2016

INSIGHT REPORT

SNPTV GUIDE

TV 2016: INSIGHT REPORT2

BROADCASTING ENVIRONMENT

national channels available to DTT viewers of which:

DIGITAL TERRESTRIAL TELEVISION (DTT) CHANNELS

11 HD

24 free channels

6 pay channels.

30

Source: CSA, CNC, DGMIC, A.C.C.e.S, SNPTV –Guide des chaînes numériques 2016

*Excluding local services and channels distributed exclusively outside mainland France.

BROADCASTING ENVIRONMENT

TV 2016: INSIGHT REPORT 3

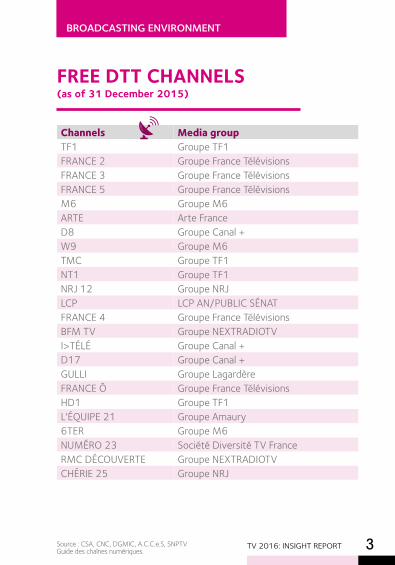

FREE DTT CHANNELS (as of 31 December 2015)

Channels Media groupTF1 Groupe TF1FRANCE 2 Groupe France TélévisionsFRANCE 3 Groupe France TélévisionsFRANCE 5 Groupe France TélévisionsM6 Groupe M6ARTE Arte FranceD8 Groupe Canal +W9 Groupe M6TMC Groupe TF1NT1 Groupe TF1NRJ 12 Groupe NRJ LCP LCP AN/PUBLIC SÉNATFRANCE 4 Groupe France TélévisionsBFM TV Groupe NEXTRADIOTVI>TÉLÉ Groupe Canal +D17 Groupe Canal +GULLI Groupe LagardèreFRANCE Ô Groupe France TélévisionsHD1 Groupe TF1L'ÉQUIPE 21 Groupe Amaury6TER Groupe M6NUMÉRO 23 Société Diversité TV FranceRMC DÉCOUVERTE Groupe NEXTRADIOTVCHÉRIE 25 Groupe NRJ

Source : CSA, CNC, DGMIC, A.C.C.e.S, SNPTVGuide des chaînes numériques.

BROADCASTING ENVIRONMENT

TV 2016: INSIGHT REPORT4

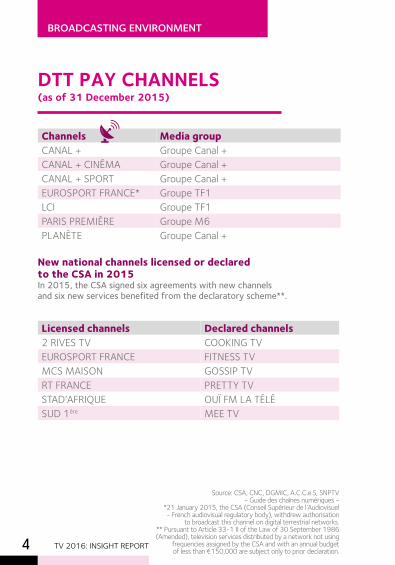

Channels Media groupCANAL + Groupe Canal +CANAL + CINÉMA Groupe Canal +CANAL + SPORT Groupe Canal +EUROSPORT FRANCE* Groupe TF1LCI Groupe TF1PARIS PREMIÈRE Groupe M6PLANÈTE Groupe Canal +

Licensed channels Declared channels2 RIVES TV COOKING TVEUROSPORT FRANCE FITNESS TVMCS MAISON GOSSIP TVRT FRANCE PRETTY TVSTAD’AFRIQUE OUÏ FM LA TÉLÉSUD 1ère MEE TV

DTT PAY CHANNELS (as of 31 December 2015)

New national channels licensed or declared to the CSA in 2015 In 2015, the CSA signed six agreements with new channels and six new services benefited from the declaratory scheme**.

Source: CSA, CNC, DGMIC, A.C.C.e.S, SNPTV - Guide des chaînes numériques -

*21 January 2015, the CSA (Conseil Supérieur de l’Audiovisuel - French audiovisual regulatory body), withdrew authorisation

to broadcast this channel on digital terrestrial networks.** Pursuant to Article 33-1 II of the Law of 30 September 1986 (Amended), television services distributed by a network not using

frequencies assigned by the CSA and with an annual budget of less than €150,000 are subject only to prior declaration.

BROADCASTING ENVIRONMENT

TV 2016: INSIGHT REPORT 5

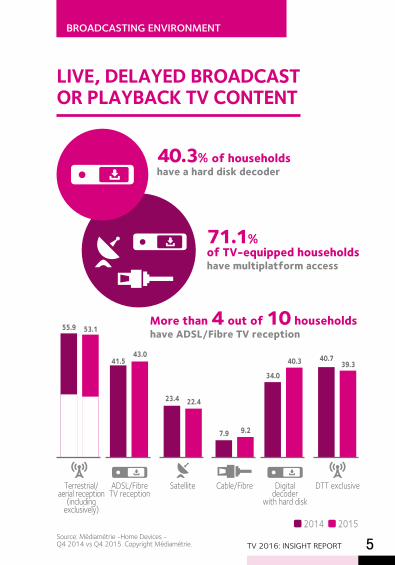

LIVE, DELAYED BROADCAST OR PLAYBACK TV CONTENT

40.3% of householdshave a hard disk decoder

71.1% of TV-equipped householdshave multiplatform access

Source: Médiamétrie -Home Devices - Q4 2014 vs Q4 2015. Copyright Médiamétrie.

9.27.9

Cable/Fibre

22.423.4

Satellite

43.041.5

ADSL/Fibre TV reception

40.3

34.0

Digital decoder

with hard disk

39.340.7

DTT exclusive

More than 4 out of 10 households have ADSL/Fibre TV reception

2014 2015

Terrestrial/ aerial reception

(including exclusively)

53.155.9

excl. 26.4

excl. 28.5

TV 2016: INSIGHT REPORT6

BROADCASTING ENVIRONMENT

Source: Médiamétrie – Médiamat - Period: 29/12/2014 to 03/01/2016 - Sample: Individuals 4-and-up / Channel scope: TF1, France 2, France 3, Canal+ uncoded, France 5,

M6 & Arte DTT channels 2005 & 2012: D8, W9, TMC, NT1, NRJ12, France 4, D17, Gulli, France Ô, HD1, 6Ter,

Numéro 23 & RMC Découverte.

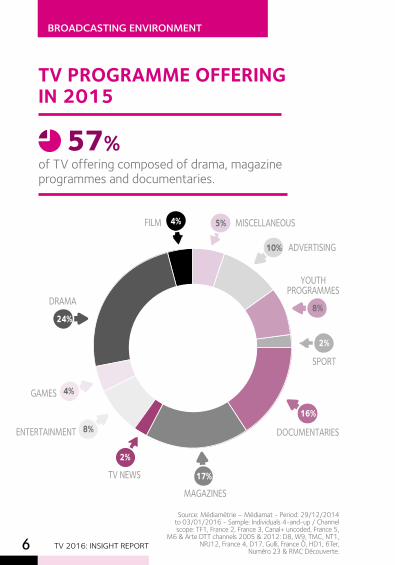

TV PROGRAMME OFFERING IN 2015

24%

2%

8%

4%

4% 5%

10%

8%

2%

16%

17%

DRAMA

TV NEWS

ENTERTAINMENT

GAMES

ADVERTISING

MISCELLANEOUS

YOUTH PROGRAMMES

SPORT

DOCUMENTARIES

MAGAZINES

FILM

of TV offering composed of drama, magazine programmes and documentaries.

57%

BROADCASTING ENVIRONMENT

TV 2016: INSIGHT REPORT 7

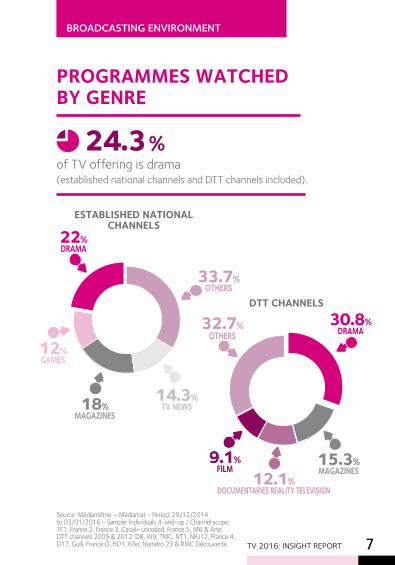

PROGRAMMES WATCHED BY GENRE

of TV offering is drama (established national channels and DTT channels included).

24.3 %

DTT CHANNELS

15.3%MAGAZINES

9.1%FILM

32.7%OTHERS

30.8%DRAMA

12.1%DOCUMENTARIES REALITY TELEVISION

18%MAGAZINES

14.3%TV NEWS

12%GAMES

22%DRAMA

33.7%OTHERS

ESTABLISHED NATIONAL CHANNELS

Source: Médiamétrie – Médiamat - Period: 29/12/2014 to 03/01/2016 - Sample: Individuals 4-and-up / Channel scope: TF1, France 2, France 3, Canal+ uncoded, France 5, M6 & ArteDTT channels 2005 & 2012: D8, W9, TMC, NT1, NRJ12, France 4, D17, Gulli, France Ô, HD1, 6Ter, Numéro 23 & RMC Découverte.

TV 2016: INSIGHT REPORT8

BROADCASTING ENVIRONMENT

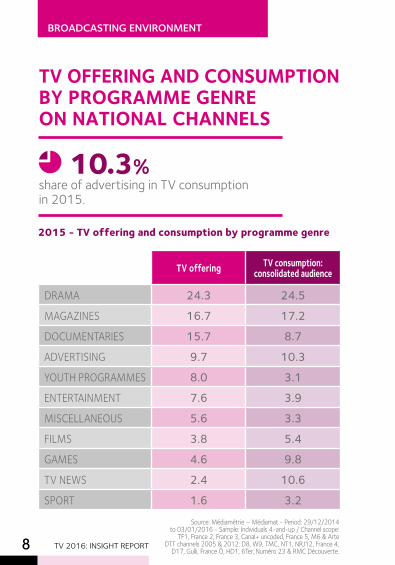

TV OFFERING AND CONSUMPTION BY PROGRAMME GENRE ON NATIONAL CHANNELS

2015 - TV offering and consumption by programme genre

share of advertising in TV consumption in 2015.

10.3%

TV offering TV consumption: consolidated audience

DRAMA 24.3 24.5

MAGAZINES 16.7 17.2

DOCUMENTARIES 15.7 8.7

ADVERTISING 9.7 10.3

YOUTH PROGRAMMES 8.0 3.1

ENTERTAINMENT 7.6 3.9

MISCELLANEOUS 5.6 3.3

FILMS 3.8 5.4

GAMES 4.6 9.8

TV NEWS 2.4 10.6

SPORT 1.6 3.2

Source: Médiamétrie – Médiamat - Period: 29/12/2014 to 03/01/2016 - Sample: Individuals 4-and-up / Channel scope:

TF1, France 2, France 3, Canal+ uncoded, France 5, M6 & ArteDTT channels 2005 & 2012: D8, W9, TMC, NT1, NRJ12, France 4,

D17, Gulli, France Ô, HD1, 6Ter, Numéro 23 & RMC Découverte.

AUDIOVISUAL PRACTICES

TV 2016: INSIGHT REPORT 9

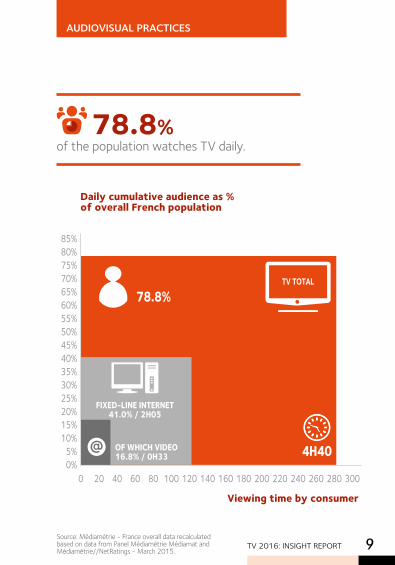

Daily cumulative audience as % of overall French population

Viewing time by consumer

4H40

TV TOTAL

FIXED-LINE INTERNET 41.0% / 2H05

85%80%75%70%65%60%55%50%45%40%35%30%25%20%15%10%

5%0%

0 20 40 60 80 100 120 140 160 180 200 220 240 260 280 300

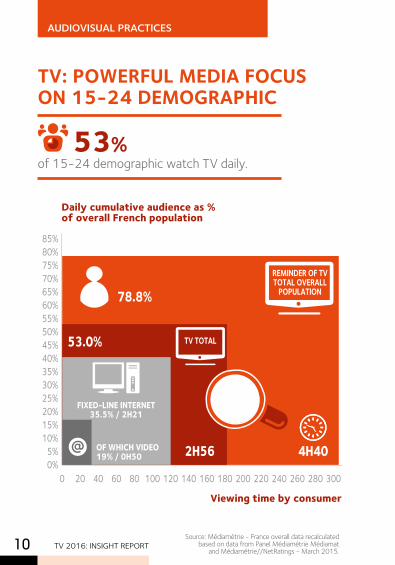

78.8%

OF WHICH VIDEO16.8% / 0H33

Source: Médiamétrie - France overall data recalculated based on data from Panel Médiamétrie Médiamat and Médiamétrie//NetRatings - March 2015.

of the population watches TV daily.78.8%

TV 2016: INSIGHT REPORT10Source: Médiamétrie - France overall data recalculated

based on data from Panel Médiamétrie Médiamat and Médiamétrie//NetRatings - March 2015.

