred tax assets and liabilities

Deferred income tax at 30 June relates to the following:

Deferred tax liabilities

Fair value of the biological asset Fair value of inventory Fair value of intangible asset (NZU's)

Effective tax on preference share Gross deferred tax liabilities

Set-off of deferred tax assets Net deferred tax liabilities

Deferred tax assets Tax losses carried forward Book value property, plant and equipment Derivatives Prepayments and accruals Gross deferred tax assets

Set-off of deferred tax liabilities Net deferred tax assets

(e) Tax Losses

Consolidated Group

2017 2016

NZD $000's NZD $000's

239,472

15,881

331 22,604

130 213,257

59,712

13,627 73,339

73,339

(454,?Cli)

112,793 (341 908)

108,043 106

4,504 140

112,793

('1'1

28,989

189

175 ()CCi)

(4i6,398)

149,795 (266,603)

142,966 103

6,726

149,795

795)

The tax benefit attributable to estimated income tax losses at 30 June 2017 is $108.0 million stated at a tax rate of 28% (2016: $143.0 million). A tax benefit has been recognised on the basis the losses are available to be carried forward and utilised against future assessable income. The ability to carry forward losses for income tax purposes is dependent on New Zealand tax law.

Page 17 EV

TAUMATA PLANTATIONS LIMITED

Notes to the Financial Statements

For the Year Ended 30 June 2017

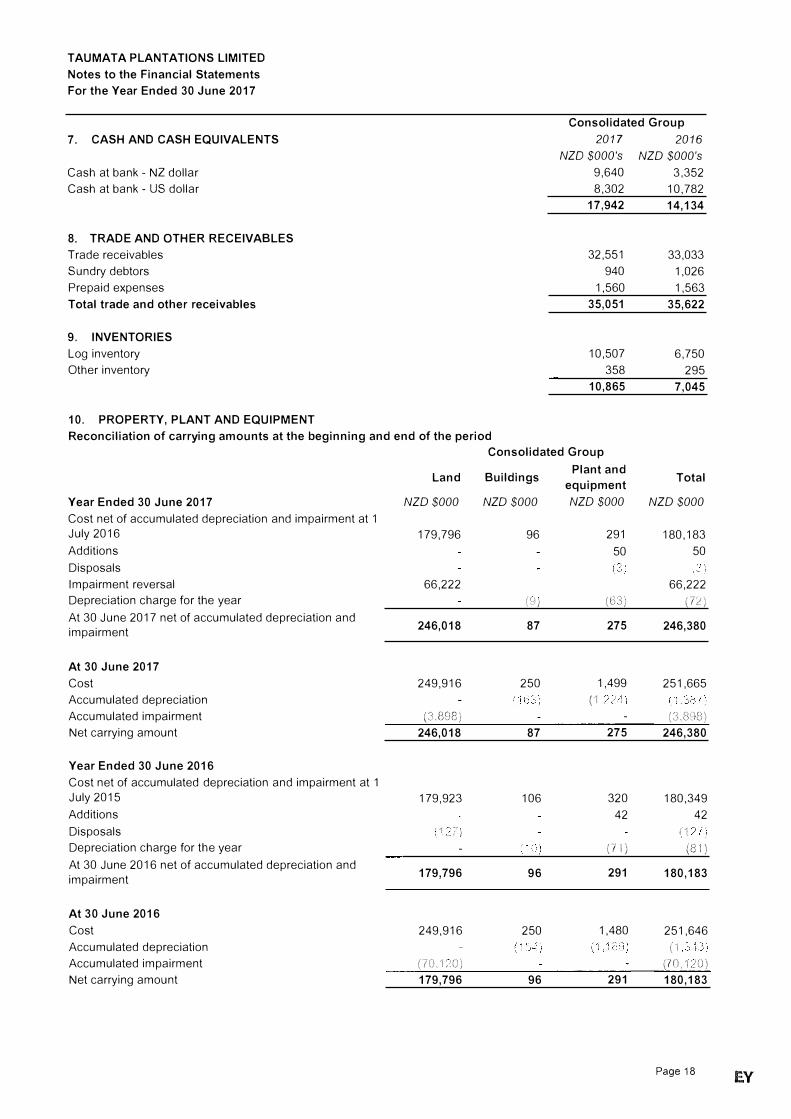

7. CASH AND CASH EQUIVALENTS

Cash at bank - NZ dollar

Cash at bank - US dollar

8. TRADE AND OTHER RECEIVABLES

Trade receivables

Sundry debtors

Prepaid expenses

Total trade and other receivables

9. INVENTORIES

Log inventory

Other inventory

10. PROPERTY, PLANT AND EQUIPMENT

Reconciliation of carrying amounts at the beginning and end of the period

Consolidated Group

2017 2016

NZO $000's NZD $000's

9,640 3,352

8,302 10,782

17,942 14,134

32,551 33,033

940 1,026

1,560 1,563

35,051 35,622

10,507 6,750

358 295

10,865 7,045

Consolidated Group

Year Ended 30 June 2017

Cost net of accumulated depreciation and impairment at 1

July2016

Additions

Disposals

Impairment reversal

Depreciation charge for the year

At 30 June 2017 net of accumulated depreciation and

impairment

At 30 June 2017

Cost

Accumulated depreciation

Accumulated impairment

Net carrying amount

Year Ended 30 June 2016

Cost net of accumulated depreciation and impairment at 1

July 2015

Additions

Disposals

Depreciation charge for the year

At 30 June 2016 net of accumulated depreciation and

impairment

At 30 June 2016

Cost

Accumulated depreciation

Accumulated impairment

Net carrying amount

Land Buildings

NZD $000 NZD $000

179,796 96

66,222

u�i)

246,018 87

249,916 250

(3J�Df3) 246,018 87

179,923 106

'1 1 i

179,796 96

249,916 250

("/0,·1:,::CJ)

179,796 96

Plant and Total

equipment

NZD $000 NZD $000

291 180,183

50 50

66,222

(l33) (l::!)

