APERSPECTIVEON

MUTUALFUNDSHARECLASS

DEVELOPMENTS

ABSTRACTAnewwaveofmutualfundshareclassesarebeingconsidered–“T”sharesand“Clean”shares–bothaddressingpotentialconflictsduetotheanticipatedDOLFiduciaryRule,aswellasrespondingtomarketplacepressuresandexpectationsbydistributors.WhilethenewWhiteHouseDirectiveabouttheDOLRuleinsurestheRuledoesnotsurviveinitscurrentform(andpossiblywillberescinded),manyindustrydevelopmentsinfluencedbythisruleareirreversible.Iwelcomeyourquestionsandcommentstothisarticle–[email protected]

ARisingFocusonAssetAllocationCultureHasLedtotheDominanceofNo-LoadShareClass

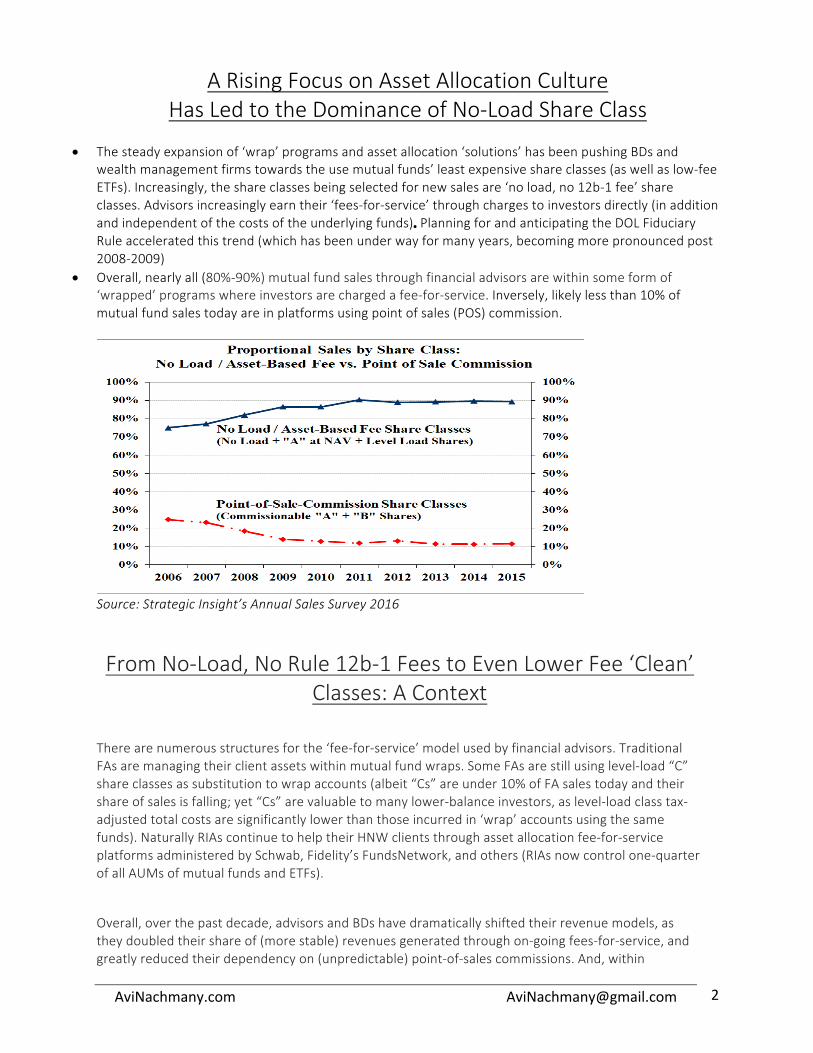

• Thesteadyexpansionof‘wrap’programsandassetallocation‘solutions’hasbeenpushingBDsand

wealthmanagementfirmstowardstheusemutualfunds’leastexpensiveshareclasses(aswellaslow-feeETFs).Increasingly,theshareclassesbeingselectedfornewsalesare‘noload,no12b-1fee’shareclasses.Advisorsincreasinglyearntheir‘fees-for-service’throughchargestoinvestorsdirectly(inadditionandindependentofthecostsoftheunderlyingfunds).PlanningforandanticipatingtheDOLFiduciaryRuleacceleratedthistrend(whichhasbeenunderwayformanyyears,becomingmorepronouncedpost2008-2009)

• Overall,nearlyall(80%-90%)mutualfundsalesthroughfinancialadvisorsarewithinsomeformof‘wrapped’programswhereinvestorsarechargedafee-for-service.Inversely,likelylessthan10%ofmutualfundsalestodayareinplatformsusingpointofsales(POS)commission.