AUDIOVISUAL PRACTICES

Daily cumulative audience as % of overall French population

Viewing time by consumer

4H402H56

REMINDER OF TV TOTAL OVERALL

POPULATION

TV TOTAL

FIXED-LINE INTERNET 35.5% / 2H21

85%80%75%70%65%60%55%50%45%40%35%30%25%20%15%10%

5%0%

0 20 40 60 80 100 120 140 160 180 200 220 240 260 280 300

78.8%

53.0%

OF WHICH VIDEO 19% / 0H50

TV: POWERFUL MEDIA FOCUS ON 15-24 DEMOGRAPHIC

of 15-24 demographic watch TV daily. 53%

FOCUS ON 15-24

DEMOGRAPHIC

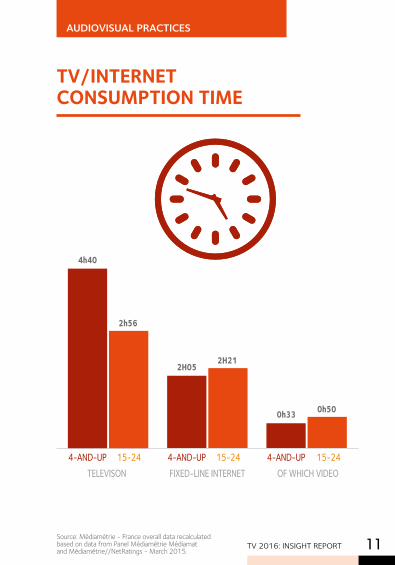

TV/INTERNET CONSUMPTION TIME

TELEVISON FIXED-LINE INTERNET OF WHICH VIDEO

0h33 0h50

2H052H21

4h40

4-AND-UP 4-AND-UP 4-AND-UP

2h56

15-24 15-24 15-24

Source: Médiamétrie - France overall data recalculated based on data from Panel Médiamétrie Médiamat and Médiamétrie//NetRatings - March 2015.

AUDIOVISUAL PRACTICES

TV 2016: INSIGHT REPORT 11

TV 2016: INSIGHT REPORT12

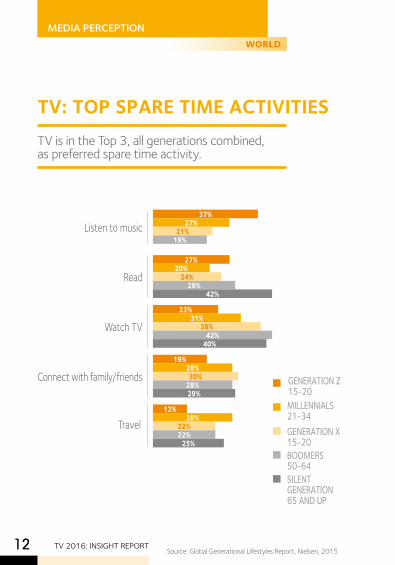

MEDIA PERCEPTION WORLD

TV: TOP SPARE TIME ACTIVITIESTV is in the Top 3, all generations combined, as preferred spare time activity.

GENERATION Z15-20MILLENNIALS21-34GENERATION X15-20BOOMERS 50-64SILENT GENERATION 65 AND UP

Listen to music37%

27%21%

19%

Read27%

20%24%

29%42%

Watch TV23%

31%38%

42%40%

Connect with family/friends 19%

28%30%

28%29%

12%28%

22%22%

25%

Travel

Source: Global Generational Lifestyles Report, Nielsen, 2015.

MEDIA PERCEPTION

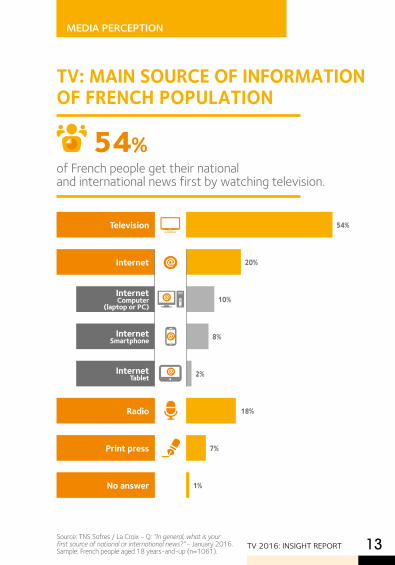

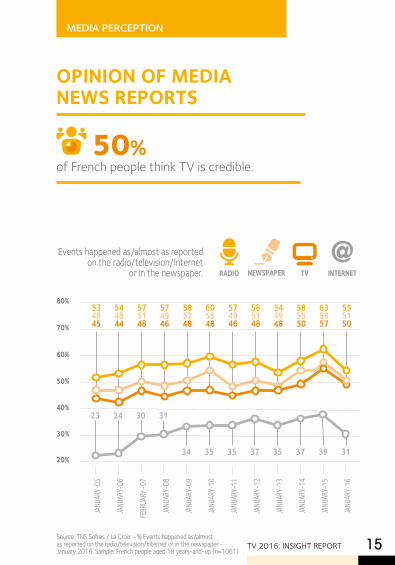

TV 2016: INSIGHT REPORT 13Source: TNS Sofres / La Croix - Q: “In general, what is your first source of national or international news?” - January 2016. Sample: French people aged 18 years-and-up (n=1061).

TV: MAIN SOURCE OF INFORMATION OF FRENCH POPULATION

of French people get their national and international news first by watching television.

54%

InternetComputer

(laptop or PC)

Print press

54%

20%

10%

8%

2%

18%

7%

1%

Television

Internet Tablet

Internet Smartphone

No answer

Radio

Internet

MEDIA PERCEPTION

Source: TNS Sofres / La Croix - Q: Source: “In general, what source of information do you use most often to learn more about certain

national or international news items?” - January 2016. Sample: French people aged 18 years-and-up (n=1061).

of French people watch news on general-interest channels, as their first and second choice, to learn more about certain news items.

of French people watch the television news on general-interest channels first to learn more about certain news items.

59%

38%

38

24

10

8

8

3

3

2

1

1

1

1

21 59

44

25

15

17

8

4

4

4

3

6

20

15

7

9

5

2

2

3

3

3

General-interest channels

24-hour news channels

Radio

Print press websites or mobile apps

National headlines of daily newspapers

Magazines

Specialist blogsTV channel or radio station websites

or mobile apps Free newspapers

Social media

Other websites

No answer

TV 2016: INSIGHT REPORT14

Events happened as/almost as reported on the radio/television/Internet

or in the newspaper.

JANU

ARY-

05

JANU

ARY-

06

FEBR

UARY

-07

JANU

ARY-

08

JANU

ARY-

09

JANU

ARY-

10

JANU

ARY-

11

JANU

ARY-

12

JANU

ARY-

13

JANU

ARY-

14

JANU

ARY-

15

JANU

ARY-

16

20%

30%

40%

50%

60%

80%

RADIO TVNEWSPAPER INTERNET

70%

23 24 30 31

3534 35 37 35 37 3139

534845

544844

575148

574946

585248

605548

574946

585148

544948

585550

555150

635857

OPINION OF MEDIA NEWS REPORTS

of French people think TV is credible. 50%

MEDIA PERCEPTION

TV 2016: INSIGHT REPORT 15Source: TNS Sofres / La Croix - % Events happened as/almost as reported on the radio/television/Internet or in the newspaper - January 2016. Sample: French people aged 18 years-and-up (n=1061)

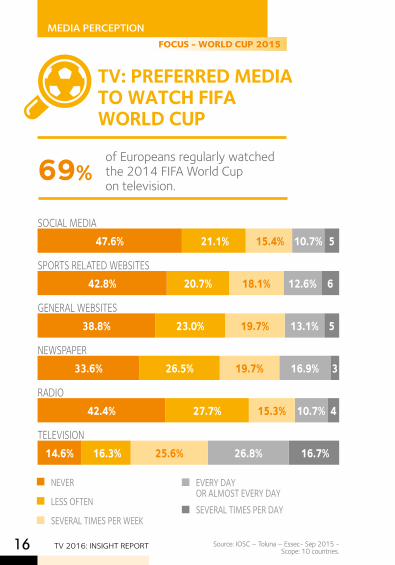

TV 2016: INSIGHT REPORT16 Source: IOSC – Toluna – Essec- Sep 2015 - Scope: 10 countries.

MEDIA PERCEPTION

of Europeans regularly watched the 2014 FIFA World Cup on television.

69%

TV: PREFERRED MEDIA TO WATCH FIFA WORLD CUP

NEVER

LESS OFTEN

SEVERAL TIMES PER WEEK

EVERY DAY OR ALMOST EVERY DAYSEVERAL TIMES PER DAY

510.7% 15.4% 21.1%47.6%

612.6%18.1%20.7%42.8%

513.1%19.7%23.0%38.8%

316.9%19.7%26.5%33.6%

410.7%15.3%27.7%42.4%

16.7%26.8%25.6% 16.3%14.6%TELEVISION

GENERAL WEBSITES

SOCIAL MEDIA

NEWSPAPER

SPORTS RELATED WEBSITES

RADIO

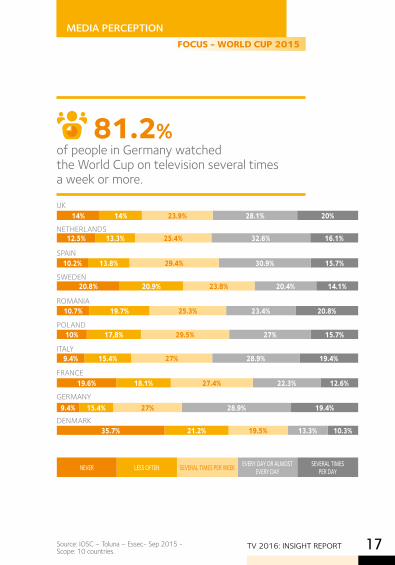

FOCUS - WORLD CUP 2015

MEDIA PERCEPTION FOCUS - WORLD CUP 2015

TV 2016: INSIGHT REPORT 17

of people in Germany watched the World Cup on television several times a week or more.

81.2%

20%28.1%23.9%14%14%

16.1%32.6%25.4%13.3%12.5%

15.7%30.9%29.4%13.8%10.2%

20.8%23.4%25.3%19.7%10.7%

15.7%27%29.5%17,8%10%

19.4%28.9%27%15.4%9.4%

19.4%28.9%27%15.4%9.4%

14.1%20.4%23.8%20.9%20.8%

10.3%13.3%19.5%21.2%35.7%

SEVERAL TIMES PER DAY

EVERY DAY OR ALMOST EVERY DAYSEVERAL TIMES PER WEEKLESS OFTENNEVER

12.6%22.3%27.4%18.1%19.6%

UK

NETHERLANDS

SPAIN

SWEDEN

ROMANIA

POLAND

ITALY

FRANCE

GERMANY

DENMARK

Source: IOSC – Toluna – Essec- Sep 2015 - Scope: 10 countries.

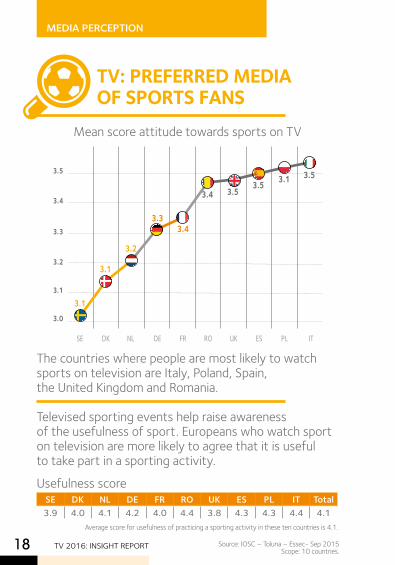

TV 2016: INSIGHT REPORT18 Source: IOSC – Toluna – Essec- Sep 2015 Scope: 10 countries.

MEDIA PERCEPTION

The countries where people are most likely to watch sports on television are Italy, Poland, Spain, the United Kingdom and Romania.

Televised sporting events help raise awareness of the usefulness of sport. Europeans who watch sport on television are more likely to agree that it is useful to take part in a sporting activity.

Usefulness score

TV: PREFERRED MEDIA OF SPORTS FANS

Average score for usefulness of practicing a sporting activity in these ten countries is 4.1.

