www.distell.co.za

annual report

2007

Distell A

nn

ual R

epo

rt 2007

Distell Annual Report 2007Distell Annual Report 2007

Dates of importance to shareholders

Annual general meeting October 2007

Financial reports Interim report February 2008

Preliminary announcement of annual results August 2008

Annual financial statements September 2008

Ordinary dividends Interim dividends

– declaration February 2008

– payable March 2008

Final dividends

– declaration August 2008

– payable September 2008

Administration

Distell Group Limited Incorporated in the Republic of South Africa

(Registration number: 1988/005808/06)

ISIN: ZAE000028668

JSE share code: DST

Company secretary CJ Cronjé

Registered office Aan-de-Wagen Road, Stellenbosch 7600

PO Box 184, Stellenbosch 7599

Telephone: 021 809 7000

Facsimile: 021 886 4611

E-mail: [email protected]

Transfer secretaries Computershare Investor Services 2004 (Proprietary) Limited

70 Marshall Street, Johannesburg 2001

PO Box 61051, Marshalltown 2107

Telephone: 011 370 7700

Facsimile: 011 688 5221

Auditors PricewaterhouseCoopers Inc.

Stellenbosch

Listing JSE Limited

Sector: Consumer Goods – Food and Beverage – Beverages

Sponsor Rand Merchant Bank (A division of FirstRand Bank Limited)

Websitewww.distell.co.za

COMPRESS ) 3460

CONTENTS

Features

Our Group 3

Annual highlights 4

How we’ve measured up 5

Our brands at a glance 8

Our global presence 10

Board matters 12

Seven-year fi nancial review 15

Analysis of shareholders 18

Cash value added statement 19

Reviews

Chairman’s statement 20

Managing director’s report 24

Corporate

Corporate governance 32

Sustainability report 37

Financials

Consolidated annual fi nancial statements 52

Notice to shareholders, voting form,

dates of importance and administration 102

DISTELLANNUAL REPORT

2007

1Distell Annual Report 2007

we craftgreat brands

2 Distell Annual Report 2007

Our culture

Who we areAfrica’s leading producer and marketer of fi ne wines,

spirits, ciders and ready-to-drinks (RTDs).

Our visionA great company rooted in South Africa crafting

leading liquor brands for people to enjoy at every

occasion the world over.

We turn into assets.

At Distell, we create brands quite literally from the ground up.

Each brand starts as a tiny seed – or a germ of an idea – and is then crafted and nurtured to its fi nal

perfection through years of care and dedication. We harvest the raw materials from the earth, blend it

with our own passion and shape it into brands that have become icons of companionship, relaxation

and celebration . . . Th at’s why we’re Brandcrafters.

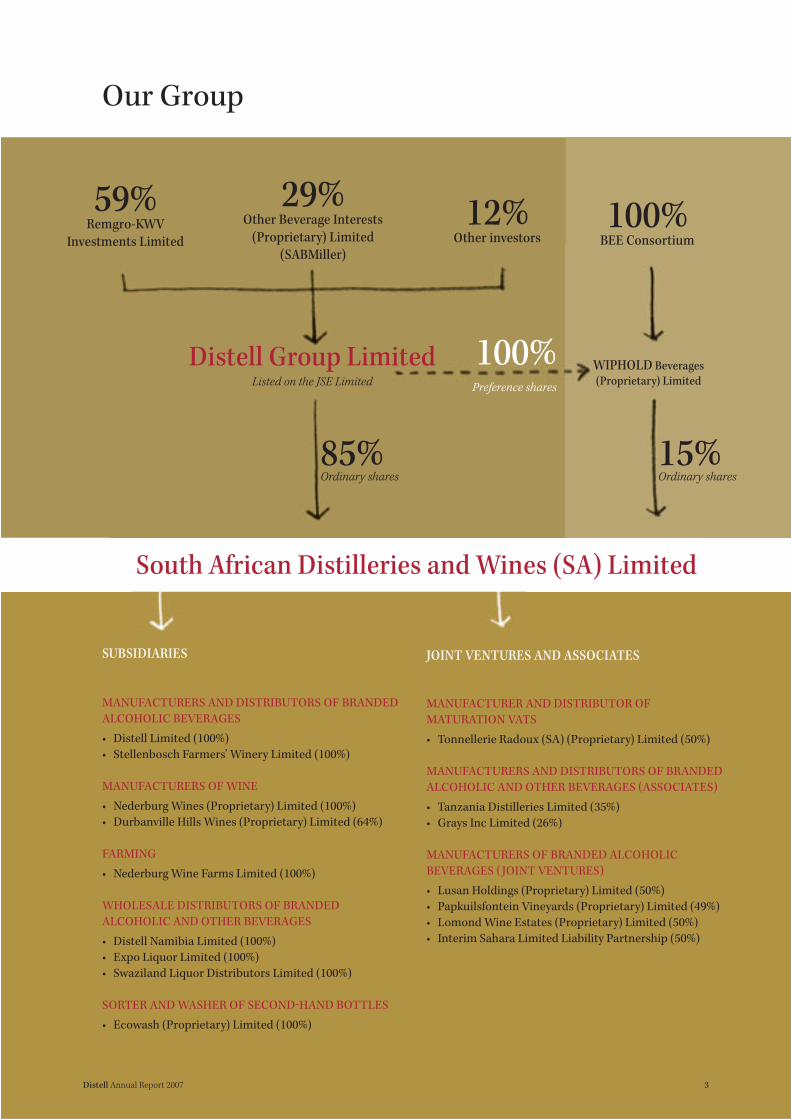

59% Remgro-KWV

Investments Limited

Distell Group Limited Listed on the JSE Limited

Our Group

29%Other Beverage Interests

(Proprietary) Limited

(SABMiller)

12%Other investors

85%Ordinary shares

South African Distilleries and Wines (SA) Limited

100%Preference shares

MANUFACTURERS AND DISTRIBUTORS OF BRANDED

ALCOHOLIC BEVERAGES

• Distell Limited (100%)

• Stellenbosch Farmers’ Winery Limited (100%)

MANUFACTURERS OF WINE

• Nederburg Wines (Proprietary) Limited (100%)

• Durbanville Hills Wines (Proprietary) Limited (64%)

FARMING

• Nederburg Wine Farms Limited (100%)

WHOLESALE DISTRIBUTORS OF BRANDED

ALCOHOLIC AND OTHER BEVERAGES

• Distell Namibia Limited (100%)

• Expo Liquor Limited (100%)

• Swaziland Liquor Distributors Limited (100%)

SORTER AND WASHER OF SECOND-HAND BOTTLES

• Ecowash (Proprietary) Limited (100%)

MANUFACTURER AND DISTRIBUTOR OF

MATURATION VATS

• Tonnellerie Radoux (SA) (Proprietary) Limited (50%)

MANUFACTURERS AND DISTRIBUTORS OF BRANDED

ALCOHOLIC AND OTHER BEVERAGES (ASSOCIATES)

• Tanzania Distilleries Limited (35%)

• Grays Inc Limited (26%)

MANUFACTURERS OF BRANDED ALCOHOLIC

BEVERAGES ( JOINT VENTURES)

• Lusan Holdings (Proprietary) Limited (50%)

• Papkuilsfontein Vineyards (Proprietary) Limited (49%)

• Lomond Wine Estates (Proprietary) Limited (50%)

• Interim Sahara Limited Liability Partnership (50%)

JOINT VENTURES AND ASSOCIATESSUBSIDIARIES

100%BEE Consortium

WIPHOLD Beverages

(Proprietary) Limited

15%Ordinary shares

3Distell Annual Report 2007

4 Distell Annual Report 2007

Annual highlights

Financial results (R’000) % change 2007 2006

Revenue 18,4 7 954 602 6 717 210

Trading income 25,3 1 114 733 889 395

Headline earnings 45,4 779 294 535 970

Adjusted headline earnings 29,2 779 294 603 211

Total assets 9,5 5 997 095 5 475 078

Share performance (cents) % change 2007 2006

Headline earnings 44,2 391,5 271,5

Adjusted headline earnings 28,1 391,5 305,6

Dividends 28,1 196,0 153,0

Net asset value 18,4 1 972,7 1 666,6

Cash fl ow from operating activities 19,8 407,8 340,5

Closing share price 38,8 5 415,0 3 900,0

Financial statistics 2007 2006

Return on equity (excluding BEE* share-based payment) 19,8 16,2

Seven-year compound growth per annum (%) 2007 2006

Total return to shareholders 34,3 29,8

Distell share price index 29,8 25,2

* BEE: black economic empowerment

Headline earnings per share

Salient features

Total revenue

Dividend per share

Total sales volumes

Trading income

Headline earnings per share, excluding non-recurring BEE expense in the previous year,

5Distell Annual Report 2007

How we’ve measured up

Objectives

Strategic priorities

• Growing Amarula’s position globally

• Building on our position as a profi table

and leading South African wine exporter

• Consolidating our position as a

domestic market leader

• Expanding our global footprint through

exploring new markets, and increasing our

focus on our operations in Africa

• Continuing on our path as a

responsible corporate citizen

• Creating shareholder value

• Accelerating transformation

A sense of ownership

Each and every one of us will be

aware of our contribution.

Performance-driven culture

We will challenge each other to ensure

continuous improvement by creating

more, better and faster.

What we stand for (our values)

Respect for the individual

We will respect each other’s diversity

and contribute to the communities

in which we live. We will promote the

responsible use of alcohol.

Entrepreneurial spirit

We will give each other the freedom

to explore and create.

Customer service orientation

We will delight our customers and

consumers everywhere.