275 246,380

1,499 251,665

( 1

(3,US1E;)

275 246,380

320 180,349

42 42

{'i'

(11) (8"1)

291 180,183

1,480 251,646 t·\ \ \

(?0,L2U)

291 180,183

Page 18 E.Y

TAUMATA PLANTATIONS LIMITED

Notes to the Financial Statements

For the Year Ended 30 June 2017

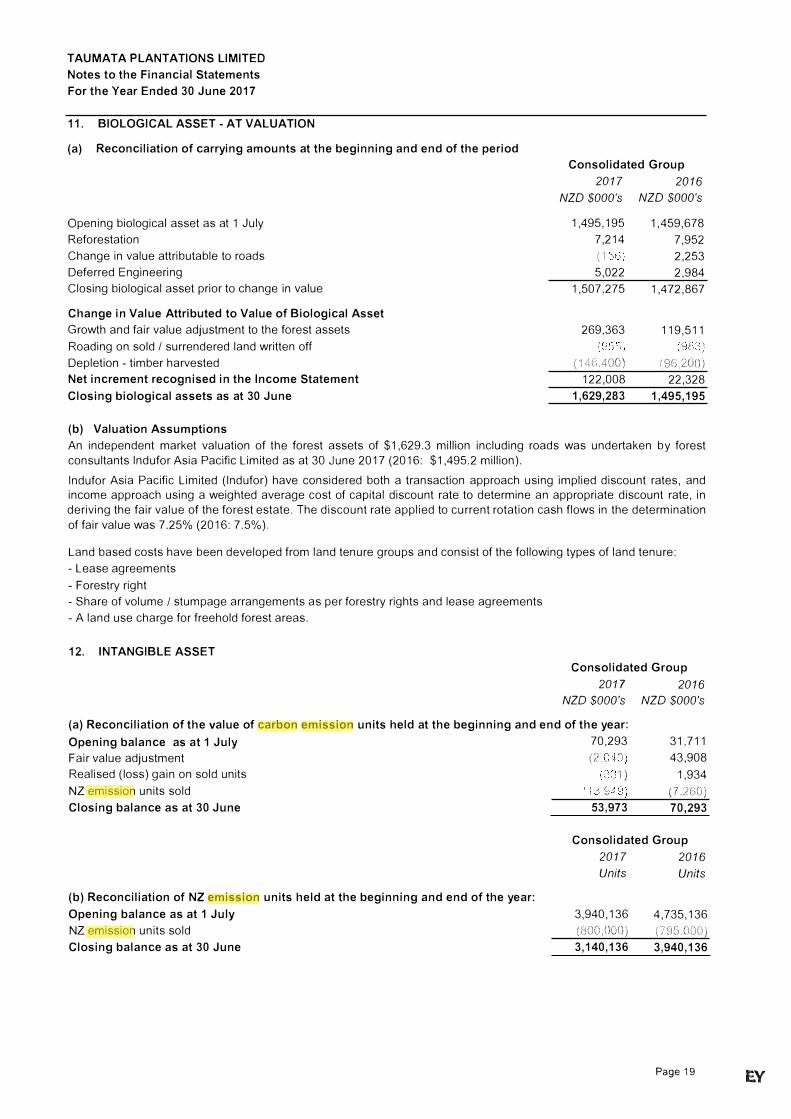

11. BIOLOGICAL ASSET - AT VALUATION

(a) Reconciliation of carrying amounts at the beginning and end of the period

Opening biological asset as at 1 July

Reforestation

Change in value attributable to roads

Deferred Engineering

Closing biological asset prior to change in value

Change in Value Attributed to Value of Biological Asset

Growth and fair value adjustment to the forest assets

Roading on sold / surrendered land written off

Depletion - timber harvested

Net increment recognised in the Income Statement

Closing biological assets as at 30 June

(b) Valuation Assumptions

Consolidated Group

2017 2016

NZD $000's NZD $000's

1,495,195 1,459,678

7,214 7,952 I' \ I 2,253

5,022 2,984

1,507,275 1,472,867

269,363 119,511

(f l{(),400) (�)6,200)

122,008 22,328

1,629,283 1,495,195

An independent market valuation of the forest assets of $1,629.3 million including roads was undertaken by forestconsultants lndufor Asia Pacific Limited as at 30 June 2017 (2016: $1,495.2 million).

lndufor Asia Pacific Limited (lndufor) have considered both a transaction approach using implied discount rates, and income approach using a weighted average cost of capital discount rate to determine an appropriate discount rate, in deriving the fair value of the forest estate. The discount rate applied to current rotation cash flows in the determination

of fair value was 7.25% (2016: 7.5%).

