7/27/2019 Analyzing the current incorporation of social, environmental nd economic measures into business strategic perfor…

http://slidepdf.com/reader/full/analyzing-the-current-incorporation-of-social-environmental-nd-economic-measures 1/12

WORLD ACADEMIC JOURNAL OF BUSINESS & APPLIED SCIENCES-MARCH-SEPTEMBER 2013 EDITION

49

Analyzing the current incorporation of social, environmental

and economic measures into business strategic performance

measurement systems: the case of Enterprises operating in

Shanghai

Jing Zhou (Corresponding author)

Fudan University, School of ManagementStarr Building 670 Guoshun Road, Shanghai, P.O Box 200433 China

E-mail: [email protected]

Li Xu

Fudan University, School of ManagementStarr Building 670 Guoshun Road, Shanghai, P.O Box 200433 China

E-mail:[email protected]

Accepted 4 March 2013

Abstract:

We theorize about the incorporation of social, environmental and economic dimensions into strategic

performance measurement systems .81Chinese companies were surveyed for the analysis. Along withthe increasing of social responsibility pressure, numbers of enterprises are promoting environmental,

social and economic performance as strategic sustainability measures. Although the addition of

sustainability measures to enterprise’s long term business strategy has long time been a major preoccupation of literature. Some empirical researches have examined if these nonfinancial measures

are effectively incorporated into strategic performance measurement systems. In this research, we will

examine why the incorporation of sustainability measures into enterprise business strategy vary across

enterprises operating in Shanghai.

Keywords: Sustainability measures, Shanghai enterprises, Enterprise strategic performance

measurement systems.

1. IntroductionThe beginning of 21th century observed unprecedented important changes in enterprise long term

strategy and management towards sustainable concerns, the incorporation of sustainability measures

as enterprise strategy, and adopting sustainability as entire part of an enterprise’s business strategy inorder to obtain important benefits (Epstein 2008).This tendency has been confirmed by S.Gates and C.Germain(2010)who demonstrated that number of enterprises are developing new strategy

approaches in relationship with attempts to incorporate sustainability measures into business strategies

such as the balanced scorecard (BSC).According to Marcus Wagner, Tobias Hahn ,Frank Figge ,StefanSchaltegger (2001) social, environmental, and economic performance have become increasingly

important for business. To the level that environmental, social and economic problems are shown inthe transactions of markets, many enterprises have implemented environmental, social and economic

management strategies during the last ten years. These strategies have rarely been incorporated with

International Journal of Business & Management MARCH 2013 VOL.1, No,1

7/27/2019 Analyzing the current incorporation of social, environmental nd economic measures into business strategic perfor…

http://slidepdf.com/reader/full/analyzing-the-current-incorporation-of-social-environmental-nd-economic-measures 2/12

WORLD ACADEMIC JOURNAL OF BUSINESS & APPLIED SCIENCES-MARCH-SEPTEMBER 2013 EDITION

50

the general management strategy of an enterprise. The role of enterprises in achieving sustainability

has been discussed both on instrumental ( Bennett & James, 1999) and strategic level ( Roome,

1998) .If enterprises are to achieve at the same time improvements of the environmental ,social and

economic performance of businesses , this lack of integration turns out to be a major obstruction. TheGlobal Reporting Initiative (GRI) that is“a network-based organization that pioneered the world’s

most widely used sustainability reporting framework ”, shows that environmental, social and economic

performance (sustainability measures) are evolving in some of Asian countries such as China. And number of these countries is incorporating sustainability measures in enterprises long term

performance strategies (OECD-DAC, 2011).Some empirical studies have examined if sustainability

measures are integrated into enterprises performance measurement systems which are crucial for the

implementation of business strategy.

This paper has two main objectives. The first objective is to investigate to what degree Enterpriseoperating in Shanghai (China) incorporate sustainability measures in their performance measurement

systems (PMS) and align them with long term business strategy. The second objective is to evaluate

the determinants which explain why these practices vary across these enterprises.

2. Literature review

2.1 Strategic performance measurement systemStrategic performance measurement system determines both the scope and focus of management

accounting. Particularly the requisite is that practice of management accounting should reflect the

choices of strategies made in enterprises for management accounting to be consistent. The process of SPMS has four important steps. Identifying:

1. The enterprise’s primary goals ( as established by its owners)

2. The role the enterprise’s stakeholders play as the enterprise pursues its primary objectives3. The requirements of each stakeholder in exchange for pursuing its role in supporting the enterprise’s

strategy.4. How to evaluate the enterprises objectives and stakeholder roles.

The process of PMS starts with the specification of enterprises primary objectives. In

profit-seeking enterprises, the primary objectives are financialIn not-for-profit enterprises the primary objectives reflect the objectives of the enterprise’s

membersFor the purpose of strategic performance measurement the enterprise’s objective can be mainly

financial, social, or a mix of both social and financial objectives. But, if there are primary objectives

that can conflict, the enterprises planners should identify rules that instruct how decision-makersshould make trade-offs among the objectives (Anthony A. Atkinson, 1998)

Finally, Strategic performance measurement systems have three characteristics in common:

1. They integrate financial measures that capture the short-term consequences of managers’ decisionsregarding asset utilization, revenue growth and cash flows problems (Kaplan & Norton, 2001a)

2. They enhance financial measures with nonfinancial measures (that indicate operational

achievements likely to drive future financial performance);

3. They are created to achieve multiple objectives (cost determination and value creation)

2.2 Enterprise Social Responsibility (ESR) and SustainabilityThe concept of ESR has been first developed by Bowen (1953). In this research, we define ESR

as a complete set of programs, practices and policies that are incorporated into specific business

operations, decision-making and supply chains processes throughout an enterprise, aiming to instruct

responsibility for past and actual actions as well as future influences (Business for SocialResponsibility, 2008). The Brundtland Commission report (1987) defines the ESR as “meeting current

needs without compromising the capacity of future generations to meet their own needs”. A

sustainable corporate contributes to sustainability by bringing social economic and environmental

benefits simultaneously (by achieving the triple bottom line) (Dyllick & Hockerts, 2002). Enterprises

have been developing new policies and strategies and redelimiting their action domains, roles, and

interdependency (Van Marrewijk, M. & Hardjono, T.2003).

