Valuation of anindustrial company

Pavia University

November 2014www.pwc.com

Agenda

1 Overview 1

2 Business Plan analysis 3

3 Discounted Cash Flow method 10

3.1 Business Plan: cash flow analysis 12

3.2 Figurative taxes on EBIT 15

3.3 Discount rate (WACC) 17

3.4 Terminal value 24

3.5 Surplus assets 30

3.6 DCF results 32

3.7 Sensitivity analysis 40

4 Market multiple methodology 44

5 Equity Value 48

Page

PwCNovember 2014

OverviewSection 1

Valuation of an industrial company • Pavia University1

PwCNovember 2014

The Group

We were asked to assist the Group in the estimate of its Enterprise Value, whichcan be divided in two separate business units:

– Business Unit Alfa: operating in the automotive lubricants industry. This sector ischaracterized by agreements between the carmakers and the oil producers for the"First Fill“

– Business Unit Beta: operating in the car cleaning and maintenance industry

Section 1 – Overview

Valuation of an industrial company • Pavia University2

PwCNovember 2014

Business Plan analysisSection 2

Valuation of an industrial company • Pavia University3

PwCNovember 2014

Business Plan analysis

Basis ofinformation:

approvedBusiness Plan

To determine the EV, the two business units were valuatedseparately in relation to different reference markets and totake into account the different risk profiles.

To do this, as a first step we analyzed the twobusinesses in order to understand the differentunderlying riskiness and specificities, which maybe taken into account in our valuation.

Section 2 – Business Plan analysis

Valuation of an industrial company • Pavia University4

PwCNovember 2014

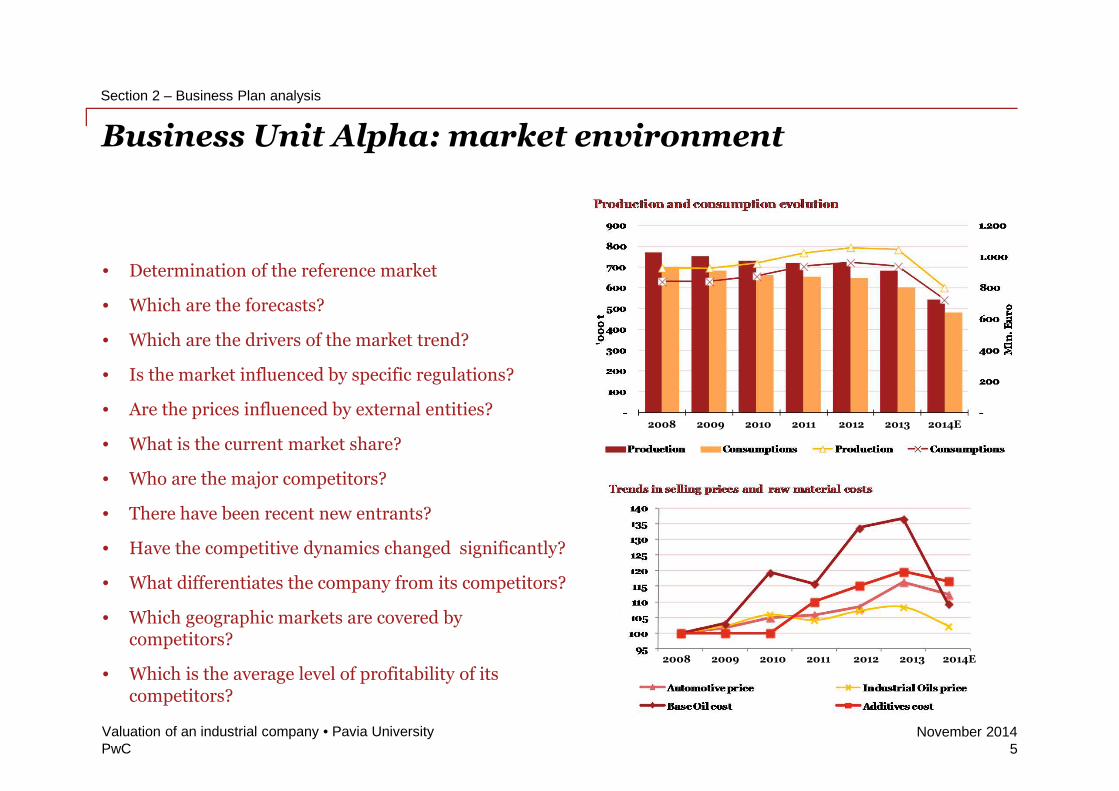

Business Unit Alpha: market environment

• Determination of the reference market

• Which are the forecasts?

• Which are the drivers of the market trend?

• Is the market influenced by specific regulations?

• Are the prices influenced by external entities?

• What is the current market share?

• Who are the major competitors?

• There have been recent new entrants?

• Have the competitive dynamics changed significantly?

• What differentiates the company from its competitors?

• Which geographic markets are covered bycompetitors?

• Which is the average level of profitability of itscompetitors?

Section 2 – Business Plan analysis

Valuation of an industrial company • Pavia University5

2006 2007 2008 2009 2010 2011 2012E

2006 2007 2008 2009 2010 2011 2012E

2008 2009 2010 2011 2012 2013 2014E

2006 2007 2008 2009 2010 2011 2012E2008 2009 2010 2011 2012 2013 2014E

PwCNovember 2014

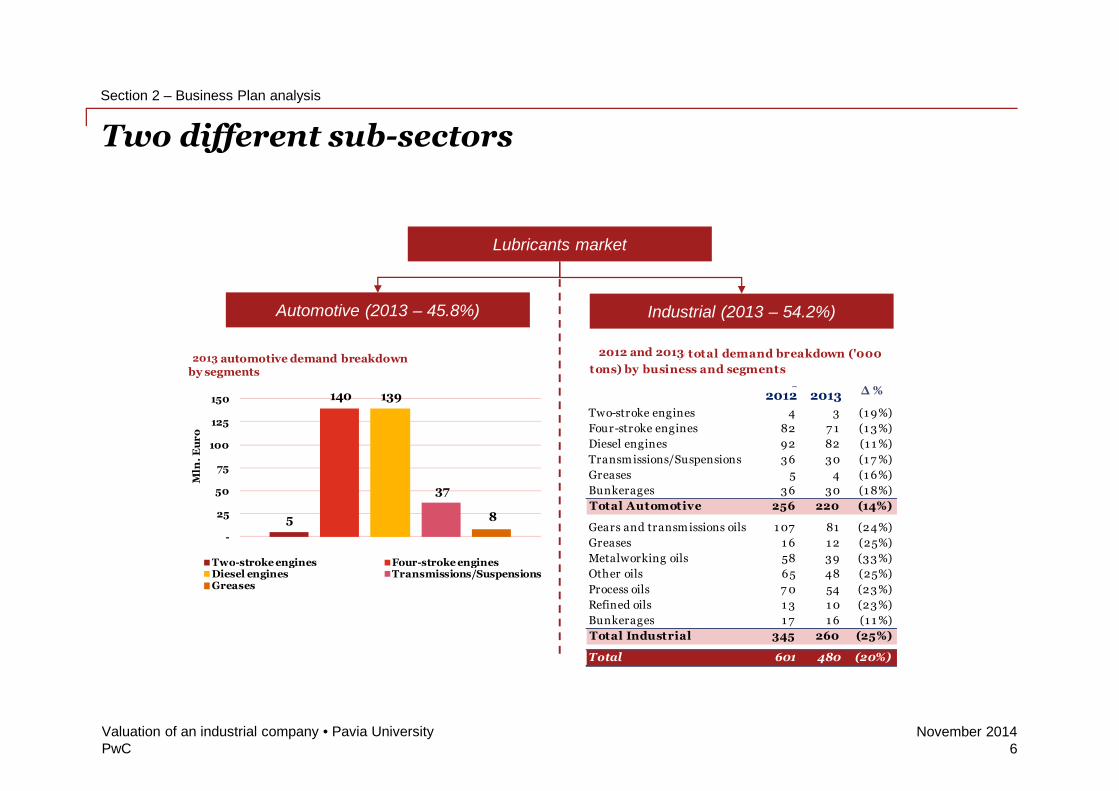

Two different sub-sectors

Automotive (2013 – 45.8%) Industrial (2013 – 54.2%)

Lubricants market

Section 2 – Business Plan analysis

Valuation of an industrial company • Pavia University6

5

140 139

37

8

-

25

50

75

100

125

150

Mln

.E

ur

o

2009 automotive demand breakdownby segments

Two-stroke engines Four-stroke enginesDiesel engines Transmissions/SuspensionsGreases

2008 2009 ∆ %

Two-stroke engines 4 3 (1 9%)

Four-stroke engines 82 7 1 (1 3%)

Diesel engines 92 82 (1 1 %)

Transmissions/Suspensions 36 30 (1 7 %)

Greases 5 4 (1 6%)

Bunkerages 36 30 (1 8%)

Total Automotive 256 220 (14%)

Gears and transmissions oils 1 07 81 (24%)

Greases 1 6 1 2 (25%)

Metalworking oils 58 39 (33%)

Other oils 65 48 (25%)

Process oils 7 0 54 (23%)

Refined oils 1 3 1 0 (23%)

Bunkerages 1 7 1 6 (1 1 %)

Total Industrial 345 260 (25%)

Total 601 480 (20%)

2008 and 2009 total demand breakdown ('000

tons) by business and segments2013

2012 and 2013

2012 2013

PwCNovember 2014

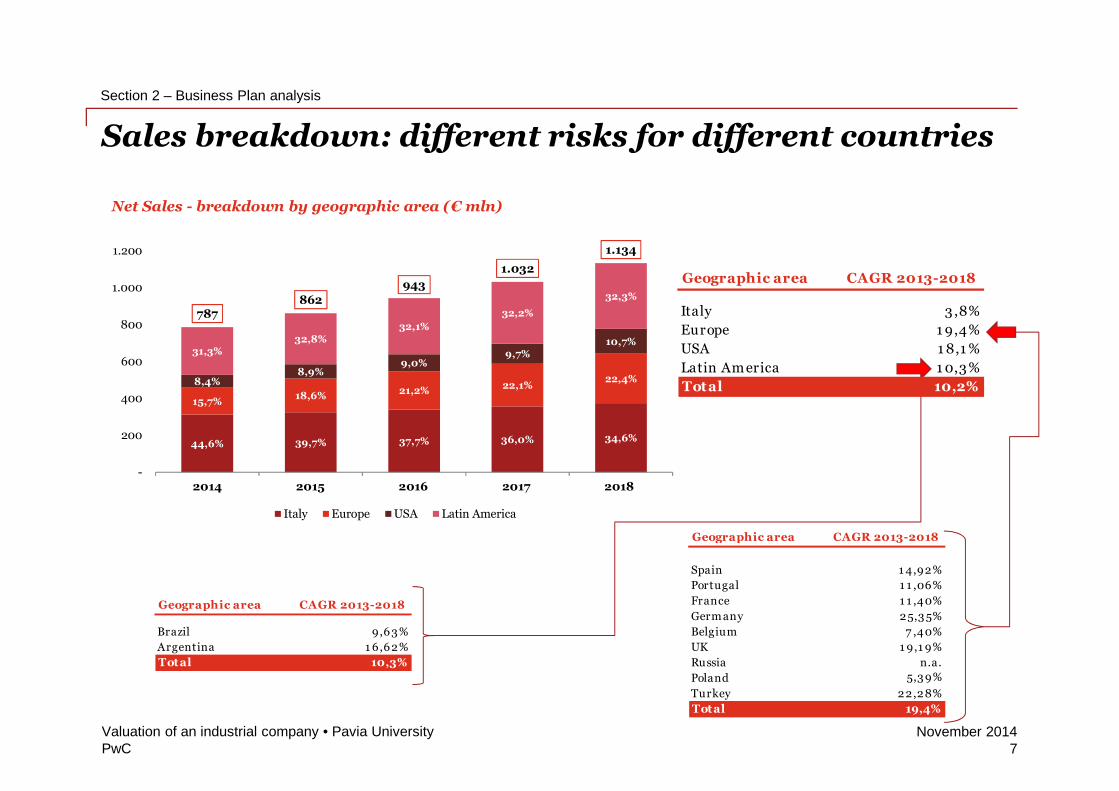

44,6% 39,7% 37,7% 36,0% 34,6%

15,7%18,6% 21,2%

22,1%22,4%8,4%

8,9%9,0%

9,7%10,7%

31,3%32,8%

32,1%

32,2%

32,3%

787862

943

1.032

1.134

-

200

400

600

800

1.000

1.200

2014 2015 2016 2017 2018

Net Sales - breakdown by geographic area (€ mln)

Italy Europe USA Latin America

Sales breakdown: different risks for different countries

Section 2 – Business Plan analysis

Valuation of an industrial company • Pavia University7

Geographic area CAGR 2013-2018

Italy 3 ,8%

Europe 1 9,4%

USA 1 8,1 %

Latin Am erica 1 0,3%

Total 10,2%

Geographic area CAGR 2013-2018

Spain 1 4,92%

Portugal 1 1 ,06%

France 1 1 ,40%

Germ any 25,3 5%

Belgium 7 ,40%

UK 1 9,1 9%

Russia n.a.

