8/10/2007

Morocco Day 1July 2008

8/10/20072

Agenda Day 1 - Valuation

• Introductions– Ted Anderson– Jeff Karras

• Valuation introduction• The difficulties of early stage valuation• The art and science of valuation

– Multiples analysis– VC or DCF Model– Beyond the numbers

• Valuation Examples• Case Study

8/10/20073

Ted Anderson

Managing General Partner

Ventures West Management Inc.

8/10/20074

Ventures West -Firm Overview

• Recognized nationally as a premier early stage technology investor – currently investing 8th fund

• Largest and oldest private Canadian venture capital firm - Venture capital manager since 1973

• Established team, in key cities (Montreal, Toronto, Ottawa, Vancouver)

• Prior funds total over $700 million; VW4-8 total $600 million (since 1993)

• 90 technology company investments in Ventures West 4-8

• Established, stable team plus recent additions

• 7 Partners—average of 14 years of VC experience and 11 years at Ventures West

• Investors represent almost all of the large private equity investors in Canada

• 36 exits (Ventures West 4-8)—26 acquisitions and 10 IPOs (NASDAQ, TSX, AIM)

• Example exits—Angiotech (19X, 88% IRR), AudeSi (3.5X, 67% IRR), Chantry (2.4X, 59% IRR), LinkAge (5.2X, 324% IRR), Pivotal (18X, 109% IRR)

8/10/20075

VW Investment Strategy

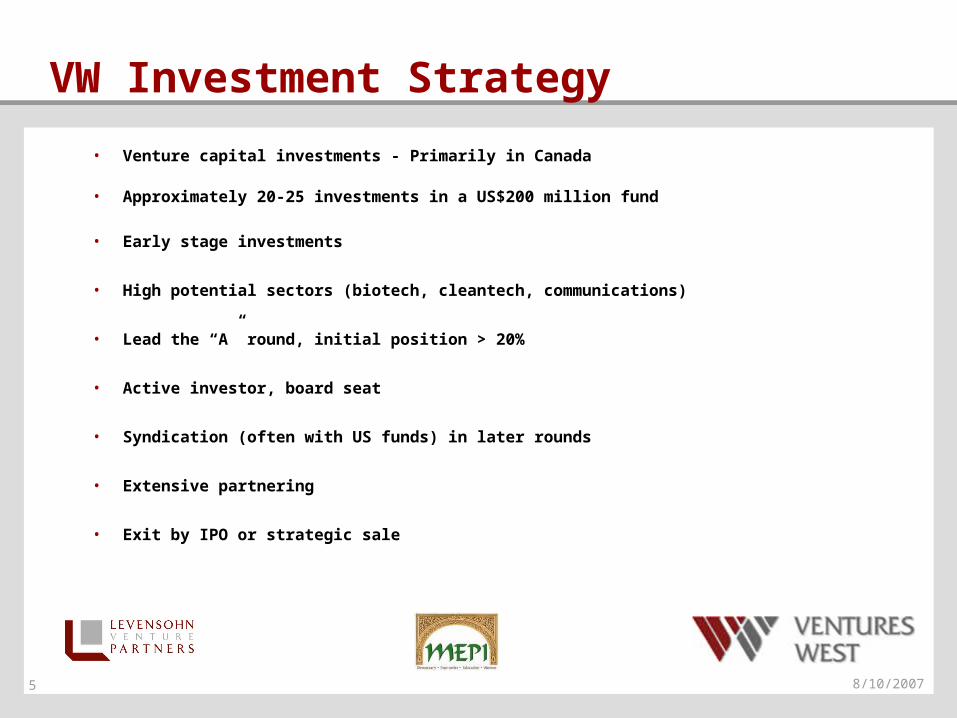

• Venture capital investments - Primarily in Canada

• Approximately 20-25 investments in a US$200 million fund

• Early stage investments

• High potential sectors (biotech, cleantech, communications)