6 Distell Annual Report 2007

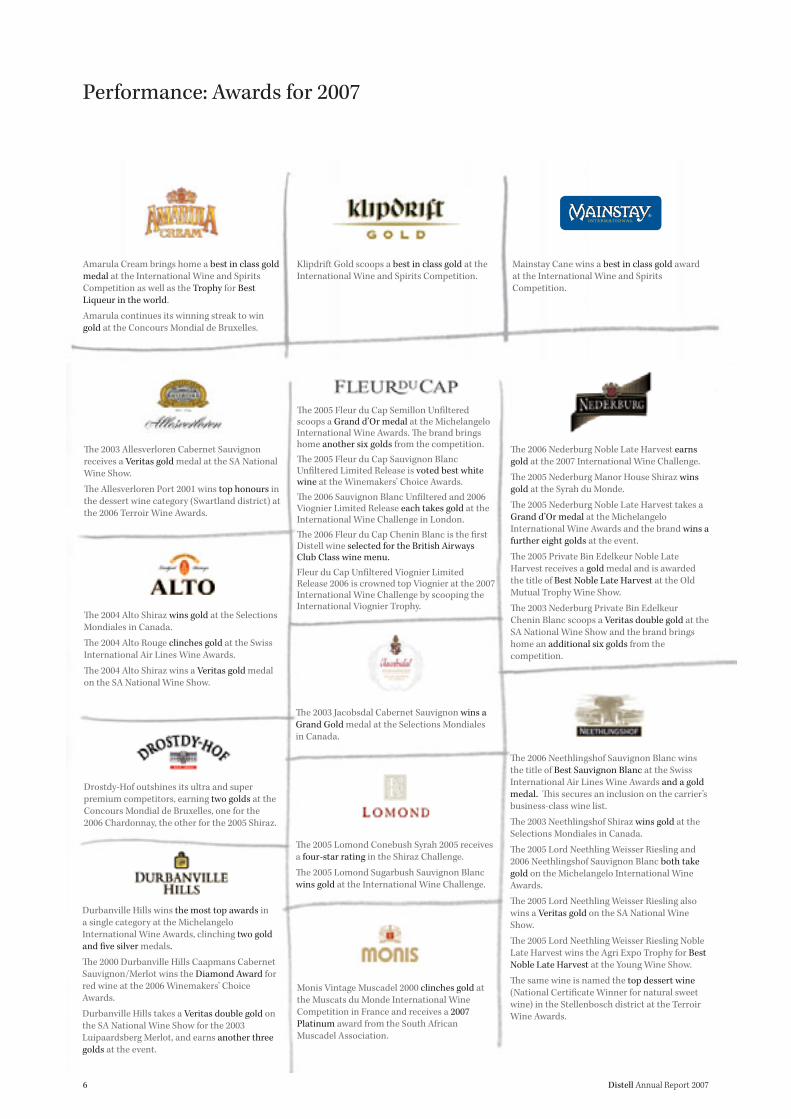

Performance: Awards for 2007

Th e 2003 Jacobsdal Cabernet Sauvignon wins a Grand Gold medal at the Selections Mondiales in Canada.

Th e 2005 Lomond Conebush Syrah 2005 receives a four-star rating in the Shiraz Challenge.

Th e 2005 Lomond Sugarbush Sauvignon Blanc wins gold at the International Wine Challenge.

Monis Vintage Muscadel 2000 clinches gold at the Muscats du Monde International Wine Competition in France and receives a 2007 Platinum award from the South African Muscadel Association.

Th e 2006 Nederburg Noble Late Harvest earns gold at the 2007 International Wine Challenge.

Th e 2005 Nederburg Manor House Shiraz wins gold at the Syrah du Monde.

Th e 2005 Nederburg Noble Late Harvest takes a Grand d’Or medal at the Michelangelo International Wine Awards and the brand wins a further eight golds at the event.

Th e 2005 Private Bin Edelkeur Noble Late Harvest receives a gold medal and is awarded the title of Best Noble Late Harvest at the Old Mutual Trophy Wine Show.

Th e 2003 Nederburg Private Bin Edelkeur Chenin Blanc scoops a Veritas double gold at the SA National Wine Show and the brand brings home an additional six golds from the competition.

Th e 2006 Neethlingshof Sauvignon Blanc wins the title of Best Sauvignon Blanc at the Swiss International Air Lines Wine Awards and a gold medal. Th is secures an inclusion on the carrier’s business-class wine list.

Th e 2003 Neethlingshof Shiraz wins gold at the Selections Mondiales in Canada.

Th e 2005 Lord Neethling Weisser Riesling and 2006 Neethlingshof Sauvignon Blanc both take gold on the Michelangelo International Wine Awards.

Th e 2005 Lord Neethling Weisser Riesling also wins a Veritas gold on the SA National Wine Show.

Th e 2005 Lord Neethling Weisser Riesling Noble Late Harvest wins the Agri Expo Trophy for Best Noble Late Harvest at the Young Wine Show.

Th e same wine is named the top dessert wine (National Certifi cate Winner for natural sweet wine) in the Stellenbosch district at the Terroir Wine Awards.

Th e 2003 Allesverloren Cabernet Sauvignon receives a Veritas gold medal at the SA National Wine Show.

Th e Allesverloren Port 2001 wins top honours in the dessert wine category (Swartland district) at the 2006 Terroir Wine Awards.

Th e 2004 Alto Shiraz wins gold at the Selections Mondiales in Canada.

Th e 2004 Alto Rouge clinches gold at the Swiss International Air Lines Wine Awards.

Th e 2004 Alto Shiraz wins a Veritas gold medal on the SA National Wine Show.

Th e 2005 Fleur du Cap Semillon Unfi ltered scoops a Grand d’Or medal at the Michelangelo International Wine Awards. Th e brand brings home another six golds from the competition.

Th e 2005 Fleur du Cap Sauvignon Blanc Unfi ltered Limited Release is voted best white wine at the Winemakers’ Choice Awards.

Th e 2006 Sauvignon Blanc Unfi ltered and 2006 Viognier Limited Release each takes gold at the International Wine Challenge in London.

Th e 2006 Fleur du Cap Chenin Blanc is the fi rst Distell wine selected for the British Airways Club Class wine menu.

Fleur du Cap Unfi ltered Viognier Limited Release 2006 is crowned top Viognier at the 2007 International Wine Challenge by scooping the International Viognier Trophy.

Drostdy-Hof outshines its ultra and super premium competitors, earning two golds at the Concours Mondial de Bruxelles, one for the 2006 Chardonnay, the other for the 2005 Shiraz.

Durbanville Hills wins the most top awards in a single category at the Michelangelo International Wine Awards, clinching two gold and fi ve silver medals.

Th e 2000 Durbanville Hills Caapmans Cabernet Sauvignon/Merlot wins the Diamond Award for red wine at the 2006 Winemakers’ Choice Awards.

Durbanville Hills takes a Veritas double gold on the SA National Wine Show for the 2003 Luipaardsberg Merlot, and earns another three golds at the event.

Amarula Cream brings home a best in class gold medal at the International Wine and Spirits Competition as well as the Trophy for Best Liqueur in the world.

Amarula continues its winning streak to win gold at the Concours Mondial de Bruxelles.

Klipdrift Gold scoops a best in class gold at the International Wine and Spirits Competition.

Mainstay Cane wins a best in class gold award at the International Wine and Spirits Competition.

7Distell Annual Report 2007

Plaisir de Merle stands out at the Swiss International Air Lines Wine Awards, where the 2006 Chardonnay is judged both the top white wine on the show, and the best Chardonnay. Th ey also clinch an overall gold medal for the vintage. Th e wine is chosen by the carrier to serve to fi rst-class passengers.

Th e Pongracz Magnum and Desiderius 2001 both win Veritas gold at the SA National Wine Show.

Desiderius 2001 is crowned top South African sparkling wine at the WINE Magazine Amorim Cork Cap Classique Challenge.

Th e 2001 Stellenzicht Syrah wins a gold medal at the inaugural Syrah du Monde and outclasses all the other South African producers as the only local contestant amongst the competition’s ten best wines.

Th e 2001 Syrah also earns gold at the Selections Mondiales in Canada.

Stellenzicht’s 2002 Syrah and 2005 Golden Triangle Pinotage both bring home gold from the Swiss International Air Lines Wine Awards.

Th e 2003 Golden Triangle Shiraz is selected for SAA’s fi rst and business-class wine lists on board intercontinental fl ights.

Stellenzicht wins a Veritas gold at the SA National Wine Show with the Golden Triangle Cabernet Sauvignon 2001.

Th e 2005 Pinotage Golden Triangle is included on the Absa Top 10 Pinotage list.

Th e 2004 Tukulu Pinotage is selected for the Absa Top Ten Pinotage line-up, a fourth such inclusion for Tukulu.

Th e 2005 Tukulu Chenin Blanc is named top white wine (Swartland district) at the 2006 Terroir Awards.

Th e Uitkyk Reserve Sauvignon Blanc 2005 is named the top Sauvignon Blanc in the Stellenbosch district and top white wine (Simonsberg-Stellenbosch ward) at the Terroir Wine Awards.

Oude Meester earns two golds at the Concours Mondial de Bruxelles, one for the 12 Year Old Reserve and the other for the Peppermint Liqueur.

Th e Ginger Liqueur wins a best in class gold medal at the International Wine and Spirits Competition.

Oude Meester Reserve also clinches a gold at the International Spirits Challenge.

Th e Th ree Ships 10 Year Old Single Malt Whisky achieves a best in class gold award at the International Wine and Spirits Competition.

Th ree Ships 5 Year Old Whisky wins gold at the Concours Mondial de Bruxelles.

Van Ryn’s 10 Year Old wins a best in class gold medal at the International Wine and Spirits Competition.

Van Ryn’s Collection Reserve 12 Year Old and 10 Year Old vintages scoop gold at the Concours Mondial de Bruxelles.

Van Ryn’s 10 Year Old continues to win best in class gold at the International Spirits Challenge.