Poland 5,3 9%

Turkey 22,28%

Total 19,4%

Geographic area CAGR 2013-2018

Brazil 9,63%

Argentina 1 6,62%

Total 10,3%

PwCNovember 2014

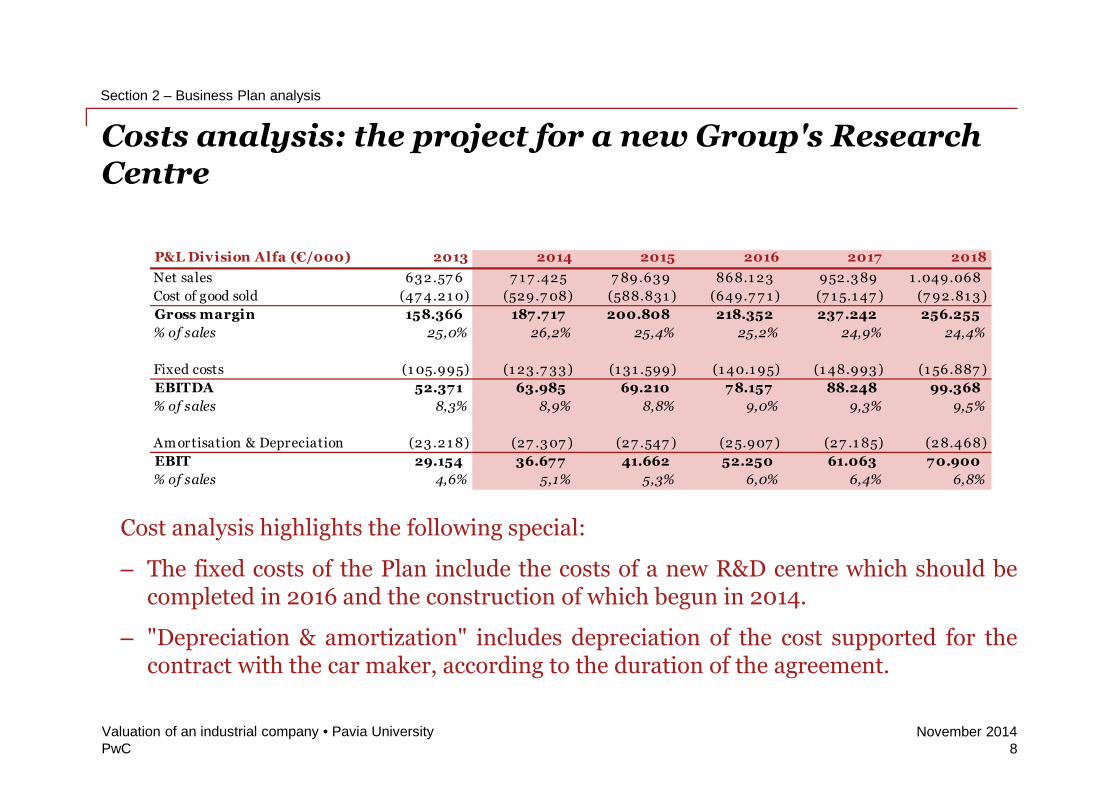

Costs analysis: the project for a new Group's ResearchCentre

Section 2 – Business Plan analysis

Valuation of an industrial company • Pavia University8

Cost analysis highlights the following special:

– The fixed costs of the Plan include the costs of a new R&D centre which should becompleted in 2016 and the construction of which begun in 2014.

– "Depreciation & amortization" includes depreciation of the cost supported for thecontract with the car maker, according to the duration of the agreement.

P&L Division Alfa (€/000) 2013 2014 2015 2016 2017 2018

Net sales 632.57 6 7 1 7 .425 7 89.639 868.1 23 952.3 89 1 .049.068

Cost of good sold (47 4.21 0) (529.7 08) (588.831 ) (649.7 7 1 ) (7 1 5.1 47 ) (7 92.81 3 )

Gross margin 158.366 187.717 200.808 218.352 237.242 256.255

% of sales 25,0% 26,2% 25,4% 25,2% 24,9% 24,4%

Fixed costs (1 05.995) (1 23 .7 33 ) (1 3 1 .599) (1 40.1 95) (1 48.993 ) (1 56.887 )

EBITDA 52.371 63.985 69.210 78.157 88.248 99.368

% of sales 8,3% 8,9% 8,8% 9,0% 9,3% 9,5%

Amortisation & Depreciation (23 .21 8) (27 .3 07 ) (27 .547 ) (25.907 ) (27 .1 85) (28.468)

EBIT 29.154 36.677 41.662 52.250 61.063 70.900

% of sales 4,6% 5,1% 5,3% 6,0% 6,4% 6,8%

PwCNovember 2014

Business Unit Beta

• Similarly, for Business Unit Beta were conducted the same analysis made forthe Business Unit Alpha:

– Analysis of competitive environment and market dynamics;

– Business Plan analysis

• From these analysis, the following features have to be taken into accountduring the valuation process:

– It isn’t required and flows normalization;

– The industry is significantly different with respect to the Business Unit Alfa(dynamics, competitors, reference markets, etc ..) and for this reason differentevaluation parameters were adopted for the two Business Units.

Section 2 – Business Plan analysis

Valuation of an industrial company • Pavia University9

PwCNovember 2014

Discounted Cash Flow methodSection 3

Valuation of an industrial company • Pavia University10

PwCNovember 2014

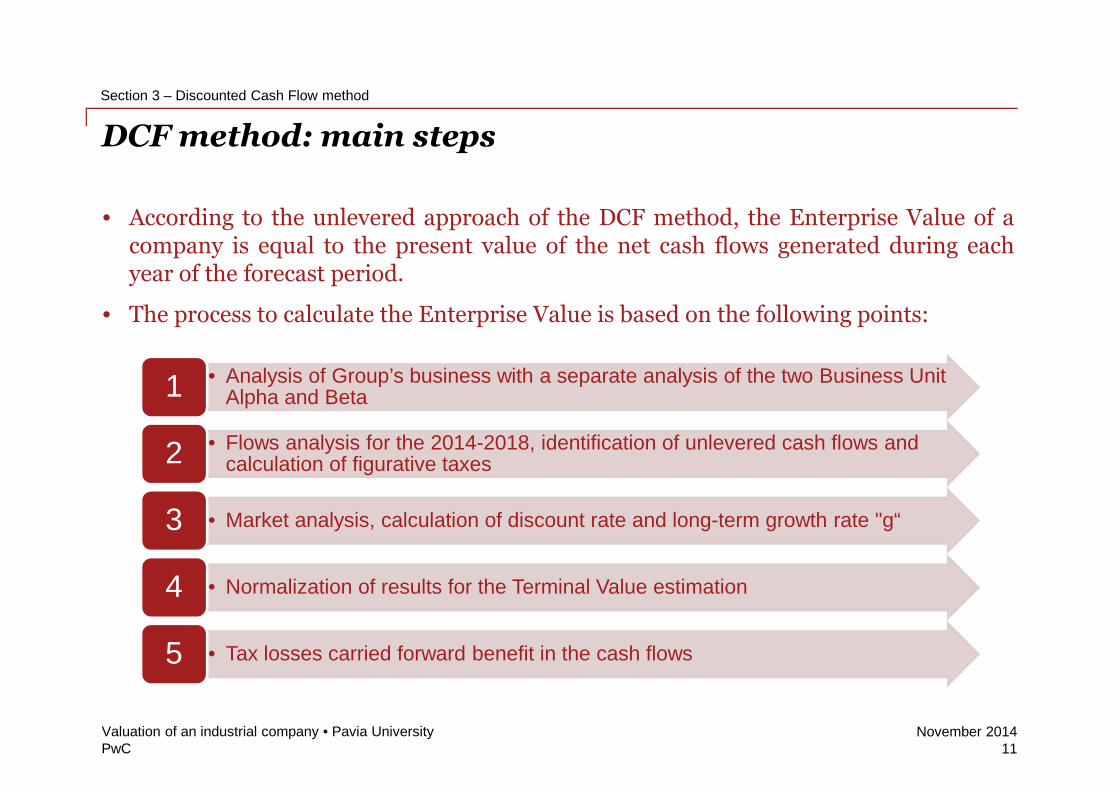

DCF method: main steps

• According to the unlevered approach of the DCF method, the Enterprise Value of acompany is equal to the present value of the net cash flows generated during eachyear of the forecast period.

• The process to calculate the Enterprise Value is based on the following points:

• Analysis of Group’s business with a separate analysis of the two Business UnitAlpha and Beta1

• Flows analysis for the 2014-2018, identification of unlevered cash flows andcalculation of figurative taxes2

• Market analysis, calculation of discount rate and long-term growth rate "g“3

• Normalization of results for the Terminal Value estimation4

• Tax losses carried forward benefit in the cash flows5

Section 3 – Discounted Cash Flow method

Valuation of an industrial company • Pavia University11

PwCNovember 2014

Business Plan: cash flow analysisSection 3.1

Valuation of an industrial company • Pavia University12

PwCNovember 2014

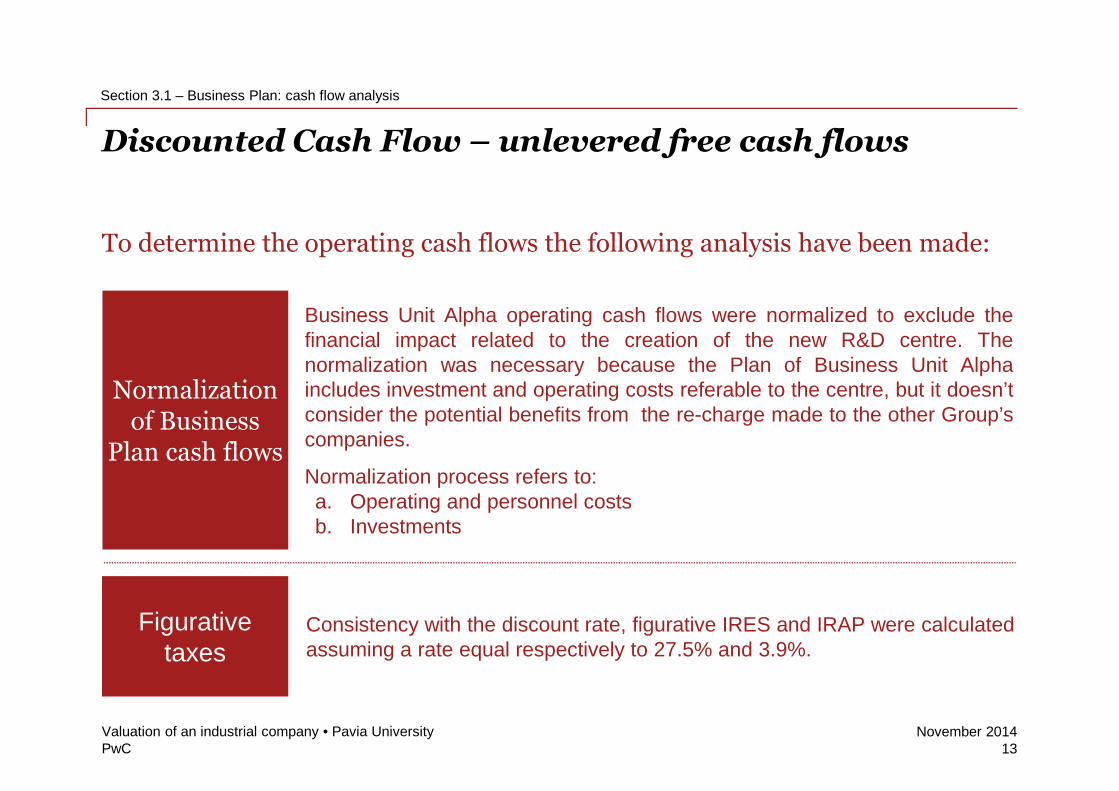

Discounted Cash Flow – unlevered free cash flows

Normalizationof Business

Plan cash flows

To determine the operating cash flows the following analysis have been made:

Figurativetaxes

Business Unit Alpha operating cash flows were normalized to exclude thefinancial impact related to the creation of the new R&D centre. Thenormalization was necessary because the Plan of Business Unit Alphaincludes investment and operating costs referable to the centre, but it doesn’tconsider the potential benefits from the re-charge made to the other Group’scompanies.

Normalization process refers to:a. Operating and personnel costsb. Investments

Consistency with the discount rate, figurative IRES and IRAP were calculatedassuming a rate equal respectively to 27.5% and 3.9%.