• Lead the “A” round, initial position > 20%

• Active investor, board seat

• Syndication (often with US funds) in later rounds

• Extensive partnering

• Exit by IPO or strategic sale

8/10/20076

Jeff Karras

General Partner

Levensohn Venture Partners

8/10/20077

Levensohn Venture Partners -Firm Overview

• Established presence in Silicon Valley since 1996

• $193 million in total committed capital

• $334 million in distributions to date since inception

• Investment Team of five together since 2002

• Focused, selective strategy fewer investments and more time per portfolio company

• Hands-on investment style with proven ability to identify, build, and harvest winning companies

• 30 investments since 1996– 16 exits to date– 23% IPO– 30% M&A– 30% Remain private

8/10/20078

LVP Investment Strategy

• Early stage investor emphasizing companies that have completed initial technology development

• Thematic team-based approach to technology investing with California focus

• Lead deals and require board seat, with subsequent active role on boards

• Proactive engagement in operating and strategic projects across portfolio companies

8/10/20079

VALUATION

8/10/200710

The Stages

• Expansion Stage- Revenues increase, low or negative earnings, limited operating history, some but few comparables, value based mostly on future growth

• High Growth- Rapidly growing revenues and earnings, meaningful operating history, large number of comparables, value in both assets and future growth

• Mature Growth- Revenue growth slows but operating income still growing, lots of operating history, lots of comparables, value driven more from existing assets than future growth

• Declining- Revenue and operating income begins to decline, substantial operating history, declining number of mostly mature comps, value driven by existing assets.

8/10/200711

Early Stage

If everything was Ideal, • There would be historical financials• An entrepreneur’s financial projections would be accurate• VCs would know the timing and exit value• A company would know exactly how much cash was require to break-

even• There would be no competition for deals

The challenge with early stage startups

• Non existent or low revenue• Negative operating income• Little operating history• Few if any true pure play comparable companies• Value based entirely on future growth- value relies on the ability of

