3. What do you want your post-retirement standard of living to be?

Realistic strategy is to plan on having the same standard of living both pre- and post-retirement.

Retirement Income Options for Discretionary Retirement Savings?

Typical Considerations include: minimizing risk (via diversification) minimizing taxes some liquidity ease of transfer upon the death of the

retiree

What happens to my property if I die without a will? Probate

Legal process required to administer an estate or a will Only legal way to change the title when the owner has died

Costly $1500-$2000 for the average estate in Utah

Time consuming National average = 9 months – 2 years UT typically 2-3 months

Source: Kyle H. Barrick, estate planning attorney

Intestate Succession Laws Intestate succession laws

Property transfers with no will according to the law of the state in which you reside

Surviving spouse; descendents; parents; descendents of parents; ½ to each set of grandparents or descendents of grandparents; state of Utah school fund

120 – hour survival rule If you do not survive the decedent by 120 hours, you are treated

as predeceasing the decedent Step-parent rules

If decedent has descendents that are not descendents of the surviving spouse, the spouse inherits $50,000 plus ½ of the balance of the remaining estate

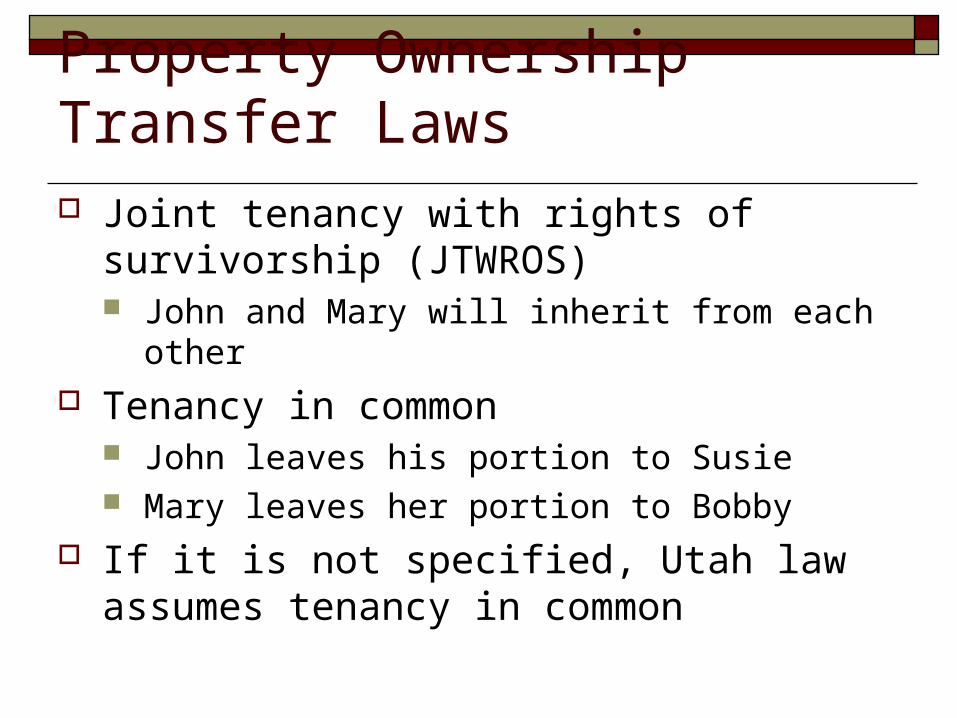

Property Ownership Transfer Laws Joint tenancy with rights of survivorship

(JTWROS) John and Mary will inherit from each other

Tenancy in common John leaves his portion to Susie Mary leaves her portion to Bobby