3.5

3.4

3.3

3.2

3.1

3.0

UKNL ESSE RO PL ITFRDEDK

3.1

3.1

3.2

3.33.4

3.4 3.53.5 3.1 3.5

Mean score attitude towards sports on TV

Country

Estim

ated

marg

inal m

eans

SE DK NL DE FR RO UK ES PL IT Total 3.9 4.0 4.1 4.2 4.0 4.4 3.8 4.3 4.3 4.4 4.1

Mean score attitude towards sports on TV

TV 2016: INSIGHT REPORT 19

GLOBAL VIEWERS CONTINUE TO WATCH SPORT ON TV

watched the France vs New Zealand World Cup Quarter Final, record audience 2015, all genres and channels combined.

REPUBLIC OF IRELAND: Irish sports account for 33% of sport broadcast on television and 48% of consumption.

THAILAND:• 14.9 million viewers - South East Asia Cup Final (AFF Suzuki Cup) against Malaysia on Channel 7 (69.5% audience share). • Women’s volleyball: China vs Thailand match: 8.7 million viewers in Thailand (43.4% audience share) 16 July 2015 on Channel 7.MALAYSIA and PORTUGAL, respectively 79% and 82% of sport watched on television was football / 87% in TURKEY.

33%

MEDIA PERCEPTION

12.2 million people in France

14.9 million viewers

TV 2016: INSIGHT REPORT20 Source: Yearly Sport Fact 2015 - Eurodata TV Médiamétrie.

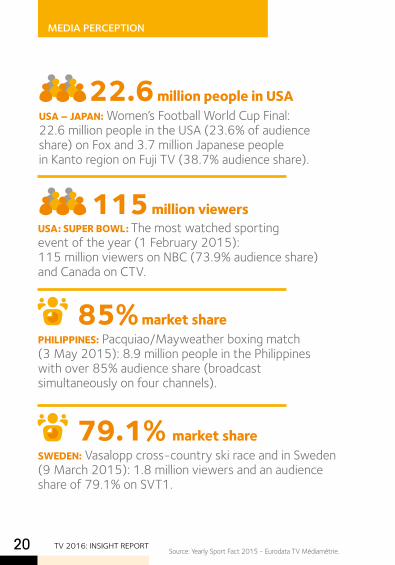

USA – JAPAN: Women’s Football World Cup Final: 22.6 million people in the USA (23.6% of audience share) on Fox and 3.7 million Japanese people in Kanto region on Fuji TV (38.7% audience share).

USA: SUPER BOWL: The most watched sporting event of the year (1 February 2015): 115 million viewers on NBC (73.9% audience share) and Canada on CTV.

22.6 million people in USA

115 million viewers

85% market share

79.1% market share

PHILIPPINES: Pacquiao/Mayweather boxing match (3 May 2015): 8.9 million people in the Philippines with over 85% audience share (broadcast simultaneously on four channels).

SWEDEN: Vasalopp cross-country ski race and in Sweden (9 March 2015): 1.8 million viewers and an audience share of 79.1% on SVT1.

MEDIA PERCEPTION

Daily or almost

Once a week

Once a month

Less often or never

Girls 11-1489% 9%

Boys 4-682% 8% 10%

1%

8%Boys 7-10

91%

1%Girls 7-1088% 8%

1%Boys 11-1491% 3% 5%

Girls 4-692% 2% 6%

3%

3%

MEDIA PERCEPTION

TV 2016: INSIGHT REPORT 21

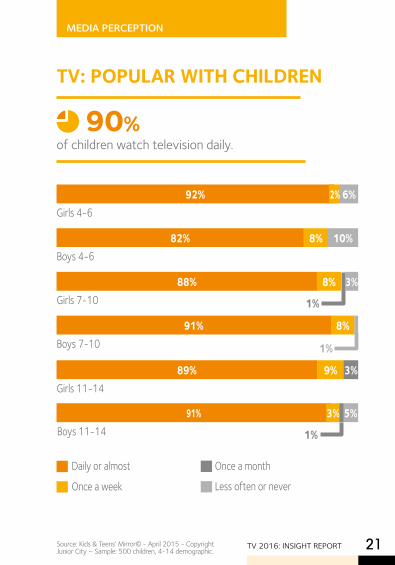

of children watch television daily.

TV: POPULAR WITH CHILDREN

90%

Source: Kids & Teens’ Mirror© - April 2015 - Copyright Junior City – Sample: 500 children, 4-14 demographic.

TV 2016: INSIGHT REPORT22

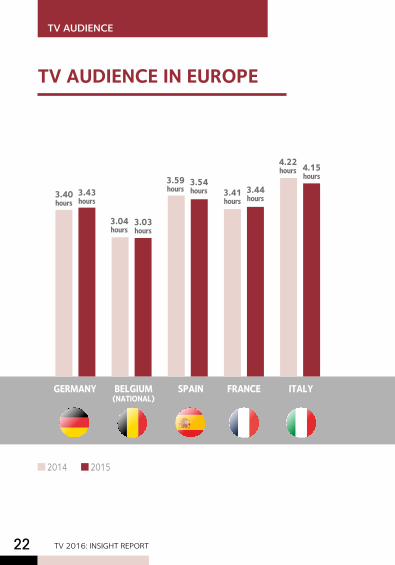

TV AUDIENCE IN EUROPE

3.43 hours

3.40 hours

GERMANY BELGIUM SPAIN FRANCE ITALY (NATIONAL)

3.04 hours

3.03 hours

3.59 hours

3.54 hours 3.41

hours3.44 hours

4.22 hours 4.15

hours

2014 2015

AUDIENCE TVTV AUDIENCE

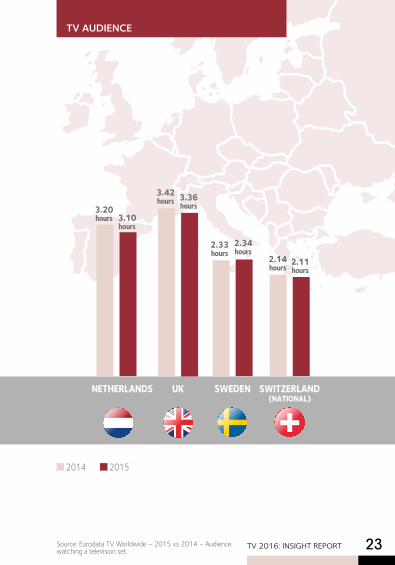

TV 2016: INSIGHT REPORT 23Source: Eurodata TV Worldwide – 2015 vs 2014 – Audience watching a television set.

2.33 hours

2.34 hours

3.20 hours 3.10

hours

3.42 hours 3.36

hours

2.14 hours

2.11 hours

NETHERLANDS UK SWEDEN SWITZERLAND (NATIONAL)

AUDIENCE TVTV AUDIENCE

2014 2015

TV 2016: INSIGHT REPORT24

In 2015, French people had on average 15.6 contacts with television on an average day.

15.6 contacts

Source: Media In Life - Sample Monday to Sunday, cumulative 2015. Sample: individuals 13-and-up

TV: MAIN MEDIA CONTACT

MONDAY TO SUNDAY CUMULATIVE 2015 MONDAY TO SUNDAY CUMULATIVE 2014

RADIO 8.9

9.0

TELEVISION 16.3

15.6

INTERNET 5.5

3.1PRINT PRESS

1.5

1.6GAME/VIDEO GAME

1.0

1.2VIDEO

2.4

2.4MUSIC

5.2

5.2MOBILE PHONE

5.4

3.2

AUDIENCE TVTV AUDIENCE

TV 2016: INSIGHT REPORT 25

TV: 2015 KEY FIGURES

Source: Médiamétrie – Médiamat – Consolidated audience in 2015 – Sample: individuals 4-and-up.

viewers watch TV daily on a television set.45.2 million

DAILY VIEWING TIME PER TV VIEWER

3.44 hours

4.41 hours

DAILY VIEWING TIME PER INDIVIDUAL

45.2M

DAILY TV VIEWERS

9.20 pm

PEAK TIME: NUMBER OF TV VIEWERS

25.6M

AUDIENCE TVTV AUDIENCE

TV 2016: INSIGHT REPORT26

Source: Médiamétrie – Médiamat – Consolidated audience in 2015 – Sample: individuals 4-and-up / 1989: 6-and-up

/ since 2011: Consolidated audience with delayed broadcast / since 29/09/14: Consolidated audience with delayed

broadcast and playback. Individual viewing time on TV screen in hours, minutes.

EVOLUTION OF TV AUDIENCES BETWEEN 1989 AND 2015 RECAP

more daily TV viewing time over 26 years.44 minutes

1989 1994 1999 2004 2009 2014 2015

3.44hours

3.00 hours

2.57 hours

3.09 hours

3.24 hours

3.25 hours

3.41 hours

AUDIENCE TVTV AUDIENCE

TV 2016: INSIGHT REPORT 27

AUDIENCE TVTV AUDIENCE

50,0

40,0

30,0

20,0

10,0

0,0

3.00 -

3.15

AM

4.00 -

4.15

AM

5.00 -

5.15

AM

6.00 -

6.15

AM

7.00 -

7.15

AM

8.00 -

8.15 A

M

9.00 -

9.15 A

M

10.00

-10.1

5 AM

11.00

-11.1

5 AM

12.00

-12.1

5 PM

1.00 -

1.15 P

M

2.00 -

2.15 P

M

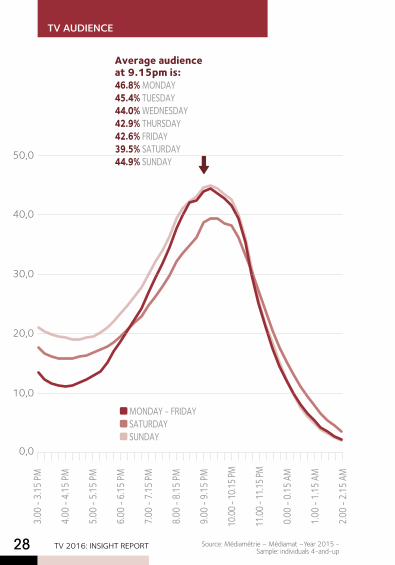

Average audience at 8am is:7.1% MONDAY7.2% TUESDAY7.2% WEDNESDAY7.1% THURSDAY7.1% FRIDAY6.3% SATURDAY5.2% SUNDAY

Average audience at 1.15pm is:23.3% MONDAY22.2% TUESDAY23.9% WEDNESDAY21.9% THURSDAY22.4% FRIDAY25.9% SATURDAY26.1% SUNDAY

AVERAGE DAILY AUDIENCE IN A TYPICAL WEEK

TV 2016: INSIGHT REPORT28

AUDIENCE TVTV AUDIENCE3.0

0 - 3.

15 PM

4.00 -

4.15

PM

5.00 -

5.15

PM

6.00 -

6.15

PM

7.00 -

7.15

PM

8.00 -

8.15

PM

9.00 -

9.15

PM

10.00

- 10.1

5 PM

11.00

- 11.1

5 PM

0.00 -

0.15

AM

1.00 -

1.15

AM

2.00 -

2.15

AM

Average audience at 9.15pm is:46.8% MONDAY45.4% TUESDAY44.0% WEDNESDAY42.9% THURSDAY42.6% FRIDAY39.5% SATURDAY44.9% SUNDAY

MONDAY - FRIDAY SATURDAY SUNDAY

50,0

40,0

30,0

20,0

10,0

0,0

Source: Médiamétrie – Médiamat –Year 2015 - Sample: individuals 4-and-up

TV 2016: INSIGHT REPORT 29

AUDIENCE TVTV AUDIENCE

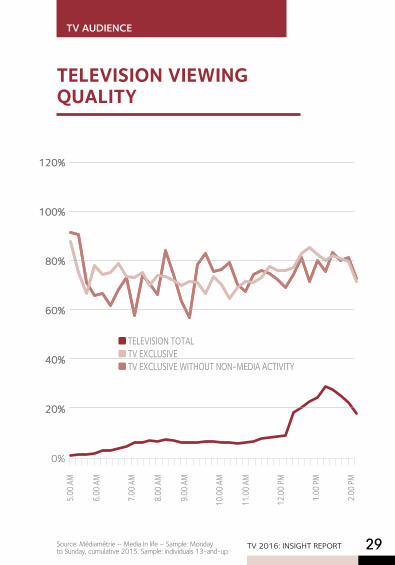

TELEVISION TOTAL TV EXCLUSIVE TV EXCLUSIVE WITHOUT NON-MEDIA ACTIVITY

5.00 A

M

6.00 A

M

7.00 A

M

8.00 A

M

9.00 A

M

10.00

AM

11.00

AM

12.00

PM

1.00 P

M

2.00 P

M

0%

20%

40%

60%

80%

120%

100%

20%

40%

60%

80%

120%

100%

TELEVISION VIEWING QUALITY

Source: Médiamétrie – Media In life – Sample: Monday to Sunday, cumulative 2015. Sample: individuals 13-and-up.

