2011Bank Hapoalim

Annual Report 2011

The Bank Hapoalim Group Major Subsidiaries & Affiliates

Commercial Banks Bank Hapoalim B.M.Bank Hapoalim (Switzerland) Ltd.Bank Hapoalim (Luxembourg) S.A.Hapoalim (Latin America) S.A.Bank Hapoalim (Cayman) Ltd.Bank Pozitif Kredi Ve Kalkinma Bankasi a.s.JSC Bank Pozitiv Kazakhstan(1)

Investment HousePoalim Capital Markets - Investment House Ltd.

Trust CompaniesPoalim Trust Services Ltd.

Underwriting CompaniesPoalim I.B.I. Managing and Underwriting Ltd.

Portfolio ManagementPeilim – Portfolio Management Company Ltd.Hapoalim Securities USA, Inc.

Asset Management Poalim Sahar Ltd.PAM - Poalim Asset Management (UK) Ltd.Poalim Asset Management (Ireland) Ltd.

Financial CompaniesIsracard Ltd.Poalim Express Ltd.

(1) 100% owned by Bank Pozitif

Consolidated Financial Highlights

2011 2010 2011 2010

NIS Millions USD Millions*

Total Assets 356,688 321,089 93,349 84,033

Net Profit 2,746 2,201 719 576

Credit to the Public 246,495 225,288 64,511 58,960

Deposits from the Public 256,417 233,965 67,107 61,231

Shareholders' Equity 23,845 22,561 6,241 5,904

* US dollar figures have been converted at the representative exchange rate prevailing on December 31, 2011, NIS 3.821 = USD 1.00

Bank Hapoalim B.M. and its Consolidated Subsidiaries3

Group Profile Israel’s leading financial institution

Since its founding in 1921, Bank Hapoalim has played a pivotal role in the rapid growth of Israel’s economy. Today Hapoalim continues to be the leading financial institution in Israel. The bank maintains a global presence, operating in 20 countries throughout the world.

Bank Hapoalim is a universal bank in structure and operations. The bank boasts a very strong retail banking business with the largest distribution network in the country. Through a wide range of banking offerings it caters to consumers, SMEs and corporations across Israel.

Bank Hapoalim is the lender of choice to Israel’s largest corporations and is active in financing industrial and commercial enterprises, as well as major infrastructure projects.

The bank runs a thriving foreign trade, foreign exchange, and brokerage & custody business and maintains a global private banking arm serving private clients across the globe.

In Israel, Bank Hapoalim operates over 280 full-service branches, focusing on households, private (affluent) banking & small businesses.The bank offers a deep shelf of banking and payments products, capital market and foreign trade facilities and a full gamut of financial planning advisory services including pension and retirement planning.

Bank Hapoalim is currently strengthening its domestic presence through “express branches” for retail banking in high traffic areas, and “boutique” branches in affluent neighborhoods. Through its celebrated direct banking platform and state-of-the-art 24/7 call centers; the Bank promotes convenient, interpersonal interaction, providing customers the ability to bank through whichever technological channel they choose.

Commercial and corporate clients are professionally served through eight regional business centers, business branches and specialized industry desks for major corporate clients. The Bank, which has long been the favored financial address for Israel’s leading corporations, is now strengthening its middle market activities. A network of 22 business branches will make services more convenient and diversified, as this sector plays an expanding role in the domestic economy.

Internationally, Bank Hapoalim operates through a network of subsidiaries, branches and representative offices in the United States, Europe, South America and Asia. The Bank’s thriving Global Private Banking services, led by Bank Hapoalim (Switzerland), serves high net-worth clients from around the world, with offices in Zurich, Geneva, Luxembourg, Tel Aviv, Miami, Singapore and Hong Kong. In this competitive market, clients are attracted to the Bank’s very extensive wealth management expertise, stellar reputation and global spread. Global Private Banking activities are supported by PAM, a fully-owned subsidiary in London, which provides investment products through the world’s leading investment firms.

Building on its experience in structuring complex trade packages, the Bank is promoting its overseas corporate services, primarily targeting Israeli companies establishing or strengthening their presence in established and growth markets.

The Bank Hapoalim Group includes Isracard Ltd, Israel's leading credit card company, as well as financial companies involved in investment banking, trust services and portfolio management.

The Bank plays an active role in the community, contributing generously to educational, social and cultural projects, and encouraging personal volunteering among its employees.

Bank Hapoalim is one of the most actively traded stocks on the Tel Aviv Stock Exchange. In addition, a Level-1 ADR is traded "over-the -counter" in New York, under ticker BKHYY. The Bank is rated by Moody's, S&P and Fitch.

Bank Hapoalim B.M. and its Consolidated Subsidiaries4

Letter from the Chairman of the Board and the CEO

Dear Stakeholders,

On behalf of the Board of Directors and the Board of Management we are pleased to present the annual financial statements of the Bank Hapoalim Group for 2011. During this period, Bank Hapoalim continued to successfully implement its three-year strategic plan. We achieved impressive business results and a double-digit return on shareholders' equity, in line with our stated goals.

Strategic Plan Implementation - Second YearLast year we stated that the Bank’s strategic plan would further our position as Israel’s leading bank. In 2011, the Bank successfully completed the second year of its three-year strategic plan. We are pleased to report that during this period we solidified our leading market position across most business segments and in the financial markets in Israel. Furthermore, we are proud to report that the Bank’s leadership was honored by the prestigious magazine 'The Banker' in selecting Bank Hapoalim as the "Bank of the Year" in Israel for 2011. Currently we are formulating the strategic plan for the following three years.

The year 2011 was a period of renewal for the Bank, as management concentrated its efforts on strengthening Bank Hapoalim’s growth engines. We grew our revenues across business divisions, adapting our business to the increasingly competitive environment. Ambitious, results-driven implementation of the strategic plan yielded an annual 12% return on equity, demonstrating our capacity to generate year-over-year double-digit returns for investors. Our results reflect the Bank’s strong commitment to generate stakeholder value in line with the Bank's risk appetite and the macro-economic conditions in Israel and in global markets.

The Global Economy: The long tail of the sovereign debt crisisThroughout the year 2011, the sovereign debt crisis was looming over the global economy. Buried in debt, fearing contagion from badly over-leveraged countries such as Greece, the European economy slipped into recession. European banks, in particular, came under severe pressure having purchased, in the last three years, hundreds of billions of sovereign bonds. Across the Atlantic, the United States' economy began to show signs of recovery. A recapitalized banking system was better equipped to support the American economy even as corporate America concentrated on productivity gains, cost cutting and improving balance sheets. Renewed consumer confidence replaced the general gloom, ushering in consecutive quarters of positive market returns. Emerging markets contributed 3.8% to global growth in 2011, assisted by the very expansive fiscal policy of Western nations. However, the prospects of a hard landing in the Chinese economy added to global market uncertainty, and led to significant fluctuations in capital markets.

Israel’s Economic EnvironmentDuring the first half of 2011, Israel’s economy continued to exhibit great strength. The business sector enjoyed positive momentum, as GDP growth reached 4.7%, significantly higher than expected. In the second half of 2011, the Israeli economy began to slow down in response to the European crisis and growing uncertainties about the direction of the global economy. Israeli exports declined while the over-heated real-estate market quickly cooled off. Bank of Israel responded with measured cuts in interest rates.The slowdown in economic activity, and increased pressure on companies' earnings, had an impact on the Tel Aviv Stock Exchange as well, with lower turnover on securities and an increase in yields on corporate bonds of major Israeli companies. The latter made it more difficult for these companies to refinance their outstanding debt in the capital markets. Among the outcomes were various debt arrangements in the capital market, a downturn in bond issuances and an increase in the demand for bank credit.The year 2011 was a reminder for the Israeli economy of the critical importance of strong corporate balance sheets. During the year markets saw the beginning of a gradual de-leveraging process, especially among larger companies. This is a long and often painful process, but, in the long-term, should be a healthy development for the companies themselves and the Israeli economy as a whole.

Bank Hapoalim B.M. and its Consolidated Subsidiaries5

Growth Rooted in StabilityThe Bank’s performance in 2011 expressed the Board of Directors and the Board of Management’s commitment to grow the Bank through activities in line with the Bank’s risk appetite, while increasing and strengthening its capital base. This was achieved despite the implementation of accounting directives required by the Bank of Israel, which led to the reduction of over NIS 1 billion from the Bank’s capital. The positive results were attained by focusing on sustainable profitability in core banking activities. Thus, the Bank was able to increase its total capital adequacy ratio to 14.1%.The implementation of the strategic plan during 2009-2010 gave the Bank the required stability and, equally paramount, the corporate culture of commitment and motivation. In 2011, our divisions efficiently met their business goals. At the end of the year, Bank Hapoalim recorded profits of NIS 2.7 billion, an increase of about 25% from 2010.