If it is not specified, Utah law assumes tenancy in common

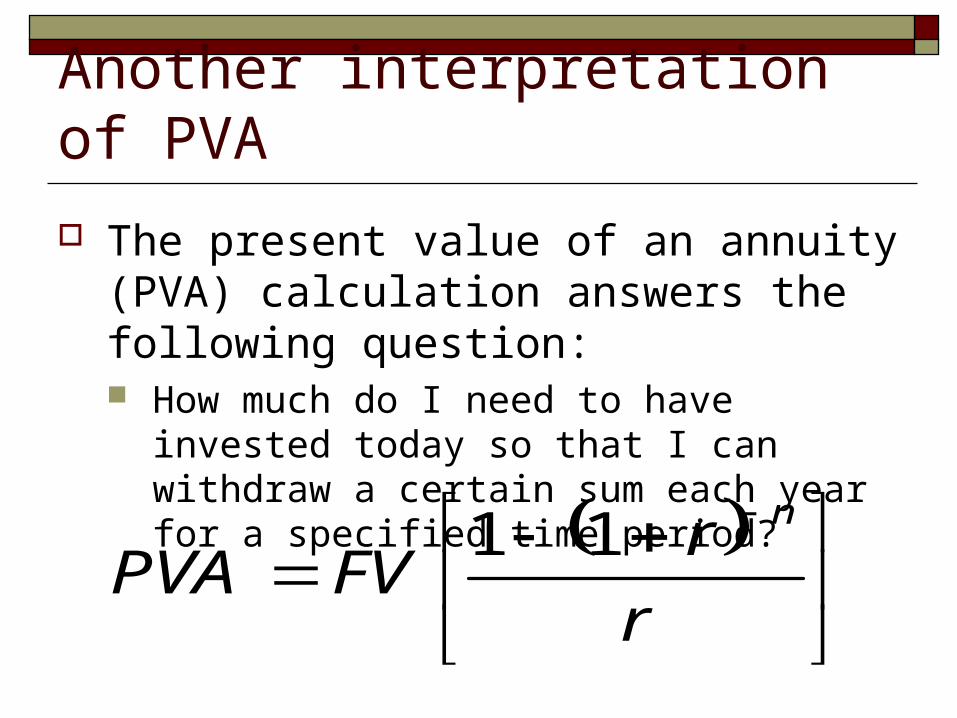

The present value of an annuity (PVA) calculation answers the following question: How much do I need to have invested today so

that I can withdraw a certain sum each year for a specified time period?

r

rFVPVA

n11

Another interpretation of PVA

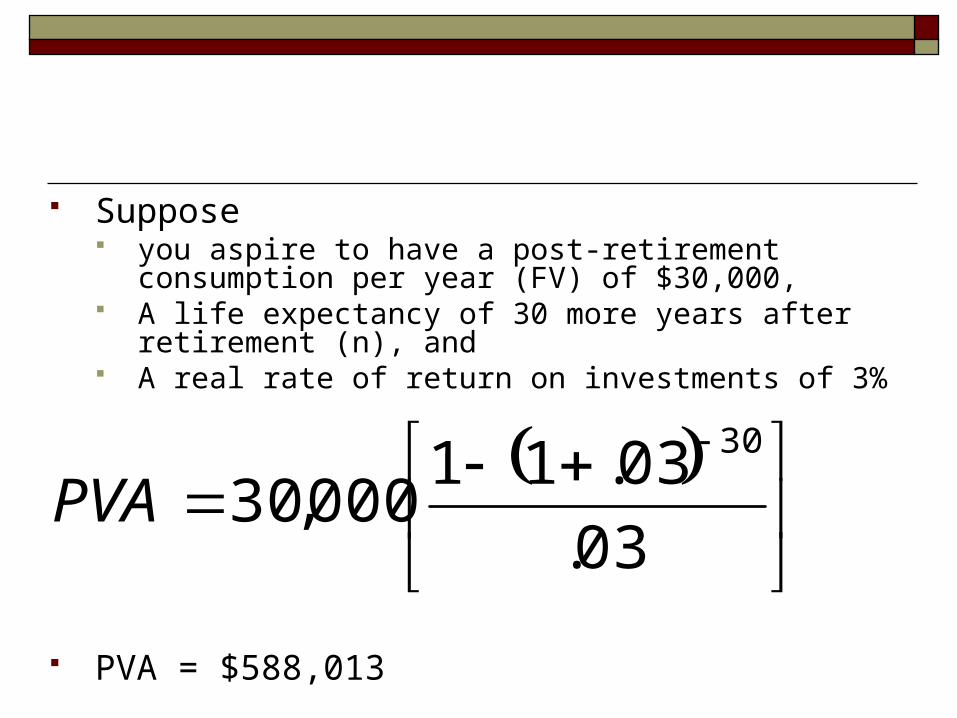

Suppose you aspire to have a post-retirement consumption per year

(FV) of $30,000, A life expectancy of 30 more years after retirement (n), and A real rate of return on investments of 3%

PVA = $588,013

03.