Section 3.1 – Business Plan: cash flow analysis

Valuation of an industrial company • Pavia University13

PwCNovember 2014

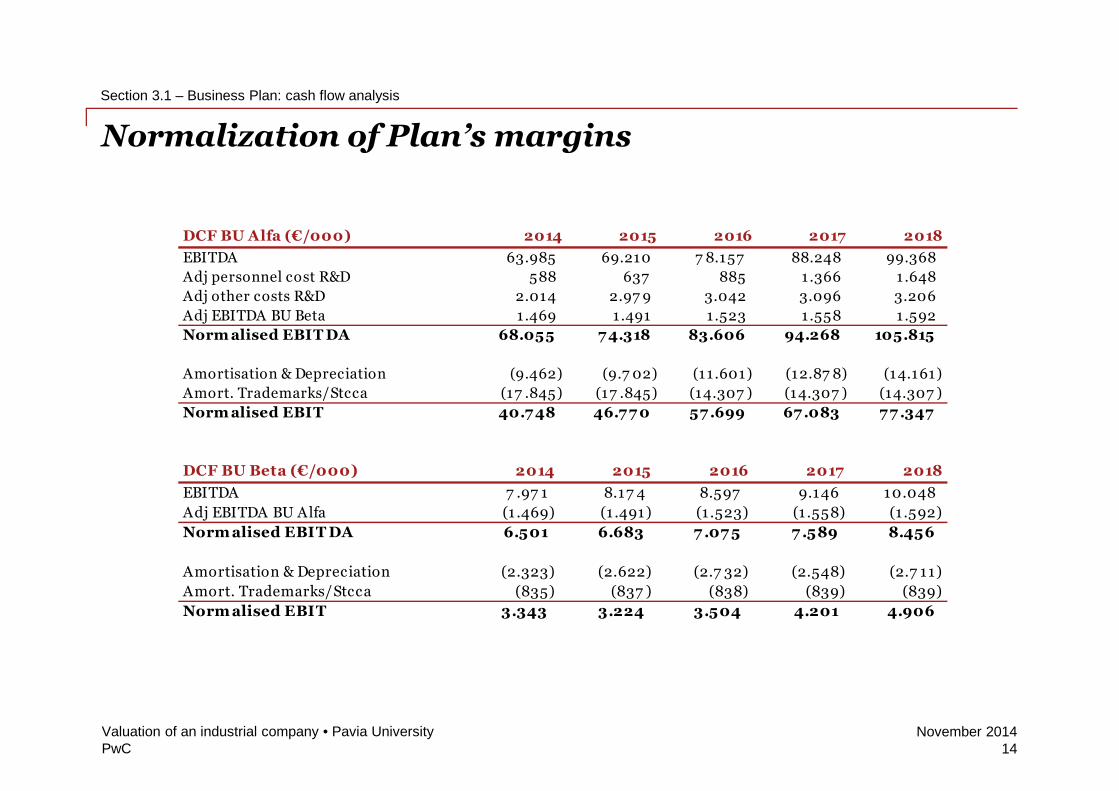

Normalization of Plan’s margins

Section 3.1 – Business Plan: cash flow analysis

Valuation of an industrial company • Pavia University14

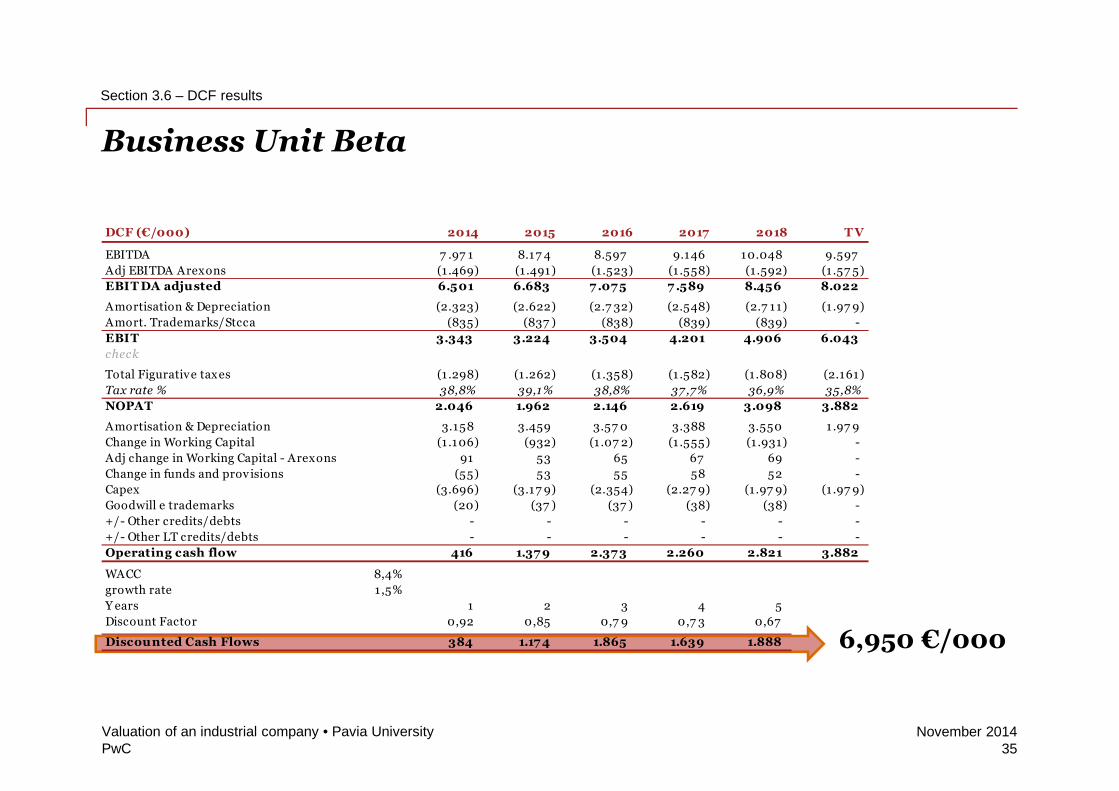

DCF BU Beta (€/000) 2014 2015 2016 2017 2018

EBITDA 7 .97 1 8.17 4 8.597 9.146 10.048

Adj EBITDA BU Alfa (1 .469) (1 .491) (1 .523) (1 .558) (1 .592)

Norm alised EBIT DA 6.501 6.683 7 .07 5 7 .589 8.456

Amortisation & Depreciation (2.323) (2.622) (2.7 32) (2.548) (2.7 11)

Amort. Trademarks/Stcca (835) (837 ) (838) (839) (839)

Norm alised EBIT 3.343 3.224 3.504 4.201 4.906

DCF BU Alfa (€/000) 2014 2015 2016 2017 2018

EBITDA 63.985 69.210 7 8.157 88.248 99.368

Adj personnel cost R&D 588 637 885 1.366 1 .648

Adj other costs R&D 2.014 2.97 9 3.042 3.096 3.206

Adj EBITDA BU Beta 1.469 1.491 1 .523 1.558 1 .592

Norm alised EBIT DA 68.055 7 4.318 83.606 94.268 105.815

Amortisation & Depreciation (9.462) (9.7 02) (11 .601) (12.87 8) (14.161)

Amort. Trademarks/Stcca (17 .845) (17 .845) (14.307 ) (14.307 ) (14.307 )

Norm alised EBIT 40.7 48 46.7 7 0 57 .699 67 .083 7 7 .347

PwCNovember 2014

Figurative taxes on EBITSection 3.2

Valuation of an industrial company • Pavia University15

PwCNovember 2014

Calculation of figurative taxes

With regard to figurative taxes, we have proceeded with the following approach:

– Italy: we calculated IRES tax base (tax rate 27.5%) and "Carbon Tax" (tax rate 6.5%)on the basis of the EBIT of the Plan, adjusted in order to take into account:

o normalization of structural and personnel costs related to the creation of aglobal R&D centre;

o non-tax deductibility of brands’ amortization;

o Intercompany revenues from royalties.

– Rest of World: we considered country-specific EBIT and costs for royalties paid tothe BU Italy that are tax deductible.

Section 3.2 – Figurative taxes on EBIT

Valuation of an industrial company • Pavia University16

PwCNovember 2014

Discount rate (WACC)Section 3.3

Valuation of an industrial company • Pavia University17

PwCNovember 2014

Discounted Cash Flow – discount rate (WACC) 1/2

• In calculating the discount rate (WACC), you should refer to the different riskand performance profiles of each Business Unit that makes up the Group.Business Unit Alpha operates throughout the world, both in developingcountries and more mature countries, while the Business Unit Beta operatesmainly in Italy.

• Consequently, regarding the Alfa Business Unit, cash flows discounted usinga discount rate (WACC) different for each year of the Plan to weigh the"country risk" in discounting perspective flows. For Beta Business Unit,however, we used a single discount rate.

Section 3.3 – Discount rate (WACC)

Valuation of an industrial company • Pavia University18

PwCNovember 2014

Discounted Cash Flow – discount rate (WACC) 2/2

• The calculation of the discount rate by country was built over the followingassumptions:

– risk free rate of 10-year-BTP (or equivalent in the country) equal to the net yieldas of December 31, 2013;

– country risk premium for each country on the base of an additional risk spread,according to the methodology suggested by Damodaran;

– Market Risk Premium ("MRP") equal to 5.0%: this value was consideredreasonable after the analysis of the Plan of Business Unit Alpha that highlighted a“conservative" approach by management for projections and estimates ofinvestments necessary to support the Group's competitive positioning;

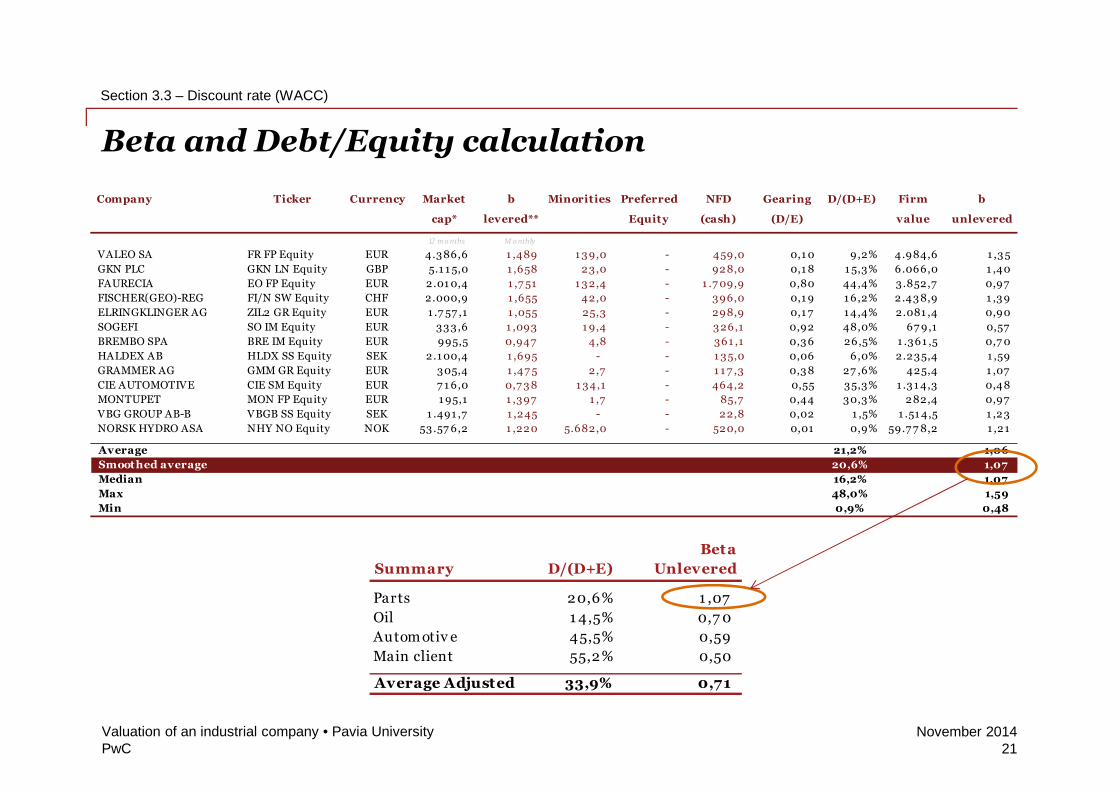

– Beta levered equal to 1.08 and Beta unlevered equal to 0.71;

– D/E structure depending on the analysis carried out on the market compared tothe identified comparable companies.

Section 3.3 – Discount rate (WACC)

Valuation of an industrial company • Pavia University19

PwCNovember 2014

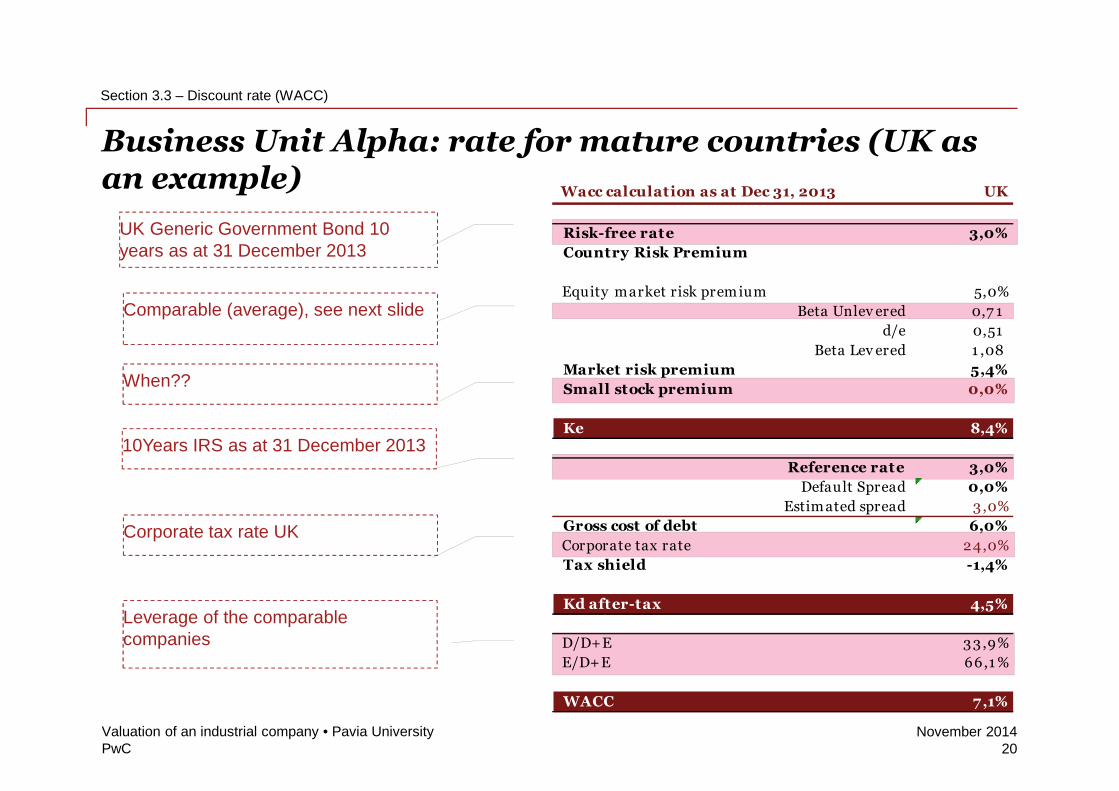

Business Unit Alpha: rate for mature countries (UK asan example)

Section 3.3 – Discount rate (WACC)

Valuation of an industrial company • Pavia University20

Corporate tax rate UK

UK Generic Government Bond 10years as at 31 December 2013

Comparable (average), see next slide

When??