2011 Activities and AchievementsDuring the past year, the Retail Banking Division further developed Bank Hapoalim’s strong distribution network. New branches were opened on the basis of geographic planning, based on the Bank’s strategy of strengthening its presence and relevance among segments with high potential.Protecting its customer base and pursuing new customers, the Retail Division brought to market a rich product portfolio, delivered through advanced multi-channel platforms. Employing innovative technology, developed by Hapoalim's IT Division, the bank reaffirmed its technological leadership. A series of new applications were introduced to provide solutions for all types of media and platforms used by today’s customers.The Retail Division played a key role in implementing the Bank’s strategy of improving its funding resources. In 2011, the Retail Division was able to grow deposit balances using a series of products and plans among which our branded "Dan the Saver" plans, which were met with great enthusiasm in the market.Encouraging long-term savings is in accord with the Bank’s strategy of fostering financial planning habits among its customers, as a key driver towards their financial freedom.In 2011, the Corporate Banking Division continued to lead Israel’s corporate credit market, financing the largest deals in the market, while preserving

margins and strict risk management practices.Notably, the Corporate Division was able to maintain the quality of its credit portfolio. The division began implementing the Bank’s strategy of diversifying the concentration risk in the portfolio, while attending to the credit needs of Israeli businesses during a period of economic slowdown.During 2011 the Corporate Division opened 21 business branches, producing a quantum leap in its ability to provide corporate and SME customers with the appropriate level of service. Within the division, the Commercial Banking sector actively recruited new clients and increased its scope of activities with existing clients. These measures followed the strategic plan’s goal, and led to a considerable increase in the credit balances and deposits from medium-sized businesses. These achievements were of great importance for the Bank, having set itself the target of increasing our presence in commercial banking, a clear growth sector which serves as an important dimension in the local economy.The International Banking Division strengthened its activities during the year, placing emphasis on Global Private Banking in Switzerland, and the development of corporate activities in the US, as directed by the Board of Directors. The International Division is considered a significant long-term growth engine for the bank, thereby

Yair SeroussiChairman of the Board of Directors

Bank Hapoalim B.M. and its Consolidated Subsidiaries6

attracting considerable management attention. The development of international activities is emphasized in the current and future strategic plans of the Bank.Towards the end of 2011 we decided to reorganize certain Bank activities. The Bank’s trading activities were integrated with its brokerage operation, as well as its services to asset managers. These activities were combined under the Global Treasury Division, which recently changed its name to the Financial Markets Division. This step is designed to strengthen the Bank’s leadership in financial markets and to offer clients an efficient and professional one-stop-shop for their trading needs across all financial instruments. In addition, the Financial Markets Division continued to lead and develop ALM and nostro activities to assure efficient management of balances, liquidity and the Bank’s balance sheet.Throughout the year we continued to allocate resources and significant efforts towards further strengthening the Bank Hapoalim Group’s Risk Management capabilities, including supporting systems and procedures. Our risk management platform is based on an integrated global view of the Bank’s activities in Israel as well as in international markets, in line with the Bank’s risk appetite and the activities of its subsidiaries. The Risk Management Division is in close contact with Israel’s Supervisor of Banks to ensure that the Bank is in full compliance with regulatory requirements at all times.

Cultivating Human Resources and Work RelationsThroughout 2011, we at Bank Hapoalim continued to promote and develop our most important resource: our employees. During the year the Bank invested in inculcating the Bank’s vision among its employees, with notable involvement of both management and employees alike.The Bank continues to nurture employee relations, which for years has been one of the Bank’s strategic advantages. The employees' union is a full partner in driving the Bank’s success, as exemplified most recently in the 2011 results. We are confident that this partnership will continue to nourish the Bank’s success in the future as well.

Corporate Social Responsibility as a Core ValueThe Bank Hapoalim Group continues to lead Israel’s banking sector in contribution to the community. The Bank focuses on activities related to education, with particular emphasis on responsible financial

behavior, as a key to promoting financial freedom.About half of the “Poalim in the Community” budget is allocated to support educational activities. The remainder is distributed among non-profit organizations active in social welfare, healthcare, and other areas.This is also the fourth consecutive year that the Bank published a comprehensive Sustainability and Corporate Responsibility Report. Similar to previous reports, the 2011 document received the highest rating from the international GRI organization. Furthermore, at the end of the first quarter, the Bank’s was included in the FTSE4GOOD global index, considered the world’s leading index for sustainability and investments based on social responsibility.

Looking to the Future - Main Focuses for 2012The Bank’s strategic plan is designed to ensure a firm foundation for Bank Hapoalim’s position as the leading financial and banking institution in Israel, as the Bank continues to be committed to the credit needs of the entire Israeli economy. We intend to put special emphasis on rapidly growing customer segments, e.g. Israel’s Arab population and orthodox Jews. In addition, we plan to strongly compete for a larger share in the important middle-market business sector.The Bank is also preparing to expand its activities in the small businesses sector. During 2012 we plan to add resources within the framework of a variety of funds, both stand-alone internal funds and funds run in cooperation with the Ministry of Finance, the Israel Manufacturers Association, and other organizations. All these efforts will improve accessibility to financing for this important business sector.

Retail and Corporate Banking LeadershipWe plan to continue to expand our branch network - the largest and most wide-spread in Israel - and to dynamically manage our resources while opening innovative concept branches in competitive geographic locations. These measures will enable us to better adapt our offering to different market segments, offer value-added products and platforms directly to customers and enhance our multi-channel approach as we continue to sharpen our technological edge.We are committed to ensuring the continued standing of our Corporate Division as the most professional and sophisticated lender in Israel, while maintaining appropriate capital adequacy ratios and fulfilling all

Bank Hapoalim B.M. and its Consolidated Subsidiaries7

regulatory requirements. Our strategy calls for a process of continued improvement of client service by further strengthening the business branches we established. We plan on further increasing the share of income from non-credit products from all business segments. Among the steps we plan to take are investments in direct banking channels and greater use of syndications and sale of credit as a core tool for dynamically managing our credit portfolio.

Emphasis on Operational ExcellenceImproved customer service and continuous improvement of our efficiency ratios will lead our drive to operational excellence, as we move resources from outdated activities to support new and strategic initiatives, without increasing headcount. We plan to expand our Central Back Office, the first of its kind and largest in Israel’s banking sector, so that branch efficiency can be honed and work processes at Head Office can be streamlined as well. We expect that these measures will lead to gradual, sustainable improvements in operating efficiency ratios.

Continued Focus on the Implementation of our Strategic PlanThe Bank is formulating its next multi-year strategic plan for the coming three years, as the current plan enters its final year of execution. We continue to seek the path of growth and profitability. We remain confident in our ability to produce for our stakeholders a double-digit return on equity in the long term. This goal takes into account the Bank’s risk appetite, in light of the changes in the economic environment and the increasingly competitive banking market.The Bank is preparing for compliance with Basel III directives which call for strengthening capitalization and the adoption of advanced methodologies vis-à-vis the calculation of risk-weighted assets.

As Israel’s leading bank, with a significant global presence, we place great emphasis on maintaining an on-going dialogue with all stakeholders across all markets in which we are active. We have strong, sustainable contacts in the capital markets and the investor community, and we are proud to be the leading bank in Israel in terms of investor relations. We will continue to deepen this productive dialogue in the future as well.We wish to take this opportunity to extend our deep gratitude to our colleagues in the Board of Management and Board of Directors, to our loyal customers who choose us time and time again, and of course, a sincere and embracing thanks to our employees, who are our most important asset, and whose professionalism and dedication generated the excellent 2011 results.

Sincerely yours,

Yair Seroussi Zion Kenan Chairman of the Board of Directors President and Chief Executive Officer

Zion KenanPresident and CEO

Bank Hapoalim B.M. and its Consolidated Subsidiaries8

Board of Management

Zion Kenan President and Chief Executive OfficerZion Kenan was named President and CEO in August 2009. Mr. Kenan has been with Bank Hapoalim since 1979 and joined the Board of Management in 2001. Before his appointment, he was Deputy CEO and Head of Corporate Banking (2007-2009); Head of Retail Banking (2003-2007), and Head of Human Resources and Logistics (2001-2003). Prior to that, Mr. Kenan fulfilled many senior executive positions in the Retail and Human Resources and Logistics Areas including Southern Regional Manager (1998-2000)Mr. Kenan holds a BA from the Open University and an MA from the Tel Aviv University, both in Social Sciences. He also attended a number of advanced professional courses at Harvard University.

Lilach Asher-TopilskyHead of Retail BankingMs. Asher-Topilsky joined Bank Hapoalim in 1998 and was appointed to the Board of Management in December 2007 as Head of Corporate Strategy. She assumed her current position on October 1, 2009. Prior to joining the Board, she served as Marketing and Planning Division Manager in Retail Banking (9/2006-12/2007), Central Regional Manager (3/2005-9/2006) and Head of the E-Banking Division (3/2001-3/2005)Ms. Asher-Topilsky has a BA in Economics & Management from Tel Aviv University and a Masters degree in Management from Kellogg Business School in Northwestern University, Chicago.

