A Distinctively Different Way to Enhance Your Benefits Portfolio

8545-03-102008-4653

Disability insurance policy form 1200 is underwritten and issued by Berkshire Life Insurance Company of America, Pittsfield, MA, a wholly owned stock subsidiary of The Guardian Life Insurance Company of America, New York, NY. Product provisions and features may vary by state.

How can you build a better benefits offering?

Offer more options to key executives?

All this and more with the help of DI@Work!

Extend more benefits to all employees?

Control costs for your organization?

More about this distinctively different benefit

What does the DI@Work program offer?

• More disability insurance that can complement your Group Long-Term Disability plan or stand alone

• More coverage for individuals—available at discounted rates for groups

• More flexibility in how the program is designed and how it is funded

• More comprehensive support for promoting the benefit, enrolling your employees, and servicing your participants

More about this distinctively different benefit

Let’s talk more about who can benefit—and how:

Top executives who need higher income protection

All employees who need access to additional, affordable coverage

Employers who want to enhance their benefits—while controlling their costs

More Options for Top Talent

More Value for All Employees

More Advantages for Your

Organization

What “more” can you provide for your top talent?

More disability insurance coverage?

All this and morewith DI@Work!

More protection for all sources of income?

More flexibility in structuring their benefits plan?

More ways to attract and keep top talent

Benefit Caps

Limited Definition of “Income”

Monthly benefit limits, e.g., 60% of salary, up to $10,000 per month

Incentive compensation or bonuses aren't typically included

Taxation Employees pay taxes on Group LTD* benefits when they receive them, reducing the net benefit

* When employer-paid

This publication is offered for the purpose of education and information only and is not intended to constitute tax or legal advice. For information on your specific situation, please consult your personal tax or legal advisor.

Why Group Long-Term Disability Insurance may not be enough

More ways to attract and keep top talent

60% of Base Salary, up to $10,000 a monthAnnual Gross Salary

$120K

What Group LTD may cover: Replaces only 48% of total income!

Could be as much as 100% of total income

What Group LTD Plus Individual Disability Insurance may cover:

Individual Disability InsuranceAnnual Gross Salary Bonus 401(k) Deferral/Match

Let’s look at an example:

$250K + 401(k) Deferral/Match

401(k) Deferral/MatchAnnual Gross Salary

$200KBonus

$50K

Total Current Compensation

More ways to attract and keep top talent

Benefits of buying Individual Disability coverage through the DI@Work program

X

Special coverage for key personnel

Portable

Guaranteed renewable to age 65/67

XFlexible design options on individual basis

Not TypicallyTax-free benefits

Not TypicallyProtects retirement contributions

Not TypicallyProtects incentive income

Not TypicallyEmployee-paid

Group LTD

Group Long-Term Disability vs. DI@Work

1If employee-paid.

X

X

Optional

IDI through DI@Work

1

More Options for Top Talent

More Value for All Employees

More Advantages for Your

Organization

What “more” could you provide your all employees?

Would employees really value more disability insurance? What % of employees are concerned about having enough income if they become disabled?

27%

48%

62%

83%

Will employees value supplemental disability insurance?

Would employees really value more disability insurance? What % of employees are concerned about having enough income if they become disabled?

Navigating the Workplace Benefits Landscape, LIMRA, 2006 Report.

27%

48%

62%

83%

83%

More ways to meet the needs of all employees

Three out of every 10 workers will become disabled before they retire.

U.S. Census Bureau, Table 198 Surveys, 1997.

Not just for highly compensated employees…

That makes adequate disability insurance no longer a luxury, but a key benefit.