Source:StrategicInsight’sAnnualSalesSurvey2016

FromNo-Load,NoRule12b-1FeestoEvenLowerFee‘Clean’Classes:AContext

Therearenumerousstructuresforthe‘fee-for-service’modelusedbyfinancialadvisors.TraditionalFAsaremanagingtheirclientassetswithinmutualfundwraps.SomeFAsarestillusinglevel-load“C”shareclassesassubstitutiontowrapaccounts(albeit“Cs”areunder10%ofFAsalestodayandtheirshareofsalesisfalling;yet“Cs”arevaluabletomanylower-balanceinvestors,aslevel-loadclasstax-adjustedtotalcostsaresignificantlylowerthanthoseincurredin‘wrap’accountsusingthesamefunds).NaturallyRIAscontinuetohelptheirHNWclientsthroughassetallocationfee-for-serviceplatformsadministeredbySchwab,Fidelity’sFundsNetwork,andothers(RIAsnowcontrolone-quarterofallAUMsofmutualfundsandETFs).

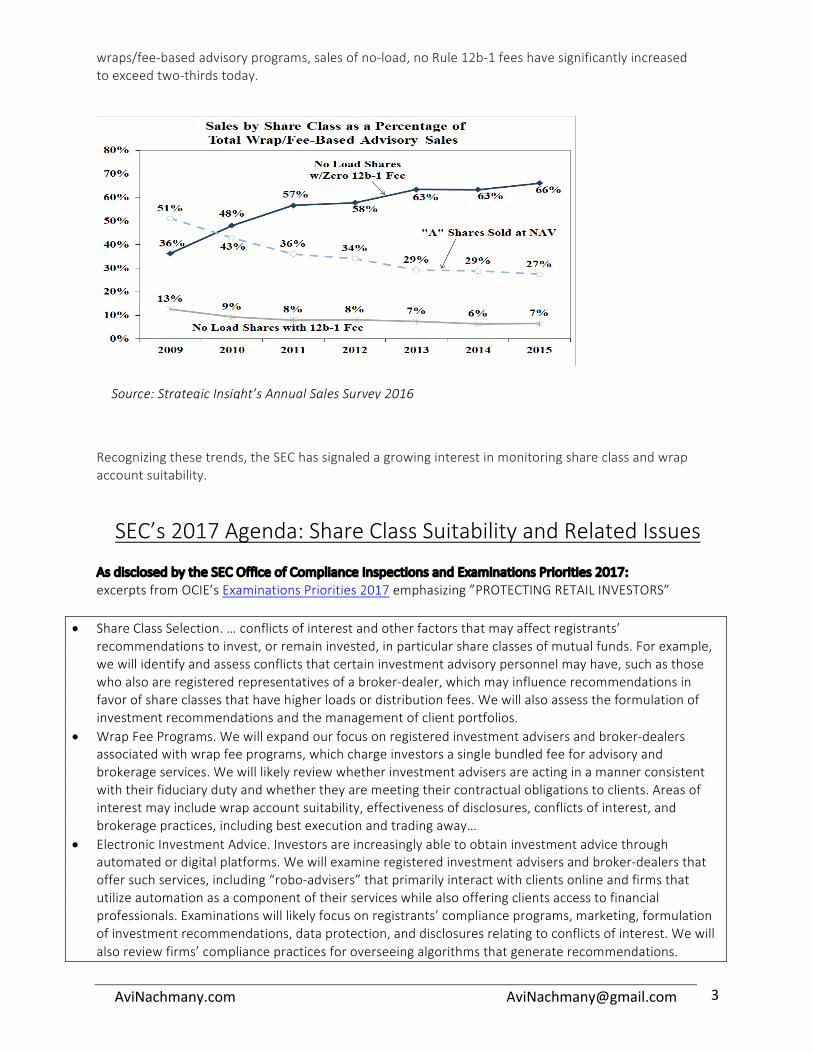

Overall,overthepastdecade,advisorsandBDshavedramaticallyshiftedtheirrevenuemodels,astheydoubledtheirshareof(morestable)revenuesgeneratedthroughon-goingfees-for-service,andgreatlyreducedtheirdependencyon(unpredictable)point-of-salescommissions.And,within

wraps/fee-basedadvisoryprograms,salesofno-load,noRule12b-1feeshavesignificantlyincreasedtoexceedtwo-thirdstoday.

Recognizingthesetrends,theSEChassignaledagrowinginterestinmonitoringshareclassandwrapaccountsuitability.