TV 2016: INSIGHT REPORT30

AUDIENCE TVTV AUDIENCE

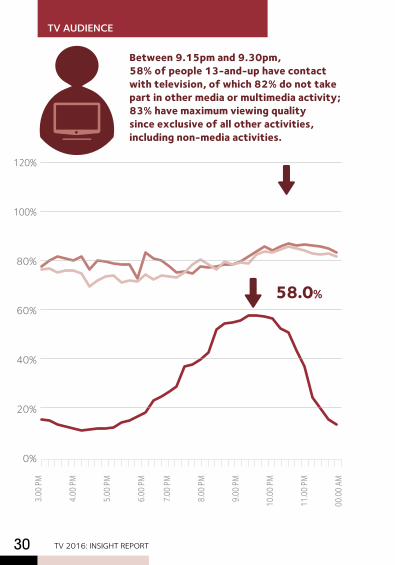

Between 9.15pm and 9.30pm, 58% of people 13-and-up have contact with television, of which 82% do not take part in other media or multimedia activity; 83% have maximum viewing quality since exclusive of all other activities, including non-media activities.

3.00 P

M

4.00 P

M

5.00 P

M

6.00 P

M

7.00 P

M

8.00 P

M

9.00 P

M

10.00

PM

11.00

PM

00.00

AM

58.0%

0%

20%

40%

60%

80%

120%

100%

ADVERTISING MARKET

TV 2016: INSIGHT REPORT 31

3 KEY FIGURES: “NET” ADVERTISING REVENUES

Source IREP.

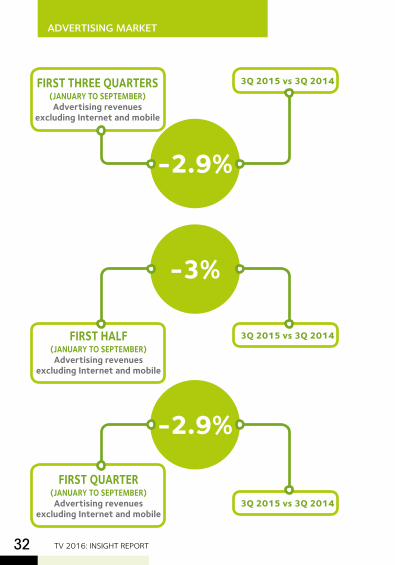

Over the first three quarters of 2015, media advertising revenues (established + advertising mail + unaddressed mail, excluding Internet and mobile) were down 2.9% to €6.118 million.

Over the same period in 2014, revenues were down 4% (€6.299 million). The one percentage point differential reported in the first half of 2015 therefore continued in the first three quarters of 2015.

On a comparable basis, the trend observed by the French institute of advertising research and studies (IREP) continued.Market remains stable in each quarter (negative trend):Down 2.9% in first quarter (first quarter, advertising revenues excluding Internet and mobile / Q1 2015 vs Q1 2014)Down 3% in first half (first half, advertising revenues excluding Internet and mobile / First half 2015 vs First half 2014)Down 2.9% in first nine months of year (first three quarters, January to September, advertising revenues excluding Internet and mobile / 3Q 2015 vs 3Q 2014).

ADVERTISING MARKET

TV 2016: INSIGHT REPORT32

3Q 2015 vs 3Q 2014 FIRST HALF (JANUARY TO SEPTEMBER)Advertising revenues

excluding Internet and mobile

-3%

3Q 2015 vs 3Q 2014FIRST THREE QUARTERS (JANUARY TO SEPTEMBER)Advertising revenues

excluding Internet and mobile

-2.9%

3Q 2015 vs 3Q 2014

FIRST QUARTER (JANUARY TO SEPTEMBER)Advertising revenues

excluding Internet and mobile

-2.9%

TV 2016: INSIGHT REPORT 33

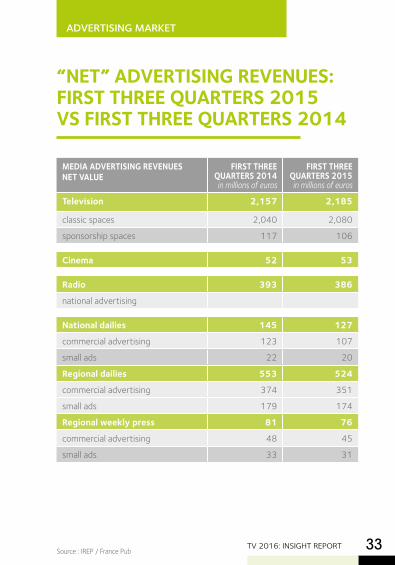

“NET” ADVERTISING REVENUES: FIRST THREE QUARTERS 2015 VS FIRST THREE QUARTERS 2014

Source : IREP / France Pub

MEDIA ADVERTISING REVENUES NET VALUE

FIRST THREE QUARTERS 2014 in millions of euros

FIRST THREE QUARTERS 2015 in millions of euros

Television 2,157 2,185

classic spaces 2,040 2,080

sponsorship spaces 117 106

Cinema 52 53

Radio 393 386

national advertising

National dailies 145 127

commercial advertising 123 107

small ads 22 20

Regional dailies 553 524

commercial advertising 374 351

small ads 179 174

Regional weekly press 81 76

commercial advertising 48 45

small ads 33 31

ADVERTISING MARKET

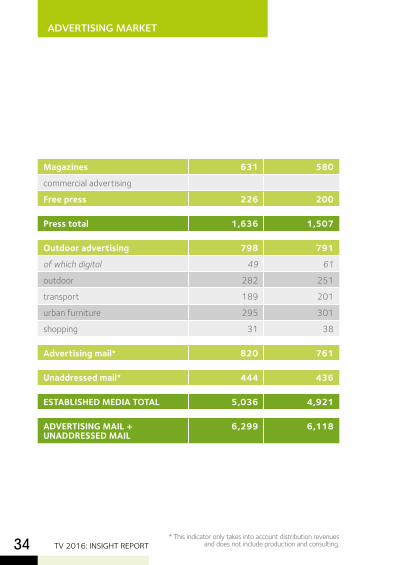

TV 2016: INSIGHT REPORT34* This indicator only takes into account distribution revenues

and does not include production and consulting.

Magazines 631 580

commercial advertising

Free press 226 200

Press total 1,636 1,507

Outdoor advertising 798 791

of which digital 49 61

outdoor 282 251

transport 189 201

urban furniture 295 301

shopping 31 38

Advertising mail* 820 761

Unaddressed mail* 444 436

ESTABLISHED MEDIA TOTAL 5,036 4,921

ADVERTISING MAIL + UNADDRESSED MAIL

6,299 6,118

ADVERTISING MARKET

CROSS-MEDIA ADVERTISING MARKET

TV 2016: INSIGHT REPORT 35

CROSS-MEDIA ADVERTISING MARKET - ADVERTISING FIGURES AND TRENDS IN NET VALUE

invested by advertisers in 2015 all media combined.

€9.3 billion net (down 0.6%)

METHODOLOGICAL NOTEAdTrends combines raw data from Kantar Media with net data from France Pub. The raw/net conversion is performed monthly based on modelling that takes into account France Pub key conversion data calculated per media and per advertiser grouping. Media scope: Press excluding trade press; television excluding sponsorship; outdoor advertising only in large-format segments; urban furniture and transport; Internet (display and search); radio and cinema. These initial trends were identified based on the results from first 11 months of the year and an estimate for December 2015.

NB:

Source: Kantar Media - AdTrends.

CROSS-MEDIA ADVERTISING MARKET

TV 2016: INSIGHT REPORT36

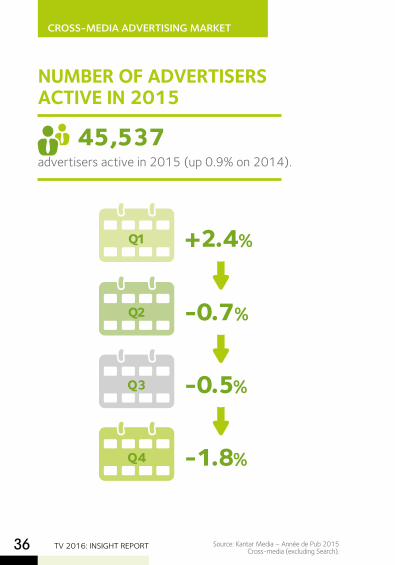

NUMBER OF ADVERTISERS ACTIVE IN 2015

advertisers active in 2015 (up 0.9% on 2014).45,537

+2.4%

-0.7%

-0.5%

-1.8%

Source: Kantar Media – Année de Pub 2015 Cross-media (excluding Search).

Q1

Q2

Q3

Q4

CROSS-MEDIA ADVERTISING MARKET

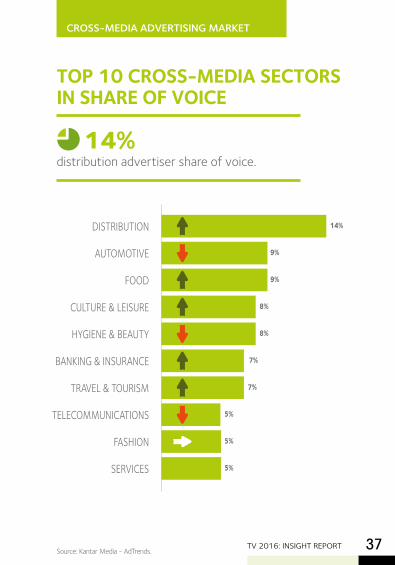

DISTRIBUTION

AUTOMOTIVE

FOOD

CULTURE & LEISURE

HYGIENE & BEAUTY

BANKING & INSURANCE

TRAVEL & TOURISM

TELECOMMUNICATIONS

FASHION

SERVICES

TOP 10 CROSS-MEDIA SECTORS IN SHARE OF VOICE

distribution advertiser share of voice.14%

TV 2016: INSIGHT REPORT 37

14%

9%

9%

8%

8%

7%

7%

5%

5%

5%

Source: Kantar Media - AdTrends.

Source : Kantar Media - Current cross-media.

ADVERTISING MARKET - TTV

TV 2016: INSIGHT REPORT38

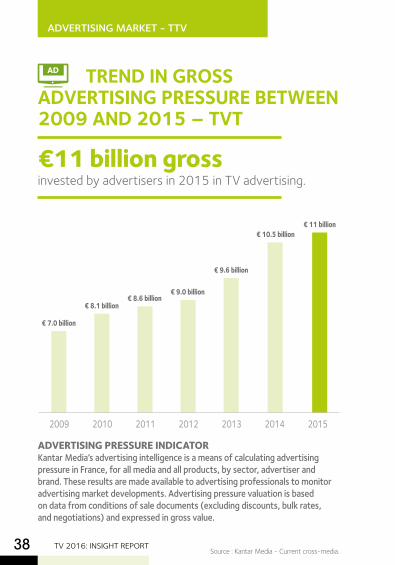

TREND IN GROSS ADVERTISING PRESSURE BETWEEN 2009 AND 2015 – TVT

2009 2010 2011 2012 2013 2014 2015

invested by advertisers in 2015 in TV advertising.€11 billion gross

AD

€ 7.0 billion

€ 8.1 billion€ 8.6 billion

€ 9.0 billion

€ 9.6 billion

€ 10.5 billion€ 11 billion

ADVERTISING PRESSURE INDICATORKantar Media’s advertising intelligence is a means of calculating advertising pressure in France, for all media and all products, by sector, advertiser and brand. These results are made available to advertising professionals to monitor advertising market developments. Advertising pressure valuation is based on data from conditions of sale documents (excluding discounts, bulk rates, and negotiations) and expressed in gross value.

ADVERTISING MARKET - TTV

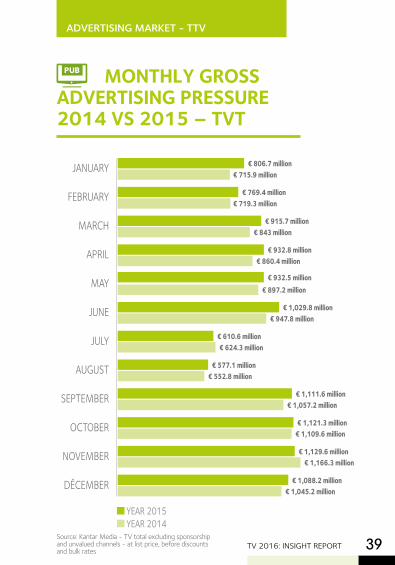

JANUARY

FEBRUARY

MARCH

APRIL

MAY

JUNE

JULY

AUGUST

SEPTEMBER

OCTOBER

NOVEMBER

DÉCEMBER

YEAR 2015 YEAR 2014

€ 715.9 million

€ 719.3 million

€ 843 million

€ 860.4 million

€ 897.2 million

€ 947.8 million

€ 624.3 million

€ 552.8 million

€ 1,057.2 million

€ 1,109.6 million

€ 1,166.3 million

€ 1,045.2 million

€ 806.7 million

€ 769.4 million

€ 915.7 million

€ 932.8 million

€ 932.5 million

€ 1,029.8 million

€ 610.6 million

€ 577.1 million

€ 1,111.6 million

€ 1,121.3 million

€ 1,129.6 million

€ 1,088.2 million

MONTHLY GROSS ADVERTISING PRESSURE 2014 VS 2015 – TVT

TV 2016: INSIGHT REPORT 39Source: Kantar Media - TV total excluding sponsorship and unvalued channels - at list price, before discounts and bulk rates

PUB

Source: Kantar Media - TV total excluding sponsorship and unvalued channels - at list price, before discounts and bulk rates.