10Years IRS as at 31 December 2013

Leverage of the comparablecompanies

Wacc calculation as at Dec 31, 2013 UK

Risk-free rate 3,0%

Country Risk Premium

Equity market risk prem ium 5,0%

Beta Unlev ered 0,7 1

d/e 0,51

Beta Lev ered 1 ,08

Market risk premium 5,4%

Small stock premium 0,0%

Ke 8,4%

Reference rate 3,0%

Default Spread 0,0%

Estim ated spread 3,0%

Gross cost of debt 6,0%

Corporate tax rate 24,0%

Tax shield -1,4%

Kd after-tax 4,5%

D/D+E 33,9%

E/D+E 66,1 %

WACC 7,1%

PwCNovember 2014

Beta and Debt/Equity calculation

Section 3.3 – Discount rate (WACC)

Valuation of an industrial company • Pavia University21

Company Ticker Currency Market b Minorities Preferred NFD Gearing D/(D+E) Firm b

cap* levered** Equity (cash) (D/E) value unlevered

12 m o nths M o nthly

VALEO SA FR FP Equity EUR 4.386,6 1 ,489 1 3 9,0 - 459,0 0,1 0 9,2% 4.984,6 1 ,3 5

GKN PLC GKN LN Equity GBP 5.1 1 5,0 1 ,658 23,0 - 928,0 0,1 8 1 5,3% 6.066,0 1 ,40

FAURECIA EO FP Equity EUR 2.01 0,4 1 ,7 51 1 3 2,4 - 1 .7 09,9 0,80 44,4% 3.852,7 0,97

FISCHER(GEO)-REG FI/N SW Equity CHF 2.000,9 1 ,655 42,0 - 396,0 0,1 9 1 6,2% 2.43 8,9 1 ,3 9

ELRINGKLINGER AG ZIL2 GR Equity EUR 1 .7 57 ,1 1 ,055 25,3 - 298,9 0,1 7 1 4,4% 2.081 ,4 0,90

SOGEFI SO IM Equity EUR 33 3,6 1 ,093 1 9,4 - 3 26,1 0,92 48,0% 67 9,1 0,57

BREMBO SPA BRE IM Equity EUR 995,5 0,947 4,8 - 361 ,1 0,3 6 26,5% 1 .361 ,5 0,7 0

HALDEX AB HLDX SS Equity SEK 2.1 00,4 1 ,695 - - 1 35,0 0,06 6,0% 2.235,4 1 ,59

GRAMMER AG GMM GR Equity EUR 305,4 1 ,47 5 2,7 - 1 1 7 ,3 0,3 8 27 ,6% 425,4 1 ,07

CIE AUTOMOTIVE CIE SM Equity EUR 7 1 6,0 0,7 3 8 1 34,1 - 464,2 0,55 35,3% 1 .3 1 4,3 0,48

MONTUPET MON FP Equity EUR 1 95,1 1 ,397 1 ,7 - 85,7 0,44 30,3% 282,4 0,97

VBG GROUP AB-B VBGB SS Equity SEK 1 .491 ,7 1 ,245 - - 22,8 0,02 1 ,5% 1 .51 4,5 1 ,23

NORSK HYDRO ASA NHY NO Equity NOK 53 .57 6,2 1 ,220 5.682,0 - 520,0 0,01 0,9% 59.7 7 8,2 1 ,21

Average 21,2% 1,06

Smoothed average 20,6% 1,07

Median 16,2% 1,07

Max 48,0% 1,59

Min 0,9% 0,48

Summary D/(D+E)

Beta

Unlevered

Parts 20,6% 1 ,07

Oil 1 4,5% 0,7 0

Autom otiv e 45,5% 0,59

Main client 55,2% 0,50

Average Adjusted 33,9% 0,71

PwCNovember 2014

Wacc calculation as at Dec 31, 2013 Argentina

Risk-free rate 3,0%

Country Risk Premium 9,8%

Equity market risk prem ium 5,0%

Beta Unlev ered 0,7 1

d/e 0,51

Beta Lev ered 1 ,08

Market risk premium 5,4%

Small stock premium 0,0%

Ke 18,2%

Business Unit Alpha: developing countries’ discountrate and Country Risk Premium

Section 3.3 – Discount rate (WACC)

Valuation of an industrial company • Pavia University22

Country Region Local Currency Rating Rating-based Default

Spread

Total Equity Risk

Premium

Country Risk

Premium

Abu Dhabi Middle East Aa2 0,50% 5,75% 0,75%

Albania Eastern Europe & Russia B1 4,50% 11,75% 6,75%

Andorra Western Europe A3 1,20% 6,80% 1,80%

Angola Africa Ba3 3,60% 10,40% 5,40%

Argentina Central and South America B3 6,50% 14,75% 9,75%

Armenia Eastern Europe & Russia Ba2 3,00% 9,50% 4,50%

Aruba Caribbean Baa1 1,60% 7,40% 2,40%

Australia Australia & New Zealand Aaa 0,00% 5,00% 0,00%

Wacc calculation as at Dec 31, 2013 Argentina

Reference rate 3,0%

Default Spread 6,5%

Estim ated spread 3,0%

Gross cost of debt 12,5%

Corporate tax rate 3 5,0%

Tax shield -4,4%

Kd after-tax 8,1%

!

!@

@

D/D+ E 33 ,9%

E/D+E 66,1 %

WACC 14,8%

PwCNovember 2014

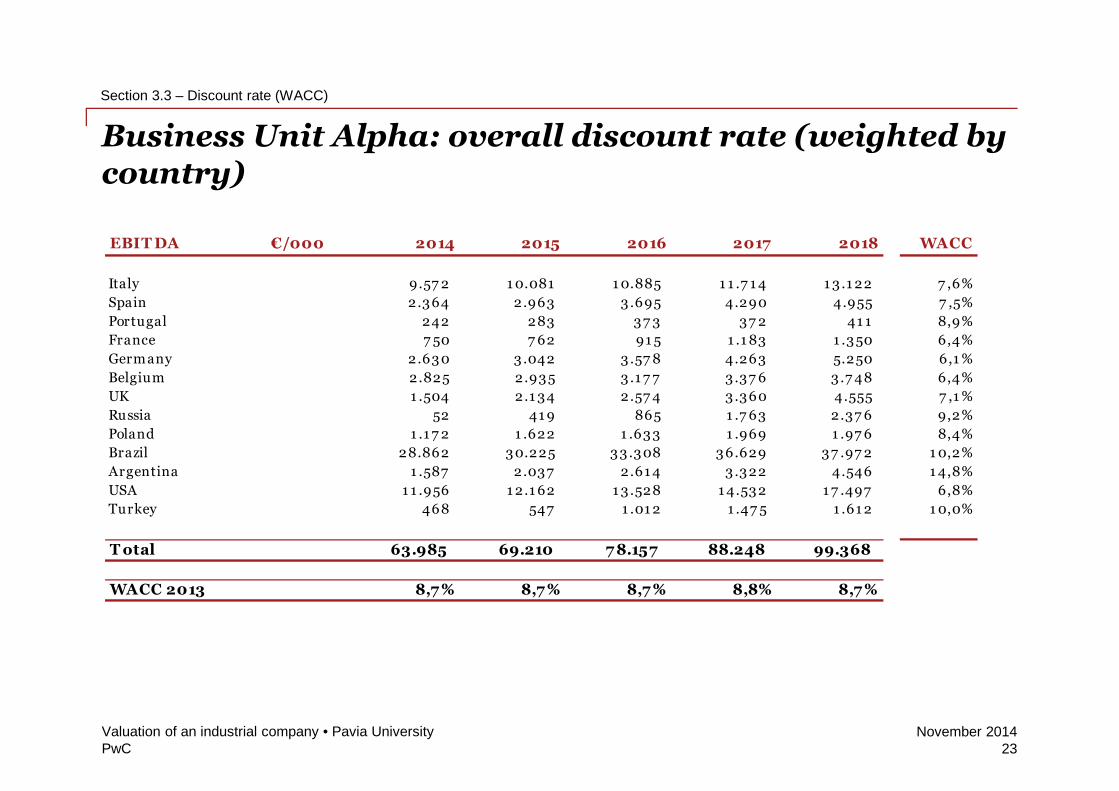

Business Unit Alpha: overall discount rate (weighted bycountry)

Section 3.3 – Discount rate (WACC)

Valuation of an industrial company • Pavia University23

EBIT DA €/000 2014 2015 2016 2017 2018 WACC

Italy 9.57 2 1 0.081 1 0.885 1 1 .7 1 4 1 3.1 22 7 ,6%

Spain 2.364 2.963 3.695 4.290 4.955 7 ,5%

Portugal 242 283 37 3 37 2 41 1 8,9%

France 7 50 7 62 91 5 1 .1 83 1 .350 6,4%

Germany 2.630 3.042 3.57 8 4.263 5.250 6,1 %

Belgium 2.825 2.935 3.1 7 7 3.37 6 3.7 48 6,4%

UK 1 .504 2.1 34 2.57 4 3.360 4.555 7 ,1 %

Russia 52 41 9 865 1 .7 63 2.37 6 9,2%

Poland 1 .1 7 2 1 .622 1 .633 1 .969 1 .97 6 8,4%

Brazil 28.862 30.225 33.308 36.629 37 .97 2 1 0,2%

Argentina 1 .587 2.037 2.61 4 3.322 4.546 1 4,8%

USA 1 1 .956 1 2.1 62 1 3.528 1 4.532 1 7 .497 6,8%

Turkey 468 547 1 .01 2 1 .47 5 1 .61 2 1 0,0%

T otal 63.985 69.210 7 8.157 88.248 99.368

WACC 2013 8,7 % 8,7 % 8,7 % 8,8% 8,7 %

PwCNovember 2014

Terminal valueSection 3.4

Valuation of an industrial company • Pavia University24

PwCNovember 2014

Business Unit Alpha: Terminal Value

The operating cash flow used to calculate the TV of Alfa Business Unit wasidentified on the base of the following analysis:

– Normalization of EBITDA (TV EBITDA = last two years average) to consider thefollowing effects:

1. expenses related to R&D centre;2. costs associated with the implicit renewal of a multiyear contract with the

Group’s largest customer;

3. Recharge to Beta division.

– The TV was calculated with reference to the Gordon formula (growing perpetuity):we assumed a growth factor "g" of 3.1%, calculated for each country by weighting thelong-term inflation rate and the related weight in terms of overall EBITDA as fromthe Plan.

– The medium-normal level of maintenance investments has been estimated equal €14.2 million, based on a detailed analysis of the capex included in the Business Plan,identifying those to be considered recurring and those not recurring.

Section 3.4 – Terminal value

Valuation of an industrial company • Pavia University25

PwCNovember 2014

Business Unit Beta: Terminal Value

The operating cash flow used to calculate the TV of Beta Business Unit wasidentified on the base of the following analysis:

– TV EBITDA as average of the last two years of the plan.

– The TV was calculated with reference to the Gordon formula (growing perpetuity):we assumed a growth factor "g" of 1.5%, lower than the Alfa Business Unit as themain Beta Business Unit’s market is Italy, a country with a lower expected long-termgrowth rates.

– The medium-normal level of maintenance investments has been estimated (some €2 million).

Section 3.4 – Terminal value

Valuation of an industrial company • Pavia University26

PwCNovember 2014

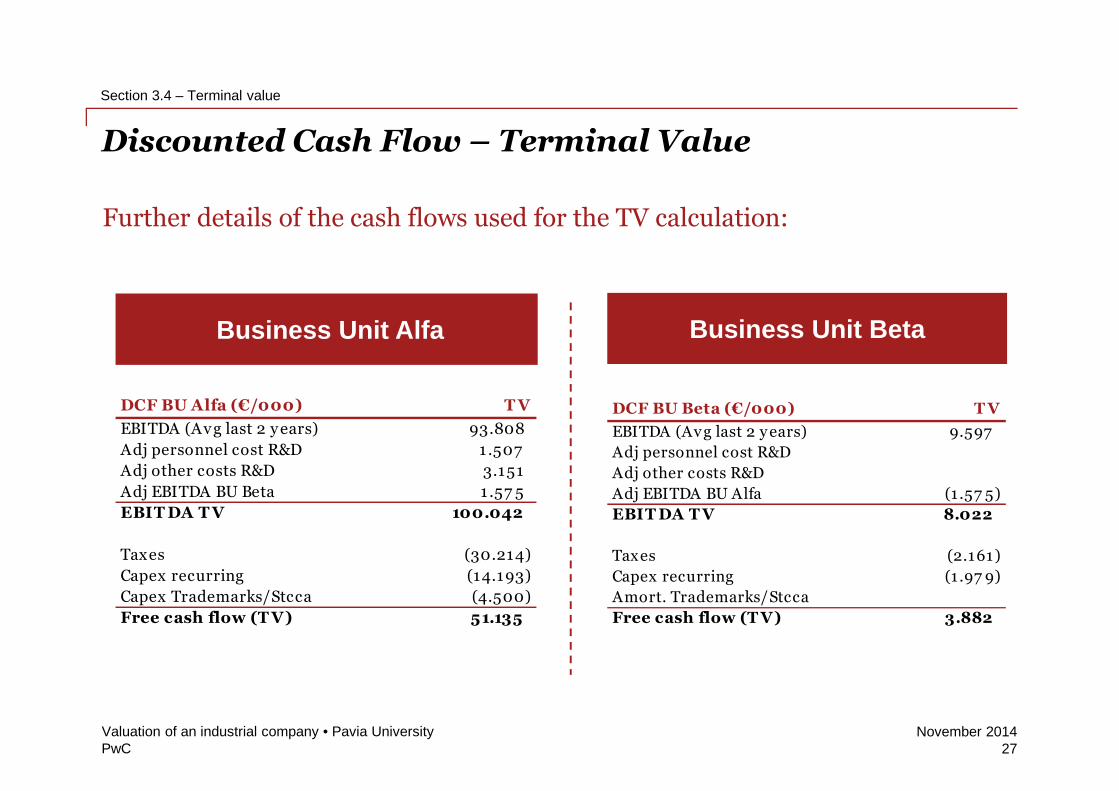

Discounted Cash Flow – Terminal Value

Further details of the cash flows used for the TV calculation:

Section 3.4 – Terminal value

Valuation of an industrial company • Pavia University27

Business Unit Alfa Business Unit Beta

DCF BU Alfa (€/000) T V

EBITDA (Avg last 2 y ears) 93.808

Adj personnel cost R&D 1.507

Adj other costs R&D 3.151

Adj EBITDA BU Beta 1 .57 5

EBIT DA T V 100.042

Taxes (30.214)

Capex recurring (14.193)

Capex Trademarks/Stcca (4.500)

Free cash flow (T V) 51.135

DCF BU Beta (€/000) T V

EBITDA (Avg last 2 y ears) 9.597

Adj personnel cost R&D

Adj other costs R&D

Adj EBITDA BU Alfa (1 .57 5)

EBIT DA T V 8.022

Taxes (2.161)

Capex recurring (1.97 9)

Amort. Trademarks/Stcca

Free cash flow (T V) 3.882

PwCNovember 2014

Long-term growth rate calculation (“g”)