ESR and sustainability have gradually converged and nowadays they include similar aspects and

are often utilized as comparable terms (Mazon, 2004).

7/27/2019 Analyzing the current incorporation of social, environmental nd economic measures into business strategic perfor…

http://slidepdf.com/reader/full/analyzing-the-current-incorporation-of-social-environmental-nd-economic-measures 3/12

WORLD ACADEMIC JOURNAL OF BUSINESS & APPLIED SCIENCES-MARCH-SEPTEMBER 2013 EDITION

51

First, both ESR and sustainability concepts include different levels of analysis and different

stakeholders (suppliers, clients, community members, shareholders, employees, partners.). Secondly,

these concepts deal with problems related to environmental, social, and economic. The economic

dimension is not centralized to short-term performance indicators (return on investment), but alsorefers to aspects that contribute to long-term financial success (enterprise’s reputation and

relationships).

Managing ESR and sustainability implies seeking equilibrium between long and short-termfactors, and among the interests of a larger group of stakeholders than those applied by traditional

management (Raynard and Forstarter, 2002).ESR and sustainability have come represent an important

aspect of enterprise strategy, with an increasing number of enterprises trying to monitor, improve and

determine the environmental and social influences of their activities. Despite such interest, effective

integration of sustainability into performance measurement systems and management faces manyobstacles, raising the need for new research.

2.3 The triple bottom lineAfter the World Commission on Environment and Development (WCED), many definitions of

sustainability have been made and this concept has been interpreted in different ways. Most of these

definitions are based upon the concept of triple bottom line (or three-pillar): social, environment and economy (P., J., Annandale, D. and Morrison-Saunders, A., 2004). According to the Portland state

university (2011) “The triple bottom line term is a phrase that originated in the corporate sector as a

way to think about the social, environmental and economic, value that is added (or destroyed) by aninvestment”. In others words the meaning behind the “three pillar” is that the health and success of an

enterprise not only can be estimated by the economical dimension but also is influenced by social and

environmental determinants. Triple bottom line model has been developed by Elkington,J.,(1998).Nowadays number of business companies are implementing this model in their business

strategy, and utilizing the terminology in their annual press releases. According to Russel (2008) anactive sustainability policy can be advantageous for an enterprise in terms of image and the way the

enterprise is profiled in a market.

Enterprises developed a need for a model that could help them to integrate the sustainability in their business in a way that was beneficial in according to the triple bottom line.

2.4 Incorporating environmental, social and economic dimensions into strategic PMSEnterprises are progressively inclined to incorporate social and economic dimensions into their

business strategies, to respond to increasing pressure of employees, consumers, and other important

stakeholders and also to examine opportunities for building competitive advantage (Bielak, Bonini, &

Oppenheim, 2007). Management researchers are aiming to identify a set of determinants for

promoting effective incorporation of sustainability into enterprises practices.

Leadership has been recognized as a fundamental alternative, promoting the commitment of enterprise as a whole (Environmental Protection Agency of United States, 2001).

Marrewijk (2004) in his study, describes a set of ideal types of enterprises, and develops a system of

values and associated institutional structures (governance and the role of leadership).

Fineman (1996) debates the role of leadership in the process of change, highlighting that

leadership appears to play an important role in the enterprise adoption of sustainability practices.

Others determinants such as communication and training (institutional mechanisms) have been

recognized as promoters of sustainability initiatives. Stone (2006) demonstrates that, in order to

achieve a high degree of organizational commitment, well-defined training and communication plans

are key determinants in promoting a clear understanding of the role of sustainable practices for enterprise strategy and objectives.

Tregidga and Milne (2006) investigate enterprise reports in order to understanding the development of

the discourse of sustainability. They mainly debate the role of reporting and communication

mechanisms in creating enterprise sustainability initiatives.

Bansal (2003) affirms that organizational commitment to sustainability is promoted when top

management buy the concept (but also when lower organizational levels engage in sustainability)Henriques and Sadorsky (1999) link perception of management of stakeholders' pressures with more

proactive undertakings towards environmental commitment.

7/27/2019 Analyzing the current incorporation of social, environmental nd economic measures into business strategic perfor…

http://slidepdf.com/reader/full/analyzing-the-current-incorporation-of-social-environmental-nd-economic-measures 4/12

WORLD ACADEMIC JOURNAL OF BUSINESS & APPLIED SCIENCES-MARCH-SEPTEMBER 2013 EDITION

52

Sharma and Henrique (2005) suggest an analysis associating different types of stakeholder

influence strategies with different sustainability practices adopted by enterprises.

The literature review proposes that even if researchers are aiming to identify and understand the

factors that might influence the incorporation of sustainability by enterprise. Few studies havesuggested a more centralized view of these factors. Basu and Palazzo (2008)’s article is one of the rare

articles that consider internal and external impacts, suggesting a group of cognitive, linguistic and

conative aspects in order to identify an enterprise’s intrinsic orientation toward the choice of ESR .The cognitive aspect has to do with dimensions including enterprise orientation, identity and

legitimacy, managerial beliefs and values regarding the choice of sustainability (USEPA, 2001). The

linguistic aspect includes organizational modes of justification and is associated to considerations of

transparency and communication (Marrewijk, 2004; Stone, 2006; Tregidga and Milne 2006). The

conative aspects involves the way enterprises tend to operate, including coherence among strategic

policies and levels of commitment (Marrewijk, 2004; Sharma and Henriques, 2005)。

2.5 Performance measurement system and sustainability managementThe Balanced Scorecard (BSC) was created as a new approach to performance measurement

(PMS) because of problems of past orientation and short-termism in corporate management (Figge F,

Hahn T, Schaltegger S, Wagner M., 2001a.). The Balanced Scorecard is found on the assumption that

the efficient utilization of investment capital is not the sole factor for enterprise competitive

advantages, but factors such as intellectual capital, customer orientation, knowledge, become very

important .Norton and Kaplan proposed then a new performance measurement system approachcentered on enterprise strategy in four perspectives(figure1): financial, customer, internal business

processes, and learning and growth (Kaplan and Norton, 2001).