Shimon GalHead of Corporate BankingMr. Gal joined Bank Hapoalim in November 2009 upon his appointment to the Board of Management of the Bank. Before joining the Bank, he served as Head of Corporate Banking (2008-2009) and as Head of the Comptroller, Planning and Operations Division (2004-2007) at Mizrahi-Tefahot Bank Ltd. Mr. Gal has a BA in Economics and Statistics from the Hebrew University of Jerusalem.

Dan KollerChief Risk OfficerMr. Koller joined Bank Hapoalim in 1999 and was appointed to his current position in the Board of Management on January 1, 2008. He served as Manager of the ALM Division from April 2003 and prior to that, was Manager of Financial Planning.Mr. Koller has a BA and a Masters degree in Economics and Business Administration from the Hebrew University of Jerusalem.

Orit Lerer Head of International Banking Ms. Lerer joined Bank Hapoalim in 1977 and was appointed Chief Internal Auditor in February 2004. On January 1, 2010 she was appointed to the Board of Management as Head of International Banking. She also serves as Chairperson of the Board of Bank Hapoalim Switzerland and PAM-Poalim Asset Management, based in London, and as Deputy Chairperson of BankPozitif Kredi Ve Kalkinma Bankasi A.S.Previously, she fulfilled several senior positions in the bank.Ms. Lerer has a BA in Economics from Tel Aviv University.

Anath Levin Head of Financial Markets Ms. Levin joined Bank Hapoalim upon her appointment to the Board of Management of the Bank in May 2010. Before joining the Bank, she served as a Member of the Board of Management and Chief Investment Officer at Migdal Insurance Holdings (2002-2010). Ms. Levin has a BA and a Masters degree in Economics and Business Administration from the Hebrew University of Jerusalem.

Ofer LevyChief AccountantMr. Levy joined Bank Hapoalim in 1981 and was appointed to the Board of Management In 2006. Prior to that, he served as Manager of the Comptrolling Division for ten years. Mr. Levy is a Certified Public Accountant and has a BA in Accounting and Economics from Tel Aviv University.

Ilan MazurChief Legal Advisor Mr. Mazur joined Bank Hapoalim in 1981 and was appointed to his current position in 2003. From 1995-2003 he served as General Counsel to the Corporate Area. Prior to that, he was General Counsel for the International Activity. Before joining the Bank, he worked in private law firms.Mr. Mazur has a degree in Law from the Hebrew University of Jerusalem. He is a member of the Israeli Bar Association.

Zvi NagganHead of Information Technology Mr. Naggan joined Bank Hapoalim in March 2011 upon his appointment to the Board of Management of the Bank.Before joining the Bank, he was President of the Product Business Group and a Member of Senior Management at Amdocs (Israel) Ltd. Mr. Naggan has a B.Sc. in Industrial Engineering from the Technion in Haifa and an MBA in Business Management from Tel-Aviv University.

Bank Hapoalim B.M. and its Consolidated Subsidiaries9

Jacob Orbach Chief Internal Auditor Mr. Orbach joined Bank Hapoalim in 1980 and was appointed to his current position on January 1, 2010. Prior to that, he fulfilled several senior positions including Manager of the Corporate Banking Division (2006-2009) and Manager of the Commercial Banking Division (2002-2006). Mr. Orbach has a BA in Economics from Tel Aviv University.

Ran OzChief Financial OfficerMr. Oz joined Bank Hapoalim in April 2009 upon his appointment to the Board of Management as CFO of the Bank.Before joining the Bank, he served as Deputy CEO & CFO of Bezeq - Israel Telecom (2007-2008) and as Corporate VP & CFO of Nice Systems (2004-2007).Mr. Oz is a Certified Public Accountant and has a BA in Accounting and Economics and a Masters degree in Economics and Business Administration from the Hebrew University of Jerusalem.

Ari PintoHead of Corporate StrategyMr. Pinto has been with Bank Hapoalim since 1980 and was appointed to the Board of Management in September 2009. Before his current appointment, he served as Retail Credit and Mortgages Division Manager (11/2007-9/2009), and as Human Resources Division Manager (12/2002-8/2007). Mr. Pinto has a BA in Business Administration and a Masters degree in Public Administration.

Hanna Pri-Zan Head of Client Asset ManagementMs. Pri-Zan joined Bank Hapoalim in 1972 and was appointed to the Board of Management on February 2004. Before her current appointment on January 1, 2008, Ms. Pri-Zan served as Head of Human Resources, Logistics & Procurement (3/07-12/07), and Head of Banking Subsidiaries and Head of Risk Management (2/2004-3/2007). Prior to her appointment to the Board, Ms. Pri-Zan fulfilled many senior executive positions including Head of the Securities and Financial Assets Division.Ms. Pri-Zan is a member of the Board of Directors in several subsidiaries of Bank Hapoalim and in the TASE (Tel Aviv Stock Exchange).Ms. Pri-Zan has a BA in Economics and Statistics from the Hebrew University of Jerusalem.

Efrat YavetzHead of Human Resources, Logistics and ProcurementMs. Yavetz has been with Bank Hapoalim since 1988 and was appointed to the Board of Management in October 2009. Before her current appointment, she served as Securities and Financial Assets Division Manager (10/2006-10/2009), and as Retail Sales Management Department Manager (2/2004-10/2006). Ms. Yavetz has a BA in Biochemistry from the Hebrew University of Jerusalem and a Masters degree in Business Management from Tel Aviv University.

Board of Directors

Yair SeroussiChairman of the Board of Directors

Mali BaronAmnon DickNira DrorIrit IzaksonMoshe KorenMoshe Luhmany(1)

Yacov PeerEfrat PeledNehama RonenYair Tauman(2)

Imri TovMeir WietchnerYosef YaromNir Zichlinskey

Pnina Dvorin(3)

(1) Serves as a director as of December 1, 2011(2) Serves as a director as of December 1, 2011(3) Served as a director until November 29, 2011

Information for Shareholders

Listing InformationBank Hapoalim’s ordinary shares are listed on the Tel Aviv Stock Exchange and trade under the ticker symbol POLI. As of December 31, 2011 1,323,805,735 ordinary shares were outstanding.

POLI IL

0

200m

100m

300m

POLI IL Volume

Jan Feb Mar Apr May AugJulJun Sep Oct DecNov

2011

1500

1000

2000

The following table presents, the highest and lowest prices for Bank Hapoalim’s ordinary shares. The prices are those recorded at the close of business on the Tel Aviv Stock Exchange.

Tel Aviv

High Low

(NIS) (NIS)

2011 1866 1171

2010 1848 1404

2009 1660 645

2008 1955 713

Past share price performance should not be regarded as a guide to future performance. In mid-2006, Bank Hapoalim Level-1 ADR shares were launched on the OTC market in New York under the following information:

Symbol: BKHYY CUSIP: 062510300 Ratio: 1:5Country: Israel Industry: Banks Depositary: Bank of NY (Sponsored) Underlying SEDOL: 6075808 Underlying ISIN: IL0006625771 US ISIN: US0625103009

GDR's for Bank Hapoalim’s ordinary shares are also listed on the London Stock Exchange and trade under the ticker symbol BKHD.

Earnings per Share (EPS) in NIS

EPS

2011 2.07

2010 1.66

2009 0.99

2008 (0.69)

Dividend PolicyBank Hapoalim’s dividend policy is to distribute up to 50% of annual net operating profit to its shareholders. The dividends paid over the last five years were:

Dividend Per Share

Total PaidNIS Millions

2011 0.204 270

2010 - -

2009 - -

2008 - -

2007 1.27 1,600

The dividend distribution is subject to the provisions of the law, including limitations specified in the directives of the Supervisor of Banks.

Furthermore, according to Directive 331, no dividends shall be distributed when one or more of the last three calendar years ended in a loss, unless the Supervisor of Banks has approved the distribution in advance.Since the year 2008 ended in a loss, the Bank will require such approval in order to distribute dividends until 2012.

Credit RatingsBank Hapoalim is rated by the three major credit rating agencies: Moody’s, Standard and Poors and Fitch.