03.11000,30

30

PVA

4. What interest rate will you get on retirement investments? Difficult to answer with high degree of accuracy

because of investment risks

But remember… The real rate of return on ALL financial investments

has averaged 3.5% over the last 100 years And the real rate of return on stock market

investments has averaged 7 % over the last 100 years

5. What other retirement saving is being done for you?

Social Security Private Pension Plans

There are some elements of risk associated with each of these...

Risks with mandatory savings plans...

Social Security solvency of plan in the future future changes in eligibility rules

Private Pension Plans DB plans and default risk - Pension Benefit

Guaranty Corporation DB plans and vesting requirements /

portability

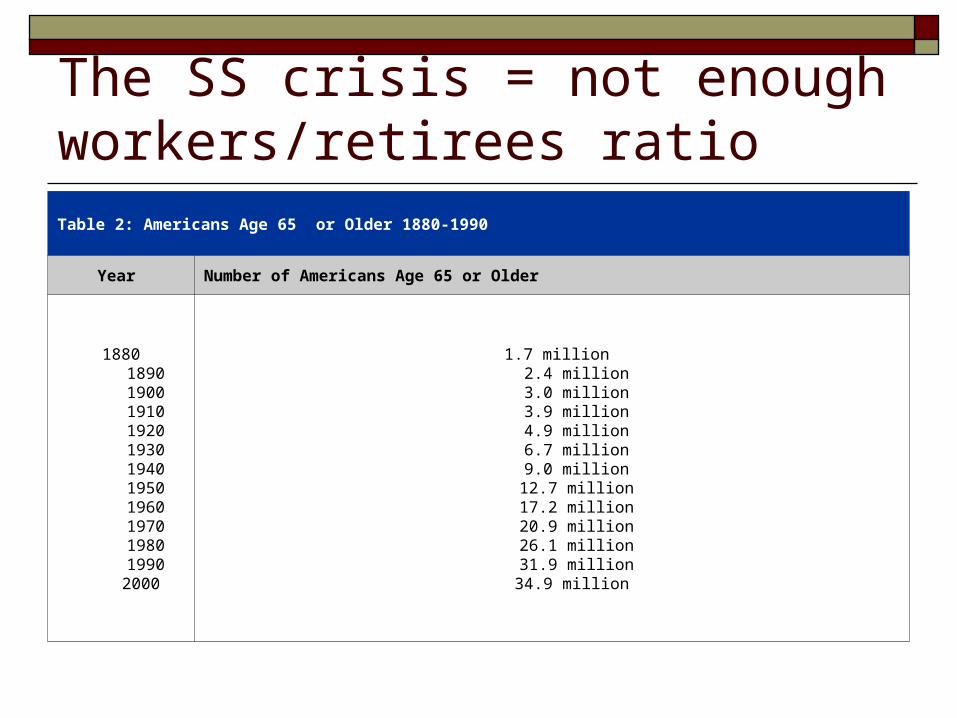

The SS crisis = not enough workers/retirees ratioTable 2: Americans Age 65 or Older 1880-1990

Year Number of Americans Age 65 or Older

1880189019001910192019301940195019601970198019902000

1.7 million2.4 million3.0 million3.9 million4.9 million6.7 million9.0 million12.7 million17.2 million20.9 million26.1 million31.9 million34.9 million