managers to turn a promising idea into commercial success

8/10/200712

Art and Science

From a practical standpoint, valuation tends to be both

Art and Science

Typically more Art than Science

8/10/200713

The Science of Early Stage Valuation

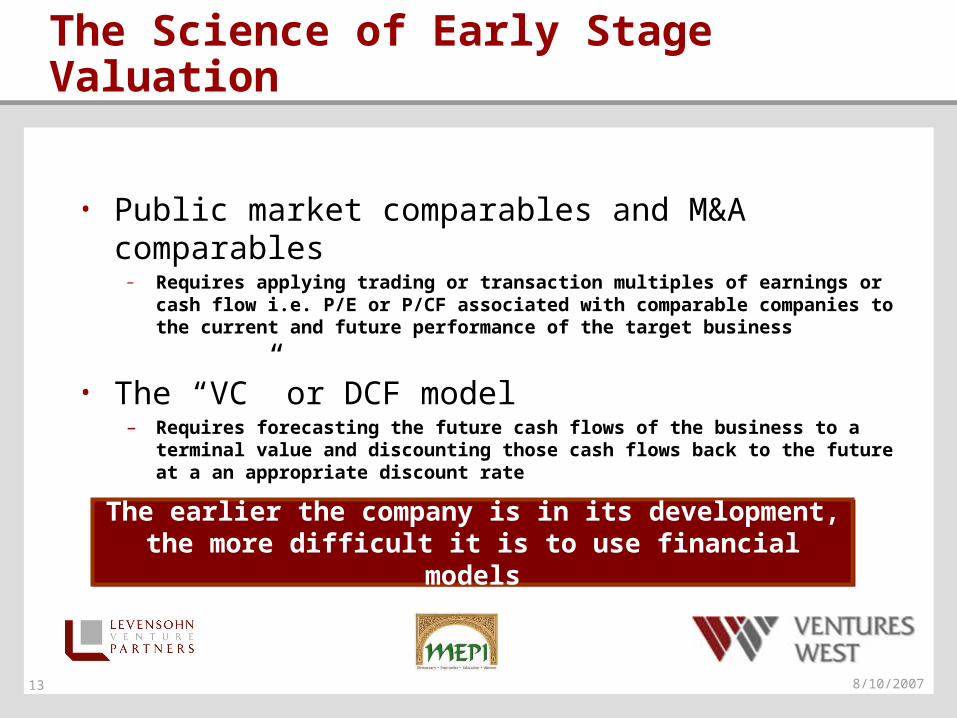

• Public market comparables and M&A comparables– Requires applying trading or transaction multiples of earnings or cash flow i.e. P/E or

P/CF associated with comparable companies to the current and future performance of the target business

• The “VC” or DCF model– Requires forecasting the future cash flows of the business to a terminal value and

discounting those cash flows back to the future at a an appropriate discount rate

The earlier the company is in its development, the more difficult it is to use financial models

The earlier the company is in its development, the more difficult it is to use financial models

8/10/200714

Public Comparable Analysis

Composite Valuation Ent. Val./ Mix of Components 2004 Sales BusinessSupply Chain 1.9x 50%CRM 1.3x 10%ERP 3.3x 10%Analytics 2.2x 30%Average 2.2x 100%

Composite Multiple 2.1x

2003E 2004E BeginningRevenue Scenario Revenue Revenue Cash (1Q03)High Case $12,000 $25,000 $1,000Low Case $8,000 $12,000 $1,000Actual Forecasat $10,000 $16,000 $1,000

Low Actual HighImplied Enterprise Value (2004) $24,761 $33,015 $51,585 less Marketability Discount (30.0%) (30.0%) (30.0%) plus Cash $1,000 $1,000 $1,000Recommended Valuation $18,333 $24,110 $37,110

8/10/200715

M&A Analysis

Universe of Software Acquisitions 2002

Acquirer Acquiree Purchase Price Revenue Multiple Software Sectors Median Price/SalesIBM Rational Software $2,100,000,000 3.2x Business Intelligence/Analytics 2.0xMicrosoft Navision $1,300,000,000 6.4x Content Management 1.9xFair Isaac & Company HNC Software $810,000,000 3.6x Consumer Relationship Management 0.7xVeritas Software Precise $537,000,000 7.5x Document Management 1.5xMicrosoft Rare Ltd. $375,000,000 NA E-Learning 1.2xBMC Software Peregrine $350,000,000 1.4x EAI/Milddleware 1.3xCadence Design Systems Simplex Systems $300,000,000 6.2x Engineering/CAD/CAM 2.2xNetIQ PentaSafe $255,000,000 7.1x Large Cap ERP 3.0xAdobe Systems Accelio Corporation $71,287,000 1.1x Gaming 1.2xBusiness Objects Acta Technology $65,000,000 2.6x Human Resource 1.7xInktomi Quiver $12,000,000 4.8x Infrastructure 3.3xPeopleSoft Calico Commerce $5,000,000 0.3x Internet Pure Plays 2.6xSyngistix Ecometry Corporation $36,250,000 1.4x IT Service 0.7xBorland Software Starbase Corporation $24,000,000 0.6x Network/Systems Management 2.4xBorland Software Togethersoft Corporation $185,000,000 3.6x Security 2.9xASG Corporation Landmark Systems $59,100,000 1.0x Software Development Tools 1.7xIntuit Blue Ocean Software $170,000,000 3.4x Storage 1.5xAspen Technology Hyprotech $99,000,000 1.4x Supply Chain Management 1.5xCognos Software Adaytum Software $160,000,000 2.8x Wireless 1.0xMaptics Frontstep $50,100,000 0.6x Average 1.8xSSA Global Technologies Infinium Software $94,500,000 1.4x Source: Corum Mergers & AcquisitionsLawson Software Armature Holdings $7,750,000 1.4xItron Regional Economic Research $14,000,000 1.8x