Rating

Moody’s

Long-Term Deposits A2

Short-Term Deposits P-1

Standard & Poor’s

Long-Term BBB+

Short-Term A2

Fitch

Long-Term A-

Short-Term F2

Shareholder Structure:Shareholders as of December 31, 2011 were:

Public 77.4%

Controlling stake 22.6% of which:

Arison Holdings (1998) 20.2%

Salt of the Earth 2.4%

Institutional Investors InformationFor additional copies of this report, other investor materials or questions, please visit our website at: www.bankhapoalim.com

or contact us at: Bank Hapoalim Investor Relations Dept Yehuda Halevy 63, Tel Aviv Tel. 972-3-5673440 Fax. 972-3-5673470

Bank Hapoalim B.M. and its Consolidated Subsidiaries11

Bank Hapoalim Worldwide

IsraelThe Bank is a recognized leader in Israel's capital markets.In Israel, Bank Hapoalim has hundreds of full-service branches organized into customer lines, such as retail, private banking, small businesses and business branches for the mid-market and large corporate clients.Direct banking channels now play an increasingly important role in serving both retail and corporate customers.A trading room, part of a global trading network, offers advanced services. A Global Private Banking Center provides personalized service and portfolio management.

United StatesThe Miami branch provides private banking services mainly to non-US citizens, serving Latin American clients.The New York branch is focused on providing comprehensive banking servicesto Israeli and local companies operating in the United States, corporate credit and treasuryactivities. In addition, the branch offers investment services to private and corporate clients, including trading in derivatives and brokerage services.The Bank operates an advanced trading room in New York.

United KingdomBank Hapoalim's branch in the West End of London offers a range of corporate and private banking services as well as a sophisticated trading room.

SwitzerlandBank Hapoalim (Switzerland) Ltd, is a wholly owned subsidiary headquartered in Zurich, with branches in Zurich, Geneva, Luxembourg and Singapore and representative offices in Moscow, Hong Kong and Tel Aviv. The Swiss bank is engaged primarily in private banking services, including global portfolio management.

LuxembourgBank Hapoalim (Switzerland) Ltd maintains a branch in Luxembourg for private banking business. In addition, Bank Hapoalim BM operates in Luxembourg through a banking subsidiary.

BHI Investment Advisors (Asia) LimitedA wholly owned subsidiary of Bank Hapoalim (Switzerland) Ltd. The company aims to deliver advisory services to high net worth individuals, focusing primarily on local Asian markets.

SingaporeIn 2007, Bank Hapoalim (Switzerland) inaugurated a full-service private banking branch in Singapore.

TurkeyBank Pozitif is headquartered in Istanbul. The Bank is active mainly in corporate banking.

KazakhstanBank Pozitiv, headquartered in Almaty, is a wholly owned subsidiary of Bank Pozitif. The Bank maintains 3 branches in Kazakhstan.

UruguayFocused on private banking, Hapoalim (Latin America) S.A. is a wholly owned subsidiary of Bank Hapoalim BM. The Bank is based in Montevideo and has branches in Colonia and Punta del Este.

Representative OfficesBank Hapoalim has representative offices in major financial centers worldwide. The offices assist the GPB branches in new client acquisitions, provide personalized service and support in maintaining existing clients, and are active in upholding strong community relations. Representative offices do not engage in banking activities.

Main Locations of Representative Offices

• Toronto• Montreal• Paris• Frankfurt• Budapest• Sydney• Mexico City• Panama City• Santiago

2011Bank Hapoalim

Annual Report 2011

Bank Hapoalim B.M. and its Consolidated Subsidiaries14

ContentsLetter from the Chairman of the Board and the CEO of the Bank 4

Board of Directors' Report for 2011 16

Description of the General Development of the Bank Group's Business 16

Activities of the Bank Group and Description of the Development of its Business 16Principal Data of the Bank Hapoalim Group 18Forward-Looking Information 20Chart of Holdings 21Ratings of the Bank 22Control of the Bank 22Investments in the Capital of the Bank and Transactions in its Shares 22Dividend Distribution 24Capital and Capital Adequacy 25Economic and Financial Review 26Accounting Policies on Critical Matters and Critical Accounting Estimates 28Disclosure Regarding the Procedure for Approval of the Financial Statements 35Profit and Profitability 36Composition and Development of the Bank Group's Assets and Liabilities 46Description of the Bank Group's Business by Segments of Activity 63General – The Segments and Customer Assignment Criteria 63Condensed Financial Information on the Segments of Activity 65The Households Segment 68The Private Banking Segment 79The Small Business Segment 87The Commercial Segment 93The Corporate Segment 100The Financial Management Segment 108Others and Adjustments 113Additional Information Concerning Activity in Certain Products 113Principal Subsidiary and Affiliated Companies 121Activity of the Bank Group Abroad 122General information and Additional Matters 131Fixed Assets and Facilities 131Human Capital 137Liquidity and Raising of Sources of Funds at the Bank 141Taxation Status 144Restrictions and Supervision of the Activity of the Banking Corporation 145Legal Proceedings 148Business Strategy and Objectives 150Risk Management 153Basel II 188Capital Adequacy Target 192Disclosure Regarding the Internal Auditor 209Poalim in the Community – Social Involvement and Contribution to the Community 211Sustainability and Corporate Social Responsibility 213The Board of Directors and the Discharge of its Functions 215Report on Directors with Accounting and Financial Expertise and Professional Qualification 220Board of Directors of the Bank 229Board of Management of the Bank 231Other Matters 232Salaries and Benefits of Office-Holders 238Remuneration of the Auditors 255Controls and Procedures 255

Bank Hapoalim B.M. and its Consolidated Subsidiaries15

Board of Management's Review 257

Appendix I: Consolidated Balance Sheet for the years 2007-2011 - Multi-Period Data 259

Appendix 2: Consolidated Statement of Profit and Loss for the years 2007-2011 - Multi-Period Data 260

Appendix 3: Rates of Financing Income and Expenses - Consolidated 261

Appendix 4: Exposure of the Bank and Subsidiaries to Changes in Interest Rates 266

Appendix 5: Total Credit Risk to the Public by Economic Sectors - Consolidated 274

Appendix 6: Exposure to Foreign Countries - Consolidated 280

Appendix 7: Quarterly consolidated Balance Sheet for the years 2010-2011 - Multi-Quarterly Data 285

Appendix 8: Quarterly consolidated Statement of Profit and Loss for the years 2010-2011

Multi-Quarterly Data 287

CEO Certification 288

Chief Accountant Certification 289

Report of the Board of Directors and the Board of Management

on the Internal Control of Financial Reporting 290

Financial Statements 291

Auditors' Report – Internal Control over Financial Reporting 292

Auditors' Report to the Shareholders 293

Consolidated Balance Sheets 294

Consolidated Statements of Profit and Loss 295

Statement of Changes in Equity 296

Consolidated Statements of Cash Flows 300

Notes to the Financial Statements 302

Condensed Financial Statements of the Bank’s Offices Abroad 445

Periodic Report for 2011 451

The Bank has received approval from the Supervisor of Banks to publish its annual financial statements on a consolidated basis only. Note 34 to the Financial Statements contains the condensed financial statements of the Bank alone. Data concerning the Bank alone is available in hard copy upon request, or at the Bank's website at www.bankhapoalim.co.il.

This is a translation of the Hebrew report and has been prepared for convenience only. In case of any discrepancy, the Hebrew will prevail.

Bank Hapoalim B.M. and its Consolidated Subsidiaries16

Board of Directors' Report for 2011

At the meeting of the Board of Directors held on March 28, 2012, it was resolved to approve and publish the

consolidated financial statements of Bank Hapoalim B.M. for the year ended December 31, 2011.

Description of the General Development of the Bank Group's Business

Activities of the Bank Group and Description of the Development of its BusinessGeneral

• TheBankwasfoundedin1921bythecentralinstitutionsoftheJewishSettlement(theYishuv)atthetime,the

Zionist Histadrut and the Histadrut General Federation of Hebrew Workers in Eretz Yisrael, and incorporated

as a limited company under the Companies Ordinance. The Bank is a "banking corporation" and holds a "bank"

license under the directives of the Banking Law. In 1983, within an arrangement formulated between the Israeli

government and the banks, the shares of the Bank were brought under the control of the state. The Bank was

privatized in 1997, with the controlling interest transferred to the current controlling shareholders and others.

• TheBankGroupoperatesinIsraelinallofthevariousareasofbankingthroughtwomainunits:theCorporate

Area and the Retail Area. The Corporate Area provides service to most of the Bank's business customers; activities

with large corporate clients are conducted through sectors specializing in specific industries, which operate within

the Head Office, while middle-market clients are served through eight Business Centers located throughout Israel.

The various banking services are provided to all customers of this Area through the Bank's branches. A network

of business branches was created in response to customers' business needs, consisting of 21 branches as at the

end of 2011; additional branches are planned to open during 2012. The Retail Area, through the network of

branches, serves customers including households, private banking clients, and small businesses; is responsible for

operating direct-channel services: Internet services, Poalim by Telephone, and mobile services; and also oversees

consumer credit and mortgage activities. The Retail Area operates through 277 branches, which provide the full

range of banking services.