Land based costs have been developed from land tenure groups and consist of the following types of land tenure:

- Lease agreements

- Forestry right

- Share of volume I stumpage arrangements as per forestry rights and lease agreements

- A land use charge for freehold forest areas.

12. INTANGIBLE ASSET

Consolidated Group

2017 2016

NZD $000's NZD $000's

(a) Reconciliation of the value of carbon emission units held at the beginning and end of the year:

Opening balance as at 1 July 70,293 31,711

Fair value adjustment 12 43,908

Realised (loss) gain on sold units 1) 1,934

NZ emission units sold

Closing balance as at 30 June

(b) Reconciliation of NZ emission units held at the beginning and end of the year:

Opening balance as at 1 July

NZ emission units sold

Closing balance as at 30 June

(7.:2CO;

53,973 70,293

Consolidated Group

2017 2016

Units Units

3,940,136

UJ00,000)

3,140,136

4,735,136

(79().000)

3,940,136

Page 19 E.Y

TAUMATA PLANTATIONS LIMITED

Notes to the Financial Statements

For the Year Ended 30 June 2017

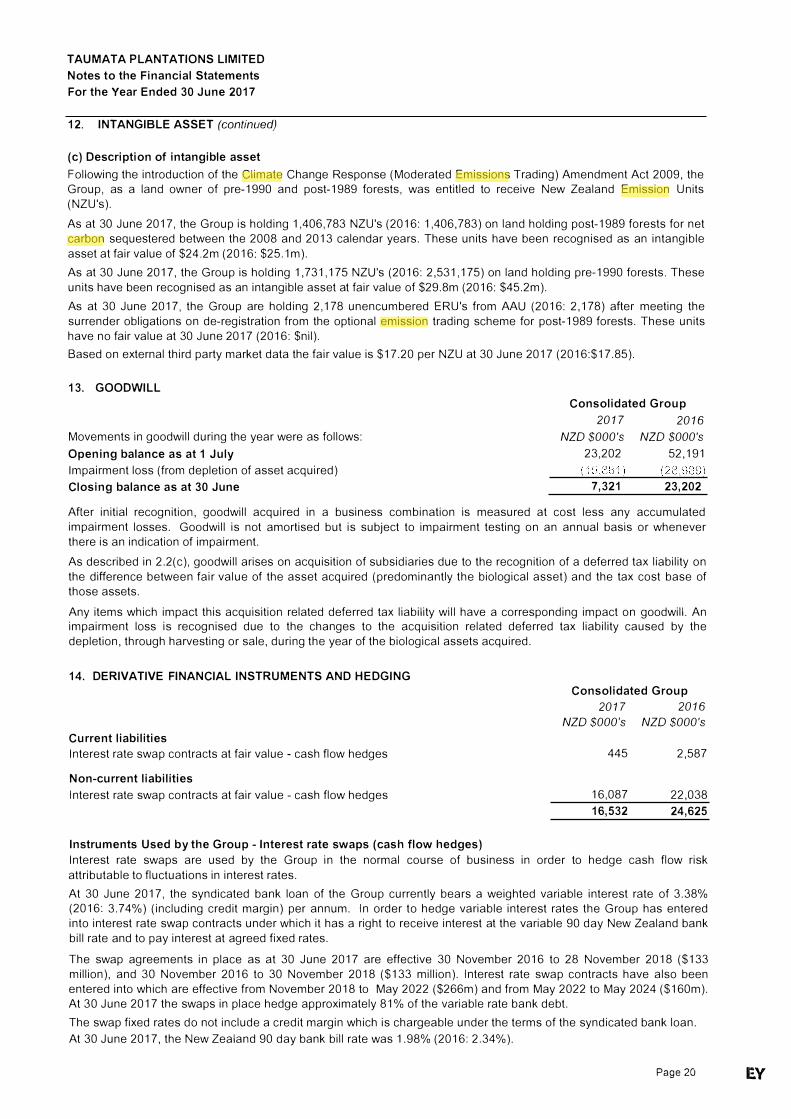

12. INTANGIBLE ASSET (continued)

(c) Description of intangible asset

Following the introduction of the Climate Change Response (Moderated Emissions Trading) Amendment Act 2009, theGroup, as a land owner of pre-1990 and post-1989 forests, was entitled to receive New Zealand Emission Units

(NZU's).

As at 30 June 2017, the Group is holding 1,406,783 NZU's (2016: 1,406,783) on land holding post-1989 forests for net carbon sequestered between the 2008 and 2013 calendar years. These units have been recognised as an intangible

asset at fair value of $24.2m (2016: $25.1 m).

As at 30 June 2017, the Group is holding 1,731,175 NZU's (2016: 2,531,175) on land holding pre-1990 forests. These

units have been recognised as an intangible asset at fair value of $29.8m (2016: $45.2m).

As at 30 June 2017, the Group are holding 2,178 unencumbered ERU's from AAU (2016: 2,178) after meeting the

surrender obligations on de-registration from the optional emission trading scheme for post-1989 forests. These units

have no fair value at 30 June 2017 (2016: $nil).

Based on external third party market data the fair value is $17 .20 per NZU at 30 June 2017 (2016:$17.85).

13. GOODWILL

Movements in goodwill during the year were as follows:

Opening balance as at 1 July

Impairment loss (from depletion of asset acquired)

Closing balance as at 30 June

Consolidated Group

2017 2016

NZO $000's NZO $000's

23,202 52,191

7,321 23,202

After initial recognition, goodwill acquired in a business combination is measured at cost less any accumulated impairment losses. Goodwill is not amortised but is subject to impairment testing on an annual basis or whenever there is an indication of impairment.