ADVERTISING MARKET - TTV

TV 2016: INSIGHT REPORT40

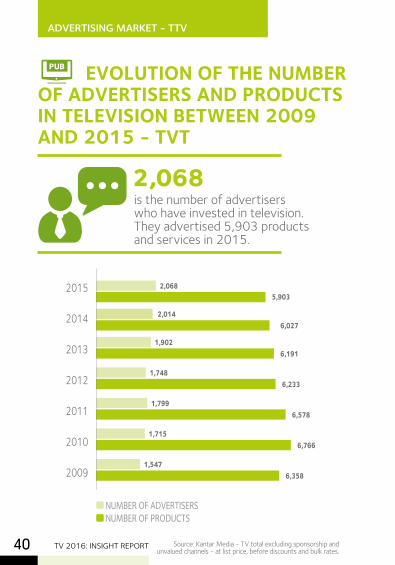

EVOLUTION OF THE NUMBER OF ADVERTISERS AND PRODUCTS IN TELEVISION BETWEEN 2009 AND 2015 - TVT

NUMBER OF ADVERTISERS NUMBER OF PRODUCTS

is the number of advertisers who have invested in television. They advertised 5,903 products and services in 2015.

2,068

2015

2014

2013

2012

2011

2010

2009

1,902

2,014

1,748

1,799

1,715

1,547

2,068

6,191

6,027

6,233

6,578

6,766

6,358

5,903

PUB

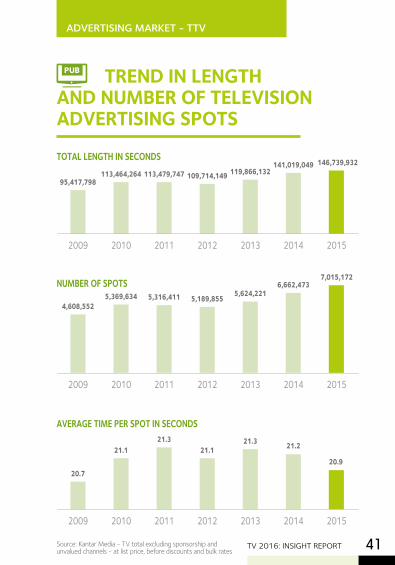

TREND IN LENGTH AND NUMBER OF TELEVISION ADVERTISING SPOTS

ADVERTISING MARKET - TTV

TV 2016: INSIGHT REPORT 41

2009 2010 2011 2012 2013 2014 2015

2009 2010 2011 2012 2013 2014 2015

2009 2010 2011 2012 2013 2014 2015

146,739,932

95,417,798113,464,264 113,479,747 109,714,149 119,866,132

141,019,049

7,015,172

20.9

4,608,552

20.7

5,369,634

21.1

5,316,411

21.3

5,189,855

21.1

5,624,2216,662,473

21.3 21.2

TOTAL LENGTH IN SECONDS

NUMBER OF SPOTS

AVERAGE TIME PER SPOT IN SECONDS

PUB

Source: Kantar Media - TV total excluding sponsorship and unvalued channels - at list price, before discounts and bulk rates

Source: Kantar Media - TV total excluding sponsorship and unvalued channels - at list price, before discounts and bulk rates

ADVERTISING MARKET - TTV

TV 2016: INSIGHT REPORT42

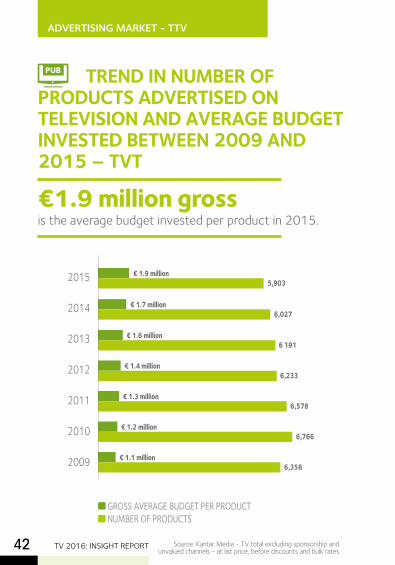

TREND IN NUMBER OF PRODUCTS ADVERTISED ON TELEVISION AND AVERAGE BUDGET INVESTED BETWEEN 2009 AND 2015 – TVT

PUB

is the average budget invested per product in 2015.€1.9 million gross

2015

2014

2013

2012

2011

2010

2009

GROSS AVERAGE BUDGET PER PRODUCT NUMBER OF PRODUCTS

€ 1.6 million

€ 1.7 million

€ 1.9 million

€ 1.4 million

€ 1.3 million

€ 1.2 million

€ 1.1 million

6 191

6,027

5,903

6,233

6,578

6,766

6,358

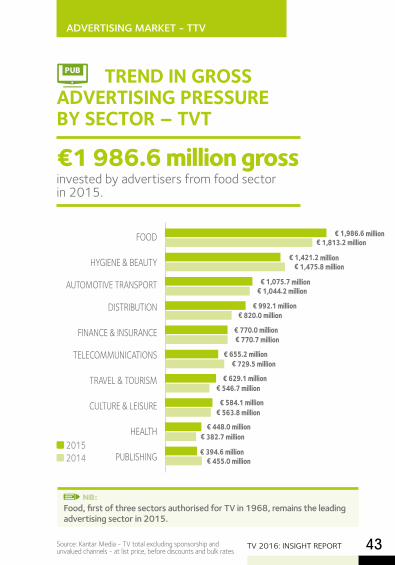

FOOD

HYGIENE & BEAUTY

AUTOMOTIVE TRANSPORT

DISTRIBUTION

FINANCE & INSURANCE

TELECOMMUNICATIONS

TRAVEL & TOURISM

CULTURE & LEISURE

HEALTH

PUBLISHING 2015 2014

€ 1,813.2 million€ 1,986.6 million

€ 1,475.8 million

€ 1,044.2 million

€ 820.0 million

€ 770.7 million

€ 729.5 million

€ 546.7 million

€ 563.8 million

€ 382.7 million

€ 455.0 million

€ 1,421.2 million

€ 1,075.7 million

€ 992.1 million

€ 770.0 million

€ 655.2 million

€ 629.1 million

€ 584.1 million

€ 448.0 million

€ 394.6 million

TREND IN GROSS ADVERTISING PRESSURE BY SECTOR – TVT

invested by advertisers from food sector in 2015.

€1 986.6 million gross

ADVERTISING MARKET - TTV

TV 2016: INSIGHT REPORT 43

Food, first of three sectors authorised for TV in 1968, remains the leading advertising sector in 2015.

NB:

Source: Kantar Media - TV total excluding sponsorship and unvalued channels - at list price, before discounts and bulk rates

PUB

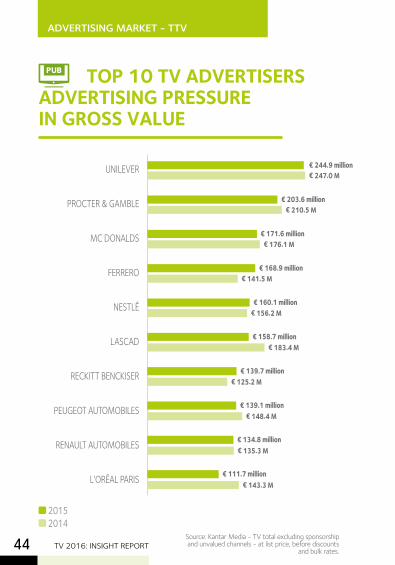

€ 247.0 M€ 244.9 million

€ 210.5 M

€ 176.1 M

€ 141.5 M

€ 156.2 M

€ 183.4 M

€ 125.2 M

€ 148.4 M

€ 135.3 M

€ 143.3 M

€ 203.6 million

€ 171.6 million

€ 168.9 million

€ 160.1 million

€ 158.7 million

€ 139.7 million

€ 139.1 million

€ 134.8 million

€ 111.7 million

Source: Kantar Media - TV total excluding sponsorship and unvalued channels - at list price, before discounts

and bulk rates.

TOP 10 TV ADVERTISERS ADVERTISING PRESSURE IN GROSS VALUE

UNILEVER

PROCTER & GAMBLE

MC DONALDS

FERRERO

NESTLÉ

LASCAD

RECKITT BENCKISER

PEUGEOT AUTOMOBILES

RENAULT AUTOMOBILES

L‘ORÉAL PARIS

2015 2014

ADVERTISING MARKET - TTV

TV 2016: INSIGHT REPORT44

PUB

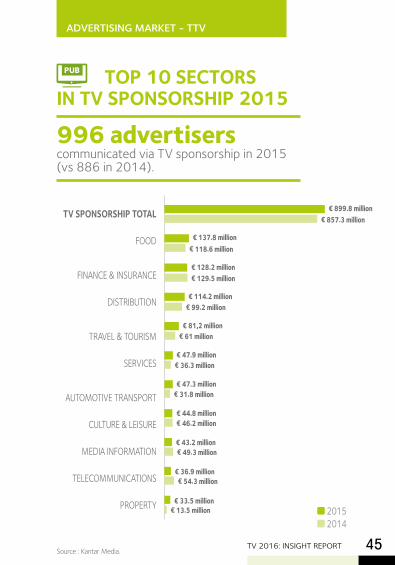

TV SPONSORSHIP TOTAL

FOOD

FINANCE & INSURANCE

DISTRIBUTION

TRAVEL & TOURISM

SERVICES

AUTOMOTIVE TRANSPORT

CULTURE & LEISURE

MEDIA INFORMATION

TELECOMMUNICATIONS

PROPERTY 2015 2014

€ 857.3 million€ 899.8 million

€ 118.6 million

€ 129.5 million

€ 99.2 million

€ 61 million

€ 36.3 million

€ 31.8 million

€ 46.2 million

€ 49.3 million

€ 54.3 million

€ 13.5 million

€ 137.8 million

€ 128.2 million

€ 114.2 million

€ 81,2 million

€ 47.9 million

€ 47.3 million

€ 44.8 million

€ 43.2 million

€ 36.9 million

€ 33.5 million

ADVERTISING MARKET - TTV

TV 2016: INSIGHT REPORT 45

communicated via TV sponsorship in 2015 (vs 886 in 2014).

996 advertisers

Source : Kantar Media.

TOP 10 SECTORS IN TV SPONSORSHIP 2015

PUB

Source: Kantar Media - TV total excluding sponsorship and unvalued channels - at list price, before discounts

and bulk rates.

BOOKING COM BRASSERIES KRONENBOURG

AMAZON MACHINE ZONE

AIR FRANCE PAGES JAUNES

LASTMINUTE MONABANQ.

YVES ROCHER ORCHESTRA KAZIBAO

SE FAIRE AIDER INTEL CORPORATION

LOKEO LAVAZZA

FAGOR BRANDT L’OLIVIER ASSURANCES

CALZEDONIA AIRBNB

HTC TÉLÉPHONIE DELTA DORÉ ÉLECTRONIQUE

TOP 20 OF THE NEW ANNOUNCERS TV ON 2015

€ 6.2 million

€ 6.0 million

€ 5.9 million

€ 5.8 million

€ 5.8 million

€ 5.7 million

€ 5.6 million

€ 5.4 million

€ 5.1 million

€ 13.4 million

€ 11,6 million

€ 11.2 million

€ 10.8 million

€ 9.7 million

€ 9.0 million

€ 8.1 million

€ 7.8 million

€ 7.8 million

€ 6.6 million

€ 20.4 million

ADVERTISING MARKET - TTV

TV 2016: INSIGHT REPORT46

on tv in 2015.788 new announcers

PUB

Source: Kantar Media - TV total excluding sponsorship and unvalued channels - at list price, before discounts and bulk rates.

VISTAPRINT KAYAK EURO

TRIVAGO TRIPADVISOR

COURTANET (LESFURETS.COM) ILIUS (MEETIC)

SUPERCELL OY KING COM

ING DIRECT MOVITEX SA DAXON (BALSAMIK)

NETFLIX CELLFISH MEDIA

BOOKING COM AFFINITAS (E.DARLING-ELITE.RENCONTRE)

ZALANDO EXPEDIA

ADMIRAL GROUP PLC (LELYNX.FR) BFORBANK

MONALBUMPHOTO FORTUNEO

2015 2014

€ 36.1 million€ 20.4 million € 20.4 million

€ 26.3 million€ 20.3 million

€ 19.2 million€ 19.9 million

€ 13 million€ 18.7 million

€ 9.4 million€ 18.6 million

€ 4.1 million€ 16.4 million

€ 12.1 million€ 15.8 million

€ 22.4 million€ 15.5 million

€ 36.7 million€ 32.3 million

€ 36.7 million € 31.5 million

€ 15.9 million€ 30.9 million

€ 20.8 million€ 29.7 million

€ 31.9 million€ 29.7 million

€ 16.7 million€ 28.9 million

€ 40.3 million€ 26.8 million

€ 24.4 million€ 23.7 million

€ 27.2 million€ 22.9 million

€ 22.2 million€ 22.9 million

€ 33.7 million€ 34.9 million

ADVERTISING MARKET - TTV

TV 2016: INSIGHT REPORT 47

PURE PLAYER ADVERTISERS ON TV

is the amount invested in television by 20 pure player advertisers in 2015.