Many employees live paycheck to paycheck

More ways to meet the needs of all employees

More ways to meet the needs of all employees

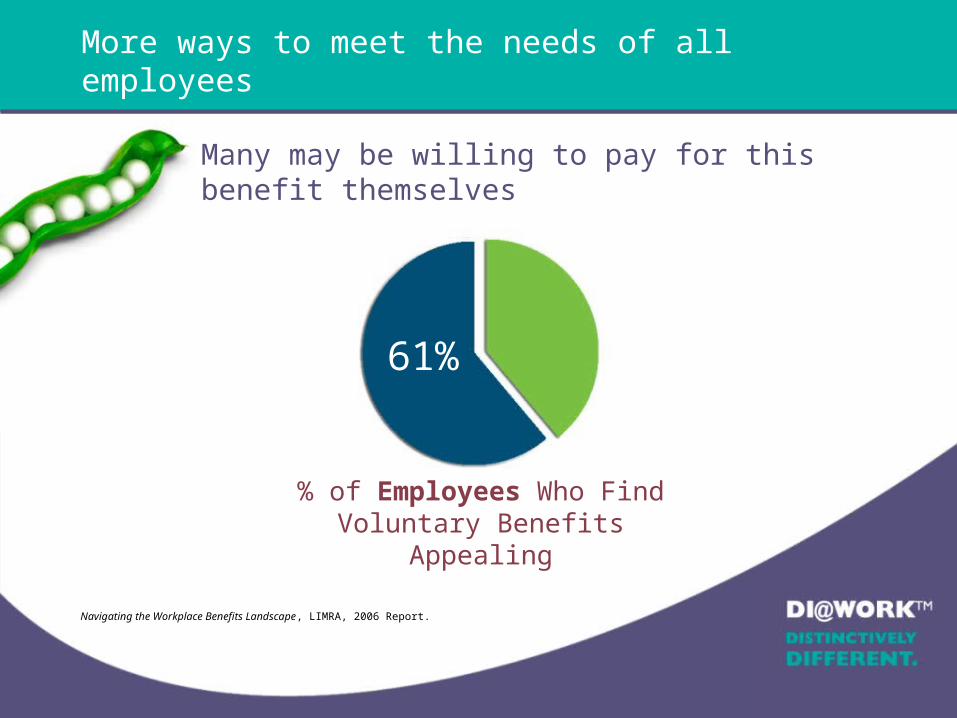

Navigating the Workplace Benefits Landscape, LIMRA, 2006 Report.

Many may be willing to pay for this benefit themselves

60%

% of Employees Who Find Voluntary Benefits Appealing

61%

More ways to meet the needs of all employees

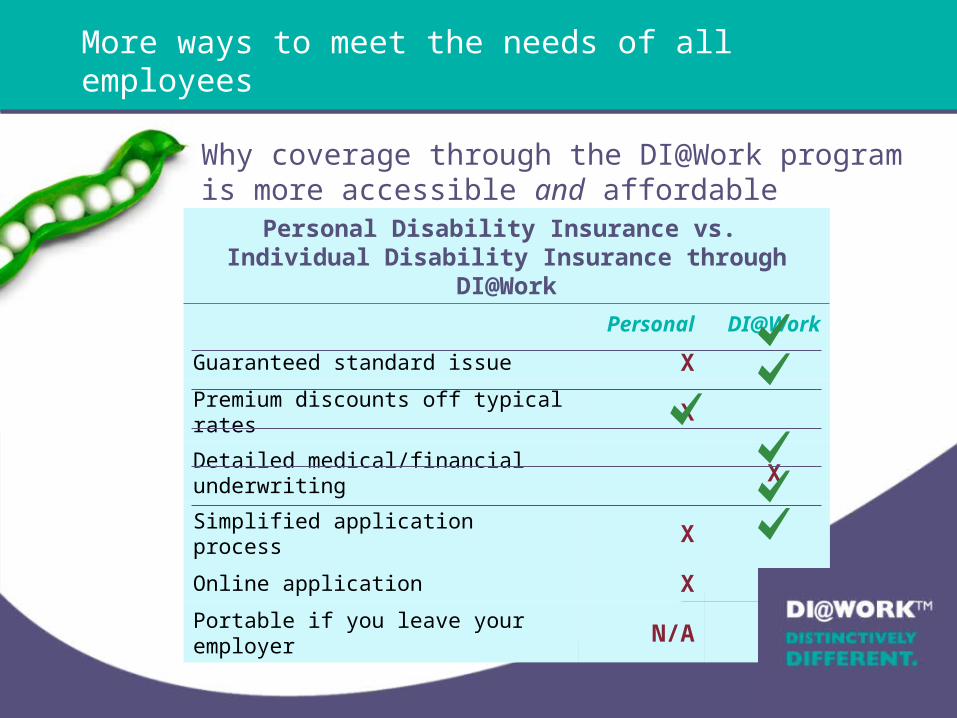

Personal Disability Insurance vs. Individual Disability Insurance through DI@Work