Average 2.9xHigh 7.5x

Low 0.3xStripped Mean 2.8x

8/10/200716

The “VC” or DCF Method

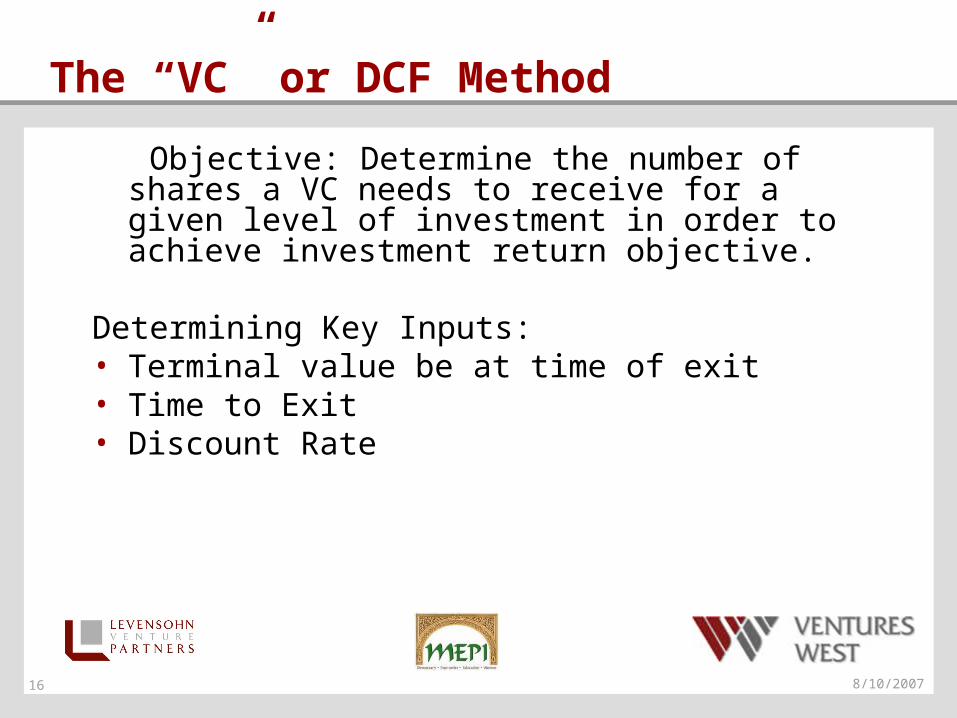

Objective: Determine the number of shares a VC needs to receive for a given level of investment in order to achieve investment return objective.

Determining Key Inputs:• Terminal value be at time of exit • Time to Exit• Discount Rate