The balanced scorecard’s purpose is to contribute and to transform “soft factors” and intangible

assets into long-term financial success explicit .The balanced scorecard’s four perspectives can be

summarized as follows (Kaplan & Norton, 2001,Weber & Schaffer, 2000)

(1) The financial perspective shows if the transformation of a strategy leads to ameliorated economic

success.

(2) The customer perspective determines the customer or the market segments in which the enterprise

competes.

(3) The internal process perspective defines internal business processes that enable the firm to meetthe customers’ expectations in the target markets.

(4) The learning and growth perspective identifies the infrastructure necessary for the achievement of the objectives of qualification, motivation and goal orientation of employees, and information

systems.

Beside the four perspectives of the balanced Scorecard, a fifth aspect (society) can integrate social and environmental aspects that show nonmarket societal mechanisms (sociocultural mechanism).

Figure 1: Four perspectives to integrate sustainability into the balanced scorecard

Source: Kaplan, R. S. and Norton D. P. (1992, Jan-Feb) ‘The Balanced Scorecard – Measures ThatDrive Performance’, Harvard Business Review, Vol.70, No.1, pp.71-79

Thus the new approach is to create a balanced scorecard devoted to social and environmental

problems that cover the traditional balanced Scorecard. This choice of a balanced scorecard focused on sustainability (social and environmental) is very important for enterprises management departments

that are devoted to social and environmental and issues.There are many possibilities to incorporate sustainability measures into performance

measurement systems, but enterprises’ current practices and the determinants that explain their procedures remain uninvestigated. Sustainability management with the balanced Scorecard aims tofocus on the problem of enterprises contributions to sustainability in a centralized way. It assumes that

for enterprises to contribute to sustainable development, it’s very important that enterprise performance improves simultaneously in social, economic and environmental dimensions (Figge F,

Hahn T, Schaltegger S.,Wagner M., 2001a).

In a balanced scorecard all aspects appropriate for accomplishing a permanent competitiveadvantage should be incorporated. In the four perspectives of the balanced scorecard, therefore, the

enterprise’s activities important for long-term business success are included and causes are connected

7/27/2019 Analyzing the current incorporation of social, environmental nd economic measures into business strategic perfor…

http://slidepdf.com/reader/full/analyzing-the-current-incorporation-of-social-environmental-nd-economic-measures 5/12

WORLD ACADEMIC JOURNAL OF BUSINESS & APPLIED SCIENCES-MARCH-SEPTEMBER 2013 EDITION

53

to effects.

In the formulation of a balanced scorecard all the objectives and measures are estimated from the

long-term strategic financial objectives in a top-down process.This structure of the balanced scorecard ensures that all business activities are associated to the

successful application of the business strategy. This particularity of the balanced scorecard can also be

utilized for the management of social and environmental dimensions. The capacity of the balanced

scorecard to incorporate the three dimensions of sustainability gives the opportunity to integrate the

management of social and environmental dimensions into normal business activities.

The link between the three performance aspects of sustainability (environmental, social and

economic) must be taken into account. Incorporating the three aspects of sustainability into business

management offers three principal advantages (Figge F, Hahn T, Schaltegger S, Wagner M. 2001a):

(1) Sustainability management that is economically sound is not menaced by economic crisis becauseit is not only achieved as long as the enterprise is successful.

(2) Enterprises that want to promote their social and environmental management sometimes direct

themselves towards competitors.

(3) An inclusion of social and environmental and dimensions into business management confirms that

enterprise sustainability management take into account all three aspects of sustainability.

There are three possibilities to incorporate social and environmental dimensions in the balanced scorecard. Firstly, environmental and social dimensions can be incorporated in the current four

perspectives. Secondly, an additional perspective can be added to consider social and environmental

FINANCIAL“To succeed financially,

how should we appear to

our shareholders?”

CUSTOMER“To achieve our vision,

how should we appear

to our customer?”

LEARNING AND

GROWTH“To achieve our vision,

how should we sustain

our ability to change and

improve?”

INTERNAL

BUSINESS PROCESS“To satisfy our

shareholders and

customers, what business

process must we excel?”

VISION AND

STRATEGY

7/27/2019 Analyzing the current incorporation of social, environmental nd economic measures into business strategic perfor…

http://slidepdf.com/reader/full/analyzing-the-current-incorporation-of-social-environmental-nd-economic-measures 6/12

WORLD ACADEMIC JOURNAL OF BUSINESS & APPLIED SCIENCES-MARCH-SEPTEMBER 2013 EDITION

54

dimensions. Third, a particular social and environmental scorecard can be conceived (Deegen T., 2001,

Figge F, Hahn T, Schaltegger S, Wagner M. 2001a).

Environmental and social aspects can be classified under the four current bsc perspectives

(Deegen T., 2001). This signifies that social and environmental dimensions are included in the four perspectives through particular performance drivers for which leading indicators as well as objectives

are conceived (Kaplan and Norton, 2001).

The approach of the incorporation of social and environmental dimensions by classifying them under the four perspectives is very important for social and environmental dimensions that are already

incorporated in the market system.