SEC’s2017Agenda:ShareClassSuitabilityandRelatedIssuesAsdisclosedbytheSECOfficeofComplianceInspectionsandExaminationsPriorities2017:excerptsfromOCIE’sExaminationsPriorities2017emphasizing”PROTECTINGRETAILINVESTORS”

• ShareClassSelection.…conflictsofinterestandotherfactorsthatmayaffectregistrants’recommendationstoinvest,orremaininvested,inparticularshareclassesofmutualfunds.Forexample,wewillidentifyandassessconflictsthatcertaininvestmentadvisorypersonnelmayhave,suchasthosewhoalsoareregisteredrepresentativesofabroker-dealer,whichmayinfluencerecommendationsinfavorofshareclassesthathavehigherloadsordistributionfees.Wewillalsoassesstheformulationofinvestmentrecommendationsandthemanagementofclientportfolios.

• WrapFeePrograms.Wewillexpandourfocusonregisteredinvestmentadvisersandbroker-dealersassociatedwithwrapfeeprograms,whichchargeinvestorsasinglebundledfeeforadvisoryandbrokerageservices.Wewilllikelyreviewwhetherinvestmentadvisersareactinginamannerconsistentwiththeirfiduciarydutyandwhethertheyaremeetingtheircontractualobligationstoclients.Areasofinterestmayincludewrapaccountsuitability,effectivenessofdisclosures,conflictsofinterest,andbrokeragepractices,includingbestexecutionandtradingaway…

• ElectronicInvestmentAdvice.Investorsareincreasinglyabletoobtaininvestmentadvicethroughautomatedordigitalplatforms.Wewillexamineregisteredinvestmentadvisersandbroker-dealersthatoffersuchservices,including“robo-advisers”thatprimarilyinteractwithclientsonlineandfirmsthatutilizeautomationasacomponentoftheirserviceswhilealsoofferingclientsaccesstofinancialprofessionals.Examinationswilllikelyfocusonregistrants’complianceprograms,marketing,formulationofinvestmentrecommendations,dataprotection,anddisclosuresrelatingtoconflictsofinterest.Wewillalsoreviewfirms’compliancepracticesforoverseeingalgorithmsthatgeneraterecommendations.

Source:StrategicInsight’sAnnualSalesSurvey2016

Towards“CleanShares:”NewLowFeeShareClass(no12b-1;NoTA/SubTAFees)?