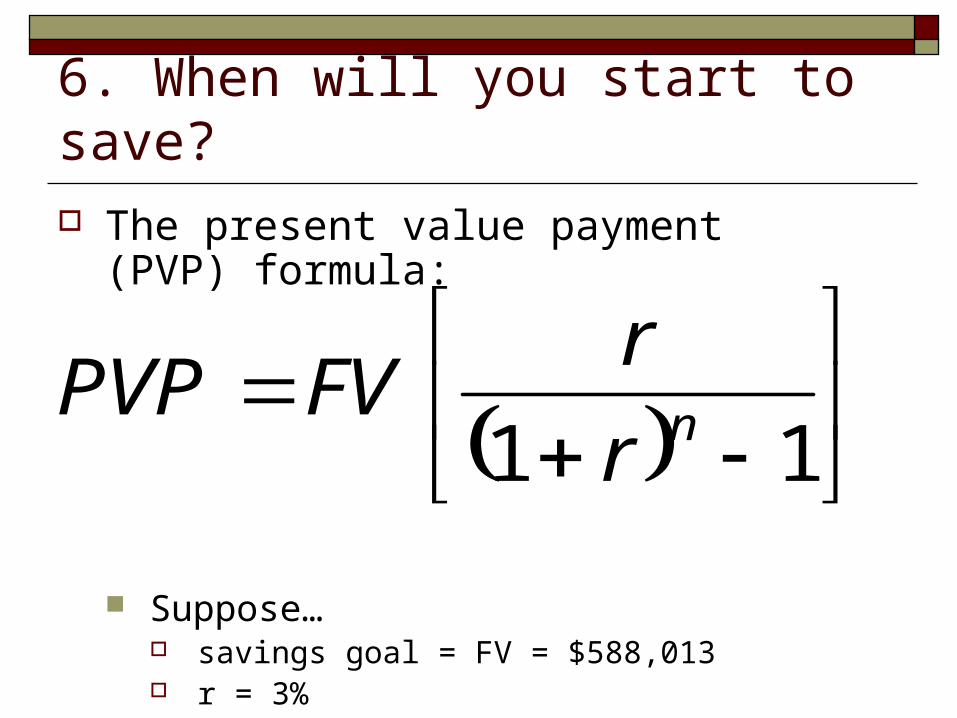

6. When will you start to save? The present value payment (PVP) formula:

Suppose… savings goal = FV = $588,013 r = 3%

11 nr

rFVPVP

103.1

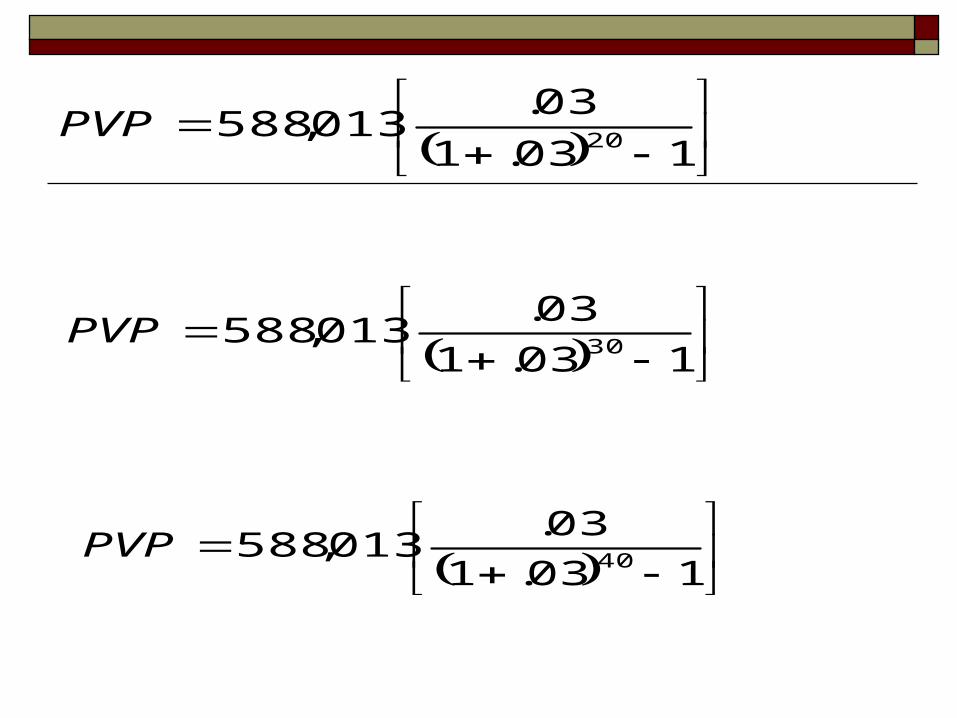

03.013,588 30PVP

103.1

03.013,588 20PVP

103.1

03.013,588 40PVP