Personal DI@Work

Guaranteed standard issue X

Premium discounts off typical rates X

Detailed medical/financial underwriting X

Simplified application process X

Online application X

Portable if you leave your employer N/A

Why coverage through the DI@Work program is more accessible and affordable

More ways to meet the needs of all employees

Total disability definition options:

can help tailor when benefits are paid

How individual disability insurance expands protection options

Partial disability option:

can be added to expand covered situations

Catastrophic* disability benefit option:

may replace up to 100% of income

Product provisions and features may vary by state.

*Catastrophic Disability Benefit Rider is not available in CA, CT or TX.

More ways to meet the needs of all employees

Flexible benefit levelsTo meet the varying needs of diverse groups

How individual disability insurance expands protection options

Guaranteed access to additional coverage:

Option to buy more each year

at discounted rate

Annual cost-of-living adjustment option*

Retirement protection coverage option:

replaces up to 100% of employee contributions and employer match

*Not necessarily protection against increases in the cost of living.

More Options for Top Talent

More Value for All Employees

More Advantages for Your

Organization

What “more” is your organization looking for?

More control over your benefits costs?

More ways to streamline benefits administration?

More flexibility to tailor your benefits portfolio?

More support educating employees on their benefits?

Now you can have it all…with DI@Work from Berkshire Life Insurance Company of America!

What “more” is your organization looking for?

More advantages for your organization

Your choice of funding arrangements:

• Voluntary: paid for by employees; benefits paid to them would be tax-free

• Employer-Paid: may be for just a select group of employees; deductible as a corporate expense

• Cost-Sharing: costs can be shared by both the employer and the employee

• Combination: any mix of the arrangements listed above for different groups

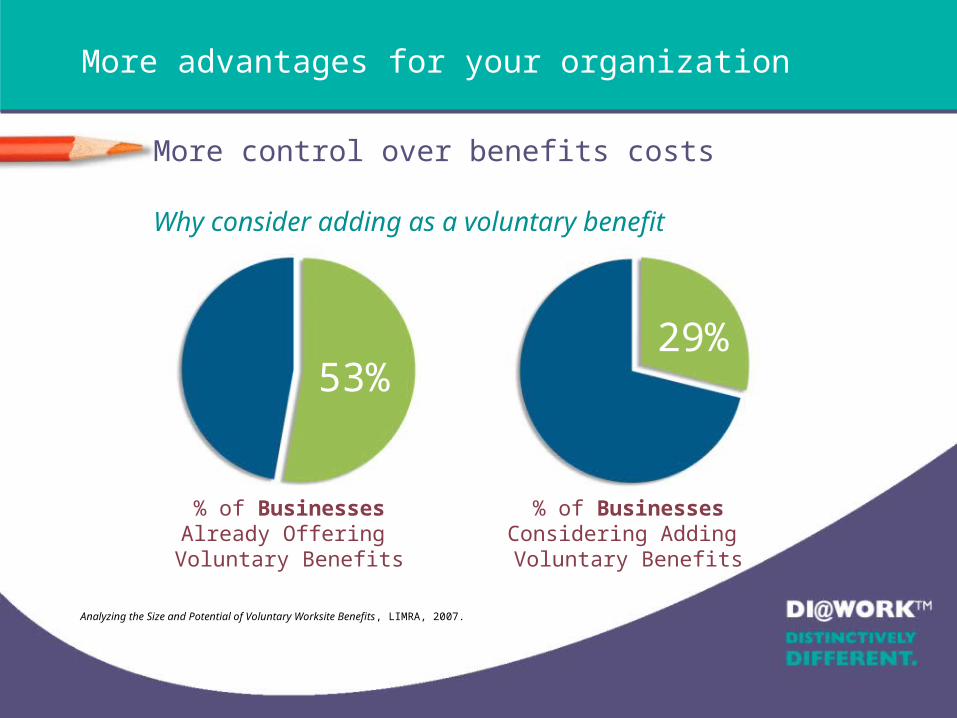

More control over benefits costs

This publication is offered for the purpose of education and information only and is not intended to constitute tax or legal advice. For information on your specific situation, please consult your personal tax or legal advisor.