• Inadditiontoitsbankingbusiness,theBankGroupalsoengagesinrelatedactivities,mainlyintheareasofcredit

cards and the capital market. In the credit-card sector, the Bank Group, through a subsidiary (the "Isracard

Group"), issues, operates, and markets credit cards, within and outside the Bank, for use in Israel and overseas,

and clears transactions executed using its credit cards as well as credit cards issued by others. The Bank Group's

capital-market activity includes the provision of services for the execution of trading transactions in securities

(brokerage), securities custody services, research and consulting, services for financial asset managers, investment

portfolio management, and issuance underwriting and management.

Bank Hapoalim B.M. and its Consolidated Subsidiaries17

• AlongsideitsactivitiesinIsrael,theBankGroupalsooperatesoverseas,intheprivate-bankingsectorandinthe

corporate sector. This activity encompasses Israel, Europe, the United States, Canada, Latin America, Australia, Hong

Kong, and Singapore, by means of branches, representative offices, banking subsidiaries, and asset-management

subsidiaries. The Bank Group also operates in the households sector and in the commercial sector in Turkey

and Kazakhstan. In its private-banking activity, the Bank Group provides its high-net-worth customers abroad

with advanced professional products and services, including investment products and global asset management.

Corporate sector activity abroad includes the provision of credit to local and foreign borrowers, mainly through

the acquisition of participation in credit organized by leading banks abroad; the provision of credit to borrowers

with an affinity to Israel; and investments in bonds. As part of its international activity, the Bank Group maintains

ties with over 2,400 foreign banks around the world (hereinafter : "correspondent banks"). The Bank's strategy is

currently aimed at the development and expansion of its international activity, both in the area of Global Private

Banking and in the business activities of its London and New York branches. The Bank aims to continue to expand

its service package and improve its capabilities in the areas of products, marketing, and customer service.

The following are details of the principal developments and changes that occurred during 2011.

Development of the Bank Group’s Business

Net profit of the Bank Group attributed to shareholders of the Bank totaled approximately NIS 2,746 million in 2011,

compared with profit in the amount of approximately NIS 2,201 million in 2010.

Net return on equity attributed to shareholders of the Bank was 12.0% in 2011, compared with 10.4% in 2010.

Basic net profit per share of par value NIS 1 amounted to NIS 2.07 in 2011, compared with NIS 1.66 in 2010.

Total assets of the Bank Group as at December 31, 2011 amounted to approximately NIS 356.7 billion, compared

with approximately NIS 321.1 billion at the end of 2010, an increase of 11.1%.

Net total credit to the public amounted to NIS 246.5 billion as at December 31, 2011, compared with NIS 225.3 billion

at the end of 2010, an increase of 9.4%.

Total deposits from the public amounted to NIS 256.4 billion as at December 31, 2011, compared with NIS 234.0 billion

at the end of 2010, an increase of 9.6%.

Total shareholders’ equity amounted to NIS 23.8 billion as at December 31, 2011, compared with NIS 22.6 billion

at the end of 2010, an increase of 5.7%.

The total capital ratio as at December 31, 2011 was 14.1%, compared with 13.9% at the end of 2010.

Bank Hapoalim B.M. and its Consolidated Subsidiaries18

Principal Data of the Bank Hapoalim Group

For the year ended December 31 Change vs.

2011 2010 2009 2010 2009

NIS millions

Profit and Profitability

Profit from financing activity before provisions for credit losses 8,231 7,775 6,718 5.9% 22.5%

Operating and other income 4,852 *5,052 *5,039 (4.0%) (3.7%)

Total income 13,083 *12,827 *11,757 2.0% 11.3%

Provisions for credit losses 1,202 1,030 2,017 16.7% (40.4%)

Operating and other expenses 8,365 *8,291 *7,457 0.9% 12.2%

Net operating profit attributed to the shareholders of the Bank 2,741 *2,185 *1,272 25.4% 115.5%

Profit from extraordinary transactions, after taxes, before attribution to non controlling interests 5 16 28 (68.8%) (82.1%)

Net profit attributed to the shareholders of the Bank 2,746 *2,201 *1,300 24.8% 111.2%

December 31 Change vs.

Balance sheet - Principal Data

Total balance sheet 356,688 *321,089 *309,757 11.1% 15.2%

Net credit to the public 246,495 225,288 215,788 9.4% 14.2%

Securities 34,411 31,604 28,055 8.9% 22.7%

Deposits from the public 256,417 233,965 231,993 9.6% 10.5%

Bonds and subordinated notes 32,933 27,608 23,112 19.3% 42.5%

Shareholders’ equity 23,845 *22,561 *20,097 5.7% 18.6%

Total problematic debts as reported in the past - 14,895 16,636 - -

Total problematic credit risk under the new directive** 12,799 ***14,575 - (12.2%) -

Of which: impaired balance-sheet debts** 7,044 8,316 - (15.3%) -

2011 2010 2009

Main Financial Ratios

Net loan to deposit ratio 96.1% 96.3% 93.0%

Net loan to deposit ratio including bonds and subordinated notes 85.2% 86.1% 84.6%

Shareholders’ equity to total assets 6.7% *7.0% *6.5%

Core Tier I capital to risk-adjusted assets 7.9% *8.0% *7.5%

Tier I capital to risk-adjusted assets 8.7% *8.9% *8.3%

Total capital to risk-adjusted assets 14.1% *13.9% *13.5%

Financing margin from regular activity(a) 2.52% 2.59% 2.36%

Cost-income ratio 63.9% *64.6% *63.4%

Rate of provisions for credit losses for the period, of total credit to the public(b) 0.48% 0.49% 0.90%

Net return of operating profit attributed to shareholders of the Bank on equity 12.0% *10.3% *6.6%

Net return of profit attributed to shareholders of the Bank on equity 12.0% *10.4% *6.8%

Basic net profit per share in NIS attributed to shareholders of the Bank 2.07 *1.66 *0.99

Diluted net profit per share in NIS attributed to shareholders of the Bank 2.05 *1.65 *0.98

* Restated, due to the retroactive implementation of the directives of the Supervisor of Banks regarding financial reporting on employee benefits. Most of the change is in the items "operating and other income", "other expenses", and "shareholders’ equity". For further details, see Note 1(E)(18) in the Financial Statements.

** Net of the individual allowance and the allowance according to the extent of arrears.*** Pro forma data.(a) Calculation: Financing profit from regular activity is divided by monetary assets generating financing income. (b) In 2011, calculated as the provisions for credit losses as a percentage of the recorded balance of credit to the public. In previous years, calculated as the specific provision for the period as a percentage of total credit to the public.

Bank Hapoalim B.M. and its Consolidated Subsidiaries19

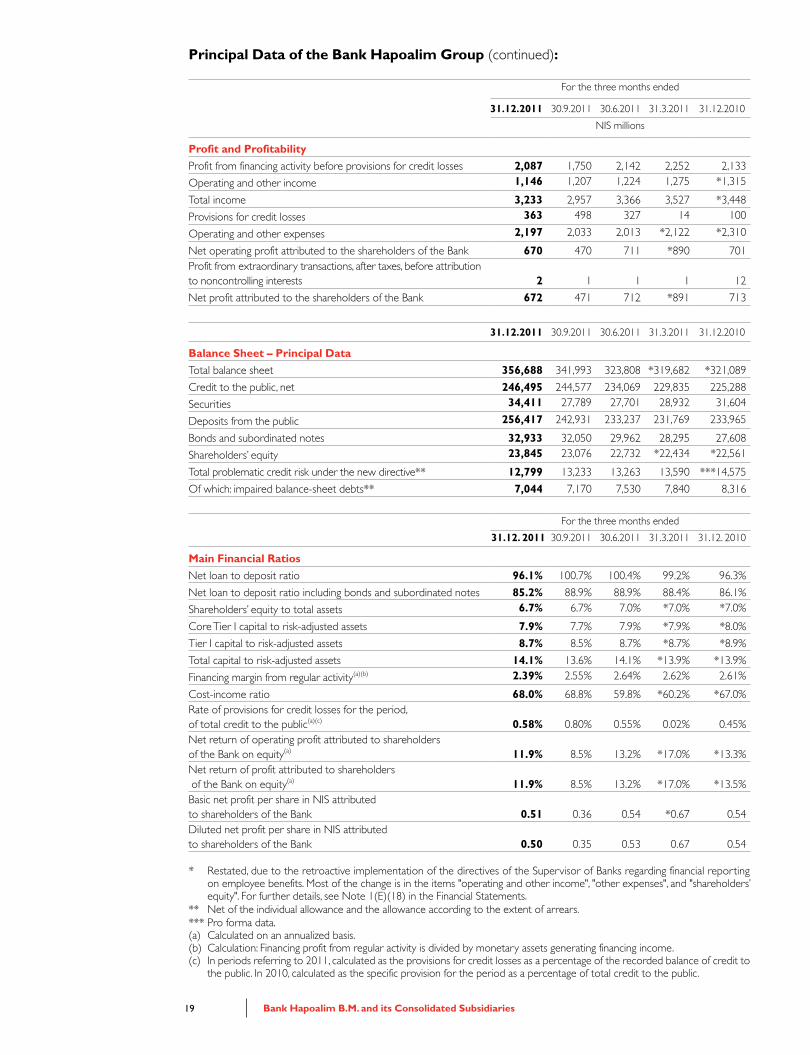

Principal Data of the Bank Hapoalim Group (continued):