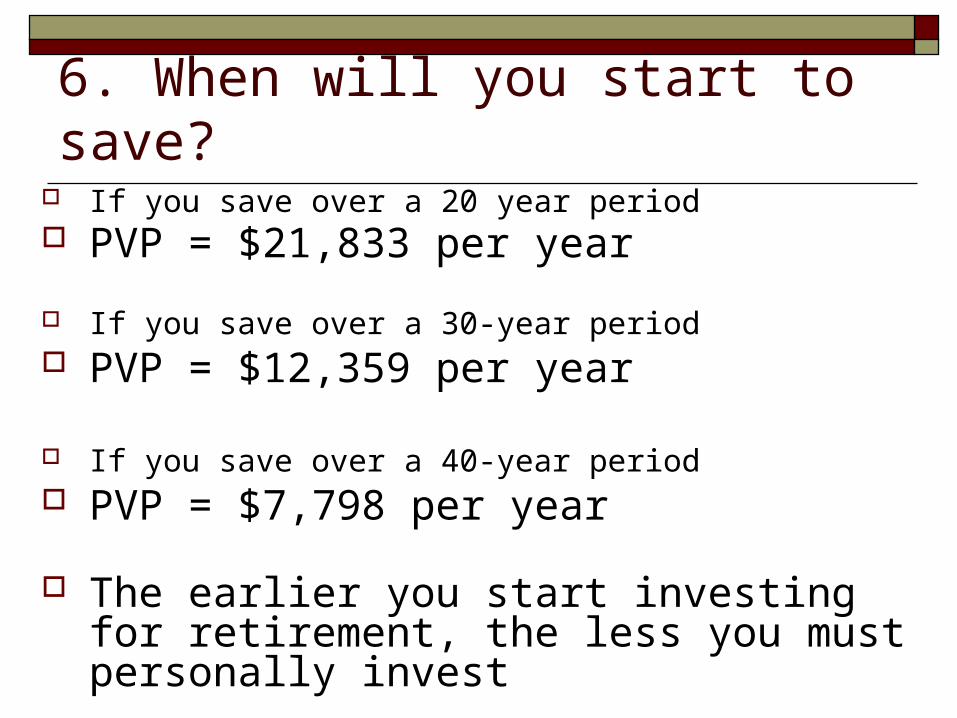

6. When will you start to save? If you save over a 20 year period PVP = $21,833 per year

If you save over a 30-year period PVP = $12,359 per year

If you save over a 40-year period PVP = $7,798 per year

The earlier you start investing for retirement, the less you must personally invest