8/10/200717

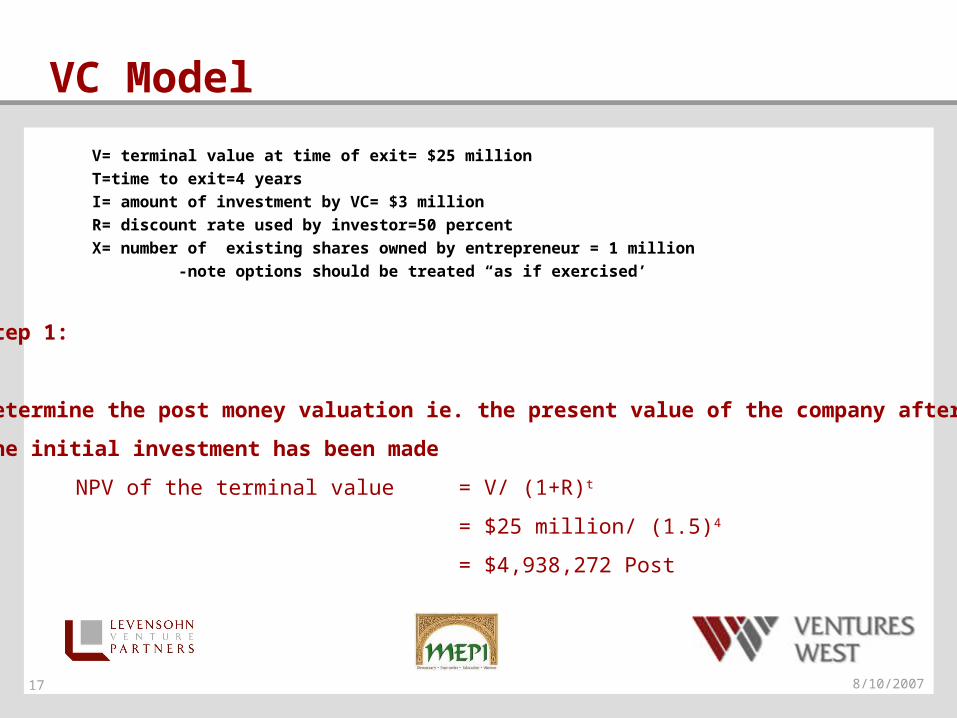

VC Model

V= terminal value at time of exit= $25 million

T=time to exit=4 years

I= amount of investment by VC= $3 million

R= discount rate used by investor=50 percent

X= number of existing shares owned by entrepreneur = 1 million

-note options should be treated “as if exercised’

Step 1:

Determine the post money valuation ie. the present value of the company after

the initial investment has been made

NPV of the terminal value = V/ (1+R)t

= $25 million/ (1.5)4

= $4,938,272 Post

8/10/200718

VC Model

V= terminal value at time of exit= $25 million

T=time to exit=4 years

I= amount of investment by VC= $3 million

R= discount rate used by investor=50 percent

X= number of existing shares owned by entrepreneur= 1 million

-note options should be treated “as if exercised’

Step 2:

Determine the pre- money valuation

PRE = Post – investment cost

= $4,938,272 - $3 million

=$1,938,272

8/10/200719

VC Model

V= terminal value at time of exit= $25 million

T=time to exit=4 years

I= amount of investment by VC= $3 million

R= discount rate used by investor=50 percent

X= number of existing shares owned by entrepreneur = 1 million

-note options should be treated “as if exercised’

Step 3:

Determine the ownership fraction required to achieve required rate of return

Ownership Fraction = $3 million/ $4,938,272

=60.75%

8/10/200720

VC Model

V= terminal value at time of exit= $25 million

T=time to exit=4 years

I= amount of investment by VC= $3 million

R= discount rate used by investor=50 percent

X= number of existing shares owned by entrepreneur = 1 million

-note options should be treated “as if exercised’

Step 4:

Calculate the number of shares

If x = founders shares and

y = # of shares required

y/ (1,000,000 +y) = ownership fraction or 60.75%

y = 1,000,000 [(0.6075 / (1-0.6075)]

=1,547,771 shares

8/10/200721

VC Model

V= terminal value at time of exit= $25 million

T=time to exit=4 years

I= amount of investment by VC= $3 million

R= discount rate used by investor=50 percent

X= number of existing shares owned by entrepreneur = 1 million

-note options should be treated “as if exercised’

Step 5:

Calculate the Price Per Share

$3 million / 1,547,771= $1.94 per share

8/10/200722

The Art

• Beyond the numbers, countless other factors influence valuation– Market pressures of a deal– Prior investor or management expectations– Recent data on comparable financings– Level of comfort with company including

• Business plan• Executive team• Stage in the market

• Beyond valuation, there are many tools used to mitigate risk (Option pool, Liquidation Preferences, Participation, Drag-along) – This is Day 2

• Often we will use the financial model as a part of the negotiation and share the models with the entrepreneurs. This take some of the emotion out of the process

8/10/200723

Case Study: Shotspotter

• Shotspotter Gunshot Location system– Combination of themes: wireless technology, mesh networks,