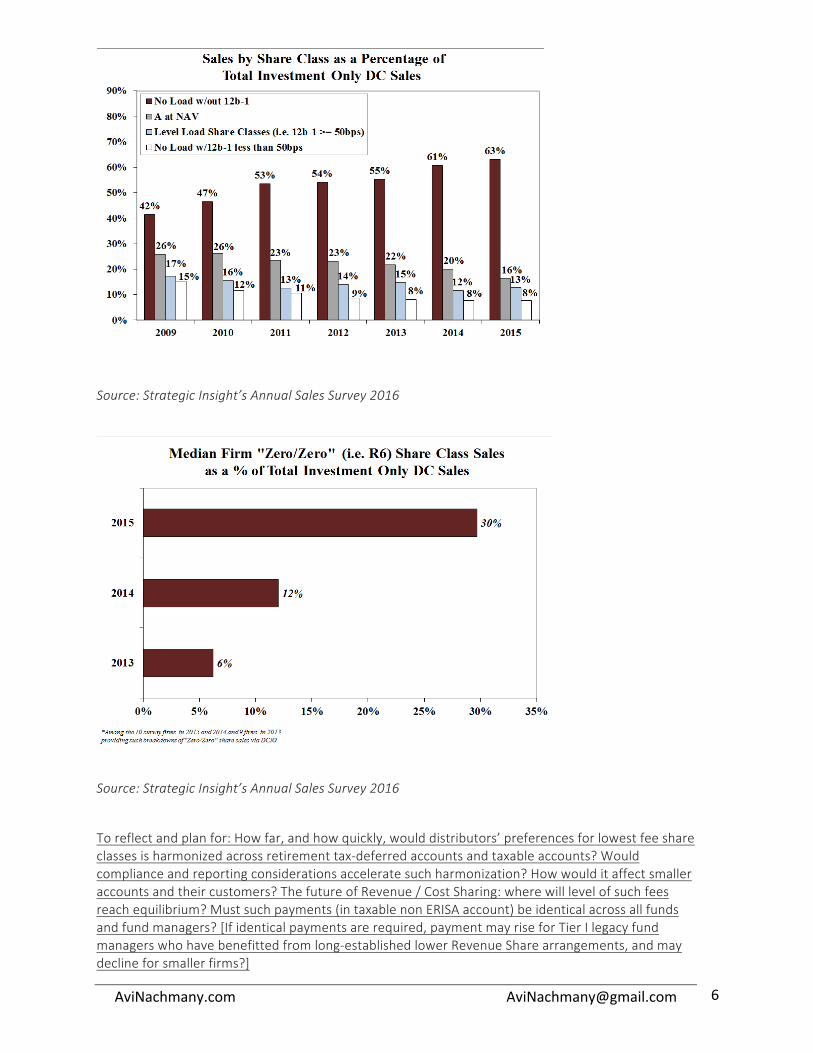

Shareclassesstrippedofmanyembeddedcosts(distributionfeesviaRule12b-1orTA/SubTAfees)havebecomedominantwithDCplans(typicallysuchshareclassesaredesignedR6).In2015,withinDCInvestmentOnlyplans,anestimated30%ofsaleswerecapturedbysuchclasses–justtwoyearsbefore,theshareofsuchfundswasatiny6%.NaturallytheshareofDCIOplansalescapturedbyR6classesisevenhighernow.

R6‘zero/zero’shareclassesareleading(generallylarge)retirementplans(shiftinfluencedbycostconsideration,litigationrisk,ERISArules,andplanningaheadoftheDOLFiduciaryRule,nowunlikelytosurviveinitscurrentformifnotcompletelyrescinded).Yet,beyondretirementplans,anewwaveof‘zero/zero’shareclassesarebeingconsiderednow.MuchofsuchdiscussionhascenteredonthenewSECNo-ActionLetterattherequestofCapitalGroup(parentofAmericanFunds).

Thesenewshareclassesaredubbed‘Clean,’(aUKterminology…)andcanbeusedinbothretirementaccountsornon-retirementaccounts.Usingsuchshareclassesallowbrokerstosettheirowncommission(naturallythefund'sprospectuswouldhavetodisclosethatthebrokermaychargeacommissiononthesaleoftheshares.Otherstatedconditions:thebrokerisactingonlyonan“agencybasis”forthesaleoftheshares;sharesdonotincludeanydistribution-relatedpaymentstothebroker).[Thereissomeambivalenceaboutpaymentofrevenuesharingin‘Clean’shares.ItisunderstoodthatinitsNo-ActionLettertheSECdidnotspecifywhethersub-TAfeeswouldbepermissible,wereafundmanagertocreateaversionofcleansharesthatincludesthem–suchshouldbepermissibleastheyarenotdistribution-relatedpayments.]

Inplanningforafuturewhere‘Clean’shareclassesarepopular(noRule12(b)1feesandnoTA/SubTAfees):who’llpayforservicingcostsoffundsonaBDplatform?WillsuchfeesbeabsorbedbyBDs,paiddirectlybyinvestors,orpaidbyfundmanagersoutoftheirfallingprofits?Whatwillbethemechanismforsuchpayment(nolongerenjoyingthemutualizationoffees)?Whattheframeworktopermitthepaymentofsuchfees)?

“T”ShareClasses:NewCommissionShareClassesforCommissionPlatform

Source:StrategicInsight’sAnnualSalesSurvey2016

Theuseoftraditional‘load’shareclasseshasdramaticallydeclinedinrecentyears.AndanticipatingtheDOLFiduciaryRulehasintroducedthepotentialfornewconflictsintheuseofsuchshareclasses,triggeringdecisionamongsomeBDstoexitcommissionplatformsforretirementaccounts.

1. Documentedinpriorchart:“A”shareswith2-4%commissionshavebeenthemostcommonlyusedinrecentyears,accountingforunder10%ofsalesin2015(inaggregate)andforalowersharelastyearandin2017(surveydatafor2016isnotyetavailable).Actuallyformostfundfirms,theshareofany“As”soldwithcommissionsaresignificantlylowerthantheaboveaggregatedatasuggest(assuchaggregateddataisdistortedduetotheexperienceofonelargefundcompany).

2. Naturally,forwealthierinvestorsthelevelofsalescommissionsforanewpurchaseareinfluencedbylargebalancesalreadyownedwithinsamehousehold(orBD),allowingcustomerstherightoflowercommissions.[Note:“Ts”donotallowsuchscalediscounts,aseachtransactionPOScommissionsaresetbythesizeofthatpurchasealone.]