€480.2 million gross

TV EFFECTIVENESS

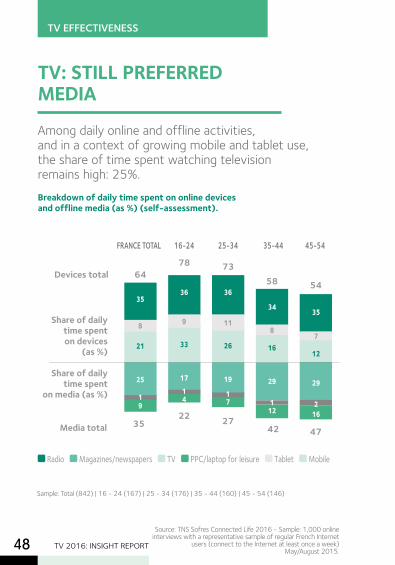

TV 2016: INSIGHT REPORT48

Breakdown of daily time spent on online devices and offline media (as %) (self-assessment).

TV: STILL PREFERRED MEDIA

Among daily online and offline activities, and in a context of growing mobile and tablet use, the share of time spent watching television remains high: 25%.

Source: TNS Sofres Connected Life 2016 - Sample: 1,000 online interviews with a representative sample of regular French Internet

users (connect to the Internet at least once a week) May/August 2015.

Sample: Total (842) | 16 - 24 (167) | 25 - 34 (176) | 35 - 44 (160) | 45 - 54 (146)

Radio Magazines/newspapers TV PPC/laptop for leisure Tablet Mobile

FRANCE TOTAL 16-24 25-34 35-44 45-54

Share of daily time spent on devices

(as %)

Share of daily time spent

on media (as %)

Media total 35 22

27

42 47

35

8

21

25

19

36

9

33

1714

36

11

26

19

17

35

7

12

29

216

34

8

16

29

112

Devices total 64 78

73

58

54

TV EFFECTIVENESS

TV 2016: INSIGHT REPORT 49Source: TNS Sofres Connected Life 2016 - Sample: 1,000 online interviews with a representative sample of regular French Internet users (connect to the Internet at least once a week) – May/August 2015.

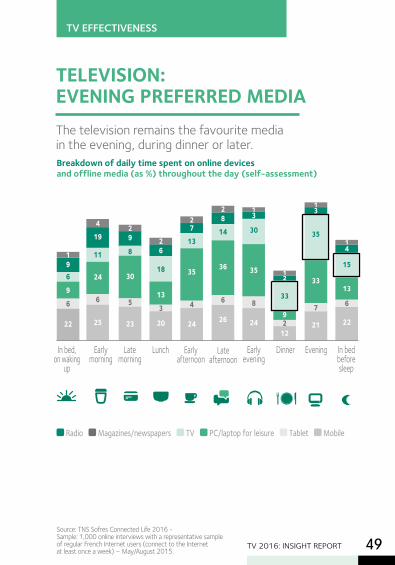

TELEVISION: EVENING PREFERRED MEDIA The television remains the favourite media in the evening, during dinner or later. Breakdown of daily time spent on online devices and offline media (as %) throughout the day (self-assessment)

Radio Magazines/newspapers TV PC/laptop for leisure Tablet Mobile

In bed, on waking

up

Early morning

Late morning

Lunch Early afternoon

Late afternoon

Early evening

Dinner Evening In bed before sleep

419

11

24

6

25

196

9

6

22

29

8

30

5

23

13

30

35

8

24

26

18

13

3

20

27

13

35

4

24

28

14

36

6

26

12

33

92

12

13

35

33

7

21

14

15

13

6

22

TV 2016: INSIGHT REPORT50Source: DENTSU AEGIS NORTH / Data2Decisions – May 2015. Sample: 914 individuals representative of the French population,

15-65 demographic, in terms of socio-demographic criteria.

TV EFFECTIVENESS

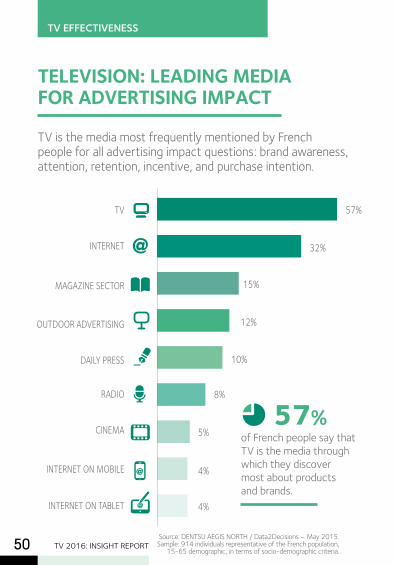

TELEVISION: LEADING MEDIA FOR ADVERTISING IMPACT

TV is the media most frequently mentioned by French people for all advertising impact questions: brand awareness, attention, retention, incentive, and purchase intention.

TV

INTERNET

MAGAZINE SECTOR

OUTDOOR ADVERTISING

DAILY PRESS

RADIO

CINEMA

INTERNET ON MOBILE

INTERNET ON TABLET

57%

32%

15%

12%

10%

8%

5%

4%

4%

of French people say that TV is the media through which they discover most about products and brands.

57%

TV 2016: INSIGHT REPORT 51

TV

OUTDOOR ADVERTISING

INTERNET

MAGAZINE SECTOR

CINEMA

RADIO

DAILY PRESS

INTERNET ON MOBILE

INTERNET ON TABLET

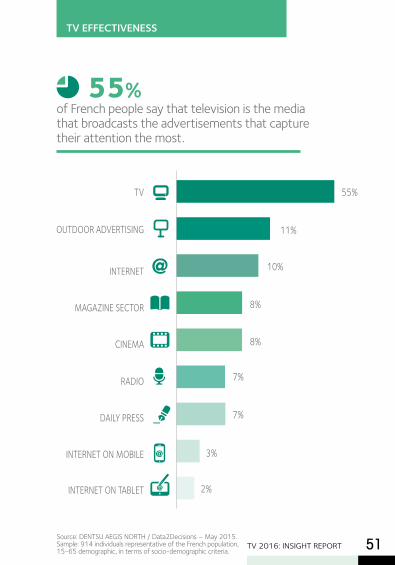

55%

11%

10%

8%

8%

7%

7%

3%

2%

of French people say that television is the media that broadcasts the advertisements that capture their attention the most.

55%

Source: DENTSU AEGIS NORTH / Data2Decisions – May 2015. Sample: 914 individuals representative of the French population, 15-65 demographic, in terms of socio-demographic criteria.

TV EFFECTIVENESS

TV EFFECTIVENESS

TV 2016: INSIGHT REPORT52

TV

MAGAZINE SECTOR

INTERNET

ADVERTISING DISPLAY

RADIO

CINEMA

DAILY PRESS

INTERNET ON MOBILE

INTERNET ON TABLET

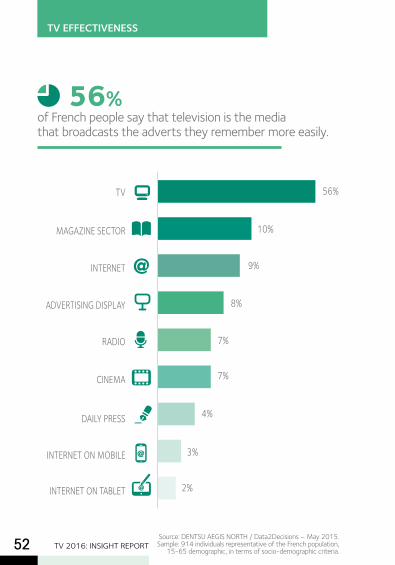

56%

10%

9%

8%

7%

7%

4%

3%

2%

of French people say that television is the media that broadcasts the adverts they remember more easily.

56%

Source: DENTSU AEGIS NORTH / Data2Decisions – May 2015. Sample: 914 individuals representative of the French population,

15-65 demographic, in terms of socio-demographic criteria.

TV EFFECTIVENESS

TV 2016: INSIGHT REPORT 53

TV

INTERNET

MAGAZINE SECTOR

ADVERTISING DISPLAY

RADIO

CINEMA

DAILY PRESS

INTERNET ON MOBILE

INTERNET ON TABLET

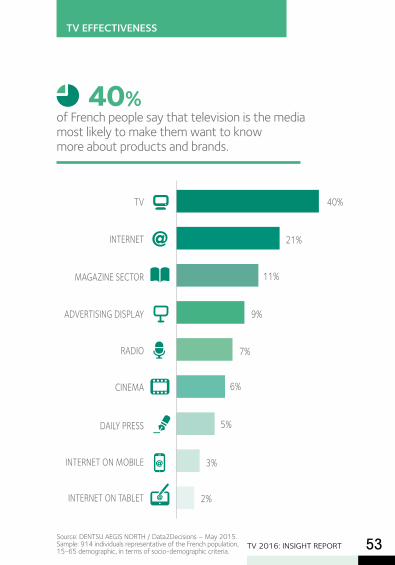

40%

21%

11%

9%

7%

6%

5%

3%

2%

of French people say that television is the media most likely to make them want to know more about products and brands.

40%

Source: DENTSU AEGIS NORTH / Data2Decisions – May 2015. Sample: 914 individuals representative of the French population, 15-65 demographic, in terms of socio-demographic criteria.

TV EFFECTIVENESS

TV 2016: INSIGHT REPORT54

TV

INTERNET

MAGAZINE SECTOR

ADVERTISING DISPLAY

DAILY PRESS

RADIO

CINEMA

INTERNET ON MOBILE

INTERNET ON TABLET

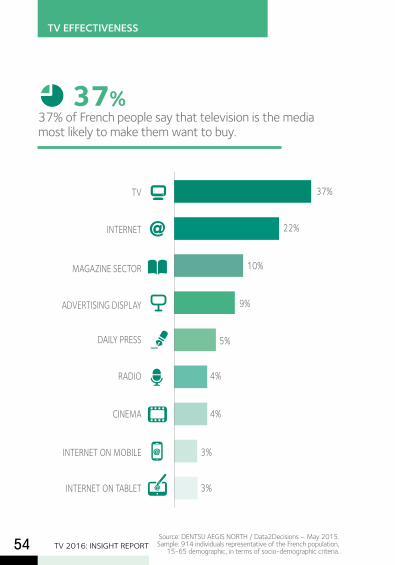

37%

22%

10%

9%

5%

4%

4%

3%

3%

37% of French people say that television is the media most likely to make them want to buy.

37%

Source: DENTSU AEGIS NORTH / Data2Decisions – May 2015. Sample: 914 individuals representative of the French population,

15-65 demographic, in terms of socio-demographic criteria.

TV EFFECTIVENESS

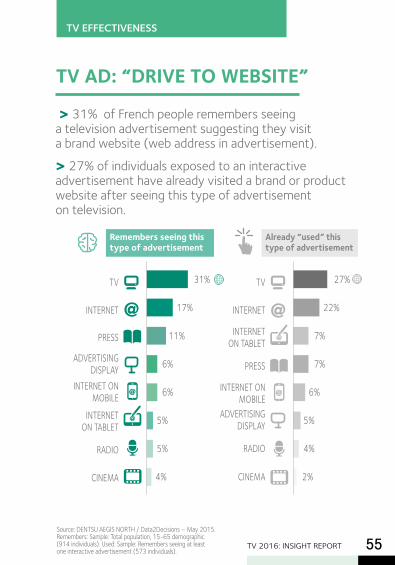

TV 2016: INSIGHT REPORT 55Source: DENTSU AEGIS NORTH / Data2Decisions – May 2015. Remembers: Sample: Total population, 15-65 demographic (914 individuals). Used: Sample: Remembers seeing at least one interactive advertisement (573 individuals).

TV AD: “DRIVE TO WEBSITE”

> 31% of French people remembers seeing a television advertisement suggesting they visit a brand website (web address in advertisement).

> 27% of individuals exposed to an interactive advertisement have already visited a brand or product website after seeing this type of advertisement on television.

TV

INTERNET

PRESS

ADVERTISING DISPLAY

INTERNET ON MOBILE

INTERNET ON TABLET

RADIO

CINEMA

31%

17%

11%

6%

6%

5%

5%

4%

Remembers seeing this type of advertisement

TV

INTERNET

INTERNET ON TABLET

PRESS

INTERNET ON MOBILE

ADVERTISING DISPLAY

RADIO

CINEMA

27%

22%

7%

7%

6%

5%

4%

2%

Already “used” this type of advertisement

TV EFFECTIVENESS

TV 2016: INSIGHT REPORT56Source: DENTSU AEGIS NORTH / Data2Decisions – May 2015.

Remembers: Sample: Total population, 15-65 demographic (914 individuals). Used: Sample: Remembers seeing at least

one interactive advertisement (573 individuals).