More advantages for your organization

% of BusinessesAlready Offering

Voluntary Benefits

53%

Why consider adding as a voluntary benefit

29%

% of BusinessesConsidering Adding Voluntary Benefits

Analyzing the Size and Potential of Voluntary Worksite Benefits, LIMRA, 2007.

More control over benefits costs

More advantages for your organization

• As a complement to an existing Group LTD plan

• As a stand-alone option for all or some of your employees

• As a seamless program combining both Group Long-Term Disability from Guardian and Individual Disability Insurance from Berkshire Life, one of the few providers that can offer both

Different ways you can structure your individualdisability insurance through the DI@Work program:

More flexibility to tailor your program

More advantages for your organization

• Expert hands-on management of the program announcement and enrollment process

• Flexible billing arrangements, including direct billing your employees if you choose

• Award-winning customer service team

How we can minimize your workload:

More ways to streamline your benefits administration

More advantages for your organization

- Customized letters/brochures

- HTML emails- Flyers/posters- Intranet/

newsletter text- Postcards- Automated voicemails

Initial enrollment period:- Online enrollment site- Personalized emails- Group meeting/recorded

presentations- Education-based enrollment - True e-signature—no paper

applications

Ongoing enrollment promotion- Reminder emails/follow-up calls- Automated voicemails- Personalized proposals- Choice of product packages

Enrollment tracking- Monitoring of enrollment activities- Demographic reporting

ENGAGE ENROLL SERVICE RE-ENGAGE

- Customized letters/brochures

- HTML emails- Flyers/posters- Intranet/

newsletter text- Postcards- Automated voicemails

Initial enrollment period:- Online enrollment site- Personalized emails- Group meeting/recorded

presentations- Education-based enrollment - True e-signature—no paper

applications

Ongoing enrollment promotion- Reminder emails/follow-up calls- Automated voicemails- Personalized proposals- Choice of product packages

Enrollment tracking- Monitoring of enrollment activities- Demographic reporting

More ways to streamline your benefits administration

- Ongoing campaignfor newly eligible, previous declines, and those eligible forcoverage increases

- Payroll deduction reminders

- Billing options- Welcome kit/policy- Toll-free claim service- Ongoing communication

- Ongoing campaignfor newly eligible, previous declines, and those eligible forcoverage increases

- Payroll deduction reminders

- Billing options- Welcome kit/policy- Toll-free claim service- Ongoing communication

More advantages for your organization

Berkshire Life Insurance Company of America: 2007 Dalbar Award for outstanding service

More ways to streamline your benefits administration

More advantages for your organization

• Not a “generic” process, but customized to address your organization’s specific needs

• Can accommodate unique messaging for different groups within the same plan

• Flexible billing arrangements, including direct billing your employees if you choose

• State-of-the-art online enrollment Web site (or traditional paper options if you prefer)

More support educating your employees

More advantages for your organization

State-of-the-art online experience

More support educating your employees

More Streamlined

Ability to apply online by answering a few simple questions

More Educational

Personalized education/ income scenarios with actionable navigation

More Customized

A customized experience that provides enrollment information for employees and various coverage options to choose

More advantages for your organization

Your organization’s branding

Your plan design: coverage limits and available options

Each group’s unique arrangements: e.g., employees versus executives

Each individual’s specific situation: ability to choose less coverage or even apply for more coverage beyond guaranteed offer

Enrollment site can be customized to reflect:

More support educating your employees

More advantages for your organization

A distinctively different option to helpbuild your benefits plan:

More insights into the benefits people truly value

More flexible solutions tailored for each organization

More customized communications

More streamlined processes

More expertise every step of the way

See how DI@Work can offer your organization

more flexibility and your employees more value.

Talk to your plan advisor or Berkshire Life today

at 1-866-590-8847.

To receive a proposal simply provide a high-level

census and your company's LTD booklet.

Recommended