• ISO 9001:2000 certifi cation at all our distilleries,

wineries, secondary production sites, distribution

centres and brand homes in the Republic of South

Africa. Distell Namibia Windhoek and Walvis Bay

are also included in the ISO 9001:2000

certifi cation. Distell’s ISO 9001:2000 certifi cation,

which is valid until November 2008, includes the

corporate functions quality management and

research, group purchasing, logistics, technical

services, export logistics and group human

resource management.

• Hazard Analysis and Critical Control Points

(HACCP) certifi cation at the majority of our

wineries and secondary production sites.

Accreditation and certifi cation as at 30 June 2007

Worcester Distillery is the fi rst distillery to be

listed for HACCP.

• ISO 17025 accreditation of Distell’s central

laboratory at Adam Tas cellar.

• International Food Standards higher-level

certifi cation at Adam Tas.

• British Retail Consortium (BRC) food safety

certifi cation of Adam Tas, Bergkelder, J.C. Le Roux

and Nederburg wineries, Durbanville Hills, Paarl

and Green Park. During this fi nancial year BRC

certifi cation was given to Plaisir de Merle, while all

the sites previously certifi ed retained their status.

• ISO 14001:2004 certifi cation of Durbanville Hills

and Nederburg. Plaisir de Merle and Bergkelder

have been assessed and recommended for listing.

• Integrated Production of Wine certifi cation of all

Distell and Lusan farms and the winemaking

cellars.

• Wine and Agricultural Ethical Trade Association

certifi cation of Worcester/Robertson, Goudini,

Wellington and Van Ryn Distilleries.

• Organic certifi cation for certain vineyards at

Papkuilsfontein and Plaisir de Merle. Nederburg

cellar has been certifi ed to produce organic wines.

Mellow-Wood 5 Year old wins a gold medal at the International Spirits Challenge.

8 Distell Annual Report 2007

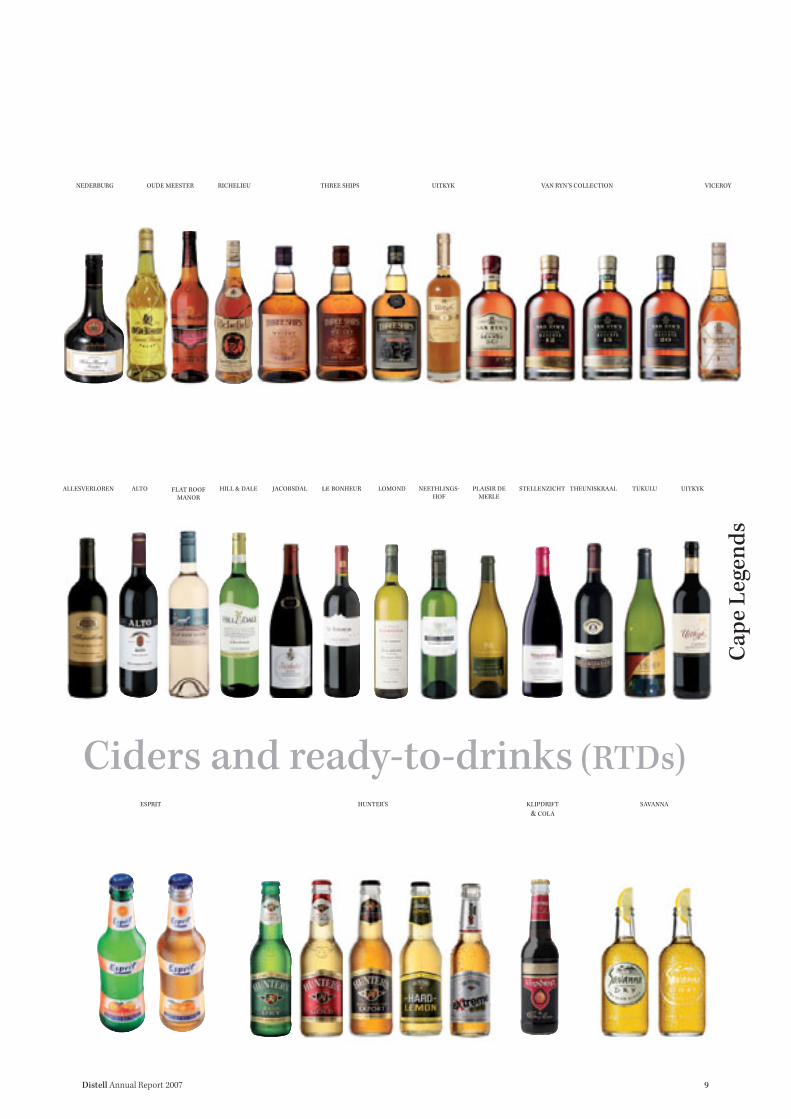

Our brands at a glance

Spirits

Wines

Do

mes

tic

Inte

rna

tio

na

l

AMARULA COUNT PUSHKIN

COLLISON’SWHITE GOLD

MAINSTAYCOMMANDO MELLOW-WOODKLIPDRIFTFLIGHT OF THEFISH EAGLE

AUTUMN HARVEST

CELLAR CASK

CHATEAU LIBERTAS

GRAÇA GRÜNBERGER J.C. LE ROUX SEDGWICK’S OLD

BROWN SHERRY

PAARL PERLÉ PONGRÁCZ TASSENBERG ZONNEBLOEM

DROSTDY-HOF DURBANVILLE HILLS

FLEUR DU CAP NEDERBURG OBIKWA TWO OCEANS

9Distell Annual Report 2007

Ciders and ready-to-drinks (RTDs)C

ap

e L

egen

ds

HILL & DALE le BONHEUR LOMOND TUKULUNEETHLINGS-HOF

PLAISIR DE MERLE

STELLENZICHT UITKYKALTOALLESVERLOREN THEUNISKRAALJACOBSDALFLAT ROOF MANOR

ESPRIT SAVANNAHUNTER’S KLIPDRIFT

& COLA

OUDE MEESTER RICHELIEU VAN RYN’S COLLECTION VICEROYTHREE SHIPSNEDERBURG UITKYK

Our global presence

Year-on-year growth

Trend Amarula Wine

Volume +31% +17%

Value +67% +30%

% of total exports 4% 3%Asia Pacifi c

Trend Amarula Wine

Volume +20% +1%

Value +54% +27%

% of total exports 25% 40%Europe

Trend Amarula Wine

Volume +34% +14%

Value +45% +21%

% of total exports 28% 46%

Trend Amarula Wine

Volume +12% +12%

Value +29% +29%

% of total exports 20% 9%North America

Africa (including BLNS*)

Trend Amarula Wine

Volume +52% +23%

Value +69% +27%

% of total exports 20% 1%Latin America

Trend

Volume Value

% of total export volumes

Total exports

* BLNS: Botswana, Lesotho, Namibia and Swaziland

10 Distell Annual Report 2007

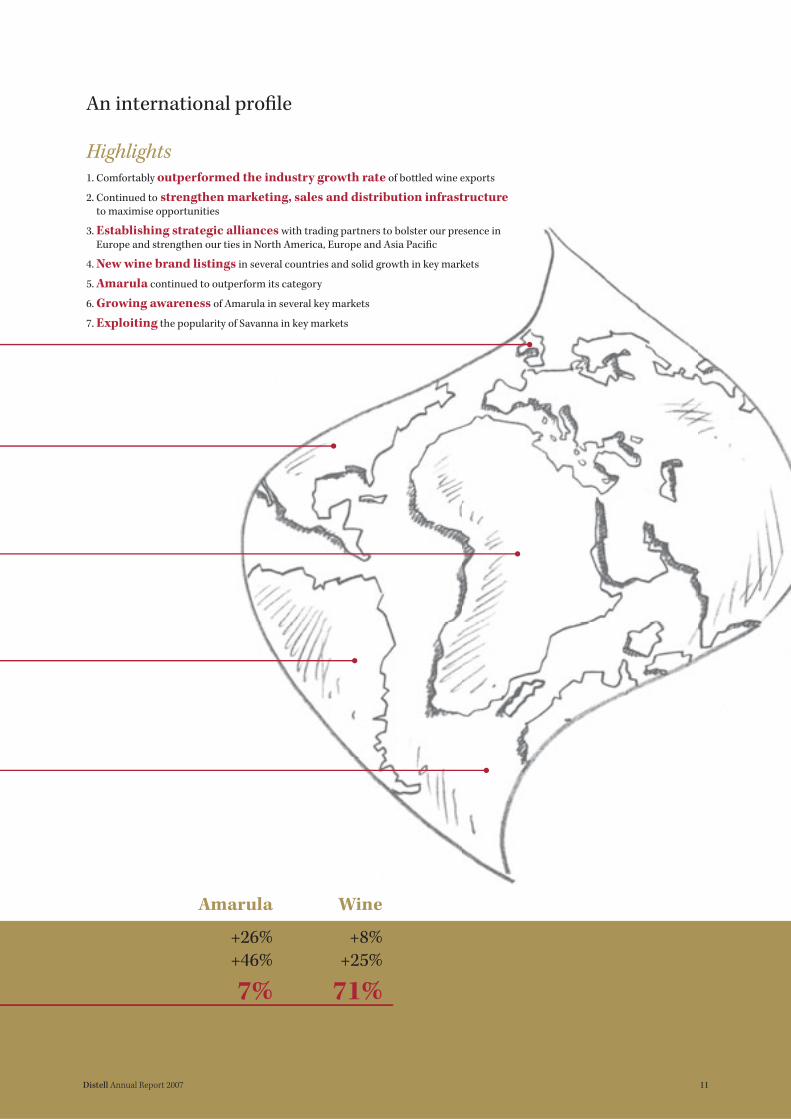

Highlights1. Comfortably outperformed the industry growth rate of bottled wine exports

2. Continued to strengthen marketing, sales and distribution infrastructure to maximise opportunities

3. Establishing strategic alliances with trading partners to bolster our presence in Europe and strengthen our ties in North America, Europe and Asia Pacifi c

4. New wine brand listings in several countries and solid growth in key markets

5. Amarula continued to outperform its category

6. Growing awareness of Amarula in several key markets

7. Exploiting the popularity of Savanna in key markets

An international profi le

Amarula Wine

+26% +8%+46% +25%

7% 71%

11Distell Annual Report 2007

12 Distell Annual Report 2007

Board matters

Board of directors

Duimpie Bayly*

Director of Duimpie Bayly & Associates,

technical consultant and adviser to the

wine industry. Attended 6 of 6 board

meetings.