3 Methodology3.1 Data collection

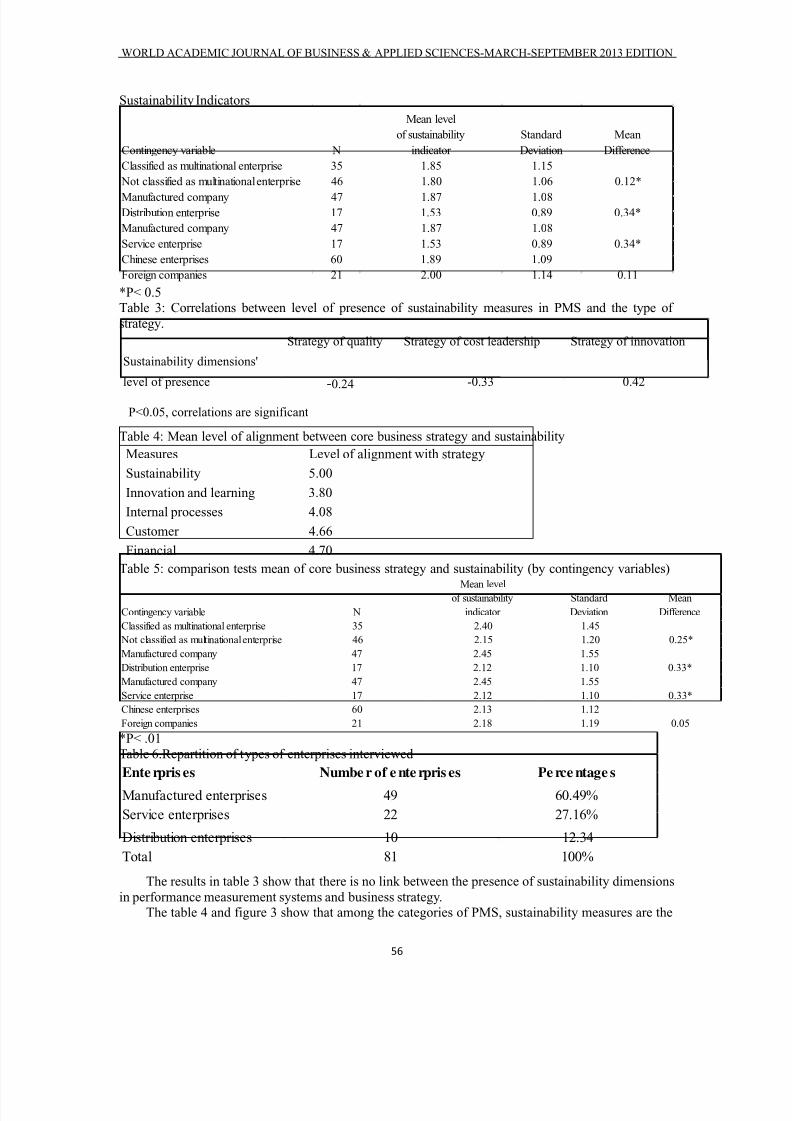

We conducted an empirical study of large enterprises operating in Shanghai. We identified asample of 250 enterprises. But only 81 companies showed interest in the study which represented

32.4% responses. The type of enterprises chosen for the study are: manufactured enterprises, service

enterprises, and distribution enterprises(Table 6,figure 4).We used the strategy of independentcontingency variables(ICV) in the survey instrument developed by Edward J. Garrity, G. Lawrence

Sanders (1998) to assess enterprise strategy. Respondents were asked to rate on a five-point likertscale to what extent they agreed with a number of statements relating to enterprise principal strategic

orientation (Sinkovics, Rudolf R, Roath, Anthony S.,2004,citing Gatignon and Xuereb ,1997 ,define

strategic orientation as the specific approach a firm implements to create superior and continuous performance. Strategic orientation provides a foundation of guidelines upon which to continuously

improve a company's performance).The statistical method we used to determine enterprises strategies

in the overall sample is Factor Analysis(It can be defined as a statistical technique used todescribe variability among observed variables in terms of a potentially lower number of unobserved

variables called factor). We have chosen three dimensions (1.the strategy of product differentiationaccording to service and product quality; 2. strategy according to cost leadership; 3.the strategy of

product differentiation based on innovation) with eigenvalues higher than 1 (3.21, 1.79, and 1.3).And

the percentage of variance explained by each dimension is 32.15%, 17.9%, and 10.30%.The respondents were also asked to indicate the type of business strategy or performance

measurement systems they use to conduct performance, their business sector, and if their enterprise is

classified as multinational company.

We additionally asked them to indicate on a five-point likert scale to what extent they think the

performance measurement system includes both performance and sustainability dimensions (financial

PM, internal processes, innovation and learning, customers, and sustainability).

We used SPSS software for performing data analysis.