Section 3.4 – Terminal value

Valuation of an industrial company • Pavia University28

Countries

Italy 1 ,1 % 1 ,2% 1 ,3 % 1 ,4% 1 ,5%

Spain 1 ,0% 1 ,2% 1 ,2% 1 ,3 % 1 ,2%

Portugal 1 ,0% 1 ,5% 1 ,5% 1 ,5% 1 ,5%

France 1 ,5% 1 ,5% 1 ,6% 1 ,7 % 1 ,8%

Germany 1 ,8% 1 ,8% 1 ,8% 1 ,9% 1 ,9%

Belgium 1 ,1 % 1 ,2% 1 ,2% 1 ,2% 1 ,3%

UK 2,3 % 2,0% 1 ,9% 2,0% 2,0%

Russia 5,3 % 5,4% 5,5% 5,5% 5,5%

Poland 2,0% 2,3 % 2,5% 2,5% 2,5%

Brazil 5,8% 5,0% 4,5% 4,5% 4,5%

Argentina 1 0,8% 1 0,8% 1 0,8% 1 0,8% 1 0,8%

USA 1 ,7 % 1 ,9% 2,0% 2,2% 2,2%

Turkey 6,0% 6,0% 6,0% 6,0% 6,0%

Inflation rates

Countries 2014 2015 2016 2017 2018

Italy 0,9% 0,9% 1,1% 1,2% 1,3%

Spain 0,8% 1,0% 1,0% 1,0% 1,0%

Portugal 0,7 % 1,2% 1,2% 1,2% 1,3%

France 1,2% 1,2% 1,4% 1,4% 1,6%

Germany 1,5% 1,6% 1,6% 1,7 % 1,7 %

Belgium 0,8% 0,9% 1,0% 1,0% 1,0%

UK 2,1% 1,8% 1,7 % 1,8% 1,8%

Russia 4,9% 5,0% 5,1% 5,1% 5,1%

Poland 2% 2,0% 2,3% 2,3% 2,3%

Brazil 5,4% 4,6% 4,1% 4,1% 4,1%

Argentina 9,4% 9,4% 9,4% 9,4% 9,4%

USA 1,4% 1,6% 1,8% 2,0% 2,0%

Turkey 5,6% 5,6% 5,6% 5,6% 5,6%

Final Rate

(0,5% )

(1 ,5% ) for countries with an expected inflaction > = 8%

Discount factor

for countries with an expected inflaction < 8%

PwCNovember 2014

Long-term growth rate calculation (“g”)

Section 3.4 – Terminal value

Valuation of an industrial company • Pavia University29

Countries 2014 2015 2016 2017 2018

Italy 0,9% 0,9% 1,1% 1,2% 1,3%

Spain 0,8% 1,0% 1,0% 1,0% 1,0%

Portugal 0,7 % 1,2% 1,2% 1,2% 1,3%

France 1,2% 1,2% 1,4% 1,4% 1,6%

Germany 1,5% 1,6% 1,6% 1,7 % 1,7 %

Belgium 0,8% 0,9% 1,0% 1,0% 1,0%

UK 2,1% 1,8% 1,7 % 1,8% 1,8%

Russia 4,9% 5,0% 5,1% 5,1% 5,1%

Poland 2% 2,0% 2,3% 2,3% 2,3%

Brazil 5,4% 4,6% 4,1% 4,1% 4,1%

Argentina 9,4% 9,4% 9,4% 9,4% 9,4%

USA 1,4% 1,6% 1,8% 2,0% 2,0%

Turkey 5,6% 5,6% 5,6% 5,6% 5,6%

Final Rate

Countries 2014 2015 2016 2017 2018

Italy 9.57 2 1 0.081 1 0.885 1 1 .7 1 4 1 3 .1 22

Spain 2.3 64 2.963 3 .695 4.290 4.955

Portugal 242 283 37 3 37 2 41 1

France 7 50 7 62 91 5 1 .1 83 1 .350

Germany 2.630 3 .042 3 .57 8 4.263 5.250

Belgium 2.825 2.935 3 .1 7 7 3.37 6 3 .7 48

UK 1 .504 2.1 3 4 2.57 4 3.360 4.555

Russia 52 41 9 865 1 .7 63 2.37 6

Poland 1 .1 7 2 1 .622 1 .63 3 1 .969 1 .97 6

Brazil 28.862 30.225 33 .308 3 6.629 37 .97 2

Argentina 1 .587 2.03 7 2.61 4 3.322 4.546

USA 1 1 .956 1 2.1 62 1 3 .528 1 4.53 2 1 7 .497

Turkey 468 547 1 .01 2 1 .47 5 1 .61 2

63.985 69.210 7 8.157 88.248 99.368

EBIT DA

2014 2015 2016 2017 2018

0,131% 0,132% 0,147 % 0,155% 0,167 %

0,028% 0,041% 0,046% 0,049% 0,048%

0,003% 0,005% 0,006% 0,005% 0,005%

0,014% 0,014% 0,016% 0,019% 0,021%

0,063% 0,068% 0,07 1% 0,080% 0,087 %

0,037 % 0,039% 0,039% 0,038% 0,038%

0,048% 0,054% 0,054% 0,067 % 0,080%

0,004% 0,030% 0,056% 0,101% 0,121%

0,032% 0,047 % 0,047 % 0,050% 0,045%

2,421% 1,992% 1,7 26% 1,681% 1,548%

0,233% 0,27 6% 0,314% 0,354% 0,430%

0,267 % 0,285% 0,312% 0,323% 0,349%

0,041% 0,044% 0,07 2% 0,093% 0,091%

3,3% 3,0% 2,9% 3,0% 3,0%

Weighted Rate

Average = 3.1%

PwCNovember 2014

Surplus assetsSection 3.5

Valuation of an industrial company • Pavia University30

PwCNovember 2014

Calculation of tax benefits related to the use of past taxlosses

• We have also considered the discounted tax benefits arising from the use ofpast tax losses carried forward indefinitely and referable to Italy and Spain.The value so determined was regarded as a surplus asset.

• Conservatively, we didn’t consider tax losses that may accrue in the future onthe base of Plan’s results.

Section 3.5 – Surplus assets

Valuation of an industrial company • Pavia University31

PwCNovember 2014

DCF resultsSection 3.6

Valuation of an industrial company • Pavia University32

PwCNovember 2014

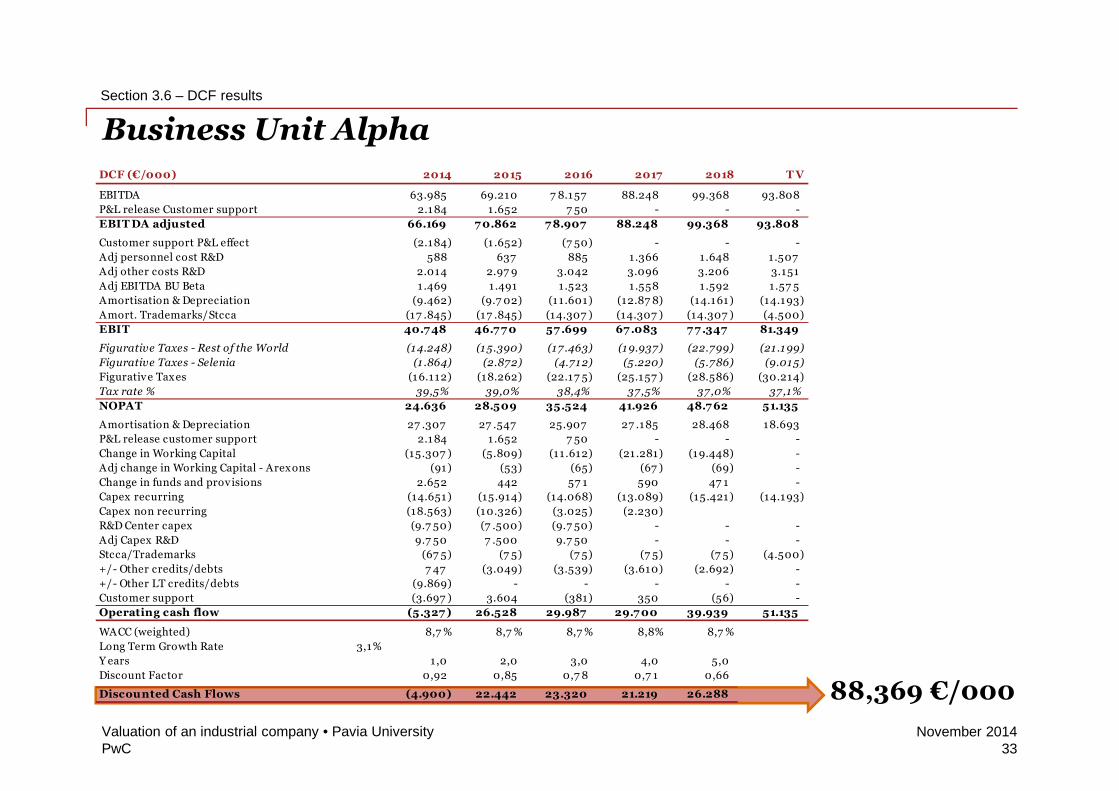

Business Unit Alpha

Section 3.6 – DCF results

Valuation of an industrial company • Pavia University33

DCF (€/000) 2014 2015 2016 2017 2018 T V

EBITDA 63.985 69.210 7 8.157 88.248 99.368 93.808

P&L release Customer support 2.184 1 .652 7 50 - - -

EBIT DA adjusted 66.169 7 0.862 7 8.907 88.248 99.368 93.808

Customer support P&L effect (2.184) (1 .652) (7 50) - - -

Adj personnel cost R&D 588 637 885 1.366 1.648 1.507

Adj other costs R&D 2.014 2.97 9 3.042 3.096 3.206 3.151

Adj EBITDA BU Beta 1 .469 1.491 1.523 1.558 1.592 1.57 5

Amortisation & Depreciation (9.462) (9.7 02) (11.601) (12.87 8) (14.161) (14.193)

Amort. Trademarks/Stcca (17 .845) (17 .845) (14.307 ) (14.307 ) (14.307 ) (4.500)

EBIT 40.7 48 46.7 7 0 57 .699 67 .083 7 7 .347 81.349

Figurative Taxes - Rest of the World (14.248) (15.390) (17 .463) (19.937) (22.799) (21.199)

Figurative Taxes - Selenia (1 .864) (2.872) (4.712) (5.220) (5.786) (9.015)

Figurativ e Taxes (16.112) (18.262) (22.17 5) (25.157 ) (28.586) (30.214)

Tax rate % 39,5% 39,0% 38,4% 37,5% 37,0% 37,1%

NOPAT 24.636 28.509 35.524 41.926 48.7 62 51.135

Amortisation & Depreciation 27 .307 27 .547 25.907 27 .185 28.468 18.693

P&L release customer support 2.184 1 .652 7 50 - - -

Change in Working Capital (15.307 ) (5.809) (11.612) (21 .281) (19.448) -

Adj change in Working Capital - Arexons (91) (53) (65) (67 ) (69) -

Change in funds and provisions 2.652 442 57 1 590 47 1 -

Capex recurring (14.651) (15.914) (14.068) (13.089) (15.421) (14.193)

Capex non recurring (18.563) (10.326) (3.025) (2.230)

R&D Center capex (9.7 50) (7 .500) (9.7 50) - - -

Adj Capex R&D 9.7 50 7 .500 9.7 50 - - -

Stcca/Trademarks (67 5) (7 5) (7 5) (7 5) (7 5) (4.500)

+/- Other credits/debts 7 47 (3.049) (3.539) (3.610) (2.692) -

+/- Other LT credits/debts (9.869) - - - - -

Customer support (3.697 ) 3.604 (381) 350 (56) -

Operating cash flow (5.327 ) 26.528 29.987 29.7 00 39.939 51.135

WACC (weighted) 8,7 % 8,7 % 8,7 % 8,8% 8,7 %

Long Term Growth Rate 3,1%

Y ears 1,0 2,0 3,0 4,0 5,0

Discount Factor 0,92 0,85 0,7 8 0,7 1 0,66

Discounted Cash Flows (4.900) 22.442 23.320 21.219 26.288 88,369 €/000

PwCNovember 2014

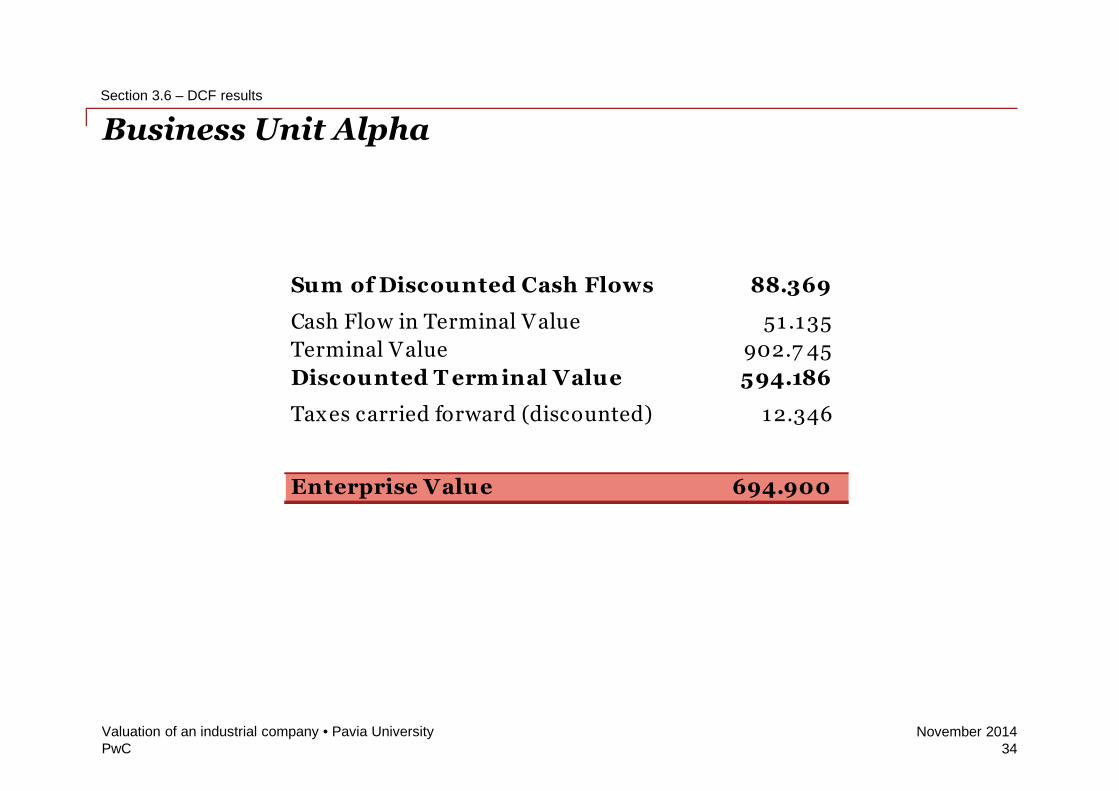

Business Unit Alpha

Section 3.6 – DCF results

Valuation of an industrial company • Pavia University34

Sum of Discounted Cash Flows 88.369

Cash Flow in Terminal Value 51 .135

Terminal Value 902.7 45

Discounted T erm inal Value 594.186

Taxes carried forward (discounted) 12.346

Enterprise Value 694.900

PwCNovember 2014

Business Unit Beta

Section 3.6 – DCF results

Valuation of an industrial company • Pavia University35

6,950 €/000

DCF (€/000) 2014 2015 2016 2017 2018 T V

EBITDA 7 .97 1 8.17 4 8.597 9.146 10.048 9.597

Adj EBITDA Arexons (1 .469) (1 .491) (1.523) (1 .558) (1.592) (1 .57 5)