Peter Bester*

Director of Agrinet, Dorbyl and South

African Property Opportunities Plc,

amongst others. He was formerly executive

chairperson of Cadbury Schweppes (SA)

until retiring in 2001. Attended 6 of 6

board meetings and 3 of 3 remuneration

committee meetings.

Piet Beyers

Director of Remgro and Unilever Bestfoods

Robertsons (Holdings) LLC. Attended 6

of 6 board meetings.

Merwe Botha#

Financial director

Attended 6 of 6 board meetings.

Johan Carinus*

Wine farmer and director of Het Jan

Marais Fund and Zeder Investments.

Attended 6 of 6 board meetings.

Smartie Genade#

Business director: Wines

Attended 6 of 6 board meetings.

Jakes Gerwel*

Chancellor of Rhodes University, non-

executive director of Naspers and Old

Mutual, non-executive chairperson of

Brimstone Investment Corporation,

Africon Engineering International, Life

Healthcare, Media 24 and South African

Airways. He chairs the boards of trustees

of the Nelson Mandela Foundation, the

Mandela Rhodes Foundation and the

Human Sciences Research Council,

amongst others and is vice chairperson of

the Peace Parks Foundation. Attended 2

of 6 board meetings.

Dr Edwin de la H Hertzog

Chairperson of Medi-Clinic Corporation,

non-executive deputy chairperson of

Remgro, non-executive director of Total

(SA) and Trans Hex Group as well as

Chair of Council, Stellenbosch University.

Attended 6 of 6 board meetings.

Robert Lumb*

Independent non-executive director of

New Clicks Holdings, Metje & Ziegler and

HomeChoice Holdings. He was formerly

managing partner, Western Cape, of Ernst

& Young. Attended 3 of 4 board meetings

and 2 of 2 audit committee meetings since

joining the board on 19 October 2006.

Joe Madungandaba*

Chief executive offi cer of Community

Investment Holdings. Executive director

of Jasco Electronic Holdings and

non-executive director of Air Liquide

Healthcare. Attended 3 of 6 board

meetings.

Louisa Mojela*

A founder and group chief executive offi cer

of Women Investment Portfolio Holdings

(WIPHOLD). Serves on the boards of Sun

International, ABB SA, South African

Airways and the Financial Services

Board, amongst others. Attended 5 of 6

board meetings and 3 of 3 remuneration

committee meetings.

Gugu Mthethwa*

Investment executive at WIPHOLD and

non-executive board member of ABB SA,

MCG Industries and Landis+Gyr. Attended

6 of 6 board meetings and 4 of 4 audit

committee meetings.

David Nurek*

Regional chairperson of Investec Western

Cape, chairperson of New Clicks Holdings

and Lewis Group, deputy chairperson

of Foschini and, amongst others, also a

director of Pick ’n Pay, Aspen Pharmacare,

Sun International and Trencor. Attended

6 of 6 board meetings, 4 of 4 audit

committee meetings and 3 of 3

remuneration committee meetings.

Jan Scannell#

Managing director

Attended 6 of 6 board meetings.

Peter Swartz*

Proprietor of Swartz Properties and

Southern Pumps and also a director

of Absa Group, Absa Bank and Sun

International. Attended 6 of 6 board

meetings and 3 of 3 remuneration

committee meetings.

Th ys Visser

Chief executive offi cer of Remgro and also

a director of Rainbow Chicken, Nampak,

British American Tobacco Plc, Medi-

Clinic Corporation, Unilever Bestfoods

Robertsons (Holdings) LLC. Attended 5

of 6 board meetings, 3 of 4 audit

committee meetings and 2 of 3

remuneration committee meetings.

* Independent

# Executive

13Distell Annual Report 2007

Jan Scannell (56)

Managing director

BCom, LLB

Jan joined Distillers Corporation in 1979.

He was appointed a director in 1988, and

managing director in 1994. In December

2000, he was appointed managing director

of Distell. Jan’s role is to ensure the

company delivers on its key objectives. He

is also responsible for building a high-

performance culture within the company.

Merwe Botha (54)

Financial director

BCom Hons (Taxation), BCompt Hons,

CA(SA)

Merwe joined Distillers Corporation

in 1980. He was appointed fi nancial

director in 1997 and to his present

position at Distell in December 2000. He

is responsible for fi nancial planning and

control, information technology, statutory

reporting and internal auditing.

Stoff el Cronjé (53)

Company secretary and corporate

development director

MA

Stoff el joined Distillers Corporation in

1980. He was appointed group company

secretary and human resources director

in 1990 and to his present position at

Distell in December 2000. He performs all

statutory company secretarial functions

and is also responsible for the company’s

human resources, legal, corporate aff airs

and corporate strategy planning divisions.

Don Gallow (49)

International director

Don joined Distillers Corporation in 1986.

He was appointed Distell’s international

director in 2005 and is responsible for

growing our international revenue by

providing superior service to existing

customers and obtaining new listings.

Smartie Genade (56)

Business director: Wines

BCom (Hons), MBA

Smartie joined Stellenbosch Farmers’

Winery in1972, was appointed director

of the company in 1988 and managing

director in 2000. He was appointed

operations director at Distell in December

2000, assuming his present position in

2004. He is responsible for the profi tability

and sustainability of Distell’s wine

interests.

Hennie Heÿl (61)

Primary production director

MSc Agric

Hennie joined Distillers Corporation in

1974, was appointed technical director

in 1988 and production director in 1997.

He took up his present position at Distell

in December 2000. He is responsible for

our farms; grape, wine, brandy and other

raw material procurement; distillation,

winemaking and blending.

Gert Loubser (59)

Quality management and research director

MSc, PhD

Gert joined Stellenbosch Farmers’ Winery

in 1974, was appointed research and

development director in 1994 and to his

present position at Distell in December

2000. His role is to ensure total quality

management is implemented throughout

the Group and that ongoing research leads

to new products and processes.

Nantha Moodley (48)

Business director: Ciders and RTDs

BA, NDip

Nantha joined Stellenbosch Farmers’

Winery in 1989 and has over 15 years’

experience in sales, training and

distribution. He was appointed to his

current position in November 2004 and

is responsible for the profi tability and

sustainability of Distell’s business in the

cider and ready-to-drink (RTD) categories.

Malcolm Searle (47)

Marketing director

BCom (Hons)

Malcolm joined Distell as marketing

director in January 2004 with almost

20 years’ experience in fast-moving

consumer goods, working as a marketing

executive in several countries worldwide.

He is responsible for building strong brand

portfolios based on market strategies that

leverage consumer insights and drive

innovation.

Caroline Snyman (32)

Business director: Spirits

BEng (Chemical), MSc, PhD, CWM

Caroline joined Distell in January 2000

as technical manager: spirits and was

appointed to her current position in

November 2004. She is responsible for the

profi tability and sustainability of Distell’s

spirits interests.

Tim Tarr (49)

Sales director

Tim joined Distillers Corporation in 1979

and was appointed national sales director

in 1995. He took up his present position

at Distell in December 2000. His role is to

ensure we retain and improve our market

leadership in South Africa, Botswana,

Lesotho, Namibia and Swaziland and he

oversees all our sales forces operating in

these areas.

Valerio Toros (43)

Operations director

BEng (Mech), MBA

Valerio joined Distillers Corporation in

1991 as project engineer. After overseeing

the SFW/Distillers merger, he was made

group manager of business process

improvement (BPI), and then appointed

BPI director at the end of 2003. He took

up his present position in November

2004 and oversees the operations of the

Group, including packaging, distribution,

technical services, procurement and

supply chain management.

Executive management

14 Distell Annual Report 2007

Klipdrift, South Africa’s best-selling

brandy is synonymous with generosity and

hospitality. No matter where you are, open a bottle

of Klipdrift and make yourself at home.

15Distell Annual Report 2007

Seven-year fi nancial reviewfor the years ended 30 June

Balance sheets (R’000)AssetsNon-current assets

Property, plant and equipment 1 330 516 1 256 900 1 223 036 1 225 351 1 197 900 1 139 182 1 022 442

Biological assets 114 675 104 380 107 170 98 939 94 585 – –

Financial assets and

investments in associates 96 092 418 490 307 711 558 839 313 707 565 208 654 551

Intangible assets 34 060 11 211 14 501 – – – –

Retirement benefit assets 187 052 48 795 – – – – –

Deferred income tax assets 28 762 36 770 44 118 36 431 19 402 16 789 8 745

Total non-current assets 1 791 157 1 876 546 1 696 536 1 919 560 1 625 594 1 721 179 1 685 738

Current assets

Inventories 2 703 336 2 499 217 2 246 268 2 207 296 2 074 364 1 651 076 1 600 341

Trade and other receivables 809 024 617 097 552 542 513 414 529 192 581 978 477 079

Financial assets 361 152 254 640 309 249 – 324 106 195 452 –

Current income tax assets – – 51 636 33 230 31 864 29 741 25 403

Cash and cash equivalents 332 426 227 578 196 989 159 390 139 304 185 221 178 227

Total current assets 4 205 938 3 598 532 3 356 684 2 913 330 3 098 830 2 643 468 2 281 050

Total assets 6,7 5 997 095 5 475 078 5 053 220 4 832 890 4 724 424 4 364 647 3 966 788

Equity and liabilitiesTotal shareholders’ equity 3 940 680 3 316 048 2 894 248 2 572 091 2 363 184 2 127 516 2 039 812

Non-current liabilities

Interest-bearing borrowings 2 629 330 646 329 014 754 601 424 130 598 791 791 347

Retirement benefit obligations 12 842 12 191 21 391 16 905 15 297 15 297 15 592

Deferred income tax liabilities 164 033 120 647 110 646 101 127 105 128 80 959 47 275

Total non-current liabilities 179 504 463 484 461 051 872 633 544 555 695 047 854 214

Current liabilities

Trade payables and provisions 1 489 940 1 196 201 1 023 333 1 003 788 791 961 673 844 562 324

Interest-bearing borrowings 329 264 432 502 674 588 384 378 1 024 724 868 240 510 438

Current income tax liabilities 57 707 66 843 – – – – –

Total current liabilities 1 876 911 1 695 546 1 697 921 1 388 166 1 816 685 1 542 084 1 072 762

Total equity and liabilities 5 997 095 5 475 078 5 053 220 4 832 890 4 724 424 4 364 647 3 966 788

Note: The figures for 2001 to 2004 have not been adjusted, except for reclassifications, for the adoption of IFRS.