GPS technology, and acoustic algorithms

• Met CEO at conference

• Company had history of successful field deployments in public Safety

• Well suited to multiple markets

8/10/200724

Case Study: The Process

• Initial meetings to understand company and meet team

• Subsequent meetings to understand the technology, business model, customers, traction, etc…

• Customers are important part of our diligence. Spoke with existing and potential customers. Looking to hear commitment and believe that SS is relieving a pain

• Technology Demonstration

• Intellectual property – Hired IP attorney to review the portfolio

• Deployment process and costs

• Pipeline review

8/10/200725

Case Study: Key Findings

• Public safety market progressing, but less certainty around military– Worked through strategy to penetrate military market

– Bottom line, Military remained a risk and was factored into valuation

• Revenue Forecast was too aggressive– Discounted as a part of the valuation exercise

• No immediate competitive threat, but patent portfolio important– IP Attorney helped company identify areas of weakness and plan put in

place

• Margins were too low for the business– Worked with company to understand plan to bring them in line

8/10/200726

Case Study: The Valuation

• We were pre-emptive and the company was not out officially raising money

• We did not want to overpay, but understood that if we were too low, they would talk to other VCs for a higher valuation

• Worked on a comp analysis, M&A analysis, and even a DCF. Modeled the round and the returns for all of the investors

• Disagreed over the revenue forecast and got creative with the valuation

8/10/200727

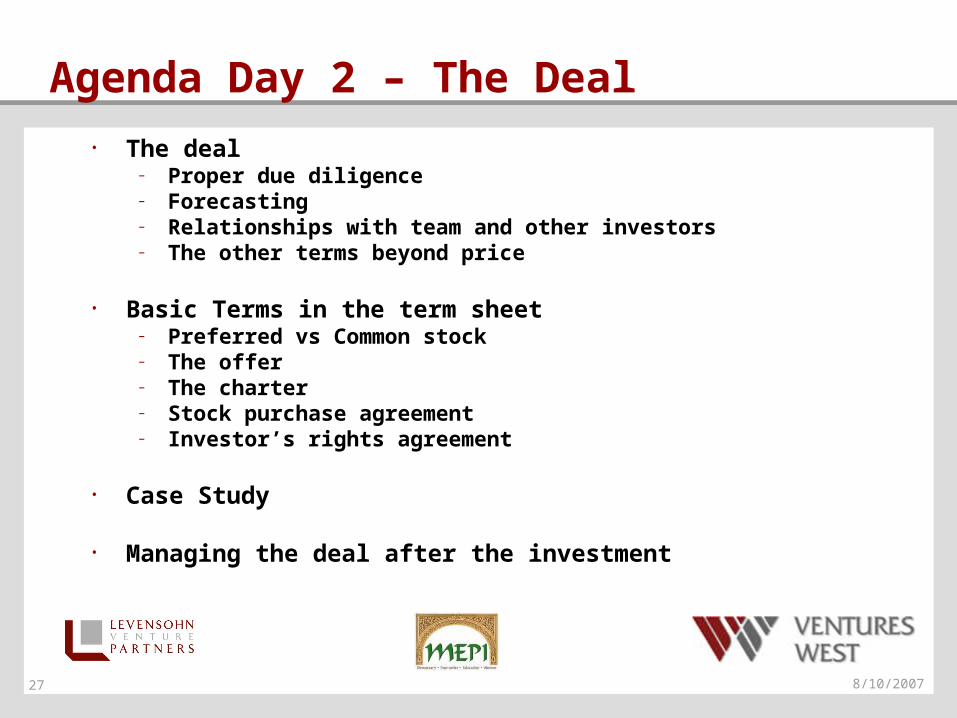

Agenda Day 2 – The Deal• The deal

– Proper due diligence– Forecasting– Relationships with team and other investors– The other terms beyond price

• Basic Terms in the term sheet– Preferred vs Common stock– The offer– The charter– Stock purchase agreement– Investor’s rights agreement