As described in 2.2(c), goodwill arises on acquisition of subsidiaries due to the recognition of a deferred tax liability on

the difference between fair value of the asset acquired (predominantly the biological asset) and the tax cost base of

those assets.

Any items which impact this acquisition related deferred tax liability will have a corresponding impact on goodwill. An impairment loss is recognised due to the changes to the acquisition related deferred tax liability caused by the

depletion, through harvesting or sale, during the year of the biological assets acquired.

14. DERIVATIVE FINANCIAL INSTRUMENTS AND HEDGING

Current liabilities

Interest rate swap contracts at fair value - cash flow hedges

Non-current liabilities

Interest rate swap contracts at fair value - cash flow hedges

Instruments Used by the Group - Interest rate swaps (cash flow hedges)

Consolidated Group

2017 2016

NZO $000's NZO $000's

445 2,587

16,087 22,038

16,532 24,625

Interest rate swaps are used by the Group in the normal course of business in order to hedge cash flow risk

attributable to fluctuations in interest rates.

At 30 June 2017, the syndicated bank loan of the Group currently bears a weighted variable interest rate of 3.38% (2016: 3.74%) (including credit margin) per annum. In order to hedge variable interest rates the Group has entered into interest rate swap contracts under which it has a right to receive interest at the variable 90 day New Zealand bank

bill rate and to pay interest at agreed fixed rates.

The swap agreements in place as at 30 June 2017 are effective 30 November 2016 to 28 November 2018 ($133

million), and 30 November 2016 to 30 November 2018 ($133 million). Interest rate swap contracts have also been

entered into which are effective from November 2018 to May 2022 ($266m) and from May 2022 to May 2024 ($160m). At 30 June 2017 the swaps in place hedge approximately 81 % of the variable rate bank debt.

The swap fixed rates do not include a credit margin which is chargeable under the terms of the syndicated bank loan.

At 30 June 2017, the New Zealand 90 day bank bill rate was 1.98% (2016: 2.34%).

Page 20 EV

TAUMATA PLANTATIONS LIMITED

Notes to the Financial Statements

For the Year Ended 30 June 2017

14. DERIVATIVE FINANCIAL INSTRUMENTS AND HEDGING (continued)

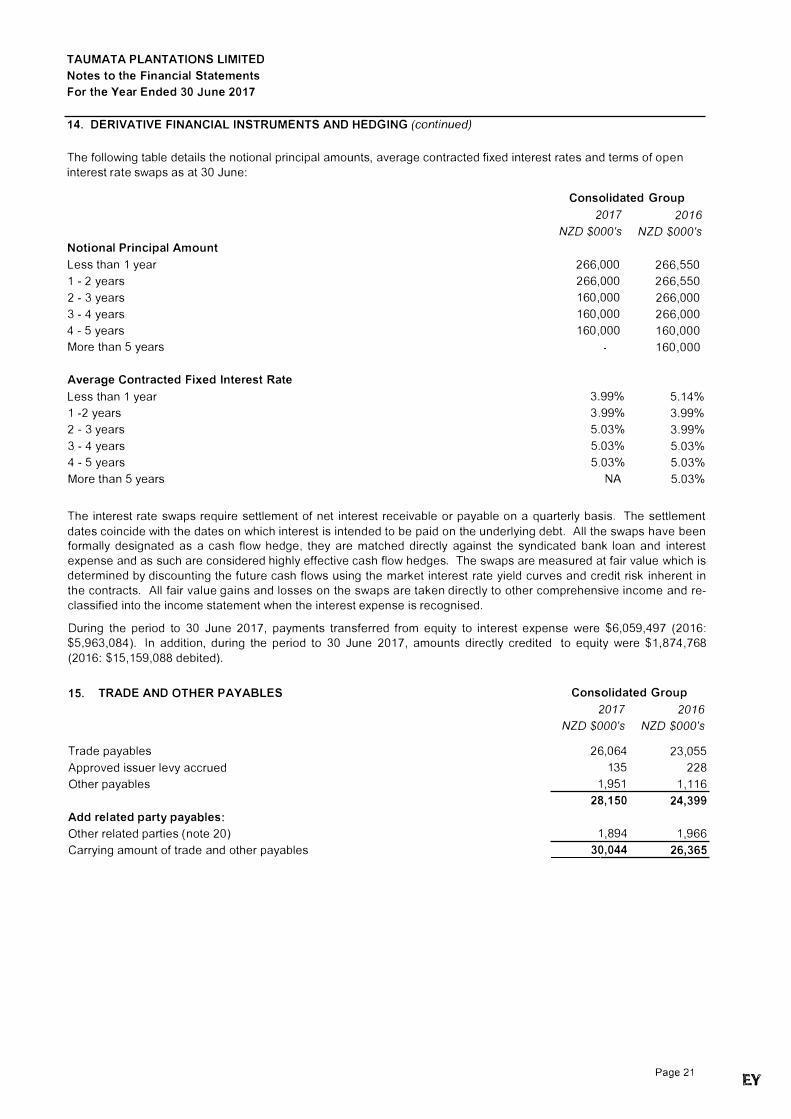

The following table details the notional principal amounts, average contracted fixed interest rates and terms of open interest rate swaps as at 30 June:

Notional Principal Amount

Less than 1 year

1 - 2 years

2 - 3 years

3 - 4 years

4 - 5 years

More than 5 years

Average Contracted Fixed Interest Rate

Less than 1 year

1 -2 years

2 - 3 years

3 - 4 years

4 - 5 years

More than 5 years

Consolidated Group

2017 2016

NZD $000's NZD $000's

266,000 266,550

266,000 266,550

160,000 266,000

160,000 266,000

160,000 160,000

160,000

3.99% 5.14%

3.99% 3.99%

5.03% 3.99%

5.03% 5.03%

5.03% 5.03%

NA 5.03%

The interest rate swaps require settlement of net interest receivable or payable on a quarterly basis. The settlement

dates coincide with the dates on which interest is intended to be paid on the underlying debt. All the swaps have been formally designated as a cash flow hedge, they are matched directly against the syndicated bank loan and interest expense and as such are considered highly effective cash flow hedges. The swaps are measured at fair value which is determined by discounting the future cash flows using the market interest rate yield curves and credit risk inherent in the contracts. All fair value gains and losses on the swaps are taken directly to other comprehensive income and reclassified into the income statement when the interest expense is recognised.

During the period to 30 June 2017, payments transferred from equity to interest expense were $6,059,497 (2016: $5,963,084). In addition, during the period to 30 June 2017, amounts directly credited to equity were $1,874,768

(2016: $15,159,088 debited).

15. TRADE AND OTHER PAYABLES

Trade payables

Approved issuer levy accrued

Other payables

Add related party payables:

Other related parties (note 20)

Carrying amount of trade and other payables

Consolidated Group

2017 2016

NZD $000's NZD $000's

26,064 23,055

135 228

1,951 1,116

28,150 24,399

1,894 1,966

30,044 26,365

Page 21 EV

TAUMATA PLANTATIONS LIMITED

Notes to the Financial Statements

For the Year Ended 30 June 2017

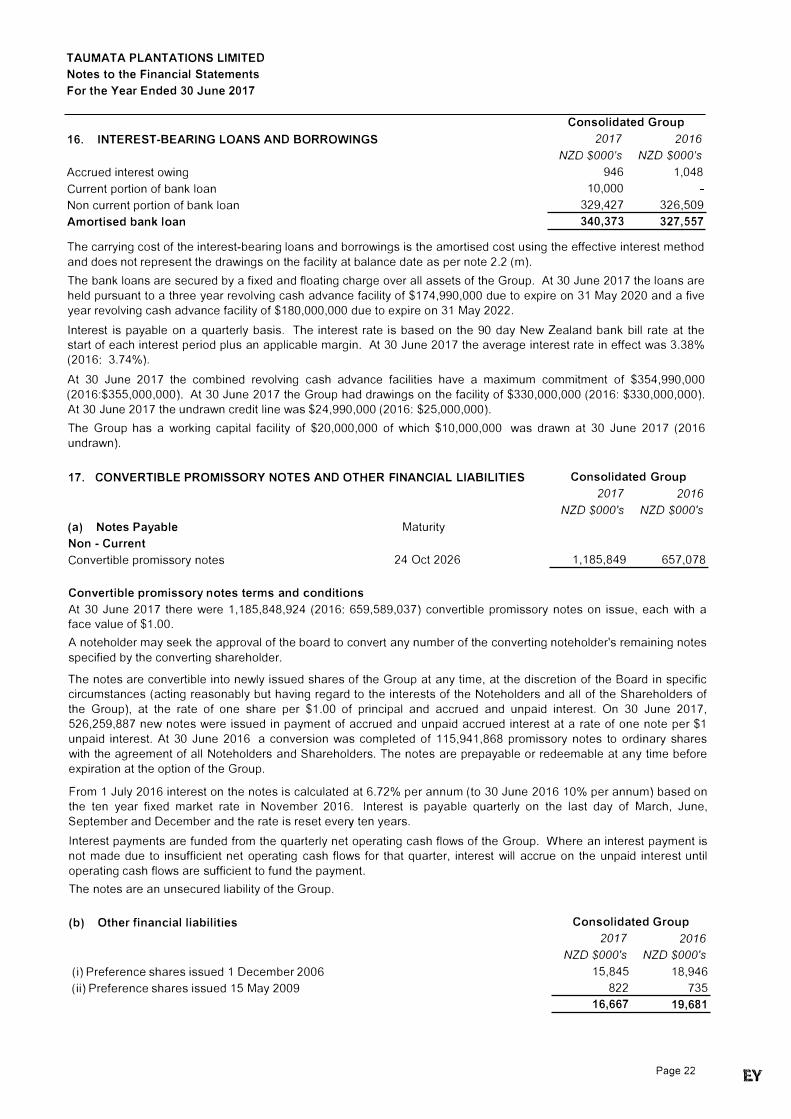

16. INTEREST-BEARING LOANS AND BORROWINGS

Accrued interest owing

Current portion of bank loan

Non current portion of bank loan

Amortised bank loan

Consolidated Group

2017 2016

NZD $000's NZO $000's

946 1,048

10,000

329,427 326,509

340,373 327,557

The carrying cost of the interest-bearing loans and borrowings is the amortised cost using the effective interest method

and does not represent the drawings on the facility at balance date as per note 2.2 (m).