Seven-year

compound 2007 2006 2005 2004 2003 2002 2001

growth % p.a. IFRS IFRS IFRS SA GAAP SA GAAP SA GAAP SA GAAP

16 Distell Annual Report 2007

Seven-year fi nancial reviewfor the years ended 30 June

Income statements (R’000)Revenue 8,5 7 954 602 6 717 210 5 964 003 5 563 969 5 032 563 4 777 536 4 471 202

Operating expenses (6 839 869) (5 827 815) (5 241 696) (4 994 128) (4 579 560) (4 296 757) (4 129 073)

Trading income 15,9 1 114 733 889 395 722 307 569 841 453 003 480 779 342 129

Dividend income 1 284 1 497 1 210 949 922 1 776 618

Net financing costs 7 969 (27 363) (53 071) (95 702) (119 056) (89 440) (76 974)

Share of profit of associates 14 255 9 856 9 316 10 674 12 723 13 387 5 731

Profit before exceptional

items and taxation 19,7 1 138 241 873 385 679 762 485 762 347 592 406 502 271 504

Exceptional items 73 876 (67 241) – – 51 462 (73 175) (145 602)

Profit before taxation 1 212 117 806 144 679 762 485 762 399 054 333 327 125 902

Taxation (367 243) (271 756) (187 265) (124 790) (86 277) (96 575) (10 862)

Minority interest 2 979 – (844) (390) (315) (266) (283)

Net profit attributable to

equity holders 17,9 847 853 534 388 491 653 360 582 312 462 236 486 114 757

Cash fl ow statements (R’000)Cash generated from

operating activities 15,5 1 188 101 900 123 795 348 761 195 408 778 496 710 609 703

Dividend income 1 284 1 497 1 210 949 922 1 776 618

Net financing costs (23 179) (75 987) (101 685) (161 381) (214 228) (133 736) (152 181)

Taxation paid (365 380) (153 388) (219 980) (143 915) (91 015) (71 292) (50 600)

Dividends paid (342 729) (266 788) (209 948) (158 420) (146 685) (148 641) (104 670)

Cash retained from normal

operating activities 458 097 405 457 264 945 298 428 (42 228) 144 817 302 870

Exceptional items 11 006 – – 46 500 4 962 (73 175) (145 602)

Cash retained by operating

activities 469 103 405 457 264 945 344 928 (37 266) 71 642 157 268

Cash inflow from investment

activities 50 800 (164 364) (92 486) (19 265) 9 841 (229 628) (148 941)

Ordinary shares issued 11 542 18 406 8 406 5 708 – – –

Treasury shares sold 1 893 5 348 (7 981) (1 480) – – –

Minority interest 2 692 (1 417) – 70 (315) (266) (270)

Decrease in interest-bearing

borrowings (325 472) (101 638) (85 364) (984) 41 240 12 764 8 987

Cash outflow from

financing activities (309 345) (79 301) (84 939) 3 314 40 925 12 498 8 717

Increase in net cash and

cash equivalents 210 558 161 792 87 520 328 977 13 500 (145 488) 17 044

Seven-year

compound 2007 2006 2005 2004 2003 2002 2001

growth % p.a. IFRS IFRS IFRS SA GAAP SA GAAP SA GAAP SA GAAP

17Distell Annual Report 2007

Performance per share (cents)Earnings

attributable earnings basis 17,6 425,9 270,7 250,6 184,3 159,8 120,9 58,7

adjusted headline basis 18,9 391,5 305,6 250,6 183,3 130,1 110,4 106,1

cash equivalent basis 15,7 475,7 377,5 300,4 219,1 162,6 143,5 103,6

Dividends 17,9 197,0 153,0 123,0 97,0 75,0 70,0 53,0

Cash flow 20,2 407,8 340,5 242,1 257,3 55,9 112,6 133,9

Net asset value 10,2 1 972,7 1 666,6 1 466,6 1 309,9 1 208,3 1 087,8 1 043,0

Liquidity and solvencyFinancial gearing ratio 0,00 0,16 0,28 0,38 0,55 0,60 0,55

Total liabilities on total equity Avg 0,8 0,52 0,65 0,75 0,88 1,00 1,05 0,94

Interest-free liabilities on total assets 0,26 0,23 0,21 0,21 0,17 0,16 0,15

Dividend cover (times) 2,0 2,0 2,0 1,9 1,7 1,6 2,0

Current ratio 2,24 2,12 1,98 2,10 1,71 1,71 2,13

Acid test ratio 0,80 0,65 0,65 0,51 0,56 0,64 0,63

Returns (%)Trading income on turnover 14,0 13,2 12,1 10,2 9,0 10,1 7,7

Pretax return on equity Avg 19,5 30,8 24,3 23,5 18,9 16,9 15,7 6,2

Effective tax rate 30,3 33,7 27,5 25,7 21,6 29,0 8,6

Return on equity Avg 14,3 19,8 18,2 17,0 13,9 10,8 10,2 10,2

Attributable earnings on total assets 14,1 9,8 9,7 7,5 6,6 5,4 2,9

Attributable earnings on turnover 10,7 8,0 8,2 6,5 6,2 4,9 2,6

Dividend yield 4,2 4,5 5,8 6,8 5,8 6,9 6,7

ProductivityCash value added (R million) 12,9 3 743,1 3 090,8 2 601,1 2 314,7 1 794,6 1 704,6 1 727,4

Net asset turn (times) 2,0 2,0 2,1 2,2 2,2 2,3 2,3

Net assets per employee (R’000) 15,7 926,3 800,8 693,7 614,7 544,3 468,6 401,7

Revenue per employee (R’000) 13,6 1 869,9 1 622,1 1 429,5 1 329,8 1 159,0 1 052,3 880,5

Number of employees 4 254 4 141 4 172 4 184 4 342 4 540 5 078

Seven-year

compound 2007 2006 2005 2004 2003 2002 2001

growth % p.a. IFRS IFRS IFRS SA GAAP SA GAAP SA GAAP SA GAAP

18 Distell Annual Report 2007

Analysis of shareholdersat 30 June

Distribution of shareholders

Public shareholders 3 456 99,37 21 838 590 10,93

Non-public shareholders

Major beneficial shareholders 2 0,06 176 022 000 88,12

Directors, including those of subsidiaries, and their associates 19 0,54 1 746 840 0,87

The Distell Group Share Trust 1 0,03 152 074 0,08

3 478 100,00 199 759 504 100,00

Number of shares in issue 2007 2006

Total number of shares in issue 199 759 504 198 968 930

Shares purchased by The Distell Group Share Trust

and accounted for as treasury shares (152 074) (434 636)

199 607 430 198 534 294

Weighted number of shares 199 078 536 197 413 974

Major beneficial shareholders Number of % of

shares total

The following shareholders have a holding of greater than 5% of the issued shares of the company:

Remgro-KWV Investments Limited 117 348 000 58,74

Other Beverage Interests (Proprietary) Limited (SABMiller) 58 674 000 29,37

JSE Limited

2007 2006 2005 2004 2003 2002 2001

Price per share (cents)

highest during the year 5 500 4 000 2 600 1 725 1 500 1 500 1 000

lowest during the year 3 605 2 475 1 500 1 100 1 105 735 675

closing at year-end 5 415 3 900 2 600 1 500 1 201 1 350 730

weighted average 4 738 3 377 2 121 1 418 1 287 1 008 788

Price earnings ratio 13,8 14,4 10,4 8,1 7,5 11,2 12,4

JSE actuaries’ price index

at year-end (2000: 100 cents)

Distell Group Limited 622 448 299 172 138 155 84

Closing price/net asset value per share 2,7 2,3 1,8 1,1 1,0 1,2 0,7

Weighted average number of

shares in issue (’000) 199 079 197 414 196 194 195 626 195 580 195 580 195 580

Number of shares traded (’000) 6 575 4 692 5 099 3 533 2 784 6 263 3 647

Shares traded/shares in issue (%) 3,3 2,4 2,6 1,8 1,4 3,2 1,9

Value of shares traded (R’000) 311 556 158 440 108 145 50 114 35 833 63 124 28 722

Number of transactions 1 259 1 274 1 214 1 069 981 1 386 1 220

Number of shareholders 3 478 3 445 3 381 3 283 3 389 1 738 2 268

Market capitalisation (R million) 10 817 7 760 5 131 2 945 2 349 2 640 1 428

Net asset value/market capitalisation 0,36 0,43 0,56 0,87 1,01 0,81 1,43

Number of % Number of % of issued

Ordinary shares holders of holders shares shares

19Distell Annual Report 2007

Cash value added statementfor the years ended 30 June

GR OU P 2007 2006

R’000 R’000

Cash generated

Cash derived from sales 7 762 675 6 652 655

Net financing costs paid (23 179) (75 987)