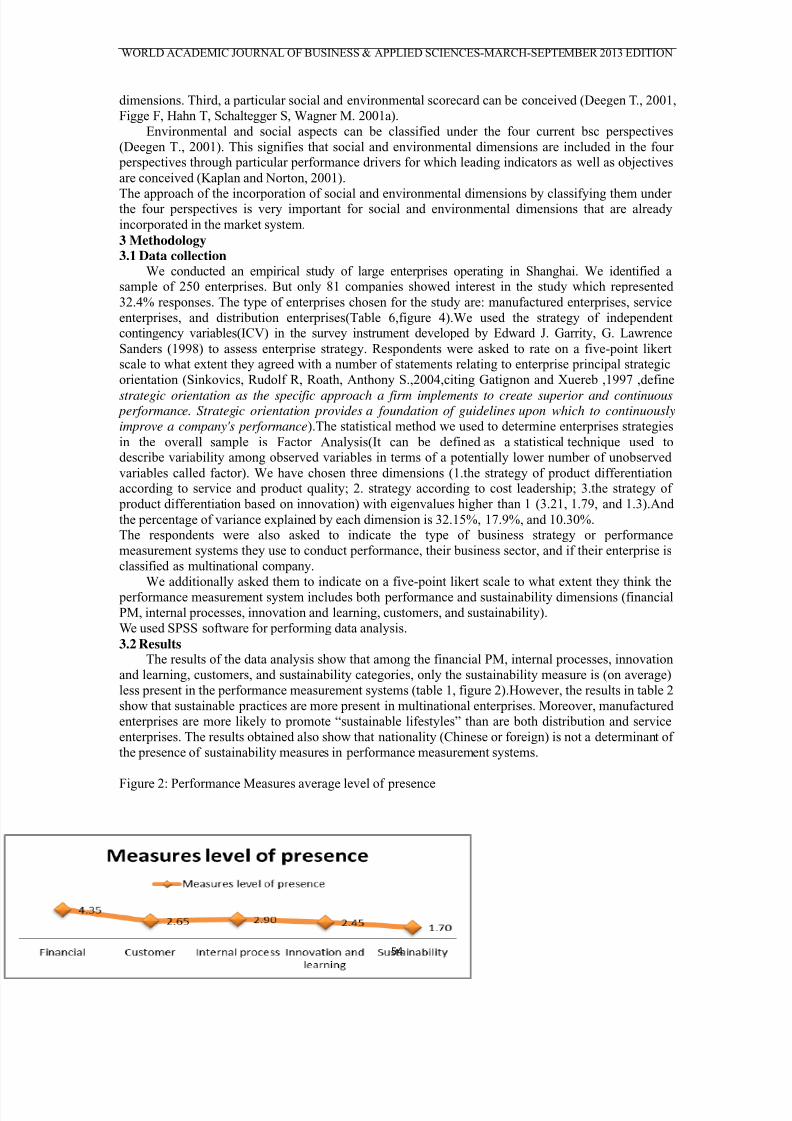

3.2 ResultsThe results of the data analysis show that among the financial PM, internal processes, innovation

and learning, customers, and sustainability categories, only the sustainability measure is (on average)

less present in the performance measurement systems (table 1, figure 2).However, the results in table 2

show that sustainable practices are more present in multinational enterprises. Moreover, manufactured

enterprises are more likely to promote “sustainable lifestyles” than are both distribution and service

enterprises. The results obtained also show that nationality (Chinese or foreign) is not a determinant of

the presence of sustainability measures in performance measurement systems.

Figure 2: Performance Measures average level of presence

7/27/2019 Analyzing the current incorporation of social, environmental nd economic measures into business strategic perfor…

http://slidepdf.com/reader/full/analyzing-the-current-incorporation-of-social-environmental-nd-economic-measures 7/12

WORLD ACADEMIC JOURNAL OF BUSINESS & APPLIED SCIENCES-MARCH-SEPTEMBER 2013 EDITION

55

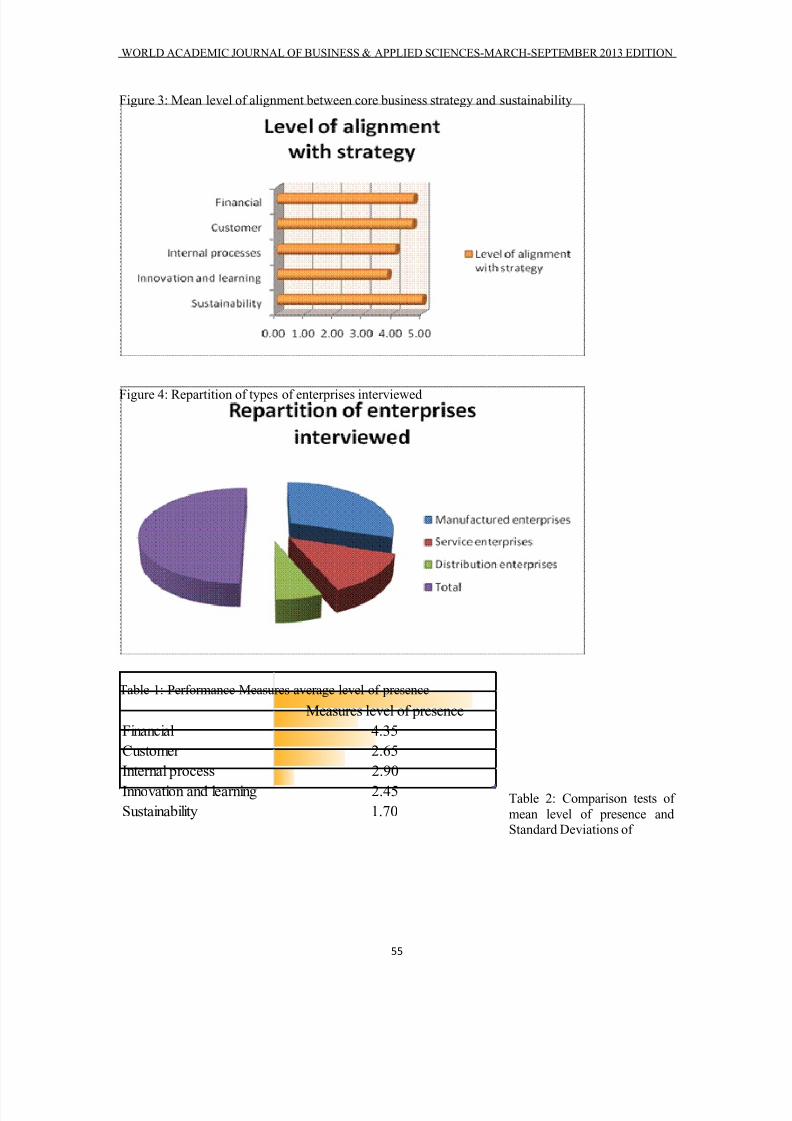

Figure 3: Mean level of alignment between core business strategy and sustainability