3. PlanningfortheDOLFiduciaryRulehasledtoanewgenerationoffundshareclassestobeusedincommission-basedplatforms.Underwayareadaptationstotherule–whichIbelievearelikelytosurvivethelikelydemiseoftheRuleinitscurrentform–aroundcommission-basedplatforms.

4. SomeBDsareexitingsuchcommissionplatformfortheirERISAassets–andlikelyovertimeintheirtaxableaccounts;othersareintroducingmodificationstothetypeoffundspermittedintheircommission-basedplatform.

5. SomeBDsbelievethattheircustomersbenefit(throughlowerlifetimetotalcostsandotherways)iftheymaintaintheavailabilityofcommissionplatform.Thiscanbeaccomplishedwiththenewly-introducedshareclasses(designedtosidesteptheDOLFiduciaryRuleperceivedconflicts;existingshareclasses–historicallyusedincommissionplatforms--‘A’s,‘B’s,‘C’s–werebelievedtocreateconflictsfordistributorsadheringtotheDOLRule).Enter“T”shares:anewshareclass.Atypicalstructure[tosimplifytheiracceptanceanduse,itisimperativethata‘standard’of‘Ts’isestablished]:POSchargeof2.5%;breakpointsupto$1millionand1%salesloadforalltransactions$1millionandabove);NoshareholderAUMaccumulationprivileges(NoROA,NoLOI);NoCDSC;0.25%Rule12b-1fee.Generally,“Ts”donothaveaseparateShareholderServicingFees(anexceptionisJPMorgan’sAMfilingswhichinclude0.25%ShareholderServicesFeeswhichmaybeusedforpaymentforsub-transferagentorforshareholderandadministrativeservice).(Onceafirmintroduces‘Ts,’existingtransactionalshareclasses–‘As,’‘Bs,’,(possibly)‘Cs’-mayhavetobeclosedandtheirAUMsexchangedintothisnewshareclass.)

AHarmonizationofShareClassesUsedinRetirementAccountsandinTaxableAccounts?

ItisclearthatnoRule12b-1feeshareclasses,andattimes,shareclasseswithoutTA/Sub-TAfee(‘R6’)havebecomeadominantstructurewithinthemajorityofIODCnewsales,asillustratedinthenexttwocharts(2016dataisbeingcollectedandavailableinthecomingmonthsbutthetrendisirrefutable).

Source:StrategicInsight’sAnnualSalesSurvey2016

Source:StrategicInsight’sAnnualSalesSurvey2016

Toreflectandplanfor:Howfar,andhowquickly,woulddistributors’preferencesforlowestfeeshareclassesisharmonizedacrossretirementtax-deferredaccountsandtaxableaccounts?Wouldcomplianceandreportingconsiderationsacceleratesuchharmonization?Howwoulditaffectsmalleraccountsandtheircustomers?ThefutureofRevenue/CostSharing:wherewilllevelofsuchfeesreachequilibrium?Mustsuchpayments(intaxablenonERISAaccount)beidenticalacrossallfundsandfundmanagers?[Ifidenticalpaymentsarerequired,paymentmayriseforTierIlegacyfundmanagerswhohavebenefittedfromlong-establishedlowerRevenueSharearrangements,andmaydeclineforsmallerfirms?]

Inconclusion

Ithasbeenmyobservationthatitisbettertobeafastfollowerthatanearlyinnovatorofnewshareclasses,allowingsuchpatientfirmtofine-tunetheirofferingifneeded.Furthermore,theWhiteHouseFebruary3rdnewDirectiveabouttheDOLFiduciaryRule(whichiscertaintoresultintheRulebeingrescindedorgreatlymodified)suggeststhatsomefundmanagementcompaniesdelayfilingsandlaunchingnewshareclassuntilthe‘dustsettles’inthecomingmonths.Yet,somedistributorshavealreadysetinmotionprogramsaroundtheselectionanduseofshareclasseswhichmayrequiretheintroductionsofnewsuitesofsuchclassesindependentofthefutureoftheDOLRule.Overall,marketplacetrendssuggestthatthemutualfundindustryisevolvingtoafuturewhereamajorityoffundnewsalesandassetsundermanagementuseshareclasseswhichcoveronlycoremanagement,administration,andlegallyrequiredfees,side-by-sidewithlowfeeETFs,allwrappedwithanassetallocationprogramsinwhichadditionalfees-forservice,feesforplatformparticipation,andotheradministrativefeesarechargedseparatelytotheinvestor.Thepathinthatdirectionisset,andfundmanagementfirmsandtheirfundtrusteeshouldcontinuetoplanforsuchafuture.AviNachmanyNewYorkCity,[email protected]

Recommended