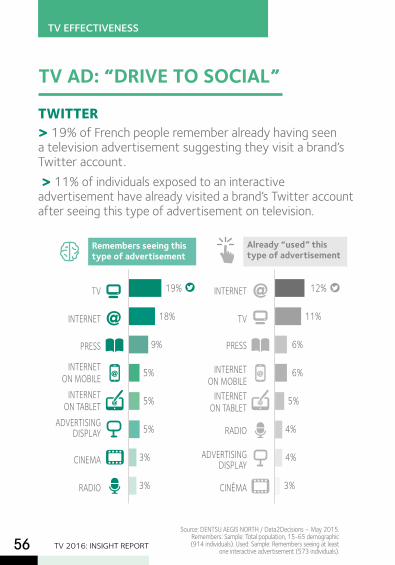

TV AD: “DRIVE TO SOCIAL”

TWITTER> 19% of French people remember already having seen a television advertisement suggesting they visit a brand’s Twitter account. > 11% of individuals exposed to an interactive advertisement have already visited a brand’s Twitter account after seeing this type of advertisement on television.

TV

INTERNET

PRESS

INTERNET ON MOBILE

INTERNET ON TABLET

ADVERTISING DISPLAY

CINEMA

RADIO

19%

18%

9%

5%

5%

5%

3%

3%

Remembers seeing this type of advertisement

INTERNET

TV

PRESS

INTERNET ON MOBILE

INTERNET ON TABLET

RADIO

ADVERTISING DISPLAY

CINÉMA

12%

11%

6%

6%

5%

4%

4%

3%

Already “used” this type of advertisement

TV EFFECTIVENESS

TV 2016: INSIGHT REPORT 57Source: DENTSU AEGIS NORTH / Data2Decisions – May 2015. Remembers: Sample: Total population, 15-65 demographic (914 individuals). Used: Sample: Remembers seeing at least one interactive advertisement (573 individuals).

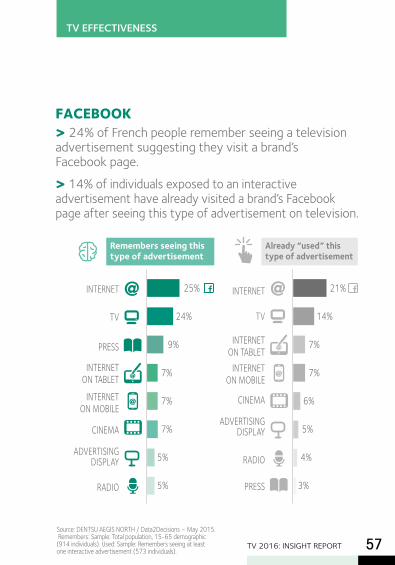

FACEBOOK> 24% of French people remember seeing a television advertisement suggesting they visit a brand’s Facebook page.> 14% of individuals exposed to an interactive advertisement have already visited a brand’s Facebook page after seeing this type of advertisement on television.

INTERNET

TV

PRESS

INTERNET ON TABLET

INTERNET ON MOBILE

CINEMA

ADVERTISING DISPLAY

RADIO

25%

24%

9%

7%

7%

7%

5%

5%

Remembers seeing this type of advertisement

INTERNET

TV

INTERNET ON TABLET

INTERNET ON MOBILE

CINEMA

ADVERTISING DISPLAY

RADIO

PRESS

21%

14%

7%

7%

6%

5%

4%

3%

Already “used” this type of advertisement

TV EFFECTIVENESS

TV 2016: INSIGHT REPORT58Source: DENTSU AEGIS NORTH / Data2Decisions – May 2015.

Remembers: Sample: Total population, 15-65 demographic (914 individuals). Used: Sample: Remembers seeing at least

one interactive advertisement (573 individuals).

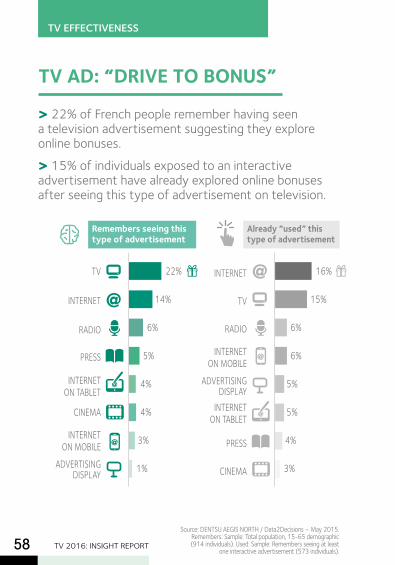

TV AD: “DRIVE TO BONUS”

> 22% of French people remember having seen a television advertisement suggesting they explore online bonuses.> 15% of individuals exposed to an interactive advertisement have already explored online bonuses after seeing this type of advertisement on television.

TV

INTERNET

RADIO

PRESS

INTERNET ON TABLET

CINEMA

INTERNET ON MOBILE

ADVERTISING DISPLAY

22%

14%

6%

5%

4%

4%

3%

1%

Remembers seeing this type of advertisement

INTERNET

TV

RADIO

INTERNET ON MOBILE

ADVERTISING DISPLAY

INTERNET ON TABLET

PRESS

CINEMA

16%

15%

6%

6%

5%

5%

4%

3%

Already “used” this type of advertisement

TV 2016: INSIGHT REPORT 59Source: DENTSU AEGIS NORTH / Data2Decisions – May 2015. Remembers: Sample: Total population, 15-65 demographic (914 individuals). Used: Sample: Remembers seeing at least one interactive advertisement (573 individuals).

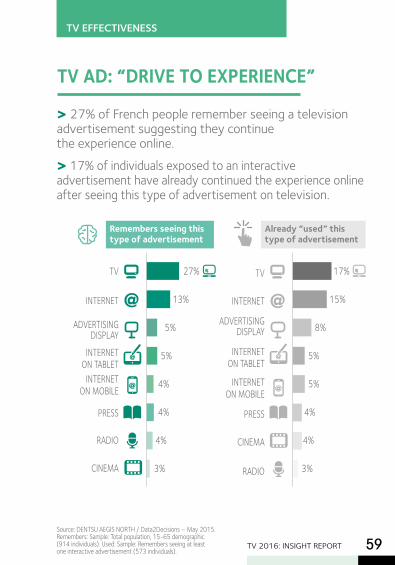

TV AD: “DRIVE TO EXPERIENCE”

> 27% of French people remember seeing a television advertisement suggesting they continue the experience online.> 17% of individuals exposed to an interactive advertisement have already continued the experience online after seeing this type of advertisement on television.

TV

INTERNET

ADVERTISING DISPLAY

INTERNET ON TABLET

INTERNET ON MOBILE

PRESS

RADIO

CINEMA

27%

13%

5%

5%

4%

4%

4%

3%

Remembers seeing this type of advertisement

TV

INTERNET

ADVERTISING DISPLAY

INTERNET ON TABLET

INTERNET ON MOBILE

PRESS

CINEMA

RADIO

17%

15%

8%

5%

5%

4%

4%

3%

Already “used” this type of advertisement

TV EFFECTIVENESS

TV 2016: INSIGHT REPORT60

Source: DENTSU AEGIS NORTH / Data2Decisions – May 2015. Remembers: Sample: Total population, 15-65 demographic (914 individuals). Used: Sample: Remembers seeing at least

one interactive advertisement (573 individuals).

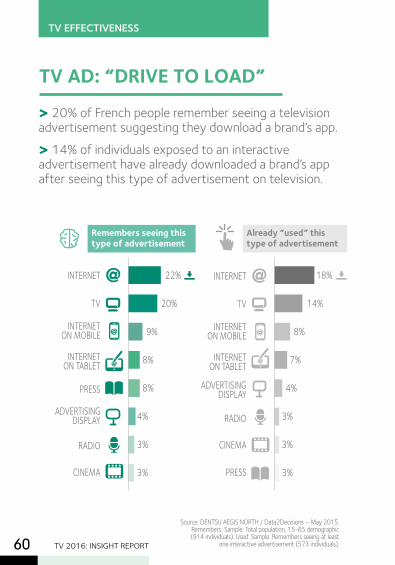

TV AD: “DRIVE TO LOAD”

> 20% of French people remember seeing a television advertisement suggesting they download a brand’s app.> 14% of individuals exposed to an interactive advertisement have already downloaded a brand’s app after seeing this type of advertisement on television.

INTERNET

TV

INTERNET ON MOBILE

INTERNET ON TABLET

PRESS

ADVERTISING DISPLAY

RADIO

CINEMA

22%

20%

9%

8%

8%

4%

3%

3%

Remembers seeing this type of advertisement

INTERNET

TV

INTERNET ON MOBILE

INTERNET ON TABLET

ADVERTISING DISPLAY

RADIO

CINEMA

PRESS

18%

14%

8%

7%

4%

3%

3%

3%

Already “used” this type of advertisement

TV EFFECTIVENESS

TV 2016: INSIGHT REPORT 61Source: DENTSU AEGIS NORTH / Data2Decisions – May 2015. Remembers: Sample: Total population, 15-65 demographic (914 individuals). Used: Sample: Remembers seeing at least one interactive advertisement (573 individuals).

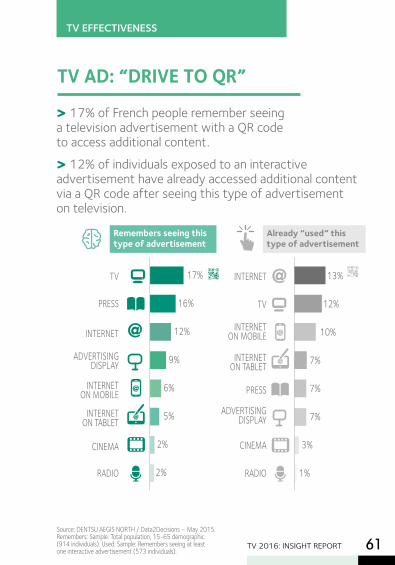

TV AD: “DRIVE TO QR” > 17% of French people remember seeing a television advertisement with a QR code to access additional content.> 12% of individuals exposed to an interactive advertisement have already accessed additional content via a QR code after seeing this type of advertisement on television.

TV

PRESS

INTERNET

ADVERTISING DISPLAY

INTERNET ON MOBILE

INTERNET ON TABLET

CINEMA

RADIO

17%

16%

12%

9%

6%

5%

2%

2%

Remembers seeing this type of advertisement

INTERNET

TV

INTERNET ON MOBILE

INTERNET ON TABLET

PRESS

ADVERTISING DISPLAY

CINEMA

RADIO

13%

12%

10%

7%

7%

7%

3%

1%

Already “used” this type of advertisement

TV EFFECTIVENESS

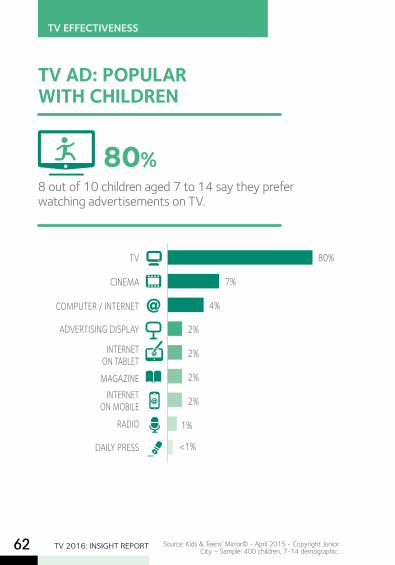

Source: Kids & Teens’ Mirror© - April 2015 - Copyright Junior City – Sample: 400 children, 7-14 demographic.

TV 2016: INSIGHT REPORT62

TV AD: POPULAR WITH CHILDREN

8 out of 10 children aged 7 to 14 say they prefer watching advertisements on TV.

80%

TV

CINEMA

COMPUTER / INTERNET

ADVERTISING DISPLAY

INTERNET ON TABLETMAGAZINE

INTERNET ON MOBILE

RADIO

DAILY PRESS

80%

7%

4%

2%

2%

2%

2%

1%

<1%

TV EFFECTIVENESS

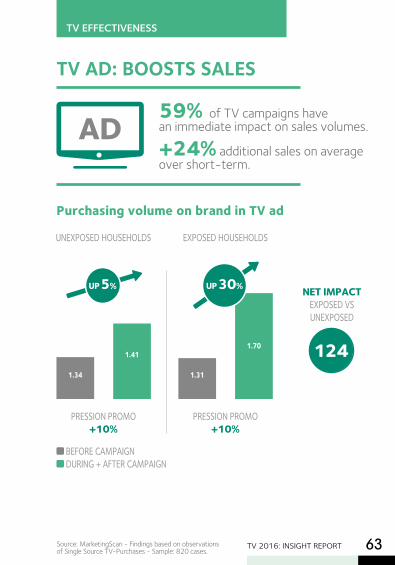

TV 2016: INSIGHT REPORT 63Source: MarketingScan - Findings based on observations of Single Source TV-Purchases - Sample: 820 cases.

BEFORE CAMPAIGN DURING + AFTER CAMPAIGN

TV AD: BOOSTS SALES

Purchasing volume on brand in TV ad

59% of TV campaigns have an immediate impact on sales volumes.