For the three months ended

31.12.2011 30.9.2011 30.6.2011 31.3.2011 31.12.2010

NIS millions

Profit and Profitability

Profit from financing activity before provisions for credit losses 2,087 1,750 2,142 2,252 2,133

Operating and other income 1,146 1,207 1,224 1,275 *1,315

Total income 3,233 2,957 3,366 3,527 *3,448

Provisions for credit losses 363 498 327 14 100

Operating and other expenses 2,197 2,033 2,013 *2,122 *2,310

Net operating profit attributed to the shareholders of the Bank 670 470 711 *890 701Profit from extraordinary transactions, after taxes, before attribution to noncontrolling interests 2 1 1 1 12

Net profit attributed to the shareholders of the Bank 672 471 712 *891 713

31.12.2011 30.9.2011 30.6.2011 31.3.2011 31.12.2010

Balance Sheet – Principal Data

Total balance sheet 356,688 341,993 323,808 *319,682 *321,089

Credit to the public, net 246,495 244,577 234,069 229,835 225,288

Securities 34,411 27,789 27,701 28,932 31,604

Deposits from the public 256,417 242,931 233,237 231,769 233,965

Bonds and subordinated notes 32,933 32,050 29,962 28,295 27,608

Shareholders’ equity 23,845 23,076 22,732 *22,434 *22,561

Total problematic credit risk under the new directive** 12,799 13,233 13,263 13,590 ***14,575

Of which: impaired balance-sheet debts** 7,044 7,170 7,530 7,840 8,316

For the three months ended

31.12. 2011 30.9.2011 30.6.2011 31.3.2011 31.12. 2010

Main Financial Ratios

Net loan to deposit ratio 96.1% 100.7% 100.4% 99.2% 96.3%

Net loan to deposit ratio including bonds and subordinated notes 85.2% 88.9% 88.9% 88.4% 86.1%

Shareholders’ equity to total assets 6.7% 6.7% 7.0% *7.0% *7.0%

Core Tier I capital to risk-adjusted assets 7.9% 7.7% 7.9% *7.9% *8.0%

Tier I capital to risk-adjusted assets 8.7% 8.5% 8.7% *8.7% *8.9%

Total capital to risk-adjusted assets 14.1% 13.6% 14.1% *13.9% *13.9%

Financing margin from regular activity(a)(b) 2.39% 2.55% 2.64% 2.62% 2.61%

Cost-income ratio 68.0% 68.8% 59.8% *60.2% *67.0%Rate of provisions for credit losses for the period, of total credit to the public(a)(c) 0.58% 0.80% 0.55% 0.02% 0.45%Net return of operating profit attributed to shareholders of the Bank on equity(a) 11.9% 8.5% 13.2% *17.0% *13.3%Net return of profit attributed to shareholders of the Bank on equity(a) 11.9% 8.5% 13.2% *17.0% *13.5%Basic net profit per share in NIS attributed to shareholders of the Bank 0.51 0.36 0.54 *0.67 0.54Diluted net profit per share in NIS attributed to shareholders of the Bank 0.50 0.35 0.53 0.67 0.54

* Restated, due to the retroactive implementation of the directives of the Supervisor of Banks regarding financial reporting on employee benefits. Most of the change is in the items "operating and other income", "other expenses", and "shareholders’ equity". For further details, see Note 1(E)(18) in the Financial Statements.

** Net of the individual allowance and the allowance according to the extent of arrears.*** Pro forma data.(a) Calculated on an annualized basis. (b) Calculation: Financing profit from regular activity is divided by monetary assets generating financing income. (c) In periods referring to 2011, calculated as the provisions for credit losses as a percentage of the recorded balance of credit to

the public. In 2010, calculated as the specific provision for the period as a percentage of total credit to the public.

Bank Hapoalim B.M. and its Consolidated Subsidiaries20

Forward-Looking InformationSome of the information in this report that does not refer to historical facts constitutes forward-looking information,

as defined in the Securities Law. The Bank's actual results may differ materially from those included in forward-looking

information, as a result of a large number of factors, including changes in capital markets in Israel and globally,

macro-economic changes, changes in geopolitical conditions, regulatory changes, and other changes not under the

Bank's control, which may lead to the failure of estimates to materialize and/or changes in the Bank's business plans.

Forward-looking information is marked by words or phrases such as "we believe", "expect", "forecast", "estimate",

"intend", "plan", "aim", "may change", and similar expressions, as well as words such as "plan", "target", "wish", "should",

"can", or "will". Such forward-looking information and expressions involve risk and uncertainty, because they are based

on management's estimates regarding future events, which include changes in the following parameters, among others:

economic conditions, public tastes, interest rates in Israel and overseas, inflation rates, new legislation and regulation in

the area of banking and the capital market, exposure to financial risks, the financial stability of borrowers, the behavior

of competitors, aspects related to the Bank's image, technological developments, and manpower-related matters,

and other areas that affect the activity of the Bank and the environment in which it operates, the materialization of

which is uncertain by nature.

The information presented below is based, among other things, on information known to the Bank and based, among

other things, on publications by various entities, such as the Central Bureau of Statistics, the Ministry of Finance, the

Bank of Israel, the Ministry of Housing, and other entities that publish data and estimates regarding the capital markets

in Israel and globally.

This information reflects the Bank’s current viewpoint with regard to future events, which is based on estimates, and

is therefore subject to risks and uncertainty, as well as to the possibility that expected events or developments may

not materialize at all or may only partially materialize.

Bank Hapoalim B.M. and its Consolidated Subsidiaries21

Chart of Holdings Set out below is a chart of the Bank’s main holdings*:

100%100%100%

100%

69.8%

100%98.2%100%

Poalim Sahar Ltd.Poalim Express

Bank PozitifTurkey

Bank PozitivKazakhstan

Poalim Capital MarketsIsracard

Bank Hapoalim(Switzerland)

Bank Hapoalim(Cayman)

Other FinancialServicesCredit Cards

The Bank

Banks Abroad

* The chart includes the principal companies held directly by the Bank or indirectly through private subsidiaries under the full ownership of the Bank. The wholly-owned subsidiaries through which the companies in the above chart are held do not appear in the chart. For the purposes of this chart, a principal company is a company engaged in business operations which in the opinion of the Board of Management of the Bank is a principal company in the Group, and in which the Bank's investment is at least 1% of the shareholders' equity of the Bank, or the Bank's share of whose net operating profit (loss) attributed to shareholders of the Bank exceeds 5% of the net operating profit (or loss) attributed to shareholders of the Bank (similar to the criterion established in Public Reporting Directive No. 662 of the Supervisor of Banks regarding the statement of data on principal subsidiaries in financial statements of banking corporations).

Bank Hapoalim B.M. and its Consolidated Subsidiaries22

Ratings of the Bank The following ratings have been assigned to the Bank by rating agencies in Israel and abroad:

In Israel, in local currency, the Bank is rated AA+ by S&P Maalot Ltd. and Aaa by Midroog.

In August 2011, the rating agency Midroog published a rating of Aaa for long-term deposits and P-1 for short-term

deposits of the Bank, for the first time. These ratings are the highest possible for a financial institution in Israel.

Ratings of the Bank and of Israel by the international rating agencies:

Rating agency Long-term foreign currency

Short-term foreign currency

Rating outlook Last update

Israel – sovereign rating:

Moody’s A1 P-1 Stable April 2011

S&P A+ A-1 Stable September 2011

Fitch Ratings A F1 Stable May 2011

Bank Hapoalim:

Moody’s A2 P-1 Stable April 2011

S&P BBB+ A-2 Stable December 2011

Fitch Ratings A- F2 Stable June 2011

In April 2011, the rating agency Moody’s revised its rating of the Israeli banking system. As a result, long-term ratings of the five major banking groups in Israel were lowered by one notch. The Bank’s rating was downgraded from A1 to A2, due to the rating agency’s expectation that the profitability of the banks would remain low relative to international comparison groups of similarly rated companies. In addition, the Bank’s rating outlook was revised from Negative to Stable. In June 2011, the rating agency Fitch Ratings reaffirmed the Bank’s rating, with no change. In September 2011, the rating agency S&P upgraded Israel’s long-term sovereign rating from A to A+. In December 2011, the rating agency S&P and its Israeli subsidiary S&P Maalot reaffirmed the Bank’s ratings, with no change.