Figure 4: Repartition of types of enterprises interviewed

Table 1: Performance Measures average level of presence

Table 2: Comparison tests of

mean level of presence and Standard Deviations of

Measures level of presence

Financial 4.35

Customer 2.65

Internal process 2.90

Innovation and learning 2.45

Sustainability 1.70

7/27/2019 Analyzing the current incorporation of social, environmental nd economic measures into business strategic perfor…

http://slidepdf.com/reader/full/analyzing-the-current-incorporation-of-social-environmental-nd-economic-measures 8/12

WORLD ACADEMIC JOURNAL OF BUSINESS & APPLIED SCIENCES-MARCH-SEPTEMBER 2013 EDITION

56

Sustainability Indicators

Contingency variable N

Mean level

of sustainability

indicator

Standard

Deviation

Mean

Difference

Classified as multinational enterprise 35 1.85 1.15

Not classified as multinational enterprise 46 1.80 1.06 0.12*

Manufactured company 47 1.87 1.08Distribution enterprise 17 1.53 0.89 0.34*

Manufactured company 47 1.87 1.08

Service enterprise 17 1.53 0.89 0.34*

Chinese enterprises 60 1.89 1.09

Foreign companies 21 2.00 1.14 0.11 *P< 0.5Table 3: Correlations between level of presence of sustainability measures in PMS and the type of

strategy.

Table 4: Mean level of alignment between core business strategy and sustainability

Measures Level of alignment with strategy

Sustainability 5.00

Innovation and learning 3.80

Internal processes 4.08

Customer 4.66

Financial 4.70

Table 5: comparison tests mean of core business strategy and sustainability (by contingency variables)

Contingency variable N

Mean levelof sustainability

indicator

Standard

Deviation

Mean

Difference

Classified as multinational enterprise 35 2.40 1.45

Not classified as multinational enterprise 46 2.15 1.20 0.25*

Manufactured company 47 2.45 1.55

Distribution enterprise 17 2.12 1.10 0.33*

Manufactured company 47 2.45 1.55

Service enterprise 17 2.12 1.10 0.33*

Chinese enterprises 60 2.13 1.12

Foreign companies 21 2.18 1.19 0.05 *P< .01

Table 6.Repartition of types of enterprises interviewed

Ente rpris es Numbe r of e nte rpris es Pe rce ntage s

Manufactured enterprises 49 60.49%

Service enterprises 22 27.16%

Distribution enterprises 10 12.34

Total 81 100%

The results in table 3 show that there is no link between the presence of sustainability dimensions

in performance measurement systems and business strategy.The table 4 and figure 3 show that among the categories of PMS, sustainability measures are the

Strategy of quality Strategy of cost leadership Strategy of innovation

Sustainability dimensions'

level of presence -0.24 -0.33 0.42

P<0.05, correlations are significant

7/27/2019 Analyzing the current incorporation of social, environmental nd economic measures into business strategic perfor…

http://slidepdf.com/reader/full/analyzing-the-current-incorporation-of-social-environmental-nd-economic-measures 9/12

WORLD ACADEMIC JOURNAL OF BUSINESS & APPLIED SCIENCES-MARCH-SEPTEMBER 2013 EDITION

57

most correlated to enterprise strategy. This result has been confirmed by Rodney Mc Adam and Brian

Bailie (2002). They demonstrated that “ performance measures associated to strategy are more

effective. Also, the alignment between the measures, measurement framework and the strategy must be

continually reviewed and treated as a dynamic and complex issue, rather than a linear mechanistic

relationship”.

The results in table 5 show that the alignment between core business strategy and sustainability is

more correlated with multinational enterprises and with manufactured enterprises.4 Discussions and Conclusion

In investigating to what degree enterprises operating in Shanghai incorporate sustainability

measures in their performance measurement systems (PMS) and align them with long term business

strategy, we found that among the performance measurement categories, only the sustainability

measures appear to be faintly present in strategic performance measurement system and are not fullyaligned with business strategies(figure 1,table 2).The alignment of SPMS with business strategies

depend on each enterprise objectives .Nowadays only few enterprises align PMS with business

strategies. As the results suggest, in China, both multinational and manufactured enterprises align themost SPMS with their business strategies.

We also found that multinational enterprises and manufactured enterprises influence theincorporation of sustainability measures into business strategic performance measurement systems.

Others reasons that explain the incorporation of sustainability measures are: the high impact nature

of these enterprises operations on the environment ;the need to be responsible to environment and build trust with important stakeholders(NGOs and local communities ); high competition ; the need to

influence business leaders; the need to make difference between them and competitors in order to

increase market share and improving profitability, the requirement of shareholder to monitor and to report sustainability measures internally and externally in order to enhance enterprise valuation’s

prospect.Additionally, the development of ethical investing(also known as sustainable,

socially-conscious .It describes an investment strategy which seeks to maximize both financial return

and social good. Ehical investors favor enterprise practices that promote environmental stewardship,consumer protection and diversity) and its shareholder activism to get the best sustainability reporting

constitute the main reason why multinational enterprises are more likely to integrate sustainability

reporting into performance measurement systems (S.Gates and C. Germain ,2010).

We did not find any relationship between the presence of sustainability measures and enterprises

nationality and business strategy. Generally, performance measurement systems require that the performance measures must emanate from enterprise’ strategic objectives, because sustainability

aspects just now starting to be implemented into many enterprise’ strategic objectives, the relationship

between the process of business strategic planning and the formulation of PMS should be nearby tonot dissociate the PMS from enterprise’ sustainability strategy

Based on Gabriele Rosani and German Rueda (2011)’s recommendation, when building

performance strategic measurement system there are important problems that we need to pay

attention .The first problem is related to whether the performance measurement system is an

instrument for strategy formulation or implementation. The second problem refer to whether the most

appropriate approach to sustainability aspects is to treat them collectively or in separately such as

social, environmental, and economic. The third problem is related to whether sustainability activities

and measures must be controlled by a separate unit in the enterprise.