EBIT DA adjusted 6.501 6.683 7 .07 5 7 .589 8.456 8.022

Amortisation & Depreciation (2.323) (2.622) (2.7 32) (2.548) (2.7 11) (1 .97 9)

Amort. Trademarks/Stcca (835) (837 ) (838) (839) (839) -

EBIT 3.343 3.224 3.504 4.201 4.906 6.043

check

Total Figurative taxes (1 .298) (1 .262) (1.358) (1 .582) (1.808) (2.161)

Tax rate % 38,8% 39,1% 38,8% 37 ,7% 36,9% 35,8%

NOPAT 2.046 1.962 2.146 2.619 3.098 3.882

Amortisation & Depreciation 3.158 3.459 3.57 0 3.388 3.550 1.97 9

Change in Working Capital (1 .106) (932) (1 .07 2) (1 .555) (1 .931) -

Adj change in Working Capital - Arexons 91 53 65 67 69 -

Change in funds and prov isions (55) 53 55 58 52 -

Capex (3.696) (3.17 9) (2.354) (2.27 9) (1.97 9) (1 .97 9)

Goodwill e trademarks (20) (37 ) (37 ) (38) (38) -

+/- Other credits/debts - - - - - -

+/- Other LT credits/debts - - - - - -

Operating cash flow 416 1.37 9 2.37 3 2.260 2.821 3.882

WACC 8,4%

growth rate 1 ,5%

Y ears 1 2 3 4 5

Discount Factor 0,92 0,85 0,7 9 0,7 3 0,67

Discounted Cash Flows 384 1.17 4 1.865 1.639 1.888

PwCNovember 2014

Business Unit Beta

Section 3.6 – DCF results

Valuation of an industrial company • Pavia University36

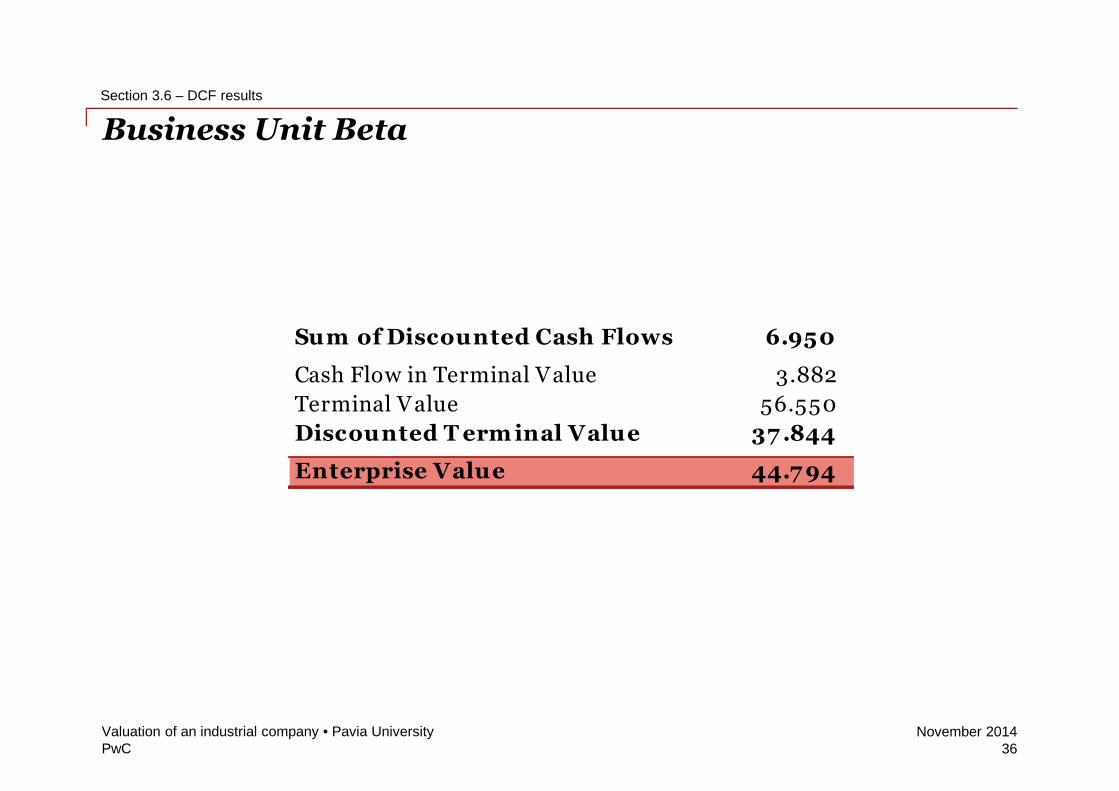

Sum of Discounted Cash Flows 6.950

Cash Flow in Terminal Value 3.882

Terminal Value 56.550

Discounted T erm inal Value 37 .844

Enterprise Value 44.7 94

PwCNovember 2014

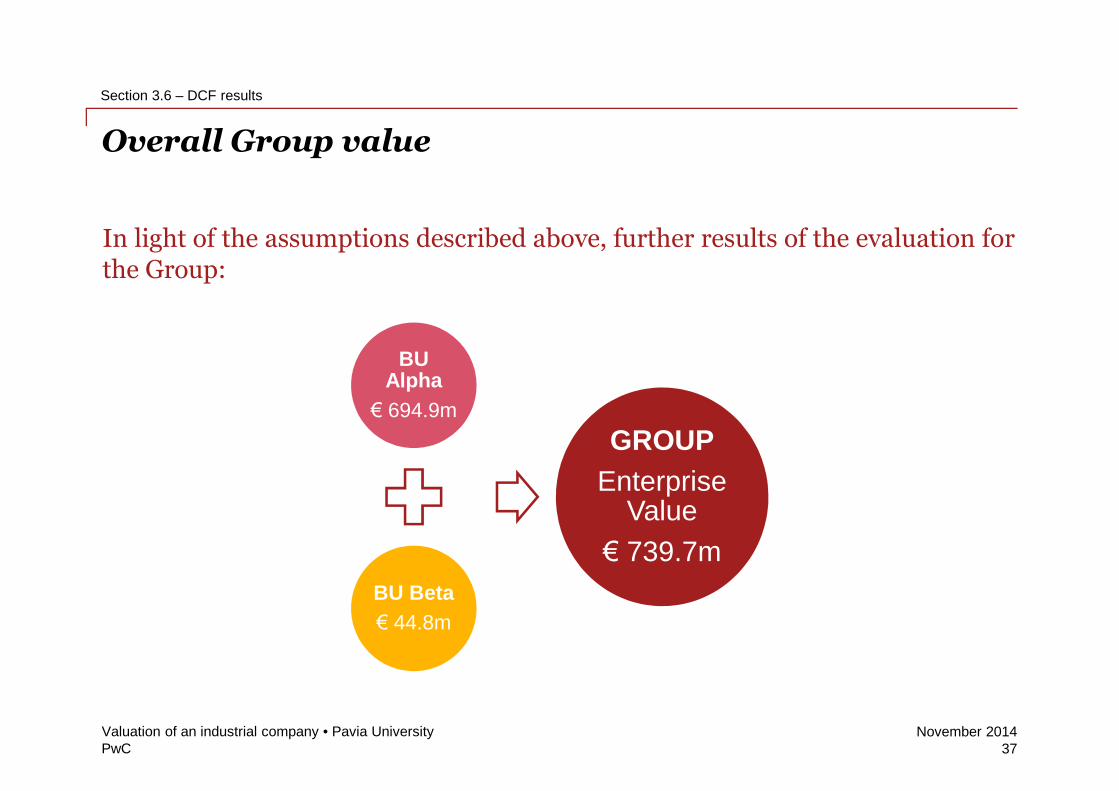

Overall Group value

In light of the assumptions described above, further results of the evaluation forthe Group:

BUAlpha

€ 694.9m

BU Beta

€ 44.8m

GROUP

EnterpriseValue

€ 739.7m

Section 3.6 – DCF results

Valuation of an industrial company • Pavia University37

PwCNovember 2014

"Reconciliation" between values determined in differentmoments in time (1/2)

With regard to the value arising from this valuation exercise, it was decided tocompare this EV with those calculated in the previous year to assess the logicalconsistency. In particular, the comparison was made on the base of thefollowing:

– time horizon is homogeneous with respect to explicit flows;

– analysis of major changes for both Alpha and Beta Business Units;

– analysis of the impact on the value of the main components identified, both inexplicit flows and Terminal Value;

– quantification of the main effects with regard to cash flows and discount rate(WACC).

Section 3.6 – DCF results

Valuation of an industrial company • Pavia University38

PwCNovember 2014

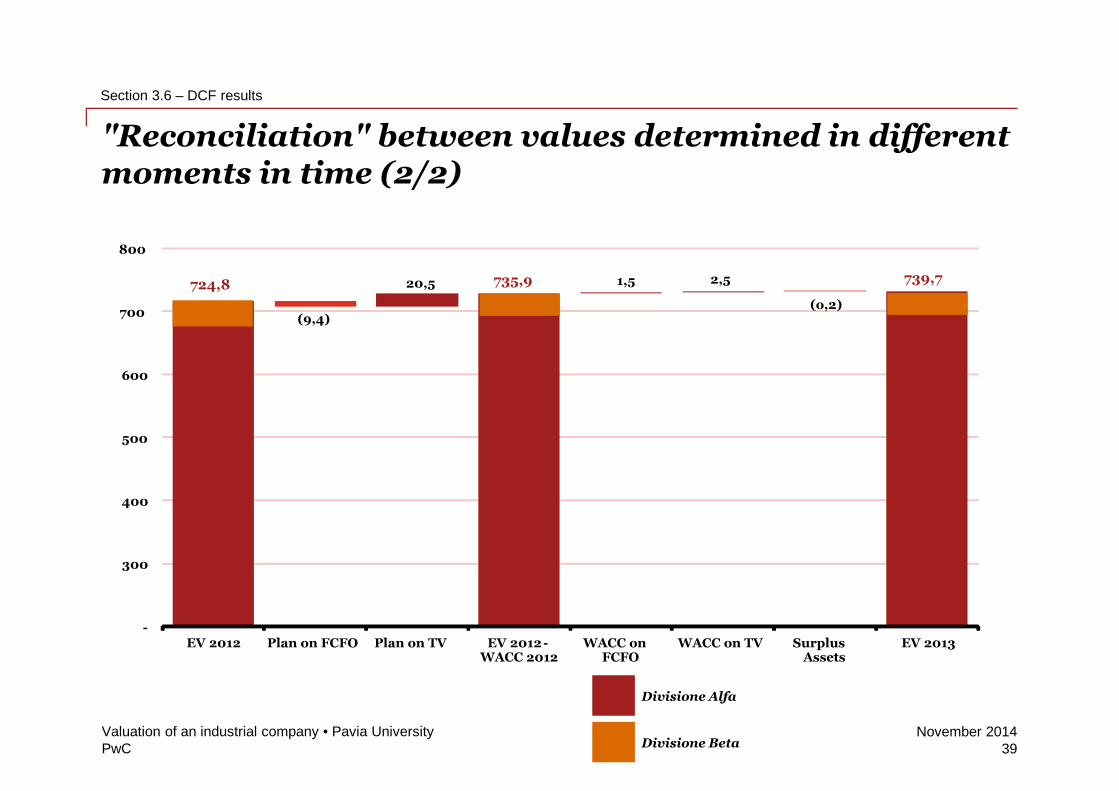

"Reconciliation" between values determined in differentmoments in time (2/2)

Section 3.6 – DCF results

Valuation of an industrial company • Pavia University39

724,8

(9,4)

20,5 735,9 1,5 2,5

(o,2)

739,7

-

300

400

500

600

700

800

EV 2012 Plan on FCFO Plan on TV EV 2012 -WACC 2012

WACC onFCFO

WACC on TV SurplusAssets

EV 2013

Divisione Beta

Divisione Alfa

PwCNovember 2014

Sensitivity analysisSection 3.7

Valuation of an industrial company • Pavia University40

PwCNovember 2014

Sensitivity analysis

• In the final phase of the valuation, we have to verify the value of thecompany/asset and interpret the results in light of the general framework inorder to check the logical consistency and minimize the possibility of error.In fact, since the results are related to plans, and therefore to uncertaintiesand risks, you "must consider the value in terms of scenarios and valueranges that reflects such uncertainty" (Tom Copeland, The value of thecompany).