Control of the Bank The holder of the permit for control of the Bank, near the date of publication of the financial statements, is Ms. Shari

Arison. Her stake in the Bank is held through several trusts that have holdings in the Israeli companies noted below,

which own shares of the Bank.

Arison Holdings (1998) Ltd. ("Arison Holdings") holds shares comprising approximately 20.20% of the Bank’s share

capital near the date of publication of the financial statements, which constitute the "controlling interest" of the Bank

(as defined in the control permit issued by the Governor of the Bank of Israel).

Arison Investments Ltd. (a sister company of Arison Holdings; hereinafter : "Arison Investments"), through

a wholly-owned subsidiary, holds the entire share capital of Salt Industries Ltd., which holds shares comprising

approximately 2.40% of the share capital of the Bank.

Near the date of publication of the financial statements, the Arison Group (through Arison Holdings and Arison

Investments) holds a total of approximately 22.60% (22.37% fully diluted) of the share capital of the Bank.

Investments in the Capital of the Bank and Transactions in its Shares The issued and paid-up share capital of the Bank, as at December 31, 2011, is NIS 1,323,805,735 par value, composed

of 1,323,805,735 ordinary shares of par value NIS 1 each. This is the issued capital following the subtraction of

5,183,853 ordinary shares purchased by the Bank, as detailed below.

The issued and paid-up capital of the Bank near the date of publication of the financial statements is NIS 1,324, 587,125

par value, composed of 1,324,587,125 ordinary shares of NIS 1 par value each. This is the issued capital following the

subtraction of 5,653,853 ordinary shares purchased by the Bank. The principal developments related to the capital of

the Bank, including investments in the capital of the Bank and transactions in the shares of the Bank, are detailed below.

Bank Hapoalim B.M. and its Consolidated Subsidiaries23

Interested Parties

The Delek Group Ltd., which includes The Phoenix Insurance Company Ltd. and Excellence Investments Ltd., is an

interested party of the Bank. Its stake is held through a proprietary account, and through and together with holdings

in profit-participatory life insurance accounts, holdings of mutual fund management companies, provident funds, or

provident fund management companies under its control or management, directly or indirectly.

Near the date of publication of the financial statements, the rate of holdings of the Delek Group Ltd. is 6.52%.

The changes in the capital of the Bank from January 1, 2011 up to near the date of publication of

the financial statements are described below:

In 2011, and up to the date of publication of the financial statements, an increase of approximately 5,296,168 ordinary

shares occurred in the issued and paid-up capital of the Bank, as a result of the conversion of 5, 296,168 options

allocated to employees of the Bank under the plan from May 2004. The remaining option notes granted to employees

of the Bank under this program amount to 7,146,954 option notes.

The last packet of options pursuant to the extension plan of September 30, 2009, consisting of 4,332,998 share option

notes, was allocated in February 2012. Near the date of publication of the Financial Statements, 12,526,743 option

notes had been allocated and not yet exercised; these options will be converted into shares, as described above,

from the pool of shares to be purchased for this purpose.

For further details regarding the issuance of stock options to the Chairman of the Board of Directors, the CEO, senior

executives, and employees of the Bank, see Note 16 to the financial statements.

On February 28, 2012, the Board of Directors of the Bank, following approval by the Salaries and Remuneration

Committee and the Audit Committee of the Board of Directors of the Bank, resolved to replace restricted phantom

shares that have been granted, the restriction period of which is scheduled to end on December 31, 2013 or later,

with restricted stock units ("RSU"), pursuant to the "Bank Hapoalim B.M. Secondary Plan for the Grant of Restricted

Stock Units (RSU) to Senior Executives 2011", which represents the implementation of certain directives of the 2010

remuneration plan, and constitutes an integral part thereof. RSU are units of restricted shares, which upon fulfillment

of the appropriate vesting conditions are automatically exercised into ordinary shares of the Bank, which will be held

by the Bank as dormant shares, without the payment of any exercise price. The vesting and restriction periods of

the RSU shall be identical, as a rule, to those of the restricted phantom shares that they are replacing. The RSU shall

be allocated according to the capital gains track pursuant to Section 102(B)(2) of the Income Tax Ordinance [New

Version], 1961. The RSU shall be allocated following the publication of an appropriate outline by the Bank and the

fulfillment of additional requirements pursuant to the Securities Law, 1968, and the related regulations.

Buybacks of Shares of the Bank

1. On November 11, 2010, the Supervisor of Banks approved a buyback of 12,750,000 shares for the purpose of

employee compensation under the extension plan of September 2009 (see Note 16(A)(1) to the Financial Statements),

as well as a buyback of up to 14,000,000 shares for the purpose of the senior executives’ compensation plan (see

Note 15 to the Financial Statements). The Board of Directors approved a share purchase plan on March 30, 2011.

Near the date of publication of the Financial Statements, the balance of the acquired shares amounts to 5,000,000

shares, at a cost of approximately NIS 81 million.

2. Pursuant to an approval of the Supervisor of Banks, in 2009, the Bank purchased 700,000 ordinary shares of par

value NIS 1 each of the Bank through an external entity, with the aim of using the shares as a pool from which to

transfer shares in the event of the exercise of options allocated to the former chairman of the board of directors and

the former chief executive officer of the Bank, as detailed in Note 16(A)(4) to the Financial Statements. The remaining

shares, following the exercise by the former chairman of the board, as described above, amount to 653,853 ordinary

shares at a cost of approximately NIS 10 million.

Bank Hapoalim B.M. and its Consolidated Subsidiaries24

Dividend Distribution The Board of Directors updated the Bank’s policy on dividend distribution on May 30, 2011. Pursuant to the policy

established, up to half of net operating profits will be distributed each year, subject to the capital targets of the Bank,

as established by the Board of Directors. Dividends from nonrecurring profits will be distributed according to ad-hoc

decisions by the Board of Directors.

In addition to restrictions under the Companies Law, dividend distribution by banking corporations is subject to

regulation applicable to banking corporations in Israel, pursuant to which no dividends shall be distributed: (A) If the

cumulative balance of retained earnings of the bank according to its last published financial statements is not positive,

or if the payout would lead to a negative balance; (B) when one or more of the last three calendar years ended in

a loss; (C) when the cumulative result of the three quarters ended at the end of the interim period for which the

last financial statement has been released indicates a loss; (D) if the payout would cause the bank's ratio of capital

to risk-adjusted assets to fall below the required rate; (E) from capital reserves or positive differences resulting from

the translation of financial statements of autonomous units abroad; (F) if after the payout the bank's non-monetary

assets would exceed its shareholders' equity; or (G) if the bank does not comply with the requirements of Section

23A of the Banking Law, which establishes a limit on the percentage of capital that a banking corporation may invest

in non-financial corporations. Notwithstanding the above, in certain cases the Bank can distribute dividends even if

the aforesaid circumstances apply, if it obtains prior written approval of the Supervisor of Banks for such distribution,

up to the amount thus approved.

In addition, according to the circular of the Supervisor of Banks of June 2010, a banking corporation shall not distribute

dividends unless it has a core Tier I capital ratio of at least 7.5%, or if such distribution would cause a failure to comply

with the aforesaid ratio.

In addition, pursuant to the terms of the Subordinated Notes (Series A), no dividends shall be distributed in the

following cases: (A) If interest payments in respect of these notes are suspended, the Bank shall not pay dividends

to its shareholders until all of the suspended interest payments are paid in full, whether such dividends are declared

prior to the Bank's announcement regarding the formation of circumstances for suspension, or whether the dividends

are declared after such an announcement; and (B) If the payout would cause the Bank's ratio of core Tier I capital to

risk-adjusted assets to fall below 6.5%.

Furthermore, the permission granted by the Governor of the Bank of Israel to the Arison Group to acquire a

controlling interest in the Bank states that no dividend shall be distributed from profits accrued at the Bank up to

June 30, 1997 (the day prior to the acquisition of the controlling interest), unless the Supervisor of Banks has consented

in advance and in writing.

Further to the approval of the Supervisor of Banks regarding the distribution of a dividend in respect of the profits

of the first quarter of 2011, on June 30, 2011, the Board of Directors of the Bank resolved on the payment of a

dividend in the amount of NIS 270 million, constituting NIS 0.204 per share of par value NIS 1. The dividend was

paid on July 27, 2011.

The balance of retained earnings at the Bank as at December 31, 2011 totaled approximately NIS 15,371 million, of

which a total of approximately NIS 2,734 million cannot be distributed as dividends.

Bank Hapoalim B.M. and its Consolidated Subsidiaries25

Capital and Capital AdequacyThe capital target of the Bank is the appropriate level of capital required in respect of the various risks to which the

Bank is exposed, as identified, assessed, and estimated by the Bank. This target total capital ratio is higher than the

regulatory minimum capital requirement, and includes the capital requirement in respect of Pillar I risks, plus capital

in respect of Pillar II risks, with the aim of allowing the Bank to comply with capital requirements in cases of external

crisis events (extreme scenarios) while complying with regulatory minimum capital requirements. This target takes

into consideration actions of the Board of Management of the Bank aimed at reducing the risk level and/or increasing

the capital base.