The bank loans are secured by a fixed and floating charge over all assets of the Group. At 30 June 2017 the loans are

held pursuant to a three year revolving cash advance facility of $174,990,000 due to expire on 31 May 2020 and a five

year revolving cash advance facility of $180,000,000 due to expire on 31 May 2022.

Interest is payable on a quarterly basis. The interest rate is based on the 90 day New Zealand bank bill rate at the start of each interest period plus an applicable margin. At 30 June 2017 the average interest rate in effect was 3.38% (2016: 3.74%).

At 30 June 2017 the combined revolving cash advance facilities have a maximum commitment of $354,990,000

(2016:$355,000,000). At 30 June 2017 the Group had drawings on the facility of $330,000,000 (2016: $330,000,000).

At 30 June 2017 the undrawn credit line was $24,990,000 (2016: $25,000,000).

The Group has a working capital facility of $20,000,000 of which $10,000,000 was drawn at 30 June 2017 (2016

undrawn).

17. CONVERTIBLE PROMISSORY NOTES AND OTHER FINANCIAL LIABILITIES

(a) Notes Payable

Non - Current

Convertible promissory notes

Convertible promissory notes terms and conditions

Maturity

24 Oct 2026

Consolidated Group

2017 2016

NZO $000's NZO $000's

1,185,849 657,078

At 30 June 2017 there were 1,185,848,924 (2016: 659,589,037) convertible promissory notes on issue, each with a face value of $1.00.

A noteholder may seek the approval of the board to convert any number of the converting noteholder's remaining notes

specified by the converting shareholder.

The notes are convertible into newly issued shares of the Group at any time, at the discretion of the Board in specific circumstances (acting reasonably but having regard to the interests of the Noteholders and all of the Shareholders of

the Group), at the rate of one share per $1.00 of principal and accrued and unpaid interest. On 30 June 2017, 526,259,887 new notes were issued in payment of accrued and unpaid accrued interest at a rate of one note per $1

unpaid interest. At 30 June 2016 a conversion was completed of 115,941,868 promissory notes to ordinary shares

with the agreement of all Noteholders and Shareholders. The notes are prepayable or redeemable at any time before

expiration at the option of the Group.

From 1 July 2016 interest on the notes is calculated at 6.72% per annum (to 30 June 2016 10% per annum) based on the ten year fixed market rate in November 2016. Interest is payable quarterly on the last day of March, June,

September and December and the rate is reset every ten years.

Interest payments are funded from the quarterly net operating cash flows of the Group. Where an interest payment is not made due to insufficient net operating cash flows for that quarter, interest will accrue on the unpaid interest until

operating cash flows are sufficient to fund the payment.

The notes are an unsecured liability of the Group.

(b) Other financial liabilities

(i) Preference shares issued 1 December 2006

(ii) Preference shares issued 15 May 2009

Consolidated Group

2017 2016

NZO $000's NZO $000's

15,845

822

16,667

18,946

735

19,681

Page 22 EV

TAUMATA PLANTATIONS LIMITED

Notes to the Financial Statements

For the Year Ended 30 June 2017

17. CONVERTIBLE PROMISSORY NOTES AND OTHER FINANCIAL LIABILITIES (continued)

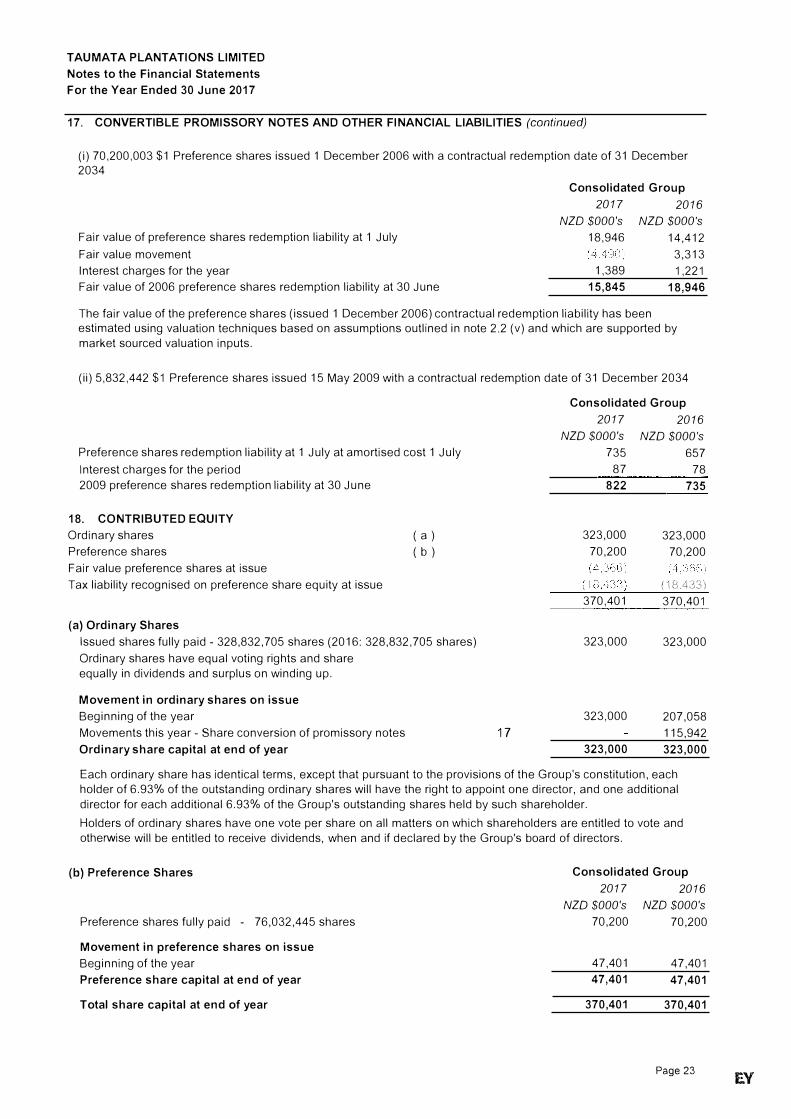

(i) 70,200,003 $1 Preference shares issued 1 December 2006 with a contractual redemption date of 31 December2034