Income from investments 1 284 1 497

Cash value generated 7 740 780 6 578 165

Cash payments to suppliers of materials and services (3 997 691) (3 487 335)

Cash value added/wealth created 3 743 089 3 090 830

Cash utilised to:

Pay excise duty to the State 1 757 671 1 510 664

Pay tax on income to the State 365 380 153 388

Remunerate employees for their services 808 206 754 533

Provide shareholders with a return on the use of their risk capital 342 729 266 788

Cash disbursed among stakeholders 3 273 986 2 685 373

Net cash retained from operating activities 469 103 405 457

Reconciliation with cash generated

Cash value added (above) 3 743 089 3 090 830

Less: Remuneration to employees for their services (808 206) (754 533)

Net financing costs paid 23 179 75 987

Payment of excise duty to the State (1 757 671) (1 510 664)

Cash generated from operating activities 1 200 391 901 620

State taxes

Excise duty 1 757 671 1 510 664

Tax on income 365 380 153 388

Value added tax 372 022 304 790

Employees’ tax deducted from remuneration 99 084 90 501

Regional Services Council levies and property taxes 17 009 22 753

Channelled through the Group 2 611 166 2 082 096

2007

State 65%Employees 25%

Other 10%

Employees 28%State 62%

2006Other 10%

20 Distell Annual Report 2007

Trading environmentDuring the year under review the

economy remained buoyant, given

positive consumer spending, an

encouraging momentum in fi xed

investments and stronger than expected

export growth. Th e anticipated slowdown

in consumer spending did not materialise

despite several interest rate hikes.

Investor confi dence, in particular,

was boosted by Government’s stated

commitment, as it prepares for the 2010

FIFA World Cup, to tackle crime with

integrated strategies that address root

causes, as well as ineffi ciencies in the

policing and justice systems.

Th e country’s economic upswing,

however, has been led largely by

consumer spending, much of it on credit.

A voracious consumer appetite not only

adds to infl ationary pressures and the

risk of still further interest rate increases

but has also pushed household debt to

record highs. Such high levels of spending

will likely temper to some degree, as the

impact of the National Credit Act comes

into eff ect, petrol prices continue to rise

and further interest rate hikes are

anticipated.

Nevertheless, the positive impact of

greater domestic affl uence is marked.

South Africa’s black diamonds, as the

upwardly mobile black middle class are

now being named, pumped an extra

R60 billion into the economy in the last

year, according to the University of Cape

Town Unilever Institute of Research.

Estimated to have an annual spending

power of R180 billion, they represent a

relatively small percentage of black

consumers, but have a signifi cantly larger

proportion of black buying power.

Although the study has been criticised for

using too liberal a defi nition of the term

middle class, to include relatively low-

wage earners as well as students, there

can be no denying that greater access to

education, as well as to job opportunities

and career advancement, has contributed

to the growth in spending, creating a

climate in which strong brands can

fl ourish.

While extensive fi xed investment

spending across many sectors has

accelerated job creation, the high rates of

unemployment continue, impacting on

both economic and social stability. It is

also cause for concern that potential

development, which could further curb

joblessness, is being impeded by a

collapse in infrastructure. Water and

electricity supply, roads and other

utilities are buckling under the strain of

increased demand. Government and local

authorities need to step in and provide

the necessary resources and skills, not

only to sustain much-needed growth, but

to improve South Africa’s global

competitiveness.

We note the slip in our ratings with the

World Economic Forum. South Africa

now ranks 46th of 125 countries in terms

of global competitiveness, compared with

40th place of 117 countries in 2005.

Overstretched infrastructure, along with

the costs to business of crime and

violence, a shortage of skills and

infl exible labour policies, has contributed

to the lower rating.

Th ese drawbacks notwithstanding, we

see great opportunities for South African

companies keen to operate on a broad

geographic front. South Africans are

recognised for their entrepreneurship

and good business practices. All over the

world, there are organisations willing to

partner local operations and Distell is no

exception. We recently entered into

distribution agreements with major

players on European wine markets. We

have also established a joint venture with

Burn Stewart Distillers, a Scotch whisky

producer and brand owner with a

portfolio of leading whisky brands.

Relationships such as these allow us to

exploit opportunities and extend our

global reach, and we shall continue to

investigate options for international

relationships and investment, in the

process building on what has already

been exciting export growth.

Ciders, made from the juice derived from

apples, are now the fastest growing

alcoholic beverage worldwide. Distell, as

one of the world’s largest producers of

ciders, is well-placed to capitalise on this

trend, domestically, on the African

continent, and further afi eld, as you will

read in the managing director’s report,

which follows.

In recent months, there have been reports

about a crisis in our wine industry. Th at

there is a global oversupply, now in its

fourth year, is not in dispute. Nor is it

disputed that some farmers are under

fi nancial pressure as a result. However, it

is our view that the wine industry

remains viable, with a potentially

encouraging long-term future. Research

undertaken by the international Wine &

Spirits Record, on behalf of Vinexpo,

points to ongoing growth in international

wine consumption and there is reason to

expect that South African producers will

continue to participate in this growth,

provided their off erings are consistent

with market demand.

Nevertheless, we believe the industry

would be in a far healthier state and

generating far more jobs if there were

access to Government funding for market

research, development and promotional

activity, as is provided in countries such

as Australia and New Zealand, for

example.

“ . . . we see great opportunities for South African

companies keen to operate on a broad geographic front”

Chairman’s statement

21Distell Annual Report 2007

A large portion of the global market is

concentrated in the premium sector and

that is where much future growth has

been identifi ed. However, if South Africa

is to compete eff ectively in this sector, we

shall have to plan and produce our wines

cost effi ciently and support our brands

with long-term investment and

strategies. Winegrowers should also seek

to align themselves with viable brands.

To maximise success, however, calls for a

collective eff ort to market Brand South

Africa, our single biggest asset, so our

individual brands can follow in its

slipstream.

Distell’s policy is to protect its brands

and, tempting as it may be in the short

term, not to chase volume at the expense

of profi tability. We employ over

4 200 people. Th ere are also some

44 000 hectares under cultivation for

Distell wine brands, representing many

suppliers, their workers and their

families. Protecting our brands is also a

way of protecting them. By building

sustainable brands, we are assuring them

of a continuous uptake of production,

even in times of oversupply.

LegislationTh e progress of provincial liquor

legislation has been slow but now appears

to be gaining at least some momentum.

We believe that once legislation is in

place nationwide, it will be far easier to

promote the responsible consumption of

alcohol, as well as monitor and address

transgressions. While ad hoc

interventions can contain on-trade abuse

to a limited extent, a formalised

infrastructure will make for far greater

effi ciencies in this regard. Most

important, however, is to recognise that

unless legislation in all provinces refl ects

the needs of the communities and

consumers it intends to serve, it will be

unrealistic to expect widespread

compliance.

We also call on Government to address

the continued illicit trading and

smuggling of alcoholic beverages that

pose a threat not only to our industry but

also to the domestic excise regime. Th e

National Treasury has also voiced its

concerns and is in consultation with the

industry as well as the South African

Revenue Service. We look forward to the

outcome of these discussions in curbing

illegal liquor production and distribution.

Superbly matured since 1845, Viceroy’s success has increased

throughout Africa with it becoming one of the best-selling

premium brandies in Kenya.

22 Distell Annual Report 2007

Chairman’s statement (continued)

Th e release earlier this year of the

Department of Trade and Industry’s Code

of Good Practice meant the drafting of

the Liquor Manufacturers’ and

Distributors’ Industry Charter could be

brought closer to completion and we look

forward to its conclusion. We also await

the response of the Minister of

Agriculture to the Wine Industry

Transformation Charter submitted at the

end of July.

TransformationTh e establishment of the South African

Wine Industry Council has been an

extremely important development in

underpinning transformation. It has been

structured to allow for greater

representativity and improved

collaboration between the major players

in the industry. Its success will require

unity of purpose amongst all players, who

will have to overlook sectoral interests for

the greater good of the industry. Without

a cohesive industry, we cannot expect

progress to continue unimpeded, nor can

we expect to make the much-needed

advance in developing our domestic wine

market.

Excise duties on wines and spiritsAn understanding has been reached with

the National Treasury regarding the basis

on which average retail prices should be

calculated. We hope this will lead to a fair

and consistent excise dispensation for all

alcoholic beverages.

Drinking responsiblyDistell fully supports existing legislation

in respect of under-age consumption, as

well as of driving under the infl uence of

alcohol. Abuse of alcohol across the

spectrum and under-age drinking are, in

our view, best addressed through closely

targeted and holistic measures adopted

by the industry as a whole. To this end, we

have taken an active role in the Industry

Association for the Responsible Use of

Alcohol (ARA) of which we are a leading

corporate member, with Distell’s head of

regulatory aff airs, Michael Mokhoro,

currently serving as chairman. Our belief

is that working as a unifi ed force in co-

operation with Government in developing

educational, early identifi cation and

interventionist measures that target the

vulnerable and marginalised, provides

the strongest, most eff ective and cost-

effi cient basis for combating excessive,

harmful and inappropriate consumption.

Th e Liquor Manufacturers’ and

Distributors’ Industry Charter, in its

current form, accepts that membership of

ARA is ample demonstration of

commitment to combat abuse and should

further strengthen the very positive

contribution made by the organisation.

We also express our thanks to former

ARA director, Chan Makan, for the

laudable and very successful initiatives

he has developed and implemented, and

we welcome his successor, Adrian Botha,

who formerly served on ARA’s

management committee. His extensive

background and experience make him

ideally suited to the task.

ProspectsWe expect the present tempo of consumer

spending to moderate to some degree.