Finally, aligning enterprise sustainability measures with Strategic PMS constitute one of the mostcomplex challenges enterprises are facing. While this important topic has broad implications that

touch the enterprises daily operations as well as its budgeting, planning, and processes of goal-setting ,

at the end of the day if employees have not produced enough goods( or services), enterprises will

“take a hit” to the bottom-line and fall sadly short of goal achievement. Developing (or implementing)

a strategic PMS will help enterprise to keep employees committed to a enterprise's business system

and objectives .Responsibility for implementing a strategic PMS lies with the enterprise managementdepartment function.

According to Althea DeBrule (2011), for successfully building a strategic performance measurement

7/27/2019 Analyzing the current incorporation of social, environmental nd economic measures into business strategic perfor…

http://slidepdf.com/reader/full/analyzing-the-current-incorporation-of-social-environmental-nd-economic-measures 10/12

WORLD ACADEMIC JOURNAL OF BUSINESS & APPLIED SCIENCES-MARCH-SEPTEMBER 2013 EDITION

58

system, it’s important to:

1. Associate PM to enterprise business planning (tie resulting performance metrics to enterprise

business result).

2. Design training programs and worker orientation and to help employees become moreconscientious about how their work influence the enterprise's bottom line.

3. Reexamine the program of current worker performance management .Remember integrating

multiple-rater, 360-degree feedback and transfer into the PMS4. Involve employees in the PMS project.

5 Implement competency models and use them as a basis for connecting PMS with other people

management processes.

6. Disassociated performance evaluation from professional development.

Performing a measurement system can be a difficult task. The system becomes visible to the overallenterprise and its reliability is authenticated at this point. Operation must be very well projected and

stakeholders’ involvement is important at this step.

To answer to the question “where to start for incorporating sustainability measures into strategic performance measurement system?” Gabriele Rosani and German Rueda (2011) argue that, “d ecision

makers in any enterprise can create added value (AV) for their stakeholders by determining and implementing sustainability strategies”.

Peter Drucker (Globally renowned management consultant) argues: “you can’t manage what you don’t

measure”. The first step for integrating sustainability into strategic PMS is therefore to create anappropriate enterprise sustainability scorecard. Managers need to understand the impact their

enterprises have across the value chain. Integrating sustainability into enterprise strategic PMS

ultimately gives enterprise a competitive advantage lowers short-term costs and enhances potentiallong-term revenue.

Enterprises managers could be helped to balance sustainability objectives with their profit and revenuegoals by integrating social, environment and economic measures into their enterprise’s strategic

performance measurement systems. Otherwise, organization’s management runs the risk that its

sustainability goals will remain separated from operations (S.Gates and C. Germain (2010)..Future research could examine how both manager administrator and labor force manage sustainability

measures.

ReferencesAtkinson, A.A. (1998).Strategic Performance Measurement and Incentive Compensation,

European Management Journal, Vol. 16, No. 5, Oct, pp. 552-561

Althea DeBrule(2011),from

http://www.ehow.com/how_4470888_develop-strategic-performance-measurement-system.htmlBansal (2003). From issues to actions: the importance of individual concerns and organizational

values in responding to natural environmental issues. Organization Science, 14(5), 510-527.

Basu, K., & Palazzo, G. (2008). Corporate social responsibility: a process model of sensemaking’.The

Academy of Management Review, 33(1), 122-136.

values in responding to natural environmental issues. Organization Science, 14(5), 510-527.

Bielak, D., Bonini, S.M.J., & Oppenheim, J.M. (2007). CEOs on strategy and social issues. McKinsey

Quarterly, 8-12

Bennett M, James P. (1999). Sustainable Measures: Evaluation and Reporting of Environmental and

Social Performance. Greenleaf: Sheffield.BSR Conference (2008). Sustainability: Leadership Required November 4-7, 2008 . Grand Hyatt .

New York.

Brundtland Commission (1987).World Commission on Environment and Development(WCED).

Oxford University Press in.

Business for Social Responsibility(2008).Independent auditors ‘report financial statements and single

audit reports and schedules independent auditors report, financial statements and single audit reportsand schedules.From http://www.bsr.org/pdfs/about/2008_BSR_FS.pdf

Deegen T.,(2001). Ansatzpunkte zur Integration von Umweltaspekten in die “Balanced

7/27/2019 Analyzing the current incorporation of social, environmental nd economic measures into business strategic perfor…

http://slidepdf.com/reader/full/analyzing-the-current-incorporation-of-social-environmental-nd-economic-measures 11/12

WORLD ACADEMIC JOURNAL OF BUSINESS & APPLIED SCIENCES-MARCH-SEPTEMBER 2013 EDITION

59

Scorecard”Center for Sustainability Management: Luneburg.

Dyllick and Hockerts(2002). Beyond the business case for corporate sustainability. Env. 11,

130–141 .Wiley InterScience.

Edward J. Garrity, G. Lawrence Sanders (1998). Information systems success measurement. IdeaGroup Inc (IGI), 1998 - Idea Group Inc (IGI) P101-102

Epstein, M. J. (2008). Making Sustainability Work: Best practices in managing and measuring social

and environmental impacts, Greenleaf, Sheffield.Forester, J., 1999: The Deliberative Practitioner: Encouraging Participatory Planning Processes,

Massachusetts Institute of Technology Press, Cambridge, Massachusetts

Frank Figge,Tobias Hahn,Stefan Schaltegger and Marcus Wagner(2002). The sustainability balanced

scorecard .Linking sustainability management to business strategy. Business Strategy and the

Environment Bus. Strat. Env. 11, 269–284 (2002)Frank Figge,Tobias Hahn,Stefan Schaltegger and Marcus Wagner(2001b). The Sustainability Balanced

Scorecard – a tool for value-oriented sustainability management in strategy focused organizations.