• In order to reduce the error margin, who perform the valuation may:

– identify factors that can invalidate the assumptions of the plan;

– estimate the likelihood of those events and factors, related to a general situationand/or the specific company, to occur;

– develop alternative scenarios suggested by the results of the analysis previouslyundertaken in order to highlight "the value ...in each assumption made, rather thandevelop a single forecast, considered the most likely and determine a singlevalue...“ (Tom Copeland).

Section 3.7 – Sensitivity analysis

Valuation of an industrial company • Pavia University41

PwCNovember 2014

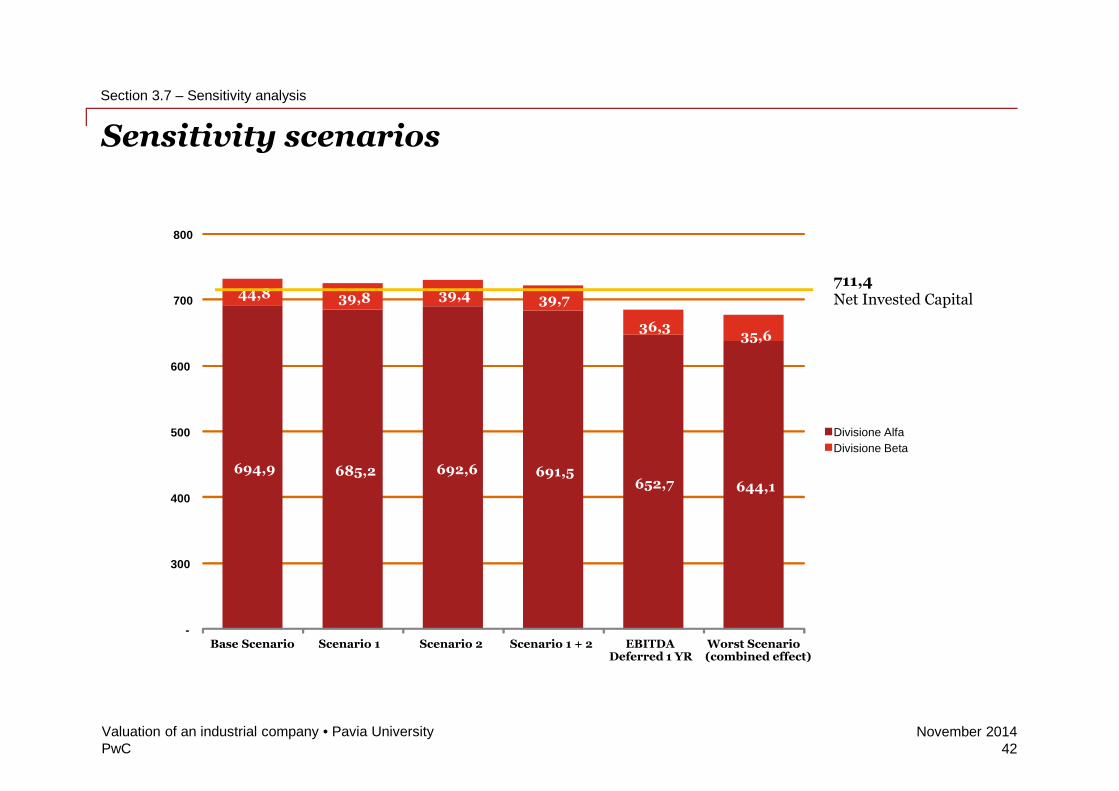

Sensitivity scenarios

Section 3.7 – Sensitivity analysis

Valuation of an industrial company • Pavia University42

694,9 685,2 692,6 691,5652,7 644,1

44,8 39,8 39,4 39,7

36,335,6

-

300

400

500

600

700

800

Base Scenario Scenario 1 Scenario 2 Scenario 1 + 2 EBITDADeferred 1 YR

Worst Scenario(combined effect)

Divisione Beta

Divisione Alfa

711,4Net Invested Capital

PwCNovember 2014

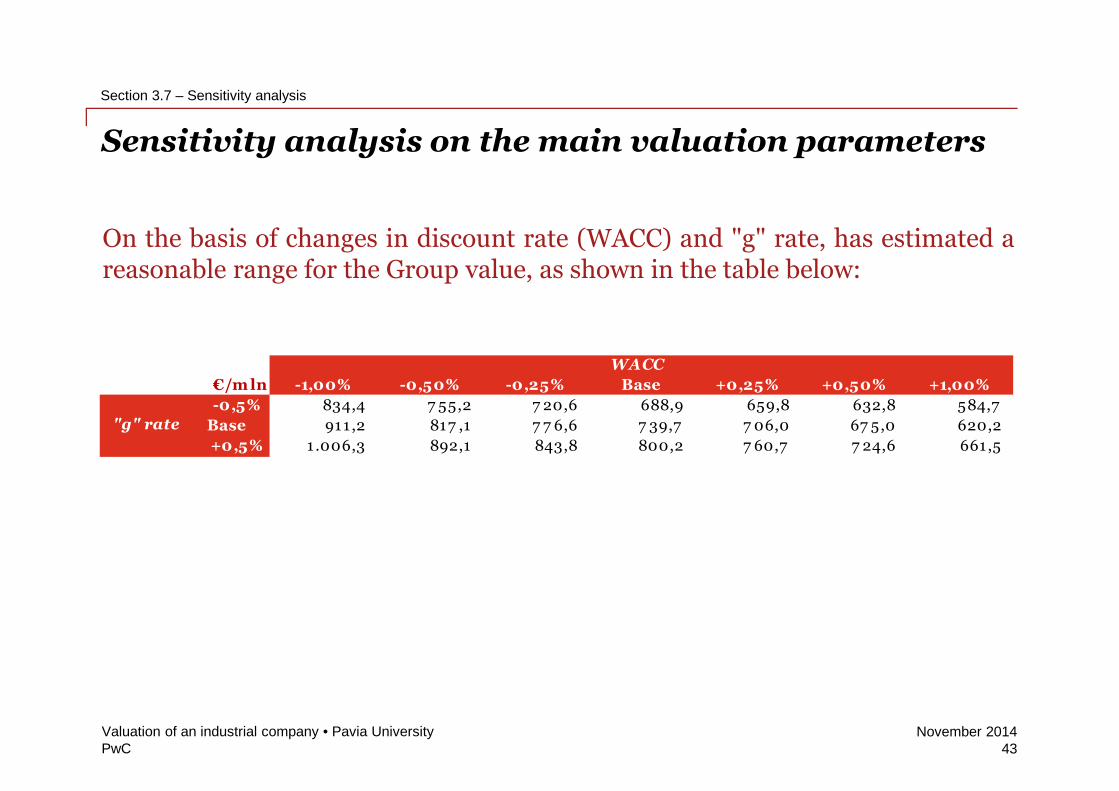

Sensitivity analysis on the main valuation parameters

On the basis of changes in discount rate (WACC) and "g" rate, has estimated areasonable range for the Group value, as shown in the table below:

Section 3.7 – Sensitivity analysis

Valuation of an industrial company • Pavia University43

€/m ln -1,00% -0,50% -0,25% Base +0,25% +0,50% +1,00%

-0,5% 834,4 7 55,2 7 20,6 688,9 659,8 632,8 584,7

Base 911 ,2 817 ,1 7 7 6,6 7 39,7 7 06,0 67 5,0 620,2

+0,5% 1 .006,3 892,1 843,8 800,2 7 60,7 7 24,6 661 ,5

WACC

"g" rate

PwCNovember 2014

Market multiple methodologySection 4

Valuation of an industrial company • Pavia University44

PwCNovember 2014

The market multiples as a control method

In order to check the "sustainability" of the Enterprise Value determinedthrough the DCF method we have done a comparison with the EV obtained withthe market multiples method, referring to the same "panel" of comparablecompanies used for beta determination.