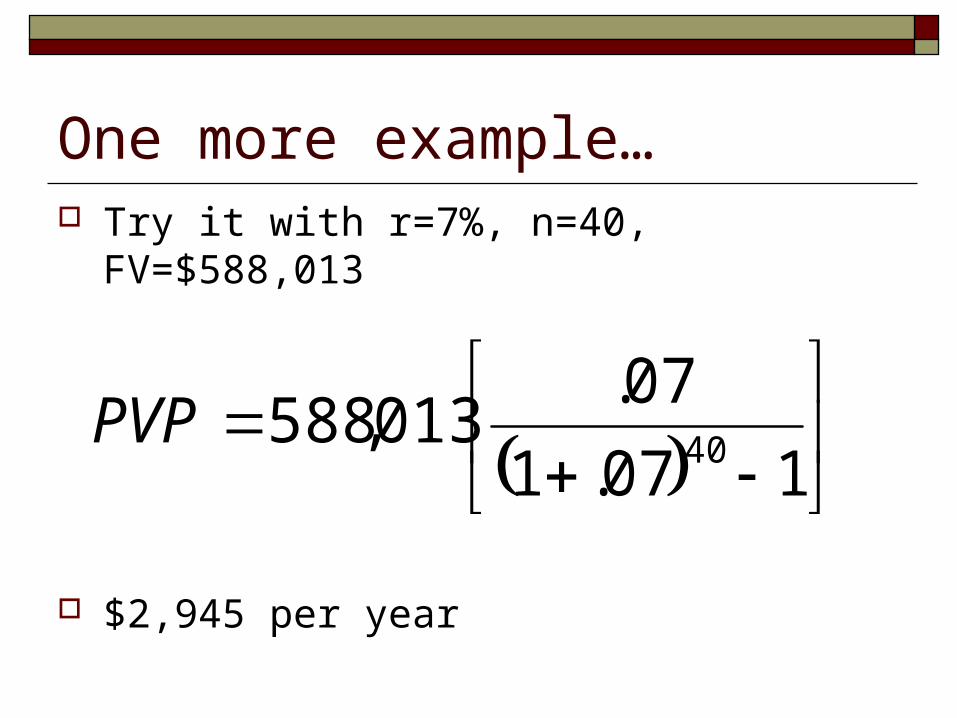

One more example… Try it with r=7%, n=40, FV=$588,013

$2,945 per year

107.1

07.013,588 40PVP

Just remember… Increased retirement savings = Increased Freedom

Don’t rely on the govt or an inheritance Take responsibility for yourself ANYONE can become a millionaire It’s all about choices

How much should you invest for retirement?

A common benchmark figure used by financial planners is 10% of your income This assumes that your income will grow at a

7% real r before retirement and 3% real r after retirement

Assumes the same pre- and post-retirement consumption

But, this savings goal may be more daunting if...

Labor force participation is intermittent reduces Social Security and risks eligibility reduces likelihood of vesting in a private pension plan

(temptation to cash out if option offered!)

Earnings are low high opportunity costs of investing for retirement can’t capitalize on tax advantages of defined

contribution plans, IRA’s, etc.

Who’s at Greatest Risk of Under-Saving for Retirement? Women

Greater discontinuities in labor market work More likely to think of husband as being the

only one who needs to have retirement savings because he is consistent wage earner.

Reliance on Social Security dependent benefits as “retirement savings”

Greater longevity

But… four out of five women who do not end their

marriages through divorce will out-live their husbands

these women on average will live another 15 years (with little prospect of remarriage)

In those households where husbands have private pension plans, 60% do not continue after his death

Social Security benefits are also cut back when a spouse dies

Roughly 1/3 of all newly widowed women who were non-poor prior to their husbands’ deaths experience one or more years of poverty in the first five years after they become widows

BOTTOM LINE - Saving for retirement is critical for women

Pros fess up to their retirement-building blunders USA Today 9/23/07 Mark Zandi (Chief Economist at

Economy.com) Mistake: Letting savings languish

He saved in low-yielding cash instruments through his 30s

Wishes he had set up automatic transfers to a stock index fund

Sheryl Garrett (founder of Garrett Planning Network: fee-only financial planners for middle income consumers) Mistake: Investing in time shares

Skip the freebies and don’t get caught up in the pitch Time shares are more expensive than you think

Tom Gardner (founder of The Motley Fool) Mistake: Selling too soon

Think of yourself as an investor in the business, and not an investor in stock

Quotes Buffett saying, “I would have made more money if I had never sold a share of stock I’d bought since I was 11 years old. I lost a lot of money fiddling around.”

Robert Willens (managing director Lehman Bros) Mistake: Waiting too long to sell

Have a stop-loss in your head: I will sell if it loses this much…

Jim Gillespie (CEO of Coldwell Banker) Mistake: Begin saving too late

Start now! Don’t wait for 8-10 years

Robert Rodriguez (manager of FPA funds) Mistake: Overconfidence

Always be suspicious – don’t think you know more than you really do

Recommended