Conference Proceedings of the 2001 Eco-Management and Auditing Conference. ERP Environment:Shipley; 83–90.

Figge F, Hahn T, Schaltegger S, Wagner M. (2001a).Sustainability Balanced Scorecard.Wertorientiertes Nachhaltigkeits management mit der Balanced Scorecard.Center for Sustainability

Management: Luneburg.

Fineman (1996). Emotional subtexts in corporate greening. Organization Studies, 17(3), 479-500.Henriques and P. Sadorsky (1999).”The relationship between environmental commitment and

managerial perceptions of stakeholder importance”, Academy of Management Journal, February, 42

(1): 87-99.Gabriele Rosani and German Rueda(2011) . Incorporating Sustainability into Strategy. Tefen

Tribune.Winter Issue, 2011Kaplan R, Norton D.,(2001). The Strategy-Focused Organization: how Balanced Scorecard

Companies Thrive in the New Business Environment. Harvard Business School Press:Boston

Henriques, I., & Sadorsky, P. (1999). The relationship between environmental commitment and managerial perceptions of stakeholder importance. Academy of Management Journal, 42(1), 87-

99.

Mazon, R. (2004). Uma abordagem conceitual aos negocios sustentaveis: manual de negocios

sustentáveis. Sao Paulo: FGV-EAESP.

Marrewijk, M. van (2004). A value based approach to organization types: towards a coherent set of stakeholder-oriented management tools. Journal of Business Ethics, 55(2), 147-158.

Marcus Wagner, Tobias Hahn ,Frank Figge ,Stefan Schaltegger (2001)

The sustainable balanced scorecard linking sustainability management to business strategy. BusinessStrategy and the Environment Bus. Strat. Env. 11, 269–284

N., A. & Adams, C. (2000) .“Perspectives on Performance: The Performance Prism”, In Handbook of

Performance Measurement (ed. Bourne, M.), Gee Publishing, London.

OECD-DAC (2011). Enterprise Development and Economic Transformation:

Creating the Enabling Environment. 16-17 February 2011 African Union Conference Centre and

Hilton Hotel, Addis Ababa, Ethiopia

Portland state university (2011) .From

http://www.pdx.edu/cupa/initiative-triple-bottom-line-development.

Peter Drucker (1954).Drucker, Peter F., “The Practice of Management”.HarperBusiness book . ISBN0060110953

Raynard,P.,Forstarter,M.(2002).Corporate Social Responsibility:Implications for Small and.Medium

Enterprises in Developing Countries. United Nations Industrial Development .Strategy and the

Environment 11(2), 130–141 (2002)

S.Gates and C. Germain (2010).Integrating sustainability measures into strategic performance

measurement systems: an empirical study. Spring 2010, Vol 11, No. 3Sharma, S., & Henriques, I. (2005). Stakeholder influences on sustainability practices in the Canadian

forest products industry. Strategic Management Journal, 26(2), 159-180.

7/27/2019 Analyzing the current incorporation of social, environmental nd economic measures into business strategic perfor…

http://slidepdf.com/reader/full/analyzing-the-current-incorporation-of-social-environmental-nd-economic-measures 12/12

WORLD ACADEMIC JOURNAL OF BUSINESS & APPLIED SCIENCES-MARCH-SEPTEMBER 2013 EDITION

60

Roome (1998). Sustainability Strategies for Industry: the Future of Corporate Practice. Island:

Washington, DC.

Stone (2006). Limitations of cleaner production programmes as organisational change agents. II.

Leadership, support, communication, involvement and programme design. Journal of Cleaner Production, 14(1), 15-30.

Tregidga, H., & Milne, M. (2006). From sustainable management to sustainable development: a

longitudinal analysis of a leading New Zealand environmental reporter. Business Strategy and the Environment, 15(4), 219-241.

United States Environmental Protection Agency. (2001). An organizational guide to pollution

prevention. Retrieved July 18, 2007:http://www.ecy.wa.gov/programs/hwtr/P2/printguid.pdf

USEPA. (2001). Inventory of Greenhouse Gas Emissions and Sinks 1990-1999. Office of

Atmospheric Programs, U.S. Environmental Protection Agency, Washington, DC; EPA 236-R-01-001.Van Marrewijk, M. & Hardjono, T. (2003). European corporate sustainability framework for managing

complexity and corporate transformation. Journal of Business Ethics, 44 (2-3), 121-132.

Weber J, Schaffer U.,(2000). Balanced Scorecard and Controlling: Implementierung, Nutzen fur Manager und Controller – Erfahrungen in deutschen Unternehmen.Gabler: Wiesbaden.

P., J., Annandale, D. and Morrison-Saunders, A., (2004). Conceptualizing sustainabilityassessment, Institute for Sustainability and Technology Policy. Murdoch University. Environmental

Impact Assessment Review, Science Direct.

Elkington, J., (1998). Cannibals With Forks: The Triple Bottom Line of 21st CenturyBusiness. CT: New Society Publishers

Russel, J., (2008). Corporate Social Responsibility: What It Means for the Project Manager. PMI

Global Congress Proceedings. Denver, Colorado, USA.Sinkovics, Rudolf R, Roath, Anthony S (2004).Strategic orientation,capabilities,and performance in

manufacturer-3PL relationships,Journal of Business Logistics.Rodney Mc Adam and Brian Bailie (2002).Business performance measures and alignment impact on

strategy. International Journal of Operations & Production Management. Volume 22

Recommended