Even a slight downward adjustment in

disposable income should see well-

marketed brands as the best positioned

to build loyalty and attract newcomers.

Our task will be to further strengthen our

market visibility and our existing

relationships with retail and on-

consumption channels, as well as with

consumers locally and globally, ensuring

ever better quality and service.

AcknowledgementsWe have set and to a large extent met

demanding standards across every facet

of the business, all the while maintaining

stringent fi nancial disciplines. Our aim is

to delight our customers and consumers

wherever we trade and to maintain the

highest quality in every one of the

functions we perform. We strive to be a

worthy employer and a responsible

corporate citizen, mindful of the impact

we make at an economic, social and

environmental level.

We have not only weathered a diffi cult

wine market locally and abroad but we

have also played a key role in advancing

the domestic popularity of brandy, still

South Africa’s favourite spirit. We have

established a global platform for

Amarula, internationally the most widely

known South African consumer product.

We have introduced many product

innovations and we have set the

benchmark for the local cider industry.

We have been acknowledged on local and

international showcases for our products

across the portfolio and we have

extended our international footprint,

despite the ferocity of the competition.

We have also managed to participate

actively in technical forums worldwide in

pursuit of ever better quality systems and

products.

None of these activities or successes

would have been possible without the

shared goals, dedication and support at

every level of the business from

co-directors, management, staff and

suppliers. I thank each one of you

personally and look forward to your

continued commitment.

We also thank Daan Prins, who has

resigned from the board, for his

contributions and insights over the

years, and we welcome Robert Lumb.

DM Nurek

Chairman

Stellenbosch

22 August 2007

23Distell Annual Report 2007

Savanna, one of the country’s most popular dry cider

brands, embraces the attitude of a new South Africa with

its off -the-wall dry humour. Th is trendy brand’s popularity

is now spreading to international shores where, amongst

others, it is sold at leading supermarket

chains in the United Kingdom.

24 Distell Annual Report 2007

Th e domestic marketSouth Africa’s economic climate has

generally been favourable, with gross

domestic product (GDP) growing at 5%.

Business and consumer confi dence

remained high during the period under

review, fuelled by accelerated economic

growth in the fi nal quarter of 2006 and

ever-increasing employment levels.

Rising infl ation and interest rates did

little to curb cash or credit spending

amongst consumers.

Th e alcoholic beverage sector continued

to benefi t from ongoing premiumisation

for the third consecutive year. Th is trend

of trading up to distinctively packaged

alcoholic beverages that denote a sense of

luxury has in large part been driven by

the black diamond phenomenon,

described in the chairman’s statement.

Newly affl uent black middle class

consumers have grown dramatically in

number and spending power.

Growth in the alcoholic beverage sector

was driven mostly by premium priced

beer, whisky and ready-to-drink (RTD)

beverages.

In the case of our own portfolio, a further

increase in market investment and a

continuation of our relentless pursuit of

quality at intrinsic and packaging levels,

supported by compelling advertising

campaigns, resulted in greater consumer

support across all product categories.

Performance highlights in our spirits

segment included the sustained growth

of Klipdrift and Richelieu brandies.

Exclusive brands such as the Van Ryn’s

Collection Reserve range of potstill

brandies, Klipdrift Gold and Oude

Meester 12 Year Old also benefi ted from

ongoing premiumisation.

Amarula Cream had another excellent

year, further entrenching its position as

the category leader. On the wine front,

Durbanville Hills and Two Oceans

experienced sound growth, the latter

benefi ting from the greater exposure

brought by television advertising. Other

good performances came from Drostdy-

Hof (especially the Extra Light and

Natural Sweet variants), J.C. Le Roux

sparkling wines, and Sedgwick’s Old

Brown Sherry. Within the RTD category,

our cider brands performed exceptionally

well. Hunter’s posted strong growth

across its entire brand range, while

Savanna was once again the star

performer of the entire Distell brand

portfolio.

Continued focus on and investment in

brand building, market activation, trade

channel management, as well as

customer and consumer relationship

management strategies, have allowed us

to capitalise on favourable economic

conditions and remain fi rmly on our

growth path.

We also explored new investment

opportunities to enhance our spirit

portfolio during the year under review as

mentioned in the chairman’s statement.

In April, we entered into a joint venture

as equal partners with Burn Stewart

Distillers, a Scotch whisky producer and

brand owner with a portfolio of leading

whisky brands. Burn Stewart is owned by

CL WorldBrands, the global drinks group

of Trinidad-based CL Financial with

distribution networks in Europe, the USA

and the Far East. Th e joint venture owns

and markets three of Burn Stewart’s

leading brands in sub-Saharan Africa.

In addition to Scottish Leader (which

Distell has represented in South Africa

Managing director’s report

We have improved shareholder value through considerable growth in earnings and by extracting even better performance from our assets.

“Th is has been another successful year for Distell”

Headline earnings, excluding the non-recurring black economic empowerment (BEE) expense incurred the previous year, grew 29,2%, achieving compound annual growth of 19,2% over a seven-year period.

Over the same period, net operating assets (i.e. fi xed assets, inventory and accounts receivable, less accounts payable) refl ected compound annual growth of 3,3%.

Returns on shareholders’ funds continued to improve, from 18,2% last year to 19,8%.

Our sound fi nancial performance has been the result of strong and profi table volume growth, and a very satisfactory performance by operating units across the business.

Management uses a range of fi nancial and non-fi nancial key performance indicators to monitor progress against our strategic priorities and business plans. Divisions across the business succeeded in meeting, if not improving, most of these performance measurements.

25Distell Annual Report 2007

Nederburg, the country’s most awarded name in wine, continues

to fi nd favour in markets abroad. A South African

brand leader in Germany, Nederburg is delighting

wine lovers in the UK, across Europe, the USA, Asia Pacifi c and

closer to home, on the African continent.

26 Distell Annual Report 2007

Managing director’s report (continued)

since 1999), they are the Bunnahabhain

Islay Single Malt, and Black Bottle Scotch

Whisky, a blend of seven Islay malts.

International marketTh e expansion of our international

business forms an integral part of

Distell’s strategic focus. To this end, we

are concentrating on:

• Building a core portfolio of brands in

key markets.

• Still further advancing Amarula’s

global position, strengthening

support where we currently trade and

establishing a presence in new

markets. Amarula is the company’s

biggest spirit brand and also South

Africa’s most widely distributed

alcoholic beverage internationally.

• Building on our position as a

profi table and leading South African

wine exporter. We succeeded in

exporting 43% of our premium wine

production, with drive brands,

Nederburg, Fleur du Cap, Two

Oceans, Durbanville Hills and

Drostdy-Hof, all showing signifi cant

growth in key markets.

• Exploiting the popularity of Savanna

in key markets.

• Giving greater attention to our

African operations.

International sales volumes have shown

compound annual growth of 10,3% over

a fi ve-year period. Currently,

international business contributes

18% of total revenue. Th is year export

volumes grew 9,8%, a refl ection of a

favourable sales mix.

African markets Th e International Monetary Fund, in its

April 2007 World Economic Outlook,

painted a fairly optimistic picture of

Africa. Th e continent’s economic growth

is being fuelled mainly by strong global

growth, increased capital infl ows,

a buoyant commodities sector, improved

economic stability in many countries and

the positive impact of debt relief.

Since 2000, real GDP growth in sub-

Saharan Africa has averaged around

4,5% per annum. We began focusing

assiduously on the subcontinent in 2003

and have been expanding our presence in

the region ever since, with our eff orts

continuing to bear fruit. Th is year, sales

volumes for Africa (excluding Botswana,

Lesotho, Namibia and Swaziland) grew

31,5%, well ahead of target.

Wine sales volumes grew 24,5% and

spirits 47,8%. We are particularly

encouraged by the acceptance and

growth of brandy outside South Africa.

Although off a low base, sales volumes of

ciders and RTDs grew 62,5%.

Angola, Kenya and Zambia delivered

excellent results, with sales volume growth

driven particularly by Amarula, Viceroy,

J.C. Le Roux, Nederburg and Savanna.

In line with strong growth trends, we

have substantially strengthened our

marketing structures and sales

representation in key markets in the

region. We are confi dent that our

increased investment, both in terms of

infrastructure and brand support, will

allow us to eff ectively exploit market

potential.

At the same time, we remain committed

to our philosophy of partnering with local

players to expand our footprint across the

continent, while building capacity in

developing markets. Th e Group adds

signifi cant value by providing technical

and manufacturing skills in countries

such as Zimbabwe, Kenya, Tanzania and

Mauritius.

We hold a 35% share in Tanzania

Distilleries Limited that continues to

deliver excellent results. With sales

volumes far exceeding targets, capacity

has recently been expanded. In a major

boost to the local industry, the operation

is now also bottling Tanzanian wines.

Zimbabwean company African Distillers

Limited, in which we have an eff ective

31% share, has demonstrated remarkable

resilience under extremely challenging

conditions. Present circumstances have,

however, necessitated the adoption of a

survival as opposed to a growth strategy.

Nevertheless, the performance of this

investment has no material bearing on

Distell’s overall performance.

During the review period we fi nalised a

transaction giving us a 26% interest in

the Mauritian company, Grays Inc

Limited, and initial results have proved

encouraging.

Our production and distribution

agreement with Kenya Wine Agencies

Limited once again resulted in

substantial volume growth for key

brands, especially brandies.

BLNS countries (Botswana, Lesotho, Namibia, Swaziland)Th e countries immediately beyond our

borders have long been important

markets for us and over the years we have

continued to strengthen marketing, sales

and distribution infrastructure to

maximise opportunities. Growth across

all product segments has been in line

with projections.

Other markets (outside the African continent)Th is year export volumes grew 7,2%, a

refl ection of a favourable sales mix.