+24% additional sales on average over short-term.

PRESSION PROMO+10%

PRESSION PROMO+10%

UNEXPOSED HOUSEHOLDS EXPOSED HOUSEHOLDS

1.34 1.31

1.411.70

UP 5% UP 30% NET IMPACT EXPOSED VS UNEXPOSED

124

AD

TV EFFECTIVENESS

Source: MarketingScan - Findings based on observations of Single Source TV-Purchases - Sample: 820 cases.

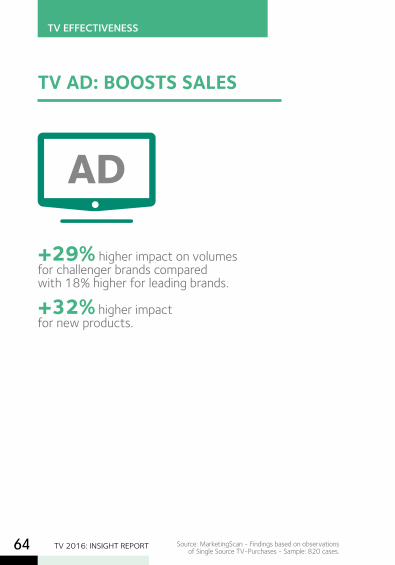

TV 2016: INSIGHT REPORT64

TV AD: BOOSTS SALES

AD

+29% higher impact on volumes for challenger brands compared with 18% higher for leading brands. +32% higher impact for new products.

TV EFFECTIVENESS

TV 2016: INSIGHT REPORT 65

CASES AVERAGE

at the end of 2015

at the end of 2012

% OF EFFECTIVE CAMPAIGNS

INCREASE IN PROMOTIONAL PRESSURE DURING CAMPAIGN

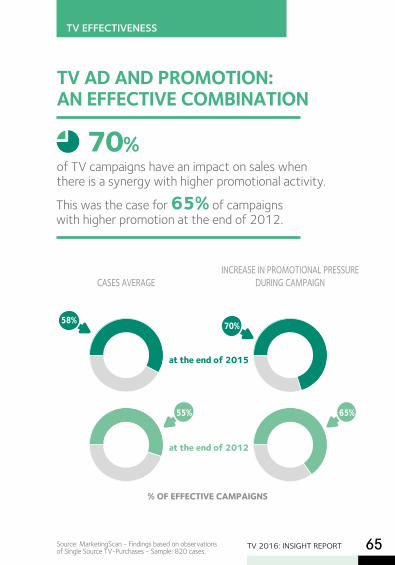

TV AD AND PROMOTION: AN EFFECTIVE COMBINATION

of TV campaigns have an impact on sales when there is a synergy with higher promotional activity.

This was the case for 65% of campaigns with higher promotion at the end of 2012.

70%

58%

55% 65%

70%

TV EFFECTIVENESS

Source: MarketingScan - Findings based on observations of Single Source TV-Purchases - Sample: 820 cases.

TV EFFECTIVENESS

TV 2016: INSIGHT REPORT66

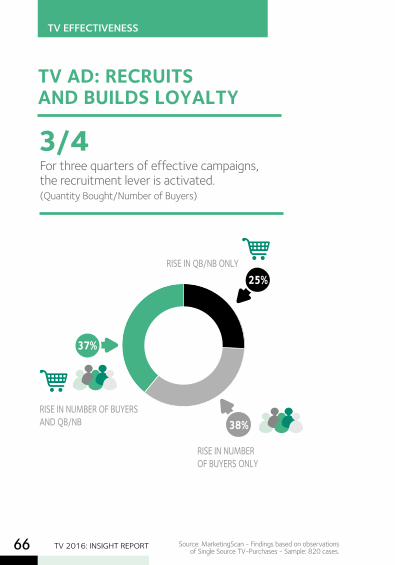

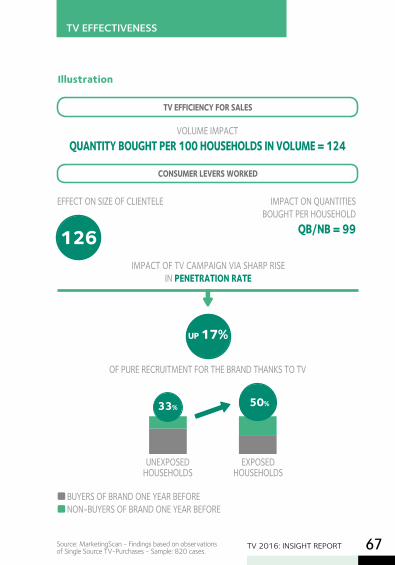

TV AD: RECRUITS AND BUILDS LOYALTY

38%

37%

25%

RISE IN NUMBER OF BUYERS ONLY

RISE IN QB/NB ONLY

RISE IN NUMBER OF BUYERS AND QB/NB

For three quarters of effective campaigns, the recruitment lever is activated. (Quantity Bought/Number of Buyers)

3/4

Source: MarketingScan - Findings based on observations of Single Source TV-Purchases - Sample: 820 cases.

TV EFFECTIVENESS

TV 2016: INSIGHT REPORT 67

BUYERS OF BRAND ONE YEAR BEFORE NON-BUYERS OF BRAND ONE YEAR BEFORE

TV EFFICIENCY FOR SALES

CONSUMER LEVERS WORKED

EFFECT ON SIZE OF CLIENTELE

OF PURE RECRUITMENT FOR THE BRAND THANKS TO TV

VOLUME IMPACT QUANTITY BOUGHT PER 100 HOUSEHOLDS IN VOLUME = 124

IMPACT OF TV CAMPAIGN VIA SHARP RISE IN PENETRATION RATE

Illustration

UP 17%

126

UNEXPOSED HOUSEHOLDS

EXPOSED HOUSEHOLDS

33% 50%

IMPACT ON QUANTITIES BOUGHT PER HOUSEHOLD

QB/NB = 99

Source: MarketingScan - Findings based on observations of Single Source TV-Purchases - Sample: 820 cases.

TV EFFECTIVENESS

TV 2016: INSIGHT REPORT68

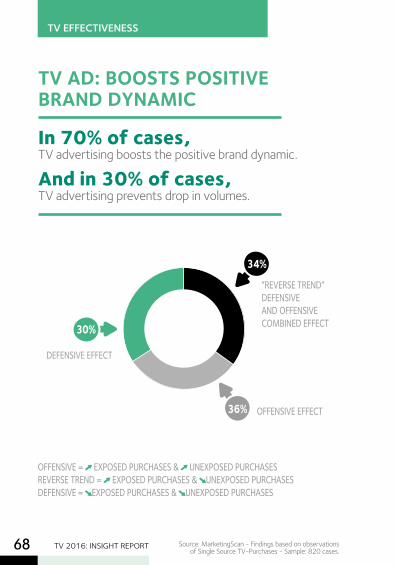

OFFENSIVE EFFECT

“REVERSE TREND” DEFENSIVE AND OFFENSIVE COMBINED EFFECT

DEFENSIVE EFFECT

OFFENSIVE = EXPOSED PURCHASES & UNEXPOSED PURCHASES REVERSE TREND = EXPOSED PURCHASES & UNEXPOSED PURCHASES DEFENSIVE = EXPOSED PURCHASES & UNEXPOSED PURCHASES

TV AD: BOOSTS POSITIVE BRAND DYNAMIC

In 70% of cases,TV advertising boosts the positive brand dynamic.

And in 30% of cases, TV advertising prevents drop in volumes.

36%

30%

34%

Source: MarketingScan - Findings based on observations of Single Source TV-Purchases - Sample: 820 cases.

TV 2016: INSIGHT REPORT 69

TV EFFECTIVENESS

Source: MarketingScan - Findings based on observations of Single Source TV-Purchases - Sample: 820 cases.

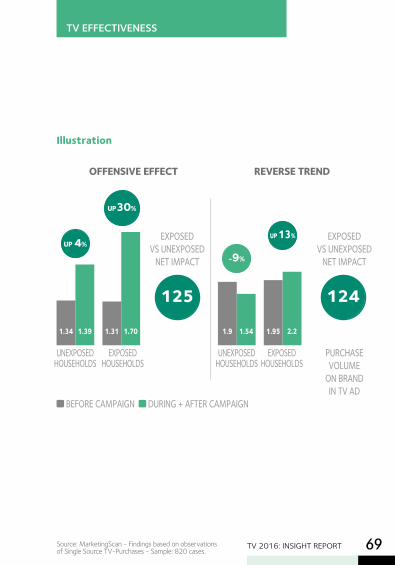

REVERSE TREND

Illustration

UNEXPOSED HOUSEHOLDS

UNEXPOSED HOUSEHOLDS

EXPOSED HOUSEHOLDS

EXPOSED HOUSEHOLDS

EXPOSED VS UNEXPOSED

NET IMPACT

EXPOSED VS UNEXPOSED

NET IMPACT

PURCHASE VOLUME

ON BRAND IN TV AD

1.34 1.9 1.541.39

UP 4%

-9%

BEFORE CAMPAIGN DURING + AFTER CAMPAIGN

1.31 1.95 2.21.70

UP30%

OFFENSIVE EFFECT

UP 13%

125 124

Source: MarketingScan - Findings based on observations of Single Source TV-Purchases - Sample: 820 cases.

TV 2016: INSIGHT REPORT70

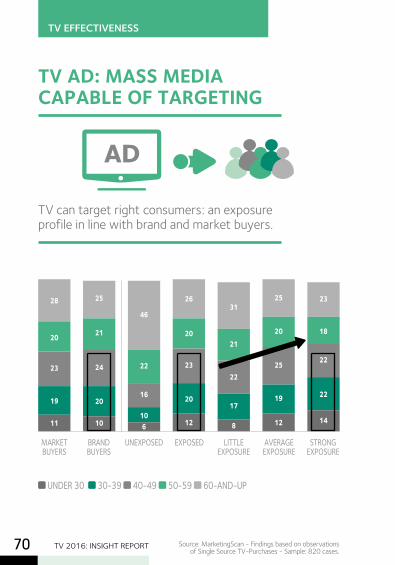

TV AD: MASS MEDIA CAPABLE OF TARGETING

TV can target right consumers: an exposure profile in line with brand and market buyers.

UNDER 30 30-39 40-49 50-59 60-AND-UP

MARKET BUYERS

BRAND BUYERS

UNEXPOSED EXPOSED LITTLE EXPOSURE

AVERAGE EXPOSURE

STRONG EXPOSURE

11

19

23

20

28

10

20

24

21

25

610

16

22

46

8

17

22

21

31

12

20

23

20

26

12

19

25

20

25

14

22

22

18

23

AD

TV EFFECTIVENESS

Source: MarketingScan - Findings based on observations of Single Source TV-Purchases - Sample: 820 cases.

TV 2016: INSIGHT REPORT 71

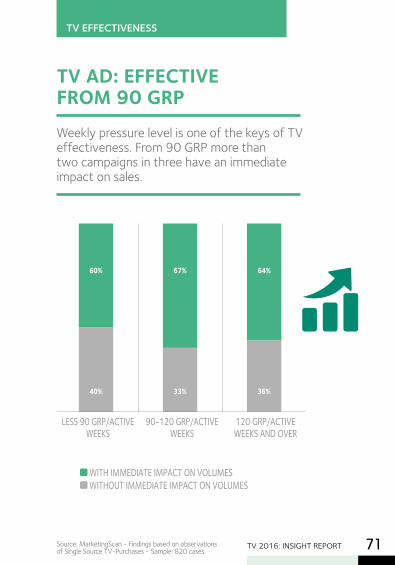

TV AD: EFFECTIVE FROM 90 GRPWeekly pressure level is one of the keys of TV effectiveness. From 90 GRP more than two campaigns in three have an immediate impact on sales.

WITH IMMEDIATE IMPACT ON VOLUMES WITHOUT IMMEDIATE IMPACT ON VOLUMES

LESS 90 GRP/ACTIVE WEEKS

90-120 GRP/ACTIVE WEEKS

120 GRP/ACTIVE WEEKS AND OVER

67%

33%

64%

36%

60%

40%

TV EFFECTIVENESS

Promotes TV advertising, including by supporting its members in general interest campaigns,

Studies TV advertising and its ongoing effectiveness for advertisers, media buying consulting firms and communications agencies,

Monitors developments in TV advertising, particularly global,

Represents its members and establish a dialogue with representative bodies for advertising players.

4

1, quai du Point du JourF-92656 Boulogne CedexFranceTél.: + 33 (0)1 41 41 43 22 Fax: + 33 (0)1 41 41 43 30www.snptv.orgcontact: [email protected]

core missions

Recommended

![La planète inconnue [24] - Free-scores.com · 24 - La planète inconnue 01-1-24 ... NO 24 - La planète inconnue p 02 . c NO 24 - La planète inconnue p 02 . c NO 24 - La planète](https://img.pdfslide.us/doc/110x75/5b158b777f8b9afb0a8ce119/la-planete-inconnue-24-free-24-la-planete-inconnue-01-1-24-no-24.jpg)