A resolution of the Board of Directors of the Bank of December 30, 2010 established minimum targets of 7.5% for

the Bank's core Tier I capital ratio and 12.5% for the Bank's total capital ratio.

With regard to the draft instruction of the Supervisor of Banks of March 14, 2012, concerning the establishment of

a minimum core Tier 1 capital ratio, see the section "Basel II," below.

December 31, 2011

December 31, 2010*

December 31, 2010*

Reported Pro-forma**

Audited Unaudited

NIS millions

1. Capital for the calculation of the capital ratio

Core capital 23,795 22,251 21,395

Tier I capital, after deductions 26,183 24,579 23,723

Tier II capital, after deductions 16,175 13,968 13,968

Total overall capital 42,358 38,547 37,691

2. Weighted balances of risk-adjusted assets

Credit risk 274,063 252,277 251,421

Market risks 7,018 5,483 5,483

Operational risk 20,047 19,154 19,154

Total weighted balances of risk-adjusted assets 301,128 276,914 276,058

3. Ratio of capital to risk-adjusted assets

%

Ratio of core capital to risk-adjusted assets 7.90% 8.04% 7.75%

Ratio of Tier I capital to risk-adjusted assets 8.69% 8.88% 8.59%

Ratio of total capital to risk-adjusted assets 14.07% 13.92% 13.65%

Minimum total capital ratio required by the Supervisor of Banks 9.00% 9.00% 9.00%

* Restated, due to the retroactive implementation of the directives of the Supervisor of Banks regarding financial reporting on employee benefits. For further details, see Note 1(E)(18) in the Financial Statements.

** The Bank has implemented the directives of the Supervisor of Banks regarding the measurement and disclosure of impaired debts as of January 1, 2011, as well as several IFRS adopted by the Supervisor of Banks. The pro-forma data represent the capital ratio of the Bank as it would have been if the aforesaid directives had been implemented on December 31, 2010.

The effect of the implementation on equity as of January 1, 2011, amounted to approximately NIS 856 million.

Bank Hapoalim B.M. and its Consolidated Subsidiaries26

The ratio of total capital to risk-adjusted assets as at December 31, 2011 was 14.07%, compared with a capital ratio

of 13.65% on December 31, 2010, based on a pro-forma calculation.

The core Tier I capital ratio as at December 31, 2011 was 7.90%, compared with a core Tier I capital ratio of 7.75%

at the end of 2010, based on a pro-forma calculation.

Data on capital were restated due to the retroactive implementation of the directives of the Supervisor of Banks

regarding financial reporting on employee benefits. The effect of the implementation on capital as at December 31, 2010

amounted to a decrease in capital in the amount of NIS 528 million.

Total capital for the purpose of the calculation of the capital ratio as at December 31, 2011 amounted to approximately

NIS 42,358 million, compared with NIS 37,691 million on December 31, 2010, based on a pro-forma calculation. The

increase in the capital base mainly resulted from net profit and from the issuance of subordinated notes. This increase

was offset by dividend distribution.

Risk-adjusted assets as at December 31, 2011 amounted to NIS 301.1 billion, compared with NIS 276.1 billion on

December 31, 2010, based on a pro-forma calculation. The increase in risk-adjusted assets mainly resulted from an

increase in credit to the public.

Economic and Financial Review Developments in the Global Economy

Global economic activity slowed in the second half of 2011, against a backdrop of numerous issues confronted

by the global economy, most notably the sovereign debt crisis in Europe. Overall for the year, the global economy

grew by 3.8%, with the developing economies contributing most of this growth. The developed economies posted a

moderate growth rate of 1.6% and continued to show high variance: growth was high at 1.8% in the United States

and 3.0% in Germany, whereas Japan experienced GDP contraction of 0.9%, mainly due to the immense economic

damage inflicted by the earthquake and tsunami in the first quarter. The Eurozone economy achieved an average

growth rate of 1.6%, but the countries in crisis – primarily Greece, Portugal, Spain, and Italy – experienced negative

or very low growth. The developing economies grew by 6.2%, led by China and India, at 9.2% and 7.4% respectively.

The slowdown in global activity was accompanied by high unemployment rates; unemployment in the Eurozone

climbed to 10.4% by the end of the year, while in the United States the economy began to create jobs again, as

unemployment lessened somewhat to 8.5%.

The recovery of the global economy is threatened by the mounting risks in the Eurozone and by the fragility of growth

in other regions. A crisis of credibility of economic policies and leadership emerged in almost all of the developed

countries and served as a key factor in the downgrade of credit ratings of the United States, France, and additional

European countries. Financial conditions globally have continued to deteriorate, and the debt crisis in Europe has not

yet been resolved; meanwhile, the Eurozone is expected to see a recession in 2012. The high debt financing needs

of the Eurozone economies; first and foremost Italy and Spain, which have had to refinance debt at high yields, are

jeopardizing the Eurozone’s stability. Despite the establishment and expansion of the European Financial Stability

Facility as well as support for the countries in crisis from the ECB and the heads of the European Union, yields and

insurance premiums (CDS) for debts of these countries remain high. The finance ministers of the European Union have

reached an arrangement in which another aid package will be approved for Greece, as part of a plan encompassing

a devaluation of Greece’s debt to bond holders (by approximately 70%, in terms of the present value) and the

expansion of austerity measures. In view of the deep recession in the Greek economy, there are doubts regarding

the success of this plan and the ability of Greece to remain a member of the Eurozone.

Monetary policy has continued to be highly expansive: in the United States, the Fed announced that the interest rate

would probably remain near zero until mid-2014. In Europe, the interest rate was lowered to 1.0%, with estimates

calling for a continued decrease. The European Central Bank purchased bonds of the countries in crisis during the

year, and provided loans to commercial banks.

Bank Hapoalim B.M. and its Consolidated Subsidiaries27

Economic Activity in Israel

The Israeli economy continued to grow in 2011, at a rate of 4.7%, but growth began to slow at the midyear mark,

falling from 5.3% in the first half to 3.6% in the second half of the year. The deceleration was initially mainly apparent in

exports, but in the later months of the year the slowdown was felt in demand for consumption as well. In comparison

to economic conditions in Europe and the United States, the performance of the Israeli economy was still strong;

this can be attributed to the sound condition of households, to the fact that the government was not forced to

make budget cuts, and to the stability of the financial sector. The unemployment rate continued to fall during the year,

reaching 5.4% in the fourth quarter of 2011, down from 6.5% in the fourth quarter of 2010. The housing market

experienced a turnaround over the last year, with sales of new homes dropping by 29% year-on-year in the second

half. Housing starts increased, reaching 44,000 units. As a result, the supply of unsold homes is trending up. According

to the Central Bureau of Statistics (CBS) survey on prices of homes, prices began to decrease moderately during the

last few months of the year. Social protests over the cost of living in Israel broke out during the third quarter of 2011.

The Committee for Socio-Economic Change was established, headed by Prof. Trajtenberg; the committee released

its recommendations in late September 2011. Some of these recommendations, mainly concerning taxation, have

already been implemented, as of the beginning of 2012; in the area of education, some of the recommendations have

been approved, and a gradual implementation process is planned.

As of the beginning of 2012, the economy is still growing, though at a more moderate pace. The European debt crisis

is a significant risk factor, as about one-third of Israel’s exports of goods are designated for EU countries. Another risk

factor is the financing problems facing the business sector: the volume of issues in the capital market dropped sharply in

the second half of 2011, either as a result of an increase in risk levels or due to regulation affecting institutional entities.

Fiscal and Monetary Policy

The slowdown in economic growth was reflected in government tax revenues. Starting in the second quarter of

2011, indirect tax collection decreased; in the third quarter of 2011, direct taxes began to decline as well. Overall

for the year, tax revenues were lower than planned by NIS 6 billion, and the budget deficit reached NIS 28.6 billion,

or 3.3% of GDP, versus the target of 3.0%. The decline in tax revenues and the slowdown in economic growth have

increased the probability of an above-target budget deficit in 2012; estimates by the Ministry of Finance predict a

deficit of 3.2% of GDP.

The Bank of Israel interest rate trended up during the first half of 2011, as a result of the rapid growth of the economy,

the increase in housing prices, and expectations that inflation would exceed the target range. The downturn in

economic growth and in global economic conditions caused a halt to the increase in the interest rate in the third

quarter, and the rate was lowered again in the fourth quarter of 2011. The interest rate stood at 2.0% at the beginning

of 2011 and 2.75% at the end of the year, and was lowered to 2.5% in February 2012. On the annual level, monetary