Amarula Cream

Th e past few years have seen

unprecedented global growth in the

popularity of cream liqueurs,

precipitating a signifi cant proliferation in

product off ering in all markets. However,

most players have not managed to make

any real impact and the market is

currently consolidating.

27Distell Annual Report 2007

Amarula continued to perform well with

strong growth achieved in all key

markets, in particular Canada, Germany,

Brazil and neighbouring countries, as

well as the UK. With a 25,6% growth in

export volumes, the brand continues to

outperform the category on the

international front.

Global development remains a priority.

Continuous research underpins our

investment strategy in the brand, which

focuses on both established and newer

markets. Th e travel retail channel has and

will continue to play a valuable role in

promoting Amarula’s visibility.

Wines

To underpin our international trading

activities, we have been actively engaged

in establishing strategic alliances with

trading partners, concluding several

important agency agreements that will

not only bolster our presence in Europe,

but also strengthen our ties in North

America, Europe and Asia Pacifi c.

Distell entered into a supply and agency

agreement with Altia Corporation, an

international multi-beverage company

that operates in the Nordic states, where

it is the market leader, as well as in the

emergent Baltic markets. Th is deal is

helping to forge an already strong

presence in Finland, Norway and Sweden,

while giving us exposure to new

opportunities in the Baltic states.

We also entered into an agreement with

Baarsma Wine Group Holding (BWGH) to

carry some of our drive wine brands in

the Netherlands, giving us a balanced

exposure across a range of channels and

price points. BWGH is a leading player in

the Dutch retail and on-consumption

channels and also markets directly to an

extensive base of consumers. Key brands

being represented include Fleur du Cap,

Durbanville Hills, J.C. Le Roux, Pongracz,

Two Oceans and Drostdy-Hof.

To secure a stronger presence in UK

retail, we have expanded our agreement

with distributor Waverly TBS, which has

recently taken on Two Oceans, in

addition to other focus wine brands –

Nederburg, Drostdy-Hof, Fleur du Cap

and Plaisir de Merle.

AV Imports continues to make inroads

for Two Oceans in the USA, focusing on

some of the major grocers’ chains.

Listings have been achieved with Hyvee,

across over 200 stores in the mid-west;

Publix in the south; 500 Food Lion stores

in the south; and mid-Atlantic and

Pennsylvania Liquor Commission.

Distell’s competitive edge is, we believe,

the result of ongoing brand investment,

a relentless focus on quality, fl exibility of

service off erings, solid agency structures

and a balanced product portfolio.

Drive brands have shown compound

annual growth in volume of 16,8 % over

a fi ve-year period, increasing the

contribution of international markets to

total group brand income from wine.

During the review period, these key

brands showed a 12,6% volume growth in

an international market characterised by

oversupply and contracting market share

for many players. However, overall wine

volume growth was signifi cantly lower,

increasing just 3,3%, given the decline in

sales of second-tier brands.

We have seen solid growth in key markets

such as Scandinavia, Canada (where Two

Oceans is one of the top ten wine brands)

and the USA. Although our performance

in the UK and the Netherlands did not

meet our expectations, we were able to

increase our share of the South African

category in these markets.

Our continued focus on emerging

markets is also starting to show

encouraging results and a number of

breakthroughs have been made in

Central Eastern Europe and Asia Pacifi c.

Although off a small base, we are heartened

by brand developments, most notably in

Russia, China, Vietnam and South Korea.

Our intention remains to establish and

maintain profi table brands. We have

increased our earnings from wine

exports this year, while substantially

increasing advertising support for our

brands.

OperationsStrategies and initiatives designed to

achieve and entrench a sustainable

competitive cost advantage remain a top

priority in our goal to participate

successfully in competitive global

markets. Year-on-year improvement in

operational performance is refl ected in

a continuous reduction in unit cost and

a constant improvement in net operating

margin. Excellence in operational

performance demands that we:

• place customers and consumers at

the centre of our thinking,

• deliver superior products, and

• provide excellent service at

competitive prices.

It is, however, imperative that we

constantly raise the performance of our

operating units to maintain our lead and

competitive edge. Business process

improvement is therefore integral to the

way we work.

Th is year we have made further advances

in enhancing effi ciencies. Progress

against cost leadership goals has been in

line with targets, with most key

performance indicators showing an

improvement on the previous year. Sales

volumes increased 14,4% while expenses,

excluding sales and marketing

expenditure, rose 15,7%, resulting in a

mere 1,2% increase in cost per litre, well

below the producer price index (PPI) of

10,4%. Th e benefi ts fl owing from

28 Distell Annual Report 2007

Managing director’s report (continued)

improved effi ciencies allow us to reinvest

in strategic areas of the business,

particularly marketing expenditure on

drive brands and by extending sales

representation and marketing

capabilities in key markets.

Th e principle of managing by project has

contributed to an overall improvement in

effi ciencies. Consequently we have

formalised this approach by establishing

a central Enterprise Project Offi ce. We

successfully implemented the Six Sigma

methodology, training project managers

and placing them in business units. Th is

has further boosted a sense of ownership

amongst staff and impacted positively on

both team and individual performance.

Th is year our secondary production

division, responsible for bottling and

blending, extended the implementation

of the “overall equipment effi ciency”

process monitoring systems to all

production sites. Th e system is designed

to signifi cantly reduce unplanned

downtime and changeover time on

production lines, resulting in enhanced

throughput and a substantial

improvement in resource utilisation.

To capitalise on the trend towards

premiumisation, while still maintaining

a competitive advantage, we continue to

invest diligently in measures to improve

product intrinsics, as well as extrinsics

such as packaging. Advances in this

regard include:

• Establishing labelling capability to

produce complex product

confi gurations

• A programme to expand automatic

packers to prevent damage caused by

manual processes

• Investment in equipment to produce

new packaging concepts

We also have to ensure that our service

off erings are aligned with customer

needs in a changing environment. Our

‘Route to Market’ project, aimed at

identifying customer needs, market

opportunities and gaps in our service

model, is close to completion and

recommendations, based on research

fi ndings, are in the process of being

implemented. SAP functionality is

currently being implemented in Distell

TradeXpress outlets that service specifi c

customer channels in the South African

market. Not only will this enable us to

raise our service levels to customers, but

also to reduce inventory and optimise

inter-depot transport.

Th e quality of our employees impacts

directly on our operational performance.

We therefore promote values such as:

• A sense of ownership where

employees at every level are aware of

their contributions, and are

empowered and accountable

• A performance-driven culture, where

we challenge ourselves to ensure

continuous improvement, by creating

more, better and faster

• A customer-service orientation, to

delight our customers and consumers

everywhere

• Entrepreneurship, by allowing

employees the freedom to explore and

create

• Respect for the individual where we

respect each other’s diversity and

contribute to the communities in

which we operate. We also promote

the responsible use of alcohol.

Th e Group continues to maintain mission

directed work teams in all operation

environments. We believe this approach

provides a valuable foundation for

ongoing improvement. It encourages and

builds a culture that is performance-

driven and oriented towards customer

service. It also promotes team work, a

sense of ownership and stimulates

innovation. Given the excellent results

from initiatives already under way, we

recently expanded the parameters by

introducing additional modules that

focus on areas such as ‘asset care’ and

‘process control’.

We have embarked on a programme to

align our people competencies with

future business requirements. In this way

we are able to engage in more meaningful

and targeted training programmes.

Th e phenomenal growth of the RTD market

in which Distell is a signifi cant player, has

resulted in greater investment to meet

demand, of ciders in particular. We are

increasing cider capacity at our production

plant in Paarl, as well as at our bottling

facility in Green Park. Th ese expansions

are expected to be commissioned early in

the 2008 fi nancial year.

A national shortage of carbon dioxide

(CO2 )

prompted us to explore the

viability of CO2 recovery. We have since

entered into an agreement with Air

Liquide for the installation of a full-scale

CO2 recovery plant in Paarl which will

give us continued supply of CO2 needed in

the production of many of our products.

Procurement practices remain a top

priority. Close collaboration with our

suppliers plays a major role in enabling us

to further expand our business, both in

the local and international markets,

benefi ting all industry participants. It is

therefore crucial to ensure continuous

product availability, quality standards

and cost reduction through improved

effi ciencies throughout the value chain.

Th is is particularly important given the

challenging trading conditions faced by

the industry and the need to provide

a stable operating environment over

the long term for the mutual benefi t of

all participants in the supply chain.

During the year signifi cant progress was

made in establishing a global supply

network. Th is gives us access to better

product, service and pricing options and

29Distell Annual Report 2007

Amarula Cream is enjoyed in over 90 countries worldwide and

continues to outperform the category on the

international front. Amarula, the spirit of Africa, achieved strong

growth in all key markets, in particular Brazil, Canada,

Germany, neighbouring countries as well as the UK.

30 Distell Annual Report 2007

also helps to counter local supplier

production capacity constraints,

particularly in the case of packaging

materials.

We have also initiated a low-tech, labour-

intensive scheme in the Northern Cape

and Free State, to ensure Distell of a cost-

eff ective source of distilling wine. Using

virgin land that does not require the

grafting of vines onto rootstock (thus

reducing input costs), applying low-cost

trellising, as well as fl ood irrigation, the

intention is to establish high-density

vineyard planting on some 700 hectares.

Expected to optimally yield an average of

45 tons per hectare, crops will be

processed at existing wine cellars with

underutilised capacity. Further details

regarding this project appear on page 44

in the sustainability report.

A section of our production plant in

Wadeville was destroyed by fi re late in

2006. We are pleased to report that

eff ective business resumption procedures

meant production remained virtually

uninterrupted as alternative sites

stepped in to provide the necessary

support. Repairs are on schedule and

we expect the plant to be fully

operational by October 2007.

Financial reviewRevenueRevenue grew 18,4% to R8,0 billion on

a sales volume increase of 14,4%.

Locally, sales volumes increased 15,6%,

with growth accelerating signifi cantly

during the second six months. Our