• Case Study

• Managing the deal after the investment

8/10/200728

Deal Negotiation

• Experienced VCs and Entrepreneurs understand that valuation alone is a small part of the investment process

• Critical elements to a deal– Proper due diligence– Working relationship with team– Relationship with existing investors– Term Sheet

8/10/200729

Proper Due Diligence

• The management team– Personal reference checks

• Technology (if applicable)– Consultants that can help to validate

• Business model

• Pipeline review– Customer reference checks

• Financials including forecast

• Legal due diligence – Intellectual property review– Existing company documents around governance

8/10/200730

Forecasting in Venture Capital

• It is the responsibility of the entrepreneur to provide a well thought analysis of the market opportunity and the cost structure needed to properly to execute on the opportunity

• A VC must pay attention to a number of factors including– Product development– Margins on product– Cash burn and cash out date– Critical milestones– Validation of near term sales forecasts– Fixed costs such as office space and other contractual money owed (in case of

shut down)

• A sensitivity analysis is a critical tool for evaluating the risks in a forecast

8/10/200731

Board Dynamics

• Critical to have aligned interests among board members and entrepreneurs

• Prior to any investment, must speak with each member of the board and the management team to

• White papers with best practices for Board Participation– A Simple Guide to The Basic Responsibilities of VC-Backed Company

Directors – After the Term Sheet: How Venture Boards Influence the Success or

Failure of Technology Companies – Rites of Passage: Managing CEO Transition in Venture-Backed

Technology Companies

• http://www.levp.com/news/whitepapers.shtml

8/10/200732

The Term Sheet

• Starting point for a good faith negotiation/ few binding provisions

• Structure contracts to protect investment from negligence or malice

Four Sections of a Term Sheet

1. The basic description of the offer

2. The Charter

3. Stock Purchase Agreement

4. Investor Rights Agreement

8/10/200733

Preferred vs Common Stock

• Common Stock– The basic stock held by founders, employees, and public shareholders

upon IPO– In general, provides basic voting privileges

• Preferred Stock– Preferred shares give holders preference over Common shares– Seniority in liquidation (i.e. preferred shareholder paid first)– Seniority in payment of dividends– Special privileges documented in the Shareholders agreement including

Board Seat, voting rights on additional capital, right to participate in future financings, and ability to veto the choice of CEO

– Right to approve spending

• VCs almost always take Preferred Stock

8/10/200734

Basic Offer

• Fully Diluted Ownership- assumes all preferred stock is converted and options are exercised

• Original Purchase Price- price paid per share

• Capitalization Table- lists all securities in the capital structure before and after the deal -typically includes common, preferred, options pool

• Aggregate Purchase Price- price paid for all shares of a security

• Post-money Valuation= price per share*fully diluted share count -analogous to market cap for a public company

• Pre-money Valuation= post money valuation-$ investment

8/10/200735

The Charter

• The Charter establishes the rights, preferences, privileges and restrictions of each class and series of the company’s stock

• Dividend Preference- restricts the payment of dividends to common stock unless first paid to preferred

– cumulative dividends accrue even if not paid– non cumulative dividends do not accrue except in the final period prior to payment

• Deemed Liquidation Event- sale, merger or shut down– Liquidation Preference- determines where an investor stands in the investor hierarchy in the case of a

liquidation event– pari passu means all (or some) preferred investors are treated equally – 3X liquidation preference means an investor get back triple their investment before any other equity claims

are satisfied

• Preferred Stock– Non- participating Preferred Stock- receives only Original Purchase price plus any accrued dividends– Fully Participating Preferred Stock- receives Original Purchase price plus accrued dividends and then

participates with commons stockholders on an as-converted basis.– Cap on Preferred Stock Participation Rights- receives Original Purchase Price plus accrued dividends and

participates with common stock up to an agreed multiple of the Original Purchase Price

• Protective Provisions- give minority investors a laundry list of protections against possible expropriation by managers or other investors