Section 4 – Market multiple methodology

Valuation of an industrial company • Pavia University45

PwCNovember 2014

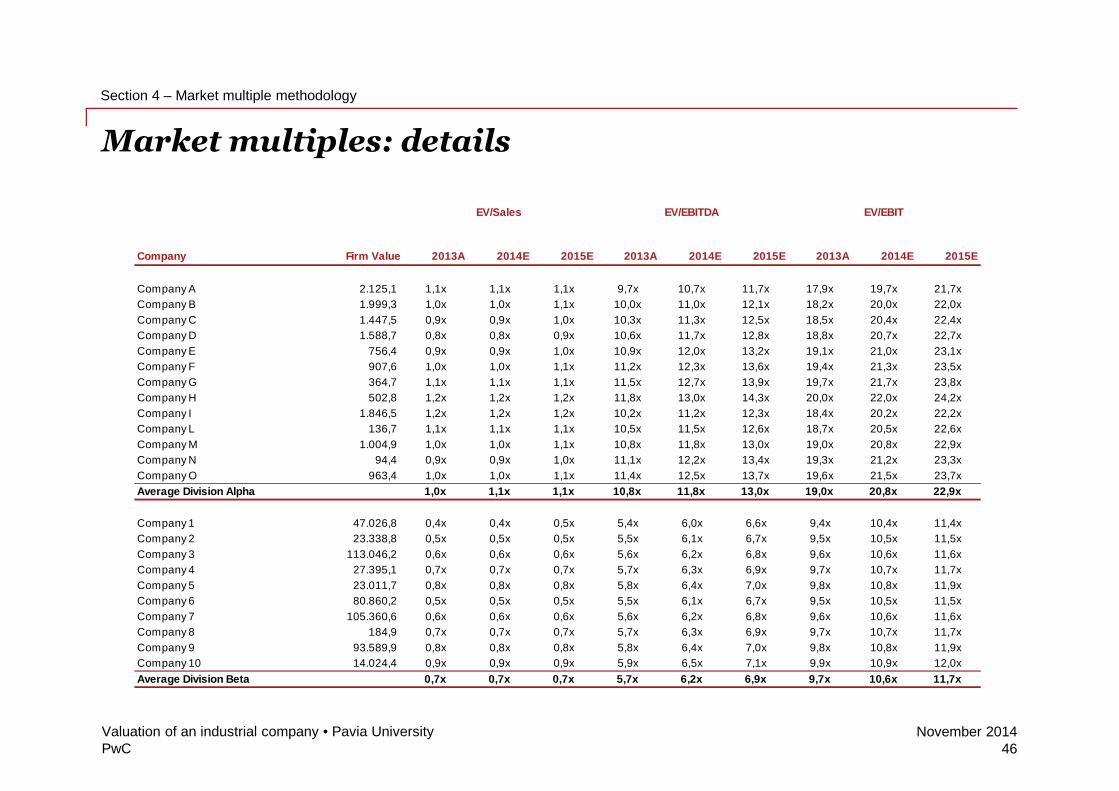

Market multiples: details

Section 4 – Market multiple methodology

Valuation of an industrial company • Pavia University46

Company Firm Value 2013A 2014E 2015E 2013A 2014E 2015E 2013A 2014E 2015E

Company A 2.125,1 1,1x 1,1x 1,1x 9,7x 10,7x 11,7x 17,9x 19,7x 21,7x

Company B 1.999,3 1,0x 1,0x 1,1x 10,0x 11,0x 12,1x 18,2x 20,0x 22,0x

Company C 1.447,5 0,9x 0,9x 1,0x 10,3x 11,3x 12,5x 18,5x 20,4x 22,4x

Company D 1.588,7 0,8x 0,8x 0,9x 10,6x 11,7x 12,8x 18,8x 20,7x 22,7x

Company E 756,4 0,9x 0,9x 1,0x 10,9x 12,0x 13,2x 19,1x 21,0x 23,1x

Company F 907,6 1,0x 1,0x 1,1x 11,2x 12,3x 13,6x 19,4x 21,3x 23,5x

Company G 364,7 1,1x 1,1x 1,1x 11,5x 12,7x 13,9x 19,7x 21,7x 23,8x

Company H 502,8 1,2x 1,2x 1,2x 11,8x 13,0x 14,3x 20,0x 22,0x 24,2x

Company I 1.846,5 1,2x 1,2x 1,2x 10,2x 11,2x 12,3x 18,4x 20,2x 22,2x

Company L 136,7 1,1x 1,1x 1,1x 10,5x 11,5x 12,6x 18,7x 20,5x 22,6x

Company M 1.004,9 1,0x 1,0x 1,1x 10,8x 11,8x 13,0x 19,0x 20,8x 22,9x

Company N 94,4 0,9x 0,9x 1,0x 11,1x 12,2x 13,4x 19,3x 21,2x 23,3x

Company O 963,4 1,0x 1,0x 1,1x 11,4x 12,5x 13,7x 19,6x 21,5x 23,7x

Average Division Alpha 1,0x 1,1x 1,1x 10,8x 11,8x 13,0x 19,0x 20,8x 22,9x

Company 1 47.026,8 0,4x 0,4x 0,5x 5,4x 6,0x 6,6x 9,4x 10,4x 11,4x

Company 2 23.338,8 0,5x 0,5x 0,5x 5,5x 6,1x 6,7x 9,5x 10,5x 11,5x

Company 3 113.046,2 0,6x 0,6x 0,6x 5,6x 6,2x 6,8x 9,6x 10,6x 11,6x

Company 4 27.395,1 0,7x 0,7x 0,7x 5,7x 6,3x 6,9x 9,7x 10,7x 11,7x

Company 5 23.011,7 0,8x 0,8x 0,8x 5,8x 6,4x 7,0x 9,8x 10,8x 11,9x

Company 6 80.860,2 0,5x 0,5x 0,5x 5,5x 6,1x 6,7x 9,5x 10,5x 11,5x

Company 7 105.360,6 0,6x 0,6x 0,6x 5,6x 6,2x 6,8x 9,6x 10,6x 11,6x

Company 8 184,9 0,7x 0,7x 0,7x 5,7x 6,3x 6,9x 9,7x 10,7x 11,7x

Company 9 93.589,9 0,8x 0,8x 0,8x 5,8x 6,4x 7,0x 9,8x 10,8x 11,9x

Company 10 14.024,4 0,9x 0,9x 0,9x 5,9x 6,5x 7,1x 9,9x 10,9x 12,0x

Average Division Beta 0,7x 0,7x 0,7x 5,7x 6,2x 6,9x 9,7x 10,6x 11,7x

EV/Sales EV/EBITDA EV/EBIT

PwCNovember 2014

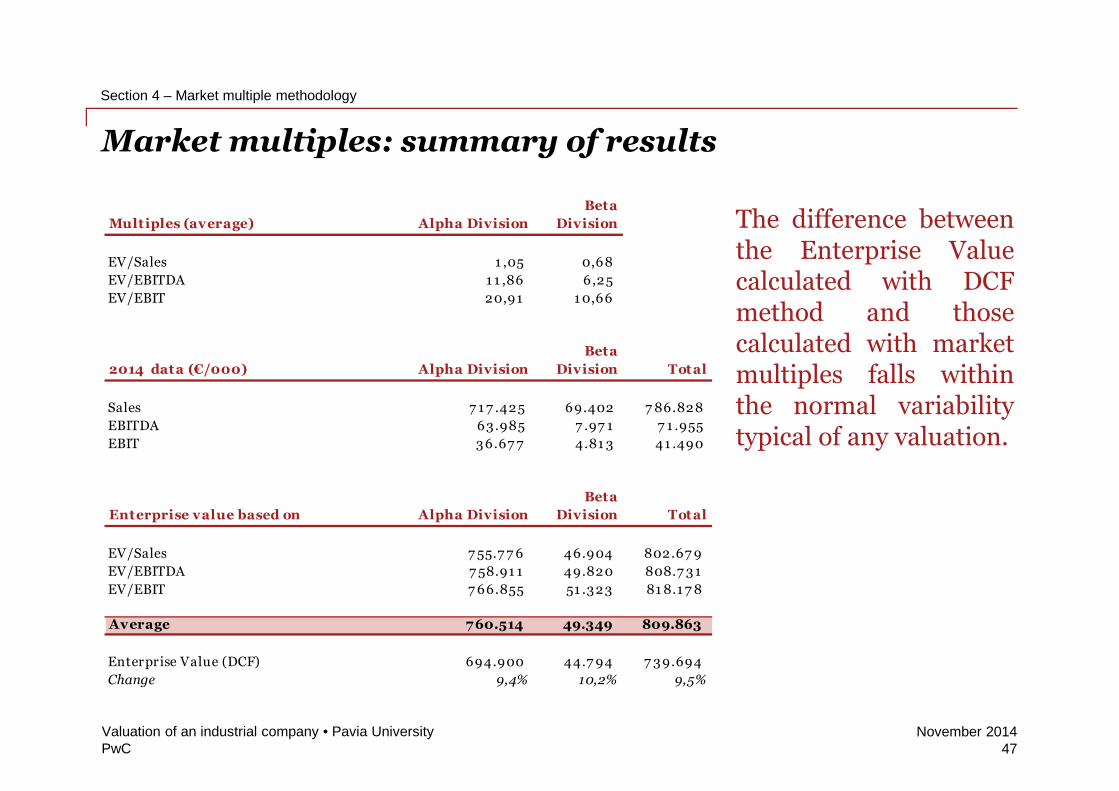

Market multiples: summary of results

The difference betweenthe Enterprise Valuecalculated with DCFmethod and thosecalculated with marketmultiples falls withinthe normal variabilitytypical of any valuation.

Section 4 – Market multiple methodology

Valuation of an industrial company • Pavia University47

Multiples (average) Alpha Division

Beta

Division

EV/Sales 1 ,05 0,68

EV/EBITDA 1 1 ,86 6,25

EV/EBIT 20,91 1 0,66

2014 data (€/000) Alpha Division

Beta

Division Total

Sales 7 1 7 .425 69.402 7 86.828

EBITDA 63.985 7 .97 1 7 1 .955

EBIT 36.67 7 4.81 3 41 .490

Enterprise value based on Alpha Division

Beta

Division Total

EV/Sales 7 55.7 7 6 46.904 802.67 9

EV/EBITDA 7 58.91 1 49.820 808.7 31

EV/EBIT 7 66.855 51 .323 81 8.1 7 8

Average 760.514 49.349 809.863

Enterprise Value (DCF) 694.900 44.7 94 7 39.694

Change 9,4% 10,2% 9,5%

PwCNovember 2014

Equity ValueSection 5

Valuation of an industrial company • Pavia University48

PwCNovember 2014

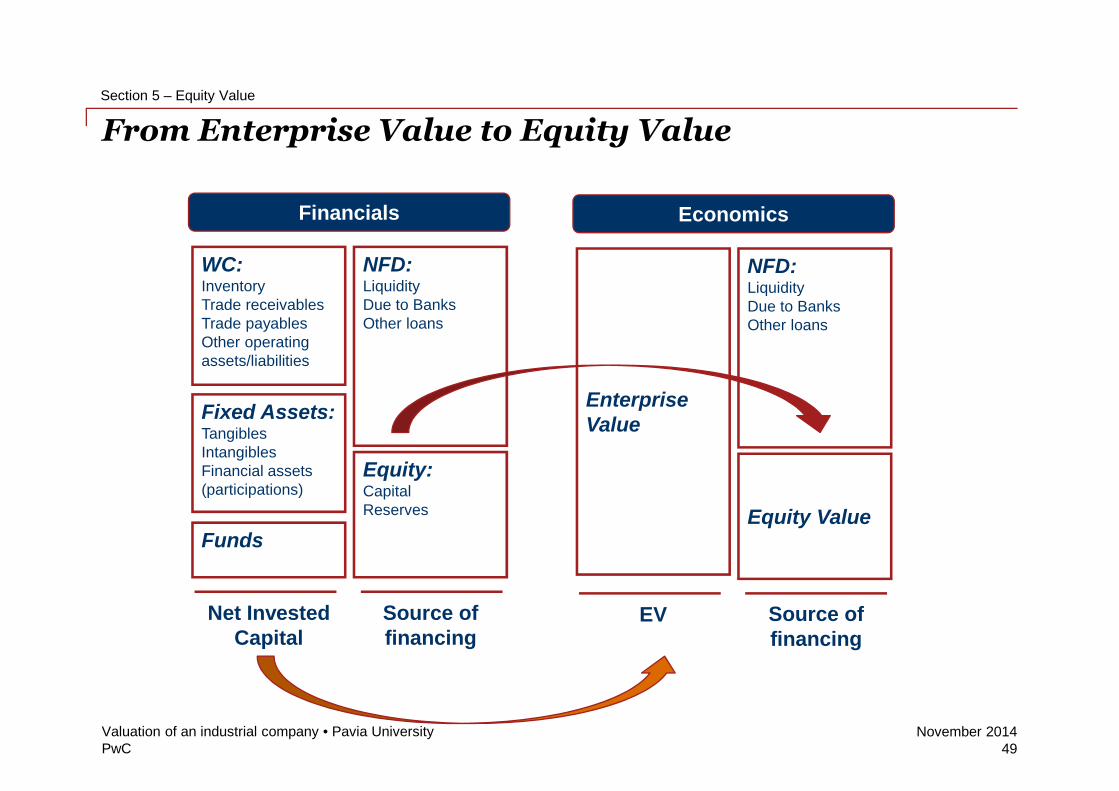

From Enterprise Value to Equity Value

WC:InventoryTrade receivablesTrade payablesOther operatingassets/liabilities

Funds

NFD:LiquidityDue to BanksOther loans

Equity:CapitalReserves

Fixed Assets:TangiblesIntangiblesFinancial assets(participations)

Net InvestedCapital

Source offinancing

Financials

EnterpriseValue

NFD:LiquidityDue to BanksOther loans

Equity Value

EV Source offinancing

Economics

Section 5 – Equity Value

Valuation of an industrial company • Pavia University49

PwCNovember 2014

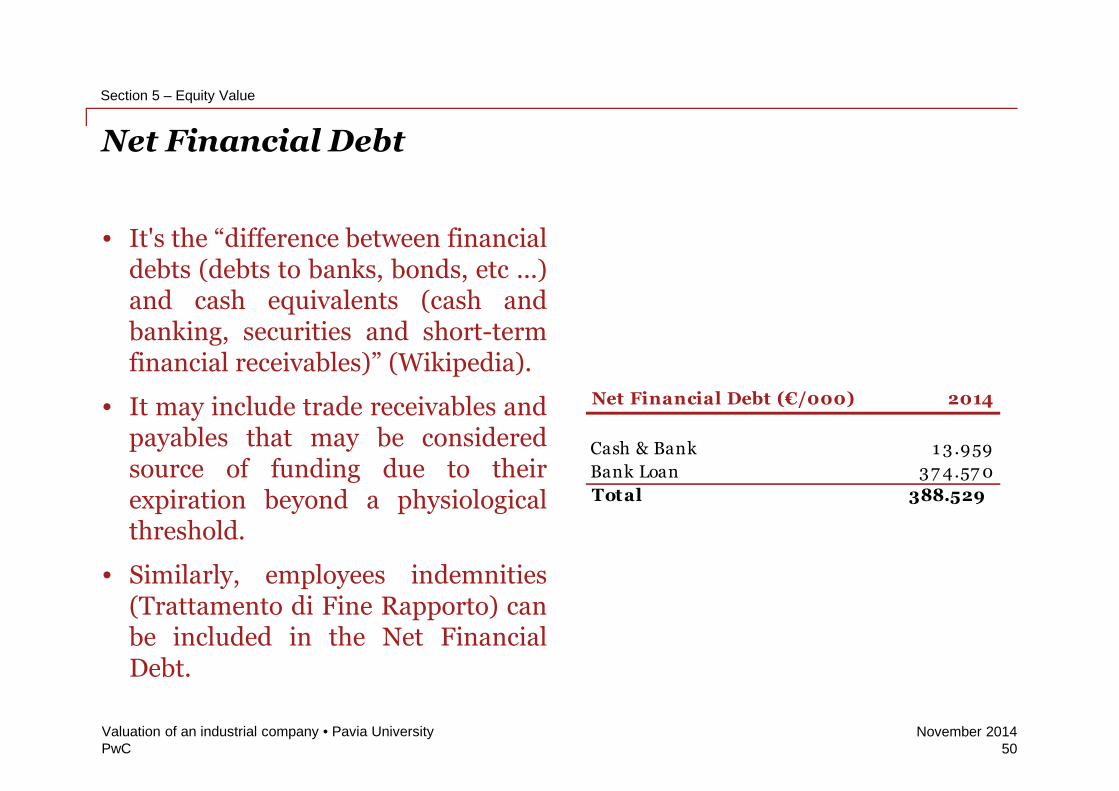

Net Financial Debt

• It's the “difference between financialdebts (debts to banks, bonds, etc ...)and cash equivalents (cash andbanking, securities and short-termfinancial receivables)” (Wikipedia).

• It may include trade receivables andpayables that may be consideredsource of funding due to theirexpiration beyond a physiologicalthreshold.

• Similarly, employees indemnities(Trattamento di Fine Rapporto) canbe included in the Net FinancialDebt.

Section 5 – Equity Value

Valuation of an industrial company • Pavia University50

Net Financial Debt (€/000) 2014

Cash & Bank 1 3.959

Bank Loan 37 4.57 0

Total 388.529

PwCNovember 2014

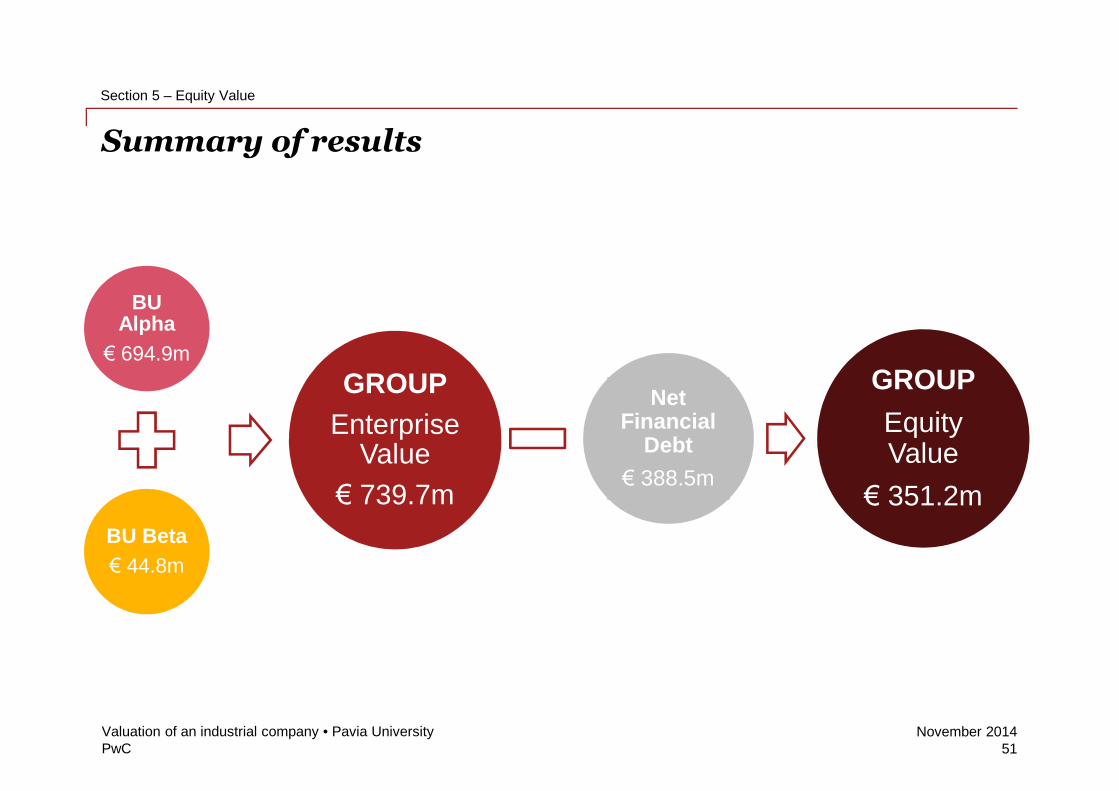

Summary of results

NetFinancial

Debt

€ 388.5m

GROUP

EquityValue

€ 351.2m

Section 5 – Equity Value

Valuation of an industrial company • Pavia University51

BUAlpha

€ 694.9m

BU Beta

€ 44.8m

GROUP

EnterpriseValue

€ 739.7m

Recommended