Fair value of preference shares redemption liability at 1 July

Fair value movement

Interest charges for the year

Fair value of 2006 preference shares redemption liability at 30 June

Consolidated Group

2017 2016

NZD $000's NZO $000's

18,946

1,389

15,845

14,412

3,313

1,221

18,946

The fair value of the preference shares (issued 1 December 2006) contractual redemption liability has been estimated using valuation techniques based on assumptions outlined in note 2.2 (v) and which are supported by

market sourced valuation inputs.

(ii) 5,832,442 $1 Preference shares issued 15 May 2009 with a contractual redemption date of 31 December 2034

Preference shares redemption liability at 1 July at amortised cost 1 July

Interest charges for the period

2009 preference shares redemption liability at 30 June

18. CONTRIBUTED EQUITY

Ordinary shares

Preference shares

Fair value preference shares at issue

Tax liability recognised on preference share equity at issue

(a) Ordinary Shares

( a )

( b )

Issued shares fully paid - 328,832,705 shares (2016: 328,832,705 shares)

Ordinary shares have equal voting rights and share

equally in dividends and surplus on winding up.

Movement in ordinary shares on issue

Beginning of the year

Movements this year - Share conversion of promissory notes

Ordinary share capital at end of year

17

Consolidated Group

2017

NZO $000's

735

87

822

323,000

70,200

370,401

323,000

323,000

323,000

2016

NZO $000's

657

78

735

323,000

70,200

('le.4:\3'}

370,401

323,000

207,058

115,942

323,000

Each ordinary share has identical terms, except that pursuant to the provisions of the Group's constitution, each

holder of 6.93% of the outstanding ordinary shares will have the right to appoint one director, and one additional

director for each additional 6.93% of the Group's outstanding shares held by such shareholder.

Holders of ordinary shares have one vote per share on all matters on which shareholders are entitled to vote and

otherwise will be entitled to receive dividends, when and if declared by the Group's board of directors.

(b) Preference Shares

Preference shares fully paid - 76,032,445 shares

Movement in preference shares on issue

Beginning of the year

Preference share capital at end of year

Total share capital at end of year

Consolidated Group

2017 2016

NZO $000's NZD $000's

70,200 70,200

47,401 47,401

47,401 47,401

370,401 370,401

Page 23 EV

TAUMATA PLANTATIONS LIMITED

Notes to the Financial Statements

For the Year Ended 30 June 2017

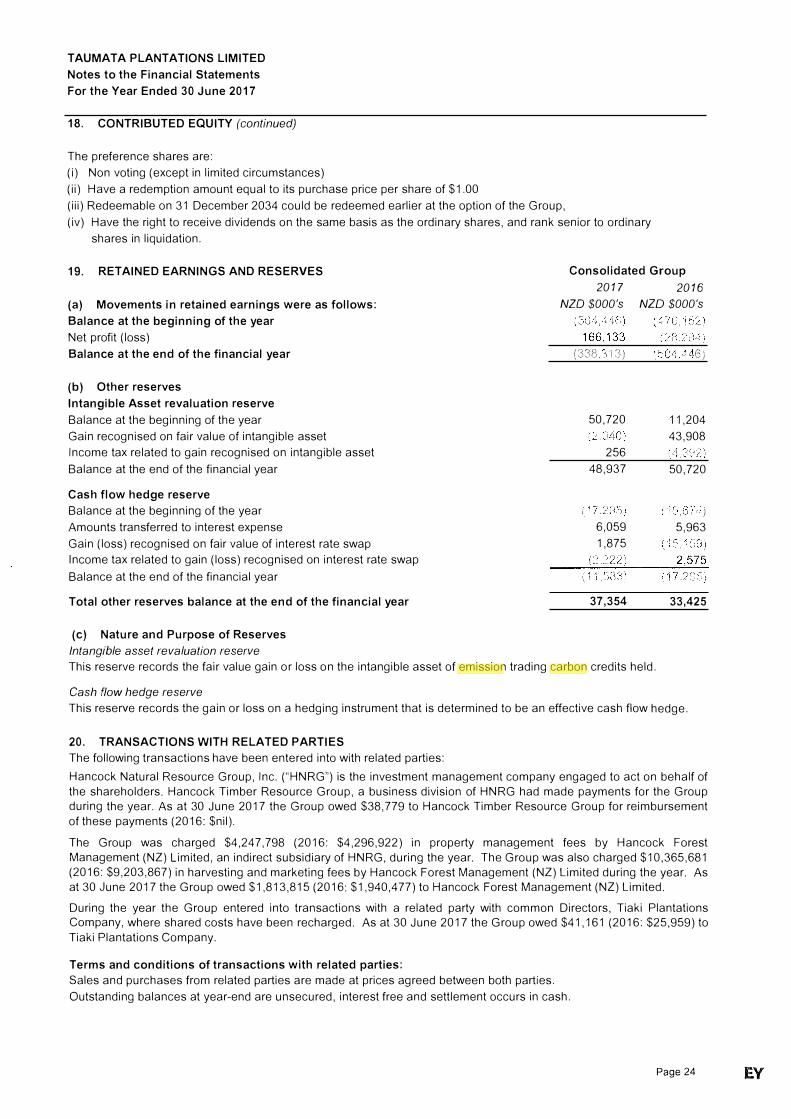

18. CONTRIBUTED EQUITY (continued)

The preference shares are:

(i) Non voting (except in limited circumstances)

(ii) Have a redemption amount equal to its purchase price per share of $1.00

(iii) Redeemable on 31 December 2034 could be redeemed earlier at the option of the Group,

(iv) Have the right to receive dividends on the same basis as the ordinary shares, and rank senior to ordinary

shares in liquidation.

19. RETAINED EARNINGS AND RESERVES Consolidated Group

2017 2016

(a) Movements in retained earnings were as follows: NZD $000's NZD $000's

Balance at the beginning of the year

Net profit (loss)

Balance at the end of the financial year

(b) Other reserves

Intangible Asset revaluation reserve

Balance at the beginning of the year

Gain recognised on fair value of intangible asset

Income tax related to gain recognised on intangible asset

Balance at the end of the financial year

Cash flow hedge reserve

Balance at the beginning of the year

Amounts transferred to interest expense

Gain (loss) recognised on fair value of interest rate swap

Income tax related to gain (loss) recognised on interest rate swap

Balance at the end of the financial year

Total other reserves balance at the end of the financial year

(c) Nature and Purpose of Reserves

Intangible asset revaluation reserve

(338 '13)

50,720

256

48,937

6,059

1,875

37,354

This reserve records the fair value gain or loss on the intangible asset of emission trading carbon credits held.

Cash flow hedge reserve

r.o, UJ

11,204

43,908

50,720

) 5,963

33,425

This reserve records the gain or loss on a hedging instrument that is determined to be an effective cash flow hedge.

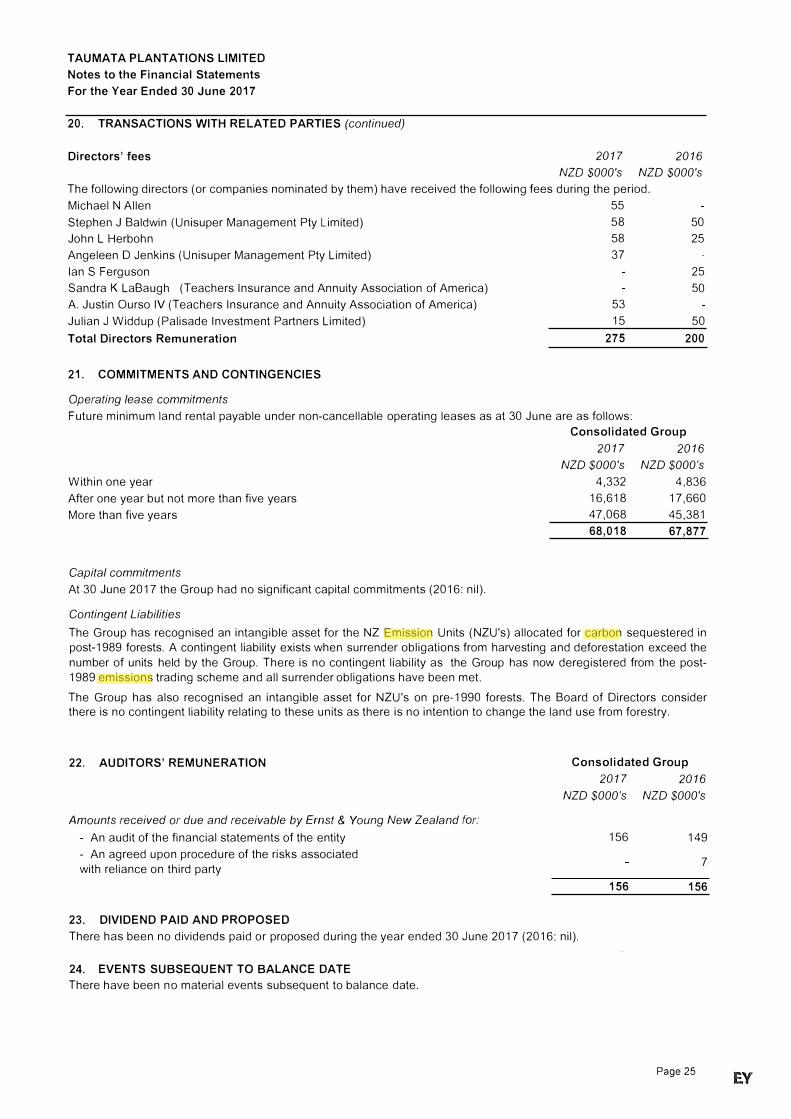

20. TRANSACTIONS WITH RELATED PARTIES

The following transactions have been entered into with related parties:

Hancock Natural Resource Group, Inc. ("HNRG") is the investment management company engaged to act on behalf of