8/10/200736

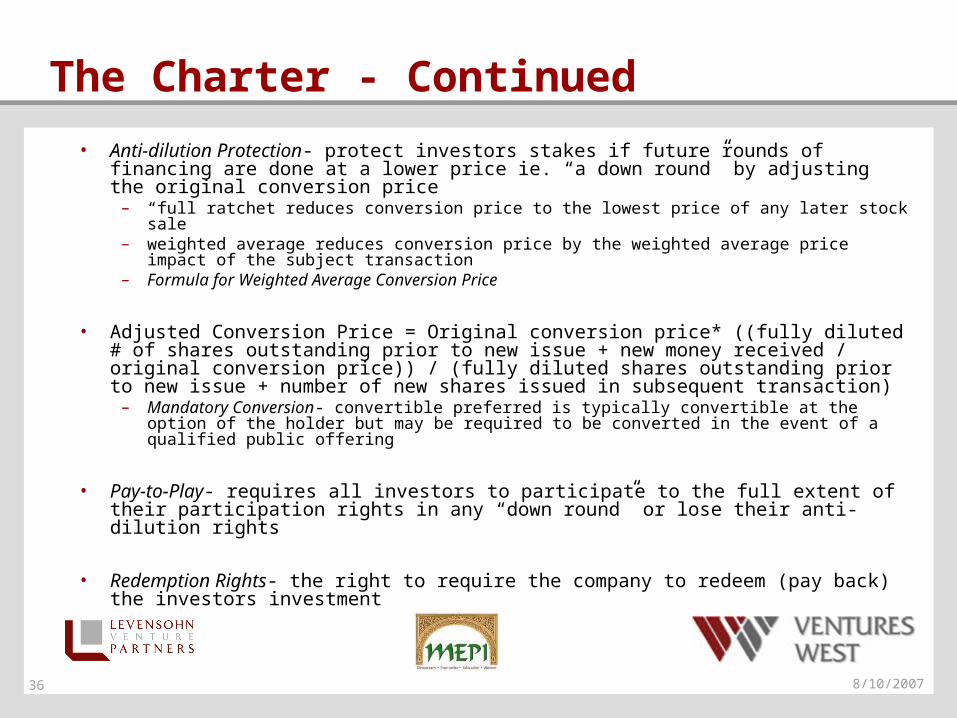

The Charter - Continued

• Anti-dilution Protection- protect investors stakes if future rounds of financing are done at a lower price ie. “a down round” by adjusting the original conversion price

– “full ratchet reduces conversion price to the lowest price of any later stock sale– weighted average reduces conversion price by the weighted average price impact of the

subject transaction– Formula for Weighted Average Conversion Price

• Adjusted Conversion Price = Original conversion price* ((fully diluted # of shares outstanding prior to new issue + new money received / original conversion price)) / (fully diluted shares outstanding prior to new issue + number of new shares issued in subsequent transaction)

– Mandatory Conversion- convertible preferred is typically convertible at the option of the holder but may be required to be converted in the event of a qualified public offering

• Pay-to-Play- requires all investors to participate to the full extent of their participation rights in any “down round” or lose their anti-dilution rights

• Redemption Rights- the right to require the company to redeem (pay back) the investors investment

8/10/200737

Stock Purchase Agreement

• Contains company reps and warranties • Conditions to closing and • Outlines responsibilities for fees and expenses.

8/10/200738

Investor Rights Agreement

• Matters pertaining to a company going public

• Matters Requiring Investor Approval- give minority investors a laundry list of protections against possible expropriation by managers or other investors.

• Employee Stock Options- shares or options set aside for employee compensation and incentives - cliff vs. step vesting

8/10/200739

Case Study – McLean Watson/Media Synergy Inc

8/10/200740

After the Investment

• Due diligence and reviews on valuation continue after the investment

• Follow-on investments

• On-going portfolio valuation

• The exit

Recommended